Embed Size (px)

Citation preview

Nebraska Small Credit Union Resource Guide 2.0

Scott Sullivan 2014

Nebraska Small Credit Union Resource Guide 2.0 With a large percentage of Nebraska credit unions designated as small credit unions, the Nebraska Credit Union League has dedicated many resources to help these credit unions thrive, grow and continue to succeed. By providing targeted education and training, regulatory and compliance assistance, Hot Topics notifications and operational guidance, we are poised to assist in meeting the needs of all smaller institutions and help them address their unique challenges and opportunities.

Dues Supported Services

Small Credit Union Dues Reduction Program

The Nebraska Credit Union League provides credit unions with $10 million or less in assets a 50% reduction in standard League dues. The reduction does not apply to CUNA dues. CUNA offers their own small credit union discount program.

Small Credit Union Committee

The mission of this committee is to ensure first hand insight into the needs of small credit unions, giving them an empowering voice. The committee is appointed by the Nebraska Credit Union League Board Chairman and is comprised of credit union leaders from across the state. The members serve as a contact in their area, facilitating quarterly meetings to provide training and networking opportunities.

Small Credit Union Training & Education

Nebraska Credit Union League offers training specific to the needs of small credit unions. Training is offered throughout the year at workshops, roadshows and area chapter meetings.

No Cost Registration for League Conferences

Nebraska Credit Union League affiliated credit unions with $15 million in assets or less (based on assets as of year-end) are allowed free registration to major League conferences.

Small Credit Union Chapter Area Meetings

Regular meetings are held in respective chapter areas focusing on small credit union issues, and providing an excellent opportunity to network. The meeting is coordinated by the Small CU Committee member representing the chapter area and is available free or low-cost.

Small Credit Union Consulting

Nebraska credit union League is very familiar with the day-to-day operational issues facing small credit unions. The League is available to provide a host of consultative support to small credit unions.

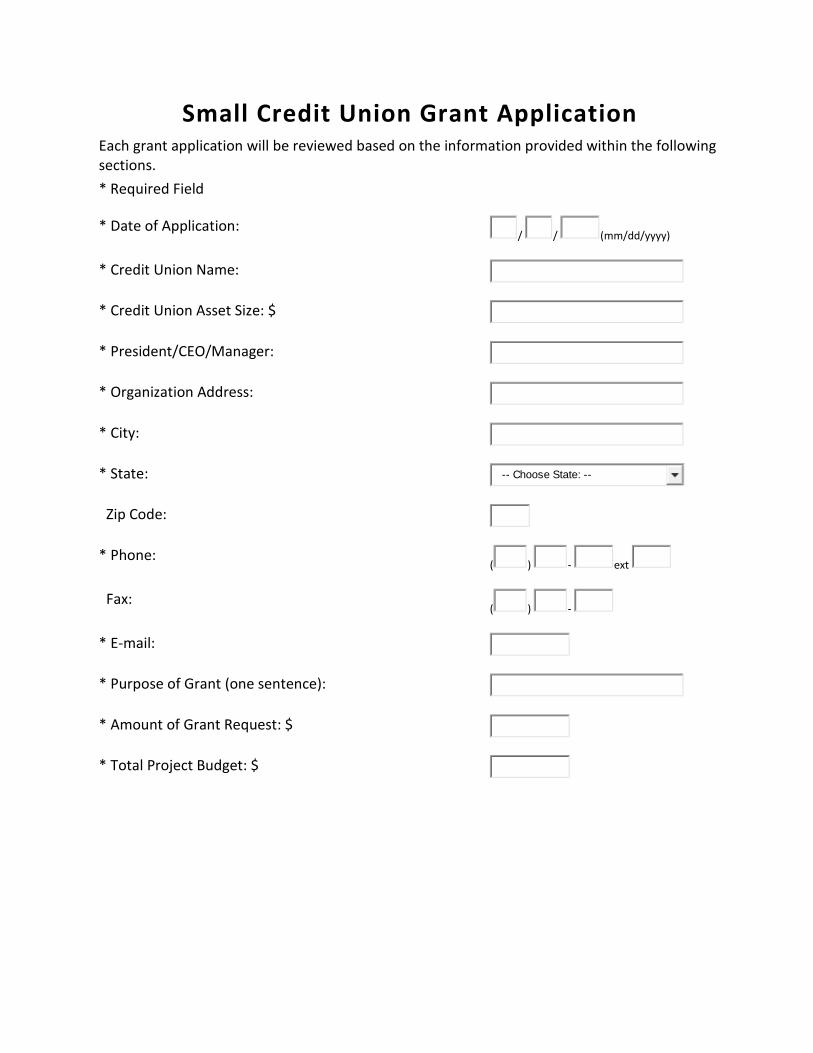

Small Credit Union Operation, Planning & Technology Grants

The League provides support for Nebraska credit unions with $15 million or less in assets through Operational, Planning, and Technology Grants that will measurably assist the credit union in serving its members. As Grant funds are limited, interested credit unions are encouraged to apply early in the year to optimize their chances of securing a grant. Grants are capped at $1,500 per credit union.

To apply:

1. The credit union CEO must submit the online application detailing the request and how it will assist in the credit union's operations.

2. Include supporting materials including quotes or invoices as available. 3. Grant applications are reviewed on a first come, first serve basis as funding is available.

Priority may be given to credit unions who have not been awarded a League Grants in recent years.

4. Grant checks are sent to recipients upon receipt of the paid invoice by the League.

Please contact Amy Shaw, Director of League Initiatives, at 800-950-4455 ext.207 or [email protected] for more information.

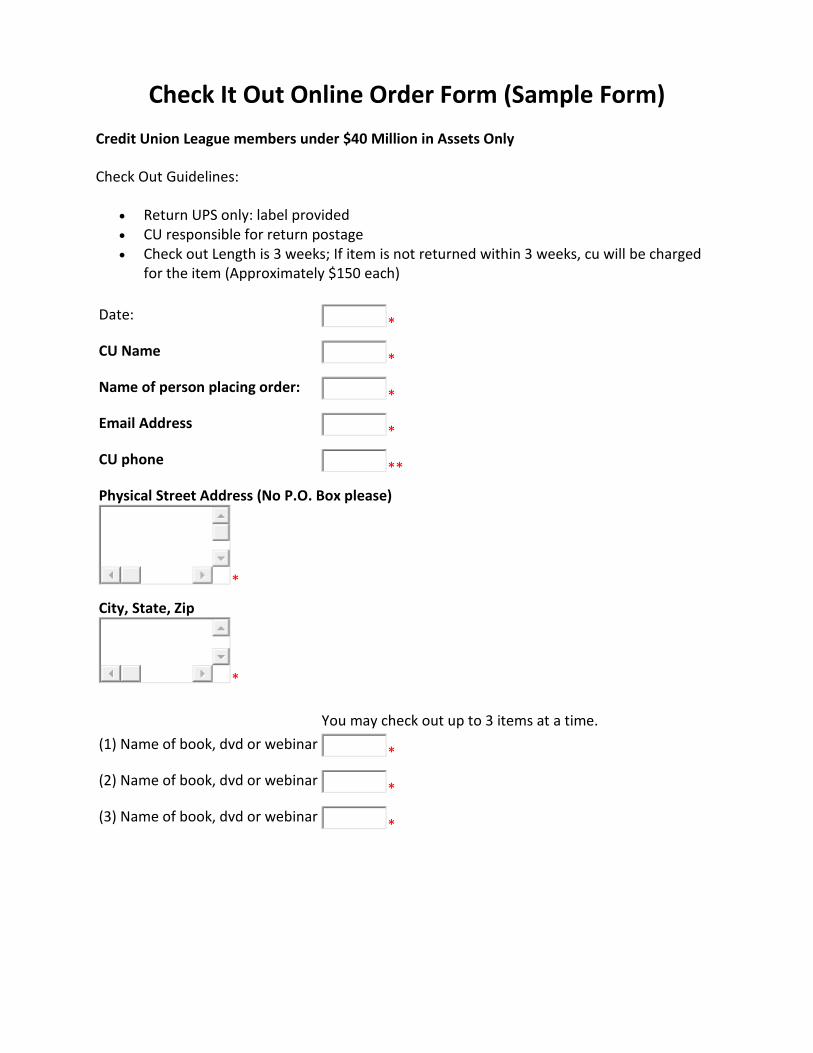

Check-It-Out Library

Providing on-going education opportunities, the Check-It-Out Library provides inexpensive and convenient access to credit union books, webinars, and DVDs. There is no charge with the exception of shipping the items back to the League. The service is available to affiliated credit unions under $40 million in assets. Contact Amy Shaw at 800-950-4455 ext. 207 or [email protected] for additional information.

Tools & Handouts

We continuously strive to provide helpful resources and tools to help small credit unions grow and thrive. The League offers many handouts, a required policies list, and several presentations from various small credit union workshops held.

CUNA CPD Online Training Program

CPD Online is an online training resource offered through CUNA that is specific to the credit union industry’s training needs. This online training program offers over 350 training courses that include everything from Accounting, Budgeting and Finance courses to Volunteer courses and everything in between. Preferred pricing is available for credit unions with assets under $50M and even deeper discounts for credit unions under $20M in assets.

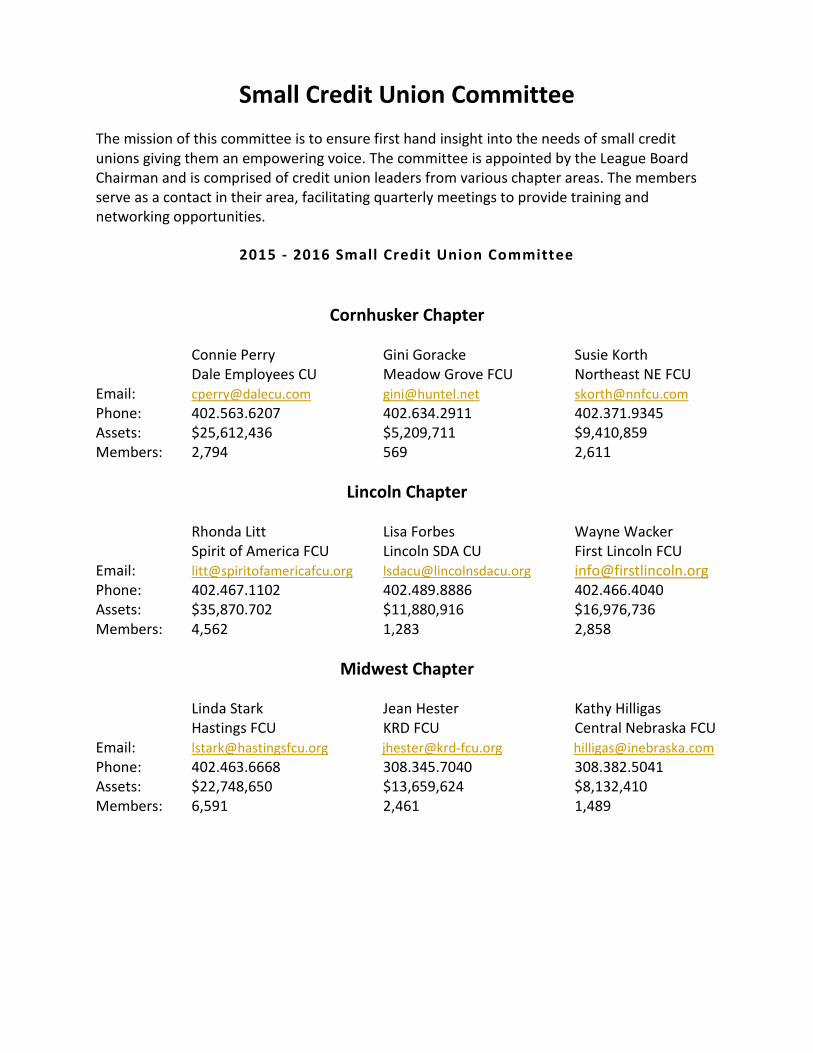

Small Credit Union Committee The mission of this committee is to ensure first hand insight into the needs of small credit unions giving them an empowering voice. The committee is appointed by the League Board Chairman and is comprised of credit union leaders from various chapter areas. The members serve as a contact in their area, facilitating quarterly meetings to provide training and networking opportunities.

2015 - 2016 Small Credit Union Committee

Cornhusker Chapter

Connie Perry Gini Goracke Susie Korth Dale Employees CU Meadow Grove FCU Northeast NE FCU

Email: [email protected] [email protected] [email protected] Phone: 402.563.6207 402.634.2911 402.371.9345 Assets: $25,612,436 $5,209,711 $9,410,859 Members: 2,794 569 2,611

Lincoln Chapter

Rhonda Litt Lisa Forbes Wayne Wacker Spirit of America FCU Lincoln SDA CU First Lincoln FCU

Email: [email protected] [email protected] [email protected] Phone: 402.467.1102 402.489.8886 402.466.4040 Assets: $35,870.702 $11,880,916 $16,976,736 Members: 4,562 1,283 2,858

Midwest Chapter

Linda Stark Jean Hester Kathy Hilligas Hastings FCU KRD FCU Central Nebraska FCU

Email: [email protected] [email protected] [email protected] Phone: 402.463.6668 308.345.7040 308.382.5041 Assets: $22,748,650 $13,659,624 $8,132,410 Members: 6,591 2,461 1,489

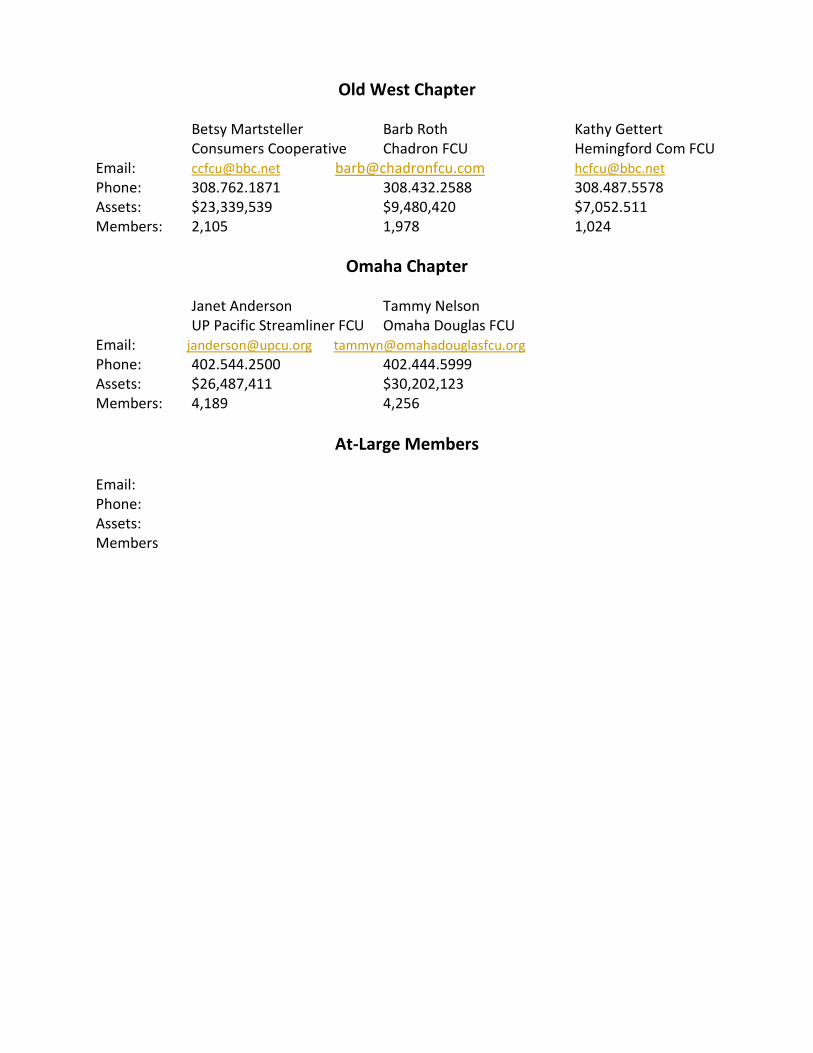

Old West Chapter

Betsy Martsteller Barb Roth Kathy Gettert Consumers Cooperative Chadron FCU Hemingford Com FCU

Email: [email protected] [email protected] [email protected] Phone: 308.762.1871 308.432.2588 308.487.5578 Assets: $23,339,539 $9,480,420 $7,052.511 Members: 2,105 1,978 1,024

Omaha Chapter

Janet Anderson Tammy Nelson UP Pacific Streamliner FCU Omaha Douglas FCU

Email: [email protected] [email protected] Phone: 402.544.2500 402.444.5999 Assets: $26,487,411 $30,202,123 Members: 4,189 4,256

At-Large Members Email: Phone: Assets: Members

Check It Out Online Order Form (Sample Form) Credit Union League members under $40 Million in Assets Only

Check Out Guidelines:

• Return UPS only: label provided • CU responsible for return postage • Check out Length is 3 weeks; If item is not returned within 3 weeks, cu will be charged

for the item (Approximately $150 each)

Date: * CU Name * Name of person placing order: * Email Address * CU phone ** Physical Street Address (No P.O. Box please)

