Embed Size (px)

Citation preview

BOMBAY CHARTERED ACCOUNTANTS’ SOCIETY

NEGATIVE LIST BASED TAXATION

OF SERVICES: IMPORTANT ISSUES

PULOMA DALAL

Chartered Accountant

03 September 2012

At Indian Merchants’ Chamber, Mumbai

METAMORPHOSIS OF THE

SERVICE TAX SYSTEM

After 18 years of its introduction in 1994, service tax has been conceptually transformed from a “selective levy” to “comprehensive levy” w.e.f. July 01, 2012. The metamorphosis of the tax system contains the following significant features:

• Introduction of definitions of “service,” “taxable territory” and “India”

• Redefining “charging section” to encompass the concept of “taxable territory”

• Introduction of a “Negative List” to replace specified list of taxable services and also specifying “declared services”

• Introduction of principles for interpretation of service and taxation of bundled services in place of principles of classification of services

2 Puloma Dalal

METAMORPHOSIS OF THE

SERVICE TAX SYSTEM

• Consolidation of all major exemptions under one notification.

• Introduction of single set of Place of Provision of Services Rules, 2012 to determine place of provision of service for import and export replacing export rules and import rules.

• Providing definitions at multiple places:

– In Finance Act, 1994 (the Act)

– In Service tax Rules, 1994

– In mega Exemption Notification No.25/2012-ST

– In Place of Provision Rules, 2012 etc

3 Puloma Dalal

SELECT ISSUES IN THE NEW

“NEGATIVE LIST” BASED TAXATION SYSTEM

1. Service

2. Declared services

3. Interpretation Issues in:

– Negative List

– Mega Exemption Notification

4. Bundled Service

Puloma Dalal 4

“SERVICE”

Puloma Dalal 5

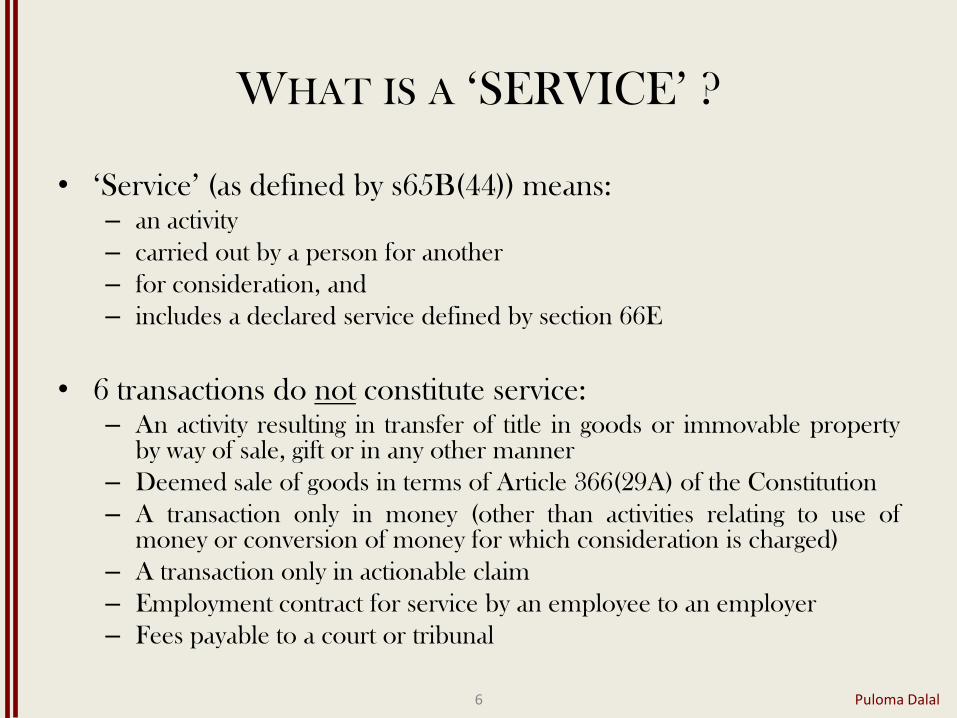

WHAT IS A ‘SERVICE’ ?

• ‘Service’ (as defined by s65B(44)) means: – an activity

– carried out by a person for another

– for consideration, and

– includes a declared service defined by section 66E

• 6 transactions do not constitute service: – An activity resulting in transfer of title in goods or immovable property

by way of sale, gift or in any other manner

– Deemed sale of goods in terms of Article 366(29A) of the Constitution

– A transaction only in money (other than activities relating to use of money or conversion of money for which consideration is charged)

– A transaction only in actionable claim

– Employment contract for service by an employee to an employer

– Fees payable to a court or tribunal

Puloma Dalal 6

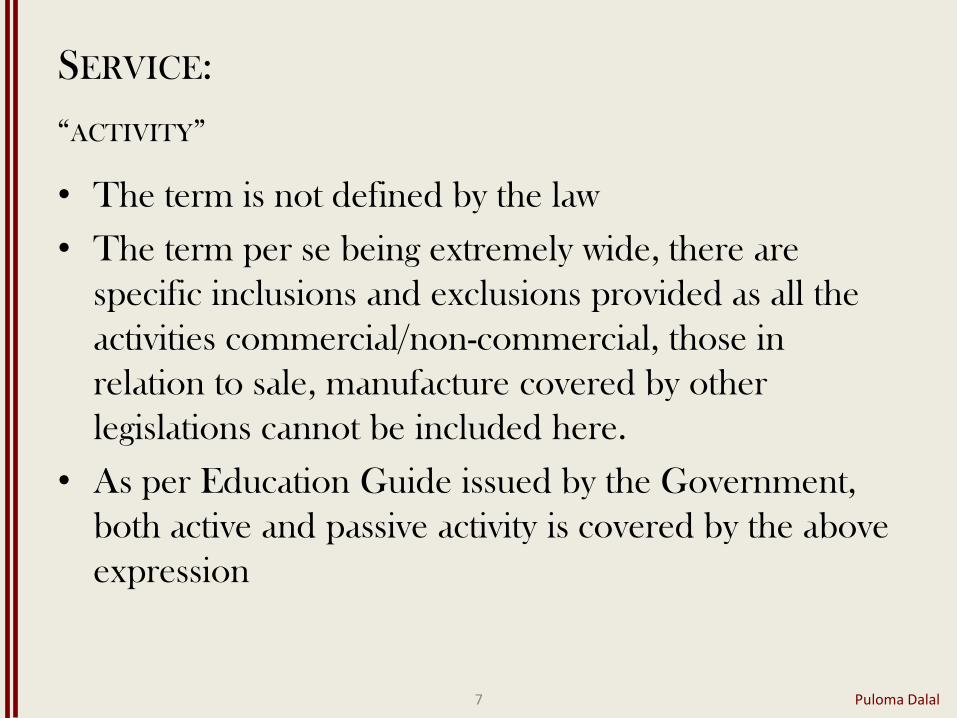

SERVICE:

“ACTIVITY”

• The term is not defined by the law

• The term per se being extremely wide, there are

specific inclusions and exclusions provided as all the

activities commercial/non-commercial, those in

relation to sale, manufacture covered by other

legislations cannot be included here.

• As per Education Guide issued by the Government,

both active and passive activity is covered by the above

expression

Puloma Dalal 7

SERVICE:

“CARRIED OUT BY A PERSON FOR ANOTHER”

• Only transactions occurring between two persons are covered by the definition

• Nobody can provide service to himself [CCE vs. Nahar Industrial Enterprise Ltd. 2010 (19) STR 166 (P&H)]

• When one renders service to oneself, as in the present case, there is no question of leviability of service tax

[Precot Mills vs. CCE 2006 (2) STR 495 (Tri.-Bang)]

• There should be existence of two side entities for having transaction as against consideration. In a members’ club, there is no question of two sides. Members and club both are same entities

[Saturday Club Ltd. vs. A.C. Service Tax 2006 (3) STR 305 (Cal)]

• If club provides any service to its member, may be as mandap keeper, then it is not a service by one to another as foundation facts of existence of two legal entities in such transaction is missing

[Ranchi Club Ltd. vs. CCE&ST 2012 (26) STR 401 (Jhar)]

Puloma Dalal 8

• Service between two establishments of the same person is taxable

In terms of Explanation No.3 & 4 to the definition of service in section 65B(44) –

• An unincorporated association or a body of persons as the case may be and its members on the other hand are treated as distinct persons

• An establishment of a person in taxable territory and any of his other establishments in a non-taxable territory are considered distinct persons

• Whether a service provided by a New York branch to its head office of an Indian company in Mumbai would be considered taxable if other ingredients relating to taxability are fulfilled?

