Embed Size (px)

Citation preview

Namibia Market Structure

MSB: Final Design

JUNE 2019

INTRODUCTION

19 June 2019 MSB Presentation - Funders Workshop 3

INTRODUCTION

Market change drivers

1.Affordable tariffs

2.Become self-sufficient

possibility to export (jobs)

3.Encourage IPPs

4.Increase competition

5.Reduce need for GRN

financial support (equity /

loans / guarantees)

6.Increase access

7.Lights to stay on

8.Etc.

Why change?

Market Drivers (Bottom Up)

1.High and incorrect tariffs in combination with low cost new

technologies (SWH & PV) make it easy for customers to

reduce electricity purchases

2.It is happening as we speak, REDs and customers are

installing own generation (est. 50~60MW)

3.Customers are using services they are not paying for

(resulting in cross subsidisation)

4.Customers want services that the utilities don’t offer

5.Utilities losing sales, revenues and customers

6.Potential for stranded assets

7.Impede on efforts to increase access

8.Reduction in cost of storage will trigger customer defection

if utility is unable to meet customer needs.

9.Some customer want to purchase 100% renewable energy

10.Etc.

Policy Drivers (Top Down)

19 June 2019 MSB Presentation - Funders Workshop 4

INTRODUCTION

Market structure options

Market Drivers

(Bottom Up)

Policy Drivers

(Top Down)

New market design

Options Comments

Monopoly No longer a valid option for generation

SB Utility conflicts – not delivering on all policy objectives - not meeting customer needs

I(S)(M)(T)O High cost of restructuring – rationale should be clear – potential to swop one monopoly for another

MSB Managed approach towards more competition and customer participation while meeting policy objectives

Competition Very high cost of restructuring (breaking up NamPower)

Do nothing Death spiral

TRADING

ARRANGEMENTS

19 June 2019 MSB Presentation - Funders Workshop 5

19 June 2019 MSB Presentation - Funders Workshop 6

TRADING ARRANGEMENTS

1a

Contestable Customers

MSB(SO/MO)

IPPs (Existing)

Imports (NP)

Generation (NP)

REDs, LA, & RC

Distribution Customers

Embedded IPPs

Exports (NP)

IPP

NP Tx Connected Customers

Captive Generation

Off-grid & mini-grids

Eligible Sellers

Exporter

Transactionall Flows from Seller to Buyer

Existing arrangementNew optional arrangement

19 June 2019 MSB Presentation - Funders Workshop 7

TRADING ARRANGEMENTS

1b

Contestable Customers

MSB(SO/MO)

IPPs (Existing)

Imports (NP)

Generation (NP)

REDs, LA, & RC

Distribution Customers

Embedded IPPs

Exports (NP)

IPP

NP Tx Connected Customers

Captive Generation

Off-grid & mini-grids

Eligible Sellers

Exporter

Trader Trader

Transactional Flows from Seller to Buyer

Existing arrangementNew optional arrangement

1. Phase 1a: Sep 2019 - June 2021; Tx Customers only

2. Phase 1b: July 2021 – June 2026; Tx + Dx ≥ 1MVA

3. Two stage approach to allow Distributors to unbundle sufficiently to enable wheeling

for their customers

4. Phase 2: July 2026 – onwards; Tx + Dx (as determined by Regulator); Imports

allowed

5. Imports only allowed from 2026 to support government policy of self-sufficiency and

to align with unwinding of current import contracts

19 June 2019 MSB Presentation - Funders Workshop 8

TRADING ARRANGMENTS

Phase 1 vs. Phase 2

19 June 2019 MSB Presentation - Funders Workshop 9

TRADING ARRANGEMENTS

2

Contestable Customers

MSB(SO/MO)

IPPs (Existing)

Imports (NP)

Generation (NP)

REDs, LA, & RC

Distribution Customers

Embedded IPPs

Exports (NP)

