Embed Size (px)

Citation preview

OORRGGAANNIISSAATTIIOONN FFOORR EECCOONNOOMMIICC CCOO-OOPPEERRAATTIIOONN AANNDD DDEEVVEELLOOPPMMEENNTT

STABILITY PACT

SOUTH EAST EUROPE COMPACT FOR REFORM, INVESTMENT, INTEGRITY AND GROWTH

NATIONAL TREATMENT OF

INTERNATIONAL INVESTMENT IN SOUTH

EAST EUROPEAN COUNTRIES:

MEASURES PROVIDING EXCEPTIONS

OOCCTTOOBBEERR 22000033

National Treatment Couv.qxd 19/11/2003 11:49 Page 2

STABILITY PACT

SOUTH EAST EUROPE COMPACT FOR REFORM, INVESTMENT, INTEGRITY AND GROWTH

NATIONAL TREATMENT OF

INTERNATIONAL INVESTMENT IN SOUTH

EAST EUROPEAN COUNTRIES:

MEASURES PROVIDING EXCEPTIONS

ORGANISATION FOR ECONOMIC CO-OPERATION AND DEVELOPMENT

TThhee SSttaabbiilliittyy PPaacctt ffoorr SSoouutthh EEaasstteerrnn EEuurrooppee is a political declaration and framework agreementadopted in June 1999 to encourage and strengthen co-operation among the countries of South EastEurope (SEE) and to facilitate, co-ordinate and streamline efforts to ensure stability and economicgrowth in the region. (see www.stabilitypact.org)

TThhee SSoouutthh EEaasstt EEuurrooppee CCoommppaacctt ffoorr RReeffoorrmm,, IInnvveessttmmeenntt,, IInntteeggrriittyy aanndd GGrroowwtthh ((““TThhee IInnvveessttmmeennttCCoommppaacctt””)) is a key component of the Stability Pact under Working Table II on EconomicReconstruction, Development and Co-operation. Private investment is essential to facilitate thetransition to market economy structures and to underpin social and economic development. TheInvestment Compact promotes and supports policy reforms that aim to improve the investment cli-mate in South East Europe and thereby encourage investment and the development of a strong pri-vate sector. The main objectives of the Investment Compact are to:

– Improve the climate for business and investment. – Attract and encourage private investment.– Ensure private sector involvement in the reform process.– Instigate and monitor the implementation of reform.

The participating SEE countries in the Investment Compact are: Albania, Bosnia and Herzegovina,Bulgaria, Croatia, former Yugoslav Republic of Macedonia (henceforth Republic of Macedonia or FY Republic of Macedonia), Moldova, Romania and Serbia and Montenegro. Building on the coreprinciple of the Investment Compact that “ownership” of reform rests within the region itself, theInvestment Compact seeks to share the long experience of OECD countries. It provides region-widepeer review and capacity building through dialogue on successful policy development and ensuresidentification of practical steps to implement reform and transition.

The work of the Investment Compact is actively supported and financed by seventeen OECDmember countries: AAuussttrriiaa,, BBeellggiiuumm,, CCzzeecchh RReeppuubblliicc,, FFiinnllaanndd,, FFrraannccee,, GGeerrmmaannyy,, GGrreeeeccee,, HHuunnggaarryy,,IIrreellaanndd,, IIttaallyy,, JJaappaann,, NNoorrwwaayy,, SSwweeddeenn,, SSwwiittzzeerrllaanndd,, TTuurrkkeeyy,, UUnniitteedd KKiinnggddoomm aanndd UUnniitteedd SSttaatteess.. (see www.investmentcompact.org)

22 NATIONAL TREATMENT OF INTERNATIONAL INVESTMENT IN SOUTH EAST EUROPEAN COUNTRIES – © OECD 2003

FFOORREEWWOORRDD

National treatment is a key element of a favourable investment climate. It provides to non resident foreigninvestors and foreign controlled enterprises established in the country, treatment no less favourable than thataccorded to domestic enterprises in like circumstances. This principle is embodied in numerous bilateralinvestment treaties and the OECD Investment Instruments. The application of the national treatment principlein all countries of the Region represents a tangible medium-term goal for South East European (SEE) countriesas part of their reform agenda to create a high-quality investment environment. Success here will constitute astrong message to the investor community of the political will of the countries of the Region to matchrecognised international standards of investor treatment and to provide for equality of competitive conditions.

At their first meeting at ministerial level held in Vienna in July 2002, the Ministers of Economy and designatedMinisters dealing with business and investment in SEE countries called for the elimination of obstacles tonational treatment and invited the Investment Compact to survey any remaining deviations from this standard.In response, the Investment Compact has conducted national treatment reviews for all SEE countries the resultsof which are contained in this report. The report shows that the laws of most countries contain relatively fewdiscriminatory elements. However, a number of significant exceptions remain and the uneven implementationof formal non discriminatory rules still raise concern. Most of these barriers are the heritage of the past and havevery little economic justification.

The national treatment review was prepared by the OECD and a network of regional experts in cooperationwith the SEE Country Economic Teams. These reports were finalised through a process of questionnaires,individual meetings, dialogue and peer review in which all SEE countries and the private sector commentedon various drafts and included a drafting meeting hosted by Romania in Bucharest in June 2003. Theinformation contained in the report is current as at July 2003.

Earlier drafts of Chapters 1 (Regional Overview) and 2 (Summary of Most Significant National Measures) havebeen considered by the second meeting of the South East Europe Investment Compact at Ministerial level heldin Vienna in July 2003. The statement adopted by ministers on this occasion (see Appendix 1 to Chapter 1) drewsubstantially on the recommendations identified in this report. The summary of the most important deviationsfrom national treatment contained in Chapter 2 are discussed in greater detail in the individual country chapters(Chapters 3 to 10) which also provide a full assessment of laws and regulations faced by international investors.

Progress in applying national treatment throughout South East Europe will be regularly reviewed in theMonitoring Instruments of the Investment Compact and at the annual SEE Ministerial meeting to be held inVienna in July 2004. This report, including the Regional Overview as well as individual chapters for each SEEcountry, is published under the responsibility of the Investment Compact Project Team.

33NATIONAL TREATMENT OF INTERNATIONAL INVESTMENT IN SOUTH EAST EUROPEAN COUNTRIES – © OECD 2003

Cristian Diaconescu State Secretary Ministry of Foreign Affairs of Romania Co-Chair, Investment CompactProject Team

Manfred Schekulin Director, Export and InvestmentPolicy Department Federal Ministry for Economic Affairsand Labour of Austria Co-Chair, Investment Compact Project Team

Rainer Geiger Deputy Director Directorate for Financial Fiscaland Enterprise Affairs, OECDCo-Chair, Investment CompactProject Team

AACCKKNNOOWWLLEEDDGGEEMMEENNTTSS

This study has been undertaken by the Investment Compact Project Team co-chaired by Austria, OECD andRomania. The work has been led by Rainer Geiger (Deputy Director for Financial, Fiscal and Enterprise Affairs,OECD), Manfred Schekulin (Director for Export and Investment Policy, Austrian Ministry for Economic Affairsand Labour) and Cristian Diaconescu (State Secretary for Bilateral Affairs, Romanian Ministry of Foreign Affairs).

The research has benefited from the contributions of a team of expert consultants, mainly from the region.Slavica Penev (Economics Institute, Belgrade) and Matija Rojec (Faculty of Social Sciences, University ofLjubljana) organised and coordinated the work of the consultants and presentation of the draft report.

Input for individual country reports has been provided by Will Bartlett (School for Public Studies, Universityof Bristol), Fikret Cauševiƒ (Economics Institute, Sarajevo), Nevenka Cuckoviƒ (Institute for InternationalRelations, Zagreb), Ahmet Mancellari (Department of Economics, University of Tirana), Slavica Penev(Economics Institute, Belgrade), Matija Rojec (Faculty of Social Sciences, University of Ljubljana), Stoyan Totev(Institute of Economics, Bulgarian Academy of Sciences, Sofia) and Liviu Voinea (Academy of EconomicStudies, Bucharest).

Marie-France Houde, DAF/CMIS, OECD advised on the preparation of the questionnaire. The CountryEconomic Team Leaders of Albania, Bosnia and Herzegovina and Bulgaria provided information in response tothe ’Questionnaire on the Identification of Deviations from National Treatment for Incoming Investment and forActivities by Established Foreign-Controlled Enterprises'. The report has been reviewed and enhanced by theparticipants of the Drafting Session of the 2nd Ministerial Conference on Attracting Investment to South EastEurope: Removing Obstacles, held in Bucharest, 5-6 June 2003 (see Appendix 2 to Chapter 1).

The final report has been edited and prepared for publication by Declan Murphy (Programme Director),Deniz Eröcal (Administrator) and Georgiana Pop (Regional and Policy Reform Assistant), from the OECDInvestment Compact team.

