Embed Size (px)

Citation preview

DUTIES OF A PROFESSIONAL ACCOUNTANT (SA)

WEBINAR 12 JULY 2017

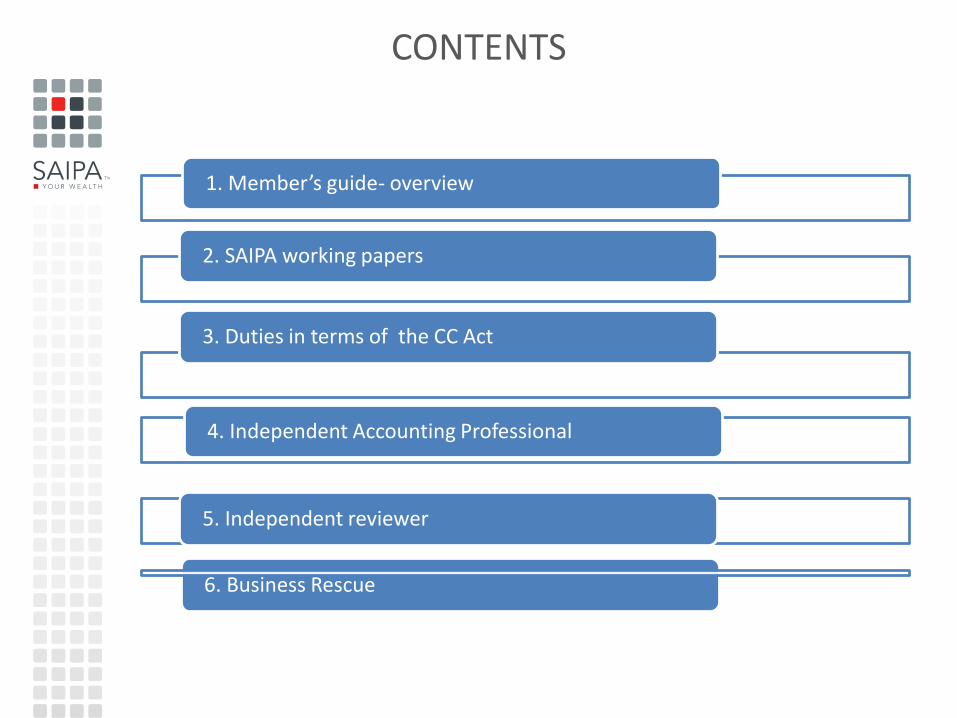

CONTENTS

1. Member’s guide- overview

2. SAIPA working papers

3. Duties in terms of the CC Act

6. Business Rescue

4. Independent Accounting Professional

5. Independent reviewer

Resources available from SAIPA

Working paper file

Independent review

Member’s guide

Close Corporations Act 69 of 1984

Members appoint an Accounting

officer

Prepare and present AFS

Duty to report financial

irregularities –trading when

insolvent

Section 59 – Appoint an AO on the date of registration. Vacancy must be filled within 6 months

