-

8/6/2019 NAB: Domestic sector struggling to gain momentum as

confidence slumps.

1/10

Embargoed until:

11.30am Tuesday 12 July 2011

Monthly Business Survey June 2011

Domestic sector struggling to gain momentum as confidence

slumps. Forecasts for growth lowered and rate rises delayed

reflecting current slowdown and, in the medium term, carbon.

Activity in the domestic economy was a little stronger in June,

although overall conditions

remained fairly subdued suggesting the economy is still

struggling to find traction following theflood-induced slowdown.

Business confidence deteriorated sharply in June, with the index

nowin line with the relatively weak levels recorded in December

(surveyed immediately following thefloods).

Conditions in retail fell to worryingly low levels (to around

that of Nov 2008, just prior to theGovernments initial cash

handouts), while manufacturing, construction and wholesale

wereagain poor. The high Australian dollar, continued cautiousness

of households and concernsabout the global outlook appear to be

eroding sentiment, with weak confidence reported inconstruction,

manufacturing, retail and wholesale. While conditions were weaker

in mining, theoutlook remains strong as reflected in high

confidence levels.

Overall the gap between weak & strong industries is reaching

historical highs (see page 3). Thislargely reflects weakening in

the poor performers similar to the 2000 slowdown.

Orders weakened in June and continued to contract; the stocks

index was also lower, implyingan expectation of softer near-term

demand. Capacity utilisation marginally higher in the monthat above

average levels. Based on average conditions for the June quarter,

we estimate6-monthly annualised growth in domestic demand and GDP

of around 3%.

Labour costs growth picked up in the month, while price

inflation was a little softer.

Implications for NAB forecasts:

Global growth is slowing from the exceptionally strong pace seen

last year reflecting tighterpolicy, the Japanese disasters impact

on global supply chains, oil prices and lower realhousehold

incomes. Despite this, global growth is expected to remain a touch

above its 4%trend through 2011 and 2012, mainly due to solid

outcomes in China, India, Latin America and

the Asian Tiger economies. Developed economy growth is nearer 2%

while emerging economygrowth is 6 to 7%.

Australian forecasts weaker in Q2 & Q3 reflecting continuing

softness in discretionary spending,and delays in recovery of coal

export volumes. Severe weakness in retail in latest survey,

alongwith continuing softness in wholesale, parts of transport,

manufacturing and construction pointsto ongoing softness. Strong

export prices, mining investment and Queensland rebuildingexpected

to lift GDP growth in Q4 with more solid growth in 2012. In 2012/13

forecasts includetentative impacts from the carbon tax announcement

(-0.2% off GDP). Inflation % higher,assuming no wages impact. We

now expect GDP growth of 1.7% in 2011 and 4.6% in 2012.

Next 25 bp rise in cash rate deferred until December, when

growth momentum more apparentand labour market tightens

significantly. Final 25 bp rise put back to May 2012.

Key monthly business statistics*

Apr May Jun Apr May Jun

2011 2011 2011 2011 2011 2011

Net balance Net balance

Business confidence 7 6 0 Employment 4 2 5

Business conditions 5 0 2 Forward orders -1 -2 -4

Trading 7 1 4 Stocks 2 0 -2

Profitability 3 -1 -1 Exports -2 -4 -3

% change at quarterly rate % change at quarterly rate

Labour costs 1.5 1.0 1.3 Retail prices 0.1 0.1 0.6

Purchase costs 0.9 0.9 0.6 Per cent

Final products prices 0.6 0.4 0.3 Capacity utilisation rate 81.7

81.6 81.7

* All data seasonally adjusted and subject to revision. Cost and

prices data are monthly percentage changes expressed at a

quarterlyrate. All other data are net balance indexes, except

capacity utilisation, which is an average rate, expressed as a

percentage. Fieldworkfor this Survey was conducted from 24 to 30

June, covering over 400 firms across the non-farm business

sector.

For more information contact:Alan Oster, Chief Economist(03)

8634 2927 0414 444 652

Next release: 21 July 2011 (June quarterly)

-

8/6/2019 NAB: Domestic sector struggling to gain momentum as

confidence slumps.

