Embed Size (px)

Citation preview

Brand South Africa Annual Report 2012 2013

Nation Brand PerformanceOver the past 15 years the concept of managing the reputation of Nation Brands has emerged as a global trend. One of the primary reasons for this is that nation branding is able to provide a competitive advantage in an increasingly competitive world that is striving to attract investment, tourism, events and skills and to drive exports.

“The overall reputation of a nation brand has to be measured, managed and infl uenced by a partnership between tourism, culture, government, business and civil society” says nation branding pioneer Simon Anholt.

A useful model is the Anholt-GfK Nation Branding Hexagon, which describe the elements that make up a nations brand and provides a thorough assessment of a country's standing, making it one of the most eff ective tools available for managing a country's reputation around the world.

Investment Potential and attractiveness to outsiders

Level of satisfactionwith country's productsand services

Competency fairgovernance, human rights, international

contribution

Potentialattractiveness and

economicalcontribution

Commercial and culturalProducts and sporting prowess

Tourism

Investment &

Immigration

Governance People

Culture & Heritage

Exports

Nation Brand Hexagon

Building nation brands, including brand South Africa, is a long journey which requires a consistent and coordinated eff ort. The South African nation brand must be built through consistent communications and reputation management both domestically and internationally. A nation brand has major impact if all stakeholders work together around a single, visionary national reputational strategy.

South Africa’s national strategy was driven and monitored through the Offi ce of the Presidency, and the Nation Brand Strategy formed an integral part of this plan. Nation branding to increase

“The overall reputation of a nation brand has to be measured, managed and infl uenced by a partnership between tourism, culture, government, business and civil society,” Simon Anholt.

21

22 Brand South Africa Annual Report 2012 2013

global competitiveness can make a vital contribution to the goals of the South African Planning Commission, which is located in the Presidency. South Africa’s value-proposition and positioning must refl ect the country’s Vision 2030: and so the benefi ts of a close connection are evident.

International research shows that in countries with the most dynamic global rankings, the President is the key ‘brand champion’ who leads and personifi es the positioning of the country. For example, in Brazil, USA, UK, and Tunisia’s branding eff orts are all led by the Presidency, - apart from the UK who has a monarchy and not a President - whether through an organisation like Brand South Africa or by the Presidents and their ministers.

The President has the most infl uence over the content and tone of those speaking and writing about the country, and creating consistency in messaging by the President. The Presidency strengthens a nation’s brand standing within the global community.

In an early paper on nation branding in 1998, “Nation Brands of the Twenty-First Century” Anholt pointed out that a country’s image and reputation are acquired as a result of the things governments, business and the people do and how they are perceived, but generally they evolve slowly over time – unless there was a dynamic intervention or defi ning moments (which serve as accelerators) occur.

South Africa has had various defi ning moments which have propelled the brand forward in a hugely positive manner. Some notable ones were the country’s peaceful transition to democracy and the successful hosting of the soccer world cup in 2010. South Africa’s recent rise to the BRICS grouping of countries is undeniably the next defi ning moment, in the country’s journey, to becoming one of the strongest nation brands globally.

The same holds true for the fourth and highly successful municipal elections (2011), which refl ected the maturing of South Africa’s democracy and a broadly inclusive and participatory electoral process. From a brand building perspective these achievements are critical milestones and defi ning moments, as they refl ect the country’s forward movement, to being a successful country brand.

In reality, Brand South Africa ’belongs’ to all citizens of South Africa, and they are the true custodians of the brand, and Brand South Africa’s role is to Coordinate, Articulate, Enable and Inspire, creating a voluntary franchise. However, Brand South Africa does not have line authority to enforce compliance with the brand framework, and requires the support of the Offi ce of the Presidency to ensure traction for the nation

branding eff ort. For this reason the championing of nation brand building eff orts from the centre and the top, is imperative for eff ective and impactful brand building, both domestically and internationally.

Aligned to this, is the need for coordination between all the diff erent role players: government, business and civil society organs.

An analysis of the research

South Africa: A top developing and globally competitive nation.

Brand South Africa worked hard to improve South Africa’s global reputation, and to position the country as an investment destination of choice and trade partner. The emphasis throughout is on South Africa being open to new global business.

In a year when South Africa hosted, for the fi rst time on the African continent, the annual BRICS Summit, the theme of the fi fth BRICS Summit refl ected changes taking place in the global political economy. In this report we bring together several pieces of analysis, published in the year under review, of country performance Brand South Africa developed to understand country competitiveness in rapidly changing global environment. We also identifi ed the key strengths unique to the South African economy. These indicators highlight that South Africa has unique competitive strengths in the context of the developing world. The broader context of South Africa’s inclusion into the BRICS formation, as well as South Africa’s competitiveness performance compared to other developing nations, shape the approach taken to the research presented in this report.

Highlights include the World Economic Forum’s competitiveness report that ranks South Africa 15th globally for Quality of Air Transport Infrastructure, while the country’s fi nancial services sector, banks and stock exchange are top global performers. In addition South Africa, compared to the BRICS grouping of nations, came fi rst in fi ve of the ten criteria the World Bank uses to assess ease of doing business, namely starting a business, dealing with construction permits, getting credit, protecting investors, and paying taxes. This means that South Africa off ers protection to direct foreign investments, and is certainly a business friendly environment in which new trade, investment, and related economic interactions are fostered. As South Africa heads towards the milestone of 20 years of democracy, it is important to assess the road travelled, and to understand the position the country occupies globally, as a developing nation in the early 21st century.

Brand South Africa’s research tracks a wide variety of competitiveness, reputation, and related global studies and indices. The goal is to monitor

Brand South Africa Annual Report 2012 2013 23

and evaluate overall country performance in a highly competitive and uncertain global economy. These third party information sources are then supplemented by Brand South Africa commissioned research projects, and subscriptions to domestic research vehicles. In order to further deliver on research insights, Brand South Africa convenes Research Reference Groups that refl ect on, and provide Brand South Africa with expert input and advice on key issues of concern at the time.

In this Report we refl ect on the key fi ndings from research conducted by Brand South Africa in the past year. Signifi cant fi ndings include an analysis of indicators showing that South Africa is a top performing globally competitive developing nation. This is important in the context of the country’s membership of the BRICS grouping, as well as macro-economic changes taking place in the world system. Hence the specifi c focus on developing a comparative understanding of how South Africa performs in terms of competitiveness in relation to fellow developing nations.