* City, State, Zip

*

You may check out up to 3 items at a time. (1) Name of book, dvd or webinar * (2) Name of book, dvd or webinar * (3) Name of book, dvd or webinar *

Small Credit Union Grant Application Each grant application will be reviewed based on the information provided within the following sections. * Required Field

* Date of Application: / / (mm/dd/yyyy)

* Credit Union Name:

* Credit Union Asset Size: $

* President/CEO/Manager:

* Organization Address:

* City:

* State: -- Choose State: --

Zip Code:

* Phone: ( ) - ext

Fax: ( ) -

* E-mail:

* Purpose of Grant (one sentence):

* Amount of Grant Request: $

* Total Project Budget: $

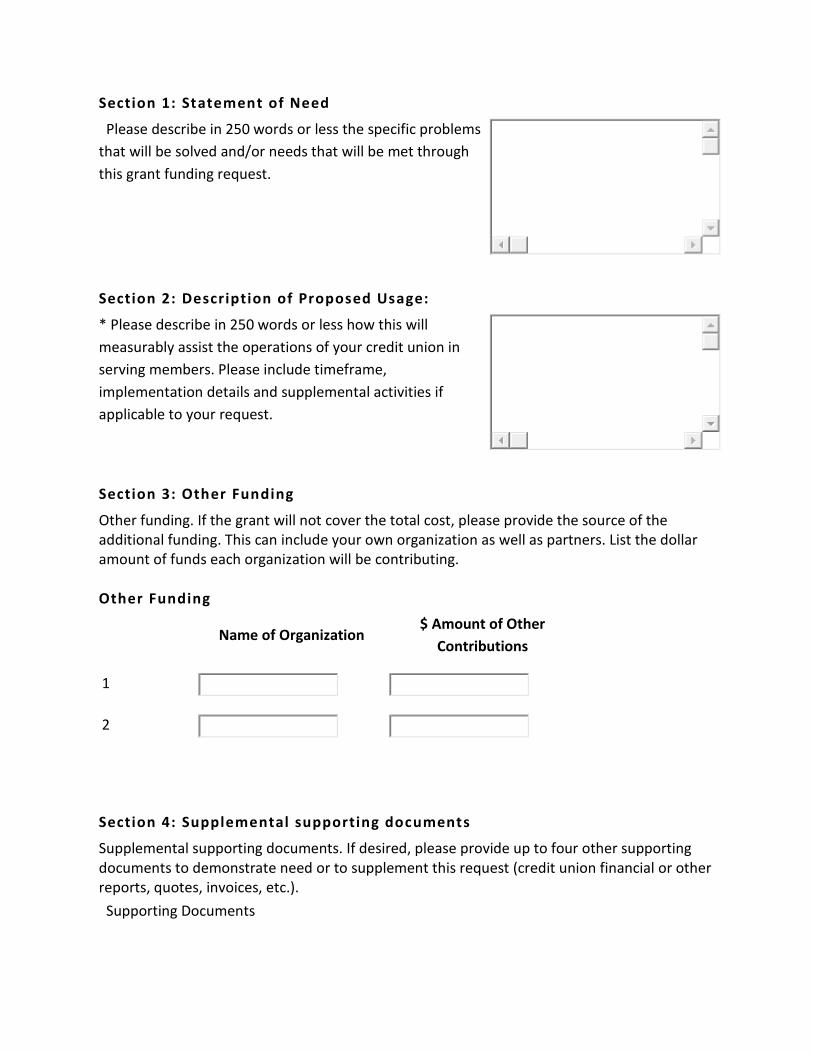

Section 1: Statement of Need

Please describe in 250 words or less the specific problems that will be solved and/or needs that will be met through this grant funding request.

Section 2: Description of Proposed Usage:

* Please describe in 250 words or less how this will measurably assist the operations of your credit union in serving members. Please include timeframe, implementation details and supplemental activities if applicable to your request.

Section 3: Other Funding

Other funding. If the grant will not cover the total cost, please provide the source of the additional funding. This can include your own organization as well as partners. List the dollar amount of funds each organization will be contributing.

Other Funding

Name of Organization $ Amount of Other

Contributions

1

2

Section 4: Supplemental supporting documents

Supplemental supporting documents. If desired, please provide up to four other supporting documents to demonstrate need or to supplement this request (credit union financial or other reports, quotes, invoices, etc.). Supporting Documents

Tools & Handbooks

• Compliance Support - PolicyWorks • Yearly Report Checklist for Nebraska Credit Unions • Required Policies List • CEO Handbook • Consulting Services • CU Services & Products Implementation Resources • Low Income Designation Benefits • Cloud Computing • CU Analyzer

Compliance Support – PolicyWorks At the League we understand the challenges credit unions, especially smaller ones continue to face in meeting todays compliance demands. That is why we have partnered with PolicyWorks. PolicyWorks is a ‘Best in Class’ credit union compliance company. They have the resources, vision and experience necessary to help credit unions resolve their most challenging compliance issues Nebraska credit unions get personal and timely compliance support. The service is simple to use and is provided at no cost. Start using it by calling 866.499.7350 or email at [email protected] For additional information visit: www.PolicyWorksLLC.com PolicyAid is a comprehensive, online policy library that helps credit unions develop and maintain policies as regulations change Policies are updated on a quarterly basis to reflect any new and/or amended regulation. The policies are available for credit unions to download in Word format so they can adapt them to fit the credit union’s operation PolicyWorks trained professionals study the regulations and review the footnotes and fine print in order to construct compliant policies, which frees up credit unions so they can concentrate on the day-to-day needs of their members.

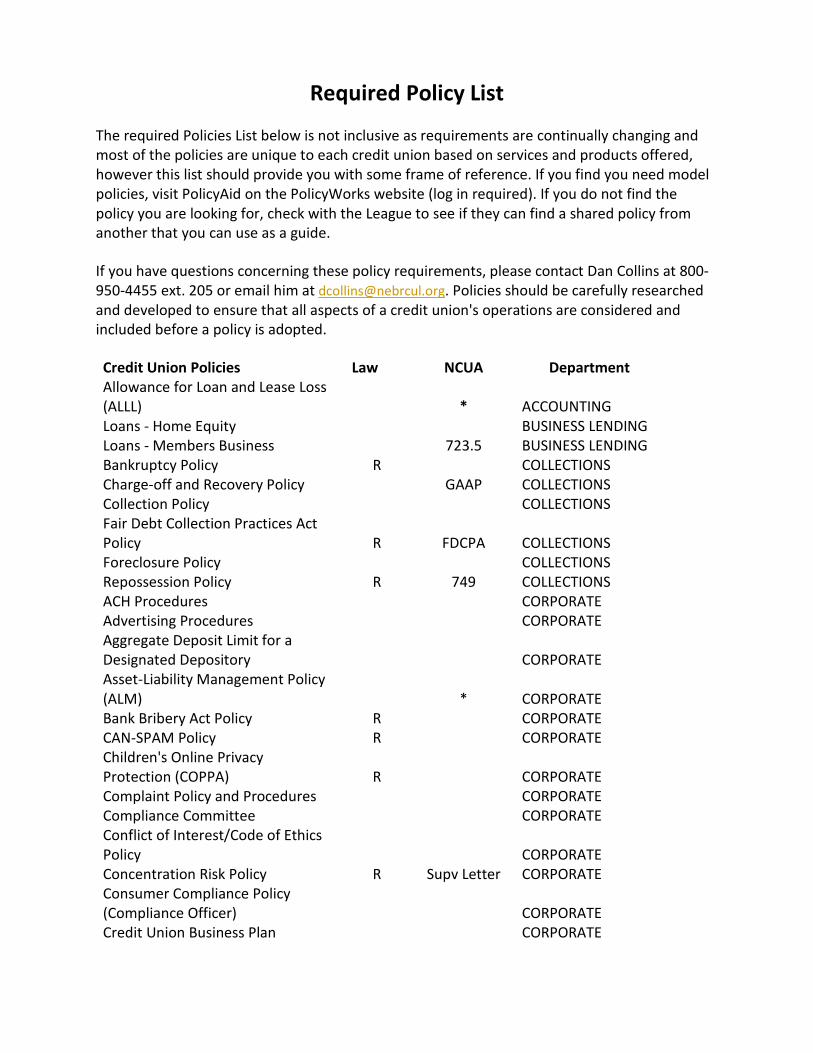

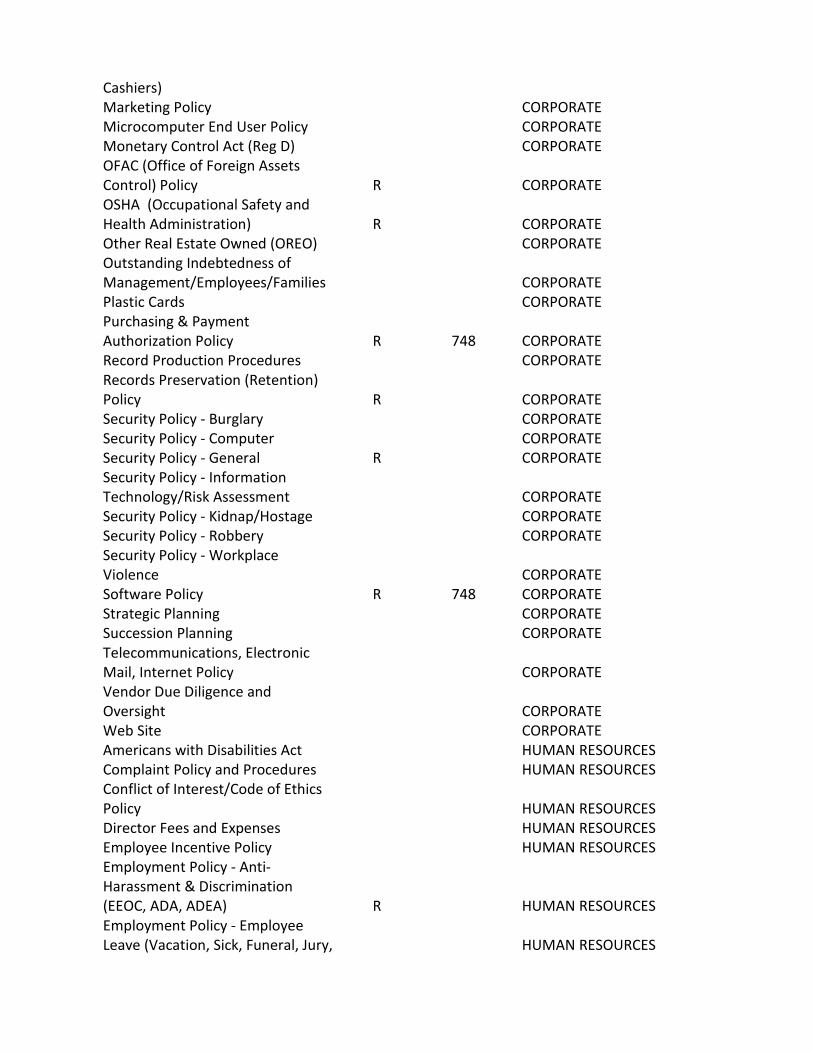

Required Policy List

The required Policies List below is not inclusive as requirements are continually changing and most of the policies are unique to each credit union based on services and products offered, however this list should provide you with some frame of reference. If you find you need model policies, visit PolicyAid on the PolicyWorks website (log in required). If you do not find the policy you are looking for, check with the League to see if they can find a shared policy from another that you can use as a guide.

If you have questions concerning these policy requirements, please contact Dan Collins at 800-950-4455 ext. 205 or email him at [email protected]. Policies should be carefully researched and developed to ensure that all aspects of a credit union's operations are considered and included before a policy is adopted.

Credit Union Policies Law NCUA Department Allowance for Loan and Lease Loss

(ALLL)

* ACCOUNTING Loans - Home Equity

BUSINESS LENDING

Loans - Members Business

723.5 BUSINESS LENDING Bankruptcy Policy R

COLLECTIONS

Charge-off and Recovery Policy

GAAP COLLECTIONS Collection Policy

COLLECTIONS

Fair Debt Collection Practices Act Policy R FDCPA COLLECTIONS Foreclosure Policy

COLLECTIONS

Repossession Policy R 749 COLLECTIONS ACH Procedures

CORPORATE

Advertising Procedures

CORPORATE Aggregate Deposit Limit for a Designated Depository

CORPORATE

Asset-Liability Management Policy (ALM)

* CORPORATE

Bank Bribery Act Policy R

CORPORATE CAN-SPAM Policy R

CORPORATE

Children's Online Privacy Protection (COPPA) R

CORPORATE

Complaint Policy and Procedures

CORPORATE Compliance Committee

CORPORATE

Conflict of Interest/Code of Ethics Policy

CORPORATE

Concentration Risk Policy R Supv Letter CORPORATE Consumer Compliance Policy

(Compliance Officer)

CORPORATE Credit Union Business Plan

CORPORATE

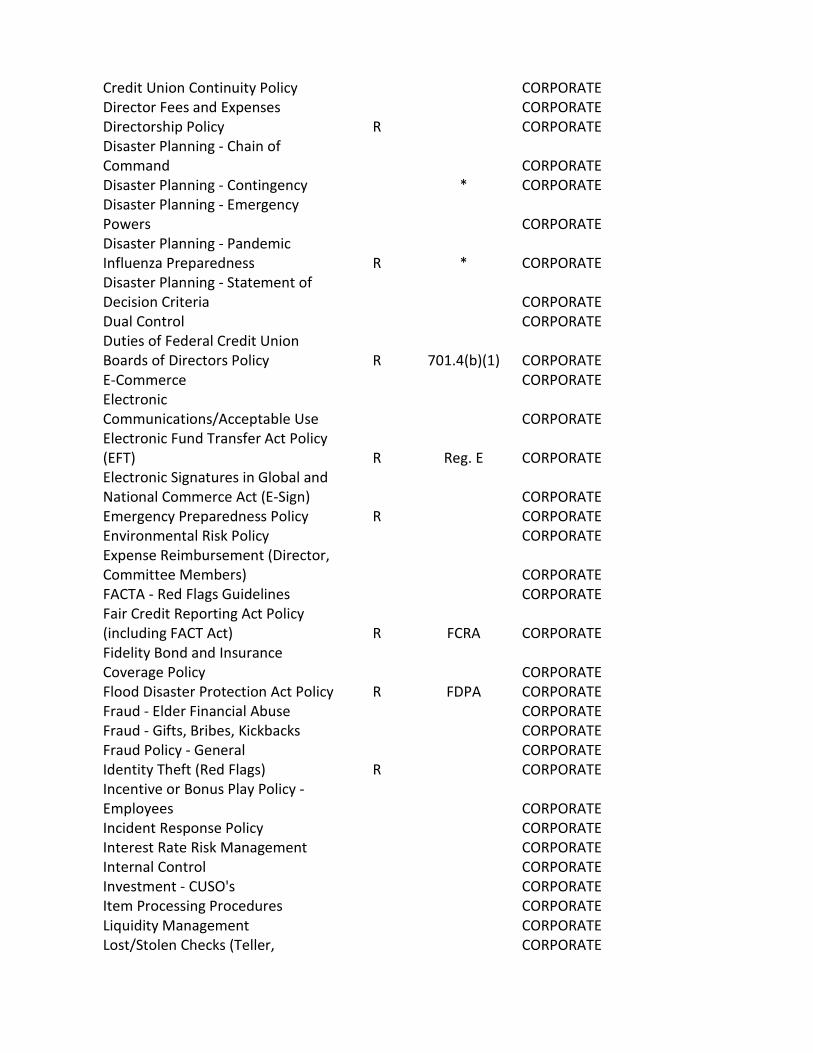

Credit Union Continuity Policy

CORPORATE Director Fees and Expenses

CORPORATE

Directorship Policy R

CORPORATE Disaster Planning - Chain of Command

CORPORATE

Disaster Planning - Contingency

* CORPORATE Disaster Planning - Emergency Powers

CORPORATE

Disaster Planning - Pandemic Influenza Preparedness R * CORPORATE Disaster Planning - Statement of Decision Criteria

CORPORATE

Dual Control

CORPORATE Duties of Federal Credit Union Boards of Directors Policy R 701.4(b)(1) CORPORATE E-Commerce

CORPORATE

Electronic Communications/Acceptable Use

CORPORATE

Electronic Fund Transfer Act Policy (EFT) R Reg. E CORPORATE Electronic Signatures in Global and National Commerce Act (E-Sign)

CORPORATE

Emergency Preparedness Policy R

CORPORATE Environmental Risk Policy

CORPORATE

Expense Reimbursement (Director, Committee Members)

CORPORATE

FACTA - Red Flags Guidelines

CORPORATE Fair Credit Reporting Act Policy (including FACT Act) R FCRA CORPORATE Fidelity Bond and Insurance Coverage Policy

CORPORATE

Flood Disaster Protection Act Policy R FDPA CORPORATE Fraud - Elder Financial Abuse

