Embed Size (px)

Citation preview

CSRS

National Associationof Letter Carriers

AQ

Civil Service Retirement System

uestions

nswerson

Whether covered by the Civil Service RetirementSystem (CSRS) or the Federal EmployeesRetirement System (FERS), letter carriers planningto retire face many different options and electionswhen completing an application for retirement—questions regarding proper annuity calculation, sur-vivor annuity, life insurance options and many more.This booklet has been prepared and updated to

provide CSRS carriers with answers to these ques-tions. Because FERS benefits differ greatly fromthose offered under the Civil Service RetirementSystem, a separate booklet is available for those

carriers enrolled under FERS.I recognize that retirement is not only an impor-

tant stage in one’s life, it is sometimes a difficultone—full of complex questions and answers. That iswhy this booklet will also be of assistance to carriersalready retired by enabling them to make informedchoices during their retirement years.So whether you are already retired or planning to

retire, this booklet will serve as a handy referenceguide. Use it well and enjoy your retirement years.

Sincerely,

Fredric V. RolandoPresident

Dear NALC Member:

National Association

of Letter Carriers

100 Indiana Avenue, N.W.

Washington, D.C. 20001

QUESTIONSA N D

A N SWER SO N T H E

CIVIL SERVICERETIREMENT SYSTEM

This booklet refers ONLY tothe Civil Service RetirementSystem (CSRS). A bookletregarding the FederalEmployees RetirementSystem (FERS) is availablethrough the NALC SupplyDepartment. The purpose ofthis booklet is to answermany of the questions posedto the NALC RetirementDepartment.

Revised 2018 Edition

Where can I call if I havequestions/problems concerning my retirement benefits?

The NALC RetirementOffice operates a toll freenumber (800-424-5186) on Monday, Wednesday andThursday, 10-12 noon and2-4 pm, Eastern Time.

What is the number forthe RetirementInformation Office of theU.S. Office of PersonnelManagement?

Toll Free 888-767-6738

Where can I call for SocialSecurity information?

800-772-1213

CONTENTS

QuestionNumber

Financing the Civil Service Retirement Fund 1-6Employees Covered and Crediting of Civilian Service 7-21Military Service Credit 22-27Types of Retirement—Qualifying for CSRS Annuity 28-34Alternative Annuity (Lump Sum Option) 35Disability Retirement 36-50Deferred Annuity 51-55Survivor Annuity Elections 56-67How Annuity Is Determined 68-88How To Claim a Survivor Annuity 89-100Survivor Predeceases Annuitant/Annuitant Marries or Remarries 101-102Refund—Redeposit 103-113How CSRS Benefits Are Paid/Can Benefits Be Attached 114-119Federal Income Taxes 120-122Politics/Jury Duty/Declination of Annuity 123-126Forms Used Under CSRS 127-129CSRS and Social Security 130-134General Information on the TSP 135-139The TSP, IRAs and Taxes 140-145Employee Contributions to the TSP 146-148TSP Investment Options 149-151TSP Interfund Transfers 152-155Getting Funds Out of the TSP 156-162The TSP Loan Program 163-165Spousal Rights and TSP Savings in Death of CSRS Participant 166-169Federal Employees Group Life Insurance and Health BenefitsCoverage 170-178What an Annuitant Should Do when Divorced/Death of Spouse 179-180General Retirement Information 181-189

because they wereseparated fromCSRS-covered feder-al employment formore than a year andreturned to a positionin which they werecovered by CSRS af -ter 1983. For theseemployees, their So -cial Security with-holdings are offsetfrom their CSRScon tributions, so that the combinedSocial Security andCSRS contributionsare the same as foremployees who haveCSRS coverage only.

When CSRS-Offsetemployees retire,they receive fullCSRS benefits untilthey are eligible forSocial Security bene-fits, generally at age

overtime pay, mili-tary pay, specialallowances such as uniforms, cashawards for suggestions or superior accom -plishment.

5 Has this deductionrate always beenseven percent?

No. Changes indeduction rates areshown in the tablebelow.

6 What are CSRS-Offset contributions?

CSRS-Offsetemployees are cover -ed by Social Security

FINANCING THE

CIVIL SERVICE

RETIREMENT

FUND

Percentage rates for deductions Dates of Service from basic pay From August 1920 to June 1926 21/2%

From July 1926 to June 1942 31/2%

From July 1942 to June 1948 5%

From July 1948 to September 1956 6%

From October 1956 to December 1969 61/2%

From January 1970* 7%

1 What is the CivilService RetirementFund?

It is the accumula-tion of money held intrust by the U.S.Treasury for the pur-pose of paying annu-ity, refunds, or deathbenefits.

2 How is the moneyinvested?

It is invested by theU.S. Treasury in government securities.

3 How much is de -ducted from thesal ary of eachmember of theretirement system?

Seven percent of thebasic pay (except forlaw enforcement andfirefighter personnel,Congressional em -ployees, and Mem -bers of Congress).

4 What is meant bybasic pay?

Basic pay is the payor compensation set by law or regula-tion. It does notinclude bonuses,

*There were temporary increases in 1999 and 2000 but the deduction rate was rolled back to 7% effective January 2001.

Security benefit thatrepresents the period of time they were covered

by both CSRS andSocial Security.

62. At that time, theCSRS benefit is offset by the portionof their Social

EMPLOYEES

COVERED AND

CREDITING OF

CIVILIAN SERVICE

7 Who are membersof the Civil ServiceRetirementSystem?

Appointive and elec-tive officers and em -ployees in or underthe executive, judi-cial, and legislativebranches of the U.S.Government andother employeesspecifically coveredby law or regulationwho were hired priorto January 1, 1984.

8 Is membership op -tional with the em -ployee?

For persons em -ployed beforeJanuary 1, 1984 itwas automatic exceptin the case ofMembers of Con -gress and certainemployees in the legislative branchwho had the optionof becoming mem-bers.

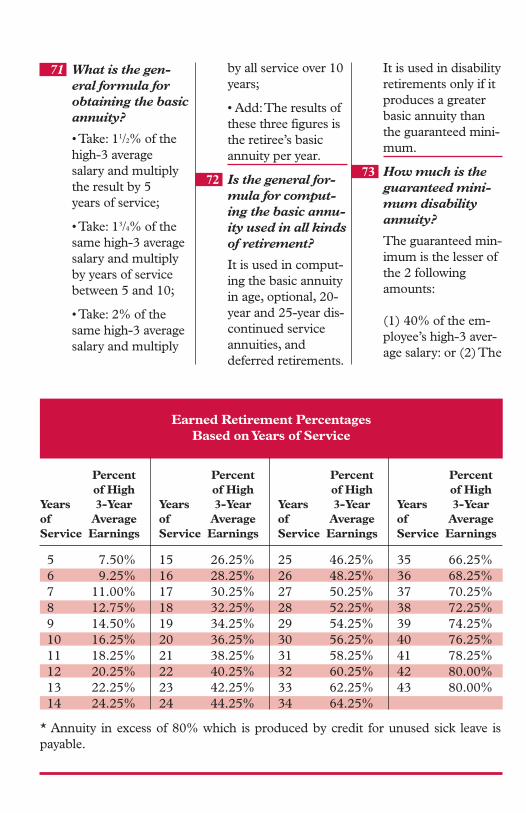

9 May credit beallowed for servicefor which no retire-ment deductionswere taken?

Yes, provided theemployee became amember of CSRS af -ter such service wasperformed.

10 Is deposit requiredto obtain credit forperiods of servicefor which no retire-ment deductionswere taken?

It depends uponwhen the service was performed. If the service was priorto October 1, 1982,payment of thedeposit is required inorder to receive themaximum annuity,but not to receivecredit for the service.If the service wasperformed on orafter October 1,1982, and deposit is

not made, the servicecounts toward retire-ment eligibility andthe service can beused for high-3 aver-age salary purposes,but the service is notused in determiningtotal service for an -nuity computationpurposes.

11 How is the annuityaffected if the de -posit is not madefor service prior toOctober 1, 1982?

The annuity is re -duced by 10 percentof the amount due asde posit. For example:If a retiring em ployeehas an un paid depositwhich amounts to$1,200.00, the yearlyreduction in theannuity will be 10percent of $1,200.00,or $120.00, or$10.00 a month.

12 Is it to the employ-ee’s advantage tomake the deposit?

This question can-not be answered by a simple yes or no.There are good rea-sons for making it,

and there are goodreasons for not mak-ing it. It depends onthe length of servicethat the depositwould cover, thenumber of years ofcreditable servicethat an employeewould have whenretiring, and thenumber of years that the employeefigures his/her life ex -pectancy will be af-ter retiring. The ac -tual amount of adeposit made atretirement will be re -turned to the annui-tant in ten years. Ifthe retiree lives longenough, he/she willget the investmentback plus the addedannuity for all theyears that he/shelives.

13 May deposit orredeposit be madein installment pay-ments?

Payment may bemade in a lump sumor in installments ofnot less than $25.00each, paid directly tothe U.S. Office ofPersonnel Manage -ment while the indi-vidual is still in activeemployment.

14 In case of the deathof an employee,may a survivor en -titled to annuitybenefits make thedeposit or rede-posit?

Yes.

15 Is credit allowedfor leave withoutpay?

Credit is given with-out deposit to thefund for so much offurlough or leavewithout pay (LWOP)as does not exceedsix months in anycal endar year. If inreceipt of OWCPbenefits, credit isgenerally given forthe entire period ofcompen sation if car-ried on the rolls in aLWOP status.

16 Is service with stateand municipal gov -ernments credit -able under the CivilService RetirementSystem?

No.

