Embed Size (px)

Citation preview

NBER WORKING PAPERS SERIES

UNION THREAT EFFECTS AND NONUNIONINDUSTRY WAGE DIFFERENTIALS

David Neumark

Michael L. Wachter

Working Paper No. 4046

NATIONAL BUREAU OF ECONOMIC RESEARCH1050 Massachusetts Avenue

Cambridge, MA 02138April 1992

We thank John Blomquist for research assistance, and William Dickens, Christopher Hanes,David Levine, and Jaewoo Ryoo for helpful comments. Research support was provided by theInstitute for Law and Economics, University of Pennsylvania, This paper is part of NBER'sresearch program in Labor Studies. Any opinions expressed are those of the authors and notthose of the National Bureau of Economic Research.

NBER Working Paper #4046April 1992

UNION THREAT EFFECTS AND NONUNIONINDUSTRY WAGE DIFFERENTIALS

ABSTRACT

We investigate the impact of union strength on changes in nonunion wages and

employment. The prevailing model in this area is the threat model, which predicts that increases

in union strength cause increases in nonunion wages and decreases in nonunion employment.

In testing the threat model, we are also testing two alternatives, the crowding and complements

models. In contrast to the prediction of the threat model, decreases in the percent organized

(reflecting a declining union threat) are associated with increases in the nonunion wage.

Furthermore, increases in union wages appear to decrease, rather than to increase, nonunion

wages. Evidence on the determinants of intra-industry variation in nonunion wage premia is

somewhat more consistent with the crowding model and is strikingly consistent with the

complements model of union and nonunion wage determination. Further evidence on the

determinants of intra-industry variation in nonunion employment is consistent with the

complements model and the threat model; movements in nonunion industry employment are

negatively related to changes in proxies for union strength. Thus, the combined evidence

supports the complements model, but neither the threat model nor the crowding model.

David Neumark Michael L. WatcherAssistant Professor Professor, and Director,Department of Economics Institute for Law and EconomicsUniversity of Pennsylvania Department of EconomicsPhiladelphia, PA 19104 University of Pennsylvaniaand NBER Philadelphia, PA 19104

In the union literature of the past several years, considerable evidence has been

marshalled to support the fact that union employment and overall union strength have

declined dramatically over the 1970s and 1980s, while union wage premiums have

increased just as dramatically (see, e.g., Bell, 1989; Linneman, Wachter, and Carter,

1991; Wachter and Carter, 1990, and Neumark, forthcoming). Little attention has been

paid, however, to the effect of these developments on the nonunion sectors of the

economy. This paper examines these developments, with the goal of providing empirical

tests of alternative models of the effects of union sector developments on nonunion

wages and employment.

The prevailing model of the impact of unionization on the nonunion sector has

been based on the threat model. First tested by Rosen (1969), the threat model predicts

that an increase in union power will cause an increase in nonunion wages. The

nonunion response occurs because nonunion employers calculate that nonunion workers

are less likely to unionize when the nonunion firms are independently responding to

union wage increases. Wage developments in the nonunion sector therefore follow, to

some extent, wage developments in the union sector; for example, an increase in union

wages leads nonunion employers to increase their own wage premium, thereby moving

up their demand curve and laying off workers and reducing output.

In the theoretical and empirical analysis of the union threat model in the existing

literature, the level of analysis is typically the industry rather than the overall economy.

Paralleling this, the union threat model has been offered as an explanation of inter-

industry wage differentials in the nonunion sector (e.g., Dickens, 1986; Dickens and

Katz, 1987a; Krueger and Summers, 1988). Because one goal of our analysis is to test

this explanation of the nonunion wage structure, we also conduct our analysis at the

industry level. Since unions or in Dunlop's terms 'industrial relations systems" (Dunlop,

1944) are not neatly organized along two- or three-digit industry categories, and because

threat effects of any particular union may affect firms in a number of industries ('orbits

of coercive comparison" (Ross, 1948)), we conduct our analysis for both one-digit and

two-digit industry classifications.

There are two principal alternatives to the threat model: the crowding and

complements models. Although our equation specifications are tailored to test the

threat model, we also consider the predictions of the crowding and complements models

for these specifications, to clarify the interpretation of any rejections of the threat model

that may arise.

The "crowding model' is labor supply driven. It is based on the view that

nonunion workers are labor market substitutes for union workers. Higher union wages

and any resulting lower union employment cause an outward labor supply shift in the

nonunion sector. The result is lower wages and higher employment in the nonunion

sector. Although nonunion labor demand may also increase if nonunion output is a

substitute for union output, the prevailing view is that labor supply effects dominate

labor demand effects.

The "complements model," which has received less attention in the literature,

focuses on the labor demand ties between union and nonunion labor within the same

industry. In this model, there are three sectors: a union sector, a "substitute" nonunion

sector that competes with the union sector, and a "complement" nonunion sector that

serves as a production complement to both the union and substitute nonunion sectors.

2

Workers in the complements sector may include nonunion workers employed in the

same establishment as union workers (perhaps in other occupations), or nonunion

workers in nonunion firms that act as suppliers to the union and substitute nonunion

sectors. Lower union sector output would thus reduce the demand for nonunion

complements workers, thereby driving down their wages and employment.

The prevailing empirical literature supports, albeit weakly, the threat model. The

major papers in the area are cross-sectional tests focusing on nonunion wages as the

dependent variable. Little attempt has been made to analyze whether the results

support either the crowding or complements models. Nor have the alternative models

been tested on time-series data, at the industry or the aggregate level.

In this paper we test the threat model in a pooled cross-section time-series data

set, using the period 1973 to 1989, a period during which union wages increased, and

union employment decreased dramatically. We also test the predictions generated by the

other models of the relationships between the union and nonunion sectors.

Finally, we consider an additional dependent variable. The threat model has

typically been analyzed in the context of threat effects on nonunion wages. We extend

the analysis by considering the implications of the threat model, as well as the crowding

and complements models, for nonunion employment as well. We show that by jointly

considering union-nonunion interactions for both wages and employment, we can

provide a sharper differentiation among the competing models.

In general, our results are inconsistent with the union threat model and the

crowding model, and are largely consistent with the complements model. These

3

conclusions come from a number of empirical tests, and hold at both the one-digit and

the two-digit industry level.

Section I discusses the relevant literature and Section II presents the alternative

models. The data are described in Section III and the empirical tests performed in

Section IV. Section V concludes the paper.

I. Literature Review

A formal model of the threat hypothesis, in which nonunion employers pay

above-market-clearing wages to deter unionization, is developed in Dickens (1986). In

this model the determinants of the wage that a nonunion employer must pay to avoid

unionization are the magnitude of supra-competitive rents (which may or may not exist

in the long-run), and the costs of organizing. The large existing literature which ties the

percent organized in an industry to the wages of nonunion workers in cross-sectional

data (e.g., Freeman and Medoff, 1981; Kahn, 1980; Podgursky, 1986), can be interpreted

as testing the validity of this model, on the assumption that the costs of organizing are

negatively related to the percent organized or, equivalently, to the percentage of industry

employment that is unionized.1 Dickens and Katz (1987b) interpret their research tying

nonunion industry wage premia to measures of market power and profitability (in

addition to the percent organized), as conducting indirect tests of the union threat

model, since these variables presumably proxy for industry rents; however, as they

'Rosen (1969) develops this argument in more detail. He suggests that threat effects on nonunionwages will be largest when the demand for union labor is least elastic, since there are then smaller laborflows to the nonunion sector in response to the union wage increase. This elasticity is likely to be smallest(in absolute value) when the industry is relatively more unionized, since there are then fewer substitutionpossibilities, so that the percent organized is positively related to threat effects. But Rosen also argues thatthere may be offsetting factors, perhaps because as the percent organized increases, the remaining nonunionfirms are particularly resistant to unionization.