CORPORATE

Fraud - Gifts, Bribes, Kickbacks

CORPORATE Fraud Policy - General

CORPORATE

Identity Theft (Red Flags) R

CORPORATE Incentive or Bonus Play Policy - Employees

CORPORATE

Incident Response Policy

CORPORATE Interest Rate Risk Management

CORPORATE

Internal Control

CORPORATE Investment - CUSO's

CORPORATE

Item Processing Procedures

CORPORATE Liquidity Management

CORPORATE

Lost/Stolen Checks (Teller,

CORPORATE

Cashiers) Marketing Policy

CORPORATE

Microcomputer End User Policy

CORPORATE Monetary Control Act (Reg D)

CORPORATE

OFAC (Office of Foreign Assets Control) Policy R

CORPORATE

OSHA (Occupational Safety and Health Administration) R

CORPORATE

Other Real Estate Owned (OREO)

CORPORATE Outstanding Indebtedness of Management/Employees/Families

CORPORATE

Plastic Cards

CORPORATE Purchasing & Payment Authorization Policy R 748 CORPORATE Record Production Procedures

CORPORATE

Records Preservation (Retention) Policy R

CORPORATE

Security Policy - Burglary

CORPORATE Security Policy - Computer

CORPORATE

Security Policy - General R

CORPORATE Security Policy - Information Technology/Risk Assessment

CORPORATE

Security Policy - Kidnap/Hostage

CORPORATE Security Policy - Robbery

CORPORATE

Security Policy - Workplace Violence

CORPORATE

Software Policy R 748 CORPORATE Strategic Planning

CORPORATE

Succession Planning

CORPORATE Telecommunications, Electronic Mail, Internet Policy

CORPORATE

Vendor Due Diligence and Oversight

CORPORATE

Web Site

CORPORATE Americans with Disabilities Act

HUMAN RESOURCES

Complaint Policy and Procedures

HUMAN RESOURCES Conflict of Interest/Code of Ethics Policy

HUMAN RESOURCES

Director Fees and Expenses

HUMAN RESOURCES Employee Incentive Policy

HUMAN RESOURCES

Employment Policy - Anti-Harassment & Discrimination (EEOC, ADA, ADEA) R

HUMAN RESOURCES

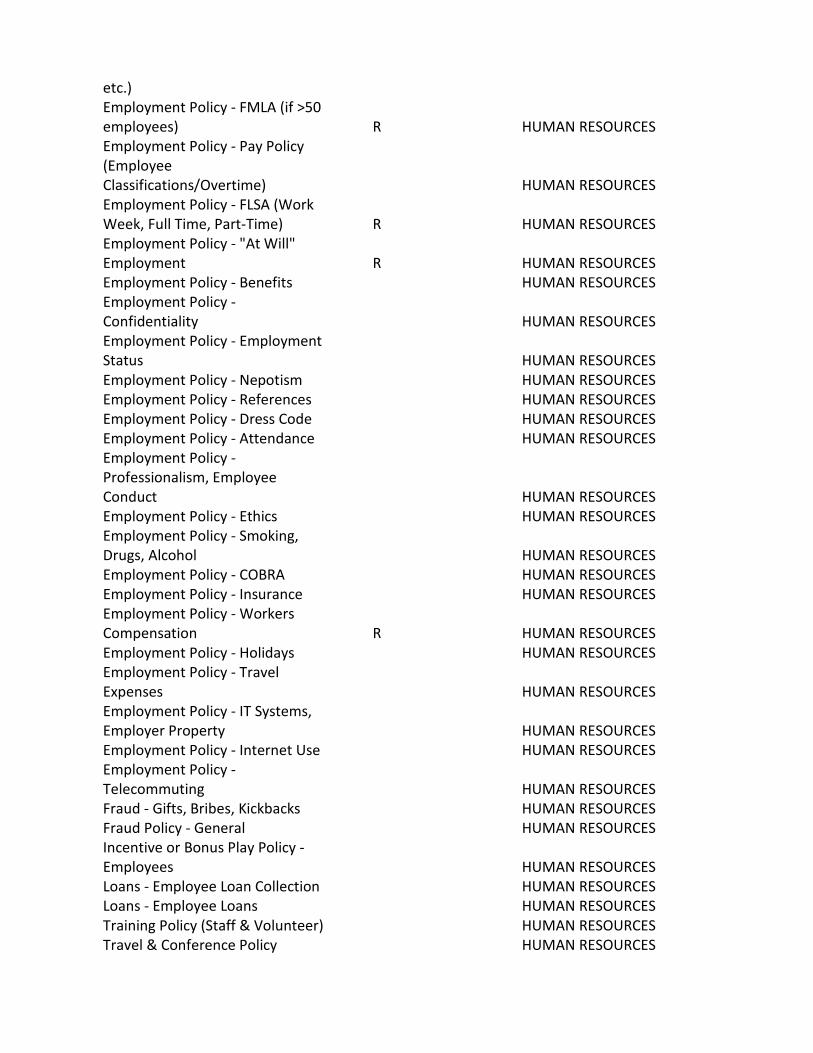

Employment Policy - Employee Leave (Vacation, Sick, Funeral, Jury,

HUMAN RESOURCES

etc.) Employment Policy - FMLA (if >50 employees) R

HUMAN RESOURCES

Employment Policy - Pay Policy (Employee Classifications/Overtime)

HUMAN RESOURCES

Employment Policy - FLSA (Work Week, Full Time, Part-Time) R

HUMAN RESOURCES

Employment Policy - "At Will" Employment R

HUMAN RESOURCES

Employment Policy - Benefits

HUMAN RESOURCES Employment Policy - Confidentiality

HUMAN RESOURCES

Employment Policy - Employment Status

HUMAN RESOURCES

Employment Policy - Nepotism

HUMAN RESOURCES Employment Policy - References

HUMAN RESOURCES

Employment Policy - Dress Code

HUMAN RESOURCES Employment Policy - Attendance

HUMAN RESOURCES

Employment Policy - Professionalism, Employee Conduct

HUMAN RESOURCES

Employment Policy - Ethics

HUMAN RESOURCES Employment Policy - Smoking, Drugs, Alcohol

HUMAN RESOURCES

Employment Policy - COBRA

HUMAN RESOURCES Employment Policy - Insurance

HUMAN RESOURCES

Employment Policy - Workers Compensation R

HUMAN RESOURCES

Employment Policy - Holidays

HUMAN RESOURCES Employment Policy - Travel Expenses

HUMAN RESOURCES

Employment Policy - IT Systems, Employer Property

HUMAN RESOURCES

Employment Policy - Internet Use

HUMAN RESOURCES Employment Policy - Telecommuting

HUMAN RESOURCES

Fraud - Gifts, Bribes, Kickbacks

HUMAN RESOURCES Fraud Policy - General

HUMAN RESOURCES

Incentive or Bonus Play Policy - Employees

HUMAN RESOURCES

Loans - Employee Loan Collection

HUMAN RESOURCES Loans - Employee Loans

HUMAN RESOURCES

Training Policy (Staff & Volunteer)

HUMAN RESOURCES Travel & Conference Policy

HUMAN RESOURCES

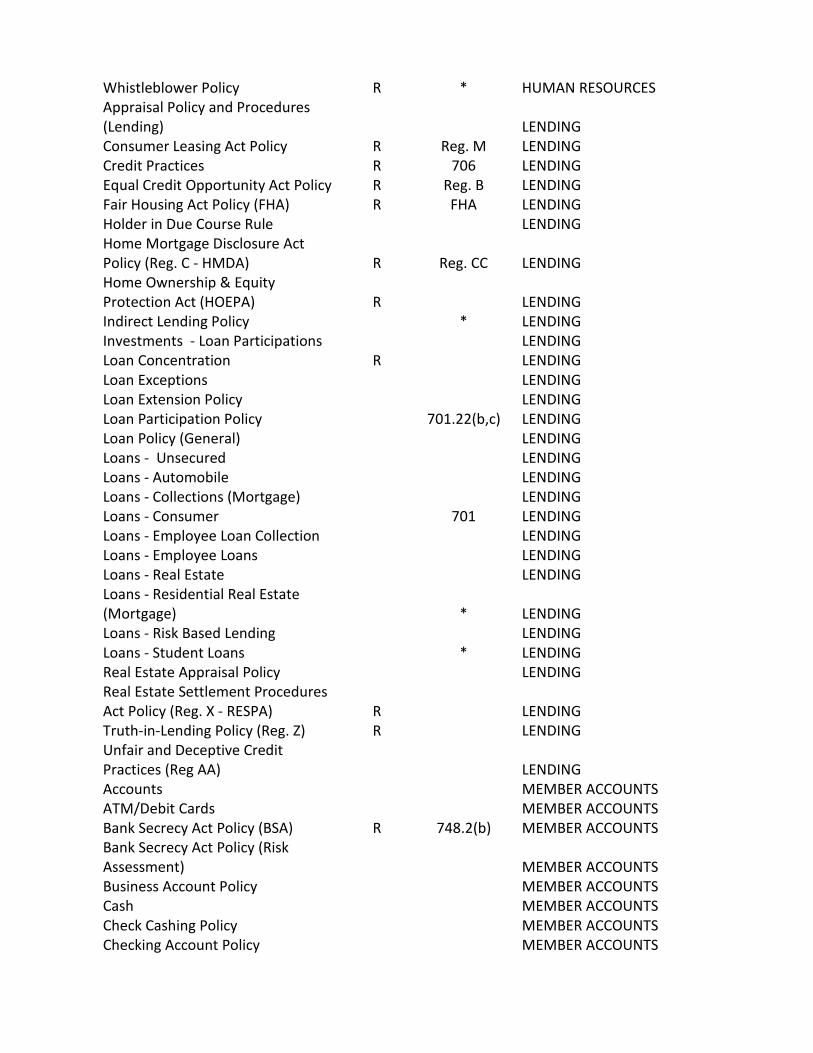

Whistleblower Policy R * HUMAN RESOURCES Appraisal Policy and Procedures (Lending)

LENDING

Consumer Leasing Act Policy R Reg. M LENDING Credit Practices R 706 LENDING Equal Credit Opportunity Act Policy R Reg. B LENDING Fair Housing Act Policy (FHA) R FHA LENDING Holder in Due Course Rule

LENDING

Home Mortgage Disclosure Act Policy (Reg. C - HMDA) R Reg. CC LENDING

Home Ownership & Equity Protection Act (HOEPA) R

LENDING

Indirect Lending Policy

* LENDING Investments - Loan Participations

LENDING

Loan Concentration R

LENDING Loan Exceptions

LENDING

Loan Extension Policy

LENDING Loan Participation Policy

701.22(b,c) LENDING

Loan Policy (General)

LENDING Loans - Unsecured

LENDING

Loans - Automobile

LENDING Loans - Collections (Mortgage)

LENDING

Loans - Consumer

701 LENDING Loans - Employee Loan Collection

LENDING

Loans - Employee Loans

LENDING Loans - Real Estate

LENDING

Loans - Residential Real Estate (Mortgage)

* LENDING

Loans - Risk Based Lending

LENDING Loans - Student Loans

* LENDING

Real Estate Appraisal Policy

LENDING Real Estate Settlement Procedures

Act Policy (Reg. X - RESPA) R

LENDING Truth-in-Lending Policy (Reg. Z) R

LENDING

Unfair and Deceptive Credit Practices (Reg AA)

LENDING

Accounts

MEMBER ACCOUNTS ATM/Debit Cards

MEMBER ACCOUNTS

Bank Secrecy Act Policy (BSA) R 748.2(b) MEMBER ACCOUNTS Bank Secrecy Act Policy (Risk Assessment)

MEMBER ACCOUNTS

Business Account Policy

MEMBER ACCOUNTS Cash

MEMBER ACCOUNTS

Check Cashing Policy

MEMBER ACCOUNTS Checking Account Policy

MEMBER ACCOUNTS

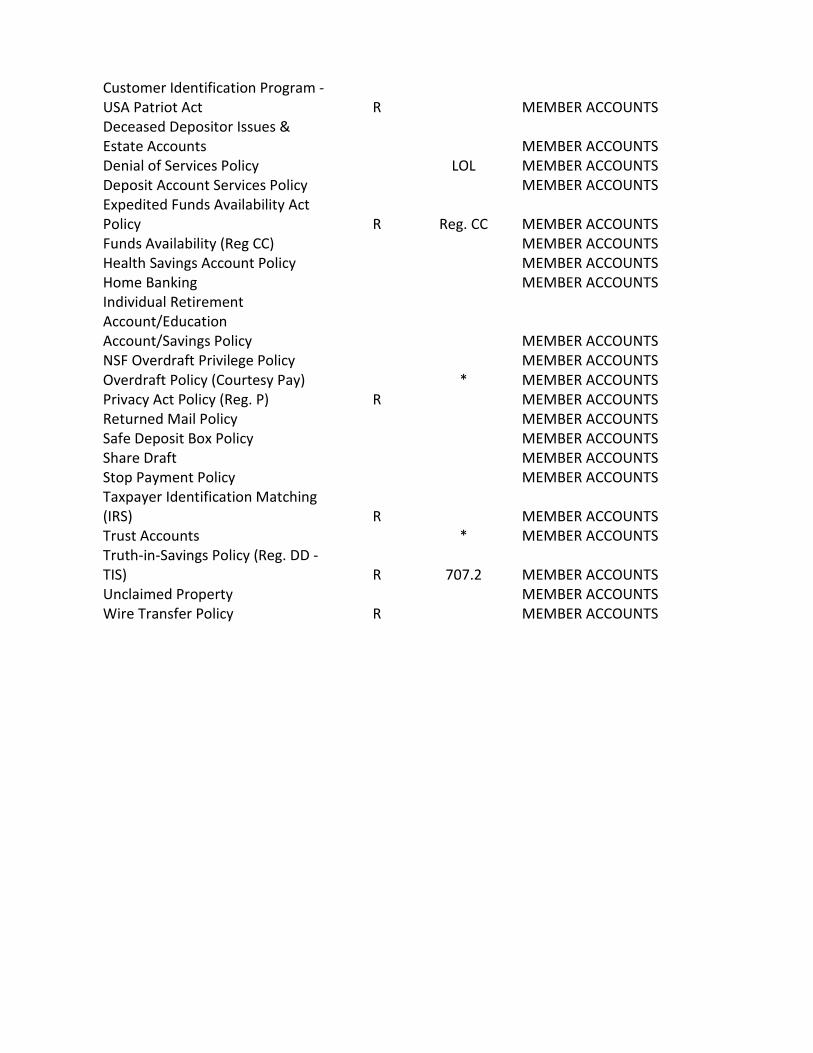

Customer Identification Program - USA Patriot Act R

MEMBER ACCOUNTS

Deceased Depositor Issues & Estate Accounts

MEMBER ACCOUNTS

Denial of Services Policy

LOL MEMBER ACCOUNTS Deposit Account Services Policy

MEMBER ACCOUNTS

Expedited Funds Availability Act Policy R Reg. CC MEMBER ACCOUNTS Funds Availability (Reg CC)

MEMBER ACCOUNTS

Health Savings Account Policy

MEMBER ACCOUNTS Home Banking

MEMBER ACCOUNTS

Individual Retirement Account/Education Account/Savings Policy

MEMBER ACCOUNTS

NSF Overdraft Privilege Policy

MEMBER ACCOUNTS Overdraft Policy (Courtesy Pay)

* MEMBER ACCOUNTS

Privacy Act Policy (Reg. P) R

MEMBER ACCOUNTS Returned Mail Policy

MEMBER ACCOUNTS

Safe Deposit Box Policy

MEMBER ACCOUNTS Share Draft

MEMBER ACCOUNTS

Stop Payment Policy

MEMBER ACCOUNTS Taxpayer Identification Matching (IRS) R

MEMBER ACCOUNTS

Trust Accounts

* MEMBER ACCOUNTS Truth-in-Savings Policy (Reg. DD - TIS) R 707.2 MEMBER ACCOUNTS Unclaimed Property

MEMBER ACCOUNTS

Wire Transfer Policy R

MEMBER ACCOUNTS

Small Credit Union Consulting Services

The League offers a wide array of small credit union consultative services. The League understands and appreciates the demands placed on small credit unions and want you to know that we are committed to your success.

The following menu of available services is not all inclusive. Contact Dan Collins at 800-950-4455, extension 205 or [email protected] with any consultative request.

Accounting Training and Assistance

The League will assist with normal accounting questions and will offer advice on best practices on how to solve accounting issues. Additionally, staff can train on payroll, depreciation, allowance for loan loss, closing entries, and more.

Asset-Liabil ity Management

The League will assist small credit unions in evaluating the impact of their deposit and loan pricing in either a falling rate or rising rate environment.

Budget Assistance

The League will assist small credit unions with an analytical based budget. League staff will determine the current rate of asset, loan, investment, share, capital, and return on asset growth. Staff will then assist management compile a realistic budget that matches their current performance and goals.

Business Plan Development

The League will assist small credit unions with the development of various levels of business plans. Staff will assist the credit union in identifying strategic issues and then facilitate Board & Management planning on those particular issues. Staff will then assist the credit union as they create goals and an action plan to accomplish each identified goal.

Charter, Field of Membership, and By Law Changes

The League will provide small credit unions with assistance and guidance when planning for charter, field-of-membership, and by law changes.

