Embed Size (px)

DESCRIPTION

FATCA White paper

Citation preview

FATCA: The Long Arm of the IRSHow Foreign Financial Institutions Should Prepare for the United States Government’s Effort to Combat Offshore Tax Evasion

BYEllEn ZimilEs, Managing Director, Head of Global Investigations & ComplianceJEffrEY lockE, FATCA Task Force Leader, Global Investigations & Compliancerichard kando, FATCA Task Force Leader, Global Investigations & Compliance

TaBlE of conTEnTsI. Introduction 1

A. How We Got Here 1

B. The Intent of FATCA versus Execution 1

II. Understanding Select FATCA Terms 2

A. FFI 2

B. U.S. Person or Owner 2

C. FFI Reporting Requirements 2

III. First Preview of the Complexities of FATCA Implementation 3

A. Pre-Existing Accounts 3

B. New Accounts 4

IV. Worldwide Coordination: Key to Building a Strong FATCA Compliance Program 5

A. Publicity, Publicity, Publicity: Create an Awareness Program 5

B. Information Already Maintained on Our Clients versus The Collection of Additional Information 6

C. The Headache Begins 7

V. Conclusion 8

BIOGRAPHIES 9

ExhiBiT a 10FATCA: The FFI’s Preliminary Workflow Concerning Pre-Existing Individual Accounts

ExhiBiT B 11FATCA: The FFI’s Preliminary Workflow Concerning Pre-Existing Entity Accounts

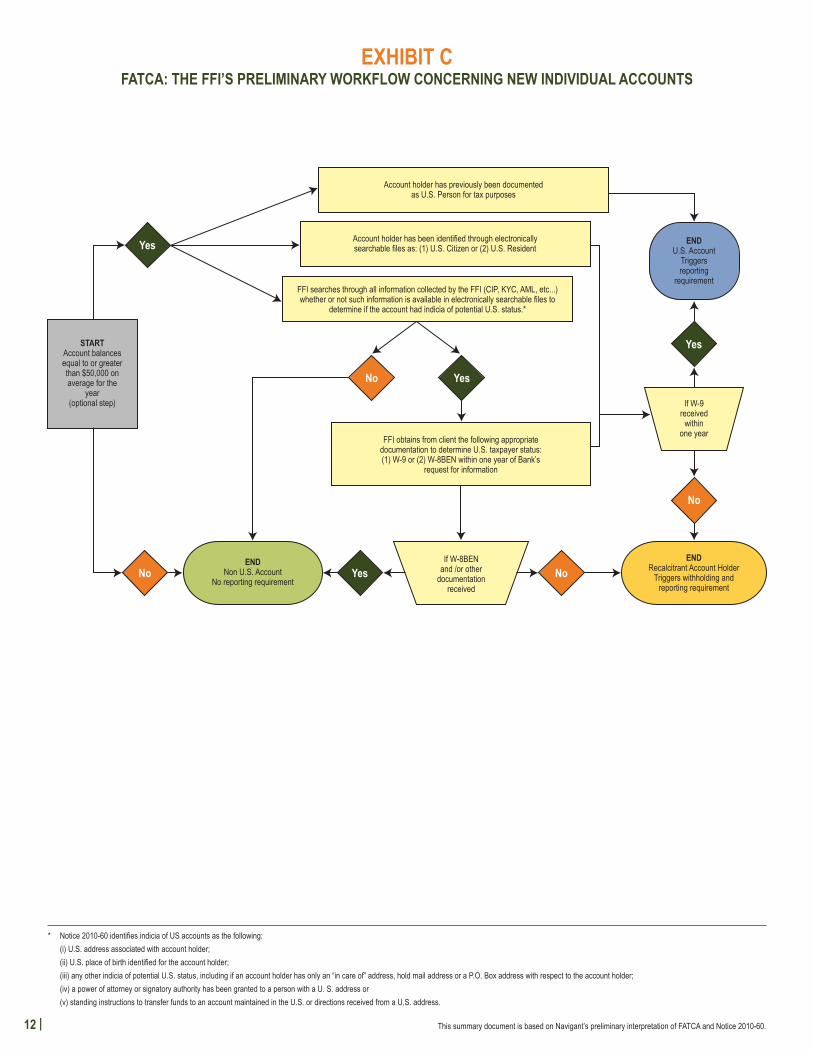

ExhiBiT c 12FATCA: The FFI’s Preliminary Workflow Concerning New Individual Accounts

