Embed Size (px)

Citation preview

NAME BRANDS VERSUS STORE BRANDS: A LOOK INTO CONSUMER

PERCEPTIONS OF STORE BRANDS

A THESIS

Presented to

The Faculty of the Department of Economics and Business

The Colorado College

In Partial Fulfillment of the Requirements for the Degree

Bachelor of Arts

By

Wyatt Babb

May 2012

NAME BRANDS VERSUS STORE BRANDS: A LOOK INTO CONSUMER

PERCEPTIONS OF STORE BRANDS

Wyatt Babb

May 2012

Economics

Abstract

Store brands have been gaining popularity and market share over the past century

and nearly all large retailers have their own private label brands. The central focus of this

study was to explore consumer perceptions towards these brands and the factors that

influence these perceptions. We focused on brand name, packaging and store reputation.

A taste test experiment was designed to test only these factors and revile consumer’s true

perceptions. The tests were conducted but not enough data was collected to make

meaningful conclusions. Although our results were not conclusive we found some

interesting patterns and behaviors.

KEYWORDS: (Store Brand, National Brand, Generic, Branding, Taste Test)

TABLE OF CONTENTS

1 INTRODUCTION 1

2 LITERATURE REVIEW 2

2.1 Who Buys Store Brands…………………………………………………...... 3

2.2 Increasing Quality and Multi-Tier Store Brands…………………………..... 5

2.3 Store Brand Loyalty and Store Loyalty Relationship……………………….. 9

2.4 Packaging……………………………………………………………………. 10

2.5 Consumer Perceptions………………………………………………………. 12

2.6 Taste Tests…………………………………………………………………... 14

2.7 Research Questions and Hypotheses………………………………………… 16

3 METHODOLOGY 19

3.1 Subjects……………………………………………………………………… 20

3.2 Procedure……………………………………………………………………. 21

3.3 Instructions………………………………………………………………….. 22

3.4 Product Selection……………………………………………………………. 22

3.5 Experiment Conditions……………………………………………………… 25

3.6 Questionaire…………………………………………………………………. 26

4 RESULTS AND DISCUSION 27

4.1 Questionnaire Results………………………………………………………. 28

4.2 Hypotheses Discusion………………………………………………………. 32

5 CONCLUSION 40

5.1 Sources of Error…………………………………………………………….. 41

5.2 Limitations and Future Research…………………………………………… 42

Appendix A-C 44

LIST OF TABLES

3.1 Taste Test Groups………………….. ………. ……………………………... 21

4.1 Participant Groups…………………………….…………………………….. 27

4.2 Taste Test Results………... ………………………………………………… 28

LIST OF FIGURES

3.1 Chips Ahoy and Ritz………………………….………………………………. 23

3.2 Great Value Cookies and Crackers…………..……………………………….. 24

3.3 King Soopers Cookies and Crackers……………..…………………………... 24

4.1 Question One Results………………………..……………………………….. 29

4.2 Question Two Results….…………………………………………………….. 30

4.3 Question Three Results..……………………………………………………... 31

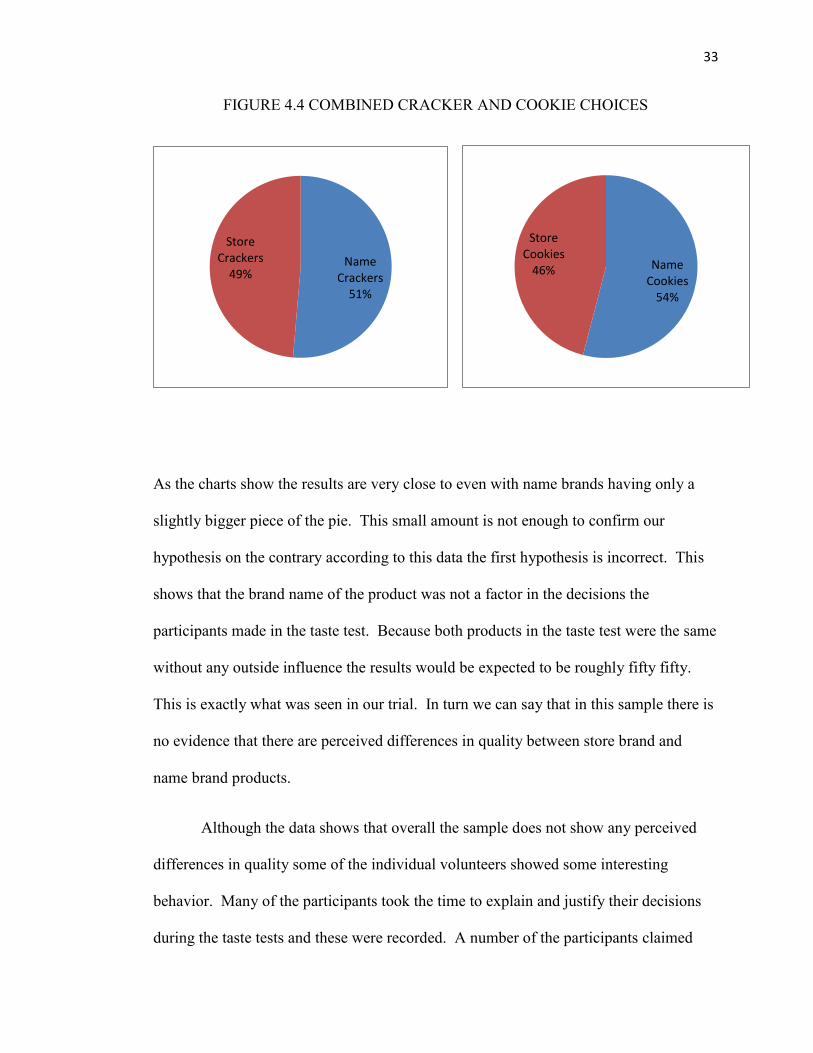

4.4 Combined Cracker and Cookie Choices……………………………………...

4.5 Wal-Mart and King Soopers Cookie Choices………………………………...

4.6 Wal-Mart and King Soopers Cookie Choices………………………………...

4.7 Wal-Mart and King Soopers Combined Choices……………………………..

33

36

37

38

1

CHAPTER I

INTRODUCTION

Everyone at some point in their lives has been in the grocery store and seen store

brand products. All of the big retailers have them in just about every product category.

Wal-Mart has their Great Value line, and Safeway has its Safeway Select label. Costco

has Kirkland Signature and Target has Market Pantry. These products fill the shelves

right next to their brand name counter parts tempting every customer that walks by.

They come in all different types and styles but they almost all have one thing in

common, low prices. Every consumer has seen these goods in the market place but

what do they think of them? Why do they think of them that way? Do they see them as

cheap low quality goods or a great deal? Why would they pay more for a name brand

good? Do they by name brands in some product categories and store brands in others?

This study and many others like it take a deep look at this very subject. This study

focuses on the perceptions consumers have of these store brand goods and what drives

these perceptions.

2

CHAPTER II

LITERATURE REVIEW

Store brands have been a growing force in the retail world over the past century

offering products in a wide variety of categories ranging from marshmallows to facial

tissues. Most big supermarkets and discount stores have their own store brands and they

are typically offered for 15 to 30 percent cheaper than brand names. Because there are

no marketing costs and lower supply costs for store brands, they can be sold at lower

prices than name brands.1 According to the Private Label Manufacturers Association,

store brands have grown in sales by 40 percent annually in supermarkets over the past

decade and now account for almost one out of every four items sold in US supermarkets

and discount stores.2 In 2010 store brand overall sales were around $100 billion. Store

brands have become a large part of retail and many studies have been conducted on the

subject. These studies have focused on many different aspects of store brands from the

consumer, retailer and manufactures points of view.

11

George Baltas, "Determinants of Store Brand Choice: A Behavioral Analysis," Journal of Product &

Brand Management 6, no. 5 (05 1997): 315.

2 "Private Lable Manufacturers Association," [cited 2011]. Available from http://plma.com/.

3

Who Buys Store Brands?

When store brands first hit the market and started becoming popular, a lot of

studies focused on the characteristics of the people who bought store brand goods.

These studies explained the demographics and the behavioral characteristics of the

consumers that are buying store brands and generic products. Demographics are

important pieces of information when marketing a product. It is good for retailers and

manufacturers to know who is buying what so that they can make their products more

appealing and capture more of the market. The studies concerning store brands would

be valuable information for both retailers with store brands and brand names. The

behavioral characteristics of consumers would also be important information that

retailers and manufactures could use to better understand how to appeal to their

customers.

Early studies of store brands and generics focused on demographics. These

studies found characteristics that store brand purchasers were more likely to have than

non store brand purchasers. Previous research generally agreed that store brand buyers

tend to be married, shopping for a lager household, higher educated, and paying a

higher grocery bill.3 The research disagreed on age and income. Granzin argues that

the savings that buying store brands would appeal more to lower income and younger

consumers who out of necessity have to stay on budgets. These were interesting results

and opened up new areas for research around store brands and generic goods. By better

3 Kent L. Granzin, "An Investigation of the Market for Generic Products," Journal of Retailing 57, no. 4

(Winter81 1981): 39.

4

understanding the consumers who buy store brand goods, researchers could look at the

way these consumers make the choice to buy or not to buy store brand goods.

Further research focused on the behavioral characteristics of store brand

consumers. These studies aimed to explain why buyers of store brands and generics act

the way they do. It was found that store brand goods appeal more to consumers who are

open to new products and are more willing to take a chance to find savings without

sacrificing much in the way of quality or taste.4 It was hypothesized that changing to a

new product (especially a store brand) carried a risk of being unsatisfied so to avoid risk

shoppers continue to buy the goods they normally buy. This is referred to as brand

inertia. When consumers are satisfied with the product they purchased on their previous

shopping trip they are reluctant to switch to a new product.5 The result of this can be

that consumers become habitual buyers of certain products. Because of previous

satisfaction with the product consumers will keep purchasing it. This explains why

some consumers are reluctant to try store brands. Another interesting point that has

come up in the research is that consumers are more prone to buy store brands during

economic down turns but they keep buying them after the down turn is over.6 This

suggests that brand inertia can work for both brand names and store brands. This

research shows that there are behavioral characteristics that make certain consumers

more prone to buy store brands and that there is a perceived risk of un-satisfaction when

4 Ibid

5 Marcel Corstjens and Rajiv Lal, "Building Store Loyalty through Store Brands," Journal of Marketing

Research (JMR) 37, no. 3 (08 2000): 281-291. 6 Mercedes Martos-Partal and Óscar González-Benito, "Store Brand and Store Loyalty: The Moderating

Role of Store Brand Positioning," Marketing Letters 22, no. 3 (09 2011): 297-313.

5

switching from one product to another. Researchers have taken this into account and

have done further studies to determine what consumers take into account when

purchasing goods.

This early research revealed a very important concept that plays a huge role in

store brand research and the practices of retailers. The idea is that of a quality-price

trade off. Many of the articles about store brands and generics think of it as a ratio. If

the product has a favorable price-to-quality ratio it then becomes a bargain for the

consumer and they are more likely to purchase it.7 This ratio equates to a perceived

value of the good. The consumer will purchase the good with the higher perceived

value. Price and quality have been a main focus of a lot of the literature concerning

store brand and generic products for obvious reasons. Price and quality are the factors

that determine a products perceived value and therefore if a consumer will buy the

product. Retailers have taken this research to heart and have made changes to their

store brand offerings.

Increasing Quality and Multi-Tier Store Brands

In recent years, the quality of store brands has been climbing to levels as good

as, if not better than that of national brand products. Retailers have increased the value

of their store brand products. This helps explain the tremendous sales growth store

brands have experienced in recent years. Along with broadly increasing quality

retailers have adopted multi-tier store brand offerings with product lines to appeal to all

7Granzin, An Investigation of the Market for Generic Products, 39.