4

recognize, other theories of non-market-clearing wages would also predict a positive

relationship between rents and wages (e.g., Akerlof, 1982; Lindbeck and Snower, 1988).

Finally, Montgomery (1989) examines the effects of the percent organized and the union

wage premium on employment probabilities of individuals.

The formulation closest to ours is Dickens and Katz (1987a), which conducts an

empirical analysis of the union threat explanation of nonunion industry wage premia.

They use 1983 annual files of the CPS to estimate individual-level wage regressions,

including three-digit Census of Population industry dummy variables.2 In a second-stage

equation they then regress the estimated industry coefficients on a rich set of industry

characteristics, to identify the correlates of industry wage premia.3'4 -

Consistent with the threat hypothesis, Dickens and Katz find that the sign of the

percent unionized variable in the nonunion wage regressions is generally positive. But

they point out that the hypothesis is only weakly supported because the coefficient is not

always positive, and is often statistically insignificant. Some of the other variables do

support the threat model, particularly the positive coefficient on profitability, which they

indicate supports the hypothesis that the higher the potential rents, the higher the wage

(Dickens, 1986). Since industry characteristics are highly correlated, however, Dickens

2The cross-sectional equation includes the measurable human capital of workers, demographiccharacteristics of workers, and controls for state of residence, living in an MSA, and occupation.

3These include: average wages; average income; average demographic characteristics; unemployment andlayoff rates; injury rates; overtime; non-wage compensation; average establishment size; measures of marketpower, concentration, and profitability; other industry characteristics; and, most directly related to the unionthreat explanation, the percent of workers in the industry covered by collective bargaining agreements.

4Dickens and Katz rationalize this 'two-step' approach, arguing that estimating an individual-levelregression with some variables (i.e., industry characteristics) aggregated to the industry level may lead tobiased coefficients because the industry aggregates measure the characteristics of the worker's firm witherror (Dickens and Ross, 1984).

5

and Katz note that it is difficult to sort out the independent influence of the large

number of industry characteristics that they consider. In addition, because the key

percent unionized variable does not provide robust support for the threat model, it is

more difficult to interpret the meaning of the profitability variable.5

As indirect evidence against the threat model, researchers have cited the fact that

the nonunion inter-industry wage structure is quite stable over time and across regions

(e.g., Krueger and Summers 1988; Helwege, 1991). According to these researchers,

given variation in union wage premia across time or regions, a nonunion wage structure

that is highly correlated across time or regions makes it less likely that a strong threat

effect exists. However, the variation in union wage premia that might be expected to

affect the nonunion wage structure is changes in intra-industry union wage premia across

time or regions, not simply changes in overall union wage premia across time or regions.

Consequently, the sharp changes in intra-industry union wage premia in the 1970s and

1980s (Linneman, Wachter and Carter, 1990) provide a natural testing ground for the

union threat explanation of the nonunion wage structure. In particular, we can ask

whether changes have occurred, in nonunion inter-industry wage differentials, that are

related to changes in union threats.

5lndeed, they cite factor analysis results for industry data suggesting that one factor can account formuch of the variation in industry chacacteristics. A related result is suggested in their paper, in which theyshow that two principal components can explain about 50 percent of the covariation in their industry data.

6

II. The Union Threat, Crowding, and Complements Models

Data Set and Dependent Variables

In this paper we construct a panel data set, rather than a cross-sectional data set

as in Dickens and Katz (1987a). The dependent variable--the nonunion wage

differential or premium by industry and year--is estimated from cross-sectional wage

equations using CPS data, including skill and other related control variables. One of the

central independent variables, the union wage premium, is formed in the same fashion.

The method of construction is discussed in Section III.

The nonunion wage premia (denoted w") are then regressed on the proxies for

union strength in a second-stage regression, in which we control for other industry

characteristics with industry-specific dummy variables. The hypothesis is that the greater

the threat effect, the greater the nonunion premium.

In addition, we add a second equation to test the threat model. Besides

estimating an equation where the nonunion wage is the dependent variable, we also

analyze the threat effect in terms of the nonunion industry employment share (denoted

es') as a dependent variable.6 If the union threat increases, it should affect not only

the nonunion wage, but also nonunion employment. We define employment shares as a

percent of total economy employment rather than industry employment. The reason is

twofold. Since the threat model, as well as the crowding and complements models,

suggest spillovers between the union and nonunion sectors in the same industry, a

within-industry variable would be difficult to interpret. In addition, losses in either

6Union and nonunion employment-share variables were estimated directly from the CPS data. Detailsare provided in Section III.

7

union or nonunion employment need not be to the other sector in the same industry, as

shown in Linneman, Wachter, and Carter (1991).

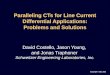

Independent Variables or Measures of Union Threats

The next step is to determine the variables that can serve as measures of the

magnitude of the union threat. The traditional view is to measure union strength by the

percent organized (%org), with a predicted positive coefficient in an equation for

nonunion wage premia (w). This is shown diagrammatically in Figure 1, where a

decrease in %org means a downward shift in the demand for union labor from D° to

and an increase in the demand for nonunion labor from to DnUI.7 The impact of

the decline in union employment is to cause the threat locus, which measures nonunion

firms' perceived threat from unionization, to decline from T to T', allowing w to

decline.8

We expand this framework by introducing the union wage premium as another

measure of the union threat (as in the model in Dickens, 1986), also with a predicted

positive coefficient. In Figure 1, an increase in the union wage (and hence an increase

in the union wage premium) from w to causes a movement up the demand curve

7Since neither sector is a market-clearing sector, and both pay above market wages, employment isdemand constrained. Hence, the supply curves can be omitted.

8The T locus shows the nonunion wage premium that must be paid to deter unionization. It isdownward sloping because as e? is increasing, the threat is decreasing. It shifts when other variables,particularly the union variables described in this section, change.

8

for union labor Di'. This in turn causes the threat locus, T, to shift to 12, causing w"' to

increase and ef' to decrease.9

In addition, we add three additional independent variables that can proxy for the

'costs of organizing. We include two election variables: the percentage of National

Labor Relations Board (NLRB) representation elections won by unions (denoted

%won), and the overall number of representation elections (denoted rep). We also

include the number of unfair labor practice claims against employers (denoted ulp). Our

hypothesis is that the coefficient(s) on the election variables will be positive in the threat

model.1° Specifically, when union certification elections are low and when unions are

losing many of the elections, the relative cost of remaining nonunion decreases, and T

shifts down to T3.

On the other hand, when the number of unfair labor practice charges against

management is high, unions themselves are facing increased costs of organizing workers

or maintaining their union status. U/p charges are high when management's opposition

to unions is high and unions contest the legality of management's activities.

Management opposition in this form allows nonunion wages to be lower; an increase in

u/p shifts the threat locus, T, downwards. Hence, in the threat model the hypothesis is

that the coefficient of ulp will be negative.

Our data formulation has the advantage that the statistical experiment is

conducted on a data set in which there are sharp changes in variables that are plausibly

9Some difficulties posed by using this variable in an equation where the nonunion wage w°°1' is thedependent variable are discussed below. The union wage variable, however, is pivotal in the equationwhere the nonunion employment share is the dependent variable.

