Embed Size (px)

DESCRIPTION

U.S. Customs & Border Protection NAFTA audit and verification manual from the CBP website.

Citation preview

U.S. Customs and Border Protection - Import

Tuesday, September 25, 2007

Home About CBP Contacts Ports Questions Forms Publications Legal Contracting Sitemap

Import

Antidumping and Countervailing Duties (ADCVD)

Broker Management

Cargo Control

Cargo Summary

Carriers

Commercial Enforcement

Communications to Trade

Duty Rates/HTS

Informed Compliance

Infrequent Importer/Traveler

International Agreements

Operations Support

Regulatory Audit

Textiles and Quotas

Trade Initiatives

Home / Import / International Agreements / International Free Trade Agreements / North American Free Trade Agreement (NAFTA) /

NAFTA Verification/Audit Manual

The NAFTA Verification/Audit Manual is developed to support the verification of goods for which NAFTA preferential tariff treatment has been claimed comply with the rules of origin. This trilateral guide details the recommended technical verification framework to be observed by each Party when conducting NAFTA verifications. This trilaterally agreed upon manual also provides significant automobile information.

- Introduction and Executive Summary

doc - 27 KB.

- Chapter 1: Purpose of the Manual and Legislative Framework

doc - 32 KB.

- Chapter 2: Co-operation Among the Parties

doc - 30 KB.

- Chapter 3: Auditing Standards

doc - 75 KB.

- Chapter 4: Objectives of NAFTA Audits (Verifications)

doc - 28 KB.

- Chapter 5: Scope of the NAFTA Audits (Verifications)

doc - 196 KB.

- Chapter 6: Methodology for Rules of Origin Audits (Verifications)

doc - 90 KB.

- Chapter 7: NAFTA Working Groups

doc - 24 KB.

- U.S. Appendix

doc - 1,136 KB.

Search NAFTA Verification/Audit Manual for:

section sitemap for NAFTA Verification/Audit Manual

see also:in North American Free Trade Agreement (NAFTA) :

Advance Rulings

Annex 401

Appeals

Certificate of Origin

Claiming Preferential Treatment

Commercial Samples

Commodity Specific Information

...more

How to Use the Website

Featured RSS Links

Newsroom Border Security Import Export Travel Careers Home About CBP Contacts Ports Questions Forms

Publications Legal Contracting Sitemap EEO | FOIA | Privacy Statement | Get Plugins

Department of Homeland Security

U.S. Customs & Border Protection | 1300 Pennsylvania Avenue, NW Washington, D.C. 20229 | (202) 354-1000

http://www.cbp.gov/xp/cgov/import/international_agreements/free_trade/nafta/verification_audit_manual/9/25/2007 10:54:40 AM

Dow

nloaded 9/25/2007

NORTH AMERICAN FREE TRADE AGREEMENT (NAFTA) AUDIT (VERIFICATION) MANUAL

UNITED STATES CUSTOMS SERVICE

REGULATORY AUDIT DIVISION NORTH AMERICAN FREE TRADE AGREEMENT

AUDIT (VERIFICATION) MANUAL TABLE OF CONTENTS Introduction

Executive Summary

INTRODUCTION

With the entry in force of the North American Free Trade Agreement (NAFTA), the Parties have experienced a significant increase in the trade of goods and services between them. The three Customs Administrations have agreed that the Rules of Origin as set out in Chapter Four of the NAFTA and the NAFTA Rules of Origin Regulations (the Regulations), define the framework to be observed by exporters/producers in order to have their goods qualify as "originating goods", and be eligible for a NAFTA preferential tariff treatment when imported into the territory of any of the other Parties to the Agreement.

As a result, it has become important for the Customs Administration of each Party to verify that the goods for which NAFTA preferential tariff treatment has been claimed comply with the Rules of Origin.

In this respect, the three Customs Administrations have considered that the establishment of verification guidelines is important and useful. The Customs Administrations of all Parties have consulted during the development of this manual and these guidelines include general, examination and reporting standards for NAFTA origin verifications.

This manual is intended to be used by: Origin Audits Unit of Revenue Canada (Canada); Direction of International Audit of the Ministry of Finance and Public Credit (Mexico); and, the offices of Regulatory Audit and Field Operations, U.S. Customs Service (United States). However, portions of this manual may also be used by other areas within each Customs Administration as deemed appropriate.

The main purpose of this document is to establish the recommended technical verification framework to be observed when conducting NAFTA verifications. The application of the provisions included therein should take into consideration the circumstances involved in each verification and be adapted accordingly. It is understood that this document will be updated on a continual basis.

This of the NAFTA Verification Manual provides revisions to the November 1995 version to reflect changes in the Regulations which became effective on October 1, 1995.

EXECUTIVE SUMMARY

This manual considers all types of verifications, but focuses on the on-site audit process for exporter verifications where the regional value content requirement, tariff change requirement, or both, must be met. It should be noted that this manual provides verification procedures that are recommended by all Parties.

Dow

nloaded 9/25/2007

There are seven chapters contained in this manual. Included is an annex at the end of most chapters. The Annex contains information for the particular chapter that may differ among the Parties. The chapters within this U.S. version of the NAFTA Verification Manual includes information unique to the U.S. Information differing in Mexico and/or Canada, is included at the end of the chapter in the Annex. The highlights for each chapter are as follows:

Chapter 1, Purpose of the Manual and Legislative Framework, points out the need for this audit (verification) manual, and refers to the legal framework by which NAFTA verifications are conducted.

Chapter 2, Co-operation Among the Parties, discusses the exchange of information and communication between Customs Administrations subject to NAFTA.

Chapter 3, Auditing Standards, demonstrates how the Generally Accepted Auditing Standards have been incorporated into each Party's audit (verification) process.

Chapter 4, Objectives of NAFTA Audits (Verifications), outlines the objectives of NAFTA exporter on-site verifications as well as the verification program objectives for this type of verification.

Chapter 5, Scope of the NAFTA Audits (Verifications), describes the parameters of coverage for NAFTA exporter verifications including the verification period, coverage, importer identification, and assessment/liquidation period. This Chapter also includes recommended verification procedures that are identical and uniform for all Customs Administrations.

Chapter 6, Methodology for Rules of Origin Audits (Verifications), explains the verification process for NAFTA exporter verifications.

Chapter 7, NAFTA Working Groups, refers to the contact areas within the Customs Administration of each Party with respect to verification issues and their relationships with the NAFTA Working Groups.

