Embed Size (px)

Citation preview

National Broadband Network (NBN) – Middle East

Table of Contents

1 Overview ...............................................................................1

2 NBN Initiative ......................................................................... 2

3 NBN Investment Models ......................................................... 3

4 NBN Operational Models ........................................................ 4

5 NBN Trends: Policies & Framework in the Middle East ...... ....... 5

6 Deployment Considerations for NBN .......................................7

7 Middle East NBN Challenges and Obstacles ............................8

8 Vision and Goal of NBN in Middle East ..................................10

9 Scope for Middle East NBN Deployment ................................11

10 Recommendations .................................. ........................... 12

11 Conclusion ........................................................................ 13

1

1 Overview

The greatest infrastructure and architectural challenge of the 21st century is

broadband. It can stimulate economic growth, job creation and improve the

standard of living. It can change the way we deliver our health and education

services, the way we educate our children along with ensuring public safety,

and help fulfill government functions whilst shrinking the digital divide.

The countries of the Middle East have shown great enthusiasm for investing

and innovating within the broadband ecosystem over the past several years,

although 60% of the population still cannot access broadband at home.

We are currently behind more advanced markets—Japan, Korea, Australia,

and Singapore being a few—in the adoption of broadband technology.

The nomenclature for National Broadband Networks (NBNs) actually began

in Australia, where there is a national wholesale-only, open-access data

network under development whereby one gigabit per second connections

are sold to retail service providers (RSP). These RSPs then sell Internet access

and other services to consumers, adding their own unique flavor to the

network functionalities & services to offer tailored products required by their

customers.

"In the 21st century, affordable broadband access

to the Internet is becoming as vital to social and

economic development as networks like transport,

water and power"

—Dr Hamadoun Touré, ITU Secretary-General

2

2 NBN Initiative

To ensure every citizen has access to broadband applications and contents,

countries are developing National Broadband Network plans which include

a detailed strategy to create value for consumers and business customers

in conjunction with broadband-capable devices that can deliver attractive

services at affordable costs. Such plans within the broadband ecosystem can

ensure that networks, devices, services, applications and content are being

used in the most effective and healthy way possible.

Governments and public entities (e.g. National Regulatory Authorities) can

influence the broadband ecosystem in five important ways:

Making laws, policies and standards to ensure fair competition at 1.

different layers of the network, provide control of national assets, and

maximize resources to create affordability of advanced services.

Encourage service providers to support the deployment of broadband 2.

and voice in high-cost areas whilst ensuring that even low-income

citizens can afford broadband—in turn supporting efforts to boost

adoption and utilization.

Accelerate reforms and incentives that can maximize the benefits 3.

of broadband in sectors where the government extends significant

influence, such as public education, healthcare and other public

operations.

While assuring that there are cost-effective investments made in 4.

broadband technology, this should be coupled with a focus on integrity,

reliability, resilience of telecommunication infrastructure so that

networks can be depended upon in times of disaster and emergency.

Encourage innovation in the development of new applications while 5.

ensuring that they can be universally offered to all consumers and

businesses.

