Embed Size (px)

Citation preview

26 February 2015

Compiled by:

Research and Information Department

Project and Corporate Finance Department

National Budget 2015:

Addressing fiscal imbalances in a challenging economic

environment

2

Contents

• Economic and fiscal developments

• National Budget 2015: Tax proposals

• National Budget 2015: Expenditure

• Budget Review 2015: Select issues

• Concluding remarks

3

Economic and fiscal developments:

SA economic growth to recover modestly in 2015

• SA is experiencing a very difficult economic environment.

• Growth is not only extremely weak (a mere 1.5% in 2014), but has been on a declining trend.

• A modest recovery is anticipated, with GDP growth projected by NT at 2% for 2015, rising gradually in subsequent years.

• Domestic demand to remain subdued, with moderate rates of growth projected for consumer spending and investment.

• Government consumption spending forecast to expand, on average, by only 1% in real terms over MTEF.

• Exports still expected to take some strain in 2015, rising thereafter.

-2

-1

0

1

2

3

4

5

6

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

% C

han

ge (

y-o

-y)

Real GDP growth and outlook

Source: Stats SA, NT forecast

Forecast

4

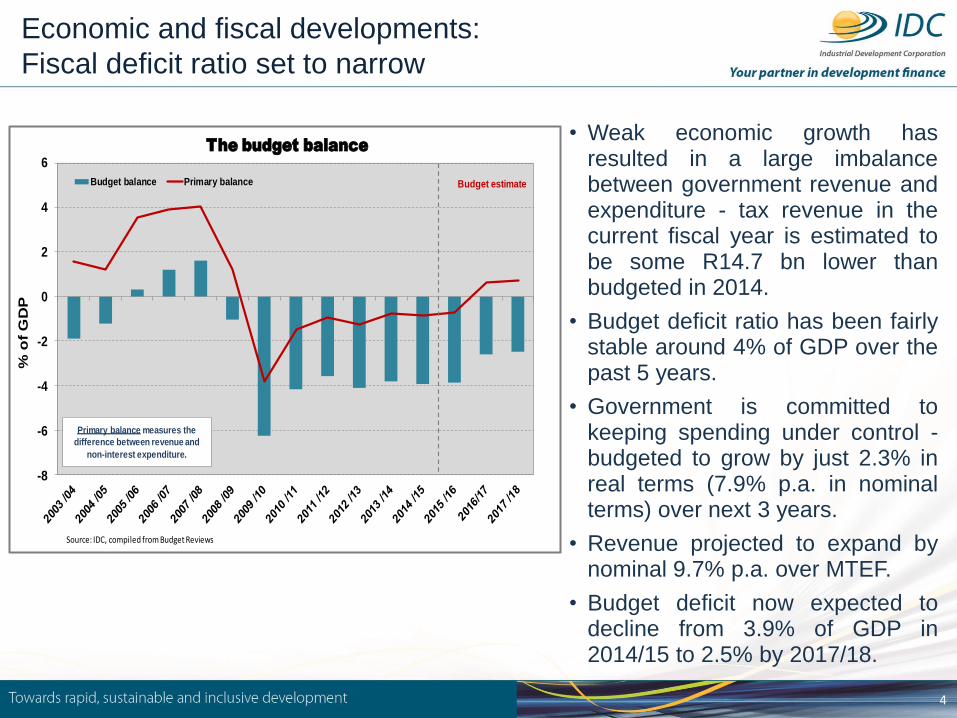

• Weak economic growth has resulted in a large imbalance between government revenue and expenditure - tax revenue in the current fiscal year is estimated to be some R14.7 bn lower than budgeted in 2014.

• Budget deficit ratio has been fairly stable around 4% of GDP over the past 5 years.

• Government is committed to keeping spending under control -budgeted to grow by just 2.3% in real terms (7.9% p.a. in nominal terms) over next 3 years.

• Revenue projected to expand by nominal 9.7% p.a. over MTEF.

• Budget deficit now expected to decline from 3.9% of GDP in 2014/15 to 2.5% by 2017/18.

Economic and fiscal developments:

Fiscal deficit ratio set to narrow

-8

-6

-4

-2

0

2

4

6

% o

f G

DP

The budget balance

Budget balance Primary balance

Source: IDC, compiled from Budget Reviews

Primary balance measures the

difference between revenue and

non-interest expenditure.

Budget estimate

5

-8

-7

-6

-5

-4

-3

-2

-1

0

1

% o

f G

DP

The budget balance in 2014 and 2017

2014 2017

Source: IDC, compiled from IMF data, National Treasury data for SA

Economic and fiscal developments:

SA budget balance within the global context

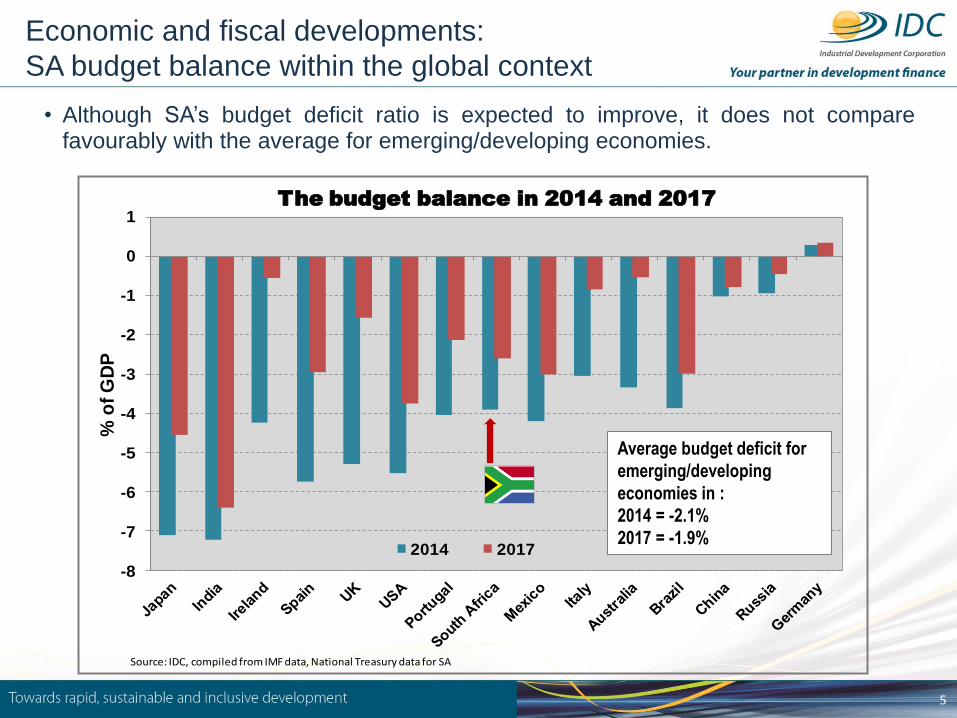

• Although SA’s budget deficit ratio is expected to improve, it does not compare favourably with the average for emerging/developing economies.

