Embed Size (px)

Citation preview

No. ISSN: 2180-0448

MITI Weekly Bulletin | www.miti.gov.my

“DR

IVIN

G T

ransformation, P

OW

ERIN

G G

rowth”

MITI Weekly Bulletin | www.miti.gov.my

National Automotive Policy (NAP) 2014

1. National Automotive Policy (NAP) 2014 announced today will transform Malaysia’s automotive industry to be one of the important components for our economy. The automotive industry contributed RM30 billion to the national GDP in 2013 and employs about 550,000 employees.

2. NAP 2014 outlines key directions and strategies in preparing the local automotive players towards the liberalization of the industry. Extensive studies and consultations were carried out with relevant government agencies, industry players, and consumers in formulating this policy.

3. NAP 2014:

a. focuses on structural issues affecting the domestic automotive industry and outlines measures to meet global quality, cost and delivery requirements. b. is aligned to United Nation safety regulations of vehicles. c. looks at issues affecting consumers and puts forth mechanisms to address these issues. 4. The objectives of the NAP 2014 are to:

a. promote a competitive and sustainable domestic automotive industry including the national automotive companies; b. make Malaysia the regional automotive hub in energy efficient vehicles (EEV); c. promote increase in value-added activities in a sustainable manner; d. promote increase in exports of vehicles and automotive components; e. promote participation of Bumiputera companies in the total value chain of the domestic automotive industry; and f. safeguard consumers’ interest by offering safer and better quality products at competitive prices.

5. There are 6 roadmaps and action plans developed to complement the implementation of the NAP 2014. These roadmaps also serve as guidelines for the transformation of the local automotive industry. They are:

(i) Malaysia Automotive Technology Roadmap (MATR); (ii) Malaysia Automotive Supply Chain Development Roadmap;

(iii) Malaysia Automotive Human Capital Development Roadmap; (iv) Malaysia Automotive Remanufacturing Roadmap; (v) Development of Automotive Authorized Treatment Facilities (ATF) Framework; and (vi) Malaysia Automotive Bumiputera Development Roadmap.

6. One of the key objectives of the NAP 2014 is to increase exports of vehicles and automotive component levels. The NAP targets for at least 200,000 units of cars to be exported while exports of components will reach a minimum value of RM10 billion in 2020.

ENERGY- EFFICIENT VEHICLE (EEV) 7. Central to this policy is the vision of Malaysia to become an energy efficient vehicle (EEV) hub. This encompasses strategies and measures to strengthen the entire value chain of the automotive industry and will also lead to environment conservation, high-income job creation, transfer of technology and create new economic opportunities for local companies.

8. The global definition of EEV is vehicles that meet a set of specifications in terms of carbon emission level (CO2/km) and fuel consumption (L/km). EEV includes fuel-efficient vehicles, hybrid, Electric Vehicle and alternatively fuelled vehicles e.g. CNG, LPG, Biodiesel, Ethanol, Hydrogen and Fuel Cell. Based on this vision, about 85% of vehicles produced in Malaysia in 2020 will be EEVs.

VENDOR DEVELOPMENT

9. Vendor development is very important in creating a competitive automotive industry. The NAP 2014 targets to develop world-class vendors. Domestic vendors will be transformed to become global and regional level component manufacturers.

EMPLOYMENT OPPORTUNITY

10. Employment is one of the main contributions of the NAP 2014. About 550,000 people are directly employed in the automotive industry. With this policy, it is expected that 150,000 more employment opportunities will be created by 2020; while local skilled and semi-skilled workers will replace 80% of foreign workers in the automotive manufacturing sector by 2020.

CAR PRICE REDUCTION

11. During the GE13, BN promised a gradual reduction of prices ranging 20% to 30% over the next 5 years. A Car Price Reduction framework has been developed to fulfill the promise of gradual price reduction. The framework consists of measures to be taken by the Government and industry.

12. The NAP 2014 will see a bigger base of new models being introduced in the domestic market. These models will not only be greener but also safer.

13. The Government is constantly reviewing its fiscal position and is open to possibility to reduce excise duties when the fiscal situation permits.

“DR

IVIN

G T

ransformation, P

OW

ERIN

G G

rowth”

MITI Weekly Bulletin / www.miti.gov.my

14. Models such as Saga SV, Persona SV, Viva, Alza and MyVi S Series, the new Honda Jazz and Nissan Almera were introduced at reduced prices of between 3 and 17%. These models accounted for 30% of market share in 2013.

15. In 2014, more new models and variants will be introduced at competitive prices.

VOLUNTARY VEHICLE INSPECTION (VVI)

16. VVI (Pemeriksaan Kenderaan Secara Sukarela) policy is meant to enhance the awareness of Malaysians on the need to ensure roadworthiness of their cars. The voluntary vehicle inspection is not limited to just one agency or company.

BUMIPUTERA AGENDA

17. The policy will focus on human capital development, supply chain components, spare parts and technology development. There are two measures - First, funding from year 2014 to 2019 to increase the competitiveness of Bumiputera companies in all sector.

18. Secondly, continuous supervision of car manufacturers and companies operating in after-sales services to ensure effective participation of Bumiputera companies in domestic automotive industry.

19. The Government, under NAP 2014 will continue its support of the national car industry. The support includes market expansion activities, improving quality and productivity, cost-reduction and development of supply chain based on their transformation plan.

20. Overall, the NAP 2014 provides a total financial package of about RM2 billion, as well as measures and implementation plans to realize the NAP 2014.

•Please refer to the full policy document (Dasar Automotif Nasional 2014).