Puloma Dalal 9

SERVICE:

EXCEPTION: “CARRIED OUT BY A PERSON FOR ANOTHER”

• This term is not defined in the Act

• However, section 67 dealing with valuation of taxable service has defined consideration in inclusive manner so as to include any amount that is payable for the taxable service provided or to be provided.

• Education Guide para 2.2.1 therefore refers to the definition of consideration as per the Indian Contract Act, 1872.

"When, at the desire of the promisor, the promisee or any other person has done or abstained from doing, or does or abstains from doing, or promises to do or abstain from doing, something, such act or abstinence or promise is called a consideration for the promise".

Puloma Dalal 10

SERVICE:

“CONSIDERATION”

• Legal Rules:

– Must move at the desire of the promisor

– May move from the promisee or any other person

– May be an act of doing or forbearance

– May be past, present or future

Puloma Dalal 11

SERVICE:

“CONSIDERATION”

• As such, gratis payment, donation or a grant do not attract service tax.

• In relation to grant in-aid received by the company from Government for implementing welfare scheme of Central and State Government for the benefit of poor, it was held that there did not exist relationship of service-provider and service recipient

[APITCO Ltd. vs. CST 2010 (20) STR 475 (Tri.-Bang)]

• Appeal of the revenue dismissed by the Supreme Court in ST vs. APITCO Ltd. 2011 (23) STR J94 (SC)

• (For illustrations of nature of payments which constitute consideration, see Education Guide para 2.3.2)

Puloma Dalal 12

SERVICE:

“CONSIDERATION”

1. Transfer of title in goods or immovable property

– An activity that constitutes a mere transfer of title in goods or

immovable property by way of sale or gift

– The contract of sale includes both a sale and an agreement to sell.

A mere transfer of custody or possession does not constitute sale

– In composite transactions containing both goods and services,

depending on the dominant nature of transaction or severability,

sale of goods/immovable property in a composite transaction or a

portion thereof would not constitute service

– ‘goods’ (as per s. 65B(25)) includes securities. Accordingly, sale of

shares, derivatives, units of mutual funds, government securities

etc – constitute sale, and not service

Puloma Dalal 13

SERVICE:

TRANSACTIONS NOT CONSTITUTING A SERVICE

2. ‘Deemed Sale’ – Article 366(29A) of the Constitution lists 6 transactions of

deemed sale: • A sale of goods otherwise than in pursuance of a contract

• Transfer of property in goods involved in the execution of works contract

• Delivery of goods on hire purchase or payment of installments

• Transfer of the right to use goods

• Supply of goods by unincorporated association to a member thereof

• Catering contracts

– A slump sale or transfer of a going concern is exempted vide entry 37 of Notification 25/2012-ST

– In case of Works contracts & Catering contracts, the sale of goods component is excluded from ‘service’ as it is a declared service

– In the other 4 cases, deemed sale transactions based on dominant nature theory would not constitute ‘service’

Puloma Dalal 14

SERVICE:

TRANSACTIONS NOT CONSTITUTING A SERVICE

3. Transactions only in money

– ‘money’ is defined in s. 65B (33)

– Transaction per se in money such as deposits/withdrawals

from a bank account does not constitute a service

– Where consideration is charged for a money transaction it

would constitute ‘service’

– See Education Guide paras 2.8.1 – 2.8.5 for illustrations of

money transactions and consideration in relation thereto

Puloma Dalal 15

SERVICE:

TRANSACTIONS NOT CONSTITUTING A SERVICE

4. Transactions in ‘actionable claim’

– Actionable claim means a claim to any debt, other than a debt secured by mortgage of immovable property; or by hypothecation or pledge of movable property; or to any ‘beneficial interest’ in movable property not in the possession either actual or constructive of the claimant; which the civil courts recognise as affording grounds for relief, whether such debt or beneficial interest be existent, accruing, conditional or contingent

– Examples: unsecured debts, right to participate in the lottery [Sunrise Associates (2006) 5 SCC 603]

– Also see Education Guide paras 2.8.8, 2.8.11 and 2.8.12

Puloma Dalal 16

SERVICE:

TRANSACTIONS NOT CONSTITUTING A SERVICE

5. Employment Contracts

– See Education Guide paras 2.9.1, 2.9.3 and 2.9.4

– Whether non-executive directors receiving remuneration

would be treated as payment towards employment?

Puloma Dalal 17

SERVICE:

TRANSACTIONS NOT CONSTITUTING A SERVICE

DECLARED SERVICES

Puloma Dalal 18

DECLARED SERVICES

• The definition of service in s. 65B(44) includes a ‘declared service.’

• Declared services are separately defined in section 66E, which contains 9 items, including 5 formerly contentious services: – renting of immovable property,

– construction of complex including a building or a complex intended for a sale,

– design and development of information technology software,

– works contracts,

– temporary transfer of intellectual property rights etc.

• Thus all services listed as declared services are now deemed to be services as they supplement the definition of service

• Thus, the law makers have attempted to minimize controversy over the issue of whether these activities constitute services.

• However, there are some issues that have not been addressed under the new system, namely: – Double taxation under VAT and service tax of transactions in relation to IT software,

granting or assignment of intellectual property and transferring goods by way of leasing or hiring.

Puloma Dalal 19

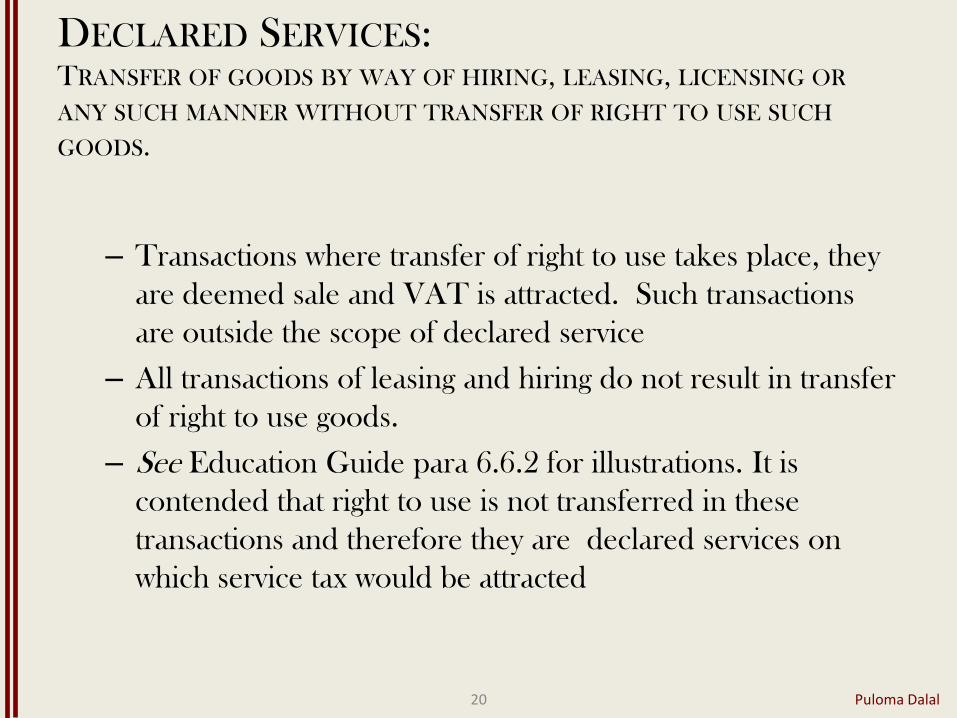

DECLARED SERVICES: TRANSFER OF GOODS BY WAY OF HIRING, LEASING, LICENSING OR

ANY SUCH MANNER WITHOUT TRANSFER OF RIGHT TO USE SUCH

GOODS.

– Transactions where transfer of right to use takes place, they

are deemed sale and VAT is attracted. Such transactions

are outside the scope of declared service

– All transactions of leasing and hiring do not result in transfer

of right to use goods.