Average budget deficit for

emerging/developing

economies in :

2014 = -2.1%

2017 = -1.9%

6

Economic and fiscal developments:

SA debt rising further

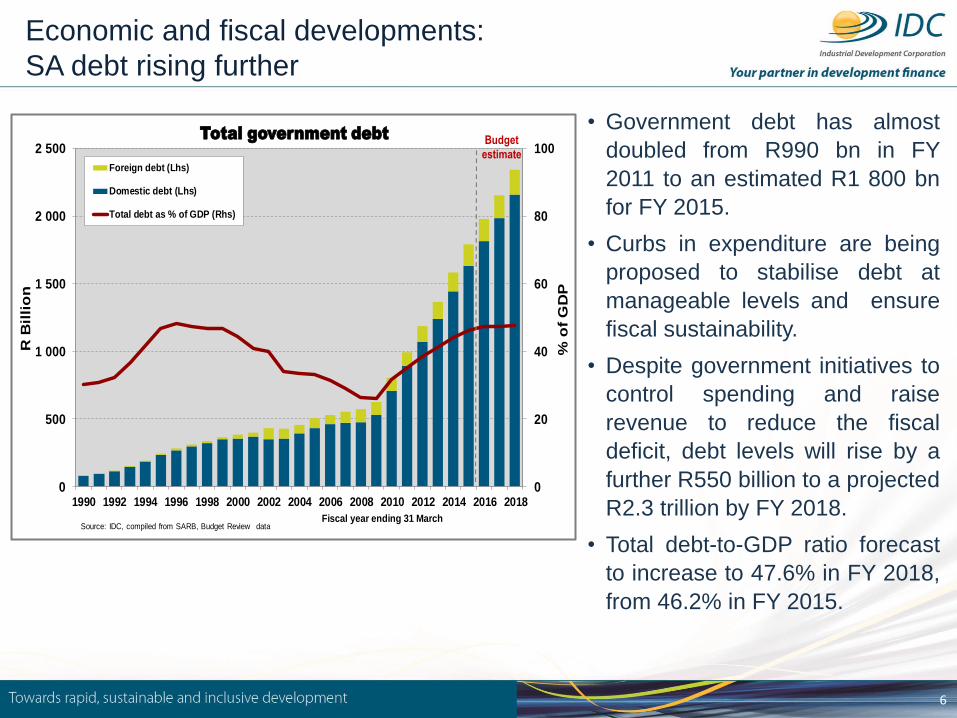

• Government debt has almost

doubled from R990 bn in FY

2011 to an estimated R1 800 bn

for FY 2015.

• Curbs in expenditure are being

proposed to stabilise debt at

manageable levels and ensure

fiscal sustainability.

• Despite government initiatives to

control spending and raise

revenue to reduce the fiscal

deficit, debt levels will rise by a

further R550 billion to a projected

R2.3 trillion by FY 2018.

• Total debt-to-GDP ratio forecast

to increase to 47.6% in FY 2018,

from 46.2% in FY 2015.

0

20

40

60

80

100

0

500

1 000

1 500

2 000

2 500

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

% o

f G

DP

R B

illi

on

Total government debt

Foreign debt (Lhs)

Domestic debt (Lhs)

Total debt as % of GDP (Rhs)

Source: IDC, compiled from SARB, Budget Review dataFiscal year ending 31 March

Budget

estimate

7

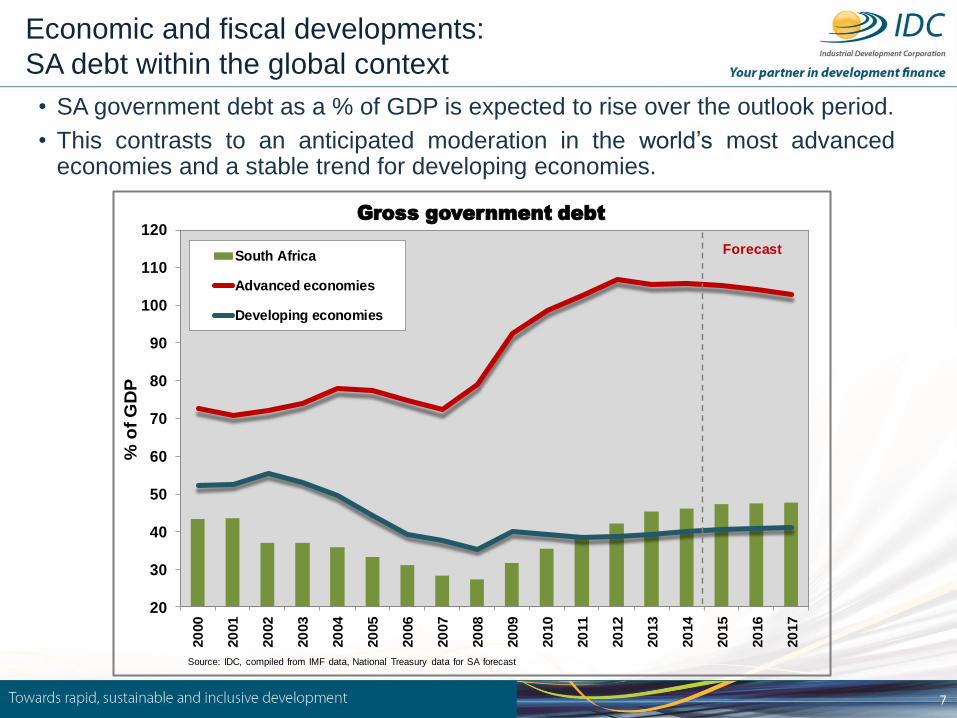

Economic and fiscal developments:

SA debt within the global context

• SA government debt as a % of GDP is expected to rise over the outlook period.

• This contrasts to an anticipated moderation in the world’s most advanced economies and a stable trend for developing economies.

20

30

40

50

60

70

80

90

100

110

120

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

% o

f G

DP

Gross government debt

South Africa

Advanced economies

Developing economies

Source: IDC, compiled from IMF data, National Treasury data for SA forecast

Forecast

8

Contents

• Economic and fiscal developments

• National Budget 2015:

Tax proposals

• National Budget 2015: Expenditure

• Budget Review 2015: Select issues

• Concluding remarks

9

National Budget 2015:

Main tax proposals

• Marginal rate of tax for individuals with

annual income > R181 900 will increase

by 1%; income tax brackets and

rebates raised by 4.2% due to fiscal

drag.

• Tax rate for Trusts to increase from 40%

to 41% (effective March 2015).

• More generous turnover regime for

small businesses.

