Embed Size (px)

Citation preview

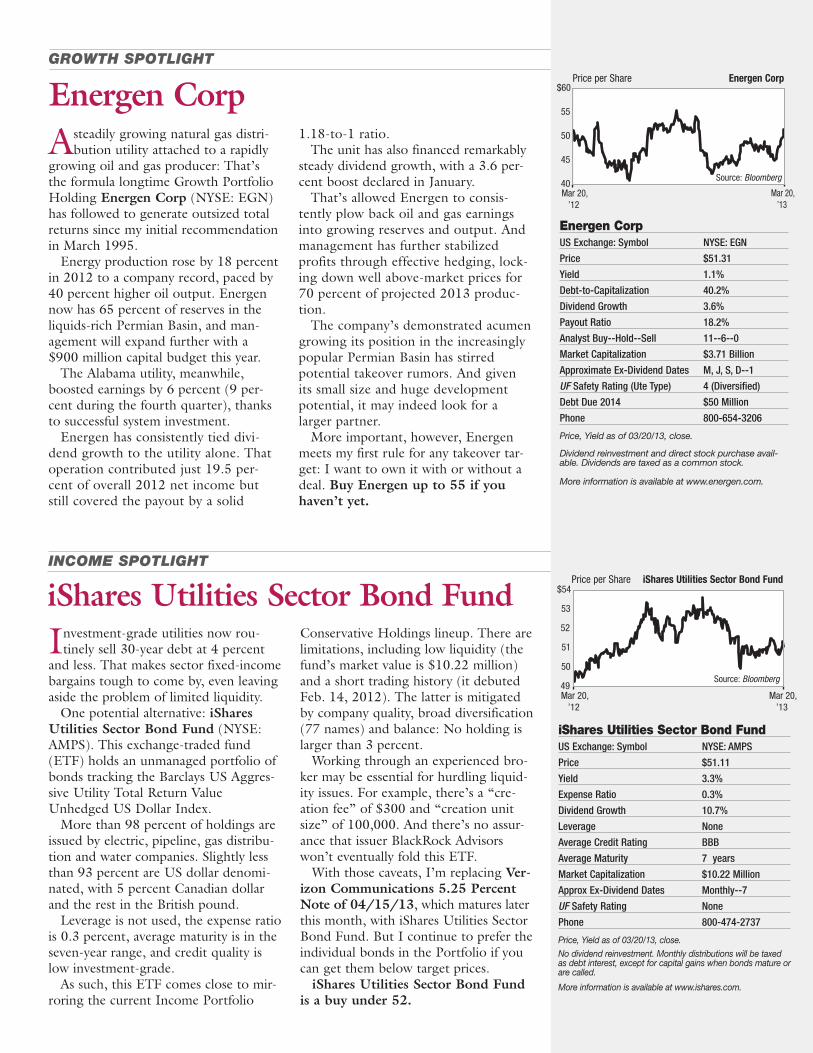

high-yielding stocks.Growth Spotlight Energen Corp (NYSE: EGN) is a

conservative bet on energy sector consolidation. Income Spotlight iShares Utilities Sector Bond Fund (NYSE: AMPS) is an alternative for those who’ve had trouble buying the recommended Income Portfolio Conservative Holdings.

Finally, Utility Beat looks at shareholder lawsuits, sec-ondary offerings and the latest turn in sector mergers.

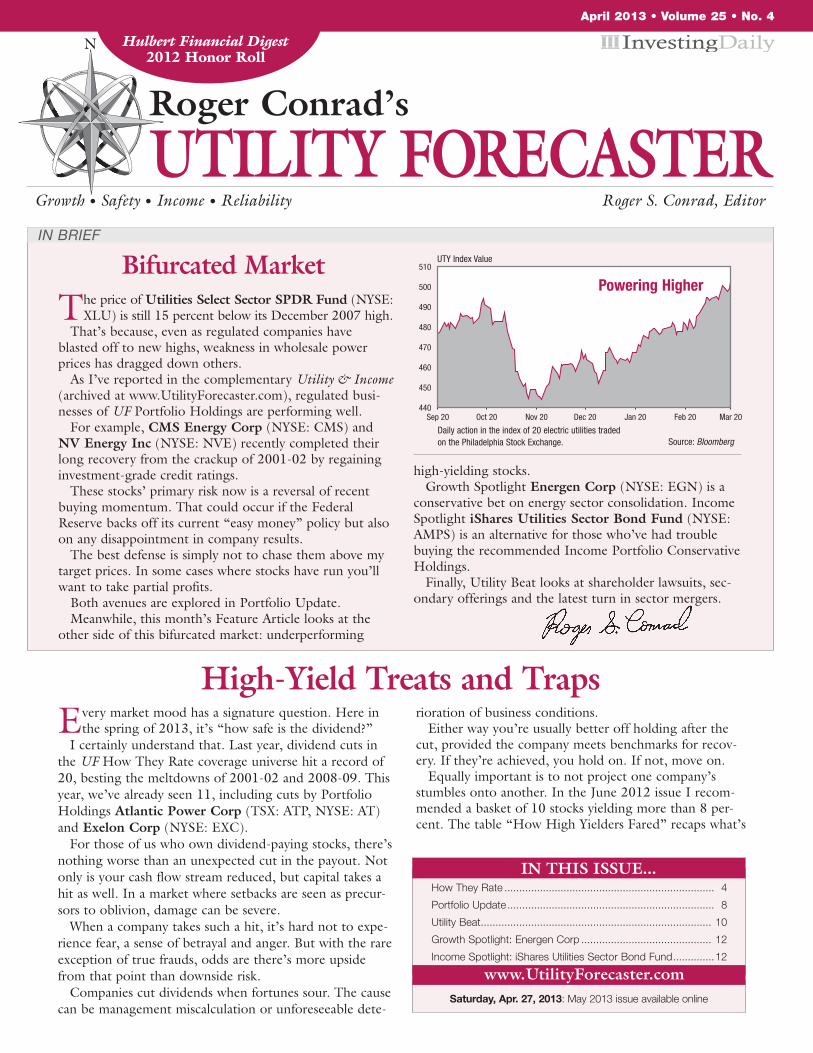

The price of Utilities Select Sector SPDR Fund (NYSE: XLU) is still 15 percent below its December 2007 high.

That’s because, even as regulated companies have blasted off to new highs, weakness in wholesale power prices has dragged down others.

As I’ve reported in the complementary Utility & Income (archived at www.UtilityForecaster.com), regulated busi-nesses of UF Portfolio Holdings are performing well.

For example, CMS Energy Corp (NYSE: CMS) and NV Energy Inc (NYSE: NVE) recently completed their long recovery from the crackup of 2001-02 by regaining investment-grade credit ratings.

These stocks’ primary risk now is a reversal of recent buying momentum. That could occur if the Federal Reserve backs off its current “easy money” policy but also on any disappointment in company results.

The best defense is simply not to chase them above my target prices. In some cases where stocks have run you’ll want to take partial profits.

Both avenues are explored in Portfolio Update.Meanwhile, this month’s Feature Article looks at the

other side of this bifurcated market: underperforming

Every market mood has a signature question. Here in the spring of 2013, it’s “how safe is the dividend?”

I certainly understand that. Last year, dividend cuts in the UF How They Rate coverage universe hit a record of 20, besting the meltdowns of 2001-02 and 2008-09. This year, we’ve already seen 11, including cuts by Portfolio Holdings Atlantic Power Corp (TSX: ATP, NYSE: AT) and Exelon Corp (NYSE: EXC).

For those of us who own dividend-paying stocks, there’s nothing worse than an unexpected cut in the payout. Not only is your cash flow stream reduced, but capital takes a hit as well. In a market where setbacks are seen as precur-sors to oblivion, damage can be severe.

When a company takes such a hit, it’s hard not to expe-rience fear, a sense of betrayal and anger. But with the rare exception of true frauds, odds are there’s more upside from that point than downside risk.

Companies cut dividends when fortunes sour. The cause can be management miscalculation or unforeseeable dete-

rioration of business conditions.Either way you’re usually better off holding after the

cut, provided the company meets benchmarks for recov-ery. If they’re achieved, you hold on. If not, move on.

Equally important is to not project one company’s stumbles onto another. In the June 2012 issue I recom-mended a basket of 10 stocks yielding more than 8 per-cent. The table “How High Yielders Fared” recaps what’s

April 2013 • Volume 25 • No. 4

Roger Conrad’s

UtIlIty FoRECAStERGrowth • Safety • Income • Reliability Roger S. Conrad, Editor

High-yield treats and traps

Bifurcated Market

How They Rate ....................................................................... 4

Portfolio Update ...................................................................... 8

Utility Beat .............................................................................. 10

Growth Spotlight: Energen Corp ............................................ 12

Income Spotlight: iShares Utilities Sector Bond Fund ..............12

IN tHIS ISSUE...

Saturday, Apr. 27, 2013: May 2013 issue available online

www.UtilityForecaster.com

IN BRIEF

Hulbert Financial Digest 2012 Honor Roll

N

Daily action in the index of 20 electric utilities traded on the Philadelphia Stock Exchange. Source: Bloomberg

UTY Index Value

440

450

460

470

480

490

500

510

Sep 20 Oct 20 Nov 20 Dec 20 Jan 20 Feb 20 Mar 20

Powering Higher

happened since. All except Atlantic have gotten stronger. Despite a

nearly 60 percent loss in that one stock, the group is up 6.1 percent on average. The key to realizing gains was to spread your bets.

The Right QuestionsEach of the 10 companies I featured last year was

cheap for a reason: perceived risk to its dividend. I set benchmarks for each, and their performance has reflected how well they’ve measured up.

Atlantic faltered because the North American wholesale power market continued to worsen. The lower dividend strategy is based on the premise that power markets in Ontario and New York are unlikely to improve before sales contracts expire next year, as well as the fact that the company must enter more early-stage projects to grow cash flow.

By contrast, Buckeye Partners lP’s (NYSE: BPL) 30 percent-plus return is thanks to recovering cash flow, as a series of acquisitions and asset construction has paid off.

The pipeline company is not only covering its quarterly distribution with profits. But management plans to resume regular dividend growth later this year now that rate-related issues have been settled with the Federal Energy Regulatory Commission.

That’s a long way from the prevailing sentiment on Buckeye just a few months ago. the only problem is the unit price is now well above my buy target of 55, though I’ll raise that back to 60 when dividend growth resumes.

AmeriGas Partners lP’s (NYSE: APU) rebound has come from diminishing concerns about its dividend and the growing likelihood management will deliver another increase later this year. the unit price is back within a stone’s throw of my buy target of 45.

Consolidated Communications Holdings Inc’s (NSDQ: CNSL) bar for success was proving it could hold its payout ratio low while transitioning to a broadband business. The stock has been all over the map, as rival wireline companies have faltered. But fourth-quarter numbers included year-over-year sales growth of 1.8 per-cent, and the payout ratio was just 58.2 percent.

The sizable returns for owning Enel SpA (Italy: ENEL, OTC: ESOCF, ADR: ENLAY) and telefónica SA (Spain: TEF, NYSE: TEF) are the biggest surprise, as both companies trimmed dividends again.

But both have reported stabilized profits, as Latin American growth has continued and results in Europe have beaten expectations.

As for linn Energy llC (NSDQ: LINE), NuStar Energy lP (NYSE: NS), PVR Partners lP (NYSE: PVR) and Windstream Corp (NYSE:WIN), they’ve nei-ther faltered nor overcome investors’ doubts. The jury is still out.