6

customers. Many articles have talked about these trends and how effective they have

been.

In today’s world, store brands are equal and sometimes even better than brand

name goods in quality and taste. This did not use to be the case. In 1981, Granzin

explained in his study how generic and store brand, were more often than not poor

quality goods.8 Retailers have stepped up their game to offer better quality store brand

goods and in turn better value to their customers. According to Consumer Reports in

2005, “buying store brands can not only get you high-quality products, it can save you

hundreds, sometimes thousands, of dollars a year.”9 In 2010, Consumer Reports stated,

“In blind tests, our trained tasters evaluated twenty one pairs of staple foods. Brand

names won seven times; store brands, three. There were eleven ties. Prices are based on

an average of what we found. The store brands cost seven to sixty percent less.”10

Many of the store brand goods are as good as brand names and in some cases they did

better. The fact that many of these products are of similar quality to brand names, and

are cheaper to purchase makes many of them a better value for consumers. In many

cases, store brand products are produced by the same manufacturers that produce brand

name products. That same Consumer Report from 2005 found, “Of the thousands of

manufacturers of store brands, many are national-brand companies.” Manufactures

included Alcoa, Hormel, Del Monte, and solo among others. Baltas argues, “Most own

labels aren’t actually produced by the retailer. Manufacturers may elect to produce

8 Ibid.

9 "Battle of the Brands," Consumer Reports 70, no. 8 (08 2005): 12-15.

10

"Store Brands Vs. Name Brands," Consumer Reports 75, no. 10 (10 2010): 16-21

7

own-label products for retailers in order to achieve scale economies in production and

distribution, utilization of excess capacity, sales increase without marketing costs, as

well as price discrimination.”11

There are a lot of incentives for manufactures to

produce store brand goods. This explains why so many do just that. In most cases

these goods are not just the same product with a different label but they are very similar.

Store brands have become the major competitors boasting similar and sometimes better

quality than name brands and consumers are beginning to take notice. “In many

instances, shoppers no longer can distinguish between national and private label

brands.”12

The Private Label Manufacturers Association also shared, “In a 2010 GfK

Group study half of the respondents said that they had recently switched to the store’s

brand in categories where they had previously only bought a national brand. Nearly all

who did switch were pleased with their decision: nine in ten compared store brands

“favorably” to their national brand choice.” These increases in quality across store

brands are starting to become common knowledge among consumers and may help in

explaining the growing popularity of store brands.

Retailers are encouraging more store brand purchases by offering several lines

of store brand products so they can appeal to a larger share of the market. These

product offerings are designed to meet the differing price and quality demands of

consumers. Martos-Partal and Mercedes explain four general store brand types in their

paper: generics, copycats, premium, and value innovators.13

Generic store brands offer

11

Baltas, Determinants of Store Brand Choice: A Behavioral Analysis, 315.

12

Private Lable Manufacturers Association

13

Martos-Partal and González-Benito, Store Brand and Store Loyalty: The Moderating Role of Store

Brand Positioning, 297-313.

8

the cheapest product in a given category and focus solely on offering the lowest cost

alternative. Copycat store brands do just as the name suggests. They offer similar

products to brand names but for less. Premium store brand products aspire to be the

best products in the category; they may not be cheaper than name brand products but

they are of very high quality. The last group is value innovators. These products focus

on giving consumers the best value in the category. They do this through low prices

and high quality. Store brand product offerings by retailers may include one or all of

these types of products. The trend in recent years is towards multi-tier store brand

offerings. Corstjens shares, “A survey of retailers that carry store brands concludes that

retailers must develop high-quality store brands, not just low-priced brands. Without a

combination of low price and high quality, store brands are not successful.”14

Retailers

need to offer a range of store brands in order to capture consumers with different price

and quality demands. By providing multi-tier store product offerings, retailers can

attract customers away from lower tier name brands and towards higher tier store

brands. Yang talks about this in his study, “the price decrease of high-quality brands

not only provides an opportunity for consumers to switch from low-quality brands to

high-quality brands, but also provides them with higher utility.”15

By offering higher

quality brands at lower prices retailers are able to attract more consumers to their

products. Retailers have started to capture more of the market by offering a wider array

of store brand products. These products have nearly become brands of their own and

14

Corstjens and Lal, Building Store Loyalty through Store Brands, 281-291.

15

Defeng Yang and Xinxin Wang, "The Effects of 2-Tier Store Brands' Perceived Quality, Perceived

Value, Brand Knowledge, and Attitude on Store Loyalty," Frontiers of Business Research in China 4, no.

1 (03 2010): 1-28.

9

rival name brands in quality. With the rise in quality of store brands there has been a lot

of curiosity regarding how store brands affect store loyalty.

Store Brand Loyalty and Store Loyalty Relationship

Store brands have always been unique in that they are goods offered exclusively

at their respective stores. In recent years with the quality of store brands rising along

with their popularity a lot of studies have been looking at how store brand loyalty

relates to store loyalty. Some researchers theorize that store brands can be a form a

differentiation for retailers that helps fosters store loyalty. Some research on the other

hand contradicts this and suggests that high level buyers of store brand goods are

actually less loyal to the store. There is an interesting dynamic between store brand

loyalty and store loyalty that this research has uncovered.

“In Britain, house brands have reached close to half of grocery sales. For

example, Asda’s private label share reached 46 percent, with Sainsbury at 45 percent

and Safeway at 39.4 percent. In some categories, house brands are the market share

leader, creating store loyalty through their exclusive distribution.”16

With store brands

become more popular and their quality rising, retailers are starting to view store brands

as a possible source of differentiation from other retailers. Because store brands are

exclusively offered by their respective retailers, loyalty to store brands can translate into

16

Colleen Collins-Dodd and Tara Lindley, "Store Brands and Retail Differentiation: The Influence of

Store Image and Store Brand Attitude on Store Own Brand Perceptions," Journal of Retailing and

Consumer Services 10, no. 6 (11 2003): 345-352.

10

store loyalty. It is a good theory these studies have not shown any concrete data to

support it.

Packaging

Product packaging has been gaining importance to manufactures and retailer

alike. A recent study found, “Analysis of finding would clearly indicate that there is a

strong association regarding the influence of packaging on the purchase decision, with

over 73 percent of interviewed consumers stating that they relied on packaging to aid

their decision making process at the point of purchase.”17

Other studies have also shown

that packaging is important and it plays a large role consumer decisions. “Good

packaging is far more than a salesman, it is a flag of recognition and a symbol of

values”18

Packaging can serve as a “salesman” and is the face of a product in the store.

Attractive packaging could convince consumer to try a product and unattractive

packaging can discourage consumers from purchasing. With no prior knowledge of a

product the packaging is the consumer’s primary way of judging the quality of a good.

With this in mind many manufactures and retailers have embraced packaging as a

marketing tool. Retailers have embraced this research and begun focusing more on

packaging for their private label brands. “Retailers are hiring more and more top-flight

marketers, designers and advertising agencies. They have embraced the fundamentals of

classic CPG marketing and, now, some have become so sophisticated that they are in a

17 Wells, L. E., H. Farley, and G. A. Armstrong. "The Importance of Packaging Design for Own-Label

Food Brands." International Journal of Retail & Distribution Management 35, no. 9 (09 2007): 677-690.

18 Ibid

11

position to teach brand marketers a thing or two. Packaging is a very effective

marketing tool especially for private label brands.”19

A 2007 study by L. E. Wells, H

Farley and G.A. Armstrong explains, “Given that only a small minority of brands are

strong enough to justify the investment that national advertising requires, for the rest,

packaging represents one of the most important vehicles for communicating brand

massage to the target consumer.”20

Packaging is a cost effective way of marketing a

product directly to consumers. “Private label’s decision to invest in packaging was born

of capital restrictions. Without the massive ad budgets of national brands, retailers had

no choice but to turn the bulk of their focus to packaging”21

This is evident on store

shelves and is a primary reason why packaging is always evolving. “As the retail

environment becomes saturated with competitors vying for consumers attention,

packaging has to work harder than ever if the product is to be noticed through the

congestion of competitive products.”22

Packaging needs to make products stand out

from the competition in order to draw buyers. The studies tend to agree that packaging

is an important marketing tool and attractive packaging can lead to more sales.

19 Koeppel, Jean. "Store Brands Vs. National Brands Who is Coming Out Ahead?" Brand Packaging 14,

no. 6 (07 2010): 22-24.

20

Wells, L. E., H. Farley, and G. A. Armstrong. "The Importance of Packaging Design for Own-Label

Food Brands." 2.

21 Koeppel, Jean. "Store Brands Vs. National Brands Who is Coming Out Ahead?" 22-24.

22

Wells, L. E., H. Farley, and G. A. Armstrong. "The Importance of Packaging Design for Own-Label

Food Brands." 3

12

Consumer Perceptions

The one subject that nearly all the literature agrees on is that consumers have

different perceptions of national brands and private label brands. A 2001 study entitled

“Consumer Perceptions of National, Private, and Generic Brands,” by Bellizzi,

Krueckeberg, Hamilton, and Martin, explored consumer perceptions through interview

surveys.23

The study found that the majority of the people surveyed rated national

brands higher in almost all categories including but not limited to reliability, quality,

texture, purity, desirability, freshness, satisfaction, aroma, and taste. Although the

national brands received the highest ratings in most categories, private labels were rated

as the best value. The study explains, “Consumers may feel that while national brands

are superior to private brands, the purchase and use of private instead of nation brands

do not entail many significant tradeoffs.”24

This study reviles that there are perceptions

by most consumers that national brands are superior to others but it fails to show which

products consumers would purchase. Retailers would want consumers to view their

private label products as comparable to national brands. This study shows that in a

sense but we do not get a real feel of what consumers would pick when purchasing

products; the product with the highest perceived value or the product with the highest

perceived quality.

23 Bellizzi, Joseph A., Harry F. Krueckeberg, John R. Hamilton, and Warren S. Martin. "Consumer

Perceptions of National, Private, and Generic Brands." Journal of Retailing 57, no. 4 (Winter81

1981): 56.

24 Ibid

13

Other studies on the subject have focused on what causes these perceptions and

what influences consumers when making purchasing decisions. Cue utilization theory

explores this subject.25

The theory basically views products as a group of cues both

intrinsic and extrinsic that convey a products quality. Extrinsic cues are ones that are

not directly related to the product itself like brand name, price, and packaging. Intrinsic

cues are the ones that directly relate to the product like ingredients, taste, and texture.

“The cue utilization literature has found repeatedly that brand name is one of the most

important cues of product quality. In fact, blind taste tests have demonstrated that

extrinsic cues, in particular brand name and price, often explain more variance in

perceptions of product quality than do intrinsic cues.”26

This is very interesting because

the majority of consumers would not identify themselves as choosing products based on

extrinsic cues. A 1994 study by found that, “Regardless of the product category or the

actual ingredients sampled, ingredients coupled with national brand extrinsic cues

received significantly more favorable quality assessment than the same ingredients

coupled with store brand extrinsic cues. For example, holding ingredients constant at

the national brand level, national brand extrinsic cues received mean quality assessment

of 5.95; the same ingredients identified with the extrinsic cues of Store I and Store II

brands received mean quality ratings of 5.20 and 5.29, respectively.”27

This study

showed that based only on extrinsic cues national brands were rated better in quality.

25

Colleen Collins-Dodd and Tara Lindley, "Store Brands and Retail Differentiation: The Influence of

Store Image and Store Brand Attitude on Store Own Brand Perceptions," 2.

26

Colleen Collins-Dodd and Tara Lindley, "Store Brands and Retail Differentiation: The Influence of

Store Image and Store Brand Attitude on Store Own Brand Perceptions," 2.

27 Richardson, Paul S., Alan S. Dick, and Arun K. Jain. "Extrinsic and Intrinsic Cue Effects on

Perceptions of Store Brand Quality." Journal of Marketing 58, no. 4 (10 1994): 28.