'°Notationally, we refer to the two election variables %won and rep, when discussed jointly, as elect.

9

related to 'the strength of the union threat effect. The specifications also include

industry dummy variables. The intent is to have the dummy variables capture the other

industry characteristics considered by Dickens and Katz (1987a), so that we can identify

union threat effects from our estimated coefficients. Using industry fixed effects avoids

the problem found in cross-sectional studies of multicollinearity among industry

characteristics. However, to identify union threat effects, the omitted characteristics that

are correlated with the threat variables must be fixed over time. This is the maintained

assumption in this paper; given the sharp changes in union strength over the sample

period, it may not be far from the truth.

The union strength proxies are treated as exogenous, because we do not believe

that there are identifying restrictions available for explicit treatment of the endogeneity

question. Denoting the industry fixed effect I, and subscripting the variables by industry

(i) and year (t), we estimate equations of the form

(1) w" = a + %orgB1 + wuPj32 + elect1B3 + u1p134 + ly +

Our specification of threat effects on the nonunion employment share parallels

the specification of equation (1). All of the variables from (1) are included in (2) with

the exception of %org. Since the dependent variable is the nonunion employment share,

using the percent organized as an independent variable could result in a spurious

negative correlation. This is the case even though our dependent variable has total

economy employment as the divisor while the independent variable would have industry

employment as the divisor.

10

Denoting the nonunion employment share as es", the equation for the nonunion

employment share is

(2) esv =a' + w.B'2 + elect113'3 + ulp1B'4 + ly' +

Since the nonunion sector is presumed to be acting like the union sector, in

response to increases in union strength or the union wage it moves up its labor demand

curve, thereby reducing employment. Hence, the threat model implies that the signs of

the union threat proxies are reversed in equation (2); the nonunion employment share

moves inversely with the nonunion wage premium. The effects on nonunion wages and

employment that are implied by the threat model are summarized in the first panel of

Table 1.

Th Crowding Model

The crowding model focuses on the implications of the labor supply spillover

from the union sector, where employment is restricted by a wage premium, to a market-

clearing nonunion sector. Whereas the nonunion sector "acts like the union sector" in

the threat model, the nonunion sector reacts competitively in the crowding model. Thus,

the responses of nonunion wages and employment to an increase in the union wage

premium, w, are the reverse of those in the threat model. This, as well as the other

differences and similarities between the two theories can be seen by comparing Figures

1 and 2.

Turning to %org, a decrease in %org causes D to shift to DU!, thus causing S to

shift out to S. The result is a decline in w9. Note that in the crowding model, the

11

traditional assumption is that labor supply spillovers dominate labor demand spillovers.

Hence, although the nonunion demand curve shifts out, the maintained assumption in

the model is that the nonunion supply curve shifts out by more. Thus, we show only the

latter shift. The resulting decline in w"° is the same as in the threat model, but for a

different reason; this is the only variable for which the two theories generate the same

prediction in equation (1).

The predicted effects of the NLRB variables are also different from those of the

threat model. One has to be careful, however, as to the interpretation given these

variables in the crowding model. The NLRB variables are introduced to serve the

primary mission of the paper, testing the threat model. With the exception of %won,

they might not be introduced as likely variables in a crowding model, were we testing

that model independently of the threat model. But we want to consider the implications

for the coefficients of these variables in equations (1) and (2), under the crowding

model (and the complements model), in order to interpret results that may be

inconsistent with the threat model.

%won is a useful variable because it measures actual or potential shifts between

the union and nonunion sector. For example, a decline in %won means that unions are

losing elections and thus D is shifting inward to D', and and S° are shifting out to

D' and as shown in Figure 2. For w, the effect is a wash, but es clearly

increases. In general %won operates in a similar fashion to %org, but has a greater

demand effect.

We interpret the NLRB variables rep and ulp as measuring costs of union labor

not reflected in w, and hence operating in a similar fashion to w'', although changes in

12

these variables result in shifts of Du, rather than shifts along it.1' The lower the

number of union elections and the greater the allegations of unfair labor practices by

management, the weaker is the union, and hence the lower are labor costs in the union

sector. Hence a decrease in rep or an increase in ulp causes an outward shift in the

demand for union labor, from DU to DU4, leading nonunion labor supply to shift in to

S'4. These shifts cause es' to decrease, and thus w to increase.

The results for the crowding model are summarized in the second panel of Table

1. In closing, we note that the crowding model is sometimes specified to include a

possible shift in labor demand in the nonunion sector in the opposite direction of the

employment change in the union sector. Including both the spillover of demand and

supply from the union sector, the final effects on w and esare ambiguous, depending

on the magnitudes of the shifts in labor supply and demand. In the existing literature, it

is usually assumed that the supply shifts dominate. For example, Kahn (1978) contrasts

the threat and crowding models by the different impacts that union wage increases have

on nonunion wages (positive for the threat model, and negative for the crowding model).

We make the same assumption here.

The Complements Model

Finally, we consider a model in which union and nonunion labor are complements

in production. This is a more complex model, since it requires the depiction of two

nonunion sectors. It does, however, capture a well recognized multiplier effect, whereby

"For example, consider two industries that have identical union wage premia, but the first industry hasmore representation elections and weaker management opposition to unions. We might expect unions in thisindustry to extract higher non-wage concessions from management, resulting in a higher cost of union labor.

13

a decline in union employment will spill over into a decline in nonunion employment

that works along with, or as a complement to, union labor.

The model is depicted in Figure 3. The nonunion substitute sector in this figure

works in the same manner as did the nonunion sector in Figure 2. The difference is that

we postulate the existence of a nonunion sector which follows the level of activity in the

union sector.

In this model, a decline in %org causes the usual decrease in union employment

and increase in demand for nonunion labor that acts as a substitute. In this case, the

outward shift of S° to S'1 causes an increase in es"' and a decline in Although not

drawn, DS may also shift outward, which would moderate the wage decline. But as in

the crowding model, it is assumed that the dominant impact of the union sector on the

nonunion substitute sector is supply shifts. More importantly, however, the overall

composite wage across the union and nonunion substitute sectors declines. The result is

an increase in demand in the complements sector. Hence D' shifts to D1. We assume

that developments in the nonunion complement sector dominate the overall nonunion

sector. Thus, the prediction is that both ef and w'°" will increase.

Moving on to the Wt variable, an increase in w' in the complements model acts

as a depressant on activity in the union sector without the same corresponding uptick in

nonunion substitute sector employment as was the case with %org variable. The result

is that D' declines to D2, causing both es and w to decline.

As noted above %won operates in a similar fashion to %org. Hence a decrease

in %won is like a decline in %org, causing both es and w to increase. Similarly rep

14

and ulp act like w"'. Hence a decrease in rep and an increase in ulp causes both es'" and

w""" to increase.

The predicted coefficient signs of the complements model are presented in the

third panel of Table 1. Scrutinizing Table 1 reveals the advantage of considering both

equation (2) (for employment) as well as equation (1) (for wages) if we are to

differentiate among the three models. Equation (1) provides sharply contrasting

predictions between the threat model, on the one hand, and the crowding and

complements models, on the other; but only the coefficient of %org, B, differentiates

between the crowding and complements models. Equation (2), in contrast, provides

sharply contrasting predictions between the crowding model, on the one hand, and the

threat and complements models, on the other.