2/10

Embargoed until 11.30am Tuesday, 12 July 2011

Analysis

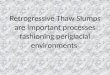

Conditions rise but still subdued

-40

-30

-20

-10

0

10

20

II III IV I II III IV I II III IV I II

2008 2009 2010 2011

Seasonally adjusted Trend

Conds 1990s recn

Business conditions (net balance)

Average of the indexes of trading conditions, profitability

andemployment.

The business conditions index rose by2 points to +2 index points

in June, partlyunwinding the previous months decline.Despite

conditions improving a little in the

month, the overall picture remains quitesubdued, likely

reflecting the negativeimpact the high Australian dollar on anumber

of trade-based industries, continuedcautiousness of households and

concernsabout global growth. The mild uptick in theconditions index

in June reflected improvedtrading conditions (up 3 to +4 points)

andemployment (up 3 to +5 points). Profitabilitywas unchanged

(-1).

The conditions index, at +2 points, ishowever still 4 points

below the long-termaverage level (of +6 points). There is still

strong evidence of a patchwork economy,with professional

service-based industriesand mining continuing to report

relativelysolid conditions, while retail is deterioratingsharply to

concerning levels, and weaknessis persisting in manufacturing,

constructionand wholesale.

The loss in economic momentum over thefirst half of this year,

together with stalledasset prices, appear to be weighing onbusiness

confidence levels, with the indexfalling by 6 points to a reading

of zero indexpoints. The sovereign debt concernscoming out of

Europe and uncertainty onthe US growth momentum are also

nothelping. The current reading on confidenceis significantly below

the average of theseries (of +7).

Business conditions by industry. Thechange in conditions across

industries wasmixed in June, with solid improvementsreported in

finance/business/property,manufacturing and recreation &

personalservices, while conditions deterioratedsharply in mining

and retail. Consistent with

a sharp improvement, conditions werestrongest in

finance/business/property(+20), followed by recreation &

personal(+17), and were by far the weakest in retail(-24).

Confidence falls

-40

-30

-20

-10

0

10

20

II III IV I II III IV I II III IV I II

2008 2009 2010 2011

Seasonally adjusted Trend

Conf 1990s recn

Business confidence (net bal., s.a.)

Excluding normal seasonal changes, how do you expect thebusiness

conditions facing your industry in the next month tochange?

Business conditions by state. Conditions, in seasonally adjusted

terms, rose solidly in NSW(up 18 to +11 points) more than reversing

last months surprising falls and are now thestrongest of any state.

Business conditions also improved in Victoria (up 2 to +3 points).

Allother states, however, recorded deteriorating conditions. The

variation in state conditionswidened in June, with the weakest

conditions recorded in Tasmania (-37, on a small sample)and SA

(-11).

2

-

8/6/2019 NAB: Domestic sector struggling to gain momentum as

confidence slumps.

3/10

Embargoed until 11.30am Tuesday, 12 July 2011

Analysis (cont.)Business confidence by industry. Confidence

deteriorated across a majority of industrieswith the exception of

mining, where confidence improved, and wholesale, where it

wasunchanged. The most significant loss in sentiment was in

construction andfinance/business/property. Confidence levels were

highest in mining (+17), followed bytransport & utilities and

finance/business/property (both +5), and weakest in construction

(-14).

Business confidence by state. Confidence levels deteriorated

across all states in the month,with the sharpest falls recorded in

Victoria, WA and Tasmania. Confidence is now weakest inTasmania

(-18), Victoria (-4) and SA (-3), and strongest in WA (+4) and NSW

(+1).

The variation in business conditionsacross sectors has become

increasinglypronounced since late 2009. Disparitybetween sector

performance can beobserved by comparing businessconditions of the

(currently) strongestperforming sectors (mining, transport

&utilities, recreation & personal servicesand

finance/business/property) withconditions of weakest performing

sectors(retail, manufacturing, construction andwholesale). As shown

in the chart, thegap between trend conditions in theseindustries is

currently around levels lastseen in the early 2000s global

recession.One key feature of the current period isthat like 2000

the opening up of the gaphas largely been explained bydeterioration

in the weak industries rather than a strengthening in one or

twosectors such as mining.

Patchwork economy pronounced

-30

-20

-10

0

10

20

2000 2003 2006 2009 2000 2003 2006 2009

Net

bal.

-30

-20

-10

0

10

20

Net

bal.