Regulator Relations and Examination Findings

The League will assist small credit unions in working through a Document of Resolution or other examiner issues or concerns. League staff maintains good relationships with examiners and are

in a unique, third party positon to provide neutral advice on issues. Occasionally an issue may necessitate an escalation to a supervisor and likewise League staff can generally help with a mutual resolution.

In-House Training for Volunteers/Staff

League employees are skilled and experienced professionals that often have the talent to assist your credit union's educational needs. Whether your credit union needs financial literacy, bank secrecy act, volunteer duties & responsibilities, or other specific training, League staff will recommend options within your budget.

Lending The League will assist small credit unions with matching your asset size with loan products that make the most sense for your membership. We will provide information regarding complexity, documentation, and usefulness. You will then be able to make an informed decision on whether not this product makes financial sense for your credit union. Financial Education The League will assist small credit unions with improving their members’ financial acumen. The League has a variety of financial education materials at its disposal and can help to empower your members and therefore create a longer lasting relationship. Marketing & Business Development The League knows the value of effective communications and how to market your mission and business services. Better marketing is vital to serving your members, growing your credit union, and boosting your bottom line. League Public Relations The League will assist small credit unions as you promote your interest to your member-owners in the media and in our communities.

Credit Union Service and Product Implementation Resources

Credit unions exist to meet the needs of their members, but as a small credit union, adding new products and services to meet those needs can sometimes be a balancing act. We need to strategically add the products and services that will strengthen the relationship with our current membership and attract new members.

There is much to be considered prior to adding a new product or service.

Considerations include:

• Is this product/service a good fit for the credit union’s membership?

• Does this product/service fit into the credit union’s overall vision?

• Is this product/service intended to simply be a service to the credit union’s membership or an income generator?

• Has the credit union conducted a cost benefit analysis to include implementation costs,

ongoing costs, expected income, etc?

• Has the credit union identified and addressed the corresponding compliance issues, including adding new policies, amending existing policies, developing procedures, acquiring required disclosures, etc.?

• Will it be necessary to upgrade the current system to support the new product/service?

• Does the credit union have adequate staffing to handle the new service/product

requirements?

• How will staff be trained on the new product/service procedures and compliance requirements?

• How will the credit union market the new product/service to the membership?

• What will be the impact on the credit union’s balance sheet?

• Has the credit union conducted a comprehensive Vendor Due Diligence?

To assist credit unions with some of the most common start up services, we have provided some resources and tools that have been shared by some of the vendors that offer these products and services.

It is very important to remember that your credit union must always conduct their vendor due diligence before entering into any contracts and ensure that the new product or service is a good fit for your credit union. Share Draft Program

Additional information on the Share Draft Program provided by Kansas Credit Union Association can be found at https://www.kcua.coop/?page=About_SFS.

ACH Program

Additional information on the ACH Program provided by Kansas Corporate FCU can be found at http://www.kansascorporate.org/kansascorp/Correspondent.asp#Apex.

Prepaid Card Program Prepaid Reloadable Debit Cards http://www.lsc.net/services/prepaid/newgen

Visa Travel Money Card http://www.lsc.net/services/prepaid/travelmoney

Everyday Spend Prepaid Debit Card http://www.lsc.net/services/prepaid/everyday-spend

Additional information on pre-paid card services provided by LSC can be found at www.lsc.net.

CEO Handbook The Small Credit Union committee has partnered with CEOs across the State to put together a comprehensive handbook. This handbook will assist CEOs with credit union acronyms, must have policies, regulations to know, and cooperative principles. The intention of this is to be a living and ever evolving handbook. If you have any documents that you feel would be an asset to this handbook, please send them to Dan Collins [email protected].

Each portion of the handbook is also available as a separate PDF file – simply click below on each link and the PDF file attachment is available for download at the bottom of each page.

ALM Glossary Alphabet Soup of Acronyms Alphabet Soup of Regulations Bank Secrecy Act/Anti-Money Laundering Acronyms Cooperative Principles for Credit Unions Differences Between Credit Unions and Banks

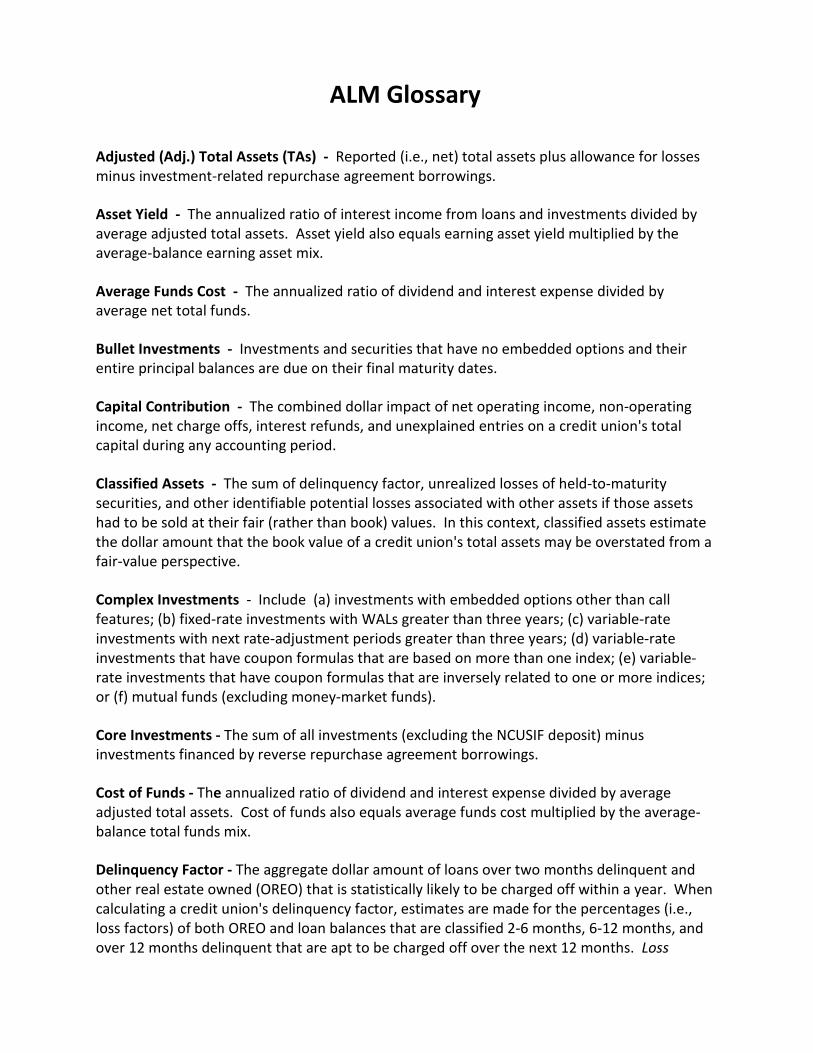

ALM Glossary

Adjusted (Adj.) Total Assets (TAs) - Reported (i.e., net) total assets plus allowance for losses minus investment-related repurchase agreement borrowings.

Asset Yield - The annualized ratio of interest income from loans and investments divided by average adjusted total assets. Asset yield also equals earning asset yield multiplied by the average-balance earning asset mix.

Average Funds Cost - The annualized ratio of dividend and interest expense divided by average net total funds.

Bullet Investments - Investments and securities that have no embedded options and their entire principal balances are due on their final maturity dates.

Capital Contribution - The combined dollar impact of net operating income, non-operating income, net charge offs, interest refunds, and unexplained entries on a credit union's total capital during any accounting period.

Classified Assets - The sum of delinquency factor, unrealized losses of held-to-maturity securities, and other identifiable potential losses associated with other assets if those assets had to be sold at their fair (rather than book) values. In this context, classified assets estimate the dollar amount that the book value of a credit union's total assets may be overstated from a fair-value perspective.

Complex Investments - Include (a) investments with embedded options other than call features; (b) fixed-rate investments with WALs greater than three years; (c) variable-rate investments with next rate-adjustment periods greater than three years; (d) variable-rate investments that have coupon formulas that are based on more than one index; (e) variable-rate investments that have coupon formulas that are inversely related to one or more indices; or (f) mutual funds (excluding money-market funds).

Core Investments - The sum of all investments (excluding the NCUSIF deposit) minus investments financed by reverse repurchase agreement borrowings.

Cost of Funds - The annualized ratio of dividend and interest expense divided by average adjusted total assets. Cost of funds also equals average funds cost multiplied by the average-balance total funds mix.

Delinquency Factor - The aggregate dollar amount of loans over two months delinquent and other real estate owned (OREO) that is statistically likely to be charged off within a year. When calculating a credit union's delinquency factor, estimates are made for the percentages (i.e., loss factors) of both OREO and loan balances that are classified 2-6 months, 6-12 months, and over 12 months delinquent that are apt to be charged off over the next 12 months. Loss

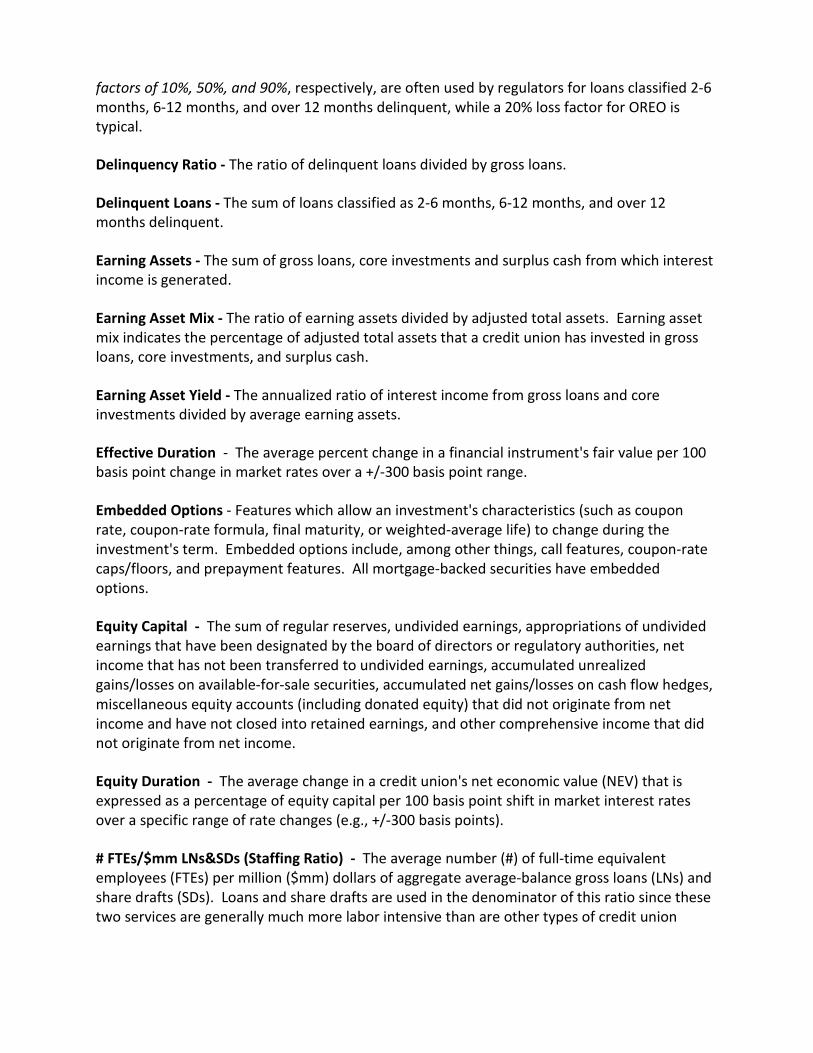

factors of 10%, 50%, and 90%, respectively, are often used by regulators for loans classified 2-6 months, 6-12 months, and over 12 months delinquent, while a 20% loss factor for OREO is typical.

Delinquency Ratio - The ratio of delinquent loans divided by gross loans.

Delinquent Loans - The sum of loans classified as 2-6 months, 6-12 months, and over 12 months delinquent.

Earning Assets - The sum of gross loans, core investments and surplus cash from which interest income is generated.

Earning Asset Mix - The ratio of earning assets divided by adjusted total assets. Earning asset mix indicates the percentage of adjusted total assets that a credit union has invested in gross loans, core investments, and surplus cash.

Earning Asset Yield - The annualized ratio of interest income from gross loans and core investments divided by average earning assets.

Effective Duration - The average percent change in a financial instrument's fair value per 100 basis point change in market rates over a +/-300 basis point range.

Embedded Options - Features which allow an investment's characteristics (such as coupon rate, coupon-rate formula, final maturity, or weighted-average life) to change during the investment's term. Embedded options include, among other things, call features, coupon-rate caps/floors, and prepayment features. All mortgage-backed securities have embedded options.

Equity Capital - The sum of regular reserves, undivided earnings, appropriations of undivided earnings that have been designated by the board of directors or regulatory authorities, net income that has not been transferred to undivided earnings, accumulated unrealized gains/losses on available-for-sale securities, accumulated net gains/losses on cash flow hedges, miscellaneous equity accounts (including donated equity) that did not originate from net income and have not closed into retained earnings, and other comprehensive income that did not originate from net income.

Equity Duration - The average change in a credit union's net economic value (NEV) that is expressed as a percentage of equity capital per 100 basis point shift in market interest rates over a specific range of rate changes (e.g., +/-300 basis points).

# FTEs/$mm LNs&SDs (Staffing Ratio) - The average number (#) of full-time equivalent employees (FTEs) per million ($mm) dollars of aggregate average-balance gross loans (LNs) and share drafts (SDs). Loans and share drafts are used in the denominator of this ratio since these two services are generally much more labor intensive than are other types of credit union

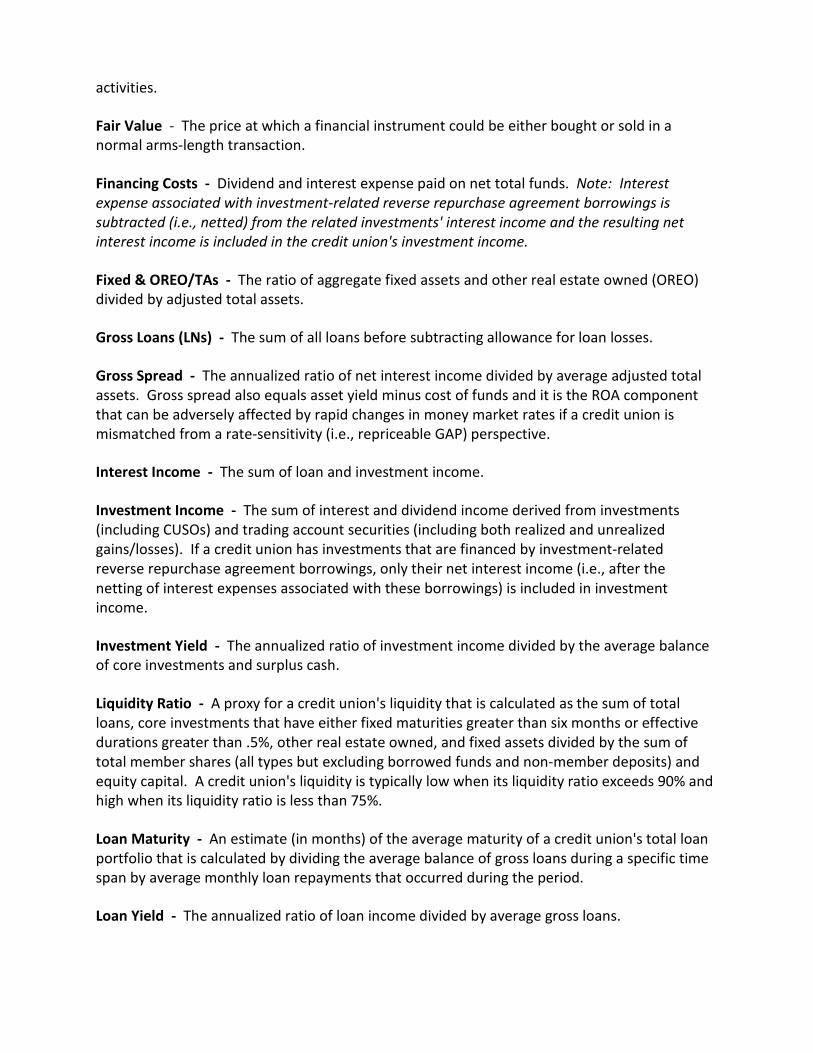

activities.

Fair Value - The price at which a financial instrument could be either bought or sold in a normal arms-length transaction.

Financing Costs - Dividend and interest expense paid on net total funds. Note: Interest expense associated with investment-related reverse repurchase agreement borrowings is subtracted (i.e., netted) from the related investments' interest income and the resulting net interest income is included in the credit union's investment income.

Fixed & OREO/TAs - The ratio of aggregate fixed assets and other real estate owned (OREO) divided by adjusted total assets.

Gross Loans (LNs) - The sum of all loans before subtracting allowance for loan losses.

Gross Spread - The annualized ratio of net interest income divided by average adjusted total assets. Gross spread also equals asset yield minus cost of funds and it is the ROA component that can be adversely affected by rapid changes in money market rates if a credit union is mismatched from a rate-sensitivity (i.e., repriceable GAP) perspective.