55NATIONAL TREATMENT OF INTERNATIONAL INVESTMENT IN SOUTH EAST EUROPEAN COUNTRIES – © OECD 2003

TTAABBLLEE OOFF CCOONNTTEENNTTSS

PPAARRTT OONNEE:: SSYYNNTTHHEESSIISS ...................................................................................................................................... 9

Chapter 1.. RREEGGIIOONNAALL OOVVEERRVVIIEEWW .................................................................................................................... 11

1. INTRODUCTION .......................................................................................................................................... 11 2. CONCEPTS, METHODOLOGY AND STRUCTURE OF THE REPORT ........................................................................ 11 3. OVERVIEW OF MEASURES ............................................................................................................................ 13 4. GENERAL RECOMMENDATIONS .................................................................................................................... 16

Chapter 2. SSUUMMMMAARRYY OOFF MMOOSSTT SSIIGGNNIIFFIICCAANNTT NNAATTIIOONNAALL MMEEAASSUURREESS .................................................... 19

1. ALBANIA .................................................................................................................................................... 19 2. BOSNIA AND HERZEGOVINA ........................................................................................................................ 21 3. BULGARIA .................................................................................................................................................. 24 4. CROATIA .................................................................................................................................................... 26 5. FY REPUBLIC OF MACEDONIA ...................................................................................................................... 29 6. MOLDOVA .................................................................................................................................................. 30 7. ROMANIA .................................................................................................................................................. 32 8. SERBIA AND MONTENEGRO.......................................................................................................................... 34

A. SERBIA .................................................................................................................................................. 35 B. MONTENEGRO ........................................................................................................................................ 38

APPENDIX 1.. MMIINNIISSTTEERRIIAALL SSTTAATTEEMMEENNTT ...................................................................................................... 41

APPENDIX 2.. LLIISSTT OOFF PPAARRTTIICCIIPPAANNTTSS TTOO TTHHEE DDRRAAFFTTIINNGG SSEESSSSIIOONN ........................................................ 45

PPAARRTT TTWWOO:: CCOOUUNNTTRRYY RREEVVIIEEWWSS .................................................................................................................... 49

Chapter 3.. AALLBBAANNIIAA ............................................................................................................................................ 51

1. INTRODUCTION .............................................................................................................................................. 51 2. DETERMINANTS OF EXISTING AND FUTURE FDI INFLOWS IN ALBANIA .................................................................... 51 3. TRANSITION PROCESS IN ALBANIA, AND THE FDI REGULATORY FRAMEWORK AND POLICIES .................................... 53 4. THE LEGAL AND REGULATORY MEASURES FOR FDI IN ALBANIA: GENERAL MEASURES ............................................ 54 5. THE LEGAL AND REGULATORY FRAMEWORK FOR FDI: SECTORIAL MEASURES ........................................................ 58 6. OTHER RELEVANT ELEMENTS OF FDI FRAMEWORK .............................................................................................. 61

Chapter 4. BBOOSSNNIIAA AANNDD HHEERRZZEEGGOOVVIINNAA ........................................................................................................ 69

1. INTRODUCTION .............................................................................................................................................. 69 2. INVESTMENT OPPORTUNITIES AND BARRIERS IN BOSNIA AND HERZEGOVINA.......................................................... 69 3. THE CONSTITUTIONAL/LEGAL CONTEXT OF BOSNIA AND HERZEGOVINIA,

CURRENT STATUS OF THE TRANSITION PROCESS AND MAJOR FUTURE TASKS.......................................................... 70 4. THE LEGAL AND REGULATORY MEASURES FOR FDI: GENERAL MEASURES .............................................................. 72 5. THE LEGAL AND REGULATORY FRAMEWORK FOR FDI: SECTORAL MEASURES .......................................................... 77 6. OTHER RELEVANT ELEMENTS OF FDI FRAMEWORK .............................................................................................. 80

Chapter 5. BBUULLGGAARRIIAA ........................................................................................................................................ 91

1. INTRODUCTION .............................................................................................................................................. 91 2. INVESTMENT OPPORTUNITIES AND BARRIERS IN BULGARIA .................................................................................. 91 3. TRANSITION PROCSS IN BULGARIA, AND FDI STRATEGY AND POLICIES .................................................................. 94 4. THE LEGAL AND REGULATORY MEASURES FOR FDI: GENERAL MEASURES .............................................................. 95 5. THE LEGAL AND REGULATORYFRAMEWORK FOR FDI: SECTORAL MEASURES ........................................................ 101 6. OTHER RELEVANT ELEMENTS OF FDI FRAMEWORK ............................................................................................ 105

77NATIONAL TREATMENT OF INTERNATIONAL INVESTMENT IN SOUTH EAST EUROPEAN COUNTRIES – © OECD 2003

Chapter 6.. CCRROOAATTIIAA .......................................................................................................................................... 115

1. INTRODUCTION ............................................................................................................................................ 1152. THE DETERMINANTS OF FDI INFLOWS: INVESTMENT OPPORTUNITIES AND BARRIERS IN CROATIA............................ 1153. ECONOMIC TRANSITION IN CROATIA: THE DEVELOPMENT OF

THE REGULATORY FRAMEWORK AND FDI STRATEGY AND POLICIES ...................................................................... 1164. THE LEGAL AND REGULATORY MEASURES FOR FDI: GENERAL MEASURES ............................................................ 1175. THE LEGAL AND REGULATORY FRAMEWORK FOR FDI: SECTORAL MEASURES ........................................................ 1216. OTHER RELEVANT ELEMENTS OF FDI FRAMEWORK ............................................................................................ 125

Chapter 7. FFYY RREEPPUUBBLLIICC OOFF MMAACCEEDDOONNIIAA .................................................................................................... 137

1. INTRODUCTION ............................................................................................................................................ 1372. DETERMINANTS OF EXISTING AND FUTURE FDI INFLOWS .................................................................................. 1373. THE LEGAL AND REGULATORY MEASURES FOR FDI: GENERAL MEASURES ............................................................ 1384. THE LEGAL AND REGULATORY FRAMEWORK FOR FDI: SECTORAL MEASURES ........................................................ 1405. OTHER RELEVANT ELEMENTS OF FDI FRAMEWORK ............................................................................................ 141

Chapter 8.. MMOOLLDDOOVVAA ...................................................................................................................................... 149

1. INTRODUCTION ............................................................................................................................................ 1492. INVESTMENT OPPORTUNITIES AND BARRIERS IN MOLDOVA ................................................................................ 1493. TRANSITION PROCESS AND FDI STRATEGY/POLICY IN MOLDOVA .......................................................................... 1504. THE LEGAL AND REGULATORY MEASURES FOR FDI: GENERAL MEASURES ............................................................ 1515. THE LEGAL AND REGULATORY FRAMEWORK FOR FDI: SECTORAL MEASURES ........................................................ 1536. OTHER RELEVANT ELEMENTS OF FDI FRAMEWORK ............................................................................................ 155

Chapter 9. RROOMMAANNIIAA ........................................................................................................................................ 161

1. INTRODUCTION ............................................................................................................................................ 1612. DETERMINANTS OF EXISTING AND FUTURE FDI INFLOWS IN ROMANIA ................................................................ 1613. TRANSITION PROCESS IN ROMANIA AND FDI STRATEGY AND POLICIES ................................................................ 1634. THE LEGAL AND REGULATORY MEASURES FOR FDI: GENERAL MEASURES ............................................................ 1665. THE LEGAL AND REGULATORY FRAMEWORK FOR FDI: SECTORAL MEASURES ........................................................ 1686. OTHER RELEVANT ELEMENTS OF FDI FRAMEWORK ............................................................................................ 170ANNEX A. SCHEDULE OF CAPITAL ACCOUNT LIBERALISATION OF ROMANIA .............................................................. 181ANNEX B. INCENTIVES GRANTED BY THE LOCAL AUTHORITIES IN ROMANIA TO INVESTORS ........................................ 183

Chapter 10. SSEERRBBIIAA AANNDD MMOONNTTEENNEEGGRROO .................................................................................................... 185

NOTE ON RECENT CONSTITUTIONAL CHANGES...................................................................................................... 185

SSEERRBBIIAA .......................................................................................................................................................... 1861. INTRODUCTION ............................................................................................................................................ 1862. DETERMINANTS OF FDI INFLOWS .................................................................................................................... 1863. TRANSITION PROCESS IN SERBIA, AND FDI STRATEGY AND POLICIES.................................................................... 1874. THE LEGAL AND REGULATORY MEASURES FOR FDI: GENERAL MEASURES ............................................................ 1895. THE LEGAL AND REGULATORY MEASURES FOR FDI: SECTORAL MEASURES .......................................................... 1936. OTHER RELEVANT ELEMENTS OF FDI FRAMEWORK ............................................................................................ 196

MMOONNTTEENNEEGGRROO ............................................................................................................................................ 2021. INTRODUCTION ............................................................................................................................................ 2022. DETERMINANTS OF EXISTING AND FUTURE FDI INFLOWS .................................................................................. 2023. THE DEVELOPMENT OF MONTENEGRO’S REGULATORY FRAMEWORK, STRATEGY AND POLICIES TOWARDS FDI .......... 2034. THE LEGAL AND REGULATORY MEASURES FOR FDI: GENERAL MEASURES ............................................................ 2045. THE LEGAL AND REGULATORY FRAMEWORK FOR FDI: SECTORAL MEASURES ........................................................ 2076. OTHER RELEVANT ELEMENTS .......................................................................................................................... 208

APPENDIX 3. PPRRIINNCCIIPPAALL CCOONNTTAACCTTSS OONN IINNVVEESSTTMMEENNTT IINN SSOOUUTTHH EEAASSTT EEUURROOPPEE ............................ 213

Table of Contents

88 NATIONAL TREATMENT OF INTERNATIONAL INVESTMENT IN SOUTH EAST EUROPEAN COUNTRIES – © OECD 2003

PPAARRTT OONNEE

SSYYNNTTHHEESSIISS

1111NATIONAL TREATMENT OF INTERNATIONAL INVESTMENT IN SOUTH EAST EUROPEAN COUNTRIES – © OECD 2003

Chapter 1.

