Embed Size (px)

Citation preview

Date 15-11-2016NCML Commodity and Market Monitor

Date 15-11-2016NCML Commodity and Market Monitor

1

Fundamentals- Domestic amp International

Price Trend ampTechnicals

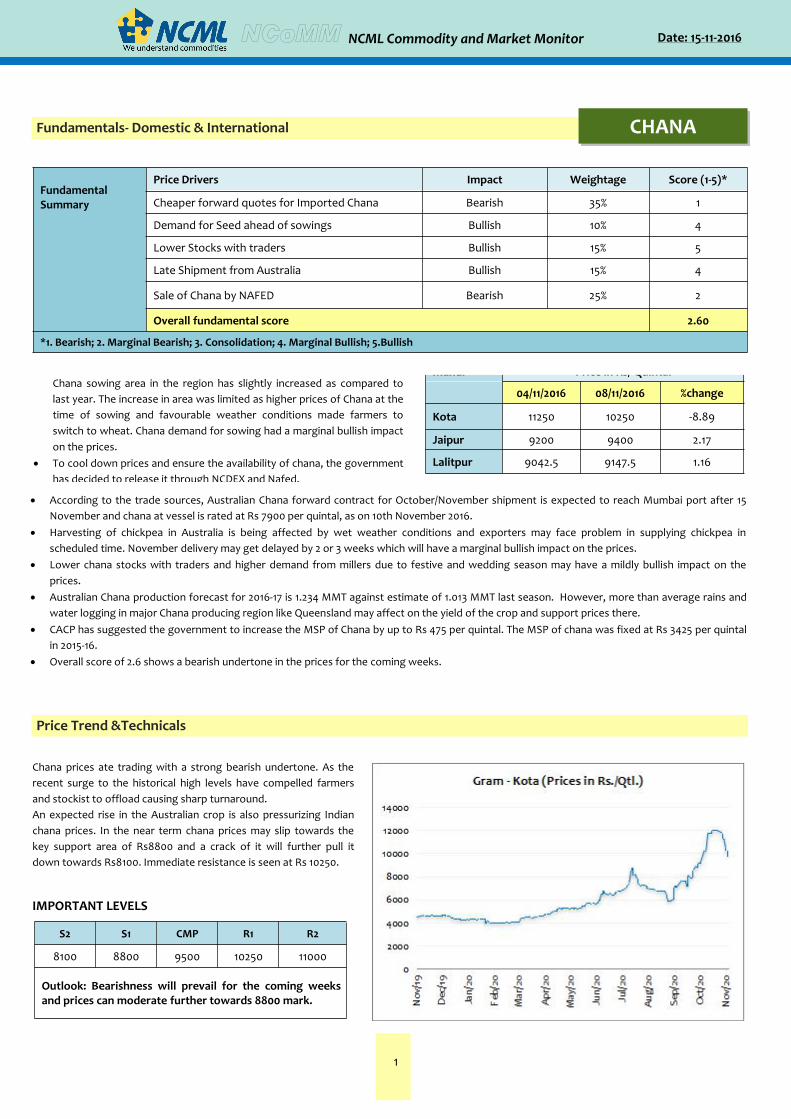

CHANA

Chana prices ate trading with a strong bearish undertone As therecent surge to the historical high levels have compelled farmersand stockist to offload causing sharp turnaroundAn expected rise in the Australian crop is also pressurizing Indianchana prices In the near term chana prices may slip towards thekey support area of Rs8800 and a crack of it will further pull itdown towards Rs8100 Immediate resistance is seen at Rs 10250

IMPORTANT LEVELS

S2 S1 CMP R1 R2

8100 8800 9500 10250 11000

Outlook Bearishness will prevail for the coming weeksand prices can moderate further towards 8800 mark

According to the local traders of Ganjbasoda region of Madhya PradeshChana sowing area in the region has slightly increased as compared tolast year The increase in area was limited as higher prices of Chana at thetime of sowing and favourable weather conditions made farmers toswitch to wheat Chana demand for sowing had a marginal bullish impacton the prices

To cool down prices and ensure the availability of chana the governmenthas decided to release it through NCDEX and Nafed

Mandi Price in Rs Quintal

04112016 08112016 change

Kota 11250 10250 -889

Jaipur 9200 9400 217

Lalitpur 90425 91475 116

According to the trade sources Australian Chana forward contract for OctoberNovember shipment is expected to reach Mumbai port after 15November and chana at vessel is rated at Rs 7900 per quintal as on 10th November 2016

Harvesting of chickpea in Australia is being affected by wet weather conditions and exporters may face problem in supplying chickpea inscheduled time November delivery may get delayed by 2 or 3 weeks which will have a marginal bullish impact on the prices

Lower chana stocks with traders and higher demand from millers due to festive and wedding season may have a mildly bullish impact on theprices

Australian Chana production forecast for 2016-17 is 1234 MMT against estimate of 1013 MMT last season However more than average rains andwater logging in major Chana producing region like Queensland may affect on the yield of the crop and support prices there

CACP has suggested the government to increase the MSP of Chana by up to Rs 475 per quintal The MSP of chana was fixed at Rs 3425 per quintalin 2015-16

Overall score of 26 shows a bearish undertone in the prices for the coming weeks

FundamentalSummary

Price Drivers Impact Weightage Score (1-5)

Cheaper forward quotes for Imported Chana Bearish 35 1

Demand for Seed ahead of sowings Bullish 10 4

Lower Stocks with traders Bullish 15 5

Late Shipment from Australia Bullish 15 4

Sale of Chana by NAFED Bearish 25 2

Overall fundamental score 260

1 Bearish 2 Marginal Bearish 3 Consolidation 4 Marginal Bullish 5Bullish

Date 15-11-2016NCML Commodity and Market Monitor

2

Fundamentals- Domestic amp International

Price Trend ampTechnicals

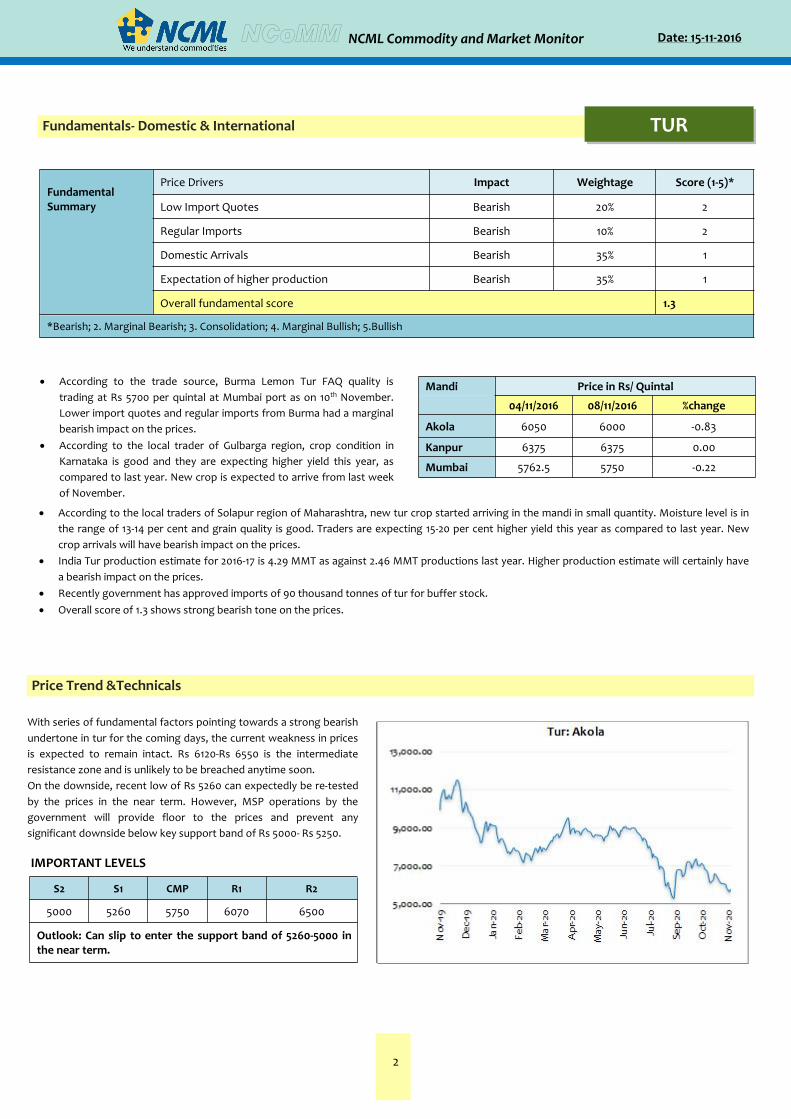

TUR

With series of fundamental factors pointing towards a strong bearishundertone in tur for the coming days the current weakness in pricesis expected to remain intact Rs 6120-Rs 6550 is the intermediateresistance zone and is unlikely to be breached anytime soonOn the downside recent low of Rs 5260 can expectedly be re-testedby the prices in the near term However MSP operations by thegovernment will provide floor to the prices and prevent anysignificant downside below key support band of Rs 5000- Rs 5250

IMPORTANT LEVELS

S2 S1 CMP R1 R2

5000 5260 5750 6070 6500

Outlook Can slip to enter the support band of 5260-5000 inthe near term

According to the trade source Burma Lemon Tur FAQ quality istrading at Rs 5700 per quintal at Mumbai port as on 10th NovemberLower import quotes and regular imports from Burma had a marginalbearish impact on the prices

According to the local trader of Gulbarga region crop condition inKarnataka is good and they are expecting higher yield this year ascompared to last year New crop is expected to arrive from last weekof November

Mandi Price in Rs Quintal

04112016 08112016 change

Akola 6050 6000 -083

Kanpur 6375 6375 000

Mumbai 57625 5750 -022

According to the local traders of Solapur region of Maharashtra new tur crop started arriving in the mandi in small quantity Moisture level is inthe range of 13-14 per cent and grain quality is good Traders are expecting 15-20 per cent higher yield this year as compared to last year Newcrop arrivals will have bearish impact on the prices

India Tur production estimate for 2016-17 is 429 MMT as against 246 MMT productions last year Higher production estimate will certainly havea bearish impact on the prices

Recently government has approved imports of 90 thousand tonnes of tur for buffer stock Overall score of 13 shows strong bearish tone on the prices

FundamentalSummary

Price Drivers Impact Weightage Score (1-5)