Interest Income - The sum of loan and investment income.

Investment Income - The sum of interest and dividend income derived from investments (including CUSOs) and trading account securities (including both realized and unrealized gains/losses). If a credit union has investments that are financed by investment-related reverse repurchase agreement borrowings, only their net interest income (i.e., after the netting of interest expenses associated with these borrowings) is included in investment income.

Investment Yield - The annualized ratio of investment income divided by the average balance of core investments and surplus cash.

Liquidity Ratio - A proxy for a credit union's liquidity that is calculated as the sum of total loans, core investments that have either fixed maturities greater than six months or effective durations greater than .5%, other real estate owned, and fixed assets divided by the sum of total member shares (all types but excluding borrowed funds and non-member deposits) and equity capital. A credit union's liquidity is typically low when its liquidity ratio exceeds 90% and high when its liquidity ratio is less than 75%.

Loan Maturity - An estimate (in months) of the average maturity of a credit union's total loan portfolio that is calculated by dividing the average balance of gross loans during a specific time span by average monthly loan repayments that occurred during the period.

Loan Yield - The annualized ratio of loan income divided by average gross loans.

Long-Term Real Estate Loans - Total real estate loans less the aggregate sum of real estate loans that will either contractually refinance, reprice, or mature within five years.

Member Fee Income - Regularly occurring fee income charged members for services such as share drafts, ATMs, processing late payments, safety deposit boxes, credit/debit cards, home banking, etc.

Minimum Cash - An estimate of a credit union's minimum daily non-earning cash requirements in settlement accounts, checking accounts, teller cash, ATMs, and accounts at the Federal Reserve.

Mix - The percentage of adjusted total assets that a credit union has either: invested in a particular type of asset (such as the various categories of loans and core investments) in the case of specific asset mixes; or financed by a particular type of funding source (such as share certificates, regular shares, non-member deposits, etc) in the case of funding mixes.

For example, loan mix is gross loans divided by adjusted total assets, while share draft mix is share draft balances divided by adjusted total assets. Mixes can be calculated on either a month-end basis or average balances over a specific time period. Note: Earning asset mix is the sum of the gross loan, core investment, and surplus cash mixes, while total funds mix is the sum of the various funding mixes.

Money Market Shares - Either share or draft accounts with dividend rates that closely track changes in money market rates according to their rate sensitivity factor.

N.OPER.EXP./LNs&SDs - The ratio of annualized net operating expenses divided by the aggregate average-balance of gross loans (LNs) and share drafts (SDs).

Net Capital - An estimate of the fair value of a credit union's total capital. When calculating net capital, classified assets are subtracted from total capital. Hence, net capital can be used as a proxy for a credit union's solvency since a negative value implies insolvency. The net capital to adjusted total asset ratio depicts the estimated fair value of a credit union's total capital per dollar of book-value adjusted total assets.

Net Capital Margin - The annualized net contribution to total capital divided by average adjusted total assets. Net contribution (i.e., capital contribution) reflects the combined impact of net operating income, non-operating income, net charge offs, interest refunds, and unexplained entries on total capital.

Net Charge Offs (NCOs) - Annualized loan charge offs minus recoveries.

Net Economic Value (NEV) - The fair value of a credit union's earning assets (i.e., loans and investments) minus the fair value of its funding liabilities (including all term and non-term

share and deposit accounts).

Net Interest Income - Interest income from loans and investments minus financing costs (dividend and interest expense). Annualized net interest income is the numerator of a gross spread calculation.

Net Operating Expenses - Operating expenses minus total fee income.

Net Operating Expense Ratio (NOER) - Annualized net operating expenses divided by average adjusted total assets.

Net Operating Income - Calculated as net interest income minus net operating expenses, net operating income reflects a credit union's operating profitability before non-operating income, unrealized gains/losses, loan loss provisions, reserve transfers and interest refunds are taken into account.

Net Total Assets - Reported total assets which are net of the allowance for loan losses.

Net Total Funds - The sum of member share accounts (all types), non-member deposits, and non-reverse notes payable on which either dividends or interest is paid. Dividends and interest payable are also included in a credit union's net total funds. Note: Net total funds exclude investment-related reverse repurchase agreement borrowings.

Net Worth - The sum of regular reserves, undivided earnings, appropriations of undivided earnings that have been designated by the board of directors or regulatory authorities, and net income that has not been transferred to undivided earnings. For a low income-designated credit union, net worth also includes uninsured secondary capital accounts that are subordinate to all other claims, including claims of creditors, shareholders, and the National Credit Union Share Insurance Fund.

Non-Interest Income - The same as total fee income.

Non-Operating Income - Sources of income and expenses that do not occur on a regular basis and that are not considered components of net operating income. Examples include realized gains/losses resulting from the sale of securities or fixed assets, non-recurring income/expenses, payments received on bonding claims, and legal settlements.

Non-Reverse (Rv) Notes Payable - The sum of all notes payable (NP), borrowed funds, promissory notes, and subordinated debt minus investment-related reverse repurchase agreement borrowings.

Operating Expenses - All expenses except dividends and interest, non-operating expenses (or losses), investment losses (both realized and unrealized), loan loss provisions and reserve transfers.

Operating Return on Assets (ROA) - The summary measurement of a credit union's core profitability which can be determined either by dividing annualized net operating income by average adjusted total assets or by subtracting the net operating expense ratio from gross spread.

Option-Free Investments - Investments with no embedded options.

Other Operating Income - Regularly occurring income (other than interest income and member fee income) such as (but not limited to) lease/rental income, endorsement fees, and gains/losses associated with the sale of real estate loans in the secondary markets.

Rate Sensitivity Factor (RSF) - An indication of the responsiveness of either an earning asset's yield or a particular funding source's dividend (or interest) rate to a change in money market rates. For example, if the yield on a pool of variable-rate loans rose 75 basis points for each 100 basis point increase in money market rates (such as six-month T-bill rates), the pool of loans would have a 75% RSF. Similarly, if the dividend rate of a credit union's IRA shares changed 50 basis points for each 100 basis point change in money market rates, the estimated RSF associated with these IRA shares would be 50%. Before measuring a credit union's six-month repriceable GAP, RSFs must be determined (or estimated) for variable-rate loans, floating-rate investments, IRA shares, money market shares, regular shares, share drafts, and other types of share accounts that don't have contractual maturity dates.

Repriceable Assets - Earning assets that either mature within the next six months or have yields (in the case of variable-rate loans and floating-rate investments) which would respond to changes in money market rates in accordance with their respective rate sensitivity factors.

Repriceable Funds - The sum of funds (such as share certificates, borrowed funds, and non-member deposits) that have contractual maturity dates within the next six months and other funding sources (such as IRA shares, money market shares, and regular shares) that can be sensitivity adjusted in accordance with their respective rate sensitivity factors.

Repriceable GAP - Repriceable assets minus repriceable funds.

Repriceable GAP Ratio - The ratio of repriceable GAP divided by adjusted total assets that indicates the potential responsiveness of a credit union's gross spread to changes in money market rates.

$m S&F/FTE Employees (Compensation Ratio) - Annualized salary and fringe (S&F) expenses that are denominated in thousands ($m) of dollars divided by the average number of full-time equivalent (FTE) employees.

$m S&F/$mm LNs&SDs - The product of the staffing and compensation ratios that indicates annualized salary and fringe (S&F) expenses in thousands ($m) of dollars incurred by a credit union to deliver each million ($mm) dollars of aggregate average-balance gross loans (LNs) and

share drafts (SDs) to its members.

Share Certificates (SC) - The sum of all member share certificates (both regular and IRA) that have contractual maturity dates. Although most SCs have fixed contractual maturity dates when they are issued, some SCs could also be callable at the credit union's option while others may contain embedded options that allow members to either lengthen or shorten the SC's original maturity date.

Statutory Reserves - The sum of regular reserves and allowance for loan losses. Statutory reserves are capital accounts that are controlled by regulation rather than by a credit union's board of directors.

Surplus Cash - Reported non-earning cash balances minus an estimate of a credit union's minimum cash needs. Surplus cash can be either positive or negative and it is included with core investments when calculating investment yield.

Total Capital - The sum of the allowance for loan & lease losses and equity capital. For a low income-designated credit union, total capital also includes uninsured secondary capital accounts that are subordinate to all other claims, including claims of creditors, shareholders, and the National Credit Union Share Insurance Fund.

Total Fee Income - The sum of member fee income and other operating income. Total fee income is often referred to as non-interest income.

Total Funds Mix - The percentage of adjusted total assets financed by net total funds (i.e., non-reverse notes payable, non-member deposits, share certificates, IRA shares, money market share accounts, club accounts, regular shares, and share drafts).

Unexplained Entries - Changes in total capital from one accounting period to another that cannot be explained by typical factors affecting total capital, such as net operating income, non-operating income, net charge offs, and interest refunds. Direct entries (such as changes in the aggregate fair value of available-for-sale securities) to any of the various capital accounts that were not recorded in the statement of income and expenses will result in unexplained entries.

Variable-Rate Loans - Either open- or closed-end loans with yields that respond to changes in money market rates according to their rate sensitivity factors.

Weighted-Average Life (WAL) - The weighted-average time of a financial instrument's principal repayments (both scheduled and unscheduled) where each repayment's weight is its percentage of the instrument's total remaining principal. The WAL for a bullet investment is its final maturity.

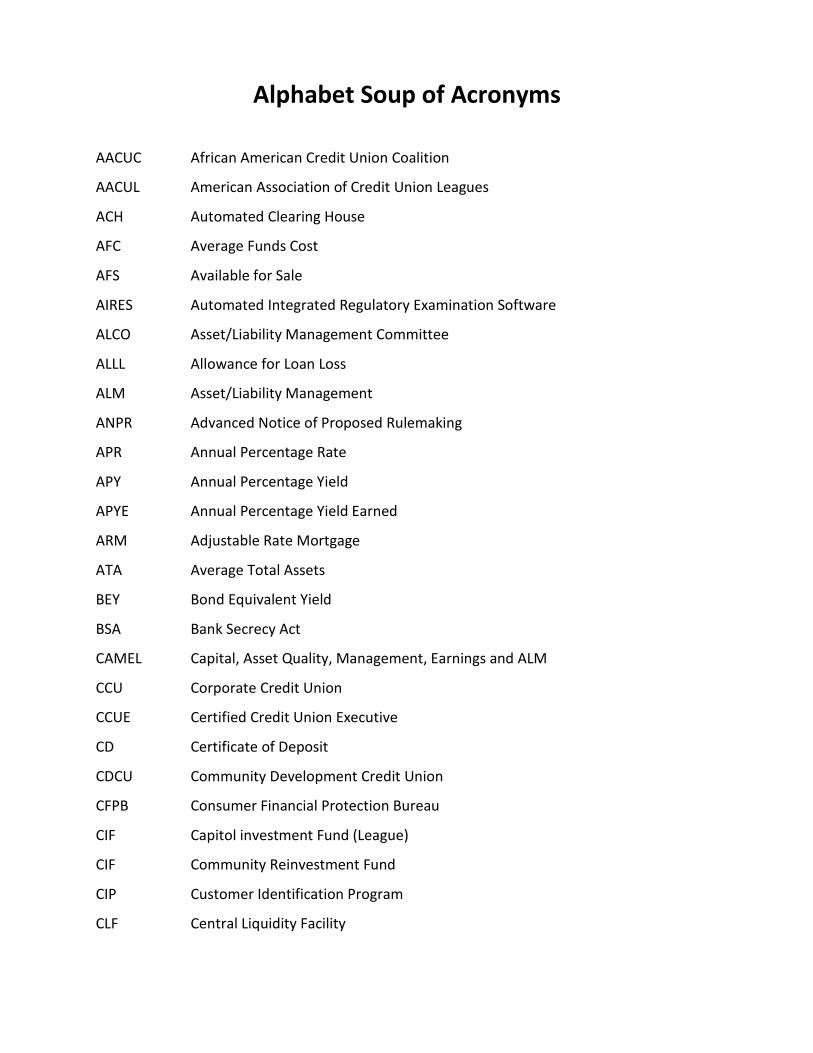

Alphabet Soup of Acronyms AACUC African American Credit Union Coalition

AACUL American Association of Credit Union Leagues

ACH Automated Clearing House

AFC Average Funds Cost

AFS Available for Sale

AIRES Automated Integrated Regulatory Examination Software

ALCO Asset/Liability Management Committee

ALLL Allowance for Loan Loss

ALM Asset/Liability Management

ANPR Advanced Notice of Proposed Rulemaking

APR Annual Percentage Rate

APY Annual Percentage Yield

APYE Annual Percentage Yield Earned

ARM Adjustable Rate Mortgage

ATA Average Total Assets

BEY Bond Equivalent Yield

BSA Bank Secrecy Act

CAMEL Capital, Asset Quality, Management, Earnings and ALM

CCU Corporate Credit Union

CCUE Certified Credit Union Executive

CD Certificate of Deposit

CDCU Community Development Credit Union

CFPB Consumer Financial Protection Bureau

CIF Capitol investment Fund (League)

CIF Community Reinvestment Fund

CIP Customer Identification Program

CLF Central Liquidity Facility

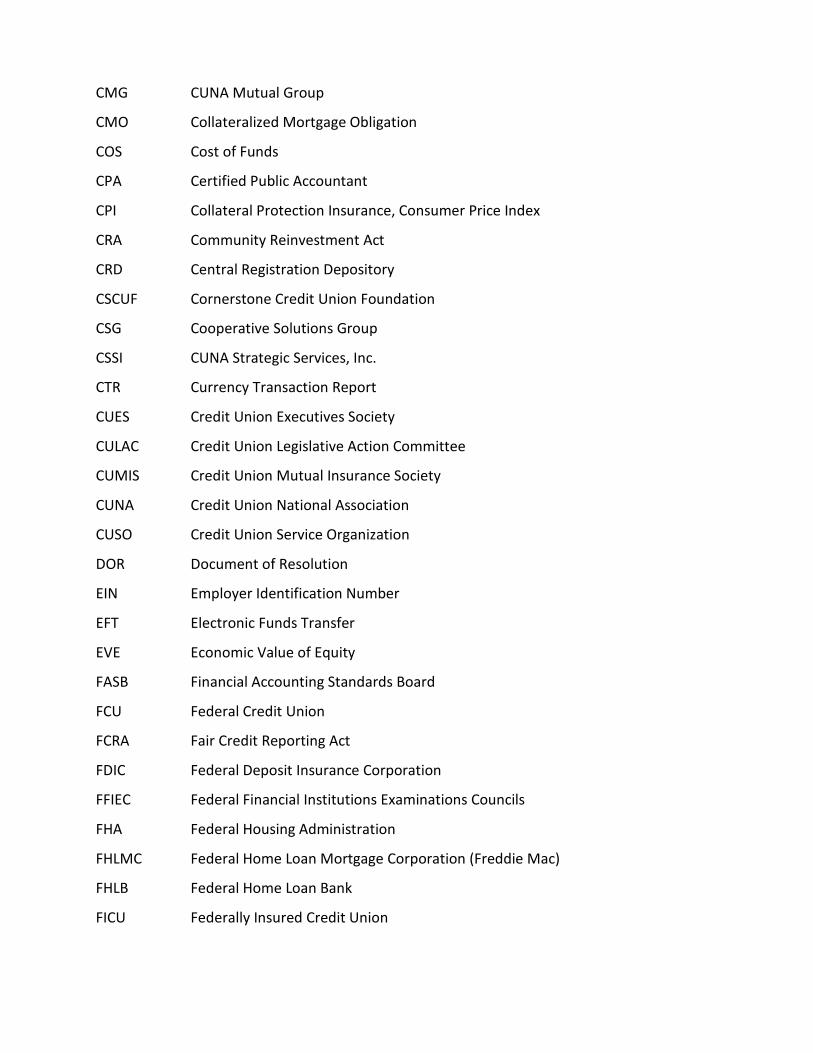

CMG CUNA Mutual Group

CMO Collateralized Mortgage Obligation

COS Cost of Funds

CPA Certified Public Accountant

CPI Collateral Protection Insurance, Consumer Price Index

CRA Community Reinvestment Act

CRD Central Registration Depository

CSCUF Cornerstone Credit Union Foundation

CSG Cooperative Solutions Group

CSSI CUNA Strategic Services, Inc.