RREEGGIIOONNAALL OOVVEERRVVIIEEWW

1. INTRODUCTION

The Ministers of Economy and designated ministers in charge of investment in South East European(SEE) countries held their first ministerial meeting in Vienna on 18 July 2002 where they adopted theMinisterial Declaration on “Attracting Investment to South East Europe: Common Principles and BestPractices.” One of the key principles of this Declaration relates to the importance of national treatment forforeign investors at both the pre and post establishment stage. SEE Ministers declared that exceptionsshould be clearly and precisely formulated and periodically reviewed with a view to phasing them out, inorder to ensure the fair and equitable treatment of domestic and foreign investments. To implement thisprinciple the Declaration called for improved notification and the publication of lists of national measuresproviding exceptions to national treatment and the rationale for maintaining these measures. This reportresponds to that request and was presented to the Second Ministerial meeting held in Vienna on 10-11July 2003. It provided background for the Ministerial Statement (see Appendix 1) and the renewedcommitment by SEE countries to extend national treatment. The explicit objective of the analysis is toidentify national measures providing deviations from national treatment for both incoming investment aswell as activities by already established foreign-controlled enterprises. The information contained in thereport is current as at July 2003.

NNaattiioonnaall ttrreeaattmmeenntt iiss tthhee ccoommmmiittmmeenntt ooff aa ccoouunnttrryy ttoo aaccccoorrdd ttoo ffoorreeiiggnn iinnvveessttoorrss aanndd ttoo ffoorreeiiggnn-ccoonnttrroolllleedd eenntteerrpprriisseess iinn iittss tteerrrriittoorryy ttrreeaattmmeenntt nnoo lleessss ffaavvoouurraabbllee tthhaann tthhaatt aaccccoorrddeedd iinn lliikkee ssiittuuaattiioonnss ttooddoommeessttiicc eenntteerrpprriisseess.. National treatment is the basic principle of the OECD liberalisation instruments,most notably of the OECD Declaration and Decisions on International Investment and MultinationalEnterprises and the Code of Liberalisation of Capital Movements. Therefore, national measures providingexceptions to national treatment represent a deviation from OECD principles and rules in the area offoreign direct investment. This holds for de jure as well as for de facto deviations from national treatment.While de jure measures mean explicitly formulated deviations from national treatment, de facto measuresmean deviations in the implementation of legal rules, which formally do not discriminate. In this sensethe latter measures can be an even more serious obstacle to foreign investors, since they are hidden and unpredictable.

2. CONCEPTS, METHODOLOGY AND STRUCTURE OF THE REPORT

FFoorreeiiggnn iinnvveessttoorrss in this report are defined as legal entities of one country (iinnvveessttiinngg oorr hhoommee ccoouunnttrryy)investing in another country (hhoosstt ccoouunnttrryy), while foreign-controlled enterprises are enterprises, whichoperate in the territory of a particular country and are owned or controlled directly or indirectly bynationals of other countries. The major concepts used in the report are as follows:

National treatment in pre-establishment is the commitment of a (host) country to accord to theinvestment by non-resident enterprises in its territory, including the right of establishment, treatment noless favourable than that accorded in like situations to resident enterprises. Deviations from nationaltreatment in pre-establishment includes any limitations on non-resident (as opposed to resident)investors affecting their operations and other requirements set at the time of entry or establishment; for

instance, prohibition of foreign investment in certain sectors, ceilings of foreign equity share, prohibitionof foreign acquisitions, prohibition of foreign investment in certain geographical areas, authorisationprocedures, specific corporate organisation requests, etc.

NNaattiioonnaall ttrreeaattmmeenntt iinn ppoosstt-eessttaabblliisshhmmeenntt is the commitment of a (host) country to accord to foreign-controlled enterprises operating in its territory treatment, under its laws, regulations and administrativepractices, no less favourable than that accorded in like situations to domestic enterprises. Deviationsfrom national treatment in post-establishment includes any limitations set on activities of alreadyestablished foreign-controlled (as opposed to domestic) enterprises; for instance, general authorisationor licensing requirements, limitations on acquisition or expansion of activities, ceilings on foreignownership, grants or financial assistance for specific activities, higher or special taxes, public work projectsreserved to local firms, etc.

EExxcceeppttiioonnss concern measures that do not conform to the national treatment principle because theytreat foreign controlled-enterprises different, i.e. less favourably than their domestic counterparts in likesituations. Measures, which qualify as exceptions include restrictions banning foreign investment incertain sectors, or requiring authorisation or licensing as prerequisites for investment, setting ceilings onforeign ownership, etc. For example, if authorisation for acquisition of a majority equity share in acompany is requested in general it is not an exception to national treatment, however, if this authorisationis requested only in the case when the acquirer is a foreign-controlled enterprise, this constitutes anexception to national treatment. In the report exceptions are classified into those related to:

a. Investment by foreign investors and by established foreign-controlled enterprises, with twosubgroups of measures related to: (i) approval and licensing/screening procedures and (ii) equityand other discriminatory measures on establishment and/or expansion.

b. Corporate organisation.c. Employment of foreigners and movement of key personnel.d. Privatisation.e. Government procurement.

TTrraannssppaarreennccyy iitteemmss concern measures that discriminate against foreign-controlled enterprises but aremotivated by reasons of public order and essential security interests, and other means that do notdiscriminate against foreign-controlled enterprises, but nevertheless represent an impediment to foreigninvestment. Transparency measures include restrictions on activities in areas covered by publicmonopolies and concessions, public aids and subsidies granted to government-owned enterprises by thestate as a shareholder in the enterprises concerned, and corporate organisation requirements concerningthe nationality of management or director positions in host countries. In the report transparency measuresare classified into those related to:

a. Security considerations, which relate to approvals, general/equity restrictions, location restrictions, etc.b. Public order considerations, which also relate to approvals, general/equity restrictions, location

restrictions, etc.c. Nationality of management.

Measures and transparency items are either trans-sectoral, being applied for all the sectors, orsectoral, being applied only in individual sectors .

The countries reviewed in the report are all the signatories of the Ministerial Declaration on “AttractingInvestment to South East Europe: Common Principles and Best Practices” (July 2002), i.e. Albania, Bosniaand Herzegovina, Bulgaria, Croatia, Republic of Macedonia (hereafter Macedonia), Moldova, Romania,Serbia and Montenegro. The report is based on the following sources: (i) field work of project teammembers, (ii) Questionnaire for the Identification of Deviations from National Treatment for IncomingInvestment and for Activities by Established Foreign-Controlled Enterprises prepared for the project and responded to by the Country Economic Team Leaders (Albania, Bosnia and Herzegovina, Bulgaria),

1. Regional Overview

1122 NATIONAL TREATMENT OF INTERNATIONAL INVESTMENT IN SOUTH EAST EUROPEAN COUNTRIES – © OECD 2003

(iii) available analysis, reports, guides, web pages, articles, etc., (iv) comments and suggestions of theparticipants of the Drafting Session of the 2nd Ministerial Conference Attracting Investment to South EastEurope: Removing Obstacles, held in Bucharest, 5-6 June 2003 (see Appendix 1).

The report contains two parts. This document is the first part and presents a Regional Overview ofnational measures providing exceptions to national treatment in South East European countries. The secondpart contains detailed presentations of national measures by individual countries. Recommendations forthe strengthening of national treatment principles and for the gradual phasing out of exceptions are givenon the general level for all the countries, as well as specifically for individual countries, in this second part.

