Embed Size (px)

Citation preview

NATIONAL FINANCE OLYMPIAD 2017 1

NATIONAL FINANCE OLYMPIAD 2017

MOCK QUESTIONS – ROUND 1

TYPE OF QUESTION GRIDSHEET

No. Section Selecting the right answer

Selecting the relevant

Descriptive scenario

1 Basic accounting concepts 4 6 3

2 Advanced accounting application

4 6 3

3 Business Financial Management

4 6 3

4 Governance and internal controls

4 6 3

NATIONAL FINANCE OLYMPIAD 2017 2

Section 1: Selecting the right answer Entity A has been in the business of rendering services to its clients. For provision of services, it had procured many floors of a building, each floor comprising of many apartments provided to its employees for residence. Entity A is now going into a new business of buying and selling apartments in various locations of the city. It has also re-negotiated terms of employment with its employees whereby they will no more be provided with residential apartments. It is decided that the apartments so vacated will also form part of the new business and will be available for sale in the ordinary course of business.

These apartments were earlier being carried using revaluation model i.e. carried at revalued amount less accumulated depreciation and impairment. Considering the new business model, Entity A is considering following accounting policies in respect of its apartments?

a. Continue with the existing policy

b. Cost less accumulated depreciation and impairment

c. Fair value less cost to sell

d. Lower of cost and net realisable value

Which of the above accounting policies are now available to Entity A in this respect?

PLEASE SELECT THE RIGHT ANSWER

a. Choice between A and B

b. Choice between B and C

c. C

d. D

NATIONAL FINANCE OLYMPIAD 2017 3

Selecting the right answer Smart Limited is in the business of textile manufacturing, listed on Pakistan Stock Exchange Limited with factories located at different parts of country. Management of Smart Limited intends to alter the terms and conditions of employment at one factory in such a way that overtime will be paid in future at 1.5 times the normal rate, rather than twice the normal rate as in the past. Management intends to compensate employees with a one-off payment and has put this offer to the union. The employees are also aware of this impending change. No agreement has been reached with the union at the year end. However, if the offer is not accepted, management is likely to switch overtime work to other factories. Management can withdraw the offer to the union at any time prior to the union’s acceptance. Management is in the process of finalizing its financial statements and seeking views about how to account for one off compensation payment in its financial statements? (a) Provision should not be made for proposed one-off compensation payment because the entity can

avoid that expenditure by changing its method of future operation and by withdrawing the offer prior to the union’s acceptance.

(b) A provision should be recognized for the payment at the year end because the Company cannot

avoid the payment of compensation.

(c) A provision should be recognized because management has created a valid expectation among the employees with regard to such compensation and hence there is a constructive obligation and amount of payment can be estimated reliably.

(d) A provision cannot be made for future payments.