Low Import Quotes Bearish 20 2

Regular Imports Bearish 10 2

Domestic Arrivals Bearish 35 1

Expectation of higher production Bearish 35 1

Overall fundamental score 13

Bearish 2 Marginal Bearish 3 Consolidation 4 Marginal Bullish 5Bullish

Date 15-11-2016NCML Commodity and Market Monitor

3

Price Trend ampTechnicals

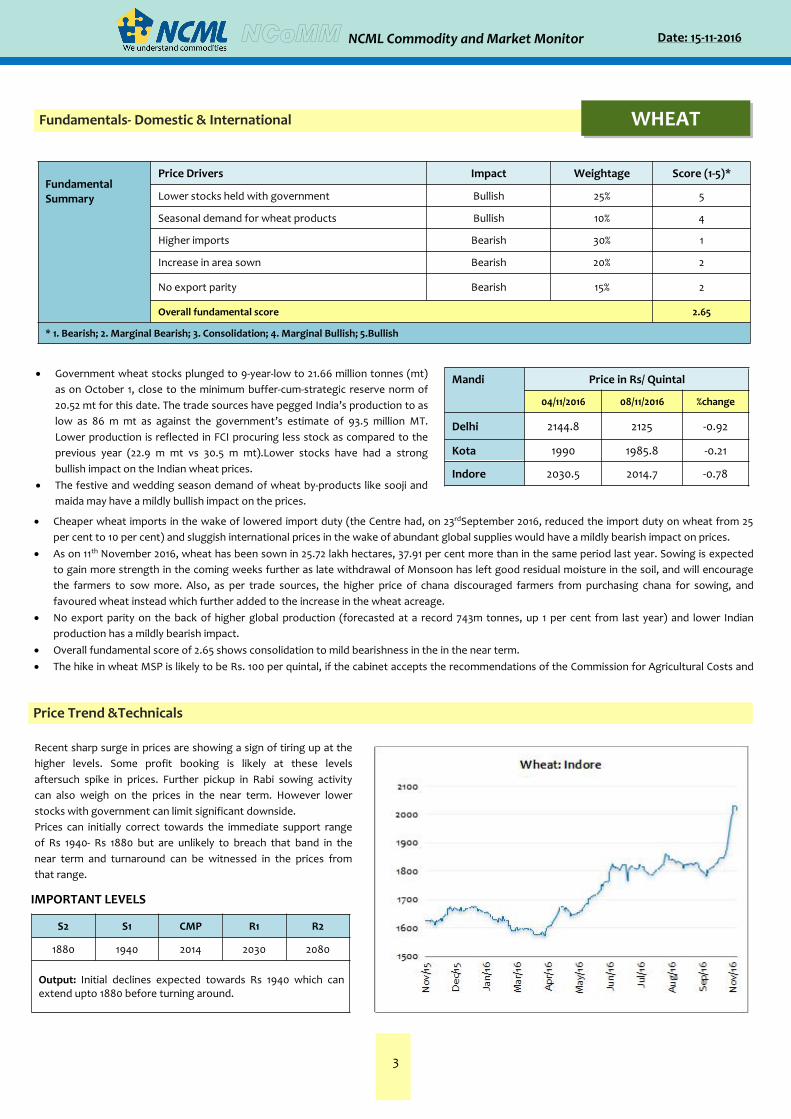

Recent sharp surge in prices are showing a sign of tiring up at thehigher levels Some profit booking is likely at these levelsaftersuch spike in prices Further pickup in Rabi sowing activitycan also weigh on the prices in the near term However lowerstocks with government can limit significant downsidePrices can initially correct towards the immediate support rangeof Rs 1940- Rs 1880 but are unlikely to breach that band in thenear term and turnaround can be witnessed in the prices fromthat range

IMPORTANT LEVELS

S2 S1 CMP R1 R2

1880 1940 2014 2030 2080

Output Initial declines expected towards Rs 1940 which canextend upto 1880 before turning around

Government wheat stocks plunged to 9-year-low to 2166 million tonnes (mt)as on October 1 close to the minimum buffer-cum-strategic reserve norm of2052 mt for this date The trade sources have pegged Indiarsquos production to aslow as 86 m mt as against the governmentrsquos estimate of 935 million MTLower production is reflected in FCI procuring less stock as compared to theprevious year (229 m mt vs 305 m mt)Lower stocks have had a strongbullish impact on the Indian wheat prices

The festive and wedding season demand of wheat by-products like sooji andmaida may have a mildly bullish impact on the prices

Mandi Price in Rs Quintal

04112016 08112016 change

Delhi 21448 2125 -092

Kota 1990 19858 -021

Indore 20305 20147 -078

Cheaper wheat imports in the wake of lowered import duty (the Centre had on 23rdSeptember 2016 reduced the import duty on wheat from 25per cent to 10 per cent) and sluggish international prices in the wake of abundant global supplies would have a mildly bearish impact on prices

As on 11th November 2016 wheat has been sown in 2572 lakh hectares 3791 per cent more than in the same period last year Sowing is expectedto gain more strength in the coming weeks further as late withdrawal of Monsoon has left good residual moisture in the soil and will encouragethe farmers to sow more Also as per trade sources the higher price of chana discouraged farmers from purchasing chana for sowing andfavoured wheat instead which further added to the increase in the wheat acreage

No export parity on the back of higher global production (forecasted at a record 743m tonnes up 1 per cent from last year) and lower Indianproduction has a mildly bearish impact

Overall fundamental score of 265 shows consolidation to mild bearishness in the in the near term The hike in wheat MSP is likely to be Rs 100 per quintal if the cabinet accepts the recommendations of the Commission for Agricultural Costs and

Prices

FundamentalSummary

Price Drivers Impact Weightage Score (1-5)

Lower stocks held with government Bullish 25 5

Seasonal demand for wheat products Bullish 10 4

Higher imports Bearish 30 1

Increase in area sown Bearish 20 2

No export parity Bearish 15 2

Overall fundamental score 265

1 Bearish 2 Marginal Bearish 3 Consolidation 4 Marginal Bullish 5Bullish

Fundamentals- Domestic amp International WHEAT

Date 15-11-2016NCML Commodity and Market Monitor

4

Fundamentals- Domestic amp International

Price Trend ampTechnicals

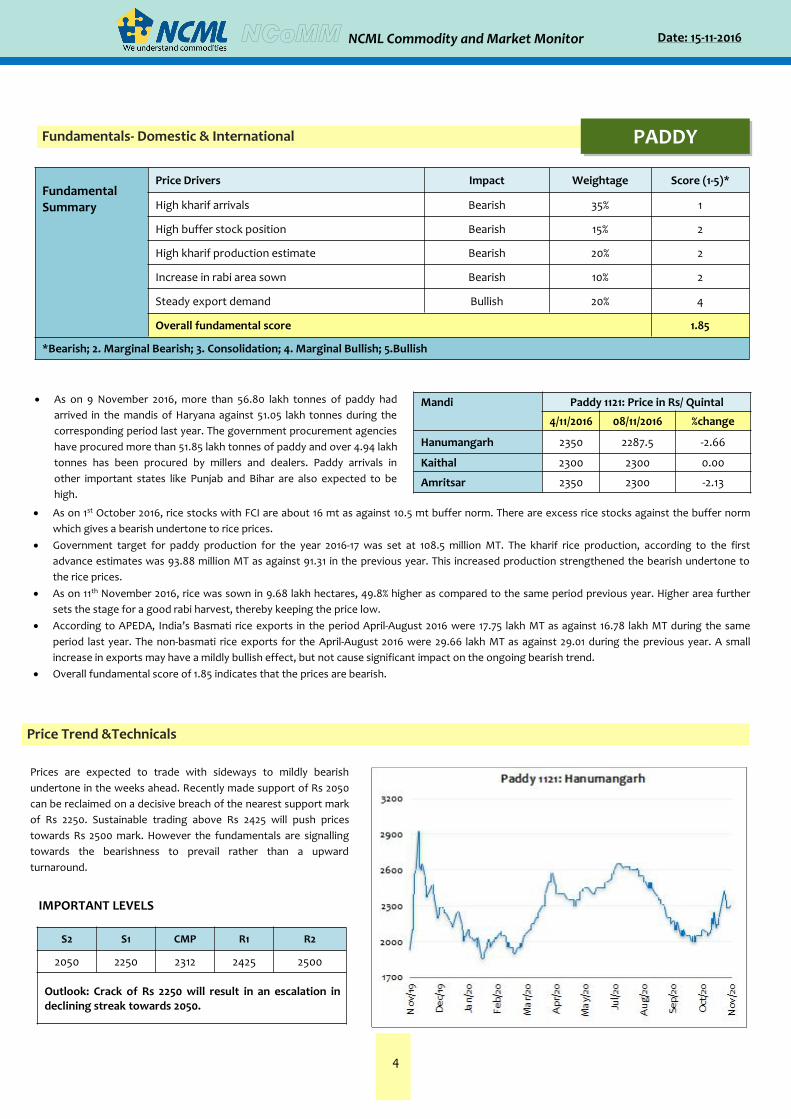

PADDY

Prices are expected to trade with sideways to mildly bearishundertone in the weeks ahead Recently made support of Rs 2050can be reclaimed on a decisive breach of the nearest support markof Rs 2250 Sustainable trading above Rs 2425 will push pricestowards Rs 2500 mark However the fundamentals are signallingtowards the bearishness to prevail rather than a upwardturnaround

IMPORTANT LEVELS

S2 S1 CMP R1 R2

2050 2250 2312 2425 2500

Outlook Crack of Rs 2250 will result in an escalation indeclining streak towards 2050

As on 9 November 2016 more than 5680 lakh tonnes of paddy hadarrived in the mandis of Haryana against 5105 lakh tonnes during thecorresponding period last year The government procurement agencieshave procured more than 5185 lakh tonnes of paddy and over 494 lakhtonnes has been procured by millers and dealers Paddy arrivals inother important states like Punjab and Bihar are also expected to behigh

Mandi Paddy 1121 Price in Rs Quintal

4112016 08112016 change

Hanumangarh 2350 22875 -266

Kaithal 2300 2300 000

Amritsar 2350 2300 -213

As on 1st October 2016 rice stocks with FCI are about 16 mt as against 105 mt buffer norm There are excess rice stocks against the buffer normwhich gives a bearish undertone to rice prices

Government target for paddy production for the year 2016-17 was set at 1085 million MT The kharif rice production according to the firstadvance estimates was 9388 million MT as against 9131 in the previous year This increased production strengthened the bearish undertone tothe rice prices

As on 11th November 2016 rice was sown in 968 lakh hectares 498 higher as compared to the same period previous year Higher area furthersets the stage for a good rabi harvest thereby keeping the price low

According to APEDA Indiarsquos Basmati rice exports in the period April-August 2016 were 1775 lakh MT as against 1678 lakh MT during the sameperiod last year The non-basmati rice exports for the April-August 2016 were 2966 lakh MT as against 2901 during the previous year A smallincrease in exports may have a mildly bullish effect but not cause significant impact on the ongoing bearish trend

Overall fundamental score of 185 indicates that the prices are bearish

FundamentalSummary

Price Drivers Impact Weightage Score (1-5)

High kharif arrivals Bearish 35 1

High buffer stock position Bearish 15 2

High kharif production estimate Bearish 20 2

Increase in rabi area sown Bearish 10 2

Steady export demand Bullish 20 4

Overall fundamental score 185

Bearish 2 Marginal Bearish 3 Consolidation 4 Marginal Bullish 5Bullish

Date 15-11-2016NCML Commodity and Market Monitor

5

Fundamentals- Domestic amp International

Price Trend ampTechnicals

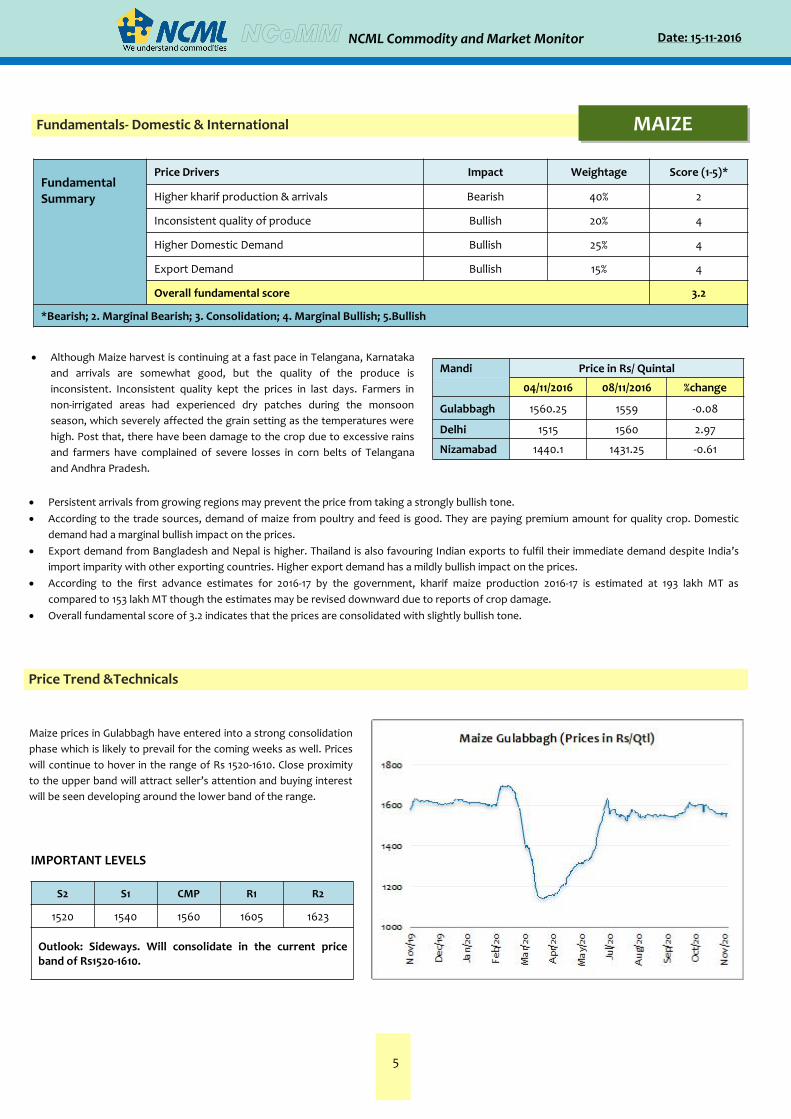

MAIZE

Maize prices in Gulabbagh have entered into a strong consolidationphase which is likely to prevail for the coming weeks as well Priceswill continue to hover in the range of Rs 1520-1610 Close proximityto the upper band will attract sellerrsquos attention and buying interestwill be seen developing around the lower band of the range

