Embed Size (px)

Citation preview

NBAA AND BOT JOINT SEMINAR ON ACCOUNTING, FINANCIAL MARKETS AND GOVERNANCE ISSUES AT AICC-

ARUSHA

EFFICIENT MARKET HYPOTHESIS (EMH): IS IT A THEORY IN DEVELOPING COUNTRIES

CPA GODFREY MALEKANO

CAPITAL MARKETS• Capital markets are important institutions that enables

– Financial instruments to be traded, – Provide choice to investors- investors to choose where, when and how to channel

their investment. – Enable corporates to raise capital

• The institution is an organized market that converts companies’ assets into financial instruments known as security which can be in the form of – stocks, – bonds, – options and futures.

• Capital markets– price discovery, cost reduction and risk management• One important step for a company instrument to be traded at the exchanges is

that it has to be listed. • Capital market plays important role in strengthening the relationship between

investors and the companies whose assets are traded by helping in: – mobilizing the savings of people and channeling them to the growth of

trade, commerce and industrial sectors of an economy.• For the past decade Capital markets in most developing countries have

experienced significant positive developments as reflected in market capitalization, liquidity, turnover and increase in value of stock prices.

Stock Markets in the continent• The African market is not an exception to the current reforms and

development in global stock market exchanges. • Over the last three decades, there has been a substantial increase in the

number of stock markets in Africa. • With only 8 active stock markets in 1980s, the number of stock markets in

Africa increased to 29 by the end of 2016. • Proposals to open new stock markets in Congo D.R., Burundi, Equatorial

Guinea, Ethiopia, the Gambia, Lesotho, Madagascar, Mauritania and Sierra Leone

• Eight stock exchanges has remained very active in African stock market including the– Johannesburg Stock Exchange (SouthAfrica, 1887), – the Cairo and Alexander Stock Exchange (Egypt, 1888), – the Zimbabwean Stock Exchange (Zimbabwe, 1896), – the Casablanca Stock Exchange (Morocco, 1929), – the Nairobi Stock Exchange (Kenya,1954), – the Nigerian Stock Exchange (Nigeria, 1960), and – the Tunisian Stock Exchange (Tunisia, 1969).

• The ratio of active to total stock exchanges in Africa is about 28% indicating that African stock market is current inactive.

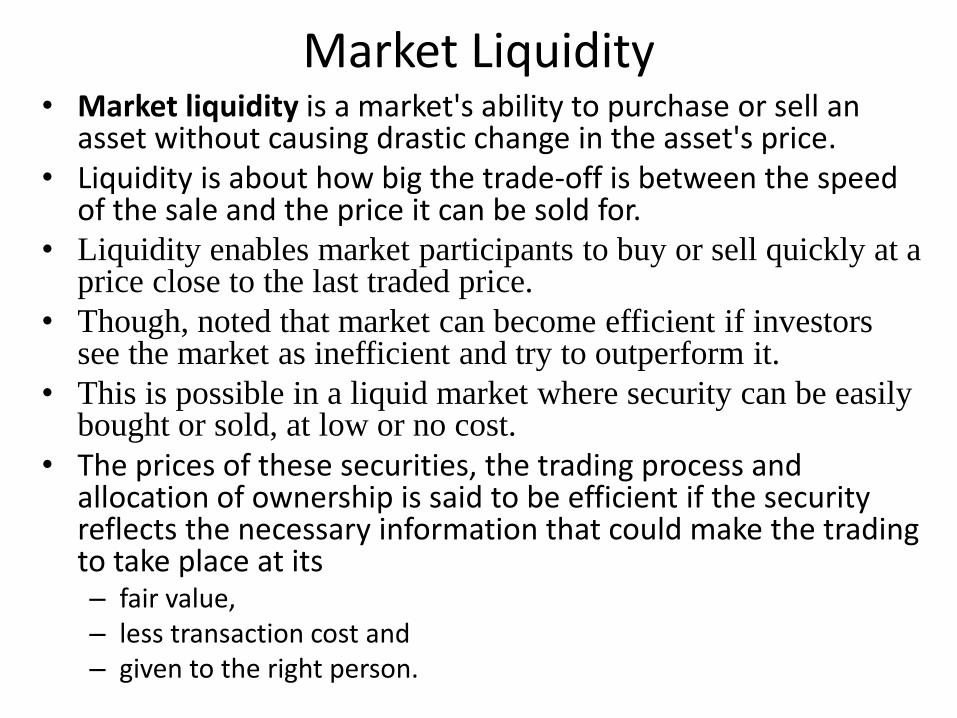

Market Liquidity• Market liquidity is a market's ability to purchase or sell an

asset without causing drastic change in the asset's price.• Liquidity is about how big the trade-off is between the speed

of the sale and the price it can be sold for.• Liquidity enables market participants to buy or sell quickly at a

price close to the last traded price.