Section 58Statement of Financial PositionStatement of comprehensive income

Accounting Officers report – ISRS 4400 agreed upon procedure

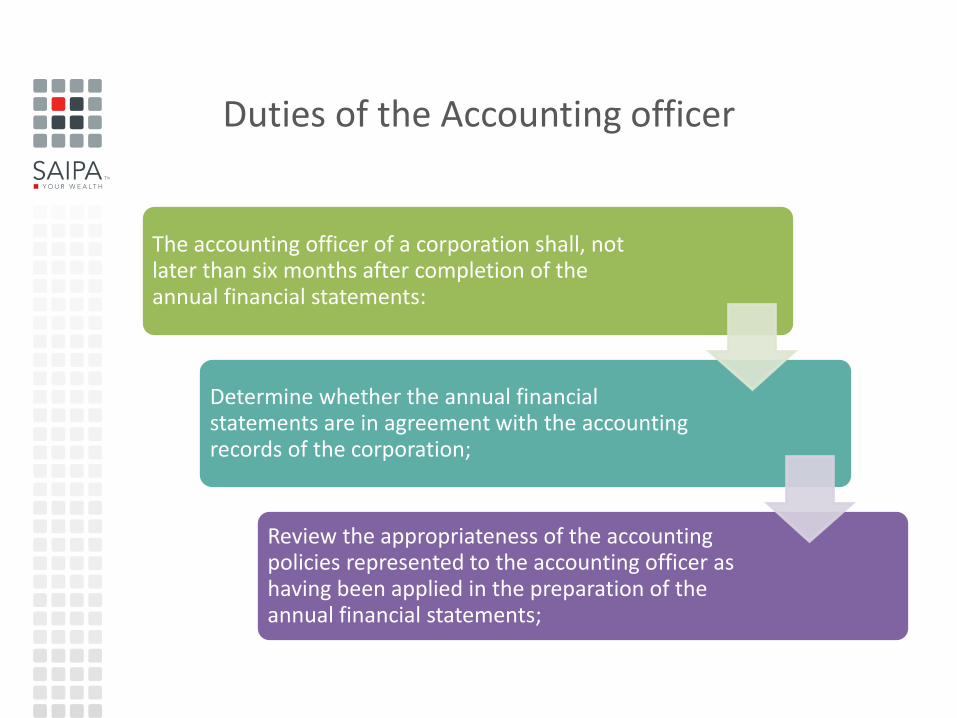

Duties of the Accounting officer

The accounting officer of a corporation shall, not later than six months after completion of the annual financial statements:

Determine whether the annual financial statements are in agreement with the accounting records of the corporation;

Review the appropriateness of the accounting policies represented to the accounting officer as having been applied in the preparation of the annual financial statements;

If during the performance of his duties an accounting officer becomes aware of any contravention of a

provision of this Act

Describe the nature of the contravention in his report.

If during the performance of his duties an accounting officer becomes aware of any contravention of a

provision of this Act

Where an accounting officer is a member or employee of a corporation, or is a firm of which a partner or employee is a member or employee of the corporation, his report shall state that fact.

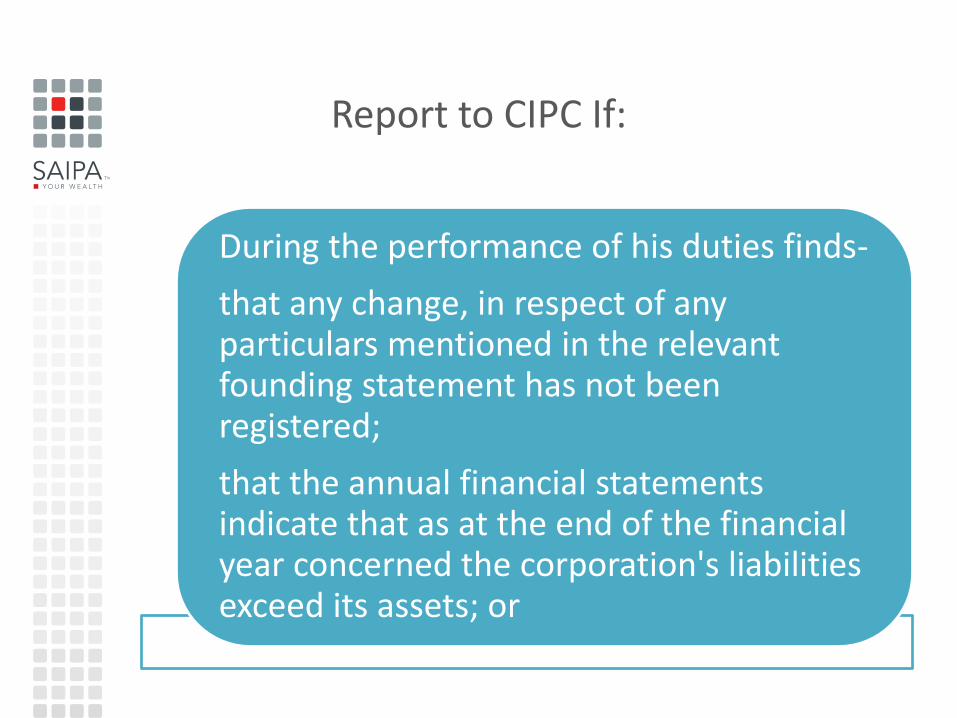

Report to CIPC If:

Has reason to believe, that the corporation is not carrying on business or is not in operation and has no intention of resuming operations in the foreseeable future; or

Report to CIPC If:

During the performance of his duties finds-

that any change, in respect of any particulars mentioned in the relevant founding statement has not been registered;

that the annual financial statements indicate that as at the end of the financial year concerned the corporation's liabilities exceed its assets; or

Report to CIPC:

That the annual financial statements incorrectly indicate that as at the end of the financial year concerned, the assets of the corporation exceed its liabilities, or has reason to believe that such an incorrect indication is given,

Duties of accounting officers

If an accounting officer of a corporation has reported to the Commissioner (CIPC) that the AFS indicate that as at the end of the financial year the corporation's liabilities exceed its assets

and he finds that any subsequent financial statements of the corporation concerned indicate that the situation has changed or has been rectified

and that the assets concerned then exceed the liabilities or that they no longer incorrectly indicate that the assets exceed the liabilities or that he no longer has reason to believe that such an incorrect indication is given, as the case may be,

Must report to the Registrar accordingly.

12

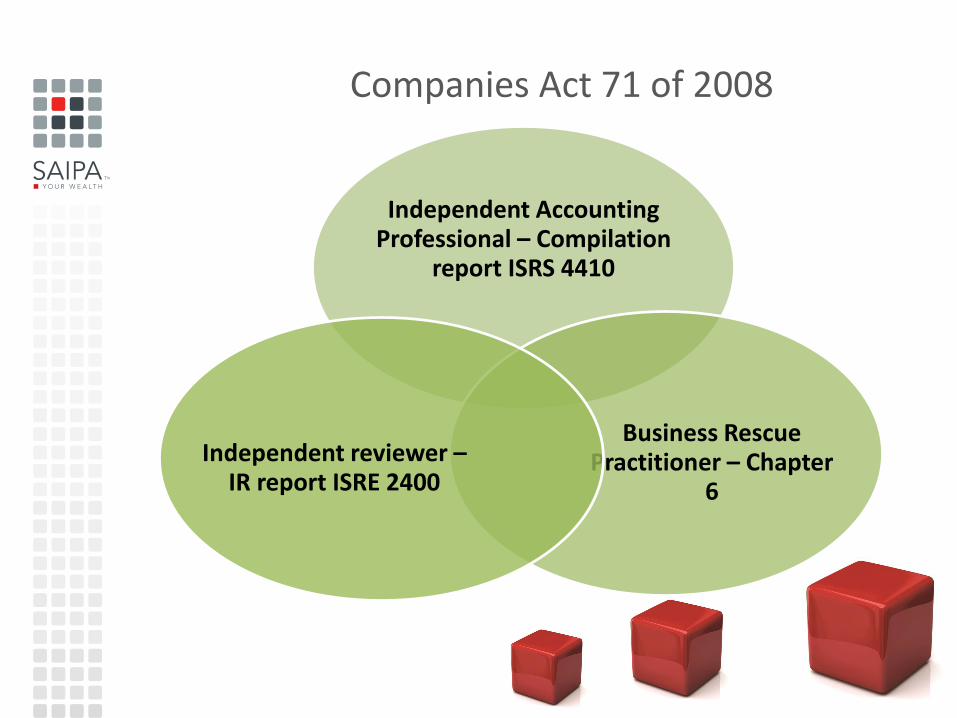

Companies Act 71 of 2008

Independent Accounting Professional – Compilation

report ISRS 4410

Business Rescue Practitioner – Chapter

6

Independent reviewer –IR report ISRE 2400

1. Is the company a public company or astate-owned company?

2. Is company a private company andcontrols fiduciary assets >R5m?

