Embed Size (px)

Citation preview

MYANMAR REPORTCONSTRUCTION MARKET UPDATE

DECEMBER 2015

MYANMARREPORT

MARKET TRENDS

Myanmar’s economy grew 8.5% in real terms in FY 2014/15 with economic reforms supporting consumer and investor confidence despite ongoing business environment and socio-political challenges. General investment activity appears to remain subdued in FY2015/16. The World Bank revised its growth estimates for Myanmar in FY 2015/16 from 8.2% to 6.5% on the back of nationwide flooding and the ensuing uncertainty surrounding the political transition after landmark elections November 2015.

The country’s inflation rate had exceeded 10% in the 12 months to July 2015. However the International Monetary Fund (IMF) had cautioned about the country’s widening trade deficit and rapid credit growth and therefore expects inflation to exceed 13% in FY 2015/16.

The Myanmar economy is exposed to the fragile economic recoveries in the EU, China and the US, who are major investors in the country. Between January and August 2015, the Myanmar kyat depreciated by around 20% against the strong US dollar, on top of a growing current account deficit and slowing foreign investment inflow.

The country had received US$8.1 billion worth of foreign direct investment (FDI) for FY 2014/15. This amount was 25 times the sum received in fiscal year 2009/10, the year before economic reform began. For FY 2015/16, the Ministry of National Planning and Economic Development has targeted US$6 billion worth of FDI entering the country.

The construction industry is currently growing exponentially due to the country’s rising population and sustained economic growth. Leveraging on a booming building & construction sector as well as support from the government’s economic reform programmes, this growth trend is expected to continue at 7.8% in FY 2015/16, according to the Asian Development Bank (ADB).

In IMF’s latest report published in October 2015, IMF maintains an optimistic outlook for Myanmar’s economic growth, with an average expansion of 8.4% per annum for years 2016 to 2018. Meanwhile, the World Bank projects Myanmar’s medium-term economic growth prospects to remain stable assuming continued progress on reforms, albeit with a 7.8% per annum growth forecast for 2016.

MYANMAR ECONOMY

1 |

DECEMBER 2015|

2 |

MARKET TRENDS

CONSTRUCTION INDUSTRY

Myanmar’s construction industry expanded 4.4% in 1Q 2015 from 1Q 2014. Evidence of the construction boom is visible throughout the country, particularly inside Yangon. There was however a slight slowdown in the period leading up to the general elections in November 2015 and investors adopted a cautious attitude over the long-term viability of the political and economic reforms promised by the new government.

An increasingly large portion of Myanmar’s construction activity is taken up by residential projects, reportedly valued at US$1.5 billion. Moreover, the country’s Ministry of Construction targets to build more than one million houses in the pe-riod of 20 years (2015 to 2035) to meet the demand for residential real estate. However, overall con-struction activities slumped in 2015 due to the lack of bank financing after the Yangon City Develop-ment Committee instituted many rules for contractors and increased the required deposit for a licence.

The construction sector is seen by many as “not organised”. The opaqueness of rules and regula-tions has posed deterrence to po-tential construction projects. Fur-thermore, many local construction companies lack the technical ex-pertise, technology and experience in undertaking large and complex construction projects, which have caused delays to processes and the approval of building plans and designs.

For the first time after the general election, Myanmar’s construction body, the Myanmar Construc-tion Entrepreneurs Association (MCEA) had urgently called for reforms for transparent tender-ing processes in order to compete with big foreign developers in state projects. The MCEA also de-manded for legislation to enforce work site safety.

The existing rules under Myan-mar’s National Building Code, which was enacted in 2012, have been deemed unsuitable for high-rise developments. Some of the amendments to the law include new regulations on green energy technology and green construc-tion methods. The law was also ex-panded to cover areas of electric-ity, structures, piping systems and architecture. There are still some of those amendments pending ap-proval since 2013.

Meanwhile, the development of Special Economic Zones (SEZ) at Yangon’s Thilawa district; at Da-wei, in the south of the country; and at Kyaukphyu in the north-west is projected to further drive urbanisation and the construction of new production facilities.

MYANMARREPORT | DECEMBER 2015

MARKET TRENDS

CONSTRUCTION INDUSTRY (CONT’D)

The growth in the construction industry is expected to remain strong, driven by the govern-ment’s increasing expenditure on improving Myanmar’s public infra-structure, and the rising interest of domestic and foreign real estate developers on constructing resi-dential units to meet the popula-tion’s huge housing demand.

Post-election, the general market sentiments are focused on whether the new government could transit fast enough to continue the drive to modernise the country and advance its economic potential. Construction cost is projected to be an upward trend in the upcoming years. Barring any unforeseen market conditions, local building prices in Yangon are anticipated to increase by 8.0% - 10.0% in 2016.