• Fuel levy rockets 30.5c/l and Road

Accident Fund levy by 50c/l.

• Electricity levy increases from 3.5c/kWh

to 5.5c/kWh.

• Energy-efficiency savings tax incentive

rises from 45c/kWh to 95c/kWh.

• Further refinement on 3rd party backed

shares to be introduced.

• Several anomalies in legislation to be

reviewed.

-20 -15 -10 -5 0 5 10 15 20

Company taxes

Customs duties

VAT

Electricity levy

Other taxes

Personal income tax

Total tax revenue

Rand Billions

Change in tax collections in 2014/15 vs 2014 Budget

Overall tax shortfall = R14.7 bn

10

National Budget 2015:

Income tax on individuals

Rebates:

• Primary: R13 257 (2014: R12 726 )

• Secondary: R7 407 (2014: R7 110 )

• Tertiary rebate: R2 466 (2014: R2 367 )

Tax-free threshold:

• Age < 65: R73 650 (2014: R70 700 )

• Age 65 and over: R114 800 (2014: R110 200 )

• Age 75 and over: R128 500 (2014: R123 350 )

Tax-free interest-income annual threshold:

• Age < 65: R23 800 (2014: R23 800)

• Age 65 and over: R34 500 (2014: R34 500)

11

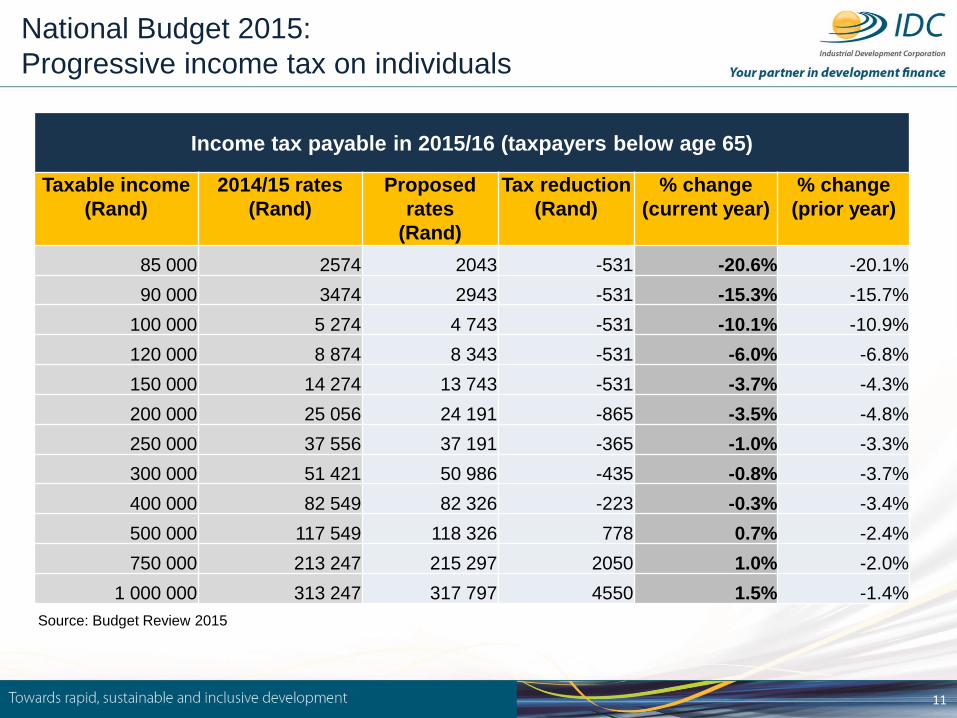

National Budget 2015:

Progressive income tax on individuals

Income tax payable in 2015/16 (taxpayers below age 65)

Taxable income

(Rand)

2014/15 rates

(Rand)

Proposed

rates

(Rand)

Tax reduction

(Rand)

% change

(current year)

% change

(prior year)

85 000 2574 2043 -531 -20.6% -20.1%

90 000 3474 2943 -531 -15.3% -15.7%

100 000 5 274 4 743 -531 -10.1% -10.9%

120 000 8 874 8 343 -531 -6.0% -6.8%

150 000 14 274 13 743 -531 -3.7% -4.3%

200 000 25 056 24 191 -865 -3.5% -4.8%

250 000 37 556 37 191 -365 -1.0% -3.3%

300 000 51 421 50 986 -435 -0.8% -3.7%

400 000 82 549 82 326 -223 -0.3% -3.4%

500 000 117 549 118 326 778 0.7% -2.4%

750 000 213 247 215 297 2050 1.0% -2.0%

1 000 000 313 247 317 797 4550 1.5% -1.4%

Source: Budget Review 2015

12

National Budget 2015:

Income tax on individuals

Medical tax credits:

• Monthly medical tax credits for medical

scheme contributions will increase to R270

(2014: R257) for first 2 beneficiaries and

R181 (2014: R172) for each additional one

(effective 1 March 2015).

• Medical tax credits to be taken into account

for both PAYE and provisional tax for

employees over 65.

Bus rapid transit payments:

• Tax treatment of payment (compensation for

loss of income) to affected taxi operators will

be reviewed.

13

National Budget 2015:

Income tax on individuals

Employee share schemes:

• Taxation of directors and employees on

vesting of equity instruments will be

reviewed in light of the anomalies that

exist in the application of section 8C of

the Income Tax Act (ITA) in relation to the

attribution of capital gains, income tax

exemption of dividends and the provision

related to the return of capital.

Retirement

• Non-residents who have worked in SA for

a fixed term of employment and

contributed to a Retirement Annuity (RA)

will be allowed to withdraw their RA once

they return to their home countries.

14

National Budget 2015:

Income tax on individuals

• The taxation of contributions and the

rules on compulsory annuitisation for

pension funds, provident funds and

retirement annuity funds will change

from 1 March 2016.

• Deductible contributions will be limited

to 27.5% of the greater of taxable

income or remuneration per year.

• From 1 March 2015 a retirement fund

member will be able to defer the

drawings of their retirement income until

after their retirement date (if the

retirement fund allows it). A maximum

age at which withdrawals must be taken

will be introduced.

15

National Budget 2015:

Income tax on individuals

Estate duty:

• Section 25 of the ITA provides that no income

or disposal is triggered in the deceased’s

hands upon death, but that income may be

recognised in the hands of the deceased

estate, heir or legatee.

• Paragraph 40 of schedule 8, however,

recognises capital gains and losses upon

death. To address the anomalies created

when the two regimes interact, the provisions

will be examined and amendments maybe

proposed.

• To eliminate the possibility for estate duty

avoidance, government proposes that an

amount equal to the nondeductible

contributions to retirement funds be included

in the dutiable estate when a retirement fund

member passes away.

16

National Budget 2015:

Corporate tax

Corporate re-organisation rules:

• Relief to be provided to township developers

to transfer their township development

allowance in terms of the section 45 of the

ITA.

