Embed Size (px)

Citation preview

8/9/2019 Mutual Fund Report Final

http://slidepdf.com/reader/full/mutual-fund-report-final 1/66

1

A PROJECT REPORT

ON

A STUDY ON AWARENESS OF PEOPLE ABOUT

MUTUAL FUNDS IN VISAKHAPATNAM

Submitted by

J.R.A. SANTOSH

In partial fulfillment for the award of the degree

Of MASTERS IN BUSINESS ADMINISTRATION (IBF)

2009-11

Submitted to

DR. VIJAY DAS (Functional Guide)

DR. RADHA RAGURAMAPATRUNI (Industrial Guide)

GITAM INSTITUTE OF INTERNATIONAL BUSINESS

GITAM UNIVERSITY: VISHAKAPATNAM

8/9/2019 Mutual Fund Report Final

http://slidepdf.com/reader/full/mutual-fund-report-final 2/66

2

DECLARATION

I hereby declare that this summer internship project report entitled ³A study on awareness of

people about Mutual funds in Visakhapatnam´ submitted in the partial fulfillment of the

requirements of the award of the Master Degree in Business Administration, of GITAM Institute

of International Business, Visakhapatnam, Andhra Pradesh is a bonafide record of the project

work carried out by me during the period of eight weeks from 21 st April 2010 to 20th June 2010

under the guidance of Mr.Kumar (Relationship Manager) at ICICI Prudential Asset Management

Company. The report is thoroughly for education purpose only and I also assure that no part of

this work has been presented earlier in for any degree or similar awards from any other

universities.

Date: 26-07-2010

Place: Visakhapatanam

J.R.A. SANTOSH

MBA (IBF)

GITAM Institute of International Business.

8/9/2019 Mutual Fund Report Final

http://slidepdf.com/reader/full/mutual-fund-report-final 3/66

3

ACKNOWLEDGEMENT

I avail this opportunity to express my profound sense of sincere and deep gratitude to

many people who are responsible for the knowledge and experience I have gained during the

internship programme.

My heartful thanks to the industrial and functional guides Dr. Vijay Das, Professor and

Dr. Radha Raguramapatruni, Professor, GITAM Institute of International Business,

Visakhapatnam, for keeping the faith in me by being my Guide and providing me with the

valuable guidance and suggestions throughout my project.

I have great pleasure in expressing my deep sense of gratitude to guide Mr. Kumar

(Relationship Manager, ICICI Prudential Asset Management Company, Vishakapatnam),

I would like to express a special word of thanks to each and every division and the staff

of the Vijay Home Appliances ltd. for providing all the required information and the facilities for

the successful completion of my project. I bow down to my family and my well wishers for the

care, moral support and the encouragement that they have given me, which gave me the strength

and courage in reaching to the successful completion of this project.

Above all, I thank the ALMIGHTY GOD without whose blessings and grace nothing

would have been possible.

J.R.A.SANTOSH

8/9/2019 Mutual Fund Report Final

http://slidepdf.com/reader/full/mutual-fund-report-final 4/66

4

EXECUTIVE SUMMARY

In few years Mutual Fund has emerged as a tool for ensuring one¶s financial well being. Mutual

Funds have not only contributed to the India growth story but have also helped families tap into

the success of Indian Industry. As information and awareness is rising more and more people are

enjoying the benefits of investing in mutual funds. The main reason the number of retail mutual

fund investors remains small is that nine in ten people with incomes in India do not know that

mutual funds exist. But once people are aware of mutual fund investment opportunities, the

number who decide to invest in mutual funds increases to as many as one in five people. The

trick for converting a person with no knowledge of mutual funds to a new Mutual Fund customer

is to understand which of the potential investors are more likely to buy mutual funds and to use

the right arguments in the sales process that customers will accept as important and relevant to

their decision.

This Project gave me a great learning experience and at the same time it gave me enough scope

to implement my analytical ability. The analysis and advice presented in this Project Report is

based on market research on the saving and investment practices of the investors and preferences

of the investors for investment in Mutual Funds. This Report will help to know about the

investors¶ Preferences in Mutual Fund means. Are they prefer any particular Asset Management

Company (AMC), Which type of Product they prefer, Which Option (Growth or Dividend) they

prefer or Which Investment Strategy they follow (Systematic Investment Plan or One time Plan).

This Project as a whole can be divided into two parts.

The first part gives an insight about Mutual Fund and its various aspects, the Company Profile,

Objectives of the study, Research Methodology. One can have a brief knowledge about Mutual

Fund and its basics through the Project.

8/9/2019 Mutual Fund Report Final

http://slidepdf.com/reader/full/mutual-fund-report-final 5/66

5

The second part of the Project consists of data and its analysis collected through survey done on

100 people. For the collection of Primary data I made a questionnaire and surveyed of 100

people. I also taken interview of many People those who were coming at the ICICI

Dwarakanagar Branch where I done my Project. The data collected has been well organized and

presented. I hope the research findings and conclusion will be of use

8/9/2019 Mutual Fund Report Final

http://slidepdf.com/reader/full/mutual-fund-report-final 6/66

6

Chapter 1

INTRODUCTION

8/9/2019 Mutual Fund Report Final

http://slidepdf.com/reader/full/mutual-fund-report-final 7/66

7

INTRODUCTION

Mutual funds are financial intermediaries, which collect the savings of investors and invest themin a large and well-diversified portfolio of securities such as money market instruments,

corporate and government bonds and equity shares of joint stock companies. A mutual fund is a

pool of common funds invested by different investors, who have no contact with each other.

Mutual funds are conceived as institutions for providing small investors with avenues of

investments in the capital market. Since small investors generally do not have adequate time,

knowledge, experience and resources for directly accessing the capital market, they have to rely

on an intermediary, which undertakes informed investment decisions and provides consequential

benefits of professional expertise. The raison d¶être of mutual funds is their ability to bring

down the transaction costs. The advantages for the investors are reduction in risk, expert

professional management, diversified portfolios, and liquidity of investment and tax benefits. By

pooling their assets through mutual funds, investors achieve economies of scale. The interests of

the investors are protected by the SEBI, which acts as a watchdog. Mutual funds are governed by

the SEBI (Mutual Funds) Regulations, 1993.

THE GOAL OF MUTUAL FUND

The goal of a mutual fund is to provide an individual to make money. There are several

thousand mutual funds with different investments strategies and goals to chosen from. Choosing

one can be over whelming, even though it need not be different mutual funds have different

risks, which differ because of the fund¶s goals fund manager, and investment style.

The fund itself will still increase in value, and in that way you may also make money therefore

the value of shares you hold in mutual fund will increase in value when the holdings increases in

value capital gains and income or dividend payments are best reinvested for younger investors

Retires often seek the income from dividend distribution to augment their income with

reinvestment of dividends and capital distribution your money increase at an even greater rate.

When you redeem your shares what you receive is the value of the share.

8/9/2019 Mutual Fund Report Final

http://slidepdf.com/reader/full/mutual-fund-report-final 8/66

8

SCOPE OF THE STUDY:

A big boom has been witnessed in Mutual Fund Industry in recent times. A large number of new players have entered the market and trying to gain market share in this rapidly improving market.