14

Based on these results it is safe to say that extrinsic cues play a large in building

consumer perceptions towards goods and therefore product purchasing choices.

Taste Tests

Taste tests have been steadily becoming a more widely used tool in food product

marketing. They are mostly used to change consumer’s perceptions about a product or

draw in new customers. A 2001 article by Ghose and Lowengart explains, “Taste tests

are a common activity of marketers in various industries. Such tests are major selling

and advertising message design tools that are aimed at convincing potential customers

about the superiority of one brand over another.”28

For years these taste tests have been

used for marketing and a lot of examples come to mind. The Pepsi Challenge created in

1975 is a prime example that is fairly well known. Pepsi simple challenged consumers

to do a blind taste test comparing Coke to Pepsi. Other examples simply state taste test

results, for example: 68% of people prefer product A to Product B in taste tests. Coors

did this in a 1991 add campaign against Budweiser.29

There are many variations of

these taste tests but their primary focus is to show one product’s superiority over

another.

28

Ghose, Sanjoy, and Oded Lowengart. "Taste Tests: Impacts of Consumer Perceptions and Preferences

on Brand Positioning Strategies." Journal of Targeting, Measurement & Analysis for Marketing 10, no. 1

(08 2001): 26.

29

Ibid

15

The business world has taken a different focus when it comes to taste test.

“Several academic studies have looked at the different perspectives of taste testing.

Broadly these measurements of taste can be divided into two categories: perceptual

discrimination tests and preference tests”30

Perceptual discrimination tests are designed

to see if consumers can tell the product apart from other similar products. This type of

taste test would be useful in launching a new product or comparing the quality of two

very similar products. Preference tests are used to rank a product against competing

products. These two types of tests reveal the biggest concerns for companies selling

products. Ghose an Lowengart would argue, “It is clear then that with respect to taste

testing, two factors dominate. One is the consumers’ perceptions of the dissimilarity

between brands and the other is their feelings of preference for each brand.”31

This

subject has also been the interest of academics. A 1994 study entitled “Extrinsic and

Intrinsic Cue Effects on Perceptions of Store Brand Quality” used taste tests to explore

consumer perceptions.32

The study used manipulated taste tests to view the role

extrinsic cues had on consumer’s perceptions. They volunteers were given packaging

and other extrinsic cues to examine like: price, ingredients, and nutritional information.

The volunteers were then asked to sample the product and rate it. The product given to

the volunteers was not necessarily the product that the extrinsic cues represented. This

30

Ibid

31

Ibid

32 Richardson, Paul S., Alan S. Dick, and Arun K. Jain. "Extrinsic and Intrinsic Cue Effects on

Perceptions of Store Brand Quality." 28.

16

study used taste tests to discover consumer’s true perceptions about goods. Taste tests

have long been a reliable tool for discovering or changing consumer perceptions.

Research Questions and Hypotheses

The academic literature on the subject of private label goods has left some

lingering questions that I feel need to be better explored. The literature does a good job

of exploring subjects but they cover a very wide focus or they bring up new areas that

need to be explored.

The first research question of this study was inspired by the 1994 study by Paul

S. Richardsoii, Alan S. Dick, and Arun K. Jain entitled “Extrinsic and Intrinsic Cue

Effects on Perceptions of Store Brand Quality”.33

Their study examined the roles

extrinsic and intrinsic cues have on consumers. They found that extrinsic cues had

more influence over consumer’s perceptions than intrinsic cues. This study aims to take

these results and explore them further. How does brand alone affect consumer

perceptions of a good, specifically between store band and name brand goods? Collins-

Dodd and Lindley explain, “In fact, blind taste tests have demonstrated that extrinsic

cues, in particular brand name and price, often explain more variance in perceptions of

product quality than do intrinsic cues.”34

It has been found that extrinsic cues have a

33

Ibid

34

Colleen Collins-Dodd and Tara Lindley, "Store Brands and Retail Differentiation: The Influence of

Store Image and Store Brand Attitude on Store Own Brand Perceptions," 2.

17

large impact on consumer perceptions but how large of a role does brand name alone

play?

Hypothesis one: Brand name has a large effect on consumer perceptions towards

a product, and more specifically consumers perceive name brand products to be

superior to store brand products.

The second research question of this study was also inspired by “Extrinsic and

Intrinsic Cue Effects on Perceptions of Store Brand Quality.” Like the first research

question this question focuses on specific extrinsic cues. Product packaging is said to

be one of the most important extrinsic cues so we decided to make it the focus of the

second hypothesis. How does a product’s packaging affect consumer perceptions

towards that product? Does a more appealing packaging give a product a more

favorable perception to consumers? Does imitating name brand product packaging

make private label goods more alluring or does it simply make them disappear on the

shelf?

Hypothesis two: Appealing product packaging has a positive effect on consumer

perceptions of that product.

The third research question was inspired by “Store brands and retail

differentiation: the influence of store image and store brand attitude on store own brand

18

perceptions” a 2003 study by Colleen Collins-Dodd and Tara Lindley.35

Their study

examines consumer perceptions towards store brands and store image. The study found

a positive relationship between a stores image and perceptions of its private label

brands. Our study wants to recreate the results of this study. Store brands are in a way

an extension of the store so it would make sense that consumer perceptions of the store

influence consumer perceptions of that store’s private label goods. This leads to

Hypothesis three: Private label goods will be perceived as better if the store they

originate from is perceived highly by consumers. In other words if a store is

perceived as a good store its private label goods will be perceived better.

35

Ibid

19

CHAPTER III

METHODOLOGY

Overview

To test my hypotheses, we designed an experiment with intentions of revealing

subjects perceptions towards store brands and national brands based only on the brands

themselves. The experiment was also designed to explore how differences in store

reputation or store brand packaging affect consumer’s perception of store’s brands.

Room 119 in the Economics Department in Palmer Hall was the sight of the

experiment. It was set up like a taste test that subjects take one at a time. Outside the

room an assistant checked subjects in and had them fill out a consent form as well as a

quick survey. In the room there was a table with two packages of each category,

crackers and cookies; a store brand and a name brand product of each. The chosen

products looked almost identical to one another. In front of each of the packages there

was a sample that the subject will taste test. Both samples were of the store brand

product. The subjects assumed that the samples represent the product they are in front

of, and if they asked during the taste test, we were not allowed to answer. The subject

was then asked to pick their favorite in each category. If the subjects have no

perceptions about name brands versus store brands the experiment should result in

around fifty percent preferring the store brand and fifty percent preferring the name

brand in both categories. We will test the effect of store reputation and packaging on

20

that store’s brand by changing the store brand that is used in the experiment. If the

same results are seen for the two store’s brands then store reputation has no effect.

Subjects

The experiment was designed to provide the best results if 100 or more subjects

participate. These subjects were told that they were participating in a taste test to

research snack food preferences. The subjects were people over the age of 18 and

include Colorado College students, Colorado College faculty and staff, and members of

the Colorado Springs community. Subjects were recruited using the Colorado College

list server, bulletin boards, class announcements, and emails. The majority of the

participants were recruited through personal emails. The subjects were told that they

would be put into a drawing for $45 worth of prizes. Each subject was randomly put in

one of four groups. The first group sampled crackers first and cookies second with

Wal-Mart store brand “Great Value.” The second group sampled cookies first and

crackers second with Great Value. The third group sampled crackers first and cookies

second with King Soopers store brand “Kroger.” The fourth group will sample cookies

first and crackers second with Kroger. Subjects completed the taste test one at a time in

a controlled environment. The experiment took aproximently five minutes per subject.

Upon completing the experiment subjects were asked not to talk about the experiment

until after all the subjects have completed the experiment. When all the subjects had

completed the experiment, We sent out a debriefing letter of the experiment to explain

what the experiment was truly about. (See appendix A)

21

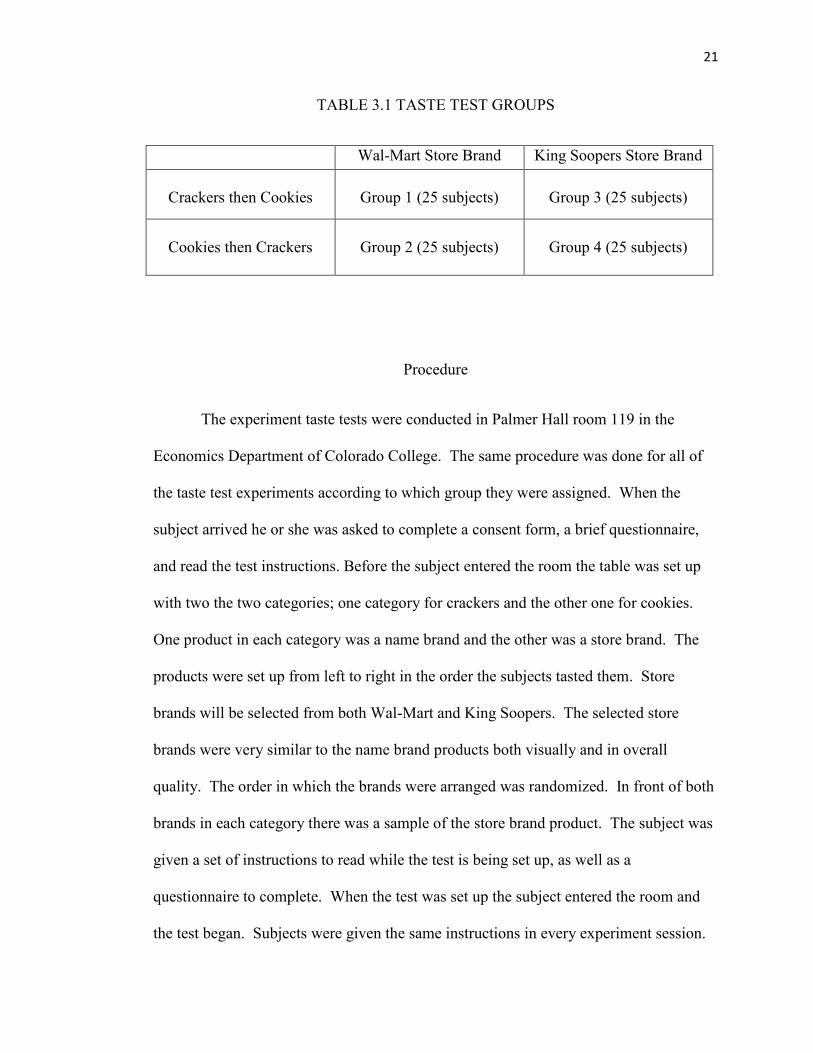

TABLE 3.1 TASTE TEST GROUPS

Wal-Mart Store Brand King Soopers Store Brand

Crackers then Cookies

Group 1 (25 subjects)

Group 3 (25 subjects)

Cookies then Crackers

Group 2 (25 subjects)

Group 4 (25 subjects)

Procedure

The experiment taste tests were conducted in Palmer Hall room 119 in the

Economics Department of Colorado College. The same procedure was done for all of

the taste test experiments according to which group they were assigned. When the

subject arrived he or she was asked to complete a consent form, a brief questionnaire,

and read the test instructions. Before the subject entered the room the table was set up

with two the two categories; one category for crackers and the other one for cookies.

One product in each category was a name brand and the other was a store brand. The

products were set up from left to right in the order the subjects tasted them. Store

brands will be selected from both Wal-Mart and King Soopers. The selected store

brands were very similar to the name brand products both visually and in overall

quality. The order in which the brands were arranged was randomized. In front of both

brands in each category there was a sample of the store brand product. The subject was

given a set of instructions to read while the test is being set up, as well as a

questionnaire to complete. When the test was set up the subject entered the room and

the test began. Subjects were given the same instructions in every experiment session.