17 Is extra creditallowed for unusedsick leave?

Yes, where the em -ployee retires on animmediate annuityor dies. The time represented by theunused sick leave isadded to the em -ployee’s actual serv -ice used in comput-ing annuity.

18 What is an im -medi ate annuity?

One that begins nolater than one monthafter separation fromthe service.

19 How much time isallowed for unusedsick leave?

It is on the day-for-day basis; 8 hours ofunused sick leaveequals one day. Onthis basis, approxi-mately 22 days ofunused sick leaveequals one month.

20 Is deposit requiredto receive credit forunused sick leave?

No.

No of 1 Day 1 Mo. 2 Mo. 3 Mo. 4 Mo. 5 Mo. 6 Mo. 7 Mo. 8 Mo. 9 Mo. 10 Mo. 11 Mo. Days & Up & Up & Up & Up & Up & Up & Up & Up & Up & Up & Up & Up

0 0 174 348 522 696 870 1044 1217 1391 1565 1739 1913

1 6 180 354 528 701 875 1049 1223 1397 1571 1745 1919

2 12 186 359 533 707 881 1055 1229 1403 1577 1751 1925

3 17 191 365 539 713 887 1061 1235 1409 1583 1757 1930

4 23 197 371 545 719 893 1067 1241 1415 1588 1762 1936

5 29 203 377 551 725 899 1072 1246 1420 1594 1768 1942

6 35 209 383 557 730 904 1078 1252 1426 1600 1774 1948

7 41 214 388 562 736 910 1084 1258 1432 1606 1780 1954

8 46 220 394 568 742 916 1090 1264 1438 1612 1786 1959

9 52 226 400 574 748 922 1096 1270 1444 1617 1791 1965

10 58 232 406 580 754 928 1101 1275 1449 1623 1797 1971

11 64 238 412 586 759 933 1107 1281 1455 1629 1803 1977

12 70 243 417 591 765 939 1113 1287 1461 1635 1809 1983

13 75 249 423 597 771 945 1119 1293 1467 1641 1815 1988

14 81 255 429 603 777 951 1125 1299 1472 1646 1820 1994

15 87 261 435 609 783 957 1130 1304 1478 1652 1826 2000

16 93 267 441 615 788 962 1136 1310 1484 1658 1832 2006

17 99 272 446 620 794 968 1142 1316 1490 1664 1838 2012

18 104 278 452 626 800 974 1148 1322 1496 1670 1844 2017

19 110 284 458 632 806 980 1154 1328 1501 1675 1849 2023

20 116 290 464 638 812 986 1159 1333 1507 1681 1855 2029

21 122 296 470 643 817 991 1165 1339 1513 1687 1861 2035

22 128 301 475 649 823 997 1171 1345 1519 1693 1867 2041

23 133 307 481 655 829 1003 1177 1351 1525 1699 1873 2046

24 139 313 487 661 835 1009 1183 1357 1530 1704 1878 2052

25 146 319 493 667 841 1015 1188 1362 1536 1710 1884 2058

26 151 325 499 672 846 1020 1194 1368 1542 1716 l890 2064

27 157 330 504 678 852 1026 1200 1374 1548 1722 1896 2070

28 162 336 510 684 858 1032 1206 1380 1554 1728 1901 2075

29 168 342 516 690 864 1038 1212 1386 1559 1733 1907 2081How to use this chart—To find the increased service time credit for unused sick leave, use the fol-lowing formula. Find the number of hours of unused sick leave. In the horizontal column you willfind the number of months and in the vertical column the remaining number of days. For example,441 hours equals 2 months and 16 days. Another example: 1455 hours equals 8 months and 11 days.

21 Does the limitationon annuity of notmore than 80% ofthe high-3 averagesalary apply toannuity based onunused sick leave?

sick leave intoincreased servicetime for higherannui ties follows:

No. Additional annu-ity attributable to thesick leave credit isallowable over andabove this limitationof 80%. A chart forconverting unused

22 What does thetermmilitary ser-vice cover?

Time spent in serv -ice to: the Army;Navy; Air Force;Marine Corps; CoastGuard; Regular orReserve Corps ofPublic HealthService after June 30,1960; orCommissionedOfficers of NationalOceanic & Atmos -pheric Adminis tra -tion after June 30,1961.

23 Is military servicecreditable for Civil Service re -tirement purposes?

Military service iscreditable provided it was active serviceand was termi-nated under honor-able conditions andwas performedbefore separationfrom a civilian posi-tion under theRetirement System.

24 What is Chapter12731, Title 10, U. S. Code?

It is a provisiongranting retired pay to members ofthe reserve compo-nents of the ArmedForces on the basisof service. The basic requirement is the attainment ofage 60 with the completion of 20years of service in the Armed Forces.This provision pro-vides that you candraw a reserve mili-tary pension and stillreceive credit for themilitary servicetoward your CivilService annuity.

25 May militaryretired pay bewaived so that themilitary servicewill be creditedunder the CivilService Retire-ment System?

Yes.

26 May military service be creditedto ward retirementrather than towardSocial Security?

Credit will auto -matically be givenunder the CivilService RetirementSystem for militaryservice performedbefore January 1,1957. Credit may be given under theCSRS for militaryservice performed on or after January 1, 1957, only if theemployee is not eli -gible for Social Se -curity old age bene-fits. Your military ser-vice which took placeafter December 31,1956 is automaticallycredited towardsSocial Security bene-fits if you become eli-gible for such bene-fits. Such servicecannot simultane-ously be cred ited inthe computation ofyour civil service an -nuity unless, beforere tirement, you pay ade posit to cover the service. If you first cameunder the CivilService Re tirementSystem on or afterOctober 1, 1982

MILITARY

SERVICE

CREDIT

your post-1956 militaryservice will not be includ-ed in your civil serviceannuity without paymentof a deposit, even if youare not eligible for SocialSecurity benefits.Individuals first

employed by the federalgovernment under theCivil Service RetirementSystem before October 1,1982, will have theoption of either: (1) mak-ing the seven-percentdeposit for post-1956military service—therebyavoiding a possiblereduction in annuity atage 62, or (2) receivingcredit as in the past andhaving his/her annuityreduced at age 62 ifhe/she becomes eligiblefor Social Security.The basic deposit

is equal to seven percentof the base pay (not al -lowances) earned duringa period or periods ofactive military serviceperformed afterDecember 31, 1956.Interest is charged on

the basic deposit at thefollowing market interestrates.

1985 - 13%1986 - 11.125%1987 - 9.0%1988 - 8.375%1989 - 9.125%1990 - 8.75%

1991 - 8.625%1992 - 8.125%1993 - 7.125%1994 - 6.25%1995 - 7.0%1996 - 6.875%1997 - 6.875%1998 - 6.75%1999 - 5.75%2000 - 5.875%2001 - 6.375%2002 - 5.5%2003 - 5.0%2004 - 3.875%2005 - 4.375%2006 - 4.125%2007 - 4.875%2008 - 4.750%2009 - 3.875%2010 - 2.75%2011 - 2.25%2012 - 2.25%2013 - 1.625%2014 - 1.625%2015 - 2016 - 2.0%2017 - 1.875%

Future years to bedetermined by theDepartment of Treasury.No credit for any

military service isgiven to an employeewho receives militaryretired pay unless theretired pay is awardedfor: (a) service-connecteddisability incurred incombat with an enemy ofthe United States, or (b)service-connected dis-ability caused by aninstrumentality of warand incurred in the lineof duty during a period

of war, or (c) under theprovisions of Chapter12731, Title 10, U.S.C.(pertaining to retirementfrom a reserve compo-nent of the ArmedForces).An employee who is

receiving military retiredpay which bars credit formilitary service may electto waive the retired payand have the military ser-vice added to civilian ser-vice in computing theannuity. However, if thisemployee does not waivemilitary retired pay,retirement rights will bebased on civilian serviceonly and military servicewill not be included incomputing the annuity.The employee may, how-ever, receive both militaryretired pay and civil ser-vice annuity at the sametime.

27 May an employeereceive credit forservice with theNational Guard?

Only when the or -ganization is acti -vated in the U. S.Army or Air Force.

28 What kinds ofretirement are provided for in theretirement law?

They are known asoptional, earlyoptional, disability,deferred, and discon -tinued service an -nuity for either 25 years of service or 20 years of service, ifat least age 50. Forboth early optionalretirement (e.g.,reduction in force)and discontinuedservice retirement(e.g., involuntaryseparation except formisconduct),employees can retireat any age with 25years of service orage 50 with 20 yearsof service. Therewould be an annuityreduction of 2 per-cent for each yearemployee is underage 55.

29 Is there a mini-mum requirementas to the amount of civilian service?

Yes. Five years ofcivilian service isrequired beforeannuity benefits maybe paid in any case.

30 Must an employeeapply for retire-ment?

Yes. An applicationmust be completedfor any annuity benefits.

31 Under what condi-tions may anemployee retireoptionally?

• Age 62 with a minimum of 5 years of service;

• Age 60 with 20years of service; or

• Age 55 with 30years of service.

32 Must applicationfor optional retire-ment be made be -fore the employeeis separated fromthe service?

No. However, it isadvisable to applyabout 6 weeks inadvance of the datescheduled for separa-tion.

33 What is the maxi-mum annual leavea letter carrier canbe paid for?

440 hours. Anyamount over 440hours will be forfeited, if not used.

34 What day should you retire on?

For optional retire-ment, an employeeshould retire on thelast day of a month,or on the first 3 daysof the month so thatannuity will com-mence the followingday after the effectivedate of retirement. Ifthe employee isretired after the 3rdof the month, annu-ity will commencethe first of the fol-lowing month.