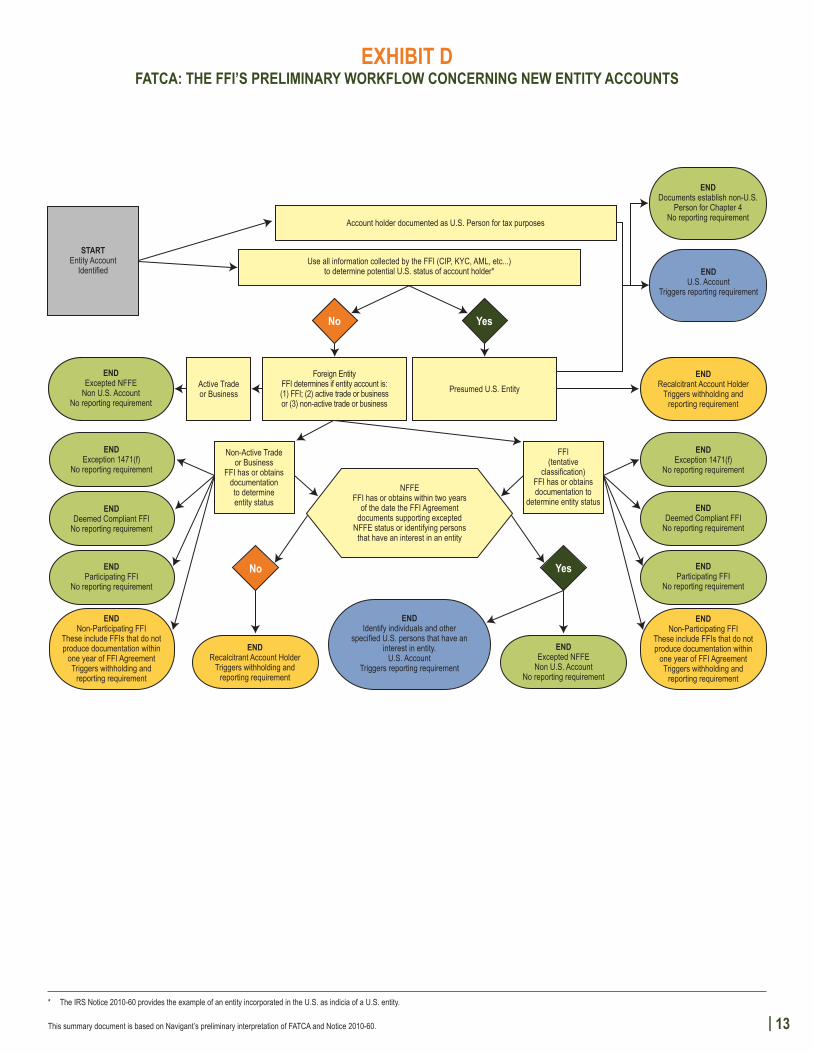

ExhiBiT d 13FATCA: The FFI’s Preliminary Workflow Concerning New Entity Accounts

| 1

I. Introductiona. how wE GoT hErE

In the past two years we have seen:

1. UBS AG enter into a deferred prosecution agreement and pay $780 million to the U.S. government for maintaining undeclared offshore accounts for U.S. taxpayers;

2. more than a dozen U.S. taxpayers plead guilty or be charged with tax fraud for maintaining undisclosed accounts and many others still under criminal investigation; and

3. thousands of U.S. citizens disclose to the Internal Revenue Service (“IRS”) their secret bank accounts.

Indeed, the veil of bank secrecy in Switzerland has been shattered.

In addition to the efforts of the IRS and the U.S. Department of Justice to combat offshore tax evasion, other countries have followed suit by purchasing account data from former bankers and pursuing the tax gap resulting from citizens’ maintenance of previously undisclosed accounts. Moreover, the U.S. Government’s efforts have culminated in the Foreign Account Tax Compliance Act (“FATCA”), which mandates that a foreign financial institution (“FFI”) identifies U.S. taxpayers with accounts at the FFI or suffer a 30% withholding on certain United States sourced income payments to the FFI. To avoid the withholding tax, which would be remitted directly to the IRS, FATCA requires FFIs to obtain and report information on its accounts used in whole or in part by U.S. taxpayers (“U.S. Accounts”) to the IRS. FATCA is likely the most far-reaching statute to combat tax evasion in recent history.

B. ThE inTEnT of faTca vErsus ExEcuTionThe goal of FATCA seems simple and to the point: to combat offshore tax evasion. When put into practice, however, it becomes an extremely complicated process requiring coordination by personnel not only across business lines of the FFI but also across the globe. Even though FFIs have until Janu-ary 1, 2013 to comply, these complexities necessitate that the first steps of preparation should begin immediately. After setting forth some background information on FATCA and IRS Notice 2010-601 (the “Notice”), this article will address the three steps that all FFIs should start now: (1) create an aware-ness program; (2) identify the information collected by the FFI through the Customer Identification Program (“CIP”), Know Your Customer Program (“KYC”) or other relevant programs and (3) develop and implement a program of systems, policies and procedures and corporate governance.

1 On August 27, 2010, the IRS issued Notice 2010-60, “Notice and Request for Comments Regarding Implementation of Information Reporting and Withholding Under Chapter 4 of the Code”, which “provides preliminary guidance regarding priority issues involving the implementation” of FATCA. Notice p. 1.

2 |

II. Understanding Select FATCA TermsOn March 18, 2010, FATCA was signed into law as part of the Hiring Incentives to Restore Employ-ment Act (“the Act”).2 FATCA goes into effect on January 1, 2013 and provides the United States Treasury and the IRS with oversight responsibility.

a. ffiAccording to FATCA, an FFI is a foreign entity that: (1) accepts deposits in the ordinary course of a banking or similar business, (2) as a substantial portion of its business, holds financial assets for the account of others, or (3) is engaged (or holds itself out as being engaged) primarily in the business of investing, reinvesting, or trading securities, partnership interests, commodities, or any interest in these mentioned items.3

