Embed Size (px)

Citation preview

General Literature Strategy definitions Data Strategies

Mutual Funds’ Credit Default Swap Strategies

Tim AdamHumboldt University

Andre GuettlerUlm University

Li MaHumboldt University

preliminaryCRC649 Conference

07.2014 1/25

General Literature Strategy definitions Data Strategies

Bill "Bond King" Gross...

Source: http://assets.nerdwallet.com/blog/investing/files/2012/08/billgross.jpg

CRC649 Conference

07.2014 2/25

General Literature Strategy definitions Data Strategies

A brief introduction of CDS

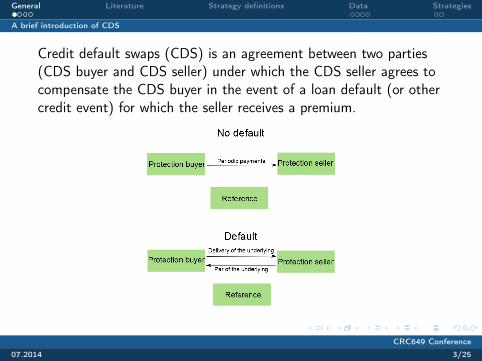

Credit default swaps (CDS) is an agreement between two parties(CDS buyer and CDS seller) under which the CDS seller agrees tocompensate the CDS buyer in the event of a loan default (or othercredit event) for which the seller receives a premium.

CRC649 Conference

07.2014 3/25

General Literature Strategy definitions Data Strategies

A brief introduction of CDS

• CDS are private contracts and are not traded on anyexchanges1. But investment companies (e.g. mutual funds)are required to disclose their derivatives usage, including CDSpositions, to the SEC quarterly.(Investment Bank Act 1940).

• Naked CDS positions are always allowed except for naked longCDS positions written on EU sovereign debt.

• Market size: By the end of 2007, the outstanding CDSamount was $62 trillion, more than the total notional of bondson this planet. It has fallen to $29 trillion by the end of 2011.

1This is changing due to recent regulation changes, including central clearingand the introduction of swap execution facilities.

CRC649 Conference

07.2014 4/25

General Literature Strategy definitions Data Strategies

A brief introduction of CDS

Why does it matter?• Short a CDS generates high implicit leverage at low costs.• Long CDS positions are (still) not regulated in the U.S.• AIG, Bear Stearns, Oppenheimer Champion Income Fundsuffered from significant losses trading CDS during the GFC.

CRC649 Conference

07.2014 5/25

General Literature Strategy definitions Data Strategies

A brief introduction of CDS

In a complete market, CDS would be redundant since it can bereplaced by a cash flow equivalent position in the underlying bondand a risk free asset.• Selling a CDS and investing the notional amount intoTreasuries would allow synthesizing a bond.

But:• Transaction costs, Garleanu and Redersen(2011), Shen, Yanand Zhang(2013)

• Liquidity, Oehmke and Zawadowski(2014)• Risk transfer, Zawadowski(2013)• Arbitrage, Fontana(2011), Bai and Collin-Dufresne(2010)

CRC649 Conference

07.2014 6/25

General Literature Strategy definitions Data Strategies

CDS Strategies in general:• Oehmke and Zawadowski(2013)

CDS usage by other financial institutions:• Mahieu and Xu (2007), Minton, Stulz, and Williamson (2009),Hirtle (2009), Van Ofwegen, Verschoor, and Zwinkels (2012)

• Aragon and Martin (2012)Mutual funds’ derivative usage:• Koski and Pontiff (1999); Johnson and Yu (2004); Marin andRangel (2006)

• Cici and Palacios (2010)First paper to examine credit default swap strategies at eachindividual position level.

CRC649 Conference

07.2014 7/25

General Literature Strategy definitions Data Strategies

ConceptsNegative basis trading• Basis

• Spread difference on the same asset between cash andderivatives market

• CDS basis• The difference in spread between CDS and underlying asset,

usually bonds, for the same debt issuer and with similarmaturities.

• CDS basis = CDS spread - bond spread• Negative basis trade

• Given the existence of negative basis, explore the difference bypurchasing the CDS and bond simultaneously.

• The negative basis will eventually narrow near maturity ofbonds. The investor can lock in a profit.

CRC649 Conference

07.2014 8/25

General Literature Strategy definitions Data Strategies

Definition

Negative basis trading• ∆bond notional ≈ ∆long CDS notional > 0 and CDS basist <

0• Entering into (or increasing the amount of) long Sname CDS

positions and bond positions at the same period.• The respective CDS basis is less than 0 basis point.