The research was carried on in Visakhapatnam. I had been sent to the Dwaraka Nagar branch of

ICICI Prudential Asset Management Company where I completed my Project work. I surveyed

on my Project Topic ³A study of preferences of the Investors for investment in Mutual Fund´ on

the visiting customers of the ICICI AMC.

The study will help to know the preferences of the customers, which company, portfolio, mode

of investment, option for getting return and so on they prefer. This project report may help the

company to make further planning and strategy.

OBJECTIVES OF STUDY:

1. To study the consumer awareness regarding Mutual Funds

2. To study the pattern of consumer behavior within the available investment options and to

test awareness among the consumer about the various mutual funds.

3. To create awareness about mutual funds industry and different products of mutual funds

available in ICICI Prud.AMC. Various respondents are not aware of the mutual fund

products and the risk and returns involved with them.

8/9/2019 Mutual Fund Report Final

http://slidepdf.com/reader/full/mutual-fund-report-final 9/66

9

LIMITATIONS TO THE STUDY:

Though the present study aimed to achieve the above-mentioned objectives in full earnest andaccuracy, it was in a weak position due to certain limitations. Some of the limitations of this

study may be summarized as follows:

y Getting accurate responses from the respondents due to their inherent problems was

difficult. They were partial, and refused to cooperate.

y Very few people have knowledge about Mutual funds and the other products of the

Mutual Funds.

y Locating the target respondents was very time consuming.

y Sample size was limited due to the limited period of days allocated for the survey.

y The selection of respondents to cover the various strata of the society was tedious and

time consuming.

STUDY METHODOLOGY

Research Design : Descriptive Research

Research Instrument : Structured, non-disguised

Sample Method : Non-Probability Sampling

Sample Size : 100

Sampling Design : Convenience Sampling

8/9/2019 Mutual Fund Report Final

http://slidepdf.com/reader/full/mutual-fund-report-final 10/66

10

SOURCES OF DATA

Primary Data : Structured, Non-Disguised Questionnaire

Secondary Data : Reference from distributors & banks

The whole study is based upon primary and secondary data. Therefore, information has been

collected from interacting with different investors and from various magazines, journals,

websites, and bulletins.

8/9/2019 Mutual Fund Report Final

http://slidepdf.com/reader/full/mutual-fund-report-final 11/66

11

LITERATURE REVIEW

Mutual funds are as much about marketing as investing in the 1990¶s,which is why the hoary

cliché´ Mutual funds are sold, not bought´ is a true as ever. As Glorianne Stromberg oncetold Canadian Business magazine, the fund business may have started out in the portfolio

management business, but ³somewhere along the line, the marketers got hold of it, and the

advisory function has been almost superseded by the sales function.´

-JONATHAN CHEVREAU, THE WEALTHY BOOMER

Successful fund marketing creates value for Fund companies, dealers and unit holders so that

each is satisfied. The definition goes much deeper than simply "selling something to somebody".

Fund marketers must understand. Both "Needs &Wants" side of the equation and ³Product, Ideas

Services" side of the equation. Not only must marketing fully understand both sides of the

equation, but it must also effectively communicate the details of each in order to successfully

bridge the gap between the two. Every facet of modern marketing has been effectively employed

to dramatically grow the Indian mutual fund industry

8/9/2019 Mutual Fund Report Final

http://slidepdf.com/reader/full/mutual-fund-report-final 12/66

12

Chapter 2

HISTORY OF MUTUAL FUNDS

8/9/2019 Mutual Fund Report Final

http://slidepdf.com/reader/full/mutual-fund-report-final 13/66

13

BACKGROUND

HISTORY AND STRUCTURE OF INDIAN MUTUAL FUND INDUSTRY:

The mutual fund industry in India started in 1963 with the formation of Unit Trust of India, at the

initiative of the Government of India and Reserve Bank. The history of mutual funds in India can

be broadly divided into four distinct phases:

First Phase ± 1964-87

Unit Trust of India (UTI) was established on 1963 by an Act of Parliament. It was set up by the

Reserve Bank of India and functioned under the Regulatory and administrative control of the

Reserve Bank of India. In 1978 UTI was de-linked from the RBI and the Industrial Development

Bank of India (IDBI) took over the regulatory and administrative control in place of RBI. The

first scheme launched by UTI was Unit Scheme 1964. At the end of 1988 UTI had Rs.6,700

crores of assets under management.

Second Phase ± 1987-1993 (Entry of Public Sector Funds)

1987 marked the entry of non- UTI, public sector mutual funds set up by public sector banks and

Life Insurance Corporation of India (LIC) and General Insurance Corporation of India (GIC).

SBI Mutual Fund was the first non- UTI Mutual Fund established in June 1987 followed by

Canbank Mutual Fund (Dec 87), Punjab National Bank Mutual Fund (Aug 89), Indian Bank

Mutual Fund (Nov 89), Bank of India (Jun 90), Bank of Baroda Mutual Fund (Oct 92). LIC

established its mutual fund in June 1989 while GIC had set up its mutual fund in December

1990. At the end of 1993, the mutual fund industry had assets under management of Rs.47, 004

crores.

8/9/2019 Mutual Fund Report Final

http://slidepdf.com/reader/full/mutual-fund-report-final 14/66

14

Third Phase ± 1993-2003 (Entry of Private Sector Funds)

With the entry of private sector funds in 1993, a new era started in the Indian mutual fund

industry, giving the Indian investors a wider choice of fund families. Also, 1993 was the year in

which the first Mutual Fund Regulations came into being, under which all mutual funds, except

UTI were to be registered and governed. The erstwhile Kothari Pioneer (now merged with

Franklin Templeton) was the first private sector mutual fund registered in July 1993. The 1993

SEBI (Mutual Fund) Regulations were substituted by a more comprehensive and revised Mutual

Fund Regulations in 1996. The industry now functions under the SEBI (Mutual Fund)

Regulations 1996. The number of mutual fund houses went on increasing, with many foreign

mutual funds setting up funds in India and also the industry has witnessed several mergers and

acquisitions. As at the end of January 2003, there were 33 mutual funds with total assets of Rs. 1,21,805 crores. The Unit Trust of India with Rs.44, 541 crores of assets under management was

way ahead of other mutual funds.

Fourth Phase ± since February 2003

In February 2003, following the repeal of the Unit Trust of India Act 1963 UTI was bifurcated

into two separate entities. One is the Specified Undertaking of the Unit Trust of India with assets

under management of Rs.29, 835 crores as at the end of January 2003, representing broadly, the

assets of US 64 scheme, assured return and certain other schemes. The Specified Undertaking of

Unit Trust of India, functioning under an administrator and under the rules framed by

Government of India and does not come under the purview of the Mutual Fund Regulations. The

second is the UTI Mutual Fund Ltd, sponsored by SBI, PNB, BOB and LIC. It is registered with

SEBI and functions under the Mutual Fund Regulations. With the bifurcation of the erstwhile

UTI which had in March 2000 more than Rs.76, 000 crores of assets under management and with

the setting up of a UTI Mutual Fund, conforming to the SEBI Mutual Fund Regulations, and

with recent mergers taking place among different private sector funds, the mutual fund industry

has entered its current phase of consolidation and growth. As at the end of September, 2004,

there were 29 funds, which manage assets of Rs.153108 crores under 421 schemes.