PROPERTY MARKET

Currently, Yangon’s property mar-ket is severely undersupplied as the country is in the early stages of an expansion cycle with new mixed-use developments that are still underway. A majority of the ongoing projects are expected to be completed in 2016.

The surge in demand for real es-tate, especially office space and luxury housing in Yangon can be attributed to the incoming inter-national investments. Occupancy rates have been pushed up and property prices expected to re-main high in the short term ahead. In addition, most of the commer-cial complexes contain shopping malls that have been designed to cater to the emerging middle class in the country’s urban areas.

According to Myanmar’s Internal Revenue Department (IRD), most property transactions are usually

3 |

MYANMARREPORT | DECEMBER 2015

made with informal contracts for a variety of property purchases, including those of apartments and condominiums. These informal transactions have jeopardised many property buyer’s real estate interests as they fall short of transferring full legal ownership of the property, which makes it difficult for the buyer to prove ownership of the disputed property in the courts.

The Business Monitor International predicts a real growth rate at an average of 10.8% between years 2016 and 2023 for the property sector. In addition, industry play-ers expect the real estate mar-ket in Nay Pyi Taw to see a posi-tive turn as the country move to a National League of Democracy (NLD)-led government in 1Q 2016, albeit observers’ belief that the ar-ea’s property market remains slow with its steady prices.

CURRENCYUNITS PER USD

1Q2015 2Q2015 3Q2015 4Q2015p

Myanmar Kyat (MMK) 1,050 1,105 1,265 1,308

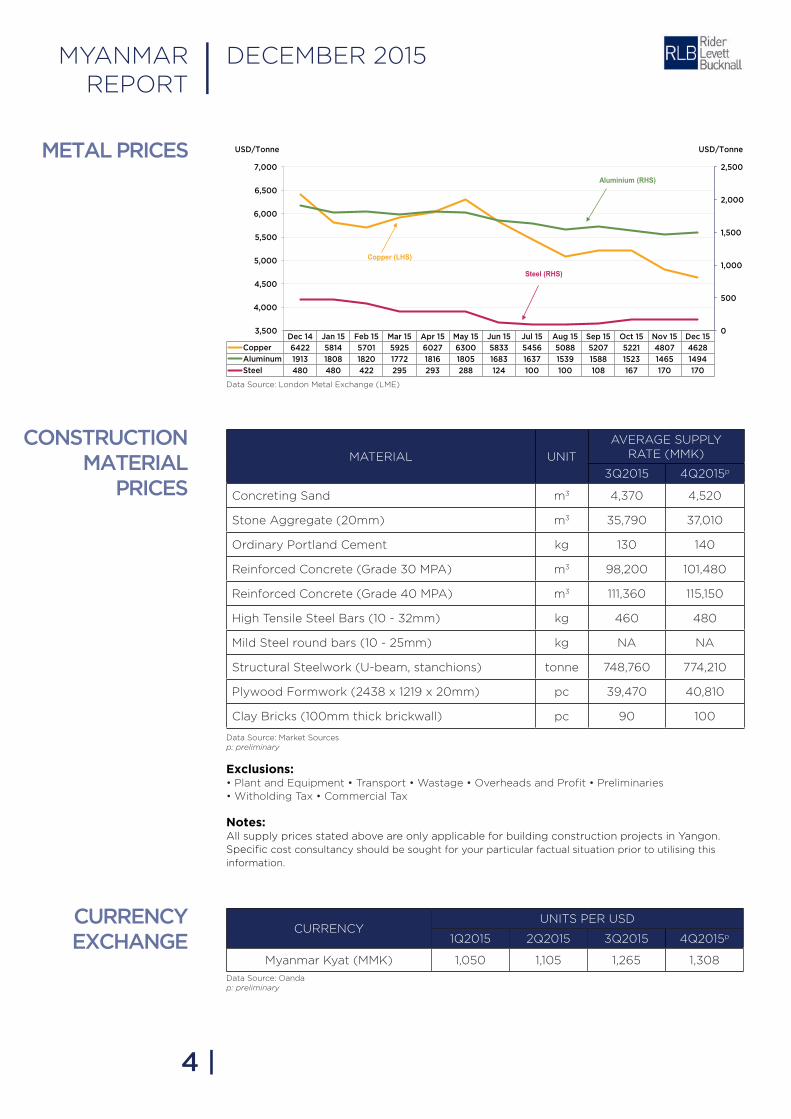

METAL PRICES

Data Source: London Metal Exchange (LME)

CONSTRUCTION MATERIAL

PRICES

Data Source: Market Sourcesp: preliminary

Exclusions: • Plant and Equipment • Transport • Wastage • Overheads and Profit • Preliminaries • Witholding Tax • Commercial Tax

Notes: All supply prices stated above are only applicable for building construction projects in Yangon. Specific cost consultancy should be sought for your particular factual situation prior to utilising this

information.

