Embed Size (px)

Citation preview

Company No.

965488-H

NATIONAL BANK OF ABU DHABI MALAYSIA BERHAD

(Incorporated in Malaysia)

BASEL II: PILLAR 3 DISCLOSURE

AS AT 30 JUNE 2015

National Bank of Abu Dhabi Malaysia Berhad

(Company No. 965488-H)

Incorporated in Malaysia

Basel II: Pillar 3 Disclosure as at 30th June 2015

Page | 2

1. OVERVIEW

The Pillar 3 Disclosures attached herewith is governed under the Bank Negara

Malaysia’s (“BNM”) Risk-Weighted Capital Adequacy Framework (“RWCAF”) –

Disclosure Requirements (“Pillar 3”), which is the equivalent of that issued by the Basel

Committee on Banking Supervision entitled “International Convergence of Capital

Measurement and Capital Standards”(commonly referred to as Basel II).

This Pillar 3 Disclosures is to be read in conjunction with the Financial Statements as of

30 June 2015.

2. SCOPE OF APPLICATION

The Pillar 3 Disclosures relates to National Bank of Abu Dhabi Malaysia Berhad (“the

Bank”) only. The Bank does not have any subsidiary or associated company as at 30th

June 2015.

The Bank adopts the Standardised Approach in determining the capital requirements for

credit risk and market risk and applied the Basic Indicator Approach for operational

risk.

3. CAPITAL MANAGEMENT

The Bank’s capital management approach is driven by its desire to maintain appropriate

capital base and maintain adequate buffer in support of its business development and to

meet BNM regulatory capital requirements at all times. As such, implications on the

Bank’s capital position are taken into account by the Board and senior management prior

to implementing major business decisions in order to preserve the Bank’s overall capital

requirements.

Capital Plan

The Bank’s Capital Plan is drawn up annually in conjunction with the financial

budgeting exercise and approved by the Board for implementation at the beginning of

each financial year. The Capital Plan is the establishment of the Internal Capital Target

(“ICT”) of which takes into account, inter alia, the Bank’s strategic objectives and

business plans, regulatory capital requirements, views of key stakeholders such as the

parent company, regulators, development on BNM capital guidelines, available supply

of capital and capital raising options and performance of business sectors.

National Bank of Abu Dhabi Malaysia Berhad

(Company No. 965488-H)

Incorporated in Malaysia

Basel II: Pillar 3 Disclosure as at 30th June 2015

Page | 3

ALCO is responsible for the on-going assessment of the demand and usage of capital.

Capital Contingency Plan

In addition to the Capital Plan, the Bank has also developed a documented Board-

approved Capital Contingency Plan in December 2014. The Plan is intended to ensure

that capital is managed effectively in the event of a capital crisis.

The Capital Contingency Plan (“CCP”) is an extension of the Capital Plan. The CCP

provides a comprehensive approach to the management and restoration of capital in the

unlikely event of a capital crisis by:

Establishing policies and procedures for capital contingency planning;

Establishing governance for capital contingency planning;

Providing early warning signals and establish monitoring and escalation process;

and

Establishing strategies and action plans to ensure that capital is managed promptly.

In order to ensure healthy capital levels at all times, the minimum capital requirements

and capital adequacy ratios are monitored actively by the senior management and

relevant committees on a monthly basis. Appropriate trigger points are established

based on the minimum capital requirements and capital adequacy ratios computed in

accordance with BNM guidelines in order to facilitate reporting, monitoring and

escalation, decision-making and action planning.

Circumstances that could lead to deficiencies in capital position include, amongst others,

economic environment, market conditions and financial conditions. In this regard,

appropriate strategies and action plans have been developed so that, in the unlikely

event of a capital crisis, the Bank will be prepared to deal with the event promptly and

restore capital back to healthy levels.

National Bank of Abu Dhabi Malaysia Berhad

(Company No. 965488-H)

Incorporated in Malaysia

Basel II: Pillar 3 Disclosure as at 30th June 2015

Page | 4

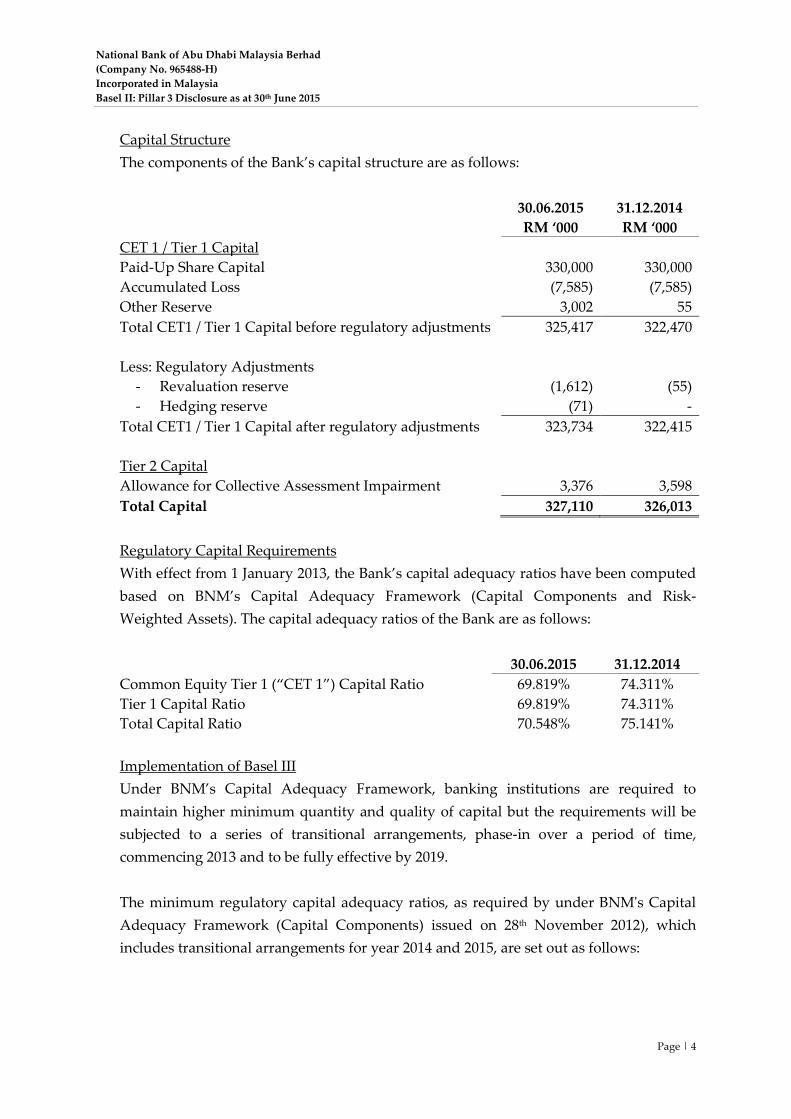

Capital Structure

The components of the Bank’s capital structure are as follows:

30.06.2015

RM ‘000

31.12.2014

RM ‘000

CET 1 / Tier 1 Capital

Paid-Up Share Capital 330,000 330,000

Accumulated Loss (7,585) (7,585)

Other Reserve 3,002 55

Total CET1 / Tier 1 Capital before regulatory adjustments 325,417 322,470

Less: Regulatory Adjustments

- Revaluation reserve (1,612) (55)

- Hedging reserve (71) -

Total CET1 / Tier 1 Capital after regulatory adjustments 323,734 322,415

Tier 2 Capital

Allowance for Collective Assessment Impairment 3,376 3,598

Total Capital 327,110 326,013

Regulatory Capital Requirements

With effect from 1 January 2013, the Bank’s capital adequacy ratios have been computed

based on BNM’s Capital Adequacy Framework (Capital Components and Risk-

Weighted Assets). The capital adequacy ratios of the Bank are as follows:

30.06.2015 31.12.2014

Common Equity Tier 1 (“CET 1”) Capital Ratio 69.819% 74.311%

Tier 1 Capital Ratio 69.819% 74.311%

Total Capital Ratio 70.548% 75.141%

Implementation of Basel III

Under BNM’s Capital Adequacy Framework, banking institutions are required to

maintain higher minimum quantity and quality of capital but the requirements will be

subjected to a series of transitional arrangements, phase-in over a period of time,

commencing 2013 and to be fully effective by 2019.