IMPORTANT LEVELS

S2 S1 CMP R1 R2

1520 1540 1560 1605 1623

Outlook Sideways Will consolidate in the current priceband of Rs1520-1610

Although Maize harvest is continuing at a fast pace in Telangana Karnatakaand arrivals are somewhat good but the quality of the produce isinconsistent Inconsistent quality kept the prices in last days Farmers innon-irrigated areas had experienced dry patches during the monsoonseason which severely affected the grain setting as the temperatures werehigh Post that there have been damage to the crop due to excessive rainsand farmers have complained of severe losses in corn belts of Telanganaand Andhra Pradesh

Mandi Price in Rs Quintal

04112016 08112016 change

Gulabbagh 156025 1559 -008

Delhi 1515 1560 297

Nizamabad 14401 143125 -061

Persistent arrivals from growing regions may prevent the price from taking a strongly bullish tone According to the trade sources demand of maize from poultry and feed is good They are paying premium amount for quality crop Domestic

demand had a marginal bullish impact on the prices Export demand from Bangladesh and Nepal is higher Thailand is also favouring Indian exports to fulfil their immediate demand despite Indiarsquos

import imparity with other exporting countries Higher export demand has a mildly bullish impact on the prices According to the first advance estimates for 2016-17 by the government kharif maize production 2016-17 is estimated at 193 lakh MT as

compared to 153 lakh MT though the estimates may be revised downward due to reports of crop damage Overall fundamental score of 32 indicates that the prices are consolidated with slightly bullish tone

FundamentalSummary

Price Drivers Impact Weightage Score (1-5)

Higher kharif production amp arrivals Bearish 40 2

Inconsistent quality of produce Bullish 20 4

Higher Domestic Demand Bullish 25 4

Export Demand Bullish 15 4

Overall fundamental score 32

Bearish 2 Marginal Bearish 3 Consolidation 4 Marginal Bullish 5Bullish

Date 15-11-2016NCML Commodity and Market Monitor

6

Fundamentals- Domestic amp International

Price Trend ampTechnicals

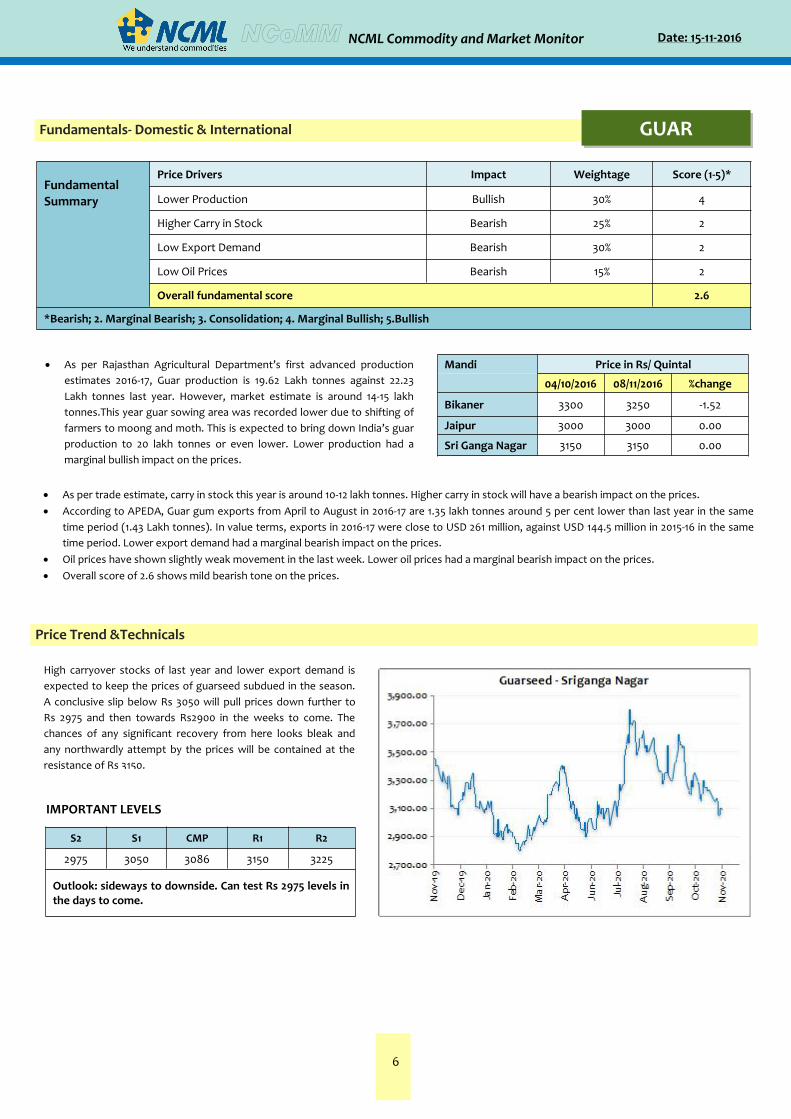

GUAR

High carryover stocks of last year and lower export demand isexpected to keep the prices of guarseed subdued in the seasonA conclusive slip below Rs 3050 will pull prices down further toRs 2975 and then towards Rs2900 in the weeks to come Thechances of any significant recovery from here looks bleak andany northwardly attempt by the prices will be contained at theresistance of Rs 3150

IMPORTANT LEVELS

S2 S1 CMP R1 R2

2975 3050 3086 3150 3225

Outlook sideways to downside Can test Rs 2975 levels inthe days to come

As per Rajasthan Agricultural Departmentrsquos first advanced productionestimates 2016-17 Guar production is 1962 Lakh tonnes against 2223Lakh tonnes last year However market estimate is around 14-15 lakhtonnesThis year guar sowing area was recorded lower due to shifting offarmers to moong and moth This is expected to bring down Indiarsquos guarproduction to 20 lakh tonnes or even lower Lower production had amarginal bullish impact on the prices

Mandi Price in Rs Quintal

04102016 08112016 change

Bikaner 3300 3250 -152

Jaipur 3000 3000 000

Sri Ganga Nagar 3150 3150 000

As per trade estimate carry in stock this year is around 10-12 lakh tonnes Higher carry in stock will have a bearish impact on the prices According to APEDA Guar gum exports from April to August in 2016-17 are 135 lakh tonnes around 5 per cent lower than last year in the same

time period (143 Lakh tonnes) In value terms exports in 2016-17 were close to USD 261 million against USD 1445 million in 2015-16 in the sametime period Lower export demand had a marginal bearish impact on the prices

Oil prices have shown slightly weak movement in the last week Lower oil prices had a marginal bearish impact on the prices Overall score of 26 shows mild bearish tone on the prices

FundamentalSummary

Price Drivers Impact Weightage Score (1-5)

Lower Production Bullish 30 4

Higher Carry in Stock Bearish 25 2

Low Export Demand Bearish 30 2

Low Oil Prices Bearish 15 2

Overall fundamental score 26

Bearish 2 Marginal Bearish 3 Consolidation 4 Marginal Bullish 5Bullish

Date 15-11-2016NCML Commodity and Market Monitor

7

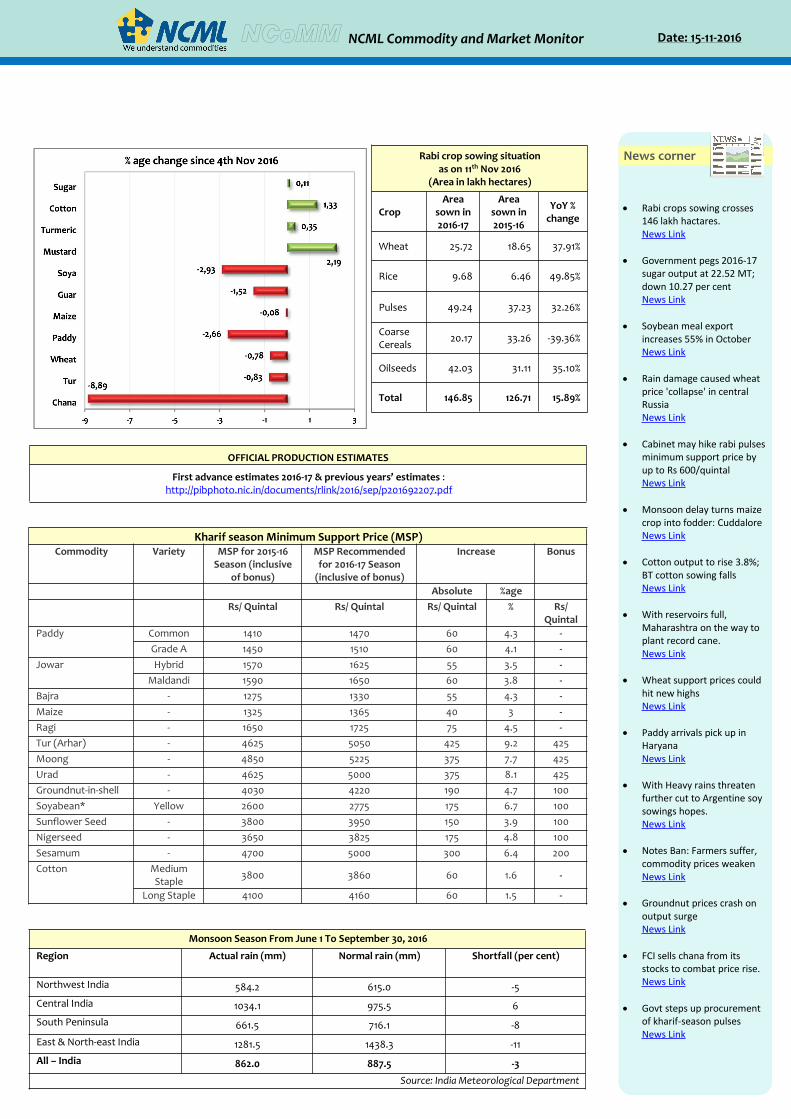

Rabi crop sowing situationas on 11th Nov 2016

(Area in lakh hectares)