– See Education Guide para 6.6.2 for illustrations. It is

contended that right to use is not transferred in these

transactions and therefore they are declared services on

which service tax would be attracted

Puloma Dalal 20

Sr.

No.

Nature of transaction Whether transaction involves transfer of right

to use

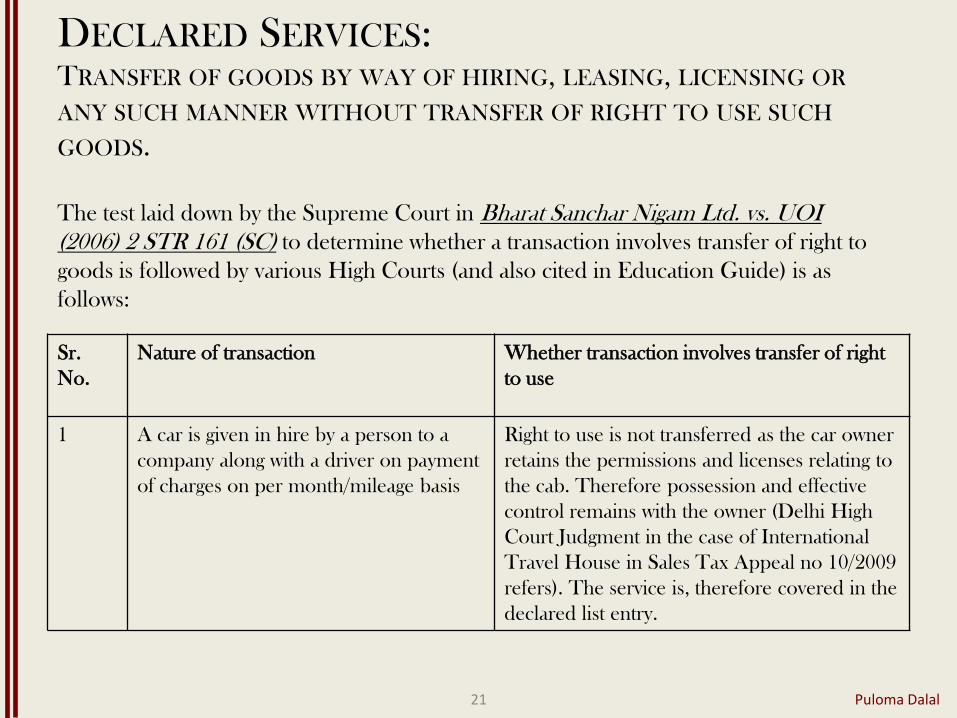

1 A car is given in hire by a person to a

company along with a driver on payment

of charges on per month/mileage basis

Right to use is not transferred as the car owner

retains the permissions and licenses relating to

the cab. Therefore possession and effective

control remains with the owner (Delhi High

Court Judgment in the case of International

Travel House in Sales Tax Appeal no 10/2009

refers). The service is, therefore covered in the

declared list entry.

Puloma Dalal 21

The test laid down by the Supreme Court in Bharat Sanchar Nigam Ltd. vs. UOI

(2006) 2 STR 161 (SC) to determine whether a transaction involves transfer of right to

goods is followed by various High Courts (and also cited in Education Guide) is as

follows:

DECLARED SERVICES: TRANSFER OF GOODS BY WAY OF HIRING, LEASING, LICENSING OR

ANY SUCH MANNER WITHOUT TRANSFER OF RIGHT TO USE SUCH

GOODS.

Sr.

No.

Nature of transaction Whether transaction involves transfer of right

to use

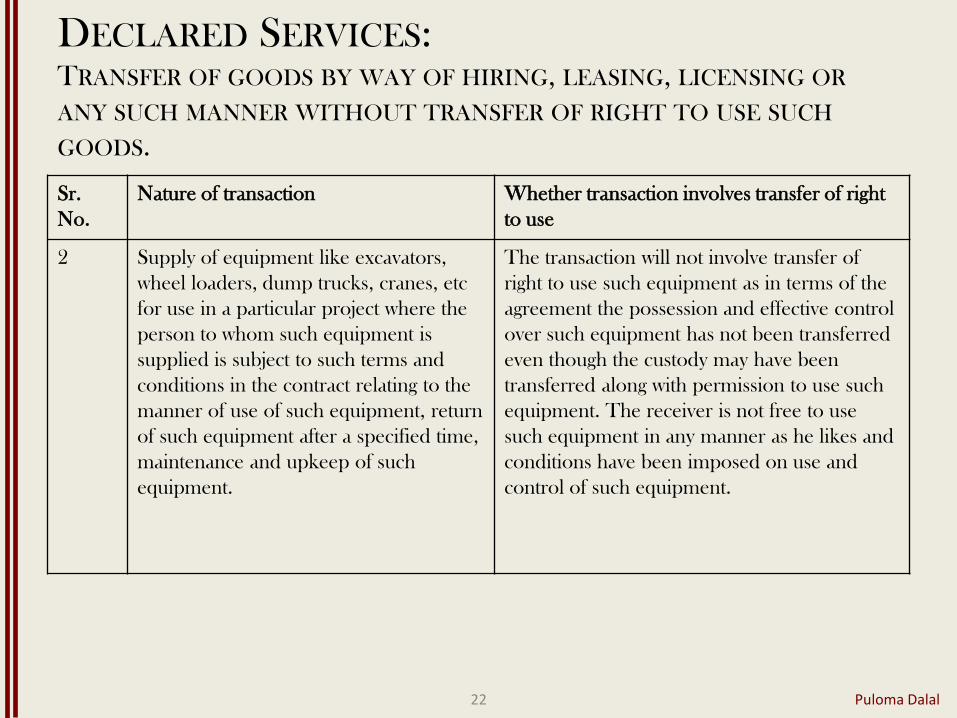

2 Supply of equipment like excavators,

wheel loaders, dump trucks, cranes, etc

for use in a particular project where the

person to whom such equipment is

supplied is subject to such terms and

conditions in the contract relating to the

manner of use of such equipment, return

of such equipment after a specified time,

maintenance and upkeep of such

equipment.

The transaction will not involve transfer of

right to use such equipment as in terms of the

agreement the possession and effective control

over such equipment has not been transferred

even though the custody may have been

transferred along with permission to use such

equipment. The receiver is not free to use

such equipment in any manner as he likes and

conditions have been imposed on use and

control of such equipment.

Puloma Dalal 22

DECLARED SERVICES: TRANSFER OF GOODS BY WAY OF HIRING, LEASING, LICENSING OR

ANY SUCH MANNER WITHOUT TRANSFER OF RIGHT TO USE SUCH

GOODS.

Sr.

No.

Nature of transaction Whether transaction involves transfer of

right to use

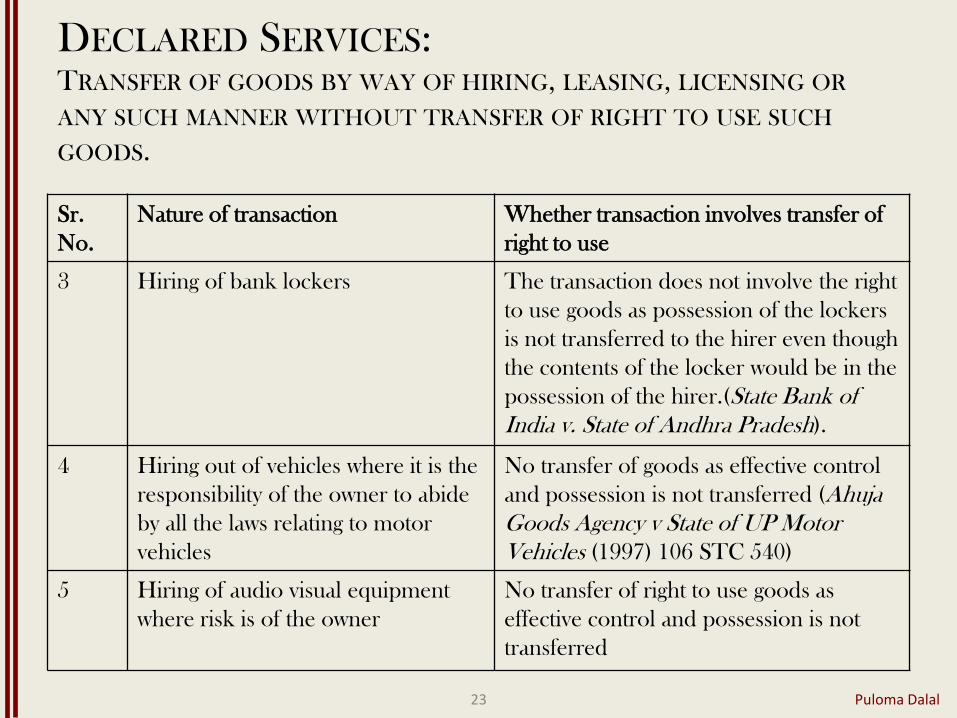

3 Hiring of bank lockers The transaction does not involve the right

to use goods as possession of the lockers

is not transferred to the hirer even though

the contents of the locker would be in the

possession of the hirer.(State Bank of

India v. State of Andhra Pradesh).