The competitive strengths, together with indicators on international investor perceptions of the country, can be viewed as an inspiration to indicate the strengths in the national economy. These become building blocks of excellence for the realisation of the Vision 2030 in the National Development Plan, whilst at the same time contributing positively to enhancing South Africa’s reputation globally.

But, why is this important? In this report we highlight Brand South Africa research regarding country performance in a broad range of competitiveness, doing business, governance, and reputation indicators. In this regard the analysis of the country’s reputation and competitiveness has to be seen in the context of larger patterns of change unfolding in the global political economy.

The 2013 United Nations Development Programme, Human Development Report, contains powerful insights regarding the increasingly important role developing countries, such as South Africa, are playing in the 21st century. The UNDP indicated that the South (developing nations and emerging markets) currently produced half the world’s economic output. In 1990 these countries contributed only about a third of world economic output. To further illustrate the signifi cant shift in the global economic balance of power, the UNDP claimed that the combined GDP of eight developing countries: Argentina, Brazil, China, India, Indonesia, Mexico, South Africa and Turkey matched the GDP of the United States. The UNDP implied that countries such as Brazil, South Africa, India and China, have become major drivers of the global economy and are forces for change in the developing world. It is pertinent to understand how South Africa is

positioned within this rapidly changing global economy and by the implication of its geopolitical environment.

This report brings together a range of competitiveness and human development indicators which are used to benchmark South Africa’s strengths, in relation to fellow BRICS and other promising developing nations, broadly referred to as the Next11. What emerges is a pattern of each country’s performance, indicating that South Africa matches and outperforms other peer developing countries in critical areas of national competency. These are important indicators to use in positioning South Africa as a reliable trade partner, and attractive investment destination.

We also refl ect on fi ndings from an annual international investor perception study commissioned by Brand South Africa, as well as the fi ndings from the annual Anholt Gfk-Roper Nation Brand Index (NBI). The NBI studies the global reputation of a select group of 50 nations. South Africa’s performance in the NBI, together with fi ndings from the investor perception study, should provide high-level insights into the overall perception of South Africa.

Competitiveness and related Human Development indicators

In a rapidly changing global economic and geopolitical environment, competition for FDI, trade opportunities, and related business activity increased. The sections below present some highlights and comparisons between South Africa, the BRICS nations, and the Next11 group of developing nations.

As indicated below, South Africa performed well in comparison to other developing nations. This implies that South Africans can have confi dence in their capabilities, skill, and knowledge necessary to improve the country’s overall global competitiveness, create jobs, and realise human and skills development goals in the future.

World Economic Forum - Global Competitiveness Report 2012/13

Top issues emerging from the World Economic Forum’s Competitiveness Report indicate that South Africa compares quite well with fellow developing nations and emerging markets. South Africa’s strengths in the 2012/13 report include globally leading performance in:

Legal Rights Index (1st)

Regulation of Securities Exchanges (1st)

Effi cacy of Corporate Boards (1st)

24 Brand South Africa Annual Report 2012 2013

Strength of Auditing and Reporting Standards (1st)

Availability of Financial Services (2nd)

Financing through local equity market (3rd).

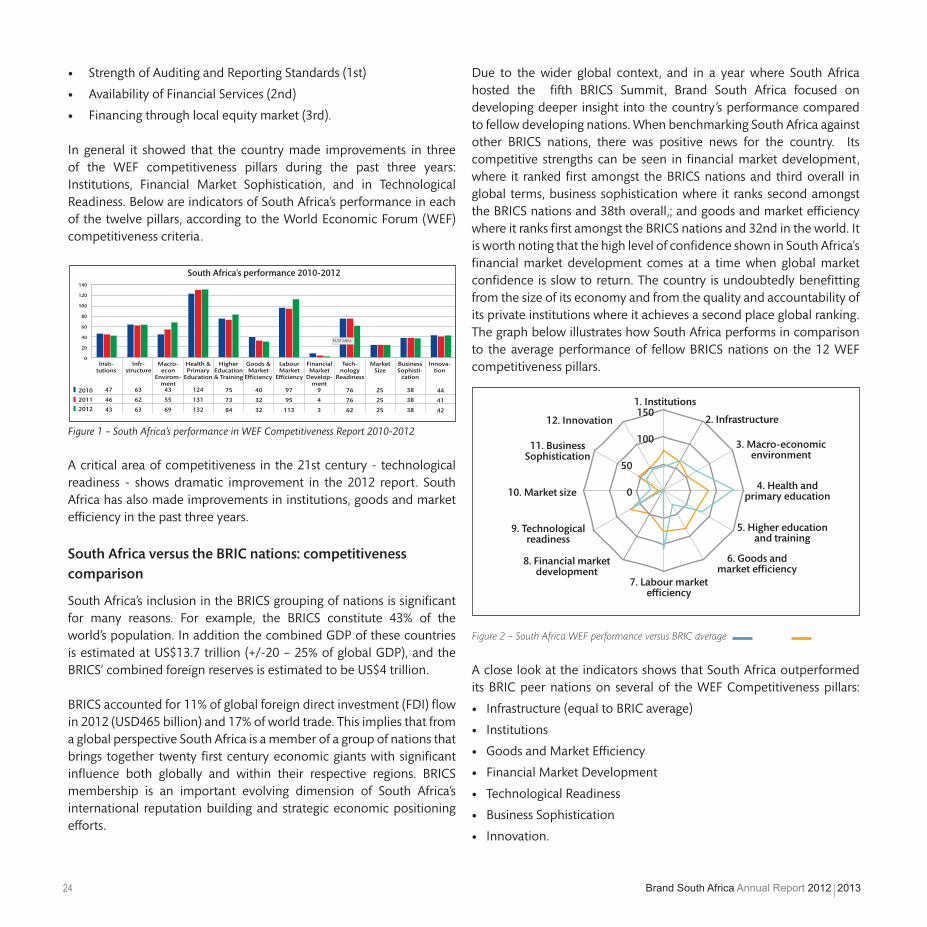

In general it showed that the country made improvements in three of the WEF competitiveness pillars during the past three years: Institutions, Financial Market Sophistication, and in Technological Readiness. Below are indicators of South Africa’s performance in each of the twelve pillars, according to the World Economic Forum (WEF) competitiveness criteria.