CropArea

sown in2016-17

Areasown in2015-16

YoY change

Wheat 2572 1865 3791

Rice 968 646 4985

Pulses 4924 3723 3226

CoarseCereals 2017 3326 -3936

Oilseeds 4203 3111 3510

Total 14685 12671 1589

Kharif season Minimum Support Price (MSP)Commodity Variety MSP for 2015-16

Season (inclusiveof bonus)

MSP Recommendedfor 2016-17 Season(inclusive of bonus)

Increase Bonus

Absolute ageRs Quintal Rs Quintal Rs Quintal Rs

QuintalPaddy Common 1410 1470 60 43 -

Grade A 1450 1510 60 41 -Jowar Hybrid 1570 1625 55 35 -

Maldandi 1590 1650 60 38 -Bajra - 1275 1330 55 43 -Maize - 1325 1365 40 3 -Ragi - 1650 1725 75 45 -Tur (Arhar) - 4625 5050 425 92 425Moong - 4850 5225 375 77 425Urad - 4625 5000 375 81 425Groundnut-in-shell - 4030 4220 190 47 100Soyabean Yellow 2600 2775 175 67 100Sunflower Seed - 3800 3950 150 39 100Nigerseed - 3650 3825 175 48 100Sesamum - 4700 5000 300 64 200Cotton Medium

Staple 3800 3860 60 16 -

Long Staple 4100 4160 60 15 -

Monsoon Season From June 1 To September 30 2016

Region Actual rain (mm) Normal rain (mm) Shortfall (per cent)

Northwest India 5842 6150 -5Central India 10341 9755 6South Peninsula 6615 7161 -8

East amp North-east India 12815 14383 -11All ndash India 8620 8875 -3

Source India Meteorological Department

OFFICIAL PRODUCTION ESTIMATES

First advance estimates 2016-17 amp previous yearsrsquo estimates httppibphotonicindocumentsrlink2016sepp201692207pdf

Rabi crops sowing crosses146 lakh hactaresNews Link

Government pegs 2016-17sugar output at 2252 MTdown 1027 per centNews Link

Soybean meal exportincreases 55 in OctoberNews Link

Rain damage caused wheatprice collapse in centralRussiaNews Link

Cabinet may hike rabi pulsesminimum support price byup to Rs 600quintalNews Link

Monsoon delay turns maizecrop into fodder CuddaloreNews Link

Cotton output to rise 38BT cotton sowing fallsNews Link

With reservoirs fullMaharashtra on the way toplant record caneNews Link

Wheat support prices couldhit new highsNews Link

Paddy arrivals pick up inHaryanaNews Link

With Heavy rains threatenfurther cut to Argentine soysowings hopesNews Link

Notes Ban Farmers suffercommodity prices weakenNews Link

Groundnut prices crash onoutput surgeNews Link

FCI sells chana from itsstocks to combat price riseNews Link

Govt steps up procurementof kharif-season pulsesNews Link

News corner

Date 15-11-2016NCML Commodity and Market Monitor

8

Advisory TeamBasant Vaid Head TCIG basantvncmlcom

Sreedhar Nandam Vice President SCM sreedharnncmlcom

Research TeamSuresh Solanki Assistant Manager TCIG sureshsncmlcom

KamnaMalhotra Economist TCIG kamnamncmlcom

Akash Jaiswal Research Analyst TCIG akashjncmlcom

Ansh Aggarwal Senior Officer Trade Support anshancmlcom

For any research queries contact us at researchncmlcom

Disclaimer

This consultancy report has been prepared by National Collateral Management Services Limited (NCML) for the sole benefit of the addresseeNeither the report nor any part of the report shall be provided to third parties without the written consent of NCML Any third party inpossession of the report may not rely on its conclusions without the written consent of NCML NCML has exercised reasonable care and skill inpreparation of this consultancy report but has not independently verified information provided by others No other warranty express orimplied is made in relation to this report Therefore NCML assumes no liability for any loss resulting from errors omissions ormisrepresentations made by others Any recommendations opinions and findings stated in this report are based on circumstances and facts asthey existed at the time of preparation of this report Any change in circumstances and facts on which this report is based may adversely affectany recommendations opinions or findings contained in this report

copy National Collateral Management Services Limited (NCML) 2016

Date 15-11-2016NCML Commodity and Market Monitor

1

Fundamentals- Domestic amp International

Price Trend ampTechnicals

CHANA

Chana prices ate trading with a strong bearish undertone As therecent surge to the historical high levels have compelled farmersand stockist to offload causing sharp turnaroundAn expected rise in the Australian crop is also pressurizing Indianchana prices In the near term chana prices may slip towards thekey support area of Rs8800 and a crack of it will further pull itdown towards Rs8100 Immediate resistance is seen at Rs 10250

IMPORTANT LEVELS

S2 S1 CMP R1 R2

8100 8800 9500 10250 11000

Outlook Bearishness will prevail for the coming weeksand prices can moderate further towards 8800 mark

According to the local traders of Ganjbasoda region of Madhya PradeshChana sowing area in the region has slightly increased as compared tolast year The increase in area was limited as higher prices of Chana at thetime of sowing and favourable weather conditions made farmers toswitch to wheat Chana demand for sowing had a marginal bullish impacton the prices

To cool down prices and ensure the availability of chana the governmenthas decided to release it through NCDEX and Nafed

Mandi Price in Rs Quintal

04112016 08112016 change

Kota 11250 10250 -889

Jaipur 9200 9400 217

Lalitpur 90425 91475 116

According to the trade sources Australian Chana forward contract for OctoberNovember shipment is expected to reach Mumbai port after 15November and chana at vessel is rated at Rs 7900 per quintal as on 10th November 2016

Harvesting of chickpea in Australia is being affected by wet weather conditions and exporters may face problem in supplying chickpea inscheduled time November delivery may get delayed by 2 or 3 weeks which will have a marginal bullish impact on the prices

Lower chana stocks with traders and higher demand from millers due to festive and wedding season may have a mildly bullish impact on theprices

Australian Chana production forecast for 2016-17 is 1234 MMT against estimate of 1013 MMT last season However more than average rains andwater logging in major Chana producing region like Queensland may affect on the yield of the crop and support prices there

CACP has suggested the government to increase the MSP of Chana by up to Rs 475 per quintal The MSP of chana was fixed at Rs 3425 per quintalin 2015-16

Overall score of 26 shows a bearish undertone in the prices for the coming weeks

FundamentalSummary

Price Drivers Impact Weightage Score (1-5)

Cheaper forward quotes for Imported Chana Bearish 35 1

Demand for Seed ahead of sowings Bullish 10 4

Lower Stocks with traders Bullish 15 5

Late Shipment from Australia Bullish 15 4

Sale of Chana by NAFED Bearish 25 2

Overall fundamental score 260

1 Bearish 2 Marginal Bearish 3 Consolidation 4 Marginal Bullish 5Bullish

Date 15-11-2016NCML Commodity and Market Monitor

2

Fundamentals- Domestic amp International

Price Trend ampTechnicals

TUR

With series of fundamental factors pointing towards a strong bearishundertone in tur for the coming days the current weakness in pricesis expected to remain intact Rs 6120-Rs 6550 is the intermediateresistance zone and is unlikely to be breached anytime soonOn the downside recent low of Rs 5260 can expectedly be re-testedby the prices in the near term However MSP operations by thegovernment will provide floor to the prices and prevent anysignificant downside below key support band of Rs 5000- Rs 5250

IMPORTANT LEVELS

S2 S1 CMP R1 R2

5000 5260 5750 6070 6500

Outlook Can slip to enter the support band of 5260-5000 inthe near term

According to the trade source Burma Lemon Tur FAQ quality istrading at Rs 5700 per quintal at Mumbai port as on 10th NovemberLower import quotes and regular imports from Burma had a marginalbearish impact on the prices

According to the local trader of Gulbarga region crop condition inKarnataka is good and they are expecting higher yield this year ascompared to last year New crop is expected to arrive from last weekof November

Mandi Price in Rs Quintal

04112016 08112016 change

Akola 6050 6000 -083

Kanpur 6375 6375 000

Mumbai 57625 5750 -022

According to the local traders of Solapur region of Maharashtra new tur crop started arriving in the mandi in small quantity Moisture level is inthe range of 13-14 per cent and grain quality is good Traders are expecting 15-20 per cent higher yield this year as compared to last year Newcrop arrivals will have bearish impact on the prices

India Tur production estimate for 2016-17 is 429 MMT as against 246 MMT productions last year Higher production estimate will certainly havea bearish impact on the prices

Recently government has approved imports of 90 thousand tonnes of tur for buffer stock Overall score of 13 shows strong bearish tone on the prices

FundamentalSummary

Price Drivers Impact Weightage Score (1-5)

Low Import Quotes Bearish 20 2

Regular Imports Bearish 10 2

Domestic Arrivals Bearish 35 1

Expectation of higher production Bearish 35 1

Overall fundamental score 13

Bearish 2 Marginal Bearish 3 Consolidation 4 Marginal Bullish 5Bullish

Date 15-11-2016NCML Commodity and Market Monitor

3

Price Trend ampTechnicals

Recent sharp surge in prices are showing a sign of tiring up at thehigher levels Some profit booking is likely at these levelsaftersuch spike in prices Further pickup in Rabi sowing activitycan also weigh on the prices in the near term However lowerstocks with government can limit significant downsidePrices can initially correct towards the immediate support rangeof Rs 1940- Rs 1880 but are unlikely to breach that band in thenear term and turnaround can be witnessed in the prices fromthat range

IMPORTANT LEVELS

S2 S1 CMP R1 R2

1880 1940 2014 2030 2080

Output Initial declines expected towards Rs 1940 which canextend upto 1880 before turning around

Government wheat stocks plunged to 9-year-low to 2166 million tonnes (mt)as on October 1 close to the minimum buffer-cum-strategic reserve norm of2052 mt for this date The trade sources have pegged Indiarsquos production to aslow as 86 m mt as against the governmentrsquos estimate of 935 million MTLower production is reflected in FCI procuring less stock as compared to theprevious year (229 m mt vs 305 m mt)Lower stocks have had a strongbullish impact on the Indian wheat prices

The festive and wedding season demand of wheat by-products like sooji andmaida may have a mildly bullish impact on the prices

Mandi Price in Rs Quintal

04112016 08112016 change

Delhi 21448 2125 -092

Kota 1990 19858 -021

Indore 20305 20147 -078

Cheaper wheat imports in the wake of lowered import duty (the Centre had on 23rdSeptember 2016 reduced the import duty on wheat from 25per cent to 10 per cent) and sluggish international prices in the wake of abundant global supplies would have a mildly bearish impact on prices

As on 11th November 2016 wheat has been sown in 2572 lakh hectares 3791 per cent more than in the same period last year Sowing is expectedto gain more strength in the coming weeks further as late withdrawal of Monsoon has left good residual moisture in the soil and will encouragethe farmers to sow more Also as per trade sources the higher price of chana discouraged farmers from purchasing chana for sowing andfavoured wheat instead which further added to the increase in the wheat acreage

No export parity on the back of higher global production (forecasted at a record 743m tonnes up 1 per cent from last year) and lower Indianproduction has a mildly bearish impact

Overall fundamental score of 265 shows consolidation to mild bearishness in the in the near term The hike in wheat MSP is likely to be Rs 100 per quintal if the cabinet accepts the recommendations of the Commission for Agricultural Costs and

Prices

FundamentalSummary

Price Drivers Impact Weightage Score (1-5)