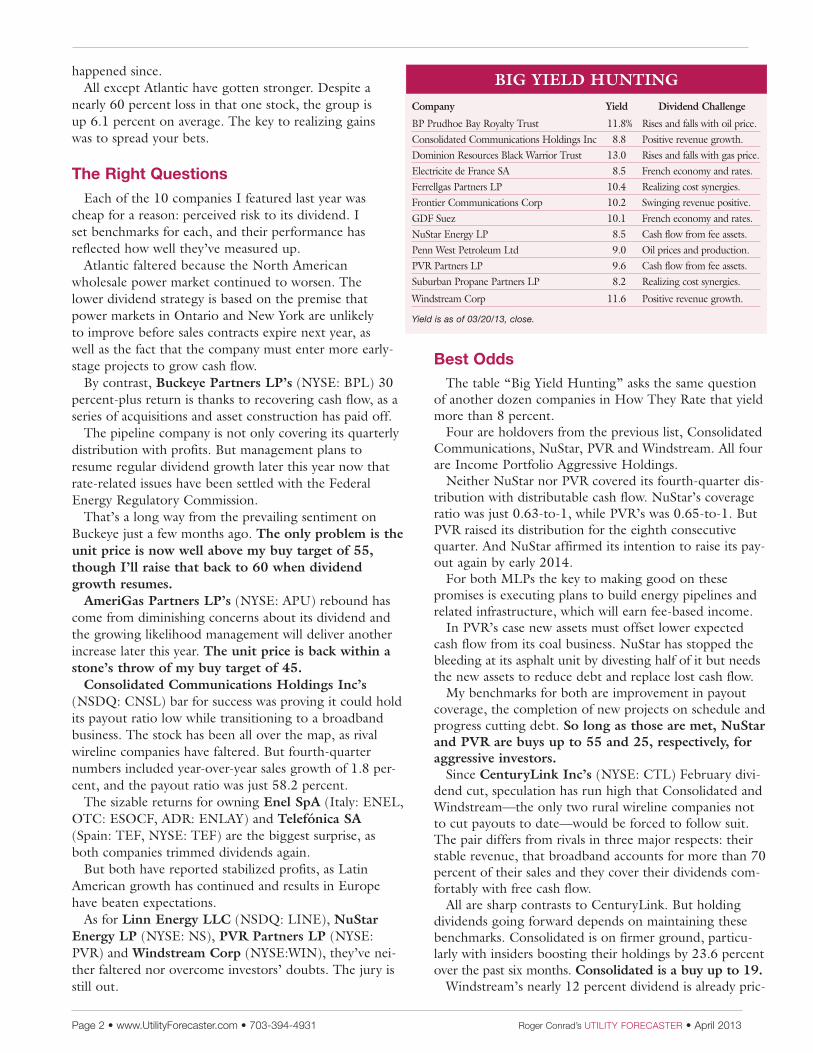

Best OddsThe table “Big Yield Hunting” asks the same question

of another dozen companies in How They Rate that yield more than 8 percent.

Four are holdovers from the previous list, Consolidated Communications, NuStar, PVR and Windstream. All four are Income Portfolio Aggressive Holdings.

Neither NuStar nor PVR covered its fourth-quarter dis-tribution with distributable cash flow. NuStar’s coverage ratio was just 0.63-to-1, while PVR’s was 0.65-to-1. But PVR raised its distribution for the eighth consecutive quarter. And NuStar affirmed its intention to raise its pay-out again by early 2014.

For both MLPs the key to making good on these promises is executing plans to build energy pipelines and related infrastructure, which will earn fee-based income.

In PVR’s case new assets must offset lower expected cash flow from its coal business. NuStar has stopped the bleeding at its asphalt unit by divesting half of it but needs the new assets to reduce debt and replace lost cash flow.

My benchmarks for both are improvement in payout coverage, the completion of new projects on schedule and progress cutting debt. So long as those are met, NuStar and PVR are buys up to 55 and 25, respectively, for aggressive investors.

Since Centurylink Inc’s (NYSE: CTL) February divi-dend cut, speculation has run high that Consolidated and Windstream—the only two rural wireline companies not to cut payouts to date—would be forced to follow suit. The pair differs from rivals in three major respects: their stable revenue, that broadband accounts for more than 70 percent of their sales and they cover their dividends com-fortably with free cash flow.

All are sharp contrasts to CenturyLink. But holding dividends going forward depends on maintaining these benchmarks. Consolidated is on firmer ground, particu-larly with insiders boosting their holdings by 23.6 percent over the past six months. Consolidated is a buy up to 19.

Windstream’s nearly 12 percent dividend is already pric-

Page 2 • www.UtilityForecaster.com • 703-394-4931 Roger Conrad’s UTIlITy FoRECaSTER • April 2013

Company yield Dividend Challenge

BP Prudhoe Bay Royalty Trust 11.8% Rises and falls with oil price.Consolidated Communications Holdings Inc 8.8 Positive revenue growth.Dominion Resources Black Warrior Trust 13.0 Rises and falls with gas price.Electricite de France SA 8.5 French economy and rates.Ferrellgas Partners LP 10.4 Realizing cost synergies.Frontier Communications Corp 10.2 Swinging revenue positive.GDF Suez 10.1 French economy and rates.NuStar Energy LP 8.5 Cash flow from fee assets.Penn West Petroleum Ltd 9.0 Oil prices and production.PVR Partners LP 9.6 Cash flow from fee assets.Suburban Propane Partners LP 8.2 Realizing cost synergies.

Windstream Corp 11.6 Positive revenue growth.

Yield is as of 03/20/13, close.

BIG yIElD HUNtING

Roger Conrad’s UTIlITy FoRECaSTER • April 2013 703-394-4931 • www.UtilityForecaster.com • Page 3

Roger Conrad’s Utility Forecaster (ISSN 10645373) is published monthly by Investing Daily, a division of Capitol Information Group, Inc., 7600A Leesburg Pike, West Building, Suite 300, Falls Church, VA 22043. © 2013 by Investing Daily, a division of Capitol Information Group, Inc. Address editorial correspondence to Roger Conrad’s Utility Forecaster, 7600A Leesburg Pike, West Building, Suite 300, Falls Church, VA 22043. SUBSCRIPTIONS: $149 for one year. EDITOR: Roger S. Conrad; MANAGING EDITOR: David Dittman; DIRECTOR OF PRODUCTION AND DESIGN: Melanie Selmer; ANALYSTS: Ari Charney and Benjamin Shepherd; CUSTOMER SERVICE DIRECTOR: Andrea Prendergast; PUBLISHER: Phil Ash. POSTMASTER: Send address changes to Roger Conrad’s Utility Forecaster , P.O. Box 4123, McLean, VA 22103. Please send subscription-related correspondence to above address; enclose mailing label from a recent issue and a new address. For customer service, call 800-832-2330. Readers should not assume that recommendations will be profitable or will equal the performance of previous recommendations. All contents are derived from original or published sources believed to be reliable, but accuracy is not guaranteed. Investing Daily, a division of Capitol Information Group, Inc., its officers and owners and the editors of Roger Conrad’s Utility Forecaster may from time to time have a position in investments referred to in this newsletter. Peri-odicals postage paid at Falls Church, Va. and other mailing offices. Printed in U.S.A. For permission to photocopy or use material electronically from Roger Conrad’s Utility Forecaster (ISSN 10645373), please access www.copyright.com or contact Copyright Clearance Center, Inc. (CCC) 222 Rosewood Drive, Danvers, MA 01923, 978-750-8400. CCC is a not-for-profit organization that provides licenses and registration for a variety of users.

ing in a cut. Windstream is a buy up to 11 only for aggressive investors.

Suburban Propane Partners lP (NYSE: SPH) is a good candidate to repeat AmeriGas’ success realizing the benefits of scale in the US propane distribution sector.

The MLP raised its distribution in January for the first time since late 2010 and later reported strong fiscal 2013 first-quarter earnings, as increased scale and lower whole-sale propane prices offset mild weather.

Suburban is smaller than AmeriGas and further price gains will depend on realizing more scale advantages. But Subur ban is a buy up to 44 for aggressive income seekers.

Electricite de France SA (France: EDF, OTC: ECIFF, ADR: ECIFY) is that rare European utility that managed a dividend increase this year. Management boosted its final payout by 17.2 percent from last year’s level.

The company has the advantage of massive scale, gov-ernment support, a dominant position in European nuclear power and a list of global projects to lift future earnings.

The key challenges are refinancing EUR11.1 billion in maturing debt over the next two years and avoiding blow-ups with French and European regulators. For US investors there’s also the risk of a strength-ening US dollar. But Electricite de France is again a buy up to USD20.

Riskier BusinessThe remaining six stocks are holds at best.

Frontier Communications Corp (NYSE: FTR) has cut its dividend twice since mid-2010. That’s when the company announced the purchase of 5 million wireline connec-tions from Verizon Communications Inc (NYSE: VZ).

Frontier has since made strides integrating this business, and cost-cutting has routinely exceeded expectations. But the erosion of the traditional phone business continues to outpace the addition of broadband users. The result is a continuing decline in revenue and lack of progress cutting debt.

Free cash flow covered the dividend, with a 41 percent payout ratio for 2012. But fourth-quarter revenue was nearly 4 percent lower, as it lost both residential and busi-ness customers. Until that number improves Frontier is a hold.

GDF Suez (France: GSZ, OTC: GDSZF, ADR: GDFZY) is committed to the current dividend rate of EUR1.50 per share. Growth prospects, however, are less well defined after a 61 percent drop in 2012 profit,

largely due to writedowns of natural gas-fired power plants. In stark contrast to the US--where natural gas prices are

one-third to one-quarter European prices--gas-fired power is not competitive in Europe.

The dividend should hold as long as the company avoids blowups with regulators in Belgium and France and plans to develop renewable energy and a range of projects in Asia stay on track. But GDF Suez is a hold for now.

Ferrellgas Partners lP (NYSE: FGP) posted a 50 per-cent boost in fiscal 2013 second-quarter distributable cash flow, as scale benefits from recent mergers and lower wholesale propane costs offset mild winter weather. Despite the gain, however, the payout ratio was 108.1 percent.

Until that number comes down a lot, there’s not going to be distribution growth here. And that means there are far better investments in propane distribution elsewhere. Sell Ferrellgas.

The remaining three Big Yielders on my list are all

energy producers. BP Prudhoe Bay Royalty trust’s (NYSE: BPT) and Dominion Resources Black Warrior trust’s (NYSE: DOM) distributions rise and fall with energy prices, BP with oil and Dominion with natural gas.

Current yields reflect potential for dividend cuts going forward. But with operating companies selling cheaply, there’s no reason to hold either of these royalty trusts.

The same goes for Penn West Petroleum ltd (TSX: PWT, NYSE: PWE), which sells at less than very conser-vative valuations of its proven reserves.

Management has pledged to maintain the current divi-dend. But its success is going to depend on energy prices holding up and the company executing on production plans, and there’s real risk on both counts. Penn West is a hold.

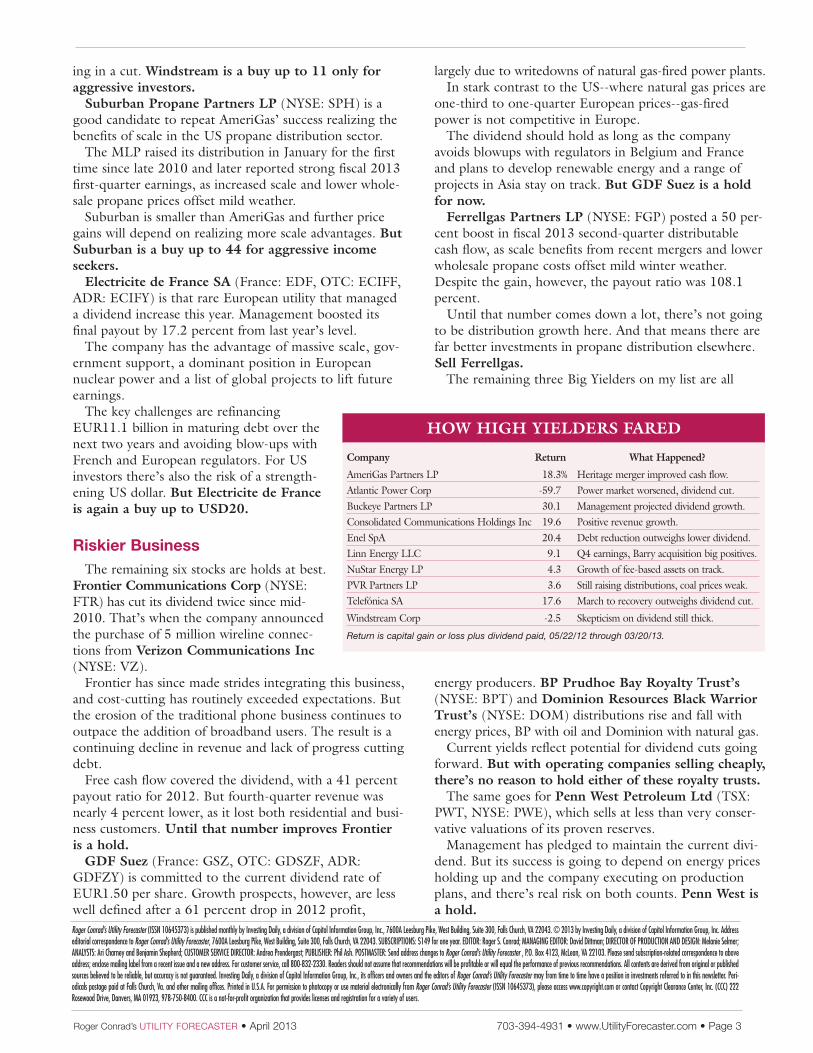

Company Return What Happened?

AmeriGas Partners LP 18.3% Heritage merger improved cash flow.Atlantic Power Corp -59.7 Power market worsened, dividend cut.Buckeye Partners LP 30.1 Management projected dividend growth.Consolidated Communications Holdings Inc 19.6 Positive revenue growth.Enel SpA 20.4 Debt reduction outweighs lower dividend.Linn Energy LLC 9.1 Q4 earnings, Barry acquisition big positives.NuStar Energy LP 4.3 Growth of fee-based assets on track.PVR Partners LP 3.6 Still raising distributions, coal prices weak.Telefónica SA 17.6 March to recovery outweighs dividend cut.