Weak**

Strong*

Business conditions3-month moving average

* Strong industries include mining, transport & utili ties,

recreation & personal

services and finance/business/property

** Weak industries include retail, manufacturing, construction

and wholesale

Gap between weak &

strong industry conditions

The new orders index eased further in June (down 2 points to -4

index points) and is now

5 points below its long-term average level. There were

particularly sharp falls in transport &utilities orders partly

offset by stronger mining orders. Overall orders levels remain very

poor inmanufacturing, transport & utilities and retail but

strong in mining. Capacity utilisation edgedup a little to 81.7% in

June, from 81.6% in May, and remains marginally above its

long-termaverage (81.2%). By industry, capacity appears to have

tightened in finance/property/business,manufacturing and recreation

& personal services, while less capacity was utilised in

mining,transport & utilities and wholesale. Capital expenditure

was unchanged at +4 points in June held up by strength in expected

mining investment remaining 2 points below the averagelevel.

Forward orders implied softer 6-monthlyannualised demand growth

for June quarter2011 than the 3.8% reported in the March

quarter national accounts. Based on theaverage forward orders

for the June quarter,we estimate 6-monthly annualised demandgrowth

of around 3%.

Demand growth moderating

-4

-2

0

2

4

6

8

10

02 03 04 05 06 07 08 09 10 11

Domestic demand Prediction from orders

Forward orders (change & level) as an indicator of

domestic demand (6-monthly annualised)

3

-

8/6/2019 NAB: Domestic sector struggling to gain momentum as

confidence slumps.

4/10

Embargoed until 11.30am Tuesday, 12 July 2011

Analysis (cont.)

In contrast, business conditions imply that6-monthly annualised

GDP growth wassignificantly higher than the -0.8% recorded in

theMarch quarter accounts. The average of the Junequarter monthly

business conditions readings

would imply 6-monthly annualised GDP growth ofaround 3%.

But again this is likely to overstate GDP growth incurrent

circumstances, because the survey is notfully capturing the

(significant) effects of the floodson coal mine and iron ore

production. Rather ourexpectations are for around a flat outcome in

thefirst half of 2011.

GDP growth around average

-2

0

2

4

6

8

02 03 04 05 06 07 08 09 10 11

GDP Prediction from bus conds

Business conditions (change & level) as an indicator of

GDP (6-monthly annualised)

Elsewhere in the survey, cash flow was strongest in

finance/business/property and transport &storage, and weakest

in retail.

Labour costs growth (a wages bill measure) picked up in June and

was a little higher inannualised 3-monthly-average terms, at 5.1%.

Annualised 3-monthly average growth wasstrongest in mining and

softest in recreation & personal services.

Price inflation was softer in June, at 1.7% inannualised

3-monthly-average terms. It appearsthat retailers have passed some

of the rise inlabour costs on to consumers, with retail

priceinflation picking up to 1.1% in annualised3-monthly-average

terms, from 0.6% in May. Incontrast, purchase cost pressures appear

tohave eased further in June, down 1 percentagepoint to 3.2% in

annualised 3-monthly-averageterms.

Based on respondent estimates of changes in labour costsand

product. Retail prices are based on retail sector productprice

estimates.

Retail prices pick up somewhat

-4

-2

0

2

4

6

8

II III IV I II III IV I II III IV I II

2008 2009 2010 2011

Labour Product price Retail price

Costs & prices(3-mth ave, annualised %)

4

-

8/6/2019 NAB: Domestic sector struggling to gain momentum as

confidence slumps.

5/10

Embargoed until 11.30am Tuesday, 12 July 2011

Current business conditions

Business conditions Conditions improve slightly

While the overall business conditions index roseby 2 points to

+2 index points in June, it remainsbelow the long-term average (of

+6 points). In

trend terms, the index eased from +5 points to+2 points.

Trading conditions, profitability andemployment

According to the June survey, the rise in businessconditions

reflected both a rise in tradingconditions and employment, while

profitability wasunchanged at a subdued level

(seasonallyadjusted).

Trading conditions were mixed across industries(seasonally

adjusted); the most notable

improvements in trading conditions were recordedin

finance/business/property (up 16 to +18 points)and recreation &

personal services (up 15 to+27 points), while conditions

weakenedsignificantly in retail (down 19 to -33 points) andmining

(down 14 to +27 points). In trend terms,trading conditions were

again strongest in mining(+29) and weakest in retail (-17).

