Embed Size (px)

Citation preview

Dixon: National Provident Funds 197

National Provident Funds: The Challenge of Harmonizing Their Social

Security, Social and Economic Objectives

John Dixon Monash University

This paper examines the national provident funds (NPFs) that oper- ate in 23 developing countries which seek to provide their members with basic social security protection by means of compulsory savings (see Appendix). It explores how the juxtaposition of economic, social and social security objectives has made NPFs generally resilient to fundamenfal change and has, in some instances, resulted in the evolution of a social security hybrid-neither a pure compulsory savings scheme nor a social insurance system.

NATIONAL PROVIDENT FUNDS AS A SOCIAL SECURITY CONCEPT

NPFs are, in their purist form, compulsory savings schemes (see Dixon, 1982, 1985, 1986, 1987, 1989, 1990). Covered em- ployees and their employers pay regular contributions to a central, publicly supervised fund where the contributions are credited to a separate account maintained for each employee. The balance in this account accrues interest and is payable in a lump sum upon the occurrence of specified contingencies (typi- cally, old age, retirement, disability or death). This approach to providing social security involves no risk poolings, preventing income transfer among individual members.

NPFs advance the proposition that acceptable social secu- rity protection can be provided by means of compulsory sav- ings without risk-pooling. This proposition has a most curious corollary: As NPF members are able to identify their social security savings, they tend to claim proprietary rights over them. This brings into question, of course, whether or not social security should be defined narrowly (in terms of income sup- port) or broadly (so as to include quality-of-life factors). Singapore, for example, has adopted the broader concept (see Chow, 1981, 1985b; Kalirajan and Wiboonchutikula, 1986; Robinson, 1984). It also brings into focus the libertarian prin- ciple that individuals are the best judges of their own well- being. NPFs do not sit comfortably in the social security arena.

198 Policy Studies Review, Spring/Summer 1993, 12:1/2

PERFORMANCE OF NATIONAL PROVIDENT FUNDS

NPFs are, at one and the same time, social security institu- tions, providing benefits to members in the event of an interrup- tion to or loss of their earning power; social development institutions, improving the quality of life of members and other beneficiaries; and financial institutions, mobilizing savings to promote socioeconomic development. NPFs have a significant impact on the societies that foster them in all these domains.

Social Security Performance The International Labor Organization’s (ILO) Social Secu-

rity (Minimum Standard) Convention of 1952 provides an inter- nationally accepted set of goals for social security systems in developing (and developed) countries. In terms of these goals or standards, NPFs must be judged to provide inadequate social security protections.

Lump-sum Payments. The 1952 convention endorses only the use of periodic payments, expressed as either a percentage of a beneficiary’s previous earnings, for a particular period of time (Articles 63 and 64) or an income-tested flat rate ”sufficient to maintain the family of the beneficiary in health and decency” (Article 65) to meet social security needs. The provision of lump-sum benefits are, thus, an inferior form of social security payment because they are not determined in accordance with social security needs; rather, they are the product of past savings. Because NPFs are unable to ensure that their beneficia- ries use their lump-sum payments to provide a future source of income for themselves, they cannot guarantee that their benefi- ciaries do not quickly become impoverished as inflation eats away at their means of support. Hence, the ability of NPFs to protect their members in the event of a loss or interruption of their earning power depends on the efficacy of the lump-sum payment. The extent to which such payments can provide social security protection depends on the balance of members’ ac- counts, the uses to which the withdrawn amounts are put, and the rate of inflation.

Low Level of Deposits. This is one of the major dilemmas confronting NPFs seeking to provide adequate social security protection for their members. The balance in any member’s account would be greater, the higher the contribution rate payable; the higher the earnings to which that rate applies; the longer the contribution period (or the shorter the periods of unemployment or uncovered employment); the higher the in- terest periodically credited; the smaller the interim withdraw-

Dixon: National Provident Funds 199

als permitted and the smaller proportion of outstanding contri- butions. Two particular issues needed to be considered in this context. First, many NPFs are relatively recent in origin: ten (17 percent) were established in the 1980s, six (26 percent) in the 1970s, eight (35 percent) in the 1960s and five (22 per cent) in the 1950s). Thus, the maximum possible contribution period is such that insufficient time has elapsed for members to have accumulated a sizable deposit. Moreover, a member’s actual contribution period may be less than the maximum because they were not among the foundation membership or because of periods of unemployment or uncovered employment. Second, if members are permitted to make interim withdrawals prior to their final withdrawal, the result, clearly, will be smaller final payouts. Thus, the issue is to establish priorities among the competing claims for interim and final withdrawal payments. Most NPFs permit interim withdrawals to varying degrees, which may indeed constitute an attempt to give some protec- tion to workers confronting selected short-run social security contingencies (which applies to 11 NPFs), or they may be justified on some other socially desirable grounds (as is the case in 10 NPFs). However, the opportunity costs of such interim withdrawal is a reduced ability to protect members in the event of the long-term cessation of their earning capacities. Allowing members to borrow from their accounts has a similar effect until the amount is repaid in full, with interest at least equal to that credited to members’ accounts.

