Embed Size (px)

Citation preview

NCURA Regional Meeting April 5, 2011

Allowable Costs – Proposal Development to Project Closeout

Presented by: Ralph L. BrownDirector of Research AdministrationColorado School of Mines

Gale YamadaDirector of Administrative ServicesUniversity of Hawaii at Manoa

Goals for this session

Guiding principles Research award cycle Best practices Roles and Responsibilities

INTRODUCTION TO OMB CIRCULAR A-21

DEFINES AN "ALLOWABLE COST"

INSTRUCTIONS FOR THE UNIVERSITY TO ALLOCATE FACILITIES AND ADMINISTRATIVE COSTS PROPERLY AND TO CALCULATE THE FACILITIES AND ADMIN RATE

APPLIES TO PROJECT COSTS REIMBURSED BY THE GOVERNMENT AND TO COST SHARING OR MATCHING FUNDS

GENERAL REQUIREMENTS: REASONABLE: ALLOCABLE TO (BENEFITS) THE PROJECT SUPPORTED BY THE

GRANT OR CONTRACT TREATED CONSISTENTLY (INCLUDING CONSISTENT

TREATMENT AS EITHER A DIRECT OR INDIRECT COST

http://www.whitehouse.gov/omb/circulars/a021/a21_2004.html

EXAMPLES OF COSTS NOT USUALLY ALLOWABLE

Travel Fly America Act (handout)

First Class Travel

General Purpose Equipment

Paper Towels

UNALLOWABLE COSTS

Section J of A-21 specifically lists and defines categories of allowable and unallowable costs

OMB Circular A-21 website

UNALLOWABLE COSTS

Section J, specific expenses identified as unallowable: Advertising and public relations costs Alcoholic beverages Alumni activities Bad debts Institution-furnished automobiles Donations or contributions Entertainment Lobbying Fines and penalties Goods and services for personal use

UNALLOWABLE COSTS (cont’d)

Housing and personal living expenses Interest, fund raising and investment

management costs Membership in social, dining, country clubs, or

civic organizations Selling and marketing Student activities Airfare costs in excess of the lowest available

commercial discount airfare (with specific exceptions)

Flowers, gifts Parking tickets

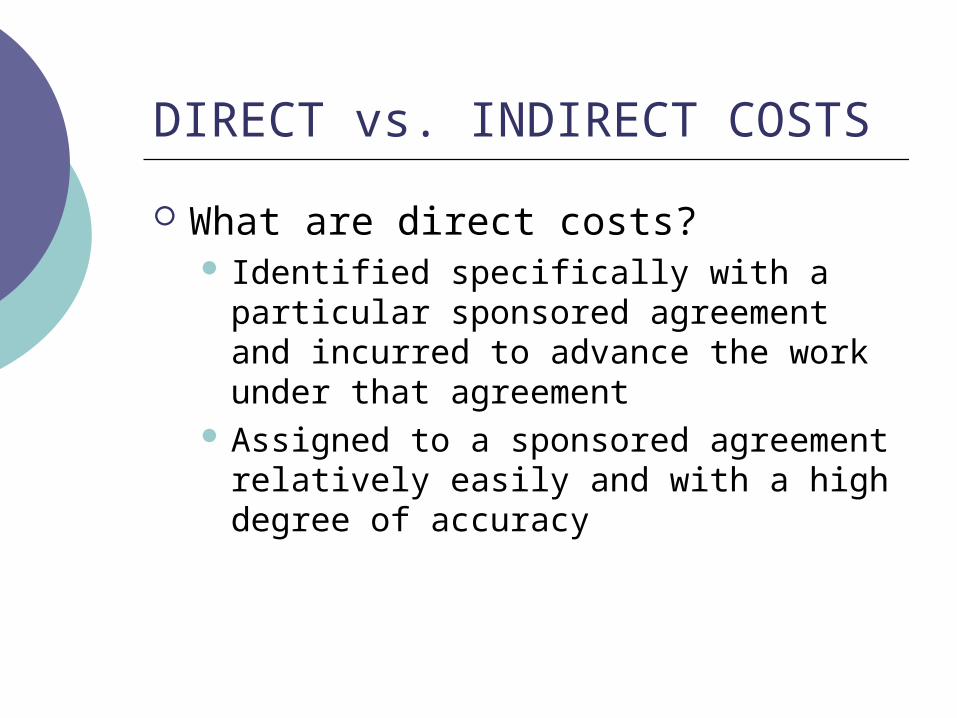

DIRECT vs. INDIRECT COSTS

What are direct costs? Identified specifically with a particular

sponsored agreement and incurred to advance the work under that agreement

Assigned to a sponsored agreement relatively easily and with a high degree of accuracy

