Embed Size (px)

Citation preview

Guide to the FHA Basics

Navigating your way to FHA success !!Rev. 6/13/2016

FHA Basics• FHA insures the loan for an insurance fee (referred to as UFMIP) which is collected at loan closing.

UFMIP can be paid in cash or financed. Upfront and monthly mortgage insurance required on all loans. Any unearned premium may be refunded if borrower refinances to another FHA insured mortgage within the first three years.

• Can be used for Purchases, Rate and Term and Cash Out Refinances• Available for 1-4 unit primary residences, FHA approved Condos and PUDs• Borrower must invest a minimum of 3.5% on a purchase of the lesser of the purchase price or

appraised value• No second homes or investment properties• The lower of purchase price or appraised value is used to calculate the maximum mortgage amount.

Maximum LTV is 96.5% on a purchase, 97.75% on a rate/term refinance if the borrower has occupied for at least 12 months (85% if borrower occupied less than 12 months) and 85% on a cash out refinance. This is what is referred to as the base loan amount. Base loan amount is limited by county

• Any closing costs including origination fee, discount points, UFMIP, buydown cost and prepaid items may be paid by the seller. However, the amount paid by the seller is limited to 6.0% of the sales price of the property. Any amount in excess of 6.0% must be deducted from the sale price in arriving at the maximum mortgage amount.

• FHA late charge is 4%.• PITI reserves - No reserves required on 1 & 2 family properties. 3 months reserves are required on 3

& 4 unit properties. Reserves may come from a gift with AUS approval. On a manual underwrite, this must be from borrowers own funds. 3 & 4 units must also be self-sufficient.

FHA Advantages

• All gift fund down payments

• Up to 6% seller contributions allowed at all LTV’s

• Shorter seasoning on major derogatory accounts

• Very competitive rates!

• Shorter self employment timeframes allowed

• More lenient credit score and credit history requirements. MMC also has special programs for credit scores as low as 600.

Loan PurposePurchaseRate/Term Refinance

• Loan must be current• New loan may include any accrued late charges/escrow shortages• Any cash back to the borrower may not exceed $500• Payoff of a seasoned non-purchase money subordinate lien allowed as r/t

Cash Out Refinances:• The maximum insurable mortgage is calculated based on 85% of the appraised value.

Borrower must have resided in the property for the past 12 months . Inheritated properties are the only exception.

Streamlined Refinance (*please see additional guidelines)• Rate cannot exceed existing rate an the new PITI plus MIP cannot exceed the

existing by more than $50• Evidence that borrower is currently employed (Paystub and verbal required)• Loan must be current (No 30 day lates. From the day of case assignment, must be

with current servicer for at least 6 months and 6 months must have passed since first payment date and 210 days must have passed since the closing)

• Cash back not to exceed $250

Target Borrowers

• Borrowers with limited traditional credit history

•Multi-family borrowers

•Borrowers with a higher DTI

•Borrowers with lower credit scores•Borrowers needing shorter seasoning periods for major derogatory credit

•Limited cash available for down payment

Eligible Borrowers

• US Citizens and Permanent Resident Aliens

• Non-Permanent Resident Aliens who have valid EADs

• Non-Occupant Co-borrowers (limited to 75% LTV unless a blood relative. Must be a single family residence only. Not allowed on cash out refinances)

Max Loan Amounts

• FHA maximum loans amounts are determined by County.

• https://entp.hud.gov/idapp/html/hicostlook.cfm

• When calculating the maximum mortgage amount, please use the Calculating the Maximum Loan Amount Worksheet

• Base loan amount only is subject to the county limit

Upfront MIP and the Refund

*Note The total mortgage can exceed the statutory limit by the amount of the UFMIP

Refunds/Refinance Transactions

• FHA to FHA Refinances (non-streamline)– On any refinance where the MIP refund exceeds the new UFMIP (based on 1.75%), HUD will refund the overage directly to the borrower. The lesser of the MIP refund or the new UFMIP (based on 1.75%) should be subtracted from the unpaid principal balance before calculating the new mortgage amount. Use the purchase transactions charts above to determine the annual premium.