Yes Audit

No

Application of PIS to PrivateCompanies and CCs

Owner Managed

Greater/= than 350 PIS

Yes

No

Audit

No Audit/No

IR

Non-Owner Managed

Less than 350 PIS and greater/equal to than

100 PIS

Independent Review

Int Ext

Less than 100 PIS

Is entity CCYes

Acc Officer Non CA/CA

CA

Greater/= than 350 PIS

Less than 350 PIS and greater/equal

to than 100 PIS

EXT

INT

OM < 100No Aud/IRDuties of Acc Off

Public Interest Score Non owner managed

Public Interest Score Financial Reporting Standard Audit Independent

Review

Independent

Accounting

Professional’s

Report

PIS ≥ 350 IFRS / IFRS for SMEs YES NO YES

PIS ≥100 and < 350 and

AFS were internally

compiled

IFRS / IFRS for SMEs YES NO YES

PIS ≥ 100 and < 350 and

AFS independently

compiled

IFRS / IFRS for SMEs NO YES YES

PIS < 100 and AFS

independently

compiled

IFRS / IFRS for SMEs NO NO YES

PIS < 100 and AFS

internally compiled

The Financial Reporting Standard as

determined by the company for as

long as no Financial Reporting

Standard is prescribed

NO YES YES

15

Public Interest ScoreOwner managed

Public Interest Score Financial Reporting Standard Audit Independent

Review

Independent

Accounting

professional’s or

AO’s Report

PIS ≥ 350 IFRS / IFRS for SMEs YES NO YES

PIS ≥100 and < 350 and

AFS were internally

compiled

IFRS / IFRS for SMEs YES NO YES

PIS ≥ 100 and < 350 and

AFS independently

compiled

IFRS / IFRS for SMEs NO NO YES

PIS < 100 and AFS

independently

compiled

IFRS / IFRS for SMEs NO NO YES

PIS < 100 and AFS

internally compiled

The Financial Reporting Standard as

determined by the company for as

long as no Financial Reporting

Standard is prescribed

NO NO YES

16

Professional Accountant (SA)