CRC649 Conference

07.2014 9/25

General Literature Strategy definitions Data Strategies

Quasi negative basis trade with positive basis• ∆bond notional ≈ ∆long CDS notional > 0 and CDS basist >

0• Entering into (or increasing the amount of) long Sname CDS

positions and bond positions at the same period.• The respective CDS basis is more than 0 basis point.• The strategy is plausible if the trader expects the basis to

become even wider.

CRC649 Conference

07.2014 10/25

General Literature Strategy definitions Data Strategies

Hedging• ∆long CDS notional > 0 and bond notionalt 6=

0 and bond notionalt−1 6= 0 and bond notionalt <=bond notionalt−1

• There is an increase in long Sname CDS position, and therespective bond position remains unchanged or is decreasing.• Bond position exists in both t and t-1.• If the increase of long Sname CDS positions makes the CDS

notional to pass through the notional of the respective bond,then the fund is over hedging. Over hedging can be due to thefact that funds do duration matching.

CRC649 Conference

07.2014 11/25

General Literature Strategy definitions Data Strategies

Naked long CDS• ∆long CDS notional > 0 and bond notionalt == 0• The increase of long Sname CDS positions, and during which

period there is no underlying in the portfolio holdings.

CRC649 Conference

07.2014 12/25

General Literature Strategy definitions Data Strategies

Synthetic bond• ∆short CDS notional < 0 and basist > 0• There is an increase in short Sname CDS positions, and the

CDS basis is positive.

CRC649 Conference

07.2014 13/25

General Literature Strategy definitions Data Strategies

Outright CDS• ∆short CDS notional < 0 and synthetict ==

0 and bond notionalt == 0• The increase of short Sname CDS positions that are not

synthetic bonds, and during which period there is nounderlying in the portfolio holdings.

CRC649 Conference

07.2014 14/25

General Literature Strategy definitions Data Strategies

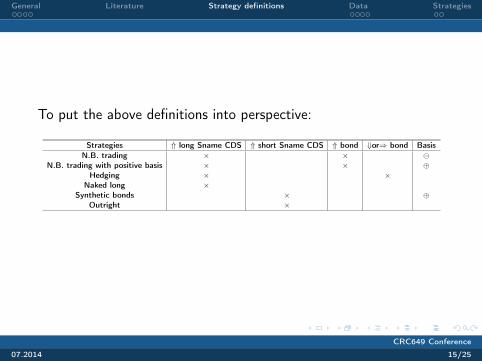

To put the above definitions into perspective:

Strategies ⇑ long Sname CDS ⇑ short Sname CDS ⇑ bond ⇓or⇒ bond BasisN.B. trading × ×

N.B. trading with positive basis × × ⊕Hedging × ×

Naked long ×Synthetic bonds × ⊕

Outright ×

CRC649 Conference

07.2014 15/25

General Literature Strategy definitions Data Strategies

Data source

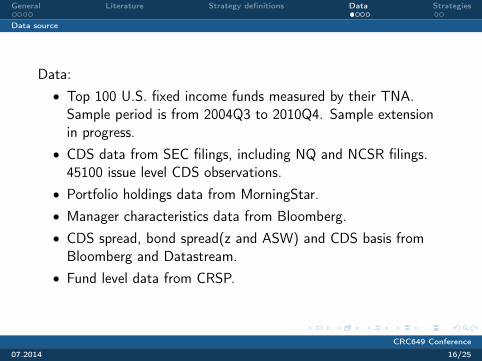

Data:• Top 100 U.S. fixed income funds measured by their TNA.Sample period is from 2004Q3 to 2010Q4. Sample extensionin progress.

• CDS data from SEC filings, including NQ and NCSR filings.45100 issue level CDS observations.

• Portfolio holdings data from MorningStar.• Manager characteristics data from Bloomberg.• CDS spread, bond spread(z and ASW) and CDS basis fromBloomberg and Datastream.

• Fund level data from CRSP.