Ministry of International Trade and Industry Kuala Lumpur 20 January 2014

“DR

IVIN

G T

ransformation, P

OW

ERIN

G G

rowth”

MITI Weekly Bulletin / www.miti.gov.my

MALAYSIA

Indicators January - November 2013

IPI*

126.62.9% growth

Employment (As at end ofNovember)

1,031,393 persons

1.0% growth

Salaries & WagesRM30.1 b

8.7% growth

SalesRM568.9b

-0.3% growth

Jan-Sep 2013 GDP

(Manufacturing Sector) RM142.3b

3.0% growth

ExportsRM441.3b

2.0% growth

Imports

RM446.1b5.0% growth

Source : Department of Statistics, Malaysia

50.3

46.3

51.7

49.7 50.6

51.7

54.3 53.4 53.5 54.1

53.2

42

44

46

48

50

52

54

56

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov

Note: IPI*= Industrial Production Index

SalesJanuary - November 2013

RM billion

Manufacturing Sector Performance

“DR

IVIN

G T

ransformation, P

OW

ERIN

G G

rowth”

MITI Weekly Bulletin / www.miti.gov.my

Source : Department of Statistics, Malaysia

1,04

0

1,03

2

1,04

2

1,04

0

1,04

2

1,03

8

1,03

5

1,03

2

1,03

1

1,03

1

1,03

1

2.7

2.6

2.8

2.72.7

2.7 2.72.7

2.8 2.8 2.8

2.3

2.4

2.5

2.6

2.7

2.8

2.9

1,015

1,020

1,025

1,030

1,035

1,040

1,045

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov

January - November 2013

Manufacturing Sector

Employment and Salaries & Wages

“DR

IVIN

G T

ransformation, P

OW

ERIN

G G

rowth”

Salaries & Wages(RMbil.)

Employment (‘000 persons) Salaries & Wages Employment

MITI Weekly Bulletin / www.miti.gov.my

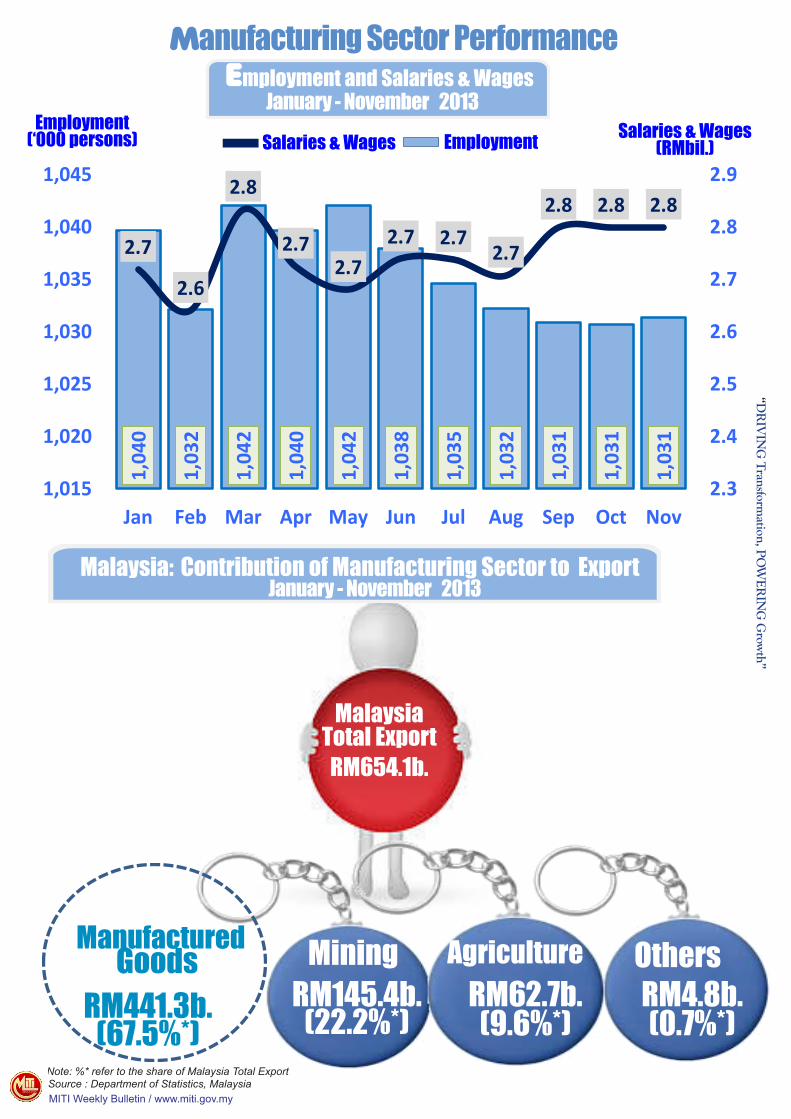

Malaysia: Contribution of Manufacturing Sector to ExportJanuary - November 2013

Manufactured

MalaysiaTotal ExportRM654.1b.

MiningRM145.4b.

(22.2%*)

AgricultureRM62.7b.(9.6%*)

OthersRM4.8b.(0.7%*)

Goods RM441.3b.

(67.5%*)