3

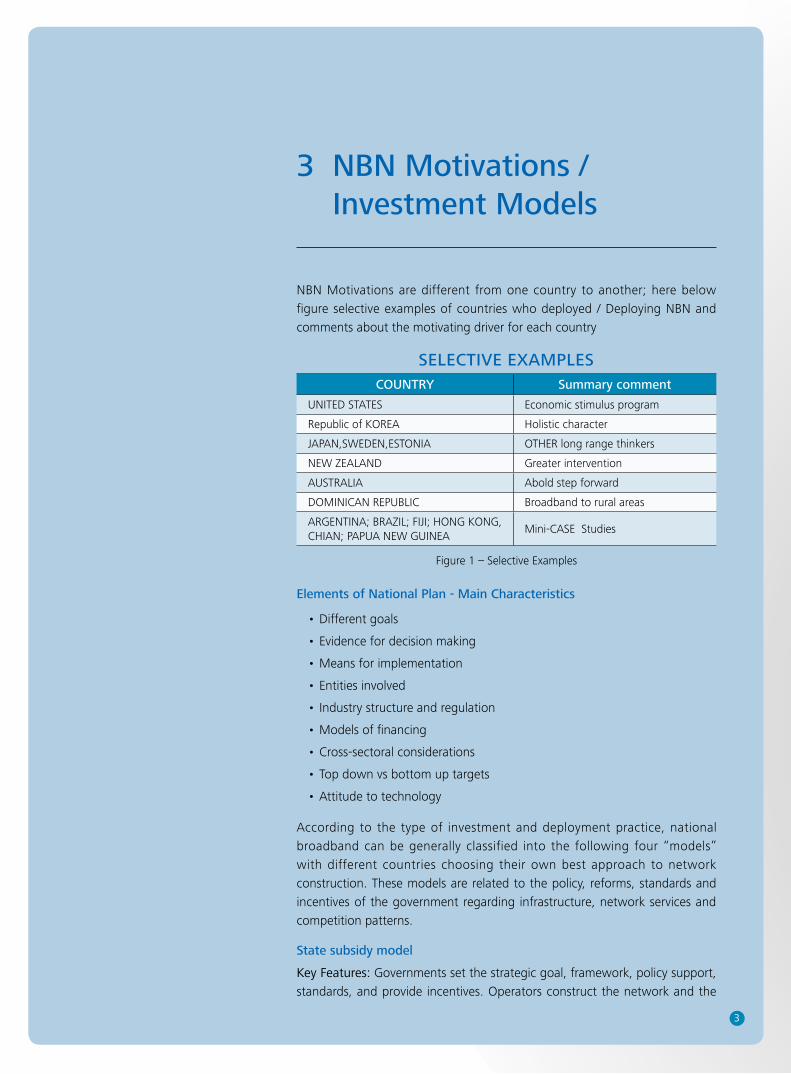

3 NBN Motivations / Investment Models

NBN Motivations are different from one country to another; here below

figure selective examples of countries who deployed / Deploying NBN and

comments about the motivating driver for each country

Elements of National Plan - Main Characteristics

Different goals •

Evidence for decision making •

Means for implementation •

Entities involved•

Industry structure and regulation•

Models of financing •

Cross-sectoral considerations•

Top down vs bottom up targets •

Attitude to technology •

According to the type of investment and deployment practice, national

broadband can be generally classified into the following four “models”

with different countries choosing their own best approach to network

construction. These models are related to the policy, reforms, standards and

incentives of the government regarding infrastructure, network services and

competition patterns.

State subsidy model

Key Features: Governments set the strategic goal, framework, policy support,

standards, and provide incentives. Operators construct the network and the

Figure 1 – Selective Examples

COUNTRY Summary comment

UNITED STATES Economic stimulus program

Republic of KOREA Holistic character

JAPAN,SWEDEN,ESTONIA OTHER long range thinkers

NEW ZEALAND Greater intervention

AUSTRALIA Abold step forward

DOMINICAN REPUBLIC Broadband to rural areas

ARGENTINA; BRAZIL; FIJI; HONG KONG, CHIAN; PAPUA NEW GUINEA

Mini-CASE Studies

SELECTIVE EXAMPLES

4

network assets are attributable to operators. This can be seen in cases such as

the Malaysia HSBB project and UK BT NGA project.

State major owner model

Key Features: Governments set the strategic goal, framework, policy, and set

up special NBN companies which are responsible for the National Broadband

Network construction and operation. NBN companies do not support retail

business for the end-user, and only provide wholesale services for RSP (Layer 3).

A typical case of this would be Australia's NBN project.

Third-party construction model

Key Features: Governments set the strategic goal, framework, provide

financial support, and select the third-party companies differed from current

network operations to construct the NBN by way of tender. Governments

provide some financial support. The typical case is the Singapore model,

where the Singapore government chose two companies to construct Layer

1 (passive part) and Layer 2 (active part) of the network separately, with

operators as the RSP (Layer 3) to provide user-oriented retail business.

Federal construction model

Key Features: Governments set the strategic goal, framework and vision. The

existing operators will construct NBN and provide end-to-end broadband

services independently. Individual companies are responsible for their CAPEX

and OPEX from Layer 1 to Layer 3.