-40

-30

-20

-10

0

10

20

II III IV I II III IV I II III IV I II

2008 2009 2010 2011

Trading Profitability EmploymentConds 1990s recn

All components of business conditions (net bal., s.a.)

Net balance of respondents who regard lastmonths trading /

profitability / employmentperformance as good.

Profitability (seasonally adjusted) was also varied across

industries, with particularly sharpdeclines recorded in mining and

retail, while finance/business/property rebounded strongly inthe

month. In trend terms, profitability was strongest in

finance/business/property(+13 points) and weakest in retail

(-20).

Employment (seasonally adjusted) fell very sharply in mining

(down 49 to +15), more thanoffsetting the significant rise in the

previous month, while transport & utilities employmentwas

broadly unchanged (down 1 to +9). All other industries recorded an

improvement inemployment conditions, with retail and manufacturing

improving most significantly in themonth. Trend employment was

weaker in mining and manufacturing, while it was unchangedin retail

and recreation & personal services, and was a little better in

the remaining industries.

Business conditions components (net balance)

-30

-20

-10

0

10

20

II III IV I II III IV I II

2009 2010 2011

Seasonally adjusted Trend

Trading performance

-30

-20

-10

0

10

20

II III IV I II III IV I II

2009 2010 2011

Seasonally adjusted Trend

Profitability

-30

-20

-10

0

10

20

II III IV I II III IV I II

2009 2010 2011

Seasonally adjusted Trend

Employment

Net balance of respondents reporting trading performance /

profitability / employment as good or very good (ratherthan poor or

very poor).

5

-

8/6/2019 NAB: Domestic sector struggling to gain momentum as

confidence slumps.

6/10

Embargoed until 11.30am Tuesday, 12 July 2011

Current business conditions (cont.)

Forward orders Fewer customer orders

The forward orders index (seasonally adjusted)fell further in

June (down 2 points to -4 points),and was also weaker in trend

terms (down 3 to-3 points).

By industry, forward orders were by far thestrongest in mining

(+23), followed by recreation &personal services (+1) and

wholesale (0). Orderscontracted in all other industries, and

wereweakest in manufacturing (-11) and transport &utilities

(-10).

Net balance of respondents with more orders from customers

last month.

-40

-30

-20

-10

0

10

20

II III IV I II III IV I II III IV I II

2008 2009 2010 2011

Seasonally adjusted Trend

Orders 1990s recn

Forward orders (net balance)

Capacity utilisation Capacity edges up a touch

Capacity utilisation (seasonally adjusted) was alittle higher at

81.7% in June, compared to 81.6%in May, remaining somewhat above

its long-termaverage level (81.2%) but significantly belowrecent

peaks (84.5% in late 2007).

Capacity utilisation by industry rose most notablyin

finance/business/property followed bymanufacturing and recreation

& personal services.Less capacity was utilised in the

remainingindustries, with mining and transport & utilities

recording the largest declines. In levels terms,capacity

utilisation was highest in recreation &personal services

(85.3%) and finance/ business/property (84.3%), and was lowest

inmanufacturing (77.4%) and mining (79.9%) withflood damage still

evident.

Full capacity is the maximum desirable level of output

usingexisting capital equipment.

76

78

80

82

84

86

II III IV I II III IV I II III IV I II

2008 2009 2010 2011

Seasonally adjusted Trend

CapU 1990s recn

Capacity utilisation (per cent)

Stocks Stocks decline further

The stocks index (seasonally adjusted) was2 points lower in

June, at -2 index points, with the

now slightly negative index number possiblysuggesting some

expectation of a deterioration infuture demand.

By industry, the stocks index fell very sharply inmining (down

30 to -34 points), more thanunwinding the sharp rise in the

previous month.More of a concern were the heavy falls inwholesale

stocks (down 10 to -6 points). Incontrast, the stocks index was a

little higher inconstruction, retail and transport &

utilities.

Net balance of respondents with an increase in stocks

lastmonth.

-20

-15

-10

-5

0

5

10

II III IV I II III IV I II III IV I II

2008 2009 2010 2011

Seasonally adjusted Trend

Stocks(net balance)

6

-

8/6/2019 NAB: Domestic sector struggling to gain momentum as

confidence slumps.

7/10

Embargoed until 11.30am Tuesday, 12 July 2011

Current business conditions (cont.)