IPP

NP Tx Connected Customers

Captive Generation

Off-grid & mini-grids

Eligible Sellers

Exporter

Trader Trader

Transactional Flows from Seller to Buyer

Existing arrangementNew optional arrangement

Importer

ELIGIBILITY CRITERIA

19 June 2019 MSB Presentation - Funders Workshop 10

19 June 2019 MSB Presentation - Funders Workshop 11

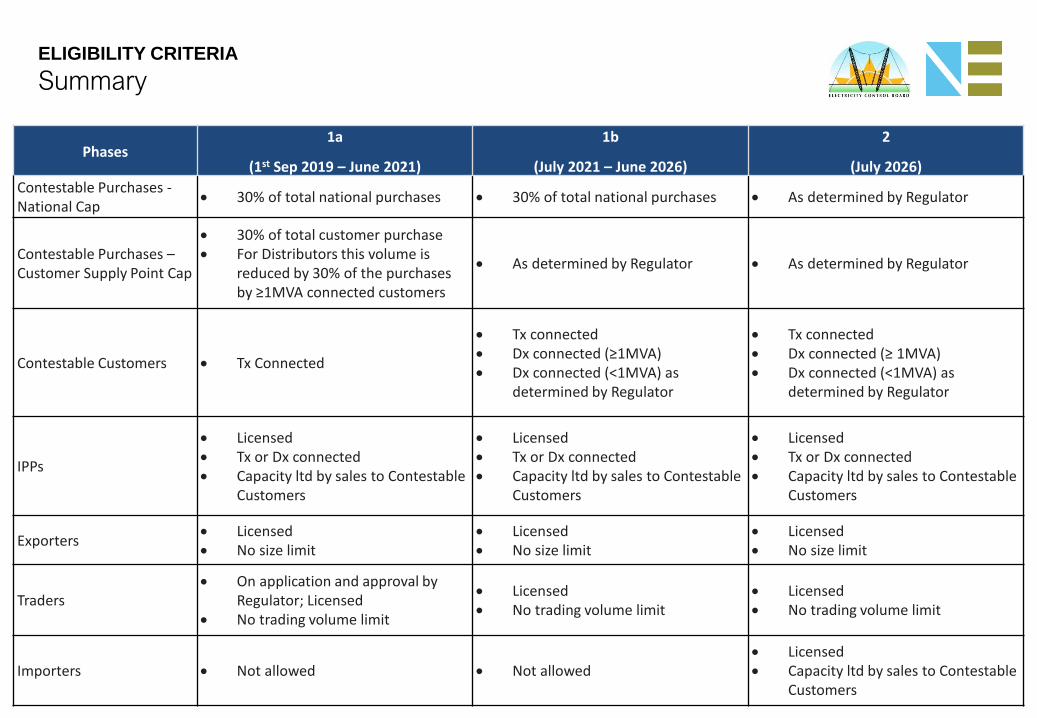

ELIGIBILITY CRITERIA

Summary

Phases1a

(1st Sep 2019 – June 2021)

1b

(July 2021 – June 2026)

2

(July 2026)

Contestable Purchases -National Cap

• 30% of total national purchases • 30% of total national purchases • As determined by Regulator

Contestable Purchases –Customer Supply Point Cap

• 30% of total customer purchase • For Distributors this volume is

reduced by 30% of the purchases by ≥1MVA connected customers

• As determined by Regulator • As determined by Regulator

Contestable Customers • Tx Connected

• Tx connected• Dx connected (≥1MVA)• Dx connected (<1MVA) as

determined by Regulator

• Tx connected• Dx connected (≥ 1MVA)• Dx connected (<1MVA) as

determined by Regulator

IPPs

• Licensed• Tx or Dx connected• Capacity ltd by sales to Contestable

Customers

• Licensed• Tx or Dx connected• Capacity ltd by sales to Contestable

Customers

• Licensed• Tx or Dx connected• Capacity ltd by sales to Contestable

Customers

Exporters• Licensed• No size limit

• Licensed• No size limit

• Licensed• No size limit

Traders• On application and approval by

Regulator; Licensed• No trading volume limit

• Licensed• No trading volume limit

• Licensed• No trading volume limit

Importers • Not allowed • Not allowed• Licensed• Capacity ltd by sales to Contestable

Customers

SIZE OF CONTESTABLE

MARKET

19 June 2019 MSB Presentation - Funders Workshop 12

Focus:

• Examines the potential size of the contestable market

• Recommends level of contestability

Methodology:

• The Consultant worked with the ECB and NamPower to develop a forward view of the most likely energy sources for Namibia over the next 10 years

• The analysis divided the sources between:

– “Non-Displaceable”: There is a significant fixed cost (financial or contractual) associated with these sources. Not economic to displace.

