Embed Size (px)

Citation preview

Myanmar

Legislation, Tax

and Accounting

Systems

12 July 2013

Wirat Sirikajornkij

Disclaimer

This brief presentation on Myanmar tax and structuring investments into Myanmar

is intended to provide an introduction to some of the key issues and

considerations relevant to potential investors.

The information is intended for general information purposes only and should not

be used for decision making purposes. The applicability of the information to

specific situations should be determined through consultation with professional

advisors, including any updates to Myanmar tax legislation which is a regular

event.

July 2013 Investment in Myanmar © 2013 KPMG Phoomchai Tax Ltd. a Myanmar limited liability company and a member firm of the KPMG network of independent member firms affiliated

with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

A brief introduction to Investment in Myanmar

Foreign Direct Investment

Key Legislations:

Myanmar Foreign Investment Law, 2012 (MFIL)

• Foreign Investment Rules

• Myanmar Investment Commission Notification No.

1/2013 (Notification 1/2013)

Myanmar Companies Act, 1913 (MCA)

Types of Incorporation/ Registration

100% owned foreign subsidiaries

Joint Venture companies with Myanmar citizens

Branch of Foreign Company

Representative Offices

Under Notification 1/2013, the types of allowed and

prohibited economic activities and forms of entities

relevant to those activities are stipulated.

Such Notifications and MFIL remain under the close

interpretation of the Myanmar government authorities

and a foreign investment proposal will be considered on

a case by case basis.

July 2013 Investment in Myanmar © 2013 KPMG Phoomchai Tax Ltd. a Myanmar limited liability company and a member firm of the KPMG network of independent member firms affiliated

with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Corporate Income Tax

• Tax Residency based on registration.

• Resident companies subject to tax on world wide source

income – except companies registered under the MFIL which

are subject to tax on Myanmar source income only.

• Corporate Income Tax Rates:

• Resident companies – 25%

• Branch with incentives under the MFIL – 25%

• Branches without MFIL incentives – 35%

• Thus, Branches, without tax incentives are taxed 10% more

than Myanmar companies.

• Capital Gains Tax rates:

• Resident tax payers – 10%

• Non-resident tax payers – 40%

• Oil and gas industry – 40 to 50%

• Withholding Tax on transactions with Non-Residents:

• Dividends – 0%

• Interest – 15%

• Royalties – 20%

• Services and goods – 3.5%

July 2013 Investment in Myanmar © 2013 KPMG Phoomchai Tax Ltd. a Myanmar limited liability company and a member firm of the KPMG network of independent member firms affiliated

with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Double Tax Agreements

Myanmar has entered DTA’s with

• United Kingdom

• Singapore

• Malaysia

• Vietnam

• Thailand

• India

• South Korea

• Laos

• Bangladesh - Negotiated, not yet in force

• Indonesia – Negotiated, note yet in force

8 DTS’s out of 10 above, i.e. United Kingdom,

Singapore, Malaysia, Thailand, India, Vietnam,

South Korea and Laos have already been ratified

and are enforceable.

Recommend verifying DTA application before

arranging structures.

July 2013

Investment in Myanmar © 2013 KPMG Phoomchai Tax Ltd. a Myanmar limited liability company and a member firm of the KPMG network of independent member firms affiliated