• Asset for share transaction: current anti-

avoidance measure in section 42(5) of the ITA

will be clarified.

• Cross-border intra-group transactions:

proposed that this sub-paragraph be

amended to clarify that the provisions of this

section refer to the same group of companies

as defined in section 1 of the ITA.

Section 9C – shares held for 3 years

• The “return of capital” and meaning of

“disposal” will be reviewed.

17

National Budget 2015:

Corporate tax

Third-party backed shares:

• In 2014, changes were made in the ITA

regarding the refinancing of 3rd-party-backed

shares for qualifying transactions and limited

pledges. Further refinements are needed to

clarify the requirements or meaning of

“qualifying purpose” to further the provisions’

objectives.

REITS (Real Estate Investment Trusts):

• Unlisted property-owning companies do not

qualify for the same special tax dispensation

as listed real estate investment trusts.

Government proposes that unlisted property-

owning companies should qualify for the

same tax treatment if they become regulated.

A regulatory framework for unlisted property-

owning companies will be developed.

18

National Budget 2015:

Corporate tax

Industrial policy projects:

• Section 12I incentive will be extended to 31 December 2017.

Depreciation allowance for hydropower generation

• The restriction of 30 megawatt for electricity generation will be

reconsidered if the environmental concerns are addressed.

Hedge funds:

• Hedge funds to be declared “collective investment schemes”,

subjecting them to similar rules in terms of the Collective

Investment Schemes Control Act (2002).

• Tax amendments will be considered to minimise any inadvertent

tax consequences that may arise from the restructuring.

Securities lending arrangements:

• Current tax treatment of securities’ lending arrangements will be

reviewed.

• Tax treatment of the transfer in beneficial ownership of collateral

will be reviewed to account for corporate actions during the term

of such arrangements.

19

National Budget 2015:

Corporate tax

Urban development zone incentive (UDZ):

• Consideration will be given to allow

municipalities to demarcate 2 or more UDZs

per municipality with an overall limit of the

area of the UDZs.

Research and development:

• The backlog in approvals of applications by

the adjudication committee will be addressed

to ensure that businesses who have to wait

months are not disadvantaged.

• The issue of third-party funding for R&D

activities will be considered.

Government grants:

• Tax treatment of government grants to be

reviewed.

20

National Budget 2015:

Corporate tax

Right of use of transmitting electronic

communications outside SA territorial

waters:

• Review of the deduction for premiums, or

consideration paid for the “right of use” of

transmission lines or cables used to transmit

electronic communications outside SA

territorial waters, where the term of the right

of use is 20 years or more.

Film incentive:

• Government will refine film incentives in

section 12O of the ITA to remove anomalies

arising as a result of the interaction of its

provisions with other provisions in the Act.

• Excise duty on digital cinema projector

costing > R250 000 will be abolished to

promote commercial usage.

21

National Budget 2015:

Corporate tax

Section 12C manufacturing asset allowance:

• Due to changes in the business models of

some manufacturing activities, government

will review the conditions of the granting of

this allowance.

Special Economic Zones (SEZs):

• The risk that profits may be artificially shifted

from fully taxable connected persons to the

qualifying SEZ company will be mitigated.

Government proposes that a company be

disqualified from the tax benefit if more than

20% of its expenditure or gross income arises

from transactions with connected persons.

Turnover tax regime for micro businesses:

• Government proposes to adjust the rates and

thresholds to make the turnover tax more

attractive.

22

National Budget 2015:

International tax

Foreign tax credits for service fees:

• The special foreign tax credit for withholding

taxes imposed on SA residents by foreign

countries for services rendered in SA for

clients who were residents in those countries

will be withdrawn.

Capital gains tax implications on cross-

issue of shares:

• If a SA resident company issues shares as a

consideration for an acquisition of shares in a

foreign company, it will result in a capital gain

for the resident company. Government will

consider relaxing the provision, as it curtails

the growth and expansion of SA

multinationals.

23

National Budget 2015:

International tax

Controlled foreign company rules (CFC):

• Certain CFC legislation to prevent the shifting

of income offshore through the sale of goods

by a CFC to a connected resident will be re-

introduced following their removal with the

application of the transfer pricing rules in 2011.

Sale of immovable property by non-residents:

• Section 35A of the ITA states that a purchaser

does not need to withhold tax from a deposit

until the agreement for that disposal has been

entered into. It is proposed that the wording

should be amended to clarify the timing of the

withholding.

• The definition of “immovable property” will be

reviewed.

24

National Budget 2015:

International tax

Withholding tax on interest and services:

• “Interest” for withholding tax purposes will be

defined to avoid confusion with other

definitions of interest in the ITA.

• Interest paid to a non-resident for debt owed

by another non-resident will be exempted

unless the other non-resident was present in

SA for a period exceeding 183 days or the

debt is effectively connected to a permanent

establishment in SA.

• Withholding tax on services will be reviewed

to clarify definitions and remove any

anomalies.

Base erosion and profit shifting

• Government will propose amendments to

improve transfer-pricing documentation and

reporting.

25

National Budget 2015:

Indirect taxes

Fuel levies:

• General fuel levy to increase by 30.5c/l.

• Road Accident Fund levy to rise by 50c/l.

Excise duties on tobacco and alcohol:

• Excise duties on alcoholic beverages increase

between 4.8% and 8.5%.

• The excise duties on tobacco products increase

between 5% and 7%.

• To level the paying field, an additional excise duty

category is proposed for grain-based fermented

beverages (flavoured alcoholic beverages using

100% unconverted grains).

26

National Budget 2015:

Indirect taxes

Electricity levies:

• Set to increase from 3.5c/kWh to 5.5c/kWh to

fund energy-efficiency savings tax incentive.

Value Added Tax:

• The current exempt status for “educational

services” will be reviewed.

• The threshold of R2,5m for natural persons and

unincorporated bodies registered on the payment

basis rather than on the accrual basis may

increase and the scope may be broadened to

include incorporated businesses.

• The regulations on foreign electronic services will

be updated to include software and other

electronic services.

27

National Budget 2015:

Indirect taxes

• The threshold requirements of an establishment that

provides “commercial accommodation” will be

reviewed to limit potential abuse.

• The corporate relief granted in applying the corporate

reorganisation rules (section 8(25) of the VAT Act)

does not currently apply to joint ventures and

partnerships. The VAT Act will be amended to allow

reorganisation for all vendors.

• The time of supply rules will be amended to clarify the

time and value of supply where the supply cannot be

determined until a future date.

• Section 11(1)(q) of the VAT Act provides for the zero-

rating of goods supplied to a non-resident recipient

that are delivered to the recipient’s customer in SA. It

is proposed that a comparable provision be included in

the VAT Act to cater for such transactions where the

supply is of services only and they do not relate to any

goods situated in SA.