22

They were first asked to taste the samples in the first category. The subjects were given

water to cleanse their pallet in between samples. They were then asked to indicate

which sample they liked best and it was recorded on the back of their questionnaire.

Next they were asked to test the next set of samples in the same way. They were asked

to again indicate which sample they liked the best and it was recorded. The subjects

were then asked not to discuss the experiment until all of the subjects have completed

the taste test and they will be excused.

Instructions

The subjects were each given an instructions sheet that tells them what they will

be doing when they come into the room to participate in the experiment. This will help

the experimenter with giving the test and also minimize the amount of verbal contact

needed to administer the test. (See appendix B)

Product selection

There were several considerations to take into account when choosing the

products for the taste test. First was the type of food. The foods chosen were simple

and have very little variation in taste, quality, or visual appeal. Also we wanted product

categories that had a clear market leader as well as high brand recognition. With all of

this in mind, we chose Ritz crackers and Chunky Chips Ahoy cookies as the name

brand products for the taste tests. Ritz and Chips Ahoy are both highly recognized

brands and a lot of private label brands have products targeting these product categories.

23

FIGURE 3.1 CHIPS AHOY AND RITZ

Next the store brands that would be tested were selected. First we considered which

stores we would get the store brand products from. We selected Wal-Mart and King

Soopers. Wal-Mart was picked because it is known as a low cost provider and they

retail a large variety of products other than groceries. We selected King Soopers

because they are a traditional grocery store and they employ a different packaging

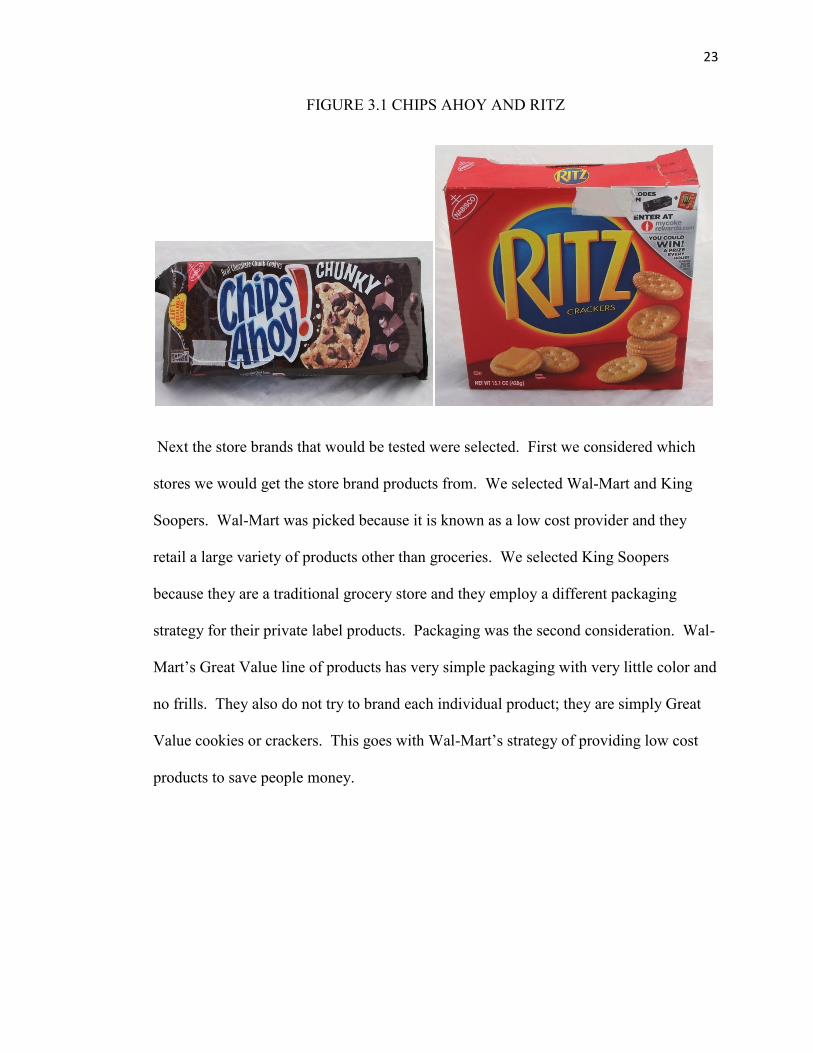

strategy for their private label products. Packaging was the second consideration. Wal-

Mart’s Great Value line of products has very simple packaging with very little color and

no frills. They also do not try to brand each individual product; they are simply Great

Value cookies or crackers. This goes with Wal-Mart’s strategy of providing low cost

products to save people money.

24

FIGURE 3.2 GREAT VALUE COOKIES AND CRACKERS

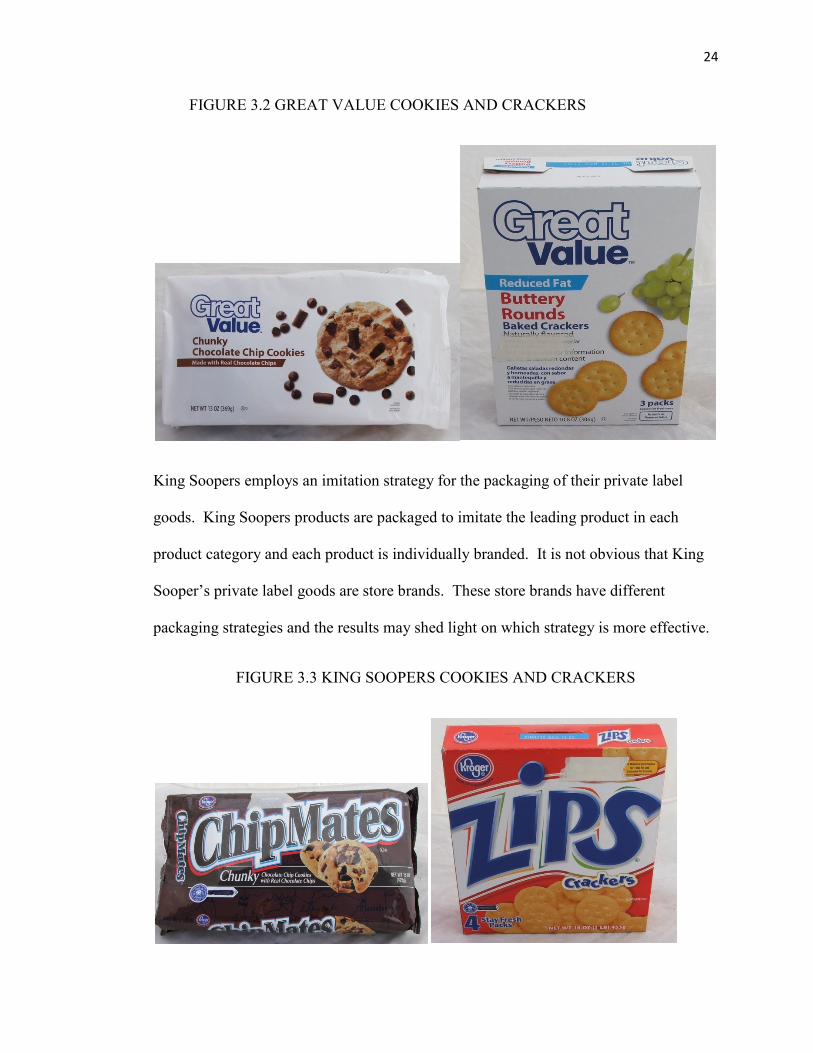

King Soopers employs an imitation strategy for the packaging of their private label

goods. King Soopers products are packaged to imitate the leading product in each

product category and each product is individually branded. It is not obvious that King

Sooper’s private label goods are store brands. These store brands have different

packaging strategies and the results may shed light on which strategy is more effective.

FIGURE 3.3 KING SOOPERS COOKIES AND CRACKERS

25

The six products used for the tests were Ritz crackers, Chunky Chips Ahoy cookies,

Great Value buttery rounds crackers, Great Value chocolate chip cookies, Kroger Chip

Mate cookies, and Kroger Zips crackers. Ritz crackers and Chips Ahoy were both

$2.50 each. The Great Value cookies and King Soopers cookies were $2.18 and $1.99

respectively. The Great Value crackers were $1.38. King Soopers Zips crackers were

more expensive than the Ritz crackers coming in at $2.89.

Experiment Conditions

The taste tests were conducted in a small classroom. Two tables were set up;

one outside the room and one inside the room. The table outside the room served as a

check-in area for the subjects. An assistant checked in subjects and gave them a

questionnaire and consent form to fill out. The assistant also had the subjects read the

taste test instructions while they wait for the taste test to be set up. At this table there

was also Power Point presentation and flyers to help recruit walk-in subjects. The table

inside the room was set up right inside the door with two chairs on opposite sides of the

table from each other. The taste test was set up according to the group each individual

subject is put in. The taste test samples were placed in front of the product packaging

that they represent in the test. In the middle of the table there was a cup of water for

each subject.

During the set up process the packages of the products were censored. Some of

the packages had writing on them that did not pertain to the brand or the store they

came from that could have influenced the subjects. These writings included things like

26

“0 grams fat” on both of the King Super’s products, “reduced fat” on the Wal-Mart

crackers, and “vegetarian” on the King Super’s cookies. Because these writings on the

package are not the focus of the study they were censored. Pieces of tape were used to

censor the packages. The tape will be put on all of the packages even if they don’t have

writing that needs censored so that the tape itself will not have an effect on the subject

choices.

Questionnaire

Each subject completed a short questionnaire focusing on some demographics

and consumer preferences. We wrote the questions to look at some of the areas that

other studies have looked at. Some questions will give insight into the hypotheses that

We have made. Specifically question two showed how important store reputation is and

question five will give insight into how much consumers are affected by packaging.

These are the questions on the questionnaire.

27

CHAPTER IV

RESULTS AND DISCUSION

The taste test experiments gathered data from 37 subjects who included

Colorado College students, staff, faculty, as well as members from the surrounding

community. The composition of the sample was: 5 CC faculty/staff members, 30 CC

students and 7 members of the surrounding community. The participants were put in to

the four main test groups as follows.

TABLE 4.1 PARTICIPANT GROUPS

Wal-Mart Store Brand King Soopers Store Brand

Crackers then Cookies

10 Participants

9 Participants

Cookies then Crackers

9 Participants

9 Participants

The following table shows the results of the taste tests. The data from the groups were

compared using T-tests and no substantial differences in the samples were found so the

data could be combined.