with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

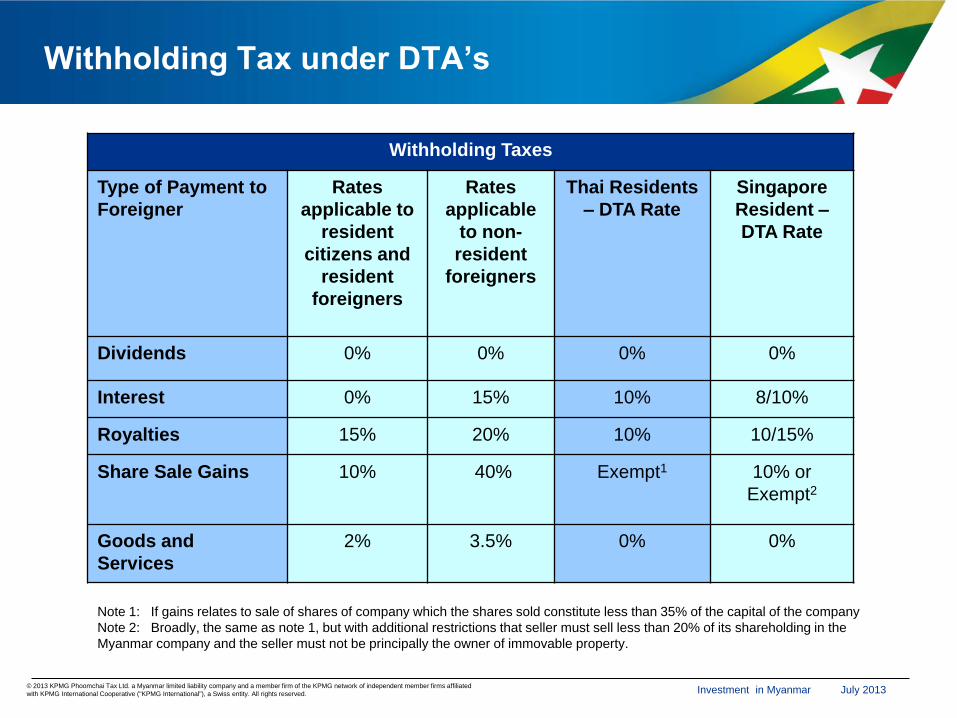

Withholding Tax under DTA’s

Withholding Taxes

Type of Payment to

Foreigner

Rates

applicable to

resident

citizens and

resident

foreigners

Rates

applicable

to non-

resident

foreigners

Thai Residents

– DTA Rate

Singapore

Resident –

DTA Rate

Dividends 0% 0% 0% 0%

Interest 0% 15% 10% 8/10%

Royalties 15% 20% 10% 10/15%

Share Sale Gains 10% 40% Exempt1 10% or

Exempt2

Goods and

Services

2% 3.5% 0% 0%

Note 1: If gains relates to sale of shares of company which the shares sold constitute less than 35% of the capital of the company

Note 2: Broadly, the same as note 1, but with additional restrictions that seller must sell less than 20% of its shareholding in the

Myanmar company and the seller must not be principally the owner of immovable property.

July 2013

Investment in Myanmar © 2013 KPMG Phoomchai Tax Ltd. a Myanmar limited liability company and a member firm of the KPMG network of independent member firms affiliated

with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Tax Incentives

Companies registered under the Myanmar Foreign

Investment Law can be granted a number of

incentives, including:

• 5 year corporate income tax holiday from the

month of commencement the commercial

operation (normally, 25%)

• CIT exemption on profits that are reinvested

within one year

• Accelerated depreciation

• Reduction of 50% of CIT for export income

generating activities (following a tax holiday

period)

• 3 years carry forward losses (no carry back)

• Exemption from customs duties for machinery

• Exemption from customs duties on raw

materials

The benefits are approved by the Myanmar

Investment Commission (MIC) upon application.

July 2013 Investment in Myanmar

© 2013 KPMG Phoomchai Tax Ltd. a Myanmar limited liability company and a member firm of the KPMG network of independent member firms affiliated

with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Commercial Tax

Commercial Tax

• Turnover based

• Certain mechanisms to prevent aggregation

• Also applies to non-resident entities

• Changes from April 2012

• Includes new reference to services

• little guidance from tax authorities

July 2013

Investment in Myanmar © 2013 KPMG Phoomchai Tax Ltd. a Myanmar limited liability company and a member firm of the KPMG network of independent member firms affiliated