Windstream Corp -2.5 Skepticism on dividend still thick.

Return is capital gain or loss plus dividend paid, 05/22/12 through 03/20/13.

HoW HIGH yIElDERS FARED

AES Corp (AES) 703-682-6336 1.3% 54.7% 9--0--0 1.56% 2 D 2012 free cash flow up 33%, as expense cuts, renewable energy growth offset weakness in Brazil, Ohio. Buy @ 15

Allete (ALE) 800-535-3056 3.9 91.0 6--0--1 4.70 5 R Minnesota unit files new, 15-year plan for power in state, with addition of 200 MW renewable, coal plant retirements. Hold

Alliant Energy (LNT) 800-255-4268 3.8 99.2 8--3--1 3.25 5 R Iowa unit issues preferred stock at 5.1% interest rate. Regulated electric utility unit looks solid. Hold

Ameren Corp (AEE) 800-255-2237 4.6 89.7 2--10--0 5.73 4 D Writes down $300 million for sale of coal-fired merchant power plants in Illinois to Dynegy. FERC must OK deal. Hold

American Electric Power (AEP) 800-551-1237 3.9 95.3 11--12--0 4.62 5 D Will close three coal power plants as part of settlement with EPA, resulting in projected 25% to 30% cut in CAPEX. Hold

Black Hills Corp (BKH) 800-468-9716 3.5 92.3 4--5--0 3.79 3 D Dividend covered by regulated utility operations, but earnings and dividend growth held back by coal-price weakness. Hold

Centerpoint Energy (CNP) 800-231-6406 3.6 68.0 8--7--1 14.45 5 D Q4 earnings up 14.8%, producing 65.9% payout ratio. Partners with OG&E to launch new midstream MLP. Hold

CLECO (CNL) 800-253-2652 3.0 100.0 4--2--1 3.98 6 R Cash flow is boosted by addition of regulated assets. 2013 EPS guidance is still $2.45 to $2.55. Buy @ 42

CMS Energy (CMS) 517-788-0550 3.7 63.5 11--5--0 -5.00 5 R Sells $250 million 30-year note at 4.7%. Moody’s boosts to investment-grade, S&P raises to BBB. Buy @ 25

Dominion Resources (D) 800-552-4034 3.9 70.0 7--15--1 3.67 7 D Sells wholesale-market coal plants in Illinois and Massachusetts for $650 million. Plans to double asset base over next five years. Buy @ 55

DTE Energy (DTE) 866-388-8558 3.7 76.1 4--11--0 11.59 4 D Sierra Club files suit against company for alleged pollution violations at coal-fired plants. Sells 30-year debt at rate of 4%. Hold

Duke Energy (DUK) 800-488-3853 4.3 70.0 8--16--0 6.38 7 D Files for 16% rate hike in South Carolina. Buys California transmission line from Atlantic Power in potential expansion move. Buy @ 62

Edison International (EIX) 800-347-8625 2.7 89.1 14--5--1 3.08 4 D Rate lag hurts Q4 net. NRC delays decision on re-opening San Onofre nuclear plant. Sells 30-year debt at 3.9%. Hold

El Paso Electric (EE) 800-592-1634 3.0 100.0 2--5--0 5.80 4 R Plan to build new natural gas power plant in Texas is controversial. New Texas law could force more solar building. Hold

Empire District (EDE) 800-468-9716 4.5 100.0 1--3--0 2.11 3 R Files for approval of rate settlement in Missouri, with $27.5 million in new revenue to pay for CAPEX. Hold

Entergy Corp (ETR) 800-292-9960 5.2 86.1 2--11--5 4.11 5 D NRC rumored near new rules for extending licenses of existing nuclear plants. Could be breakthrough for Indian Point in New York. Buy @ 75

Exelon Corp (EXC) 800-626-8729 6.2 45.5 5--20--1 -3.63 4 D Maryland regulators OK 62% of request for electric rate boost and 71% of request for gas increase. Buy @ 35

FirstEnergy (FE) 800-736-3402 5.2 67.9 5--13--1 -1.67 4 D Q4 earnings up 39%. But company doesn’t set dividend increase due to debt reduction needs, Ohio uncertainty. Hold

Great Plains Energy (GXP) 816-556-2312 3.8 100.0 7--6--0 4.15 4 D Sets 2013 EPS guidance of $1.44 to $1.64. Rate hikes drive solid 2012 results. Hold

Hawaiian Electric (HE) 808-532-5841 4.6 88.2 0--7--1 0.51 3 D Sells 6.1 million shares of common stock to help fund renewable energy build-out without running up more debt. Hold

IdaCorp (IDA) 208-388-2200 3.2 90.9 2--3--1 1.34 5 R Sets 2013 EPS guidance of $3.20 to $3.35. Range is tighter than past years due to better cost controls. Hold

Integrys Energy Group (TEG) 920-433-4901 4.8 78.6 1--9--0 12.91 5 D Rate lag hurts, drags Q4 earnings down by 11.7%. Payout ratio still solid at 83.9%. Sets 2013 EPS guidance at $3.03 to $3.53. Buy @ 55

MDU Resources (MDU) 701-222-7900 2.8 32.8 5--5--1 1.49 6 D Expects 25% to 30% oil production growth in 2013, higher construction group backlog and new Dakota refinery in service by late 2014. Buy @ 24

MGE Energy (MGEE) 800-356-6423 2.9 100.0 1--2--0 1.12 8 R Cold weather lifts natural gas sales and Q4 earnings by 23.8%. Payout ratio is 56.6%. Invites dividend growth. Hold

NextEra Energy (NEE) 888-218-4392 3.5 74.1 15--10--1 7.20 5 D Florida utility targets 5% to 9% rate-base growth through 2016. Sets 2014 EPS guidance at $5.05 to $5.45. Hold

NiSource (NI) 888-884-7790 3.4 100.0 2--9--0 3.37 4 R Affirms 2013 EPS guidance of $1.50 to $1.60, with $1.8 billion CAPEX at upper end of prior guidance. Buy @ 24

Northwestern Corp (NWE) 605-978-2908 3.9 97.2 2--6--0 6.52 5 R System investment to drive future earnings. Montana regulators appear supportive now. Gets interim gas-rate boost of 5.42%. Hold

OG&E Energy (OGE) 405-553-3000 2.5 99.0 6--3--1 9.53 6 D Q4 earnings up 5.4%, pushing payout ratio down to 46.7%. Joint venture with Centerpoint to launch MLP is a plus. Hold

Otter Tail Corp (OTTR) 800-664-1259 3.9 39.9 1--4--0 -1.06 2 D More asset divestitures likely needed to stabilize earnings. 2013 EPS guidance of $1.30 to $1.55 would cover dividend. SELL

PS Enterprise Group (PEG) 800-242-0813 4.3 67.3 3--15--3 12.86 6 D Reaffirms EPS forecast for 2013 at $2.25 to $2.50. Has 10-year plan in New Jersey for system investment. Buy @ 32

PG&E Corp (PCG) 800-719-9056 4.1 100.0 7--13--0 -7.36 5 R Targets $5.1 billion CAPEX for 2013. Sells 7.2 million shares but will need more to meet capital-raise target. SELL

Pinnacle West (PNW) 800-457-2983 3.8 97.0 2--14--1 21.92 3 D Sells 30-year debt at 4.5% interest rate. Targets 6% rate-base growth through 2015, 4% annual dividend growth. Hold

PNM Resources (PNM) 505-241-2700 2.9 95.0 3--6--0 15.79 4 D 2012 earnings up 21.3%, payout ratio is 50.4%, as company boosts dividend 13.8%. Hold

PPL Corp (PPL) 610-774-5151 4.9 51.2 7--10--2 1.51 4 D Sells $400 million of debt due 2073 at 5.9% interest rate. Pennsylvania utility to invest $1 billion in 2013. Buy @ 30

SCANA Corp (SCG) 803-217-9000 4.1 77.1 3--8--2 -0.25 7 R Boosts dividend 2.5%. 2013 EPS guidance is $3.25 to $3.45. Completes first concrete pour at new nuclear plant. Hold

Sempra Energy (SRE) 877-773-6772 3.2 89.6 10--4--1 -4.76 6 D Boosts dividend 5%, targets 6% to 8% annual earnings growth through 2017. 2012 payout ratio 57.9%. Buy @ 68

Southern Company (SO) 800-554-7626 4.3 95.0 3--15--5 51.79 8 R Sells 30-year debt at 4.3%. Projected cost of nuclear plant rises 12%, but Moody’s says increase is manageable at current rating. Buy @ 45

TECO Energy (TE) 800-650-9222 5.0 81.7 1--14--1 4.43 3 D Regulated ops large, healthy enough to carry dividend. Weak prices for coal remain a drag on earnings, dividend growth. Buy @ 18

UNS Energy (UNS) 520-571-4000 3.7 100.0 2--4--0 13.72 3 R Boosts dividend 1.2%. Won’t issue 2013 guidance until decision made in Arizona rate case. 2012 payout ratio 79.1%. Hold

Vectren Corp (VVC) 812-491-4209 4.1 60.6 1--7--1 1.72 4 D Sets 2013 EPS guidance of $1.90 to $2.10. Losses in coal mining offset by solid regulated results. Hold

Westar Energy (WR) 800-527-2495 4.2 100.0 6--8--0 -7.41 4 R Boosts dividend 3%, as strong Q4 results from rate hikes push down payout ratio to 63.3%. Hold

Wisconsin Energy (WEC) 800-881-5882 3.3 91.0 3--15--0 2.78 8 R Sets 2013 EPS guidance of $2.38 to $2.48. Biggest risk to stock is high valuation. Hold

Xcel Energy (XEL) 877-778-6786 3.8 99.0 5--16--0 6.09 8 R Sets 2013 EPS guiance of $1.85 to $1.95. Sells 30-year debt at 3.95% interest rate. Buy @ 25

ENErgy DistributioN regulated Analyst insider sfty ute Company (symbol) Phone yield revenue ratings Holdings rtg type Comment Advice

AGL Resources (GAS) 800-633-4236 4.5% 69.2% 2--8--0 -2.93% 7 D Well-diversified company is affected by weather. But geographic diversification should keep results steady in 2013. Buy @ 40

AmeriGas Partners LP (APU) 610-337-7000 7.2 0.0 1--4--4 3.22 4 D Fitch boosts outlook to “stable” from “negative,” citing company’s ability to maintain profitability with scale in face of mild winter. Buy @ 45

Atmos Energy (ATO) 800-543-3038 3.4 64.5 2--8--0 3.32 7 D Targets rise in EPS to $3.00 to $3.20 by 2016 on strength of CAPEX and reliable regulation. Buy @ 33

Avista Energy (AVA) 800-642-7365 4.6 93.3 1--7--1 0.25 6 R Reaffirms 2013 EPS forecast of $1.70 to $1.90. Energy management business continues to grow with new contracts. Hold

Buckeye Partners LP (BPL) 484-232-4000 7.0 23.7 5--6--1 29.34 6 D FERC authorizes market rates on pipelines, will resolve remaning commercial disputes in settlement. DCF on track for big rise in 2013. Buy @ 55

CH Energy Group (CHG) 845-486-5439 3.4 71.1 1--1--1 6.58 4 D 2012 payout ratio 85.1%. New York regulators still need to approve settlement to close takeover by Fortis at $65 per share. SELL

Chesapeake Utilities (CPK) 888-742-5275 2.9 65.4 5--0--0 0.03 5 D Q4 earnings up 22.9%, payout ratio down to 48.8%, as higher retail propane margins ensure sixth consecutive record year. Hold

Consolidated Edison (ED) 800-522-5522 4.2 86.9 3--10--5 20.37 4 R Sells 30-year debt at rate of 3.95%, a much better price than company had originally guided to. Hold

Delta Natural Gas (DGAS) 859-744-6171 3.3 62.6 0--3--0 0.11 2 D Industrial sales to mining industry could take a hit this year due to weak coal prices and curtailed production in some areas. Hold

El Paso Pipe Partners LP (EPB) 713-420-2600 5.9 100.0 3--12--1 1.35 8 R Moody’s shifts outlook to “positive.” May sell up to $500 million in new units to fund future asset growth. Buy @ 40

Enbridge Energy LP (EEP) 800-481-2804 7.4 79.1 5--10--1 14.55 5 R Completes major new oil transport system in Bakken Shale, on schedule and under budget, to produce big cash flow in 2013. Buy @ 32

Energy Transfer LP (ETP) 214-981-0700 7.4 65.0 6--10--0 4.57 5 D Contributes interest in former Sunoco assets to new entity, ETP Holdco, of which MLP currently owns 40%. Buy @ 50

DiVErsifiED ENErgy regulated Analyst insider sfty ute Company (symbol) Phone yield revenue ratings Holdings rtg type Comment Advice