– “Displaceable”: These sources have low or no fixed costs (or fixed cost could be avoided). These sources could be displaced at the right price or time

19 June 2019 MSB Presentation - Funders Workshop 13

SIZE OF CONTESTABLE MARKET

Focus & Methodology

• The figure on the right shows

the expected energy sources to

2026

• “Non-displaceable” sources

include:

–Existing Public

–Existing Private

–Committed Private

–Ministerial Determinations

–Existing Firm Imports

• “Displaceable” sources include:

–Flexible Imports

–New Supply

19 June 2019 MSB Presentation - Funders Workshop 14

SIZE OF CONTESTABLE MARKET

Definitions & Concepts

• The figure on the left shows the split between “Non-Displaceable” and “Displaceable” energy sources.

• “Displaceable” energy varies between 33-48% of total production.

• The figure on the right shows the total contribution (GWh) of “Displaceable” energy

19 June 2019 MSB Presentation - Funders Workshop 15

SIZE OF CONTESTABLE MARKET

”Displaceable” Energy Sources Potential

ENABLING MECHANISMS

MARKET OPERATIONS

19 June 2019 MSB Presentation - Funders Workshop 17

PRE-DISPATCH

19 June 2019 MSB Presentation - Funders Workshop 18

MARKET OPERATIONS

Trading Process

DISPATCH POST-DISPATCH

1. Seller and buyer enter into

bilateral

2. Seller meet requirements of

MSB

3. Submit data in accordance with

grid code

4. Specify nominated percentage

per customer

5. Notify MSB of any changes in

plant ability to meet schedule

6. MSB develop day-ahead hourly

demand forecast

7. Publish a day-ahead least-cost

Dispatch Schedule

1. Eligible Sellers dispatch their

plant in accordance with the

most recent Dispatch Schedule

2. The MSB adjust the output from

centrally dispatched units to

ensure that demand and supply

is balanced

3. Under certain Emergency

Conditions, instruct the Eligible

Producer to increase or

decrease output or to disconnect

from the grid

4. The MSB shall balance the total

integrated system in real time

1. MSB shall collect and record the

actual production

2. Once a month, the MSB shall

perform settlement functions

including meter reconciliation

and calculation of invoices

3. Disseminate relevant data to the

licensed distributors in order for

them to reconcile and settle

4. Review, and if needed, update

MSB Financial Security

requirements

5. Compare Delivered Energy from

every Eligible Seller against the

last Dispatch Schedule, adjusted

for Dispatch Instructions

6. Assess against balancing

mechanism/ determine

balancing energy

MARKET OPERATIONS

Balancing Mechanism

1. MSB will monitor scheduled production against actual production

2. A deviation away from scheduled position will attract a balancing payment

3. A tolerance band defined as lesser of:

a) ± 0.5MW, or

b) ± 2.5% of the plants last dispatch schedule

4. Balancing charge:

a) for negative deviations the charge will be set as a 100% of energy component of Bulk Supply Tariff

b) for positive deviations there will be no charge

5. Balancing payment (plus sale to bilateral customer) to pay for balancing the system

a) Only negative deviations will attract a balancing payment – no compensation for over generation

b) Deviations between the Lower and Upper limits do not attract a balancing payment

c) The bigger the deviation the higher the balancing payment

6. Financial Security will be placed with MSB for Balancing charges

19 June 2019 MSB Presentation - Funders Workshop 19

Deviation from Dispatch Schedule (MW/h)