• Though, noted that market can become efficient if investors see the market as inefficient and try to outperform it.

• This is possible in a liquid market where security can be easily bought or sold, at low or no cost.

• The prices of these securities, the trading process and allocation of ownership is said to be efficient if the security reflects the necessary information that could make the trading to take place at its – fair value, – less transaction cost and – given to the right person.

Efficient-market hypothesis (EMH)• Efficient-market hypothesis (EMH) is a theory in financial economics

that states that an asset's prices fully reflect all available information. • A direct implication is that it is impossible to "beat the market"

consistently on a risk-adjusted basis since market prices should only react to new information or changes in discount rates (the latter may be predictable or unpredictable).

• The EMH was developed by Professor Eugene Fama who argued that stocks always trade at their fair value, making it impossible for investors to either purchase undervalued stocks or sell stocks at inflated prices.

• It is impossible to outperform the overall market through expert stock – selection or market timing, – the only way an investor can possibly obtain higher returns is by chance or

by purchasing riskier investments.

• His 2012 study with Kenneth French confirmed this view, showing that – the distribution of abnormal returns of US mutual funds is very similar to

what would be expected if no fund managers had any skill—a necessary condition for the EMH to hold.

Stock Market Efficiency• The stock market efficiency is one of the major

and all-important concept for – understanding the workings of capital markets, – their performance and – role in the development of a country’s economy

• A stock market is defined as efficient if its prices – fully reflect all available information.

• In such an efficient market, prices represent the intrinsic values of the stocks and – scarce savings are automatically allocated to

productive investments in a way that benefits both investors and the economy.

Stock Market Efficiency• A stock market is said to be efficient if it fully and

correctly reflects all relevant information indetermining security prices.

• The market is said to be efficient with respect to some information set…

– if security price would be unaffected by revealing that information to all participants.

• Moreover, efficiency with respect to an informational set …

– implies that it is impossible to make economic profits by trading on the basis of (that informational set).

Stock Market Efficiency• Stock market efficiency goes beyond the mere understanding of the

structural relationship between risk and expected return to include the precision with which the market information reflect in its prices.

• The key issues are: – when new information unveils about a particular company, – how quickly do the prices of that company’s share adjust to reflect the

new information?• When the prices respond to and reflect all relevant new information in a

rapid fashion,– we can say that the market is relatively efficient.

• On the other hand, when, the information disseminates– rather slowly throughout the market, and– when investors allow time lags in analyzing the information and reacting to it,

or possibly overreacting to it,

– stock values at the market may depart from intrinsic values of the stock.

• The time it takes for the analyses of such information and the attitude of investors are key elements of an inefficient market.