• How they rate • How they rate • How they rate • How they rate • How they rate • How they rate • How they rate • How they rate • How they rate • How they rate • How they rate • How they rate •

Page 4 • www.UtilityForecaster.com • 703-394-4931 How They Rate Chart Key located on Page 7 • April 2013

Enterprise Products LP (EPD) 713-880-6500 4.6% 65.0% 19--4--0 -2.54% 8 D Sells 31-year debt at rate of 4.85%. S&P raises rating to BBB+. Moody’s boosts to Baa1. Buy @ 55

Ferrellgas Partners LP (FGP) 816-792-1600 10.4 0.0 0--1--5 0.77 1 D FY Q2 distributable cash flow up 50%, taking payout ratio to 108.1%, as lower revenue offset by reduced propane costs. SELL

Gas Natural (EGAS) 406-791-7500 5.4 86.8 1--0--0 0.12 5 D Weather has impact on natural gas business, but long-term returns will be fueled by customer growth and cost controls. Buy @ 11

ITC Holdings (ITC) 248-374-7100 1.8 100.0 7--5--0 57.88 8 R Q4 earnings up 18.5%, driving payout ratio down to 36.5%. Affirms 2013 EPS target of $4.80 to $5.00. Hold

Kinder Morgan Energy LP (KMP) 713-369-9490 5.9 90.0 4--14--0 0.00 6 D Buys up rest of El Paso Pipeline and plans solid expansion of assets focused on oil. Will be accretive to earnings. Buy @ 86

Laclede Group (LG) 800-884-4225 4.1 69.4 1--6--0 4.12 6 R Now a larger utility with geographic focus and considerable opportunities to take advantage of economies of scale. Hold

Magellan Midstream LP (MMP) 877-934-6571 4.0 83.3 5--12--0 13.75 7 D Buys 800-mile refined products pipeline from Plains All-American for $190 million. Longhorn pipeline now shipping oil in Texas. Buy @ 42

MarkWest Energy LP (MWE) 303-290-8700 5.5 70.0 9--1--0 -7.21 3 D Q4 distributable cash flow up 26.4%. Payout ratio at 94.3%, as company maintains robust 2013 DCF forecast. Buy @ 55

New Jersey Resources (NJR) 732-938-1480 3.6 70.0 2--3--3 5.17 8 D Management sticks to FY 2013 EPS target range of $2.55 to $2.75, despite impact of shortfall in FY Q1. Buy @ 40

Northeast Utilities (NU) 800-665-3249 3.4 88.3 10--7--1 -11.91 6 R Massachusetts regulators let CEO off the hook on pay issue. Affirms 2013 EPS guidance of $2.40 to $2.60. Hold

Northwest Natural Gas (NWN) 888-777-0321 4.1 95.0 1--4--4 3.12 7 R Regulatory disallowance knocks down 2012 earnings by 2.9%, making payout ratio 78.5%. Sets 2013 EPS range of $2.15 to $2.35. Hold

NuStar Energy LP (NS) 972-699-4062 8.5 70.0 0--9--4 5.82 5 D In dispute over purchase of pipeline from Textron. Expected cash flows from project won’t affect abilty to cover distribution by Q4. Buy @ 55

NV Energy (NVE) 800-662-7575 3.8 100.0 3--13--0 22.95 5 R S&P boosts rating to investment-grade. Projects 2013 EPS of $1.25 to $1.35. May file 2013 rate case. Buy @ 20

ONEOK (OKE) 918-588-7158 3.1 67.0 10--3--1 25.11 5 D Q4 earnings dip 3.6%, cuts guidance for 2013 due to unfavorable impact of weak NGLs prices. Buy @ 50

ONEOK Partners LP (OKS) 877-208-7318 5.3 67.0 2--13--1 1.38 6 D Cuts 2013 DCF guidance due to lower NGLs prices. Reduces projected dividend growth through 2015 to 8% to 12%. Buy @ 52

Pembina Pipeline (PPL, PBNPF) 403-231-7500 5.2 70.0 6--1--1 1.13 7 D Plans an additional CAD1 billion in NGLs infrastructure. Posts 69.5% payout ratio in Q4 on 51.3% profit growth. Buy @ 30

PEPCO Holdings (POM) 866-254-6502 5.2 92.2 2--13--0 7.12 2 D Q4 earnings up 26.7%, payout ratio comes down to 89.3%. Issues 30-year debt at 4.15% interest rate. Hold

Piedmont Natural Gas (PNY) 704-731-4438 3.7 95.0 2--4--3 7.23 8 R Boosts dividend 3.3%, affirms FY 2013 EPS guidance of $1.67 to $1.77 after FY Q1 earnings gain of 12.4%. Buy @ 32

Plains All-American Pipeline LP (PAA) 713-646-4100 4.1 65.0 18--5--0 -0.76 5 D Sells 800 miles of “non-core” pipeline to Magellan Midstream to focus portfolio and provide funds for further expansion. Buy @ 45

Portland General (POR) 503-464-8000 3.6 100.0 4--6--1 23.16 5 R Sees FY 2013 EPS of $1.85 to $2.00. Ramps up purchases of renewable energy in Oregon. Hold

Questar Corp (STR) 801-324-5497 2.9 95.0 4--6--0 7.59 3 D Results very predictable at regulated utility and pipeline as well as regulated natural gas production in Utah. Hold

RGC Energy (RGCO) 540-777-4427 3.9 100.0 None 2.39 6 R Conservative financial and operating policies ensure dividends remain steady and growing despite soft local economy. Hold

South Jersey Industries (SJI) 609-561-9000 3.2 70.0 3--1--1 9.57 7 D 2012 economic earnings up 7%, as company posts highest customer growth since 2006, hits annual profit growth target. Hold

Southwest Gas (SWX) 800-331-1119 2.8 73.7 5--3--1 11.49 4 R Boosts dividend 11.9%. S&P raises rating to A- after company posts 12.5% Q4 earnings growth and 45.7% payout ratio. Hold

Spectra Energy (SE) 800-488-3853 4.2 70.0 5--8--1 16.39 6 D Buys rest of Express-Platte Pipeline System for $1.49 billion to raise cash flow and fee-based business portfolio. Buy @ 33

Spectra Energy LP (SEP) 713-627-5400 5.1 100.0 1--11--2 0.94 8 R Asset drop-downs will remain primary source of cash flow and distribution growth. Current price looks lofty. Buy @ 34

Suburban Propane LP (SPH) 973-887-5300 8.2 0.0 2--7--1 5.08 2 D Additional scale boosts profitability along with low wholesale propane prices, offsetting mild weather. Buy @ 44

UGI Corp (UGI) 610-337-1000 2.9 25.0 3--2--0 8.33 4 D Longtime CEO Lon Greenberg to retire this year. Will be replaced by COO John Walsh. Hold

UIL Holdings (UIL) 800-722-5584 4.5 100.0 3--9--1 -1.35 3 R FY 2013 EPS guidance set at $2.05 to $2.25. Management targets oil-to-gas conversions as key focus for growth. Hold

Unitil Corp (UTL) 800-999-6501 5.0 98.0 2--3--0 9.00 4 R Unregulated Usource energy management and marketing business is prime earnings variable. Regulated ops are steady. Hold

WGL Holdings (WGL) 703-750-2000 3.8 45.8 3--3--3 0.04 6 D Future dividend growth will be fueled by utility CAPEX and regulatory support, along with select unregulated operations. Hold

Williams Companies (WMB) 800-600-3782 3.8 70.0 12--2--1 16.90 5 D Plans CAD900 million NGLs plant in Alberta. Forms NGLs pipeline joint venture with Boardwalk LP. Buy @ 35

NAturAl rEsourCEs Production Analyst insider sfty ute Company (symbol) Phone yield growth ratings Holdings rtg type Comment Advice

ARC Resources (ARX, AETUF) 888-272-4900 4.4% 28.5% 11--8--1 1.59% 2 M Late-winter recovery in natural gas prices could be a huge plus later in 2014. Liquids sales support dividend, growth. Buy @ 25

Atlantic Power Corp (AT) 617-977-2700 7.5 128.2 0--3--5 0.05 2 T Cuts dividend 65.2% in huge shift to shore up cash flow to invest, with North American power market weak. 2012 results in line. Hold

Boralex Inc (BLX, BRLXF) 514-982-7888 0.0 -10.6 6--2--1 0.00 3 D Has generally avoided projects in the US due to difficulty locking in long-term pricing for contracts. Hold

BP Plc (BP) 44-20-7496-4000 5.3 -7.0 16--18--4 3.04 2 M Loses bid to bar charge of gross negligence from ongoing court case over 2010 Gulf of Mexico oil spill. Hold

BP Prudhoe Bay (BPT) 212-815-6908 11.8 0.0 1--0--0 0.00 1 M Leverage to high oil prices continues to grow, as BP’s North Slope oil reserve continues to diminish past trust’s scheduled wind-up. SELL

Brookfield Renewable (BEP-U, BRPFF) 819-561-2722 5.0 5.0 8--3--0 17.05 8 D Wins takeover bid for Western Wind. Closes purchase of 351 MW of Southeast US hydropower. Still no US listing. Buy @ 32

Calpine Corp (CPN) 800-359-5115 0.0 23.0 10--6--1 67.14 2 M Future success will depend on company’s ability to lock in price of natural gas for power plant fuel. Hold

Chesapeake Energy (CHK) 405-848-8000 1.7 9.0 11--22--1 6.74 2 M Now faces trial over disputed bond redemption. Natural gas recovery likely to help in 2013, though leverage remains key challenge. SELL

Chevron (CVX) 800-368-8357 3.0 1.1 19--9--1 0.36 5 M Management targets 25% growth in global energy output within five years, drawn from range of gas and oil projects. Buy @ 105

ConocoPhillips (COP) 800-814-0299 4.4 1.8 12--8--4 1.25 4 M Management reports significant discovery of energy in deepwater Gulf of Mexico. Sets dividend growth as priority. Hold

Covanta (CVA) 973-882-9000 3.3 -0.4 6--4--1 5.41 4 M Boosts dividend 10% and increases stock buyback to $150 million. Reaffirms leverage targets. Buy @ 16

Devon Energy (DVN) 405-235-3611 1.5 4.2 19--12--1 -20.75 3 M Boosts dividend 10%. Solid presence in Permian Basin reflects further focus on liquids output. Hold

Dominion Warrior Trust (DOM) 800-365-6548 13.0 -0.2 None 0.00 1 M Unit price recovers sharply, as higher natural gas prices allow sizable boost in distribution. Hold

Dynegy (DYN) 713-507-6400 0.0 13.6 0--4--2 -99.19 1 M Buys coal-fired power plant in Illinois from Ameren, doubling capacity in the state, with management citing potential synergies. SELL

EnCana (ECA) 403-645-2000 4.1 -12.1 2--19--5 4.65 3 M DBRS affirms rating at BBB with a “stable” outlook. Locks in higher gas prices with hedging. Hold

Energen Corp (EGN) 800-654-3206 1.1 18.0 11--6--0 6.31 4 D Takeover talk gives boost to share price. But company’s long-term fortunes appear set and steady on their own. Buy @ 55

Enerplus Corp (ERF) 403-298-2200 7.1 9.0 9--6--2 1.06 2 M Q4 profit up 26.7%, payout ratio at 32.8% on production gains and 25% drop in operating costs. Hold

Eni (E) 39-06-59821 4.7 7.0 23--13--2 16.27 5 M Boosts production growth target to 4% per year following recent energy discoveries. Targets 2% dividend growth in 2013. Buy @ 50

EOG Resources (EOG) 877-363-3647 0.6 10.0 29--7--2 0.77 4 M Barclays says company has low extraction risk for projects. Value of Eagle Ford properties soars. Buy @ 120

EQT Corp (EQT) 412-553-5700 0.2 33.0 11--8--1 6.56 4 D Natural gas price recovery could lift price in the near term. But long-term build-out plans are set even if prices stay low. Hold

ExxonMobil (XOM) 800-252-1800 2.6 -5.2 11--18--0 9.50 5 M Buys more Oklahoma shale. Allies with Rosneft in Gulf of Mexico. Find off Tanzanian coast boosts African gas resources. Buy @ 80

Linn Energy LLC (LINE) 281-240-4100 7.7 88.0 14--5--0 -0.57 3 M US Dept of Justice signs off on acquistion of Barry. Deal looks set to close in Q2. Huge lift to cash flow and production. Buy @ 40

National Fuel Gas (NFG) 800-648-8166 2.4 34.0 4--6--1 0.32 5 D Reaffirms 2013 forecast. Guides to 28% production growth this year, 25% next year. Hold

• How they rate • How they rate • How they rate • How they rate • How they rate • How they rate • How they rate • How they rate • How they rate • How they rate • How they rate • How they rate •

How They Rate Chart Key located on Page 7 • April 2013 www.UtilityForecaster.com • Page 5