4 NBN Operational Models

Any telecommunications network can be divided into three layers. The first

layer is the infrastructure layer and here we refer to it as Passive Layer. The

second layer is the communication layer which we refer to as the Active

Layer, and the third layer is the Service Layer.

In a NBN environment, the infrastructure layer is the most costly layer and

normally is built with government investment through a Public Private

Partnership (PPP). The communications layer is normally handed to the

licensed service providers or by setting up a new entity to operate this layer.

For the final service layer, any licensed service provider can have equal access

to the network and provide its services.

In some parts of the world there are Retail Service Providers (RSPs), but in the

Middle East region there are no RSPs licensed to date for fixed networks. They

are therefore not covered in this white paper.

5

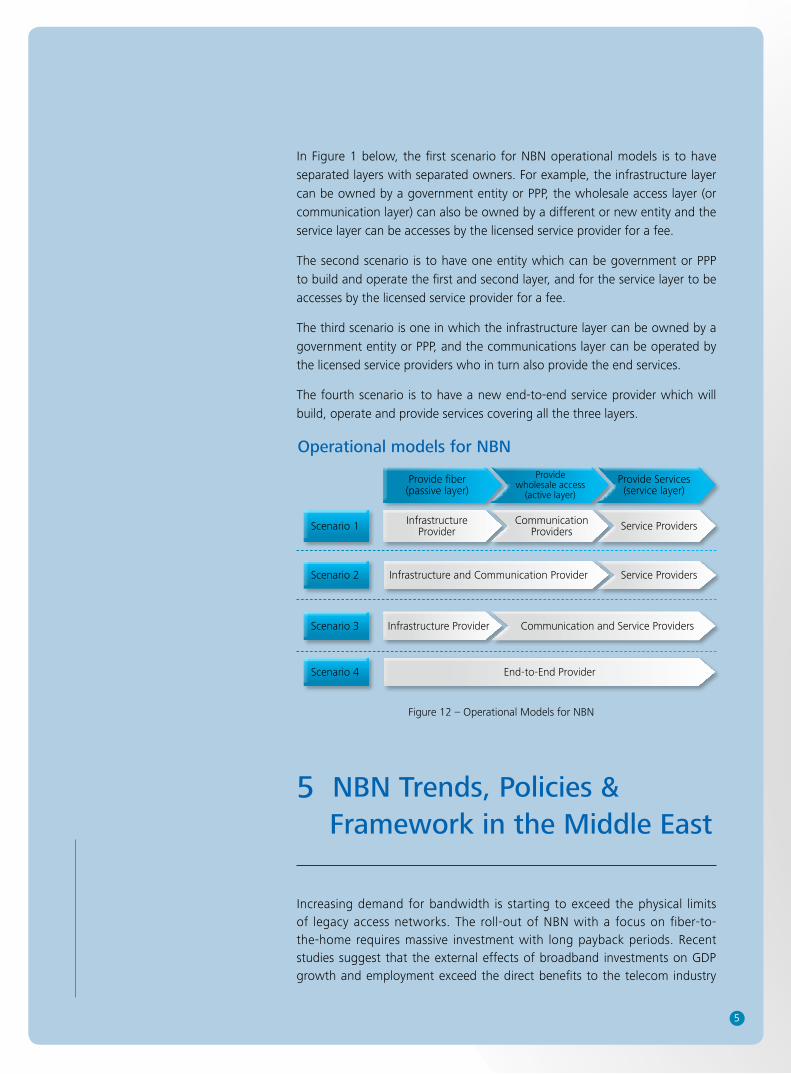

In Figure 1 below, the first scenario for NBN operational models is to have

separated layers with separated owners. For example, the infrastructure layer

can be owned by a government entity or PPP, the wholesale access layer (or

communication layer) can also be owned by a different or new entity and the

service layer can be accesses by the licensed service provider for a fee.

The second scenario is to have one entity which can be government or PPP

to build and operate the first and second layer, and for the service layer to be

accesses by the licensed service provider for a fee.