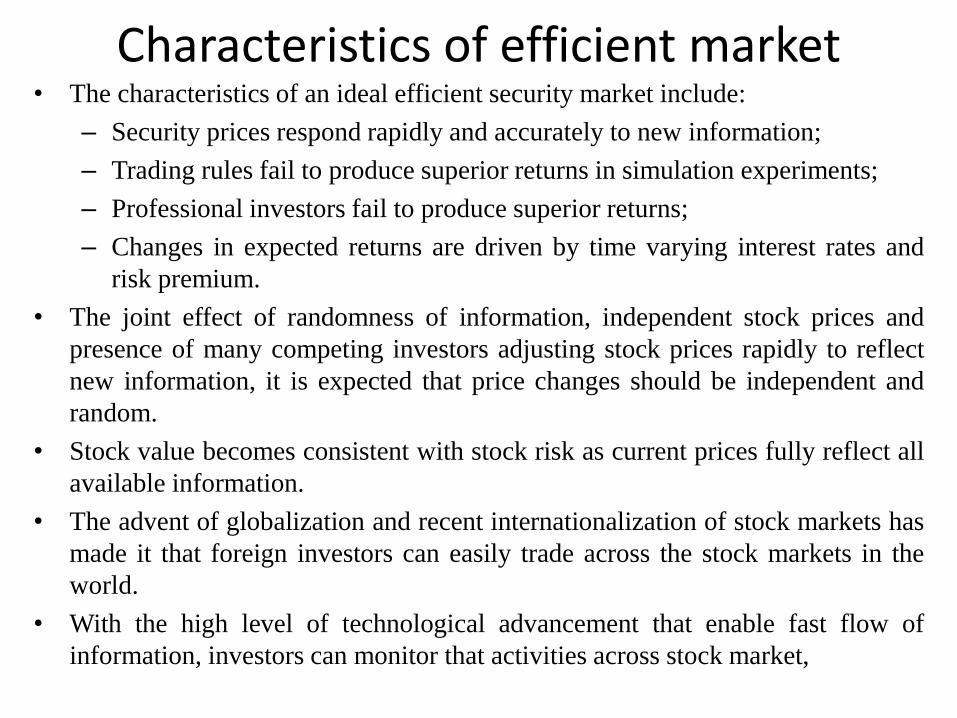

Characteristics of efficient market• The characteristics of an ideal efficient security market include:

– Security prices respond rapidly and accurately to new information;

– Trading rules fail to produce superior returns in simulation experiments;

– Professional investors fail to produce superior returns;

– Changes in expected returns are driven by time varying interest rates and

risk premium.

• The joint effect of randomness of information, independent stock prices and

presence of many competing investors adjusting stock prices rapidly to reflect

new information, it is expected that price changes should be independent and

random.

• Stock value becomes consistent with stock risk as current prices fully reflect all

available information.

• The advent of globalization and recent internationalization of stock markets has

made it that foreign investors can easily trade across the stock markets in the

world.

• With the high level of technological advancement that enable fast flow of

information, investors can monitor that activities across stock market,

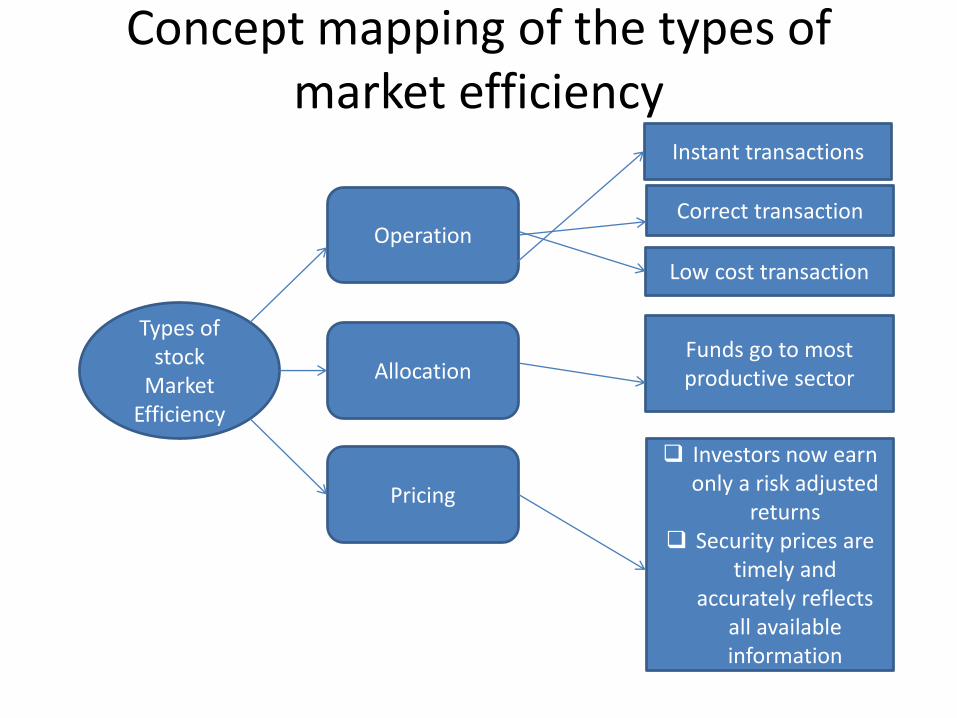

Types of Capital Market Efficiency• The following three types of market efficiency defines the criteria for

stock market efficiency – operational, – allocation and– pricing efficiency

• Operational efficiency implies that all transactions in securities are carried out – instantly, correctly, and at a low cost. – Operational efficiency may be promoted through enhancing competition

between exchanges for secondary market transaction.

• The allocation efficiency refers to mechanism which allocates scarce resources to where they can be most productive.– The highest bidders is allowed to have the investment opportunity which

implies that most efficient use of scarce resource is ensured in the economy.

• Pricing efficiency connotes that an investor can only expect to earn risk adjusted returns from an investment as – prices move instantaneous and in an unbiased manner to any news.