NATIONAL FINANCE OLYMPIAD 2017 4

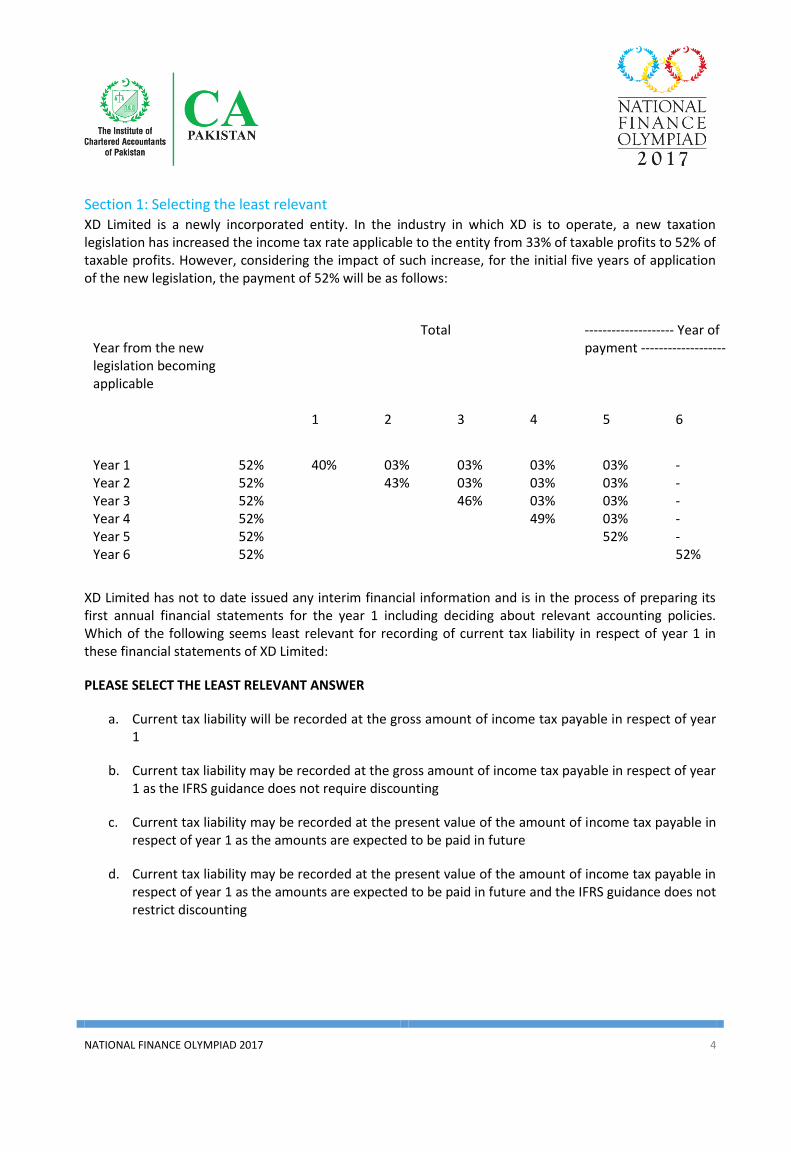

Section 1: Selecting the least relevant XD Limited is a newly incorporated entity. In the industry in which XD is to operate, a new taxation legislation has increased the income tax rate applicable to the entity from 33% of taxable profits to 52% of taxable profits. However, considering the impact of such increase, for the initial five years of application of the new legislation, the payment of 52% will be as follows:

XD Limited has not to date issued any interim financial information and is in the process of preparing its first annual financial statements for the year 1 including deciding about relevant accounting policies. Which of the following seems least relevant for recording of current tax liability in respect of year 1 in these financial statements of XD Limited:

PLEASE SELECT THE LEAST RELEVANT ANSWER

a. Current tax liability will be recorded at the gross amount of income tax payable in respect of year 1

b. Current tax liability may be recorded at the gross amount of income tax payable in respect of year 1 as the IFRS guidance does not require discounting

c. Current tax liability may be recorded at the present value of the amount of income tax payable in respect of year 1 as the amounts are expected to be paid in future

d. Current tax liability may be recorded at the present value of the amount of income tax payable in respect of year 1 as the amounts are expected to be paid in future and the IFRS guidance does not restrict discounting

Year from the new legislation becoming applicable

Total -------------------- Year of payment -------------------

1

2

3

4

5

6

Year 1 52% 40% 03% 03% 03% 03% - Year 2 52% 43% 03% 03% 03% - Year 3 52% 46% 03% 03% - Year 4 52% 49% 03% - Year 5 52% 52% - Year 6 52% 52%