4 Hiring out of vehicles where it is the

responsibility of the owner to abide

by all the laws relating to motor

vehicles

No transfer of goods as effective control

and possession is not transferred (Ahuja

Goods Agency v State of UP Motor

Vehicles (1997) 106 STC 540)

5 Hiring of audio visual equipment

where risk is of the owner

No transfer of right to use goods as

effective control and possession is not

transferred

Puloma Dalal 23

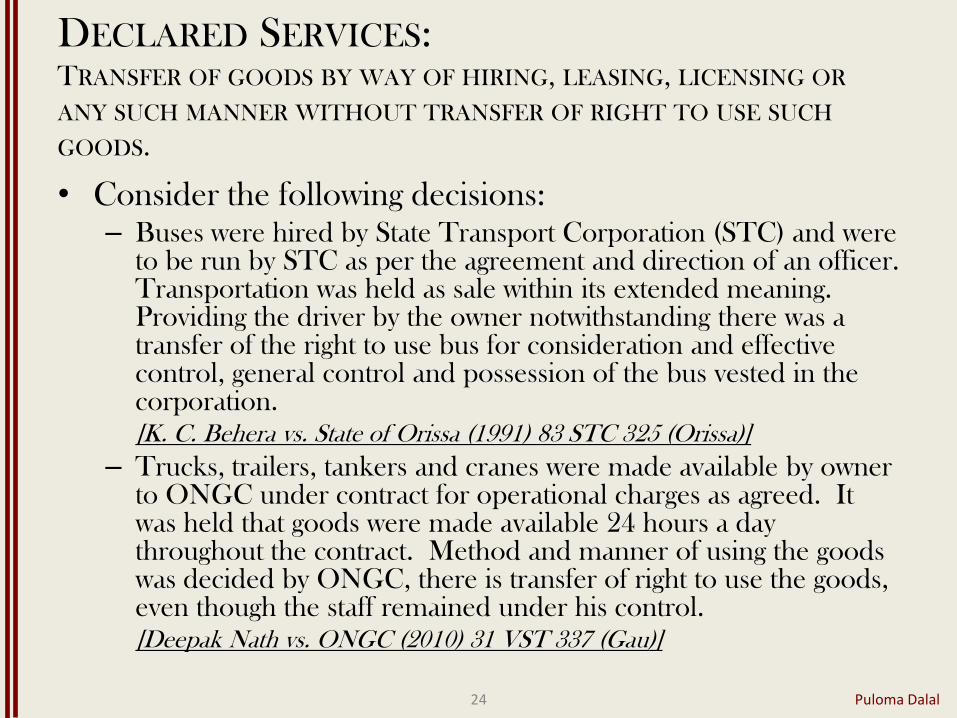

DECLARED SERVICES: TRANSFER OF GOODS BY WAY OF HIRING, LEASING, LICENSING OR

ANY SUCH MANNER WITHOUT TRANSFER OF RIGHT TO USE SUCH

GOODS.

• Consider the following decisions: – Buses were hired by State Transport Corporation (STC) and were

to be run by STC as per the agreement and direction of an officer. Transportation was held as sale within its extended meaning. Providing the driver by the owner notwithstanding there was a transfer of the right to use bus for consideration and effective control, general control and possession of the bus vested in the corporation.

[K. C. Behera vs. State of Orissa (1991) 83 STC 325 (Orissa)]

– Trucks, trailers, tankers and cranes were made available by owner to ONGC under contract for operational charges as agreed. It was held that goods were made available 24 hours a day throughout the contract. Method and manner of using the goods was decided by ONGC, there is transfer of right to use the goods, even though the staff remained under his control.

[Deepak Nath vs. ONGC (2010) 31 VST 337 (Gau)]

Puloma Dalal 24

DECLARED SERVICES: TRANSFER OF GOODS BY WAY OF HIRING, LEASING, LICENSING OR

ANY SUCH MANNER WITHOUT TRANSFER OF RIGHT TO USE SUCH

GOODS.

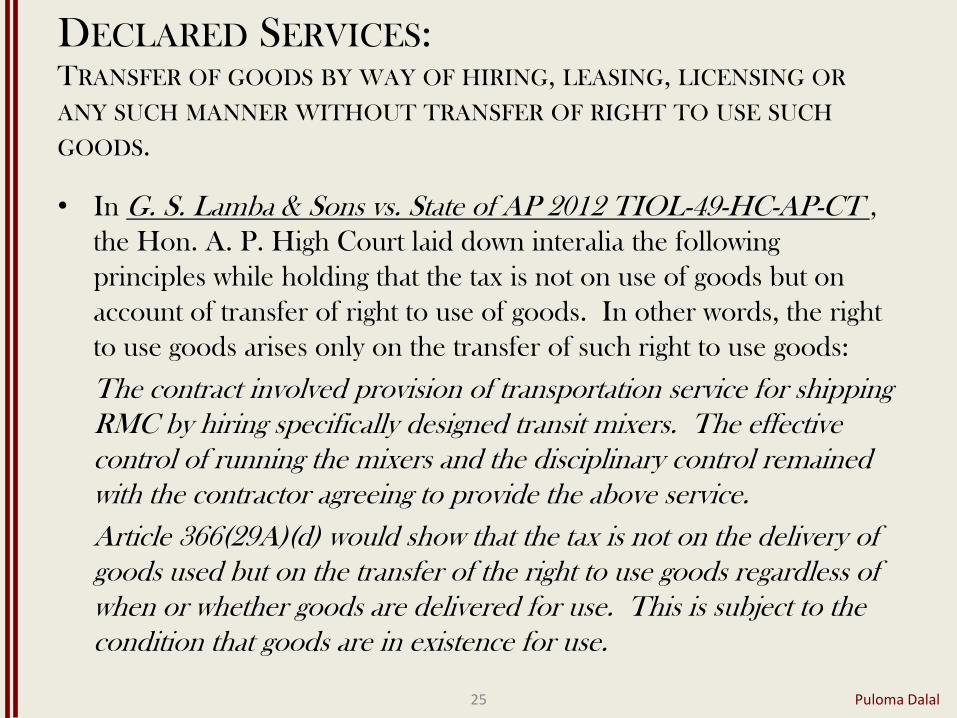

• In G. S. Lamba & Sons vs. State of AP 2012 TIOL-49-HC-AP-CT ,

the Hon. A. P. High Court laid down interalia the following

principles while holding that the tax is not on use of goods but on

account of transfer of right to use of goods. In other words, the right

to use goods arises only on the transfer of such right to use goods:

The contract involved provision of transportation service for shipping

RMC by hiring specifically designed transit mixers. The effective

control of running the mixers and the disciplinary control remained

with the contractor agreeing to provide the above service.

Article 366(29A)(d) would show that the tax is not on the delivery of

goods used but on the transfer of the right to use goods regardless of

when or whether goods are delivered for use. This is subject to the

condition that goods are in existence for use.

Puloma Dalal 25

DECLARED SERVICES: TRANSFER OF GOODS BY WAY OF HIRING, LEASING, LICENSING OR

ANY SUCH MANNER WITHOUT TRANSFER OF RIGHT TO USE SUCH

GOODS.