According to a DELPHI survey conducted in the late 1980s, NPF managers have clearly recognized that there is a need to increase the level of deposits (Dixon, 1990).’ They placed considerable emphasis on the need for NPFs to continue realiz- ing a suitable return on investment and on increasing the contribution rates payable by both employers and employees. Moreover, they placed little importance on either extending the range of interim withdrawal or loan rights available to mem- bers, or seeking a government subsidy to improve the benefits provided to members.

The way in which lump-sum payments are spent determines the extent to which this form of benefit provides social security support. The principle justification for lump-sum payments is that they pro- vide members with the ability to acquire income-generating assets, so as to avoid subsequent recourse to any form of public assistance. Although data on the dispersal of the NPF lump- sum payments are sparse, there is some evidence to suggest that acquisition of an asset generating an immediate income is only

Dispersal of Lump-Sum Payments.

200 Policy Studies Review, Spring/Summer 1993,12:1/2

one, relatively modest, use to which payments are put. Surveys in Ghana in 1973 and Zambia in 1978 revealed that the most popular use of lump-sum payments was to pay for children’s education (Mulozi, 1980, p. 58; International Social Security Association, 1977, p. 11). In the Caribbean, the evidence sug- gests that lump-sum payments in the 1970s were used to pur- chase consumer goods (Gobin, 1977).

Little doubt exists that there is broad-based support among NPF members for the continuation of lump-sum payments. A 1986 survey of NPF members in India revealed that an over- whelming majority favored the withdrawal/final settlement system (Lall, 1986). Reflecting this broad-based membership support for lump-sum payments, NPF managers did not con- sider the periodic payment or annuity options to be very impor- tant issues nor did they expect them to have much impact on their NPF’s future cost, efficiency or effectiveness (Dixon, 1990).

Inflation. The effectiveness of lump-sum payments as a social security device is affected by inflation in two ways. If inflation occurs over the contribution period, then the real value of the member’s deposits falls unless the interest rate periodically credited exceeds the inflation rate. If inflation occurs after the final lump-sum payment has been made, the real value of the benefits generated by its dispersal diminishes over time, which provides a clear incentive to divert this pay- ment to current rather than to future consumption. In both situations, inflation diminishes the capacity of lump-sum pay- ments to provide members with adequate social security pro- tection. It is most likely that this is a matter of concern to NPF members. The 1986 Indian NPF membership survey reveals that the depreciation of the real value of savings is a very significant negative aspect of the provident fund (Lall, 1986, p. 64). NPF managers have recognized inflation as being impor- tant although, curiously, they judged it as likely to have little impact on the future cost, efficiency or even the effectiveness of their provident fund (Dixon, 1990).

Periodic Payments and Annuities. Because lump-sum pay- ments are not an effective means of providing social security protection, some NPFs offer their members the alternative of periodic payments. Although this may overcome the problems associated with inappropriate dispersal of lump-sum payments from a social security perspective, periodic payments in the form of installments or actuarial-determined annuities does not solve the problem of low deposit levels or inflation. Aug- mented annuities, as provided in Fiji and Western Samoa, somewhat alleviate the problem of low deposit levels and offer

Dixon: National Provident Funds 201

a more effective means of providing social security protection. However, the problem of inflation remains, however, as there is still no mechanism for subsequent supplementation.

Supplementary Benefits. In order to further strengthen the social security protection offered, some NPFs provide supple- mentary benefits. Of particuIar interest is the Family Pension Scheme established in India and the purchasing of life insur- ance. It is interesting to note that NPF managers consider such supplementary benefits to be of very little or no importance, but likely to have a modest impact on their provident fund’s future effectiveness (Dixon, 1990). However, they have conflicting perceptions of the likely effects that such supplementary ben- efits would have on their provident fund’s costs and efficiency (Dixon, 1990).

While the provision of supplementary benefits has helped to obviate the problem of low deposit levels in some NPFs, the problem with inflation remains unsolved. Even so, NPFs still fall well short of the minimum standard set out in the Interna- tional Labor Organization’s Social Security Convention of 1952.

Employee Coverage. The 1952 ILO convention established minimum coverage standards to include less than 20 percent of all residents; all residents with means below a particular limit; or not less than 50 percent of all employees in industria1 work places employing 20 persons or more. Few NPFs meet these requirements (see Dixon, 1990, Table 4). It also must be recog- nized that most social security protection is provided to the burgeoning urban middle class, those long-standing members who have not experienced periods of either unemployment, uncovered employment or absence from the work force. Un- questionably, the less fortunate receive less support which is a product of the fact that NPFs do not engage in risk-pooling.

It is clear that employee coverage is a matter of considerable importance to NPF managers, particularly as they expect it to have a moderate-to-large positive effect on their NPF’s costs (Dixon, 1990). Interestingly, most NPF managers expect it to have a positive impact on their NPF’s efficiency or effective- ness, although there is no consensus on the magnitude of this impact.