8/9/2019 Mutual Fund Report Final

http://slidepdf.com/reader/full/mutual-fund-report-final 15/66

15

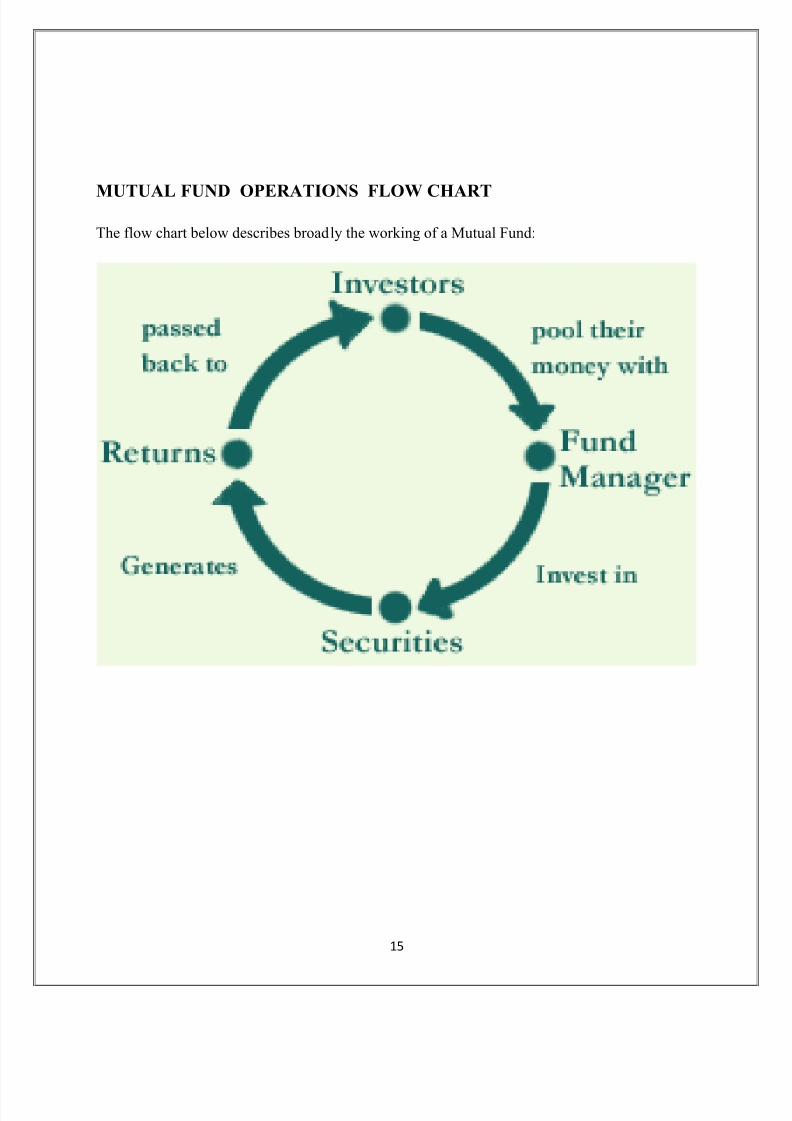

MUTUAL FUND OPERATIONS FLOW CHART

The flow chart below describes broadly the working of a Mutual Fund:

8/9/2019 Mutual Fund Report Final

http://slidepdf.com/reader/full/mutual-fund-report-final 16/66

16

Chapter ± 3

CLASSIFICATION OF MUTUAL FUNDS

8/9/2019 Mutual Fund Report Final

http://slidepdf.com/reader/full/mutual-fund-report-final 17/66

17

CLASSIFICATION OF MUTUAL FUND SCHEMES:

Any mutual fund has an objective of earning income for the investors and/ or getting increased

value of their investments. To achieve these objectives mutual funds adopt different strategies

and accordingly offer different schemes of investments. On this basis the simplest way to

categorize schemes would be to group these into two broad classifications:

OPERATIONAL CLASSIFICATION AND PORTFOLIO CLASSIFICATION.

Operational classification highlights the two main types of schemes, i.e., open-ended and close-

ended which are offered by the mutual funds.

Portfolio classification projects the combination of investment instruments and investment

avenues available to mutual funds to manage their funds. Any portfolio scheme can be either

open ended or close ended.

OPERATIONAL CLASSIFICATION

(A) Open Ended Schemes:

As the name implies the size of the scheme (Fund) is open ± i.e., not specified or pre-

determined. Entry to the fund is always open to the investor who can subscribe at any time. Such

fund stands ready to buy or sell its securities at any time. It implies that the capitalization of the

fund is constantly changing as investors sell or buy their shares. Further, the shares or units are

normally not traded on the stock exchange but are repurchased by the fund at announced rates.

Open-ended schemes have comparatively better liquidity despite the fact that these are not

listed. The reason is that investors can any time approach mutual fund for sale of such units. No

intermediaries are required. Moreover, the realizable amount is certain since repurchase is at a

price based on declared net asset value (NAV). No minute to minute fluctuations in rates haunt

the investors. The portfolio mix of such schemes has to be investments, which are actively

traded in the market. Otherwise, it will not be possible to calculate NAV. This is the reason

8/9/2019 Mutual Fund Report Final

http://slidepdf.com/reader/full/mutual-fund-report-final 18/66

18

that generally open-ended schemes are equity based. Moreover, desiring frequently traded

securities, open-ended schemes hardly have in their portfolio shares of comparatively new

and smaller companies since these are not generally traded. In such funds, option to reinvest its

dividend is also available. Since there is always a possibility of withdrawals, the management of

such funds becomes more tedious as managers have to work from crisis to crisis. Crisis may

be on two fronts, one is, that unexpected withdrawals require funds to maintain a high level

of cash available every time implying thereby idle cash. Fund managers have to face questions

like µwhat to sell¶. He could very well have to sell his most liquid assets. Second, by virtue of

this situation such funds may fail to grab favourable opportunities. Further, to match quick cash

payments, funds cannot have matching realization from their portfolio due to intricacies of the

stock market. Thus, success of the open- ended schemes to a great extent depends on the

efficiency of the capital market and the selection and quality of the portfolio.

(B) Close Ended Schemes:

Such schemes have a definite period after which their shares/ units are redeemed. Unlike open-

ended funds, these funds have fixed capitalization, i.e., their corpus normally does not changethroughout its life period. Close ended fund units trade among the investors in the secondary

market since these are to be quoted on the stock exchanges. Their price is determined on the

basis of demand and supply in the market. Their liquidity depends on the efficiency and

understanding of the engaged broker. Their price is free to deviate from NAV, i.e., there is every

possibility that the market price may be above or below its NAV. If one takes into account the

issue expenses, conceptually close ended fund units cannot be traded at a premium or over NAV

because the price of a package of investments, i.e., cannot exceed the sum of the prices of the

investments constituting the package. Whatever premium exists that may exist only on account

of speculative activities. In India as per SEBI (MF) Regulations every mutual fund is free to

launch any or both types of schemes.

8/9/2019 Mutual Fund Report Final

http://slidepdf.com/reader/full/mutual-fund-report-final 19/66

19

PORTFOLIO CLASSIFICATION OF FUNDS

Following are the portfolio classification of funds, which may be offered. This classification may

be on the basis of (A) Return, (B) Investment Pattern, (C) Specialised sector of investment, (D)

Leverage and (E) Others.