Capital expenditure Capital spending remains solid

Capital expenditure was unchanged at +4 pointsin June, while in

trend terms the index was a littlelower. Expenditure was lower in

transport &

utilities and mining in the month, broadly offsettingsimilar

sized increases in May, while constructionand manufacturing both

provided a boost toexpenditure.

Net balance of respondents with an increase in

capitalexpenditure last month.

-30

-20

-10

0

10

20

II III IV I II III IV I II

2009 2010 2011

Seasonally adjusted Trend

Capital expenditure (net balance)

Exports Exports pick up, but still falling

The exports index, which represents exportconditions for the

economy as a whole, rose by1 point to -3 index points in the month,

afterdeclining sharply in May.

By industry, exports rose most notably inconstruction and

manufacturing, while the largestdeclines were recorded in wholesale

and mining.

Similarly, the exporters sales index, whichrepresents export

conditions for exportingindustries, picked up in the month, but

remainedmore subdued at -11 index points.

Net balance of respondents with an increase in export saleslast

month.

-10

-8

-6

-4

-2

0

2

II III IV I II III IV I II III IV I II

2008 2009 2010 2011

Seasonally adjusted Trend

Exports (net balance)

Credit availability Less demand for credit

Firms reported less difficulty inobtaining finance in June,

withthe net index (easier minusharder) rising to -3 index

points.This outcome reflected a fall inthe proportion of

respondentsfinding it less difficult to obtain

finances, which was more thanoffset by a fall in the

proportionof respondents finding it moredifficult to obtain

finance. Theproportion of businessesreporting that they did

notrequire credit increased from44% in May to 56% in June

suggesting a fall back in creditdemand.

0

20

40

60

80

100

I II III IV I II

2010 2011

More difficult Unchanged Easier No borrowing required

Borrowing conditions (% of firms)

In terms of the borrowings required for your business in the

last month,has it been

7

-

8/6/2019 NAB: Domestic sector struggling to gain momentum as

confidence slumps.

8/10

Embargoed until 11.30am Tuesday, 12 July 2011

Industry sectors

Business confidence Mining strongest; construction weakest

In seasonally adjusted terms, business confidence levels fell

across all industries with theexception of mining (up 6 points),

and wholesale (unchanged). Confidence levelsdeteriorated most

significantly in construction (down 21 to -14 points) followed by

finance/business/ property, retail and recreation & personal

services. Consistent with the rise inconfidence in the month,

mining recorded the highest confidence levels (+17), followed

bytransport & utilities and finance/business/property (both

+5). In contrast, constructionrecorded the weakest confidence (-14)

followed by manufacturing (-2), retail and wholesale(both -1).

Trend confidence was strongest in mining (+13) and

finance/business/property(+11), and weakest in manufacturing (-2)

and construction (-1).

Business confidence by industry (net balance)3-month moving

average

-40

-30

-20

-10

0

10

20

30

40

II III IV I II III IV I II

2009 2010 2011

Mining Manuf Constn

-40

-30

-20

-10

0

10

20

30

40

II III IV I II III IV I II

2009 2010 2011

Retail Wsale Transp

-40

-30

-20

-10

0

10

20

30

40

II III IV I II III IV I II

2009 2010 2011

Fin, bus, prop Rec, pers

Business conditions Finance/business/property the strongest;

manufacturing and construction weakestChanges in business

conditions were mixed across industries in seasonally adjusted

terms;conditions deteriorated significantly in mining and retail in

June, while conditions improvednotably in

finance/business/property, recreation & personal and

manufacturing (albeit to stillpoor levels). The strongest

conditions were recorded in finance/business/property

(+20),recreation & personal services (+17) and mining (+14),

while business conditions wereweakest (and negative) inn retail

(-24), construction and manufacturing (both -5) andwholesa le (-1).

In trend terms, business conditions were again varied across

industries.Trend conditions were strongest in mining (+27) and

transport & utilities (+15) and weakest inretail (-13) and

manufacturing (-8).

Business conditions by industry (net balance)

3-month moving average

-40

-30

-20

-10

0

10

20

30

40

II III IV I II III IV I II

2009 2010 2011

Mining Manuf Constn

-40

-30

-20

-10

0

10

20

30

40

II III IV I II III IV I II

2009 2010 2011

Retail Wsale Transp

-40

-30

-20

-10

0

10

20

30

40

II III IV I II III IV I II

2009 2010 2011

Fin, bus, prop Rec, pers

8

-

8/6/2019 NAB: Domestic sector struggling to gain momentum as

confidence slumps.