ENErgy DistributioN (CoNt.) regulated Analyst insider sfty ute Company (symbol) Phone yield revenue ratings Holdings rtg type Comment Advice

Page 6 • www.UtilityForecaster.com • 703-394-4931 How They Rate Chart Key located on Page 7 • April 2013

NAturAl rEsourCEs (CoNt.) Production Analyst insider sfty ute Company (symbol) Phone yield growth ratings Holdings rtg type Comment Advice

• How they rate • How they rate • How they rate • How they rate • How they rate • How they rate • How they rate • How they rate • How they rate • How they rate • How they rate • How they rate •

NRG Energy (NRG) 609-524-4500 1.4% -17.4% 13--1--1 29.90% 2 M Targets 33% dividend growth in 2013. Boosts forecast for 2013-14 cash flow. Ramps up solar build-out. Buy @ 22

Peabody Energy (BTU) 314-342-3400 1.6 -7.0 18--8--2 8.60 3 M Sets FY 2013 CAPEX budget 50% below previous year. Patriot Coal sues company for health care costs. Hold

Penn West Petroleum Ltd (PWE) 866-318-1767 9.0 -1.2 4--12--7 9.29 2 M Follow-through on 2013 production plans a concern. Trades at steep discount to conservative value of reserves. Hold

PVR Partners LP (PVR) 610-687-8900 9.6 -25.8 4--4--0 13.48 3 D Challenge is getting midstream build-out on track after a light Q4. Coal likely to remain weak at least until 2013 H2. Buy @ 25

Petrobras (PBR) 303-477-1350 0.6 -1.2 1--8--1 0.00 3 D May sell Argentine assets. Maintains aggressive CAPEX. May have trouble meeting simultaneous leverage targets as well. Hold

Royal Dutch Shell (RDS/A) 212-218-3112 4.4 3.3 13--14--3 159.20 5 M Suspends Arctic drilling amid technical difficulties. Plans to re-enter polyethylene market after eight-year hiatus. Hold

Southwestern Energy (SWN) 281-618-4700 0.0 13.0 13--20--2 -2.07 2 M Fitch affirms rating at BBB-. Higher natural gas prices may help cash flow in 2013. Hold

Total Fina Elf (TOT) 33-1-47-44-45-46 5.5 -3.8 28--8--4 0.87 4 M Free cash flow remains strong. Sells non-core assets to control debt and deploy with more focus in more promising areas. Buy @ 52

CommuNiCAtioNs growth Analyst insider sfty ute Company (symbol) Phone yield businesses ratings Holdings rtg type Comment Advice

Alaska Communications (ALSK) 907-297-3000 0.0% 47.0% 0--2--2 42.21% 2 D Q4 revenue up 8.7%, as 14% increase in wholesale operations offsets 5.9% decline in revenue from access and local service. SELL

AT&T Corp (T) 800-351-7221 5.0 81.0 12--21--5 1.24 5 D Aggressive rollout of 4G network continues, with 60% of 2013 CAPEX targeted there. Continues to win post-paid customers. Buy @ 35

Cablevision (CVC) 516-803-2300 4.0 70.0 7--11--4 12.56 3 D Q4 revenue drops 1.4%, cash flow declines 44.2%, as basic cable business slides. Faces higher cost from Superstorm Sandy. SELL

CenturyLink (CTL) 800-969-6718 6.2 50.0 7--10--4 -6.20 4 D Stock has stabilized since dividend cut. Debt refinancing efforts proceed mostly successfully. Hold

Cincinnati Bell (CBB) 800-345-6301 0.0 50.0 4--7--1 -13.12 2 D Q4 revenue flat, cash flow dips 2%. Biggest trouble spot is 17% drop in wireless revenue, as it sheds post-paid customers. SELL

Comcast Corp (CMCSA) 866-281-2100 1.9 80.0 23--7--0 -22.43 5 D Commercial revenue growth hits 30%. Reduces target leverage ratios, reflecting robust free cash flow, bright 2013 outlook. Buy @ 40

Consolidated Communications (CNSL) 217-235-3311 8.8 74.0 3--1--1 23.64 4 D Pro forma revenue up 1.8%, cash flow up 5.8% adjusted for items, as Q4 payout slips to 58.2%. Buy @ 19

Fairpoint Communications (FRP) 704-344-8150 0.0 50.0 1--2--0 0.00 0 M Data/Internet revenue up 13.1%. But Q4 revenue drops 5.5% due to 7.8% decline in voice-access lines. Hold

Frontier Communications (FTR) 203-614-5600 10.2 70.0 7--8--3 -6.28 2 D Q4 revenue drops 3.9%. But Q4 payout ratio remains low at 45%. Still adding broadband users. Hold

IDT Communications (IDT) 973-438-1000 0.0 50.0 3--0--0 -8.45 0 M FY Q2 revenue up 12.7%. Gross profit up 13.7%. But consumer phone business continues to shrink. SELL

Level3 Communications (LVLT) 720-888-5085 0.0 100.0 5--10--1 -4.92 0 M Expands data center capability. CEO James Crowe III plans to step down. Settles with FCC in rural phone case. Hold

Otelco (OTT) 205-625-3574 0.0 17.0 0--0--1 0.00 0 T Revenue drops 6.9% in Q4, as company loses 4.8% of access lines and 0.7% of data lines. Restructuring likely in Q2. SELL

Sprint Nextel (S) 800-259-3755 0.0 100.0 11--15--2 -2.65 0 M Sprint, SoftBank, Clearwire talk to FCC about potential combinations. Currency hedges keep SoftBank from taking a bath on declining yen. SELL

Telephone & Data Systems (TDS) 312-630-1900 2.4 90.1 6--2--0 -5.41 4 D Boosts dividend 4.1%. Cuts CAPEX 30%, as revenue drops 1%. Continues to lose post-paid wireless customers. SELL

Time Warner Cable (TWC) 866-463-6899 2.7 80.0 18--12--0 30.17 5 D Management projects 3% to 4% organic revenue growth in 2013. Could accelerate further if company makes another acquisition. Hold

Verizon Communications (VZ) 212-395-2121 4.2 81.0 17--18--1 82.60 5 D Rumors resurface of bid for Vodafone’s 45% interest in Verizon Wireless. Uses acquired cable spectrum to boost wireless speeds. Buy @ 45

Windstream Corp (WIN) 972-373-1000 11.6 70.0 6--8--5 3.71 5 D Expands switched ethernet system to meet demand from carriers for bandwidth. Stock continues to carry heavy short interest. Buy @ 11

utility tECHNology revenue Analyst insider sfty ute Company (symbol) Phone yield growth ratings Holdings rtg type Comment Advice

Aegion Corp (AEGN) 636-530-8000 0.0% 6.5% 6--3--0 26.14% 3 M 2012 earnings up 50%, as energy, mining and North American water, wastewater revenues offset delays in Asian projects. Hold

American Superconductor (AMSC) 508-836-4200 0.0 -73.3 1--3--1 142.42 2 M US wind-power tax credit extension should be a big plus this year for alternative energy business. Hold

Apple (AAPL) 408-996-1010 2.3 44.6 51--10--3 1.15 1 M Rumored to be considering dividend hike of as much as 50% in 2013. Battle with Samsung for device dominance is global. Buy @ 480

Ballard Power Systems (BLDP) 604-412-3195 0.0 -22.1 0--3--0 0.00 0 M Sells fuel-cell modules to Europe’s No. 4 bus manufacturer. Anglo American gives company $4 million cash infusion. SELL

Convergys (CVG) 800-344-3000 1.4 -13.0 4--4--1 -0.55 1 M Targets large companies in search of cost savings. Top 10 customers outsource just a third of customer service, leaving room to expand. Hold

Ericsson (ERIC) 212-685-4030 2.4 0.4 24--9--5 0.96 3 M Plans to cut 1,600 jobs. Dissolves venture with ST Microelectronics. Launches new network processor product. Buy @ 11

FuelCell Inc (FCEL) 203-825-6000 0.0 -1.6 3--1--1 0.90 1 M Targets increase in annual production run rate of 25% in 2013. FY Q1 revenue up 16.3% and backlog rises. Hold

Hyflux (HYFXF) 65-6214-0777 3.5 41.6 2--4--3 0.03 0 M FY 2012 profit up 15% on gains from municipal contracts outside China. Boosts interim dividend 19%. Buy @ 1.25

Itron (ITRI) 509-891-3523 0.0 -8.3 11--8--1 10.38 2 M Plans to buy back up to $50 million in stock. Wins smartmeter contract with Las Vegas Valley Water District. Buy @ 45

Ormat Tech (ORA) 775-356-9029 0.0 17.7 4--4--1 0.00 2 M Q4 revenue drops 6.2% in deceleration from annual growth rate of 17.7%. But reason is basically one-time events. Buy @ 22

Plug Power (PLUG) 518-782-7700 0.0 -5.4 1--0--0 10.86 0 D Interinvest reports 17.22% ownership of company. Solvency becoming a major question mark. SELL

Power-One (PWER) 925-946-9432 0.0 0.0 8--6--3 -5.13 1 M Inverter sales pass 1 million mark in volume. Hangs in despite very tough market. Buy @ 5

Sasol (SSL) 27-11-441-3111 2.4 19.0 7--7--5 -5.76 1 M Synfuel product sales up 10% in FY 2013 H1. Operating profit rises 9%, ex items, as expansion plans pay off. Buy @ 48

SunPower (SPWR) 408-991-0900 0.0 4.3 4--11--5 49.63 2 M CEO says company will see major boost in 2013 H2. Success will depend on winning big contracts. Hold

Vestas Wind Systems (VWSYF) 45-973-0000 0.0 24.1 6--10--12 0.00 2 M May sell Colorado facility to cut debt and costs. Focus is on Asian wind markets, with the Philippines the primary target. Hold

WAtEr regulated Analyst insider sfty ute Company (symbol) Phone yield revenue ratings Holdings rtg type Comment Advice

American States Water (AWR) 909-394-0711 2.5% 80.0% 1--6--0 -8.24% 7 R Q4 earnings up 51.4%. Contract services spur increase due to expansion of all military bases served. SELL

American Water Works (AWK) 856-346-8200 2.5 85.1 14--4--0 37.22 8 R 2012 revenue growth 7.9%, as company hits target. Sets 2013 EPS guidance of $2.15 to $2.25. Buys two Pennsylvania systems. Buy @ 33

Aqua America (WTR) 610-527-8000 2.3 98.0 6--7--2 0.55 8 R Q4 revenue up 12.9%. Earnings up 13%, ex items, the payout ratio comes in at 50%. Buys Pennsylvania, Virginia systems. Buy @ 24

Artesian Resources (ARTNA) 302-453-6900 3.7 88.5 3--2--0 2.46 7 R Rate hikes, cost controls push up 2012 earnings 36.1%. Payout ratio at 71.8%. Buy @ 19

California Water (CWT) 800-750-8200 3.2 94.2 1--7--0 8.68 6 R 2012 earnings up 29.5% on rate increases and CAPEX booked as earnings. California rate case this year is critical. SELL

Connecticut Water (CTWS) 800-428-3985 3.4 91.8 1--3--1 3.08 8 R Q4 earnings drop 23.8% on timing of costs. But full-year profit up 18.3%, payout ratio 62.6%. Buy @ 25

Middlesex Water (MSEX) 732-634-1500 3.8 89.5 1--2--0 2.11 5 R Q4 revenue up 16.3% on benefit from recent rate cases. Payout ratio 83.3%. Hold

SJW Corp (SJW) 408-279-7800 2.7 98.0 2--1--1 0.93 4 R Q4 earnings drop 11.1%, as water production costs surge 16.5%, offsetting revenue growth. Payout ratio 61.9%. SELL

York Water (YORW) 717-845-3601 2.9 100.0 2--3--1 0.76 8 R Q4 revenue up 3.2%, earnings up 12.5%, producing a 76.8% payout ratio on steady rate-base growth. Buy @ 18