CTR Currency Transaction Report

CUES Credit Union Executives Society

CULAC Credit Union Legislative Action Committee

CUMIS Credit Union Mutual Insurance Society

CUNA Credit Union National Association

CUSO Credit Union Service Organization

DOR Document of Resolution

EIN Employer Identification Number

EFT Electronic Funds Transfer

EVE Economic Value of Equity

FASB Financial Accounting Standards Board

FCU Federal Credit Union

FCRA Fair Credit Reporting Act

FDIC Federal Deposit Insurance Corporation

FFIEC Federal Financial Institutions Examinations Councils

FHA Federal Housing Administration

FHLMC Federal Home Loan Mortgage Corporation (Freddie Mac)

FHLB Federal Home Loan Bank

FICU Federally Insured Credit Union

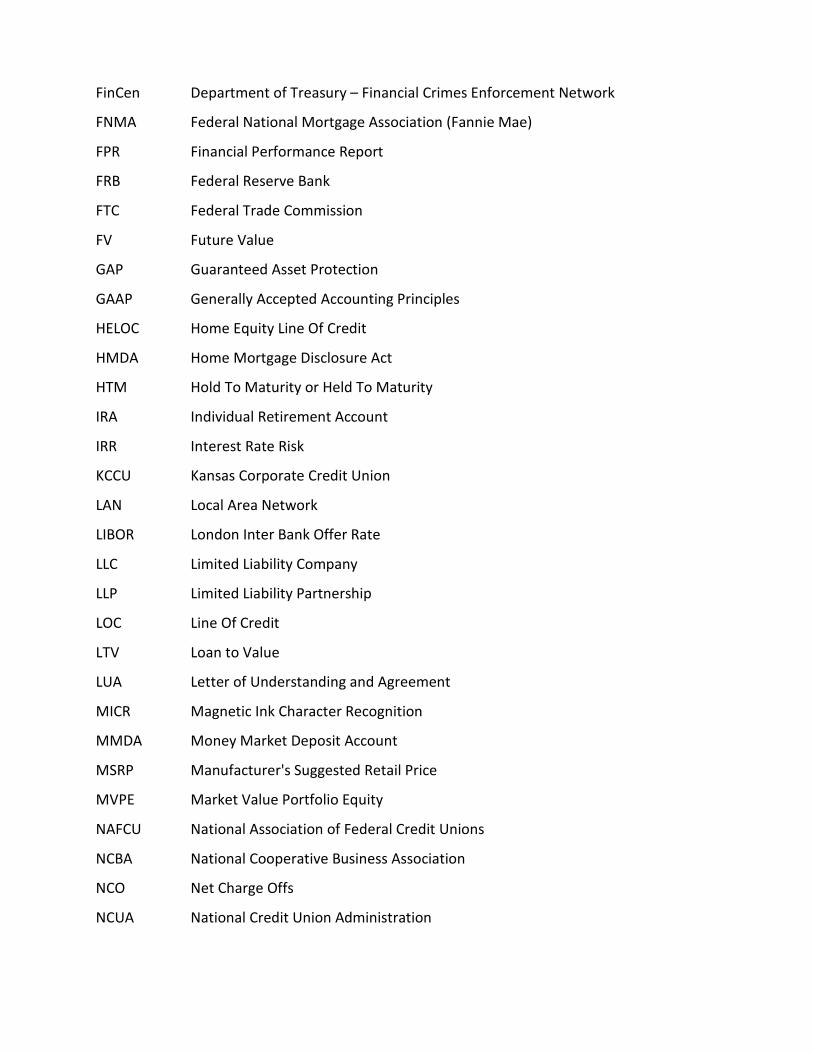

FinCen Department of Treasury – Financial Crimes Enforcement Network

FNMA Federal National Mortgage Association (Fannie Mae)

FPR Financial Performance Report

FRB Federal Reserve Bank

FTC Federal Trade Commission

FV Future Value

GAP Guaranteed Asset Protection

GAAP Generally Accepted Accounting Principles

HELOC Home Equity Line Of Credit

HMDA Home Mortgage Disclosure Act

HTM Hold To Maturity or Held To Maturity

IRA Individual Retirement Account

IRR Interest Rate Risk

KCCU Kansas Corporate Credit Union

LAN Local Area Network

LIBOR London Inter Bank Offer Rate

LLC Limited Liability Company

LLP Limited Liability Partnership

LOC Line Of Credit

LTV Loan to Value

LUA Letter of Understanding and Agreement

MICR Magnetic Ink Character Recognition

MMDA Money Market Deposit Account

MSRP Manufacturer's Suggested Retail Price

MVPE Market Value Portfolio Equity

NAFCU National Association of Federal Credit Unions

NCBA National Cooperative Business Association

NCO Net Charge Offs

NCUA National Credit Union Administration

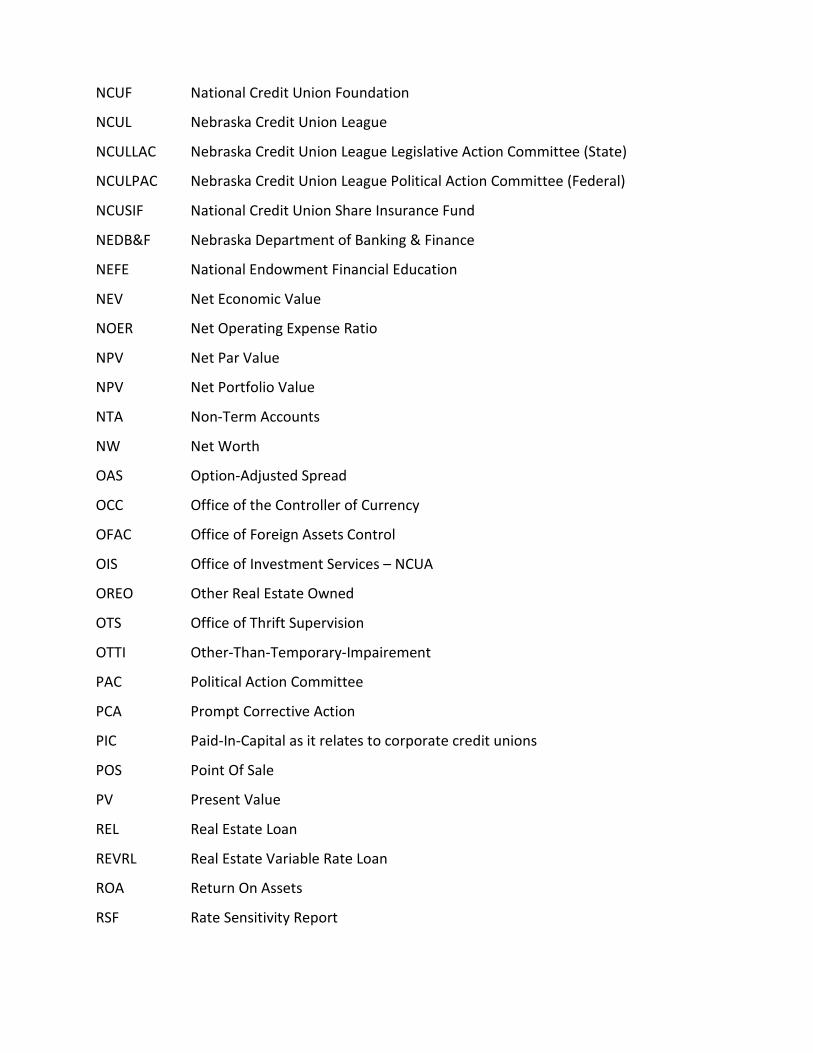

NCUF National Credit Union Foundation

NCUL Nebraska Credit Union League

NCULLAC Nebraska Credit Union League Legislative Action Committee (State)

NCULPAC Nebraska Credit Union League Political Action Committee (Federal)

NCUSIF National Credit Union Share Insurance Fund

NEDB&F Nebraska Department of Banking & Finance

NEFE National Endowment Financial Education

NEV Net Economic Value

NOER Net Operating Expense Ratio

NPV Net Par Value

NPV Net Portfolio Value

NTA Non-Term Accounts

NW Net Worth

OAS Option-Adjusted Spread

OCC Office of the Controller of Currency

OFAC Office of Foreign Assets Control

OIS Office of Investment Services – NCUA

OREO Other Real Estate Owned

OTS Office of Thrift Supervision

OTTI Other-Than-Temporary-Impairement

PAC Political Action Committee

PCA Prompt Corrective Action

PIC Paid-In-Capital as it relates to corporate credit unions

POS Point Of Sale

PV Present Value

REL Real Estate Loan

REVRL Real Estate Variable Rate Loan

ROA Return On Assets

RSF Rate Sensitivity Report

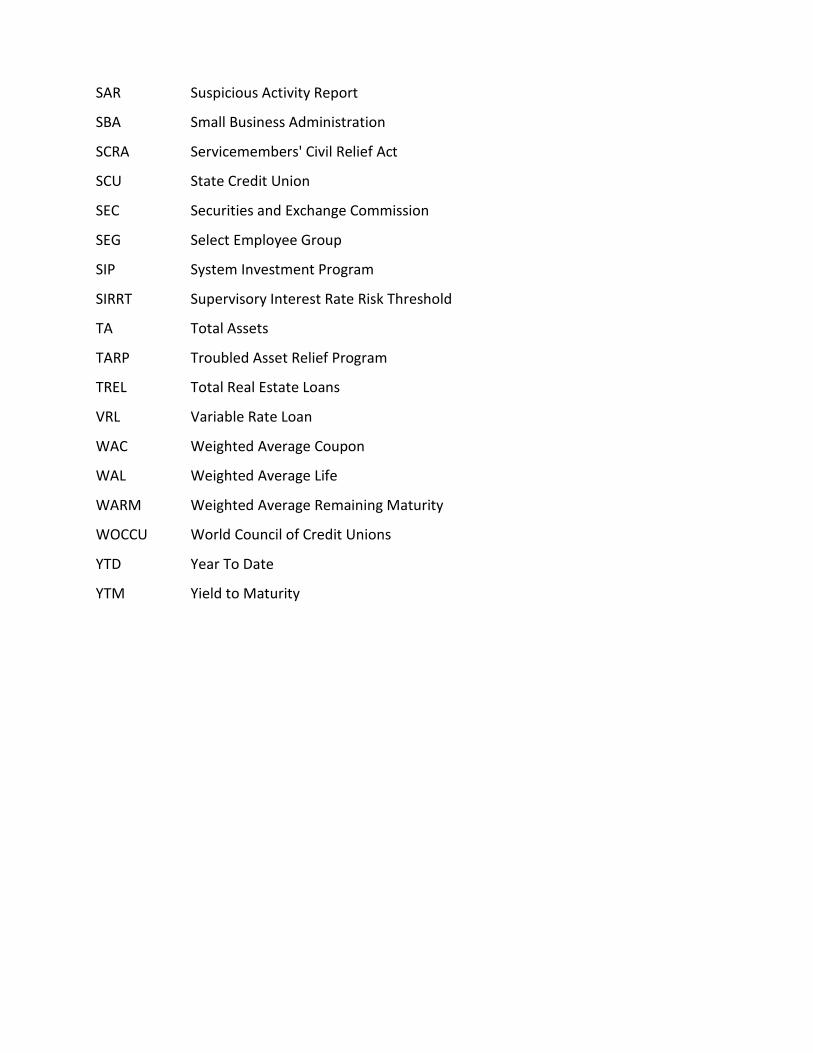

SAR Suspicious Activity Report

SBA Small Business Administration

SCRA Servicemembers' Civil Relief Act

SCU State Credit Union

SEC Securities and Exchange Commission

SEG Select Employee Group

SIP System Investment Program

SIRRT Supervisory Interest Rate Risk Threshold

TA Total Assets

TARP Troubled Asset Relief Program

TREL Total Real Estate Loans

VRL Variable Rate Loan

WAC Weighted Average Coupon

WAL Weighted Average Life

WARM Weighted Average Remaining Maturity

WOCCU World Council of Credit Unions

YTD Year To Date

YTM Yield to Maturity

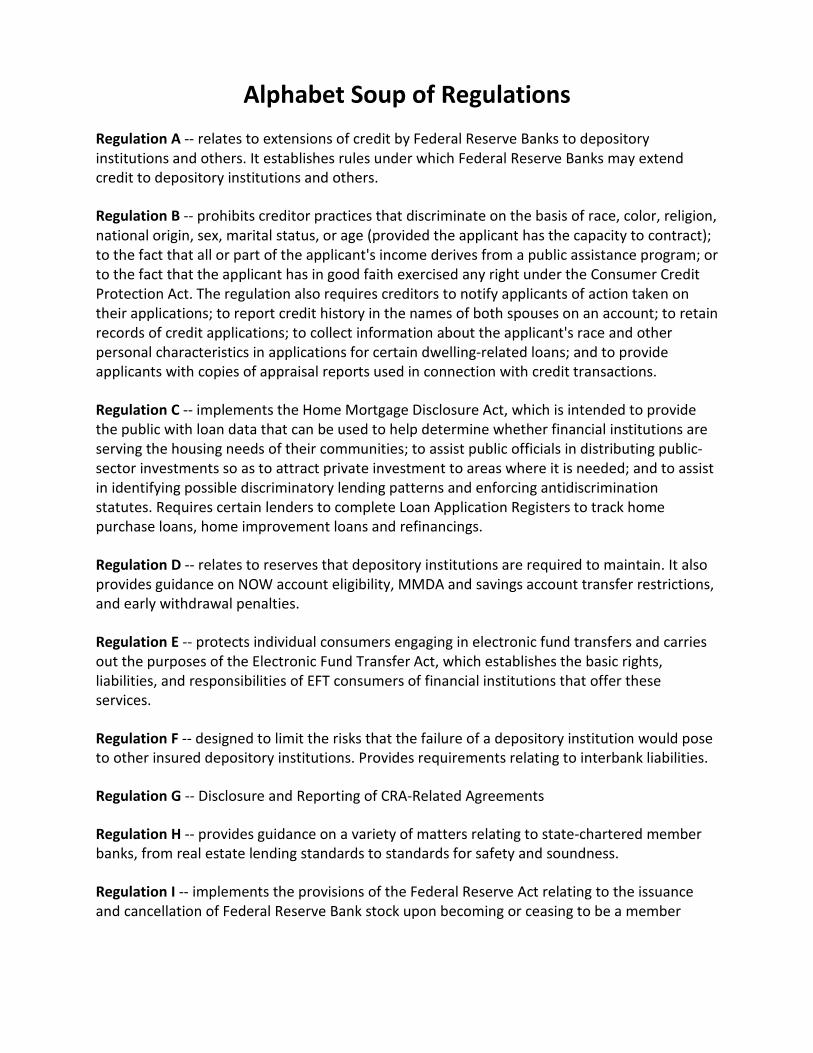

Alphabet Soup of Regulations Regulation A -- relates to extensions of credit by Federal Reserve Banks to depository institutions and others. It establishes rules under which Federal Reserve Banks may extend credit to depository institutions and others.

Regulation B -- prohibits creditor practices that discriminate on the basis of race, color, religion, national origin, sex, marital status, or age (provided the applicant has the capacity to contract); to the fact that all or part of the applicant's income derives from a public assistance program; or to the fact that the applicant has in good faith exercised any right under the Consumer Credit Protection Act. The regulation also requires creditors to notify applicants of action taken on their applications; to report credit history in the names of both spouses on an account; to retain records of credit applications; to collect information about the applicant's race and other personal characteristics in applications for certain dwelling-related loans; and to provide applicants with copies of appraisal reports used in connection with credit transactions.

Regulation C -- implements the Home Mortgage Disclosure Act, which is intended to provide the public with loan data that can be used to help determine whether financial institutions are serving the housing needs of their communities; to assist public officials in distributing public-sector investments so as to attract private investment to areas where it is needed; and to assist in identifying possible discriminatory lending patterns and enforcing antidiscrimination statutes. Requires certain lenders to complete Loan Application Registers to track home purchase loans, home improvement loans and refinancings.

Regulation D -- relates to reserves that depository institutions are required to maintain. It also provides guidance on NOW account eligibility, MMDA and savings account transfer restrictions, and early withdrawal penalties.

Regulation E -- protects individual consumers engaging in electronic fund transfers and carries out the purposes of the Electronic Fund Transfer Act, which establishes the basic rights, liabilities, and responsibilities of EFT consumers of financial institutions that offer these services.

Regulation F -- designed to limit the risks that the failure of a depository institution would pose to other insured depository institutions. Provides requirements relating to interbank liabilities.

Regulation G -- Disclosure and Reporting of CRA-Related Agreements

Regulation H -- provides guidance on a variety of matters relating to state-chartered member banks, from real estate lending standards to standards for safety and soundness.