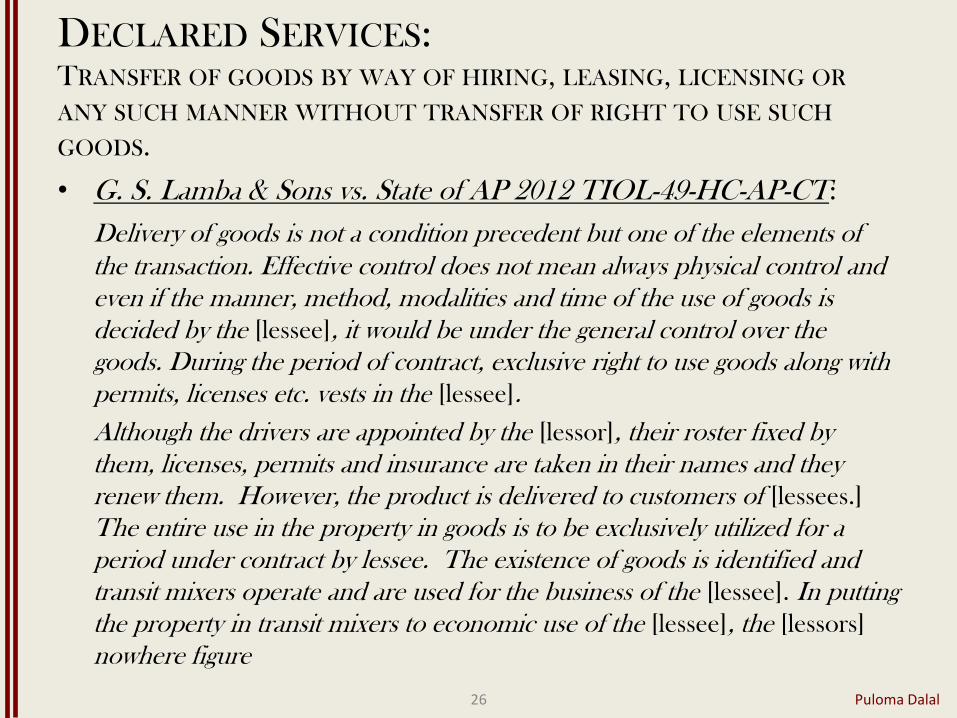

• G. S. Lamba & Sons vs. State of AP 2012 TIOL-49-HC-AP-CT:

Delivery of goods is not a condition precedent but one of the elements of

the transaction. Effective control does not mean always physical control and

even if the manner, method, modalities and time of the use of goods is

decided by the [lessee], it would be under the general control over the

goods. During the period of contract, exclusive right to use goods along with

permits, licenses etc. vests in the [lessee].

Although the drivers are appointed by the [lessor], their roster fixed by

them, licenses, permits and insurance are taken in their names and they

renew them. However, the product is delivered to customers of [lessees.]

The entire use in the property in goods is to be exclusively utilized for a

period under contract by lessee. The existence of goods is identified and

transit mixers operate and are used for the business of the [lessee]. In putting

the property in transit mixers to economic use of the [lessee], the [lessors]

nowhere figure

Puloma Dalal 26

DECLARED SERVICES: TRANSFER OF GOODS BY WAY OF HIRING, LEASING, LICENSING OR

ANY SUCH MANNER WITHOUT TRANSFER OF RIGHT TO USE SUCH

GOODS.

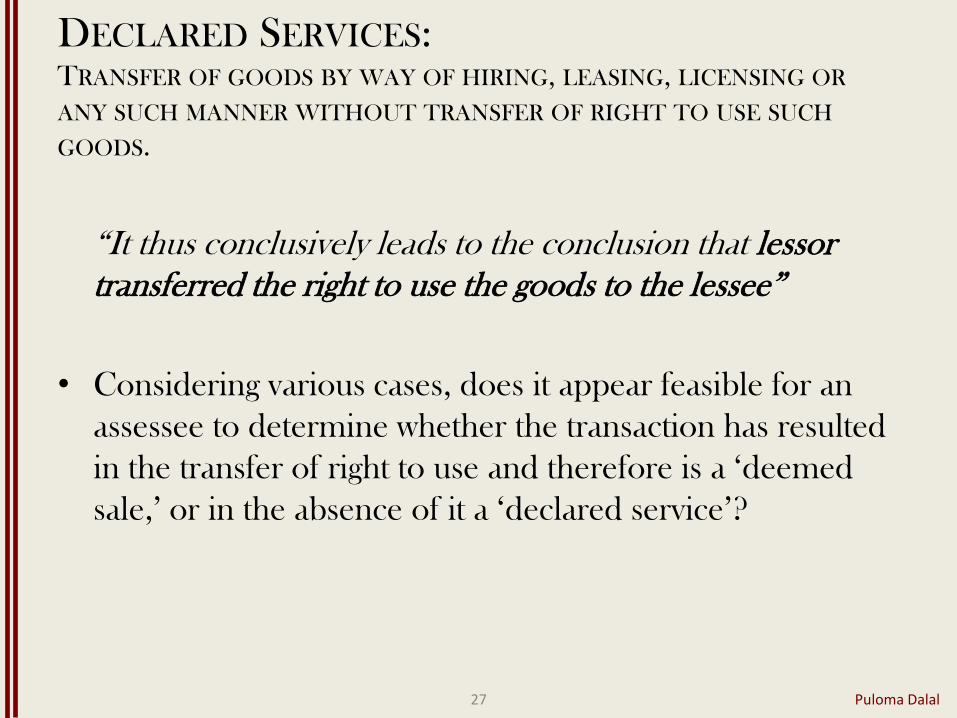

“It thus conclusively leads to the conclusion that lessor

transferred the right to use the goods to the lessee”

• Considering various cases, does it appear feasible for an

assessee to determine whether the transaction has resulted

in the transfer of right to use and therefore is a ‘deemed

sale,’ or in the absence of it a ‘declared service’?

Puloma Dalal 27

DECLARED SERVICES: TRANSFER OF GOODS BY WAY OF HIRING, LEASING, LICENSING OR

ANY SUCH MANNER WITHOUT TRANSFER OF RIGHT TO USE SUCH

GOODS.

DECLARED SERVICES: INFORMATION TECHNOLOGY SOFTWARE

• Information Technology Software is defined in section 65B(28) and

also defind by Central Excise Tariff Act for the purpose of Heading

8523, in Chapter 85 almost the same way.

• Placing reliance on Tata Consultancy Service vs. State of Andhra

Pradesh (2002) 178 ELT 22 (SC), the Education Guide has clarified

that sale of pre-packaged or canned software is in the nature of goods

and such ‘sale’ is not part of declared service.

• Prior to 2007, Chapter Heading 8524 covered software and the

prescribed rate was 8%. This was raised to 12% wef 01/03/2008.

• Customized software is exempted at S.No. 27 for Chapter Heading

8523 in the Exemption Notification No.6/2006-CE of 01/03/2006.

Thus, “customized software” is excisable goods but exempted under

Notification issued under the Central Excise Act.

Puloma Dalal 28

DECLARED SERVICES: INFORMATION TECHNOLOGY SOFTWARE

• Can the transaction be both goods and service? Consider the following:

“transaction cannot be for both goods and services.”

“Software whether customized or non-customized, would become goods provided it satisfies the attributes of the goods mainly (a) its utility; (b) capability of being bought and sold and (c) capability of being transmitted, transferred, delivered, stored and processed.”

[Bharat Sanchar Nigam Ltd. vs. UOI 2006 (2) STR 161 (SC)]

“If the software whether customized or non-customized satisfies the rule as ‘goods’, it will also be goods for the purpose of sales tax.

[Infosys Technologies Ltd. 2009 (233) ELT 56 (Mad)]

Puloma Dalal 29

DECLARED SERVICES: INFORMATION TECHNOLOGY SOFTWARE

• While examining whether software supplied by the dealer members to the customers consequent upon end user license agreements amounted to deemed sale or service, it was held that to bring the deemed sale under Article 366(29A)(d) of the Constitution, there must be a transfer of right to use any goods and if no goods were transferred, the question of deeming sale did not arise and in that sense, transaction would be of service and not a sale.

[Infotech Software Dealers Association vs. UOI 2010 (20)STR (Mad)]

• Does licensing of software constitute a transfer of right to use software? Depending on the answer, is it a ‘good’ or a ‘service’? Would it make a difference if it is transferred electronically? Does the means of transfer alter the characteristic of the transaction?

• Does the uncertainty on account of the conflict lead to the conclusion that the safer recourse is dual taxation?