MATERIAL UNIT

AVERAGE SUPPLY RATE (MMK)

3Q2015 4Q2015p

Concreting Sand m3 4,370 4,520

Stone Aggregate (20mm) m3 35,790 37,010

Ordinary Portland Cement kg 130 140

Reinforced Concrete (Grade 30 MPA) m3 98,200 101,480

Reinforced Concrete (Grade 40 MPA) m3 111,360 115,150

High Tensile Steel Bars (10 - 32mm) kg 460 480

Mild Steel round bars (10 - 25mm) kg NA NA

Structural Steelwork (U-beam, stanchions) tonne 748,760 774,210

Plywood Formwork (2438 x 1219 x 20mm) pc 39,470 40,810

Clay Bricks (100mm thick brickwall) pc 90 100

CURRENCY EXCHANGE

Data Source: Oandap: preliminary

4 |

MYANMARREPORT | DECEMBER 2015

Dec 14 Jan 15 Feb 15 Mar 15 Apr 15 May 15 Jun 15 Jul 15 Aug 15 Sep 15 Oct 15 Nov 15 Dec 15Copper 6422 5814 5701 5925 6027 6300 5833 5456 5088 5207 5221 4807 4628

Aluminum 1913 1808 1820 1772 1816 1805 1683 1637 1539 1588 1523 1465 1494

Steel 480 480 422 295 293 288 124 100 100 108 167 170 170

0

500

1,000

1,500

2,000

2,500

3,500

4,000

4,500

5,000

5,500

6,000

6,500

7,000

USD/Tonne USD/Tonne

Aluminium (RHS)

Copper (LHS)

Steel (RHS)

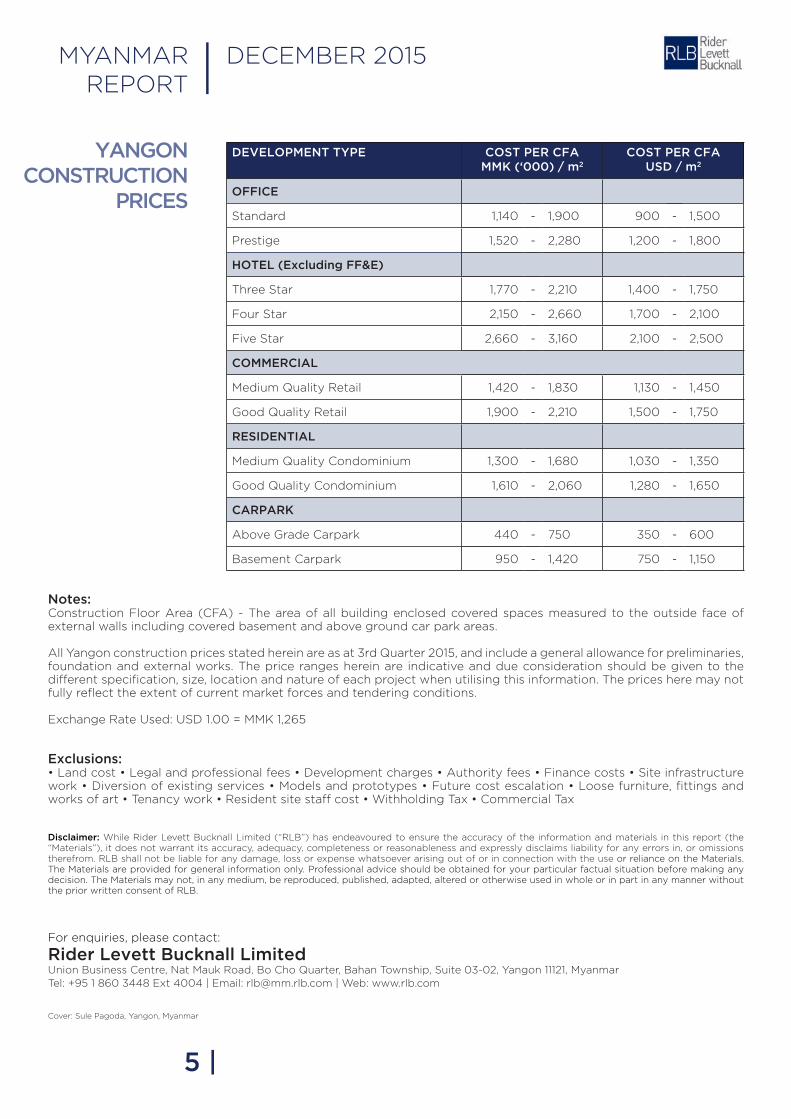

YANGON CONSTRUCTION

PRICES

5 |

DEvELOPMENT TYPE COST PER CFA MMK (‘000) / m2

COST PER CFA USD / m2

OFFICE

Standard 1,140 - 1,900 900 - 1,500

Prestige 1,520 - 2,280 1,200 - 1,800

HOTEL (Excluding FF&E)