South Africa's performance 2010-2012140

120

100

80

60

40

20

0Insti-

tutionsInfr-

structureMacro-

econEnvirom-

ment

Health &Primary

Education

HigherEducation& Training

Goods &Market

Effi ciency

LabourMarket

Effi ciency

FinancialMarket

Develop-ment

Tech-nology

Readiness

MarketSize

BusinessSophisti-

cation

Innova-tion

2010

2011

2012

47

46

43

63

62

63

43

55

69

75

73

84

124

131

132

40

32

32

97

95

113

9

4

3

76

76

62

25

25

25

38

38

38

44

41

42

PLOT AREA

Figure 1 – South Africa’s performance in WEF Competitiveness Report 2010-2012

A critical area of competitiveness in the 21st century - technological readiness - shows dramatic improvement in the 2012 report. South Africa has also made improvements in institutions, goods and market effi ciency in the past three years.

South Africa versus the BRIC nations: competitiveness comparison

South Africa’s inclusion in the BRICS grouping of nations is signifi cant for many reasons. For example, the BRICS constitute 43% of the world’s population. In addition the combined GDP of these countries is estimated at US$13.7 trillion (+/-20 – 25% of global GDP), and the BRICS’ combined foreign reserves is estimated to be US$4 trillion.

BRICS accounted for 11% of global foreign direct investment (FDI) fl ow in 2012 (USD465 billion) and 17% of world trade. This implies that from a global perspective South Africa is a member of a group of nations that brings together twenty fi rst century economic giants with signifi cant infl uence both globally and within their respective regions. BRICS membership is an important evolving dimension of South Africa’s international reputation building and strategic economic positioning eff orts.

Due to the wider global context, and in a year where South Africa hosted the fi fth BRICS Summit, Brand South Africa focused on developing deeper insight into the country’s performance compared to fellow developing nations. When benchmarking South Africa against other BRICS nations, there was positive news for the country. Its competitive strengths can be seen in fi nancial market development, where it ranked fi rst amongst the BRICS nations and third overall in global terms, business sophistication where it ranks second amongst the BRICS nations and 38th overall,; and goods and market effi ciency where it ranks fi rst amongst the BRICS nations and 32nd in the world. It is worth noting that the high level of confi dence shown in South Africa's fi nancial market development comes at a time when global market confi dence is slow to return. The country is undoubtedly benefi tting from the size of its economy and from the quality and accountability of its private institutions where it achieves a second place global ranking. The graph below illustrates how South Africa performs in comparison to the average performance of fellow BRICS nations on the 12 WEF competitiveness pillars.

1. Institutions

2. Infrastructure

3. Macro-economicenvironment

4. Health and primary education

5. Higher educationand training

6. Goods and market effi ciency

7. Labour marketeffi ciency

8. Financial marketdevelopment

9. Technologicalreadiness

11. Business Sophistication

10. Market size

12. Innovation150

100

50

0

Figure 2 – South Africa WEF performance versus BRIC average

A close look at the indicators shows that South Africa outperformed its BRIC peer nations on several of the WEF Competitiveness pillars:

Infrastructure (equal to BRIC average)

Institutions

Goods and Market Effi ciency

Financial Market Development

Technological Readiness

Business Sophistication

Innovation.

Brand South Africa Annual Report 2012 2013 25

This clearly established South Africa as a competitive developing nation among the BRICS grouping. South Africa was a natural choice for inclusion in the BRICS when it comes to competitiveness.

South Africa - Next11 Comparison

In a similar comparison with Next11 nations, further insights emerge. A comparison between South Africa and the Next11’s average performance for each pillar indicated that South Africa has tremendous competitive advantages over the Next11 nations.

The Next11 group of nations include other developing nations, and emerging markets that have signifi cant roles to play in their respective regions, as well as in the emerging global economic reality. It is interesting to track the overall competitiveness scores for this group of countries. As the indicators in the graph below shows, if South Africa was part of this group, it would have been a top fi ve competitive nation.

South Africa vs. Next 11 - Country Score Comparison

South Africa Bangladesh Egypt Indonesia Iran Mexico Nigeria Pakistan Maldives Turkey South Korea Malaysia

52 120 107 50 64 53 115 124 65 41 19 75

140

120

100

80

60

40

20

0

2012

52

118

107

50

64

53

115

124

65

41

19

75

Figure 3 – Next11 and South Africa overall rankings in the WEF Competitiveness Report 2012/13

In terms of overall ranking, South Africa is located in the top fi ve among the Next11 group of developing nations. This shows that South Africa can confi dently say that it is a top fi ve globally competitive developing nation. Fig. 4 illustrates South Africa’s competitive strengths per WEF competitiveness pillar compared to the average performance of the Next11 nations.

1. Institutions

2. Infrastructure

3. Macro-economicenvironment

4. Health and primary education

5. Higher educationand training

6. Goods and market effi ciency

7. Labour marketeffi ciency

8. Financial marketdevelopment

9. Technologicalreadiness

11. Business Sophistication

10. Market size

12. Innovation

South Africa vs. Next 11

140

120

100

80

60

40

20

0

South Africa Next 11 (Average)

Figure 4 – South Africa WEF performance versus. Next 11 average

The above indicators show that South Africa outperforms the Next11 on the following seven pillars:

Institutions

Infrastructure

Goods and market effi ciency

Financial market development

Technological readiness

Business readiness

Innovation.

In addition, South Africa equals the Next11’s average on the following two pillars:

Higher education and training

Market size.

The above demonstrates South Africa’s competitiveness in 9 of the 12 pillars, in comparison to the Next11, which is indicative of a top fi ve developing nation.

26 Brand South Africa Annual Report 2012 2013

Institute for Management Development (IMD) Global Competitiveness Report 2012/13

According to the IMD 2012/13, South Africa improved its overall ranking and performance from number 52 in 2011, to 50 in 2012. The IMD assessed competitiveness since 1989, and provided long term measured assessments of the performance of 59 countries, according to 329 criteria.

In terms of South Africa’s overall performance in the 2012 IMD report, the country has improved its ranking in:

Government effi ciency 29 (up from 32 in 2011)

Business effi ciency 37 (up from 40 in 2011)

Infrastructure 54 (up from 56 in 2011)

Economic performance 57 (down from 54 in 2011).