3. OVERVIEW OF MEASURES

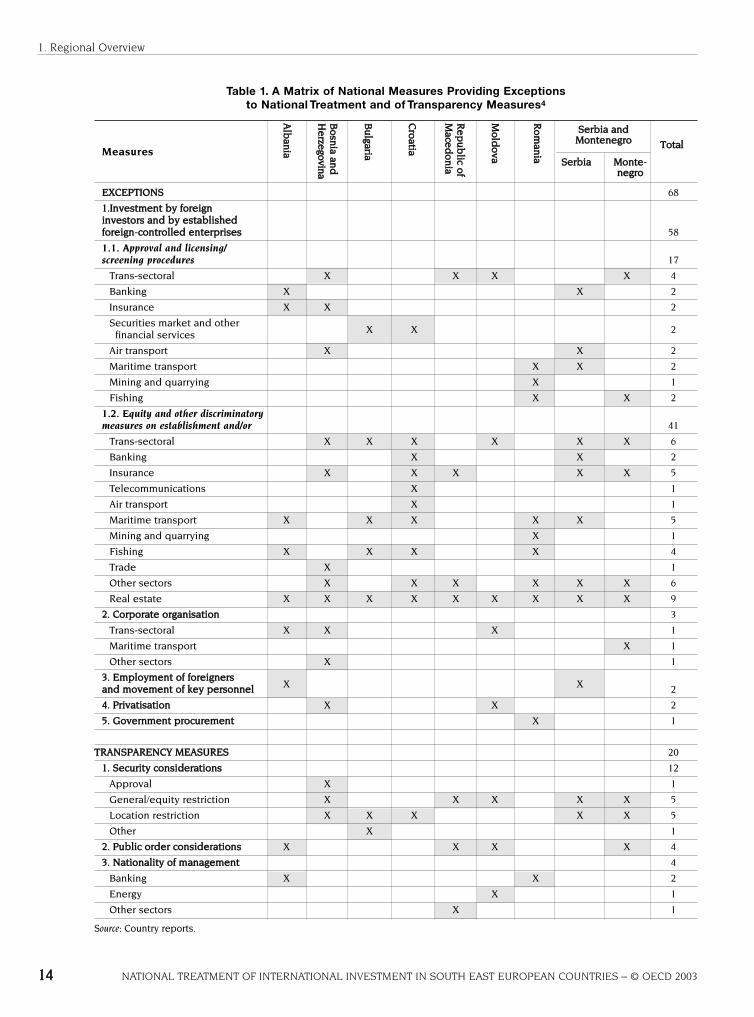

AA MMaattrriixx ooff NNaattiioonnaall MMeeaassuurreess PPrroovviiddiinngg EExxcceeppttiioonnss ttoo NNaattiioonnaall TTrreeaattmmeenntt aanndd ooff TTrraannssppaarreennccyyMMeeaassuurreess (see Table 1) provides an overall summary of exceptions and transparency measures inindividual SEE countries and in the region as a whole. The major intention of the matrix is to show thefrequency of individual country exceptions and transparency measures and in the region as a whole.

The analysis has revealed that eight SEE countries altogether have exceptions in 68 fields. Therespective number for transparency measures is 202. By far the most frequent type of exception measuresrelate to:

• Equity and other discriminatory measures on establishment and/or expansion (41 out of 68exceptions),

• Measures in the field of approval and licensing/screening procedures (17 out of 68 exceptions) • Corporate organisation measures (5). • Exceptions in the field of employment of foreigners and movement of key personnel, privatisation and

government procurement are very few.

Among the transparency measures, the most frequent are those related to: • Security considerations (12 out of 20 transparency measures), • Nationality of management requests (4) • Public order considerations (4).

3.1. Exceptions

Exceptions in the field of aauutthhoorriissaattiioonn aanndd lliicceennssiinngg//ssccrreeeenniinngg pprroocceedduurreess relate to various approval,authorisation, licensing/screening and registration procedures for foreign investors and foreign-controlledenterprises. Four countries (Bosnia and Herzegovina, Republic of Macedonia, Moldova and Montenegro)have trans-sectoral measures of this kind. They relate to the permission of each foreign investment,approval for the establishment of a branch, approval of larger foreign investments and specific registrationprocedures for foreign-controlled enterprises. The overwhelming trend in the world is the elimination oftrans-sectoral authorisations and licensing/screening procedures. It is broadly recognised that theyrepresent an unnecessary administrative barrier, which complicates life for foreign investors and makesthe investment climate of a host country less attractive and unpredictable.

Almost all the SEE countries also have authorisation and licensing/screening procedures in individualsectors. The sectors, which are subject to such procedures, are the banking sector, insurance, securitiesmarket, air transport, maritime transport, fishing, and mining and quarrying. Most of these procedures inbanking, insurance and securities market are in the context of prudential regulation.

The following are the main features of exceptions in the field of eeqquuiittyy aanndd ootthheerr ddiissccrriimmiinnaattoorryymmeeaassuurreess oonn eessttaabblliisshhmmeenntt aanndd//oorr eexxppaannssiioonn:

a. Six countries (Bosnia and Herzegovina, Bulgaria, Croatia, Moldova, Serbia, and Montenegro) havecertain types of ttrraannss-sseeccttoorraall mmeeaassuurreess which restrict the establishment and/or expansion of

1. Regional Overview

1133NATIONAL TREATMENT OF INTERNATIONAL INVESTMENT IN SOUTH EAST EUROPEAN COUNTRIES – © OECD 2003

1. Regional Overview

1144 NATIONAL TREATMENT OF INTERNATIONAL INVESTMENT IN SOUTH EAST EUROPEAN COUNTRIES – © OECD 2003

Table 1. A Matrix of National Measures Providing Exceptions to National Treatment and of Transparency Measures4

Measures

EEXXCCEEPPTTIIOONNSS 68

11..IInnvveessttmmeenntt bbyy ffoorreeiiggnn iinnvveessttoorrss aanndd bbyy eessttaabblliisshheedd ffoorreeiiggnn-ccoonnttrroolllleedd eenntteerrpprriisseess 58

1.1. Approval and licensing/ screening procedures 17

Trans-sectoral X X X X 4

Banking X X 2

Insurance X X 2

Securities market and otherfinancial services X X 2

Air transport X X 2

Maritime transport X X 2

Mining and quarrying X 1

Fishing X X 2

1.2. Equity and other discriminatory measures on establishment and/or 41

Trans-sectoral X X X X X X 6

Banking X X 2

Insurance X X X X X 5

Telecommunications X 1

Air transport X 1

Maritime transport X X X X X 5

Mining and quarrying X 1

Fishing X X X X 4

Trade X 1

Other sectors X X X X X X 6

Real estate X X X X X X X X X 9

22.. CCoorrppoorraattee oorrggaanniissaattiioonn 3

Trans-sectoral X X X 1

Maritime transport X 1

Other sectors X 1

33.. EEmmppllooyymmeenntt ooff ffoorreeiiggnneerrss aanndd mmoovveemmeenntt ooff kkeeyy ppeerrssoonnnneell X X 2

44.. PPrriivvaattiissaattiioonn X X 2

55.. GGoovveerrnnmmeenntt pprrooccuurreemmeenntt X 1

TTRRAANNSSPPAARREENNCCYY MMEEAASSUURREESS 20

11.. SSeeccuurriittyy ccoonnssiiddeerraattiioonnss 12

Approval X 1

General/equity restriction X X X X X 5

Location restriction X X X X X 5

Other X 1

22.. PPuubblliicc oorrddeerr ccoonnssiiddeerraattiioonnss X X X X 4

33.. NNaattiioonnaalliittyy ooff mmaannaaggeemmeenntt 4

Banking X X 2

Energy X 1

Other sectors X 1

Source: Country reports.

RRoo

mmaann

iiaa

MMoo

llddoo

vvaa

RRee

ppuu

bblliicc oo

ffMM

aacceedd

oonn

iiaa

CCrroo

aattiiaa

BBuu

llggaarriiaa

BBoo

ssnniiaa aann

ddHH

eerrzzeeggoovviinnaa

AAllbb

aanniiaa TToottaall

SSeerrbbiiaa aannddMMoonntteenneeggrroo

SSeerrbbiiaa MMoonnttee-nneeggrroo

foreign-controlled enterprises in general. These trans-sectoral measures typically put forward thereciprocity condition. Denial of national treatment due to a reciprocity consideration conflicts withthe multilateral approach to international economic relations as embodied in the national treatmentinstrument of the OECD. A very important reason for allowing foreign-controlled enterprises toengage in business on the same basis as domestic firms is the benefit of that investment flow to thehost country regardless of whether the home country of that firm provides equal treatment to hostcountry firms . Also, it is very difficult to implement the reciprocity principle in practice, which is whyit may become a real obstacle for foreign investors.

b. The most numerous are exceptions related to ffoorreeiiggnn rreeaall eessttaattee oowwnneerrsshhiipp, which is restricted inone or the other way in all of the analysed countries. The real estate restrictions typically apply toagricultural land and/or residential ownership and/or request reciprocity, while foreign-controlledcompanies established under the national law are as a rule given the same rights as indigenousnatural and legal persons. Sometimes foreigners are permitted limited real estate rights (to buildand to use), ownership rights on buildings, or the ownership rights are linked to business purposes.It is a necessity to enable foreign investors and foreign-controlled enterprises normal access to realestate for the purpose of operating the investment. Long term leases, which may be subject toperiodical adjustment of lease payments are not an equivalent solution unless their duration is atleast 50 years.

c. SSeeccttoorraall rreessttrriiccttiioonnss are the most frequent in insurance (Bosnia and Herzegovina, Croatia, Republicof Macedonia, Serbia, Montenegro), maritime (cabotage) transport (Albania, Bulgaria, Croatia,Romania, Serbia) and fishing (Albania, Bulgaria, Croatia, Romania). Other sectors include banking,telecommunications, air transport, audit and legal services, gaming, trade and handicrafts. Typicalmeasures are restrictions on foreign equity or requests for local equity/partner participation andreciprocity requests. While air transport, maritime transport and fishing might be considered asbeing a specific case in many countries, restrictions in sectors like banking, telecommunications,trade and other business services oppose the basic development needs of SEE countries. Businessservices, being among the major promoters of modern economies, are relatively under representedin the whole region.