Concept mapping of the types of market efficiency

Types of stock

Market Efficiency

Operation

Pricing

Allocation

Instant transactions

Correct transaction

Low cost transaction

Funds go to most productive sector

Investors now earn only a risk adjusted

returns Security prices are

timely and accurately reflects

all available information

Concept of Capital Market Efficiency• Capital market is efficient if security prices are timely and accurately

reflects all available information about the current and future likely worth

of assets.

– is such that the ability of securities to reflect and incorporate relevant

information, almost instantaneously, in their prices.

• This implies efficient in processing information that related to the stock that

is being priced.

• In this scenario, as the stock and bond markets are perfectly efficient and

current prices fully reflect all available information,

– both the buyers and sellers cannot take undue advantage of information

to make abnormal profits from the market.

• Incase of inefficiency, stock prices do not possess all available information

in the market and as such

– financial analyst can earn above normal return from stocks by using

previous stock prices to predict the pattern of future price changes and

future stock return.

FORMS OF STOCK MARKET EFFICIENCYWeak-form efficiency: the information set includes only the

history of prices or returns themselves.

if it fully incorporate the information in past stock prices.

Semi strong-form efficiency: the information set includes allinformation known to all market participants (publicly availableinformation).

prices reflect all publicly available information.

Strong-form efficiency: the information set includes allinformation known to any market participant (privateinformation).

Anything that is pertinent to the value of the stock and that isknown to at least one investor is, in fact fully incorporated intothe stock value.

Weak Form Efficiency• Weak form efficiency, also known as the random walk theory, states that

future securities' prices are random and not influenced by past events. • Weak form efficiency assume that all current information is reflected in stock

prices and past information has no relationship with current market prices.• Past earnings growth does not predict current or future earnings growth.• The main tenet of weak form efficiency is the randomness of stock prices

makes it impossible to find price patterns and take advantage of price movements.

• Daily stock price movements are completely independent of each other, and it is assumed price momentum does not exist.

• Markets that are weak form efficient do not follow patterns.– If, for example, a trader sees a stock continuously decline on Mondays and

increase in value on Fridays, he may assume he can profit if he buys the stock at the beginning of the week and sells at the end of the week.

– If, however, the price declines on Monday but does not increase on Friday, the market can be considered weak form efficient

• The test for weak form market efficiency usually involved testing for linear serial dependence between successive prices to establish if the price process follows a random walk.

semi-strong efficiency• The semi-strong efficiency is the level of efficiency which assumes that all

publicly available information about a given security has been accuratelyfactored into the present price of that security.

• looked at semi-strong efficiency as a situation where the security pricesreflect not only past information but all other published information.

• This form is concerned with both the speed and accuracy of the market’sreaction to information as it becomes available.

– GBP 305- GBP 265.90 GBP 39.10 12.82% GBP 433- GBP 265.9 40%

• Event studies that examine how stock prices adjust to specific significanteconomic events have been used to directly test semi-strong form efficiency.

• Events normally tested are stock splits, initial public offerings (IPO), companyannouncements (especially earnings and dividend announcements) and otherunexpected economic and other world events.

• The semi strong form of market efficiency deduces that the share pricesreflect all available information both publicly and privately existing.

• Various other methods have been employed to test the semi-strong efficiency.

Strong Form Efficiency• The strong-form efficiency is a situation where the security prices

reflect not only public information

– but all information that can be acquired by painstaking analysis of the company and the security.

• According to the strong-form efficiency, the security prices reflect all

– published and unpublished, public and private information.

• It seems to be more concerned with the disclosure efficiency of the information market than the pricing efficiency of the securities market.

• Tests for the strong form efficiency are mainly centred on finding whether any group of investors,

– especially those who can have access to information otherwise not publicly available, can consistently enjoy abnormal returns.

• This implies that no one, having private or public information can out-beat the market, because the market automatically anticipates in an unbiased manner the stock prices and incorporates the effect of all these information on the share prices

FORMS OF STOCK MARKET EFFICIENCY• diagramWeak form

Security prices reflect all the past information

Fundamental analyses can not predict future

security prices Semi – strong All publicly available

information are reflected in the present price of

securities Event studies…………… Stock splits, IPO coy

announcement etc

Strong-form Security prices reflect all

published and unpublished, public and

private information

Empirical Studies• Evidences from empirical studies further showed that

– economic conditions, – reforms and – nature of data can influence the efficiency of the markets.