Contingencies Covered. The 1952 ILO convention speci- fied a range of social security contingencies that are not gener- ally covered by NPFs: namely, the short-term contingency of sickness, unemployment, employment injury, maternity and child-bearing. It must be noted, of course, that most countries operating NPFs also cover, at least to some extent, one or more of these contingencies by other means, most commonly by

202 Policy Studies Review, Spring/Summer 1993, 12:1/2

employer liability measures. Moreover, most NPFs cover contingencies which are not recognized by the ILO convention and, therefore, reduces their efficacy as providers of social security protection.

There is a strong consensus among NPF managers that extending the range of social security contingencies covered to include unemployment, maternity, child-bearing or sickness is of little or no importance and has only low-to-moderate domi- nance (Dixon, 1990). In fact, the introduction of new branches of social security is perceived as having little impact on their NPF’s costs, efficiency or effectiveness.

Distribution of Costs. The 1952 ILO convention requires that the costs of social security protection be met by means of contributions and/or taxes “in a manner of which avoids hard- ship to persons of small means” (Article 67). Only a few NPFs specify either a contribution floor (India) or a lower contribu- tion rate for low-wage earners (Singapore and Uganda) in order to reduce the financial hardship caused by payment of the prescribed employee contributions.

Transformation of National Provident Funds into Social Security Insurance Systems. Because NPFs do not provide adequate social security protection against old-age, disability and the effect of an income earner’s death on dependents, from time to time attention has been given to the idea of their conversion into more comprehensive social insurance systems (Thompson, 1978, p. 191; International Social Security Associa- tion, 1975, 1977; Wadhawan, 1969, p. 256; Gerig, 1966, p. 40; Parrott, 1968; Godfrey, 1974a, 1974b). Much is said in a rhetorical vein about the desirability of converting an NPF into a social insurance system but the practical difficulties of imple- mentation discourage action. The possible reduction in the supply of developmental finance, and the almost inevitable need for government subsidies, inhibit all but the most adven- turous from taking definite steps towards establishing a social insurance system, namely, Iraq (19641, Dominica 11976), St Lucia (1978) and the Seychelles (1979).

It is interesting to note that NPF managers have conflicting beliefs on the importance of such a transformation, although most consider this issue to be of only little or moderate impor- tance (Dixon, 1990). Moreover, they have antithetic percep- tions on the likely magnitude and direction of the impact that such transformation would have on their NPF‘s costs, efficiency and effectiveness.

In an effort to become more effective social security institutions, the NPFs in

Evolution of a Social Security Hybrid.

Dixon: National Provident Funds 203

Fiji and Western Samoa provide augmented periodic payments. By so doing, they have transformed themselves into a social security hybrid. Other NPFs have been reluctant to embark on a similar transformation process, despite the fact that the limi- tations of NPFs as social security institutions are well-under- stood and accepted.

The Social Development Performance NPFs have a significant social development impact on the

countries in which they operate. They affect the quality of life of their members, who are able to use their accumulated depos- its to improve their own and their family’s current and future living standards in a variety of ways. A large minority of NPFs provide some form of assistance to members wishing to pur- chase housing (by permitting partial interim withdrawals or by providing interest-bearing or interest-free housing loans). Simi- larly, the provision of health care (as a gratis benefit from compulsory savings or on the basis of an interest-bearing loan) also enhances members’ quality of life. Indeed, Nepal had moved quite significantly in the direction of allowing members to benefit from their accumulated deposits by granting loan rights to cover the cost of various contingencies and social obligations. Ghana has adopted the novel approach of estab- lishing a subsidiary, the Social Security Bank Limited, to pro- vide long-term credit facilities to members for the purchase of durable goods and, interestingly, to contributing employers (Ghana, 1980, p. 6).

It is evident that while NPF managers consider the various partial interim withdrawal options and loan rights to be of little or moderate importance only, they did identify them as domi- nant issues facing their NPFs (Dixon, 1990). Indeed, they unambiguously perceived them as having a negative impact on both the efficiency and effectiveness of their NPFs. It must be acknowledged, of course, that NPFs must find an appropriate balance between the long-term social security needs of mem- bers and the shorter-term quality of life needs of their members. This is a far from easy balance to find and maintain. Yet, as social development institutions NPFs must be judged success- ful.

The Financial Performance NPFs have an extremely complex impact on the economies

in which they operate. In essence, they shift resources from the private sector through the receipt of employer contributions to

204 Policy Studies Review, Spring/Summer 1993, 12:1/2

the public sector as a result of portfolio management practices. In addition, they tend to generate inflationary pressures by their differential impact on aggregate demand and aggregate supply. They also tend to promote employment, especially in the public sector. Overall, NPFs probably promote the eco- nomic development of the countries that sponsor them.

Savings Mobilization. In all NPFs, the growth in revenue (contributions plus investment and other.income) greatly ex- ceeds the growth in expenditures (benefits plus administrative expenses), ensuring an accumulation of reserves. This is inevi- table for a variety of reasons. First, because NPFs focus largely on long-term social security contingencies, contributions are collected for a considerable period before benefits are payable. Of course the extent to which NPFs permit partial interim withdrawals and grant loan rights will impact the rate at which reserves are accumulated inversely. Second, the typical age structure in countries with NPFs is skewed toward the younger age groups, which means that the proportion of beneficiaries to contributors is low. Third, industrialization and urbanization are drawing people into covered employment, thus ensuring the continued growth in numbers of contributors. Finally, inflation increases NPF revenues because contributions are tied to money wages while having no significant impact on expendi- ture.