Manufacturing Sector Performance

Note: %* refer to the share of Malaysia Total Export

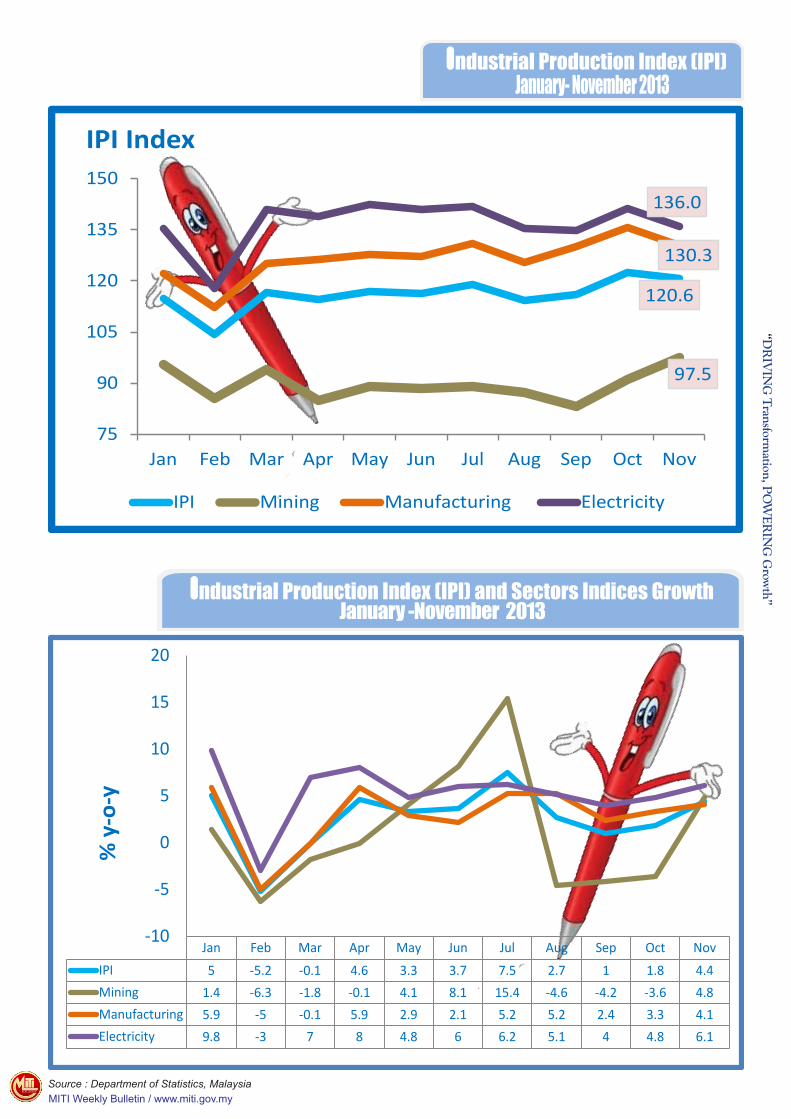

120.6

97.5

130.3

136.0

75

90

105

120

135

150

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov

IPI Index

IPI Mining Manufacturing Electricity

Jan Feb Mar Apr May Jun Jul Aug Sep Oct NovIPI 5 -5.2 -0.1 4.6 3.3 3.7 7.5 2.7 1 1.8 4.4Mining 1.4 -6.3 -1.8 -0.1 4.1 8.1 15.4 -4.6 -4.2 -3.6 4.8Manufacturing 5.9 -5 -0.1 5.9 2.9 2.1 5.2 5.2 2.4 3.3 4.1Electricity 9.8 -3 7 8 4.8 6 6.2 5.1 4 4.8 6.1

-10

-5

0

5

10

15

20

% y

-o-y

“DR

IVIN

G T

ransformation, P

OW

ERIN

G G

rowth”

Source : Department of Statistics, Malaysia

Industrial Production Index (IPI)January- November 2013

Industrial Production Index (IPI) and Sectors Indices GrowthJanuary -November 2013

MITI Weekly Bulletin / www.miti.gov.my

MITI Weekly Bulletin | www.miti.gov.my

“DR

IVIN

G T

ransformation, P

OW

ERIN

G G

rowth”