B. u.s. accounT: u.s. PErson or ownEr

A U.S. Account is, generally, a financial account held by a specified U.S person or by an entity that, directly or indirectly, had one or more “substantial” U.S. owners. FATCA defines a “substantial” U.S. owner as a direct or indirect owner of: (1) more than 10% of the stock of a corporation; (2) more than 10% of the profit or capital interest in a partnership; or (3) an owner of any portion of a trust and the holder of more than 10% of the beneficial interest of a trust. Investment vehicles owned by a U.S. person, no matter what percentage of ownership, must be reported to the IRS.4

Additionally, the Notice allows for accounts with an average account value of less than $50,000 to be classified as “other than a U.S. account.”5

c. ffi rEPorTinG rEquirEmEnTsFFIs will be required to report the following for all U.S. Accounts to the IRS: (1) the name, address and taxpayer identification number for each individual or U.S owned foreign entity account holder, (2) the account number, (3) the account balance or value and (4) gross receipts and payments from the account.6

2 H.R. 2847, Title V-Offset Provisions, Subtitle A, Foreign Account Tax Compliance. According to the Act, FATCA added §§ 1471 though 1474 to the Internal Revenue Code (“IRC”).

3 IRC §§ 1471(d)(4) and 1471(d)(5).4 IRC § 1473(2).5 According of the Notice, if the sum of the average the month-end balances or values for the year of all accounts maintained with the FFI by the

account holder is less than $50,000, the accounts can be excluded from the analysis of U.S. Accounts. The Notice also allows for the FFI to use the time period for which it reports values to its account holder to determine the average value of accounts. The Notice, pp. 29 – 30.

6 IRC § 1471(c)(1).

| 3

III. First Preview of the Complexities of FATCA Implementation: Published Guidance, IRS Notice 2010-60

The IRS’s first guidance in interpreting FATCA is over sixty pages long and contains new acronyms, workflows and requirements that each FFI must implement. Below is a high level summary of a portion of the Notice that discusses the collection of information to identify U.S. Accounts. It’s expected the IRS will issue additional guidance regarding FATCA.

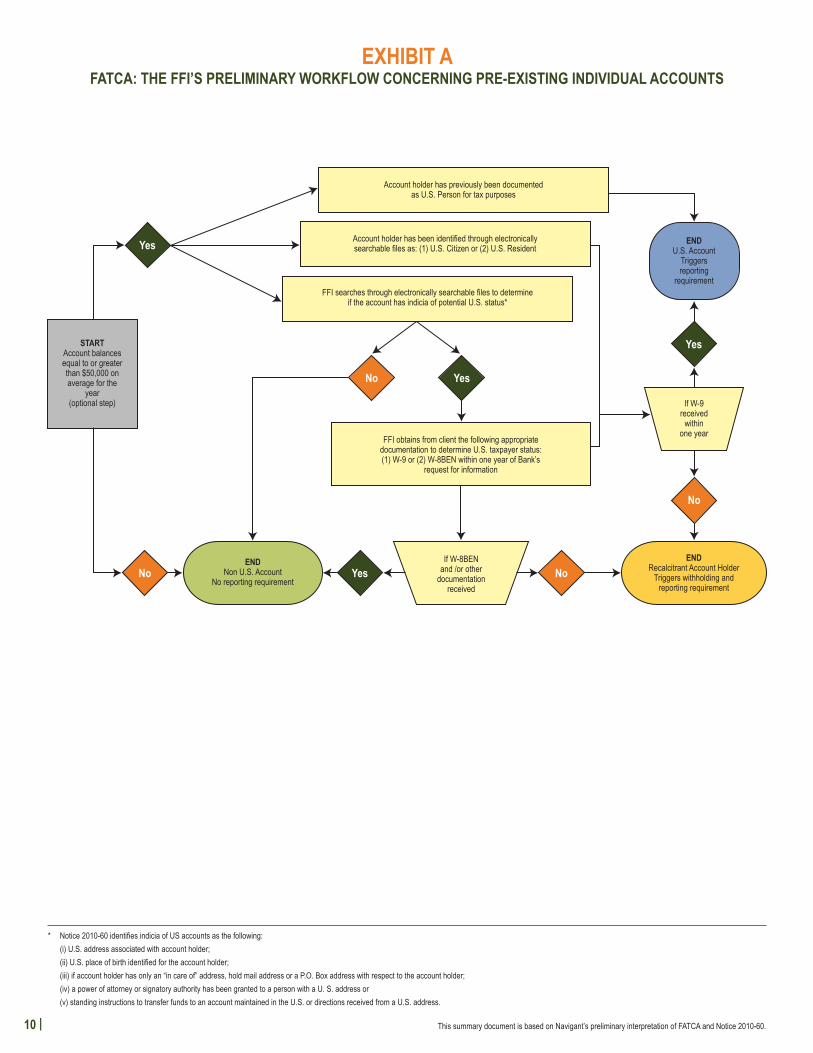

a. PrE-ExisTinG accounTsFor accounts maintained in the name of individuals or entities and established prior to the signing of an agreement (the “FFI Agreement”) between the IRS and the FFI (“Pre-Existing Accounts”)7, the Notice allows the FFI to rely on “… electronically searchable information maintained by the FFI and associ-ated with the account…”8 for indicia of potential U.S. status.9 For individual accounts,10 depending on what indicia is identified through the electronic search, the FFI will have to request a Form W-9 or Form W-8BEN and possibly other documentary evidence from the account holder to provide additional evidence of the account holder’s status.11

7 In addition to entering in an agreement with the IRS, FATCA also mandates that there be a 30% withholding on United States source income unless FFIs comply with reporting requirements. FATCA requires that FFIs:

1) obtain information to determine if the account is a U.S. Account; 2) comply with such verification and due diligence procedures as required with respect to U.S. Accounts; 3) report on an annual basis information relating to U.S. Accounts; 4) deduct and withhold a tax equal to 30% of certain specified payments; 5) comply with requests by the Secretary of Treasury for additional information regarding U.S. Accounts; and 6) obtain a valid and effective waiver if any foreign law would prevent reporting relating to U.S. Accounts.