DIRECT vs. INDIRECT COSTS

What are F&A costs (Indirect costs)? Benefit common or joint activities Benefit numerous projects

Cannot readily be identified with a particular sponsored project

Cannot be proportioned to benefit a group of sponsored projects with relative ease or with a high degree of accuracy

(Handout)

NORMALLY Indirect costs

Administrative and Clerical Salaries Office supplies, postage, dues and

memberships, local telephones(telephone equipment)

Computers – General Purpose Equipment

A-21 Exhibit C provides for exceptions for charging normally indirect costs if the project is a major project

THE COST ACCOUNTING STANDARDS

Originally created as an Act of Congress

Applicable to the Department of Defense

Added to A-21 in 1994 DOD subject to 19 CAS, only 4 were

added to A-21

CAS 501

Consistency in estimating, accumulating and reporting costs by educational institutions – all institutions must consistently follow established cost accounting practices when estimating (budgeting), accumulating, (accounting), and reporting. Collecting and classifying cost data in an

organized and consistent manner Does not prescribe the amount of detail

required, but must be able to accumulate and report actual cost at a level which permits meaningful comparison with budgeted estimates, i.e. proposal budgets “chemicals”, but accounting system charges “materials & supplies”.

CAS 502

Consistency in allocating costs incurred for the same purpose by educational institutions – requires that each type of cost be allocated only once and on only one basis to any sponsored agreement.

Double counting occurs when the same cost is charged both indirectly and directly if it is incurred for the same purpose.

Telephone equipment costs “normally” charged as indirect charged directly to project

CAS 505

Accounting for Unallowable Costs – unallowable costs must be identified and excluded from all claims for reimbursement. Unallowable costs must not be included as either Direct or Indirect costs in the F&A calculation – OR be used as cost-sharing!

CAS 506

Cost Accounting Period – institutions must consistently use the same cost accounting period for estimating, accumulating and reporting costs.

COST ACCOUNTING STANDARDS EXCEPTIONS

Per OMB A-21 the following three criteria must be met for F&A costs to be directly charged: 1. The costs must be specifically and readily

identifiable to a specific project with a high degree of accuracy.

2. The costs are required by the project scope, due to the project’s special purpose or circumstances.

3. The costs must be specifically budgeted as a line item in the proposal budget and justified in the proposal narrative.

COST TRANSFERS

Reassignment of costs to a sponsored project from another source of funds can be allowable when: Correcting errors Allocating costs that benefit more than

one project Removing over-expenditures to another non-restricted source of funding

COST TRANSFERS

RED FLAGS Transfers older

than 90 days Transfers in the

last month of the award or after the award has expired

Round numbers!

Explanations that raise more questions than answers

COST SHARING The portion of project costs not borne by the Sponsor. CRITERIA:

The contributions to be cost shared are verifiable by University records.

Allowable, allocable, reasonable, and necessary for proper and efficient accomplishment of specific project or program objectives.

Federal funds, directly or indirectly, are not used for cost sharing on other federally funded projects, except where authorized by federal statute.

Not included as contributions for any other project.

Directly identifiable with the sponsored project as outlined in the proposal and be included in the award notice

Best Practices

Be familiar with the regulations or at least know where to look for the answer.

Anticipate areas of vulnerability and develop management controls and/or monitoring strategies

Document, Document and Document any exceptions to the Cost Accounting Standards.(Handout)

Tough questions – seek out advice from other colleagues. NCURA, COGR etc.

The Research Cycle

Proposal Award Performance Closeout Audit

Responsibilities: PI

Prep of programmatic proposal Development of project budget Monitor programmatic and financial

performance Adhere to terms and conditions of

award Final progress report Financial responsibility and audit

Responsibilities: Dept Administrator

Assists and advises PI in the prep of proposal in accordance with sponsor terms, applicable regulations, institutional policies.

Assists PI in compliance with award terms and conditions, regulations, institutional policies

Monitors expenditure of award funds Coordinates with central offices on reporting Assists central administration with closeout and

audit activities Disclose apparent area(s) of noncompliance to an

appropriate responsible official

Responsibilities – Sponsored Programs Office

Review of Proposals for Regulatory and Policy Issues,

Notify post-award administrators of award terms in advance of spending.(handout)

Review accounting transactions based on allowability criteria, terms and conditions and agency guidelines.

Prepare final financial reports in compliance with award terms and conditions.

Closeout Responsibilities

Costs must be allowable, reasonable, allocable, and consistent with the terms of the agreement

Departmental Administrator and PI must ensure that all costs are necessary for performance of the project, incurred within the period of performance and charged to the project within the specified period.

Questions?

Evaluations

Thank You!

Ralph L. Brown – [email protected]

Gale Yamada- [email protected] Web site:

http://inside.mines.edu/administrative_departments