Implications of Portfolio Management Policies and Prac- tices. Clearly, NPFs are significant financial institutions in the countries in which they operate. Portfolio management policies have consequences not only for future beneficiaries (in terms of the interest periodically credited to members’ deposits), but also for public debt management. The manner in which NPF reserves are used is determined by any constraints specified in its enabling legislation, by the institutional arrangements sur- rounding the investment decision-making process, and by the prevailing political attitudes towards the appropriate socioeco- nomic role of the NPF.

The primary objective of an NPF’s portfolio management policy is to maintain its financial capacity to pay a reasonable rate of interest on members’ deposits. The secondary objective is to provide a relatively cheap source of finances for programs designed to promote national economic and social develop- ment. Because NPFs are not obliged to pay competitive interest rates to their members, these two objectives are not inherently incompatible. During a period of relatively modest inflation, when the real rate of interest on members’ deposits is at least positive, the achievement of both objectives is relatively easy.

Dixon: National Provident Funds 205

However, when inflation causes the real rate of interest on members’ deposits to become negative, then the simultaneous achievement of both objectives becomes substantially more difficult. The available evidence suggests that, under these circumstances, the social security objective of NPFs becomes a little blurred (Thompson, 1978). Portfolio management policies that may be appropriate when there is currency stability be- come inappropriate in times of currency depreciation. A pru- dent policy of purchasing low-yield, high-security government and government-guaranteed bonds and loans remain the domi- nant feature of all NPF portfolio management policies. How- ever, this traditional conservatism is being gradually eroded as NPFs increasingly seek ways of protecting their members from the full impact of inflation. Unquestionably, financial assets do not provide a hedge against inflation unless they are indexed in line with inflation, which commonly they are not. However, protecting their members’ deposits from currency depreciation must be considered a major problem for provident fund man- agement in the future. It is evident that NPF managers are acutely aware of this issue; hence, the importance they place on realizing a suitable return on investment (Dixon, 1990). The inevitable tradeoff between cheap development financing and adequate social security protection will become increasingly difficult for both governments and NPFs to determine.

NPFs are confronted with a variety of external and self- imposed constraints that limit the management of their invest- ment portfolios. First, all NPFs hold a significant proportion of their portfolios in government, quasi government or govern- ment-guaranteed securities or loans, whether by law, ministe- rial decree or prudence. Given the portfolio management objectives being sought by NPFs, this is an appropriate policy only if the rate of return on such investment is competitive with alternative investment opportunities. Moreover, there is evi- dence to suggest that some NPFs are having difficulties finding sufficient investment opportunities in which to invest all their surplus revenue. Second, most NPFs are not prepared or permitted to take advantage of investment opportunities out- side the country in which they operate. Finally, few NPFs have ventured into equity participation in the private sector, a strat- egy that may generate a higher rate of return although the risks are somewhat higher than those associated with government and quasi government securities and loans.

It is evident that being able to invest in property, in business undertakings and overseas are of relatively low importance to NPF managers (Dixon, 1990). They have conflicting views on

206 Policy Studies Review, Spring/Summer 1993,12:1/2

the likely impact that such investments would have on their NPF's efficiency and effectiveness, but they did generally con- sider that such investments would have a positive impact on costs.

Distributional Impact. NPFs clearly affect the distribution of income in the countries in which they operate. The distribu- tional impact is extremely difficult to determine, but two issues need to be highlighted. First, in countries with a progressive income tax rate structure, the impact of tax-deductible em- ployee NPF contribution distributions is regressive. The degree of regressiveness is, of course, restricted by specified contribu- tion ceilings. Second, because expending NPF reserves has a positive multiplier effect throughout the economy in which it operates, it has a bewilderingly complex impact on the distribu- tions of income. There is no a priori way of knowing whether this impact is generally progressive, neutral or regressive, or even which segments of the community are the principal benefi- ciaries.

CONCLUSION

NPFs seek to provide their members with basic protection in the form of lump-sum withdrawals from their accumulated deposits upon the occurrence of prescribed social security con- tingencies. Their capacity to provide adequate social security protection is generally restricted, first, by the relatively low level of the members' deposits; second, by their inability to ensure that lump-sum payments are used by their members to provide long-term social security protection; and finally, by their inability to provide their members with a hedge against inflation. NPFs are aware of their inadequacies; some have sought to remedy them by means of supplementary benefits and, more radically, by offering augmented periodic payments. None, however, have found the solution to the fundamental dilemma that makes them ineffective social security institu- tions; namely, how to provide adequate social security protec- tion on the basis of compulsory savings.