LIST OF APPENDICES

A Certificate of Origin CF-434

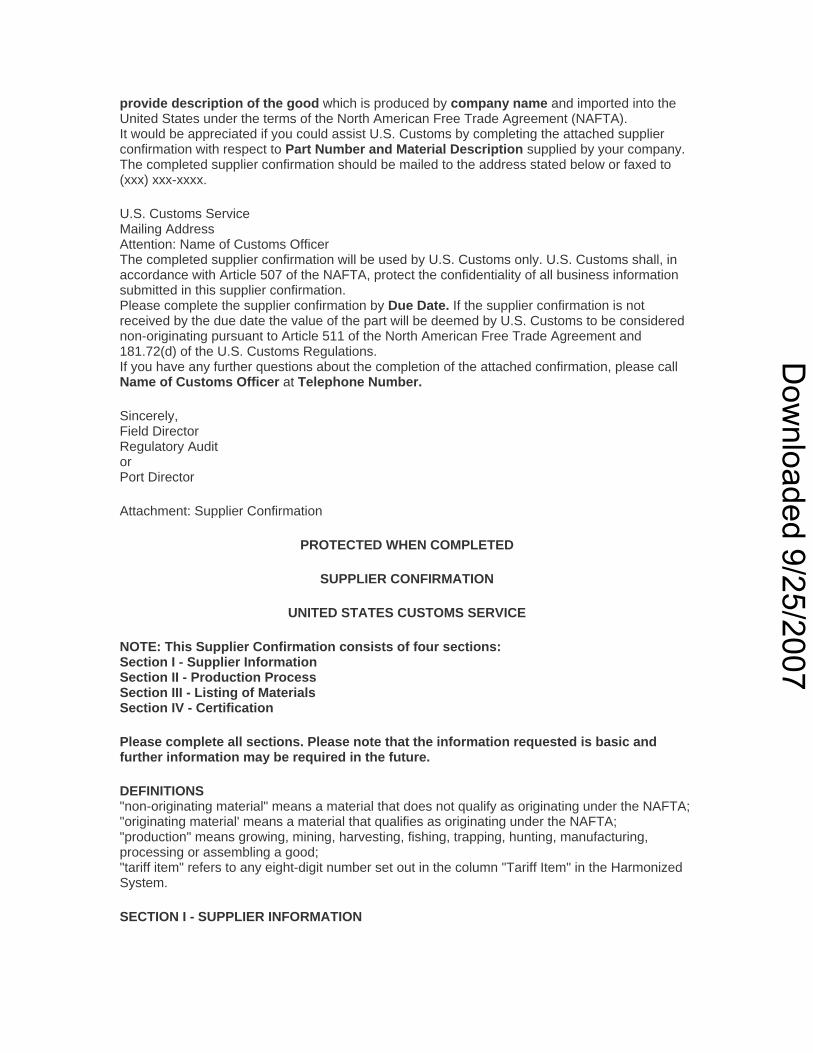

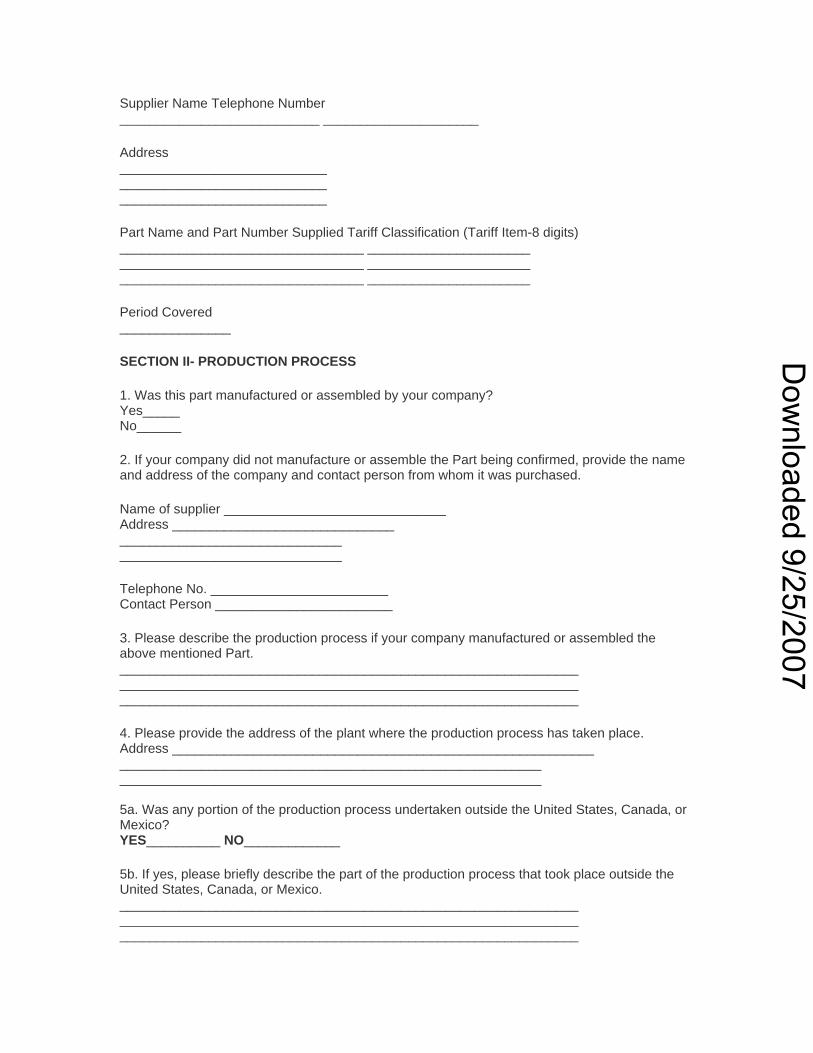

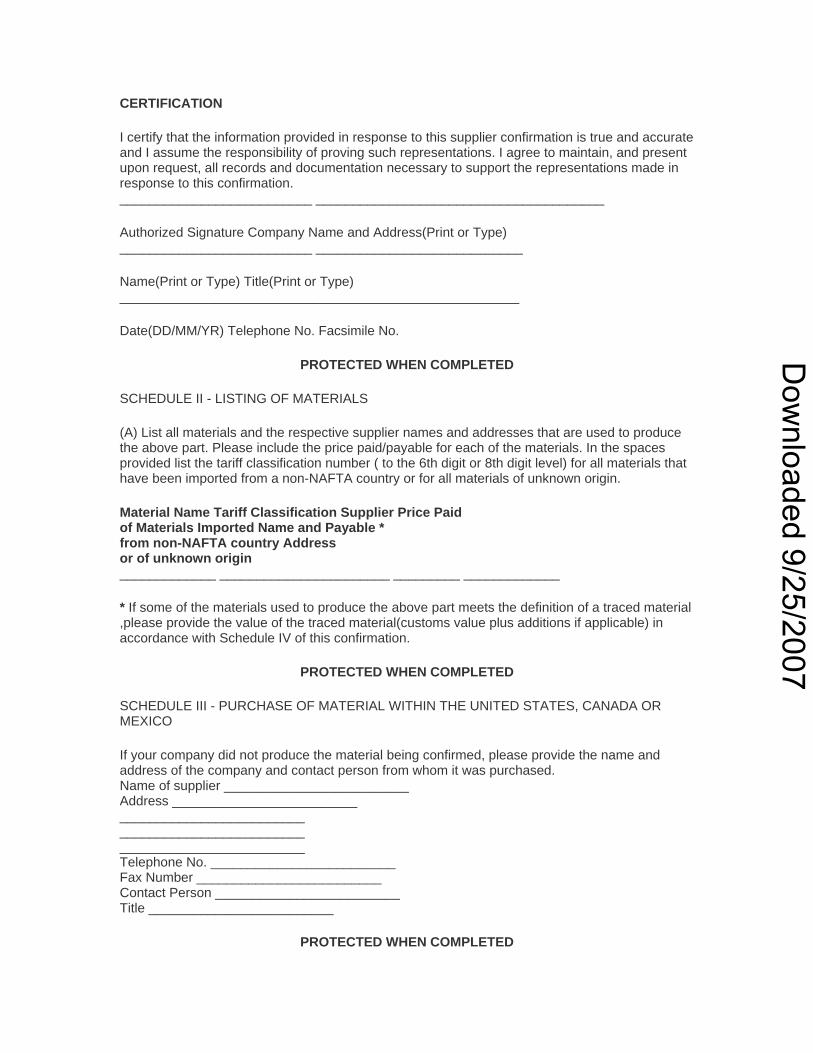

B General Questionnaire CF-446 C Election to Average Form for Vehicles CF-447 D Sample Letter Proposing NAFTA Verification Visit E Sample Notification of NAFTA Verification of Goods to Known Importers of Record F Review of Policies, Procedures, and Internal Controls Checklist G Final Written Determinations- Positive and Negative H Sample Notification of Verification Results to Known Importers (1) Goods met NAFTA rule of origin requirements (2) Goods did not meet NAFTA rule of origin requirements I Supplier Confirmation Letters (1) for non-automotive parts suppliers (2) for automotive parts suppliers J Supplier Verification Notification K Regulatory Audit Final Audit Reports L Goods Wholly Obtained or Produced Entirely in the Territory of One or more of the Parties M Goods Produced entirely in the Territory of One or More of the Parties Exclusively from Originating Materials N Preference Criteria D

Dow

nloaded 9/25/2007

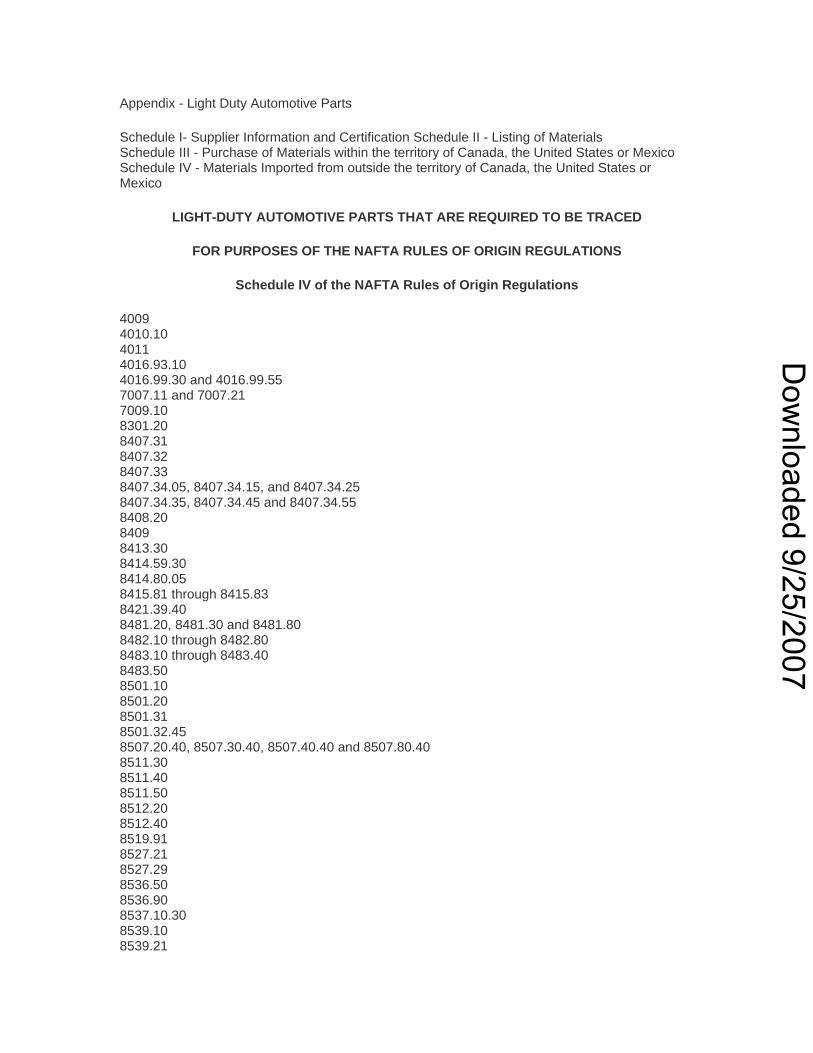

O Light Duty Automotive Goods - Averaged P Light Duty Automotive Goods - Non-Averaged Q Heavy Duty Automotive Goods - Averaged R Heavy Duty Automotive Goods - Non-Averaged