• For instance some studies posited that this weak form efficiency of themarket was under the linear framework,– whereas when nonlinearity is accounted for, a majority of the indices becomes

weak form inefficient.

• Further to the influence of trend of data, the efficiency of the market has been influenced by various factors including – financial reforms, – economic/financial crisis, – the nature of data used (daily, weekly, monthly or yearly returns) and – time variants issues wherein some periods could experience market efficiency

while other years would not.

• Depending on the data used (daily, weekly, monthly or yearly returns) and time variants issues wherein some periods could experience market efficiency while other years would not.

Empirical Studies in Africa• Ten (10) empirical works involving Nigeria, four (4) supported that Nigerian

capital market is weak form efficient while six (6) posited weak form inefficiency.

• Most of the studies show that African stock market are largely weak form inefficient

• However, some studies indicated that Namibia and Nairobi were found to have weak form efficient stock markets.

• Simons and Laryea (2005) employ various tests to examine the weak form of the efficient market hypothesis for four African stock markets – Ghana, Mauritius, Egypt and South Africa. the south African Stock returns is independent and follow a random walk, hence, is weak form efficient, whereas the others are inefficient.

Largely weak form of efficient

Zimbabwe Tunisia

Mauritius, Botswana

Kenya, West African Regional Stock Exchange

Ghana Morocco

Egypt

Empirical Studies in Africa….2• study investigates the weak form efficient market

hypothesis (EMH) for five generalized stock indices in the Johannesburg Stock Exchange (JSE) using weekly data collected from 31st January 2000 to 16thDecember 2014.

• In particular, the test for weak form market efficiency using a battery of linear and nonlinear unit root testing procedures comprising of– The classical augmented Dickey-Fuller (ADF) tests; – the two-regime threshold autoregressive;– (tar) unit root tests described in Enders and Granger (1998); – three-regime unit root tests described in Bec, Salem, and

Carrasco (2004).

• These results bridge two opposing contentions obtained from previous studies by concluding that – under a linear framework the JSE stock indices offer support in

favour of weak form market efficiency – whereas when nonlinearity is accounted for, a majority of the

indices violate the weak form EMH.

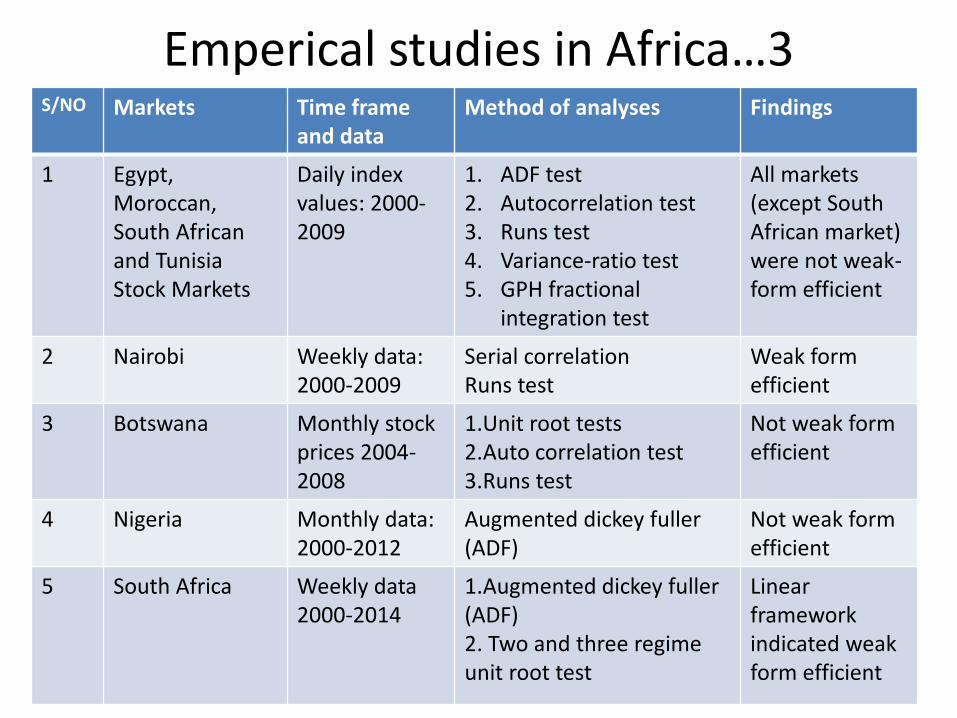

Emperical studies in Africa…3

• table

S/NO Markets Time frame and data

Method of analyses Findings

1 Egypt, Moroccan,South African and Tunisia Stock Markets

Daily index values: 2000-2009

1. ADF test2. Autocorrelation test3. Runs test4. Variance-ratio test5. GPH fractional

integration test

All markets (except South African market) were not weak-form efficient

2 Nairobi Weekly data:2000-2009

Serial correlationRuns test

Weak form efficient

3 Botswana Monthly stock prices 2004-2008

1.Unit root tests2.Auto correlation test3.Runs test

Not weak form efficient

4 Nigeria Monthly data: 2000-2012

Augmented dickey fuller (ADF)