CRC649 Conference

07.2014 16/25

General Literature Strategy definitions Data Strategies

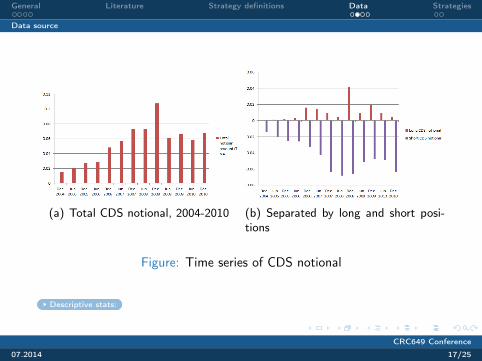

Data source

(a) Total CDS notional, 2004-2010 (b) Separated by long and short posi-tions

Figure: Time series of CDS notional

Descriptive stats:

CRC649 Conference

07.2014 17/25

General Literature Strategy definitions Data Strategies

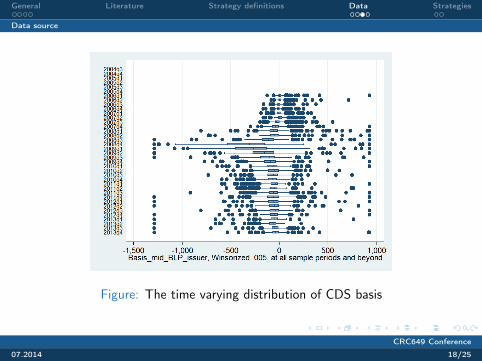

Data source

Figure: The time varying distribution of CDS basis

CRC649 Conference

07.2014 18/25

General Literature Strategy definitions Data Strategies

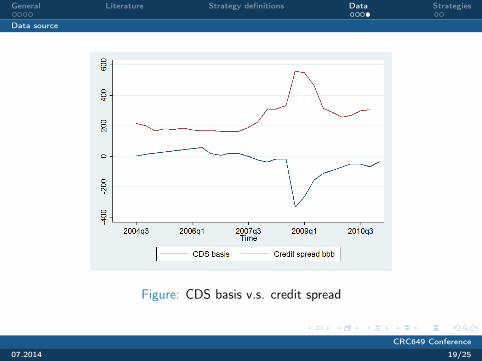

Data source

Figure: CDS basis v.s. credit spread

CRC649 Conference

07.2014 19/25

General Literature Strategy definitions Data Strategies

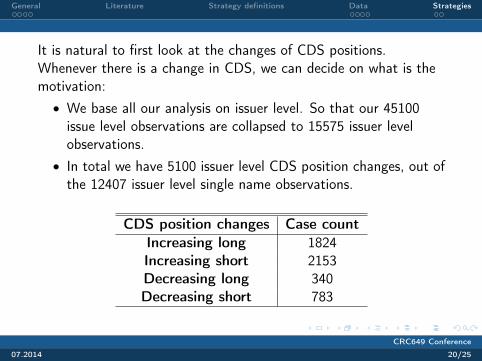

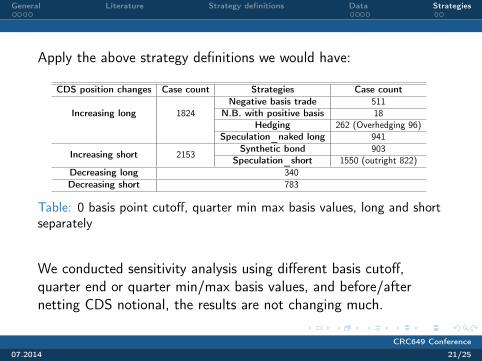

It is natural to first look at the changes of CDS positions.Whenever there is a change in CDS, we can decide on what is themotivation:• We base all our analysis on issuer level. So that our 45100issue level observations are collapsed to 15575 issuer levelobservations.

• In total we have 5100 issuer level CDS position changes, out ofthe 12407 issuer level single name observations.

CDS position changes Case countIncreasing long 1824Increasing short 2153Decreasing long 340Decreasing short 783

CRC649 Conference

07.2014 20/25

General Literature Strategy definitions Data Strategies

Apply the above strategy definitions we would have:

CDS position changes Case count Strategies Case count

Increasing long 1824Negative basis trade 511

N.B. with positive basis 18Hedging 262 (Overhedging 96)

Speculation_naked long 941

Increasing short 2153Synthetic bond 903

Speculation_short 1550 (outright 822)Decreasing long 340Decreasing short 783

Table: 0 basis point cutoff, quarter min max basis values, long and shortseparately

We conducted sensitivity analysis using different basis cutoff,quarter end or quarter min/max basis values, and before/afternetting CDS notional, the results are not changing much.