Test of the Models Based on Union Sector Adjustments

We also carry out an additional test, which is a more "direct test of the extent to

which nonunion industry wage premia estimated from cross-section wage regressions

measure threat effects within the industry. This test considers the feedback of the size

of the threat effect on the responsiveness of union employment to changes in the union

wage. Specifically, where threat effects are strong, the decline in union employment in

response to an increase in the union wage should be relatively weak. That is, union

employment is better protected against increases in union wage premia when the

nonunion sector validates the union premium by matching it with an increase in its own

premium.

15

We use the nonunion industry wage premia w to index threat effects, and test

whether the data are consistent with these premia reflecting threat effects. Denoting the

union share of total employment esu and the union wage premium w't', we estimate

equations of the form12

(3) es1 = ô + w°'1X + + (WUP5 x w"'"11)O + +

In general, union employment should respond negatively to an increase in the

union wage, so we should find X < 0. But threat effects should temper this response.

Consequently, if the nonunion industry wage premia sv"" index threat effects, then we

should find 0 > 0; that is, the decline in union employment in response to an increase in

the union wage should be less negative in industries in which there are strong threat

effects. The sign of , the coefficient of W"', is ambiguous, since w can be viewed as

the price of another input along with union labor. If nonunion and union labor are

complements, then i should be negative; can also be negative if they are substitutes,

but the scale effect of an increase in w dominates.

As before, we also consider the predictions of the crowding and complements

models for the sign of 0 in equation (3). The crowding model yields the same prediction

as the threat model for this regression. If union and nonunion labor are substitutes, then

the union labor demand response to an increase in the cost of union labor should be

smaller if accompanied by an increase in the cost of nonunion labor (i.e., a higher value

of wut), and vice versa. Thus, the crowding model also predicts that 0 > 0.

°We use the union share of total employment, rather than the union share of industry employment, tominimize the endogeneity problem. The union share of industry employment is significantly influenced bynonunion industry employment, which may in turn influence the right-hand-side variable w.

16

The complements model, however, yields opposite predictions from the threat

and crowding models. A high value of the nonunion wage premium corresponds to a

high price of a complementary input. Thus, a hike in union labor costs coupled with a

high nonunion wage premium results in a larger drop in demand for union labor. That

is, the complements model predicts that we should find 0 < 0, in contrast to the threat

model. These results are summarized in the bottom portion of Table 1.

III. Data on Nonunion Wage Premia, Union Wage Premia,and Union Strength

Our estimates of union and nonunion wage premia come from cross-sectional

wage equations estimated for individual years from CPS data. Specifically, we estimated

cross-sectional log wage equations for each year 1973-1989, with separate equations for

white men, black men, and women.13 These equations include a union status

(membership) dummy variable, and a full set of interactions of all variables, including

the industry dummy variables, with the union status dummy variable.'4'5 To focus on

competitive market effects of union wages, we exclude government workers from our

sample. In addition, we exclude managers, professionals, and technical workers. In part

because many of these workers are not covered by the National Labor Relations Act,

'3i982 is omitted because no data were collected on union membership.

'4Details of the concordance between 1970 and 1980 SIC codes are available from the authors.

°ln addition to these variables, we included: nine one-digit occupation dummy variables (with a bridgebetween the 1970 and 1980 SOC codes); linear and quadratic schooling; linear and quadratic potentialexperience; dummy variables for four regions; the MSA unemployment rate; dummy variables for threeMSA sizes; and dummy variables for married, spouse present, and overtime (based on usual hours worked).

17

these occupations have low rates of unionization, and changes in their wages and

employment are likely to be least affected by developments in the union sector.

The coefficients of the non-interacted industry dummy variables estimate the

nonunion industry wage premia.16 Our estimate of the within-industry union premium

is the sum of the coefficients of the industry-union interaction and the union status

dummy variable. In all cases we estimated the wage premia for the entire sample by

weighting (by industry and union employment) the coefficients estimated from the

separate regressions by race and sex.

Our measure of percent organized is constructed from the same CPS data,

described immediately above, used in estimating the wage premium variables. The

percentage of representation elections won by unions, the number of representation

elections held, and the number of unfair labor practice charges against employers are

from NLRB Annual Reports.'7

We constructed a data Set at both the one- and two-digit industry levels. Because

the NLRB threat proxies are available only at the one-digit level, the two-digit industry

data are used only to explore the more limited set of specifications using the union and

nonunion industry wage premia and employment shares, and the percent organized.

In Table 2 we provide summary statistics for the one-digit industry data set,

reporting mean levels and yearly changes for each of these variables, by industry. The

ft"Industry wage premia are estimated relative to services for the one-digit analysis, and relative to

business services for the two-digit analysis. The regression results are of course insensitive to whichindustry is omitted. We replicated many of our results defining industry wage premia instead relative to theaverage nonunion worker (weighting by the representation of workers across industries). The conclusionswere unchanged.

'7Details are provided in the footnotes to Table 2.

18

yearly changes are related to the data used to estimate the regressions, although fixed-

effects are used rather than first differences. The data confirm the now well-known

increase in the within-industry union premium (w') in many industries, coupled with the

decline in percent organized (%org). For the NLRB variables, the percentage of

elections won by unions (%won) and the number of representation elections (rep)

decline for nearly all industries, while the number of unfair labor practice charges (ulp)

increases for two-thirds of the industries.

In focusing on this time-series cross-sectional data set an interesting question is

raised: was the threat effect posed by unions increasing or decreasing during the 1973-

1989 period? On the one hand, the threat effect as measured by the percent organized

and the other NLRB measures was declining. As the most well-known development in

the union sector, the prevailing view is likely to be that the threat effect was declining.

On the other hand, the wage differential between union and nonunion workers within

industries, which is related to the potential gains from unionization, tended to increase

over this period, in manufacturing as well as other industries (Linneman, Wachter, and

Carter, 1990, and our Table 2). Since the weight one should give to the opposing factors

is unclear, the overall direction of the threat effect over the 1973 to 1989 sample period

is indeterminate. But, as we shall show, the question is moot. Although the nonunion

sector did respond systematically to developments in the union sector over the sample

period, the changes are not those predicted by the threat model.

19

IV. Empirical Results

Potential Biases

We have identified four sources of bias in the estimates of our equations that

may affect the conclusions to which the estimates lead. First, in equation (1) we use

as a measure of the potential wage gain from unionization, while wis the dependent

variable. The v"' variable is obtained from the wage regression as the sum of the

coefficients on the union variable and the union-industry interaction variables. The w

variable, on the other hand, is the coefficient on the industry dummy variable. To the

extent that the covariation between w and w' comes from changes in nonunion

industry wage premia that do not similarly affect union workers in the industry (perhaps

because they are locked into contracts), a negative correlation arises between the

dependent variable and the within-industry union premium that does not reflect causal

influences running from the latter variable to the former. On the other hand, variation

in w generated by union-specific forces will impact the union coefficient or the union-

industry coefficient without creating this spurious negative correlation. Because of this

potential problem, when we discuss the empirical results for equation (1), the nonunion

wage premium equation, we focus most on the specifications excluding the within-

industry union premium, w''.

A second potential problem with the within-industry union premium is that it may

reflect the influence of underlying (possibly unobservable) union threat effects, because

this measure may reflect the equilibrium after the effects of union threats are

assimilated into nonunion wages. For example, the within-industry premium may be

large in an industry precisely because unobserved union threat effects are weak, leading

20

to negative bias. Including industry dummy variables should help, however, by

controlling for unobserved industry characteristics that are fixed over time. This also

leads us to focus on specifications excluding the within-industry union premium.