28

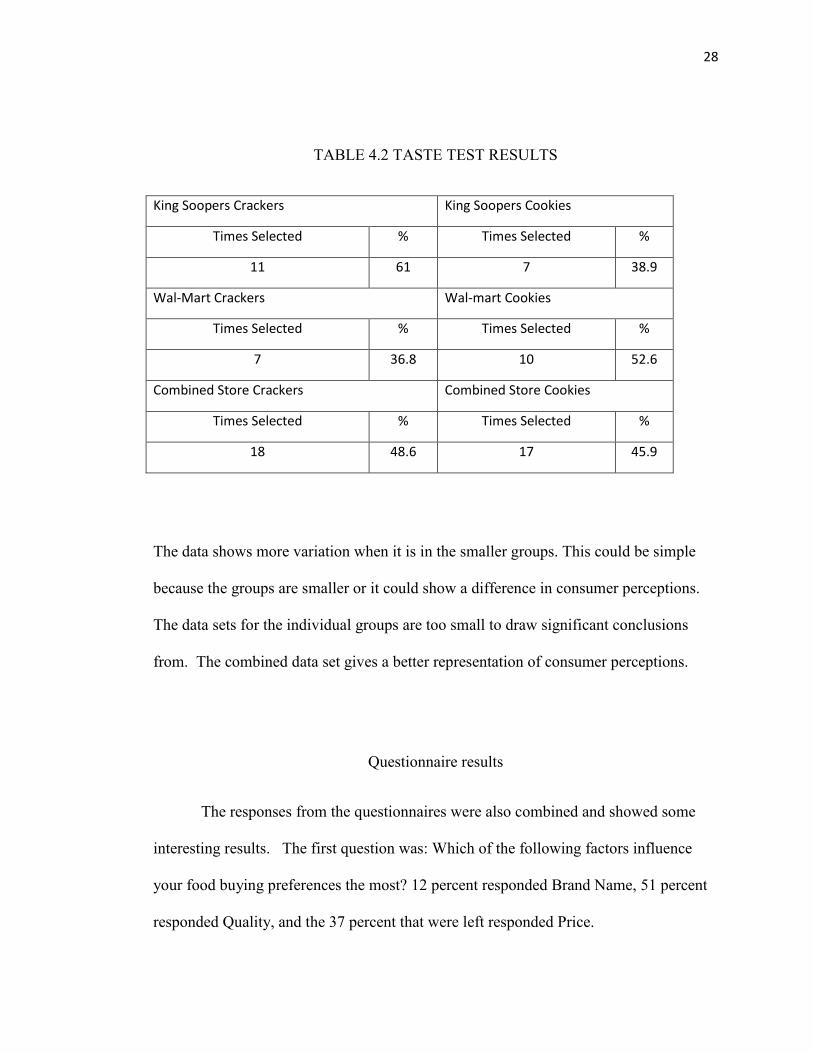

TABLE 4.2 TASTE TEST RESULTS

King Soopers Crackers King Soopers Cookies

Times Selected % Times Selected %

11 61 7 38.9

Wal-Mart Crackers Wal-mart Cookies

Times Selected % Times Selected %

7 36.8 10 52.6

Combined Store Crackers Combined Store Cookies

Times Selected % Times Selected %

18 48.6 17 45.9

The data shows more variation when it is in the smaller groups. This could be simple

because the groups are smaller or it could show a difference in consumer perceptions.

The data sets for the individual groups are too small to draw significant conclusions

from. The combined data set gives a better representation of consumer perceptions.

Questionnaire results

The responses from the questionnaires were also combined and showed some

interesting results. The first question was: Which of the following factors influence

your food buying preferences the most? 12 percent responded Brand Name, 51 percent

responded Quality, and the 37 percent that were left responded Price.

29

FIGURE 4.1 QUESTION ONE RESULTS

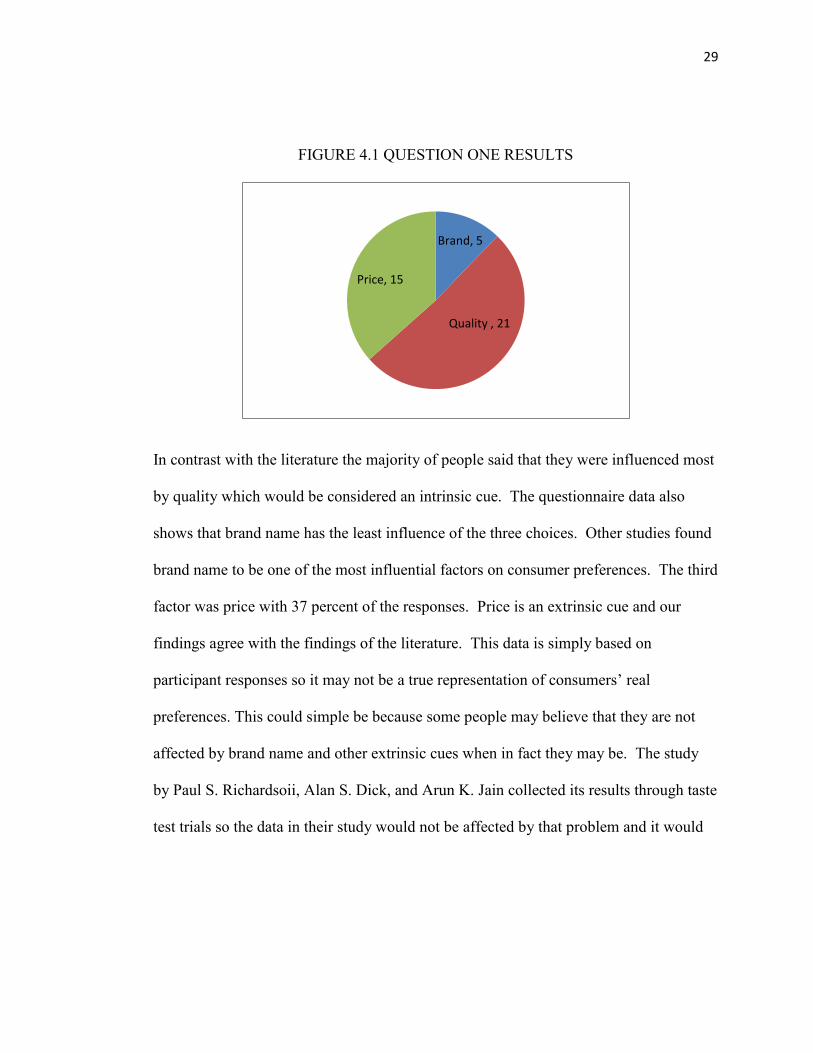

In contrast with the literature the majority of people said that they were influenced most

by quality which would be considered an intrinsic cue. The questionnaire data also

shows that brand name has the least influence of the three choices. Other studies found

brand name to be one of the most influential factors on consumer preferences. The third

factor was price with 37 percent of the responses. Price is an extrinsic cue and our

findings agree with the findings of the literature. This data is simply based on

participant responses so it may not be a true representation of consumers’ real

preferences. This could simple be because some people may believe that they are not

affected by brand name and other extrinsic cues when in fact they may be. The study

by Paul S. Richardsoii, Alan S. Dick, and Arun K. Jain collected its results through taste

test trials so the data in their study would not be affected by that problem and it would

Brand, 5

Quality , 21

Price, 15

30

produce more reliable results.1 With this in consideration we cannot draw any

conclusions based on the results from this question.

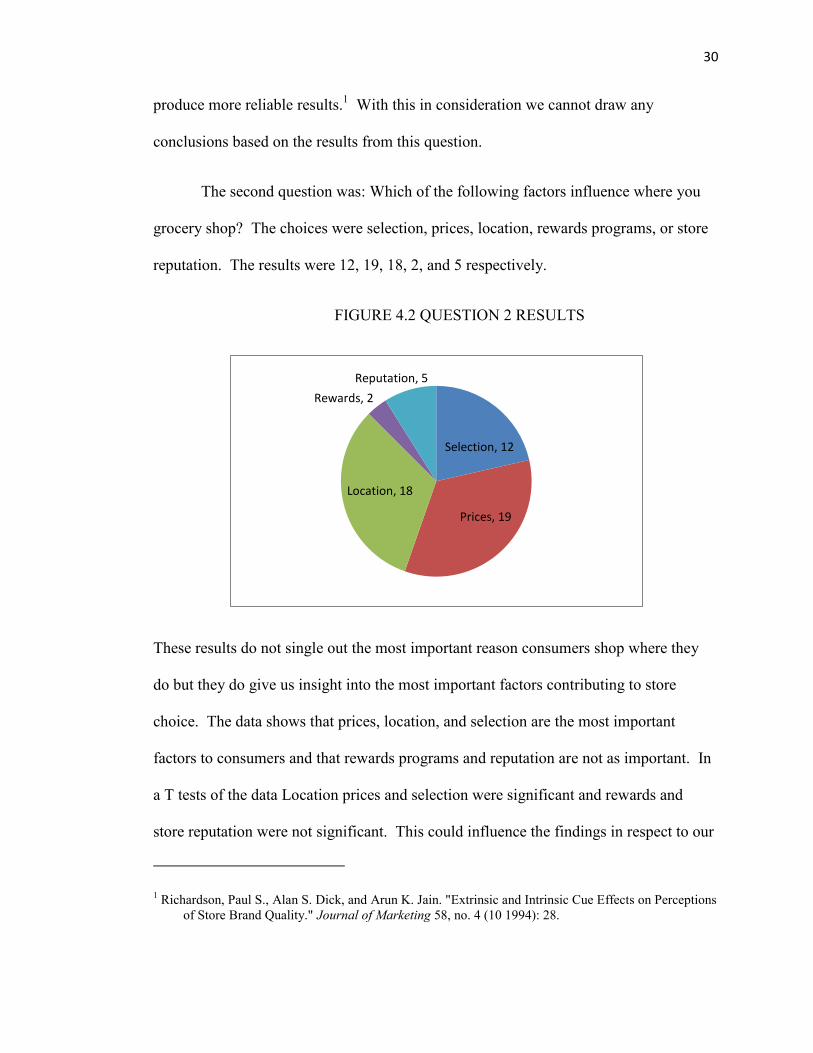

The second question was: Which of the following factors influence where you

grocery shop? The choices were selection, prices, location, rewards programs, or store

reputation. The results were 12, 19, 18, 2, and 5 respectively.

FIGURE 4.2 QUESTION 2 RESULTS

These results do not single out the most important reason consumers shop where they

do but they do give us insight into the most important factors contributing to store

choice. The data shows that prices, location, and selection are the most important

factors to consumers and that rewards programs and reputation are not as important. In

a T tests of the data Location prices and selection were significant and rewards and

store reputation were not significant. This could influence the findings in respect to our

1 Richardson, Paul S., Alan S. Dick, and Arun K. Jain. "Extrinsic and Intrinsic Cue Effects on Perceptions

of Store Brand Quality." Journal of Marketing 58, no. 4 (10 1994): 28.

Selection, 12

Prices, 19

Location, 18

Rewards, 2

Reputation, 5

31

third hypothesis which will be talked about later in this chapter. These findings are

parallel to the findings of other research on demographics so we believe they are a fair

and accurate sample.

The next to questions were simple demographic questions and did not provide

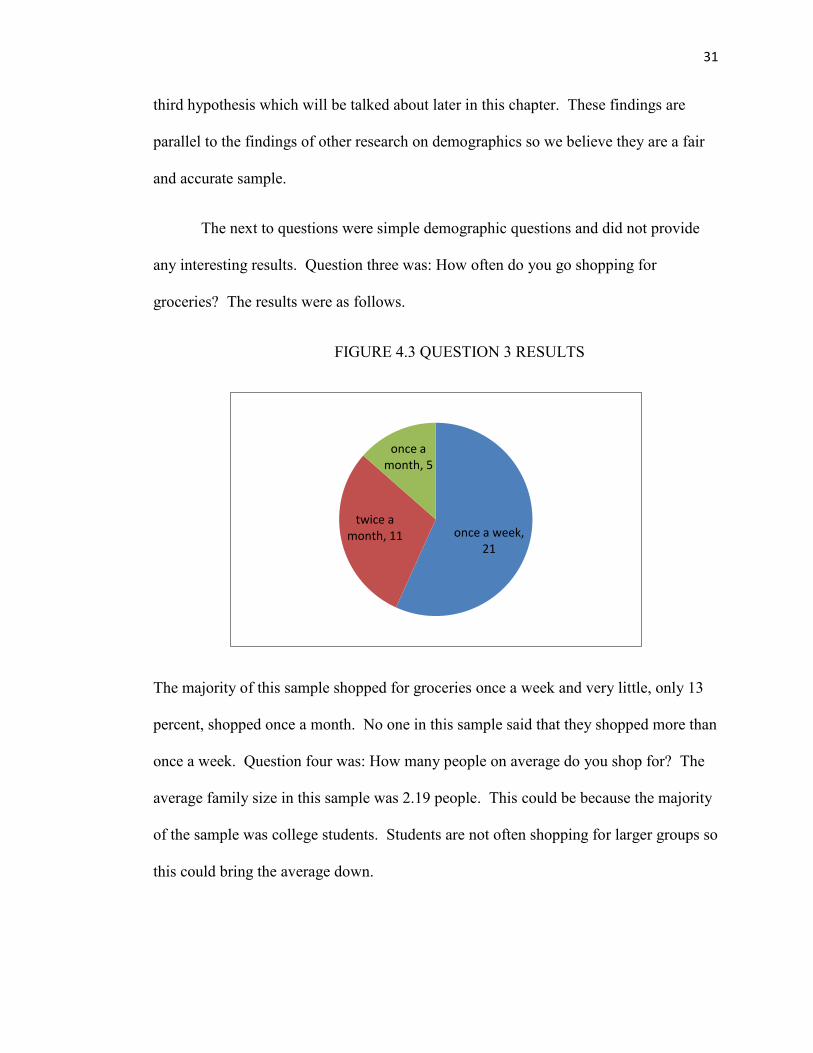

any interesting results. Question three was: How often do you go shopping for

groceries? The results were as follows.