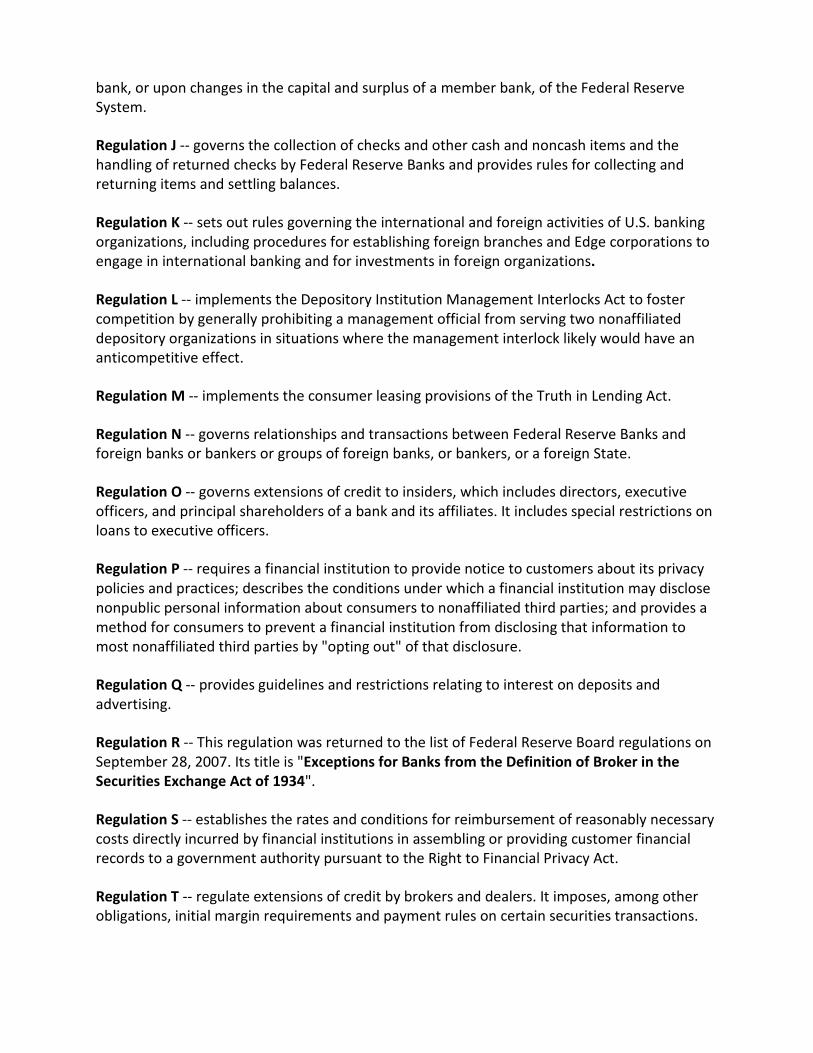

Regulation I -- implements the provisions of the Federal Reserve Act relating to the issuance and cancellation of Federal Reserve Bank stock upon becoming or ceasing to be a member

bank, or upon changes in the capital and surplus of a member bank, of the Federal Reserve System.

Regulation J -- governs the collection of checks and other cash and noncash items and the handling of returned checks by Federal Reserve Banks and provides rules for collecting and returning items and settling balances.

Regulation K -- sets out rules governing the international and foreign activities of U.S. banking organizations, including procedures for establishing foreign branches and Edge corporations to engage in international banking and for investments in foreign organizations.

Regulation L -- implements the Depository Institution Management Interlocks Act to foster competition by generally prohibiting a management official from serving two nonaffiliated depository organizations in situations where the management interlock likely would have an anticompetitive effect.

Regulation M -- implements the consumer leasing provisions of the Truth in Lending Act.

Regulation N -- governs relationships and transactions between Federal Reserve Banks and foreign banks or bankers or groups of foreign banks, or bankers, or a foreign State.

Regulation O -- governs extensions of credit to insiders, which includes directors, executive officers, and principal shareholders of a bank and its affiliates. It includes special restrictions on loans to executive officers.

Regulation P -- requires a financial institution to provide notice to customers about its privacy policies and practices; describes the conditions under which a financial institution may disclose nonpublic personal information about consumers to nonaffiliated third parties; and provides a method for consumers to prevent a financial institution from disclosing that information to most nonaffiliated third parties by "opting out" of that disclosure.

Regulation Q -- provides guidelines and restrictions relating to interest on deposits and advertising.

Regulation R -- This regulation was returned to the list of Federal Reserve Board regulations on September 28, 2007. Its title is "Exceptions for Banks from the Definition of Broker in the Securities Exchange Act of 1934".

Regulation S -- establishes the rates and conditions for reimbursement of reasonably necessary costs directly incurred by financial institutions in assembling or providing customer financial records to a government authority pursuant to the Right to Financial Privacy Act.

Regulation T -- regulate extensions of credit by brokers and dealers. It imposes, among other obligations, initial margin requirements and payment rules on certain securities transactions.

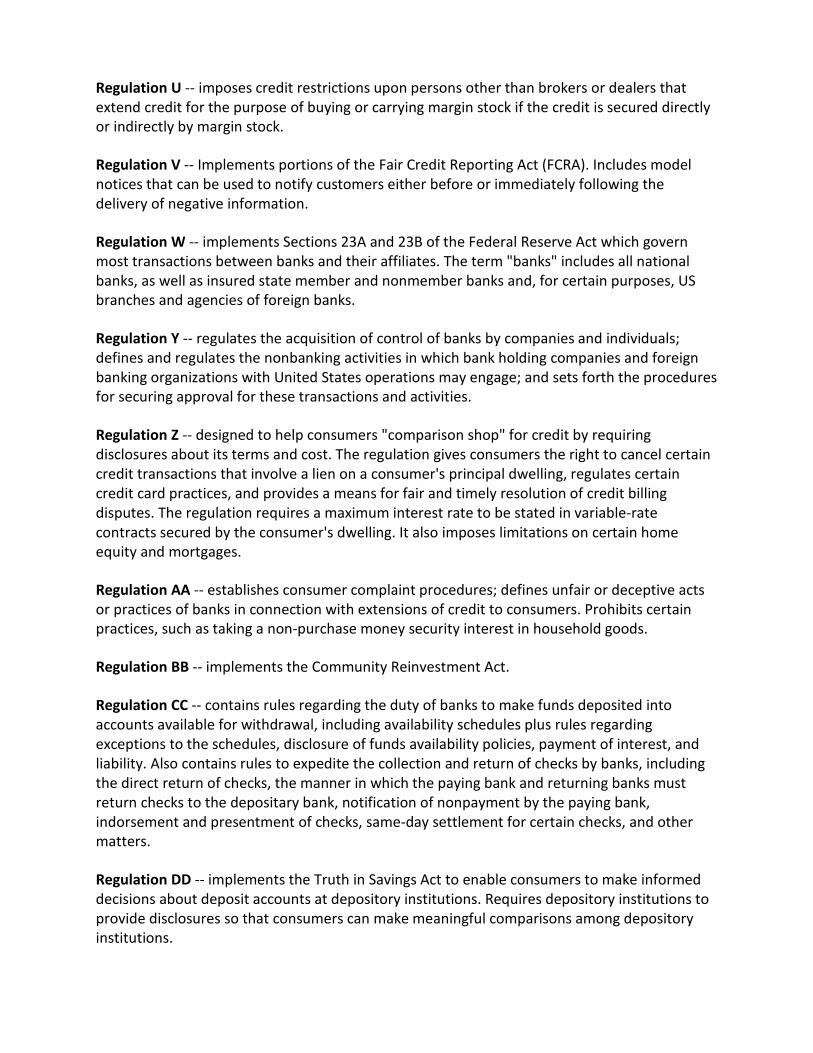

Regulation U -- imposes credit restrictions upon persons other than brokers or dealers that extend credit for the purpose of buying or carrying margin stock if the credit is secured directly or indirectly by margin stock.

Regulation V -- Implements portions of the Fair Credit Reporting Act (FCRA). Includes model notices that can be used to notify customers either before or immediately following the delivery of negative information.

Regulation W -- implements Sections 23A and 23B of the Federal Reserve Act which govern most transactions between banks and their affiliates. The term "banks" includes all national banks, as well as insured state member and nonmember banks and, for certain purposes, US branches and agencies of foreign banks.

Regulation Y -- regulates the acquisition of control of banks by companies and individuals; defines and regulates the nonbanking activities in which bank holding companies and foreign banking organizations with United States operations may engage; and sets forth the procedures for securing approval for these transactions and activities.

Regulation Z -- designed to help consumers "comparison shop" for credit by requiring disclosures about its terms and cost. The regulation gives consumers the right to cancel certain credit transactions that involve a lien on a consumer's principal dwelling, regulates certain credit card practices, and provides a means for fair and timely resolution of credit billing disputes. The regulation requires a maximum interest rate to be stated in variable-rate contracts secured by the consumer's dwelling. It also imposes limitations on certain home equity and mortgages.

Regulation AA -- establishes consumer complaint procedures; defines unfair or deceptive acts or practices of banks in connection with extensions of credit to consumers. Prohibits certain practices, such as taking a non-purchase money security interest in household goods.

Regulation BB -- implements the Community Reinvestment Act.

Regulation CC -- contains rules regarding the duty of banks to make funds deposited into accounts available for withdrawal, including availability schedules plus rules regarding exceptions to the schedules, disclosure of funds availability policies, payment of interest, and liability. Also contains rules to expedite the collection and return of checks by banks, including the direct return of checks, the manner in which the paying bank and returning banks must return checks to the depositary bank, notification of nonpayment by the paying bank, indorsement and presentment of checks, same-day settlement for certain checks, and other matters.

Regulation DD -- implements the Truth in Savings Act to enable consumers to make informed decisions about deposit accounts at depository institutions. Requires depository institutions to provide disclosures so that consumers can make meaningful comparisons among depository institutions.

Regulation EE -- expands the FDIC Improvement Act of 1991 definition of a "financial institution" for financial market participants who avail themselves of the netting provisions of the Act regarding contracts in which the parties agree to pay or receive the net, rather than the gross, payment due.

Regulation FF -- extends the rules on obtaining and using medical information in connection with credit to creditors other than those regulated by the OCC, FRB, FDIC, OTS and NCUA.

HUD's Reg X -- implements the provisions of the Real Estate Settlement Procedures Act (RESPA).