0

Balancing Payment

Upper LimitLower Limit

TARIFF UNBUNDLING

19 June 2019 MSB Presentation - Funders Workshop 20

19 June 2019 MSB Presentation - Funders Workshop 21

TARIFFS

Unbundled Services

Service Customers Generators

Energy (Utility) ✓ -

Less Wheeled Energy Rebate (✓) -

Wheeled Energy Addback (✓) -

IPP Purchases (✓)

Balancing - ✓

Tx/ Dx Use of System ✓ -

Tx/ Dx losses ✓ (✓)

Network Capacity Reserve - (✓)

Distributor Wheeling Charge (✓)* -

Reliability ✓* -

Net Billing (Banking/ Storage) - (✓)

Customer service ✓ ✓

Levies ✓* -

VAT ✓ ✓

WHEELING

19 June 2019 MSB Presentation - Funders Workshop 22

19 June 2019 MSB Presentation - Funders Workshop 23

WHEELING

Simulated Wheeling Transaction in Model

19 June 2019 MSB Presentation - Funders Workshop 24

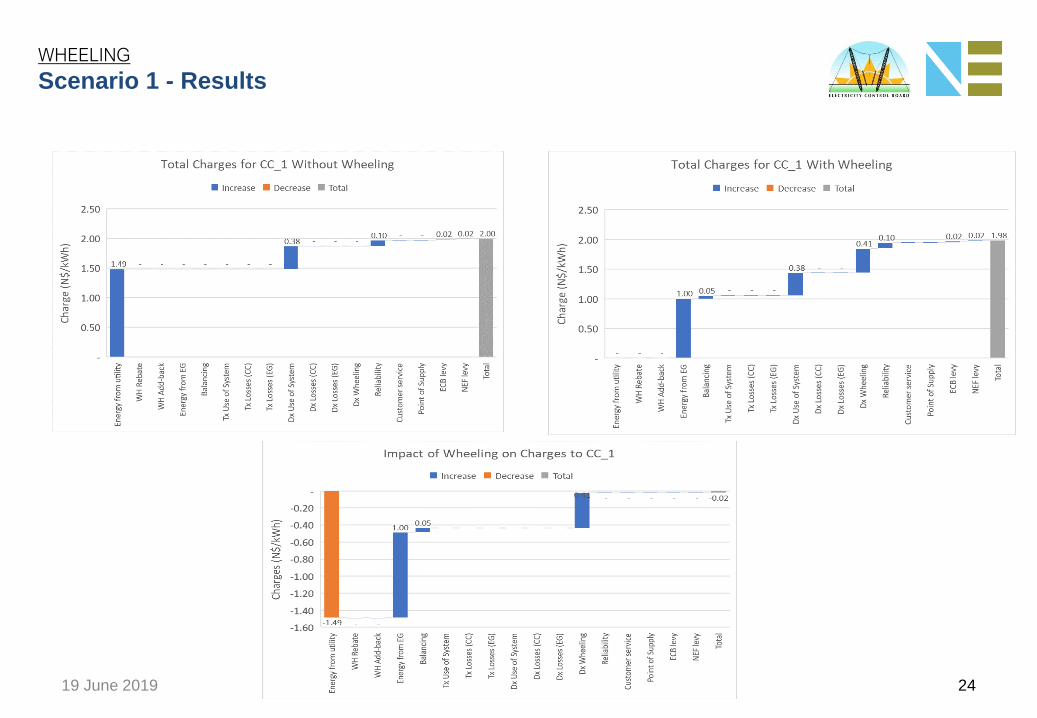

WHEELING

Scenario 1 - Results

19 June 2019 MSB Presentation - Funders Workshop 25

WHEELING

Scenario 4 - Results

19 June 2019 MSB Presentation - Funders Workshop 26

WHEELING TARIFFS

Potential Congestion scenarios and mitigations

Network congestion resulting inImpact Mitigation

Evacuation constraint

Delivery constraint

1 No No None • None

2 Yes NoSeller unable to produce energy and sell to Buyer

• Deemed payments in exchange for network capacity reserve charge

3 No YesSeller can produce but not sell to Buyer

The Seller may select one of the following prior to submitting the Day-ahead Production Schedules:

• The Seller could nominate an alternative Buyer for the unused power.