FIGURE 4.3 QUESTION 3 RESULTS

The majority of this sample shopped for groceries once a week and very little, only 13

percent, shopped once a month. No one in this sample said that they shopped more than

once a week. Question four was: How many people on average do you shop for? The

average family size in this sample was 2.19 people. This could be because the majority

of the sample was college students. Students are not often shopping for larger groups so

this could bring the average down.

once a week, 21

twice a month, 11

once a month, 5

32

The final question on the questionnaire focused on packaging. How much does

product packaging affect your grocery purchases from 1(low) to 10(high)? The average

response was five. It is clear that packaging has some influence on all consumers. Four

volunteers in this sample responded with one, saying that packaging had no effect on

their purchasing behavior. The thirty three respondents, or eighty nine percent, that

were left responded that packaging does have an effect. Thirteen of these respondents

gave ratings of seven or above meaning that packaging played a major role in their

purchasing behaviors. This goes along with the study by L. E. Wells, H Farley and

G.A. Armstrong in which seventy three percent of participants agreed that packaging

played a role at the point of purchase.2 This data will be discussed further in the section

regarding hypothesis two.

Hypothesis Discussion:

Hypothesis One

The first hypothesis was the main focus of this study. Based on the findings of

other studies we expected to see a clear perception difference between the products

presented in each category during the taste testes. We hypothesized that brand name

has a large effect on consumer perceptions towards a product, and more specifically

consumers perceive name brand products to be superior to store brand products. This

was not supported with our data.

2 Wells, L. E., H. Farley, and G. A. Armstrong. "The Importance of Packaging Design for Own-Label

Food Brands." 2.

33

FIGURE 4.4 COMBINED CRACKER AND COOKIE CHOICES

As the charts show the results are very close to even with name brands having only a

slightly bigger piece of the pie. This small amount is not enough to confirm our

hypothesis on the contrary according to this data the first hypothesis is incorrect. This

shows that the brand name of the product was not a factor in the decisions the

participants made in the taste test. Because both products in the taste test were the same

without any outside influence the results would be expected to be roughly fifty fifty.

This is exactly what was seen in our trial. In turn we can say that in this sample there is

no evidence that there are perceived differences in quality between store brand and

name brand products.

Although the data shows that overall the sample does not show any perceived

differences in quality some of the individual volunteers showed some interesting

behavior. Many of the participants took the time to explain and justify their decisions

during the taste tests and these were recorded. A number of the participants claimed

Name Cookies

54%

Store Cookies

46% Name

Crackers 51%

Store Crackers

49%

34

that the Chips Ahoy cookies had “Better Chocolate” or that they were “cruncher” even

though they essentially tasted the same cookie twice. These participants claimed that

the Chips Ahoy cookie was greatly superior to the store brand cookie. Perhaps these

participants held a preconceived notion that Chips Ahoy Cookies were the better quality

product and therefore used “better chocolate” or tasted better. This type of behavior

was also seen in the cracker category but it was never seen in favor of the store brand

product only for the name brand product. It is possible that these participants have

perceptions of goods based on brand name. The explanations of participants also

showed that these perceptions may be based only in certain categories. Many of the

participants that claimed the name brand product to be greatly superior in one category

then chose the store brand product in the other category. This would suggest that brand

perceptions may be different for different categories of products. These responses

would suggest that the first hypothesis still has some validity.

Participants in the study often stated that they could not tell the difference

between the two products. When this happened they were picking a product based on

something other than taste. Both the name brand product and the store brand product

were chosen. In the case of the name brand product being chosen this could have been

for several reasons. First the participant could not tell a difference so they chose the

name brand product because it is better know or more popular. They may have also

chosen the name brand because they perceive it to be a better product even though they

could not taste the difference. Another reason could be that the name brand is the

product they regularly buy and they chose it because of brand inertia. In the case of the

store brand product being chosen there are also several explanations. First the

35

participant could have inferred that the store brand product would cost less and

therefore had a better price-to-quality ratio and selected it for that reason. This would

reflect the results from question one of the questionnaire. Price maters more than brand

name with quality being held equal.

Based on these findings I do not believe the first hypothesis can neither be

denied or confirmed. There is data that would render the hypothesis false but there

were also findings that support the hypothesis. The collection of more data would be

the best way to further test this hypothesis.

Hypothesis Two

The second hypothesis like the first focuses on the effect of extrinsic cues on

purchasing decisions. Based on other research we expect that products with more

appealing packaging will be selected more than other products. We hypothesized that

appealing product packaging has a positive effect on consumer perceptions of that

product. According to the questionnaire packaging has some effect on a majority of the

participants in our study. With this in mind to test this hypothesis we will look at the

data for all of the products and relate that data to the packaging of each product. First

we will look at the cookie category.

36

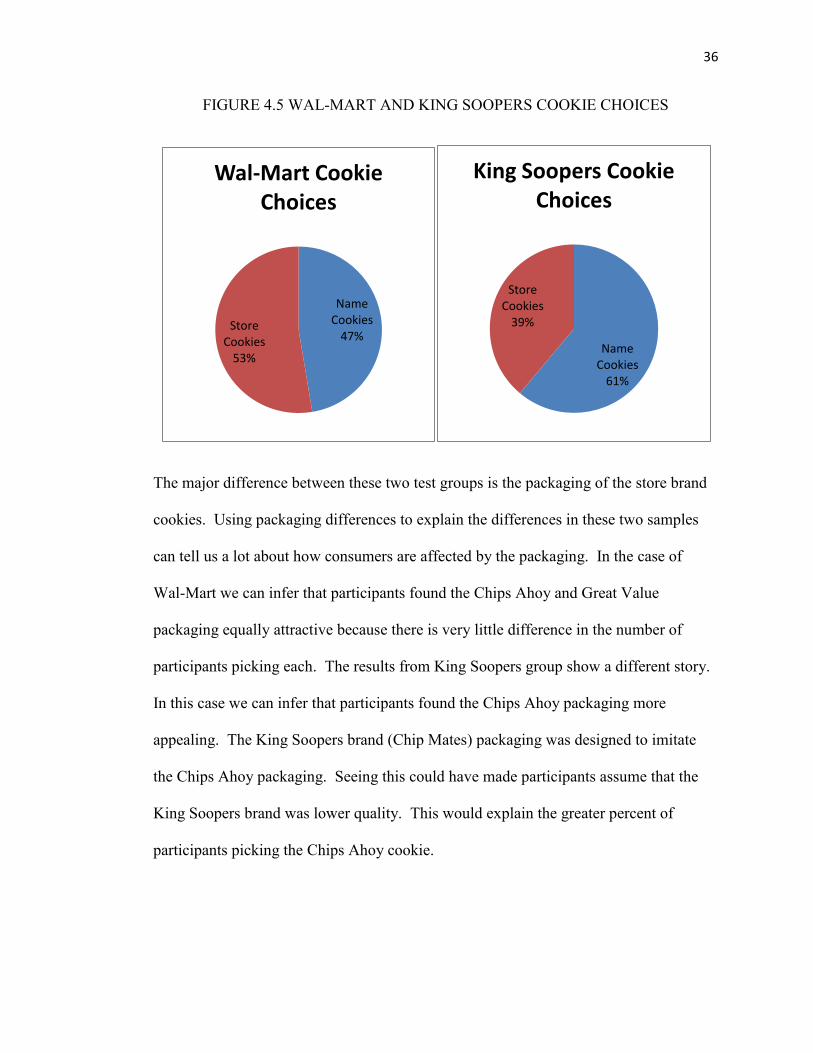

FIGURE 4.5 WAL-MART AND KING SOOPERS COOKIE CHOICES

The major difference between these two test groups is the packaging of the store brand

cookies. Using packaging differences to explain the differences in these two samples

can tell us a lot about how consumers are affected by the packaging. In the case of

Wal-Mart we can infer that participants found the Chips Ahoy and Great Value

packaging equally attractive because there is very little difference in the number of

participants picking each. The results from King Soopers group show a different story.

In this case we can infer that participants found the Chips Ahoy packaging more

appealing. The King Soopers brand (Chip Mates) packaging was designed to imitate

the Chips Ahoy packaging. Seeing this could have made participants assume that the

King Soopers brand was lower quality. This would explain the greater percent of

participants picking the Chips Ahoy cookie.

Name Cookies

47% Store

Cookies 53%

Wal-Mart Cookie Choices

Name Cookies

61%

Store Cookies

39%

King Soopers Cookie Choices

37

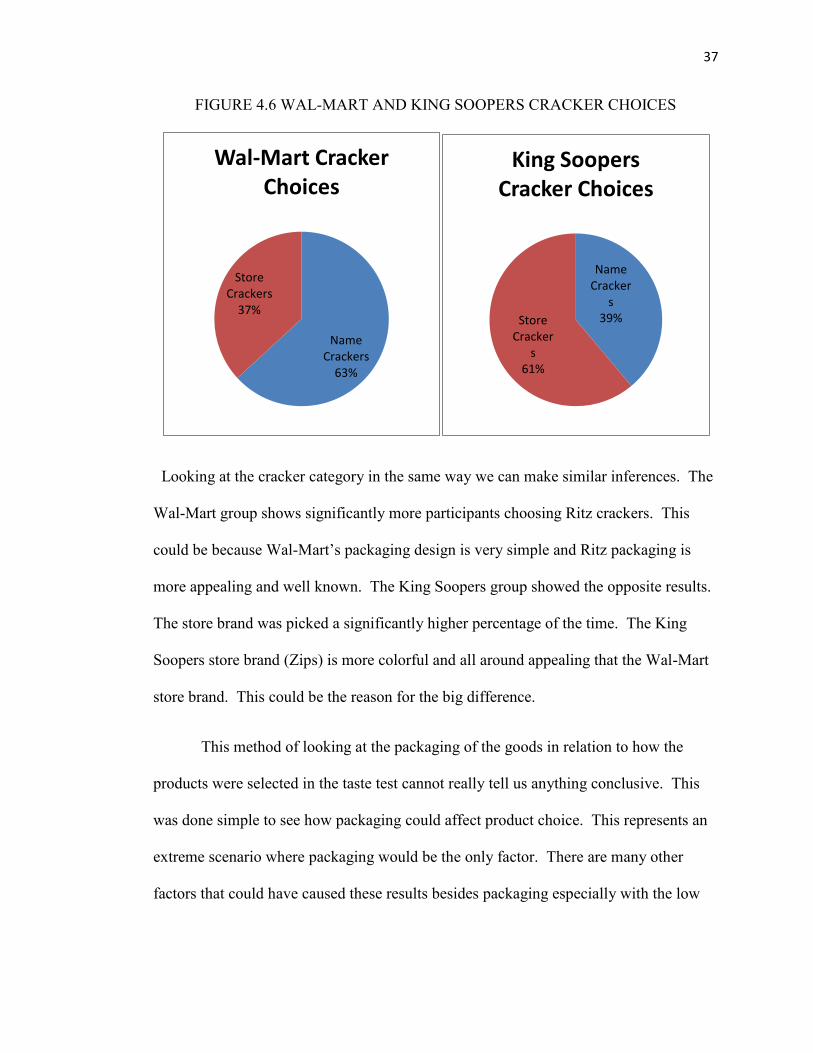

FIGURE 4.6 WAL-MART AND KING SOOPERS CRACKER CHOICES

Looking at the cracker category in the same way we can make similar inferences. The

Wal-Mart group shows significantly more participants choosing Ritz crackers. This

could be because Wal-Mart’s packaging design is very simple and Ritz packaging is

more appealing and well known. The King Soopers group showed the opposite results.