Third, in specifications excluding w", the percent organized (%org) is a key

variable of interest. The estimated coefficient of this variable may, however, be upward

biased by endogeneity. Omitted factors that shift up the nonunion premium, w, may

lead to declines in nonunion employment, and hence increases in %org; this generates a

positive association between the residual in equation (1) and %org. The implication of

this is that the results are biased against finding a negative coefficient on 91oorg, which,

as Table 1 shows, would be evidence in favor of the complements model. Since much of

our evidence ultimately points toward the complements model, this potential source of

bias only strengthens our results.18

Fourth, we have so far ignored the potential effects of industry-specific demand

shocks (stemming, perhaps from import competition) that affect both union and

nonunion labor. These could generate potentially important biases if, as seems

plausible, union wages are less flexible than nonunion wages, with union employment

consequently more flexible. In this case a downward industry demand shock, for

example, will result in a decrease in the nonunion premium ("),a decrease in the

nonunion employment share (esou), an increase in the within-industry union premium

(wuP), and a decrease in the percent organized (%org). Looking at Table 1, we can see

that in equation (1), the equation for the nonunion wage premia, this biases the

We do not believe that we have identifying information on the basis of which to correct for theendogeneity bias.

21

coefficient of w downward, and the coefficient of the percent organized upward.

Together, these biases will tend to favor the crowding model. In equation (2), the

equation for the nonunion employment share, this biases the coefficient of w"

downwards, creating a bias against the crowding model. To control for industry-specific

demand shocks, we introduce the percentage change in the GNP share accounted for by

each industry to attempt to control for shifts in industry-specific demand for labor,

although we recognize that this variable is not unambiguously exogenous. To account

for differences across industries in cyclical fluctuations in this variable, we estimated

separate regressions, for each industry, of the GNP share on the aggregate

unemployment rate and a post-1976 dummy variable for the change in accounting

methods, and used the residual in the regression estimates of equations (1) and (2).1920

Results

In Table 3 we report results from regression estimates of equation (1), in which

the nonunion industry wage differential is the dependent variable. In columns (1)-(7)

we use the one-digit industry data.2' In column (1) we present the standard model of

the union threat effect. The negative coefficient on the percent organized variable is

the opposite of that predicted by the threat model, since the estimated coefficient says

The GNP-share data are from CITIBASE for 1973-1976, and from the Survey of Current Business forthe later years.

20To explore the role of aggregate demand shocks, we experimented with the incJusion of year dummyvariables in our equations, but their coefficients were never statistically significant. Here, in contrast, we arereferring to demand shocks that affect specific industries.

21UnJess otherwise specified, statements regarding statistical significance refer to live-percent significancelevels. For regression coefficients, the statements refer to two-sided tests.

22

that the greater the union strength in organizing the industry, the lower the wage in the

remaining nonunion sector.

In column (2), the NLRB variables are added to the equation. The predictions of

the threat model are that the two election variables are positively related to the

nonunion wage premium, while the number of unfair labor practice claims is negatively

related. The percent organized variable remains largely unchanged, while the NLRB

variables present a mixed picture. The coefficients of the elections variables are

positive, consistent with the threat model, although neither is statistically significant.n

The unfair labor practice variable, on the other hand, has the opposite sign from that

predicted bythe threat model, although it, too, is statistically insignificant. In columns

(3) and (4) we replace percent organized with the within-industry union premium, first

alone and then along with the NLRB variables. In column (3) the coefficient of the

within-industry union premium is negative and strongly significant.

This result rejects the threat model, but the conclusion must be tempered by the

potential for a spurious negative correlation for reasons noted above.

When the NLRB variables are added, in column (4), the evidence against the

threat model is more one-sided. The coefficients of both election variables are negative,

We recognize, though, that the relationship between the percent organized and the union threat may beambiguous, as in Rosen (1969). However, for two reasons we have a strong expectation of a positiverelationship. First of all, while the difficulty of unionizing may become quite strong once very high levels ofunionization are reached, this hardly seems to characterize unionization rates in the U.S. in the sampleperiod. Second, much of the individual-level evidence on the union threat hypothesis looks for and findspositive relationships between individuals' wages and the percent of their industry unionized, although thisrelationship may be present only for certain demographic groups (Kahn, 1980), or in large firms (Podgursky,1986), or it may be rather weak statistically (Freeman and Medoff, 1981).

nThere was no evidence of severe multicollinearity between the two elections variables; in general, thecoefficient estimates and standard errors of the election variables were little changed when one or the otherwas omitted from the equation.

23

and the number of elections variable is statistically significant. The coefficient of the

unfair labor practices variable remains positive but not statistically significant;

furthermore, the three NLRB variables are jointly significant. The within-industry union

premium coefficient remains negative and significant.

In column (5) we reintroduce the percent organized variable. The results again

are almost entirely the opposite of those predicted by the threat model. Both the

percent organized and within-industry premium variables have statistically significant

negative coefficients. The only NLRB variable that is significant is the unfair labor

practice variable, and this also has the positive sign noted above.

In column (6) we add a variable capturing changes in the share of GNP

contributed by each industry, to the specification from column (2). As discussed at the

beginning of this section, this is intended to control for biases induced by industry-

specific demand shocks. The estimated coefficients are little changed. The same is true

when we add back in the within-industry union premium, in column (7).

In columns (8)-(1O), we report results for the subset of the specifications that can

be estimated using data at the two-digit industry level of disaggregation. The greater

disaggregation implies that our estimates of industry wage premia and employment

shares are estimated from smaller cells, leading to greater measurement error bias and

less precise coefficient estimates. The results in columns (8)-(1O) nonetheless parallel

closely the estimates of the corresponding one-digit specifications. As in the estimates at

the one-digit level, the estimates of the %org and W' coefficients are negative and

statistically significant.

24

*Besides providing strong results against the union threat model, the pattern of

results in Table 3 provides mixed support for the crowding model. Remember that in

the crowding model, the nonunion sector reacts competitively and, assuming that union

and nonunion labor are substitutes, generally in the opposite direction of the union

threat model. The crowding model successfully predicts the negative coefficient on w"'

and the positive coefficient (in some of the specifications) on ulp, at the one-digit level,

and the corresponding negative coefficient on w°, at the two-digit level. These

coefficients were incorrectly predicted by the threat model. In terms of w', the

crowding model predicts that the higher the union wage premium, the more crowding

will occur in the nonunion sector, hence the lower is w. In terms of ulp, the crowding

model predicts that the higher the number of unfair labor practice allegations, the

weaker is union power, reflecting more active management opposition, and hence, the

lower is the cost of union labor. This, in turn, means a higher w reflecting the weaker

union sector.

The percent organized variable is the one exception to the rule that the crowding

model has the opposite prediction from the threat model. For this variable, the direct

supply effects are important and probably outweigh the cost of labor interpretation

assigned to the other threat variables. Viewed in this fashion, the crowding model, like

the threat model, does not predict the negative coefficient on %org. That is, the

crowding model predicts that the lower the percent organized, the more crowding there

is in the nonunion sector, and hence the lower should be w. In fact, however, the

estimates in Table 3 indicate that lower %org leads to higher w'.

25

The complements model, however, is more successful in predicting the pattern of

results found in Table 3. Remember that in the complements model, nonunion labor

that is complementary to union labor follows the level of economic activity in the union

sector, and this complementary nonunion labor dominates the nonunion sector overall.