(A) Return based classification:

To meet the diversified needs of the investors, the mutual fund schemes are made to enjoy a

good return. Returns expected are in form of regular dividends or capital appreciation or a

combination of these two.

1. Income Funds: For investors who are more curious for returns, Income funds are floated.

Their objective is to maximize current income. Such funds distribute periodically the income

earned by them. These funds can further be splitted up into categories: those that stress constant

income at relatively low risk and those that attempt to achieve maximum income possible, even

with the use of leverage. Obviously, the higher the expected returns, the higher the potential risk

of the investment.

2. Growth Funds: Such funds aim to achieve increase in the value of the underlying investments

through capital appreciation. Such funds invest in growth oriented securities which can

appreciate through the expansion production facilities in long run. An investor who selects such

funds should be able to assume a higher than normal degree of risk.

3. Conservative Funds: The fund with a philosophy of ³all things to all´ issue offer document

announcing objectives as: (i) To provide a reasonable rate of return, (ii) To protect the value of

investment and, (iii) To achieve capital appreciation consistent with the fulfillment of the first

two objectives. Such funds which offer a blend of immediate average return and reasonable

capital appreciation are known as ³middle of the road´ funds. Such funds divide their portfolio in

common stocks and bonds in a way to achieve the desired objectives. Such funds have been most

popular and appeal to the investors who want both growth and income.

8/9/2019 Mutual Fund Report Final

http://slidepdf.com/reader/full/mutual-fund-report-final 20/66

20

(B) Investment Based Classification:

Mutual funds may also be classified on the basis of securities in which they invest. Basically, it

is renaming the subcategories of return based classification.

1. Equity Fund: Such funds, as the name implies, invest most of their investible shares in

equity shares of companies and undertake the risk associated with the investment in equity

shares. Such funds are clearly expected to outdo other funds in rising market, because these have

almost all their capital in equity. Equity funds again can be of different categories varying from

those that invest exclusively in high quality µblue chip companies to those that invest solely in

the new, unestablished companies. The strength of these funds is the expected capital

appreciation. Naturally, they have a higher degree of risk. Examples:

2. Bond Funds: Such funds have their portfolio consisted of bonds, debentures, etc. this type of

fund is expected to be very secure with a steady income and little or no chance of capital

appreciation. Obviously risk is low in such funds. In this category we may come across the funds

called µLiquid Funds¶ which specialize in investing short-term money market instruments. The

emphasis is on liquidity and is associated with lower risks and low returns.

3. Balanced Fund: The funds, which have in their portfolio a reasonable mix of equity and

bonds, are known as balanced funds. Such funds will put more emphasis on equity share

investments when the outlook is bright and will tend to switch to debentures when the future is

expected to be poor for shares.

(C) Sector Based Funds:

There are number of funds that invest in a specified sector of economy. While such funds do

have the disadvantage of low diversification by putting all their all eggs in one basket, the policy

of specializing has the advantage of developing in the fund managers an intensive knowledge of

the specific sector in which they are investing. Sector based funds are aggressive growth funds

8/9/2019 Mutual Fund Report Final

http://slidepdf.com/reader/full/mutual-fund-report-final 21/66

21

which make investments on the basis of assessed bright future for a particular sector. These

funds are characterized by high viability, hence more risky.

WHY MUTUAL FUNDS?

Mutual Funds are becoming a very popular form of investment characterized by many

advantages that they share with other forms of investments and what they possess uniquely

themselves. The primary objectives of an investment proposal would fit into one or combination

of the two broad categories, i.e., Income and Capital gains. How mutual fund is expected to be

over and above an individual in achieving the two said objectives, is what attracts investors to

opt for mutual funds. Mutual fund route offers several important advantages.

Diversification: A proven principle of sound investment is that of diversification, which is

the idea of not putting all your eggs in one basket. By investing in many companies the mutual

funds can protect themselves from unexpected drop in values of some shares. The small

investors can achieve wide diversification on his own because of many reasons, mainly funds at

his disposal. Mutual funds on the other hand, pool funds of lakhs of investors and thus can

participate in a large basket of shares of many different companies. Majority of people consider

diversification as the major strength of mutual funds.

Expertise Supervision: Making investments is not a full time assignment of investors. So

they hardly have a professional attitude towards their investment. When investors buy mutual

fund scheme, an essential benefit one acquires is expert management of the money he puts in the

fund. The professional fund managers who supervise fund¶s portfolio take desirable decisions

viz., what scrip¶s are to be bought, what investments are to be sold and more appropriate

decision as to timings of such buy and sell. They have extensive research facilities at their

disposal, can spend full time to investigate and can give the fund a constant supervision. The

performance of mutual fund schemes, of course, depends on the quality of fund managers

employed.

8/9/2019 Mutual Fund Report Final

http://slidepdf.com/reader/full/mutual-fund-report-final 22/66

22

Chapter - 4

MARKETING OF MUTUAL FUNDS

8/9/2019 Mutual Fund Report Final

http://slidepdf.com/reader/full/mutual-fund-report-final 23/66

23

MARKETING STRATEGIES ADOPTED BY THE MUTUAL FUNDS

The present marketing strategies of mutual funds can be divided into two main headings:

1. Direct marketing

2. Selling through intermediaries

DIRECT MARKETING:

This constitutes 20 percent of the total sales of mutual funds. Some of the important tools used in

this type of selling are:

1. Personal Selling:

In this case the customer support officer or Relationship Manager of the fund at a particular

branch takes appointment from the potential prospect. Once the appointment is fixed, the branch

officer also called Business Development Associate (BDA) in some funds then meets the

prospect and gives him all details about the various schemes being offered by his fund. The

conversion rate in this mode of selling is in between 30% - 40%.

2. Telemarketing:

In this case the emphasis is to inform the people about the fund. The names and phone numbers

of the people are picked at random from telephone directory. Some fund houses have their

database of investors and they cross sell their other products. Sometimes people belonging to a

particular profession are also contacted through phone and are then informed about the fund.

Generally the conversion rate in this form of marketing is 15% - 20%.

8/9/2019 Mutual Fund Report Final

http://slidepdf.com/reader/full/mutual-fund-report-final 24/66

24

3. Direct mail:

This one of the most common method followed by all mutual funds. Addresses of people are

picked at random from telephone directory, business directory, professional directory etc. The

customer support officer (CSO) then mails the literature of the schemes offered by the fund. The

follow up starts after 3 ± 4 days of mailing the literature. The CSO calls on the people to whom

the literature was mailed. Answers their queries and is generally successful in taking

appointments with those people. It is then the job of BDA to try his best to convert that prospect

into a customer.

4. Advertisements in newspapers and magazines:

The funds regularly advertise in business newspapers and magazines besides in leading national

dailies. The purpose to keep investors aware about the schemes offered by the fund and

their performance in recent past. Advertisement in TV/FM Channel: The funds are

aggressively giving their advertisements in TV and FM Channels to promote their funds.

5. Hoardings and Banners:

In this case the hoardings and banners of the fund are put at important locations of the city where

the movement of the people is very high. The hoarding and banner generally contains

information either about one particular scheme or brief information about all schemes of fund.