Dow

nloaded 9/25/2007

NORTH AMERICAN FREE TRADE AGREEMENT (NAFTA) AUDIT (VERIFICATION) MANUAL

CHAPTER 1 PURPOSE OF THE MANUAL AND LEGISLATIVE FRAMEWORK

1.1 Purpose of the Manual

This verification manual presents the audit process and the recommended verification procedures with which an auditor or officer must be familiar in order to conduct a verification and perform other related tasks for the North American Free Trade Agreement (NAFTA). This manual is intended to provide the user with a clear understanding of the verification function. Reference to, or usage of, the manual in daily activities will result in verifications and other related tasks being done in an efficient and uniform manner, that is consistent with established policies and procedures.

The Customs Administration of each Party has consulted in the writing of this manual, and a similar manual has been developed for their own Customs Administration. It is expected that by having a similar verification manual for all Customs Administrations there will be a uniform and consistent application of verification procedures when conducting rule of origin verifications under the NAFTA.

1.2 Scope

This manual covers subjects which are related to the process and the recommended procedures pertinent to conducting verifications under the provisions of the NAFTA. The manual does not deal specifically with interpretations and rulings on origin, as these subjects are covered by other directives issued by each Customs Administration. This manual explains the use of various reports, forms, and working papers that are required for the audit activity. (Examples are included in the appendices).

1.3 Amendments

Changes in legislation, regulations and administrative policies may necessitate changes or updates to the contents of this manual. All changes will be discussed among the Parties.

1.4 Legislative Framework

Article 506 of the NAFTA sets out the authority for each Party to the Agreement to conduct verifications of the books and records of the exporter or producer located in the territory of another NAFTA Party. The implementing legislation and enabling regulations support the text of the NAFTA.

For the domestic legislative framework of the other Parties, refer to the respective Annex 1, Section 1.4 at the end of this Chapter.

The provisions of the NAFTA were adopted by the United States with the enactment of the North American Free Trade Agreement Implementation Act, Public Law 103-182, 107 Stat. 2057. The principal role of the U.S. Customs Service is to administer the provisions of the NAFTA and the Act which relate to the importation of goods into the United States from Canada and Mexico. Those Customs related NAFTA provisions which require implementation through regulation include certain tariff and non-tariff provisions within Chapter Three (National Treatment and Market Access for Goods) and the provisions of Chapter Four (Rules of Origin) and Chapter Five (Customs Procedures).

Dow

nloaded 9/25/2007

The majority of the NAFTA implementing regulations are contained in Part 181 of the Customs Regulations. However, in those cases in which NAFTA implementation is more appropriate in the context of an existing regulatory provision, the NAFTA regulatory text has been incorporated in an existing Part within the Customs Regulations. The NAFTA Rules of Origin Regulations are set forth as an Appendix to Part 181. The text was trilaterally negotiated and is presented as such, except for editorial modifications necessary and appropriate for the U.S. regulatory context.

The following specific Parts of the Customs Regulations were revised to reflect changes resulting from the NAFTA:

Part 10- Articles Conditionally Free, Subject to a Reduced Rate, etc. Part 12- Special Classes of Merchandise Part 24- Customs Financial and Accounting Procedure Part 123- Customs Relations with Canada and Mexico Part 134- Country of Origin Marking Part 162- Record keeping, Inspection, Search, and Seizure Part 174- Protests Part 177- Administrative Rulings Part 178- Approval of Information Collection Requirements

Part 191- Drawback ANNEX 1 CANADA

1.4 Legislative Framework

In Canada, Department Memorandum D11-4-20, "Origin Verification Procedures" outlines the Department's program for verification procedures pursuant to section 42 of the Customs Act, and Article 506 of the NAFTA, and the Uniform Regulations of the NAFTA.

The Uniform Regulations for Chapters Three and Five of the NAFTA have been agreed to by the governments of Canada, Mexico and the United States, and for Canada are contained in Departmental Memorandum D11-4-18, "Uniform Regulations, Chapters Three and Five of NAFTA". These Uniform Regulations elaborate in detail how NAFTA Parties will interpret, apply and administer the obligations regarding customs procedures under Chapter Five, and national treatment and market access under Chapter Three, and are to be read in conjunction with these Chapters.

The NAFTA Rules of Origin Regulations (regarding the rules of origin under Chapter Four of the NAFTA) effective from January 1, 1994 to September 30, 1995 are found in Customs Notice N-840. The NAFTA Rules of Origin Regulations effective from October 1, 1995 onward are found in Departmental Memorandum D11-5-1, "NAFTA Rules of Origin Regulations".

ANNEX 1 CANADA

1.4.1 Customs Act

The Customs Act provides the domestic legal framework for administering and enforcing laws relating to Revenue Canada, Customs and Excise including the Customs Tariff.

The Customs Act, for which the Minister of National Revenue is responsible, creates the authority for the administration of Customs matters generally and for the Governor-in-Council to make specific administrative regulations. The collection of Customs duties is based on the principle of

Dow

nloaded 9/25/2007

self-assessment and voluntary compliance by the Canadian importer or owner of imported goods who must report and account for all such goods as required by the Customs Act. The Customs Act, therefore, provides the mechanism for the collection of duties and taxes imposed on imported goods by other federal statutes, and for the enforcement of the many federal statutes that prohibit, regulate or control imported and exported goods.

Section 42 of the Customs Act specifically addresses verifications conducted for the purposes of determining origin, the statement of origin, the effective date of a re-determination of origin, the denial or withdrawal of the benefit of the preferential tariff treatment, and advance rulings.

1.4.2 Customs Tariff

Through the Customs Tariff Canada gives effect to the International Convention on the Harmonized Commodity Description and Coding System. It is this Customs Tariff that is used by Revenue Canada when confirming the classification of goods and materials during the course of a verification as it is the HS tariff classification of the country into whose territory the good is imported that is applicable.

ANNEX 1 CANADA

The Customs Tariff is a fiscal statute that: - imposes customs duties on imported goods; - provides for the tariff treatment accorded to imported goods depending on their country of origin; - provides for other conditions (e.g. relating to transshipment) that goods must meet in order to be entitled to a specific tariff treatment; and - provides for the tariff rate (rate of customs duty) applicable to goods, depending on the classification of the goods; and, provides for duty relief.

ANNEX 1 MEXICO

1.4 Legislative framework Articles 511 and 514 of the NAFTA published in the Official Gazette of the Federation on December 20, 1994, set out that the Parties shall establish, and implement through their respective laws the Uniform Regulations regarding the Interpretation, Application and Administration of Chapter Four of the NAFTA.

Article 506 of the NAFTA, published in the Official Gazette of the Federation on December 20, 1994 and rules 35 trough 66, of Section VII, of Title III of the Uniform Regulations regarding the Interpretation Application and Administration of Chapter Four of the NAFTA, published in the Official Gazette of the Federation on December 30, 1994, set out the verification procedures to conduct origin verifications of goods imported into Mexico for which preferential tariff treatment was claimed, in order to determine whether such goods qualify as originating as stated in their certificates of origin. Verifications are mainly conducted by using written questionnaires and performing verification visits.

In addition to the legal proviso referred to in the previous paragraph, articles 3, and 116 of the Customs Law and Article 48 of the Fiscal Federal Code and the Interim regulations of the Ministry of Finance and Public Credit set out that the Direction of International Audit, of the Direction General of Revenue Policy and International Fiscal Affairs, acting as a Customs Authority, may request exporters, producers, customs brokers and importers to provide the information regarding the origin of imported goods for verification purposes.

Dow

nloaded 9/25/2007

The applicable importation duties for importations that received the benefit of the NAFTA preferential tariff treatment may also be verified by the Direction of International Audit mentioned before. The applicable importation duties are established in the General Importation Duty Law (Ley del Impuesto General de Importaci�on a most favored nation basis, and such Law is structured taking into account the guidelines provided for in the Harmonized System. In order to apply the General Importation Duty Law, it is required to observe the duty phase-out schedules, published on an annual basis for NAFTA purposes, for originating goods in accordance with the terms provided for in NAFTA Annex 302.2.