Puloma Dalal 30

DECLARED SERVICES: INTELLECTUAL PROPERTY RIGHT

• Post amendment of Central Sales Tax Act 1956, the definition of ‘sale’ was enlarged to incorporate transactions included in Article 366(29A) of the Constitution

• Thus, for the purpose of the said Article 366(29A) r/w Article 286(3) of the Constitution, intangible property, including trademark, patents etc are treated as ‘goods’

• Under the old regime, transfer or permitting the use or enjoyment of any intellectual property was subjected to service tax, from 10-9-04.

• Whether continuing service tax on temporary transfer etc of intellectual property rights alongside the levy of VAT is legally correct?”

Puloma Dalal 31

DECLARED SERVICES: HIRE PURCHASE OR SYSTEM OF PAYMENT BY INSTALLMENTS

• The Education Guide para 6.5.1 provides that not the delivery of goods on hire purchase, but the activity or service provided in relation to such delivery of goods is a declared service

• Hire Purchase Contract does not involve transfer of title to the goods. However, by fiction of law, it is considered ‘sale’

• Consider the following:

• In equipment leasing hire purchase agreements, there are two different and distinct transactions viz. the financing transaction where interest represents consideration and other charges like lease management fee, processing fee, documentation charge etc. is chargeable to service tax.

[Association of leasing & Financial Service Companies vs. UOI 2010 (20) STR 417 (SC)]

• Citing the above decision, the Education Guide states that financial services that accompany a hire purchase agreement would be treated as declared service.

Puloma Dalal 32

DECLARED SERVICES: HIRE PURCHASE OR SYSTEM OF PAYMENT BY INSTALLMENTS

• In this case, a distinction was drawn between hire purchase transaction and

hire purchase finance relying upon the Supreme Court’s decision in

Sundaram Finance Ltd. vs. State of Kerala 17 STC 480 and held that service

tax is not leviable on hire purchase finance and observed, “a transaction in

which the customer is the owner of the goods and with a view to finance his

purchase, he enters into an arrangement which is in the form of a hire-

purchase agreement with the financier, but in substance evidences a loan

transaction subject to hiring agreement under which the lender is given the

license to seize goods”.

[Bajaj Auto Finance Ltd. vs. CCE, Pune 2007 (7) STR 423 (Tri.-Mum)

upheld by the Supreme Court at 2008 (10)STR 433 (SC)].

• Above all, in terms of BSNL v UOI (2006) 2 STR 161 (SC) out of three types

of composite contracts, namely, hire purchase contracts, works contracts and

catering contracts, splitting of the service and supply of goods is

constitutionally permitted only in case of the latter two. Is the levy of 10% on

the value of hire purchase contracts legal? Puloma Dalal 33

DECLARED SERVICES: REFRAINING FROM, TOLERATING OR DOING AN ACT

• An activity of: – Agreeing to the obligation to refrain from an act

– Agreeing to the obligation to tolerate an act or a situation

– Agreeing to the obligation to do an act.

• Consideration paid for a non-compete agreement is intended to be covered as declared service as per Education Guide para 6.7.1

• Whether various other transactions such as forfeiture of any security deposit or advance for non-fulfillment of commitment would also be covered by this declared service? Education Guide at 2.3.2 has stated that since service becomes taxable on an agreement to provide a service, such forfeited deposit would represent consideration for the agreement that was entered into for provision of service.

• Is this in contradiction with the definition of service?

Puloma Dalal 34

INTERPRETATION ISSUES

The Negative List and Exemption Notification:

Puloma Dalal 35

INTERPRETATION ISSUES:

NEGATIVE LIST V/S EXEMPTION NOTIFICATION

• Negative list is a new concept and an exception to the charge itself

• Whereas Exemption Notification is not an executive act but a claim of delegated or

conditional legislation (UOI v Jalyan Udjog (1993) 68 ELT 9( SC))

• Therefore, equating Negative List with Exemption Notification may not be correct.

Negative List should be interpreted along the lines that a charging section is

interpreted.

• Prima facie, items listed in the Negative List should be capable of being effectuated

and unduly strict construction may narrow its compass.

• In case of Magus Construction Pvt. Ltd. vs. UOI 2008 (11) STR 225 (Gau), the court

laid stress on making distinction between comprehensive approach and selective

approach and observed that:

“under the concept of comprehensive approach all services are taxable and it is the

system of selective approach which India has adopted. This distinction needs to be

kept in mind when we proceed further”.

• Therefore, when conceptual shift is made to what is globally known as catch all

model, there is a need to examine principles governing interpretations of exemption

notification and follow a well-balanced approach based on facts of each case or

situation. Puloma Dalal 36

INTERPRETATION:

GENERALLY FOLLOWED PRINCIPLES

• Objective or context – relevant and a guiding factor

• Eligibility to be construed strictly, fulfillment of conditions may be viewed liberally

• The Department cannot add any condition on presumed legislative intent.

• An item not covered in exclusion clause does not necessarily mean it is included.

• Benefit of exemption cannot be claimed on the basis of equality.

• Assessee has an option to follow a beneficial notification when more than one notification applies

• Notification has to be read as a whole

• Burden of proving the eligibility falls on the assessee

Puloma Dalal 37

INTERPRETATION: GENERALLY FOLLOWED PRINCIPLES

CASE LAW ILLUSTRATIONS

• It is well settled law that exemption, being an exception to taxation, has to be construed strictly. In order to avail the benefit of exemption, the eligibility criteria provided in the Notification has to be fulfilled.

• In Tata Iron & Steel Co. Ltd. (2005) 4 SCC 272 (SC), the Supreme Court held that –

“The principles as regards construction of an exemption notification are no longer res integra; whereas the eligibility clause in relation to an Exemption Notification is given strict meaning wherefor the Notification has to be interpreted in terms of its language. Once an assessee satisfies the eligibility clause, the exemption clause therein may be construed literally. An eligibility criteria, therefore deserves a strict construction, although construction of a condition thereof may be given a liberal meaning if the same is directory in nature.”

Puloma Dalal 38

INTERPRETATION: GENERALLY FOLLOWED PRINCIPLES

CASE LAW ILLUSTRATIONS

• Similarly, in CCE New Delhi vs. Hari Chand Shri Gopal, 2010 (260) ELT 3 (SC), the Supreme Court held that –

“The law is well settled that a person who claims exemption or concession has to establish that he is entitled to that exemption or concession. A provision providing for an exemption, concession or exception, as the case may be, has to be construed strictly with certain exceptions depending upon the settings on which the provision has been placed in the Statute and the object and purpose to be achieved. If exemption is available on complying with certain conditions, the conditions have to be complied with. The mandatory requirements of those conditions must be obeyed or fulfilled exactly, though at times, some latitude can be shown, if there is a failure to comply with some requirements which are directory in nature, the non-compliance of which would not affect the essence or substance of the notification granting exemption.”

Puloma Dalal 39

INTERPRETATION: GENERALLY FOLLOWED PRINCIPLES

CASE LAW ILLUSTRATIONS

• Gujarat State Fertilizer Company vs. CCE 1997 (91) ELT 3 (SC):

“It is now well settled by a catena of decisions of this court that for

deciding whether an exemption notification gets attracted on the

facts of a given case, the express language of the exemption

notification has to be given its due effect”

• CC vs. Perfect Machine Tool Co. Ltd. 96 ELT 214:

“A particular item not expressly excluded from exemption

notification, is not necessarily to be treated to have been included

therein”

Also refer to • CCE v Parental Drug (India) Ltd. (2009) 236 ELT 625 (SC)

• CC v Tullow India Operation Ltd. (2005) 189 ELT 401 (SC)

Puloma Dalal 40

THE NEGATIVE LIST

Issues with select items in

Puloma Dalal 41

SELECT ITEMS IN THE NEGATIVE LIST: ISSUES

AGRICULTURE

• Services relating to agriculture or agricultural produce by way of:

Agricultural operations directly related to production of any agricultural produce

including cultivation, harvesting, threshing, plant protection or seed testing.

[Section 66D(d)(i)]

• Do agricultural operations have to be carried out in the farm only?

• Is the activity of ‘dairying’ and ‘pisciculture’ covered by the expression “agricultural

operations”?

• Which other activities would be covered by the expression, “rearing of all life-forms of

animals except rearing of horses, for food, fibre, fuel, raw material or other similar

products?”

• If agricultural produce includes various dairy products like milk, butter, cheese etc.,

should services of storage for these products be included in the “Negative List”?