The store brand was picked a significantly higher percentage of the time. The King

Soopers store brand (Zips) is more colorful and all around appealing that the Wal-Mart

store brand. This could be the reason for the big difference.

This method of looking at the packaging of the goods in relation to how the

products were selected in the taste test cannot really tell us anything conclusive. This

was done simple to see how packaging could affect product choice. This represents an

extreme scenario where packaging would be the only factor. There are many other

factors that could have caused these results besides packaging especially with the low

Name Crackers

63%

Store Crackers

37%

Wal-Mart Cracker Choices

Name Cracker

s 39% Store

Crackers

61%

King Soopers Cracker Choices

38

number participants. With a higher number of participants and further questioning

about packaging we could learn more about how packaging effects purchasing behavior.

Hypothesis Three

The third hypothesis examines the relationship between the perceptions of

retailers and their private label brands. We hypothesis that private label goods will be

perceived as better if the store they originated from is perceived highly by customers.

In other words if a store has a good reputation then its private label goods will be

perceived as better. Our data shows no support for this hypothesis.

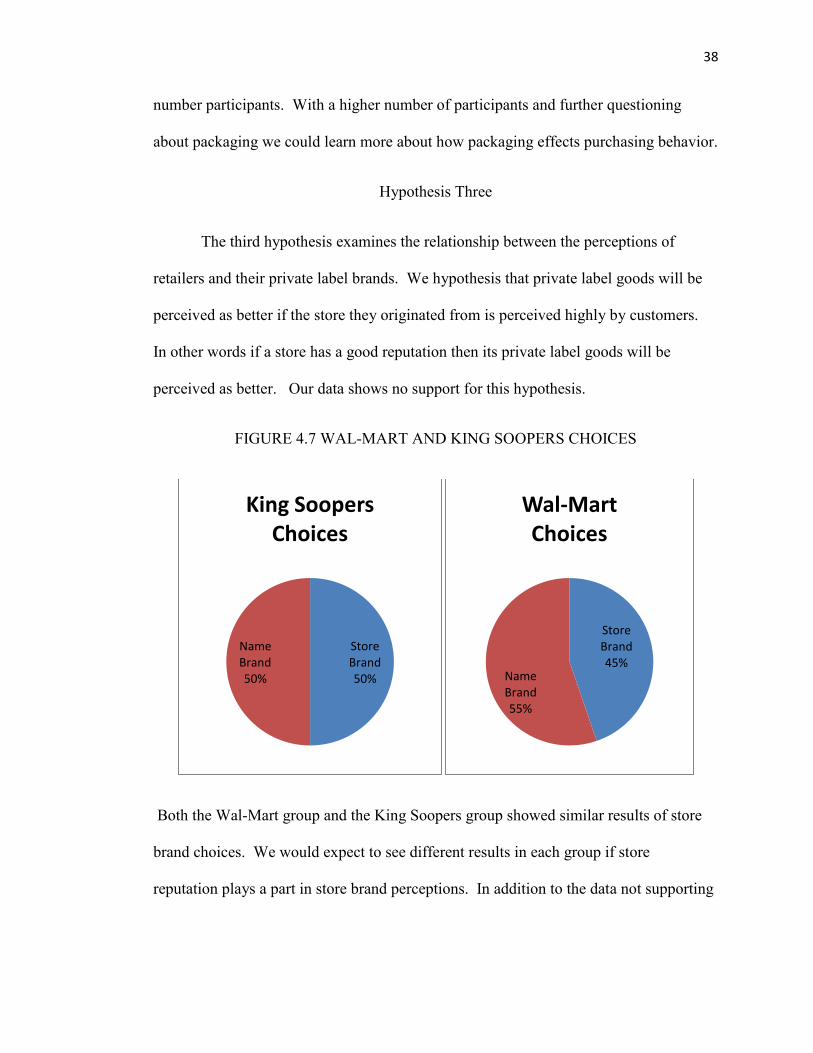

FIGURE 4.7 WAL-MART AND KING SOOPERS CHOICES

Both the Wal-Mart group and the King Soopers group showed similar results of store

brand choices. We would expect to see different results in each group if store

reputation plays a part in store brand perceptions. In addition to the data not supporting

Store Brand 50%

Name Brand 50%

King Soopers Choices

Store Brand 45%

Name Brand 55%

Wal-Mart Choices

39

the hypothesis the response collected on the questionnaires showed that store reputation

was not a significant factor in store choice. Based on this, hypothesis three is Rejected.

40

CHAPTER V

CONCLUSION

The central focus of this study was to explore extrinsic cues and how they affect

consumer perceptions. We focused on brand name, packaging and store reputation.

Although our results were not conclusive we found some interesting patterns and

behaviors. The raw data collected did not support our first hypothesis. The ratio of

participants choosing store brand goods to participants choosing name brand goods was

nearly one to one suggesting that brand had no effect. Responses during the taste tests

by individual participants showed evidence that supported the first hypothesis.

Participants were obviously influenced in some way by the brand names of the

products. Other research on the topic would support the initial hypothesis so individual

participants responses could not be ignored. The results tested in the second hypothesis

were equally as vague. We found trends that could be explained by variations in

packaging but there were many other factors that could explain these trends. More data

would need to be collected to properly research this hypothesis. The third hypothesis

had no support from the data. In the questionnaire responses store reputation was found

to be of very little importance to consumers. The data from the taste tests also showed

little difference between the results for each store’s group. In all the study was

inconclusive but it did show some parallels with other research on the subject.

41

Sources of error

There are some obvious sources of error in this study and some that are not so

obvious. The first is the possibility that participants were influenced by factors other

than the ones that were the subject of the study. This was for seen and precautions were

taken. One example was covering messages on the package like “low fat” or

“vegetarian.” These things alone could have persuaded participants to choose one

product over the other. Another precaution was the controlled environment of the test.

Every test took place in the same room with the same examiner. Although these

precautions were taking other aspects could have influenced participants such as

fondness of cookies or crackers, time of day, and if they had recently eating among

other things.

Another possible source of error was the quality consistency of the products

used in the taste tests. The tests were done with the assumption that because both

products in each category were from the same package that they would be the same

quality. If the quality fluctuated from one sample to the next participants would judge

based on the taste difference. This would be bad because the experiment was designed

so that participants judge based on the extrinsic cue of brand name. This was avoided

by using products which traditionally have good consistency, but this error could have

still been present. For example if one cookie had more chocolate chips than the other

this may affect the taste and sway the participant. With a lot of subjects this error

would be less and less significant.

42

Sample bias could also be a source of error. The participants in this study were

mostly student. Students general have less money to devote to food and therefore may

pay more attention to price and be more likely to buy store brands. Because of this

students may have very different perceptions of store brand goods than the rest of the

sample.

The questionnaire may be another area that may have been affected by error.

Some participant may have been hesitant to answer certain questions truthful. People

may not want to admit how much they are affected by things such as brand name, price,

packaging, and so on. In our study we promoted honesty by informing participants that

that all of the information they provided would be kept confidential and anonymous.

Even with this precaution participants may not have responded honestly.

Limitations and Future Research

Several limitations were reached in this study. The first was recruiting

participants. This process was a lot harder than originally anticipated especially under

time constraints. Scheduling taste tests in time slots allowed for more convenience to

the participants, and helped attract participants. The biggest hindrance in attracting

participants was the location. In our study we wanted a controlled environment but we

could not get participants to come. A better strategy may have been setting up the

experiment outside of a grocery store. This would not provide a controlled environment

but it would provide a large potential participant base. An experimenter could easily

43

get fifteen to twenty participants a day using this method. This would be an opportunity

for further research.

Another limitation was the responses gathered from the participants. Once we

began to analyze the data we realized that more data about packaging and store

reputation would have helped in the analysis of the hypotheses. For example after

participants chose their favorite product we could have asked them which product had

more appealing packaging. This would have helped better explain the second

hypothesis. The more data that is collected during an experiment the better even if it

does not get used.

This study did not show conclusive proof of any of the hypotheses but I feel that

the topic is still relevant and important and future research is required. By gathering

more data I believe that this study would have come to conclusions about all three

hypotheses. The study did find interesting consumer behavior and many similarities to

previous studies.

44

Appendix A

Written Debriefing Form

Name Brands versus Store Brands: A look into consumer

perceptions of store brands

The purpose of this research is to look at how brand name affects consumer perceptions

towards goods, specifically looking at name brands versus store brands. The main focus will be

looking at consumer’s perceived quality of goods based on the brand name. The objective is to

see how big of an impact brand name has in the market place. The secondary objective is to

research whether a store’s reputation has an effect on the perceptions of the stores private label

brands.

The best way to observe how consumers perceive the quality of goods based on their

brand name is through a comparison. We did this in through the taste test. We asked you to

sample two goods, one of which was in front of a store brand and the other that was in front of a

name brand, and then pick your favorite. The study was designed to lead you to believe that the

products you sampled represented the brand that they were in front of but that was not the case.

Both of the samples were the same good. We did this so we could see the affect that a products

brand name alone can have on consumer perceptions. Because the two samples are the same if

consumer perceptions do not rely on a product’s brand name we will expect to see roughly a

half and half split of the two samples being chosen. If not we will know that brand name is a

factor in a consumes choice between name brand and store brand goods.

Both consumers and retailers can benefit from this research. Consumers can gain

knowledge that may help them make more informed decisions between name brand and store

brand goods. Retailers can use the findings of this research to better market their private label

goods to customers.

We would ask you to maintain confidentiality about the purpose of the experiment since

any pre-knowledge of the purpose will bias the data for that person and thus cannot be used.

If you have any questions or concerns about the experiment or would like to receive a summary

of the findings contact The principal investigator Wyatt Babb at

[email protected], The faculty advisor Jim Parco at

[email protected], or the Colorado College Institutional Research Board chair,

Amanda Udis-Kessler at 719-227-8177 or [email protected]. If you feel

uncomfortable about having been deceived in this study you are free to ask that your data be

withdrawn from the study. Records of this study will be kept private. The data collected in this

study will be kept in a password protected spreadsheet and the data will not be linked in any

way to your name or other individual information. Any report of this research that is made

45

available to the public will not include your name or any other individual information by which

you could be identified.

Thank you very much for participating in our study!

Appendix B

FIGURE 3.1 TASTE TEST INSTRUCTIONS

Taste Test Instructions

This experiment has been designed to examine consumers snack food preferences. The

taste test is simple and easy. There will be a table with two sets of two products. In

front of each product there will be a sample for you to taste.

Procedure:

Upon entering the room you will sit down and the taste test supervisor will ask you to

sample the products in the first set and then describe which product was your favorite.

There will be water available to cleanse your pallet between products. Your choice will

be recorded and then you will be asked to do the same thing with the next set of

products. Once you have completed the taste test of both product sets you are finished.

The taste test supervisor has been instructed not to speak once the testing has begun as

not to influence the experiment. Please hold questions until after the taste test has been

completed.

We also ask that once the taste test has concluded please refrain from talking about the

experiment until all of the taste test have been done to prevent any undue external

influences on the testing

Thank you for participating in this study.