In addition to the legal provisions referred to in the previous paragraph the Direction of International Audit may verify the country of origin marking in accordance with the terms stated in Chapter III of the NAFTA and the Decree in which the country of origin marking guidelines were published on the Official Gazette of the Federation dated January 7, 1994.

The legal provisions above mentioned, provide the legal framework for administering and enforcing laws for NAFTA purposes, in the case of the Ministry of Finance and Public Credit of Mexico.

Dow

nloaded 9/25/2007

NORTH AMERICAN FREE TRADE AGREEMENT (NAFTA) AUDIT (VERIFICATION) MANUAL

CHAPTER 2 COOPERATION AMONG THE PARTIES

2.1 Exchange of Rulings

Both consultation and the exchange of rulings are required pursuant to paragraph 1, Article 512 of the North American Free Trade Agreement (NAFTA) which states, "Each Party shall notify the other Parties of the following determinations, measures and rulings, including to the greatest extent practicable those that are prospective in application: (a) a determination of origin issued as the result of a verification conducted pursuant to Article 506(1); (b) determination of origin that the Party is aware is contrary to; (i) a ruling issued by the customs administration of another Party with respect to the tariff classification or value of a good, or of materials used in the production of a good, or the reasonable allocation of costs where calculating the net cost of a good, that is the subject of a determination of origin, or (ii) consistent treatment given by the customs administration of another Party with respect to the tariff classification or value of a good, or of materials used in the production of a good, or the reasonable allocation of costs where calculating the net cost of a good, that is the subject of a determination of origin; (c) a measure establishing or significantly modifying an administrative policy that is likely to affect future determinations of origin, country of origin marking requirements or determinations as to whether a good qualifies as a good of a Party under the Marking Rules; and (d) an advance ruling, or a ruling modifying or revoking an advance ruling, pursuant to Article 509."

In order to ensure the uniform application of the rules of origin NAFTA meetings are held between the three Customs Administrations. NAFTA meetings are held at the audit level, Customs Sub-group level, and at the Working Group level. The auditors of each NAFTA Party meet to discuss issues and then report the results of the discussions to the Customs Sub-group. Refer to Chapter 7-NAFTA Working groups.

It is very important that this process of consultation and exchange of information continue, given that its primary objective is to ensure the uniform application of the rules of origin.

2.2 Confidentiality of Business Information

NAFTA Article 507, Confidentiality, states:

"1. Each Party shall maintain, in accordance with its law, the confidentiality of confidential business information collected pursuant to this Chapter and shall protect that information from disclosure that could prejudice the competitive position of the persons providing the information.

2. The confidential business information collected pursuant to this Chapter may only be disclosed to those authorities responsible for the administration and enforcement of determinations of origin, and of customs and revenue matters."

For specific legislation from the other Parties affecting confidentiality of business information, refer to the respective Annex 2, Section 2.2. at the end of this Chapter.

Dow

nloaded 9/25/2007

Section 181.121 of the U.S. Customs Regulations reflects the principle of maintenance of confidentiality of business information set forth in NAFTA Article 507(1); and, Section 181.122 reflects the NAFTA Article 507(2) exception to non-disclosure in the case of disclosures to governmental authorities for administrative and enforcement purposes.

2.3 Communication

As much as possible, Customs issues under dispute with respect to the NAFTA are resolved through consultation and discussion between the three administrations. Refer to Chapter 7- NAFTA Working groups. Only in instances where no possible grounds for agreement exist between the Parties would an issue be referred to the Commission - Good Offices, Conciliation and Mediation, and then possibly to the Arbitral Panel for dispute settlement.

ANNEX 2 CANADA

2.2 Confidentiality of Business Information

Sections 107 and 108 of the Customs Act set out the restrictions on the communication of information and the circumstances under which information obtained under the Act may be disclosed. Section 160 of the Customs Act sets out the penalties for contravention of sections 107 and 108.

ANNEX 2 MEXICO

2.2 Confidentiality of business information

Articles 507 of the NAFTA, and 69 of the Fiscal Federal Code set out the confidentiality of any confidential business information gathered during the course of any verification and protect that information from disclosure that could prejudice the competitive position of the persons providing the information.

Dow

nloaded 9/25/2007

NORTH AMERICAN FREE TRADE AGREEMENT (NAFTA) AUDIT (VERIFICATION) MANUAL

CHAPTER 3 AUDITING STANDARDS

There is a need for harmonization of the approach for the rules of origin verifications conducted by all parties to a free trade agreement. Harmonization will provide for consistency in verification methodology and procedures. All Parties (Mexico, U.S. and Canada), while conducting audits, will follow Generally Accepted Auditing Standards with specific modifications to make the standards applicable to North American Free Trade Agreement(NAFTA)legislation/requirements. Section 3.1 sets out how each Party's Customs Administration complies with these standards in completing verifications for the NAFTA. Section 3.2 outlines each Party's working paper requirements. (Refer to Chapter 6 for a more detailed description of the verification process.)

3.1 Details of Auditing Standards

For the auditing standards of the other Parties, refer to the respective Annex 3, Section 3.1 at the end of this Chapter.

All exporter/producer verification visits performed by the Regulatory Audit Division will be conducted in conformance with Generally Accepted Government Auditing Standards (GAGAS). These standards are embodied in the publication entitled "Government Auditing Standards" issued by the Comptroller General of the United States, General Accounting Office (GAO). The Government Auditing Standards implement the GAO standards for audit of governmental organizations, programs, activities, and functions. It is based on Generally Accepted Accounting Principles and Generally Accepted Audit Standards, requiring adherence to auditing standards covering the auditor's professional qualifications, the quality of audit effort, and the characteristics of professional and meaningful audit reports. The Government Auditing Standards incorporate audit standards and procedures adopted by the American Institute of Certified Public Accountants (AICPA).

The Government Auditing Standards set forth the following basic standards for the Generally Accepted Government Auditing Standards (GAGAS):

- General standards - Field Work standards - Reporting standards

These standards will be applied to all exporter and producer verification visits.

3.1.1 General Standards:

(1) The staff assigned to conduct the audit should collectively possess adequate professional proficiency for the tasks required.

(2) In all matters relating to the audit work, the audit organization and the individual auditors, whether government or public, should be free from personal and external impairments to independence, should be organizationally independent, and should maintain an independent attitude and appearance.

(3) Due professional care should be used in conducting the audit and in preparing related reports.

Dow

nloaded 9/25/2007

(4) Each audit organization conducting audits in accordance with these standards should have an appropriate internal quality control system in place and undergo an external quality control review.

3.1.2 Fieldwork Standards

(1) Work is to be adequately planned.

(2) Staff are to be properly supervised.

(3) When laws, regulations, and other compliance requirements are significant to audit objectives, auditors should design the audit to provide reasonable assurance about compliance with them. In all performance audits, auditors should be alert to situations or transactions that could be indicative of illegal acts or abuse.

(4) Auditors should obtain an understanding of management controls that are relevant to the audit. When management controls are significant to audit objectives, auditors should obtain sufficient evidence to support their judgement about those controls.

(5) Sufficient, competent, and relevant evidence is to be obtained to afford a reasonable basis for the auditors' findings and conclusions. A record of the auditors' work should be retained in the form of working papers. Working papers should contain sufficient information to enable an experienced auditor having no previous connection with the audit to ascertain from them the evidence that supports the auditors' significant conclusions and judgements.

3.1.3 Reporting Standards

(1) Auditors should prepare written audit reports communicating the results of each audit.

(2) Auditors should appropriately issue the reports to make the information available for timely use by management, legislative officials, and other interested parties.

(3) Auditors should report: audit objectives and the audit scope and methodology; significant audit findings, and where applicable, auditors' conclusions; recommendations for action to correct problem areas to improve operations; all significant instances of noncompliance and all significant instances of abuse that were found during or in connection with the audit; illegal acts should be reported directly to parties external to the audited entity; scope of work management controls and any significant weaknesses found; the view of responsible officials of the audited program concerning auditors' findings, conclusions, and recommendations, as well as corrections planned; noteworthy accomplishments, particularly when management improvements in one area may be applicable elsewhere; and, significant issues needing further audit work to the auditors responsible for planning future audit work.

(4) The report should be complete, accurate, objective, convincing, and as clear and concise as the subject permits.

(5) Written audit reports are to be submitted by the audit organization to the appropriate officials of the auditee and to the appropriate officials of the organizations requiring or arranging for the audits, including external funding organizations, unless legal restrictions prevent it. Copies of the report should also be sent to other officials who have legal oversight authority or who may be responsible for acting on audit findings and recommendations and to others authorized to receive such reports. Unless restricted by law or regulation, copies should be made available for public inspection.