The minimum regulatory capital adequacy ratios, as required by under BNM's Capital

Adequacy Framework (Capital Components) issued on 28th November 2012), which

includes transitional arrangements for year 2014 and 2015, are set out as follows:

National Bank of Abu Dhabi Malaysia Berhad

(Company No. 965488-H)

Incorporated in Malaysia

Basel II: Pillar 3 Disclosure as at 30th June 2015

Page | 5

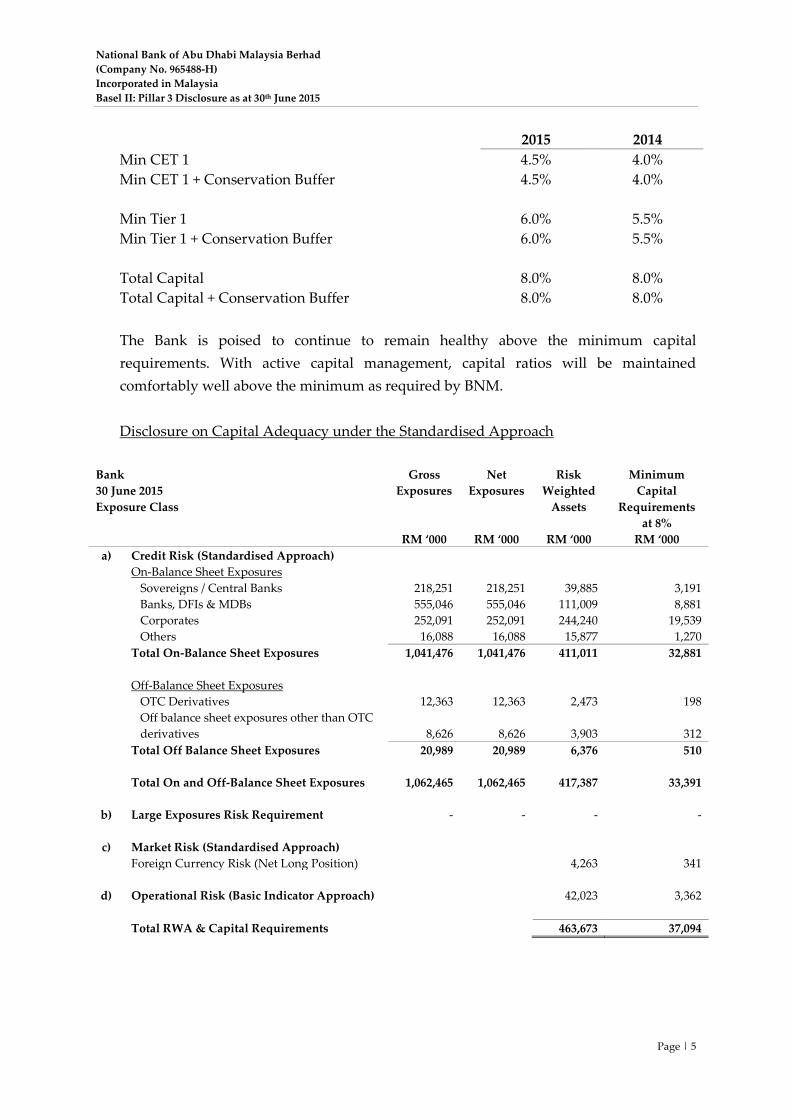

2015 2014

Min CET 1 4.5% 4.0%

Min CET 1 + Conservation Buffer 4.5% 4.0%

Min Tier 1 6.0% 5.5%

Min Tier 1 + Conservation Buffer 6.0% 5.5%

Total Capital 8.0% 8.0%

Total Capital + Conservation Buffer 8.0% 8.0%

The Bank is poised to continue to remain healthy above the minimum capital

requirements. With active capital management, capital ratios will be maintained

comfortably well above the minimum as required by BNM.

Disclosure on Capital Adequacy under the Standardised Approach

Bank

30 June 2015

Exposure Class

Gross

Exposures

Net

Exposures

Risk

Weighted

Assets

Minimum

Capital

Requirements

at 8%

RM ‘000 RM ‘000 RM ‘000 RM ‘000

a) Credit Risk (Standardised Approach)

On-Balance Sheet Exposures

Sovereigns / Central Banks 218,251 218,251 39,885 3,191

Banks, DFIs & MDBs 555,046 555,046 111,009 8,881

Corporates 252,091 252,091 244,240 19,539

Others 16,088 16,088 15,877 1,270

Total On-Balance Sheet Exposures 1,041,476 1,041,476 411,011 32,881

Off-Balance Sheet Exposures

OTC Derivatives 12,363 12,363 2,473 198

Off balance sheet exposures other than OTC

derivatives 8,626 8,626 3,903 312

Total Off Balance Sheet Exposures 20,989 20,989 6,376 510

Total On and Off-Balance Sheet Exposures 1,062,465 1,062,465 417,387 33,391

b) Large Exposures Risk Requirement - - - -

c) Market Risk (Standardised Approach)

Foreign Currency Risk (Net Long Position) 4,263 341

d) Operational Risk (Basic Indicator Approach) 42,023 3,362

Total RWA & Capital Requirements 463,673 37,094

National Bank of Abu Dhabi Malaysia Berhad

(Company No. 965488-H)

Incorporated in Malaysia

Basel II: Pillar 3 Disclosure as at 30th June 2015

Page | 6

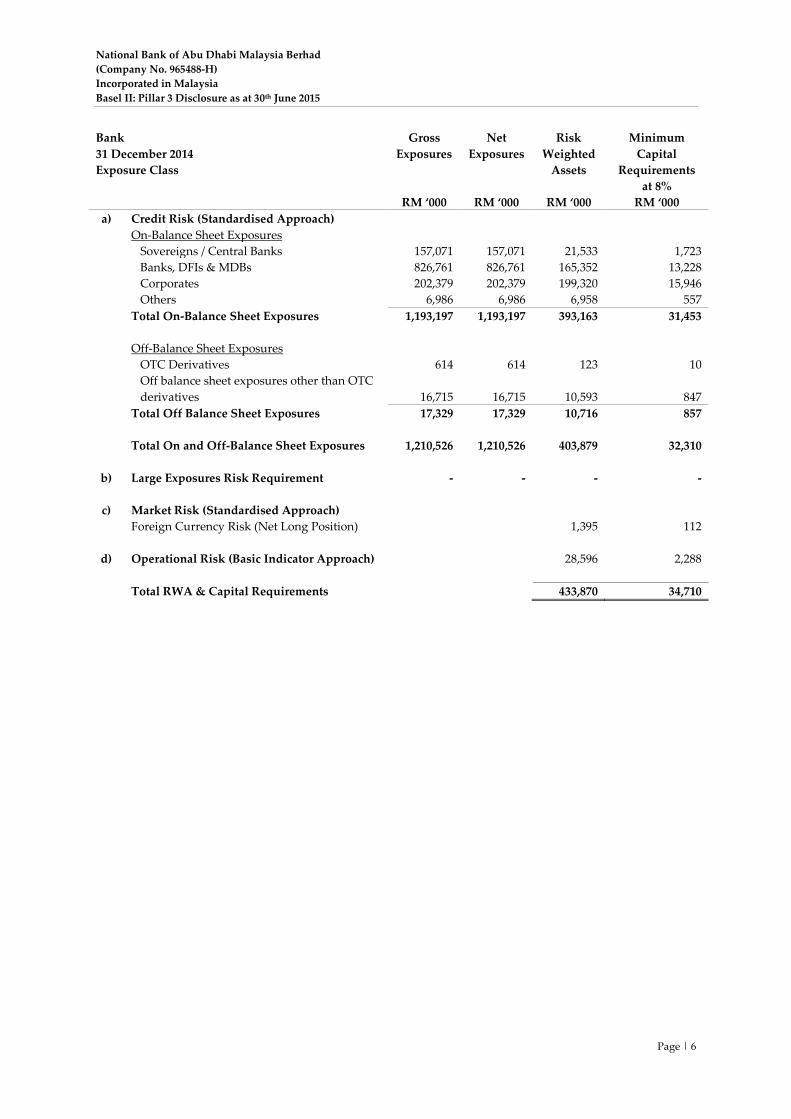

Bank

31 December 2014

Exposure Class

Gross

Exposures

Net

Exposures

Risk

Weighted

Assets

Minimum

Capital

Requirements

at 8%

RM ‘000 RM ‘000 RM ‘000 RM ‘000

a) Credit Risk (Standardised Approach)

On-Balance Sheet Exposures

Sovereigns / Central Banks 157,071 157,071 21,533 1,723

Banks, DFIs & MDBs 826,761 826,761 165,352 13,228

Corporates 202,379 202,379 199,320 15,946

Others 6,986 6,986 6,958 557

Total On-Balance Sheet Exposures 1,193,197 1,193,197 393,163 31,453

Off-Balance Sheet Exposures

OTC Derivatives 614 614 123 10

Off balance sheet exposures other than OTC

derivatives 16,715 16,715 10,593 847

Total Off Balance Sheet Exposures 17,329 17,329 10,716 857

Total On and Off-Balance Sheet Exposures 1,210,526 1,210,526 403,879 32,310

b) Large Exposures Risk Requirement - - - -

c) Market Risk (Standardised Approach)

Foreign Currency Risk (Net Long Position) 1,395 112

d) Operational Risk (Basic Indicator Approach) 28,596 2,288

Total RWA & Capital Requirements 433,870 34,710

National Bank of Abu Dhabi Malaysia Berhad

(Company No. 965488-H)

Incorporated in Malaysia

Basel II: Pillar 3 Disclosure as at 30th June 2015

Page | 7

4. RISK MANAGEMENT

The Bank adopts the parent company, NBAD PJSC (“the Group”) Risk Management

Framework. The Framework is practiced consistently across the Group’s global

operations, to support the Group’s strategic objectives and business plans. Risk

management is integrated in the business process through:

A clear governance structure, with framework of risk ownership, accountability,

standards and policy;

Alignment of risk strategy and business objectives, and integration of risk appetite

and risk-adjusted return on capital (“RAROC”) into business planning and capital

management;

Embedding risk culture as the foundation upon which a enterprise-wide risk

management framework is built on; and

Independent and integrated risk function.

Risk Governance

Ultimate responsibility for the effective management of risk rests with the Board of

Directors. The Board delegates the authority for the management of risk to several

committees, in particular:

Board Risk Management Committee (“BRMC”) is chaired by an independent non-

executive director. It is responsible to oversee the Bank's risk management policies,

systems, practices and procedures to ensure effectiveness of risk identification,

management and compliance with risk-related internal guidelines and regulatory

requirements.