Lower stocks held with government Bullish 25 5

Seasonal demand for wheat products Bullish 10 4

Higher imports Bearish 30 1

Increase in area sown Bearish 20 2

No export parity Bearish 15 2

Overall fundamental score 265

1 Bearish 2 Marginal Bearish 3 Consolidation 4 Marginal Bullish 5Bullish

Fundamentals- Domestic amp International WHEAT

Date 15-11-2016NCML Commodity and Market Monitor

4

Fundamentals- Domestic amp International

Price Trend ampTechnicals

PADDY

Prices are expected to trade with sideways to mildly bearishundertone in the weeks ahead Recently made support of Rs 2050can be reclaimed on a decisive breach of the nearest support markof Rs 2250 Sustainable trading above Rs 2425 will push pricestowards Rs 2500 mark However the fundamentals are signallingtowards the bearishness to prevail rather than a upwardturnaround

IMPORTANT LEVELS

S2 S1 CMP R1 R2

2050 2250 2312 2425 2500

Outlook Crack of Rs 2250 will result in an escalation indeclining streak towards 2050

As on 9 November 2016 more than 5680 lakh tonnes of paddy hadarrived in the mandis of Haryana against 5105 lakh tonnes during thecorresponding period last year The government procurement agencieshave procured more than 5185 lakh tonnes of paddy and over 494 lakhtonnes has been procured by millers and dealers Paddy arrivals inother important states like Punjab and Bihar are also expected to behigh

Mandi Paddy 1121 Price in Rs Quintal

4112016 08112016 change

Hanumangarh 2350 22875 -266

Kaithal 2300 2300 000

Amritsar 2350 2300 -213

As on 1st October 2016 rice stocks with FCI are about 16 mt as against 105 mt buffer norm There are excess rice stocks against the buffer normwhich gives a bearish undertone to rice prices

Government target for paddy production for the year 2016-17 was set at 1085 million MT The kharif rice production according to the firstadvance estimates was 9388 million MT as against 9131 in the previous year This increased production strengthened the bearish undertone tothe rice prices

As on 11th November 2016 rice was sown in 968 lakh hectares 498 higher as compared to the same period previous year Higher area furthersets the stage for a good rabi harvest thereby keeping the price low

According to APEDA Indiarsquos Basmati rice exports in the period April-August 2016 were 1775 lakh MT as against 1678 lakh MT during the sameperiod last year The non-basmati rice exports for the April-August 2016 were 2966 lakh MT as against 2901 during the previous year A smallincrease in exports may have a mildly bullish effect but not cause significant impact on the ongoing bearish trend

Overall fundamental score of 185 indicates that the prices are bearish

FundamentalSummary

Price Drivers Impact Weightage Score (1-5)

High kharif arrivals Bearish 35 1

High buffer stock position Bearish 15 2

High kharif production estimate Bearish 20 2

Increase in rabi area sown Bearish 10 2

Steady export demand Bullish 20 4

Overall fundamental score 185

Bearish 2 Marginal Bearish 3 Consolidation 4 Marginal Bullish 5Bullish

Date 15-11-2016NCML Commodity and Market Monitor

5

Fundamentals- Domestic amp International

Price Trend ampTechnicals

MAIZE

Maize prices in Gulabbagh have entered into a strong consolidationphase which is likely to prevail for the coming weeks as well Priceswill continue to hover in the range of Rs 1520-1610 Close proximityto the upper band will attract sellerrsquos attention and buying interestwill be seen developing around the lower band of the range

IMPORTANT LEVELS

S2 S1 CMP R1 R2

1520 1540 1560 1605 1623

Outlook Sideways Will consolidate in the current priceband of Rs1520-1610

Although Maize harvest is continuing at a fast pace in Telangana Karnatakaand arrivals are somewhat good but the quality of the produce isinconsistent Inconsistent quality kept the prices in last days Farmers innon-irrigated areas had experienced dry patches during the monsoonseason which severely affected the grain setting as the temperatures werehigh Post that there have been damage to the crop due to excessive rainsand farmers have complained of severe losses in corn belts of Telanganaand Andhra Pradesh

Mandi Price in Rs Quintal

04112016 08112016 change

Gulabbagh 156025 1559 -008

Delhi 1515 1560 297

Nizamabad 14401 143125 -061

Persistent arrivals from growing regions may prevent the price from taking a strongly bullish tone According to the trade sources demand of maize from poultry and feed is good They are paying premium amount for quality crop Domestic

demand had a marginal bullish impact on the prices Export demand from Bangladesh and Nepal is higher Thailand is also favouring Indian exports to fulfil their immediate demand despite Indiarsquos

import imparity with other exporting countries Higher export demand has a mildly bullish impact on the prices According to the first advance estimates for 2016-17 by the government kharif maize production 2016-17 is estimated at 193 lakh MT as

compared to 153 lakh MT though the estimates may be revised downward due to reports of crop damage Overall fundamental score of 32 indicates that the prices are consolidated with slightly bullish tone

FundamentalSummary

Price Drivers Impact Weightage Score (1-5)

Higher kharif production amp arrivals Bearish 40 2

Inconsistent quality of produce Bullish 20 4

Higher Domestic Demand Bullish 25 4

Export Demand Bullish 15 4

Overall fundamental score 32

Bearish 2 Marginal Bearish 3 Consolidation 4 Marginal Bullish 5Bullish

Date 15-11-2016NCML Commodity and Market Monitor

6

Fundamentals- Domestic amp International

Price Trend ampTechnicals

GUAR

High carryover stocks of last year and lower export demand isexpected to keep the prices of guarseed subdued in the seasonA conclusive slip below Rs 3050 will pull prices down further toRs 2975 and then towards Rs2900 in the weeks to come Thechances of any significant recovery from here looks bleak andany northwardly attempt by the prices will be contained at theresistance of Rs 3150

IMPORTANT LEVELS

S2 S1 CMP R1 R2

2975 3050 3086 3150 3225

Outlook sideways to downside Can test Rs 2975 levels inthe days to come

As per Rajasthan Agricultural Departmentrsquos first advanced productionestimates 2016-17 Guar production is 1962 Lakh tonnes against 2223Lakh tonnes last year However market estimate is around 14-15 lakhtonnesThis year guar sowing area was recorded lower due to shifting offarmers to moong and moth This is expected to bring down Indiarsquos guarproduction to 20 lakh tonnes or even lower Lower production had amarginal bullish impact on the prices

Mandi Price in Rs Quintal

04102016 08112016 change

Bikaner 3300 3250 -152

Jaipur 3000 3000 000

Sri Ganga Nagar 3150 3150 000

As per trade estimate carry in stock this year is around 10-12 lakh tonnes Higher carry in stock will have a bearish impact on the prices According to APEDA Guar gum exports from April to August in 2016-17 are 135 lakh tonnes around 5 per cent lower than last year in the same

time period (143 Lakh tonnes) In value terms exports in 2016-17 were close to USD 261 million against USD 1445 million in 2015-16 in the sametime period Lower export demand had a marginal bearish impact on the prices

Oil prices have shown slightly weak movement in the last week Lower oil prices had a marginal bearish impact on the prices Overall score of 26 shows mild bearish tone on the prices

FundamentalSummary

Price Drivers Impact Weightage Score (1-5)

Lower Production Bullish 30 4

Higher Carry in Stock Bearish 25 2

Low Export Demand Bearish 30 2

Low Oil Prices Bearish 15 2

Overall fundamental score 26

Bearish 2 Marginal Bearish 3 Consolidation 4 Marginal Bullish 5Bullish

Date 15-11-2016NCML Commodity and Market Monitor

7

Rabi crop sowing situationas on 11th Nov 2016

(Area in lakh hectares)

CropArea

sown in2016-17

Areasown in2015-16

YoY change

Wheat 2572 1865 3791

Rice 968 646 4985

Pulses 4924 3723 3226

CoarseCereals 2017 3326 -3936

Oilseeds 4203 3111 3510

Total 14685 12671 1589

Kharif season Minimum Support Price (MSP)Commodity Variety MSP for 2015-16

Season (inclusiveof bonus)

MSP Recommendedfor 2016-17 Season(inclusive of bonus)

Increase Bonus

Absolute ageRs Quintal Rs Quintal Rs Quintal Rs

QuintalPaddy Common 1410 1470 60 43 -

Grade A 1450 1510 60 41 -Jowar Hybrid 1570 1625 55 35 -

Maldandi 1590 1650 60 38 -Bajra - 1275 1330 55 43 -Maize - 1325 1365 40 3 -Ragi - 1650 1725 75 45 -Tur (Arhar) - 4625 5050 425 92 425Moong - 4850 5225 375 77 425Urad - 4625 5000 375 81 425Groundnut-in-shell - 4030 4220 190 47 100Soyabean Yellow 2600 2775 175 67 100Sunflower Seed - 3800 3950 150 39 100Nigerseed - 3650 3825 175 48 100Sesamum - 4700 5000 300 64 200Cotton Medium

Staple 3800 3860 60 16 -

Long Staple 4100 4160 60 15 -

Monsoon Season From June 1 To September 30 2016

Region Actual rain (mm) Normal rain (mm) Shortfall (per cent)

Northwest India 5842 6150 -5Central India 10341 9755 6South Peninsula 6615 7161 -8

East amp North-east India 12815 14383 -11All ndash India 8620 8875 -3

Source India Meteorological Department

OFFICIAL PRODUCTION ESTIMATES

First advance estimates 2016-17 amp previous yearsrsquo estimates httppibphotonicindocumentsrlink2016sepp201692207pdf

Rabi crops sowing crosses146 lakh hactaresNews Link

Government pegs 2016-17sugar output at 2252 MTdown 1027 per centNews Link

Soybean meal exportincreases 55 in OctoberNews Link

Rain damage caused wheatprice collapse in centralRussiaNews Link

Cabinet may hike rabi pulsesminimum support price byup to Rs 600quintalNews Link

Monsoon delay turns maizecrop into fodder CuddaloreNews Link

Cotton output to rise 38BT cotton sowing fallsNews Link

With reservoirs fullMaharashtra on the way toplant record caneNews Link

Wheat support prices couldhit new highsNews Link

Paddy arrivals pick up inHaryanaNews Link

With Heavy rains threatenfurther cut to Argentine soysowings hopesNews Link

Notes Ban Farmers suffercommodity prices weakenNews Link

Groundnut prices crash onoutput surgeNews Link

FCI sells chana from itsstocks to combat price riseNews Link

Govt steps up procurementof kharif-season pulsesNews Link

News corner

Date 15-11-2016NCML Commodity and Market Monitor

8

Advisory TeamBasant Vaid Head TCIG basantvncmlcom

Sreedhar Nandam Vice President SCM sreedharnncmlcom

Research TeamSuresh Solanki Assistant Manager TCIG sureshsncmlcom

KamnaMalhotra Economist TCIG kamnamncmlcom

Akash Jaiswal Research Analyst TCIG akashjncmlcom

Ansh Aggarwal Senior Officer Trade Support anshancmlcom

For any research queries contact us at researchncmlcom

Disclaimer

This consultancy report has been prepared by National Collateral Management Services Limited (NCML) for the sole benefit of the addresseeNeither the report nor any part of the report shall be provided to third parties without the written consent of NCML Any third party inpossession of the report may not rely on its conclusions without the written consent of NCML NCML has exercised reasonable care and skill inpreparation of this consultancy report but has not independently verified information provided by others No other warranty express orimplied is made in relation to this report Therefore NCML assumes no liability for any loss resulting from errors omissions ormisrepresentations made by others Any recommendations opinions and findings stated in this report are based on circumstances and facts asthey existed at the time of preparation of this report Any change in circumstances and facts on which this report is based may adversely affectany recommendations opinions or findings contained in this report

copy National Collateral Management Services Limited (NCML) 2016

Date 15-11-2016NCML Commodity and Market Monitor

2

Fundamentals- Domestic amp International

Price Trend ampTechnicals

TUR

With series of fundamental factors pointing towards a strong bearishundertone in tur for the coming days the current weakness in pricesis expected to remain intact Rs 6120-Rs 6550 is the intermediateresistance zone and is unlikely to be breached anytime soonOn the downside recent low of Rs 5260 can expectedly be re-testedby the prices in the near term However MSP operations by thegovernment will provide floor to the prices and prevent anysignificant downside below key support band of Rs 5000- Rs 5250