Dow

nloaded 9/25/2007

3.2 Audit Working Papers

For the working paper requirements of the other Parties, refer to the respective Annex 3, Section 3.2 at the end of this Chapter.

Working papers are the connecting link between the Regulatory Auditor's verification visit of the exporter and/or producer and the final report. They provide detailed information in support of the findings and conclusions set out in the report. In establishing the relationship of working papers to the audit report, considerable judgement must be exercised, keeping in mind that the objective is to explain in a clear and concise manner, what was done, what was found, conclusions arrived at, and recommendations made.

The following SOP RAD1-006-97 dated April 30,1997, provides a complete outline of working paper requirements of all audits and verifications performed by the Regulatory Audit Division.

ANNEX 3 CANADA

3.1 Details of Auditing Standards

All exporter verifications performed by the Origin Audits Unit are conducted in conformity with framework for Generally Accepted Auditing Standards (GAAS), modified where applicable in order to comply with NAFTA requirements.

In Canada, the Canadian Institute of Chartered Accountants (CICA) has set forth the following basic framework for GAAS:

- General standard (3.1.1) - Examination standards (3.1.2) - Reporting standards (3.1.3)

This framework is applied in the following way to on-site exporter or producer origin verifications:

3.1.1 General Standard:

"The examination should be performed and the report prepared by a person or persons having adequate technical training and proficiency in auditing, with due care and with an objective state of mind." (1)

The Revenue Canada verification team is usually comprised of the following people:

- Accountants possessing a professional accounting designation or working towards a professional accounting designation. In Canada, the following accounting designations are recognized: Chartered Accountant (CA); Certified General Accountant (CGA); and, Certified Management Accountant (CMA). - Employees with an appropriate combination of university education and work experience. - A specialist in the tariff classification of goods.

3.1.2 Examination Standards:

a.) "The work should be adequately planned and properly executed. If assistants are employed they should be properly supervised."

Dow

nloaded 9/25/2007

i) The planning and preparation phase of an exporter/producer verification conducted by the Origin Audits Unit consists of the following steps:

Identification and Selection of Goods for Verification: A preliminary analysis of the company's response to a preference criteria B type questionnaire is performed by the Origin Audits Unit to determine whether the good should be the subject of an on-site origin verification.

Notification (Refer to Article 506 of NAFTA): Once it has been determined that an on-site origin verification will be conducted, all relevant parties will be notified that an origin verification will be conducted with respect to the specific goods under review. The relevant parties and reasons for notification are as follows:

- The exporter or producer will be sent a notice of the Department's intention to conduct a verification, by certified mail. Written consent must be given by the exporter or producer within 30 days of receipt of the notification. If the written consent is not received by Revenue Canada officials, a written determination with a notice of intent to deny preferential tariff treatment to the Canadian importers will be sent to the exporter or producer, allowing them another 30 days in which to consent before denying preferential tariff treatment.

- All known Canadian importers identified by the Origin Audits Unit as importing these products are notified in writing that the products are under review. For non-automotive goods, should it be determined that the goods under review do not qualify for a NAFTA Tariff Treatment, the assessment period generally commences with the date the importers are notified. The assessment period for automotive goods, where there is an election to average, will be based on the averaging period. Once the verification is completed, all known importers, including those who have begun to import from the exporter or producer during the course of the verification, will also be notified of the verification results.

- The Customs regions across Canada are notified of the origin verification in order to avoid further questionnaires from being sent during the course of the review. Should importations of the goods under review occur during the course of the verification, the Customs regions will usually set the entries aside in anticipation of the verification results.

- Representatives from the U.S. or Mexican Customs Services are notified of the verification visit to the exporter's or producer's premises.

Initial Planning: The initial planning of the verification involves: (1) reviewing the Certificate of Origin; (2) analyzing the response(s) to the Questionnaire; (3) the request to the exporter/producer for further information including a chart of accounts, product literature, bills of materials, information re: representative models (if applicable), organizational charts and a complete list of models manufactured and exported to Canada; (4) the collection of other Customs information from departmental resources, such as the volume and value of importations affected by the verification; and (5) the gathering of information on the industry sector to identify the significance of the verification.

Assignment Planning Memorandum: An Assignment Planning Memorandum is developed for each exporter/producer verification. The purpose of this memorandum is to ensure that the time spent at the exporter's premises is well coordinated and managed. This planning memorandum includes topics such as the reasons for verification selection, verification objectives, verification scope (and use of representative models, if applicable), an overview of the company, verification concerns, assignment of responsibilities, milestones, conduct of the verification, analysis of the potential assessment, and a listing of specific references for the verification.

Dow

nloaded 9/25/2007

Contained in the appendices to the Assignment Planning Memorandum are the verification programs which document the specific procedures to be undertaken in order to reflect the verification concerns, the complexity of issues and the reliability of the company's record keeping system. (Refer to Chapter 4, Section 4.2 for Verification Program Objectives; and Chapter 5, Section 5.5 for the Recommended Verification Procedures.) Depending on the specific circumstances involved, origin auditors should be prepared to modify the verification procedures set out in the Assignment Planning Memorandum in accordance with any additional facts that come to the attention of the auditor during the course of the verification. Amendments to the verification procedures may be required throughout the verification process. An agenda of topics to be discussed at the opening interview may also be attached as an appendix.

ii) The execution of the verification refers to the on-site visit to the premises of the exporter/producer. The on-site visit includes an opening interview with company officials to explain the objectives of the verification, the execution of the verification procedures, the preparation of the working papers in accordance with standards set out in section 3.2 of this chapter and an exit interview with company officials to discuss the findings and their impact on the NAFTA eligibility of the product(s) shipped to Canada. Depending on the complexity of the verification and the degree of verification necessary for suppliers, an on-site visit can require two to ten calendar weeks at the premises of the exporter/producer.

iii) With respect to the supervision of assistants, the team leader is responsible for the supervision of the remainder of the team. The team leader then reports to the audit manager for guidance and advice.

b.) " A sufficient understanding of internal control should be obtained to plan the audit. When control risk is assessed below maximum, sufficient appropriate audit evidence should be obtained through tests of controls to support the assessment."

The purpose of the exporter/producer verifications conducted by the Origin Audits Unit are to ensure that the goods under review qualify as originating in accordance with the NAFTA, and therefore are primarily transaction-based as opposed to a detailed system-based verification. Therefore, the verification procedures require a brief evaluation of internal controls documented on a checklist called Review of Policies, Procedures, and Internal Controls Relative to Accounting and Management Systems. This evaluation also includes a review of manuals/procedures and internal/external audit reports, interviews with company officials , reconciliations of the cost submission made by the exporter/producer to the books and records and a walkthrough of the accounting system.

c.) "Sufficient appropriate audit evidence should be obtained, by such means as inspection, observation, enquiry, confirmation, computation and analysis, to afford a reasonable basis to support the content of the report."

Most evidence is accumulated over the course of the on-site visit during which tests and procedures are performed, such as interviews with company personnel and external auditors; walkthroughs of accounting, purchasing and other systems; evaluation of internal controls; system testing; reconciliation of the cost submissions provided in the response made by the exporter/producer to our Questionnaire to the General Ledger and other source documents; and confirmations with suppliers. Examples of documents reviewed during the verification process include policy and procedures manuals, bill of materials, vendor listings, supplier correspondence, purchasing reports/records, receiving reports/records, inventory reports/records, payable reports/records, journal entries, general ledgers and loan agreements.

Dow

nloaded 9/25/2007

Sufficient and appropriate evidence is gathered using the concepts of materiality and risk. This means that the auditors design the verification procedures so as not to waste time searching for immaterial errors that would not affect the final outcome of the verification.

3.1.3 Reporting Standards:

"When engaged to express an opinion on compliance with criteria established by provisions of an agreement, statute or regulation, the auditor should:

(a) in the introductory paragraph of his or her report:

(i) state that compliance with criteria established by provisions of the agreement, statute or regulation identified in the report has been audited;

(ii) identify the provisions of the agreement, statute, or regulation;

(iii) describe or refer to disclosure of any significant interpretation of the provisions made by the management of the entity;

(iv) when a report on compliance with criteria established by provisions of the agreement, statute or regulation has been issued in the same circumstances for the preceding period, describe or refer to disclosure of a change in any significant interpretation of the provisions made by the management of the entity;

(v) indicate any other information having particular relevance to the party to whom the report is addressed including the subject of any reservation of opinion on the most recent audited financial statements;

(vi) state that such compliance is the responsibility of the management of the entity; and

(vii) state that it is the auditor's responsibility to express an opinion on this compliance based on the audit;

(b) in the scope paragraph of his or her report state that:

(i) the audit was conducted in accordance with generally accepted auditing standards;

(ii) those standards require that the audit be planned and performed to obtain reasonable assurance whether the entity complied with criteria established by provisions of the agreement, statute or regulation; and

(iii) such an audit includes:

- examining, on a test basis, evidence supporting compliance; - evaluating the overall compliance; and - assessing, where applicable, the accounting principles used and significant estimates made by the management of the entity;

(c) in the opinion paragraph of his or her report express an opinion whether the entity has complied, in all material respects, with criteria established by provisions of the agreement, statute or regulation; and

Dow

nloaded 9/25/2007

(d) disclose the addressee, the name of the auditor (or firm), the date of the report and the place of issue."