To judge NPFs solely on their ability to provide adequate social security protection is to ignore their broader socioeco- nomic roles. Increasingly, they are becoming the means by which members can improve their quality of life because of the assistance many provide to improve housing and health care. This attribute is valued by members, who appear to be willing to trade off short-term quality of life support for long-term social security protection. In this context, provident fund

Dixon: National Provident Funds 207

managers are cursed with the problem of finding the appropri- ate balance between these competing claims. It is evident that most NPF managers perceive their NPF's primary responsibil- ity as providing social security protection for those reaching old age, retirement, becoming disabled or dying (Dixon, 1990). Hence, they place only little or moderate importance on provid- ing a range of partial interim withdrawal benefits (even for short-term social security contingencies) or a variety of inter- est-free or interest-bearing loan rights. Indeed, they perceived their NPF's future effectiveness as being enhanced most by increasing the contribution rates payable by employers and employees, and by providing noncontributory life insurance.

In their present form, NPFs are popular with their members and participating employers, as well as with their sponsoring governments. Employees see them as a compulsory savings scheme accumulating their savings, which should be reason- ably, readily accessible. Employers see them as the means by which their moral obligation to the welfare of their employees is fulfilled at a known and stable cost. Governments see them as a self-help vehicle for providing basic social protection and quality-of-life improvement, and as a readily available source of cheap finances for social and economic development.

The juxtaposition of economic, social and social security objectives has made NPFs generally resilient to fundamental changes and has, in some instances, resulted in the evolution of a social security hybrid-neither a pure NPF nor a social insur- ance system such as those in Fiji and Western Samoa. To a significant degree, social security objectives have become sub- servient to social and economic objectives, a1 though perhaps not to the immediate disadvantage of NPF members.

ENDNOTES

In 1986, the then 21 NPFs (the exclusions being Tuvalu and Vanuatu) were invited to participate in a DELPHI forecasting exercise designed to identify, prioritize and assess the major factors that are expected to effect their provident fund over the five years to 1991 (see Dixon, 1990, appendix 2). Eleven provident fund managers agreed to participate, representing a response rate of 53 percent.

REFERENCES

Clarke, C. E. (1977). Actuarial aspects of converting provident funds into social security schemes. In First meeting of the committee [on provident funds] and round table meeting on provident funds (pp. 86- 112). Geneva: International Social Security Association.

208 Policy Studies Review, Spring/Summer 1993,121 /2

Chow, N. W. S. (1981). Social security provision in Singapore and Hong Kong. Journal of Social Policy, 20(3), 353-366.

Dixon, J . (1982). Provident funds in the Third World: A cross national review. Public Administration and Development, 2 , 325-344.

Dixon, J. (1985). Provident funds: Their nature and performance. In Social Security in the South Pacific. Bangkok: International Labour Office.

Dixon, J. (1986). Social security traditions and their global applications. Canberra: International Fellowship for Social and Economic De- velopment.

Dixon, J. (1987). Provident funds: An assessment of their social security, social and economic performance and prospects. In J. Schulz and D. Davis-Friedmann (Eds.), Aging China: Family, eco- nomics, and government policies in transition (pp. 128-156). Wash- ington, DC: Gerontological Society of America.

Dixon, J. (1989). Social security traditions and their global context. In B. Mohan (Ed.), Glimpses of international 6 comparative social welfare (pp. 109-161). Canberra: International Fellowship for Social and Economic Development.

Dixon, J. (1990). National provident funds: The enfant terrible of social security. Canberra: International Fellowship for Social and Eco- nomic Development.

Ghana Annual Report, 1978-79. (1980). Accra: Social Security and National Insurance Trust.

Gobin, M. (1977). The role of social security in the development of the Caribbean territory. Internafional Social Security Review, 30(1), 7- 20.

Godfrey, V. N. (1974a). The ability of national provident funds to meet social needs: The Zambian experience. African Social Secu- rity Series, pp. 13-14.

Godfrey, V. N. (1974b). Broader role for national provident funds- Zambian experience. International Labour Review, 109(2), 137-152.

International Social Security Association. (1975). Transformation of provident funds into pension schemes. International Social Secu- rity Review, 28(3), 276-289.

International Social Security Association. (1977). Transformation of provident funds into pension schemes. In First meeting of the committee [on provident funds] and round table meeting on provident funds (pp. 97-108). Geneva: Author.

Kalirajan, K. and Wiboonchutikula, P. (1986). The social security system in Singapore. ASEAN Economic Bulletin, 3, 129-144.

Lall, V. D. (1986). Appraisal of Provident Fund and Allied Schemes: Opinion Survey Aiming Subscribers. New Delhi: National Institute of Public Finance and Policy.

Mulozi, S. L. (1980). Recent developments and future prospects of social security in Africa-with special reference to Zambia. Social Security Documentation African Series, 3, 53-61.

Parrott, A. L. 1968. Problems arising from the translation from provident funds to pension schemes. Infernational Social Security Review, 21(4), 530-557.

Dixon: National Provident Funds 209

Robinson, H. S. (1977). Fiji national provident fund augmented annuity scheme. In First meeting of the committee [on provident funds1 and round table meeting on provident funds (pp. 58, 79). Geneva: International Social Security Association.