Not weak form efficient

5 South Africa Weekly data 2000-2014

1.Augmented dickey fuller (ADF)2. Two and three regime unit root test

Linearframework indicated weak form efficient

Emperical studies in Asia…1• Saudi stock market was examined by applying a -tatistical

test (ADF and PP unit root tests and the stationarity test of KPSS) on individual, sectoral price indices, and the aggregate price index over period from March 1st 2003 to June 30th, 2006. – The results revealed that the Saudi stock market is inefficiency.

• Abdmoulah (2010) examined the weak form efficiency of 11 of Arab stock markets (include Saudi Arabia) using GARCH-M (1,1) approach along with state-space time-varying parameters. – The results showed that the 11 stock markets are not weak

form efficiency.

• Mishra et al (2009) employed the unit root tests to examine the efficiency of Indian stock market in the context of global financial crisis – concluded that there is evidence of weak-form market

inefficiency in India.

Emperical studies Asia…2

• Maghyereh (2003) examined the validity of the random walk model for Amman (Jordan) stock exchange using aggergate daily data. The result showed that the behaviourof the Amman stock exchange is inconsistent with the random walk model, so that, – the Amman stock exchange is inefficient.

• Moustafa (2004) examined the UAE stock market using daily prices of 43 stocks included in the Emirates market index. He employ the nonparametric run to test for randomness when the returns of sample stocks do not follow the normal distribution.– The results show that the returns of 40 stocks out of the 43 are

random at a 5% level of significance. Therefore, the empirical result confirmed the weak-form of EMH

The implications of inefficiency: The perception that prices do not fully reflect some information can lead the

investors to adopt portfolio strategies designed to reap abnormal profits by exploiting the informational inefficiency.

Investors may be unwilling to trade in securities if it is felt that the information is possessed by others.

They might leave the market to invest elsewhere, or they might reduce the total amount invested.

The information intermediaries will make profits, because of a big demand for information, as the information is not reflected in prices as it should be.

Companies should not expect to receive the fair value for securities they sell (price will not always reflect the present value for securities they issue).

There even might exist the opportunity to “fool” investors.

unguarded market manipulations- stock market could suffer inflated stockprices, speculation, and insider trading. This notion can have negative effect on investor confidence.

The results have negative policy implications for investment in developing countries because the efficiency of a market in processing information affects its allocation capacity, and therefore its contribution to economic growth.

Efficiency of the capital market is one important factor that spurs the development of the stock market.

Conclusion..1 • Most of developing countries stock markets are not

informational efficient. i.e. are largely weak

inefficient

• Inefficient stock market implies that stock prices are

consistent mispriced and hence prone to arbitraging

• capital market is not weak-form efficient, and the

most important causes is the low number of investors

and instruments on the markets.

• Private information exploited by insiders is highly

likely to yield abnormal returns on the stock market

and hence damage the integrity of the market

Conclusion….2• There is the need for a greater development of the developing countries

stock markets through appropriate policies which would enhance the

informational efficiency of the market;

• promoting timely disclosure and dissemination of information to

investors on the performance of listed companies;

• strengthening regulatory oversight are key elements of a strategy aimed

at improving the efficiency of the capital market as this would prevent

any stock price bubble, abnormal financial activities and other market

abuses;

• Capital market regulators should ensure that

– information provided in the market are correct and timely;

– laws to protect investors and guard against manipulation of information in

the capital market should be promulgated and enforced.

• Market operators culpable for insider trading offences should be

punished;

Conclusion….3

• At the moment when most of the market indeveloping countries are largely weak forminefficient one may conclude that it is a theory.

• However, given the level of speed of marketsgrowth in developing countries, it may notcontinue to be a theory in a near future as somemarkets have already started to demonstrate weakform efficient which is a good step in havingefficient market.

• EMH is an important tool to assess marketefficient hence it can not be ignored.