The reporting phase of the exporter/producer verification conducted by the Origin Audits Unit involves the organization of the file, the writing of the initial and final written determinations for presentation to the exporter/producer, and the formal notification to the Canadian importers and Canada Customs regional offices as to the verification result. Assessments to importers are currently issued by the Canada Customs regional offices.

The flow and timing of the notifications issued as a result of the verifications are as follows:

After every verification, an initial written determination is issued to the exporter/producer. In general, the initial written determination is only issued after the file (working papers) and the written determination have been reviewed for quality control purposes and approved by the Audit Manager and/or Senior Management.

The initial written determination's purpose is to identify the verification objectives, the scope of the verification (the period under review is typically a combination of the period for which the response to the Questionnaire was prepared, and if a significant amount of time has elapsed, the current fiscal period; the products under review; and the areas focused on during the course of the review); to formally explain the verification findings to the exporter or producer; and to conclude our verification as to the eligibility of the product. Article 506(9) of the NAFTA states that "The Party conducting a verification shall provide the exporter or producer whose good is the subject of the verification with a written determination of whether the good qualifies as an originating good, including findings of fact and the legal basis for the determination". If the goods do not qualify, the written determination will serve as the notice of the intent to deny preferential tariff treatment to the importers. This notice allows 30 days to the exporter or producer to provide, in writing, comments or additional information regarding the eligibility of the product.

After 30 days, when all of the further information has been examined (if received), a final written determination is sent to the exporter/producer.

At the time the final written determination is issued, Revenue Canada will send notifications to Canadian importers and to Canadian Customs regional offices of whether the goods were found to be originating or non-originating. A re-determination of origin made as a result of a verification would be made under section 61(c) of the Customs Act (section 61(d) of the Customs Act for re-determination of origin where there is an election to average for an automobile manufacturer). This section of the Act enables Revenue Canada to re-assess additional duties on specific importations made by the Canadian importers of the goods that have been found to be non-originating. Therefore, as a result of the goods not qualifying for preferential tariff treatment, the Canada Customs regional offices will send out re-assessments identified in Detailed Adjustment Statements (DAS) invoicing the importers for duties and taxes owing on the affected entries. As well, for each re-assessment made to an importer, the exporter will receive a corresponding notice of denial.

3.2 Working Papers

3.2.1 Introduction

Working papers provide, where necessary, detailed information in support of the findings and conclusions set out in the written determination. In establishing the relationship of working papers to the written determination, considerable judgment must be exercised, keeping in mind that the objective is to explain as simply and clearly as possible what was done, what was found,

Dow

nloaded 9/25/2007

conclusions arrived at, and recommendations made. Note that working papers or schedules will mostly be standardized and generated through laptop computers.

The working papers are the property of the Origin Audits Unit. Procedures have been established which ensure that the custody and confidentiality of the information obtained during the course of a verification. This information may be disclosed to those authorities responsible for the administration and enforcement of determinations of origin, and of customs and revenue matters, within the Administration that conducted the verification.

3.2.2 Purpose

The purpose of working papers are:

a) To provide an explanation of the nature and extent of the verification work performed.

b) To facilitate subsequent discussions with the exporter/producer.

c) To support any adjustments made, and aid in the preparation of the assessment.

d) To support significant items not requiring change, as set out in the written determination.

e) To cover any special situation that the auditor wishes to put on record such as:

- An explanation of a complex calculation; - Any difficulty encountered in public relations; - A problem with facilities provided, etc..

f) To provide evidence in support of fraud or evasion charges.

g) To identify items to be followed up in subsequent verifications.

3.2.3 Use

It is imperative to prepare the working papers in such a manner that they may be understood and utilized by appropriate parties, namely:

a) Senior officers in resolving problems (i.e. disputed assessment).

b) Officers conducting subsequent verifications.

c) Officers conducting special projects, such as industry surveys, etc.

d) Audit Unit Managers to assist in staff evaluation and identification of training needs.

e) Audit Unit Managers, Internal Audit and Auditor- General's Staff to monitor the quality of verification work and adherence to departmental standards.

f) Policy and investigations officers to review pertinent information about the exporter/producer.

g) Other departmental officers and the Department of Justice.

Dow

nloaded 9/25/2007

3.2.4 Format

The format for working papers is as follows:

a) Each set of working papers requires an index. A master index along with a detailed volume index should be placed in front of each working paper file.

b) Working papers shall be arranged, coded and numbered in the sequence provided in the index.

c) Working papers shall be prepared using 8?" x 14" size paper or any prescribed form, as applicable, in order to facilitate the verification, review and report preparation.

3.2.5 Preparation and Disclosure Requirement

The following requirements apply to computer generated and manually prepared working papers:

a) Each working paper requires the following:

- the name of the company and the file number; - the initials of the auditor who prepared the working paper along with the date should be indicated in the upper right hand corner; - the page number (in accordance with the index) in the bottom right hand corner; - the diskette filename in the bottom left hand corner; and - the objective of the work, a reference to the procedure performed, a description of the content, the source of information, the methodology and the conclusions reached.

b) Photocopies of existing relevant documentation should be obtained, thus avoiding unnecessary hand copying. All documents obtained by the auditor should identify the following information:

- the name of the company and the file number; - the initials of the auditor along with the date should be indicated in the upper right hand corner; - the page number (in accordance with the index) in the bottom right hand corner; and - an indication of the source of the information i.e. prepared by client (PBC) and document name, along with the company representative's name who provided the document and the date when the document was received.

c) The information must be presented in an orderly, concise, legible and logical manner, be clear and understandable and free of clerical errors.

d) Working papers are to be indexed and cross-referenced, as they are prepared using a red pen or pencil. Using the grandfather, father, son model, cross referencing should take place from behind the "grandfather" amount or statement, to in front of the "father"; from behind the "father" to in front of the "son".

e) The file is to be properly organized, with old, irrelevant material stripped from the file.

f) Auditors should confine their use of colored marks to red, as other colors are reserved for the reviewers. A legend of the audit tick marks should appear in the beginning of the file, section of the file or at the bottom of each working paper.

Dow

nloaded 9/25/2007

g) The audit tick marks used by the auditor should be discrete neat and legible. They should never be done on the original documents.

h) All verification procedures used by the auditor must be fully disclosed in the working paper.

i) The verification techniques employed by the auditor must be indicated in the working papers.

j) The content of the working papers must clearly disclose applicable legislation and compliance therewith.

k) Auditors are to confirm verbal advice, in writing, in order to avoid future misunderstanding, and note in the working papers information provided to the producer/exporter with respect to the NAFTA.

l) Working papers often contain confidential information and should be treated accordingly.

m) A disk copy of all working papers should be given to the auditor-in-charge when the verification is complete. 3.2.6 Verification Scope and Coverage The scope of the verification should be indicated on the working papers. The areas covered, the areas examined in depth and the areas excluded should be supported with reasons and in accordance with the assignment planning memorandum and the policies.

3.2.7 Standard Forms

The following are standardized forms, which should be completed and used in every verification file for control purposes:

a) A completed and signed Planning- Revenue Risk Analysis and Importer Notification Procedures form should be included in the file and is to be done prior to going out on an verification. The objective of these procedures is to calculate the revenue risk if the goods exported into Canada are determined to be non-originating under NAFTA and to identify all of the Canadian importers to be notified about the origin verification.

b) A profile sheet should be completed and placed in front of the file (this document contains the actual and projected completion dates, costs and time; the re-assessment amount; and the importers affected by the re-assessment). Where it is not self-evident, the auditor will explain the reasons for any unusual delay in commencing, completing and submitting the assignment.

c) A verification completion checklist should be placed in front of the file and completed in order to ensure that a complete file is submitted for review.

d) A completed and signed verification program should be placed in front of the applicable section of the file.

ANNEX 3 MEXICO

3.1 Generally Accepted Auditing Standards

In Mexico, the Instituto Mexicano de Contadores P?os, A.C. (IMPC) has set forth the following basic framework for Mexican GAAS:

Dow

nloaded 9/25/2007

Auditing Standards

Auditing Standards are the minimum quality requirements related to the auditors work with respect to the general, examination and reporting standards.

General Standards

General Standards refer to the attributes the auditor must possess in order to conduct an audit. Within these standards, an auditor should have the adequate technical training, skills and professional proficiency before conducting any audit, and should maintain these standards as long as the auditor performs his/her professional audit activities.

The auditor is obliged to conduct an audit, and the preparation of the related reports thereof, with due professional care and professional diligence. In addition, the auditor should be free from any external impairment to independence in all matters related to the audit work.