IRC § 1471(b).8 The Notice, p. 27.9 According to Section III.B.2 of the Notice, Individual Financial Accounts – Identification by Participating FFIs for Purposes of § 1471, the indicia

for pre-existing individual accounts includes: 1) identification of any account holder as a U.S. resident or U.S. Citizen; 2) a U.S. address associated with an account holder of the account (whether a residence address or a correspondence address); 3) a U.S. place of birth for an account holder; 4) an “in care of” address, a “hold mail” address, a P.O. address that is the sole address on file; 5) a power of attorney or signatory authority granted to a person with a U.S. address; or 6) standing instructions to transfer funds to an account maintained in the United States or direction received from a U.S. address.

The Notice, pp. 26 and 27.10 Attached hereto as Exhibit A is a flowchart regarding the analysis of Pre-Existing Accounts maintained by individuals to identify potential U.S.

Accounts, which is entitled “FATCA: The FFI’s Preliminary Workflow Concerning Pre-Existing Individual Accounts.”11 The Notice provides a timeframe for completing additional analyses for those Pre-Existing Accounts maintained by individuals which were identi-

fied as a non-U.S. Account after reviewing electronically searchable information. The FFI has two years from the date of the FFI Agreement to apply the steps for a new individual account holder if the pre-existing account’s value was in excess of $1,000,000 during the year preceding the FFI Agreement to determine if the account holder should still be treated as a non-US Account. Within five years of the FFI Agreement, all individual accounts analyzed using the Pre-Existing Accounts protocol with an account value equal to or more than $50,000 and identified as a non-U.S. Account will be subject to the procedures for New Accounts. The steps to analyze new individual accounts are described below. The Notice, pp. 29 and 30.

4 |

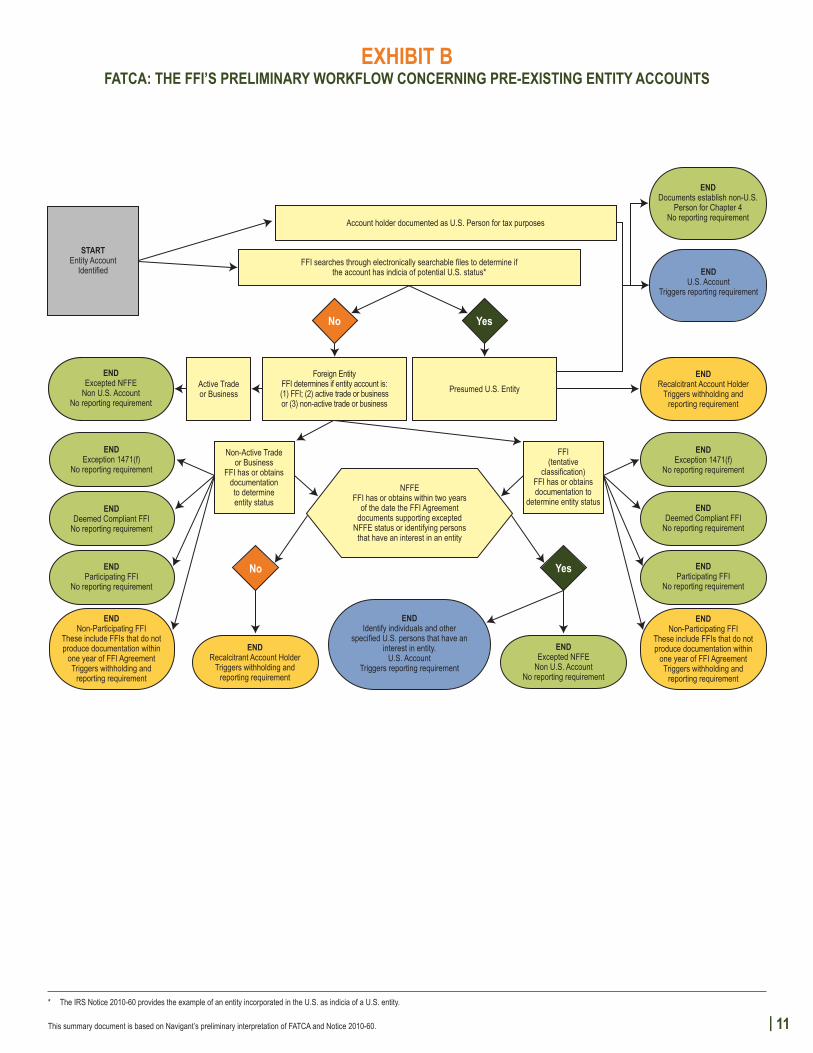

For Pre-Existing Accounts maintained in the name of an entity, the workflow is much more cumber-some as there are numerous categories in which an entity can be classified: (1) a Participating FFI, (2) a Deemed Compliant FFI, (3) a Non-Participating FFI, (4) an entity for which FATCA does not apply, or (5) a Non-Financial Foreign Entity (“NFFE”).12 If the account holder is another FFI, the FFI originating the transaction has to determine if the beneficiary FFI is FATCA compliant or exempt from reporting. If the beneficiary FFI is neither, the originating FFI must withhold 30% on the payment of U.S. source income.