with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

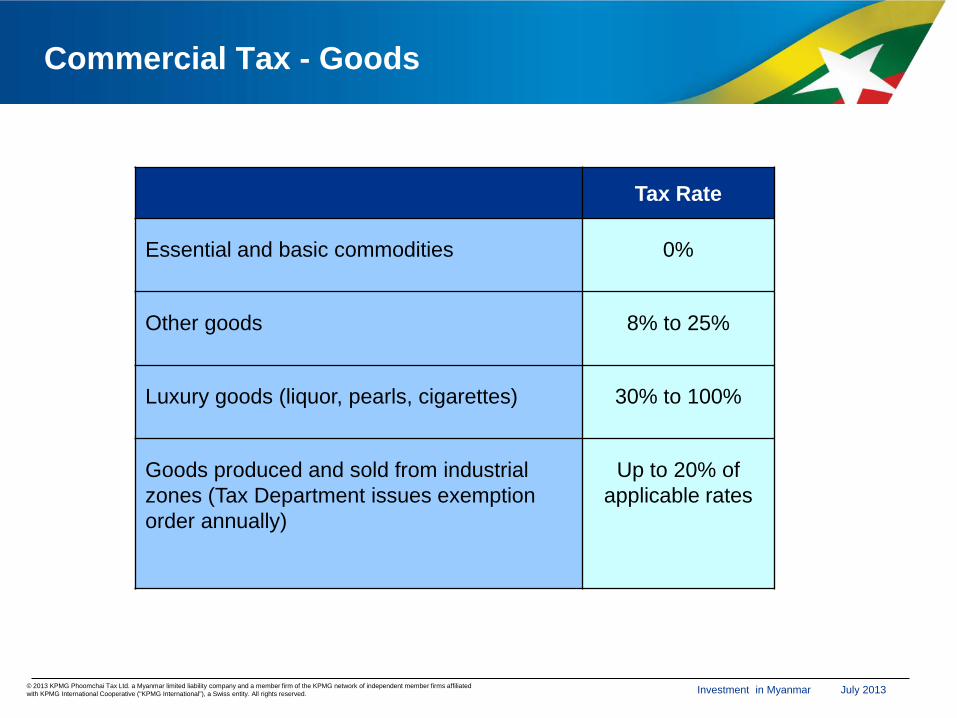

Commercial Tax - Goods

Tax Rate

Essential and basic commodities

0%

Other goods

8% to 25%

Luxury goods (liquor, pearls, cigarettes)

30% to 100%

Goods produced and sold from industrial

zones (Tax Department issues exemption

order annually)

Up to 20% of

applicable rates

July 2013

Investment in Myanmar © 2013 KPMG Phoomchai Tax Ltd. a Myanmar limited liability company and a member firm of the KPMG network of independent member firms affiliated