Thompson, K. (1978). Trends and problems of social security in developing countries in Asia. In Social security and national development (pp. 6-33). Bangkok: International Labour Office, Regional Office for Asia.

Wadhawan, S. K. (1969). Employees’ provident fund scheme- development and future plans. International Social Security Re- view, 22(2), 251-257.

210 Policy Studies Review, Spring/Summer 1993,12:1/2

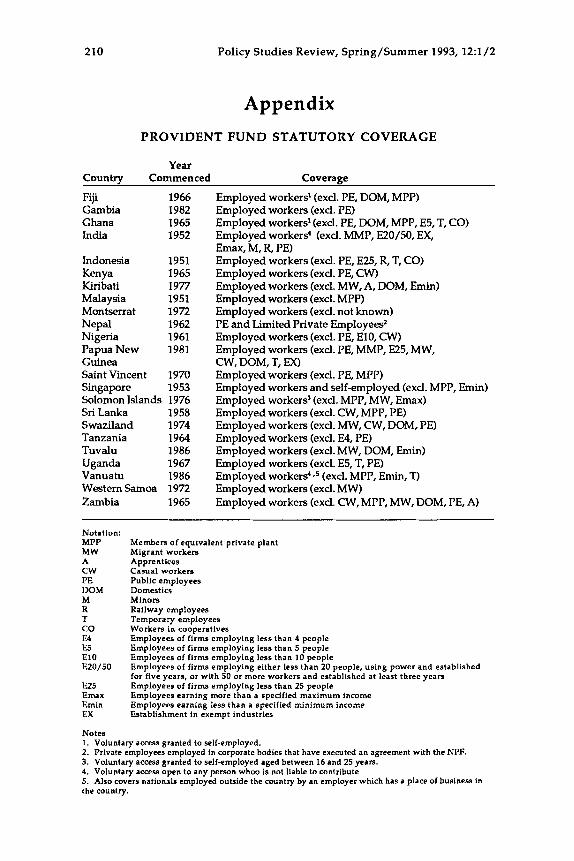

Appendix PROVIDENT FUND STATUTORY COVERAGE

Year Country Commenced Coverage

Fiji 1966 Employed workers' (excl. PE, DOM, MPP) Gambia 1982 Employed workers (excl. PE) Ghana Employed workers' (excl. PE, DOM, MPP, E5, T, CO) India 1952 Employed workers' (excl. MMP, E20/50, EX,

Emax, M, R, PE) Indonesia 1951 Employed workers (excl. PE, E25, R, T, CO) Kenya 1965 Employed workers (excl. PE, CW) Kiribati 1977 Employed workers (excl. MW, A, DOM, Emin) Malaysia 1951 Employed workers (excl. MPP) Montserrat 1972 Employed workers (exd. not known) Nepal 1962 PE and Limited Private Employees* Nigeria 1961 Employed workers (excl. PE, E10, CW) Papua New 1981 Employed workers (excl. PE, MMP, E25, MW, Guinea CW, DOM, T, EX) Saint Vincent 1970 Employed workers (excl. PE, MPP) Singapore 1953 Employed workers and self-employed (excl. MPP, Emin) Solomon Islands 1976 Sri Lanka 1958 Employed workers (excl. CW, MPP, PE) Swaziland 1974 Employed workers (excl. MW, CW, DOM, PE) Tanzania 1964 Employed workers (excl. E4, PE) Tuvalu 1986 Employed workers (excl. MW, DOM, Emin) Uganda 1967 Employed workers (excl. E5, T, PE) Vanuatu 1986 Employed workers' e 5 (excl. MPP, Emin, T) Western Samoa 1972 Employed workers (excl. MW) Zambia

1965

Employed workers' (excl. MPP, MW, Emax)

1965 Employed workers (excl. CW, MPP, MW, DOM, PE, A)

Notation: MPP MW Migrant workers A Apprentices cw Casual workers I'E Public employees DOM Domestics M Minors R Railway employees T Temporary employees co Workers in cooperatives E4 F.5 El0 E20/50

E25 Emax Emin EX Establishment in exempt industries

Notes 1. Voluntary access granted to self-employed. 2. Private employees employed in corporate bodies that have executed an agreement with the NPF. 3. Voluntary access granted to self-employed aged between 16 and 25 years. 4. Voluntary access open to any person whw is not liable to contribute 5. Also covers nationals employed outside the country by an employer which has a place of business in the country.