• Non-FHA to FHA Refinances – Use the purchase transaction charts above to determine the UFMIP and annual premium.

Identity of InterestAn identity-of-interest transaction is a transaction between family members, business partners or other business affiliates. The max LTV is 85%. The max LTV may be exceeded under the following circumstances:• A family member purchasing another family member’s principal

residence.• An employee of a builder purchasing one of the builder’s new

homes or models as a principal residence.• A current tenant purchasing the property that he or she has rented

for at least six months predating the sales contract. A lease or other written evidence must be submitted verifying occupancy.

• Sales by corporations that transfer employees out of an area, purchase the transferred employee’s home and then resell to another employee.

Ratios• Ratios are used to determine whether the borrower can reasonably be

expected to meet the expenses involved in homeownership. • Ratios will be determined by LP or DU. When a manual underwrite is

required, the ratio restrictions are limited to the following:• Housing Expense Ratio: 31% • A ratio exceeding 31% may be presented. Typically, for borrowers with

limited recurring expense, greater latitude is permissible on this ratio than the total DTI ratio described below.

• Debt to Income Ratio: 43%• A ratio exceeding 43% on a manual underwrite may be acceptable if

significant compensating factors are presented. (see next slide)• Whenever ratios are exceeded, the lender must explain its’ rationale

for approving the mortgage. The lender is responsible for explaining why it believes the mortgage is an acceptable risk.

• MMC will not exceed 55% DTI with AUS approval.

Compensating Factors• Compensating factors may be used in justifying approval of mortgages with

ratios exceeding the guidelines above. These compensating factors include: • Successfully demonstrating the ability to pay housing expenses equal to or

greater than the proposed monthly housing expense.• A large down payment toward the purchase of the property (at least 10%)• Demonstrating a conservative attitude toward the use of credit and an

ability to accumulate savings• Strong previous credit history• The borrower receives compensation or income not reflected in effective

income, but directly affecting the ability to pay the mortgage (including food stamps and similar public benefits)

• There is only a small increase (10% or less) in the borrower’s housing expense;

• At least 3 mos reserves• Increased earning potential, as indicated by job training or education in

the borrower’s profession• Household income not used for qualifying

Credit History• Past credit performance serves as the most useful guide in determining a borrower's attitude toward credit

obligations and predicting a borrower's future actions. • When looking at a borrower's credit history, the overall credit pattern is examined. A period of financial difficulty in

the past does not necessarily make the risk unacceptable if the borrower has shown a good credit history since the difficulty.

• When derogatory accounts are present, we as the lender must determine that the derogatory information was not due to disregard for financial obligations or an inability to manage debt.

• Neither the lack of credit history nor the borrower's decision not to use credit may not be used as a basis for rejecting a loan. A credit history must be developed from non-traditional sources. Examples of non-traditional sources are housing, utilities, telephone service, cable, insurance payments, child care, school tuition, payments to local stores

• When reviewing the borrower's credit and credit report, particular attention is paid to the following:Previous Rental Or Mortgage Payment History • A 12 month housing history must be verified through either the credit report, a VOR directly from the landlord or

verification of mortgage from the mortgage servicer. 12 months cancelled checks are also acceptable. Rental housing payment history only required on a manual underwrite.

Recent and/or Undisclosed Debts.• The borrower must provide a satisfactory explanation for any significant debt that is shown on the credit report but

not listed on the loan application. The borrower must explain in writing all inquiries shown on the credit report in the last 90 days.

Collections and Judgments• Court-ordered judgments must be paid off. An exception may be made if the borrower has agreed with the creditor to

make regular payments on the judgment and documentation is provided. FHA does not require that collection accounts be paid off as a condition of mortgage approval. However, collections and judgments indicate a borrower's regard for credit and must be considered by the underwriter. The borrower must explain in writing all collections and judgments. Collections exceeding $2,000 (excluding medical) if not paid off or in a payment arrangment must be included in the borrowers liabilities/DTI at a rate of 5% of the cumulative balance.