The third scenario is one in which the infrastructure layer can be owned by a

government entity or PPP, and the communications layer can be operated by

the licensed service providers who in turn also provide the end services.

The fourth scenario is to have a new end-to-end service provider which will

build, operate and provide services covering all the three layers.

Operational models for NBN

Infrastructure Provider

Infrastructure and Communication Provider

CommunicationProviders Service Providers

Service Providers

Scenario 1

Scenario 2

Infrastructure Provider Communication and Service ProvidersScenario 3

End-to-End ProviderScenario 4

Provide fiber(passive layer)

Provide Services(service layer)

Providewholesale access

(active layer)

Figure 12 – Operational Models for NBN

5 NBN Trends, Policies & Framework in the Middle East Increasing demand for bandwidth is starting to exceed the physical limits of legacy access networks. The roll-out of NBN with a focus on fiber-to-the-home requires massive investment with long payback periods. Recent studies suggest that the external effects of broadband investments on GDP growth and employment exceed the direct benefits to the telecom industry

6

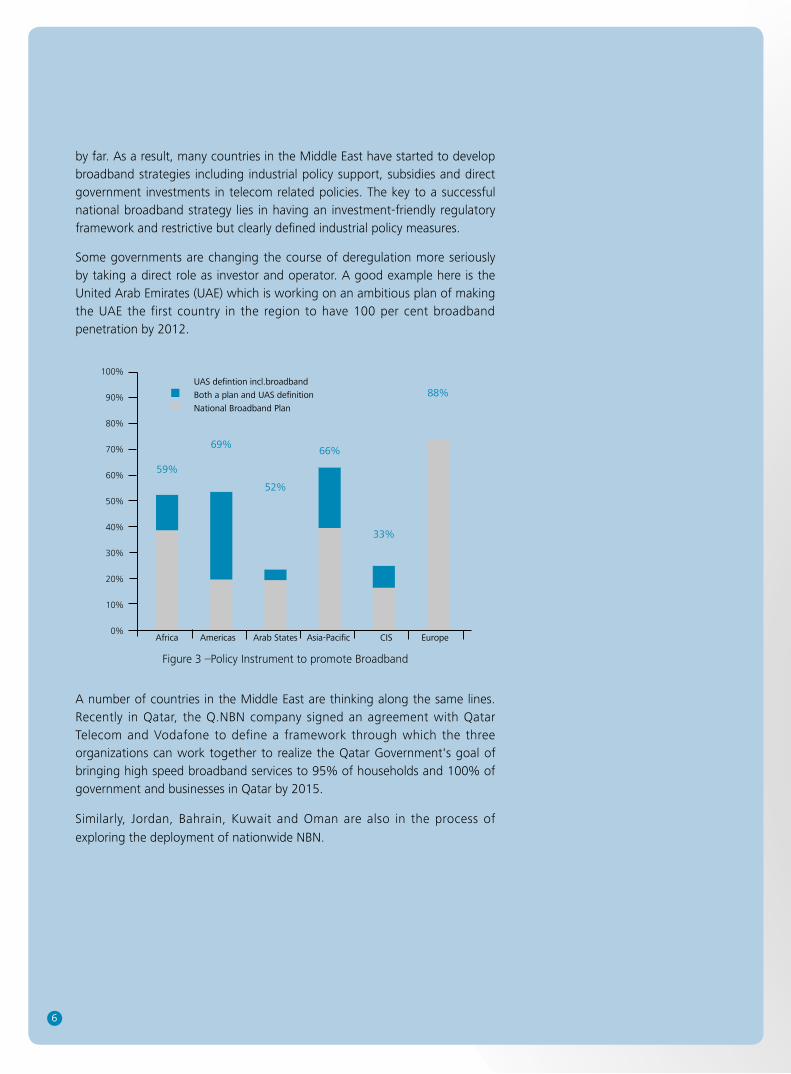

Figure 3 –Policy Instrument to promote Broadband

100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%Africa Americas Arab States Asia-Pacific CIS Europe

59%

69%

52%

66%

33%

88%UAS defintion incl.broadband

Both a plan and UAS definition

National Broadband Plan

A number of countries in the Middle East are thinking along the same lines. Recently in Qatar, the Q.NBN company signed an agreement with Qatar Telecom and Vodafone to define a framework through which the three organizations can work together to realize the Qatar Government's goal of bringing high speed broadband services to 95% of households and 100% of government and businesses in Qatar by 2015.