Exceptions in the field of business activities of foreign-controlled enterprises are relatively few andrelate to: (i) employment of foreign personnel, (ii) government procurement and (iii) privatisation.Privatisation related exceptions are in the context of mass privatisation schemes and are actually of atemporary nature. There is still reluctance in a number of countries to allow the employment of foreignskilled personnel and these restrictions can affect the viability and progress of the investment. Explicit orimplicit discrimination in government procurement should be considered not only a violation of nationaltreatment but also as a reduction of the level of competition on the local market and a sub-optimal useof government resources.

3.2. Transparency measures

Seven of the analysed countries (all except Albania and Romania) have some kind of transparencymeasures related to the security considerations and in four countries (Albania, Republic of Macedonia,Moldova, Romania) these measures relate to public order considerations. Typical mmeeaassuurreess rreellaatteedd ttoosseeccuurriittyy ccoonnssiiddeerraattiioonnss are foreign equity limitation and/or request for approval in the armamentsproduction and/or trade, and restrictions and/or approvals for foreign-controlled enterprises to locateand/or to acquire real estate in military zones and/or in border zones. Similarly, measures related topublic order considerations usually relate to foreign equity limitation and/or request for approval in thefield of medical treatment, production of narcotic, toxic material, acquisition of real estate of historicaland/or cultural relevance and/or in natural parks, the respecting of established social order and moralnorms, etc. In a number of the afore-mentioned activities, the national regulation requests licensing assuch and establishes specific supervision; in such context it is not clear why foreign investors or foreign-controlled companies should be treated specifically on the grounds of public order considerations. Four

1. Regional Overview

1155NATIONAL TREATMENT OF INTERNATIONAL INVESTMENT IN SOUTH EAST EUROPEAN COUNTRIES – © OECD 2003

of the analysed countries (Albania, Republic of Macedonia, Moldova, and Romania) also pose requestsrelated to local nnaattiioonnaalliittyy ooff mmaannaaggeemmeenntt. In two countries this request is of a trans-sectoral character,while most requirements are present in the banking, energy and gaming.

4. GENERAL RECOMMENDATIONS

The matrix gives information on the most common (typical) measures providing exceptions to nationaltreatment in SEE countries in general and in individual countries. As such it offers guidelines forindividual countries on where to concentrate efforts in strengthening the national treatment principle.Two considerations are important in this regard.

The first is that SEE countries face a number of major problems, such as economic and politicalinstability, transition process and underdevelopment. Furthermore, to varying degrees, they lack marketinstitutions and related regulatory framework, and have considerable difficulties in implementing existinglaws and regulations. These factors have served to reduce their attractiveness as investment location. Inthis broader overall business climate context, eelliimmiinnaattiioonn ooff mmeeaassuurreess pprroovviiddiinngg eexxcceeppttiioonnss ttoo nnaattiioonnaallttrreeaattmmeenntt sshhoouulldd bbee ccoonnssiiddeerreedd aammoonngg tthhee bbaassiicc pprreerreeqquuiissiitteess ffoorr ccrreeaattiinngg aa ffrriieennddllyy iinnvveessttmmeenntteennvviirroonnmmeenntt. Foreign investors do consider the exceptions to national treatment as important obstaclesand also as a reflection of host country governments’ attitude to foreign investors. Providing nationaltreatment to foreign investors is usually perceived internationally as an important indicator of thecountry’s willingness to welcome foreign investment.

The second consideration is that one should not expect SEE countries to move towards a generalelimination of exceptions and transparency measures. Some of these measures are also present in anumber of OECD countries as well and are of a quasi permanent nature, while others are of a rathertemporary nature (for instance those related to the privatisation processes) and will disappear in thetransition process. However, a thorough revision of existing exceptions and transparency measures shouldbe undertaken by each SEE country in order to define: (i) those which present a serious obstacle toforeign investors and foreign-controlled enterprises and whose elimination would obviously bringbenefits to host countries and (ii) those, which seem to be unnecessary from the host countries point ofview, and for which the motivation of their existence has not been clearly revealed or has vanished withthe process of political and economic transition.

In endeavouring to strengthen the national treatment principle, the SEE countries agree to take thefollowing key measures over the next year, taking into account the legal situation in each country:

• reduce licensing and approval procedures and special registration procedures, includingreciprocity requirement, for foreign investment, to the level necessary for normal company lawregistration

• take decisive steps with the view to allowing the acquisition of real estate by foreign investors forthe purpose of investment

• reduce reporting requirements of foreign investment for statistical purposes to a minimumnecessary

• establish transparent laws, regulations, procedures and practices regarding governmentprocurement with a view to ensuring full national treatment

• streamline measures relating to work and residence permits so as to allow the movement of keypersonnel for investment

• promote the development of an effective services sector, in particular by removing obstacles toforeign direct investment in the areas of financial and professional services

The country reports also reveal the existence of comprehensive transparency measures in the form ofmonopolies and state aids and subsidies practice in the analysed countries. These measures do notformally discriminate against foreign-controlled enterprises, but also affect domestic enterprises. In thisway, they can represent an impediment to investment, distort competition and prevent new entries in the

1. Regional Overview

1166 NATIONAL TREATMENT OF INTERNATIONAL INVESTMENT IN SOUTH EAST EUROPEAN COUNTRIES – © OECD 2003

sectors. The issues of monopolies of state aids and subsidies are at the heart of the transition process ofSEE countries, because efficient market structures and institutions are the best guarantee for therestructuring of the SEE economies. Introduction of competition via liberalisation of public utilities andfinancial services, establishment of independent regulatory mechanisms/institutions and privatisation ofstate-owned enterprises are necessary to overcome the huge investment gap of SEE countries in theinfrastructural sector. Surveys of state aids and subsidies are necessary to provide reliable information onthe nature and cost/benefit of these measures. The present situation is such that countries do not alwaysknow how much state aid individuals or enterprises obtain from various sources. A survey would providecountries with better chances: (i) to ensure that public finance is used efficiently, (ii) to monitor the resultsof state aids and subsidies policy and (iii) to reduce them as far as possible.

The national treatment review of SEE countries also reveals quite frequent national managementrequirements in companies. These measures are usually based on perceived national security and publicorder considerations and are therefore classified under the transparency measures. SEE governmentsmay nevertheless consider the elimination of these requirements, since it is in their interest to attractmanagement skills to their country. The spread of modern management knowledge and techniques fromforeign to domestic managers and from foreign-controlled to domestic companies represents one of themost appreciated and beneficial spill-over effects of FDI. Any restrictions on foreign managementparticipation reduce the scope for this kind of spill-over effects and the full maximisation of the benefitsof FDI in the host country.

1. Regional Overview

1177NATIONAL TREATMENT OF INTERNATIONAL INVESTMENT IN SOUTH EAST EUROPEAN COUNTRIES – © OECD 2003

1. Regional Overview

1188 NATIONAL TREATMENT OF INTERNATIONAL INVESTMENT IN SOUTH EAST EUROPEAN COUNTRIES – © OECD 2003

NNOOTTEESS

1. For detail on the subject see especially OECD. 1993. National Treatment for Foreign-Controlled Enterprises.Paris: Organisation for Economic Co-Operation and Development.

2. The actual number of exceptions and transparency measures is higher because individual countrieshave more than one measure in a particular category.

3. See especially OECD. 1993. National Treatment for Foreign-Controlled Enterprises. Paris: Organisation forEconomic Co-Operation and Development, p. 24.

4. Sign “X” in the matrix means that a particular category of exceptions/transparency measures exists ina country. A country might apply one or more measures in a particular category.

1199NATIONAL TREATMENT OF INTERNATIONAL INVESTMENT IN SOUTH EAST EUROPEAN COUNTRIES – © OECD 2003

Chapter 2.