9/10

Embargoed until 11.30am Tuesday, 12 July 2011

States

Business confidence WA most confident; confidence poor in

Tas

Business confidence levels (seasonally adjusted) deteriorated

across all states in June; themost significant deterioration in

sentiment was reported in Victoria (down 10 to -4 points),followed

by WA (down 8 to +4 points), Tasmania (down 8 to -18 points),

Queensland (down

4 to 0), SA (down 4 to -3 points) and NSW (down 3 to +1). Trend

confidence levels wereagain highest in WA (+7), SA and NSW (both

+6), and were lowest in Tasmania (-9, on asmall sample), Queensland

and Victoria (both +2).

Business confidence by state (net balance)3-month moving

average

-40

-30

-20

-10

0

10

20

30

40

II III IV I II III IV I II

2009 2010 2011

Australia NSW VIC

-40

-30

-20

-10

0

10

20

30

40

II III IV I II III IV I II

2009 2010 2011

Australia QLD WA

-40

-30

-20

-10

0

10

20

30

40

II III IV I II III IV I II

2009 2010 2011

Australia SA TAS

Business conditions NSW strongest; Tas deteriorates sharply

In seasonally adjusted terms, business conditions strengthened

in NSW (up 18 to +11 points)and Victoria (up 2 to +3 points), while

conditions deteriorated in all of the remaining states.The largest

deterioration in conditions was recorded in Tasmania (down 28 to

-37 points, on

a small sample), followed by Queensland (down 8 to -3 points),

SA (down 6 to -11 points)and WA (down 1 to +8 points). Trend

conditions remained strongest in WA (+10), despitedeclining a

little in the month, followed by Victoria (+4) and NSW (+3), and

were weakest inTasmania (-21) and SA (-7).

Business conditions by state (net balance)3-month moving

average

-40

-30

-20

-10

0

10

20

30

40

II III IV I II III IV I II

2009 2010 2011

Australia NSW VIC

-40

-30

-20

-10

0

10

20

30

40

II III IV I II III IV I II

2009 2010 2011

Australia QLD WA

-40

-30

-20

-10

0

10

20

30

40

II III IV I II III IV I II

2009 2010 2011

Australia SA TAS

9

-

8/6/2019 NAB: Domestic sector struggling to gain momentum as

confidence slumps.

10/10

Macroeconomic, Industry & Markets ResearchAustralia

Alan Oster Group Chief Economist +(61 3) 8634 2927

Jacqui Brand Personal Assistant +(61 3) 8634 2181

Rob Brooker Head of Australian Economics & Commodities +(61

3) 8634 1663

Alexandra Knight Economist Australia +(61 3) 9208 8035Ben

Westmore Economist Australia & Commodities +(61 3) 8634

8602

Michael Creed Economist Agribusiness +(61 3) 8634 3470

Dean Pearson Head of Industry Analysis +(61 3) 8634 2331

Gerard Burg Economist Industry Analysis +(61 3) 8634 2788

Robert De Iure Economist Property +(61 3) 8634 4611

Brien McDonald Economist Industry Analysis & Risk Metrics

+(61 3) 8634 3837

Tom Taylor Head of International Economics +(61 3) 8634 1883

John Sharma Economist Country Risk +(61 3) 8634 4514

Tony Kelly Economist International +(61 3) 9208 5049

James Glenn Economist Asia +(61 3) 9208 8129

Global Markets Research - Wholesale Banking

Peter Jolly Head of Markets Research +(61 2) 9237 1406

Robert Henderson Chief Economist Markets - Australia +(61 2)