Similarly, Jordan, Bahrain, Kuwait and Oman are also in the process of

exploring the deployment of nationwide NBN.

by far. As a result, many countries in the Middle East have started to develop broadband strategies including industrial policy support, subsidies and direct government investments in telecom related policies. The key to a successful national broadband strategy lies in having an investment-friendly regulatory framework and restrictive but clearly defined industrial policy measures.

Some governments are changing the course of deregulation more seriously by taking a direct role as investor and operator. A good example here is the United Arab Emirates (UAE) which is working on an ambitious plan of making the UAE the first country in the region to have 100 per cent broadband penetration by 2012.

7

6 Deployment Consideration for NBN

We have to consider the entire possible factor in deployment of NBNs,

including: the overarching plan, technology, standards, policies, best

practices, existing infrastructure, services and products, network operators,

competition scenarios and available retail-service providers. Moreover, we

believe the following approach to be one of the most useful technical and

business considerations for NBN deployment.

Evaluation of Current NetworkConducting an audit to existing network infrastructure, which includes •

documenting current:

Central office equipment & space•

DC and AC power•

Copper and fiber plant•

Selection of Services Determining which services and bundles will be offered on the network •

Market demand •

Deployment budget •

Immediate service offerings•

Future service offerings•

This will lead to knowing the infrastructure and equipment requirements of

the network.

Broadband Technology Options Investigating which broadband technologies are available for delivering •

the selected services

Successful FTTx network needs to be capable of evolving to keep •

pace with a growing subscriber base, increasing penetration and the

introduction of new services

Prepare the Business Case The value of existing infrastructure •

The service offerings •

The service delivery technologies •

The network bandwidth plan •

8

CAPEX + OPEX = TCO •

TCO influenced by level of detail in design, construction schedule, take-•

rates & style of FTTx network

NBN Entity Set-upCreate NBN Legal Entity•

Establish Public-Private Partnerships and Venture Funding •

Define Business and Operation Model•

License the NBN networks•

Set-up NBN governing PMO office•

NBN ImplementationDevelop implementation and servicing RFPs•

Contracting civil work and Infrastructure service providers•

Distribute work packages•

Deploy NBN infrastructure packages•

Service the NBN infrastructure (model dependant)•

NBN OperationDevelop operation RFPs•

Contract service and operation providers (Managed Services)•

Operate and maintain NBN networks•

Collect revenues as per business model•

NBN EvolutionIdentify technology trends and evolutions•

Define technology roadmap•

Manage infrastructure continuity and evolution•

7 Middle East NBN Challenges and Obstacles

Conflict of Interest: Normally if the governments adopt the deployment • of NBN there will be a conflict of interest between the incumbent and the

NBN co. as the monopoly will end and this mean an open access, open

competition over the fixed network in equal bases which mean decrees

of profit for incumbent and less turnover.

9

High initial investment: one of the major challenges in NBN deployment • is the high initial investment specially when serving the remote areas and

the challenge of long RoI.

The openness of Incumbent to its existing brown field network in order • to avoid duplication of Infrastructure and reduce the amount of civil

work.

Technology selection for business and residential areas. •

The requirement of NBN to select particular technology:

100Mb/s: Can the technology provide 100MB in DL to residential consumer •

in the next 10 years?

1 GB/S: Can the technology provide 1GB to business consumer in the next •

10 years?

Universal: Satisfactory data throughput while providing universal coverage•

Video: Video services•

Future Proof: Can this be upgraded in the medium to long-term?•

Price: Is this affordable?•

FTTH is the only technology which can offer all of the above, but it is still

expensive. FTTN+VDSL are lacking in terms of 1Gb/s Connectivity and being

future proof.