SSUUMMMMAARRYY OOFF MMOOSSTT SSIIGGNNIIFFIICCAANNTT NNAATTIIOONNAALL MMEEAASSUURREESS5

1. ALBANIA

FDI inflows in Albania have been relatively low. End-2002 FDI stock was US$ 945 million. Annual FDIinflows in 1997-1999 were US$ 47.5 million, US$ 45 million and US$ 41.2 million, respectively. This is aconsiderable decrease compared to 1996, when the inflow was roughly twice as high. The decline of FDIinflows since 1997 was due to the series of crises, which affected the country; starting with the 1997 civildisturbances that followed the collapse of the pyramid financial schemes; the coup attempt in September1998, and the Kosovo crisis in 1999. In the following years – 2000, 2001, and 2002 – FDI inflows increasedand were US$ 143 million, US$ 207 million USD, and around US$ 143 million, respectively (Bank ofAlbania). The increase is largely explained by the improvement in the overall investment climate in thecountry and by the role of the privatisation process. In 2002, the FDI inflow was much lower than in 2001due to the non-realisation of the privatisation programmes of some strategic state companies.

Out of 61,859 active enterprises in Albania at the end of 2001, 1,793 (2.9 percent) were partly foreign-owned companies (joint ventures) and 1,122 (1.8 percent) were wholly foreign-owned companies. In termsof numbers, 58.5 percent of all foreign-controlled companies is in trade and retailing, 21.2 percent inindustry, 9.7 percent in services, 5.9 percent in construction, 3.8 percent in transport, and only 0.9 percentin agriculture (INSTAT, end-2001 data). In terms of value, 27 percent of total FDI stock is in trade, 21.2percent in textile and leather manufacturing, 6.4 percent in food, beverages and tobacco, 6.2 percent inconstruction and 24.3 percent in other sectors. (Bank of Albania, end-2001 data). The only two relevantinvesting countries in Albania are Italy (48 percent of end-2001 FDI stock) and Greece (43 percent),followed by Republic of Macedonia and Turkey (2.2 percent each); the rest 6.8 percent is distributedamong other countries of Europe and USA. Foreign investments are mainly concentrated in the maindistricts of the country such as the capital of Tirana and Durres, which is the largest port handling most ofthe import-export activities. 67 percent of all foreign-controlled companies operate in these two locations.

1.1. General legislative framework for investment

Since the beginning of transition and the opening up process of the country, attracting FDI in Albaniahas been considered of critical importance for achieving the main growth, development and transitiongoals. The main piece of legislation related to FDI in Albania is the Law “On Foreign Investment” (No.7764, date 2.11.1993), which aims to ensure a favourable investment climate for foreign investors in thecountry. Subject to a limited number of exceptions, the investment conditions for foreigners are asfavourable as for local investors, i.e. national treatment principle is applied. Apart from extending thenational treatment, foreign investors are also given a number of guarantees, such as: (i) no priorauthorization is needed for foreign investments; (ii) there is no limitation on the percentage share offoreign participation in companies, 100 percent foreign ownership is possible; (iii) foreign investment maynot be expropriated or nationalised directly or indirectly, except for special cases, in the interest of thepublic use, defined by law. In the case of expropriation, an immediate, appropriate and effectivecompensation is provided; (iv) foreign investors have the right to expatriate all funds and contributionsin kind related to investments; (v) most favourable treatment according to international agreements is

also provided. The Republic of Albania has signed agreements with a number of countries for mutualprotection of investments and for avoiding the double taxation.

1.2. Exceptions

Investment by foreign investors and by established foreign-controlled enterprises

Banking – Authorisation. Foreign bank that proposes to own more than 10 percent of the authorisedcapital of a bank in Albania, should receive permission by the respective authority to engage in thebusiness of accepting and collecting money deposits or of other repayable funds in the country where itshead office is located. The foreign authority, which supervises the financial activity of the head office ofthe foreign bank, gives its written consent for granting such a licence. With the correct interpretation of“Regulation 45", the banking industry is well regulated and open to FDI.

Insurance – Authorisation. The conditions a foreign company must fulfil to get the authorisation from theAlbanian Insurance Supervisory Commission to perform insurance activities in Albania are: (i) to beauthorised for carrying out insurance activities according to the legislation of the home country and tohave at least 5 years experience in insurance activities; (ii) to establish a branch, which will carry outinsurance operations in Albania; (iii) to assume that this branch will keep and maintain special accountingand all documents related to its activity; (iv) to have in Albania assets at a value of at least ½ of minimumguarantee fund defined by one of the articles of the law and to deposit ¼ of this minimum fund as aguarantee, which will be reimbursed in case the authorisation is not issued; (v) to meet the solvencymargin; (vi) to submit a business programme.

Maritime Transport – Cabotage. Based on International Regulations but also on national legislation, onlyAlbanian ships flying Albanian flag are allowed to exercise activity in the inner maritime transport(cabotage). An Albanian register of ships does not yet exist.

Fishing. According to Article 19 of the Law “On Fishery and Aquaculture” (No. 7908, date on 5.4.1995),the Ministry of Agriculture and Food exclusively may issue licences for fishing, or other activities relatedto fishing, to foreign vessels or persons, (i) on the basis of international agreements in force with thecountry to which the foreign vessel or persons belong; or (ii) in cases when the issuing of licence isconsidered: a) necessary for the economy of the country and especially when the applicant undertakesbeneficial investments for the fishery sector in Republic of Albania in line with policies and strategiesformulated for the development of this sector; b) necessary for a sustainable use of resources,considering the national capacity for fishing and its development; c) in compliance with the policy of theRepublic of Albania regarding the foreign investments and especially with the future goals andobjectives of fishery and aquaculture administration plan. Article 20 of the Law says that the issuing oflicences is prohibited for foreign vessels applying for demersal fishing with trawls and fishing and/orcollection of bivalve molluscs.

Real estate – Land ownership. Albanian legislation contains limitation with regard to the right of foreignersto acquire land in Albania. Law “On the Land” (No. 7501, date 15.07.1991, amended in 1993, 1994, 1995),in Articles 3, 4, and 5, does not permit foreigners to buy land. According to this Law foreigners can onlylease the land they need. As for leasing, foreigners receive the same treatment as nationals. The rationalebehind this measure is to prevent speculation with land by foreigners, considering the weak financialpower of the Albanian citizens for the last decade.

Real estate – Land ownership. According to the Law “On Acquisition of Plots” (No. 7980, date 27 July 1995,amended in 1997), Article 5, foreign investors are entitled to buy state-owned non-agricultural landprovided that the value of investment is at least three times higher than the value of the land. From themoment of getting the construction permit until s/he gets the ownership of the plot, the foreign natural orlegal person pays the rent for using the plot. The rent is agreed in the contract. The price of eventual landacquisition is also predetermined in the contract as well as for how long this price is valuable. The Council

2. Summary of Most Significant National Measures

2200 NATIONAL TREATMENT OF INTERNATIONAL INVESTMENT IN SOUTH EAST EUROPEAN COUNTRIES – © OECD 2003

of Ministers determines the value of such land. (Article 8). The rationale behind this measure is thepromotion of investments and site developments.

Public health. According to the Order of Minister of Health “On Licence Granting for Health ProfessionalPractice in Free Private Activity", point 3/1 (No. 108, date 19.04.2002), the licensing of foreigners in the fieldof health care is possible only if they cooperate with an Albanian professional in the field of activity to bepractised. The purpose of introducing this measure is to ensure: (i) a better communication with thepatients; (ii) a better relationship with the Albanian government (for fiscal and administrative purposes).

Corporate organisation

Trans-sectoral – Registration fees. Costs related to the registration of the company are 1,500 Lekë when theshareholders are Albanian nationals or national companies, and 5,000 Lekë in case one of theshareholders is a foreign national/company.

Employment of foreigners and movement of key personnel

Trans-sectoral – Employment of foreigners. To be able to work in Albania a foreign national should obtain awork permit issued by the Ministry of Labour and Social Affairs. Among the documents, which shouldaccompany the application form for a work permit, is also the “written and proven confirmation from theemployer testifying that for each foreign employee, s/he has employed two Albanian citizens". Therationale of this condition is the promotion of employment of local workers and also the promotion ofemployment of qualified foreign personnel (Law “On Issuing of Work Permit to Foreigners", No. 8492, date27.05.1999 and accompanying by-laws).

1.3. Transparency measures

Nationality of management

Banking. The branch of a foreign bank must employ at least two resident administrators foradministration of the branch of the foreign bank.