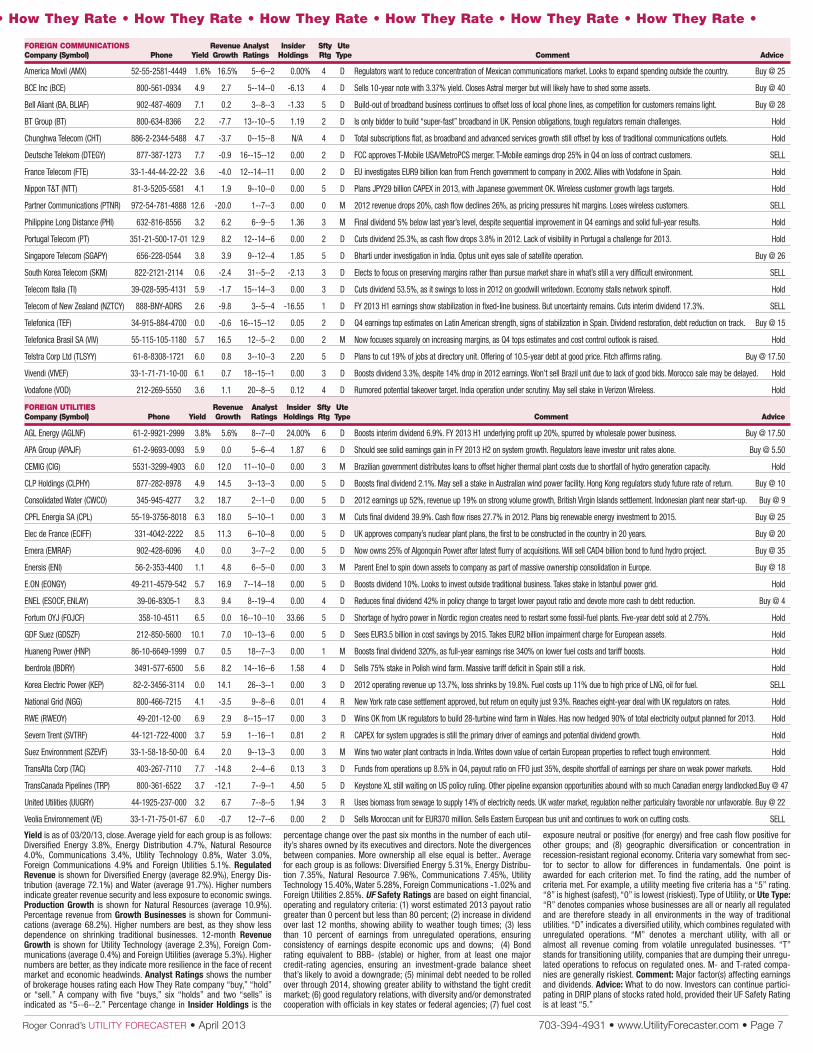

forEigN CommuNiCAtioNs revenue Analyst insider sfty ute Company (symbol) Phone yield growth ratings Holdings rtg type Comment Advice

Roger Conrad’s UTIlITy FoRECaSTER • April 2013 703-394-4931 • www.UtilityForecaster.com • Page 7

• How they rate • How they rate • How they rate • How they rate • How they rate • How they rate • How they rate • How they rate • How they rate • How they rate • How they rate • How they rate •

America Movil (AMX) 52-55-2581-4449 1.6% 16.5% 5--6--2 0.00% 4 D Regulators want to reduce concentration of Mexican communications market. Looks to expand spending outside the country. Buy @ 25

BCE Inc (BCE) 800-561-0934 4.9 2.7 5--14--0 -6.13 4 D Sells 10-year note with 3.37% yield. Closes Astral merger but will likely have to shed some assets. Buy @ 40

Bell Aliant (BA, BLIAF) 902-487-4609 7.1 0.2 3--8--3 -1.33 5 D Build-out of broadband business continues to offset loss of local phone lines, as competition for customers remains light. Buy @ 28

BT Group (BT) 800-634-8366 2.2 -7.7 13--10--5 1.19 2 D Is only bidder to build “super-fast” broadband in UK. Pension obligations, tough regulators remain challenges. Hold

Chunghwa Telecom (CHT) 886-2-2344-5488 4.7 -3.7 0--15--8 N/A 4 D Total subscriptions flat, as broadband and advanced services growth still offset by loss of traditional communications outlets. Hold

Deutsche Telekom (DTEGY) 877-387-1273 7.7 -0.9 16--15--12 0.00 2 D FCC approves T-Mobile USA/MetroPCS merger. T-Mobile earnings drop 25% in Q4 on loss of contract customers. SELL

France Telecom (FTE) 33-1-44-44-22-22 3.6 -4.0 12--14--11 0.00 2 D EU investigates EUR9 billion loan from French government to company in 2002. Allies with Vodafone in Spain. Hold

Nippon T&T (NTT) 81-3-5205-5581 4.1 1.9 9--10--0 0.00 5 D Plans JPY29 billion CAPEX in 2013, with Japanese government OK. Wireless customer growth lags targets. Hold

Partner Communications (PTNR) 972-54-781-4888 12.6 -20.0 1--7--3 0.00 0 M 2012 revenue drops 20%, cash flow declines 26%, as pricing pressures hit margins. Loses wireless customers. SELL

Philippine Long Distance (PHI) 632-816-8556 3.2 6.2 6--9--5 1.36 3 M Final dividend 5% below last year’s level, despite sequential improvement in Q4 earnings and solid full-year results. Hold

Portugal Telecom (PT) 351-21-500-17-01 12.9 8.2 12--14--6 0.00 2 D Cuts dividend 25.3%, as cash flow drops 3.8% in 2012. Lack of visibility in Portugal a challenge for 2013. Hold

Singapore Telecom (SGAPY) 656-228-0544 3.8 3.9 9--12--4 1.85 5 D Bharti under investigation in India. Optus unit eyes sale of satellite operation. Buy @ 26

South Korea Telecom (SKM) 822-2121-2114 0.6 -2.4 31--5--2 -2.13 3 D Elects to focus on preserving margins rather than pursue market share in what’s still a very difficult environment. SELL

Telecom Italia (TI) 39-028-595-4131 5.9 -1.7 15--14--3 0.00 3 D Cuts dividend 53.5%, as it swings to loss in 2012 on goodwill writedown. Economy stalls network spinoff. Hold

Telecom of New Zealand (NZTCY) 888-BNY-ADRS 2.6 -9.8 3--5--4 -16.55 1 D FY 2013 H1 earnings show stabilization in fixed-line business. But uncertainty remains. Cuts interim dividend 17.3%. SELL

Telefonica (TEF) 34-915-884-4700 0.0 -0.6 16--15--12 0.05 2 D Q4 earnings top estimates on Latin American strength, signs of stabilization in Spain. Dividend restoration, debt reduction on track. Buy @ 15

Telefonica Brasil SA (VIV) 55-115-105-1180 5.7 16.5 12--5--2 0.00 2 M Now focuses squarely on increasing margins, as Q4 tops estimates and cost control outlook is raised. Hold

Telstra Corp Ltd (TLSYY) 61-8-8308-1721 6.0 0.8 3--10--3 2.20 5 D Plans to cut 19% of jobs at directory unit. Offering of 10.5-year debt at good price. Fitch affirms rating. Buy @ 17.50

Vivendi (VIVEF) 33-1-71-71-10-00 6.1 0.7 18--15--1 0.00 3 D Boosts dividend 3.3%, despite 14% drop in 2012 earnings. Won’t sell Brazil unit due to lack of good bids. Morocco sale may be delayed. Hold

Vodafone (VOD) 212-269-5550 3.6 1.1 20--8--5 0.12 4 D Rumored potential takeover target. India operation under scrutiny. May sell stake in Verizon Wireless. Hold

forEigN utilitiEs revenue Analyst insider sfty ute Company (symbol) Phone yield growth ratings Holdings rtg type Comment Advice

AGL Energy (AGLNF) 61-2-9921-2999 3.8% 5.6% 8--7--0 24.00% 6 D Boosts interim dividend 6.9%. FY 2013 H1 underlying profit up 20%, spurred by wholesale power business. Buy @ 17.50

APA Group (APAJF) 61-2-9693-0093 5.9 0.0 5--6--4 1.87 6 D Should see solid earnings gain in FY 2013 H2 on system growth. Regulators leave investor unit rates alone. Buy @ 5.50

CEMIG (CIG) 5531-3299-4903 6.0 12.0 11--10--0 0.00 3 M Brazilian government distributes loans to offset higher thermal plant costs due to shortfall of hydro generation capacity. Hold

CLP Holdings (CLPHY) 877-282-8978 4.9 14.5 3--13--3 0.00 5 D Boosts final dividend 2.1%. May sell a stake in Australian wind power facility. Hong Kong regulators study future rate of return. Buy @ 10

Consolidated Water (CWCO) 345-945-4277 3.2 18.7 2--1--0 0.00 5 D 2012 earnings up 52%, revenue up 19% on strong volume growth, British Virgin Islands settlement. Indonesian plant near start-up. Buy @ 9

CPFL Energia SA (CPL) 55-19-3756-8018 6.3 18.0 5--10--1 0.00 3 M Cuts final dividend 39.9%. Cash flow rises 27.7% in 2012. Plans big renewable energy investment to 2015. Buy @ 25

Elec de France (ECIFF) 331-4042-2222 8.5 11.3 6--10--8 0.00 5 D UK approves company’s nuclear plant plans, the first to be constructed in the country in 20 years. Buy @ 20

Emera (EMRAF) 902-428-6096 4.0 0.0 3--7--2 0.00 5 D Now owns 25% of Algonquin Power after latest flurry of acquisitions. Will sell CAD4 billion bond to fund hydro project. Buy @ 35

Enersis (ENI) 56-2-353-4400 1.1 4.8 6--5--0 0.00 3 M Parent Enel to spin down assets to company as part of massive ownership consolidation in Europe. Buy @ 18

E.ON (EONGY) 49-211-4579-542 5.7 16.9 7--14--18 0.00 5 D Boosts dividend 10%. Looks to invest outside traditional business. Takes stake in Istanbul power grid. Hold

ENEL (ESOCF, ENLAY) 39-06-8305-1 8.3 9.4 8--19--4 0.00 4 D Reduces final dividend 42% in policy change to target lower payout ratio and devote more cash to debt reduction. Buy @ 4

Fortum OYJ (FOJCF) 358-10-4511 6.5 0.0 16--10--10 33.66 5 D Shortage of hydro power in Nordic region creates need to restart some fossil-fuel plants. Five-year debt sold at 2.75%. Hold

GDF Suez (GDSZF) 212-850-5600 10.1 7.0 10--13--6 0.00 5 D Sees EUR3.5 billion in cost savings by 2015. Takes EUR2 billion impairment charge for European assets. Hold

Huaneng Power (HNP) 86-10-6649-1999 0.7 0.5 18--7--3 0.00 1 M Boosts final dividend 320%, as full-year earnings rise 340% on lower fuel costs and tariff boosts. Hold

Iberdrola (IBDRY) 3491-577-6500 5.6 8.2 14--16--6 1.58 4 D Sells 75% stake in Polish wind farm. Massive tariff deficit in Spain still a risk. Hold

Korea Electric Power (KEP) 82-2-3456-3114 0.0 14.1 26--3--1 0.00 3 D 2012 operating revenue up 13.7%, loss shrinks by 19.8%. Fuel costs up 11% due to high price of LNG, oil for fuel. SELL

National Grid (NGG) 800-466-7215 4.1 -3.5 9--8--6 0.01 4 R New York rate case settlement approved, but return on equity just 9.3%. Reaches eight-year deal with UK regulators on rates. Hold

RWE (RWEOY) 49-201-12-00 6.9 2.9 8--15--17 0.00 3 D Wins OK from UK regulators to build 28-turbine wind farm in Wales. Has now hedged 90% of total electricity output planned for 2013. Hold

Severn Trent (SVTRF) 44-121-722-4000 3.7 5.9 1--16--1 0.81 2 R CAPEX for system upgrades is still the primary driver of earnings and potential dividend growth. Hold

Suez Environnment (SZEVF) 33-1-58-18-50-00 6.4 2.0 9--13--3 0.00 3 M Wins two water plant contracts in India. Writes down value of certain European properties to reflect tough environment. Hold

TransAlta Corp (TAC) 403-267-7110 7.7 -14.8 2--4--6 0.13 3 D Funds from operations up 8.5% in Q4, payout ratio on FFO just 35%, despite shortfall of earnings per share on weak power markets. Hold

TransCanada Pipelines (TRP) 800-361-6522 3.7 -12.1 7--9--1 4.50 5 D Keystone XL still waiting on US policy ruling. Other pipeline expansion opportunities abound with so much Canadian energy landlocked. Buy @ 47

United Utilities (UUGRY) 44-1925-237-000 3.2 6.7 7--8--5 1.94 3 R Uses biomass from sewage to supply 14% of electricity needs. UK water market, regulation neither particulalry favorable nor unfavorable. Buy @ 22

Veolia Environnement (VE) 33-1-71-75-01-67 6.0 -0.7 12--7--6 0.00 2 D Sells Moroccan unit for EUR370 million. Sells Eastern European bus unit and continues to work on cutting costs. SELL