Board Audit Committee (“BAC”) is chaired by an independent non-executive

director. It is responsible to oversee the integrity of the financial statements,

preparation of the consolidated accounts including changes to accounting policies

and practices and adherence to disclosure rules, overseeing relationship with

external auditors, overseeing internal audit, ensuring adequacy of financial controls

and internal control.

At the management level, acting through the delegated authority by the Board, the Bank

has put in place various management committees to ensure oversight of key risk areas.

Risk Management Committee (“RMC”) is responsible for the risk management and

control of all risk, except those for which ALCO have direct responsibilities. The

RMC is also responsible for the establishment of all risk policies and procedures.

Assets and Liability Management Committee (“ALCO”) is responsible for the

management of capital, and compliance with, risk policies and limits relating to the

managing of the balance sheet, capital adequacy, liquidity risk and market risk.

National Bank of Abu Dhabi Malaysia Berhad

(Company No. 965488-H)

Incorporated in Malaysia

Basel II: Pillar 3 Disclosure as at 30th June 2015

Page | 8

The Bank’s Risk Governance Approach has been structured to comply with BNM

Guideline on Risk Governance issued on 1st March 2013 and aligned with those

established at the Group.

Risk Management Approach

The Bank adopts the Group’s three lines of defence risk management approach.

The first line of defence is that all employees are required to ensure the effective

management of risks within the scope of their direct organizational responsibilities.

The second line of defence comprises the Risk Control Owners, supported by their

respective control functions. Risk Control Owners are responsible for ensuring that

the risks within the scope of their responsibilities remain within appetite. The second

line is independent of the origination, trading and sales functions, is to ensure that

the necessary balance and perspective is brought to risk/return decisions.

The third line of defence comprises the independent assurance provided by the

internal audit (“IA”) function which has no responsibilities for any of the activities it

examines. IA provides independent assurance of the effectiveness of the

management’s control of its own business activities (first line) and of the processes

maintained by the Risk Control Functions (the second line). As a result, IA provides

assurance that the overall system of control effectiveness is working as required

within the Risk Management Framework.

Risk Appetite

The Bank has in place a documented Board-approved Risk Appetite Statement. The Risk

Appetite Statement is the Bank’s articulation of the amount of risk that the Bank is

willing to take in the pursuit of its strategic and/or business objectives. The Risk Appetite

Statement is defined in terms of Risk Appetite Parameters, which are circumscribed by

self-imposed constraints and tolerance levels around them. These constraints are limits

and triggers to avoid adverse outcomes which would be out of line with internal and

external expectations, and may lead to unexpected losses of a scale that would be

detrimental to the stability of the relevant business units or of the Bank as a whole.

The Bank’s Risk Appetite Statement is aligned with those established at the Group.

National Bank of Abu Dhabi Malaysia Berhad

(Company No. 965488-H)

Incorporated in Malaysia

Basel II: Pillar 3 Disclosure as at 30th June 2015

Page | 9

5. CREDIT RISK

Credit risk is the risk that a customer or counterparty to a financial asset fails to meet its

contractual obligations and causes the Bank to incur a financial loss. It arises principally

from the Bank’s loans and advances, due from banks and financial institutions including

reverse repo, off balance sheet contingent liabilities and non-trading debt investments

and certain other assets.

Management of Credit Risk

The Credit Risk Management Framework includes policies and procedures to monitor

and manage these risks. The Bank adopts the Group’s approach of credit risk

management. This includes:

Establishment of authorization structure and limits for the approval and renewal of

credit facilities;

Reviewing and assessing credit exposures in accordance with authorization structure

and limits, prior to facilities being committed to customers. Review and renewal of

facilities are subject to the same process;

Diversification of lending and investment activities;

Limiting concentrations of exposure to industry sectors, geographic locations and

counterparties; and

Reviewing compliance, on an ongoing basis, with agreed exposure limits relating to

counterparties, industries and countries and reviewing limits in accordance with risk

management strategy and market trends.

The Bank adopts the Group’s uses of an internal risk rating system to assess the credit

quality of borrowers and counterparties. Each counterparty is assigned a rating,

including classified accounts that are either Watch List or Non-Performing. The internal

risk rating system plays a significant role in efficient use of credit risk measurement and

management including:

Risk based pricing and determination of RAROC;

Risk based monitoring (frequency and intensity of monitoring);

Determining risk based delegation of powers at various sanction authority levels;

and

Internal estimation of capital.

National Bank of Abu Dhabi Malaysia Berhad

(Company No. 965488-H)

Incorporated in Malaysia

Basel II: Pillar 3 Disclosure as at 30th June 2015

Page | 10

Credit Risk Monitoring

The Bank adopts the Group’s approach of credit risk monitoring:

a) Monitoring of risk quality (Obligor level): Periodic review of credit is based on the

internal rating grades. More frequent reviews are made for the weaker credits and

less frequent reviews for the superior credits.

b) Monitoring of risk quality (Portfolio Level): Existing portfolios are monitored based

on the economic sectors, industry, geography, ratings and business lines. These

portfolio reports are prepared monthly and the senior management is informed on

the same.

c) Monitoring of past dues on principal and interest: Past dues accounts (if any) are

reported monthly to the senior management. Measures to realize such past dues are

initiated with stringent follow up thereafter.

d) Monitoring of excess over limits: The monitoring reports are submitted to the senior

management and processes are initiated to realize and regularize such excesses.

e) Monitoring of potential loss accounts (Watch List): This category comprises accounts

where either contractual principal or interest are past due or when the accounts show

weakness in the borrower’s financial position and creditworthiness, and requires

more than normal attention. Such weakness is specifically monitored to ensure that

the quality of the asset does not further deteriorate.

f) Collateral management: The Bank has in place system of controls, reviews and

approvals to ensure effective collateral management. This includes minimum loan to

value requirement for each facility, specific collateral requirement for lending

specific portfolio, margin calls for treasury products and ensuring legal

enforceability of contracts including perfection of security interests.

Concentration Risk

Credit concentration risk refers to the level of exposure to any individual or related

group of customers, specific industry or sector, country or geographical locations. The

first level of protection against concentration risk is through country and industry

thresholds limits.

a) Single Name Concentration

Single name concentration is monitored on an individual basis with the top

exposures being reported on a weekly basis. The Bank abides by BNM Single

Counterparty Exposure Limit (“SCEL”). The SCEL represents a non-risk adjusted

back-stop measure to ensure that exposures to a single counterparty and persons

connected to it shall not exceed 25 percent of the Bank’s Total Capital.

National Bank of Abu Dhabi Malaysia Berhad

(Company No. 965488-H)

Incorporated in Malaysia

Basel II: Pillar 3 Disclosure as at 30th June 2015

Page | 11

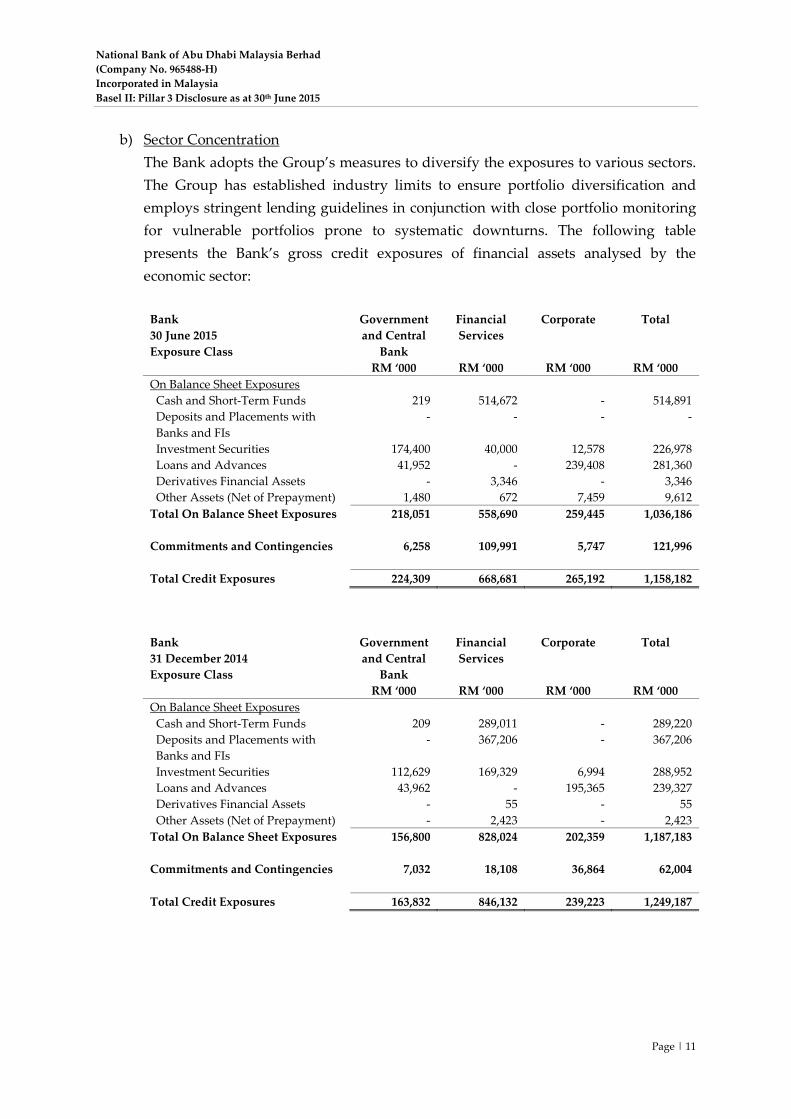

b) Sector Concentration

The Bank adopts the Group’s measures to diversify the exposures to various sectors.