Major derogatory creditPrevious Mortgage Foreclosure• A borrower who has had a foreclosure or deed-in-lieu within the past 3 years is generally

not eligible. However, if the foreclosure was due to extenuating circumstances and the borrower has reestablished good credit since the foreclosure, an exception may be granted. Extenuating circumstances include serious illness or death of a wage earner. Extenuating circumstances must be fully explained. MMC requires that at least 3 years have passed since the foreclosure.

Bankruptcy• A Chapter 7 bankruptcy must be discharged for at least 2 years. Reestablished credit

since the discharged must be demonstrated. A period or less than 2 years but not less than 1 year may be acceptable if the borrower can show that the bankruptcy was caused by extenuating circumstance and has since demonstrated a good credit history. Borrowers who have had a Chapter 13 bankruptcy must document that one year of satisfactory payments have been made and permission from the court has been given to obtain mortgage financing. MMC requires that a BK be discharged at least 2 years prior to application.

Consumer Credit Counseling Payment Plans• Documentation of satisfactory payments for at least 1 year is required and permission

from the counseling agency must be given to obtain mortgage financing.Dates used are based on case # assignment date

Self Employed Borrowers

Income from self employment is considered stable and effective, if the borrower has been self employed for two or more years. Due to the high probability of failure during the first few years of a business, the requirements described in the table below are necessary for borrowers who have been self employed for less than two years

AssetsGift Funds• A gift of the cash investment is acceptable if the donor is a relative of the borrower; the borrower’s

employer or labor union; a charitable organization; a governmental agency or public entity, that has a program to provide homeownership assistance or a close friend with a clearly defined and documented interest in the borrower.

• The file must contain a gift letter, signed by the donor and the borrower. Documentation showing the transfer of the gift funds is required.

• If the gift funds are in the home-buyer’s account a copy of the cancelled check or other withdrawal document is required

• If the gift funds are to be provided at closing, a bank statement showing the withdrawal from the donor’s account and documentation showing the transfer of the gift fund is a required.

• HUD allows the entire cash investment to be in the form of a gift from a charitable organization List of Organizations described in Section 170(c) of the Internal Revenue Code of 1986 which contains a list of eligible organizations. HUD has developed a web site that provides a list of down payment assistance providers that have had their tax-exempt status removed. This may be accessed at: www.hud.gov/offices/hsg/sfh/np/irstatus.cfm

Seller Contributions• The seller (or other interested third parties such as real estate agents, builders, developers, etc., or a

combination of parties) may contribute up to 6% the sales price toward closing costs, prepaids and discount points. Contributions exceeding 6% of the sales price or exceeding the actual cost of prepaids or discounts points will be treated as inducements to purchase, thereby reducing the amount of the mortgage.

PropertyEligible Properties:• 1-4 unit properties• PUDS• HUD Approved Condos Condominiums• Condos must be FHA approved. To find out if a

Condominium Project has been approved for FHA financing, you may either look it up on The FHA Connection or via the Internet at: https://entp.hud.gov/idapp/html/condlook.cfm. If you are unable to access FHA Connection, please contact your Account Manager for assistance.

InspectionsPest InspectionsA pest inspection is required only if evidence of active infestation, mandated by the state or local jurisdiction, if customary to area, or at lender’s discretion. If the sales contract states a termite s to be performed we will require it to be reviewed. In NH Grafton, Carroll and Coos counties require pest inspections.Water TestsPlease see announcement 2015-043R for Retail and 2015-059T for TPO.A water test is required only if :

• if there is knowledge that well water may be contaminated; when the water supply relies upon a water purification system due to presence of contaminants;

• when there is evidence of:– Corrosion of pipes (plumbing)– Areas of intensive agriculture within ¼ mile– Coal mining or gas drilling operations within ¼ mile– Dump, junkyard, landfill, factory, gas station, or dry cleaning operation within ¼ mile– Unusually objectionable taste, smell or appearance of well water

If a test is required, the water quality myst meet local or EPA standards.

• The appraiser must provide a sketch to show the proximity of the location of the well to the septic system, and state whether the well is a dug well or a drilled well. Generally there should be at least 75 feet of distance between the well and septic.

• Dug Wells will require an engineer’s report.