Three Star 1,770 - 2,210 1,400 - 1,750

Four Star 2,150 - 2,660 1,700 - 2,100

Five Star 2,660 - 3,160 2,100 - 2,500

COMMERCIAL

Medium Quality Retail 1,420 - 1,830 1,130 - 1,450

Good Quality Retail 1,900 - 2,210 1,500 - 1,750

RESIDENTIAL

Medium Quality Condominium 1,300 - 1,680 1,030 - 1,350

Good Quality Condominium 1,610 - 2,060 1,280 - 1,650

CARPARK

Above Grade Carpark 440 - 750 350 - 600

Basement Carpark 950 - 1,420 750 - 1,150

Notes:Construction Floor Area (CFA) - The area of all building enclosed covered spaces measured to the outside face of external walls including covered basement and above ground car park areas.

All Yangon construction prices stated herein are as at 3rd Quarter 2015, and include a general allowance for preliminaries, foundation and external works. The price ranges herein are indicative and due consideration should be given to the different specification, size, location and nature of each project when utilising this information. The prices here may not fully reflect the extent of current market forces and tendering conditions.

Exchange Rate Used: USD 1.00 = MMK 1,265

Exclusions:• Land cost • Legal and professional fees • Development charges • Authority fees • Finance costs • Site infrastructure work • Diversion of existing services • Models and prototypes • Future cost escalation • Loose furniture, fittings and works of art • Tenancy work • Resident site staff cost • Withholding Tax • Commercial Tax

Disclaimer: While Rider Levett Bucknall Limited (“RLB”) has endeavoured to ensure the accuracy of the information and materials in this report (the “Materials”), it does not warrant its accuracy, adequacy, completeness or reasonableness and expressly disclaims liability for any errors in, or omissions therefrom. RLB shall not be liable for any damage, loss or expense whatsoever arising out of or in connection with the use or reliance on the Materials. The Materials are provided for general information only. Professional advice should be obtained for your particular factual situation before making any decision. The Materials may not, in any medium, be reproduced, published, adapted, altered or otherwise used in whole or in part in any manner without the prior written consent of RLB.

For enquiries, please contact:

Rider Levett Bucknall LimitedUnion Business Centre, Nat Mauk Road, Bo Cho Quarter, Bahan Township, Suite 03-02, Yangon 11121, MyanmarTel: +95 1 860 3448 Ext 4004 | Email: [email protected] | Web: www.rlb.com

Cover: Sule Pagoda, Yangon, Myanmar

MYANMARREPORT | DECEMBER 2015

OCEANIA

AUSTRALIAAdelaideBrisbaneCairnsCanberraDarwinGold CoastMelbourneNewcastleNorthern New South WalesPerthSunshine CoastSydneyTownsvilleWestern Sydney

NEW ZEALANDAucklandChristchurchHamiltonOtagoPalmerston NorthTaurangaWellington

EUROPE

UNITED KINGDOMBirchwoodBirmingham BristolLondonManchesterNewcastleSheffield Welwyn Garden CityWokingham

ASIA

SINGAPORESingapore

MALAYSIAKuala Lumpur

INDONESIAJakarta

vIETNAMHo Chi Minh City

MYANMARYangon

PHILIPPINESCebuDavaoManila

JAPANTokyo

SOUTH KOREASeoul

TAIWANTaiwan

CHINABeijingChengduChongqingDalianGuangzhouGuiyangHaikouHangzhouHong KongMacauNanjingQingdaoShanghaiShenyangShenzhenTianjinWuhanWuxiXian

AMERICA

USABostonChicagoDenverGuamHiloHonoluluKennewickLas VegasLos AngelesMauiNew YorkPhoenixPortlandSan FranciscoSeattleTucsonWaikoloaWashington DC

CANADACalgary

CARIBBEANBarbadosCayman Islands

AFRICA

SOUTH AFRICACape TownJohannesburgPretoriaBotswanaMauritiusMozambique

RLB GLOBAL OFFICES

MIDDLE EAST

MIDDLE EASTAbu DhabiDoha DubaiMuscatRiyadh

RLB | EURO ALLIANCEAustriaBelgiumBulgariaCroatiaCyprusCzech RepublicDenmarkFinlandFranceGermany GreeceHungaryIrelandItalyLuxembourgMoldovaMontenegroNetherlandsNorwayPolandPortugalRomaniaRussiaSerbiaSlovakiaSpainSwedenSwitzerlandTurkeyUkraine

rlb.com