NATIONAL FINANCE OLYMPIAD 2017 5

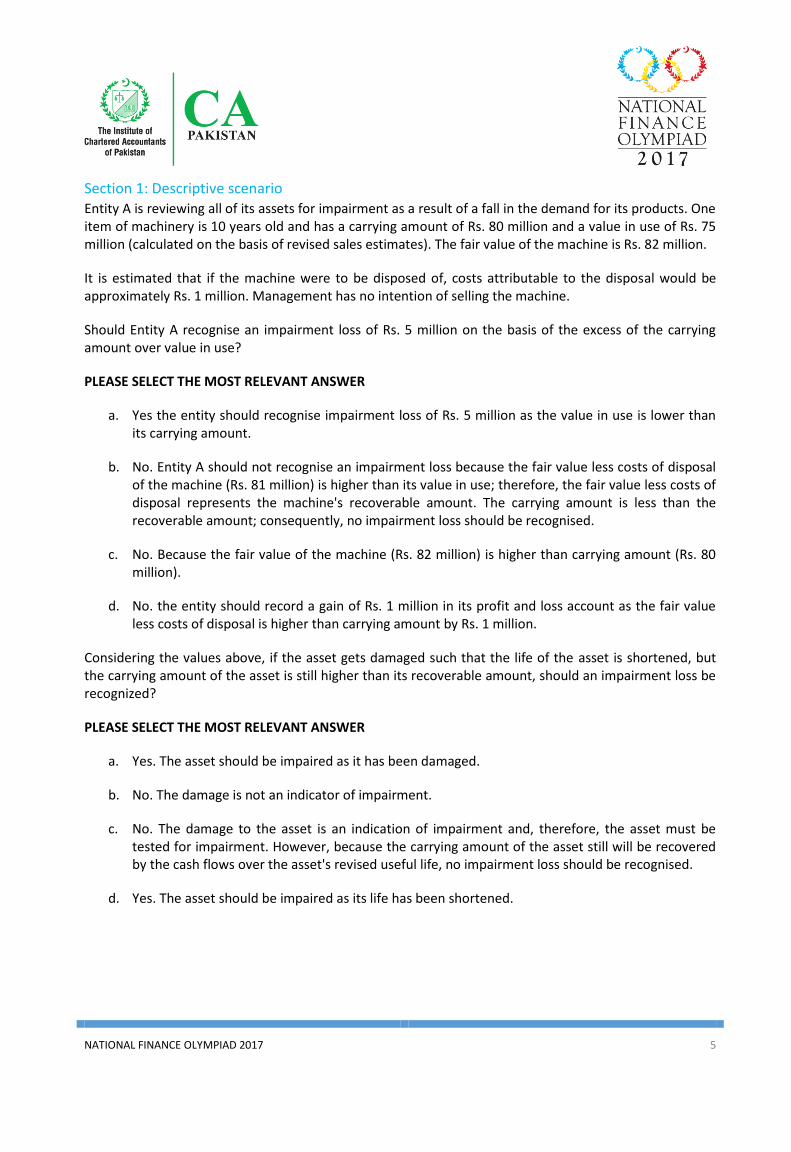

Section 1: Descriptive scenario Entity A is reviewing all of its assets for impairment as a result of a fall in the demand for its products. One item of machinery is 10 years old and has a carrying amount of Rs. 80 million and a value in use of Rs. 75 million (calculated on the basis of revised sales estimates). The fair value of the machine is Rs. 82 million.

It is estimated that if the machine were to be disposed of, costs attributable to the disposal would be approximately Rs. 1 million. Management has no intention of selling the machine.

Should Entity A recognise an impairment loss of Rs. 5 million on the basis of the excess of the carrying amount over value in use?

PLEASE SELECT THE MOST RELEVANT ANSWER

a. Yes the entity should recognise impairment loss of Rs. 5 million as the value in use is lower than its carrying amount.

b. No. Entity A should not recognise an impairment loss because the fair value less costs of disposal of the machine (Rs. 81 million) is higher than its value in use; therefore, the fair value less costs of disposal represents the machine's recoverable amount. The carrying amount is less than the recoverable amount; consequently, no impairment loss should be recognised.

c. No. Because the fair value of the machine (Rs. 82 million) is higher than carrying amount (Rs. 80 million).

d. No. the entity should record a gain of Rs. 1 million in its profit and loss account as the fair value less costs of disposal is higher than carrying amount by Rs. 1 million.

Considering the values above, if the asset gets damaged such that the life of the asset is shortened, but the carrying amount of the asset is still higher than its recoverable amount, should an impairment loss be recognized?

PLEASE SELECT THE MOST RELEVANT ANSWER

a. Yes. The asset should be impaired as it has been damaged.

b. No. The damage is not an indicator of impairment.

c. No. The damage to the asset is an indication of impairment and, therefore, the asset must be tested for impairment. However, because the carrying amount of the asset still will be recovered by the cash flows over the asset's revised useful life, no impairment loss should be recognised.

d. Yes. The asset should be impaired as its life has been shortened.

NATIONAL FINANCE OLYMPIAD 2017 6

In the recent budget, the sales tax on the products of Entity A has increased from 17% to 18%. Is this an indicator of impairment?