If the entity account holder is identified as a foreign entity that is not a FFI, there are additional tests to determine if there is evidence that the entity is operating an active trade or business. This is equivalent to a shell company test to determine if the account holder is nothing more than a company without significant operations or assets aside from the account and possibly being used to disguise true owner-ship of the account. If the account holder does not provide evidence of operating as an active trade or business, the FFI has to identify substantial beneficial owners of the account. If any of these owners are U.S. persons, the FFI has a reporting requirement.

When conducting the analysis of Pre-Existing Accounts, the workflow allows for the continual request for additional information from the account holder. After a certain time of non-responsiveness, gener-ally one or two years from the date of request, the account holder is classified as recalcitrant (“recalci-trant account holder”), which triggers a withholding and reporting requirement for the FFI.

B. nEw accounTs13 For accounts established by individuals or entities after the FFI Agreement is effectuated with the IRS (“New Accounts”), the work to determine if the New Account is for the benefit of a U.S. Person is similar to the work you would complete for a Pre-Existing Account. The main difference is that FFIs are not al-lowed to only rely on electronically searchable files, but the FFI has to use “… all information collected by the FFI… regardless of whether such information is available in electronically searchable files.”14 As such, FFIs would be well-served to begin including this information in electronic databases as soon as practicable and prior to the January 1, 2013 FATCA effective date.

12 Attached hereto as Exhibit B is a flowchart regarding the analysis of Pre-Existing Accounts maintained by entities to identify potential U.S. Ac-counts, which is entitled “FATCA: The FFI’s Preliminary Workflow Concerning Pre-Existing Entity Accounts.”

13 Attached hereto as Exhibits C and D, respectively, are flowcharts regarding the analysis of New Accounts maintained by individuals and entities to identify potential U.S. Accounts. Exhibit C is entitled “FATCA: The FFI’s Preliminary Workflow Concerning New Individual Accounts” and Exhibit D is entitled “FATCA: The FFI’s Preliminary Workflow Concerning New Entity Accounts.”

14 The Notice, p. 40.

| 5

IV. Worldwide Coordination: Key to Building a Strong FATCA Compliance Program

After analyzing the Notice, it is important that each FFI begins to take the following three preliminary steps: (1) create an awareness program, (2) identify the information already collected by the FFI on its customers, and (3) develop and implement a program of systems, policies and procedures, and corporate governance.

a. PuBliciTY, PuBliciTY, PuBliciTY: crEaTE an awarEnEss ProGram

It is important that everyone in the organization is aware of the changes that will need to be made to comply with FATCA. There will not be a “one-size fits all” solution, as each business entity of the FFI may collect different information on their customers. Additionally, the awareness program has to start early as U.S. personnel may have to persuade their counterparts and executive level business line personnel at foreign branches of the FFI of the importance of the foreign branch’s compliance with FATCA, a U.S. based law that requires FFIs demand more information of their clients. Although much of the program implementation will likely fall on operations, compliance and tax personnel, it’s impor-tant to spread awareness of FATCA to all relationship managers and client facing employees overseas as these employees will likely be receiving client questions. As part of the awareness program, a FFI should create a “FATCA Task Force” to identify all affected stakeholders and create an internal and external awareness program.

1. more responsibilities for key Personnel: developing a faTca Task force

Early on in the process, a task force should be assembled to determine how the FFI is going to comply with FATCA. The team should include individuals with tax, CIP, KYC, Anti-Money Laun-dering (“AML”), and operations responsibility, as much of the FFI’s initial compliance with FATCA as it will be driven by information already maintained by the FFI. A member of the information technology software development team should also be included because complying with FATCA may necessitate building a new database of electronic information or leveraging current systems.

2. Parties affected by faTca

The FATCA Task Force must identify all stakeholders that may be affected by FATCA. This should include domestic and foreign entities, subsidiaries, and business lines that will likely have FATCA reporting requirements including transfer agents and custody businesses. Special atten-tion should be paid to FFI operations in jurisdictions with enhanced secrecy rules. It may require extra effort to comply with FATCA in these jurisdictions given that KYC information may not be as abundant in these areas and foreign law may prevent the reporting of information by the FFI to the IRS but for a waiver by the account holder.15 Moreover, these may be the areas most vulner-able to U.S. government scrutiny.

15 FFIs are required to obtain a valid and effective waiver from the account holder if foreign law prohibits the reporting of certain information. If the waiver is not obtained within a reasonable period of time, the FFI should close the account. IRC § 1471(b)(1)(F).