SELLING THROUGH INTERMEDIARIES:

Intermediaries contribute towards 80% of the total sales of mutual funds. These are the people/

distributors who are in direct touch with the investors. They perform an important role in

attracting new customers. Most of these intermediaries are also involved in selling shares and

other investment instruments. They do a commendable job in convincing investors to invest in

mutual funds. A lot depends on the after sale services offered by the intermediary to the

8/9/2019 Mutual Fund Report Final

http://slidepdf.com/reader/full/mutual-fund-report-final 25/66

25

customer. Customers prefer to work with those intermediaries who give them right information

about the fund and keep them abreast with the latest changes taking place in the market

especially if they have any bearing on the fund in which they have invested.

Regular Meetings with distributors:

Most of the funds conduct monthly/bi-monthly meetings with their distributors. The objective is

to hear their complaints regarding service aspects from funds side and other queries related to

the market situation. Sometimes, special training programmes are also conducted for the new

agents/ distributors. Training involves giving details about the products of the fund, their present

performance in the market, what the competitors are doing and what they can do to increase the

sales of the fund.

MARKETING OF FUNDS : CHALLENGES AND OPPORTUNITIES

When we consider marketing, we have to see the issues in totality, because we cannot judge an

elephant by its trunk or by its tail but we have to see it in its totality. When we say marketing of

mutual funds, it means, includes and encompasses the following aspects:

Assessing of investors needs and market research;

Responding to investors needs;

Product designing;

Studying the macro environment;

Timing of the launch of the product;

Choosing the distribution network;

Finalizing strategies for publicity and advertisement;

8/9/2019 Mutual Fund Report Final

http://slidepdf.com/reader/full/mutual-fund-report-final 26/66

26

Preparing offer documents and other literature;

Getting feedback about sales;

Studying performance indicators about fund performance like NAV;

Creating positive image about the fund and changing the nature of the market itself.

The above are the aspects of marketing of mutual funds, in totality. Even if there is a single

weak-link among the factors which are mentioned above, no mutual fund can successfully

market its funds.

WIDENING, BROADENING AND DEEPENING THE MARKETS

There are certain issues that are directly linked with the marketing of mutual funds, the first of

which is widening, broadening and deepening of the market for the mutual fund products.

Consider the geographical spread of the investors in the mutual fund industry. Almost 80% of the

funds are mobilized from less than 10 centers in the country. In fact there are only around 35

centers in the country, which account for almost 95% of the funds mobilized. Considering the

vast nature of this country, the first priority is that the geographic spread has to be widened andthe market has to be deepened. Secondly, the mutual funds must try to spread their wings not

only within the country, but also outside the country.

A. Markets in Rural and Semi-Urban Areas

There exists a large investor base in rural and semi-urban areas, having a population of about one

lakhs, which normally has access to only post office savings and bank deposits. This is the single

largest untapped market for mutual funds in India. Rural marketing, unlike the marketing of

mutual funds in the metros and urban areas, would require a completely different strategy, and

different means of communication to the target customer. Typically, investors in the rural and

semi-urban areas are not well educated and are inadequately exposed to the capital market

8/9/2019 Mutual Fund Report Final

http://slidepdf.com/reader/full/mutual-fund-report-final 27/66

27

mechanisms. Therefore, more emphasis has to be given to the electronic media and other forms

of publicity such as wall paintings, hoardings, and educational films. It is also important to

utilize the services of local intermediaries like Gram Sevaks, Postmasters, School teachers,

Agricultural Co-operative Societies and Rural Banks. It would therefore be more expensive to

market mutual funds in such markets than marketing in the cities.

The mutual fund industry can collectively undertake this job of creating awareness among the

rural population about the mutual funds as a new form of savings; translate that awareness into

increased fund mobilization. Collective Advertisements can be released .AMFI can coordinate

this task on behalf of the various Mutual Fund houses. The retail distribution network,

comprising of the district representatives and the collection centers can be best utilized to create

such awareness and expand the market. Simplification of literature in regional languages, group

meetings in these semi-urban and rural areas, visits by mobile vans with some audio visual aids

and the like, should help develop these markets. In other words, the untapped markets in the

country should ideally be the first thing that the mutual funds in India should Endeavour to tap,

not entirely relying upon the investors in the 35 odd cities of the country. By concentrating on

these areas, the investor base will get more broad based. Once the semi urban population gets

acquainted with the concept of mutual funds, it will naturally give the much needed stability to

the market.

B. Overseas Markets

The second aspect with respect to the widening and deepening the market is expanding the

overseas investor base. A target group with large potential, which can be tapped is non-resident

Indians. If offered after sales services of international standard, reasonable return and easy access

to information, NRI¶s are willing to invest in Indian mutual funds. The expansion of the

distribution network and quick dissemination of information, coupled with prompt and timely

service, efficient collection and remittance mechanism, will play an important role in mobilizing

and retaining these funds. NRI¶s will also require a continuous presence in their market, because

that generates trust and confidence, which translates into sustained mobilization of funds.

8/9/2019 Mutual Fund Report Final

http://slidepdf.com/reader/full/mutual-fund-report-final 28/66

28

PRODUCT INNOVATION AND VARIETY

A. Investor Preferences

The challenge for the mutual funds is in the tailoring the right products that will help mobilizingsavings by targeting investors¶ needs. It is necessary that the common investor understands very

clearly and loudly the salient features of funds, and distinguishes one fund from another. The

funds that are being launched today are more or less look-alikes, or plain vanilla funds, and not

necessarily designed to take into account the investors¶ varying needs. The Indian investor is

essentially risk averse and is more passive than active. He is not interested in frequently

changing his portfolio, but is satisfied with safety and reasonable returns. Importantly, he

understands more by emotions and sentiments rather than a quantitative comparison of funds¶

performance with respect to an index. Mere growth prospects, in an uncertain market, are not

attractive to him. He prefers one bird in the hand to two in bush, and is happy if assured a rate of

reasonable return that he will get on his investment. The expectations of a typical investor, in

order of preference are the safety of funds, reasonable return and liquidity.

The investor is ready to invest his money over a long period, provided there is a purpose attached

to it which is linked to his social needs and therefore appeals to his sentiments and emotions.

That purpose may be his child¶s education and career development, medical expenses, health

care after retirement, or the need for steady and sure income after retirement. In a country where

social security and social insurance are conspicuous more by their absence, mutual funds can

pool their resources together and try to mobilize funds to meet some of the social needs of the

society.

B. Product Innovations

With the debt market now getting developed, mutual funds are tapping the investors who require

steady income with safety, by floating funds that are designed to primarily have debt instruments

in their portfolio. The other area where mutual funds are concentrating is the money market

mutual funds, sectoral funds, index funds, gilt funds besides equity funds. The industry can also

8/9/2019 Mutual Fund Report Final

http://slidepdf.com/reader/full/mutual-fund-report-final 29/66

29

design separate funds to attract semi-urban and rural investors, keeping their seasonal

requirements in mind for harvest seasons, festival seasons, sowing seasons, etc.

ADVERTISING AND SALES PROMOTION

By their very nature, mutual funds require higher advertisement and sales promotion expenses

than any consumer product offering measurable performance. Different kinds of advertising and

sales promotion exercises are required to serve the needs of different classes of investors. For

instance, an aggressive µpush¶ marketing strategy is required for retail markets, where investors

are not adequately aware of the product and do not have specialized skill in financial market, in

contrast with µpull¶ marketing strategies for the wholesale market.