Members of equivalent private plant

Employees of firms employing less than 4 people Employees of firms employing less than 5 people Employees of firms employing less than 10 people Employees of firms employing either less than 20 people, using power and established for five years, or with 50 or more workers and established at least three years Employees of firms employing less than 25 people Employees earning more than a specified maximum income Employees earning less than a specified minimum income

Dixon: National Provident Funds 21 I

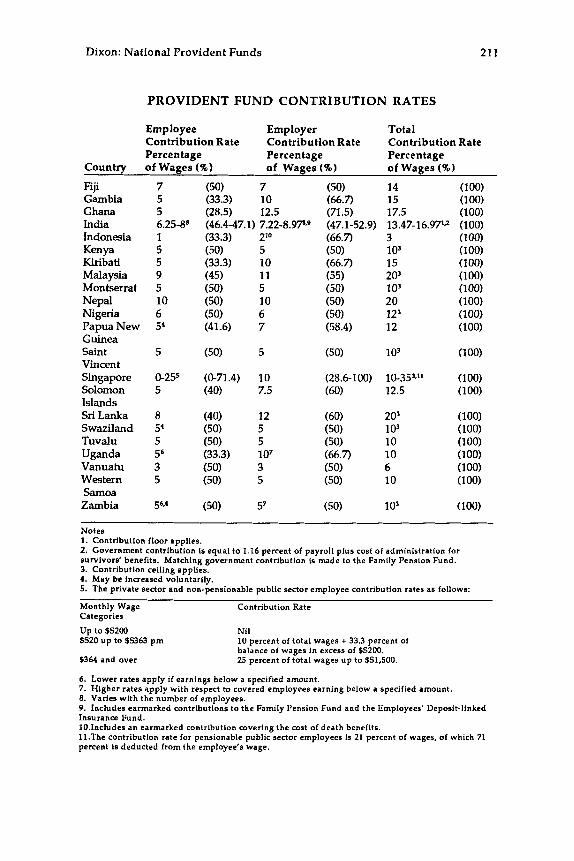

PROVIDENT FUND CONTRIBUTION RATES

Employee Employer Total Contribution Rate Contribution Rate Contribution Rate Percentage Percentage Percentage

Country of Wages (96) of Wages (%) of Wages (%)

Fiji 7 Gambia 5 Ghana 5 India 6.25-8' Indonesia 1

Kiribati 5 Malaysia 9 Montserrat 5

Nigeria 6 PapuaNew 54 Guinea Saint 5 Vincent Singapore 0-255 Solomon 5 Islands SriLanka 8 Swaziland 5' Tuvalu 5 Uganda 56 Vanuatu 3 Western 5 Samoa

Kenya 5

Nepal 10

Zambia 56.4

(50) 7 (33.3) 10 (28.5) 12.5 (46.447.1) 7.22-8.97*9 (33.3) 2'0 (50) 5 (33.3) 10 (45) 11 (50) 5 (50) 10 (50) 6 (41.6) 7

(50) 5

(0-71.4) 10 (40) 7.5

Notes 1. Contribution floor applies. 2. Government contribution is equal to 1.16 percent of payroll plus cost of administration for survivors' benefits. Matching government contribution is made to the Family Pension Fund. 3. Contribution ceiling applies. 4. May be increased voluntarily. 5. The private sector and non-pensionable public sector employee contribution rates as follows:

Monthly Wage Contribution Rate Categories

u p to $5200 Nil $520 up to $5363 pm

$364 and over

6. Lower rates apply if earnings below a specified amount. 7. Higher rates apply with respect to covered employees earning below a specified amount. 8. Varies with the number of employees. 9. Includes earmarked contributions to the Family Pension Fund and the Employees' Deposit-linked Insurance Fund. 10.Includes an earmarked contribution covering the cost of death benefits. 11.The contribution rate for pensionable public sector employees is 21 percent of wages, of which 71 percent is deducted from the employee's wage.

10 percent of total wages + 33.3 percent of balance of wages in excess of $5200. 25 percent of total wages up to $51,500.

212 Policy Studies Review, Spring/Summer 1993, 121 /2

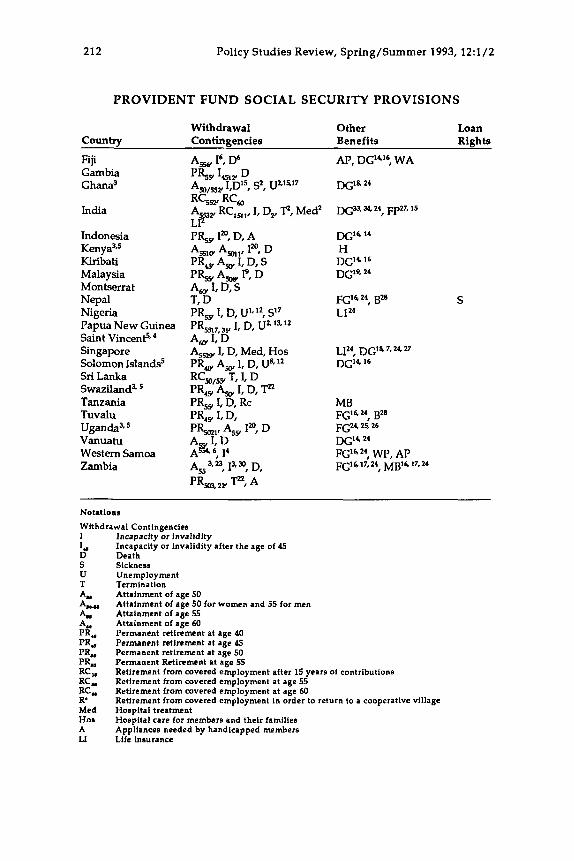

PROVIDENT FUND SOCIAL SECURITY PROVISIONS

Withdrawal Other Loan Country Contingencies Benefits Rights

Fiji A,, I", D6 AP, DG14'6, WA

Ghana3 A,/,,, I,D1', S2, U21517

India A, RCInl, I, D,, .I", Med2 DGa * 24, FPZ7,

mia 24 Gambia PRSY 1,nr D

RC,, RC,

LIP Indonesia Kenya", Kiribati Malaysia Montserrat Nepal Nigeria Papua New Guinea Saint VincenP,' Singapore Solomon Islandss Sri Lanka SwazilandJ. Tanzania Tuvalu