The various challenges that we foresee can be detailed as:

Challenges to Support High Bandwidth and Quality•

Challenges to Build Cost-effective ODN Network•

Challenges to Shorten Construction Time•

Challenges to Reduce Fiber Management Cost•

How to ensure fair competition and stimulate investment?•

How to design the Bitstream Wholesale product?•

How to design the Open Access Network to realise the wholesale •

requirements?

Risk of low take-up rate (FTTX subscription may be lower than the •

expectation)

Inadequate successful services (Content value chain need time to develop. •

How to create local content, how to educate the consumer for the benefit

of the services are major challenges)

Incumbent resistance (How to create a fair, reasonable competitive •

environment for all players?)

Regulatory & Business model uncertainty (How to protect the huge •

investment committed on the NBN? How to integrate the NBN network

with existing broadband ecosystem?)

10

8 Vision and Goals of NBN in Middle East

On the basis of financial viability, it will take operators some time to

achieve nationwide coverage with fiber access networks; much longer than

governments would like for reasons of economic recovery and national

competitiveness.

As a consequence, operators have little interest in investing in fiber

infrastructure outside of urban areas. Studies suggest that under current

ARPU and cost conditions fiber-to-the-building (FTTB) networks would only

be profitable for about 25% of Middle East households, while the more basic

fiber-to-the-curb (FTTC) networks could serve slightly above 70% profitably.

This is under monopolistic conditions. In a competitive environment, the

investment opportunity would be even more limited. This is a major challenge

to the existing regulatory system with its basic idea to solve sector problems

through liberalization and privatization. However, NBN goals can be divided as:

Short term (2-3 years) Private sector contracts for advisory, consulting and engineering, network •

Infrastructure and equipment sales •

Internet and technology startups to receive venture funding for the •

development of applications and services

Medium term (3-5 years) Business appetite for new services will rise in line with public awareness of •

the NBN’s advantages

Key technology innovations and business models will emerge to deliver •

advanced services for the telecom, media, health, education, and

consulting industries

Long term (+5 years) Deployment of new services and business models to support Internet •

protocol television (IPTV) and OTT

Utilities such as a power, water and gas – possibly combining with •

telecommunications carriers, financial services providers, media, technology

and retail operators – to offer consumers single-bill options for the

household via secure payment services that leverage FTTH infrastructure

11

9 Scope for Middle East NBN Deployment

While regulators previously saw the restriction of the incumbent’s market

power and the support of service competition as their main task, their focus

is now shifting to fostering investments in broadband access networks. This

demands new regulations, while the increasing “digital divide” between

urban centers and rural areas also require a new approach to defining

relevant regional markets, determining significant market power for each sub-

market, and identifying remedies (or industrial policy measures) for each sub-

market.

In principle, three types of regions can be determined:

Dense urban city centers where more than one fiber access network is •

viable and can compete with interactive networks and future wireless

solutions. In these areas, non-regulated infrastructure competition could

be an efficient solution requiring only clear standards for interoperability

and symmetric access obligations.

Country like KSA where 70% are Outdoor ADSL2 (Active) cabinets being •

used, shall go ahead for VDSL2 to have time-to-market advantage until

FTTH is ready within 2-3 years in theses areas.

In smaller cities and suburban areas with only one fiber network, regulated •

access to monopolistic next-generation networks and investment-friendly

regulatory remedies would suffice. The comparatively high risks faced by

the infrastructure investor should also be reflected in regulated wholesale

prices allowing risk sharing by price structures that reward long-term rental

and high capacity commitments. The bit stream will also suit these areas.

In rural areas where fiber networks are not viable, the only market solution •

could be high-speed mobile broadband offers such as Long Term Evolution

(LTE) or alternative 4G networks. However, service quality will be well

below the broadband strategy’s high-speed targets. Here the regulator

needs to develop new instruments. A start-up solution could be to allow (or

force) pooling of the LTE spectrum to be auctioned in rural areas so that

operators can offer higher bandwidth. The current practice of subsidizing

local community fiber network developments definitely needs more clear

standardization to ensure inter-operability of the individual networks.