PLEASE SELECT THE MOST RELEVANT ANSWER

a. No. The increase in sales tax does not impacts the assets of the company

b. Yes. The change in tax rates may affect levels of demand for books and is an impairment indicator.

c. No. The increase in sales tax is a pass on item

d. No. This will only impact the future years

NATIONAL FINANCE OLYMPIAD 2017 7

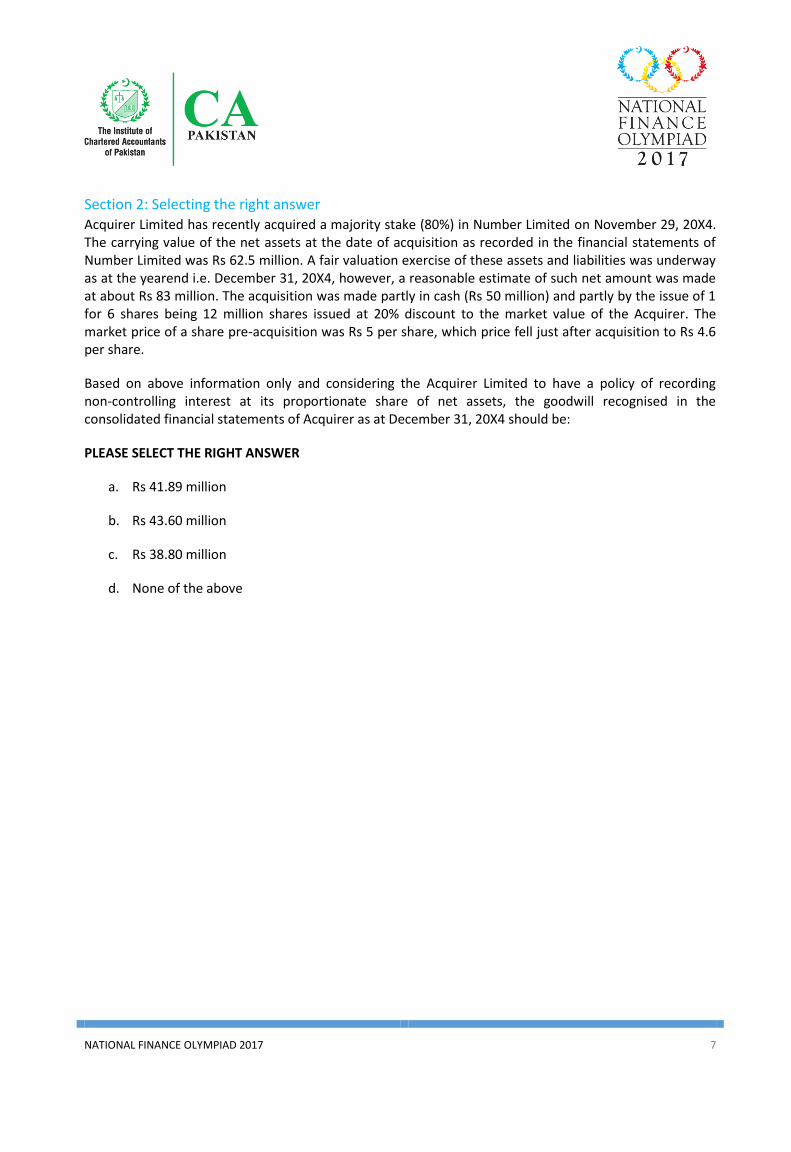

Section 2: Selecting the right answer Acquirer Limited has recently acquired a majority stake (80%) in Number Limited on November 29, 20X4. The carrying value of the net assets at the date of acquisition as recorded in the financial statements of Number Limited was Rs 62.5 million. A fair valuation exercise of these assets and liabilities was underway as at the yearend i.e. December 31, 20X4, however, a reasonable estimate of such net amount was made at about Rs 83 million. The acquisition was made partly in cash (Rs 50 million) and partly by the issue of 1 for 6 shares being 12 million shares issued at 20% discount to the market value of the Acquirer. The market price of a share pre-acquisition was Rs 5 per share, which price fell just after acquisition to Rs 4.6 per share.