28

National Budget 2015:

Environmental tax

Tyre levy:

• Government has designed additional environmental levies on a range of waste

streams to help divert waste away from landfills towards reuse, recycling and

recovery. Government proposes a tyre levy, with effect from the last quarter of 2015,

to be implemented through the Customs and Excise Act and collected by SARS.

Carbon tax:

• The draft Carbon Tax Bill will be published later in 2015 and will allow for a further

period of consultation. This will also allow for the tax to be aligned with the proposed

carbon budgets and the required amendments to the Customs and Excise Act to

provide for the administration of the carbon tax.

Diesel refund system:

• The implementation of the diesel refund system has experienced technical and

administrative challenges and will be comprehensively reviewed.

Energy-efficiency savings tax incentive:

• Increase from 45c/kWh to 95c/kWh (to be funded from carbon tax).

29

National Budget 2015:

Miscellaneous taxes

Transfer Duty Act amendments and rate adjustments:

• The definitions of “date of acquisition” and “property” in the Transfer Duty Act

need to be reviewed to align it with other legislation.

Transfer duty rate adjustments 2014/15 – 2015/16

2014/15 2015/16

Property value (R) Rates of tax Property value (R) Rates of tax

R0 - R600 000 0% of property value R0 - R750 000 0% of property value

R600 001 - R1 000 000

3% of property value above

R600 000 R750 001 - R1 250 000

3% of property value above

R750 000

R1 000 001 - R1 500

000

R12 000 + 5% of property

value above R1 000 000

R1 250 001 - R1 750

000

R15 000 + 6% of property

value above R1 250 000

R1 500 001 +

R37 000 + 8% of property

value above R1 500 000

R1 750 001 - R2 250

000

R45 000 + 8% of property

value above R1 750 000

R2 250 001+

R85 000 + 11% of property

value above R2 250 000

30

National Budget 2015:

Miscellaneous taxes

National gambling tax bill:

• The bill will be processed in 2015.

Tax administration:

• Move towards self-assessment system for income tax is

proposed.

• Appeal and dispute resolution procedures for customs

and excise: Uniform appeal and dispute resolution

procedures for taxes administered by SARS are

proposed by aligning the procedures under the Customs

Control Act (2014), the Customs Duty Act (2013) and the

Customs and Excise Act (1964) with dispute resolution

procedures under the Tax Administration Act (2011).

31

Contents

• Economic and fiscal developments

• National Budget 2015: Tax proposals

• National Budget 2015:

Expenditure

• Budget Review 2015: Select issues

• Concluding remarks

32

National Budget 2015:

Government’s commitment to fiscal discipline

• Government to reduce expenditure ceiling by

an aggregate of R25 billion over the coming 2

years.

• These reductions will emanate largely from

budgetary cuts, lower or conditional

allocations, reduced wasteful expenditure and

the implementation of cost-effective service-

delivery models.

• These include:

– National departments’ budget cuts on non-

core goods and services;

– Expenditure cuts on non-critical items of

machinery and equipment;

– Reductions in allocations to public entities

and transfers to provinces;

– Conditional allocations to local

government.

33

Procurement of goods and services:

• Following cost containment measures introduced for

items such as accommodation, flights, car rentals

and consultants, NT will expand (by June 2015)

these to categories such as conferences and

workshops.

• National price-referencing system (providing price

ranges of goods and services commonly used by

the state) to be rolled out from 1 April 2015.

• eTender portal:

– Will be available for use by national and

provincial govt. depts. from 1 April 2015 (must

publish all tenders > R500 000) and for local

govt. from 1 July 2015 (tenders > R200 000).

– It will widen state’s access to potential

suppliers, increase transparency in bid

evaluation and do away with tender viewing

costs for small businesses.

Budget Review 2015:

Public sector cost containment and tenders

34

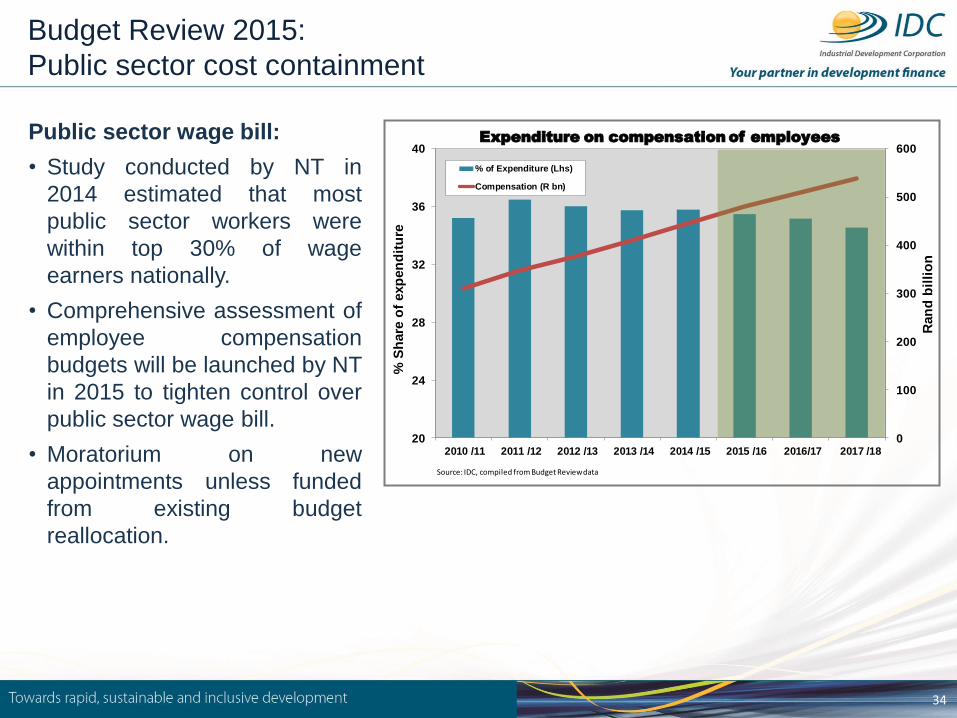

Public sector wage bill:

• Study conducted by NT in

2014 estimated that most

public sector workers were

within top 30% of wage

earners nationally.

• Comprehensive assessment of

employee compensation

budgets will be launched by NT

in 2015 to tighten control over

public sector wage bill.

• Moratorium on new

appointments unless funded

from existing budget

reallocation.

Budget Review 2015:

Public sector cost containment

0

100

200

300

400

500

600

20

24

28

32

36

40

2010 /11 2011 /12 2012 /13 2013 /14 2014 /15 2015 /16 2016/17 2017 /18

Ran

d b

illi

on

% S

hare

of

exp

en

dit

ure

Expenditure on compensation of employees

% of Expenditure (Lhs)

Compensation (R bn)

Source: IDC, compiled from Budget Review data

35

National Budget 2015:

Government spending with emphasis on development impact

• Consolidated non-interest spending will

increase from R1.1 trillion in 2015/16 to

R1.4 trillion by 2017/18.