6 |

3. internal and External awareness

a. Get Ready: The Internal Awareness Program

An internal awareness program should be developed to teach FFI employees about FATCA and its importance to the FFI. The internal awareness program should start at the highest levels of the company, both domestically and abroad, to establish the necessary “tone at the top”, and trickle down through the company to compliance personnel and finally to client-facing relationship managers. The awareness program should include the distribution of memorandums and emails as well as conference calls and live training programs.

b. Prepare for Questions from Clients: External Awareness

A list of questions that will likely be asked by clients along with sample answers should be drafted and shared with client facing personnel. This list, the “FAQs of FATCA,” should be designed to ensure that the clients of the FFI, no matter where they are located, receive consistent answers regarding FATCA and its importance to the FFI. The FFI should also assess whether it is prudent to send a mailing to its customers describing FATCA and the type of information that may be requested in the future from account holders. This could help ease the shock when clients receive requests for documentation from the FFI that it likely has not asked for before.

B. informaTion alrEadY mainTainEd on our cliEnTs vErsus ThE collEcTion of addiTional informaTion

After identifying all potentially affected groups and business lines, it is important to find out what pre-viously collected information each group has regarding its client base. According to the Notice, for pre-existing individual and entity accounts and for only a specified period of time, the FFI is allowed to rely on the information it already maintains in electronically searchable files to identify potential U.S. accounts. In addition to reviewing information available in electronically searchable files, it’s also important to inventory and assess client information not maintained in electronically searchable files as any changes to the collection of the information of account holders will likely take a considerable amount of time to implement. For example, the FATCA compliance team may want to determine:

1. Whether there is a copy of a passport in every customer’s file;16

2. If all addresses associated with the account are maintained in a single system; and

3. Whether the account opening questionnaire needs to change to address the potential identification of U.S. Accounts and indicia of potential U.S. status of the account holders, including green card holders.

The account opening process may change significantly because of FATCA reporting requirements as much of the FFIs ability to provide accurate information to the IRS is dependent on account opening documentation.

16 FFIs should be mindful of certain privacy laws regarding the transfer of information across borders when developing a new database or linking previously developed databases. For example, see Directive 95/46/EC of the European Parliament and of the Council of 24 October 1995 on the protection of individuals with regard to the processing of personal data and on the free movement of such data. Council Directive 95/46, 1995, (EC). See also Law of the Republic of Indonesia Number 11 of 2008 Concerning Electronic Information and Transactions (2008).

| 7

c. ThE hEadachE BEGins: PuTTinG ThE irs GuidancE inTo PracTicE

1. The wish list

The FATCA Task Force, in close coordination with the application developer, should think about ag-gregating necessary information for FATCA compliance in one electronic system or linking different systems to decrease the number of databases that need to be searched to identify potential U.S. Accounts and report on those accounts. The FATCA Task Force also needs to determine when infor-mation maintained in a non-searchable format should be incorporated into a searchable database. The first step to enhancing or creating a system to maintain the necessary CIP and KYC infor-mation for FATCA compliance is to identify to the software application developer a wish list of information that should be warehoused in the electronic system. The specifications of the new or linked database(s) should be driven by the steps regarding the identification of U.S. Accounts, according to the Notice. Specifically, at a minimum, the wish list should request the inclusion of the following regarding the account holder:

a. All accounts

i. The aggregation of value of all accounts maintained across the FFI by each account holder;

ii. The identification in the database of each account already identified as a U.S. account;

iii. A way to track correspondence sent to an account holder, including when it was sent, and, if a response is necessary, when it is due; and

iv. The identification of a recalcitrant account holder.17

b. Individual Accounts

i. The U.S. address associated with any account;

ii. Where the account holder was born;

iii. Whether there is an “in care of,” “hold mail” or P.O. Box associated with the address of the account holder;

iv. Whether there is a power of attorney for the account and also if that power of attorney has a U.S. address;

v. Whether there are standing instructions for transfers from a U.S. address; and

vi. Whether the account holder provided to the FFI a Form W-9 or Form W-8BEN.

17 For a discussion of recalcitrant account holders see section III.A herein and the Notice, pp. 28 and 39.

8 |

c. Entity Accounts

i. Where entity account holders were formed or incorporated;

ii. Whether an entity account holder was previously identified as a FFI;

iii. Whether an entity account holder was identified as an exception to FATCA reporting by the Act;18

iv. Whether an entity account holder operated an active trade or business; and

v. Whether the entity account holder was previously identified as having a U.S. owner or beneficial interest by a U.S. Person;

In addition to the fields addressed above, the system should be able to maintain scanned docu-ments to support each of the entries to ease the quality assurance review necessary for such a robust warehouse of information and also be able to track the FFI’s decisions as to whether the account is deemed to be a U.S. Account.

2. more Policies and Procedures and an updated corporate Governance Program

From a practical perspective, the FFI needs to incorporate the guidance provided by the Notice into its current policies and procedures. An initial draft of the additional procedures should, at a minimum, outline the steps to determine if individual and entity account holders are reportable to the IRS. The policies and procedures will likely be updated each time another notice is published by the IRS.

From a corporate governance perspective, the FFI may decide to integrate the FATCA compli-ance program with compliance programs relating to CIP and KYC. This function may also be placed in operations, tax compliance, a branch network or elsewhere. No matter where ultimate responsibility resides, however, it is obvious business line and worldwide coordination is key.