From the WEF and IMD reports we learn that South Africa has been advancing slowly on institution and government effi ciency. These competitiveness indicators show that South Africa compares well with other BRICS, and various developing nations. The comments below relate to a comparison between South Africa and the BRICS, on the twelve pillars of competitiveness, the World Economic Forum used to assess a nation’s overall competitiveness.

The identifi ed economic performance strengths of South Africa according to the IMD report are:

Cost-of-living index (ranked 7)

Terms of trade index (ranked 9)

Resilience of the economy to the economy (ranked 26)

Tourism receipts (2,5% of GDP)

Direct investment stock abroad (ranked 29)

The weaknesses, as identifi ed by the IMD report, are the unemployment rate, direct investment fl ows abroad, GDP per capita, and relocation services. However, these are not seen as threats to the future of the economy by the IMD, but relate more to cyclical market trends and prevailing conditions in the global economy.

The Ibrahim Index of African Governance (IIAG)

Governance is a key issue that results in political, economic and socio-political debate and activity on the African continent. South Africa performed well in the IIAG, which is based on the concept that

all citizens of African states have a right to access social services. It measured the governance performance of African states according to eighteen criteria. South Africa came fi fth in its overall performance in the IIAG in 2012.

South Africa ranked in the top fi ve for the following criteria:

1st – Public Management

2nd – Gender

3rd – Rule of Law

3rd – Participation and Human Rights

4th – Welfare

5th – Education

5th – Accountability

5th – Participation

World Bank’s Ease of Doing Business Index (DBI)

South Africa’s overall ranking in the 2013 World Bank Ease of Doing Business Index (DBI) slipped three positions, from the 35th position the country occupied in 2012 to 39th in 2013. South Africa showed a slight decline in its performance this year. This result is not a refl ection of the country performing badly, it is an eff ect of other countries moving up the ranking ladder, by improving the conditions of doing business at a faster pace than South Africa.

This year’s report notes that among the 50 economies with the biggest improvements since 2005, a third is in Sub-Saharan Africa. This is a signifi cant fi nding for the region, indicating improving conditions for doing business, in a period when negotiations regarding the establishment of the Trilateral Free-Trade Area, encompassing the Southern African Development Community (SADC), Community of East and Central African States (COMESA), and the East African Community (EAC) are taking place. This free trade area will create an integrated market of more than 650 million people.

Other fi ndings on South African performance in the DBI showed that the country passed a new company law, which eliminated the requirement to reserve a company name and simplifi ed the incorporation documents. This makes it easier to start a business. The DBI indicated that South Africa made transferring property less costly and more effi cient, by reducing the transfer duty and introducing electronic fi ling. South Africa also introduced a new reorganisation process to facilitate the rehabilitation of fi nancially distressed companies.

Brand South Africa Annual Report 2012 2013 27

South Africa’s improved its performance on the Trading Across Borders rank. In the DBI 2012, South Africa ranked 144th and improved its ranking by 29 positions to 115th in the DBI 2013. This is a signifi cant improvement due to the fact South Africa has decreased the time, cost, and red tape, companies have to handle to get products to port and shipped to international markets.

South Africa – BRIC DBI Comparison

The World Bank assesses the ease of doing business according to 10criteria. The country performs particularly well when compared to its BRICS partners. South Africa came fi rst in the criteria, as indicated in brackets in the table below.

BRICS Comparison - World Bank Ease of Doing Business 2013

BRAZIL RUSSIA INDIA CHINA SOUTH AFRICA

Over-all 130 112 132 91 39 (1)

Starting a business 121 101 173 151 53 (1)

Dealing with construction permits 131 178 182 181 39 (4)

Getting electricity 50 184 105 114 150 (4)

Registering property 109 46 94 44 79 (3)

Getting credit 104 104 23 70 1 (1)

Protecting investors 82 117 49 100 10 (1)

Paying taxes 156 64 152 122 32 (1)

Trading across borders 123 162 127 68 115 (2)

Enforcing contracts 116 11 184 19 82 (3)

Resolving insolvency 143 53 116 82 84 (3)

Figure 5 - BRICS comparison 2013- World Bank Ease of Doing Business

According to the indicators above, South Africa came fi rst in six of the DBI criteria, among the BRICS grouping of nations. This implies that South Africa can make a strong business case to attract trade partners, investment, and clients from fellow BRICS members. South Africa off ers several competitive advantages. One important selling point to use for South Africa as a business destination, is that it has an open business environment

World Economic Forum – World Travel and Tourism Index

South Africa improved its position in the WEF Travel and Tourism Index this year. This year’s index covered 140 countries. South Africa improved its position on the WTTC in 2013 to 64 from 66 in 2011. South Africa ranked third in the Sub-Saharan Africa region after Seychelles (1st), and Mauritius (2nd).

Comments by WEF on South Africa travel and tourism

Important WEF fi ndings indicates South Africa as a country is ranked highly at 17th place for its natural resources, and 58th for cultural resources. According to WEF, this is due to many World Heritage sites, rich fauna, creative industries, and plenty of international fairs and exhibitions hosted in the country. The latter can be interpreted as a strong selling point for the country, with positive communication implications.

A further positive fi nding from WEF indicates that South Africa’s infrastructure is well developed for the region, with the air transport infrastructure ranking 43rd, and an assessment of railroad quality (46th) and road quality (42nd).

South Africa is admired for its travel and tourism related policies, rules and regulations as these are conducive to the sector’s development (ranked 29th). WEF indicates that South Africa has been making steady improvements in this area over the past few assessments.

UNDP – Human Development Report (HDR)

The good news in the report for South Africa is that the country improved its HDR ranking, by two positions from 123 in 2011, to 121 in the 2012/13 report.

This year’s report claims there has been a transformation in the world economic system in recent years. This is partly due to the global economic situation, and the meteoric rise of developing nations and their signifi cance to the future of the world economy as a whole. The growing economic infl uence of developing nations eff ects political infl uence, which is having a signifi cant impact on the progress of human development, according to the UNDP.

South Africa HDR indicators

YEAR BANKHDR

VALUE

LIFE

EXPECT-

ANCY

MEAN

YEARS OF

SCHOOLING

EXPECTED

YEARS OF

SCHOOLING

GROSS

NATIONAL

INCOME

2012/

13 121 0.629 53.4 8.5 13.1

$ 9594

(PPP)

2011 123 0.619 52.8 8.5 13.1 $ 469 (PPP)

Figure 6 - South Africa’s performance in the UNDP Human Development Index

28 Brand South Africa Annual Report 2012 2013

The UNDP’s emphasis in this year’s report falls on the impact of the global economic situation on human development indicators. South Africa is singled out with other major developing nations as an example that refl ects the global shift of economic and political power to the east and south.