Yield is as of 03/20/13, close. Average yield for each group is as follows: Diversified Energy 3.8%, Energy Distribution 4.7%, Natural Resource 4.0%, Communications 3.4%, Utility Technology 0.8%, Water 3.0%, Foreign Communications 4.9% and Foreign Utilities 5.1%. Regulated Revenue is shown for Diversified Energy (average 82.9%), Energy Dis-tribution (average 72.1%) and Water (average 91.7%). Higher numbers indicate greater revenue security and less exposure to economic swings. Production Growth is shown for Natural Resources (average 10.9%). Percentage revenue from Growth Businesses is shown for Communi-cations (average 68.2%). Higher numbers are best, as they show less dependence on shrinking traditional businesses. 12-month Revenue Growth is shown for Utility Technology (average 2.3%), Foreign Com-munications (average 0.4%) and Foreign Utilities (average 5.3%). Higher numbers are better, as they indicate more resilience in the face of recent market and economic headwinds. Analyst Ratings shows the number of brokerage houses rating each How They Rate company “buy,” “hold” or “sell.” A company with five “buys,” six “holds” and two “sells” is indicated as “5--6--2.” Percentage change in Insider Holdings is the

percentage change over the past six months in the number of each util-ity’s shares owned by its executives and directors. Note the divergences between companies. More ownership all else equal is better.. Average for each group is as follows: Diversified Energy 5.31%, Energy Distribu-tion 7.35%, Natural Resource 7.96%, Communications 7.45%, Utility Technology 15.40%, Water 5.28%, Foreign Communications -1.02% and Foreign Utilities 2.85%. UF Safety Ratings are based on eight financial, operating and regulatory criteria: (1) worst estimated 2013 payout ratio greater than 0 percent but less than 80 percent; (2) increase in dividend over last 12 months, showing ability to weather tough times; (3) less than 10 percent of earnings from unregulated operations, ensuring consistency of earnings despite economic ups and downs; (4) Bond rating equivalent to BBB- (stable) or higher, from at least one major credit-rating agencies, ensuring an investment-grade balance sheet that’s likely to avoid a downgrade; (5) minimal debt needed to be rolled over through 2014, showing greater ability to withstand the tight credit market; (6) good regulatory relations, with diversity and/or demonstrated cooperation with officials in key states or federal agencies; (7) fuel cost

exposure neutral or positive (for energy) and free cash flow positive for other groups; and (8) geographic diversification or concentration in recession-resistant regional economy. Criteria vary somewhat from sec-tor to sector to allow for differences in fundamentals. One point is awarded for each criterion met. To find the rating, add the number of criteria met. For example, a utility meeting five criteria has a “5” rating. “8” is highest (safest), “0” is lowest (riskiest). Type of Utility, or Ute Type: “R” denotes companies whose businesses are all or nearly all regulated and are therefore steady in all environments in the way of traditional utilities. “D” indicates a diversified utility, which combines regulated with unregulated operations. “M” denotes a merchant utility, with all or almost all revenue coming from volatile unregulated businesses. “T” stands for transitioning utility, companies that are dumping their unregu-lated operations to refocus on regulated ones. M- and T-rated compa-nies are generally riskiest. Comment: Major factor(s) affecting earnings and dividends. Advice: What to do now. Investors can continue partici-pating in DRIP plans of stocks rated hold, provided their UF Safety Rating is at least “5.”

Not all of our stocks are winners thus far in 2013. But in less than three months Portfolio Holdings

are up an average of 8.5 percent. That’s despite Atlantic Power Corp (TSX: ATP, NYSE: AT) losing over half its value and a handful of other picks being slightly under-water.

Credit goes to diversification and balance, along with strong fourth-quarter earnings and positive guidance recently reported by most of our companies. We’re also seeing a great deal of buying momentum for stocks of regulated companies, which include most Portfolio Holdings.

At last count, 15 of the 18 Growth Portfolio Core

Holdings sell above my target buy prices. So do all but two Income Portfolio Conservative Holdings, one excep-tion being new addition and Income Spotlight iShares Utilities Sector Bond Fund (NYSE: AMPS).

The iShares exchange-traded fund (ETF) is replacing Verizon Communications 5.25 Percent Note of 04/15/13 (CUSIP: 92343VAN4), which matures at par value of $1,000 per bond on April 15, 2013. Cash will show up in bondholders’ accounts shortly thereafter.

Eight of the 14 Income Portfolio Aggressive Holdings trade above target, though just two of 11 Growth Port-folio Aggressive Holdings do. I’ve moved Atlantic Power there to reflect its challenges.

There are more bargains in the Aggressive Holdings of both portfolios because investors are shunning risk even as they pay up for safety. The result is our util-ities are divided into two groups of stocks facing entirely different types of risk.

The distinction will escape investors who view the world solely by sectors. In fact the Philadelphia Stock Exchange Utility Index yield of 4.1 percent is well above the 3.2 percent reached at the December 2000 sector peak as well as the 3 percent at the late-2007 high.

But utilities focused on regulated or fee-based oper-ations are moving into uncharted upside. Mean-while, those more exposed to the elements are encoun-tering major headwinds.

This month’s Feature Article focuses on the dan-gers and opportunities among the exposed. Ironi-cally, these underperforming stocks aren’t where the greatest risks lie. Rather, it’s in the “safe” stocks that have enjoyed buying momentum.

What to Do with Winners

Page 8 • www.UtilityForecaster.com • 703-394-4931 Roger Conrad’s UTIlITy FoRECaSTER • April 2013

CoNsErVAtiVE (65%) total Security and type (Exchange: Symbol) Interest Dates Price yield Return Advice

AES Corp 6.75% Pref C (NYSE: AES C) J, A, J, O—15 $50.48 6.7% 41.9% Buy @ 50

Atlantic Power 9% Note of 11/15/18 May, Nov—15 105.50 6.2 5.0 Buy @ 106

Conn Light & Power $3.24 Pref (OTC: CNLPL) J, A, J, O—1 52.06 6.2 56.1 Hold

Dominion Resources 7.195% Note of 09/15/14 Mar, Sep—15 109.07 1.1 54.1 Buy @ 108

iShares Utilities Sector Bond Fund (NSDQ: AMPS) Monthly—7 51.11 3.3 NEW Buy @ 52

Kinder Morgan Energy LP 5% Note of 12/15/13 Jun, Dec—15 103.17 1.0 35.2 Buy @ 100

Linn Energy LLC 8.625% Note of 04/15/20 Apr, Oct—15 111.00 5.7 10.9 Buy @ 110

NRG Energy Inc 7.625% Note of 05/15/19 May, Nov—15 108.00 4.7 9.8 Buy @ 104

Pacific G&E 5.5% Pref B (AMEX: PCG B) F, M, A, N—15 27.95 5.1 86.6 Buy @ 25

PNM Resources 9.25% Note of 05/15/15 May, Nov—15 113.40 2.7 40.1 Buy @ 113

San Diego G&E 5% Pref A (AMEX: SDO A) J, A, J, O—15 24.25 4.1 57.7 Buy @ 20

Verizon Communications 5.25% Note of 04/15/13 Jun, Dec—15 100.30 0.9 25.7 Maturing

Windstream Corp 7.875% Note of 11/01/17 J, A, J, O—15 114.75 4.6 18.3 Buy @ 108

Aggressive (35%) Dividend Dates

AmeriGas Partners LP (NYSE: APU) F, M, A, N—17 $44.19 7.2% 14.7% Buy @ 45

Brookfield Renewable Power Fund (TSX: BEP-U, OTC: BRPFF) J, A, J, O—30 29.03 5.0 29.6 Buy @ 32

Buckeye Partners LP (NYSE: BPL) F, M, A, N—29 58.89 7.0 160.3 Buy @ 55

Consolidated Communications (NSDQ: CNSL) F, M, A, N—1 17.68 8.8 66.1 Buy @ 19

Energy Transfer Partners LP (NYSE: ETP) F, M, A, N—14 48.53 7.4 200.3 Buy @ 50

Enterprise Products Partners LP (NYSE: EPD) F, M, A, N—9 57.17 4.6 642.2 Buy @ 55

Integrys Energy Group (NYSE: TEG) M, J, S, D—20 57.14 4.8 31.1 Buy @ 55

Kinder Morgan Energy Partners LP (NYSE: KMP) F, M, A, N—14 86.88 5.9 33.7 Buy @ 86

NiSource (NYSE: NI) F, M, A, N—20 28.58 3.4 242.3 Buy @ 24

NuStar Energy LP (NYSE: NS) F, M, A, N—10 51.72 8.5 39.9 Buy @ 55

Pembina Pipeline (TSX: PPL, NYSE: PBA) Monthly—13 30.51 5.2 256.6 Buy @ 30

Piedmont Natural Gas (NYSE: PNY) J, A, J, O—13 33.54 3.7 152.1 Buy @ 32

Windstream Corp (NYSE: WIN) J, A, J, O—16 8.59 11.6 43.6 Buy @ 11

Xcel Energy (NYSE: XEL) J, A, J, O—20 28.75 3.8 210.5 Buy @ 25

AVErAgE yiElD = 5.2%

Interest Dates/Dividend Dates shows when each security pays regular interest or dividends. Price, Yield as of 03/20/13, close. Yield-to-call or yield-to-maturity shown for fixed income, not current yields. Total Return is capital gains plus dividends since original recommendation. We consider our portfolio to consist of all securities rated either “buy” or “hold.”

INCoME PoRtFolIoThe goal of the Income Portfolio is high current yield, safety and ability for dividend growth to beat inflation.

PORTFOLIO UPDATE

It’s really just simple mathematics. The further a stock rises, the greater the percentage of your portfolio it becomes--and the more damage a drop in price will do to your overall wealth.

For example, my trio of water util-ities--American Water Works Co Inc (NYSE: AWK), Aqua America Inc (NYSE: WTR) and Connecticut Water Service Inc (NSDQ: CTWS)--carries little more dividend risk than a US Treasury bond.

But their average yield of 2.7 per-cent is well below the 3.4 percent low they reached at utilities’ late-2000 peak and the 2.9 percent hit at the late-2007 high.

There’s no rule that says these stocks can’t go higher. And the more they raise dividends the more I’ll boost their buy targets.

But at this point almost any dis -appointment could bring them lower. Connecticut Water has already come well off its late-2012 high. That’s despite reporting solid fourth-quarter and full-year results from successfully integrating its Maine acquisition.

By all means, continue reinvesting dividends in these companies. But new purchasers need to be patient. And investors with big gains should consider taking a partial profit to restore overall portfolio balance.

The same discipline should be fol-lowed for other favorites that have enjoyed parabolic rises beyond buy targets this year. If Atmos Energy Corp (NYSE: ATO) executes its plan to reach $3 to $3.20 per share in annual earnings by 2016 it will be worth its current price and then some.

Right now, however, the stock trades at 19 times earnings and yields a paltry 3.4 percent after increasing its dividend just 1.5 percent for this year.

Atmos is a buy on any dip to 33 or lower. At a price in the low 40s, however, it’s a candidate for tak-ing partial profits, particularly for the over-weighted.

I’m not suggesting wholesale selling. But taking a lit-tle money off the table to restore portfolio balance is always a good idea. And that goes double when simple measures of valuation like percentage yield are near lev-els seen at previous utility-market tops.

As for investing the proceeds, there’s nothing wrong with keeping a little cash around. But there are also plenty of values in essential-services stocks both inside

Roger Conrad’s UTIlITy FoRECaSTER • April 2013 703-394-4931 • www.UtilityForecaster.com • Page 9

GRoWtH PoRtFolIoThe goal of the Growth Portfolio is to generate high total returns consistently.

Core Holdings are generally held longer than Aggressive Holdings.