• Social spending accounts for the bulk of

government spending to address social

security gaps.

– Health department to increase its

HIV/AIDS treatment and prevention

programme.

– Basic education to improve school

infrastructure, curriculum delivery

and ensure adequate supply of

quality teachers.

– Social assistance grants account for

94.2% of the Social Development

budget over the MTEF period, with

about 17.5 million beneficiaries

receiving assistance grants over the

same period.

36

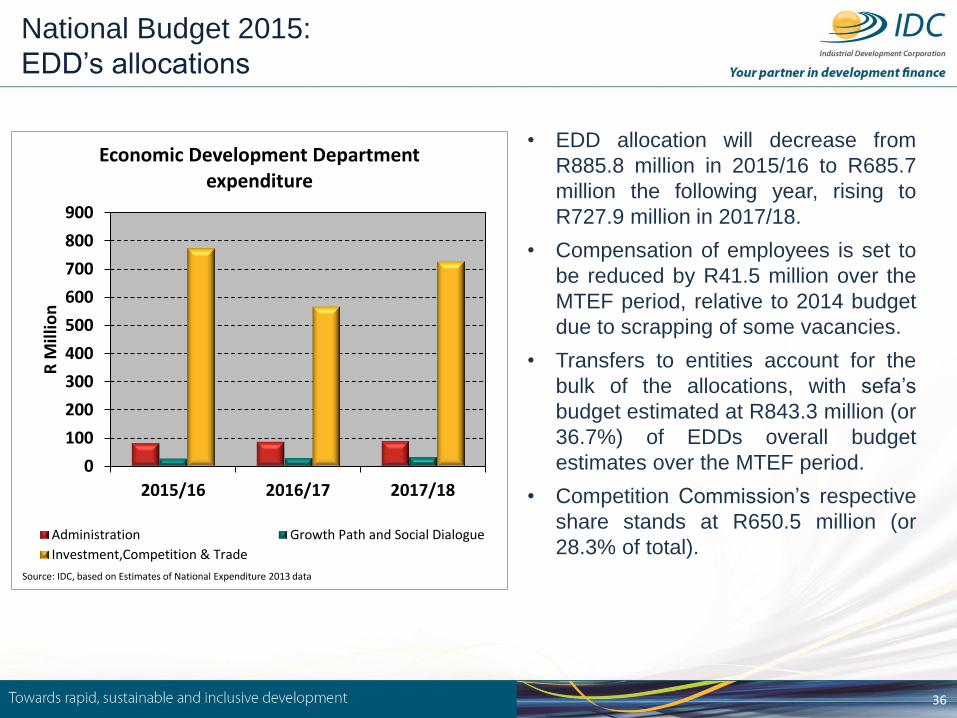

National Budget 2015:

EDD’s allocations

0

100

200

300

400

500

600

700

800

900

2015/16 2016/17 2017/18

R M

illio

n

Economic Development Department expenditure

Administration Growth Path and Social Dialogue

Investment,Competition & Trade

Source: IDC, based on Estimates of National Expenditure 2013 data

• EDD allocation will decrease from

R885.8 million in 2015/16 to R685.7

million the following year, rising to

R727.9 million in 2017/18.

• Compensation of employees is set to

be reduced by R41.5 million over the

MTEF period, relative to 2014 budget

due to scrapping of some vacancies.

• Transfers to entities account for the

bulk of the allocations, with sefa’s

budget estimated at R843.3 million (or

36.7%) of EDDs overall budget

estimates over the MTEF period.

• Competition Commission’s respective

share stands at R650.5 million (or

28.3% of total).

37

National Budget 2015:

DTI’s allocations

0

1

2

3

4

5

6

7

2015/16 2016/17 2017/18

R B

illio

n

Department of Trade and Industry expenditure

Incentive development and administrationIndustrial developmentTrade and Investment South AfricaOther

Source: IDC, based on Estimates of National Expenditure 2013 data

• The dti’s allocation is set to increase from

R9.6 billion in 2015/16, to R10.5 billion in

the subsequent year before easing to

R9.5 billion in 2017/18.

• Incentives for manufacturing

development (incl. APDP and MCEP)

projected at R10.7 billion over the MTEF

period to promote production expansions,

enhance competitiveness, create/retain

jobs.

• Customised Sector Programme (CSP)

has been allocated R490 million over the

MTEF.

• Clothing & Textile Production Incentive

(CTPI): R2.6 billion.

• Industrial Development Zones: R120

million.

• Special Economic Zones: R3.5 billion.

• Expenditure on localisation projected at

R6.2 billion over the coming 3 years.

38

Contents

• Economic and fiscal developments

• National Budget 2015: Tax proposals

• National Budget 2015: Expenditure

• Budget Review 2015:

Select issues

• Concluding remarks

39

• Review of SOEs undertaken in 2011 to determine how

well they execute their mandates. Report’s

recommendations considered at Cabinet Lekgotla

2015, with following interventions under consideration:

– Establishment of inter-ministerial committee to

improve alignment/coordination;

– Identification of SOEs deemed integral to

national development, followed by delineating

approach to acquisition/disposal of public assets

based on strategic requirements;

– Overarching legislation to govern SOEs;

– Financial implications of developmental

mandates to be more clearly set out in

shareholder compacts;

– Explore alternative options to strengthen balance

sheets (e.g. private investment) and open up

opportunities for private investment in sectors

dominated by SOEs (e.g. REIPPPP).

Budget Review 2015:

Enhance contribution of SOEs to development

40

• Development finance institutions (DFIs) have increased their lending activity rapidly in

support of NDP (loan books grew from R40.5 bn in 2008/09 to R108.7 bn in 2013/14).

• Combined loan portfolios set to expand to R178.3 bn by 2016/17.

• To ensure sustainability, risks associated with lending activities must be managed

prudently.

• Review of Land Bank, aimed at restructuring it for improved operational efficiencies,

scheduled for 2015.

Budget Review 2015:

DFIs in support of economic development

Aggregate assets of SA’s DFIs in 2013/14:

R249.1 bn out of combined SOE total of R903.6 bn

IDC56%

DBSA25%

Land Bank15%

Other DFIs4%

Other SOEs72%

DFIs28%

41

Budget Review 2015:

Infrastructure development

Electricity infrastructure:

• RE projects have added 1 522 MW by December 2014, 3 725 MW in new generation capacity is expected by 2017, with a further 14 550 MW of PV, CSP and wind capacity will be procured in future.

• A further 810 000 households will be provided with access to on-grid electricity and 65 000 households with non-grid electrification.