The Group has established industry limits to ensure portfolio diversification and

employs stringent lending guidelines in conjunction with close portfolio monitoring

for vulnerable portfolios prone to systematic downturns. The following table

presents the Bank’s gross credit exposures of financial assets analysed by the

economic sector:

Bank

30 June 2015

Exposure Class

Government

and Central

Bank

Financial

Services

Corporate Total

RM ‘000 RM ‘000 RM ‘000 RM ‘000

On Balance Sheet Exposures

Cash and Short-Term Funds 219 514,672 - 514,891

Deposits and Placements with

Banks and FIs

- - - -

Investment Securities 174,400 40,000 12,578 226,978

Loans and Advances 41,952 - 239,408 281,360

Derivatives Financial Assets - 3,346 - 3,346

Other Assets (Net of Prepayment) 1,480 672 7,459 9,612

Total On Balance Sheet Exposures 218,051 558,690 259,445 1,036,186

Commitments and Contingencies 6,258 109,991 5,747 121,996

Total Credit Exposures 224,309 668,681 265,192 1,158,182

Bank

31 December 2014

Exposure Class

Government

and Central

Bank

Financial

Services

Corporate Total

RM ‘000 RM ‘000 RM ‘000 RM ‘000

On Balance Sheet Exposures

Cash and Short-Term Funds 209 289,011 - 289,220

Deposits and Placements with

Banks and FIs

- 367,206 - 367,206

Investment Securities 112,629 169,329 6,994 288,952

Loans and Advances 43,962 - 195,365 239,327

Derivatives Financial Assets - 55 - 55

Other Assets (Net of Prepayment) - 2,423 - 2,423

Total On Balance Sheet Exposures 156,800 828,024 202,359 1,187,183

Commitments and Contingencies 7,032 18,108 36,864 62,004

Total Credit Exposures 163,832 846,132 239,223 1,249,187

National Bank of Abu Dhabi Malaysia Berhad

(Company No. 965488-H)

Incorporated in Malaysia

Basel II: Pillar 3 Disclosure as at 30th June 2015

Page | 12

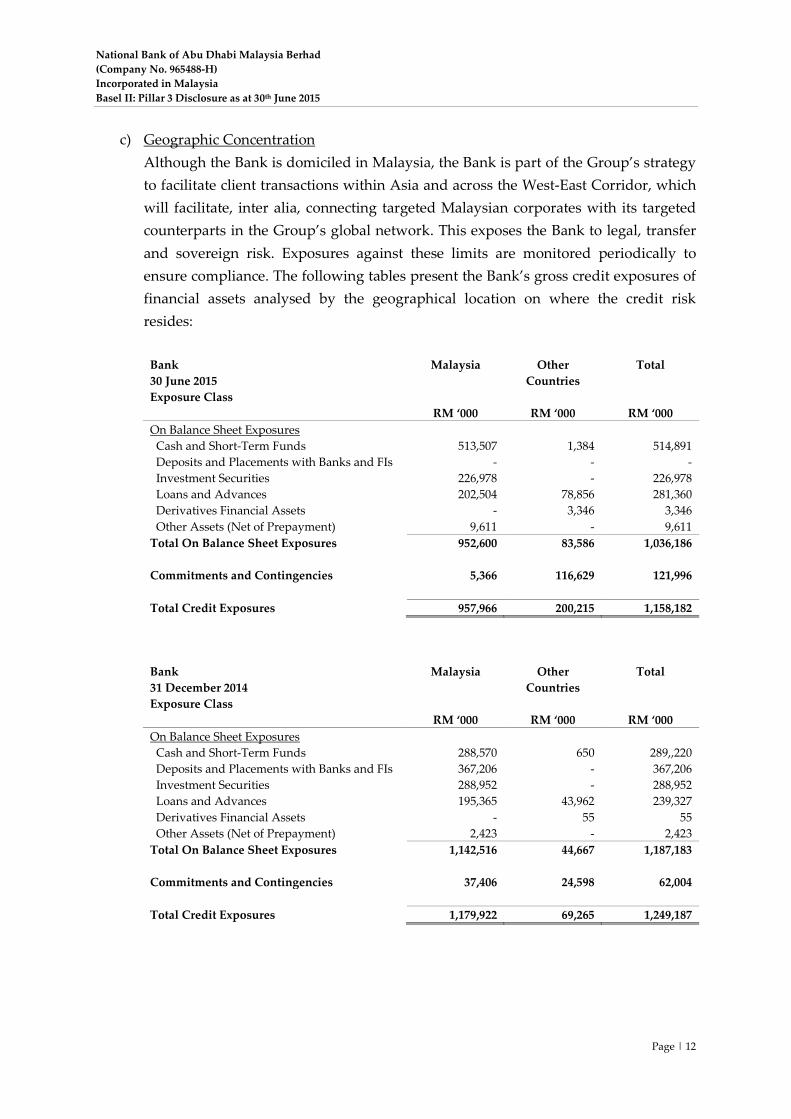

c) Geographic Concentration

Although the Bank is domiciled in Malaysia, the Bank is part of the Group’s strategy

to facilitate client transactions within Asia and across the West-East Corridor, which

will facilitate, inter alia, connecting targeted Malaysian corporates with its targeted

counterparts in the Group’s global network. This exposes the Bank to legal, transfer

and sovereign risk. Exposures against these limits are monitored periodically to

ensure compliance. The following tables present the Bank’s gross credit exposures of

financial assets analysed by the geographical location on where the credit risk

resides:

Bank

30 June 2015

Exposure Class

Malaysia Other

Countries

Total

RM ‘000 RM ‘000 RM ‘000

On Balance Sheet Exposures

Cash and Short-Term Funds 513,507 1,384 514,891

Deposits and Placements with Banks and FIs - - -

Investment Securities 226,978 - 226,978

Loans and Advances 202,504 78,856 281,360

Derivatives Financial Assets - 3,346 3,346

Other Assets (Net of Prepayment) 9,611 - 9,611

Total On Balance Sheet Exposures 952,600 83,586 1,036,186

Commitments and Contingencies 5,366 116,629 121,996

Total Credit Exposures 957,966 200,215 1,158,182

Bank

31 December 2014

Exposure Class

Malaysia Other

Countries

Total

RM ‘000 RM ‘000 RM ‘000

On Balance Sheet Exposures

Cash and Short-Term Funds 288,570 650 289,,220

Deposits and Placements with Banks and FIs 367,206 - 367,206

Investment Securities 288,952 - 288,952

Loans and Advances 195,365 43,962 239,327

Derivatives Financial Assets - 55 55

Other Assets (Net of Prepayment) 2,423 - 2,423

Total On Balance Sheet Exposures 1,142,516 44,667 1,187,183

Commitments and Contingencies 37,406 24,598 62,004

Total Credit Exposures 1,179,922 69,265 1,249,187

National Bank of Abu Dhabi Malaysia Berhad

(Company No. 965488-H)

Incorporated in Malaysia

Basel II: Pillar 3 Disclosure as at 30th June 2015

Page | 13

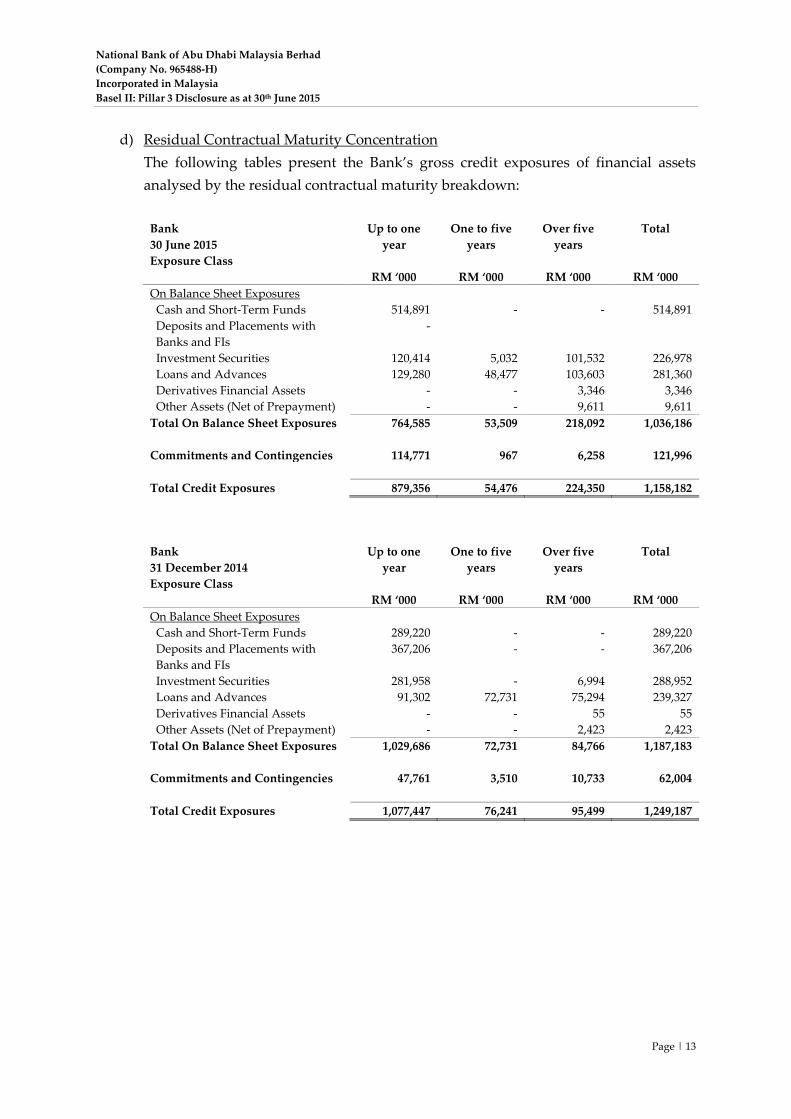

d) Residual Contractual Maturity Concentration

The following tables present the Bank’s gross credit exposures of financial assets

analysed by the residual contractual maturity breakdown:

Bank

30 June 2015

Exposure Class

Up to one

year

One to five

years

Over five

years

Total

RM ‘000 RM ‘000 RM ‘000 RM ‘000

On Balance Sheet Exposures

Cash and Short-Term Funds 514,891 - - 514,891

Deposits and Placements with

Banks and FIs

-

Investment Securities 120,414 5,032 101,532 226,978

Loans and Advances 129,280 48,477 103,603 281,360

Derivatives Financial Assets - - 3,346 3,346

Other Assets (Net of Prepayment) - - 9,611 9,611

Total On Balance Sheet Exposures 764,585 53,509 218,092 1,036,186

Commitments and Contingencies 114,771 967 6,258 121,996

Total Credit Exposures 879,356 54,476 224,350 1,158,182

Bank

31 December 2014

Exposure Class

Up to one

year

One to five

years

Over five

years

Total

RM ‘000 RM ‘000 RM ‘000 RM ‘000

On Balance Sheet Exposures

Cash and Short-Term Funds 289,220 - - 289,220

Deposits and Placements with

Banks and FIs

367,206 - - 367,206

Investment Securities 281,958 - 6,994 288,952

Loans and Advances 91,302 72,731 75,294 239,327

Derivatives Financial Assets - - 55 55

Other Assets (Net of Prepayment) - - 2,423 2,423

Total On Balance Sheet Exposures 1,029,686 72,731 84,766 1,187,183

Commitments and Contingencies 47,761 3,510 10,733 62,004

Total Credit Exposures 1,077,447 76,241 95,499 1,249,187

National Bank of Abu Dhabi Malaysia Berhad

(Company No. 965488-H)

Incorporated in Malaysia

Basel II: Pillar 3 Disclosure as at 30th June 2015

Page | 14

Credit Risk Policy

Credit risk policies are an integral part of the Bank’s risk management framework.

Policies govern all activities related to credit appraisal and underwriting. Business

segments specific policies and procedures are established to manage the risks that are

unique to their operations.

The Bank has in place Board-approved Local Credit Policy Manual (“LCPM”). The

LCPM governs the credit risk activities and has been aligned with the Group’s CPM. The

LCPM is supported by the following Board-approved key policies.

a) Single Counterparty Exposure Policy;

b) Credit Transactions and Exposures with Connected Parties Policy;

c) Risk Appetite Statement; and

d) Business Underwriting Standards for Corporates and Financial Institutions.

All of the above policies are subjected to annual review.

Disclosure for Portfolios under the Basel II Standardised Approach

For BNM regulatory reporting purposes, the Bank refers to the credit ratings assigned by

credit rating agencies in its calculation of credit risk weighted assets. The External Credit

Assessment Institutions ("ECAI") ratings accorded to the following counterparty

exposure classes are used in the calculation of risk weighted assets for capital adequacy

purposes:

Sovereigns and Central Bank;

Banks, Multi-Lateral Development Banks (“MDB”) and Development Financial

Institutions (“DFI”): and

Corporates.

Assessments provided by approved ECAI are mapped to credit quality steps as

prescribed by BNM. Where a counterparty or exposure is rated by more than one ECAI,

the second highest rating is used to determine the risk weight.

The following is a summary of the rules governing the assignment of risk weights under

the Standardised Approach. Each exposure must be assigned to one of the five credit

quality rating categories defined in the tables below.

National Bank of Abu Dhabi Malaysia Berhad

(Company No. 965488-H)

Incorporated in Malaysia

Basel II: Pillar 3 Disclosure as at 30th June 2015

Page | 15

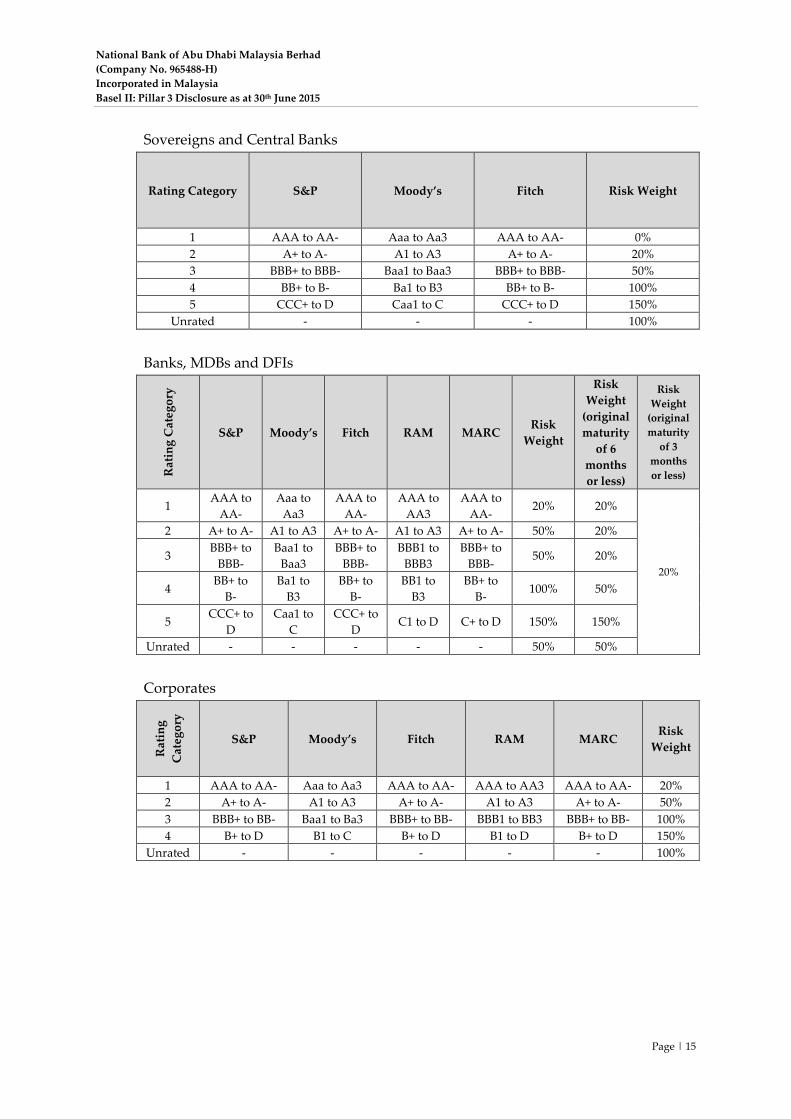

Sovereigns and Central Banks

Rating Category S&P Moody’s Fitch Risk Weight

1 AAA to AA- Aaa to Aa3 AAA to AA- 0%

2 A+ to A- A1 to A3 A+ to A- 20%

3 BBB+ to BBB- Baa1 to Baa3 BBB+ to BBB- 50%

4 BB+ to B- Ba1 to B3 BB+ to B- 100%

5 CCC+ to D Caa1 to C CCC+ to D 150%

Unrated - - - 100%

Banks, MDBs and DFIs

Rat

ing

Cat

ego

ry

S&P Moody’s Fitch RAM MARC Risk

Weight

Risk

Weight

(original

maturity

of 6

months

or less)

Risk

Weight

(original

maturity

of 3

months

or less)

1 AAA to

AA-

Aaa to

Aa3

AAA to

AA-

AAA to

AA3

AAA to

AA- 20% 20%

20%

2 A+ to A- A1 to A3 A+ to A- A1 to A3 A+ to A- 50% 20%

3 BBB+ to

BBB-

Baa1 to

Baa3

BBB+ to

BBB-

BBB1 to

BBB3

BBB+ to

BBB- 50% 20%

4 BB+ to

B-

Ba1 to

B3

BB+ to

B-

BB1 to

B3

BB+ to

B- 100% 50%

5 CCC+ to

D

Caa1 to

C

CCC+ to

D C1 to D C+ to D 150% 150%

Unrated - - - - - 50% 50%

Corporates

Rat

ing

Cat

ego

ry

S&P Moody’s Fitch RAM MARC Risk

Weight

1 AAA to AA- Aaa to Aa3 AAA to AA- AAA to AA3 AAA to AA- 20%

2 A+ to A- A1 to A3 A+ to A- A1 to A3 A+ to A- 50%

3 BBB+ to BB- Baa1 to Ba3 BBB+ to BB- BBB1 to BB3 BBB+ to BB- 100%

4 B+ to D B1 to C B+ to D B1 to D B+ to D 150%

Unrated - - - - - 100%

National Bank of Abu Dhabi Malaysia Berhad

(Company No. 965488-H)

Incorporated in Malaysia

Basel II: Pillar 3 Disclosure as at 30th June 2015

Page | 16

The following tables present the on- and off balance sheet credit exposures:

Bank

Exposure

Class

RM ‘000

Rating of Sovereigns and Central Banks by Approved ECAI

S&P AAA to

AA- A+ to A-

BBB+ to

BBB- BB+ to B-

CCC+ to

D Unrated

Moody’s Aaa to

Aa3 A1 to A3

Baa1 to

Baa3 Ba1 to B3 Caa1 to C Unrated

Fitch AAA to

AA- A+ to A-

BBB+ to

BBB- BB+ to B-

CCC+ to

D Unrated

30 Jun 2015 - 94,544 45,081 - - -

31 Dec 2014 - 40,010 54,934 - - -

Bank

Exposure

Class

RM ‘000

Rating of Banks, DFIs and MDBs by Approved ECAI

S&P AAA to

AA- A+ to A-

BBB+ to

BBB- BB+ to B-

CCC+ to

D Unrated

Moody’s Aaa to

Aa3 A1 to A3

Baa1 to

Baa3 Ba1 to B3 Caa1 to C Unrated

Fitch AAA to

AA- A+ to A-

BBB+ to

BBB- BB+ to B-

CCC+ to

D Unrated

RAM AAA to

AA3 A1 to A3

BBB1 to

BBB3 BB1 to B3 C1 to D Unrated

MARC AAA to

AA- A+ to A-

BBB+ to

BBB- BB+ to B- C+ to D Unrated

30 Jun 2015 477,823 93,351 - - - -

31 Dec 2014 13,681 599,734 176,332 3,250 - 80,813

Bank

Exposure

Class

RM ‘000

Rating of Corporates by Approved ECAI

S&P AAA to AA- A+ to A- BBB+ to BB- B+ to D Unrated

Moody’s Aaa to Aa3 A1 to A3 Baa1 to Ba3 B1 to C Unrated

Fitch AAA to AA- A+ to A- BBB+ to BB- B+ to D Unrated

RAM AAA to AA3 A1 to A3 BBB1 to BB3 B1 to D Unrated

MARC AAA to AA- A+ to A- BBB+ to BB- B+ to D Unrated

30 Jun 2015 5,031 7,651 - - 240,848

31 Dec 2014 - 6,422 - - 188,736

National Bank of Abu Dhabi Malaysia Berhad

(Company No. 965488-H)

Incorporated in Malaysia

Basel II: Pillar 3 Disclosure as at 30th June 2015

Page | 17

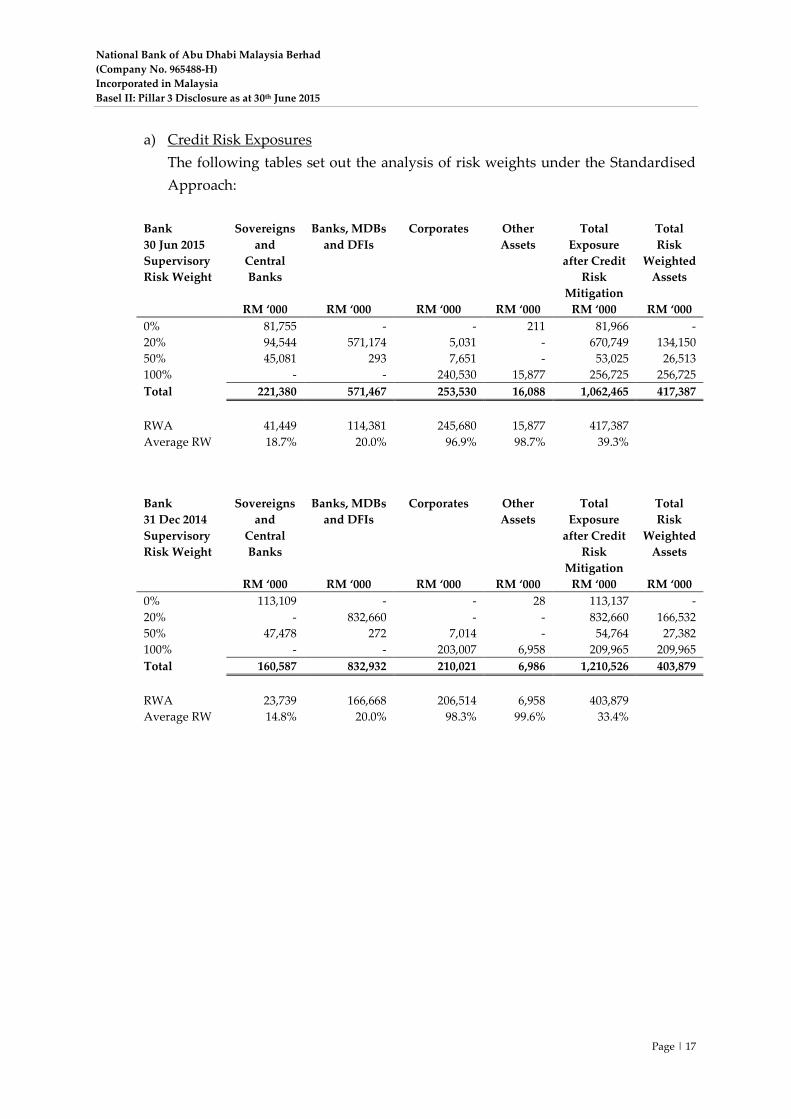

a) Credit Risk Exposures

The following tables set out the analysis of risk weights under the Standardised

Approach:

Bank

30 Jun 2015

Supervisory

Risk Weight

Sovereigns

and

Central

Banks

Banks, MDBs

and DFIs

Corporates Other

Assets

Total

Exposure

after Credit

Risk

Mitigation

Total

Risk

Weighted

Assets

RM ‘000 RM ‘000 RM ‘000 RM ‘000 RM ‘000 RM ‘000

0% 81,755 - - 211 81,966 -

20% 94,544 571,174 5,031 - 670,749 134,150

50% 45,081 293 7,651 - 53,025 26,513

100% - - 240,530 15,877 256,725 256,725

Total 221,380 571,467 253,530 16,088 1,062,465 417,387

RWA 41,449 114,381 245,680 15,877 417,387

Average RW 18.7% 20.0% 96.9% 98.7% 39.3%

Bank

31 Dec 2014

Supervisory

Risk Weight

Sovereigns

and

Central

Banks

Banks, MDBs

and DFIs

Corporates Other

Assets

Total

Exposure

after Credit

Risk

Mitigation

Total

Risk

Weighted

Assets

RM ‘000 RM ‘000 RM ‘000 RM ‘000 RM ‘000 RM ‘000

0% 113,109 - - 28 113,137 -

20% - 832,660 - - 832,660 166,532

50% 47,478 272 7,014 - 54,764 27,382

100% - - 203,007 6,958 209,965 209,965

Total 160,587 832,932 210,021 6,986 1,210,526 403,879

RWA 23,739 166,668 206,514 6,958 403,879

Average RW 14.8% 20.0% 98.3% 99.6% 33.4%

National Bank of Abu Dhabi Malaysia Berhad

(Company No. 965488-H)

Incorporated in Malaysia

Basel II: Pillar 3 Disclosure as at 30th June 2015

Page | 18

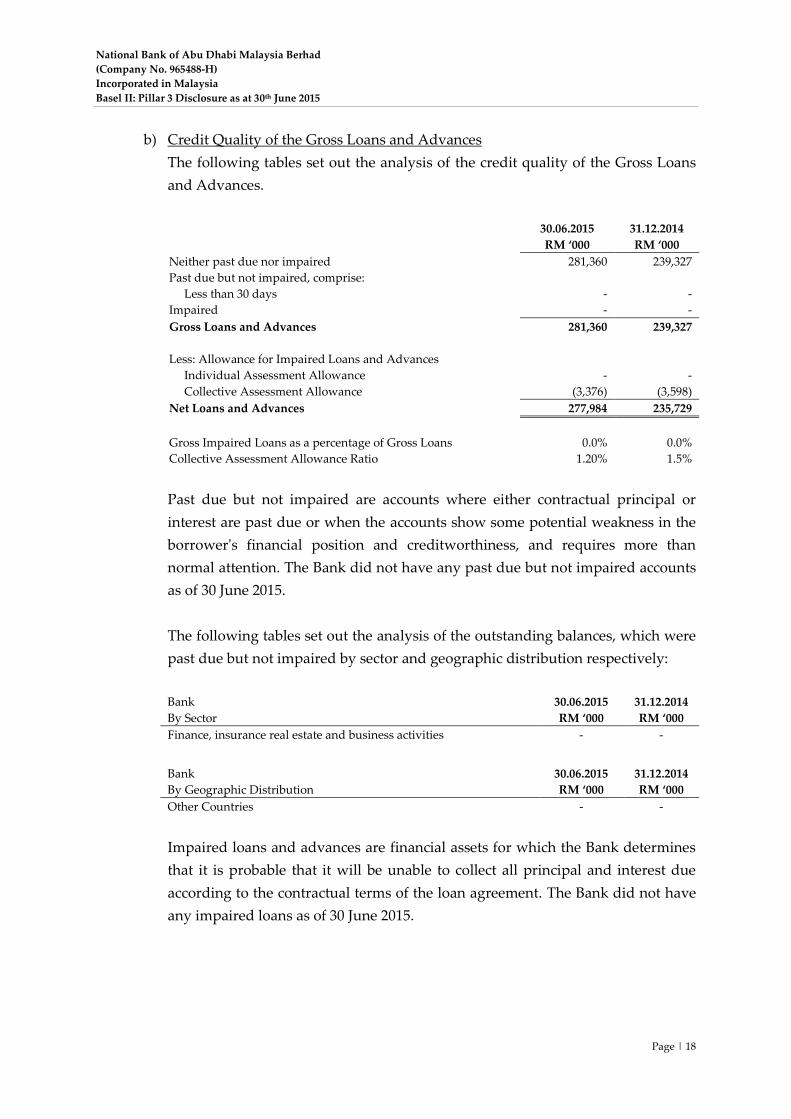

b) Credit Quality of the Gross Loans and Advances

The following tables set out the analysis of the credit quality of the Gross Loans

and Advances.