There are certain issues with reference to advertisement, publicity literature and offer

documents, which deserve attention. Most of the mutual fund advertisements look similar,

focusing on scheme features, returns and incentives. An investor exposed to the increasing

number of mutual fund products finds that all the available brands are rather identical, and

cannot appreciate any distinction.

The present form of application, brochures and other literature is generally lengthy, cumbersome

and at times complicated leading to higher emphasis on advertisement. One of the limiting

factors is the regulatory framework governing advertisements of mutual fund products. For

instance, in the offer documents, mutual funds are required to mention the fund objectives in

clear terms. Immediately thereafter, the first risk factor that has to be mentioned is that there is

no certainty whether the objectives of the fund will be achieved or not. Some more relaxation¶s

in these may facilitate bringing more novelty in advertisements, within a broad framework,

without luring investors through false promises, and will certainly improve the situation.

Another hurdle is the statutory disclaimer required to be carried along with every advertisement.Mutual funds have to provide risk factors. Under the present mutual fund regulations, a prior

approval by SEBI is a must before a mutual fund can launch its fund. In the regulation itself, a

period of one month has been provided. But in a month¶s time, perhaps the situation may so

change, that the timing of launch gets affected. The requirement for getting approval, which

normally takes about 2 months¶ time, defeats the purpose for which the fund was designed also.

8/9/2019 Mutual Fund Report Final

http://slidepdf.com/reader/full/mutual-fund-report-final 30/66

30

QUALITY OF SERVICE

This industry primarily sells quality of services, given that the performance cannot be promised.

It is with this attribute along with procedural simplicity, that the fund gradually builds its brand

and its class of loyal investors. The quality of services is broadly categorized as:

Ø Timely services after the sale of the units; and

Ø Continuous reporting of investment performance.

Mutual fund managers must give due attention and evaluate their performance on each front.

They may also consider an option of conducting a service audit for controlling and improving the

quality of service.

MARKET RESEARCH

Investment in mutual fund is not a one-time activity. It is a continuous activity. The same

investor, if satisfied, will come to the fund again and again. When the investor sends his

application, it is not only an application, but it also contains vital information. Most of thisinformation if tabulated and analyzed would provide important insights into investor needs,

preferences and behavior and enables us to target customers need more accurately, to achieve

better penetration, deeper loyalty and reduced costs. It is in this context that direct marketing will

assume increased importance. Knowing the customer thoroughly is of utmost importance. Unlike

the consumer goods industry, it is not possible for mutual fund industry to test market and have

pilot projects before launch. At the same time, focusing and concentrating on a particular

geographic area where the fund has a strong presence and proven marketing network, can help

reduce network, can help reduce issue expenses and ultimately translate into higher returns for

the investor. Very little research on investor preference is available, but the industry can

collectively have a data bank, and share the information for appropriate use.

8/9/2019 Mutual Fund Report Final

http://slidepdf.com/reader/full/mutual-fund-report-final 31/66

31

Market Segmentation:

Different segments of the market have different risk-return criteria, on the basis of which they

take investment decisions. Not only that, in a particular segment also there could be different

sub-segments asking for yet different risk-return attributes, and differential preference for

various investments attributes of financial product. Different investment attributes an investor

expects in a financial product are:

Liquidity,

Capital appreciation

Safety of principal,

Tax treatment,

Dividend or interest income,

Regulatory restrictions,

Time period for investment,

On the basis of these attributes the mutual fund market may be broadly segmented into five main

segments as under.

1) Retail Segment

This segment characterizes large number of participants but low individual volumes. It consists

of individuals, Hindu Undivided Families, and firms. It may be further sub-divided into:

i. Salaried class people;

ii. Retired people;

iii. Businessmen and firms having occasional surpluses;

8/9/2019 Mutual Fund Report Final

http://slidepdf.com/reader/full/mutual-fund-report-final 32/66

32

2) Institutional Segment

This segment characterizes less number of participants, and large individual volumes. It consists

of banks, public sector units, financial institutions, foreign institutional investors, insurance

corporations, provident and pension funds. This class normally looks for more specialized

professional investment skills of the fund managers and expects a structured product than a

ready-made product. The tax features and regulatory restrictions are the vital considerations in

their investment decisions. Each class of participants, such as banks, provides a niche to the fund

managers in this segment. It requires more of a personalized and direct marketing to sustain and

increase volumes.

3) Trust

This is a highly regulated, high volumes segment. It consists of various types of trusts, namely,

charitable trusts, religious trust, educational trust, family trust, social trust, etc. each with

different objectives. Its basic investment need would be safety of the principal, regular income

and hedge against inflation rather than liquidity and capital appreciation. This class offers vast

potential to the fund managers, if the regulators relax guidelines and allow the trusts to invest

freely in mutual funds.

4) NRI¶s:

This segment consists of very risk sensitive participants, at times referred as µfair weather

friends.¶ They need the highest cover against political and exchange risk. They normally prefer

easy exit with repatriation of income and principal. They also hold a strategic importance as they

bring in crucial foreign exchange ± a crucial input for developing country like ours. Marketing to

this segment requires special kind of products for groups of foreign countries depending upon the

provisions of tax treaties. The range of suitable products is required to design to divert the funds

flowing into bank accounts. The latest flavour in the mutual fund industry is exclusive schemes

for non-resident Indians (NRI¶s).SBI MF has already launched an exclusive scheme for NRI¶s.

ICICI Prudential and JM Mutual are in process of finalizing details and some more funds have

8/9/2019 Mutual Fund Report Final

http://slidepdf.com/reader/full/mutual-fund-report-final 33/66

33

also confirmed that they are planning such schemes. The MF industry is also looking to tap the

vast NRI funds of about $5 billion that were transferred to the local banks as FCNR and NRE

deposits on the redemption of the Resurgent India Bonds in October, 2003. HDFC was one of the

first to launch a fixed maturity plan to NRI¶s after the RIB redemption .The scheme had

collected Rs.16-17 crores. Sundaram and HDFC MF are currently in the process of

strengthening distribution net-works overseas, especially in the Middle East. Sanjay Santhanam,

Vice President Marketing &Sales of Sundaram MF says, ³We are intensifying our efforts at

tapping NRI money. To begin with, we are looking at a representative office and a distribution

network in Dubai. Then we will work out specialized products and asset allocation models.NRI

are used to seeing low interest rates so their return expectations are different from domestic

investors. The large South Indian population in the Middle East will surely connect with the

Sundaram brand.´

5) Corporates

Generally, the investment need of this segment is to park their occasional surplus funds that earn

returns more than what they have to pay on account of holding them. Alternatively, they also get

surplus fund due to the seasonality of the business, which typically become due for the payment

within a year or quarter or even a month. They need short term parking place for their fund,.

This segment offers a vast potential to specialized money market managers.

Inspired Marketing will help Mutual Funds walk away with the bank Deposits

Bankers better watch out! The Indian mutual fund industry will soon start relieving the banking

system of its prized deposits.

Innovative distribution, marketing and aggressive concept selling will drive savings into the lap

of the Indian Mutual Fund industry in the next millennium. Fund chiefs predicted that ease of

transactions, thanks to technology and increased awareness, would lead to more investors

putting their money into mutual funds. The day was not far, they said, when small savings

account s too began moving into mutual funds.