12

10 Recommendations

Our recommendation can be divided into to parts, Regulatory & Technical

recommendations

Regulatory Recommendations

Funding mechanisms for promoting the deployment of broadband • infrastructure

1) Leveraging partnerships; and

2) Modernizing universal service programmes and funds

Fostering private investment in broadband through incentive regulation•

1) Providing overall direction through a national policy,

2) Rationalizing licensing regimes,

3) Making spectrum available for mobile broadband

4) Removing barriers to broadband build-out and access to broadband

networks

5) Granting tax incentives

Stimulating innovation and development of applications and services •

Expanding digital literacy •

1) Nurturing the creation and adoption of applications, services and digital

content,

2) Spurring investment in R&D activities

3) Enforcing Intellectual Property Rights

We recognize that digital literacy has become an essential personal and

professional asset as the global economy evolves into one that is open,

competitive and digital. Countries with high levels of digital literacy are more

innovative and productive and are capturing a greater share of the world’s

trade, investment and jobs.

Technical Recommendations

Limit NBN dark fiber to the home, offering a potential 2-3 infrastructure-• based service providers

Move forward to passive architecture, enabling f lexible, active • configuration and technology choices

Possibility of bitstream regulation to enable further service providers (if • open passive networks are not possible or too expensive)

Reuse of existing assets (transfer & reuse, transfer & overbuild, •

13

replacement)

Topology of handover points (cost efficiency, operational performance, • suitability to current topologies)

Technology choice (PON, P2P, etc.) to enable potential reuse•

Rollout plan/migration plan•

What will be the commercial offering of NBN•

Demographic evolution and demand for broadband services in Oman•

Outstanding key design decisions (topology, resilience monitoring)•

Define a Brownfield approach and Greenfield approach•

Identify key terms for the NBN license (e.g. service scope, duration, • exclusivity, etc.)

Define additional separate regulation on NBN (e.g. sharing obligations & • pricing)

The trend for growing bandwidth demand remains unbroken across the

Middle East. Wide use of multi-room HDTV, cloud computing, high-end

gaming, and multimedia-intensive social networks are driving data rates per

household well beyond the physical limits of legacy copper access networks.

All major fixed line operators are now starting to install fiber in the local loop,

either as “fiber-to-the- curb” (FTTC), “fiber-to-the-building/home” (FTTB/H) or

“hybrid fiber-coax” (HFC) in the case of cable TV operators.

11 Conclusion

National Broadband Network (NBN) technology is set to become the

predominant infrastructure and as a utility-based network, it will also

provide its services to sectors such as government, healthcare, education

and business. It will have the capacity to carry existing and future data

and communication services, including voice, IPTV, VOD, OTT, high-speed

Internet access, leased line service for enterprises, and backhaul for mobile

broadband services. In the very near future, members of a single family will

be watching HDTV video at the same time that they engage in remote health

monitoring, video-conferencing, gaming, distance education classes and

social networking.

As the race to compete in the digital economy continues, NBN technology

is a key driver of national competitiveness as it can provide universal access

to high-speed broadband and improve overall socio-economic growth in the

Middle East.

Copyright © Huawei Technologies Co., Ltd. 2012. All rights reserved.

No part of this document may be reproduced or transmitted in any form or by any means without prior written consent of Huawei Technologies Co., Ltd.

General Disclaimer

The information in this document may contain predictive statements including,

without limitation, statements regarding the future financial and operating results,

future product portfolio, new technology, etc. There are a number of factors

that could cause actual results and developments to differ materially from those

expressed or implied in the predictive statements. Therefore, such information

is provided for reference purpose only and constitutes neither an offer nor an

acceptance. Huawei may change the information at any time without notice.

Trademark Notice

, HUAWEI, and are trademarks or registered trademarks of Huawei Technologies Co., Ltd.

Other trademarks, product, service and company names mentioned are the property of their respective owners.

HUAWEI TECHNOLOGIES CO., LTD.

Huawei Industrial Base

Bantian Longgang

Shenzhen 518129, P.R. China

Tel: +86-755-28780808

Version No.: M3-034166-20121008-C-1.0

www.huawei.com