Annual Financial Statements

Statement of Financial Position/ Balance Sheet

Statement of Comprehensive income/Income statement

Statement of changes in Equity

Statement of Cash Flows

Reporting

Audit report

Independent review report

Accounting Officers Report

Compilation Report

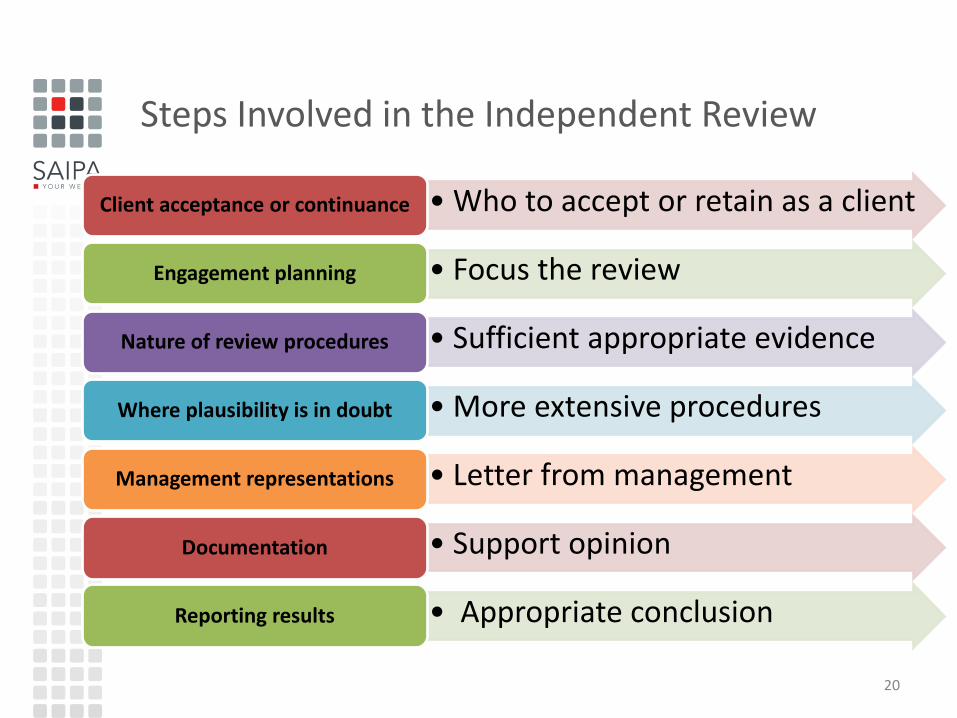

Steps Involved in the Independent Review

20

• Who to accept or retain as a clientClient acceptance or continuance

• Focus the reviewEngagement planning

• Sufficient appropriate evidenceNature of review procedures

• More extensive proceduresWhere plausibility is in doubt

• Letter from managementManagement representations

• Support opinionDocumentation

• Appropriate conclusionReporting results

The core areas to consider in planning are as follows:

21

Planning Discussions

What’s changed this period? Is there any new business or fraud risks to address?

What does the entity do?Who are the key people?What are the key areas of concern to address?

What have we learned from performing previous engagements?

What is the timing of the review engagement and who will be assigned?

What materiality to use?Identify financial statement users and their needs.

What is our response to areas of risk? Where is more work required, and where can we reduce work?

Documenting and Evaluating ResultsThe major steps in a review engagement process are summarized in the following exhibit:

Review

Engagement

Report

Assess Plausibility

Design and Performance of Review Engagement Procedures

The Foundation

The Basic Understanding of the Entity

22

Reportable irregularities

Is a practitioner obliged to report a irregularity? – S29(6)(a)

• A practitioner who performs a mandatory review engagement in terms of the Companies Act, 2008 and Companies Regulations, 2011, is obligated to report a reportable irregularity.

Reportable irregularities

For a reportable irregularity to exist the following must be confirmed

• Was the act performed by a person responsible for the management of the entity?

• Can the act be described as an unlawful act or omission?

• Will the act cause or likely cause a material financial loss to the company or to any member, shareholder, creditor or investor of the company?

• Is the act fraudulent or does it amount to theft?

• Will the act cause or has it caused the company to trade under insolvent circumstances?

Business Rescue Practitioner

Business Rescue Practitioner

A Business Rescue Practitioner (BRP) is a person who has the competencies to facilitate the rehabilitation of a business in financial distress

Accreditation of BRP

Professional Bodies (PB)

BRP –Recognition by

PB

Recognised members

applies for a licence from

CIPC

CIPC accredits Professional Bodies after meeting the accreditation requirements.

Accredited professional body recognises members as BRP based on its set criteria

Recognised BRP applies for a Licence from CIPC

BRP Competence Requirements

Full member of a recognised

Professional Body

Practical Skills

[Practical experience/ training]

Technical Competence

[Recognised Business Rescue or relevant

qualification]