8/9/2019 Mutual Fund Report Final

http://slidepdf.com/reader/full/mutual-fund-report-final 34/66

34

Significantly, fund chiefs were unanimous that the credibility gap which the industry suffered for

the past few years did not exist anymore. All the fund chiefs were unanimous that

performance, service and support were all imperative for growth. ³Performance, transparency

and after sales service and genuine retail investor interest as opposed to hot corporate money, an

important contributor to many mutual fund schemes, will drive the industry growth.

³Performance, transparency, after sales customer service and genuine retail investor interest are

opposed to hot corporate money, an important contributor to many mutual fund schemes, will

drive the industry growth, On the state of market in general, fund chiefs attempted to allay fears

that an overvalued market may pose hurdles to stock picking.

According to them, while investors may feel that information technology, pharmaceuticals and

consumer goods stocks - or the BSE Sensex for that matter ± might have peaked, new

opportunities are opening up in areas like retail, healthcare and even in internet business.

Fund chiefs also made a case for the code to prevent mutual funds from projecting short-term

gains in an attempt to attract investors into their schemes. They were of the view that, ³Mutual

Funds have to agree to present performances in an annualized fashion, over a longer period. The

industry as a whole should standardize its performance.´

8/9/2019 Mutual Fund Report Final

http://slidepdf.com/reader/full/mutual-fund-report-final 35/66

35

Chapter 5

COMPANY PROFILE

8/9/2019 Mutual Fund Report Final

http://slidepdf.com/reader/full/mutual-fund-report-final 36/66

36

ICICI Prudential Asset Management Company enjoys the

strong parentage of Prudential plc, one of UK's largest players

in the insurance & fund management sectors and ICICI Bank, a

well-known and trusted name in financial services in

India. ICICI Prudential Asset Management Company, in a span

of just over eight years, has forged a position of pre-eminence

in the Indian Mutual Fund industry as one of the largest asset

management companies in the country with average assets

under management of Rs. 73,822.45 Crore (as of June 30,

2010). The Company manages a comprehensive range of

schemes to meet the varying investment needs of its investors

spread across 230 cities in the country.

Key Indicators

At inception -

May 1998

As on June

30, 2010

Average Assets Under

Management Rs. 160 Crore

Rs. 73,822.45

Crore

Number of Funds Managed 2 40

Sponsors

8/9/2019 Mutual Fund Report Final

http://slidepdf.com/reader/full/mutual-fund-report-final 37/66

37

Securities and Exchange Board of India, vide its letter no. MFD/PM/567/02

dated June 4, 2002, has accorded its approval in recognizing ICICI Bank Ltd.

as a co-sponsor consequent to the merger of ICICI Ltd. with ICICI Bank Ltd.

ICICI Bank is India's second-largest bank with total assets of Rs. 3,997.95

billion (US$ 100 billion) at March 31, 2008 and profit after tax of Rs. 41.58

billion for the year ended March 31, 2008. ICICI Bank is second amongst all

the companies listed on the Indian stock exchanges in terms of free float market

capitalization Free float holding excludes all promoter holdings, strategic

investments and cross holdings among public sector entities. The Bank has a

network of about 1,308 branches and 3,950 ATMs in India and presence in 18

countries. ICICI Bank offers a wide range of banking products and financial

services to corporate and retail customers through a variety of delivery

channels and through its specialised subsidiaries and affiliates in the areas of

investment banking, life and non-life insurance, venture capital and asset

management. The Bank currently has subsidiaries in the United Kingdom,

Russia and Canada, branches in Unites States, Singapore, Bahrain, Hong Kong,

Sri Lanka, Qatar and Dubai International Finance Centre and representative

offices in United Arab Emirates, China, South Africa, Bangladesh, Thailand,

Malaysia and Indonesia. Our UK subsidiary has established branches in

Belgium and Germany. ICICI Bank's equity shares are listed in India on

Bombay Stock Exchange and the National Stock Exchange of India Limited

and its American Depositary Receipts (ADRs) are listed on the New York

Stock Exchange (NYSE). (Source: Overview at www.icicibank.com).

Headquartered in London, Prudential plc and its affiliated companies together

constitute one of the world's leading financial services groups. Prudential

provides insurance and financial services in a number of markets around the

8/9/2019 Mutual Fund Report Final

http://slidepdf.com/reader/full/mutual-fund-report-final 38/66

38

world, including in Asia, the US, the UK, Europe and the Middle East.

Founded in 1848, the company has £249 billion in funds under management (as

of 31 December 2008) and more than 21 million customers worldwide.

Prudential has been writing life insurance in the United Kingdom for 160 years

and has had the largest long-term fund in the United Kingdom, for over a

century. In the United Kingdom, Prudential is a leading retirement savings and

income solutions and life assurance provider. M&G is Prudential's fund

management business in the United Kingdom and Europe, with almost £140

billion in funds under management (as of 31 December 2008). In the United

States, Jackson National Life, which we acquired in 1986, is one of the largest

life insurance companies providing retirement savings and income solutions.

In Asia, Prudential is the leading Europe-based life insurer in terms of market

coverage and number of top three ranking positions. It is also one of the largest

and most successful fund managers in Asia with more top five market rankings

than any other regional player. Today, Prudential has life insurance and fund

management operations spanning 13 diverse markets in Asia.

Prudential plc is incorporated and with its principal place of business in the

United Kingdom. It is not affiliated in any manner with Prudential Financial,

Inc., a company whose principal place of business is in the United States.

8/9/2019 Mutual Fund Report Final

http://slidepdf.com/reader/full/mutual-fund-report-final 39/66

39

Chapter ± 5

DATA ANALYSIS & INTERPRETATION

8/9/2019 Mutual Fund Report Final

http://slidepdf.com/reader/full/mutual-fund-report-final 40/66

40

ANALYSIS AND INTERPRETATION OF DATA

Knowing the awareness and perception of the customers is very important in any industry. This provides insight into the customer behavior and his expectation from the industry players. A

proper understanding of the awareness and perception would definitely benefit the players. This

survey attempt to know the mutual fund investor better. It examines some interesting choices of

the retail investor including the reasons behind investing in mutual funds and the risk tolerance

levels of the investors. The investor knowledge about the mutual funds and what according to

him are the best mutual funds is also analyzed. This Visakhapatnam city survey was conducted

to know the retail investor awareness and perception about mutual funds. It is hoped that this

survey in Visakhapatnam city would go a long way in benefiting for ICICI mutual fund. The

total sample for the study was 100 across Visakhapatnam city.