46

Appendix C

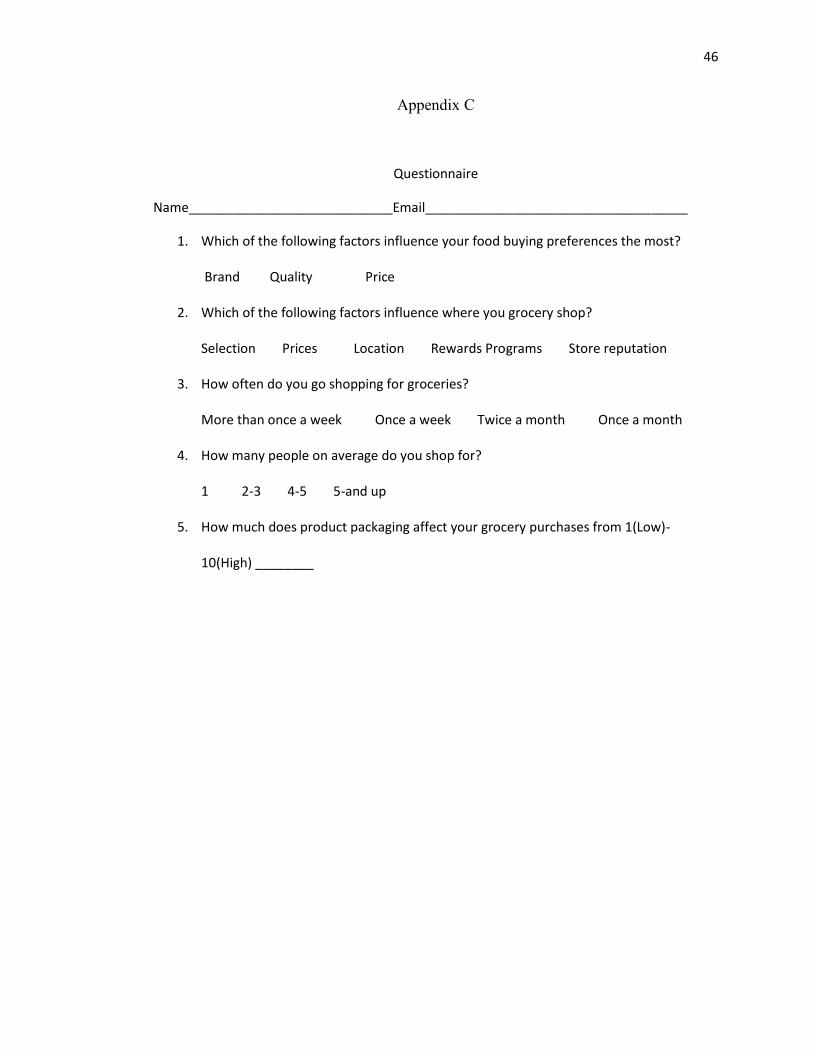

Questionnaire

Name____________________________Email____________________________________

1. Which of the following factors influence your food buying preferences the most?

Brand Quality Price

2. Which of the following factors influence where you grocery shop?

Selection Prices Location Rewards Programs Store reputation

3. How often do you go shopping for groceries?

More than once a week Once a week Twice a month Once a month

4. How many people on average do you shop for?

1 2-3 4-5 5-and up

5. How much does product packaging affect your grocery purchases from 1(Low)-

10(High) ________

47

WORKS CONSULTED

"Packaging can Set Apart Store Brands." Official Board Markets 87, no. 8 (02/19

2011): 16-16.

"Private Lable Manufacturers Association." [cited 2011]. Available from

http://plma.com/.

"Store Brands Vs. Name Brands." Consumer Reports 75, no. 10 (10 2010): 16-21.

"Battle of the Brands." Consumer Reports 70, no. 8 (08 2005): 12-15.

"The Price Factor in Private Label Purchasing Decisions." Supermarket Business

Magazine 49, no. 8 (08 1994): 16.

"The Generic Metamorphosis: Now they'Re Third-Tier Brands with Names, Colorful

Labels. (Cover Story)." Marketing News 15, no. 22 (04/30 1982): 1-7.

"Half of Consumers Now Buy More Generics, Store Brands." Marketing News 15, no. 3

(08/07 1981): 15-15.

"Brand Loyalty Beats Price in some Product Categories. (Cover Story)." Marketing

News 14, no. 11 (11/28 1980): 1-2.

Ailawadi, Kusum L., Scott A. Neslin, and Karen Gedenk. "Pursuing the Value-

Conscious Consumer: Store Brands Versus National Brand Promotions." Journal

of Marketing 65, no. 1 (01 2001): 71-89.

ALLEN, MICHAEL W., RICHA GUPTA, and ARNAUD MONNIER. "The Interactive

Effect of Cultural Symbols and Human Values on Taste Evaluation." Journal of

Consumer Research 35, no. 2 (08 2008): 294-308.

Allison, Ralph I., and Kenneth P. Uhl. "Influence of Beer Brand Identification on Taste

Perception." Journal of Marketing Research (JMR) 1, no. 3 (08 1964): 36-39.

Badrinarayanan, Vishag, and Debra A. Laverie. "Brand Advocacy and Sales Effort by

Retail Salespeople: Antecedents and Influence of Identification with

Manufacturers' Brands." Journal of Personal Selling & Sales Management 31, no.

2 (Spring2011 2011): 123-140.

48

Baltas, George. "Determinants of Store Brand Choice: A Behavioral Analysis." Journal

of Product & Brand Management 6, no. 5 (05 1997): 315.

Baltas, George, and Paraskevas C. Argouslidis. "Consumer Characteristics and Demand

for Store Brands." International Journal of Retail & Distribution Management 35,

no. 5 (05 2007): 328-341.

Beldona, Sri, and Scott Wysong. "Putting the "Brand" Back into Store Brands: An

Exploratory Examination of Store Brands and Brand Personality." Journal of

Product & Brand Management 16, no. 4 (08 2007): 226-235.

Bellizzi, Joseph A., Harry F. Krueckeberg, John R. Hamilton, and Warren S. Martin.

"Consumer Perceptions of National, Private, and Generic Brands." Journal of

Retailing 57, no. 4 (Winter81 1981): 56.

Berman, Barry. Competing in Tough Times : Business Lessons from L.L. Bean, Trader

Joe's, Costco, and Other World-Class Retailers. Upper Saddle River, N.J.: FT

Press, 2011.

Bolan, Cristen. "Private Label Still Generic?" Global Cosmetic Industry 173, no. 10 (10

2005): 46-48.

Bonfrer, André, and Pradeep K. Chintagunta. "Store Brands: Who Buys them and what

Happens to Retail Prices when they are Introduced?" Review of Industrial

Organization 24, no. 2 (03 2004): 195-218.

Brucks, Merrie, Valarie A. Zeithaml, and Gillian Naylor. "Price and Brand Name as

Indicators of Quality Dimensions for Consumer Durables." Journal of the Academy

of Marketing Science 28, no. 3 (Summer2000 2000): 359.

Chakraborty, Samrat. "Perceptions and Buyer Behavior Towards Private-Label Colas:

An Exploratory Study to Understand the Views of the Store Managers of United

Kingdom." IUP Journal of Marketing Management 10, no. 1 (02 2011): 7-18.

Collins-Dodd, Colleen, and Tara Lindley. "Store Brands and Retail Differentiation: The

Influence of Store Image and Store Brand Attitude on Store Own Brand

Perceptions." Journal of Retailing and Consumer Services 10, no. 6 (11 2003):

345-352.

Corstjens, Marcel, and Rajiv Lal. "Building Store Loyalty through Store Brands."

Journal of Marketing Research (JMR) 37, no. 3 (08 2000): 281-291.

Cunningham, Isabella C. M., Andrew P. Hardy, and Giovanna Imperia. "Generic

Brands Versus National Brands and Store Brands." Journal of Advertising

Research 22, no. 5 (Oct 1982): 25-32.

49

Dawar, Niraj, and Philip Parker. "Marketing Universals: Consumers' use of Brand

Name, Price, Physical Appearance, and Retailer.." Journal of Marketing 58, no. 2

(04 1994): 81.

Erdem, Tü, Ying Zhao, and Ana Valenzuela. "Performance of Store Brands: A Cross-

Country Analysis of Consumer Store-Brand Preferences, Perceptions, and Risk."

Journal of Marketing Research (JMR) 41, no. 1 (02 2004): 86-100.

Fitzell, Philip B. Private Label Marketing in the 21st Century : Store Brandsexclusive

Brands on the Cutting Edge. 1 ed. New York: Global Books LLC, 2003.

Geyskens, Inge, Katrijn Gielens, and Els Gijsbrechts. "Proliferating Private-Label

Portfolios: How Introducing Economy and Premium Private Labels Influences

Brand Choice." Journal of Marketing Research (JMR) 47, no. 5 (10 2010): 791-

807.

Ghose, Sanjoy, and Oded Lowengart. "Taste Tests: Impacts of Consumer Perceptions

and Preferences on Brand Positioning Strategies." Journal of Targeting,

Measurement & Analysis for Marketing 10, no. 1 (08 2001): 26.

Gómez, Móica, and Shintaro Okazaki. "Estimating Store Brand Shelf Space."

International Journal of Market Research 51, no. 2 (03 2009): 243-266.

Gómez, Mónica, and Natalia Rubio. "Re-Thinking the Relationship between Store

Brand Attitude and Store Brand Loyalty: A Simultaneous Approach." International

Review of Retail, Distribution & Consumer Research 20, no. 5 (12 2010): 515-534.

Gomez-Arias, J., and Laurentino Bello-Acebron. "Why do Leading Brand

Manufacturers Supply Private Labels?" Journal of Business & Industrial

Marketing 23, no. 4 (06/15 2008): 273-278.

Granzin, Kent L. "An Investigation of the Market for Generic Products." Journal of

Retailing 57, no. 4 (Winter81 1981): 39.

Greenberg, Allan, and Sy Collins. "Paired Comparison Taste Tests: Some Food for

Thought." Journal of Marketing Research (JMR) 3, no. 1 (02 1966): 76-80.

Groznik, Ana, and H. S. Heese. "Supply Chain Conflict due to Store Brands: The Value

of Wholesale Price Commitment in a Retail Supply Chain." Decision Sciences 41,

no. 2 (05 2010): 203-230.

Hadary, Gideon. "The use of Taste Response Tests in Market Research." Journal of

Marketing 10, no. 2 (10 1945): 152-155.

Hansen, Karsten, and Vishal Singh. "Are Store-Brand Buyers Store Loyal? an Empirical

Investigation." Management Science 54, no. 10 (10 2008): 1828-1834.

50

Hansen, Karsten, Vishal Singh, and Pradeep Chintagunta. "Understanding Store-Brand

Purchase Behavior Across Categories." Marketing Science 25, no. 1 (Winter2006

2006): 75-90.

Herstein, Ram, and Sigal Tifferet. "An Investigation of the New Generic Consumer."

Journal of Consumer Marketing 24, no. 3 (04 2007): 133-141.

Jana, Reena. "The Revenge of the Generic." BusinessWeek Online (12/27 2006): 17-17.

Juan Beristain, Jose, and Pilar Zorrilla. "The Relationship between Store Image and

Store Brand Equity: A Conceptual Framework and Evidence from Hypermarkets."

Journal of Retailing and Consumer Services 18, no. 6 (11 2011): 562-574.

Koeppel, Jean. "Store Brands Vs. National Brands Who is Coming Out Ahead?" Brand

Packaging 14, no. 6 (07 2010): 22-24.

Kuan-Yin Lee, and Yin-Chiech Hsu. "Communication and Brand Knowledge as

Determinants of Retail Service Brand Loyalty - an Empirical Test in a Multiple

Retail Service Brand Context." Journal of Global Business & Technology 6, no. 1