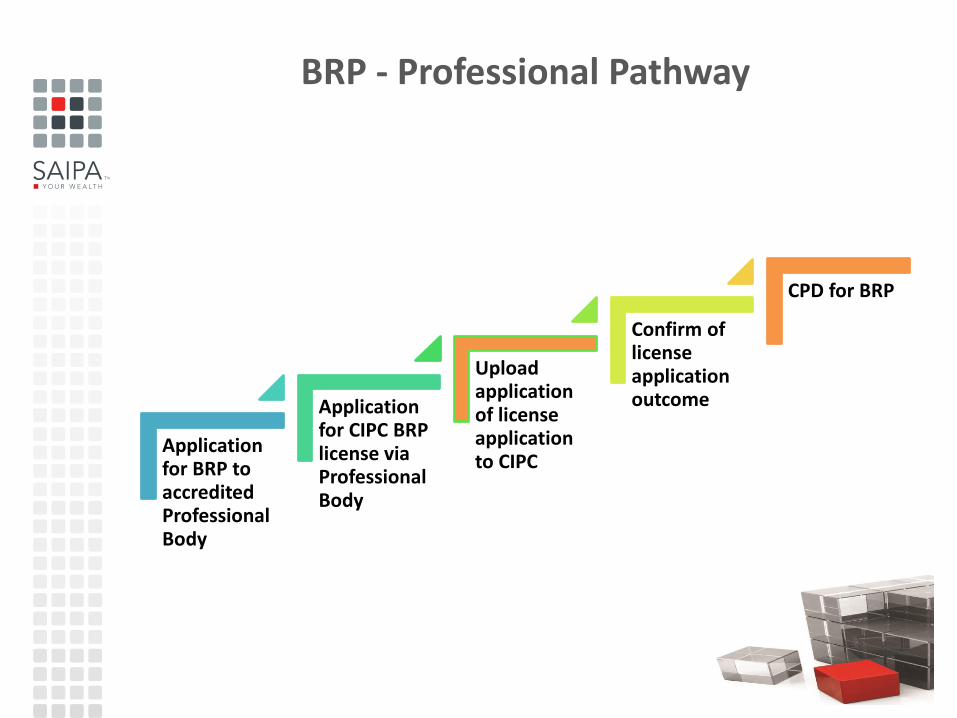

BRP - Professional Pathway

Application for BRP to accredited Professional Body

Application for CIPC BRP license via Professional Body

Upload application of license application to CIPC

Confirm of license application outcome

CPD for BRP

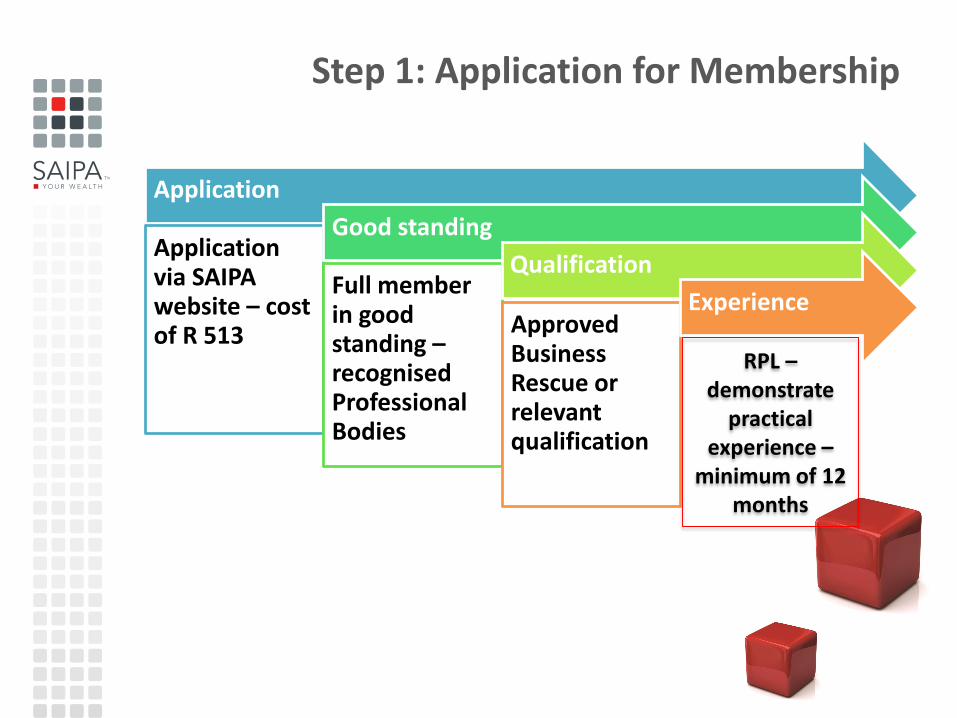

Step 1: Application for Membership

Application

Application via SAIPA website – cost of R 513

Good standing

Full member in good standing –recognised Professional Bodies

Qualification

Approved Business Rescue or relevant qualification

Experience

RPL –demonstrate

practical experience –

minimum of 12 months

STEP 2: Application for CIPC license emailed to [email protected]

Recognised members with a letter of recognition from SAIPA

Completion of COR 126.1 – duly completed and signed

Letter of SAIPA – approval of membership

Supporting documents – certified copies

Sworn statement – s138 independence + legal clearance

History of BRP license - refusal

Future webinar topics

Broad Based Black Economic Empowerment Act

Financial Advisory and Intermediate Act and the Financial Intelligence act

Protection of access to information Act (PAIA) and Protection of Personal Information Act (POPI)

Immigrations Act

Thank you