2. BOSNIA AND HERZEGOVINA

FDI inflows in Bosnia and Herzegovina (BiH) in 1994-2002 totalled US$ 848 million; 70 percent of that inthe last three years and as much as 35 percent in the last year (in 2000 US$ 147 million, in 2001 US$ 130million and in 2002 US$ 321 million). Most of FDI came in cash (60.1 percent), the rest being in the form oftangible and intangible assets (36.3 percent) and in the form of rights (3.6 percent). The major recipient ofFDI (1994-2002) has been manufacturing (55.5 percent), followed by banking (16.5 percent) and trade andservices (13 percent). The most important investing countries in BiH in 1994-2002 were Croatia (US$ 124million), Kuwait (US$ 117 million), Slovenia (US$ 99 million), Austria (US$ 92 million), Germany (US$ 92million), Serbia and Montenegro (US$ 69 million) and the Netherlands (US$ 62 million). Of the total FDI stock42 percent is allocated in 15 companies, the largest being Kuwait Consulting Investment Company with189.785 million of Convertible Marks (KM) (Ministry of Foreign Trade and Economic Relations, April 2003)

2. Summary of Most Significant National Measures

2211NATIONAL TREATMENT OF INTERNATIONAL INVESTMENT IN SOUTH EAST EUROPEAN COUNTRIES – © OECD 2003

RREECCOOMMMMEENNDDAATTIIOONNSS

AAppaarrtt ffrroomm mmeeaassuurreess ttoo bbee ttaakkeenn ttoo ssttrreennggtthheenn tthhee nnaattiioonnaall ttrreeaattmmeenntt pprriinncciippllee aass pprrooppoosseedd iinn ““GGeenneerraallRReeccoommmmeennddaattiioonnss””,, tthhee aauutthhoorriittiieess ooff AAllbbaanniiaa sshhoouulldd ssppeecciiffiiccaallllyy ccoonnssiiddeerr tthhee eelliimmiinnaattiioonn ooff rreessttrriiccttiioonnssrreellaatteedd ttoo:: ((ii)) iissssuuiinngg ooff wwoorrkk ppeerrmmiittss ffoorr ffoorreeiiggnneerrss,, ((iiii)) tthhee lliicceennssiinngg ooff ffoorreeiiggnneerrss iinn tthhee ffiieelldd ooff hheeaalltthhccaarree oonnllyyiiff tthheeyy ccoo-ooppeerraattee wwiitthh aann AAllbbaanniiaann pprrooffeessssiioonnaall,, ((iiiiii)) tthhee rreeqquueesstt tthhaatt tthhee bbrraanncchh ooff aa ffoorreeiiggnn bbaannkk mmuusstt eemmppllooyyaatt lleeaasstt ttwwoo rreessiiddeenntt aaddmmiinniissttrraattoorrss..

2.1. General legislative framework for investment

The basic piece of legislation on FDI in BiH is the Law on the Policy of Foreign Direct Investment(Official Gazette of BiH 17/98). The Law was adopted as a framework law requiring enactment of furtherregulations at the level of the Entities (Federation of Bosnia and Herzegovina – FBiH – and RepublikaSrpska – RS). It is based on national treatment principle, the general rule being that foreign investorsare entitled to invest, and to reinvest profits of such investments into any and all sectors of theeconomy of BiH, and in the same form and under the same conditions as defined for the residents ofBiH under the applicable laws and regulations of BiH and the Entities. The national treatment forforeign investors includes the participation in the process of privatisation; foreign legal and naturalpersons have equal rights as domestic legal and natural persons in the privatisation of state ownedcapital both in FBiH and RS, with reciprocity conditions being applied in some cases. There are norestrictions regarding the legal status of foreign investor. Foreign persons may invest in the same formand under the same conditions as defined for the residents of BiH. This is also true for branch offices.Foreign investors may also open representative offices. Apart from the national treatment, the Law onthe Policy of Foreign Direct Investment in BiH specifically provides for the following rights andguarantees to foreign investors: non-discriminating corporate tax regimes, exemption from payment ofcustoms and customs duties, right to open bank accounts, right to profit and capital repatriation,property rights to real estate, right to employ foreign employees, protection against expropriation,guarantees against legal changes.

2.2. Exceptions

Investment by foreign investors and by established foreign-controlled enterprises

Trans-sectoral – Approval/Registration. According to the latest amendments of the Law on the Policy ofForeign Direct Investment in BiH (Official Gazette of BiH 1798) each foreign investment in BiH shouldreceive a permission of the competent body of the State (Ministry of Foreign Trade and Economicrelations of BiH). It is not necessary to be registered with the competent body of the respective Entity(amendments passed parliamentary procedure and it has to be published in Official Gazette to be inforce). This also applies on registration of foreign representative offices. The competent bodies of theState shall confirm the registration to foreign investors within a strict time limit. The registration of foreigninvestment is confirmed by the Registration Certificate, which is necessary for a foreign-controlledenterprise to be registered at court.

Insurance – Local equity articipation, approval.FBiH. Foreign persons can establish joint stock company for insurance in FBiH only together with

domestic persons. If foreign ownership in insurance company exceeds 50 percent of the share capital itrequires approval of the Ministry of Finance of FBiH (Law on Insurance of Property and Persons of FBiH –Official Gazette of FBiH 2/95, 7/95, 14/97, 6/98, 41/98).

RS. Foreign natural and legal persons can establish joint stock company for insurance in RS onlytogether with domestic persons (Law on Insurance of Property and Persons- Official Gazette of RS 14/00).

Air transport – Approval. To invest in air transport, foreign companies have to get approval from theGovernment of BiH.

Trade – Foreign ownership restriction. According to the Law on Trade of FBiH foreign natural persons cannotbe owners of shops (trade shops) in FBiH. There is a draft of a new Law that will allow foreign citizens tobe the owner of shops under condition of reciprocity.

Handicrafts – Reciprocity. The Law on Handicrafts of FBiH/Law on Handicrafts of RS stipulates that aforeign natural person can open handicraft shop in FBiH/RS under condition of reciprocity.

2. Summary of Most Significant National Measures

2222 NATIONAL TREATMENT OF INTERNATIONAL INVESTMENT IN SOUTH EAST EUROPEAN COUNTRIES – © OECD 2003

Audit and accounting – Local participation. The Law on Audits of FBiH (Official Gazette of FBiH 2/95)/Law onAccounting of RS (Official Gazette of RS 18/99) stipulate that foreign accounting firms and auditors canperform auditing only together with local accounting firms.

Real estate. According to Article 12 of the Law on the Policy of Foreign Direct Investment in BiH, foreigninvestors have the same property rights in respect to real estate as the citizens and legal entities of BiH.There are no corresponding provisions related to real estate in the foreign investment legislation ofeither FBiH or RS. It seems, however, that the wording of Article 12 is misleading, because it appears thatit is foreign-controlled enterprises and not foreign investors which have the same real estate rights asnatural and legal persons of BiH. Namely, in RS and in FBiH, foreign persons (whether residents or non-residents, whether legal entities or natural persons) cannot own property. Under the Law on the Policyof Foreign Direct Investment in BiH, a foreign-controlled enterprise is registered as a domestic legalentity. As a result, under the principle of national treatment, such an enterprise has the same rights as adomestically-owned enterprise or natural person of BiH citizenship, including rights of and ownership ofproperty in BiH.

Real estate – Reciprocity. Foreign investors have the same property rights in respect to real estate as thecitizens and legal entities of BiH. However, foreign investors, who are citizens of one of the successorstates to the former Socialist Federal Republic of Yugoslavia (SFRY), have such rights subject to investorsof BiH citizenship and legal entity status having like rights in a respective successor state (Article 12 of theLaw on the Policy of Foreign Direct Investment).

Corporate organisation

Trans-sectoral – Registration fee. According to FIAS (2001), the court registration fee for foreign-ownedcompanies in the RS is KM 1600 compared to KM 600 for other companies.

Privatisation

Approval.FBiH. If foreign ownership in a company for managing of privatisation investment funds in FBiH

exceeds 10 percent of the share capital it requires approval of the Securities Commission of FBiH.RS. Foreign natural and legal persons can possess more than 10 percent equity share in a privatisation

fund management company in RS only with the previous consent of the Commission for Securities of RS(Article 8 of the Law on Privatisation Investment Funds and Privatisation Fund Management Companiesof RS).

Reciprocity. Enterprises or enterprise assets in the privatisation process of FBiH can not be purchasedby foreign natural and legal entities from those countries where foreign ownership of domestic enterprisesis either limited or excluded by Law (Article 12 of the Law on Privatisation of Enterprises, Official Gazetteof FBiH 27/97, 8/99, 32/00, 45/00, 54/00, 61/01 and 27/02).

Reciprocity. A foreign citizen can purchase an apartment in FBiH under the conditions determined bythis Law only if it is possible for a citizen of BiH to purchase an apartment in the respective country (Article6 of the Law on Sale of Apartments with existing Tenancy Right, Official Gazette of FBiH 27/97).

2.3. Transparency measures

Security considerations

Armaments – Approval. To register a foreign investment in the production and sale of arms, ammunitions,and explosives for military use, military equipment and public information a prior approval of thecompetent body of the respective Entity is necessary (Article 4 of the Law on the Policy of Foreign DirectInvestment in BiH).

2. Summary of Most Significant National Measures

2233NATIONAL TREATMENT OF INTERNATIONAL INVESTMENT IN SOUTH EAST EUROPEAN COUNTRIES – © OECD 2003

Armaments – Foreign ownership restriction. Foreign participation may not exceed 49 percent of the equityof the company and foreign investors must receive a prior approval of the investment from a competentbody in the relevant entity, subject to strict time limits, in the production and sale of arms, ammunitions,and explosives for military use, military equipment and public information. Public information is definedas such that is contained in radio, television (excluding cable), electronic media (excluding Internet),newspapers and other publications produced primarily for the local market (Article 4 of the Law on thePolicy of Foreign Direct Investment).