Based on above information only and considering the Acquirer Limited to have a policy of recording non-controlling interest at its proportionate share of net assets, the goodwill recognised in the consolidated financial statements of Acquirer as at December 31, 20X4 should be:

PLEASE SELECT THE RIGHT ANSWER

a. Rs 41.89 million

b. Rs 43.60 million

c. Rs 38.80 million

d. None of the above

NATIONAL FINANCE OLYMPIAD 2017 8

Section 2: Selecting the most relevant According to IAS 16 ‘Property, plant and equipment’, which of the following gives the best definition of ‘Property, Plant & Equipment’? SELECT THE MOST RELEVANT ANSWER (a) Any assets held by an entity for more than one accounting period for use in the production or

supply of goods or services, for rentals to others or for administrative purposes. (b) Tangible assets held by an entity for more than 12 month for use in the production or supply of

goods or services, for rentals to others or for administrative purposes. (c) Tangible assets held by an entity for more than one accounting period for use in the production or

supply of goods or services, for rentals to others or for administrative purposes. (d) Any assets held by an entity for more than 12 months for use in the production or supply of goods

or services, for rental to others or for administrative purposes.

NATIONAL FINANCE OLYMPIAD 2017 9

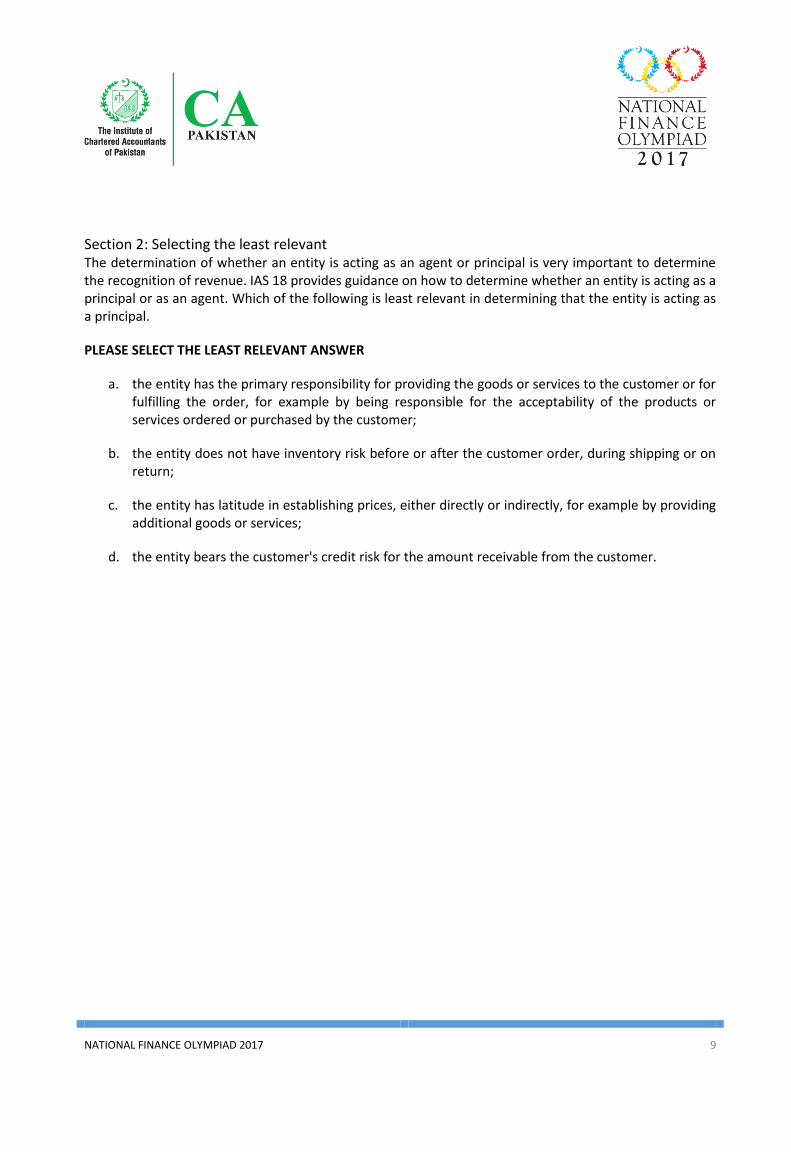

Section 2: Selecting the least relevant The determination of whether an entity is acting as an agent or principal is very important to determine the recognition of revenue. IAS 18 provides guidance on how to determine whether an entity is acting as a principal or as an agent. Which of the following is least relevant in determining that the entity is acting as a principal.

PLEASE SELECT THE LEAST RELEVANT ANSWER

a. the entity has the primary responsibility for providing the goods or services to the customer or for fulfilling the order, for example by being responsible for the acceptability of the products or services ordered or purchased by the customer;

b. the entity does not have inventory risk before or after the customer order, during shipping or on return;

c. the entity has latitude in establishing prices, either directly or indirectly, for example by providing additional goods or services;

d. the entity bears the customer's credit risk for the amount receivable from the customer.