The implication is that, with respect to regression equation (1), the complements model

has the reverse predictions from the threat model. In the threat model, increases in

union power cause the nonunion sector to mimic the union sector, moving up its demand

curve and increasing w. In the complements model, however, nonunion labor that is a

production complement to union labor responds to higher labor costs by decreasing its

wage (and reducing its employment share).

Viewed in this fashion, the complements model successfully predicts the negative

coefficient on w; the higher w', the higher the cost of union labor and thus the lower

the level of economic activity in the union sector. The less activity in the nonunion

sector that is a complement to the union sector, the lower w'. Similarly, the

complements model correctly predicts the positive sign on the unfair labor practice

variable. In terms of u!p, the higher the level of management opposition, the lower the

cost of union labor and thus the higher WUP. Finally, the negative sign on %org is

consistent with complementarity between union labor and nonunion labor, overall.

In summary, the result of estimating equation (1) is a set of coefficients that are

almost entirely contrary to the predictions of the threat model, are mixed with respect to

the predictions of the crowding model, but confirm the predictions of the complements

model. This conclusion holds at both the one- and two-digit industry levels.

26

To gain further evidence on the threat model, and to further distinguish between

the alternative models, we next turn to estimates of equation (2), in which the nonunion

employment share of total economy employment, es, is the dependent variable.

Results for these regressions at the one- and two-digit levels are reported in Table 4.

This equation has the same specification as equation (1) with the exception that the

%org variable is excluded. Although the dependent variable, es, is a share of total

economy employment, it is likely to be spuriously negatively correlated with %org (the

union share of industry employment).

In each of the specifications estimated in Table 4, all of the coefficients are

statistically significant, except for %won (and ulp in columns (2) and (3)). Focusing on

the statistically significant coefficients, with respect to the threat model, the results of

Table 4 are largely supportive. Increases in w cause decreases in es, and increases in

ulp or decreases in rep cause increases in es. Given the results in Table 3, however,

the result with respect to '' is suspect. The reason that es should fall in the threat

model is that W" has increased in response to increases in w. However, we know

from Table 3 that this is not supported by the data. Hence, the decrease in es as a

consequence of increases in w cannot support the threat modeL

For the corresponding analysis at the two-digit level, only one specification can be

estimated, the regression of es on wu (and the industry dummy variables). The

regression is reported in column (5) of Table 4. The coefficient of w is negative, but is

not statistically significant. This is consistent with the one-digit results in the table,

although it is not, by itself, informative.

27

The crowding model is rejected by the results in Table 4. Increases in w should

cause additional crowding in the nonunion sector, hence increasing es. But the

coefficiept on w'' is negative. Similarly the crowding model incorrectly signs the ulp and

representation elections variables in Table 4.

The complements model, however, is supported by the results of Table 4. In the

complements model the negative coefficient on the w variable is predicted. Since

increases in w'' cause a decline in economic activity in the union sector, they also cause

a decrease in economic activity in the nonunion complements sector, hence the decline

in es"'. Similarly the positive sign on ulp, which is an indirect measure of the cost of

union labor, is predicted by the complements model, as is the negative sign on the

representation elections variable.

Overall, the results for the employment share regressions suggest that increases in

union strength are associated with declines in nonunion industry employment. By itself,

this finding is consistent with either the threat model or the complements model, but not

the crowding model. However, only the complements model is consistent with both sets

of findings from the employment and wage regressions. Furthermore, it is reasonable to

expect that production complementarities between union and nonunion labor are weaker

at a more disaggregated level of analysis, since the disaggregation is more likely to sort

the complementary types of labor into different industries. Because of this, we view the

two-digit industry results for the wage and employment regressions as particularly

compelling evidence in favor of the complements model.

Finally, we turn to estimates of equation (3), intended to test directly whether

nonunion industry wage premia are positively related to union threat effects. Table 5

28

reports results at the one- and two-digit level. To summarize the test, the coefficient of

the within-industry union premium should be negative, reflecting movements along the

labor demand curve for union labor. If nonunion industry wage premia are positively

related to threat effects, then the interaction coefficient should be positive, as strong

threat effects diminish the substitutability between union and nonunion workers. A

positive interaction coefficient would also be consistent with the crowding model. On

the other hand, a negative coefficient on the interaction variable would be consistent

with the complements model, indicating that increases in union wages costs coupled with

increases in nonunion wage costs lead to relatively larger declines in union employment.

The estimates in column (1) are consistent with the complements model. The coefficient

of the interaction variable (-.276) is negative and statistically significant. Furthermore,

the coefficient of the within-industry union premium is negative, as expected, and the

negative coefficient of the nonunion industry wage premium is consistent with

complementarity. In column (2) we explore whether the coefficient of the interaction

variable is being identified from cross-industry variation in the responsiveness of union

employment to union wages (i.e., union labor demand elasticities). To do this we add a

set of variables interacting the within-industry union wage premium with a set of

industry dummy variables.25 The signs of the coefficients are unchanged, but the

coefficient on the interaction variable is no longer statistically significant. Columns (3)

Wedefine the nonunion industry wage premium used to construct the interaction variable as deviationsabout its mean. Consequently, the partial derivative of union employment with respect to the within-industry union wage premium, evaluated at the means, is given by the coefficient of the within-industryunion wage premium.

25We define the industry dummy variables relative to their sample means so that the within-industryunion wage premium coefficient still measures the partial derivative, evaluated at the sample means.

29

and (4) repeat this analysis at the two-digit level, with the same results; the signs of the

point estimates are consistent with the complements model, although the evidence is

statistically significant only in column (3).

Overall, the evidence in Table 5 provides additional support for the complements

model; as we suggested earlier, we find the evidence in favor of the complements model

at the two-digit level particularly compelling. Based on these findings, we can more

decisively conclude that the results provide no evidence that nonunion industry wage

premia are correlated with the strength of the union threat within industries.

V. Conclusions

In this paper we investigated the impact of union strength on changes in nonunion

wages and employment. The prevailing model in this area is the threat model, which

predicts that increases in union strength cause increases in nonunion wages and

decreases in nonunion employment. In testing the threat model, we are also testing two

alternatives, the crowding and complements models.

With respect to nonunion industry wage differentials, the statistical experiment

does not ask whether one can explain the 'entire' nonunion industry wage structure with

the union threat effect model, but only asks whether the threat effect model explains

some of the variation in this wage structure over time. The answer appears to be no. In

contrast to the prediction of the threat model, decreases in the percent organized

(reflecting a declining union threat) are associated with increases in the nonunion wage.

Furthermore, increases in union wages appear to decrease, rather than to increase,

nonunion wages. Evidence on the determinants of intra-industry variation in nonunion

30

wage premia is somewhat more consistent with the crowding model and is strikingly

consistent with the complements model of union and nonunion wage determination.

Given that the union threat model does not explain intra-industry variation in nonunion

industry wage premia over time, it seems an unlikely candidate for an explanation of the

cross-sectional variation in nonunion industry wage premia.

Further evidence on the determinants of intra-industry variation in nonunion

employment is consistent with the complements and the threat model; movements in

nonunion industry employment are negatively related to changes in proxies for union

strength.

Thus, the combined evidence supports the complements model, but neither the

threat model nor the crowding model. Evidence from a third test, based on the

responsiveness of union employment to union wage changes (again, within industry),

strengthens this finding, as it is consistent with the complements model, but neither the

threat model nor the crowding model.