Processing• Run the loan through LP or DU. If AUS determination is a “Refer”, the loan

must be manually underwritten. To be eligible for a manual underwrite, you must determine if your loan falls within FHA guidelines and MMC’s overlays.

• Using the FHA Connection, MMC will request a FHA Case Number and CAIVRS. This will not be done on pre-approvals.

• LDP checks are required. This is a list of Limited Denial Participants, including subdivisions, builders, condo’s etc. that are no longer approved by HUD. Make a note on the file that the LDP list was checked and that all the parties involved (borrower, seller, real estate agent, loan originator, processor, underwriter, settlement agent) in this transaction are not listed.

• GSA checks are also required. This is the General Service Administration Debarment List. Input the borrower, seller, real estate agent, loan originator, processer, underwriter, settlement agent name, and then search. The response will come back “no match.” Print the page. At the top of the page a date will show. Use this date along with“no match” for the GSA.

• When submitting your loan file, be sure to include all applicable FHA Disclosures and documentation loans

Closing costsAllowable Closing Costs• Fees may be charged to the mortgagors that are customary and reasonable and necessary to close the mortgage. These fees may be used to

meet the borrower’s investment requirement. • Actual cost of credit reports• Appraisal fee and any inspection fees• Origination fee• Deposit verification fees, if imposed by another depository institution.• Home inspection service fees; If included, a copy of the Insp. Report must be placed in the HUD file to FHA• Cost of title examination and title insurance;• Closing service letter fee• Document preparation• Property survey• Attorney fees• Recording fees and taxes• Test and certification fees (such as water tests, etc.)• Transfer taxes / transfer stamps / document stamp (if paid by the borrower)• Courier fees• Disbursement fee• Doc stamps on deed (Except FNMA, REO & VA)• Courier fees• Processing / Transaction fee• Transfer / Assignment of mortgage fee• Underwriting fee• Other reasonable and customary fees necessary to close the mortgage.Non-allowable Closing Costs• Discount PointsUnacceptable Closing Costs• Tax service Fee

Links

FHA Connection (requires a User ID and Password):• https://entp.hud.gov/clas/index.cfmHUDClips• http://portal.hud.gov/hudportal/HUD?

src=/program_offices/administration/hudclipsFHA FAQ• http://portal.hud.gov/hudportal/HUD?

src=/program_offices/housing/sfh/fharesourcectrGSA• https://www.sam.gov/portal/public/SAM/LDP• https://www5.hud.gov/ecpcis/main/ECPCIS_List.jsp

Calculating the max loan amount

• This calculation is used to determine and calculate a 3.5% investment from the borrower.

• Maximum Loan-to-Value Percentages/New England:• * 96.5% on a purchase transaction, 97.0% on a rate/term refinance transaction• (A) LESSOR OF SALES PRICE OR VALUE: $_____200,000__________• (B) APPROPRIATE LOAN TO VALUE: x __96.5____________%• (See above chart)• (C) MAXIMUM BASE LOAN AMOUNT: = ___193,000____________• (D) MINIMUM CASH INVESTMENT: A (x) 3% or 3.5% $_______7,000________• (E) MINIMUM DOWN PAYMENT: A (-) C $_____7,000__________• (F) MINIMUM OF CLOSING COSTS TO BE PAID BY BOR.: D (-) E $_______0________• (G) BORROWERS MINIMUM CASH INVESTMENT: E (+) F $___7,000____________• Please note that borrowers can only pay allowable closing costs determined by the Dept.

of HUD. Closing costs paid by seller or lender is not to be used in calculating the borrowers 3.5% investment requirement.