9237 1836

Spiros Papadopoulos Senior Economist Markets +(61 3) 8641

0978

David de Garis Senior Economist Markets +(61 3) 8641 3045

New ZealandTony Alexander Chief Economist BNZ +(64 4)474

6744Stephen Toplis Head of Research, NZ +(64 4) 474 6905Craig Ebert

Senior Economist, NZ +(64 4) 474 6799Doug Steel Markets Economist,

NZ +(64 4) 474 6923

London

Tom Vosa Head of Market Economics - Europe +(44 20) 7710

1573David Tinsley Market Economist Europe +(44 20) 7710 2910

Foreign Exchange Fixed Interest/Derivatives

Sydney +800 9295 1100 +(61 2) 9295 1166

Melbourne +800 842 3301 +(61 3) 9277 3321

Wellington +800 64 642 222 +800 64 644 464

London +800 747 4615 +(44 20) 7796 4761

New York +1 800 125 602 +1877 377 5480

Singapore +(65) 338 0019 +(65) 338 1789

DISCLAIMER: [While care has been taken in preparing this

material,] National Australia Bank Limited (ABN 12 004 044 937)

does not warrant or represent that the information,recommendations,

opinions or conclusions contained in this document (Information)

are accurate, reliable, complete or current. The Information has

been prepared for dissemination toprofessional investors for

information purposes only and any statements as to past performance

do not represent future performance. The Information does not

purport to contain all mattersrelevant to any particular investment

or financial instrument and all statements as to future matters are

not guaranteed to be accurate. In all cases, anyone proposing to

rely on or use theInformation should independently verify and check

the accuracy, completeness, reliability and suitability of the

Information and should obtain independent and specific advice from

appropriateprofessionals or experts.

To the extent permissible by law, the National shall not be

liable for any errors, omissions, defects or misrepresentations in

the Information or for any loss or damage suffered by persons

whouse or rely on such Information (including by reasons of

negligence, negligent misstatement or otherwise). If any law

prohibits the exclusion of such liability, the National limits its

liability tothe re-supply of the Information, provided that such

limitation is permitted by law and is fair and reasonable. The

National, its affiliates and employees may hold a position or act

as a pricemaker in the financial instruments of any issuer

discussed within this document or act as an underwriter, placement

agent, adviser or lender to such issuer.

UK Disclaimer: So far as the law and the FSA Rules allow,

National Australia Bank Limited (the Bank) disclaims any warranty

or representation as to the accuracy or reliability of

theinformation and statements in this document. The Bank will not

be liable (whether in negligence or otherwise) for any loss or

damage suffered from relying on this document. This documentdoes

not purport to contain all relevant information. Recipients should

not rely on its contents but should make their own assessment and

seek professional advice relevant to theircircumstances. The Bank

may have proprietary positions in the products described in this

document. This document is for information purposes only, is not

intended as an offer or solicitationnor is it the intention of the

Bank to create legal relations on the basis of the information

contained in it. No part of this document may be reproduced without

the prior permission of the Bank.This document is intended for

Investment Professionals (as such term is defined in The Financial

Services and Markets Act 2000 (Financial Promotion) Order 2001) and

should not be passedto any other person who would be defined as a

private customer by the rules of the Financial Services Authority

(FSA) in the UK or to any person who may not have experience of

suchmatters. Issued by National Australia Bank Limited A.C.N. 004

044 937, 88 Wood Street, London EC2V 7QQ. Registered in England

BR1924. Head Office: 500 Bourke Street, Melbourne,Victoria.

Incorporated with limited liability in the state of Victoria,

Australia. Regulated by the FSA in the UK.

U.S DISCLAIMER: This information has been prepared by National

Australia Bank Limited or one of its affiliates or subsidiaries

("NAB"). If it is distributed in the United States,

suchdistribution is by nabSecurities, LLC which accepts

responsibility for its contents. Any U.S. person receiving this

information wishes further information or desires to effect

transactions in anysecurities described herein should call or write

to nabSecurities, LLC, 28th Floor, 245 Park Avenue, New York, NY

10167 (or call (877) 377-5480). The information contained herein

has beenobtained from, and any opinions herein are based upon,

sources believed to be reliable and no guarantees, representations

or warranties are made as to its accuracy, completeness

orsuitability for any purpose. Any opinions or estimates expressed

in this information is our current opinion as of the date of this

report and is subject to change without notice. The principals

ofnabSecurities, LLC or NAB may have a long or short position or

may transact in the securities referred to herein or hold or

transact derivative instruments, including options, warrants or

rightswith securities, or may act as a market maker in the

securities discussed herein and may sell such securities to or buy

from customers on a principal basis. This material is not intended

as an

offer or solicitation for the purchase or sale of the securities

described herein or for any other action. It is intended for the

information of clients only and is not for publication in the press

orelsewhere.