Reputation Indicators and International Investor Perceptions

The sections to follow will refl ect on two issues: South Africa’s global reputation as measured annually by the Anholt Gfk-Roper Nation Brand Index, and investor perceptions of South Africa based on key fi ndings from Brand South Africa’s annual Project Thrive, International Investor Perception Research.

Anholt Gfk-Roper Nation Brand Index

Brand South Africa subscribes to the annual Nation Brand Index reputation study conducted by the Anholt-Gfk Roper Nation Brand Index (NBI). The NBI is an important measure of a country’s reputation in terms of the six criteria outlined in the hexagon below. Perceptions of Investment and Immigration, Exports, People, Cultural and Heritage, Governance, and Tourism form the main pillars according to how a country’s reputation is assessed.

Investment Potential and attractiveness to outsiders

Level of satisfactionwith country's productsand services

Competency fairgovernance, human rights, international

contribution

Potentialattractiveness and

economicalcontribution

Commercial and culturalProducts and sporting prowess

Tourism

Investment &

Immigration

Governance People

Culture & Heritage

Exports

What is a Nation Brand?

Figure 7 - Nation Brand Hexagon

In 2012 South Africa was ranked 36th out of the 50 nations for the second year in a row. This comes in a year where two-thirds of the nations have experienced overall reputation score declines. South Africa’s overall reputation has remained stable, which is no small feat.

South Africa’s Culture remains its strongest asset (28th). South Africa has seen score erosion on its top dimension, though several nations have seen a decline in this area. With a strong People profi le (31st globally), South Africans are admired across most panel countries – especially when it comes to wanting someone from South Africa as a close friend (ranked 28th). South Africa continues to rank 34th globally on Tourism, with much stronger perceptions as the country being naturally beautiful (15th) than on having historic buildings (41st). The country ranks highly on sporting excellence (16th), but is somewhat less known for its culture – both contemporary (34th) and historic (33rd).

When it comes to rankings, South Africa records some gains in 2012. South Africa surpasses fellow BRICS nations, India and Russia, on Governance and moves ahead of Russia, South Korea and China on People. Yet, it has lost some ground on Culture.

The table below shows South Africa’s performance per pillar between 2010 and 2012.

South Africa NBI performance 2012 2011 2010

Overall ranking 36 36 37Ranking by pillar

Exports 37 37 38

Governance 41 41 40

Culture 28 25 27

People 31 34 31

Tourism 34 34 35

Immigration and Investment 38 39 43

Figure 8 – South Africa's overall and pillar performance in the Nation Brand Index

Investor perceptions - Key fi ndings from Brand South Africa Project Thrive, International Investor Perception of South Africa Research

Brand South Africa conducts an annual international investor perception study. This year’s results show a steady improvement in international investor perceptions of the country as a business destination of choice. The study shows that South Africa’s economy is positively seen as an environment full of opportunities. Below are some key fi ndings from the report:

South Africa’s key performance indicators remain stable in this year’s fi ndings, despite the global economic conditions and labour issues/events experienced in the country during 2012.

Brand South Africa Annual Report 2012 2013 29

A high percentage of non-investors are currently unavailable for investment, due to global economic uncertainty.

There has been a slight increase in the number of investors currently investing in South Africa, while countries like India and Brazil have seen a slight decline in the amount of investors.

Mining and quarrying sectors remain strongly associated with South Africa. However, there has been a signifi cant increase in associations with other sectors in the South Africa economy like retail trade, construction, fi nancial/insurance/real estate business, electricity and gas water supply, post and telecommunications. This indicates that international investors are increasingly seeing South Africa as a business destination.

44% of the sample was aware of the positioning statement “Inspiring New Ways”. which was launched two months before fi eldwork for Thrive began.

Investors are most likely to have heard from an online source (60% internet, 24% blogs). These sources tend to be more neutral.

Word of mouth is also an important source of information for investors (41%).

Television was the most negative source of information (25% of reports negative).

Thrive data modelling indicates that South Africa can attract more FDI if the country off ers more suitably qualifi ed labour to investors.

Mining and Quarrying

Hospitality, Hotels, Restaurants

Agriculture, Hunting, Forestry

Wholesale and Retail Trade

Manufacture

Construction

Financial, Insurance, Real Estate

Transport, Storage and Communication

Electricity, Gas and Water Supply

Post and Telecommunications

Community, Social and Personal

Other

Don’t know

Figure 9 – Project Thrive: Economic sectors associated with the South African economy

The Thrive study questions respondents’ awareness of South Africa policies and initiatives. This can be divided into two broad categories. The fi rst speaks to government policy initiatives such as the New Growth Path (56% positive awareness), tax incentives in manufacturing (49% positive awareness), BEE (37% positive awareness), trade policies (55% positive awareness), labour policies (48% positive awareness), investor protection policies (45% positive awareness). The second category speaks to South African-led initiatives such as the Square Kilometre Array bid (33% positive awareness). The latter can have a tremendously positive impact as proof of South Africa’s technological readiness and sophistication within the developing world context.

Non-investors associate South Africa with a growing market with economic potential. This is an important fi nding, however, perceptual associations with South Africa as a country with a high crime rate persists. This issue has an adverse eff ect on the country’s reputation, and requires attention. The conclusion to be drawn is that more work remains to be done to increase positive awareness of key investor and economic policies that can attract FDI and trade.

South Africa’s performance in a range of competitiveness and human development indicators suggest the country has tremendous strengths that can be leveraged positively to position the country as a business partner and investment destination of choice. As indicated above, it is necessary to understand how South African ranks and is positioned among fellow developing nations. While the competitiveness indicators utilised above, point to high-level indicators of national competency, more research should be conducted on a sector-specifi c basis to question issues particular in specifi c areas of economic activity. Nevertheless, national strengths in the fi nancial sector, goods and market effi ciency, and indicators that show South Africa outperforming Next11 nations on a technological readiness, innovation, and institutions, clearly establish the country as a leader among developing nations. These strengths can be used as an inspiration to engage robustly with areas of competitiveness where the country’s performance is weaker.