0

10

20

30

40

50

60

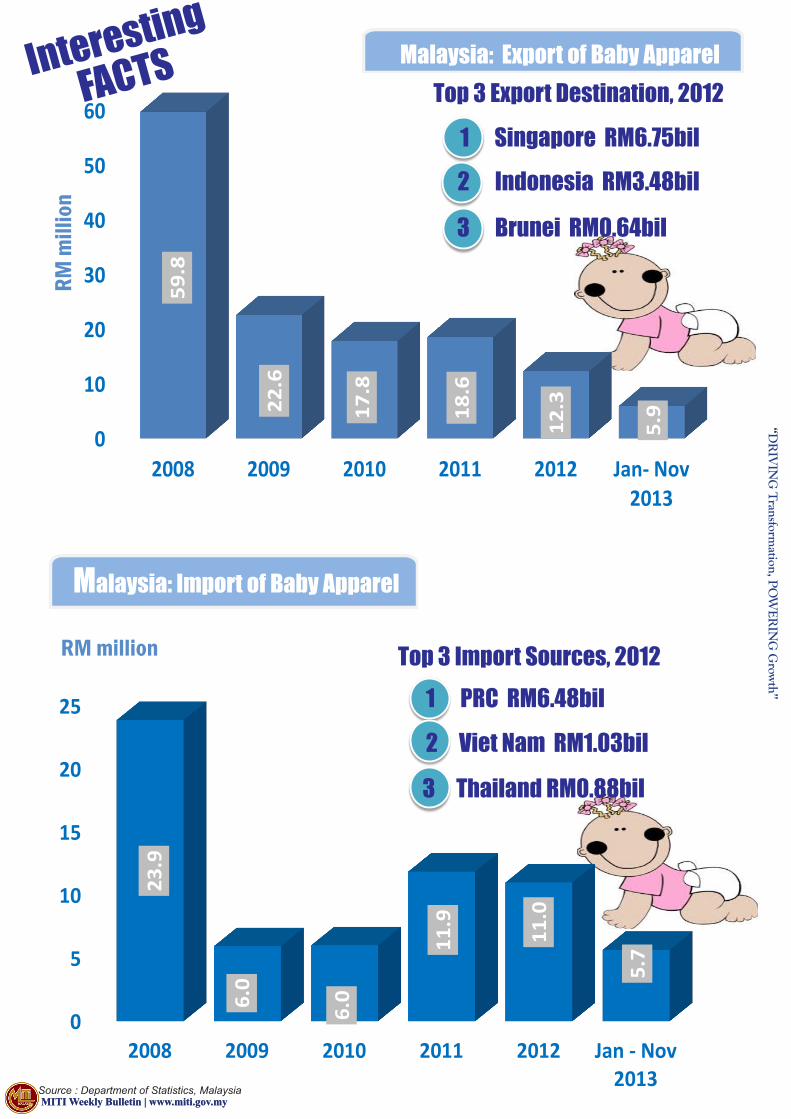

2008 2009 2010 2011 2012 Jan- Nov2013

59.8

22.6

17.8

18.6

12.3

5.9

0

5

10

15

20

25

2008 2009 2010 2011 2012 Jan - Nov2013

23.9

6.0

6.0

11.9

11.0

5.7

MITI Weekly Bulletin | www.miti.gov.my

RM m

illio

n

RM million

Malaysia: Export of Baby Apparel

Industrial Production Index (IPI) and Sectors Indices Growth

Malaysia: Import of Baby Apparel

Source : Department of Statistics, Malaysia

InterestingFACTS

Top 3 Export Destination, 20121 Singapore RM6.75bil2 Indonesia RM3.48bil

3 Brunei RM0.64bil

Top 3 Import Sources, 20121 PRC RM6.48bil2 Viet Nam RM1.03bil

3 Thailand RM0.88bil

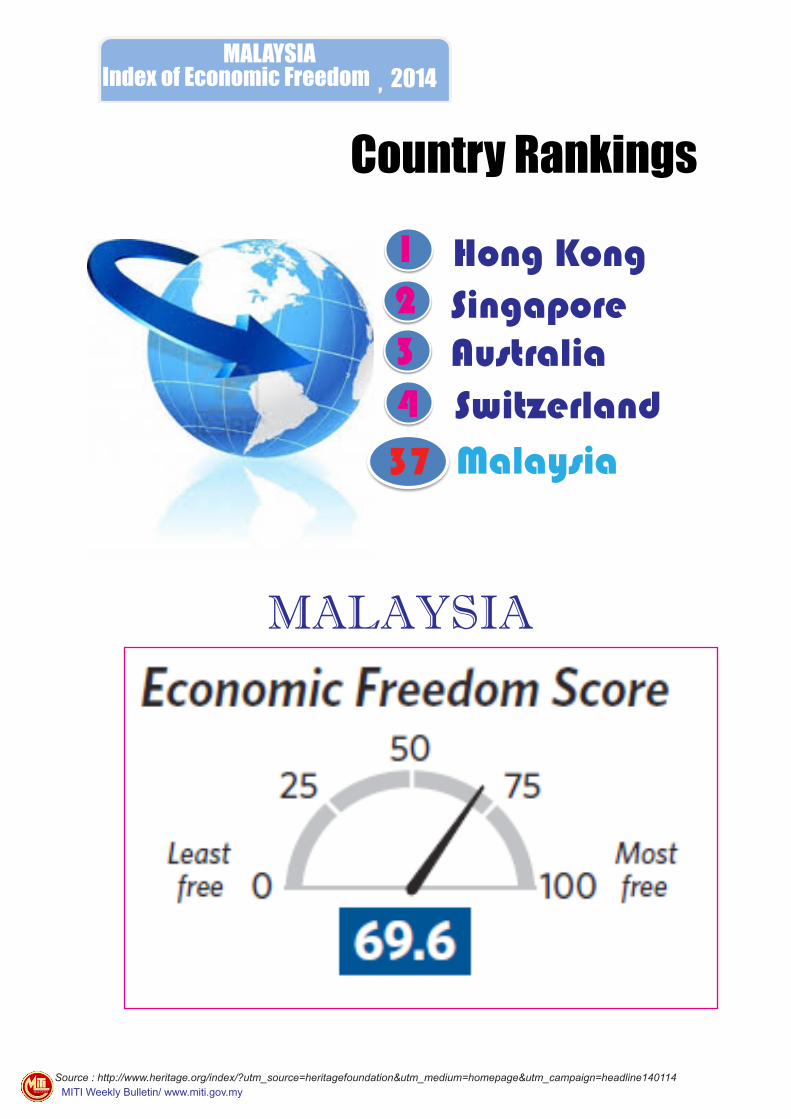

MALAYSIA Index of Economic Freedom , 2014

2014

MALAYSIA

MITI Weekly Bulletin/ www.miti.gov.mySource : http://www.heritage.org/index/?utm_source=heritagefoundation&utm_medium=homepage&utm_campaign=headline140114