• Government’s “War room” is working on:

– Resolving funding, maintenance and diesel supply concerns;

– Speeding up the construction of Medupi and Kusile (Completion of Medupi’s 1st unit expected in the second-half of 2015, that of Kusile in a year later);

– Increasing co-generation capacity by around 800MW in the short-term;

– Switching Eskom OCGT from diesel to natural gas, with an additional 3 126MW of gas generation expected to be available by 2020;

– Procuring up to 2 500MW from coal IPPs by 2020.

• Electricity tariff increases expected to be higher than previously determined by Nersa to support Eskom revenue generating ability.

.

42

Budget Review 2015:

Infrastructure development

Transport infrastructure:

• Both Transnet and PRASA are upgrading and acquiring locomotives and rolling stock, whilst Transnet is expanding capacity on its manganese, iron ore and coal lines and/or terminals.

• Transnet continued to sustain profitability as revenue increased, on the back of higher mineral volumes and rising container traffic. Substantial cost savings were realised.

• Transnet lowered its capital expenditure plans as a result of continued disappointing global growth, weaker demand and lower commodity prices.

Government spending on infrastructure:

• National, provincial and local governments are expected to increase infrastructure spending by 21.4% to R362.4 billion over the next three years, focussing on human settlements, health, water and education infrastructure.

43

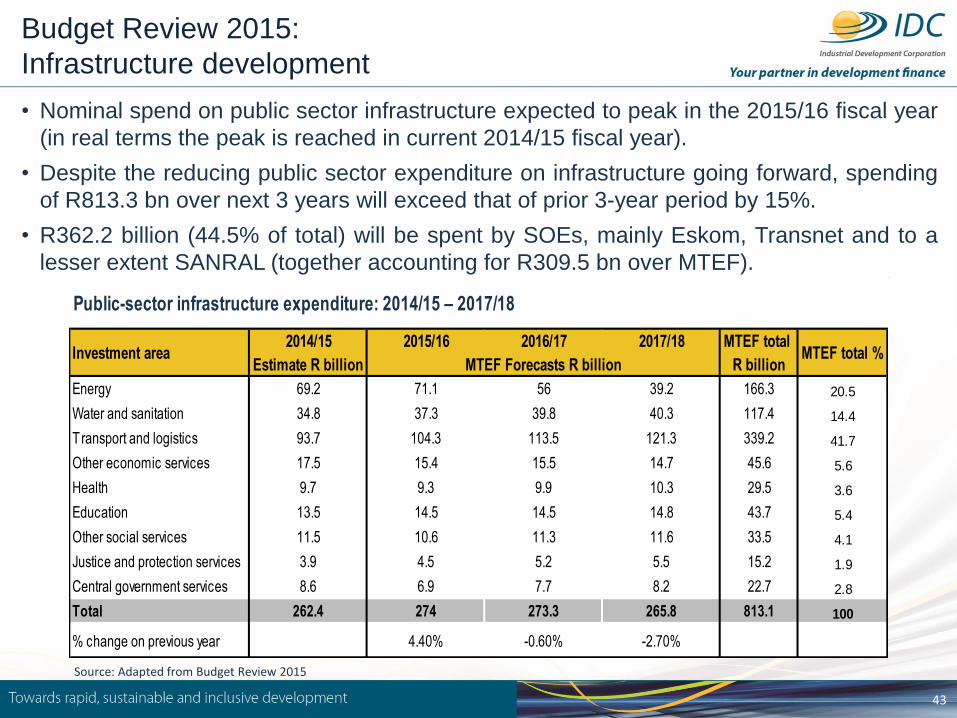

Budget Review 2015:

Infrastructure development

• Nominal spend on public sector infrastructure expected to peak in the 2015/16 fiscal year

(in real terms the peak is reached in current 2014/15 fiscal year).

• Despite the reducing public sector expenditure on infrastructure going forward, spending

of R813.3 bn over next 3 years will exceed that of prior 3-year period by 15%.

• R362.2 billion (44.5% of total) will be spent by SOEs, mainly Eskom, Transnet and to a

lesser extent SANRAL (together accounting for R309.5 bn over MTEF).

Source: Adapted from Budget Review 2015

2014/15 2015/16 2016/17 2017/18 MTEF total

Estimate R billion R billion

Energy 69.2 71.1 56 39.2 166.3 20.5

Water and sanitation 34.8 37.3 39.8 40.3 117.4 14.4

Transport and logistics 93.7 104.3 113.5 121.3 339.2 41.7

Other economic services 17.5 15.4 15.5 14.7 45.6 5.6

Health 9.7 9.3 9.9 10.3 29.5 3.6

Education 13.5 14.5 14.5 14.8 43.7 5.4

Other social services 11.5 10.6 11.3 11.6 33.5 4.1

Justice and protection services 3.9 4.5 5.2 5.5 15.2 1.9

Central government services 8.6 6.9 7.7 8.2 22.7 2.8

Total 262.4 274 273.3 265.8 813.1 100

% change on previous year 4.40% -0.60% -2.70%

Public-sector infrastructure expenditure: 2014/15 – 2017/18

Investment area MTEF total %MTEF Forecasts R billion

44

Budget Review 2015:

Infrastructure development

• SOE adherence to infrastructure spending plans has improved (98% actual spend vs.

budget ratio in 2013/14, from 80% in 2012/13).

• The improved performance could be related to improved budgeting in recent times, as

capital expenditure projections have been revised lower over consecutive years.

0

50

100

150

200

250

300

350

2006/07 2007/08 2008/09 2009/10 2010/11 2011/12 2012/13 2013/14 2014/15 2015/16 2016/17 2017/18