CRC649 Conference

07.2014 21/25

General Literature Strategy definitions Data Strategies

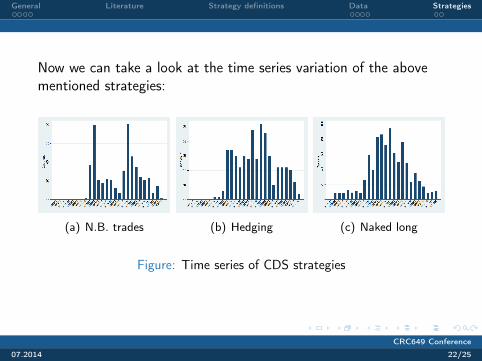

Now we can take a look at the time series variation of the abovementioned strategies:

(a) N.B. trades (b) Hedging (c) Naked long

Figure: Time series of CDS strategies

CRC649 Conference

07.2014 22/25

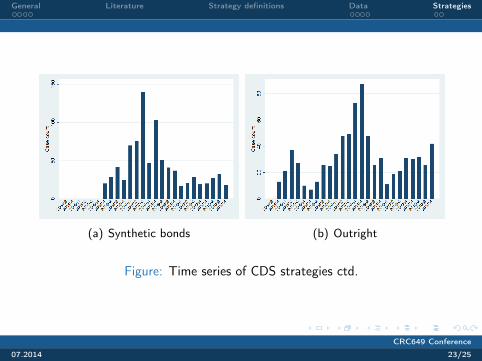

General Literature Strategy definitions Data Strategies

(a) Synthetic bonds (b) Outright

Figure: Time series of CDS strategies ctd.

CRC649 Conference

07.2014 23/25

General Literature Strategy definitions Data Strategies

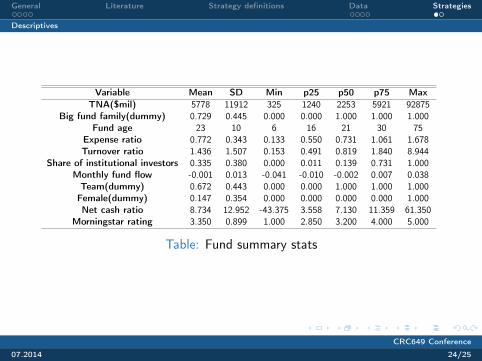

Descriptives

Variable Mean SD Min p25 p50 p75 MaxTNA($mil) 5778 11912 325 1240 2253 5921 92875

Big fund family(dummy) 0.729 0.445 0.000 0.000 1.000 1.000 1.000Fund age 23 10 6 16 21 30 75

Expense ratio 0.772 0.343 0.133 0.550 0.731 1.061 1.678Turnover ratio 1.436 1.507 0.153 0.491 0.819 1.840 8.944

Share of institutional investors 0.335 0.380 0.000 0.011 0.139 0.731 1.000Monthly fund flow -0.001 0.013 -0.041 -0.010 -0.002 0.007 0.038Team(dummy) 0.672 0.443 0.000 0.000 1.000 1.000 1.000Female(dummy) 0.147 0.354 0.000 0.000 0.000 0.000 1.000Net cash ratio 8.734 12.952 -43.375 3.558 7.130 11.359 61.350

Morningstar rating 3.350 0.899 1.000 2.850 3.200 4.000 5.000

Table: Fund summary stats

CRC649 Conference

07.2014 24/25

General Literature Strategy definitions Data Strategies

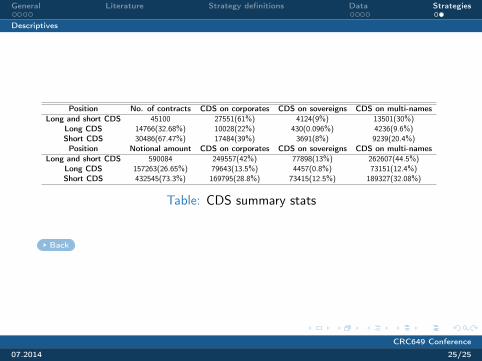

Descriptives

Position No. of contracts CDS on corporates CDS on sovereigns CDS on multi-namesLong and short CDS 45100 27551(61%) 4124(9%) 13501(30%)

Long CDS 14766(32.68%) 10028(22%) 430(0.096%) 4236(9.6%)Short CDS 30486(67.47%) 17484(39%) 3691(8%) 9239(20.4%)Position Notional amount CDS on corporates CDS on sovereigns CDS on multi-names

Long and short CDS 590084 249557(42%) 77898(13%) 262607(44.5%)Long CDS 157263(26.65%) 79643(13.5%) 4457(0.8%) 73151(12.4%)Short CDS 432545(73.3%) 169795(28.8%) 73415(12.5%) 189327(32.08%)

Table: CDS summary stats

Back

CRC649 Conference

07.2014 25/25