TYPES OF

RETIREMENT—

QUALIFYING FOR

CSRS ANNUITY

ALTERNATIVE

ANNUITY

(LUMP SUM

OPTION)

35 Can I receive alump sum pay-ment?

No, the lump sumwas eliminated bythe Omnibus BudgetReconciliation Act of

1993, except for certain non-disability retireeswho retire with a life-threatening affliction or othercritical medical

condition that limits probable life expectancy to less than two years.

36 Under what condi-tions may anemployee retire fordisability?

An employee mustbecome totally dis-abled for useful andefficient service inthe position held andmust have completedat least 5 years ofcivilian service.

37 What constitutestotal disability?

Inability of theemployee, because ofinjury or illness, tosatisfactorily performthe duties of theposition held or the

duties of a similarposition. It need notbe shown that theapplicant is disabledfor all kinds of work.Under 5 USC8337(a) it states: “Anemployee of theUnited States PostalService shall be con-sidered not qualifiedfor a reassignment …if the reassignment isto a position in a dif-ferent craft or isinconsistent with theterms of a collectivebargaining agree-ment covering theemployee.”

38 Who determineswhether an em -ployee is totallydisabled to qualifyfor an an nuity?

The U.S. Office ofPersonnel Manage -ment makes the determination.

39 Must the injury orillness be incurredwhile on duty?

No. If it is in-curred on the job,however, the em -ployee will have achoice between an -nuity under theCSRS or benefitsfrom the Depart -ment of Labor’sOffice of Workers’Compensation Pro -grams, and the em-

DISABILITY

RETIREMENT

ployee may choosewhichever is to his/her advantage.

40 Who files the annu-ity application if anemployee is men-tally incompetent?

The employee’sguardian.

41 May the employ -ing department oragency apply tohave an employeeretired for disabil -ity?

Yes. If the agencybelieves that theemployee is totallydisabled for usefuland efficient servicein the position held.

42 When does a dis-ability annuitybegin?

It begins on the dayafter separation orthe day after theemployee’s pay statusterminated and theemployee has metthe disability and ser-vice requirements.

43 Are further med-ical examinationsnecessary after theemployee is placedon the disabilityannuity rolls?

Periodic examina-tions are requireduntil the annuitantreaches age 60 oruntil it is found thatthe disability is of apermanent nature.

44 Must the annuitantpay for these med-ical examinations?

Yes.

45 In case a disabilityannuitant underage 60 re covers,what is his/her status?

The annuity will bediscontinued at theend of one year fromdate of the medicalreport showingrecovery, or uponFederal reemploy-ment, whichevercomes first.

46 Is reinstatement inthe federal serviceautomatic uponrecovery orrestoration toearning capacity?

No. The individualmust locate a posi-tion on their own.

47 What happens to adisability annui-tant whose earningcapacity isrestored?

Even if the annuitantremains totally dis-abled, an annuitantwhose earningcapacity is restoredbefore reaching age60 will have his/herannuity discontin-ued. (Annuity is notdiscontinued ifrestored after age60).

48 When is a disabilityannuitant’s earn-ing capacity con-sidered restored?

Earning capacity is consideredrestored if, in onecalendar year theannuitant’s incomefrom wages or self-employment, orboth, is at least 80% of the currentbasic pay of the position from which the employeeretired.

50 If an annuitantwho has recoveredor whose earningcapacity is restoredis not reemployedin the governmentservice, may theretiree receive afurther annuityafter the disabilitystops?

Yes. The annuitant isconsidered involun-tarily separated, andwould be eligible todraw one of the fol-lowing annuities:

• Deferred annu -ity—would beginwhen the annuitantreaches age 62;

• 20-year discon-tinued service an -nuity—if the annui-tant is age 50 with atleast 20 years of ser-vice, this annuitywould begin immedi-ately following thetermination of thedisability annuity; or

• 25-year discon-tinued service an -nuity—if the annui-tant had at least 25years of serviceregardless of age, thisannuity would beginimmediately follow-ing the terminationof the disabilityannuity.

49 Is income fromsuch sources asrents, dividends,Social Security,pensions, insur-ance policies,stocks or bondsconsidered in de -ciding whether adisability annui-tant’s earning ca -pacity is restored?

No. Only incomefrom wages or self-employment is con-sidered.

DEFERRED

ANNUITY

51 Who is eligible fordeferred retire-ment?

Any separated em -ployee who is age 62and has com pletedat least 5 years ofcivilian service pro-viding the em ployeeleft retirement con-tributions in the CivilService Retire mentFund.

52 When does thisdeferred annuitybegin?

It begins on the separated employee’s62nd birthday.

53 How do I apply formy deferred CSRSannuity?

Obtain OPM form1496A from OPMby calling, writing,orvisiting www.opm.govand send your appli-cation approximately60 days before your62nd birthday to:Office of PersonnelManagement, Retire-ment OperationsCenter, P.O. Box 45,Boyers, PA. 16017

54 Is an employee eli-gible for deferredannuity regardlessof the reason forseparation?

Yes. Providing he/she leaves the retire-ment contributionsin the Civil ServiceRetirement Fundand is not convictedof certain NationalSecurity offenses.

55 If I die beforeattaining age 62, orafter age 62 butbefore applying forannuity, will mysurvivor(s) receivesurvivor benefits?

The only benefitpayable will be yourlump-sum credit inthe retirement fund;monthly survivorannuity will not bepayable.

58 What is an annuitywithout survivorbenefit?

It is the annuitywhich is payable tothe retiring employeefor his/her lifetimeonly.

59 When is the sur-vivor annuity tothe widow or wid-ower effective?

It is effective the dayafter the employee orretiree dies and con-tinues until the endof the month beforethe one in which thewidow or widowerremarries before age55 or dies. Remarri -age after age 55 doesnot affect the sur-vivor annuity. Forremarriages occur-ring after January 1,1995, if the widow/widower remarriesbefore age 55, andwas married at least30 years to the indi-vidual on whose ser-vice the survivorannuity is based, thesurvivor annuity willnot be terminated.

60 How much sur-vivor annuitywould the widowor widowerreceive?

The widow or wid-ower of a retiredemployee will gener-ally receive 55% ofthe retiree’s basicannuity. (The annui-tant can provide apercentage less than55% if agreed uponby the spouse at timeof retirement).

61 How much is thereduction in the re -tired employee’san nuity if he/sheaccepts the annuitywith survivor ben-efit to his/her wid -ow or widower?

The reduction is 21/2% of the first$3,600, and 10% ofany amount over$3,600 used as abase for the survivorbenefit.

62 What is the annuitywith survivorbene fit to namedperson having aninsurable interest?

In this type, the retir-ing employee takes areduction in theannuity and names aperson who has aninsurable interest in

56 What are theAnnuity Elections?

There are fourannuity elections tochoose from.(1) Annuity withsurvivor benefit towidow or widower;(2) Annuity withoutsurvivor benefit;(3)Annuity to pro-vide a former spouseor combination cur-rent/former spousesurvivor annuity; or(4) Annuity withsurvivor benefit tonamed person hav-ing an insurableinterest.

57 Can an employeechoose which typeof annuity he/shewants?

Yes. A marriedemployee is automat-ically granted theannuity with survivorbenefit to widow orwidower, unless thespouse waives his/herright to the survivorbenefit.

SURVIVOR

ANNUITY

ELECTIONS

his/her life to receivea survivor annuity.

63 Who may elect anannuity with sur-vivor benefit tonamed personhaving an insur-able interest?

Any retiring em ployee who is ingood health.

64 If an employeeelects an annuitywith survivor ben-efit to named per-son having aninsurable interest,how much is thereduction in annu-ity?

This depends on thedifference in agesbetween the retiringemployee and theperson named as sur-vivor annuitant. Seethe table below:

65 How much sur-vivor annuity willthe person havingan insurable inter-est receive?

This person willreceive 55% of theretiring employee’sreduced annuity.

66 How does a retir-ing employee indi-cate the type ofannuity he/shewishes to receive?

There is a portion ofthe Application forRetirement whichmust be completedindicating the retir-ing employee’schoice.

67 Can an annuitantever change his/hertype of annuity?

In some cases, it canbe changed and inothers it cannot:

• A survivor electionmay not be revokedor changed, oranother survivornamed later than 30days after the date ofthe first regularmonthly annuitypayment. However, aretiree who was mar-ried at time of retire-ment and elected aself-only annuity, ora partially reducedannuity to a currentspouse, formerspouse or insurableinterest designee mayelect no later than 18months after retire-ment, an annuityreduction or anincreased annuityreduction to providea current spouseannuity. If the mar-riage should termi-nate before theretired employeedies, the amount ofannuity will beincreased by theamount previouslydeducted for the sur-vivor annuity, and ifthe annuitant getsremarried, an elec-

Reduction Age of person named in relation in annuity to that of retiring employee of Retiree

Older, same age or less than 5 years younger 10% 5 but less than 10 years younger 15% 10 but less than 15 years younger 20% 15 but less than 20 years younger 25% 20 but less than 25 years younger 30% 25 but less than 30 years younger 35% 30 or more years younger 40%

the spouse for a sur-vivor benefit.

NOTIFY:

U.S. Office of Per -sonnel Manage ment,Retirement Opera -tions Center, Boyers,Penn sylvania 16017,in writing of this in -tention no later than2 years after the mar-riage.

• An employee retir-ing, unmarried, andwho elected a surviv -or benefit to a namedperson having an in -sur able interest maychange this if he/shegets married andelects his/her spouse

to be covered with asurvivor benefit. Thisalso must be donewithin 2 years afterthe marriage.