1

COUNTRY RANKINGS

1 Hong Kong 2 Singapore3 Australia4 Switzerland. .37 Malaysia38 Uruguay39 Jordan

Hong KongSingaporeAustraliaSwitzerland

234

37 Malaysia

1

Country Rankings

MITI Weekly Bulletin/ www.miti.gov.my

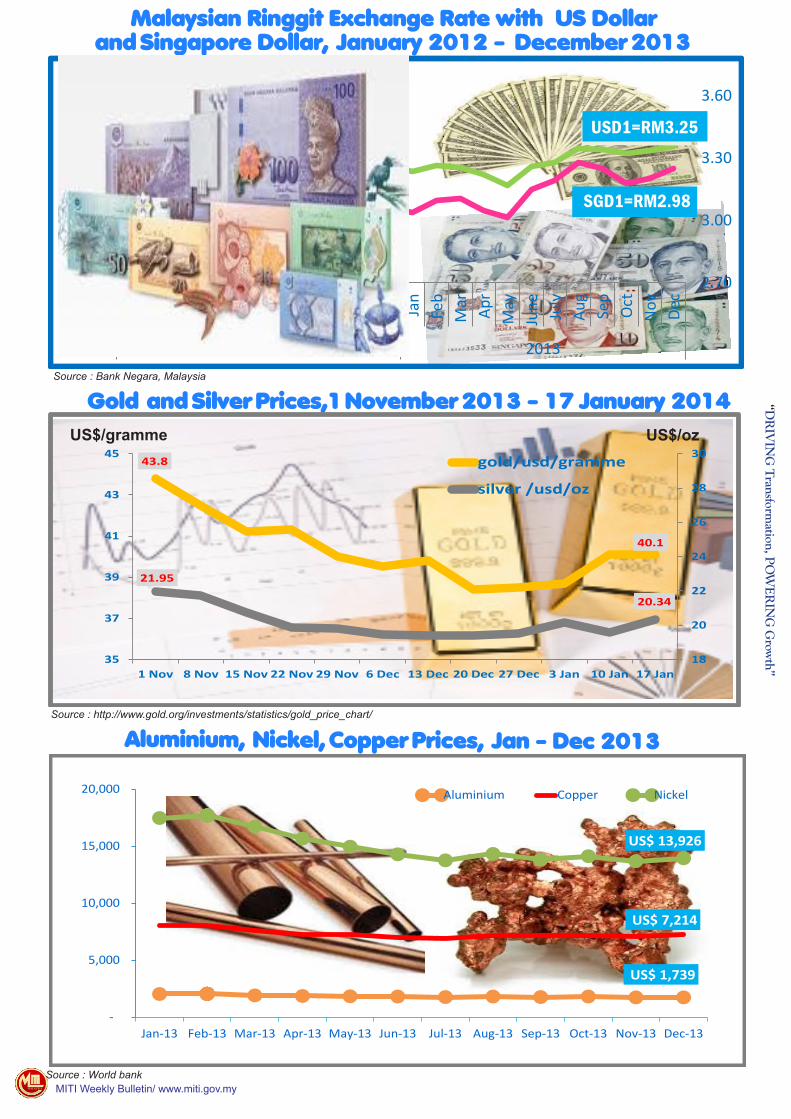

USD1=RM2.58

SGD1=RM3.25

2.70

3.00

3.30

3.60

2.00

2.20

2.40

2.60

2.80

Jan

Feb

Mar Ap

rM

ayJu

ne July

Aug

Sep

Oct

Nov De

cJa

nFe

bM

ar Apr

May

June July

Aug

Sep

Oct

Nov De

c

2012 2013Source : Bank Negara, Malaysia

Gold and Silver Prices, 1 November 2013 - 17 January 2014

Malaysian Ringgit Exchange Rate with US Dollarand Singapore Dollar, January 2012 - December 2013

43.8

40.1

21.95

20.34

18

20

22

24

26

28

30

35

37

39

41

43

45

1 Nov 8 Nov 15 Nov 22 Nov 29 Nov 6 Dec 13 Dec 20 Dec 27 Dec 3 Jan 10 Jan 17 Jan

gold/usd/gramme

silver /usd/oz

Source : http://www.gold.org/investments/statistics/gold_price_chart/

US$/ozUS$/gramme

Aluminium, Nickel, Copper Prices, Jan - Dec 2013

Source : World bank

US$ 1,739

US$ 7,214

US$ 13,926

-

5,000

10,000

15,000

20,000

Jan-13 Feb-13 Mar-13 Apr-13 May-13 Jun-13 Jul-13 Aug-13 Sep-13 Oct-13 Nov-13 Dec-13

Aluminium Copper Nickel

“DR

IVIN

G T

ransformation, P

OW

ERIN

G G

rowth”

USD1=RM3.25

SGD1=RM2.98

MITI Weekly Bulletin | www.miti.gov.my

“DR

IVIN

G T

ransformation, P

OW

ERIN

G G

rowth”

MITI Weekly Bulletin | www.miti.gov.my

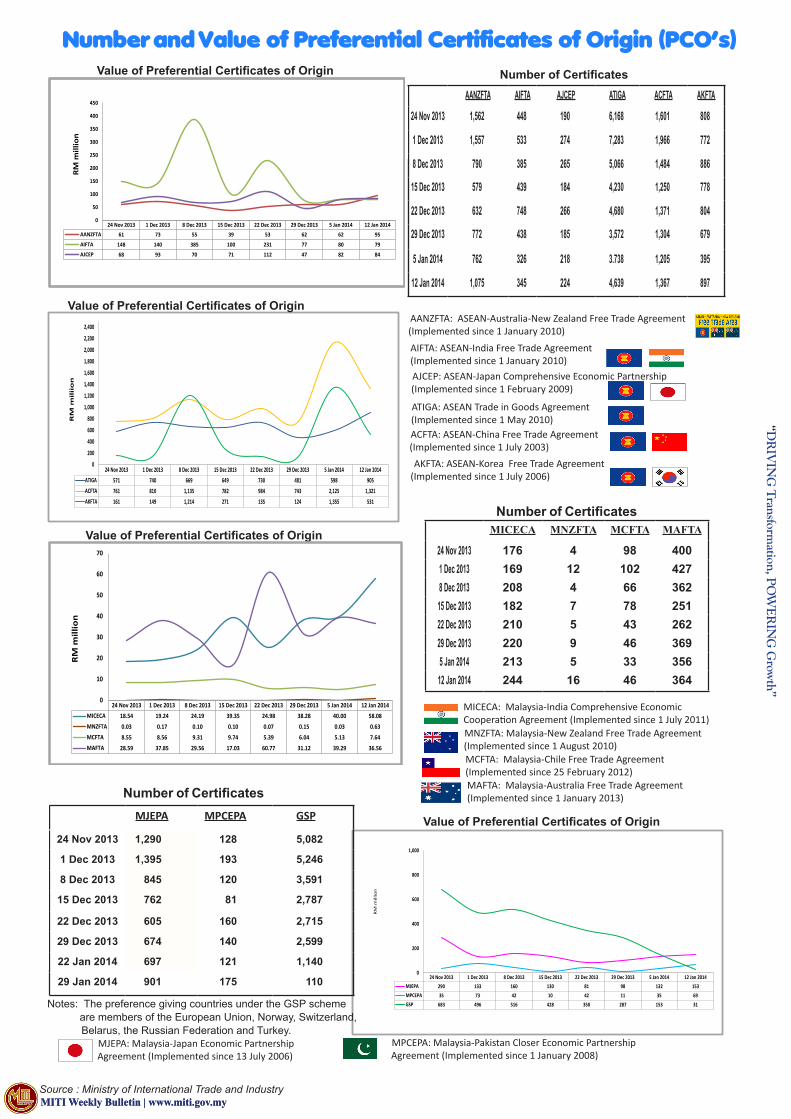

Number and Value of Preferential Certificates of Origin (PCO’s)