In terms of overall competitiveness performance, South Africa ranks third among the BRICS nations, and in the top fi ve of the Next11. The conclusion is that as a developing nation, South Africa compares well with fellow developing nations, but shares many unique social, educational, and human development challenges that are characteristic of developing societies and nations. In order to strengthen and advance the nation brand, critical areas of skills development, education, and services require attention.

2012(n=534)

30 Brand South Africa Annual Report 2012 2013

In terms of reputation the report refl ects fi ndings from an annual international investor perception study commissioned by Brand South Africa. From the Project Thrive, the results show it is clear that positive associations exist in terms of investment incentives for international investors, and that the country is increasingly seen as a business destination by international investors. This is particularly evident due to increased associations with South Africa’s retail, construction, and fi nancial services sectors.

South Africa, it can be concluded, is a globally competitive developing nation. Areas of national competency can be taken as an inspiration to develop and enhance country performance, economic social development in the future.

The WEF Competitiveness Report, South Africa and a Performance Comparison with the Next 11 Countries - By Miller Matola, CEO of Brand South Africa

When the World Economic Forum launched its annual Global Competitiveness Report last week, it provided an unprecedented opportunity for South Africa to truly benchmark its performance in the global marketplace against the 144 other nations involved in the survey. As the global economy grapples with slow growth and weak market recovery, emerging and developing countries are growing faster than advanced economies. The most interesting data emerges from a comparison not just with the other BRICS members that represent 43% of the world’s population, but also with what is commonly known as the Next 11 countries (Bangladesh, Egypt, Indonesia, Iran, Mexico, Nigeria, Pakistan, Philippines, Turkey, South Korea and Vietnam). Although each of these countries has very diff erent geographic and economic features, their common denominator is their high economic potential and their substantial populations representing exciting market opportunities.

All 11 countries demonstrate population growth rates above those of Western nations, indicating greater consumer market potential over the short to medium term. Large populations represent a wide potential pool of consumers for businesses to target; while high growth rates mean that this market will expand rapidly, providing proportionally more potential customers. It is not surprising that these markets, together with the BRICS member countries, are the focus of much global economic attention and speculation at the current time. So, how does South Africa’s competitiveness performance measure up in statistical terms against these Next 11 countries according to the 12 key pillars outlined in the Global Competitiveness Report? South Africa’s comparative strengths can be seen in the fi eld of fi nancial market development where it ranks fi rst amongst the Next 11 nations and third overall in global terms. Only Turkey featured in the top 50 nations in this important pillar from the Next

11 countries. Similarly, South Africa’s strongly performing and highly regarded Institutions helped the country to achieve a fi rst place ranking in this pillar against the Next 11 and a 43rd place globally overall in the report. None of the other Next 11 countries managed a place in the top 50 in the survey. It is worth noting that the high level of confi dence shown in South Africa's fi nancial market development comes at a time when global market confi dence is slow to return. The country is undoubtedly benefi tting from the size of its economy and from the quality and accountability of its private institutions. Against this pillar, South Africa also outperformed the Next 11 countries in the fi elds of the Legal Rights Index, the Regulation of Securities Exchanges, the Effi cacy of Corporate Boards, and the Strength of Auditing and Reporting Standards, the Availability of Financial Services and the area of Financing through Local Equity Markets.

Continuing on the positive performance note, South Africa recorded high rankings against the Next 11 countries against the pillars of Infrastructure (3rd place behind South Korea and Turkey), technological readiness (3rd place behind South Korea and Turkey) and Innovation (3rd place behind South Korea and Indonesia). Other strong performance areas for South Africa in the survey when compared with Next 11 countries are in the pillar of business sophistication where South Africa ranked 2nd behind South Korea and 38th overall. Interestingly, against this particular pillar, many of the Next 11 countries performed well with Indonesia, Mexico, Philippines and Turkey all appearing in the top 50 performing countries in the fi eld of business sophistication.

Another highlight for South Africa was in its performance against the goods and market effi ciency pillar where it ranked 2nd amongst the Next 11 nations, placed once again behind South Korea with Turkey in third place, and 32nd in the world, Overall, this pillar did not see strong performances from the majority of the Next 11 countries which appeared in the mid to bottom half of the table. South Africa’s strong performance in these areas shows that the country has a competitive advantage over many Next 11 nations in these pillars and associated sectors.

Brand South Africa Annual Report 2012 2013 31

However, this year’s Global Competitiveness Survey was not all good news for South Africa when benchmarking against the Next 11 nations. The country’s overall ranking was negatively impacted by its declining performance in critical areas for economic and social developmental growth. If South Africa is to improve its global competitiveness particularly in regard to the Next 11 countries, it will need to signifi cantly address a number of these key weaknesses. Against the pillar of health & primary education, South Africa was amongst the worst performing of the Next 11 nations, with only Nigeria recording a worse ranking, and was positioned 132nd out of 144 global economies. Interestingly, only South Korea which was placed fi rst and Iran which was placed second out of the Next 11 countries in the fi eld of health, made it into the top 50 in the global survey, signifying that this is a major problem for the majority of these nations.

Particular areas of concern for South Africa and which contributed to its poor ranking against this critical pillar remain the number of Tuberculosis cases recorded per 100,000 people in the country, where South Africa is positioned 143rd out of 144 countries. Other equally worrying statistics include the business impact of HIV/Aids where South Africa is positioned 135th, and the country's HIV prevalence rate which positions it globally in 141st position. In the Life Expectancy Years pillar, South Africa ranks 133rd in the world. These results remain a huge matter of concern and will continue to aff ect the country's future growth and development if eff ective solutions are not found.

Of equal concern to South Africa on the global competitiveness stage against the Next 11 countries was its performance against the pillar of Quality of Maths and Science Education, where it ranked 143rd place out of 144 countries. Nigeria also performed poorly, attaining 142nd place, with Bangladesh and Pakistan also scoring outside of the

top 100 global nations in this critical area. South Korea and Iran were the only two Next 11 nations to record top 50 places for the Quality of their Maths and Science Education, scoring 11th and 46th places respectively.

South Africa's performance decreased signifi cantly in the country's Macroeconomic Environment, which saw a drop from 43rd place to 69th place overall, in the survey. This ranking movement was in stark contrast to Next 11 country members such as South Korea which placed 10th globally, Indonesia in 25th global position, Philippines in 36th position in the world, Nigeria close behind in 39th position, and Mexico in 40th place in the global survey, all making the top 50 ranking.