• If a retiree remar-ries the same personthey were married toat retirement andthat person had pre-viously consented toan election of no survivor annuity, theretiree may not electto provide a survivorannuity for that per-son when he or sheremarries.

tion can be made tocover the new spousefor a survivor benefit.If the spouse prede-ceases the annuitantand that annuitantlater remarries, theannuity is reducedactuarially for all themonths that theannuity was restoredto full annuity inorder to include thenew spouse for thissurvivor benefit.

• An employee whowas not married atthe time of retire-ment and later mar-ries, can request thatthe annuity bechanged to include

HOW

ANNUITY IS

DETERMINED

68 How is the amountof employee’s basicannuity deter-mined?

The amountdepends primarilyupon an employee’slength of service andthe high-3 averagesalary.

69 How is an employ-ee’s length of ser-vice computed?

All periods of cred-itable service areadded together pluscredit for unusedsick leave. The odddays under 30 in thetotal are dropped,and the time (yearsand months) remain-

ing is the length ofservice used in theannuity computationformula.

70 How is an employ-ee’s “high-3” aver-age pay computed?

The “high-3” averagesalary is the highestsalary obtainable byaveraging the rates ofbasic pay in effectduring any 3 consec-utive years of service.(Does not have to befrom January 1 toDecember 31.)

71 What is the gen-eral formula forobtaining the basicannuity?

• Take: 11/2% of thehigh-3 average salary and multiplythe result by 5 years of service;

• Take: 13/4% of thesame high-3 averagesalary and multiplyby years of servicebetween 5 and 10;

• Take: 2% of thesame high-3 averagesalary and multiply

by all service over 10years;

• Add: The results ofthese three figures isthe retiree’s basicannuity per year.

72 Is the general for-mula for comput-ing the basic annu-ity used in all kindsof retirement?

It is used in comput-ing the basic annuityin age, optional, 20-year and 25-year dis-continued serviceannuities, anddeferred retirements.

It is used in disabilityretirements only if itproduces a greaterbasic annuity thanthe guaranteed mini-mum.

73 How much is theguaranteed mini-mum disabilityannuity?

The guaranteed min-imum is the lesser ofthe 2 followingamounts:

(1) 40% of the em -ployee’s high-3 aver-age salary: or (2) The

* Annuity in excess of 80% which is produced by credit for unused sick leave ispayable.

Earned Retirement PercentagesBased on Years of Service

Percent of High Years 3-Year of Average Service Earnings

5 7.50% 6 9.25% 7 11.00% 8 12.75% 9 14.50% 10 16.25% 11 18.25% 12 20.25% 13 22.25% 14 24.25%

Percent of High Years 3-Year of Average Service Earnings

15 26.25%16 28.25%17 30.25%18 32.25%19 34.25%20 36.25%21 38.25%22 40.25%23 42.25%24 44.25%

Percent of High Years 3-Year of Average Service Earnings

25 46.25% 26 48.25%27 50.25%28 52.25%29 54.25%30 56.25%31 58.25%32 60.25%33 62.25%34 64.25%

Percent of High Years 3-Year of Average Service Earnings

35 66.25%36 68.25%37 70.25%38 72.25%39 74.25%40 76.25%41 78.25%42 80.00%43 80.00%

amount ob tainedunder the generalformula af ter in -creas ing the em -ployee’s actual cred-itable service by thetime re maining between the date ofseparation and thedate they reach age60.

74 Do all employeeswho retire for dis-ability get the guar-anteed minimumannuity?

The guaranteed minimum offers noadvantage to anemployee when re -tiring if the em-ployee has at least 21 years and 11months service, or ifthe employee hasreached age 60 attime of retirement.

75 Is there a limita-tion on the amountof basic annuity?

Yes. The maximumbasic annuity underany formula men-tioned cannot bemore than 80% ofthe high-3 averagesalary.

76 What happens tothe retirementdeductions takenduring service inexcess of that nec-essary to producethe maximumbasic annuity?

The retirementdeductions withheldafter the month inwhich the employeereaches this 80%limitation are setaside as a specialcredit when theemployee is separat-ed. This amounttogether with applic-able interest com-puted to the date ofretirement is appliedtoward any depositdue and any balanceis refunded. In theevent of death inservice, this amountis refundable as alump sum deathbenefit.

77 Is there an excep-tion to the 80%limitation?

Yes. Additionalannuity attributableto credit for unusedsick leave is allowableover and above thislimitation. Also,additional annuitycan be purchasedwith the excessretirement deduc-

tions describedabove instead ofaccepting the refund.

78 Can voluntary con-tributions furtherincrease annuity?

Yes, at retirement,each $100 in theaccount, includinginterest earned willprovide an additionalannuity of $7 a year,plus $.20 for eachfull year the employ-ee is over age 55 atretirement.

79 How are voluntarycontributionsmade?

Only CSRS employ-ees can make volun-tary contributions(provided they donot owe a deposit orredeposit for civilianservice). The deposit/redeposit had to havebeen made to theOPM prior to retire-ment. Contributionsare made in multi-ples of $25.

80 Can a refund ofvoluntary contri-butions be receivedinstead of addi-tional annuity?

Yes. The contribu-tions can be with-drawn with interestat any time beforereceiving an annuity

based on these con-tributions.

81 Are annuitiesadjusted afterretirement to takeaccount of increas-es in the cost of liv-ing?

Yes. Annuities areadjusted annually totake into accountincreases in the costof living.

82 What were theamounts of COLAreceived during thepast 5 years underCSRS?

12-1-11 . . . .3.6% 12-1-12 . . . .1.7% 12-1-13 . . . .1.5% 12-1-14 . . . .1.7% 12-1-15 . . . .None 12-1-16 . . . .0.3% 12-1-17 . . . .2.0%

83 How is your COLA computed if you retired inthis year?

You must be re-tired for the full year to receive thefull COLA. TheCOLA year goesfrom December 1through November30. If you retired in:

December FULL COLAJanuary 11/12February 10/12March 9/12

April 8/12May 7/12June 6/12July 5/12August 4/12September 3/12October 2/12November 1/12

84 May an annuitantbe employed out-side the FederalGovernment?

Yes.

85 May an annuitantbe reemployed inthe FederalGovernment?

Yes.

86 May an annuitantwho is reemployedin the FederalGovernment con-tinue to drawannuity?

Generally yes, butthe individual’ssalary is reduced bythe amount of annu-ity paid during theperiod of reemploy-ment. Reemployedannuitants in certaindifficult to fill posi-tions such as tempo-rary census workersare exempt from thesalary offset.

87 What kind of deathbenefits are there?

• A survivor annuitybenefit which ispayable in monthlyinstallments; or

• A lump sum benefitpayable if there is nosurvivor annuity pay -able. The lump sumwould consist of theamount paid into theRetirement Fund bythe employee plusap plicable interest, ifany.

88 What happens toannual leave that isadvanced at thebeginning of theyear?

If the employeeretires and has usedadvanced annualleave in excess ofwhat has beenearned, the retireemust pay the PostalService for all un earned annualleave.

OPM will processthe request as soonas possible, but beprepared to wait sev-eral weeks for formsto arrive. All meth-ods of notification toOPM will require thefollowing informa-tion: full name of thedeceased, date ofbirth, date of death,Social Security num-ber, CSA (claim)number, and thename and address ofthe person to whomOPM should sendclaim forms.

2. If annuity pay-ments have beensent directly to abank or other finan-cial institution,promptly notify thatinstitution of theannuitant’s date ofdeath. Ask that anypayments receivedafter the date ofdeath be returned tothe Treasury Depart-ment. Return anyuncashed annuitychecks to the returnaddress shown on theTreasury Depart-

HOW TO

CLAIM A

SURVIVOR

ANNUITY

89 What should a sur-vivor annuitant doto claim benefits?

Survivors must applyto receive benefits.They should also:

1. ImmediatelyNotify the U.S.office of PersonnelManagement,Retirement Opera-tions center, Boyers,Pennsylvania 16017.The NALC Retire-ment Departmentcan help with this(202) 393-4695; ORnotify OPM online atwww.serviceonline.opm.gov/RSR/AnnuitantDeath, by phone888-767-6738, or inwriting. OPM willsend the appropriateforms to apply forsurvivor benefits: SF 2800—Application for DeathBenefits (SurvivorAnnuity or Lump-Sum Payment). FE6— Claim forDeath benefits underFederal Employees’Group Life Insur-ance Program.(FEGLI).

ment’s envelope inwhich the check wasdelivered.

Returning uncash-ed checks to theTreasury departmentis necessary becausegovernment checksmade payable to adeceased personcannot be legallynegotiated by any-one, even the execu-tor or administratorof the person’sestate. Any unpaid accru-ed annuity due to thedeceased will be paidto the eligible sur-vivor after the properapplication has beenprocessed.

3. Obtain certi-fied copies of thedeath certificate toenclose with theapplication forms. Completing anapplication (SF2800) for survivorbenefits is necessaryso that OPM canauthorize payment ofall benefits to the eli-gible survivor(s). Benefits may alsoinclude automaticcontinuation ofhealth insurance cov-erage if the survivor:1) has been coveredby the annuitant’s

is over 18 and isincapable of self-sup-port because of aphysical or mentaldisability whichbegan before age 18,or an unmarriedchild who is a stu-dent between theages of 18 and 22may also be eligible.

94 Is a child’s sur-vivor annuitypayable in additionto the widow’sannuity?

Yes. Each eligiblechild who has a sur-viving parent whowas the spouse orformer spouse of thedeceased employee,will receive approxi-mately $510 permonth. Each eligiblechild who has nosurviving parent orwhose surviving par-ent was never mar-ried to the deceasedemployee will receiveapproximately $613per month. Theseamounts are reducedproportionately ifmore than three chil-dren are eligible forsurvivor annuities.The amount of childbenefits are periodi-cally increased bycost-of-living adjust-ments.

enrollment in one ofthe government’shealth benefits plans(FEHBP), and 2) thesurvivor is eligible toreceive a survivorannuity immediatelyafter the death of theannuitant. When applying forFEGLI life insurancebenefits, there is noneed for the eligiblesurvivor to contactFEGLI. They cannot settle a claimuntil a certification ofthe deceased annui-tant or employee’sinsurance status isreceived from theemployingagency/OPM.