AANZFTA AIFTA AJCEP ATIGA ACFTA AKFTA

24 Nov 2013 1,562 448 190 6,168 1,601 808

1 Dec 2013 1,557 533 274 7,283 1,966 772

8 Dec 2013 790 385 265 5,066 1,484 886

15 Dec 2013 579 439 184 4,230 1,250 778

22 Dec 2013 632 748 266 4,680 1,371 804

29 Dec 2013 772 438 185 3,572 1,304 679

5 Jan 2014 762 326 218 3.738 1,205 395

12 Jan 2014 1,075 345 224 4,639 1,367 897

Number of CertificatesValue of Preferential Certificates of Origin

AJCEP: ASEAN-Japan Comprehensive Economic Partnership (Implemented since 1 February 2009)

ACFTA: ASEAN-China Free Trade Agreement (Implemented since 1 July 2003) AKFTA: ASEAN-Korea Free Trade Agreement (Implemented since 1 July 2006)

AANZFTA: ASEAN-Australia-New Zealand Free Trade Agreement (Implemented since 1 January 2010)AIFTA: ASEAN-India Free Trade Agreement (Implemented since 1 January 2010)

ATIGA: ASEAN Trade in Goods Agreement (Implemented since 1 May 2010)

24 Nov 2013 1 Dec 2013 8 Dec 2013 15 Dec 2013 22 Dec 2013 29 Dec 2013 5 Jan 2014 12 Jan 2014AANZFTA 61 73 55 39 53 62 62 95

AIFTA 148 140 385 100 231 77 80 79

AJCEP 68 93 70 71 112 47 82 84

0

50

100

150

200

250

300

350

400

450

RM

mill

ion

24 Nov 2013 1 Dec 2013 8 Dec 2013 15 Dec 2013 22 Dec 2013 29 Dec 2013 5 Jan 2014 12 Jan 2014ATIGA 571 740 669 649 730 481 598 905ACFTA 761 810 1,135 782 984 743 2,125 1,321AKFTA 161 149 1,214 271 135 124 1,355 531

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2,200

2,400

RM

mil

iio

n

Value of Preferential Certificates of Origin

Number of Certificates

MICECA: Malaysia-India Comprehensive Economic Cooperation Agreement (Implemented since 1 July 2011) MNZFTA: Malaysia-New Zealand Free Trade Agreement (Implemented since 1 August 2010)MCFTA: Malaysia-Chile Free Trade Agreement (Implemented since 25 February 2012)

24 Nov 2013 1 Dec 2013 8 Dec 2013 15 Dec 2013 22 Dec 2013 29 Dec 2013 5 Jan 2014 12 Jan 2014MJEPA 290 133 160 130 81 98 132 153MPCEPA 35 73 42 10 42 11 35 69GSP 683 496 516 428 350 287 153 31

0

200

400

600

800

1,000

RM

mill

ion

MJEPA MPCEPA GSP

24 Nov 2013 1,290 128 5,082

1 Dec 2013 1,395 193 5,246

8 Dec 2013 845 120 3,591

15 Dec 2013 762 81 2,787

22 Dec 2013 605 160 2,715

29 Dec 2013 674 140 2,599

22 Jan 2014 697 121 1,140

29 Jan 2014 901 175 110

Number of Certificates

Notes: The preference giving countries under the GSP scheme are members of the European Union, Norway, Switzerland, Belarus, the Russian Federation and Turkey. MJEPA: Malaysia-Japan Economic Partnership

Agreement (Implemented since 13 July 2006) MPCEPA: Malaysia-Pakistan Closer Economic Partnership Agreement (Implemented since 1 January 2008)

Value of Preferential Certificates of Origin

Value of Preferential Certificates of Origin

24 Nov 2013 1 Dec 2013 8 Dec 2013 15 Dec 2013 22 Dec 2013 29 Dec 2013 5 Jan 2014 12 Jan 2014MICECA 18.54 19.24 24.19 39.35 24.98 38.28 40.00 58.08MNZFTA 0.03 0.17 0.10 0.10 0.07 0.15 0.03 0.63MCFTA 8.55 8.56 9.31 9.74 5.39 6.04 5.13 7.64MAFTA 28.59 37.85 29.56 17.03 60.77 31.12 39.29 36.56

0

10

20

30

40

50

60

70

RM

mill

ion

MAFTA: Malaysia-Australia Free Trade Agreement (Implemented since 1 January 2013)

MICECA MNZFTA MCFTA MAFTA

24 Nov 2013 176 4 98 4001 Dec 2013 169 12 102 4278 Dec 2013 208 4 66 362

15 Dec 2013 182 7 78 25122 Dec 2013 210 5 43 26229 Dec 2013 220 9 46 3695 Jan 2014 213 5 33 356

12 Jan 2014 244 16 46 364

Source : Ministry of International Trade and Industry

MITI Weekly Bulletin | www.miti.gov.my

“DR

IVIN

G T

ransformation, P

OW

ERIN

G G

rowth”