The need to address issues such as Labour Market Effi ciency where South Africa suff ered the impact of a dramatic drop from 97th place overall in the world to 113th place today is a problem shared by all Next 11 countries, with not one single member making the top 50 ranking against this particular pillar. Four members (Bangladesh, Egypt, Nigeria and Pakistan) did not even make the top 100. In particular, South Africa’s rigid hiring and fi ring practices ranking it 143rd out of 144 in the world, its lack of fl exibility in wage determination by companies ranking it 140th; and signifi cant tensions in labour-employer relations ranking it 144th in the world; do not help the country’s reputation in this regard. These statistics require vigorous debate and a new approach, if South Africa is going to successfully hold its own, when benchmarking against the Next 11 nations and proving its worth and ensuring its economic prosperity on the global competitive stage.

[This article was published in September 2012 in the Sunday Independent]

32 Brand South Africa Annual Report 2012 2013

National Perceptions Audit

Brand South Africa subscribes to the annual National Perceptions Audit conducted by Kuper Research, to understand how South Africans view themselves and the country. The survey takes into account various issues such as class mobility, inter-generational mobility and related social perceptions.

Class Mobility

Class is essentially a self-classifi cation, based on people’s perceptions of the class they themselves fall into: lower/working class; middle class, upper middle class and upper class. Intergenerational class mobility is measured by asking about the class their parents fell into when they were the same age.

Class mobile people do not see themselves as static but as ‘moving up the ladder’ and their lifestyles and behaviour mirror their aspirations. South Africa is arguably one of the most socially mobile societies in the world. The move from the circumstances of previous generations is substantial – so there is optimism about the future despite the economic recession.

Upper Middle/Upper Class

Middle Class

Working/Lower Class

7,842m36%

9,215m43%

3,262m 15%

Source: National Perceptions Audit 2012/13

According to the National Perceptions Audit, 36% of the country’s citizens classify themselves as working/lower class, with 43% in the middle class and 15% upper middle/upper class.

Intergenerational mobility

Parents at same age you are now Own Class

Working Class Middle Class Upper Middle Upper Class Don't know Not Sure

52%

36%31%

43%

8%12%

3% 3% 6% 6%

Source: National Perceptions Audit 2012/13

The above graph illustrates individuals’ own class, versus that of their parents at the same age. Individuals, who classifi ed themselves as working class, are fewer than their parents at their own age. In a direct comparison to middle and upper class, more individuals view themselves as progressive in their class classifi cation, in relation to their parents. This suggests that South Africa is a socially mobile country.

Joblessness anxiety

30%

39%32%

40%

54%

2006 2007 2008 2009 2012

The educated (diploma or degree 42%; matric 61%) and the youth (62%) are refl ecting signifi cant anxiety levels.

Source: National Perceptions Audit 2012/13

In 2012, 54% of people indicated that they felt anxious about never getting a job. In particular, university graduates, matriculants and a large proportion of the youth (62%) specifi ed this concern. Graduates battle with the predicament of securing employment with little or no skills. In comparison to the number of matriculants and graduates entering the job market each year, there are not enough job openings in the skilled sector to accommodate them.

Brand South Africa Annual Report 2012 2013 33

Protest Consequences

When asked, 74% of people agreed with the statement ‘Government does not take issues seriously until civil action or strikes occur’. Strike actions in South Africa are a threat to job creation. This makes it diffi cult to embark on the New Growth Path, which aims to create jobs in the next few decades. Strike actions do not allow the economy to reach its potential. However, when citizens feel deprived and frustrated, it leads to aggression which manifests in strike action.

Don't know 10%Disagree16%

Agree74%

Source: National Perceptions Audit 2012/13

Standard of education in comparison to parents

The fi gure below indicates that 77% of individuals agree with the statement ‘My standard of education is better than my parents managed to achieve’. Although the education system has caused much controversy in recent years, the majority of people feel that, compared to their parents, education systems have improved. Access to education is equal across all spheres of society, race, gender, social class and economic status.

No10%To some

extent10%

Don't know 3%

Yes77%

Source: National Perceptions Audit 2012/13

Social Cohesion

The majority of people no longer see themselves in the artifi cial boxes of the apartheid era

By language group4%By race

9%

By culturalbelief3%

By religion2%

African29%

SouthAfrican52%

Source: National Perceptions Audit 2012/13

When asked how individuals in South Africa identify themselves, 52% stipulated South African, 29% African, 9% by race, 4% by language, 3% by culture and 2% by religion. This was a positive indication that the apartheid boxes that once defi ned and identifi ed individuals along racial lines is slowly disintegrating, although only along initial identifying factors.

Cultural Coexistence

The dream of cultural co existence has the potential to increase to increase our competitivein times to come

Don't know 8%Disagree11%

Yes81%

Source: National Perceptions ordered 2012/13

When asked, 81% of people agree with the following statement ‘Black and white people in South Africa need each other to survive and prosper’. This was signifi cant as it indicates that there is a desire for social and cultural harmony. South Africans agree that to prosper as a nation, they need to work together with a shared unity and vision, despite the outward and cultural diff erences.

34 Brand South Africa Annual Report 2012 2013

Mobilising the good of the country

I actively encourage fellow South Africans to be proud of their country.

I am willing to do whatever I can to help make South Africa a better place.

I believe that small actions on my part can make a diff erence.

I would like to get involved in helping things to get better in the country but I don't know how.

I would like to become more actively involved in making South Africaa better place for all its people.

I make an eff ort to help better my own or other communities.

I am already actively involved in helping to make South Africa a better place in some way.

72%

70%

69%

65%

62%

62%

54%

Source: National Perceptions Audit 2012/13

The majority of South Africans play an active role in mobilising for the good of the country, and 72% encourage others to be proud of South Africa. The majority of South Africans are proud to be South African, and they will do whatever it takes to make the country a better place via the spoken word and active participation.

South Africa is an ideal country to live in

In the last quarter of 2012 (October to December, shown in the fi gure below), over two-thirds (68%) of South Africans said that South Africa is the ideal country to live in. There has been a gradual increase (+8%) in these ratings since the survey period between September to November 2011.