90 To whom is a sur-vivor annuitypayable?

It may be payable tothe surviving spouse(widow or widower),and children of thedeceased employeeor deceased annui-tant, or to a formerspouse. It may alsobe payable to a per-son having an insur-able interest who wasnamed by theemployee at the timeof retirement.

91 What conditionsmust the deceased

employee have metto permit paymentof a survivor an nuity?

He/she must havecompleted at least 18months of civilianservice and, at thetime of death, musthave held a positionwhich was subject tothe CSRS .

92 What conditionsmust the widow or widower of a de ceased employeemeet to be eligiblefor survivor annuity?

A widow or widowermust have been mar-ried to the employeefor a total of 9months prior to theemployee’s death.The 9 monthrequirement doesnot apply if there is achild born of themarriage or theemployee’s death wasaccidental.

93 What conditionsmust a child of adeceased employeemeet to be eligiblefor a survivorannuity?

The child must beunmarried andunder age 18 or anunmarried child who

95 When a child’sannuity stops, isthe widow or widower’s annuityaffected?

No.

96 When does the sur-vivor annuity to awidow or widowerof a deceasedemployee begin?

The day after theemployee or annui-tant’s death.

97 How long will thewidow or widowercontinue to receivethe survivor annuity?

Until the end of themonth before the onein which the widowor widower dies orremarries before age55. Remar riage afterage 55 does not ter-minate the widow orwidower’s annuity.For remarriagesoccurring afterJanuary 1, 1995, ifthe widow/widowerremarries before age55, and was marriedat least 30 years tothe individual onwhose service thesurvivor annuity isbased, the survivorannuity will not beterminated.

98 How long will eachchild continue toreceive the sur-vivor’s annuity?

Until the unmarriedchild reaches age 18;or an unmarriedchild who is over 18but is incapable ofself-support becauseof a physical or men-tal disability whichbegan prior to age 18either becomes self-supporting, marriesor recovers from thedisability; or an un -mar ried child who isa student betweenages 18 and 22 ceases to be afull-time student.

99 If a child lost theirannuity because ofmarriage, can thebenefit be restoredif the marriage terminates?

Yes. The annuity andhealth insurance cov-erage can resumeupon the end of thechild’s marriage andcan continue untilage 22 for childrenwho are not married

and enrolled as stu-dents on a full-timebasis. If a child is un- married and incap -able of self-supportbecause of disabilitywhich began beforeage 18, benefits cancontinue for life.

100 Are survivor annuities paiddirectly to thechild/children?

Not usually. A child’sannuity is generallypaid to the survivingparent or legalguardian. However,an adult student maybe paid directly uponrequest.

102 What happens ifthe civil serviceannuitant marriesor remarries afterretirement?

If the annuitant mar-ries or remarries andwants to cover his/her new spouse for acivil service annuity,he/she must notify,within 2 years of themarriage, the U.S. Of -fice of Per sonnelManage ment, Retire -ment OperationsCen ter, Boyers,Pennsyl vania 16017,and furnish his/herCSA (claim) num-ber, So cial Se curity num ber, date ofbirth, and a copy ofthe marriage certifi-cate.

The retiree mustpay a deposit equalto the differencebetween the amountof annuity actuallypaid and the amountof annuity thatwould have beenpaid if the survivorelection had been in

effect continuouslysince date of retire-ment or date thereduction terminat-ed, whichever isapplicable. Thisdeposit, whichincludes interest, ispaid by a permanentactuarial reductionthat, in most cases, isless than 5% of theretiree’s annuity.

101 What happenswhen the civil service annuitant’sspouse predeceasesthe annuitant?

The annuitant canhave his/her annuityrestored to full-liferate. Members cancall the NALC Retire-ment Departmentfor assistance withthe necessary OPMnotification and pro-cedures. If there areno dependent chil-dren, health benefitscoverage can bechanged to a selfonly plan. The bene-ficiaries for life insur-ance may need to bechanged. Anotherchange which theannuitant may makeis a change in federalincome tax withhold-ing.

SURVIVOR PREDECEASES

ANNUITANT / ANNUITANT

MARRIES OR REMARRIES

REFUND—

REDEPOSIT

103 What is meant by arefund?

A refund is thereturn to an employ-ee of money tohis/her credit in theretirement fund.

104 Under what condi-tions is a refundpayable?

It is payable when anemployee is separat-ed from governmentservice and the sepa-ration takes place atleast 31 days beforethe beginning date ofany annuity forwhich he/she may beeligible.

105 May an employeewho is eligible toretire on an imme-diate annuitychoose to receive arefund rather thanan annuity?

No.

106 May a formeremployee who iseligible for deferredretirement be paida refund?

Yes. If a refund appli-cation is filed with

the U.S. Office ofPersonnelManagement, Re -tirement OperationsCenter, Boyers,Pennsylvania 16017at least 31 daysbefore annuity pay-ments are scheduledto begin.

107 If an employee whois eligible fordeferred retire-ment is paid arefund, may aredeposit of therefund be madelater so that theemployee mayreceive an annuityat age 62?

No. But if reem-ployed under CSRS,the employee couldacquire a new retire-ment right and makethe redeposit of therefund in order toreceive full credit forservice covered bythe refund.

108 If an employee isseparated beforereaching eligibilityfor retirement,may the money beleft in the retire-ment fund?

Yes. The employeedoes not have toapply for a refund.

109 Is there any advan-tage to leavingmoney in theretirement fund?

If the employee has 5 or more years ofcivilian service, he/she could receive adeferred annuity atage 62 by leaving themoney in the retire-ment fund. In dollarsreceived, the annuitycan potentially bemore valuable thanthe refund.

110 If a refund is notpaid at the time ofseparation, may itbe paid in thefuture?

Yes. Anytime prior to31 days before thebeginning date ofany annuity forwhich the employeeis eligible.

112 May the employingagency’s retire-ment contributionbe refunded?

No. The agency’scontributions aredeposited to theretirement fund in

111 What happens tomoney left in theretirement fund ifdeath occurs?

The money will berefunded as a lumpsum death benefit.

general and are notcredited to any indi-vidual employee.

113 How is applicationfor refund made?

Application must befiled on StandardForm 2802.

114 How are benefitspaid?

Payments authorizedby the Office ofPersonnelManagement areissued by the Treas -ury Department andpayable on the firstbusiness day of themonth after themonth or other peri-od for which theannuity has accrued.

115 May annuitychecks be negotiat-ed under Power ofAttorney?

No.

116 May annuity, re -funds, or lumpsum death pay-ments be attachedin order to settle ajudgment or otherin debtedness?

Such payments generally are notsubject to attach-ment, levy, gar -nishment or otherlegal process; how -ever, such pay-ments are subject to legal process toenforce child sup-port, alimony, or separate mainte-nance obligation orcommunity prop-erty settlement in connection withdivorce, annulmentor legal separation ofan annuitant.

117 Does this bar applyto indebtednessdue to the UnitedStates?

No. This is oneexception to the rule,and annuity pay-ments may be usedto settle a claimwhich the govern-ment may haveagainst an individual.

118 May an employeevoluntarily assignhis/her retirementdeductions assecurity for a loanor other purpose?

No.

119 May an employeeborrow from theretirement fund?

No.

HOW CSRS BENEFITS

ARE PAID /

CAN BENEFITS BE

ATTACHED

FEDERAL

INCOME

TAXES

POLITICS /

JURY DUTY /

DECLINATION

OF ANNUITY

120 Are annuity pay-ments subject tofederal incometaxes?

Yes. Under rules set forth and ad -ministered by theInternal RevenueService.

121 May an annuitanthave federalincome taxes with-held from annuitypayments?

Yes. Annuitants maycontact the Office ofPersonnel Man age -ment (OPM) tostart, stop or make

changes to tax with-holdings. Call OPMat 888-767-6738.

122 May an annuitantchoose not to haveincome tax with-held from annuitypayments?

Yes. The tax with-holding is entirelyvoluntary.

123 May an annuitantengage in politics?

Yes. An annuitant isnot an employeeand, therefore, is notgoverned by thepolitical activityrestriction applyingto employees.

124 If an annuitantserves on a jury,will his/her annuitybe affected?

No.

125 May a persondecline to accept allor part of the civilservice annuitythey are entitled toreceive?

Yes, if there is a per-sonal reason for suchaction.

126 How is this done?

By signing a waiverand filing it with theU.S. Office ofPersonnelManagement,RetirementOperations Center,Boyers, Pennsylvania16017.

127 What forms areused for filingapplication underCSRS?

• Standard Form 2800—Death Benefits;• Standard Form 2801—ImmediateRetirement;• Standard Form3112A—Applicant’sStatement of Disability3112B— Supervisor’sStatement3112C—Physician’sStatement 3112D—Agency Certifi -cation of Reassignmentand AccommodationEfforts 3112E—DisabilityRetirement ApplicationChecklist

FORMS

USED

UNDER

CSRS

Note: The SF 3112A,3112B, 3112C, 3112Dand 3112E should becompleted for Disabil -ity Retirement, in ad -di tion to the SF 2801,Application for Imme -diate Retirement.

• OPM Form 1496—Deferred Retirement; • Standard Form 2802—Refund of Retire -ment Deductions; • Standard Form 2803—Deposit or Rede -posit to cover previousservice;• Standard Form 2804—Voluntary contri-butions;• Standard Form 2808—Designation ofbeneficiary for accruedannuity due (payable in a lump sum);• Form FE-6—Claim for Death Benefits (Lifeinsurance).