• MSB shall allow the Seller to “bank” the Unsold Energy. The Seller is allowed to withdraw the ‘banked’ power at a later stage in accordance with the rules of the Energy Banking Service.

• The customer may withdraw the stored energy when it is able to do so and subject to the Energy Banking Service conditions.

• Sell the unsold power to the MSB at a pre-arranged price.

4 Yes Yes

Seller unable to produce and sell and Buyer unable to purchase and consume

• Combinations of Options 2 or 3

LICENSING

19 June 2019 MSB Presentation - Funders Workshop 27

• Licensing Applications and Processes currently being revised by ECB

• Licenses required for:

– Generation

– Transmission

– Distribution

– Import

– Export

– Trading

– Market Operations

• Market Participants will require multiple other approvals

– SO Approval; TNO Approval; MSB Approval & Registration; Other Permits/

Approvals

19 June 2019 MSB Presentation - Funders Workshop 28

APPROVALS

Will be aligned with requirements of the MSB

SECURITY OF SUPPLY

19 June 2019 MSB Presentation - Funders Workshop 29

• Detailed design includes the following key design features:

– Planning Criteria/ Processes/ Responsibilities: Energy, Capacity, Ancillary

Services (ST, MT, LT)

– Conditions for NamPower to Act as Supplier of Last Resort (excl. for example

Exports and Imports)

– Call Back Option

19 June 2019 MSB Presentation - Funders Workshop 30

SECURITY OF SUPPLY

Detailed Design addresses Security of Supply issues

EXPORT “CALL-BACK”

How can Namibia protect its long term low cost resources

Depending on the situation (price, location, timing, etc.), Namibia may want to access some of thepower from the large and low-cost export orientated power generation projects. There are a few waysthrough which this can be achieved :

1. Purchase all the output from the plant.

Namibia can then use what it needs and

export the remaining power.

2. Purchase only a portion of the output. In this

way Namibia can access a specified quantity

of energy from the plant. The developer will

then be able to export the remainder of the

energy to its regional customer(s).

3. Incorporation of a ‘call -option’ in the power

purchase agreement between the IPP and

Namibia (represented by the MSB)

a) The price paid by the MSB shall be

equal to what the producer would have

received

b) Quantity of energy, exercised under the

call option, shall not exceed 20% of the

plant’s maximum total output (any 12

months)

After 1 yr notice = 3%

After 3yr notice = 10%

After 5yr notice = 20%

12 months min notice

1 yr 3 yr 5 yr

% of total

export

3119 June 2019 MSB Presentation - Funders Workshop

GOVERNANCE

19 June 2019 MSB Presentation - Funders Workshop 32

• Market Rules are under development and will be part of Grid Code

• Grid Code Advisory Committee (GCAC) is best positioned to assume the governance

roles and functions of the MSB

19 June 2019 MSB Presentation - Funders Workshop 33

GOVERNANCE

The GCAC is best placed to govern and implement the MSB

BACK-UP

19 June 2019 MSB Presentation - Funders Workshop 34

RISKS

Risks and Mitigations

Risks Mitigations

Cost of supply will increase (IPPs are expensive)

Appropriate procurement process and approval criteria by regulator (IPPs risk allocation)

Complexity (governance, trading, scheduling, dispatch and balancing)

Market rules, phasing, simplicity in design, monitoring and refinement

Viability of existing licensees (cherry-picking)Phasing, eligibility criteria and transparent subsidy framework

Additional resources needed to implement and operate new market structure

Simplicity in design and offset by market gains

New systems & processes Simplicity in design and offset by market gains

Network access, usage and paymentAppropriate connection, use of system and wheeling arrangements

Lights will go out (supplier of last resort)Revised planning procedures and adequacy criteria (ST, MT & LT)

Exporting low cost resources Call option

19 June 2019 MSB Presentation - Funders Workshop 35

19 June 2019 MSB Presentation - Funders Workshop

36

MARKET OPERATIONS

Balancing Mechanism Example (Under Delivery)