Vanuatu Western Samoa Zambia

Uganda"

S

Notations

Withdrawal Contingencies Incamcitv or invaliditv Incipaciti or invalidicy after the age of 45 Death Sickness Unemployment Termination Attainment of age 50 Attainment of age 50 for women and 55 for men Attainment of age 55 Attainment of age 60 Permanent retirement at age 40 Permanent retlrement at age 45 Permanent retirement at age 50 Permanent Retirement at age 55 Retirement from covered employment after 15 years of contributions Retirement from covered employment at age 55 Retirement from covered employment at age 60 Retirement from covered employment in order to return to a cooperative village Hospital treatment Hospital care for members and their families Appliances needed by handicapped members Life insurance

Dixon: National Provident Funds 213

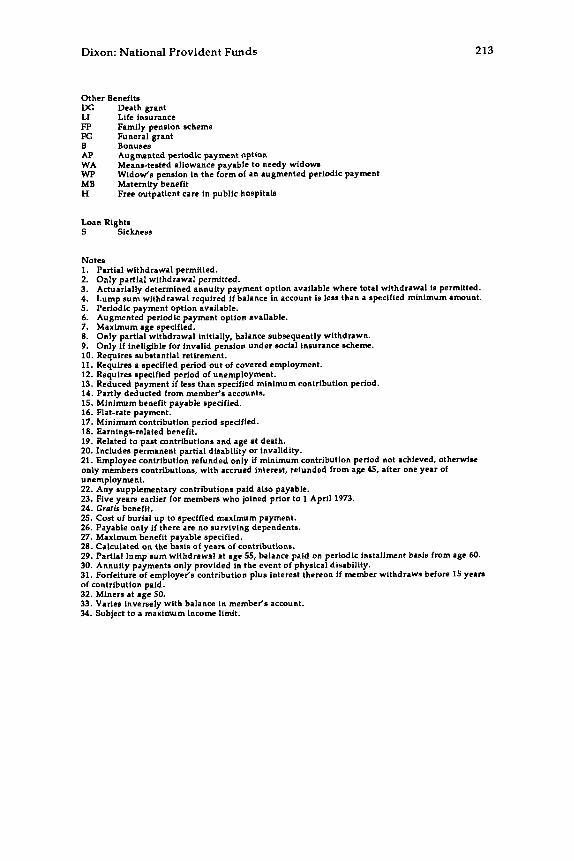

Other Benefits DG Death grant LI Life insurance FP Family pension scheme FG Funeral grant B Bonuses AP Augmented periodic payment option WA WP MB Maternity benefit H

Means-tested allowance payable to needy widows Widow's pension in the form of an augmented periodic payment

Free outpatient care in public hospitals

Loan Rights S Sickness

Notes 1. 2. 3. 4. 5. 6. 7. 8. 9.

Partial withdrawal permitted. Only partial withdrawal permitted. Actuarially determined annuity payment option available where total wlthdrawal is permltted. Lump sum withdrawal required if balance in account is less than a specified minlmum amount. Periodic payment option available. Augmented periodic payment option available. Maximum age Specified. Only partial withdrawal initially, balance subsequently withdrawn. Only if ineligible for invalid pension under social insurance scheme.

10. Requires substantial retlrement. 11. Requires a specified period out of covered employment. 12. Requires specified period of unemployment. 13. Reduced payment if less than specified minimum contrlbution period. 14. Partly deducted from member's accounts. 15. Minimum benefit payable specified. 16. Flat-rate payment. 17. Minimum contribution period specified. 18. Earnings-related benefit. 19. Related to past contributions and age at death. 20. Includes permanent partial disability or invalidity. 21. Employee contribution refunded only if minimum contribution period not achieved, otherwlme only members contributlons, wlth accrued interest, refunded from age 45, after one year of unemployment. 22. Any supplementary contributions paid also payable. 23. Five years earlier for members who joined prior to 1 April 1973. 24. Crrrfis benefit. 25. Cost of burlal up to specified maximum payment. 26. Payable only if there are no surviving dependents. 27. Maximum benefit payable specified. 28. Calculated on the basis of years of contributions. 29. Partial lump sum withdrawal at age 55, balance paid on periodic installment basis from age 60. 30. Annuity payments only provided in the event of physical disability. 31. Forfeiture of employer's contribution plus interest thereon if member withdraws before 15 yean of contribution paid. 32. Miners at age 50. 33. Varies inversely with balance in member's account. 34. Subject to a maximum income limit.