In testing the model on a cross-section, time-series data base from 1973-1989, we

are also able to explore how the extraordinary changes in the union sector during this

period have affected the nonunion sector. In the context of the threat model, increases

in the union wage premium in many industries, coupled with sharp declines in union

employment shares, raise the possibility that the strength of the union threat in different

industries varied little over this period. Thus, the threat model is not necessarily

inconsistent with the observed stability of the nonunion industry wage structure over the

31

same period. While our evidence rejects the threat model in favor of the

complements model, it still suggests that union employment shares and union wage

premia have offsetting influences on nonunion wages; but the effects have the opposite

signs from those predicted by the threat model. Thus, it is possible that union sector

developments do influence the nonunion industry wage structure, but these influences

are masked in the 1970s and 1980s because of offsetting trends in the union sector.

"Krueger and Summers (1988) reports correlations around .91 between industry wage differentialsestimated using CPS data in 1974, 1979, and 1984.

32

References

Akerlof, G.A. 1982. "Labor Contracts as Partial Gift Exchange.' Quarterly Journal ofEconomics 91(4): 543-69.

Bell, L.A. 1989. 'Union Concessions in the 1980s." Federal Reserve Bank of New YorkQuarterly Review Summer: 44-58.

Dickens, W.T. 1986. "Wages, Employment and the Threat of Collective Action byWorkers.' Mimeograph, University of California, Berkeley.

Dickens, W.T. and L.F. Katz. 1987a. "Inter-Industry Wage Differences and IndustryCharacteristics." In K. Lang and J.S. Leonard, Eds., Unemployment and the Structure ofLabor Markets (New York, NY: Basil Blackwell), 48-89.

1987b. "Inter-Industry Wage Differences and Theories of Wage Determination."NBER Working Paper No. 2271.

Dickens, W.T. and B.A. Ross. 1984. "Consistent Estimation Using Data from More thanOne Sample." NBER Technical Working Paper No. 33.

Dunlop, John T. 1944. Wage Determination Under Trade Unions (New York, NY:Macmillan).

Freeman, R.B. 1986. 'The Effect of the Union Wage Differential on ManagementOpposition and Union Organizing Success." American Economic Review 76(2): 92-6.

Freeman, R.B. and J.L. Medoff. 1981. 'The Impact of the Percentage Organized onUnion and Nonunion Wages." The Review of Economics and Statistics LXIII(4): 561-72.

Heiwege, J. 1991. "Sectoral Shifts and Interindustry Wage Differentials." Mimeograph,Federal Reserve Board.

Kahn, L.M. 1978. 'The Effect of Unions on the Earnings of Nonunion Workers."Industrial and Labor Relations Review 31(2): 205-16.

1980. "Union Spillover Effects on Organized [sic] Labor Markets." Journal ofHuman Resources 15(1): 87-98.

Krueger, A.B. and L.H. Summers. 1988. "Efficiency Wages and the Inter-Industry WageStructure." Econometrica 56(2): 259-94.

Lindbeck, A. and D.J. Snower. 1988. The Insider-Outsider Theory of Employment andUnemployment (Cambridge, MA: The MIT Press).

Linneman, P.D., M.L. Wachter, and W.H. Carter. 1990. 'Evaluating the Evidence onUnion Employment and Wages." Industrial and Labor Relations Review 44(1): 34-53.

Montgomery, E. 1989. "Employment and Unemployment Effects of Unions." Journal ofLabor Economics 7(2): 170-90.

Neumark, D. "Declining Union Strength and Labor Cost Inflation in the 1980s."Forthcoming in Industrial Relations.

Podgursky, M. 1986. 'Unions, Establishment Size, and Intra-Industry Threat Effects."Industrial and Labor Relations Review 39(2): 277-84.

Rosen, S. 1969. 'Trade Union Power, Threat Effects and the Extent of Organization."Review of Economic Studies 36(2), No. 106: 185-96.

Ross, Arthur M. 1948. Trade Union Wage Policy (Berkeley, CA: University of CaliforniaPress).

Wachter, M.L. and W.H. Carter. 1989. "Norm Shifts in Union Wages: Will 1989 Be aReplay of 1969?" Brookings Papers on Economic Activity 2: 233-64.

up

Figure 1

Union Threat Hypothesis

1. Decrease in Dora (D — V, D — D')

2. Increase in it to e°

3. Decrease In Doss, rep,

increase Is alp

esDecreases Increases (by assiaiptlsn)

Increases Decreases

— 1' Decreases Increases

5sp2 - -

Union Sector Nonunion Sector

Effect

T —.

"UPI

"up

1. Decrease in %org

2. Increase in a' to a'

3. Decrease in %aon

Figure 2

Crowding (Supply) Alternative

—D", C —

C • SM

D' — D', C —

Note: We asstana shifts in C dominate shifts in C, end therefore generalLy do not show the Latter.

"up wnup

'pup

a a

Union Sector

as

Nonunion Sector

CDecreases

Decreases

No change

on

Increases (by asaueptim)

Increases

Increases

4. Decrease in rep, increase in oLp D' —. D', C C' Increases Decreases

Figure 3

Complements (Demand) Alternative

Union Sector Nonunion sector (Comp.) Nonunion Sector (Subet.)

eC1. Decrease in Zere -. V, s — C', increases Increases (by assteçtien)

-. D'

2. Increase In a' to a° D' — D Decreases Decreases

3. Decrease is Deeti V -. D,D D, Increases IncreasesC -. r,D -.4. Decrease In rep, increase In sip D' — D', D -. D Increases Increases

este: We assune that mevee,ents In eases end esçlsytnent of nsrsoion cmp(ee,ent Labor dominate the nsnunisn setter. We assuseshuts In D dominate shifts in C, and therefore do net show the Latter.

coups 'suDs

e ea eJ' es eJ°

Table 1

Summary of Coefficient Predictions from Alternative Models

gions 1 and 2: Nonunion wage (1') Nonunion emolovinent (2')

Threat Model

%org + not included

+

%won +

rep +

ulp +

Crowding Model

%org + not included

+

%won no change

rep +

ulp +

Complements Model

%org not included

—

%won — -rep - -

ulp + +

Eanation 3: Union employment (3')

Threat ModelA -

0 +

Crowding ModelA -

w' x w 0 +

Complements ModelA -

x W" 0

Table 2

Descriptive Statistics by One—Digit Industry

Nonunion Within-industry Nonnioo Union Percent Unfair lar

wage union wage eaploylent eaployzent Percent elentiors Reprenentation practice chargespresiua prealea shares shares organized won by noOns elactiors' against eeployers'

(1) (2) (3) (4) (5) (6) (7) (8)

Construction .00 .36 .05 .03 .35 .49 .05 .09

(.01) (.01) (.001) (.002) (.02) (.01) 1,01) (.01)

Wining .34 .16 .01 .01 .40 .43 .01 .04(.02) (.02) (.0004) (.0005) (.03) (.01) (.001) (.004)

Nanufacturing— .17 .17 .12 .08 .40 .43 .20 .63durable (.01) (.01) (.001) (.01) (.02) (.01) (.02) (.33)

Manufacturing— .12 .15 .09 .04 .33 .42 .13 .37mn—durable (.01) (.02) (.001) (.003) (.01) (.01) (.02) (.02)

t'raosgartation .22 .19 .04 .05 .52 .48 .11 .36cowaunications, and (.02) (.02) (.001) (.002) (.02) (.01) (.01) (.01)piblic utilities

8bolesale trade .15 .15 .05 .01 .13 .42 .06 .13(.01) (.02) (.002) (.0004) (.00) (.01) (.01) (.01)