92%87%

90% 90%87%

90% 88% 87% 88%

6%9% 8% 9% 11%

8% 9% 8% 10%

2% 4% 2% 2% 3% 2% 3% 2% 2%

100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%

June 10 - Sept 10 - Dec 10 - March 11 - June 11 - Sep 11 - Nov 11 - March 12 - Q4 2012Sept 10 Nov 10 Mar 11 Jun 11 Aug 11 Nov 11 Mar 12 May 12

Source: GCIS Domestic Tracker

Pride levels

The fi ndings illustrated in the fi gure below, indicate that the overwhelming majority of South Africans are proud to be South African. Overall levels of national pride have remained stable since June 2010 and demographic analysis has found that the fi ndings are positive across all race groups.

Proud Neutral Not Proud

Source: GCIS Domestic Tracker

Reasons to be proudly South African

In the last quarter of 2012 national pride remained mainly centred around issues of cultural diversity (28%), the achievements of our democracy (18%), the beautiful landscape (15%) and the people of the country (14%).

Interestingly, the annual international nation reputation study conducted by Anholt -GfkRoper Nation Brands Index fi nds that South Africans are well respected globally. This is a strong feature of the country’s international reputation.

Brand South Africa Annual Report 2012 2013 35

28%The cultural diversity

Achievements of our democracy

The beautiful landscape

The people in general

0% 20% 40% 60% 80% 100%

18%

15%

14%

Source: GCIS Domestic Tracker

Attributes associated with South Africa

An attribute association was undertaken to test the credibility of various Brand South Africa elements. The results show that all of the statements in the fi gure below, which were presented to respondents in the last quarter of 2012, have high credibility and are closely associated with the brand.

South Africa has a rich diversity of people and cultures

South has a good place to travel for international tourists

South Africaha sa great potential for its own citizens

South Africa has a lot of possibilities

South Africa has good investyment opportunities for the international community

The people of South Africa embody the spirit of Ubuntu

South Africa is an environmentally conscious country

South Africa will succeed in the future

South Africa is dynamic and upcoming

South Africa is an infl uental country

South Africa is a country that will take its place as one of the top countries in the future

South Africa is a country that continuosly achieves its goals

South Africa comes up with creative solutions to problem

0% 20% 40% 60% 80% 100%

Completely believe/believe Neither believe nor disbelieve Do not believe/do not believe at all

80%

80%

77%

74%

72%

71%

69%

68%

67%

66%

61%

59%

56%

14%

15%

15%

18%

17%

18%

20%

21%

24%

21%

24%

25%

26%

4%

4%

7%

6%

6%

8%

7%

8%

7%

8%

11%

13%

15%

Source: GCIS Domestic Tracker

The top three attributes associated with South Africa that play a role in contributing to a positive brand for the country, are the rich cultural diversity, a travel destination of choice for international tourists and the potential South Africa can bring to its citizens.

Negative factors infl uencing South Africa

The vast majority of South Africans (88%) highlighted crime and safety as the major negative factors impacting on the country’s reputation. This was followed by poverty (74%), xenophobic attacks (68%), violent demonstrations and protests (67%), politics (67%) and service delivery issues (66%). These negative infl uences should not be viewed in isolation, but should be analysed on a holistic basis, including socio-economic, political and psychological factors.

88%

74%

68%

67%

67%

66%

59%

57%

49%

47%

41%

Crime and safety

Poverty

Xenophobic attacks

Violent demonstrations and protests

Politics

Service delivery

Social inequality and injustices

Economy

Nationalisation debates

Health care

Education

0 20% 40% 60% 80% 100%

Source: GCIS Domestic Tracker

Issues worrying South Africans the most

In the last quarter of 2012, the important issues that worried respondents the most, centred around their economic and personal circumstances, such as ‘being unemployed and/or having no income’ (27%), ‘fi nancial/personal problems’ (15%) and ‘poverty’ (7%).

Being unemployed / no income

The crime rate

Financial / personal problems

Poverty

Education

Financial security and safety of my family

High rate of corruption in SA

The housing shortage

0% 20% 40% 60% 80% 100%

Q4 2012 MAR 12 - MAY 12 NOV 11 - MAR 12

27%

32% 33%

17% 13% 12%

15%

15% 12%

7% 3% 6%

5%

3% 4%

4% 6% 9%

3%3%3%

2%

3%

Source: GCIS Domestic Tracker

36 Brand South Africa Annual Report 2012 2013

Summary of South Africa’s brand performance

Competitive Environment - Current Performance

Domestic Perception

Audit

2012/13 South Africa is ranked 36 out of 50 nations for the second year in a row; in a year where two thirds of the nations have experienced overall decline.

South Africa’s culture remains its strongest asset at 28th and a strong People profile 31st globally. South Africans are admired across most panel countries especially relating to “wanting a South Africa as

a close friend”. South Africa continues to rank 34th globally on Tourism; sporting excellence 16th; but less known for its

contemporary and historic culture.

South Africa’s rankings declined by two points to reach 52 in the 2012/13 GCI index. South Africa achieves highest rankings in Legal Rights index (1st); Regulation of Securities Exchanges

Financial Services (2 ); Financial t hrough local equity market (3 ). Higher Education and Training pillar - South Africa did not perform well: Quality of Maths and Science

education (143 ); Quality of Education System (140 ); Internet access in schools (111 ); In comparison to BRICS, South Africa lags behind in performance on Health and Primary Education pillars.

National Brand

Reputation

WEF GlobalCompetitiveness

Index

InternationalTrackerResults

Reputation Index

88% of South Africans are proud to be South African.

83% of South Africans believe the country is a good place for travel and international

75% of South Africans believe that the country embodies the spirit of Ubuntu.

62% of South Africans believe the country is an ideal place to live.

tourists.

Increased reporting on Business and Politics pillars across all markets due to BRICS Summit. Increased awareness of South Africa as economic, business, and service hub due to the country’s role in the African Union and BRICS. Project Thrive International Investor Perception study conducted by Brand SA indicates a substantial increase in the country seen as a business destination by international investors.

2012/13 average reputation score 35%.

During this financial year, two incidents had a negative impact on the reputation score: the Marikana

mine incident and the Oscar Pistorius case.

Increased coverage in the following markets: France, Democratic Republic of Congo, China, USA, UK, UAE.

SA’s hosting the 5th BRICS Summit marks a high point for the country as an important roleplayer in global governance. Increased volumes of reporting in BRICS member states due to South Africa being host nation.

stst

nd rd

1 st

rd th th