NATIONAL FINANCE OLYMPIAD 2017 10

Section 2: Descriptive Scenario Entity B is carrying tax losses from its prior operations, some of which are expected to be lost in the near future. The tax law provides for a limited carry forward of up to six tax years succeeding the year of loss. The expiry table of above loss is:

Within 1 year Rs 12 million

Within 2 years Rs 25 million

Within 3 years Rs 39 million

Within 4 years Rs 54 million

Within 5 years Rs 70 million

It is expecting that following future taxable profits will be available to the Entity B:

Year 1 Rs 10 million

Year 2 Rs 15 million

Year 3 Rs 10 million

Year 4 Rs 15 million

Year 5 Rs 10 million

Year 6 Rs 15 million

Considering that some of above taxable profits will not be collected in the same year as earned, adjusting for the working capital changes, the cash profits after tax is expected to be:

Year 1 Rs 9 million

Year 2 Rs 14 million

Year 3 Rs 12 million

Year 4 Rs 11 million

Year 5 Rs 09 million

Year 6 Rs 20 million

The present value of the cash profits after tax works out to Rs 53.16 million at 10% p.a. which is the rate at which the company can borrow debt, and Rs 48.48 million at 15% p.a. which is the weighted average cost of capital to the entity.

NATIONAL FINANCE OLYMPIAD 2017 11

QUESTION 1: Based on above and considering that there are no other taxable temporary differences or tax planning opportunities, the closest amount in respect of carried forward losses for which deferred tax would be recorded as at the end of Year 0 is:

PLEASE SELECT THE CLOSEST ANSWER

a. Rs 48.48 million

b. Rs 53.16 million

c. Rs 54.00 million

d. Rs 58.00 million

Now assume that due to availability of above tax losses, the entity is not envisaging any tax payments until the year these tax losses are available. Applicable taxation rate is 35%. The cash profits pre-tax per year for the years beyond Year 6 are presumed to be at the level of taxable profits for the year 6.

QUESTION 2: Based on the above information, if the entity has a single cash generating unit (CGU), what is the value in use of the CGU (other than taxation and working capital items comprised in that CGU)?

PLEASE SELECT THE RIGHT ANSWER

a. Rs 88.95 million

b. Rs 91.23 million

c. Rs 112.17 million

d. Rs 115.14 million

Assume that the ‘recoverable amount’ in the above scenario has been worked out as Rs 100 million. The carrying value of assets of the CGU is Rs 107 million. Included in such carrying value is inventory of Rs 23 million being carried at lower of cost and net realisable value, and Goodwill of Rs. 8 million. Also, the entity has a deferred tax asset recorded at Rs 21 million.

QUESTION 3: Considering the above facts, after the allocation of impairment, what is the closest from the following at which deferred tax asset is expected to stand at?

PLEASE SELECT THE RIGHT ANSWER

a. Nil

b. Rs 11 million

c. Rs 19 million

d. Rs 21 million

NATIONAL FINANCE OLYMPIAD 2017 12

Section 3: Select the right answer ZK has been asked to quote a price for a special job that must be completed within one week.

The job requires a total of 100 skilled labour hours and 50 unskilled labour hours. The current employees are paid a guaranteed minimum wage of $525 for skilled workers and $280 for unskilled workers for a 35-hour week.

Currently, skilled labour has spare capacity amounting to 75 labour hours each week and unskilled labour has spare capacity amounting to 100 labour hours each week. Additional skilled workers and unskilled workers can be employed and paid by the hour at rates based on the wages paid to the current workers.

The materials required for the job are currently held in inventory at a book value of $5,000. The materials are regularly used by ZK and the current replacement cost for the materials is $4,500. The total scrap value of the materials is $1,000.

What is the relevant cost to ZK of using the materials in inventory on this job?

PLEASE SELECT THE RIGHT ANSWER

a. $1,000

b. $3,500

c. $4,500

d. $5,000

NATIONAL FINANCE OLYMPIAD 2017 13

Section 3: Selecting the most relevant P Limited is envisaging purchase of N Limited through acquisition of its 60% controlling shares. P Limited has an issued share capital of 10 million shares presently priced on Rs 12/- per share. The market capitalisation of N Limited is Rs 96 million with a share price of Rs 10/- per share. It is expected that the right shares will be used to raise funding for the purchase.