V. ConclusionAlthough FATCA does not go into effect for two years and the IRS has stated it will issue more guid-ance, there are many practical steps FFIs can take to begin preparation of a FATCA compliance program immediately. Additionally, if the past helps predict the future at all, FFIs may see other coun-tries pass FATCA-type laws the way other countries followed the United States’ lead in pursuing the offshore accounts of their own taxpayers.19

18 Entity account holders excluded from FATCA reporting requirements include:1) Any foreign government, any political subdivision of a foreign government, or any wholly owned agency or instrumentality of any one or

more of the foregoing; 2) Any international organization or any wholly owned agency or instrumentality thereof;3) Any foreign central bank of issue; or4) Any other class of persons identified by the Secretary of Treasury for purposes of this subsection as posing a low risk of tax evasion.

IRC §1471(f).19 The Organisation for Economic Co-operation and Development (the “OECD”), over the years, has been seeking greater transparency and

an increase in the exchange of information to combat tax avoidance and evasion. For example, the OECD Global Forum Working Group on Effective Exchange of Information, which consists of OECD Member countries as well as delegates from other jurisdictions, developed an agreement to promote international cooperation in tax matters through exchanges of information. See http://www.oecd.org/document/37/0,3343,en_21571361_43854757_44270949_1_1_1_1,00.html.

Biographies EllEn ZimilEs is a Managing Director and Head of Global Investigations and Compliance in Navigant’s Disputes & Investigations practice. She has more than 25 years of litigation and investi-gation experience, including 10 years as a federal prosecutor. Ms. Zimiles is a leading authority on anti-money laundering programs, corporate governance, regulatory and corporate compliance, fraud control and public corruption matters. She has worked with a multitude of financial institutions prepar-ing for regulatory exams, developing remediation programs and assisting organizations as a regulatory liaison. Ms. Zimiles founded and served as CEO of Daylight Forensic & Advisory LLC, an international investigations and compliance consulting firm which merged with Navigant in 2010. As an assistant United States attorney in the Southern District of New York for more than 10 years, Ms. Zimiles served in the civil and criminal divisions and was chief of the forfeiture unit for more than six years. She was responsible for many high-profile money laundering, fraud and forfeiture cases.

JEffrEY lockE is an Associate Director in Navigant’s Disputes & Investigations practice, and along with Richard Kando, a leader of Navigant’s FATCA Task Force. Mr. Locke specializes in regu-latory compliance, anti-money laundering investigations and financial investigations. Prior to joining Navigant, he was a prosecutor of white collar crime for the state of New York and he worked for the United Nations Mission in Kosovo, where he conducted investigations into war crimes, corruption and organized crime.

richard kando is an Associate Director in Navigant’s Disputes & Investigations practice, and along with Jeffrey Locke, a leader of Navigant’s FATCA Task Force. Mr. Kando primarily assists coun-sel with anti-money laundering and other regulatory compliance related engagements and litigation related matters. Prior to joining the consulting industry, Mr. Kando served as a special agent for the Internal Revenue Service – Criminal Investigation Division in New York City where he investigated allegations of tax evasion and other tax related criminal offenses, mail and wire fraud, embezzlement, money laundering and identity theft. In recognition of his services as a special agent, he received the U.S. Department of Justice – Tax Division Assistant Attorney General’s Special Contribution Award.

| 9

10 |

ExhiBiT a faTca: ThE ffi’s PrEliminarY workflow concErninG PrE-ExisTinG individual accounTs

This summary document is based on Navigant’s preliminary interpretation of FATCA and Notice 2010-60.

* Notice 2010-60 identifies indicia of US accounts as the following: (i) U.S. address associated with account holder; (ii) U.S. place of birth identified for the account holder; (iii) if account holder has only an “in care of” address, hold mail address or a P.O. Box address with respect to the account holder; (iv) a power of attorney or signatory authority has been granted to a person with a U. S. address or (v) standing instructions to transfer funds to an account maintained in the U.S. or directions received from a U.S. address.

Account holder has previously been documented as U.S. Person for tax purposes

Account holder has been identified through electronicallysearchable files as: (1) U.S. Citizen or (2) U.S. Resident

FFI searches through electronically searchable files to determineif the account has indicia of potential U.S. status*

EndU.S. Account

Triggersreporting

requirement

Yes

Yes no

no

Yesno

no

Yes

FFI obtains from client the following appropriatedocumentation to determine U.S. taxpayer status:(1) W-9 or (2) W-8BEN within one year of Bank’s

request for information

If W-9received

withinone year

EndRecalcitrant Account Holder

Triggers withholding andreporting requirement

EndNon U.S. Account

No reporting requirement

If W-8BENand /or other

documentationreceived

sTarTAccount balancesequal to or greaterthan $50,000 onaverage for the

year(optional step)

| 11

ExhiBiT B faTca: ThE ffi’s PrEliminarY workflow concErninG PrE-ExisTinG EnTiTY accounTs

Yesno

Account holder documented as U.S. Person for tax purposes

EndNon-Participating FFI

These include FFIs that do notproduce documentation within

one year of FFI AgreementTriggers withholding and

reporting requirement

FFI searches through electronically searchable files to determine if the account has indicia of potential U.S. status*

Yesno

Active Tradeor Business

Foreign EntityFFI determines if entity account is: (1) FFI; (2) active trade or business or (3) non-active trade or business

Presumed U.S. Entity

Non-Active Trade or Business

FFI has or obtainsdocumentation to determine entity status

FFI(tentative

classification)FFI has or obtainsdocumentation to

determine entity statusNFFE

FFI has or obtains within two yearsof the date the FFI Agreement

documents supporting exceptedNFFE status or identifying persons

that have an interest in an entity

EndParticipating FFI

No reporting requirement

EndDeemed Compliant FFI

No reporting requirement

EndException 1471(f)

No reporting requirement

EndRecalcitrant Account Holder

Triggers withholding andreporting requirement

EndU.S. Account

Triggers reporting requirement

EndDocuments establish non-U.S.