128 Where may theseforms be secured?

The personnel officeof the employingagency or from theU.S. Office of Per -sonnel Manage-ment, RetirementOperations Center,Boyers, Pennsyl -vania 16017.

129 What recoursedoes an applicanthave if his/herclaim is denied?

The applicant mayexercise reconsidera-tion rights providedby the Office ofPersonnelManagement. Inmost cases followingan adverse final deci-sion by OPM, theapplicant will thenhave appeal rights tothe Merit SystemsProtection Board.

130 May an individualreceive a civil ser-vice annuity andSocial Securitybenefits at thesame time?

Yes, if qualified forboth benefits.

CSRS

AND

SOCIAL

SECURITY

131 What is SocialSecurity’s WindfallEliminationProvision (WEP)?

The WindfallElimination Provisionwas enacted in 1983as part of majoramendments to theSocial Security Actdesigned to shore upthe financing of theSocial Security pro-gram. It reduces theSocial Security benefitof most retirees whohave earned SocialSecurity throughemployment coveredby Social Security andalso receive a pensionbased on otheremployment that wasnot covered by SocialSecurity, such as workunder the CivilService RetirementSystem (CSRS). The reduction isdetermined by modi-fying one portion ofthe total SocialSecurity calculation asexplained below.

Social Security firstdetermines an individ-ual’s Average IndexedMonthly Earnings(AIME). This is a dol-lar amount reflectingaverage monthly earn-ings over the individ-ual’s work-life, witheach period indexedfor inflation. This dol-lar amount is dividedinto three tiers, called“bend points” bySocial Security. In2018, the first tier isthe portion of theAIME up to $895; thesecond tier is the por-tion of the AIMEfrom $895 to $5,397;and the third tier isthe amount above$5,397. (These tiers,or “bend points”, maychange each year withinflation). SocialSecurity multiplies thefirst tier by 90%, thesecond tier by 32%and the third tier by15%, and then addsthe resulting amounts,for the final monthlybenefit amount(called the PrimaryInsurance Amount –

PIA) payable at anindividual’s NormalRetirement Age(between 65 and 67,depending on year ofbirth). The WEP reducesthe calculation of thefirst tier (the first $895of the AIME) to 40%instead of the normal90%. Thus, a CSRSretiree’s entitlement toa Social Security ben-efit can be reduced asmuch as $448 amonth (in 2018) dueto the WEP. Thisequals an annualreduction of $5,376. Here is an exampleshowing how theWEP can affect aCSRS retiree with anAverage IndexedMonthly Earnings of$1,200:

Regular Social SecurityCalculation

90% x $895 = $ 805.50 32% x $305 = $ 97.60 15% x n/a = $ 0. $1,200 $ 903.10

Social Security Calculationwith WEP

40% x $895 = $ 358.00 32% x $305 = $ 97.60 15% x n/a = $ 0. $1,200 $ 455.60

However, CSRSretirees who havemore than 20 years of

Years of Substantial Earning Percentage 30 or more 90 percent 29 85 percent 28 80 percent 27 75 percent 26 70 percent 25 65 percent 24 60 percent 23 55 percent 22 50 percent 21 45 percent 20 or less 40 percent

Substantial Year Earnings 1937-54 $ 900 1955-58 $ 1,050 1959-65 $ 1,200 1966-67 $ 1,650 1968-71 $ 1,950 1972 $ 2,250 1973 $ 2,700 1974 $ 3,300 1975 $ 3,525 1976 $ 3,825 1977 $ 4,125 1978 $ 4,425 1979 $ 4,725 1980 $ 5,100 1981 $ 5,550 1982 $ 6,075 1983 $ 6,675 1984 $ 7,050 1985 $ 7,425 1986 $ 7,875 1987 $ 8,175 1988 $ 8,400 1989 $ 8,925 1990 $ 9,525 1991 $ 9,900 1992 $10,350 1993 $10,725 1994 $11,250 1995 $11,325 1996 $11,625 1997 $12,150 1998 $12,675 1999 $13,425 2000 $14,175 2001 $14,925 2002 $15,750 2003 $16,125 2004 $16,275 2005 $16,725 2006 $17,475 2007 $18,150 2008 $18,975 2009-2011 $19,800 2012 $20,475 2013 $21,075 2014 $21,750 2015-2016 $22,050 2017 $23,625 2018 $23,850

substantial earningsunder Social Securityin addition to theirPostal Service work,may mitigate, or eveneliminate, the WEPreduction. Here is anexplanation of howthis works: Social Securityestablishes the “sub-stantial” earningsamount for each year.It goes up with infla-tion each year. If aCSRS retiree has 21years of substantialearnings under SocialSecurity, the normalWEP reduction (from90% to 40% of thefirst tier of the AIME)is mitigated to 45% ofthe first tier of theAIME. If the CSRSretiree has 22 years ofsubstantial earnings,the WEP reduction ismitigated to 50% ofthe first tier of theAIME. If there are 23years of substantialearnings, the WEPreduction will be to55% of the first tier ofthe AIME. And so on,calculated at 5% eachyear, until there are 30years of substantialearnings, at whichpoint 90% is reachedand there is no WEPreduction.

Here are the SocialSecurity substantialearnings amounts foreach year beginning1951:

Individuals candetermine how manyyears of “substantialearnings” they have byaccessing their ownSocial Securityaccount online at:https://ssa.gov/myac-count/

132 What does 40 credits entitle youto un der SocialSecurity?

You are entitled to beenrolled in Medicareand draw a SocialSecurity monthlybenefit, subject tothe windfall elimina-tion provision.

133 Are the WindfallElimination Pro-vision and thePension Offset oneand the same?

No.

134 What is the Gov -ernment PensionOffset?

If you worked forfederal, state or localgovernment and werenot covered by SocialSecurity when youremployment ended,two-thirds of yourpension benefits fromthat employment willbe offset against anySocial Security bene-fit for which you areeligible as a spouse,widow, or widower.You can receive onlythe amount of SocialSecurity benefit thatexceeds two-thirds ofyour governmentpension. This fre-quently eliminatesSocial Security bene-fits altogether.

135 What is the ThriftSavings Plan(TSP)?

It is a retirement sav-ings plan similar toan Individual Retire -ment Account (IRA)or a private sector401(k) plan. Themoney employeescontribute to theTSP is tax-deferredin most cases. Thismeans that theydon’t have to paytaxes on it until it iswithdrawn duringretirement. However,the TSP offers a so-called Roth optionfor TSP contribu-tions (named afterthe Senator whosponsored thisoption into law).

This option allowsemployees to maketaxable contributionsto TSP and to with-draw the money tax-free when they retire.This option generallyonly makes sense toa small group ofemployees who

major component ofthe three tier FERSretirement package,CSRS employees canuse the TSP as a wayto save extra moneyfor the future and geta tax break today.CSRS employees donot receive agencymatching or auto-matic contributionsthat FERS employ-ees receive. However,the TSP investmentoptions, withdrawaland tax informationare the same for bothCSRS and FERSemployees.

139 What factors influ-ence how much anemployee canexpect to save andearn through theTSP?

The main factors arehow much theemployee earns inbasic pay, how muchhe or she con-tributes, how manyyears he or she con-tributes and the rateof return earned byTSP investments.

GENERAL INFORMATION

ON THE TSP

expect their incomeand taxes to be muchhigher during theirretirement years thantheir working years.Example: uniformedsoldiers in theArmed Forces.

136 Who can partici-pate in the ThriftSavings Plan?

All postal and otherfederal employeesmay participate.However, the rulesare different forCSRS and FERSemployees. In gener-al, the thrift plan ismore valuable toFERS employees.

137 Do employees haveto participate inthe Thrift SavingsPlan?

No.

138 How important isit for CSRS em -ployees to partici-pate in the ThriftSavings Plan?

While the TSP is a

140 If an employeealready has anIRA, can he or shestill participate inthe TSP?

Yes.

141 Can a TSP partici-pant roll his or herIRA into the ThriftSavings Plan?

Yes. Active or sepa-rated employees canroll over (transfer)money from a quali-fied retirement planor a traditional IRAinto their existingTSP account.However, separatedemployees cannotroll over money intotheir TSP account ifthey have alreadymade a full with-drawal of theiraccount or are receiv-ing monthly pay-ments.

142 Do employees whotransfer their TSPaccounts into IRAsupon separationfrom governmentservice pay taxeson their TSP savings?

No. TSP transfers toIRAs are not taxeduntil they are takenout of the IRAs.

143 What are the taxad vantages ofcontri buting tothe TSP?

Contributions to theTSP (non-Roth) arenot subject to federaland most stateincome taxes in theyear they are made,nor is the interestearned by anemployees’ TSPaccounts. TSP fundsare taxed only afterthey are withdrawn,usually at the time ofretirement when themarginal tax ratesfacing most taxpay-ers are lower. Contri -butions to the Roth“balances” in TSPaccounts are subjectto taxes.

144 How are fundswithdrawn fromthe TSP taxed?

It depends on themethod of with -drawal:

• Lump-sum andequal payment distri-butions of TSP fundsare treated like ordi-nary income andtaxed in the year(s)they are received.

• Annuities pur-chased by the ThriftInvestment Boardwith an employee’sTSP account aretaxed in the year(s)annuity payments arereceived.

• TSP savings trans-ferred to an IRA orother eligible planare not taxed untilthey are withdrawnfrom the IRA orplan.