30.06.2015

RM ‘000

31.12.2014

RM ‘000

Neither past due nor impaired 281,360 239,327

Past due but not impaired, comprise:

Less than 30 days - -

Impaired - -

Gross Loans and Advances 281,360 239,327

Less: Allowance for Impaired Loans and Advances

Individual Assessment Allowance - -

Collective Assessment Allowance (3,376) (3,598)

Net Loans and Advances 277,984 235,729

Gross Impaired Loans as a percentage of Gross Loans 0.0% 0.0%

Collective Assessment Allowance Ratio 1.20% 1.5%

Past due but not impaired are accounts where either contractual principal or

interest are past due or when the accounts show some potential weakness in the

borrower's financial position and creditworthiness, and requires more than

normal attention. The Bank did not have any past due but not impaired accounts

as of 30 June 2015.

The following tables set out the analysis of the outstanding balances, which were

past due but not impaired by sector and geographic distribution respectively:

Bank

By Sector

30.06.2015

RM ‘000

31.12.2014

RM ‘000

Finance, insurance real estate and business activities - -

Bank

By Geographic Distribution

30.06.2015

RM ‘000

31.12.2014

RM ‘000

Other Countries - -

Impaired loans and advances are financial assets for which the Bank determines

that it is probable that it will be unable to collect all principal and interest due

according to the contractual terms of the loan agreement. The Bank did not have

any impaired loans as of 30 June 2015.

National Bank of Abu Dhabi Malaysia Berhad

(Company No. 965488-H)

Incorporated in Malaysia

Basel II: Pillar 3 Disclosure as at 30th June 2015

Page | 19

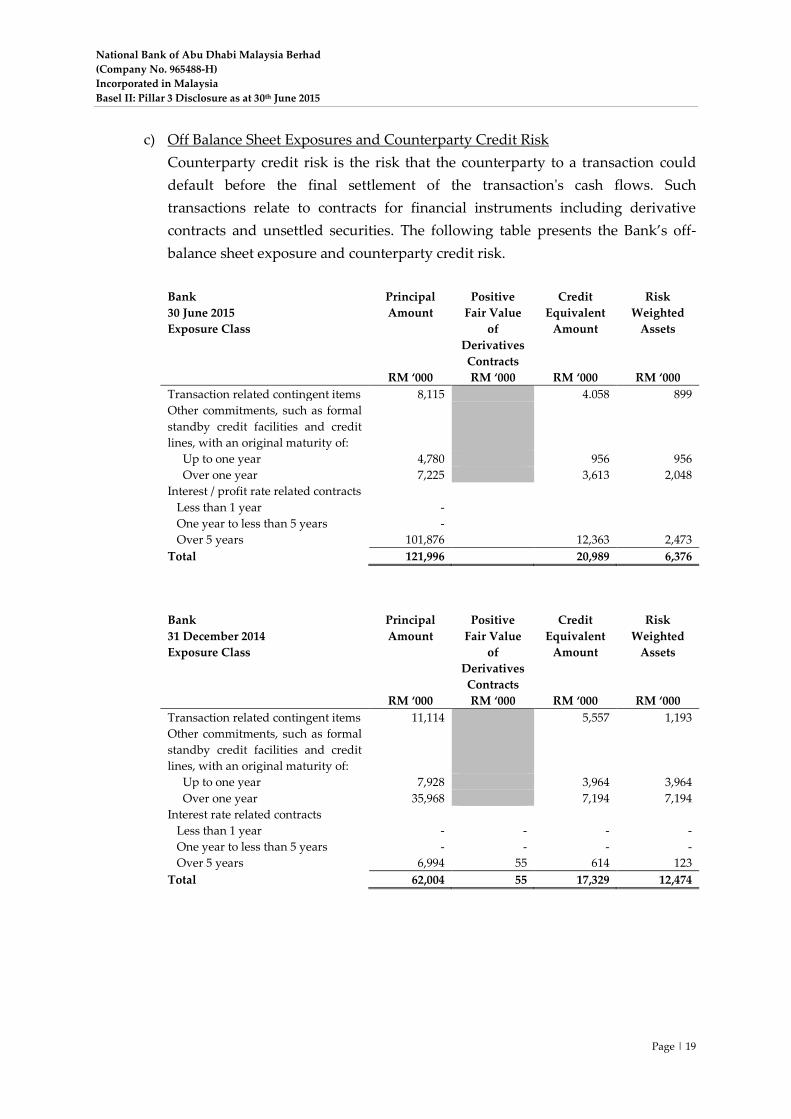

c) Off Balance Sheet Exposures and Counterparty Credit Risk

Counterparty credit risk is the risk that the counterparty to a transaction could

default before the final settlement of the transaction's cash flows. Such

transactions relate to contracts for financial instruments including derivative

contracts and unsettled securities. The following table presents the Bank’s off-

balance sheet exposure and counterparty credit risk.

Bank

30 June 2015

Exposure Class

Principal

Amount

Positive

Fair Value

of

Derivatives

Contracts

Credit

Equivalent

Amount

Risk

Weighted

Assets

RM ‘000 RM ‘000 RM ‘000 RM ‘000

Transaction related contingent items 8,115 4.058 899

Other commitments, such as formal

standby credit facilities and credit

lines, with an original maturity of:

Up to one year 4,780 956 956

Over one year 7,225 3,613 2,048

Interest / profit rate related contracts

Less than 1 year -

One year to less than 5 years -

Over 5 years 101,876 12,363 2,473

Total 121,996 20,989 6,376

Bank

31 December 2014

Exposure Class

Principal

Amount

Positive

Fair Value

of

Derivatives

Contracts

Credit

Equivalent

Amount

Risk

Weighted

Assets

RM ‘000 RM ‘000 RM ‘000 RM ‘000

Transaction related contingent items 11,114 5,557 1,193

Other commitments, such as formal

standby credit facilities and credit

lines, with an original maturity of:

Up to one year 7,928 3,964 3,964

Over one year 35,968 7,194 7,194

Interest rate related contracts

Less than 1 year - - - -

One year to less than 5 years - - - -

Over 5 years 6,994 55 614 123

Total 62,004 55 17,329 12,474

National Bank of Abu Dhabi Malaysia Berhad

(Company No. 965488-H)

Incorporated in Malaysia

Basel II: Pillar 3 Disclosure as at 30th June 2015

Page | 20

6. MARKET RISK

Market risk is the risk that the Bank’s income and / or value of its financial instruments

will fluctuate adversely because of changes in market factors such as interest rates

foreign exchange rates, and equity, commodity and option prices.

The Bank segregates all its positions, which can be either in Trading Book or Banking

Book.

Trading Book

Trading Book refers to financial instruments held either with trading intent or to hedge

other elements of the Trading Book. Positions held with trading intent are those held

intentionally for short-term resale and/or with the intent of benefiting from actual or

expected short-term price movements or to lock in arbitrage profits. These positions may

include for example, proprietary positions, positions arising from client servicing and

market making. The Bank does not have any Trading Book positions due to proprietary

trading and market making activities.

All Trading Book positions arising from client servicing are fully hedged and are

subjected to net open position limits. The Bank’s Trading Book positions consist entirely

of foreign exchange instruments. The financial impact of 1 percent movement for each

foreign currency exposure would result in a post-tax profit/loss of RM 8,068 (31

December 2014: RM 10,463) to the Bank.

The Bank does not have any interest rate risk exposure in the Trading Book.

Banking Book

The Banking Book exposure is defined as all other exposures that are not defined as

Trading Book positions. This will include both on and off-balance sheet positions.

Financial instruments held under the Banking Book are considered as investment

positions.

The Bank mitigates interest rate risk exposure in the Banking Book by hedging the long

term fixed rate assets. This is being done via interest rate swap with the parent company

and the hedge effectiveness is being monitored to ensure it is fall between the ranges of

80 to 125 percent as stipulated in Board-approved Trading Book Policy Statement.

National Bank of Abu Dhabi Malaysia Berhad

(Company No. 965488-H)

Incorporated in Malaysia

Basel II: Pillar 3 Disclosure as at 30th June 2015

Page | 21

The Bank also monitors and reports its interest rate risk exposure on regular basis using

the Economic Value Equity (“EVE”), which is being supported by a comprehensive

limits structure e.g. EVE Limit, Earning-at Risk Limit, Investment Securities Position,

Investment Securities Tenor Limit, Investment Securities PV01 Limit, etc., as articulated

in the Board-approved Asset and Liability Management Policy.

The impact to the Bank’s interest rate sensitive assets and liabilities in Banking Book to a

25 basis points movement in benchmark interest rates shall be RM 0.04 million (31

December 2014: RM 0.09 million). The treatment and assumptions applied are based on

the contractual repricing maturity and remaining maturity of the products, whichever is

earlier. Items with indefinite repricing maturity are treated based on the earliest possible

repricing date or pre-defined by regulator.

7. LIQUIDITY RISK

Liquidity risk is the risk that the Bank, though solvent, either does not have sufficient

financial resources available to meet its obligations as they fall due, or can secure them

only at excessive costs.