with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

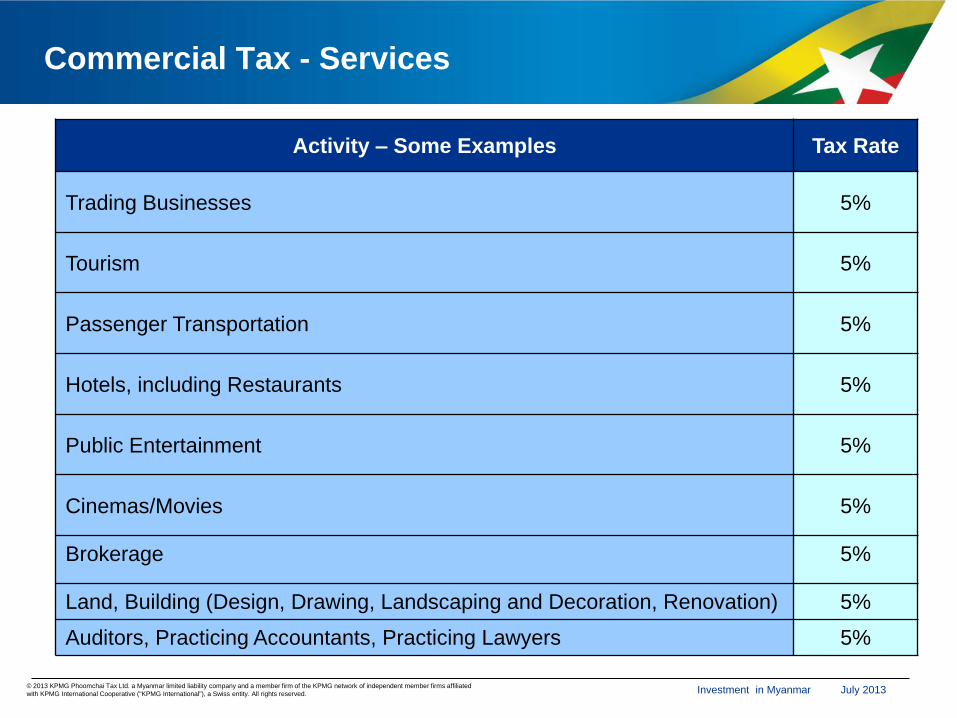

Commercial Tax - Services

Activity – Some Examples

Tax Rate

Trading Businesses

5%

Tourism

5%

Passenger Transportation

5%

Hotels, including Restaurants

5%

Public Entertainment

5%

Cinemas/Movies

5%

Brokerage 5%

Land, Building (Design, Drawing, Landscaping and Decoration, Renovation) 5%

Auditors, Practicing Accountants, Practicing Lawyers 5%

July 2013

Investment in Myanmar © 2013 KPMG Phoomchai Tax Ltd. a Myanmar limited liability company and a member firm of the KPMG network of independent member firms affiliated

with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Taxation of Individuals

• Individuals are tax resident in Myanmar if they stay

for 183 days – or more – during the fiscal year.

• Resident taxpayers subject to tax on world-wide

source income.

• Non-residents subject to tax on Myanmar source

income.

• Tax rates - Salaries:

• Resident Foreigner - 1% to 20% (effectively, 20%)

• Non-resident – 35%

• Social security contribution

• Applicable if 5 employees or more

• 4% (employer of 1.5% + employee of 2.5%) of

salary or wages

•Cap amount: Employer of MMK774/ Employee of

MMK465 per month

July 2013

Investment in Myanmar © 2013 KPMG Phoomchai Tax Ltd. a Myanmar limited liability company and a member firm of the KPMG network of independent member firms affiliated

with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Taxation of non residents

Non Resident company

• Settled WHT represents final tax payments

• If WHT not settled – tax liability?

July 2013

Investment in Myanmar © 2013 KPMG Phoomchai Tax Ltd. a Myanmar limited liability company and a member firm of the KPMG network of independent member firms affiliated

with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Repatriation

July 2013

Investment in Myanmar © 2013 KPMG Phoomchai Tax Ltd. a Myanmar limited liability company and a member firm of the KPMG network of independent member firms affiliated

with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Right to transfer Foreign Currency:

• MFIL provides investors the right to

transfer foreign currencies out of

Myanmar

• Transfer is through approved banks;

• Based on stipulated exchange rate;

• The following can be transferred:

i) Net profit after deducting all taxes,

relevant funds from annual profit

(Businesses)

ii) legitimate balance after taxes and

living expenses (Persons)

Case Study

Structures Illustration

Structuring considerations:

Equity

• Only certain economic activities is prohibited from

having 100 per cent foreign ownership, i.e. paper

manufacturing, tourism etc.

• Transfer of shares from local citizen to foreigner is

still prohibited

• Transfer of shares between foreigner to foreigner

requires an approval from the Myanmar

Investment Commission

Loans

• Need approval by Central Bank

• Interest cap: i) domestic lending – 13 percent; ii)

offshore lending – market rates

Financial Instruments

• Complex financial instruments not well known

• Legitimate? Have to consider on a case by case

basis

Management fee structures

• Indirect allocations not approved for tax

deduction?

July 2013 Investment in Myanmar © 2013 KPMG Phoomchai Tax Ltd. a Myanmar limited liability company and a member firm of the KPMG network of independent member firms affiliated

with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Offshore Holding structures

Popular Holding Regimes for investments into

Myanmar are:

• Singapore

•Thailand

Easy to structure tax efficient repatriation of

dividends

• No WHT on distributed dividends from

Myanmar

• Utilize exemption in holding regime

July 2013 Investment in Myanmar © 2013 KPMG Phoomchai Tax Ltd. a Myanmar limited liability company and a member firm of the KPMG network of independent member firms affiliated

with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Case Study – Trading Business

Key Concept:

Foreigner is prohibited from undertaking retail business in

Myanmar.

Wholesale Business?

• Currently allowed under the new MFIL on the proviso

that a recommendation from the Ministry of Commerce

is obtained.

Any solution for retail company to be able to invest

in Myanmar?

• Most common form: licensing agreement,

distributorship agreement; and

• Setting up a service company to provide marketing,

after-sale services to local distributors and customers.