Retail trade —.06 .29 .13 .02 .12 .41 .10 .25

(.01) (.01) (.01) (.001) (.01) (.01) (.01) (01)

Finance, insurance, .12 .05 .07 .003 .05 .53 .02 .03and real estate (.02) (.03) (.003) (.0001) (.002) (.02) (.001) (.003)

Services ... .14 .17 .03 .16 .54 .17 .39(.01) (.004) (.001) (.004) (.01) (.01) (.02)

Table 2 (continued)

thanoen

10000ion itbin-indostry Ronunion Union Percent Unfair 1ar

sage union sage eaployaent eaploysent Percent electiose Representation practice charges

preai presini share shar? organizeS son by unions elections' against eiployero'

(1) (2) (3) (4) (5) (6) (7) (8)

I:Cnnstruction .005 —.001 .001 —.001 —.012 .002 .007 .005

(.006) (.010) (.011) (.001) (.009) (.014) (.005) (.007)

1ining .012 —.004 .0002 —.0002 —.021 —.012 —.0002 .004

(.031) (.037) (.0003) (.0003) (.011) (.020) (.001) (.003)

Xanufactoriog— .003 .003 —.0000] —.005 —.014 —.005 —.016 —.002

durable (.012) (.022) (.002) (.003) (.005) (.005) (.009) (.020)

Oannfacturing— .00] .001 —.00005 —.002 —.011 —.003 —.010 —.0001

non—durable (.013) (.025) (.001) (.001) (.005) (.009) (.006) (.014)

Transgartatioo, .001 .003 .001 —.001 —.012 —.007 —.00] .005

onuoicatiorw, and (.019) (.027) (.001) (.001) (.009) (.009) (.005) (.009)

piblic utilities

holesa1e trade .002 .003 .001 —.0002 —.006 —.009 —.004 .00]

(.018) (.031) (.001) (.0001) (.005) (.013) (.004) (.007)

Retail trade .0003 .004 .003 —.001 —.006 —.006 —.007 —.002

(.007) (.014) (.002) (.0004) (.003) (.009) (.003) (.007)

Finance, inscrance, .005 —.002 .001 —.00003 —.001 .000 —.0007 .001

and real estate (.021) (.058) (.004) (.002) (.002) (.019) (.001) .002)

Services .,. .003 .003 .000] -.001 -.002 -.0003 .014

(.017) (.003) (.001) (.004) (.020) (.009) (.011)

1. 1leaos are reportad, with standard errors is parentheses.

2. Share of total eaplnysent.3. The representation elections variable is the nuiber of cases receiveS in the fiscal year stealing fros petitions fileS by a laher organizatiow or

esployee seeking an election for detaraioatinn of a collective bargaining representative. The ousber of elections is divideS by 10000, The unfairlaher practice variable is the nuaber of charges fileS by labar organizations or eaployee5 against esployers. the nuaber of charges is divideS by

10,000.

Table 3

Nonunion Wage Regressions, 1973—1989, Weighted Least SquaresDependent Variable: Nonunion Industry Wage Premium1

One-Dinit Results Two-Digit Results(1) (2) (3) (4) (5) (6) (7) (8) (9) (10)

Percent organized —.273 —.328 —.248 —.327 —.236 -.107 ... —.106

(.040) (.046) (.038) (.048) (.039) (.023) (.019)

Percentage of —.034 .011 .019 .014

elections eon (.039) (.035) (.031) (.040) (.032)by unions

Number of -.126 .004 .104 -.024

representation (.063) (.055) (.052) (.069) (.057)

elections/10,000

Unfair labor 045 .079 .046 .077

practice cbarges (.044) (.040) (.035) (.044) (.035)

against employers

/10,000

Within—industry —.452 -.476 —.404 ... —.411 ... —.377 -.376union premium (.052) (.051) (.046) (.046) (.029) (.028)

SN? sbare2 -.044 —.558

(.569) (.454)

.964 .965 .969 .971 .978 .965 .978 .938 .953 .956

1. Standard errors are reported in parentheses. There are 144 observations for tbe one-digit aoalysin, and480 observations for tbe two—digit analysis. Industry dummy variables are included. Observations areeeigbted by number of sbservations for year from ebicb micro—level coefficients were estimated. The within-industry union and nonunion pre.iums are estimated from log wage regressions using the outgoing rototiongroup annual files of the CPS for 1983—1989, and tbe Nay files for 1973-1981. Regressiuns care estimatedseparately by race esd ses, omitting government workers, managers esd prufessinoals, and tochsical workers.The premiums were then calculated es weigbted averages of the premiums estimated from the separate wageregressions. Other variables included in tbe individual—level wage regressions were: one—digit industrydummy variables (construction, mining, durable manufacturing, nondurable manufacturing, transportation,finance, insurance and real estate, retail trade, wbolesale trade, and services); nine one—digit occupationdummy variables (with a bridge between the 1970 and 1980 SOC codes); linear and guadratic schooling; linearand guadratic potential esperience; dummy variables for four regions; the NSA unemployment rate; and dummyvariables for three NSA sizes; and dummy variables for married, spouse present, overtime (based on anualbourn worked).2. Thin is the residual from a regression estimated for eacb industry of the SN? share of output produced bythe industry on an intercept, the aggregate civilian unemployment rate, and a post—1976 dummy variable tocapture the cbange in accounting methods used is the numbers reported in the Surveo of Current Resiness.

Table 4

Nonunion Employment Share Regressions, 1973—1989,Weighted Least Squares

Dependent Variable: Nonunion IndustryEmployment/Total Employment'

00e-Dioit Results No-Digit Results(1) (2) (3) (4) (5)

Within—industry —.033 ... —.046 —.040 — .000

union premium (.017) (.016) (.015) (.006)

Percentage of 010 .019 .011

elections woo (.011) (.011) (.010)

by unions

Nurberof ... —.082 —.090 —.057

representation (.017) (.017) (.016)elections/l0,000

Onfuir labor ... .017 .022 .022

practice charges (.013) (.013) (.011)against employers/10,000

asP share2 823

(.143)

.979 .982 .983 .986 .953

1. Standard errors are reported in parentheses. There are 144 observations f or the one—digit analysis, and 480 observations for the two-digit analysis. Industry dummy vuriableaare included. Observations are weighted by number of observations for year from whichmicro—level coefficients were estimated. See footnotes to Table 3 f or rare details.

Table 5

Employment Share Response Regressions, 1973—1989,Weighted Least Squares

Dependent Variable: Union Share of Total E]nployment

Within—industryunion wage premium (wa')

Nonunion industrywage premium (w)

Within—industryunion wage premium (w°)x nonunionindustry wagepremium (w)'

Includes industry dummyx within—industryunion wage premiuminteractions

R'

One—Digit Results

(1)

—.078(.025)

—.084(.036)

—.276(.135)

(2)

— .022(.071)-.095(.052)

—.186(.185)

Two—Digit Results

(3) (4)

—.007 .002(.003) (.017)

—.011 —.010(.004) (.005)—.039 —.030(.015) (.024)

No Yes

.805 .817

No Yes

.872 .874

1. Standard errors are reported in parentheses. industry danny variables are included. There are 144 observations for theone—digit analysis, and 400 observations for the two—digit analysis. Observations are weighted by saber of observations foryear fro. abich iicrs—level coefficients were estijated. See footnotes to Table 3 for lore details.2. This is included as deviations about its lean, no that the coefficient of the within-industry union wage preniun neasuresthe partial derivative of the eiploynent share variable with respect to the within-industry union preniuw, evaluated at theleans.