MITI Weekly Bulletin | www.miti.gov.my

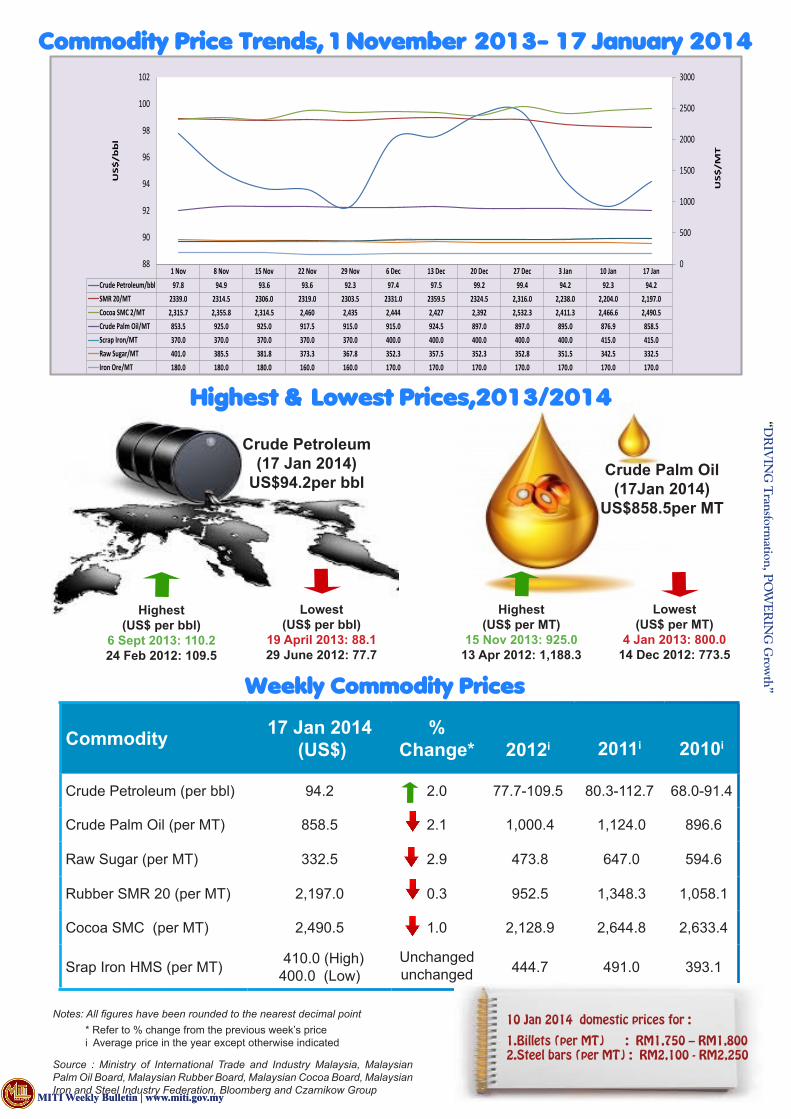

Commodity 17 Jan 2014 (US$)

% Change* 2012i 2011i 2010i

Crude Petroleum (per bbl) 94.2 2.0 77.7-109.5 80.3-112.7 68.0-91.4

Crude Palm Oil (per MT) 858.5 2.1 1,000.4 1,124.0 896.6

Raw Sugar (per MT) 332.5 2.9 473.8 647.0 594.6

Rubber SMR 20 (per MT) 2,197.0 0.3 952.5 1,348.3 1,058.1

Cocoa SMC (per MT) 2,490.5 1.0 2,128.9 2,644.8 2,633.4

Srap Iron HMS (per MT) 410.0 (High)400.0 (Low)

Unchangedunchanged 444.7 491.0 393.1

Weekly Commodity Prices

Notes: All figures have been rounded to the nearest decimal point * Refer to % change from the previous week’s price i Average price in the year except otherwise indicated

Source : Ministry of International Trade and Industry Malaysia, Malaysian Palm Oil Board, Malaysian Rubber Board, Malaysian Cocoa Board, Malaysian Iron and Steel Industry Federation, Bloomberg and Czarnikow Group

Commodity Price Trends, 1 November 2013- 17 January 2014

1 Nov 8 Nov 15 Nov 22 Nov 29 Nov 6 Dec 13 Dec 20 Dec 27 Dec 3 Jan 10 Jan 17 JanCrude Petroleum/bbl 97.8 94.9 93.6 93.6 92.3 97.4 97.5 99.2 99.4 94.2 92.3 94.2SMR 20/MT 2339.0 2314.5 2306.0 2319.0 2303.5 2331.0 2359.5 2324.5 2,316.0 2,238.0 2,204.0 2,197.0Cocoa SMC 2/MT 2,315.7 2,355.8 2,314.5 2,460 2,435 2,444 2,427 2,392 2,532.3 2,411.3 2,466.6 2,490.5Crude Palm Oil/MT 853.5 925.0 925.0 917.5 915.0 915.0 924.5 897.0 897.0 895.0 876.9 858.5Scrap Iron/MT 370.0 370.0 370.0 370.0 370.0 400.0 400.0 400.0 400.0 400.0 415.0 415.0Raw Sugar/MT 401.0 385.5 381.8 373.3 367.8 352.3 357.5 352.3 352.8 351.5 342.5 332.5Iron Ore/MT 180.0 180.0 180.0 160.0 160.0 170.0 170.0 170.0 170.0 170.0 170.0 170.0

0

500

1000

1500

2000

2500

3000

88

90

92

94

96

98

100

102

US

$/M

T

US

$/b

bl

Highest & Lowest Prices, 2013/2014

Crude Petroleum (17 Jan 2014)

US$94.2per bblCrude Palm Oil

(17Jan 2014)US$858.5per MT

Lowest (US$ per bbl)

19 April 2013: 88.129 June 2012: 77.7

Highest(US$ per bbl)

6 Sept 2013: 110.224 Feb 2012: 109.5

Highest(US$ per MT)

15 Nov 2013: 925.013 Apr 2012: 1,188.3

Lowest (US$ per MT)

4 Jan 2013: 800.0 14 Dec 2012: 773.5

10 Jan 2014 domestic prices for :1.Billets (per MT) : RM1,750 – RM1,800 2.Steel bars (per MT) : RM2,100 - RM2,250

MITI in the News

Industri automotif kini ternanti-nanti dengan pengumuman Dasar Automotif Negara (DAN) yang berkemungkinan besar diumumkan pada 20 Januari ini.Dasar tersebut menjadi pendorong untuk Malaysia kekal kukuh dalam industri automotif dan mengimbangi imbangan perdagangan negara. Umum mengetahui walaupun Malaysia mengeluarkan kereta jenamanya tersendiri iaitu Proton, tetapi dari segi bilangan kereta dalam pasaran, masih banyak yang diimport jika dibandingkan dengan eksport.Malaysia yang agak terkebelakang dari Thailand dari segi hab automotif, kini mungkin diketepikan oleh jiran, Indonesia yang menjadi tumpuan pelabur asing untuk industri itu.