CorE HolDiNgs (80%) total Company (Exchange: Symbol) Dividend Dates Price yield Return Advice

American Water Works (NYSE: AWK) M, J, S, D—1 $40.69 2.5% 127.2% Buy @ 33

Aqua America (NYSE: WTR) M, J, S, D—1 30.45 2.3 993.3 Buy @ 24

AT&T (NYSE: T) F, M, A, N—1 36.19 5.0 35.7 Buy @ 35

Atmos Energy (NYSE: ATO) M, J, S, D—12 41.64 3.4 182.3 Buy @ 33

Chevron (NYSE: CVX) F, M, A, N—17 120.35 3.0 334.6 Buy @ 105

CMS Energy (NYSE: CMS) F, M, A, N—29 27.27 3.7 250.7 Buy @ 25

Comcast Corp (NSDQ: CMCSA) J, A, J, O—25 40.98 1.9 112.8 Buy @ 40

Connecticut Water (NSDQ: CTWS) M, J, S, D—15 28.50 3.4 41.7 Buy @ 25

Dominion Resources (NYSE: D) M, J, S, D—20 57.20 3.9 566.0 Buy @ 55

Duke Energy (NYSE: DUK) M, J, S, D—16 70.40 4.3 360.9 Buy @ 62

Entergy Corp (NYSE: ETR) M, J, S, D—1 63.97 5.2 508.9 Buy @ 75

Exelon Corp (NYSE: EXC) M, J, S, D—9 33.69 6.2 11.8 Buy @ 35

MDU Resources (NYSE: MDU) J, A, J, O—1 24.84 2.8 838.2 Buy @ 24

Sempra Energy (NYSE: SRE) J, A, J, O—15 79.90 3.2 64.4 Buy @ 68

Southern Company (NYSE: SO) M, J, S, D—6 45.79 4.3 1081.1 Buy @ 45

Spectra Energy (NYSE: SE) M, J, S, D—12 28.86 4.2 24.7 Buy @ 33

TransCanada Corp (TSX: TRP, NYSE: TRP) J, A, J, O—30 48.82 3.7 19.3 Buy @ 47

Verizon Communications (NYSE: VZ) F, M, A, N—1 48.60 4.2 303.8 Buy @ 45

Aggressive Holdings (20%) Dividend Dates

AES Corp (NYSE: AES) F, M, A, N—15 $12.68 1.3% 15.1% Buy @ 15

ARC Resources (TSX: ARX, OTC: AETUF) Monthly—16 26.45 4.4 161.1 Buy @ 25

Atlantic Power Corp (TSX: ATP, NYSE: AT) Monthly—30 5.20 7.5 43.7 Hold

CLP Holdings (OTC: CLPHY) M, J, S, D—22 8.66 4.9 220.0 Buy @ 10

Enel SpA (OTC: ESOCF, ENLAY) Jun, Nov—21 3.38 8.3 -2.7 Buy @ 4

Energen Corp (NYSE: EGN) M, J, S, D—1 51.31 1.1 975.7 Buy @ 55

NV Energy (NYSE: NVE) M, J, S, D—21 20.07 3.8 136.3 Buy @ 20

ONEOK (NYSE: OKE) F, M, A, N—14 46.00 3.1 296.1 Buy @ 50

PVR Partners LP (NYSE: PVR) F, M, A, N—13 22.90 9.6 3.5 Buy @ 25

Singapore Telecom (OTC: SGAPY) Jan, Aug—12 28.07 3.8 141.1 Buy @ 26

Telefonica SA (Spain: TEF, NYSE: TEF) May, Nov—7 14.76 0.0 11.7 Buy @ 15

Dividend Dates shows approximate dates when dividends are paid. Price, Yield as of 03/20/13, close. Total Return is capital gains plus dividends since issue date of original recommendation. We consider our portfolio to consist of all stocks rated either “buy” or “hold.”

and outside the portfolios.Aggressive investors have no shortage of choices, includ-

ing the high yielders in the Feature Article.But even the most conservative can still buy Growth

Portfolio Core Holding Spectra Energy Corp (NYSE: SE) and Income Portfolio Aggressive Holdings Brookfield Renewable Energy Partners lP (TSX: BEP-U, OTC: BRPFF) and Energy transfer Partners lP (NYSE: ETP) below target prices.

We’re off to a good start this year, and hopefully there are more gains to come. But the bull market that began in early 2009 has also had plenty of twists and turns.

The keys are to be patient, don’t over-weight anything, don’t chase on the upside and don’t average down when a stock drops.

Dominion Resources Inc (NYSE: D) is exiting the merchant coal-fired power generation business.

The final cut is the sale of two large facilities in Illi-nois and another in Massachusetts, with a combined capacity of 4,110 megawatts. The $650 million in pro-ceeds—once the deal clears federal antitrust review and wins Federal Energy Regulatory Commission approval—will be used to invest in regulated businesses and to reduce debt.

The sale won’t affect company plans to double its asset base over the next five years. Future earnings growth will be tied to new regulated power and energy midstream assets, and therefore much more predictable.

Dominion Resources remains a buy on dips to 55 or lower.

Ameren Corp (NYSE: AEE) is also pulling out of merchant coal, dishing off 4,119 megawatts of capacity in Illinois to Dynegy Inc (NYSE: DYN).

Ameren, unlike Dominion, is actually paying around $133 million to dispose of its plants in taking a $300 million after-tax charge to first-quarter earnings.

The payoff is the company will also unload $825 mil-lion in debt while increasing earnings stability substan-tially. And management has also affirmed previous 2013 earnings guidance as well as the current dividend rate. Ameren is a hold.

Post-restructuring Dynegy has no pre-deal debt maturing until August 2016. If it can navigate Illinois regulation and natural gas prices avoid another steep drop, there’s considerable upside from assets acquired so cheaply.

But doubling down on coal power has raised risks as well. Sell Dynegy.

The deal has also triggered a windfall gain of 40 per-cent in Ameren Energy Generating 7 Percent Note of 04/15/18 (CUSIP: 02360XAL1), which I recom-mended in the February 2013 issue.

The bond, which will be an obligation of Dynegy when the deal is completed later this year, still trades for 82 cents on the dollar and at a yield to maturity of 11.7 percent. But it’ll be ring-fenced from other obli-gations and can be cut loose if the company’s assump-tions for coal don’t pan out.

Take at least some of your gains now.

Merger Watch

New York regulators are expected to approve CH Energy Group Inc’s (NYSE: CHG) takeover by Fortis Inc (TSX: FTS, OTC: FRTSF) for $65 in cash immi-nently.

But with no upside—and a lot of downside if offi-cials unexpectedly balk—CH Energy is a sell.

The Federal Communications Commission (FCC) has approved the union of Deutsche telekom AG’s ( Germany: DTE, OTC: DTEGF, ADR: DTEGY) T-Mobile USA unit with MetroPCS Communications Inc (NYSE: PCS). That leaves a vote by the latter’s shareholders on April 12, which should pass despite some notable opposition.

With T-Mobile still dropping its most valuable post-paid customers at an alarming rate, the new company will focus on the lower-margin pre-paid market.

Facing challenges to its survival in both the US and Europe, Deutsche telekom is a sell.

So is Sprint Nextel Corp (NYSE: S), which is attempting to shop 70 percent of itself to Japan’s Soft-bank Corp (Japan: 9984, OTC: SFTBF).

The FCC should approve the deal by its stated dead-line of May 29. But the combination will be too debt burdened to compete over the long term with At&t Inc (NYSE: T) and Verizon Communications Inc (NYSE: VZ).

The latter has emerged once again as the target of speculation that it may buy Vodafone Plc’s (Lon-don: VOD, NYSE: VOD) 45 percent stake in Verizon Wireless. Possibilities include Verizon simply buying all of Vodafone, either by itself or in conjunction with AT&T, which presumably would get the international operations.

Owning all of Verizon Wireless is a long-stated goal of Verizon. And assuming a price of $100 billion or so for the enterprise, it could be a big plus for future earnings. Verizon is a buy on dips to 45, with or without a deal.

Burdened by weak and competitive European markets, Vodafone is a hold.

The Centerpoint Energy Inc (NYSE: CNP)-oGE Energy Corp (NYSE: OGE) and Williams Companies Inc (NYSE: WMB)-Boardwalk Pipeline Partners lP (NYSE: BWP) ventures to create new master limited part-nerships (MLP) represent a new kind of utility merger.

By pooling assets companies can establish needed scale they couldn’t achieve on their own, while the MLP structure allows them to tap into the cash flows in a tax-efficient manner.

Both initial public offerings should create value for shareholders. Centerpoint and OGE are pricey. But Wil-liams Companies is a buy on dips to 35 or lower.

I expect more utilities to spin out MLP energy mid-stream assets this year, including Dominion Resources.

When to Sue

Most business stumbles are due to unfavorable mar-ket shifts or, at worst, honest miscalculation. Occasion-

Page 10 • www.UtilityForecaster.com • 703-394-4931 Roger Conrad’s UTIlITy FoRECaSTER • April 2013

UTILITY BEAT

Merchant Power Shift

ally, however, a company’s actions will stir accusations of actual fraud, and the result is often a wave of lawsuits filed seeking restitution for shareholders.

In most cases the only beneficiaries are lawyers.For one thing, the burden of proof is very high.

Most disputes simply disappear or are settled for pea-nuts. And, when a company is really found guilty, as with evaporated Enron, there’s generally not much left to fight over.

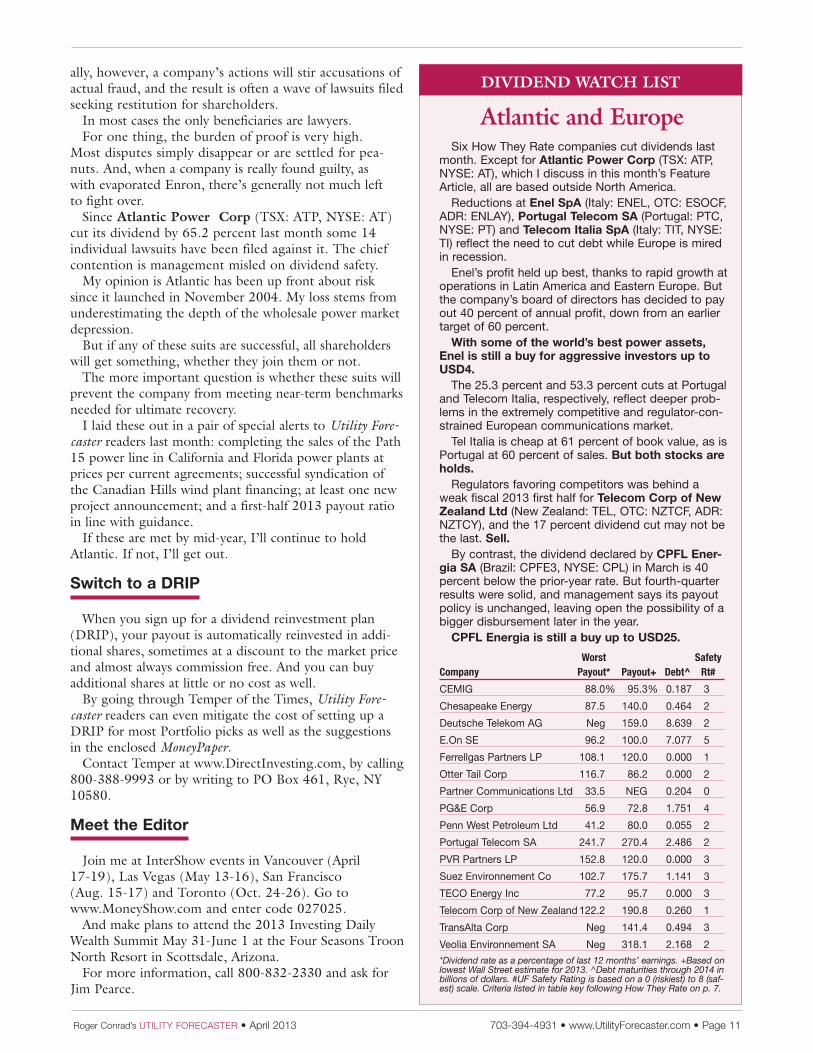

Since Atlantic Power Corp (TSX: ATP, NYSE: AT) cut its dividend by 65.2 percent last month some 14 individual lawsuits have been filed against it. The chief contention is management misled on dividend safety.

My opinion is Atlantic has been up front about risk since it launched in November 2004. My loss stems from underestimating the depth of the wholesale power market depression.

But if any of these suits are successful, all shareholders will get something, whether they join them or not.

The more important question is whether these suits will prevent the company from meeting near-term benchmarks needed for ultimate recovery.

I laid these out in a pair of special alerts to Utility Fore-caster readers last month: completing the sales of the Path 15 power line in California and Florida power plants at prices per current agreements; successful syndication of the Canadian Hills wind plant financing; at least one new project announcement; and a first-half 2013 payout ratio in line with guidance.

If these are met by mid-year, I’ll continue to hold Atlantic. If not, I’ll get out.

Switch to a DRIP

When you sign up for a dividend reinvestment plan (DRIP), your payout is automatically reinvested in addi-tional shares, sometimes at a discount to the market price and almost always commission free. And you can buy additional shares at little or no cost as well.

By going through Temper of the Times, Utility Fore-caster readers can even mitigate the cost of setting up a DRIP for most Portfolio picks as well as the suggestions in the enclosed MoneyPaper.

Contact Temper at www.DirectInvesting.com, by calling 800-388-9993 or by writing to PO Box 461, Rye, NY 10580.

Meet the Editor

Join me at InterShow events in Vancouver (April 17-19), Las Vegas (May 13-16), San Francisco (Aug. 15-17) and Toronto (Oct. 24-26). Go to www.MoneyShow.com and enter code 027025.

And make plans to attend the 2013 Investing Daily Wealth Summit May 31-June 1 at the Four Seasons Troon North Resort in Scottsdale, Arizona.

For more information, call 800-832-2330 and ask for Jim Pearce.

Six How They Rate companies cut dividends last month. Except for Atlantic Power Corp (TSX: ATP, NYSE: AT), which I discuss in this month’s Feature Article, all are based outside North America.

Reductions at Enel SpA (Italy: ENEL, OTC: ESOCF, ADR: ENLAY), Portugal Telecom SA (Portugal: PTC, NYSE: PT) and Telecom Italia SpA (Italy: TIT, NYSE: TI) reflect the need to cut debt while Europe is mired in recession.

Enel’s profit held up best, thanks to rapid growth at operations in Latin America and Eastern Europe. But the company’s board of directors has decided to pay out 40 percent of annual profit, down from an earlier target of 60 percent.

With some of the world’s best power assets, Enel is still a buy for aggressive investors up to USD4.