Examination Standards

General Standards mention that due professional care should be used in conducting an audit and for the preparation of related reports. In spite the complexity of determining the extent of due professional care and diligence in every audit, there are certain important elements that must be followed. These basic elements represent the minimum procedures in order to achieve the audit objectives.

The examination standards are the basic elements to be observed while conducting audits in order to comply with the "due care" and "professional diligence" requirements referred to in the General Standards. The examination standards are the following:

a) An audit must be adequately planned. If assistants are used to conduct the work, they must be appropriately supervised.

b) An entity's internal control structure must be evaluated to provide the auditor a reasonable assurance of its effectiveness reliability and to determine the nature, timing, and extent of tests audit procedures to be performed applied.

c) In conducting audits, by the application of audit procedures, the auditors employ auditing procedures to must obtain sufficient, competent, and relevant evidence that enables them to count on will provide a reasonable and objective basis for supporting their opinions.

Reporting Standards

The final result of the auditor?s work is the standard report or opinion. By means of this report, all interested parties may be informed of the audit findings and the auditor?s opinion. The report provides reliability on assurance to the entity's financial position and results of operations that are stated in the financial statements. Moreover, clients and third parties are informed of the results of the auditor?s work through this report or opinion, and in most cases, the report is the only part of the audit work that is at their reach.

Every time a public accountant associates his/her name in connection with financial information or financial statements, the public accountant should clearly determine his relationship with the such information, his opinion of the latter and if applicable, limitations in the conduction of his examination, reservations that derive from these limitations and any other audit evidence that

Dow

nloaded 9/25/2007

precludes constrain the auditor from reporting a professional opinion, even though his examination was conducted in accordance with GASS.

When issuing an opinion related to the financial statements, the auditor must observe the following:

a) That financial statements were prepared in accordance with generally accepted accounting principles (GAAP);

b) That GAAP was applied on a consistent basis;

c) That information stated in financial statements and related notes, is adequate and sufficient for a reasonable interpretation.

Consequently, in the event of any exception to (a),(b) or (c), the auditor must disclose such deviations and their quantified effect on the financial statements.

The reporting phase of the exporter/producer verification conducted by the Customs Administration involves the organization of the file, the writing of the initial and final written determinations for presentation to the exporter/producer, and the formal notification to the Mexican known importers and depending on each case to the Customs regional offices as to the verification result. Assessments and/or liquidation to importers are currently issued at the Ministry of Finance and Public Credit Headquarters.

The flow and timing of the notifications issued as a result of the verifications are as follows:

After every verification, an initial written determination is issued to the exporter/producer. In general, the initial written determination is only issued after the file (working papers) and the written determination have been reviewed for quality control purposes and approved by the Director of International Audit and the Director of the International Legal Department.

The initial written determination's purpose is to identify the verification objectives, the scope of the verification to formally explain the verification findings to the exporter or producer; and to conclude our verification as to the eligibility of the product. Article 506(9) of the NAFTA states that "The Party conducting a verification shall provide the exporter or producer whose good is the subject of the verification with a written determination of whether the good qualifies as an originating good, including findings of fact and the legal basis for the determination". If the goods do not qualify, the written determination will serve as the notice of the intent to deny preferential tariff treatment to the importers. This notice allows 30 days to the exporter or producer to provide, in writing, comments or additional information regarding the eligibility of the product. (Refer to Appendix N)

After 30 days, when all of the further information has been examined (if received), a final written determination is sent to the exporter/producer. (Refer to Appendix N)

After the final written determination is notified to the exporter or producer, the Direction of International Audit will send, pursuant to article 48 of the Fiscal Federal Code, notifications (oficio de observaciones) to the Mexican importers of the goods subject to verification, of whether the goods were found to be originating or non-originating. (Refer to Appendix O). This notice allows 15 labor days to the importer to provide, in writing, comments or additional information regarding the content of the notification.

Dow

nloaded 9/25/2007

After the 15 labor day period, and depending upon the result of the analysis of the further information (if received), a liquidation for duties and taxes owing on the affected entries for the goods that have been found to be non-originating may be notified to the importer of such goods.

3.2. Working Papers

Introduction

Working papers provide, where necessary, detailed information in support of the findings and conclusions set out in the written determination. In establishing the relationship of working papers to the written determination, considerable judgment must be exercised, keeping in mind that the objective is to explain as simply and clearly as possible what was done, what was found, conclusions arrived at, and recommendations made. Note that working papers or schedules will mostly be standardized and generated through laptop computers.

The working papers are the property of the Customs Administration. Procedures have been established which ensure that the custody and confidentiality of the information obtained during the course of a verification. This information may be disclosed to those authorities responsible for the administration and enforcement of determinations of origin, and of customs and revenue matters, within the Customs Administration that conducted the verification.

Purpose

The purposes of working papers are:

a) To provide an explanation of the nature and extent of the verification work performed.

b) To facilitate subsequent discussions with the exporter/producer.

c) To support any adjustments made, and aid in the preparation of the assessment.

d) To support significant items not requiring change, as set out in the written determination.

e) To cover any special situation that the auditor wishes to put on record such as:

-An explanation of a complex calculation; -Any difficulty encountered in public relations; -A problem with facilities provided, etc.

f) To provide evidence in support of customs fraud or customs evasion charges.

g) To identify items to be followed up in subsequent verifications.

Use

It is imperative to prepare the working papers in such a manner that these may be understood and utilized by appropriate parties, namely:

a) Senior officers in resolving problems (i.e. disputed assessment).

b) Officers conducting subsequent verifications.

Dow

nloaded 9/25/2007

c) Officers conducting special projects, such an industry surveys, etc.

d) Audit Unit Managers to assist in staff evaluation and identification of training needs.

e) Audit Unit Managers, Internal Audit and Auditor-General's Staff to monitor the quality of verification work and adherence to departmental standards.

f) Policy, collections and investigations officers to review pertinent information about the exporter/producer.

g) Other departmental officers within the Customs Administration.

Preparation and Disclosure Requirement

The following requirements apply to computer generated and manually prepared working papers:

a) Each working paper requires the following information:

- the name of the company and the file number; - the initials of the auditor who prepared the working paper along with the date should be indicated - the page number (in accordance with the index) in the bottom right hand corner; - the diskette filename - the objective of the work, a reference to the procedure performed, a description of the content, the source of information, the methodology and the conclusions reached (sometimes this may apply to a clearly identifiable group of working papers).

b) Photocopies of existing documentation should be obtained, thus avoiding unnecessary hand copying. All documents photocopied by the auditor should have an indication of the source of the information i.e. prepared by client (PBC) or document name. Only relevant photocopies should be included in the working papers.

c) The information must be presented in an orderly, concise, legible and logical manner, be clear and understandable and free of clerical errors.

d) Working papers are to be indexed and cross-referenced as they are prepared using a red pencil.

e) The file is to be properly organized, with old, irrelevant material stripped from the file.

f) The audit tick marks used by the auditor should be discrete neat and legible. They should never be done on the original documents.

g) All verification procedures used by the auditor must be fully disclosed in the working paper.

h) The verification techniques employed by the auditor must be indicated in the working papers.

i) The content of the working papers must clearly disclose applicable legislation and compliance therewith.

j) Auditors are to confirm verbal advice, in writing, in order to avoid future misunderstanding.

Dow

nloaded 9/25/2007

k) Working papers often contain confidential information and should be treated accordingly.

Verification Scope and Coverage

The scope of the verification will be indicated in the notice of intention to conduct an on-site verification or will be attached to in the letter related to an origin verification questionnaire.

The working papers should include the areas covered, the areas examined in depth and the areas excluded supported with reasons and in accordance with the assignment planning memorandum and the policies.

Standard Forms

The following are standardized forms, which should be completed and used in every audit file for control purposes:

a) A completed and signed Planning-Memorandum analysis and importer notification procedures form should be included in the file and is to be done prior to going out on a verification. The objective of these procedures is to calculate the revenue risk if the goods exported into territory are determined to be non-originating under NAFTA and to identify all of the known importers to be notified about the exporter/producer origin verification.

b) A profile sheet should be completed and placed in front of the file (this document contains the actual and projected completion dates, costs and time; the re-assessment amount; and the importers affected by the re-assessment). Where it is not self-evident, the auditor will explain the reasons for any unusual delay in commencing, completing and submitting the assignment. (See Appendix R).

c) A verification completion checklist should be placed in front of the file and completed in order to ensure that a complete file is submitted for review.

d) A completed and signed verification program should be placed in front of the applicable section of the file. (Standard verification programs are found in section 5.5 "Recommended Verification Procedures". It should be noted that these programs may be modified to better reflect the concerns of the verification.)

Dow

nloaded 9/25/2007

NORTH AMERICAN FREE TRADE AGREEMENT (NAFTA) AUDIT (VERIFICATION) MANUAL

CHAPTER 4 OBJECTIVES OF NAFTA AUDITS (VERIFICATIONS)

This chapter explains the overall objective for conducting a North American Free Trade Agreement (NAFTA) exporter and/or producer verification. The specific verification program bjectives are also provided.