Dasar Memperkasa Sektor Automotif

Malaysia masih mencari rentak untuk menjadi hab automotif dan pilihannya ialah hab bagi kenderaan teknologi cekap tenaga (EEV). Terdapat tiga jenis enjin kenderaan yang dirangkumkan dalam EEV seperti hibrid, elektrik dan enjin pembakaran dalam (Internal Commercial Engine) yang biasa digunakan ketika ini atau dikenali sebagai ICE dalam sektor automotif. Dua cara untuk menentukan standard EEV di dunia iaitu yang pertama adalah jumlah penggunaan minyak untuk jarak tertentu berdasarkan kelas berat kenderaan dan kedua adalah berdasarkan berat pembebasan gas karbon dioksida (Co2) untuk setiap kilometer (km) perjalanan. Polisi EEV kini merupakan di antara perkara pokok yang bakal diumumkan dalam NAP itu. Pemilihan Malaysia sebagai hab EEV setelah Thailand mengumumkan Polisi Kereta Ekologi, manakala Indonesia pula dengan dasar kereta Teknologi Hijau Harga Rendah. Dalam satu pertemuan pihak industri berkaitan NAP di Putrajaya dua minggu lalu, Menteri Perdagangan Antarabangsa dan Industri, Datuk Seri Mustapa Mohamed telah meminta mereka menyuarakan cadangan dan pendapat untuk dijadikan input dalam NAP.

Menteri itu juga membangkitkan tentang pentingnya industri automotif negara dalam imbangan perdagangan di mana import untuk sektor itu kian meningkat, sedangkan eksport masih belum memuaskan hati kerajaan. Sehubungan itu, kerajaan mungkin akan memperkenalkan beberapa insentif cukai menarik terhadap kenderaan EEV dari segi harga produk itu dan juga pengeluarnya.

Dalam hal ini, DRB-Hicom dikatakan berusaha memujuk Honda Jepun untuk melakukan pelaburan yang besar di Malaysia bagi menghasilkan kenderaan EEV yang bukan sahaja untuk pasaran domestik, tetapi untuk eksport.

Source: Malaysia Automotive Institute MITI Weekly Bulletin/ www.miti.gov.my

“DR

IVIN

G T

ransformation, P

OW

ERIN

G G

rowth”

What Investors Say

IKEA was founded in 1943 by Ingvar Kamprad and the first store (including a show room) was opened in Almhult, Sweden in 1958. Since then, IKEA has developed a strong concept and product range around home furnishing articles, focused on function, quality and low price.

Currently, there is a grand total of 229 IKEA stores in 33 countries / territories, and the company's turnover reached 14.8 billion euro in 2005. More than 400 million people have visited IKEA stores world-wide. The IKEA catalogue had a total of 160 million copies printed in 52 editions and 25 languages. IKEA was set up in Malaysia in 1999 with its distribution centre being the regional hub for the company's Asia Pacific market to its 16 stores in seven Asia Pacific countries.

"Malaysia has been chosen for its central geographical position in Asia and it's well developed logistics network and port infrastructure" says Vic Kurzeja, General Manager for IKEA's Distribution Centre Malaysia. "We found in Malaysia a stable and reliable business and social environment which enables us to focus on our long term expansion goals". Today, IKEA's distribution centre, with a 130,000 pallet storage capacity employs circa 220 co-workers. The key element of the company's logistics network and strategy is to develop its market share in the Asia Pacific in the coming years. IKEA will continue to develop and optimize its logistics hub in Malaysia by implementing Radio-Frequency technology in 2007 to monitor the company's inventory flow and continue to invest in the development of local competence. Malaysia's ethnic diversity and well educated workforce has enabled IKEA to find the suitable manpower to meet the company's human resource requirements.

Address: No.2 Jalan PJU 7/2,Mutiara Damansara,47800 Petaling Jaya,Selangor Darul Ehsan, Malaysia Phone:+(603) 7726 7777

IKEA MALAYSIA

source: http://www.mida.gov.my/env3/index.php?page=success-story-say MITI Weekly Bulletin/ www.miti.gov.my

“DR

IVIN

G T

ransformation, P

OW

ERIN

G G

rowth”

MITI Weekly Bulletin | www.miti.gov.my

“DR

IVIN

G T

ransformation, P

OW

ERIN

G G

rowth”

MITI Weekly Bulletin | www.miti.gov.my

TERMINATION OF THE GENERALIZED SYSTEM OF PREFERENCES (GSP)

1 JANUARY 2014

1. As announced since 1 January 2013 through the ePCO system and leaflets at all MITI counters, effective 1 January 2014, Malaysia will no longer enjoy the GSP schemes offered by the EU and TURKEY. Malaysia has been graduated out of the scheme in light of the country achieving upper middle income status (according to the World Bank). MITI will no longer issue FORM A to EU, TURKEY and ASEAN countries. [TURKEY is part of EU Custom Union].

2. Information on the GSP rate can be obtained http://ec.europa.eu/taxation_customs/dds2/taric/taric_consultation.jsp?Lang=en&SimDate=20121129

3. Please take note that exports to Norway, Switzerland, Russia, Belarus & Japan are not affected. MITI will continually update on any new devlopments about the GSP through ePCO system.

Ministry of International Trade & Industry Malaysia

MITI Brainstorming Retreat 9 January 2014, Cyberjaya, Selangor

MITI Senior Management

Dear Readers,Kindly click the link below for any comments in this issue. MWB reserves the right to edit and to republish letters as reprints. http://www.miti.gov.my/cms_matrix/form.jsp?formId=c1148fbf-c0a81573-3a2f3a2f-1380042c

Comments & Suggestions

Name : Haslinda MansorDesignation : SecretaryDivision : Industry and Trade Support Serrvice : Six yearsContact : 03-62000109Email : [email protected]

Name : Norrizah AyobDesignation : SecretaryDivision : Secretary General OfficeDuration of Service : 35 yearsContact : 03-62000028Email : [email protected]

“DR

IVIN

G T

ransformation, P

OW

ERIN

G G

rowth”

![PowerPoint プレゼンテーション...ep Cycle Power nap] L 770 IJ Power Nap uses the built-in accelerometer... Set alarm Prevent sleep_ Power nap Recovery nap Nap up to 20 min](https://img.pdfslide.us/doc/110x75/5e9108cd1921e42a0d77fd49/powerpoint-fffffff-ep-cycle-power-nap-l-770-ij-power-nap.jpg)