FHA Underwriting Documentation Required• Use MMC Submission Checklists• Letter or memo from LO or Processor explaining reasons for

requesting loan approval (if applicable)• FHA 1008• 1003 with HUD addendum (Form 92900A)• Credit Report with any additional documentation• Divorce Decree (if applicable• Housing Verification• Asset Verification (two month’s bank statements)• Gift Letter with supporting documentation (if applicable)• Income verification (one month’s pay stubs, two years W-2s or two

years tax returns, etc)• Purchase & Sales Contract• Appraisal (must be completed by a FHA Certified Appraiser)• FHA Disclosures• Standard Disclosures

FHA required Disclosures• For your Protection: Get a Home Inspection – HUD 92564-CN - Provide to borrower no later than the initial loan application. No signature

• Real Estate Certification and Amendatory Clause

- Executed on or before real estate contract date

- See HUD Handbook 4155.1 revision 5, Paragraph 3-3 and 3-4 for

required language if not part of the sales contract

• Initial HUD/VA Addendum to the URLA- HUD 92900-A

- Executed at application

- Pages 1 and 4 signed by loan officer

- Pages 2 and 4 signed by borrowers

• Important Notice to Homebuyers- HUD 92900-B

• - Executed at loan application

• Informed Consumer Choice Disclosure

– Executed at loan application

• FHA ARM disclosure (if applicable) within 3 days of application

• Forms can be found at http://portal.hud.gov/hudportal/HUD?src=/program_offices/administration/hudclips/forms

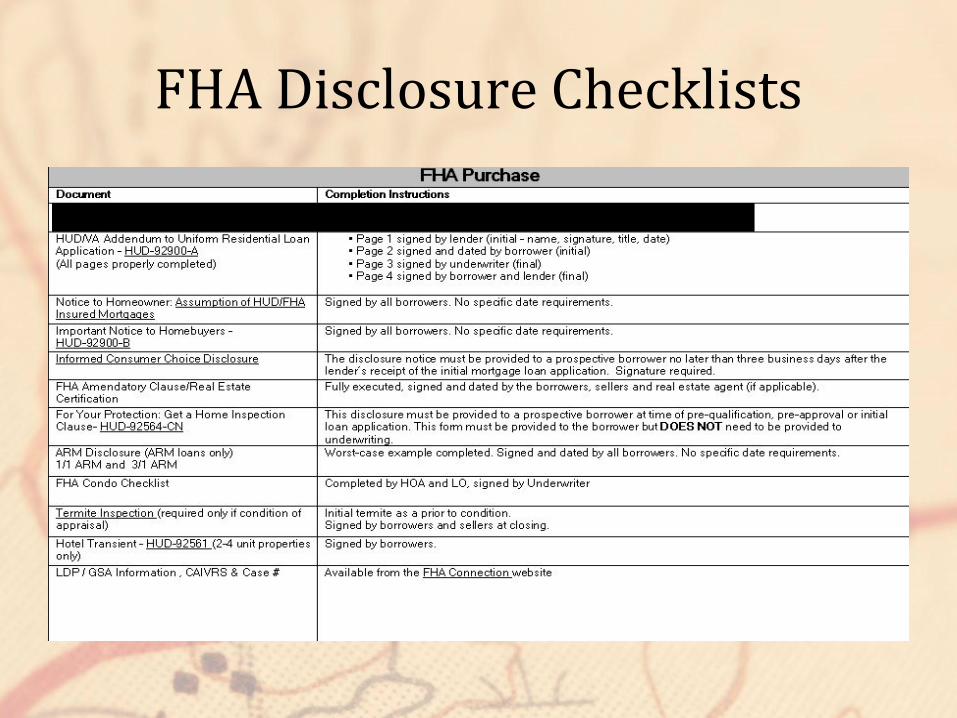

FHA Disclosure Checklists

Rate and Term Disclosure Requirements

Cash Out Refinance Disclosure Requirements

Questions?

Thanks for attending today’s presentation!

DISCLAIMER:Presentation for Industry Professionals only, not intended to be distributed to consumers.Subject to underwriting approval.Terms and conditions subject to change without notice.Information accurate as of date published.

Licensed by the New Hampshire Banking Department, Rhode Island Licensed Lender, and Licensed by the New Jersey Department of Banking and Insurance

![Welcome [] · • Speakers will be chosen by a lottery drawing method • Intimidating behavior (confronting, blocking, or interfering) will not be tolerated • Signs cannot exceed](https://img.pdfslide.us/doc/110x75/5f7abf39d6de9d5d5732d8d7/welcome-a-speakers-will-be-chosen-by-a-lottery-drawing-method-a-intimidating.jpg)