MSB

CusGen10 MW

1 MW

9 MW

MSB

CusGen1 MW @ PPA tariff

9 MW @ retail tariff8,5 MW @

balancing penalty

PHYSICAL FLOWS FINANCIAL FLOWS

= CONTRACTED ENERGY IN 1 HOUR

= DELIVERED ENERGY FROM ELIGIBLE SELLER

= DELIVERED ENERGY FROM SUPPLIER OF LAST RESORT (MSB)

= PAYMENTS ON ACTUAL ENERGY

= BALANCING PENALTY

19 June 2019 MSB Presentation - Funders Workshop

37

MARKET OPERATIONS

Balancing Mechanism Example (Over Delivery)

MSB

CusGen10 MW

10 MW

MSB

CusGen10 MW @ PPA tariff

5MW @ $0 balancing charge

PHYSICAL FLOWS FINANCIAL FLOWS

= CONTRACTED ENERGY IN 1 HOUR

= DELIVERED ENERGY FROM ELIGIBLE SELLER

= DELIVERED ENERGY FROM SUPPLIER OF LAST RESORT (MSB)

= PAYMENTS ON ACTUAL ENERGY

= BALANCING PENALTY

5 MW

• The concern is that the introduction of IPPs combined with the ability to wheel power could undermine the security of supply.

• This risk of inadequate supply over any planning horizon can be avoided by undertaking planning, scheduling and operating activities on a rolling basis, as well as by ensuring that appropriate adequacy criteria are employed.

• As the nominated supplier of last resort, many of these activities will be the responsibility of the MSB.

• MSB will not be required to act as Supplier of Last Resort on export transactions or import related purchases, unless negotiated

• The Reliability Service Charge will be used to compensate the MSB for acting as the Supplier of Last Resort

19 June 2019 MSB Presentation - Funders Workshop 40

SECURITY OF SUPPLY

Is supported by planning

Sufficient Energy Sufficient CapacitySufficient Ancillary

Services

• Well understood

• Currently managed by NIRP

• Need:

– regular updates

– to consider vRE

– to consider impact of net-metering & storage

• All of these issues can be addressed through planning

19 June 2019 MSB Presentation - Funders Workshop 41

SECURITY OF SUPPLY

Energy & Capacity Adequacy

MSB Supports Security of Supply via the following planning and operations

Long term plans 1-20 yrs

Annual Plans 12 months/ 52 week rolling

Weekly plans 4 weeks

Daily Schedules 24 hrs day ahead

Hourly operations Real time

• Given the increasingly important role that vRE is playing in electricity generation in

the region and the demands that this will place on ancillary services, it is expected

that the cost of providing these services will come under the spotlight.

• Several utilities including Eskom are reviewing their cost structures to better

understand the cost of providing these services.

• It is therefore reasonable to expect that ancillary services cost will be further

unbundled resulting in a substantial increase in the prices for the various services in

the near to medium term.

19 June 2019 MSB Presentation - Funders Workshop 42

SECURITY OF SUPPLY

Ancillary Services Adequacy

Operating Reserves

Spinning Reserves

Quick ReservesRegulating Reserves

Black Start & Islanding

Reactive Power & Voltage

ControlLoad following Other

• MSB must take pro-active stance on AS procurement, provision and payment

• MSB should develop an AS strategy

– clearly identify the need for ancillary services

– plan of who will provide these services

– and at what cost

• A system with very high levels of non-synchronous machines may experience a lack of reserves to deal with the system disturbances immediately following an incident (ltd inertia)

• Mitigation includes:

– Active power control services available to some types of vRE (e.g. wind generators can be designed to provide synthetic/pseudo inertia to the system. This means that inertia can be planned, controlled and optimised,

– Fast frequency response options such as energy storage systems and demand response.

– Regional interconnections provide access to larger network which will share the available inertia between the interconnected systems

• The above indicates that there is no natural or scientific ‘cap’ on the level of vRE in the system and that planning is needed to deal with the characteristics of new technologies

19 June 2019 MSB Presentation - Funders Workshop 43

SECURITY OF SUPPLY

Ancillary Services Procurement