• Consider the following decision: CCE vs. Himalayan Co-op. Milk Product Union Ltd.

2000 (122) ELT 327 (SC)

• Should the decision in Collector of Customs vs. Perfect Machine Tools Co. Ltd. 1997

(96) ELT 214 (SC) apply to the facility of cold storage?

Puloma Dalal 42

SELECT ITEMS IN THE NEGATIVE LIST: ISSUES:

TRADING OF GOODS

• Trading of goods in common parlance would mean buying and selling of goods.

• Is it a service at all to be included in Negative List?

– Ancillary service of a commission agent, clearing and forwarding agent, consignment agent etc. not covered – clarified by the Government in Education Guide para 4.5.1.

– Forward contracts, commodity futures are trading in goods also clarified by the Education Guide paras 4.5.2, 4.5.3 and 4.14.9

• Do ‘goods’ sold by way of electronic transfer or internet download amount to trading in goods?

Puloma Dalal 43

SELECT ITEMS IN THE NEGATIVE LIST: ISSUES:

RENTING OF RESIDENTIAL DWELLING FOR USE AS RESIDENCE

• Although residential dwelling is not defined in law, in terms of decided cases, dwelling means a place of living for an indefinite or a long period.

• Under the earlier regime, hotel accommodation service introduced from 01/05/2011 was described as short-term accommodation service. The period of occupation in order to be covered by this entry was stated as less than 3 months.

• Given these facts, would typical lodges providing cheaper accommodation on a monthly basis be covered by the above expression “residential dwelling,” if they are not covered by entry no.18 in exemption notification no.25/2012-ST? (Exemption is available to hotel accommodation having a tariff below rupees one thousand per day or equivalent).

• Would “service apartments” provided to corporate bodies for the strict use of residence by their employees under leave & license arrangements qualify under the above entry in the Negative List?

Puloma Dalal 44

SELECT ITEMS IN THE NEGATIVE LIST: ISSUES: EDUCATION AS A PART OF A CURRICULUM FOR OBTAINING A QUALIFICATION

RECOGNIZED BY ANY LAW FOR THE TIME BEING IN FORCE

• Interpretation of the phrase “recognized by any law for the time being in force” is challenging as no explanation or definition is provided by the law.

• Education Guide para 4.12.1 reads as follow:

“What is the meaning of 'education as a part of curriculum for obtaining a qualification recognized by law'?

It means that only such educational services are in the negative list as are related to delivery of education as 'a part' of the curriculum that has been prescribed for obtaining a qualification prescribed by law. It is important to understand that to be in the negative list the service should be delivered as part of curriculum. Conduct of degree courses by colleges, universities or institutions which lead grant of qualifications recognized by law would be covered. Training given by private coaching institutes would not be covered as such training does not lead to grant of a recognized qualification.”

Puloma Dalal 45

SELECT ITEMS IN THE NEGATIVE LIST: ISSUES:

EDUCATION AS A PART OF A CURRICULUM FOR OBTAINING A

QUALIFICATION RECOGNIZED BY ANY LAW FOR THE TIME BEING IN FORCE

• Can any of the following decisions hold good in terms of the new system?

• “Education has a larger scope. Education may include coaching or training and not vice versa. Education is a broader term which is a process of development of personality of body, mind and intellect”.

Magnus Society 2009 (13) STR 509 (Tri.-Bang)

• “We find that education in the instant case is not business. Primary object of GLIM is to impart education. Profit making is not its main motive. Refrain of the several judicial authorities cited is that profit motive characterizes a commercial concern”.

Great Lakes Institute of Management vs. CST 2008 (10) STR 202 (Tri.-Chennai)

• Others:

• Administrative Staff College of India 2009 (14) STR 341 (Tri.-Bang)

• Malappuram District Parallel College Association 2006 (2) STR 321 (Ker)

Puloma Dalal 46

SELECT ITEMS IN THE NEGATIVE LIST: ISSUES:

EDUCATION AS PART OF AN APPROVED VOCATIONAL COURSE

Approved vocational education course as defined in s. 65B(11) means,-

“(1) a course run by an industrial training institute or an industrial training centre affiliated to the National Council for Vocational Training offering courses in designated trades notified under the Apprentices Act, 1961 (52 of 1961); or

(2) a Modular Employable Skill Course, approved by the National Council of Vocational Training, run by a person registered with the Directorate General of Employment and training, Union Ministry of Labour and Employment; or

(3) a course run by an institute affiliated to the National Skill Development Corporation set up by the Government of India.”

• Consider recently issued Circular No.164 dated 28/08/2012

• “The training shall be considered as commercial training or coaching because the institute imparts skill or knowledge on the subject of insurance….. Such training imparted is a vocational training and would be eligible for the benefit of exemption under the relevant notification”

[Pasha Educational Training Institute 2009 (14) STR 481 (Tri.)]

• “The company is engaged into commercial pilot training……… The training does not directly result into an employment or even enable trainee to undertake self-employment”

[CAE Flight Training (India) Pvt. Ltd. 2010 (18) STR 785 (AAR)]

Puloma Dalal 47

SELECT ITEMS IN THE NEGATIVE LIST: ISSUES EXTENSION OF DEPOSITS, LOANS OR ADVANCES

(where consideration is represented by way of interest or

discount)

• Whether premium paid on redemption of debenture

issued at par would qualify to be considered interest?

• Whether foreclosure/pre-closure charge recovered by

a bank when a loan account is paid up earlier than its

term?

Puloma Dalal 48

MEGA EXEMPTION

Notification 25/2012-ST

Puloma Dalal 49

EXEMPTIONS: SELECT ENTRIES UNDER NOTIFICATION 25/2012-ST

• Charitable institutions registered under section 12AA of Income Tax Act,

1961 are exempt at entry 4. Whether charitable institutions registered under

12A and 10(23C) do not qualify under the said entry?

• “Charitable activities” as defined in clause (K) of the Notification includes:

Advancement of any other object of general public utility upto a value of

Rs.25 lakh in a financial year provided the value of such activities does not

exceed Rs.25 lakh in the preceding year. (For F.Y. 2012-13, the limit is

Rs.18.5 lakh).

Would voluntary contribution, interest income and other income not

relating to the above activity also form part of the determining rupees 25

lakh? Further, the expression, “any other object of general public utility”

also is a subject matter of interpretation, although “general public” at (q) in

the said notification is defined as “the body of people at large sufficiently

defined by some common quality of public or impersonal nature.”

Puloma Dalal 50

EXEMPTIONS: SELECT ENTRIES UNDER NOTIFICATION 25/2012-ST

• Renting of precincts of religious place meant for general public is exempt at

entry-5. The religious place like temple may be otherwise meant for the

general public but the surrounding area forming part of the temple property

is used for any wedding function. Would it qualify for exemption? The

term ‘precinct’ is not defined.

• Training or coaching in recreational activities continues to enjoy exemption

(entry 8). If a person undergoes training and coaching to become a

professional singer or a dancer, would it still be considered recreational

activity?

• Services provided by way of auxiliary educational services or renting of

immovable property to only an education institution is exempted in respect

of education exempt (entry 9). The terms “educational institution” and

“education exempted from service tax” are not defined in the Notification

25/2012 or in the Act. Does it necessarily mean education is exempted

under section 66D at entry (l)? Clarification is required to avoid dispute in

this regard.

Puloma Dalal 51

EXEMPTIONS: SELECT ENTRIES UNDER NOTIFICATION 25/2012-ST

• Single residential unit otherwise than as a part of residential complex is exempt (entry 12(f)).

• Single residential unit means a self-contained residential unit which is designed for use, fully or principally, for residential purpose for one family.

• In turn, residential complex is defined as any complex comprising of a building or buildings having more than one single residential unit.

• Whether construction of an individual house in a society or a residential colony or in any closed complex would qualify for exemption? The following decisions may be considered: – In re Hare Krishna Developers 10 STR 357 (AAR)

– Macro Marvel Projects vs. CCE 12 STR 603 (Tri.)

• Both the decisions had different conclusions. In the former it was held that if there were more than 12 units in a residential colony, it would mean residential complex whereas in the latter case, it was held otherwise.

Puloma Dalal 52

BUNDLED SERVICES

Puloma Dalal 53

BUNDLED SERVICES

• What does a bundled service mean?