July 2013

Investment in Myanmar © 2013 KPMG Phoomchai Tax Ltd. a Myanmar limited liability company and a member firm of the KPMG network of independent member firms affiliated

with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

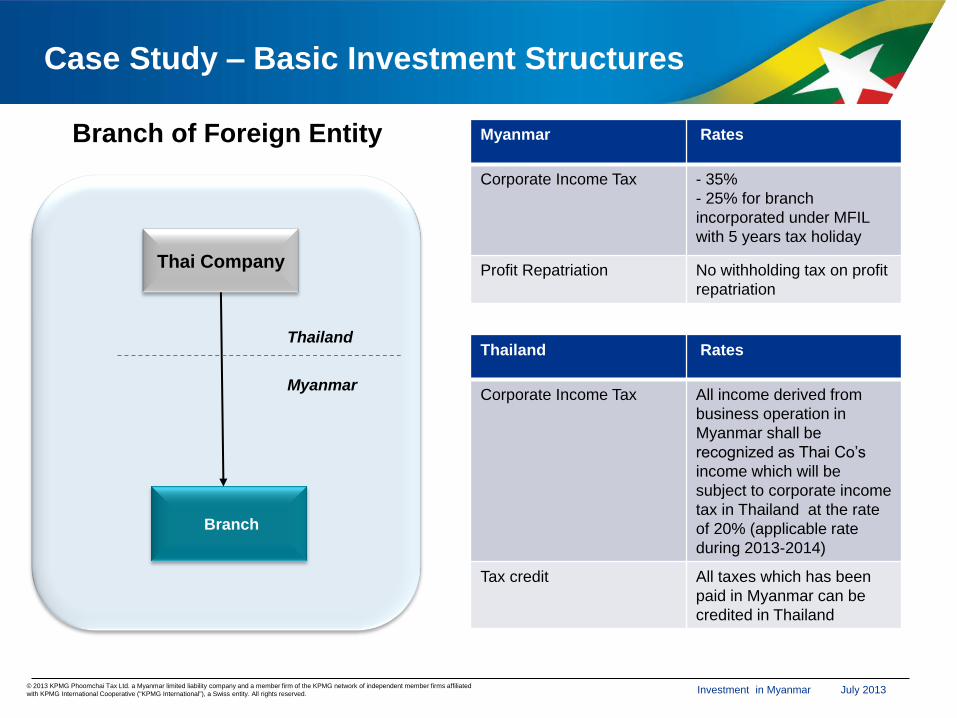

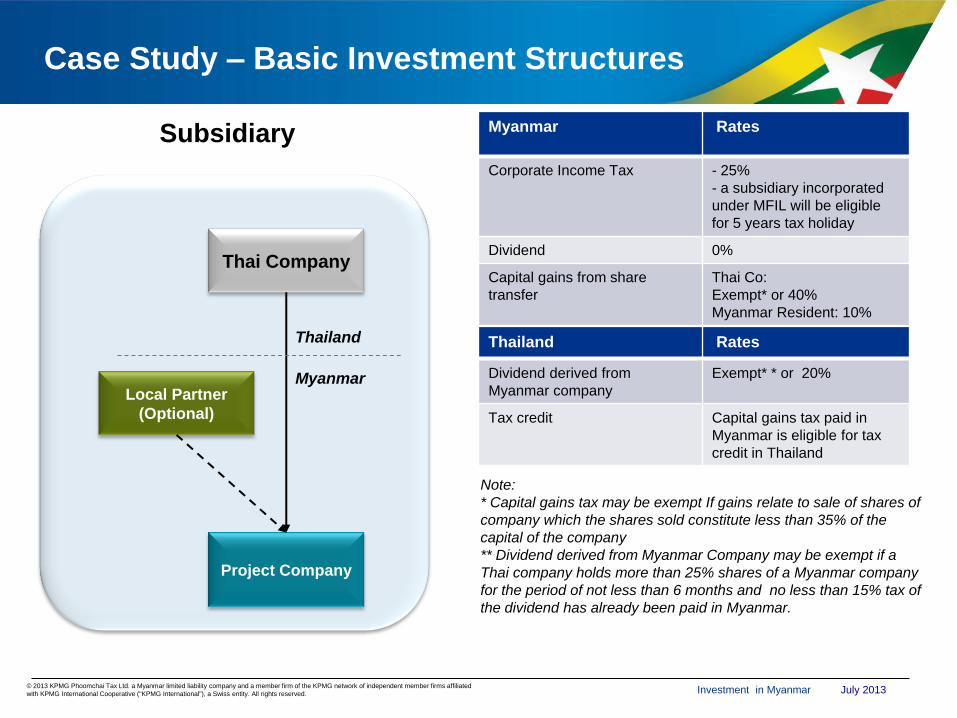

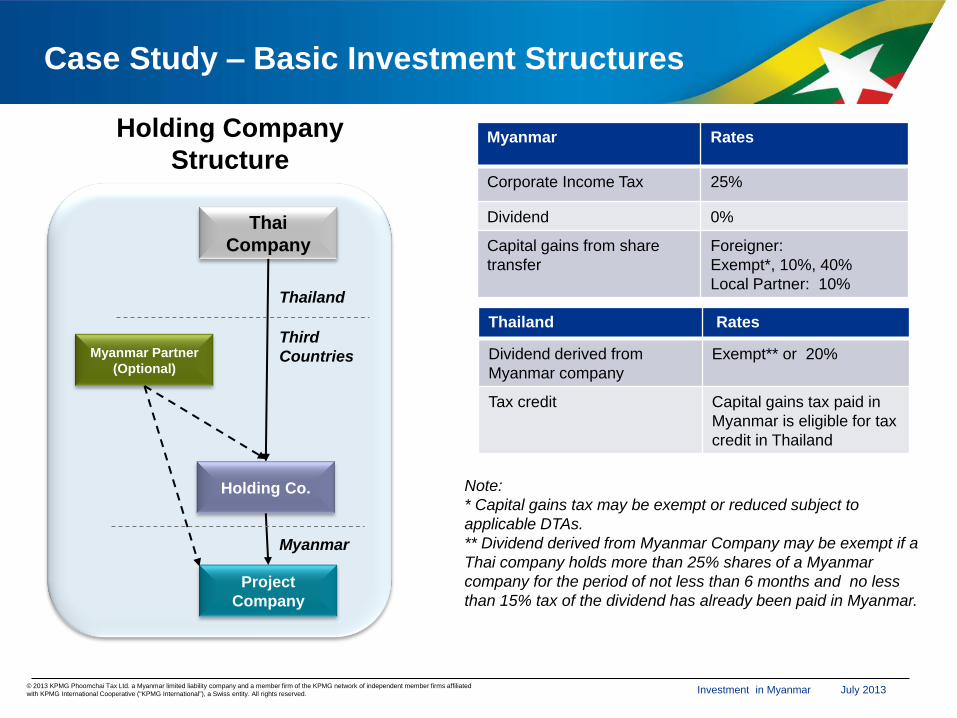

Case Study – Basic Investment Structures

Most common forms:

Branch of foreign entities

Subsidiary

Holding Company Structure

July 2013 Investment in Myanmar © 2013 KPMG Phoomchai Tax Ltd. a Myanmar limited liability company and a member firm of the KPMG network of independent member firms affiliated

with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Case Study – Basic Investment Structures

July 2013

Investment in Myanmar © 2013 KPMG Phoomchai Tax Ltd. a Myanmar limited liability company and a member firm of the KPMG network of independent member firms affiliated

with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Thai Company

Branch

Myanmar Rates

Corporate Income Tax - 35%

- 25% for branch

incorporated under MFIL

with 5 years tax holiday

Profit Repatriation No withholding tax on profit

repatriation

Branch of Foreign Entity

Thailand

Myanmar

Thailand Rates

Corporate Income Tax All income derived from

business operation in

Myanmar shall be

recognized as Thai Co’s

income which will be

subject to corporate income

tax in Thailand at the rate

of 20% (applicable rate

during 2013-2014)

Tax credit All taxes which has been

paid in Myanmar can be

credited in Thailand

Case Study – Basic Investment Structures

July 2013 Investment in Myanmar © 2013 KPMG Phoomchai Tax Ltd. a Myanmar limited liability company and a member firm of the KPMG network of independent member firms affiliated

with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Thai Company

Project Company

Local Partner

(Optional)