IMPORTANT LEVELS

S2 S1 CMP R1 R2

5000 5260 5750 6070 6500

Outlook Can slip to enter the support band of 5260-5000 inthe near term

According to the trade source Burma Lemon Tur FAQ quality istrading at Rs 5700 per quintal at Mumbai port as on 10th NovemberLower import quotes and regular imports from Burma had a marginalbearish impact on the prices

According to the local trader of Gulbarga region crop condition inKarnataka is good and they are expecting higher yield this year ascompared to last year New crop is expected to arrive from last weekof November

Mandi Price in Rs Quintal

04112016 08112016 change

Akola 6050 6000 -083

Kanpur 6375 6375 000

Mumbai 57625 5750 -022

According to the local traders of Solapur region of Maharashtra new tur crop started arriving in the mandi in small quantity Moisture level is inthe range of 13-14 per cent and grain quality is good Traders are expecting 15-20 per cent higher yield this year as compared to last year Newcrop arrivals will have bearish impact on the prices

India Tur production estimate for 2016-17 is 429 MMT as against 246 MMT productions last year Higher production estimate will certainly havea bearish impact on the prices

Recently government has approved imports of 90 thousand tonnes of tur for buffer stock Overall score of 13 shows strong bearish tone on the prices

FundamentalSummary

Price Drivers Impact Weightage Score (1-5)

Low Import Quotes Bearish 20 2

Regular Imports Bearish 10 2

Domestic Arrivals Bearish 35 1

Expectation of higher production Bearish 35 1

Overall fundamental score 13

Bearish 2 Marginal Bearish 3 Consolidation 4 Marginal Bullish 5Bullish

Date 15-11-2016NCML Commodity and Market Monitor

3

Price Trend ampTechnicals

Recent sharp surge in prices are showing a sign of tiring up at thehigher levels Some profit booking is likely at these levelsaftersuch spike in prices Further pickup in Rabi sowing activitycan also weigh on the prices in the near term However lowerstocks with government can limit significant downsidePrices can initially correct towards the immediate support rangeof Rs 1940- Rs 1880 but are unlikely to breach that band in thenear term and turnaround can be witnessed in the prices fromthat range

IMPORTANT LEVELS

S2 S1 CMP R1 R2

1880 1940 2014 2030 2080

Output Initial declines expected towards Rs 1940 which canextend upto 1880 before turning around

Government wheat stocks plunged to 9-year-low to 2166 million tonnes (mt)as on October 1 close to the minimum buffer-cum-strategic reserve norm of2052 mt for this date The trade sources have pegged Indiarsquos production to aslow as 86 m mt as against the governmentrsquos estimate of 935 million MTLower production is reflected in FCI procuring less stock as compared to theprevious year (229 m mt vs 305 m mt)Lower stocks have had a strongbullish impact on the Indian wheat prices

The festive and wedding season demand of wheat by-products like sooji andmaida may have a mildly bullish impact on the prices

Mandi Price in Rs Quintal

04112016 08112016 change

Delhi 21448 2125 -092

Kota 1990 19858 -021

Indore 20305 20147 -078

Cheaper wheat imports in the wake of lowered import duty (the Centre had on 23rdSeptember 2016 reduced the import duty on wheat from 25per cent to 10 per cent) and sluggish international prices in the wake of abundant global supplies would have a mildly bearish impact on prices

As on 11th November 2016 wheat has been sown in 2572 lakh hectares 3791 per cent more than in the same period last year Sowing is expectedto gain more strength in the coming weeks further as late withdrawal of Monsoon has left good residual moisture in the soil and will encouragethe farmers to sow more Also as per trade sources the higher price of chana discouraged farmers from purchasing chana for sowing andfavoured wheat instead which further added to the increase in the wheat acreage

No export parity on the back of higher global production (forecasted at a record 743m tonnes up 1 per cent from last year) and lower Indianproduction has a mildly bearish impact

Overall fundamental score of 265 shows consolidation to mild bearishness in the in the near term The hike in wheat MSP is likely to be Rs 100 per quintal if the cabinet accepts the recommendations of the Commission for Agricultural Costs and

Prices

FundamentalSummary

Price Drivers Impact Weightage Score (1-5)

Lower stocks held with government Bullish 25 5

Seasonal demand for wheat products Bullish 10 4

Higher imports Bearish 30 1

Increase in area sown Bearish 20 2

No export parity Bearish 15 2

Overall fundamental score 265

1 Bearish 2 Marginal Bearish 3 Consolidation 4 Marginal Bullish 5Bullish

Fundamentals- Domestic amp International WHEAT

Date 15-11-2016NCML Commodity and Market Monitor

4

Fundamentals- Domestic amp International

Price Trend ampTechnicals

PADDY

Prices are expected to trade with sideways to mildly bearishundertone in the weeks ahead Recently made support of Rs 2050can be reclaimed on a decisive breach of the nearest support markof Rs 2250 Sustainable trading above Rs 2425 will push pricestowards Rs 2500 mark However the fundamentals are signallingtowards the bearishness to prevail rather than a upwardturnaround

IMPORTANT LEVELS

S2 S1 CMP R1 R2

2050 2250 2312 2425 2500

Outlook Crack of Rs 2250 will result in an escalation indeclining streak towards 2050

As on 9 November 2016 more than 5680 lakh tonnes of paddy hadarrived in the mandis of Haryana against 5105 lakh tonnes during thecorresponding period last year The government procurement agencieshave procured more than 5185 lakh tonnes of paddy and over 494 lakhtonnes has been procured by millers and dealers Paddy arrivals inother important states like Punjab and Bihar are also expected to behigh

Mandi Paddy 1121 Price in Rs Quintal

4112016 08112016 change

Hanumangarh 2350 22875 -266

Kaithal 2300 2300 000

Amritsar 2350 2300 -213

As on 1st October 2016 rice stocks with FCI are about 16 mt as against 105 mt buffer norm There are excess rice stocks against the buffer normwhich gives a bearish undertone to rice prices

Government target for paddy production for the year 2016-17 was set at 1085 million MT The kharif rice production according to the firstadvance estimates was 9388 million MT as against 9131 in the previous year This increased production strengthened the bearish undertone tothe rice prices

As on 11th November 2016 rice was sown in 968 lakh hectares 498 higher as compared to the same period previous year Higher area furthersets the stage for a good rabi harvest thereby keeping the price low

According to APEDA Indiarsquos Basmati rice exports in the period April-August 2016 were 1775 lakh MT as against 1678 lakh MT during the sameperiod last year The non-basmati rice exports for the April-August 2016 were 2966 lakh MT as against 2901 during the previous year A smallincrease in exports may have a mildly bullish effect but not cause significant impact on the ongoing bearish trend

Overall fundamental score of 185 indicates that the prices are bearish

FundamentalSummary

Price Drivers Impact Weightage Score (1-5)

High kharif arrivals Bearish 35 1

High buffer stock position Bearish 15 2

High kharif production estimate Bearish 20 2

Increase in rabi area sown Bearish 10 2

Steady export demand Bullish 20 4

Overall fundamental score 185

Bearish 2 Marginal Bearish 3 Consolidation 4 Marginal Bullish 5Bullish

Date 15-11-2016NCML Commodity and Market Monitor

5

Fundamentals- Domestic amp International

Price Trend ampTechnicals

MAIZE

Maize prices in Gulabbagh have entered into a strong consolidationphase which is likely to prevail for the coming weeks as well Priceswill continue to hover in the range of Rs 1520-1610 Close proximityto the upper band will attract sellerrsquos attention and buying interestwill be seen developing around the lower band of the range

IMPORTANT LEVELS

S2 S1 CMP R1 R2

1520 1540 1560 1605 1623

Outlook Sideways Will consolidate in the current priceband of Rs1520-1610

Although Maize harvest is continuing at a fast pace in Telangana Karnatakaand arrivals are somewhat good but the quality of the produce isinconsistent Inconsistent quality kept the prices in last days Farmers innon-irrigated areas had experienced dry patches during the monsoonseason which severely affected the grain setting as the temperatures werehigh Post that there have been damage to the crop due to excessive rainsand farmers have complained of severe losses in corn belts of Telanganaand Andhra Pradesh

Mandi Price in Rs Quintal

04112016 08112016 change

Gulabbagh 156025 1559 -008

Delhi 1515 1560 297

Nizamabad 14401 143125 -061

Persistent arrivals from growing regions may prevent the price from taking a strongly bullish tone According to the trade sources demand of maize from poultry and feed is good They are paying premium amount for quality crop Domestic

demand had a marginal bullish impact on the prices Export demand from Bangladesh and Nepal is higher Thailand is also favouring Indian exports to fulfil their immediate demand despite Indiarsquos

import imparity with other exporting countries Higher export demand has a mildly bullish impact on the prices According to the first advance estimates for 2016-17 by the government kharif maize production 2016-17 is estimated at 193 lakh MT as

compared to 153 lakh MT though the estimates may be revised downward due to reports of crop damage Overall fundamental score of 32 indicates that the prices are consolidated with slightly bullish tone

FundamentalSummary

Price Drivers Impact Weightage Score (1-5)

Higher kharif production amp arrivals Bearish 40 2

Inconsistent quality of produce Bullish 20 4

Higher Domestic Demand Bullish 25 4

Export Demand Bullish 15 4

Overall fundamental score 32

Bearish 2 Marginal Bearish 3 Consolidation 4 Marginal Bullish 5Bullish

Date 15-11-2016NCML Commodity and Market Monitor

6

Fundamentals- Domestic amp International

Price Trend ampTechnicals

GUAR

High carryover stocks of last year and lower export demand isexpected to keep the prices of guarseed subdued in the seasonA conclusive slip below Rs 3050 will pull prices down further toRs 2975 and then towards Rs2900 in the weeks to come Thechances of any significant recovery from here looks bleak andany northwardly attempt by the prices will be contained at theresistance of Rs 3150

IMPORTANT LEVELS

S2 S1 CMP R1 R2

2975 3050 3086 3150 3225

Outlook sideways to downside Can test Rs 2975 levels inthe days to come

As per Rajasthan Agricultural Departmentrsquos first advanced productionestimates 2016-17 Guar production is 1962 Lakh tonnes against 2223Lakh tonnes last year However market estimate is around 14-15 lakhtonnesThis year guar sowing area was recorded lower due to shifting offarmers to moong and moth This is expected to bring down Indiarsquos guarproduction to 20 lakh tonnes or even lower Lower production had amarginal bullish impact on the prices

Mandi Price in Rs Quintal

04102016 08112016 change

Bikaner 3300 3250 -152

Jaipur 3000 3000 000

Sri Ganga Nagar 3150 3150 000

As per trade estimate carry in stock this year is around 10-12 lakh tonnes Higher carry in stock will have a bearish impact on the prices According to APEDA Guar gum exports from April to August in 2016-17 are 135 lakh tonnes around 5 per cent lower than last year in the same

time period (143 Lakh tonnes) In value terms exports in 2016-17 were close to USD 261 million against USD 1445 million in 2015-16 in the sametime period Lower export demand had a marginal bearish impact on the prices

Oil prices have shown slightly weak movement in the last week Lower oil prices had a marginal bearish impact on the prices Overall score of 26 shows mild bearish tone on the prices

FundamentalSummary

Price Drivers Impact Weightage Score (1-5)