Bundled service means a bundle of provisions of

various services wherein an element of provision of

one service is combined with an element or elements

of provision of any other service or services

(Explanation in s. 66F)

Puloma Dalal 54

BUNDLED SERVICES PRINCIPLES OF INTERPRETATION (S. 66F)

• Unless otherwise specified reference to a service i.e. main

service shall not include reference to a service which is used for

providing main service.

– Example: Transportation of goods by inland waterways is in the Negative List –

Agent booking for such transportation is not covered by this.

• Most specific description shall be preferred over general

description.

– Example: In the context of a real estate agent, immovable property related

service is a more specific description than service of an intermediary.

– Under the Negative-List regime, description or classification of a service is

required because it still exists in: Negative List of services, Exemption

Notification, List of declared services, Place of Provision Rules, 2012,

Abatement Notification, Reverse charge Notification , CENVAT Credit Rules,

2004, Service Tax Rules etc

Puloma Dalal 55

BUNDLED SERVICES PRINCIPLES OF INTERPRETATION (S. 66F)

• While determining the taxability of a bundled service, the rules stated below

are subject to the rule that specific description prevails over general

description.

– If various elements of a bundled service are naturally bundled in the

ordinary course of business, it would be treated as a single service.

– Example: A hotel providing breakfast or airline providing meal on board

are naturally bundled to include accommodation or transportation by air

with a catering service.

– If bundled services are not naturally bundled in the ordinary course of

business, it shall be treated as service attracting highest rate of service tax.

Puloma Dalal 56

BUNDLED SERVICES GREY AREAS

• Along with service of transportation of goods by

waterways or air, a host of services are provided by

shipping lines and freight forwarders. If freight per se

does not attract service tax, whether other services

could be treated as incidental?

• In case of multi-modal transport service providers,

which mode gives the essential character to the

bundled service?

Puloma Dalal 57

BUNDLED SERVICES: GUIDANCE ON UK VAT: MULTIPLE/COMPOSITE SUPPLIES

• Identifying whether a particular transaction is a single

or multiple supply:

– What does the recipient receive for the consideration?

– How is the supply advertised?

– Is there a contract/agreement which describes the supply?

– Is the other component one which enhances the principal or

one which stands on its own as sought by the recipient?

– What does the invoice show?

Puloma Dalal 58

BUNDLED SERVICES: GUIDANCE ON UK VAT: MULTIPLE/COMPOSITE SUPPLIES

• How to determine when services are bundled in the ordinary course of business or adopted as frequent a business practice.

– Perception of consumer/receiver

– Majority service providers of a specific service providing similar bundled service

– Nature of service - like ancillary services alongside the main service

• Indicators of single supply.

– Manner of invoicing (underlying component rather than description)

– Advertisements as package

– Non-availability of separate components

– Ordinary/frequent business practice

– Separate elements integral, ancillary or incidental to overall supply.

Puloma Dalal 59

BUNDLED SERVICES: GUIDANCE ON UK VAT: MULTIPLE/COMPOSITE SUPPLIES

• Multiple supply = more than one supply for a single payment where the components are separate, principal supplies in themselves

• Indicators of a multiple supply

– Separate pricing/invoicing

– Components are available separately

– Existence of a time differential between parts of the supply

– Components are not interdependent/connected

– More than one supplier for different parts of the service

http://www.hmrc.gov.uk/manuals/vatscmanual/VATSC80000.htm

Puloma Dalal 60

BUNDLED SERVICES: GUIDANCE ON UK VAT: MULTIPLE/COMPOSITE SUPPLIES

• Firstly, it is a question of law as applied to the facts whether a supply is multiple or composite.

• Secondly, the question must be answered by the application of common sense to the substance and reality of the matter.

• Thirdly, in certain cases it may be difficult on a practical level to apportion the consideration between the various elements in a supply and this may indicate that this is rather a composite supply.

Commissioners of Customs and Excise v MD and RW Jeffs (trading as J & J Joinery) [1995] STC 759

Puloma Dalal 61

BUNDLED SERVICES: GUIDANCE ON UK VAT: MULTIPLE/COMPOSITE SUPPLIES

• Landmark case: Card Protection Plan v Commissioners of Customs and Excise (Case C-349/96) [1999] STC 270

– The service provided was an assistance package to customers in case of the loss of personal items - mainly credit cards, but also including keys, passports or insurance documents. They also provided an insurance-backed indemnity for fraudulent use of the cards and other forms of assistance, such as medical, where the loss occurred away from the customer’s home. The insurance provider was the Continental Assurance Company.

– The question in this case was about whether this was a single or multiple supply and whether the package was an exempt supply of insurance or a taxable supply of ‘convenience’ - the customers would be paying for someone else to cancel their cards/order new cards etc.

Puloma Dalal 62

BUNDLED SERVICES: GUIDANCE ON UK VAT: MULTIPLE/COMPOSITE SUPPLIES

• Landmark case: Card Protection Plan v Commissioners of Customs and Excise (Case C-349/96) [1999] STC 270: The Court’s decision:

– The court considered that if anyone asked what the essential feature of the scheme or its dominant purpose was, or in other words, why objectively people are likely to want to join it, it was to obtain insurance cover against loss arising from the misuse of credit cards or other documents

– The other features of the scheme, such as card registration and obtaining replacement cards, were found to be ancillary to the main objective of the scheme i.e. the financial protection against loss of the card.

– Accordingly, Card Protection Plan was deemed to be making a single supply of exempt services.

Puloma Dalal 63

BUNDLED SERVICES: GUIDANCE ON UK VAT: MULTIPLE/COMPOSITE SUPPLIES

• Landmark case: Card Protection Plan v Commissioners of Customs and

Excise (Case C-349/96) [1999] STC 270: THE ECJ’s GUIDANCE

– No definitive guidelines possible: fact-based inquiry

– Regard must be given to all the circumstances in which that transaction takes

place

– Each supply of a service must normally be regarded as distinct and independent

– A supply that comprises a single service from an economic point of view should

not be artificially split

– There is a single supply in cases where one or elements are to be regarded as

ancillary services. An ancillary service is defined as something that does not

constitute for customers an aim in itself but is a means of better enjoying the

principal service supplied

– The fact that a single price is charged is not decisive. If the circumstances

indicate that customers intend to purchase two or more distinct services a single

price will not prevent these being treated as separate supplies with different

liabilities applying, if appropriate, to those services

Puloma Dalal 64

BUNDLED SERVICES: GUIDANCE ON UK VAT: CASE LAW EXAMPLES

• In Mander Laundries (unreported):

– the proprietor of a launderette argued that the money he received from operating

his shop should be apportioned between the standard rated laundering facilities

and the zero-rated supply of water, gas and electricity.

– The tribunal rejected this argument. A customer going into the launderette with a

pile of dirty washing had in mind to depart with a parcel of clean clothes. The

provision of water, gas and electricity were an integral part of the deal. Thus it

was a composite supply for VAT purposes.

• In Commissioners of Customs and Excise v Madgett & Baldwin (trading as Howden

Court Hotel) [1998] STC 1189

– The European Court of Justice found that an hotelier who, in return for a

package price, habitually offers his customers in addition to accommodation,

return transport between certain distant pick-up points and the hotel, and a

coach excursion during their stay, these transport services being bought in from

third parties, was a travel agent and not merely a hotel proprietor.

Puloma Dalal 65

BUNDLED SERVICES: GUIDANCE ON UK VAT: CASE LAW EXAMPLES

• In Commissioners of Customs and Excise v Wellington Private Hospital Ltd

[1997] STC 445

– The question was whether the supply of drugs in a private health hospital and the

supply and fitting of prostheses were an integral part of the exempt supply of

health care.

– The Court of Appeal said that it was necessary to determine whether one

element of the transaction was so dominated by another element so as to lose a

separate identity as a supply for fiscal purposes. In such a case, the dominant

element was the only supply. However, here there was no dominant supply. The

supply of the drugs and the prostheses were part of the treatment that were not

optional. They had to be supplied to the patient to get better. Thus, these were

separate supplies.

– The court found that care and treatment in a hospital involved multiple supplies.

In addition, a patient paid separately for the drugs, and the drugs were physically

and economically dissociable from other items charged for.

Puloma Dalal 66

THANK YOU

Puloma Dalal 67