Myanmar Rates

Corporate Income Tax - 25%

- a subsidiary incorporated

under MFIL will be eligible

for 5 years tax holiday

Dividend 0%

Capital gains from share

transfer

Thai Co:

Exempt* or 40%

Myanmar Resident: 10%

Subsidiary

Thailand

Myanmar

Thailand Rates

Dividend derived from

Myanmar company

Exempt* * or 20%

Tax credit Capital gains tax paid in

Myanmar is eligible for tax

credit in Thailand

Note:

* Capital gains tax may be exempt If gains relate to sale of shares of

company which the shares sold constitute less than 35% of the

capital of the company

** Dividend derived from Myanmar Company may be exempt if a

Thai company holds more than 25% shares of a Myanmar company

for the period of not less than 6 months and no less than 15% tax of

the dividend has already been paid in Myanmar.

Case Study – Basic Investment Structures

July 2013

Investment in Myanmar © 2013 KPMG Phoomchai Tax Ltd. a Myanmar limited liability company and a member firm of the KPMG network of independent member firms affiliated

with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Myanmar Rates

Corporate Income Tax 25%

Dividend 0%

Capital gains from share

transfer

Foreigner:

Exempt*, 10%, 40%

Local Partner: 10%

Holding Company

Structure

Thai

Company

Project

Company

Thailand

Third

Countries Myanmar Partner

(Optional)

Holding Co.

Myanmar

Thailand Rates

Dividend derived from

Myanmar company

Exempt** or 20%

Tax credit Capital gains tax paid in

Myanmar is eligible for tax

credit in Thailand

Note:

* Capital gains tax may be exempt or reduced subject to

applicable DTAs.

** Dividend derived from Myanmar Company may be exempt if a

Thai company holds more than 25% shares of a Myanmar

company for the period of not less than 6 months and no less

than 15% tax of the dividend has already been paid in Myanmar.

Accounting System

Corporate compliance

Accounting/Finance for Companies

• Financial Statements

• The Myanmar Accounting Standards, 2004 based very

closely on International Accounting Standards.

• Companies must maintain proper books of accounts

which are required to be kept at the registered office of

the company.

• Audit Requirements

• It is required that the annual accounts of a company to

be audited.

• Fiscal year/ Currency

• The fiscal year in Myanmar is 1 April to 31 March.

• Myanmar Kyat (MMK)

July 2013 Investment in Myanmar © 2013 KPMG Phoomchai Tax Ltd. a Myanmar limited liability company and a member firm of the KPMG network of independent member firms affiliated

with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Sample Tax Return

July 2013 Investment in Myanmar © 2013 KPMG Phoomchai Tax Ltd. a Myanmar limited liability company and a member firm of the KPMG network of independent member firms affiliated

with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

• Corporate Income Tax Return

• Corporate Income Tax Slip

• Tax Demand Note (Myanmar)

• Tax Receipts (Myanmar)

KPMG in Myanmar

KPMG first of Big 4 to re-open office in Yangon

• Mix of experienced locals and expatriates

• Backed by KPMG Thailand and KPMG

Singapore – in addition the rest of our network.

• Initially to provide Tax and Advisory services

(not audit services at this time)

KPMG’s “Investment in Myanmar” available!

in our website at www.kpmg.com/mm

July 2013 Investment in Myanmar © 2013 KPMG Phoomchai Tax Ltd. a Myanmar limited liability company and a member firm of the KPMG network of independent member firms affiliated

with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved.

Thank you

Wirat Sirikajornkij

Partner, Tax

KPMG Phoomchai Tax Ltd.

Tel: +66 2 677 2423

Email: [email protected]

![Emerging Growth Company Practice€¦ · for reading the legislation or accounting standards themselves, ... The accompanying notes are an integral part of these [consolidated] financial](https://img.pdfslide.us/doc/110x75/5f0bf6587e708231d4331442/emerging-growth-company-practice-for-reading-the-legislation-or-accounting-standards.jpg)

![Legislation Review Committee · Parliament. Legislative Assembly. Legislation Review Committee Legislation Review Digest, Legislation Review Committee, Parliament NSW [Sydney, NSW]:](https://img.pdfslide.us/doc/110x75/5f9c6bc6de302b4245453c3b/legislation-review-committee-parliament-legislative-assembly-legislation-review.jpg)