The Bank has in place a documented Board-approved Asset and Liability Management

Policy in October 2014. In the Policy, it is the Bank’s intention that the following are met:

To maintain adequate liquidity at all times and for all currencies;

To meet all obligations, to repay depositors and to fulfil commitments to provide

loans and advances, in the normal course of business;

To avoid having to liquidate assets or to raise funds at unfavourable terms;

The liquidity risk position are reviewed periodically and managed within approved

liquidity risk parameters; and

The liquidity risk limits and Management Action Triggers to be monitored and

reported periodically.

The Bank manages and mitigates the risk of its liquidity risk through a set of liquidity

risk limits, including regulatory Liquidity Framework and Liquidity Coverage Ratio as

per BNM requirements. Other liquidity risk measurement methods and risk mitigation

tools that are place are the traditional loan-to-deposit ratio and structural liquidity gap

limits.

National Bank of Abu Dhabi Malaysia Berhad

(Company No. 965488-H)

Incorporated in Malaysia

Basel II: Pillar 3 Disclosure as at 30th June 2015

Page | 22

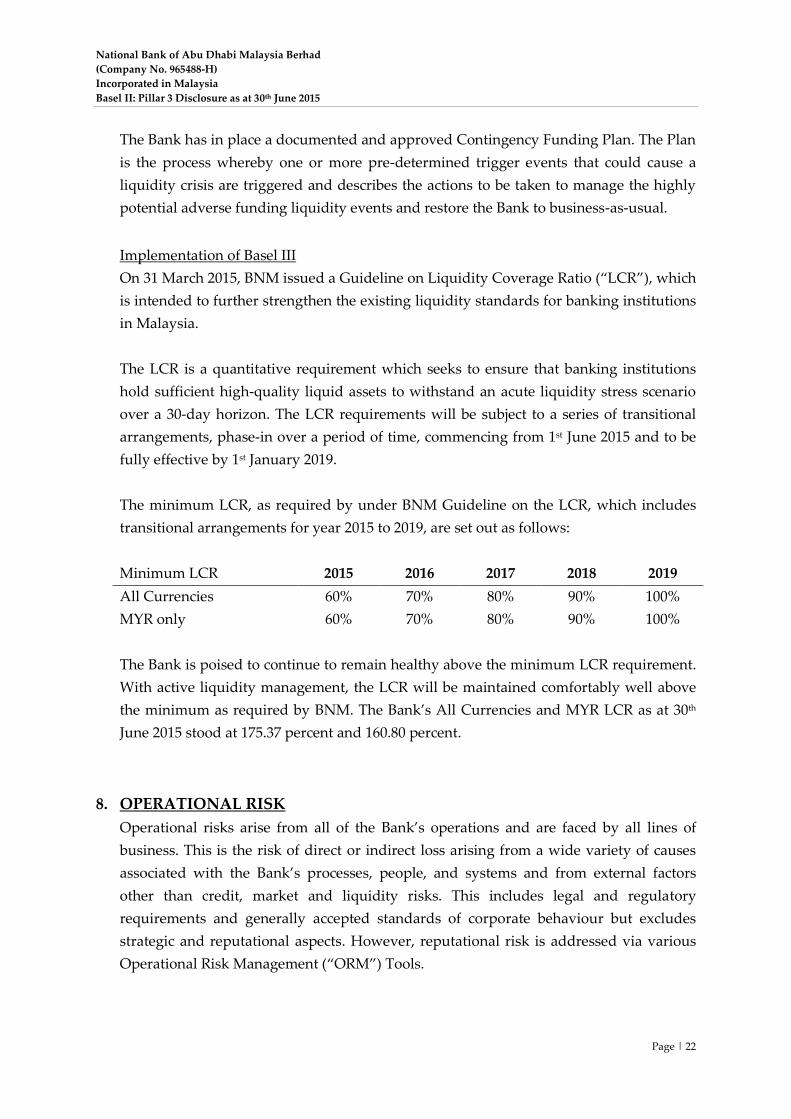

The Bank has in place a documented and approved Contingency Funding Plan. The Plan

is the process whereby one or more pre-determined trigger events that could cause a

liquidity crisis are triggered and describes the actions to be taken to manage the highly

potential adverse funding liquidity events and restore the Bank to business-as-usual.

Implementation of Basel III

On 31 March 2015, BNM issued a Guideline on Liquidity Coverage Ratio (“LCR”), which

is intended to further strengthen the existing liquidity standards for banking institutions

in Malaysia.

The LCR is a quantitative requirement which seeks to ensure that banking institutions

hold sufficient high-quality liquid assets to withstand an acute liquidity stress scenario

over a 30-day horizon. The LCR requirements will be subject to a series of transitional

arrangements, phase-in over a period of time, commencing from 1st June 2015 and to be

fully effective by 1st January 2019.

The minimum LCR, as required by under BNM Guideline on the LCR, which includes

transitional arrangements for year 2015 to 2019, are set out as follows:

Minimum LCR 2015 2016 2017 2018 2019

All Currencies 60% 70% 80% 90% 100%

MYR only 60% 70% 80% 90% 100%

The Bank is poised to continue to remain healthy above the minimum LCR requirement.

With active liquidity management, the LCR will be maintained comfortably well above

the minimum as required by BNM. The Bank’s All Currencies and MYR LCR as at 30th

June 2015 stood at 175.37 percent and 160.80 percent.

8. OPERATIONAL RISK

Operational risks arise from all of the Bank’s operations and are faced by all lines of

business. This is the risk of direct or indirect loss arising from a wide variety of causes

associated with the Bank’s processes, people, and systems and from external factors

other than credit, market and liquidity risks. This includes legal and regulatory

requirements and generally accepted standards of corporate behaviour but excludes

strategic and reputational aspects. However, reputational risk is addressed via various

Operational Risk Management (“ORM”) Tools.

National Bank of Abu Dhabi Malaysia Berhad

(Company No. 965488-H)

Incorporated in Malaysia

Basel II: Pillar 3 Disclosure as at 30th June 2015

Page | 23

The Bank’s objective is to manage operational risk so as to balance the avoidance of

financial losses resulting from operational risk events and any damage to the Bank’s

reputation. The Bank is continually improving its operating environment that will

ensure the businesses to operate in an environment to be creative and be enabled.

The Bank adopts the Group’s Operational Risk Framework. This Framework is used to

identify, assess, monitor, control, manage and report risks. This includes a unique and

effective process of assessing associated risks and approving residual risks of new and /

or significant change initiatives within the Bank and an Internal Loss Data Collection

Process. The Internal Loss Data Collected is reconciled with the General Ledger.

The Framework also sets out the interrelation with other risk categories that includes but

is not limited to regulatory requirements, Anti Money Laundering and Counter Terrorist

Financing. These functions come directly under the oversight and supervision by the

Bank’s Compliance function.

To further strengthen the Bank’s outsourcing arrangements with third parties, the Bank

has in place Board-approved Outsourcing Policy. The Policy is intended to be line with

BNM guideline on the same nature and is targeted to meet the following main objectives:

To outline the criteria of outsourcing operational functions and process flow

involved in outsourcing;

To provide a guiding principle that needs to be taken into consideration to identify

issues associated with each outsourcing arrangement;

To address some factors that needs to be considered upon renewal of outsourcing

service contract; and

To ensure that the implementation of outsourcing is in line with BNM and Group

requirements.

The Bank adopts the Group’s Information Security Policies and requirements are

intended to conform to internationally accepted IT Governance standards. More

specifically, IT security is governed by explicit security related policies based on

international standards such as ISO27001.

The Bank’s Internal Audit function conducts continuous audits and reviews of the

Bank’s critical functions and compliance to the regulatory requirements. Audit reports

are circulated once every quarter. In addition, the Group Internal Audit conducts

periodic audits and reviews so as to provide assurance to the Management on the

compliance with corporate policies and guidelines.

National Bank of Abu Dhabi Malaysia Berhad

(Company No. 965488-H)

Incorporated in Malaysia

Basel II: Pillar 3 Disclosure as at 30th June 2015

Page | 24

9. BUSINESS CONTINUITY MANAGEMENT

Business Continuity Management (“BCM”) is a management process that identifies

potential impacts that threaten an organisation and provides a framework for building

resilience and the capability for an effective response which safeguards its reputation

along with the interests of its key stake holders and customers. BCM is responsible for

assuring operational resilience to the Group’s key business processes under adverse

circumstances.

The Bank adopts the Group’s BCM Framework, which:

Identify key processes (and their dependencies) essential to ensure the delivery of

the Bank’s services;

Identify and define time frames for the recovery of those key processes;

Establish cost effective strategies and solutions to achieve the recovery time frames of

the key processes; and

Validate the selected solutions.

The Bank conducts periodic business impact analysis to identify their critical business

processes and recovery time objectives. Business continuity plans are developed and

tested annually. The Bank maintains a local IT and business operations contingency site

to ensure uninterrupted banking operations.

National Bank of Abu Dhabi Malaysia Berhad

(Company No. 965488-H)

Incorporated in Malaysia

Basel II: Pillar 3 Disclosure as at 30th June 2015

Page | 25

CHIEF EXECUTIVE OFFICER'S ATTESTATION

I, Susan Yuen Su Min, being the Chief Executive Officer of National Bank of Abu Dhabi

Malaysia Berhad, hereby state that, the Pillar 3 Disclosures are to my knowledge and

opinion is correct and have been prepared in accordance to requirements stipulated in Bank

Negara Malaysia Capital Adequacy Framework - Disclosure Requirements (Pillar 3)

guidelines.

~signed~

………………………………………

SUSAN YUEN SU MIN

CHIEF EXECUTIVE OFFICER 20th August 2015