The option being considered is that sufficient funds be raised to cover the transaction price plus issue costs of 2% of funds raised. The deal for the shares of N Limited is envisaged at 30% premium to the market price.

Considering that the assumptions of the controlling share valuation at 30% premium to the market price are in line with market expectations, and that N Limited can presently issue rights shares at a discount of 20% to the market value, what is the expected impact of above on the share price of N Limited (ex-right price) if all the details about the transaction, including issue costs, are publically disclosed.

PLEASE SELECT THE CLOSEST ANSWER

a. An increase of Rs 5.60

b. An increase of Rs 3.48

c. A decrease of Rs 1.05

d. A decrease of Rs 1.15

NATIONAL FINANCE OLYMPIAD 2017 14

Section 3: Select the least relevant Company A is working in a capital intensive industry. Considering this information only, select the least relevant of the following:

PLEASE SELECT THE LEAST RELEVANT ANSWER

a. Asset based valuations for this business are relevant due to the capital intensive nature of the business.

b. Relative valuation multiples specifically those based on asset values can be an easy proxy valuation method for Company A.

c. Cash flow models are relevant for estimating the fair value of Company A as they use the expected exploitation of the company’s earning potential.

d. Considering that the earnings of the capital intensive industry are usually consistently constant, it is always advisable to use an earning based valuation for such businesses as that of Company A.

NATIONAL FINANCE OLYMPIAD 2017 15

Section 3: Descriptive scenario Following is the data in respect of Zee Limited’s inventory management, a company involved in simple trading of FMCG items:

Ordering cost per order (Rs) 5,000 Holding cost per unit of inventory p.a. (as a %age of cost) 11% Purchase price per inventory unit (Rs) 100 Sales price per unit (Rs) 110 Recent estimate of annual inventory units to be bought for sales (units) 157,611 Discounts are offered at the various order levels for purchases as follows: More than 10,000 units but up to 20,000 units 0.50% More than 20,000 units but up to 30,000 units 0.75% More than 30,000 1.00% QUESTION 1: Considering the above, what is the most economic order quantity?

PLEASE SELECT THE RIGHT ANSWER

a. 10,000 units

b. 20,000 units

c. 30,000 units

d. None of the above

Further, an enquiry has been made into the delivery periods, and the following probabilities have been estimated:

Delivery within 7 days (%age of times) 50% Delivery within 8 days (%age of times) 75% Delivery within 9 days (%age of times) 90% Delivery within 10 days (%age of times) always

QUESTION 2: Considering equal ustilisation of stock during the 365 days of a year, what safety stock level should be kept by the Zee Limited?

PLEASE SELECT THE RIGHT ANSWER

a. No safety stock

b. 1 day’s utilisation

c. 2 day’s utilisation

d. 3 day’s utilisation

NATIONAL FINANCE OLYMPIAD 2017 16

QUESTION 3: What re-order level should be followed by Zee Limited?

PLEASE SELECT THE CLOSEST ANSWER

a. 3,000 units

b. 3,500 units

c. 4000 units

d. 5000 units

NATIONAL FINANCE OLYMPIAD 2017 17

Section 4: Selecting the right answer Section 4: Selecting the right answer Federal government being a 75% shareholder in “Power Limited” has nominated ¾ of the directors on the board of Power Limited on January 1, 2013. The meetings of the board of directors was regularly held once in every quarter during the calendar years 2013 to 2015 during the tenure of its company secretary, Abid Shah. During November 2015, the office of the company secretary of Government Limited fell vacant due to resignation of Abid Shah. The appointment of the new company secretary was approved by the board in accordance with the requirements of Code of Corporate Governance in its meeting held on July 1, 2016. The new company secretary upon resuming office w.e.f. July 1, 2016 was of the view that the tenure of 3 years of the office of the directors nominated by the Federal Government had stayed vacated w.e.f. January 1, 2016 in accordance with the requirements of section 161 of the Companies Act, 2017 and, therefore, required quorum was not present during the meeting of the board of directors held on July 1, 2016. In view of the provisions of the Companies Act, 2017 what is the status of the approval of the new company secretary’s appointment? PLEASE SELECT THE RIGHT ANSWER (a) The approval of appointment of new company secretary by the board of directors does not suffer

any legal implications in view of the requirements of the Companies Act, 2017 vis-à-vis term of office of directors (i.e. section 161 of the Companies Act, 2017).