Lower Production Bullish 30 4

Higher Carry in Stock Bearish 25 2

Low Export Demand Bearish 30 2

Low Oil Prices Bearish 15 2

Overall fundamental score 26

Bearish 2 Marginal Bearish 3 Consolidation 4 Marginal Bullish 5Bullish

Date 15-11-2016NCML Commodity and Market Monitor

7

Rabi crop sowing situationas on 11th Nov 2016

(Area in lakh hectares)

CropArea

sown in2016-17

Areasown in2015-16

YoY change

Wheat 2572 1865 3791

Rice 968 646 4985

Pulses 4924 3723 3226

CoarseCereals 2017 3326 -3936

Oilseeds 4203 3111 3510

Total 14685 12671 1589

Kharif season Minimum Support Price (MSP)Commodity Variety MSP for 2015-16

Season (inclusiveof bonus)

MSP Recommendedfor 2016-17 Season(inclusive of bonus)

Increase Bonus

Absolute ageRs Quintal Rs Quintal Rs Quintal Rs

QuintalPaddy Common 1410 1470 60 43 -

Grade A 1450 1510 60 41 -Jowar Hybrid 1570 1625 55 35 -

Maldandi 1590 1650 60 38 -Bajra - 1275 1330 55 43 -Maize - 1325 1365 40 3 -Ragi - 1650 1725 75 45 -Tur (Arhar) - 4625 5050 425 92 425Moong - 4850 5225 375 77 425Urad - 4625 5000 375 81 425Groundnut-in-shell - 4030 4220 190 47 100Soyabean Yellow 2600 2775 175 67 100Sunflower Seed - 3800 3950 150 39 100Nigerseed - 3650 3825 175 48 100Sesamum - 4700 5000 300 64 200Cotton Medium

Staple 3800 3860 60 16 -

Long Staple 4100 4160 60 15 -

Monsoon Season From June 1 To September 30 2016

Region Actual rain (mm) Normal rain (mm) Shortfall (per cent)

Northwest India 5842 6150 -5Central India 10341 9755 6South Peninsula 6615 7161 -8

East amp North-east India 12815 14383 -11All ndash India 8620 8875 -3

Source India Meteorological Department

OFFICIAL PRODUCTION ESTIMATES

First advance estimates 2016-17 amp previous yearsrsquo estimates httppibphotonicindocumentsrlink2016sepp201692207pdf

Rabi crops sowing crosses146 lakh hactaresNews Link

Government pegs 2016-17sugar output at 2252 MTdown 1027 per centNews Link

Soybean meal exportincreases 55 in OctoberNews Link

Rain damage caused wheatprice collapse in centralRussiaNews Link

Cabinet may hike rabi pulsesminimum support price byup to Rs 600quintalNews Link

Monsoon delay turns maizecrop into fodder CuddaloreNews Link

Cotton output to rise 38BT cotton sowing fallsNews Link

With reservoirs fullMaharashtra on the way toplant record caneNews Link

Wheat support prices couldhit new highsNews Link

Paddy arrivals pick up inHaryanaNews Link

With Heavy rains threatenfurther cut to Argentine soysowings hopesNews Link

Notes Ban Farmers suffercommodity prices weakenNews Link

Groundnut prices crash onoutput surgeNews Link

FCI sells chana from itsstocks to combat price riseNews Link

Govt steps up procurementof kharif-season pulsesNews Link

News corner

Date 15-11-2016NCML Commodity and Market Monitor

8

Advisory TeamBasant Vaid Head TCIG basantvncmlcom

Sreedhar Nandam Vice President SCM sreedharnncmlcom

Research TeamSuresh Solanki Assistant Manager TCIG sureshsncmlcom

KamnaMalhotra Economist TCIG kamnamncmlcom

Akash Jaiswal Research Analyst TCIG akashjncmlcom

Ansh Aggarwal Senior Officer Trade Support anshancmlcom

For any research queries contact us at researchncmlcom

Disclaimer

This consultancy report has been prepared by National Collateral Management Services Limited (NCML) for the sole benefit of the addresseeNeither the report nor any part of the report shall be provided to third parties without the written consent of NCML Any third party inpossession of the report may not rely on its conclusions without the written consent of NCML NCML has exercised reasonable care and skill inpreparation of this consultancy report but has not independently verified information provided by others No other warranty express orimplied is made in relation to this report Therefore NCML assumes no liability for any loss resulting from errors omissions ormisrepresentations made by others Any recommendations opinions and findings stated in this report are based on circumstances and facts asthey existed at the time of preparation of this report Any change in circumstances and facts on which this report is based may adversely affectany recommendations opinions or findings contained in this report

copy National Collateral Management Services Limited (NCML) 2016

Date 15-11-2016NCML Commodity and Market Monitor

3

Price Trend ampTechnicals

Recent sharp surge in prices are showing a sign of tiring up at thehigher levels Some profit booking is likely at these levelsaftersuch spike in prices Further pickup in Rabi sowing activitycan also weigh on the prices in the near term However lowerstocks with government can limit significant downsidePrices can initially correct towards the immediate support rangeof Rs 1940- Rs 1880 but are unlikely to breach that band in thenear term and turnaround can be witnessed in the prices fromthat range

IMPORTANT LEVELS

S2 S1 CMP R1 R2

1880 1940 2014 2030 2080

Output Initial declines expected towards Rs 1940 which canextend upto 1880 before turning around

Government wheat stocks plunged to 9-year-low to 2166 million tonnes (mt)as on October 1 close to the minimum buffer-cum-strategic reserve norm of2052 mt for this date The trade sources have pegged Indiarsquos production to aslow as 86 m mt as against the governmentrsquos estimate of 935 million MTLower production is reflected in FCI procuring less stock as compared to theprevious year (229 m mt vs 305 m mt)Lower stocks have had a strongbullish impact on the Indian wheat prices

The festive and wedding season demand of wheat by-products like sooji andmaida may have a mildly bullish impact on the prices

Mandi Price in Rs Quintal

04112016 08112016 change

Delhi 21448 2125 -092

Kota 1990 19858 -021

Indore 20305 20147 -078

Cheaper wheat imports in the wake of lowered import duty (the Centre had on 23rdSeptember 2016 reduced the import duty on wheat from 25per cent to 10 per cent) and sluggish international prices in the wake of abundant global supplies would have a mildly bearish impact on prices

As on 11th November 2016 wheat has been sown in 2572 lakh hectares 3791 per cent more than in the same period last year Sowing is expectedto gain more strength in the coming weeks further as late withdrawal of Monsoon has left good residual moisture in the soil and will encouragethe farmers to sow more Also as per trade sources the higher price of chana discouraged farmers from purchasing chana for sowing andfavoured wheat instead which further added to the increase in the wheat acreage

No export parity on the back of higher global production (forecasted at a record 743m tonnes up 1 per cent from last year) and lower Indianproduction has a mildly bearish impact

Overall fundamental score of 265 shows consolidation to mild bearishness in the in the near term The hike in wheat MSP is likely to be Rs 100 per quintal if the cabinet accepts the recommendations of the Commission for Agricultural Costs and

Prices

FundamentalSummary

Price Drivers Impact Weightage Score (1-5)

Lower stocks held with government Bullish 25 5

Seasonal demand for wheat products Bullish 10 4

Higher imports Bearish 30 1

Increase in area sown Bearish 20 2

No export parity Bearish 15 2

Overall fundamental score 265

1 Bearish 2 Marginal Bearish 3 Consolidation 4 Marginal Bullish 5Bullish

Fundamentals- Domestic amp International WHEAT

Date 15-11-2016NCML Commodity and Market Monitor

4

Fundamentals- Domestic amp International

Price Trend ampTechnicals

PADDY

Prices are expected to trade with sideways to mildly bearishundertone in the weeks ahead Recently made support of Rs 2050can be reclaimed on a decisive breach of the nearest support markof Rs 2250 Sustainable trading above Rs 2425 will push pricestowards Rs 2500 mark However the fundamentals are signallingtowards the bearishness to prevail rather than a upwardturnaround

IMPORTANT LEVELS

S2 S1 CMP R1 R2

2050 2250 2312 2425 2500

Outlook Crack of Rs 2250 will result in an escalation indeclining streak towards 2050

As on 9 November 2016 more than 5680 lakh tonnes of paddy hadarrived in the mandis of Haryana against 5105 lakh tonnes during thecorresponding period last year The government procurement agencieshave procured more than 5185 lakh tonnes of paddy and over 494 lakhtonnes has been procured by millers and dealers Paddy arrivals inother important states like Punjab and Bihar are also expected to behigh

Mandi Paddy 1121 Price in Rs Quintal

4112016 08112016 change

Hanumangarh 2350 22875 -266

Kaithal 2300 2300 000

Amritsar 2350 2300 -213

As on 1st October 2016 rice stocks with FCI are about 16 mt as against 105 mt buffer norm There are excess rice stocks against the buffer normwhich gives a bearish undertone to rice prices

Government target for paddy production for the year 2016-17 was set at 1085 million MT The kharif rice production according to the firstadvance estimates was 9388 million MT as against 9131 in the previous year This increased production strengthened the bearish undertone tothe rice prices

As on 11th November 2016 rice was sown in 968 lakh hectares 498 higher as compared to the same period previous year Higher area furthersets the stage for a good rabi harvest thereby keeping the price low

According to APEDA Indiarsquos Basmati rice exports in the period April-August 2016 were 1775 lakh MT as against 1678 lakh MT during the sameperiod last year The non-basmati rice exports for the April-August 2016 were 2966 lakh MT as against 2901 during the previous year A smallincrease in exports may have a mildly bullish effect but not cause significant impact on the ongoing bearish trend

Overall fundamental score of 185 indicates that the prices are bearish

FundamentalSummary

Price Drivers Impact Weightage Score (1-5)

High kharif arrivals Bearish 35 1

High buffer stock position Bearish 15 2

High kharif production estimate Bearish 20 2

Increase in rabi area sown Bearish 10 2

Steady export demand Bullish 20 4

Overall fundamental score 185

Bearish 2 Marginal Bearish 3 Consolidation 4 Marginal Bullish 5Bullish

Date 15-11-2016NCML Commodity and Market Monitor

5

Fundamentals- Domestic amp International

Price Trend ampTechnicals

MAIZE

Maize prices in Gulabbagh have entered into a strong consolidationphase which is likely to prevail for the coming weeks as well Priceswill continue to hover in the range of Rs 1520-1610 Close proximityto the upper band will attract sellerrsquos attention and buying interestwill be seen developing around the lower band of the range

IMPORTANT LEVELS

S2 S1 CMP R1 R2

1520 1540 1560 1605 1623

Outlook Sideways Will consolidate in the current priceband of Rs1520-1610

Although Maize harvest is continuing at a fast pace in Telangana Karnatakaand arrivals are somewhat good but the quality of the produce isinconsistent Inconsistent quality kept the prices in last days Farmers innon-irrigated areas had experienced dry patches during the monsoonseason which severely affected the grain setting as the temperatures werehigh Post that there have been damage to the crop due to excessive rainsand farmers have complained of severe losses in corn belts of Telanganaand Andhra Pradesh

Mandi Price in Rs Quintal

04112016 08112016 change

Gulabbagh 156025 1559 -008

Delhi 1515 1560 297

Nizamabad 14401 143125 -061

Persistent arrivals from growing regions may prevent the price from taking a strongly bullish tone According to the trade sources demand of maize from poultry and feed is good They are paying premium amount for quality crop Domestic

demand had a marginal bullish impact on the prices Export demand from Bangladesh and Nepal is higher Thailand is also favouring Indian exports to fulfil their immediate demand despite Indiarsquos

import imparity with other exporting countries Higher export demand has a mildly bullish impact on the prices According to the first advance estimates for 2016-17 by the government kharif maize production 2016-17 is estimated at 193 lakh MT as

compared to 153 lakh MT though the estimates may be revised downward due to reports of crop damage Overall fundamental score of 32 indicates that the prices are consolidated with slightly bullish tone