145 When is there anearly withdrawalpenalty tax?

The IRS imposes a10 percent earlywithdrawal tax onamounts receivedfrom the TSP if theemployee separatesor retires before theyear in which theyreach age 55 andwithdraw their

THE TSP, IRAS AND TAXES

account in a singlepayment or a seriesof monthly pay-ments. In this case,the employee wouldbe subject to thepenalty tax on allamounts receivedbefore age 59 1/2(including financial

hardship in-servicewithdrawals).

However, the penaltytax does not apply toa series of monthlypayments based onlife expectancy, nor isit imposed on annu-ity payments, pay-ments made because

of death, or pay-ments made to par-ticipants who retireon disability.

146 How do employeesmake contribu-tions to the ThriftSavings Plan?

Contributions canonly be madethrough payrolldeductions. Thus,participants must bein a pay status (i.e.,receiving a paycheckfrom the government /Postal Service) tomake contributions.

148 What are “catch-up” contributions?

“Catch-up contribu-tions” are supple-mental tax-deferredemployee contribu-tions, which are inaddition to regularTSP contributions.The amount of sup-plemental contribu-tions one may con-tribute is $6,000.These contributionscan be made by par-ticipants age 50 orolder who would liketo make contribu-tions above the maxi-mum $18,500amount they couldotherwise make tothe TSP.

147 How much canemployees put intothe Thrift SavingsPlan?

Beginning in 2006there were no longerany percentage limitson employees contri-butions to the TSP.TSP contributionswill be limited onlyby the restrictionsimposed by theInternal RevenueCode.

The IRS annual elec-tive deferral limit for2018 is $18,500.

EMPLOYEE CONTRIBUTIONS

TO THE TSP

149 How are contribu-tions to the TSPinvested?

TSP savings areinvested in five dif-ferent investmentfunds, the G, C, F, Sand I Funds. Partici -pants may choosehow to allocate theirpayroll contributionsand fund balancesamong these fivefunds on their own,or they may allow theFederal Thrift Invest -ment Board to auto-matically managetheir investmentsamong the five fundsby selecting theLifecycle Fund or LFund option. Eachinvestment option isdescribed below:

• GovernmentSecuritiesInvestment (G)Fund. Contributions

Because catch-upcontributions aresupplemental, theydo not count againsteither the regularTSP contribution

(percentage) limits orthe IRS electivedeferral limit.However, the combi-nation of regular and

catch-up TSP contri-butions cannotexceed the total IRScontribution limit forthe year.

to the G Fund areinvested in specialshort-term U.S.Treasury securities.Treasury securities,which are essentiallyloans to the FederalGovernment, are thesafest investmentsavailable to TSP par-ticipants.

• Common StockIndex Investment(C) Fund. Fundcontributions areinvested in a repre-sentative sample (orindex) of all stockslisted on the majordomestic stockexchanges. Stocksare certificates ofownership in a com-pany which mayappreciate in valueover time and fre-quently pay periodic,variable paymentscalled dividends.

• Fixed IncomeIndex Investment(F) Fund.Contributions direct-ed to the F Fund areinvested in a repre-sentative sample ofU.S. government andcorporate bonds.Bonds are debt secu-rities, with maturitiesof between 10 and30 years, that usuallypay a fixed interestrate or coupon.Bonds may be tradedand frequently riseand fall in value inre sponse to changesin the economy and,to a lesser extent,corporate perfor-mance, interest ratesand the fortunes ofcompanies whichissue them.

• SmallCapitalizationStock IndexInvestment (S)Fund.Contributions to theS Fund are investedin the stocks ofsmaller companies(i.e., those not in -

TSP INVESTMENT OPTIONS

cluded in the S&P500), shares thatoften offer higherreturns but at muchgreater risk than thelarge company stocksof the C Fund.

• InternationalStock IndexInvestment (I)Fund. Retirementsavings invested inthe I Fund are usedto purchase shares incompanies activeoutside the UnitedStates—shares thatare subject to cur -rency risk as well asthe market and credit risk associatedwith the C Fund’sdomestic shares.

• Lifecycle (L)Fund. The L Fundsare “lifecycle funds”that are investedaccording to a pro-fessionally deter-mined mix of stocks,

bonds, and securi-ties. There are five LFund options, eachoffering a differentcombination ofinvestments in thefive basic TSP funds(G, C, F, S and I).The precise combi-nation is determinedby how many yearsparticipants are fromwithdrawing theirTSP funds. Overtime, the mix ofinvestments in the LFunds become moreconservative—morebonds and fewerstocks—as partici-pants get older.

150 Can an employeelose money invest-ing in the TSP?

Yes, it is possible,though all invest-ments carry risk.Investing in the GFund is consideredless risky, even in theshort-term. Otherfunds do involvesome risk, with apotential for higherrates of return.

151 Who manages theTSP’s investmentfunds?

The FederalRetirement ThriftInvestment Boardmanages the G Fundand the L Funds.The assets of the F,C, S, and I Fundsare managed by out-side investmentfirms.

participants withfund balances inboth traditional andRoth investmentscannot transfer fundsbetween such segre-gated funds. Roth-option TSP fundscan only be trans-ferred to other Roth-option TSP fundsand the same is truefor traditional TSPfunds.

154 How do TSP participantsrequest interfundtransfers?

The TSP Web site,www.tsp.gov and theThriftLine, 877-968-3778 are the mostefficient ways.Participants can alsosubmit an interfundtransfer request onForm TSP-50,InvestmentAllocation, and mailit to the TSP ServiceOffice.

155 When will myinterfund transferbe effective?

If you request aninterfund transfer onthe Web site or theThriftLine before12:00 noon, easterntime, your requestwill ordinarily beprocessed and postedto your account atthe close of businesson that day. Requestsmade after 12:00noon, eastern time,will ordinarily beprocessed and postedto your account atthe close of businesson the followingbusiness day. If youuse Form TSP-50,your request willgenerally be proc -essed and posted toyour account withinfive business days ofthe day it is receivedby the TSP.

152 What is a TSPinterfund transfer?

An interfund transferis the movement ofpast TSP contribu-tions from one in -vest ment fund toanother (e.g., fromthe G Fund to the FFund). TSP partici-pants may make twointerfund transfersper month. However,participants maytransfer Funds intothe “safe” G Fund atany time, even if theyhave already madetwo interfund trans-fers during the samecalendar month.

153 Are there restric-tions on what con-tributions andearnings anemployee maytransfer?

There are generallyno restrictions onInterfund transferswithin traditional(tax-deferred) TSPaccounts. However,

TSP INTERFUND TRANSFERS

GETTING FUNDS OUT

OF THE TSP

156 Can a TSP partici-pant withdraw themoney in his or herTSP account whilestill employed bythe Postal Serviceor other govern-ment agency?

Yes, employees whoare facing hardshipsituations or whoreach age 591/2 andwant to makeaccount withdrawalsfor any reason maynow do so.

In-service with-drawals before age591/2 will be subjectto the 10 percentearly withdrawalpenalty tax (whichdoes not apply tothose making age-based withdrawals).Both forms of with-drawals will be tax-able income in theyear in which pay-ment is made, andmay be subject to themandatory 20 per-cent federal incometax withholdingunless rolled overinto an IRA.

157 Can a TSP partici-pant who separatesfrom the USPS orother federalagency leave his orher savings in theTSP?

Yes. After leaving theservice, the entireaccount balance canbe left in the TSPuntil April 1 of thecalendar year afterthe participantreaches age 701/2, orin which the partici-pant retires if work-ing beyond that age.If you do not with-draw (or begin with-drawing) youraccount balance bythe required dead-line, your accountbalance will be for-feited to the TSP. Youcan reclaim youraccount; howeveryou will not receiveearnings on youraccount from thetime the account wasforfeited.

158 May an employeecontinue to makecontributions tothe TSP after sepa-rating from thePostal Service orother federalagency?

No. Although theywill continue toreceive TSP partici-pant statements andcontinue to have theright to shift theirsavings among theTSP’s investmentfunds, separatedemployees may notmake additional con-tributions to the TSP.Their accounts willcontinue to accrueearnings as long astheir savings remainin the TSP.

159 What are the basicTSP withdrawaloptions?

• Transfer his or hervested account bal-ance to an IndividualRetirement Account(IRA) or other eligi-ble retirement plan;or• Receive his or heraccount balance in alump-sum payment;or• Receive his or heraccount balance insubstantially equalpayments over a

the same withdrawaloptions as thosedescribed in theanswer to question159.

161 If an employeechooses to with-draw his or herfunds from the TSPby means of a lifeannuity, how manydifferent types ofannuities are avail-able?

The TSP offers dif-ferent types of annu-ities, which fall intothree major cate-gories:

• Single Life annu-ities, payable as longas the participantlives. Variations with-in this type of annu-ity include those withcost-of-living adjust-ments, cash refundoptions and featureswhich guarantee thedistribution of theparticipant’s TSPaccount balanceswithin 10 years.

• Joint Life withSpouse annuities,payable as long asthe participant andhis or her spouselives. Variations with-in this type of annu-ity include those withcost-of-living adjust-

ments, cash refundoptions and varyinglevels of survivorannuities.

• Joint Life with OtherSurvivor annuities,payable as long asthe participant and anamed person withan insurable interestlives.

Variations within thistype of annuityinclude those withcash refund optionsand varying levels ofsurvivor annuities.

Additional informa-tion is available in abooklet entitled“Summary of theThrift Savings Plan,’’January 2018 editionavailable online atwww.tsp.gov or bycalling the NALCRetirement Depart- ment.