R B

illi

on

Public sector infrastructure expenditure

Budget 2010 Budget 2011

Budget 2012 Budget 2013

Budget 2014 Budget 2015

Source: IDC, compiled from Budget Review data

3-year outlook

45

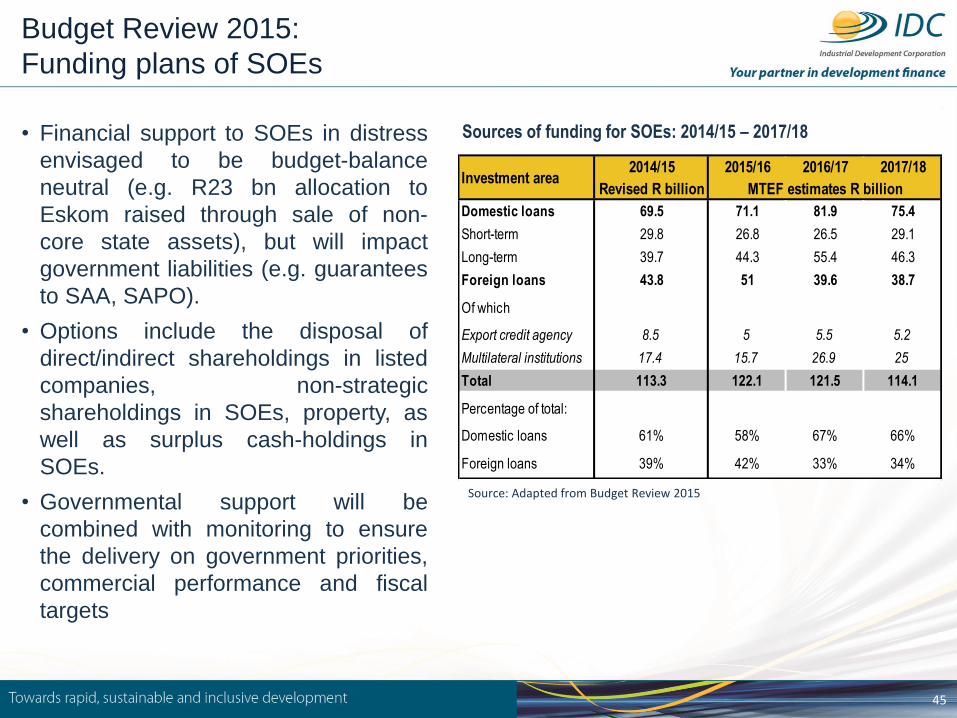

Budget Review 2015:

Funding plans of SOEs

• Financial support to SOEs in distress

envisaged to be budget-balance

neutral (e.g. R23 bn allocation to

Eskom raised through sale of non-

core state assets), but will impact

government liabilities (e.g. guarantees

to SAA, SAPO).

• Options include the disposal of

direct/indirect shareholdings in listed

companies, non-strategic

shareholdings in SOEs, property, as

well as surplus cash-holdings in

SOEs.

• Governmental support will be

combined with monitoring to ensure

the delivery on government priorities,

commercial performance and fiscal

targets

Source: Adapted from Budget Review 2015

2014/15 2015/16 2016/17 2017/18

Revised R billion

Domestic loans 69.5 71.1 81.9 75.4

Short-term 29.8 26.8 26.5 29.1

Long-term 39.7 44.3 55.4 46.3

Foreign loans 43.8 51 39.6 38.7

Of which

Export credit agency 8.5 5 5.5 5.2

Multilateral institutions 17.4 15.7 26.9 25

Total 113.3 122.1 121.5 114.1

Percentage of total:

Domestic loans 61% 58% 67% 66%

Foreign loans 39% 42% 33% 34%

Sources of funding for SOCs: 2014/15 – 2017/18

Investment areaMTEF estimates R billion

Sources of funding for SOEs: 2014/15 – 2017/18

46

Contents

• Economic and fiscal developments

• National Budget 2015: Tax proposals

• National Budget 2015: Expenditure

• Budget Review 2015: Select issues

• Concluding remarks

47

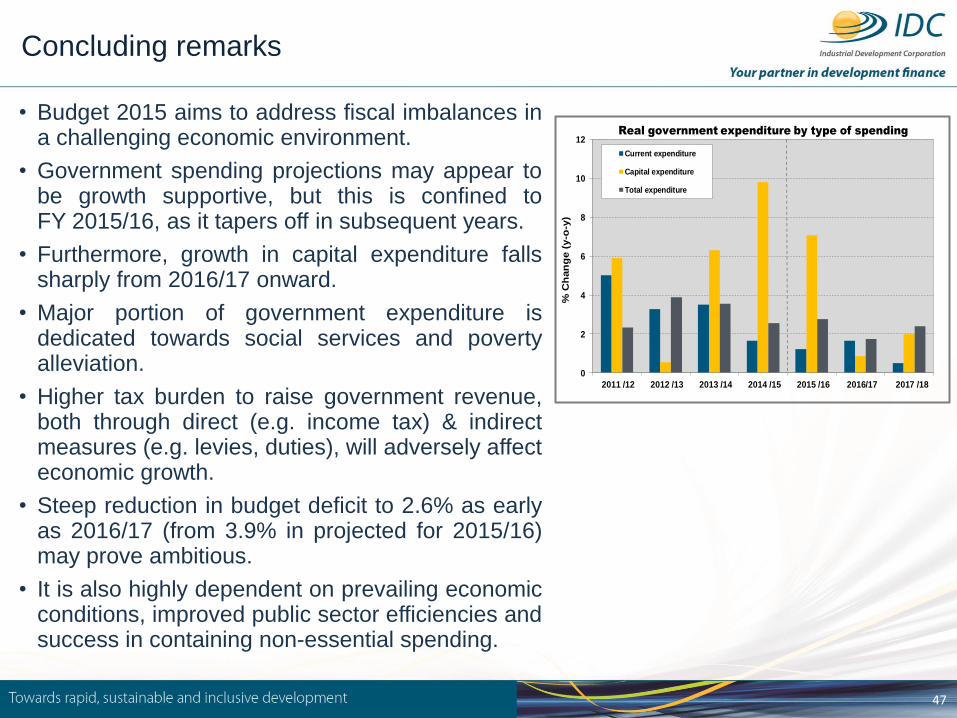

Concluding remarks

• Budget 2015 aims to address fiscal imbalances in a challenging economic environment.

• Government spending projections may appear to be growth supportive, but this is confined to FY 2015/16, as it tapers off in subsequent years.

• Furthermore, growth in capital expenditure falls sharply from 2016/17 onward.

• Major portion of government expenditure is dedicated towards social services and poverty alleviation.

• Higher tax burden to raise government revenue, both through direct (e.g. income tax) & indirect measures (e.g. levies, duties), will adversely affect economic growth.

• Steep reduction in budget deficit to 2.6% as early as 2016/17 (from 3.9% in projected for 2015/16) may prove ambitious.

• It is also highly dependent on prevailing economic conditions, improved public sector efficiencies and success in containing non-essential spending.

0

2

4

6

8

10

12

2011 /12 2012 /13 2013 /14 2014 /15 2015 /16 2016/17 2017 /18

% C

han

ge (

y-o

-y)

Current expenditure

Capital expenditure

Total expenditure

Real government expenditure by type of spending

48

Concluding remarks

• Government’s gross debt to rise by a further R550

billion, with the debt-to-GDP ratio increasing to

47.6% by the end of the MTEF period. Debt largely

sourced domestically.

• Rating agencies will continue to monitor fiscal

developments closely.

• Some of the tax reform proposals have now

incorporated, such as taxation of small

businesses.

• However, reports on various other issues are yet

to be published by Davis Tax Committee (e.g.

overall tax system, VAT, estate duty, wealth,

mining taxes).

• Several measures in support of government’s

immediate priorities, as captured in 9-point plan

announced by President Zuma in the SONA, are

highlighted in the Budget Review 2015.

Thank you