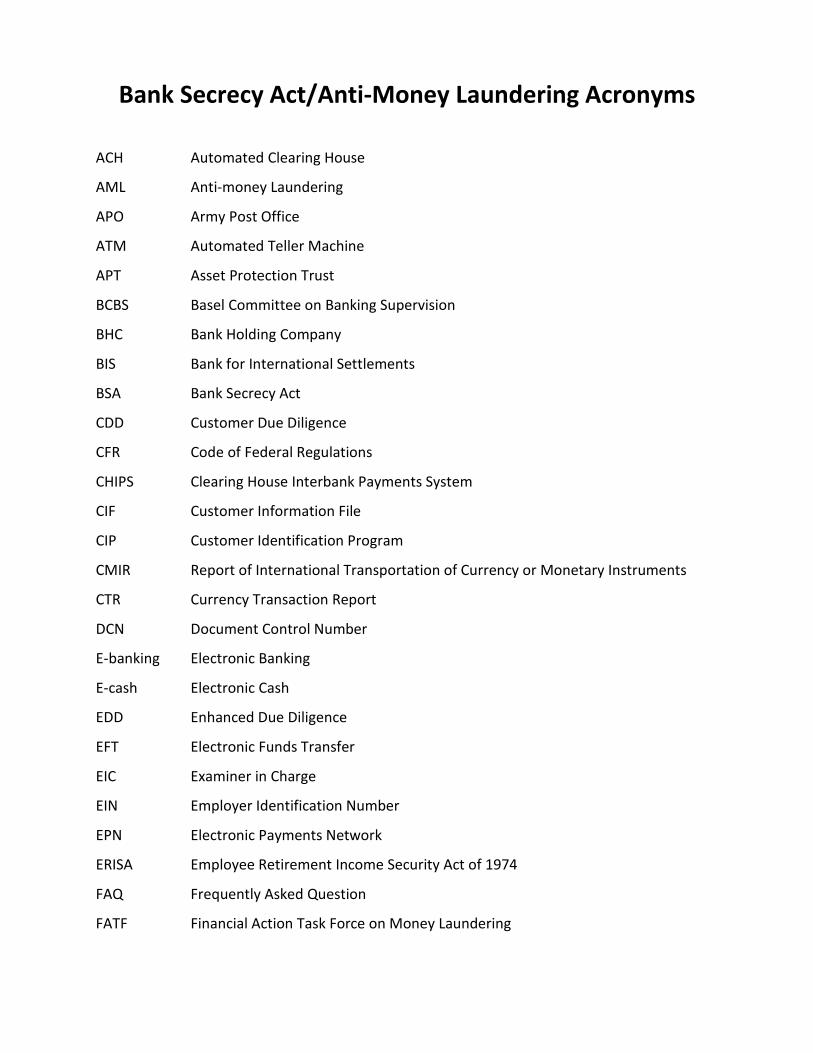

Bank Secrecy Act/Anti-Money Laundering Acronyms ACH Automated Clearing House

AML Anti-money Laundering

APO Army Post Office

ATM Automated Teller Machine

APT Asset Protection Trust

BCBS Basel Committee on Banking Supervision

BHC Bank Holding Company

BIS Bank for International Settlements

BSA Bank Secrecy Act

CDD Customer Due Diligence

CFR Code of Federal Regulations

CHIPS Clearing House Interbank Payments System

CIF Customer Information File

CIP Customer Identification Program

CMIR Report of International Transportation of Currency or Monetary Instruments

CTR Currency Transaction Report

DCN Document Control Number

E-banking Electronic Banking

E-cash Electronic Cash

EDD Enhanced Due Diligence

EFT Electronic Funds Transfer

EIC Examiner in Charge

EIN Employer Identification Number

EPN Electronic Payments Network

ERISA Employee Retirement Income Security Act of 1974

FAQ Frequently Asked Question

FATF Financial Action Task Force on Money Laundering

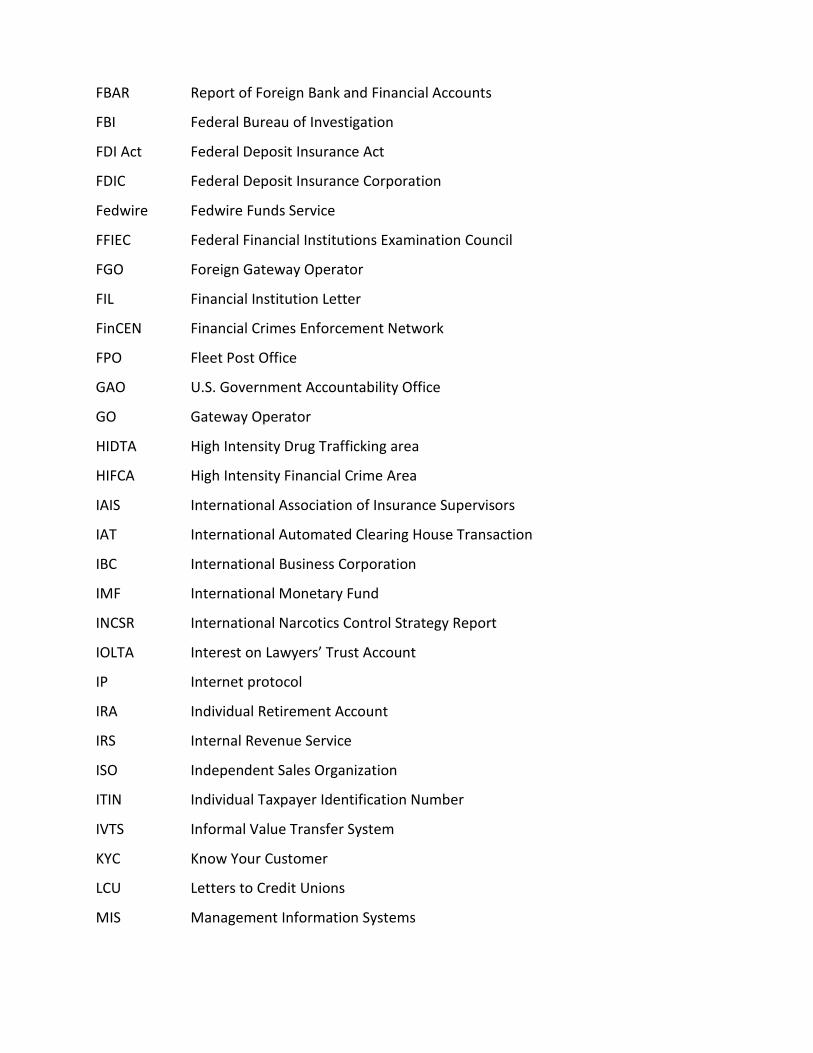

FBAR Report of Foreign Bank and Financial Accounts

FBI Federal Bureau of Investigation

FDI Act Federal Deposit Insurance Act

FDIC Federal Deposit Insurance Corporation

Fedwire Fedwire Funds Service

FFIEC Federal Financial Institutions Examination Council

FGO Foreign Gateway Operator

FIL Financial Institution Letter

FinCEN Financial Crimes Enforcement Network

FPO Fleet Post Office

GAO U.S. Government Accountability Office

GO Gateway Operator

HIDTA High Intensity Drug Trafficking area

HIFCA High Intensity Financial Crime Area

IAIS International Association of Insurance Supervisors

IAT International Automated Clearing House Transaction

IBC International Business Corporation

IMF International Monetary Fund

INCSR International Narcotics Control Strategy Report

IOLTA Interest on Lawyers’ Trust Account

IP Internet protocol

IRA Individual Retirement Account

IRS Internal Revenue Service

ISO Independent Sales Organization

ITIN Individual Taxpayer Identification Number

IVTS Informal Value Transfer System

KYC Know Your Customer

LCU Letters to Credit Unions

MIS Management Information Systems

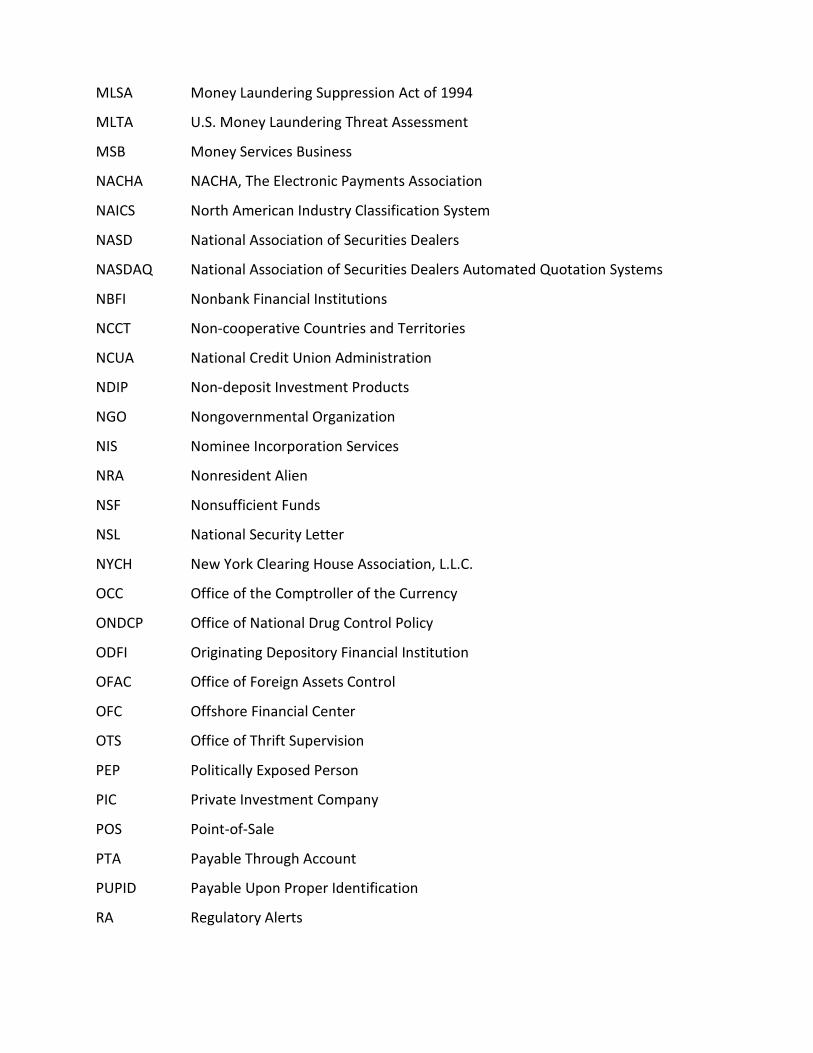

MLSA Money Laundering Suppression Act of 1994

MLTA U.S. Money Laundering Threat Assessment

MSB Money Services Business

NACHA NACHA, The Electronic Payments Association

NAICS North American Industry Classification System

NASD National Association of Securities Dealers

NASDAQ National Association of Securities Dealers Automated Quotation Systems

NBFI Nonbank Financial Institutions

NCCT Non-cooperative Countries and Territories

NCUA National Credit Union Administration

NDIP Non-deposit Investment Products

NGO Nongovernmental Organization

NIS Nominee Incorporation Services

NRA Nonresident Alien

NSF Nonsufficient Funds

NSL National Security Letter

NYCH New York Clearing House Association, L.L.C.

OCC Office of the Comptroller of the Currency

ONDCP Office of National Drug Control Policy

ODFI Originating Depository Financial Institution

OFAC Office of Foreign Assets Control

OFC Offshore Financial Center

OTS Office of Thrift Supervision

PEP Politically Exposed Person

PIC Private Investment Company

POS Point-of-Sale

PTA Payable Through Account

PUPID Payable Upon Proper Identification

RA Regulatory Alerts

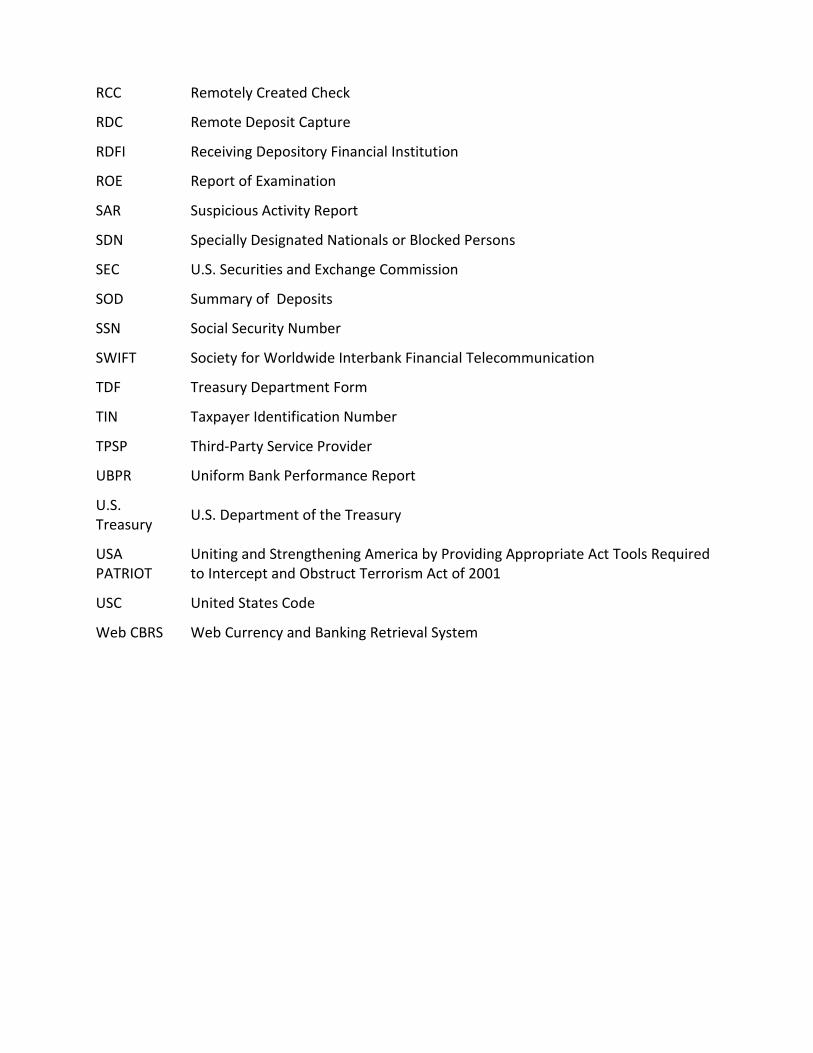

RCC Remotely Created Check

RDC Remote Deposit Capture

RDFI Receiving Depository Financial Institution

ROE Report of Examination

SAR Suspicious Activity Report

SDN Specially Designated Nationals or Blocked Persons

SEC U.S. Securities and Exchange Commission

SOD Summary of Deposits

SSN Social Security Number

SWIFT Society for Worldwide Interbank Financial Telecommunication

TDF Treasury Department Form

TIN Taxpayer Identification Number

TPSP Third-Party Service Provider

UBPR Uniform Bank Performance Report

U.S. Treasury U.S. Department of the Treasury

USA PATRIOT

Uniting and Strengthening America by Providing Appropriate Act Tools Required to Intercept and Obstruct Terrorism Act of 2001

USC United States Code

Web CBRS Web Currency and Banking Retrieval System

Cooperative Principles for Credit Unions Voluntary Membership

Credit unions are voluntary, cooperative organizations, offering services to people willing to accept the responsibilities and benefits of membership, without gender, social, racial, political or religious discrimination.

Many cooperatives, such as credit unions, operate as not-for-profit institutions with volunteer boards of directors. In the case of credit unions, members are drawn from defined fields of membership.

Democratic Member Control

Cooperatives are democratic organizations owned and controlled by their members – one member, one vote – with equal opportunity for participation in setting policies and making decisions.

Members’ Economic Participation

Members are the owners. As such, they contribute to and democratically control the capital of the cooperative. This benefits members in proportion to their transactions with the cooperative, rather than on the capital invested.

For credit unions, which typically offer better rates, fees and service than for-profit financial institutions, members recognize benefits in proportion to the extent of their financial transactions and general usage.

Autonomy and Independence

Cooperatives are autonomous, self-help organizations controlled by their members. If the cooperative enters into agreements with other organizations or raises capital from external sources, it does so based on terms that ensure democratic control by its members and maintains the cooperative autonomy.

Education, Training and Information

Cooperatives provide education and training for members, elected representatives, managers and employees so they can contribute effectively to the development of the cooperative.

Credit unions place particular importance on educational opportunities for their volunteer directors and financial education for their members and the public, especially the nation’s youth. Credit unions also recognize the importance of ensuring the general public and policy makers are informed about the nature, structure and benefits of cooperatives.

Cooperation Among Cooperatives

Cooperatives serve their members most effectively and strengthen the cooperative movement by working together through local, state, national and international structures.

Concern for Community

While focusing on member needs, cooperatives work for the sustainable development of communities, including people of modest means, through policies developed and accepted by the members.

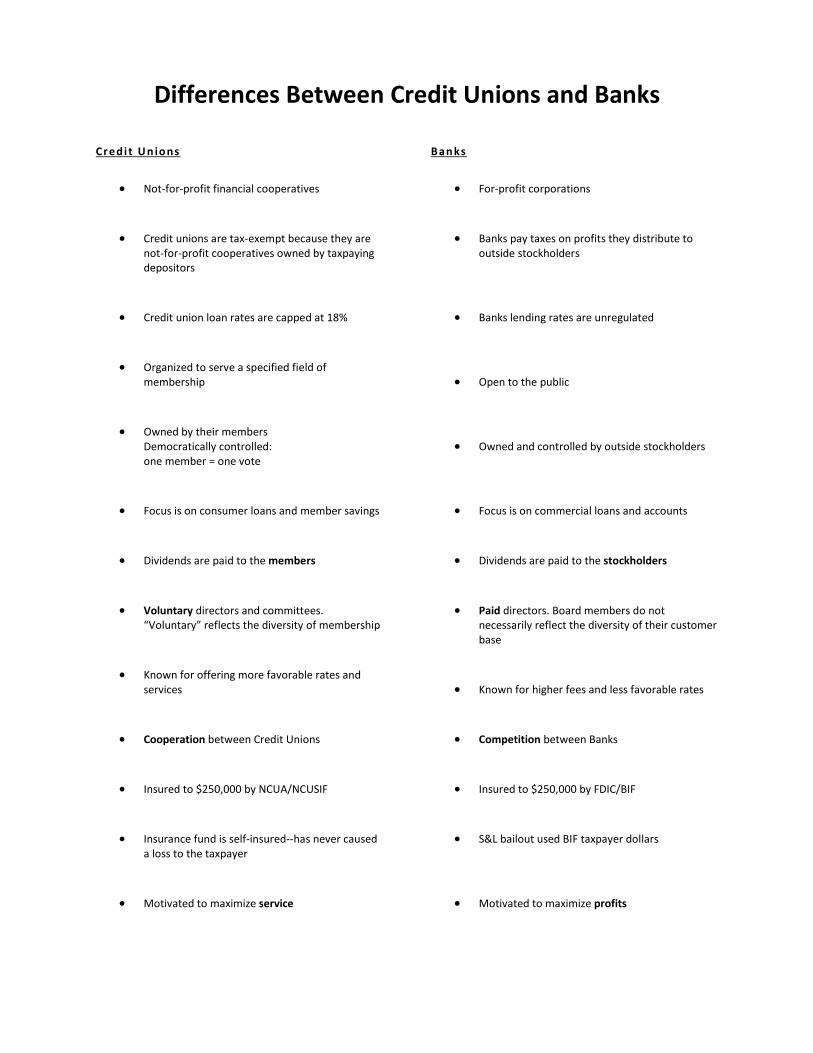

Differences Between Credit Unions and Banks

Credi t U n io ns

• Not-for-profit financial cooperatives

• Credit unions are tax-exempt because they are not-for-profit cooperatives owned by taxpaying depositors

• Credit union loan rates are capped at 18%

• Organized to serve a specified field of membership

• Owned by their members Democratically controlled: one member = one vote

• Focus is on consumer loans and member savings

• Dividends are paid to the members

• Voluntary directors and committees. “Voluntary” reflects the diversity of membership

• Known for offering more favorable rates and services

• Cooperation between Credit Unions

• Insured to $250,000 by NCUA/NCUSIF

• Insurance fund is self-insured--has never caused a loss to the taxpayer

• Motivated to maximize service

Ban ks

• For-profit corporations

• Banks pay taxes on profits they distribute to outside stockholders

• Banks lending rates are unregulated

• Open to the public

• Owned and controlled by outside stockholders

• Focus is on commercial loans and accounts

• Dividends are paid to the stockholders

• Paid directors. Board members do not necessarily reflect the diversity of their customer base

• Known for higher fees and less favorable rates

• Competition between Banks

• Insured to $250,000 by FDIC/BIF

• S&L bailout used BIF taxpayer dollars

• Motivated to maximize profits

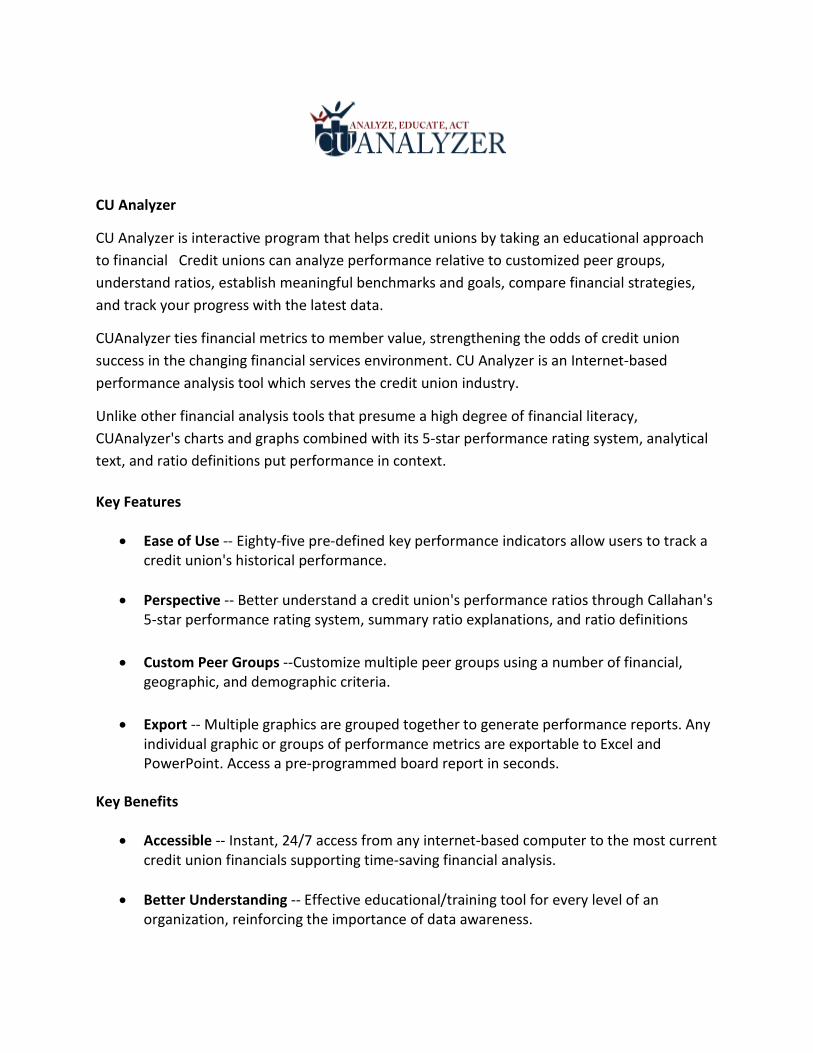

CU Analyzer

CU Analyzer is interactive program that helps credit unions by taking an educational approach to financial Credit unions can analyze performance relative to customized peer groups, understand ratios, establish meaningful benchmarks and goals, compare financial strategies, and track your progress with the latest data.

CUAnalyzer ties financial metrics to member value, strengthening the odds of credit union success in the changing financial services environment. CU Analyzer is an Internet-based performance analysis tool which serves the credit union industry.

Unlike other financial analysis tools that presume a high degree of financial literacy, CUAnalyzer's charts and graphs combined with its 5-star performance rating system, analytical text, and ratio definitions put performance in context.

Key Features

• Ease of Use -- Eighty-five pre-defined key performance indicators allow users to track a credit union's historical performance.

• Perspective -- Better understand a credit union's performance ratios through Callahan's 5-star performance rating system, summary ratio explanations, and ratio definitions

• Custom Peer Groups --Customize multiple peer groups using a number of financial, geographic, and demographic criteria.

• Export -- Multiple graphics are grouped together to generate performance reports. Any individual graphic or groups of performance metrics are exportable to Excel and PowerPoint. Access a pre-programmed board report in seconds.

Key Benefits

• Accessible -- Instant, 24/7 access from any internet-based computer to the most current credit union financials supporting time-saving financial analysis.

• Better Understanding -- Effective educational/training tool for every level of an organization, reinforcing the importance of data awareness.

• Better Comparisons -- Dynamic peer groups provide unique performance insight with your most relevant peer credit unions.

• Performance Insights -- Charting and graphing functionality help users prepare presentations materials. Spend more time analyzing trends rather than building materials.