4.1 Verification Objective

The overall objective of the exporter and/or producer verification is to confirm that the product(s) certified by the exporter and/or producer qualify as originating in accordance with Chapter 4 of the NAFTA and the NAFTA Rules of Origin Regulations (the Regulations).

4.2 Objectives of the Verification Programs

Verification programs should be developed based on the verification objective stated in Section 4.1, the information gathered, and the concerns identified during the planning and preparation phase of the audit. Listed below are the specific verification program objectives subject to the verification process. Chapter 5 contains the verification programs and sub-programs which identify the recommended verification procedures to be utilized in meeting these objectives.

OBJECTIVES OF THE VERIFICATION PROGRAMS

A. NON-QUALIFYING OPERATIONS PROGRAM

To ensure that the good does not qualify as originating because of mere dilution with water or another substance or because of a production or pricing practice designed to circumvent the Rules of Origin as set out in Chapter 4 of the NAFTA.

B. TARIFF CLASSIFICATION PROGRAM

To ensure that all non-originating materials are sufficiently transformed in the NAFTA territory so as to undergo the necessary tariff classification change as required by the Specific Rule of Origin applicable to the exported good and to ensure that the finished good and the non-originating materials used to produce it are properly classified.

REGIONAL VALUE CONTENT REQUIREMENT

C. TRANSACTION VALUE METHOD - (RVC) - PROGRAM

To ensure that the Regional Value Content requirement, as required by the rules of origin, has been met where the Transaction Value Method has been used.

D. NET COST METHOD - (RVC) - PROGRAM

To ensure that the Regional Value Content requirement, as required by the rules of origin, has been met where the Net Cost Method has been used.

E. TRANSSHIPMENT PROGRAM

Dow

nloaded 9/25/2007

To verify that the originating good, by reason of having undergone production that satisfies the requirements of Article 401 of the NAFTA, (1) Is not withdrawn from Customs control outside the territories of the NAFTA countries and (2) Does not undergo further production or any other operation outside the territories of the NAFTA countries, other than unloading, reloading, or any other operation necessary to preserve it in good condition, such as inspection, removal of dust that accumulates during shipment, ventilation, spreading out or drying, chilling, replacing salt, sulphur dioxide or other aqueous solutions, replacing damaged packing materials and containers and removal of units of the good that are spoiled or damaged and present a danger to the remaining units of the good, or to transport the good to the territory of a NAFTA country.

For additional verification programs from the other Parties, refer to the respective Annex, Section 4.2 at the end of this Chapter.

ANNEX 4 CANADA

4.2 Objectives of the Verification Programs

F. TARIFF TREATMENT PROGRAM

TO ENSURE THAT THE ORIGINATING GOODS ARE IMPORTED USING THE CORRECT TARIFF TREATMENT AS SET OUT IN ANNEX 302.2 OF THE NAFTA AND TO ENSURE THAT NON-ORIGINATING GOODS ARE IMPORTED USING THE CORRECT NON-NAFTA TARIFF TREATMENT.

Dow

nloaded 9/25/2007

NORTH AMERICAN FREE TRADE AGREEMENT (NAFTA) AUDIT (VERIFICATION) MANUAL

CHAPTER 5 SCOPE OF NAFTA AUDITS (VERIFICATIONS)

This chapter outlines the extent of the coverage for the exporter and/or producer audits conducted by the Customs Administrations of each Party. The scope has been defined to include the verification period, coverage, identification of importers, the assessment/liquidation period and the use of recommended verification procedures.

5.1 Verification Period

For establishment of the verification periods of the other Parties, refer to the respective Annex 5, Section 5.1 at the end of this Chapter.

The period subject to audit verification would in most cases be the fiscal year of the exporter/producer.

For this period, the goods imported should be matched to the period in which the goods were produced. In those cases involving a complex production process or where there is a time lapse between the production and the importation periods, appropriate measures will be taken to reasonably satisfy this requirement.

5.2 Coverage

For determining the coverage of verifications conducted by the Customs Administrations of the other Parties, refer to the respective Annex 5, Section 5.2 at the end of this Chapter.

The scope of verifications conducted by Regulatory Audit may include all models of goods reported on the Certificate of Origin produced by that exporter/producer that are exported to the U.S. for which preferential tariff treatment is claimed.

5.3 Identification of Importers

For the purposes of identification of importers by the Customs Administrations of the other Parties, refer to the respective Annex 5, Section 5.3 at the end of this Chapter.

An important function during the initial stages of a verification is the identification and notification of all known United States importers. The current policy followed by Regulatory Audit is to query the Automated Commercial System (ACS) using the Manufacturer's Identification Number to identify U.S. importers. The United States companies who have imported goods from that exporter/producer are identified and notified in writing that the goods are under review.

5.4 Assessment/Liquidation Period

For purposes of determining the assessment/liquidation period for the other Parties, refer to the respective Annex 5, Section 5.4 at the end of this Chapter.

Results of a verification will be applied to unliquidated entries.

5.5 Recommended Verification Procedures - Verification Programs

Dow

nloaded 9/25/2007

Verification teams prepare verification programs based on factors such as the verification concerns identified during the planning and preparation phase, the complexity of the issues, and the reliability of the company's record keeping system.

Verification Programs are evolving documents, created during the planning phase and added to throughout the course of the verification as new concerns are identified or more comprehensive testing is required, based on the materiality of the costs involved.

This is not to say, however, that there are not procedures in the verification programs that can be standardized. With this in mind the following verification programs have been prepared, incorporating procedures used during the exporter and/or producer audits conducted by the Customs Administration of each Party. These procedures have been found to be useful during several verifications already conducted. The inclusion of these procedures in a verification program would of course be dependent on the risks and concerns associated with that particular situation.

Note that the following programs contain procedures that are oriented towards an on-site visit, verifying goods for which preference criterion B is applicable.

Also note that goods that fall under preference criterion B could be categorized as either non-automotive goods or automotive goods. The following programs (Chapter 5) contain the recommended verification procedures that are oriented towards verifying that a non-automotive good satisfied the rule of origin requirements

The Verification Programs contained in Chapter 5 are as follows:

A. VERIFICATION PROGRAM - NON-QUALIFYING OPERATIONS B. VERIFICATION PROGRAM - TARIFF CLASSIFICATION VERIFICATION PROGRAMS - REGIONAL VALUE CONTENT (RVC): C. TRANSACTION VALUE METHOD VERIFICATION PROGRAM

Sub-programs 1 through 13

1) Eligibility for the transaction value method 2) General- RVC information 3) Plant tour 4) Review of management of information system 5) Transaction value of the good 6) Originating and non-originating materials 7) Value of materials 8) Intermediate materials 9) Packaging materials and containers for retail sale 10) Packing materials and containers for shipment 11) Accessories, spare parts, and tools 12) Inventory management system 13) Calculation of the regional value content

D. NET COST METHOD VERIFICATION PROGRAM

Sub-programs 1 through 13 1) General- RVC information 2) Plant Tour

Dow

nloaded 9/25/2007

3) Review of management of information system 4) Originating and non-originating materials 5) Value of materials 6) Intermediate materials 7) Net cost calculation i Total Costs ii Excluded costs 8) Packaging materials and containers for retail sale 9) Packing materials and containers for shipment 10) Accessories, spare parts and tools 11) Inventory management system 12) Accumulation 13) Calculation of the regional value content E. VERIFICATION PROGRAM - TRANSSHIPMENT

For additional verification programs from the other Parties, refer to the respective Annex, Section 5.5 at the end of this Chapter.

Appendix L is the verification program which contains the recommended verification procedures associated with verifying goods claimed to be wholly obtained or produced entirely in the territory of one or more of the Parties (preference criterion A).

Appendix M is the verification program which contains the recommended verification procedures associated with verifying goods claimed to be produced entirely in the territory of one or more of the Parties exclusively from originating materials (preference criterion C).

Appendix N is the verification program which contains the recommended verification procedures associated with verifying goods claimed to satisfy preference criterion D.

Appendix O is the verification program which contains the recommended verification procedures to be used in the verification of a light duty automotive good for which the motor vehicle producer has elected to average.

Appendix P is the verification program which contains the recommended verification procedures to be used in the verification of a light duty automotive good for which the motor vehicle producer has not elected to average.

Appendix Q is the verification program which contains the recommended verification procedures to be used in the verification of a heavy duty automotive good for which the motor vehicle producer has elected to average.

Appendix R is the verification program which contains the recommended verification procedures to be used in the verification of a heavy duty automotive good for which the motor vehicle producer has not elected to average.

Where applicable, the above noted verification programs for automotive goods contain procedures to verify the applicable regional value content when the provisions concerning new and refit plants are being used. As well, the programs consider the possibility of the automotive parts producers deciding to calculate RVC based on averaged costs.

- All of the above verification programs are identical and uniform for all Parties.