Location restriction. In the FBiH, wholly foreign owned companies are forbidden to be located in amilitary zone. Wholly foreign-owned companies need confirmation from the Municipal Office of theFederation Ministry of Defence confirming that the business location is not in a military zone (FIAS 2001).The same rules are in practice in RS. Wholly foreign-owned companies are forbidden to be located in amilitary zone. Wholly foreign-owned companies need confirmation from the Ministry of Defence of the RSconfirming that the business location is not in a military zone.

3. BULGARIA

FDI inflows in Bulgaria in 1992-October 2002 totalled US$ 4,927 million, of which US$ 1,583 million (32percent) is in privatisation, and US$ 3,344 million in other FDI (greenfield, additional investment inforeign investment enterprises, reinvestment, joint ventures). Inflows have increased considerably since1997; the period from January 1999 to October 2002 accounted for almost 60 percent of all inflows . Since1998 greenfield FDI is far more substantial than FDI in privatisation (www.bfia.org). Most of the inflowswent to the manufacturing sector (43.4 percent), finance (18.1 percent), sale and repair (15.5 percent),communications (5.4 percent), hotels and restaurants (4.2 percent) etc. Most FDI has came from Germany(12.4 percent), Greece (11.9 percent), Italy (9.9 percent), Belgium (9.2 percent), Austria (7.7 percent), USA(6.1 percent), etc, (1992-2001 data, BFIA 2002).

3.1. General legislative framework for investment

The major piece of legislation on FDI in Bulgaria is the Foreign Investments Act (promulgated in 1997and amended in 1998, 1999 and 2002). The Bulgarian Constitution and the Foreign Investments Actprovide national treatment to foreign investors in pre- and post-establishment. Article 2 of the ForeignInvestments Act says that “a foreign person can make investments in the country by the order stipulatedfor Bulgarian citizens, having equal rights with them, inasmuch as this Act does not provide otherwise, andarticle 8 stipulates that “a company with foreign holding shall have all rights as a company without foreignholding, except in the cases stipulated by this Act". The amount and or the share of the foreign holding innewly founded or existing companies is not restricted. There are no minimum capital requirements. Thenational treatment principle covers the whole range of economic and legal forms of business. Foreignpersons can also register branches and open representative offices in Bulgaria. The national treatment forforeign investors includes the participation in the process of privatisation and acquisition of shares,

2. Summary of Most Significant National Measures

2244 NATIONAL TREATMENT OF INTERNATIONAL INVESTMENT IN SOUTH EAST EUROPEAN COUNTRIES – © OECD 2003

RREECCOOMMMMEENNDDAATTIIOONNSS

IInn oorrddeerr ttoo iimmpprroovvee tthhee iinnvveessttmmeenntt cclliimmaattee iinn tthhee ccoouunnttrryy,, tthhee aauutthhoorriittiieess ooff BBoossnniiaa aanndd HHeerrzzeeggoovviinnaasshhoouulldd ppaayy ssppeecciiaall aatttteennttiioonn ttoo ssttrreennggtthheenniinngg tthhee ccoohheerreennccee ooff tthhee lleeggaall ffrraammeewwoorrkk aanndd aaddmmiinniissttrraattiivveepprraaccttiiccee iinn bbootthh eennttiittiieess,, ttoo rreessoollvvee tthhee pprroobblleemm ooff mmuullttiippllee rreeggiissttrraattiioonnss,, aanndd ttoo iimmpprroovvee tthhee iimmppllee-mmeennttaattiioonn ccaappaacciittyy.. AAppaarrtt ffrroomm mmeeaassuurreess ttoo bbee ttaakkeenn ttoo ssttrreennggtthheenn tthhee nnaattiioonnaall ttrreeaattmmeenntt pprriinncciippllee aasspprrooppoosseedd iinn ““GGeenneerraall rreeccoommmmeennddaattiioonnss"",, tthhee aauutthhoorriittiieess ooff BBoossnniiaa aanndd HHeerrzzeeggoovviinnaa sshhoouulldd ssppeecciiffiiccaallllyyccoonnssiiddeerr tthhee eelliimmiinnaattiioonn ooff tthhee mmeeaassuurreess rreellaatteedd ttoo:: ((ii)) eeqquuiittyy lliimmiittaattiioonn ooff ffoorreeiiggnn iinnvveessttoorrss iinn iinnssuurraann-ccee ccoommppaanniieess aanndd iinn pprriivvaattiissaattiioonn iinnvveessttmmeenntt ffuunnddss,, ((iiii)) tthhee rreeqquueesstt tthhaatt ffoorreeiiggnn-ccoonnttrroolllleedd aaccccoouunnttaannccyyccoommppaanniieess ccaann ppeerrffoorrmm aauuddiittiinngg oonnllyy ttooggeetthheerr wwiitthh llooccaall aaccccoouunnttiinngg ffiirrmmss..

debentures, treasury bonds and other kind of securities. There are no restrictions regarding the legalstatus of foreign investors. Apart from the national treatment, Bulgarian legislation provides the followingguarantees to foreign investors: most favourite nation status, more favourable treatment according tointernational agreement, legal guarantees against adverse legislative changes, and protection againstexpropriation, profit and capital repatriation (BFIA 2002, Ivanov et al. 2002).

3.2. Exceptions

Investment by foreign investors and by established foreign-controlled enterprises

Trans-sectoral – Reciprocity. The provisions of the Foreign Investments Act do not apply entirely orpartially for the investments of foreigners from countries specified by the Council of Ministers where,discriminating measures are applied regarding Bulgarian companies or citizens (Article 3 of ForeignInvestments Act).

Securities market. Foreign persons, who have the permit for carrying out transactions with securities onthe territory of Bulgaria, are obliged to identify their clients and the transactions for their account beforethe Commission within 3 work days from the written request. The names of the foreign persons, who haveacquired securities in their names but for the account of other foreign persons, are entered in the registerof the Central Depository.

Maritime transport – Cabotage. Article 6 of the Merchant Shipping Code stipulates that the cabotagewithin Bulgaria (maritime cabotage) could be carried out by: (i) ships flying Bulgarian flag, (ii) ships flyinga flag of an EU Member State, when they comply with all the conditions for carrying out the cabotage, (iii)ships flying a flag of a third country if this is agreed in International Agreement, to which Bulgaria is a partyor a decision of the Council of Ministers ad hoc. In case of serious disturbances to the domestic market,resulting from market liberalisation, the Minister of Transport and Communications is entitled to notifythe competent EU bodies and bodies of countries with International Agreement of introduction ofderogations from their right to carry out cabotage for a term of up to 12 months.

Conditions for ships to fly the Bulgarian flag. The Bulgarian national flag could be flown by (i) Bulgarian ships,registered in Bulgarian register, (ii) ships, which are under the conditions of bareboat charter, (iii) ships,which are property of natural or legal persons from EU Member States, when they have authorisedBulgarian natural or legal persons to represent them (Article 27 of Merchant Shipping Code). Ship isBulgarian when it is: (i) property of the state, (ii) property of Bulgarian legal or natural person, (ii) morethan 50 percent of the property belongs to Bulgarian legal and natural person, (iv) under the conditionsof bareboat charter (Article 28 of Merchant Shipping Code). A vessel, entered on a foreign register ofvessels, may be entered on a Bulgarian register after having been struck off the foreign register (Article 37of Merchant Shipping Code). Vessels, hired under the terms of bareboat charter contracts, may beentered into the registers, provided the following conditions have been met: (i) hire by a Bulgarian naturalor legal person; (ii) entry on a compatible register; (iii) not being entered on other registers under theterms of a bareboat charter contract; (iv) submission of an excerpt from the principal registration of thevessel, containing a description of the vessel, data regarding the ship-owner and all registered mortgagesand other encumbrances, if any (Article 39a of Merchant Shipping Code).

Fishing. Only national flag vessels may fish in country’s territorial waters (The Executive Agency forFishing and Aquaculture and the Executive Agency “Maritime Administration” are responsible forregistration of fishing ships). Foreign vessel cannot perform industrial fishing in the Bulgarian extremeeconomic zone unless there is an agreement between Bulgaria and the country, under which flag the shipis sailing.

Real estate – Land ownership/Residential property rights. Foreign persons, including through a branch or as asole entrepreneur, cannot acquire ownership of land in Bulgaria. This restriction does not apply tocompanies with foreign participation, irrespective of the foreign equity share, incorporated under the

2. Summary of Most Significant National Measures

2255NATIONAL TREATMENT OF INTERNATIONAL INVESTMENT IN SOUTH EAST EUROPEAN COUNTRIES – © OECD 2003

Bulgarian legislation. The same rule applies with regard to residential property rights (Article 23 of ForeignInvestments Act). Foreign persons may acquire ownership rights on buildings and limited ownershiprights (right to build and right to use) on real estate in Bulgaria (Article 3 of the Foreign Investments).

Residence. Long term residence permits cannot be obtained by foreign persons performing commercialactivity in Bulgaria and employing less than 10 Bulgarian citizens.

3.3. Transparency measures

Security considerations