162 How does anemployee apply towithdraw his orher savings fromthe TSP?

Upon separation, thePostal Service (orother federal agency)is required to furnishthe employee a TSPWithdrawal Packagewith the requiredforms.

fixed period of timeor in a fixed amountuntil the account isdepleted; or• Receive a life annu-ity based on theamount in his or heraccount. The TSP Modern-ization Act of 2017, a law signed by thepresident on 11/17/2017, provides TSPparticipants withmore flexible with-drawal options. Iteliminates the prohi-bition on multiplepostseparation with-drawals and multipleage-based withdrawalswhile still working. The law gives theFederal RetirementThrift InvestmentBoard up to twoyears to make theregulatory and opera-tional changes neces-sary to enact thechanges in the law. In the meantime,all of the old with-drawal and other pro-visions will continueto apply.

160 May an employeewho qualifies forFERS or CSRS dis-ability benefitswithdraw his orher TSP savings?

Yes. He or she has

entitled “Loans”which is availableonline atwww.tsp.gov.

164 How much can anemployee borrowfrom his or herTSP account?

Loan amounts arelimited to the valueof the employee’sown contributionsthough not allemployees may beable to borrow themaximum, giventheir salary and abili-ty to repay loans on atimely basis. Theminimum loanamount is $1,000.Participants mayhave one outstand -ing loan for generalpurposes and oneresidential loan at atime.

165 What are the termsof TSP loans?

Prepayment in full ispermitted by certi-fied check, moneyorder or cashier’scheck. Otherwise,employees repayloans against theiraccounts throughpayroll deductionsand must pay inter-est. The term of theloan is set in theapplication and therate of interestcharged is the rate ofreturn earned by theG Fund during themonth in which theloan application isreceived by the TSPService Office.Employees who sep-arate from govern-ment service mustrepay their loans infull in order toprocess any with-drawal request.

163 Can an employeeborrow from his orher TSP account?

Yes, there are twotypes of loans—ageneral purpose loanand a loan for thepurchase of your pri-mary residence. Youcan apply for a gen-eral purpose loanwith a repaymentperiod of 1 to 5years, or you canapply for a residen-tial loan with arepayment period of1 to 15 years. Nodocumentation isrequired for a generalpurpose loan, butyou must submitdocumentation (suchas a contract for thepurchase of your res-idence) to supportthe amount you arerequesting for a resi-dential loan. Infor -ma tion about theTSP loans is pro -vided by a booklet

THETSP LOAN PROGRAM

• TSP accounts maybe used to enforceTSP participants’legal obligations toprovide alimony and/or child support pay-ments.

• The former spousesof TSP participantsmust be notifiedwhen participantswho leave federalservice prior tobecoming eligible forretirement benefitstransfer their TSPaccounts to an IRAor other pensionplan.

168 Who gets anemployee’s TSPfunds if he or sheshould die beforereceiving any TSPpayments?

The person identi-fied by the employeeas the beneficiary ofhis or her account onForm TSP-3, theDesignation ofBeneficiary form. Ifno beneficiary isnamed, the account

will be distributedaccording to thestandard order ofprecedence.

169 Who gets anemployee’s TSPannuity if he or sheshould die afterretirement?

In the event of deathafter the TSP officereceives a completedannuity request, ben-efits will be providedin accordance withthe former employ-ee’s annuity selec-tion.

166 What rights dospouses of partici-pants have withregard to the TSP?

Spouses have certainrights when partici-pants apply to bor-row from theiraccounts or with-draw funds from theTSP. The spouses ofTSP participants cov-ered by CSRS will benotified when partic-ipants apply for aTSP loan or apply towithdraw from theirTSP accounts.

167 What rights do for-mer spouses ofparticipants havewith regard to theTSP?

• TSP participantsmay not make anydecision with regardto their accountswhich conflict withan applicable courtorder, decree, orcourt-approvedagreement obtainedby their formerspouses.

SPOUSAL RIGHTS AND TSP

SAVINGS IN CASES OF DEATH

Those who retiredafter December 31,1989 and are underage 65 pay for thebasic life insuranceuntil they reach 65.

• They may also elect to have the amount only reduce by 1%per month at age 65to no less than 50%of the basic policyvalue—

THE EXTRA PRE-MIUM FOR THISLESSER REDUC-TION COVERAGEIS $0.71 PERMONTH FOREACH $1,000 OFBASIC INSUR-ANCE PAYABLEFROM THE COM-MENCING DATEOF ANNUITYUNTIL DEATH.

• Thirdly, they mayelect that the amountof basic insurancewill not reduce afterage 65.

THE EXTRA PREMIUM RE -QUIRED FOR NOREDUCTION INBASIC INSUR-ANCE COVERAGEIS $2.13 PERMONTH FOREACH $1,000 OFBASIC INSUR-ANCE PAYABLE

ance. When theemployee retireshe/she must pay forbasic life insurancecover age until age 65at the monthly rateof $0.325 per thou-sand dollars of cover -age. At that timethere are no fur therpayments and thebasic coverage beginsto reduce by 2% permonth until it reach-es 25% of the facevalue, payable uponthe retiree’s death.

172 What other op -tions are availablefor continuingbasic life insur-ance coverage?

There are 3 choices aretiree may make:

• A retiree may electto continue underthe old systemwhereby a reductionof 2% per month inthe basic life insur-ance policy valuebegins at age 65 anddeclines to 25% ofthe basic value —nocost to retirees whoretired beforeJanuary 1, 1990.

FEDERAL EMPLOYEES

GROUP LIFE INSURANCE

AND HEALTH BENEFITS

COVERAGE

170 May an employeekeep the basic cov -erage of FederalEmployees’ GroupLife Insurance af -ter retirement?

Yes. The employeemust have been en -rolled in the basiccoverage for the 5years immediatelypreceding retire mentor the full period orperiods of serviceduring which thebasic life insurancewas available to theem ployee, if less than5 years. On and af terDecember 9, 1980those who re tiremust make a writtenelection as to theamount of theirpost-retire ment basiclife insurance cover-age they want toretain after age 65,on a form obtainedat the employing of -fice.

171 What is the cost of basic life insurance?

As an active employ-ee, the USPS paysfor basic life insur -

FROM THE COM-MENCING DATEOF ANNUITYUNTIL DEATH.

If a retiree decides tocancel the increasedpost -retirement cov-erage, the amount ofbasic coverage wouldbe reduced to 25%of face value.

173 May an employeekeep the standardoptional life insur-ance after retire-ment?

Yes. You may alsoretain your cover-age if you are eligi-ble to continue thebasic insurance andif, in addition, youhave also had thestandard optionalcoverage in force fornot less than the fullperiod or periods ofservice during whichthe coverage wasavailable to you orthe 5 years of serviceimmediately preced-ing your retirement.YOU MUST PAYFOR THIS INSUR-ANCE UNTIL YOUREACH AGE 65 atwhich time the cov-erage will reduce by2% per month untilit reaches 25% of theface value ($2,500).

174 May an employeekeep the addi-tional optional orfamily optional life insurance afterretirement?

Yes. This coveragemay be retained ifyou are eligible tocontinue the basicinsurance and if, inaddition, you havealso had the life in -surance in force fornot less than the fullperiod or periods ofservice during whichit was available toyou or the 5 years ofservice immedi atelypreceding yourretirement. YOUMUST PAY FORTHIS INSUR-ANCE UNTIL YOUREACH AGE 65 atwhich time the cov-erage will reduce by2% per month for 50months, at whichtime the coverageceases. Employeesseparating for retire-ment on or afterApril 24, 1999 canelect to continuethese coverages onan unreduced basisby paying premiumspast age 65.

175 What are livingbenefits?

Effective July 25,1995, you may electto receive a lump-sum payment (livingbenefits) if you areterminally ill andhave a documentedmedical prognosisthat your lifeexpectancy is 9months or less. Theform for electing liv-ing benefits (FE-8) isonly available fromthe Office of FederalEmployees’ GroupLife Insurance (800-633-4542).

176 May an employeekeep his/her healthbenefits coverageafter retirement?

Yes. If retiring on an immediate an -nuity and if you have been continu-ously en rolled un-der the program (or covered as a family member)since the first op -portunity to enroll,or for the 5 years ofservice im mediatelypreceding retire-ment.

eligible for TRI-CARE and CHAM-PVA coverage cansuspend the FEHBPcoverage and laterreturn to theFEHBP if TRI-CARE or CHAMP-VA coverage is termi-nated.

178 If an employeedies, may his/hersurvivors continuehealth benefits coverage?

If there is a survivorannuity payable andif the survivor hasbeen covered as adependent on yourFEHBP while youwere living, the cov-erage will continueand the premium willbe de duct ed from thecivil service survivorannuity.

177 If a retiree cancelsthe Federal Em -ployees HealthBenefit Programcov erage, canhe/she reenroll at alater date?

No. Once a retireecancels health cover-age under theFEHBP, it can neverbe reinstated.However, formermilitary members

WHAT AN ANNUITANT

SHOULD DO IN THE EVENT OF

DIVORCE/DEATH OF SPOUSE

179 What should theannuitant do if theperson chosen as asurvivor annuitantpredeceaseshim/her or themarriage is termi-nated by divorce orannulment?

Write to: U.S. Office of Person-nel Management,Retirement Opera -tions Center, Boyers, Pennsyl vania16017, requesting theannuity be re-stored to the full liferate. Be sure to signthe letter and giveyour CSA (claim)number. If there are

180 What should anannuitant do if afamily memberdies who is cov-ered by his/herfamily optional lifeinsurance?

Write to: U.S. Officeof Personnel Man -age ment, RetirementOperations Center,Boyers, Pennsyl vania16017, requestingFE-6 DEP to claim death benefits. Besure to give yourfull name, CSA(claim) number,Social Security number, and date of birth. Send a copy of the deathcertificate when youreturn the com-pleted FE-6 DEP to OPM.

no other eligibledependents you may request tochange the healthcoverage to self only.