Person for Chapter 4No reporting requirement

EndExcepted NFFE

Non U.S. AccountNo reporting requirement

EndException 1471(f)

No reporting requirement

EndDeemed Compliant FFI

No reporting requirement

EndParticipating FFI

No reporting requirement

EndIdentify individuals and other

specified U.S. persons that have aninterest in entity.

U.S. AccountTriggers reporting requirement

EndExcepted NFFE

Non U.S. AccountNo reporting requirement

EndRecalcitrant Account Holder

Triggers withholding andreporting requirement

EndNon-Participating FFI

These include FFIs that do notproduce documentation within

one year of FFI AgreementTriggers withholding and

reporting requirement

sTarTEntity Account

Identified

This summary document is based on Navigant’s preliminary interpretation of FATCA and Notice 2010-60.

* The IRS Notice 2010-60 provides the example of an entity incorporated in the U.S. as indicia of a U.S. entity.

12 |

* Notice 2010-60 identifies indicia of US accounts as the following: (i) U.S. address associated with account holder; (ii) U.S. place of birth identified for the account holder; (iii) any other indicia of potential U.S. status, including if an account holder has only an “in care of” address, hold mail address or a P.O. Box address with respect to the account holder; (iv) a power of attorney or signatory authority has been granted to a person with a U. S. address or (v) standing instructions to transfer funds to an account maintained in the U.S. or directions received from a U.S. address.

ExhiBiT c faTca: ThE ffi’s PrEliminarY workflow concErninG nEw individual accounTs

Account holder has previously been documented as U.S. Person for tax purposes

Account holder has been identified through electronicallysearchable files as: (1) U.S. Citizen or (2) U.S. Resident

FFI searches through all information collected by the FFI (CIP, KYC, AML, etc...) whether or not such information is available in electronically searchable files to

determine if the account had indicia of potential U.S. status.*

EndU.S. Account

Triggersreporting

requirement

Yes

Yes no

no

Yesno

no

Yes

FFI obtains from client the following appropriatedocumentation to determine U.S. taxpayer status:(1) W-9 or (2) W-8BEN within one year of Bank’s

request for information

If W-9received

withinone year

EndRecalcitrant Account Holder

Triggers withholding andreporting requirement

EndNon U.S. Account

No reporting requirement

If W-8BENand /or other

documentationreceived

sTarTAccount balancesequal to or greaterthan $50,000 onaverage for the

year(optional step)

This summary document is based on Navigant’s preliminary interpretation of FATCA and Notice 2010-60.

| 13

ExhiBiT d faTca: ThE ffi’s PrEliminarY workflow concErninG nEw EnTiTY accounTs

Yesno

Account holder documented as U.S. Person for tax purposes

EndNon-Participating FFI

These include FFIs that do notproduce documentation within

one year of FFI AgreementTriggers withholding and

reporting requirement

Use all information collected by the FFI (CIP, KYC, AML, etc...)to determine potential U.S. status of account holder*

Yesno

Active Tradeor Business

Foreign EntityFFI determines if entity account is: (1) FFI; (2) active trade or business or (3) non-active trade or business

Presumed U.S. Entity

Non-Active Trade or Business

FFI has or obtainsdocumentation to determine entity status

FFI(tentative

classification)FFI has or obtainsdocumentation to

determine entity statusNFFE

FFI has or obtains within two yearsof the date the FFI Agreement

documents supporting exceptedNFFE status or identifying persons

that have an interest in an entity

EndParticipating FFI

No reporting requirement

EndDeemed Compliant FFI

No reporting requirement

EndException 1471(f)

No reporting requirement

EndRecalcitrant Account Holder

Triggers withholding andreporting requirement

EndU.S. Account

Triggers reporting requirement

EndDocuments establish non-U.S.

Person for Chapter 4No reporting requirement

EndExcepted NFFE

Non U.S. AccountNo reporting requirement

EndException 1471(f)

No reporting requirement

EndDeemed Compliant FFI

No reporting requirement

EndParticipating FFI

No reporting requirement

EndIdentify individuals and other

specified U.S. persons that have aninterest in entity.

U.S. AccountTriggers reporting requirement

EndExcepted NFFE

Non U.S. AccountNo reporting requirement

EndRecalcitrant Account Holder

Triggers withholding andreporting requirement

EndNon-Participating FFI

These include FFIs that do notproduce documentation within

one year of FFI AgreementTriggers withholding and

reporting requirement

sTarTEntity Account

Identified

* The IRS Notice 2010-60 provides the example of an entity incorporated in the U.S. as indicia of a U.S. entity.

This summary document is based on Navigant’s preliminary interpretation of FATCA and Notice 2010-60.

©2010 Navigant Consulting, Inc. All rights reserved.Navigant Consulting is not a certified public accounting firm and does not provide audit, attest, or public accounting services.See www.navigantconsulting.com/licensing for a complete listing of private investigator licenses.

EllEn [email protected]

JEffrEY [email protected]

richard [email protected]

www.navigantconsulting.com