(b) Approval of the new company secretary can now take place only in the meeting of the board of

directors after the vacated positions are filled.

(c) Section 161 of the Companies Act, 2017 now stands deleted.

(d) The status of non-compliance / factual position is to be disclosed by the Board of Directors in statement of compliance with the best practices contained in the Code of Corporate Governance for the calendar year 2016.

NATIONAL FINANCE OLYMPIAD 2017 18

Section 4: Selecting the most relevant Is segregation of duties (SOD) a preventive or detective control?

PLEASE SELECT THE MOST RELEVANT

a. Preventive control as SOD prevent an individual from committing errors, fraud, theft, or other illegal acts, concealing errors or irregularities, or causing the inaccurate or incomplete reporting of financial information.

b. Detective control as SOD detect errors, etc., by an individual, since another person must be involved before the transaction is completed and has a chance to affect the accounting system.

c. Both

d. Segregation of duties is not a control in itself.

NATIONAL FINANCE OLYMPIAD 2017 19

Section 4: Selecting the least relevant The shareholders of Careful Limited (a company listed on Pakistan Stock Exchange) submitted a requisition before the directors of Careful Limited to hold an extraordinary general meeting (EOGM) to remove the auditor. The directors did not proceed within 21 days of the requisition to call the EOGM. Which of the following course of action is available to the above mentioned shareholders in view of the provisions of the Companies Act, 2017? PLEASE SELECT THE LEAST RELEVANT ANSWER (a) The above mentioned shareholders may themselves call the EOGM within three months from the

date of the deposit of the requisition, if the directors do not proceed to call the EOGM. (b) The above mentioned shareholders are required to provide a minimum of 21 days to the directors

to proceed to call the EOGM. (c) Fresh elections of directors is to be held as the office of all the directors stay vacated after lapse of

21 days of the requisition as they did not proceed to call the EOGM. (d) The above mentioned shareholders should at least represent the minimum threshold of 20% of the

voting powers.

NATIONAL FINANCE OLYMPIAD 2017 20

Section 4: Descriptive scenario You are company secretary of a listed company. In order to ensure the compliance of the code of corporate governance among other declarations, you have asked the directors of the company to provide the list of companies in which they are directors. In reply one of the directors of the company informs you that he is serving on the board of 10 listed companies including three listed subsidiary companies of your company.

QUESTON 1: Is he compliant with the requirement of maximum number of directorships of the code of corporate governance?

PLEASE SELECT THE RIGHT ANSWER

a. No because code of corporate governance restrict that no person shall be elected or nominated as a director of more than seven listed companies simultaneously.

b. Yes because maximum number of directorships of seven does not include listed subsidiaries of a listed holding company.

c. There is no such restriction in the code of corporate governance

d. In reply to the above, one of the independent director has confirmed that he has served as CEO of an associated company two years back.

QUESTION 2: Would he be still considered as an Independent Director?

PLEASE SELECT THE RIGHT ANSWER

a. Yes. There is no restriction in the Code of Corporate Governance that an independent director cannot be a CEO of an associated company

b. Yes. The Code requires that he/she is or has been the CEO of subsidiaries, associated company, associated undertaking or holding company in the last two years;

c. No. The Code requires that he/she is not or has not been the CEO of subsidiaries, associated company, associated undertaking or holding company in the last three years;

d. No. Any person who has served as CEO of an associated company cannot be considered as independent director

NATIONAL FINANCE OLYMPIAD 2017 21

QUESTION 3: In case the director as mentioned earlier is not considered as independent director, can you still meet the compliance of code of corporate governance with regards to independent director if you have one more independent direct out of total seven director.

PLEASE SELECT THE RIGHT ANSWER

a. No. A listed company is required to have at least three independent directors

b. Yes. The requirement of having an independent director is not mandatory. A listed company is preferred to have at least one independent director. So the company will be in compliance.

c. No. A listed company is required to have majority of the directors as independent director.

d. Yes. The board of directors of each listed company is required to have at least one and preferably one third of the total members of the board as independent directors.