FundamentalSummary

Price Drivers Impact Weightage Score (1-5)

Higher kharif production amp arrivals Bearish 40 2

Inconsistent quality of produce Bullish 20 4

Higher Domestic Demand Bullish 25 4

Export Demand Bullish 15 4

Overall fundamental score 32

Bearish 2 Marginal Bearish 3 Consolidation 4 Marginal Bullish 5Bullish

Date 15-11-2016NCML Commodity and Market Monitor

6

Fundamentals- Domestic amp International

Price Trend ampTechnicals

GUAR

High carryover stocks of last year and lower export demand isexpected to keep the prices of guarseed subdued in the seasonA conclusive slip below Rs 3050 will pull prices down further toRs 2975 and then towards Rs2900 in the weeks to come Thechances of any significant recovery from here looks bleak andany northwardly attempt by the prices will be contained at theresistance of Rs 3150

IMPORTANT LEVELS

S2 S1 CMP R1 R2

2975 3050 3086 3150 3225

Outlook sideways to downside Can test Rs 2975 levels inthe days to come

As per Rajasthan Agricultural Departmentrsquos first advanced productionestimates 2016-17 Guar production is 1962 Lakh tonnes against 2223Lakh tonnes last year However market estimate is around 14-15 lakhtonnesThis year guar sowing area was recorded lower due to shifting offarmers to moong and moth This is expected to bring down Indiarsquos guarproduction to 20 lakh tonnes or even lower Lower production had amarginal bullish impact on the prices

Mandi Price in Rs Quintal

04102016 08112016 change

Bikaner 3300 3250 -152

Jaipur 3000 3000 000

Sri Ganga Nagar 3150 3150 000

As per trade estimate carry in stock this year is around 10-12 lakh tonnes Higher carry in stock will have a bearish impact on the prices According to APEDA Guar gum exports from April to August in 2016-17 are 135 lakh tonnes around 5 per cent lower than last year in the same

time period (143 Lakh tonnes) In value terms exports in 2016-17 were close to USD 261 million against USD 1445 million in 2015-16 in the sametime period Lower export demand had a marginal bearish impact on the prices

Oil prices have shown slightly weak movement in the last week Lower oil prices had a marginal bearish impact on the prices Overall score of 26 shows mild bearish tone on the prices

FundamentalSummary

Price Drivers Impact Weightage Score (1-5)

Lower Production Bullish 30 4

Higher Carry in Stock Bearish 25 2

Low Export Demand Bearish 30 2

Low Oil Prices Bearish 15 2

Overall fundamental score 26

Bearish 2 Marginal Bearish 3 Consolidation 4 Marginal Bullish 5Bullish

Date 15-11-2016NCML Commodity and Market Monitor

7

Rabi crop sowing situationas on 11th Nov 2016

(Area in lakh hectares)

CropArea

sown in2016-17

Areasown in2015-16

YoY change

Wheat 2572 1865 3791

Rice 968 646 4985

Pulses 4924 3723 3226

CoarseCereals 2017 3326 -3936

Oilseeds 4203 3111 3510

Total 14685 12671 1589

Kharif season Minimum Support Price (MSP)Commodity Variety MSP for 2015-16

Season (inclusiveof bonus)

MSP Recommendedfor 2016-17 Season(inclusive of bonus)

Increase Bonus

Absolute ageRs Quintal Rs Quintal Rs Quintal Rs

QuintalPaddy Common 1410 1470 60 43 -

Grade A 1450 1510 60 41 -Jowar Hybrid 1570 1625 55 35 -

Maldandi 1590 1650 60 38 -Bajra - 1275 1330 55 43 -Maize - 1325 1365 40 3 -Ragi - 1650 1725 75 45 -Tur (Arhar) - 4625 5050 425 92 425Moong - 4850 5225 375 77 425Urad - 4625 5000 375 81 425Groundnut-in-shell - 4030 4220 190 47 100Soyabean Yellow 2600 2775 175 67 100Sunflower Seed - 3800 3950 150 39 100Nigerseed - 3650 3825 175 48 100Sesamum - 4700 5000 300 64 200Cotton Medium

Staple 3800 3860 60 16 -

Long Staple 4100 4160 60 15 -

Monsoon Season From June 1 To September 30 2016

Region Actual rain (mm) Normal rain (mm) Shortfall (per cent)

Northwest India 5842 6150 -5Central India 10341 9755 6South Peninsula 6615 7161 -8

East amp North-east India 12815 14383 -11All ndash India 8620 8875 -3

Source India Meteorological Department

OFFICIAL PRODUCTION ESTIMATES

First advance estimates 2016-17 amp previous yearsrsquo estimates httppibphotonicindocumentsrlink2016sepp201692207pdf

Rabi crops sowing crosses146 lakh hactaresNews Link

Government pegs 2016-17sugar output at 2252 MTdown 1027 per centNews Link

Soybean meal exportincreases 55 in OctoberNews Link

Rain damage caused wheatprice collapse in centralRussiaNews Link

Cabinet may hike rabi pulsesminimum support price byup to Rs 600quintalNews Link

Monsoon delay turns maizecrop into fodder CuddaloreNews Link

Cotton output to rise 38BT cotton sowing fallsNews Link

With reservoirs fullMaharashtra on the way toplant record caneNews Link

Wheat support prices couldhit new highsNews Link

Paddy arrivals pick up inHaryanaNews Link

With Heavy rains threatenfurther cut to Argentine soysowings hopesNews Link

Notes Ban Farmers suffercommodity prices weakenNews Link

Groundnut prices crash onoutput surgeNews Link

FCI sells chana from itsstocks to combat price riseNews Link

Govt steps up procurementof kharif-season pulsesNews Link

News corner

Date 15-11-2016NCML Commodity and Market Monitor

8

Advisory TeamBasant Vaid Head TCIG basantvncmlcom

Sreedhar Nandam Vice President SCM sreedharnncmlcom

Research TeamSuresh Solanki Assistant Manager TCIG sureshsncmlcom

KamnaMalhotra Economist TCIG kamnamncmlcom

Akash Jaiswal Research Analyst TCIG akashjncmlcom

Ansh Aggarwal Senior Officer Trade Support anshancmlcom

For any research queries contact us at researchncmlcom

Disclaimer

This consultancy report has been prepared by National Collateral Management Services Limited (NCML) for the sole benefit of the addresseeNeither the report nor any part of the report shall be provided to third parties without the written consent of NCML Any third party inpossession of the report may not rely on its conclusions without the written consent of NCML NCML has exercised reasonable care and skill inpreparation of this consultancy report but has not independently verified information provided by others No other warranty express orimplied is made in relation to this report Therefore NCML assumes no liability for any loss resulting from errors omissions ormisrepresentations made by others Any recommendations opinions and findings stated in this report are based on circumstances and facts asthey existed at the time of preparation of this report Any change in circumstances and facts on which this report is based may adversely affectany recommendations opinions or findings contained in this report

copy National Collateral Management Services Limited (NCML) 2016

Date 15-11-2016NCML Commodity and Market Monitor

4

Fundamentals- Domestic amp International

Price Trend ampTechnicals

PADDY

Prices are expected to trade with sideways to mildly bearishundertone in the weeks ahead Recently made support of Rs 2050can be reclaimed on a decisive breach of the nearest support markof Rs 2250 Sustainable trading above Rs 2425 will push pricestowards Rs 2500 mark However the fundamentals are signallingtowards the bearishness to prevail rather than a upwardturnaround

IMPORTANT LEVELS

S2 S1 CMP R1 R2

2050 2250 2312 2425 2500

Outlook Crack of Rs 2250 will result in an escalation indeclining streak towards 2050

As on 9 November 2016 more than 5680 lakh tonnes of paddy hadarrived in the mandis of Haryana against 5105 lakh tonnes during thecorresponding period last year The government procurement agencieshave procured more than 5185 lakh tonnes of paddy and over 494 lakhtonnes has been procured by millers and dealers Paddy arrivals inother important states like Punjab and Bihar are also expected to behigh

Mandi Paddy 1121 Price in Rs Quintal

4112016 08112016 change

Hanumangarh 2350 22875 -266

Kaithal 2300 2300 000

Amritsar 2350 2300 -213

As on 1st October 2016 rice stocks with FCI are about 16 mt as against 105 mt buffer norm There are excess rice stocks against the buffer normwhich gives a bearish undertone to rice prices

Government target for paddy production for the year 2016-17 was set at 1085 million MT The kharif rice production according to the firstadvance estimates was 9388 million MT as against 9131 in the previous year This increased production strengthened the bearish undertone tothe rice prices

As on 11th November 2016 rice was sown in 968 lakh hectares 498 higher as compared to the same period previous year Higher area furthersets the stage for a good rabi harvest thereby keeping the price low

According to APEDA Indiarsquos Basmati rice exports in the period April-August 2016 were 1775 lakh MT as against 1678 lakh MT during the sameperiod last year The non-basmati rice exports for the April-August 2016 were 2966 lakh MT as against 2901 during the previous year A smallincrease in exports may have a mildly bullish effect but not cause significant impact on the ongoing bearish trend

Overall fundamental score of 185 indicates that the prices are bearish

FundamentalSummary

Price Drivers Impact Weightage Score (1-5)

High kharif arrivals Bearish 35 1

High buffer stock position Bearish 15 2

High kharif production estimate Bearish 20 2

Increase in rabi area sown Bearish 10 2

Steady export demand Bullish 20 4

Overall fundamental score 185

Bearish 2 Marginal Bearish 3 Consolidation 4 Marginal Bullish 5Bullish

Date 15-11-2016NCML Commodity and Market Monitor

5

Fundamentals- Domestic amp International

Price Trend ampTechnicals

MAIZE

Maize prices in Gulabbagh have entered into a strong consolidationphase which is likely to prevail for the coming weeks as well Priceswill continue to hover in the range of Rs 1520-1610 Close proximityto the upper band will attract sellerrsquos attention and buying interestwill be seen developing around the lower band of the range

IMPORTANT LEVELS

S2 S1 CMP R1 R2

1520 1540 1560 1605 1623

Outlook Sideways Will consolidate in the current priceband of Rs1520-1610

Although Maize harvest is continuing at a fast pace in Telangana Karnatakaand arrivals are somewhat good but the quality of the produce isinconsistent Inconsistent quality kept the prices in last days Farmers innon-irrigated areas had experienced dry patches during the monsoonseason which severely affected the grain setting as the temperatures werehigh Post that there have been damage to the crop due to excessive rainsand farmers have complained of severe losses in corn belts of Telanganaand Andhra Pradesh

Mandi Price in Rs Quintal

04112016 08112016 change

Gulabbagh 156025 1559 -008

Delhi 1515 1560 297

Nizamabad 14401 143125 -061

Persistent arrivals from growing regions may prevent the price from taking a strongly bullish tone According to the trade sources demand of maize from poultry and feed is good They are paying premium amount for quality crop Domestic

demand had a marginal bullish impact on the prices Export demand from Bangladesh and Nepal is higher Thailand is also favouring Indian exports to fulfil their immediate demand despite Indiarsquos

import imparity with other exporting countries Higher export demand has a mildly bullish impact on the prices According to the first advance estimates for 2016-17 by the government kharif maize production 2016-17 is estimated at 193 lakh MT as

compared to 153 lakh MT though the estimates may be revised downward due to reports of crop damage Overall fundamental score of 32 indicates that the prices are consolidated with slightly bullish tone

FundamentalSummary

Price Drivers Impact Weightage Score (1-5)

Higher kharif production amp arrivals Bearish 40 2

Inconsistent quality of produce Bullish 20 4

Higher Domestic Demand Bullish 25 4

Export Demand Bullish 15 4

Overall fundamental score 32