I. AN OVERVIEW:

This section shows a simple overview of respondents like their age, gender, income profile,

saving habits and qualification

8/9/2019 Mutual Fund Report Final

http://slidepdf.com/reader/full/mutual-fund-report-final 41/66

41

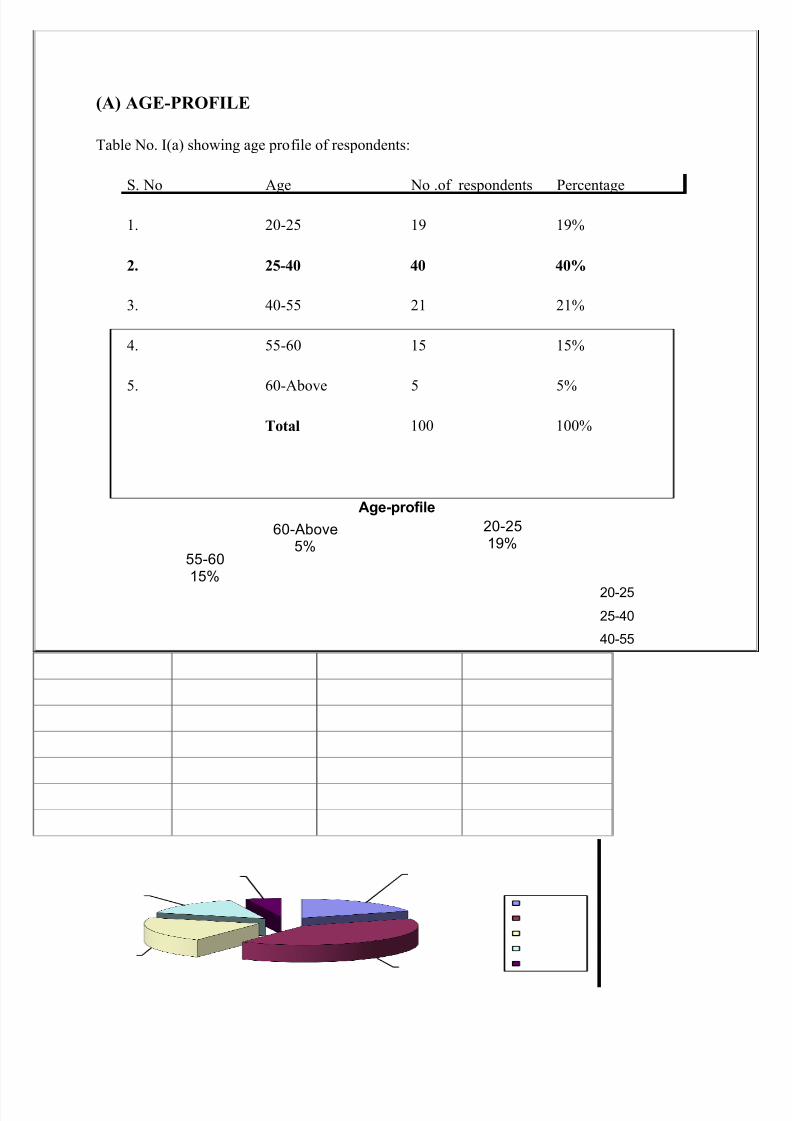

(A) AGE-PROFILE

Table No. I(a) showing age profile of respondents:

S. No Age No .of respondents Percentage

1. 20-25 19 19%

2. 25-40 40 40%

3. 40-55 21 21%

4. 55-60 15 15%

5. 60-Above 5 5%

Total 100 100%

INTERPRETATION :

The maximum number of respondents belongs to the age group of 25-40 years, followed by 40-

55 years of age category.

20-2519%

25-4040%

40-5521%

55-6015%

60-Above5%

Age-profile

20-25

25-40

40-55

55-60

60-Above

8/9/2019 Mutual Fund Report Final

http://slidepdf.com/reader/full/mutual-fund-report-final 42/66

42

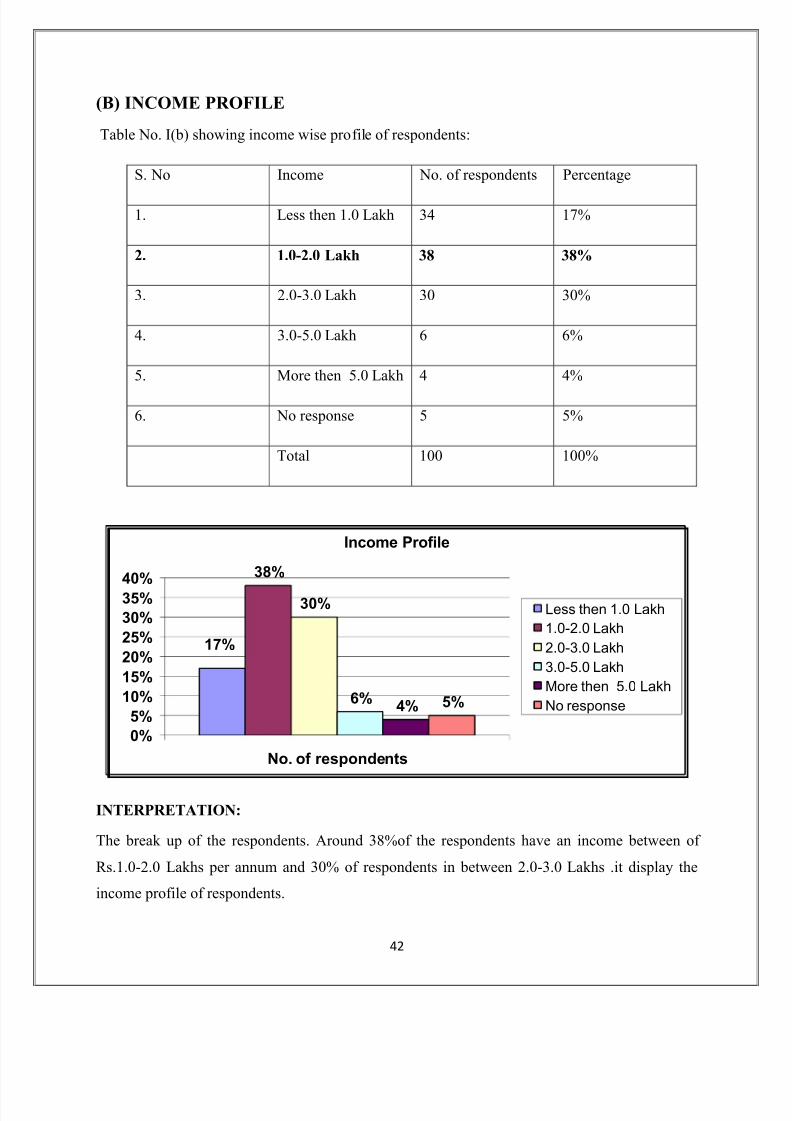

(B) INCOME PROFILE

Table No. I(b) showing income wise profile of respondents:

S. No Income No. of respondents Percentage

1. Less then 1.0 Lakh 34 17%

2. 1.0-2.0 Lakh 38 38%

3. 2.0-3.0 Lakh 30 30%

4. 3.0-5.0 Lakh 6 6%

5. More then 5.0 Lakh 4 4%

6. No response 5 5%

Total 100 100%

INTERPRETATION:

The break up of the respondents. Around 38%of the respondents have an income between of

Rs.1.0-2.0 Lakhs per annum and 30% of respondents in between 2.0-3.0 Lakhs .it display the

income profile of respondents.

17%

38%

30%

6%4% 5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

No. of respondents

Income Profile

Less then 1.0 Lakh

1.0-2.0 Lakh

2.0-3.0 Lakh

3.0-5.0 Lakh

More then 5.0 Lakh

No response

8/9/2019 Mutual Fund Report Final

http://slidepdf.com/reader/full/mutual-fund-report-final 43/66

43

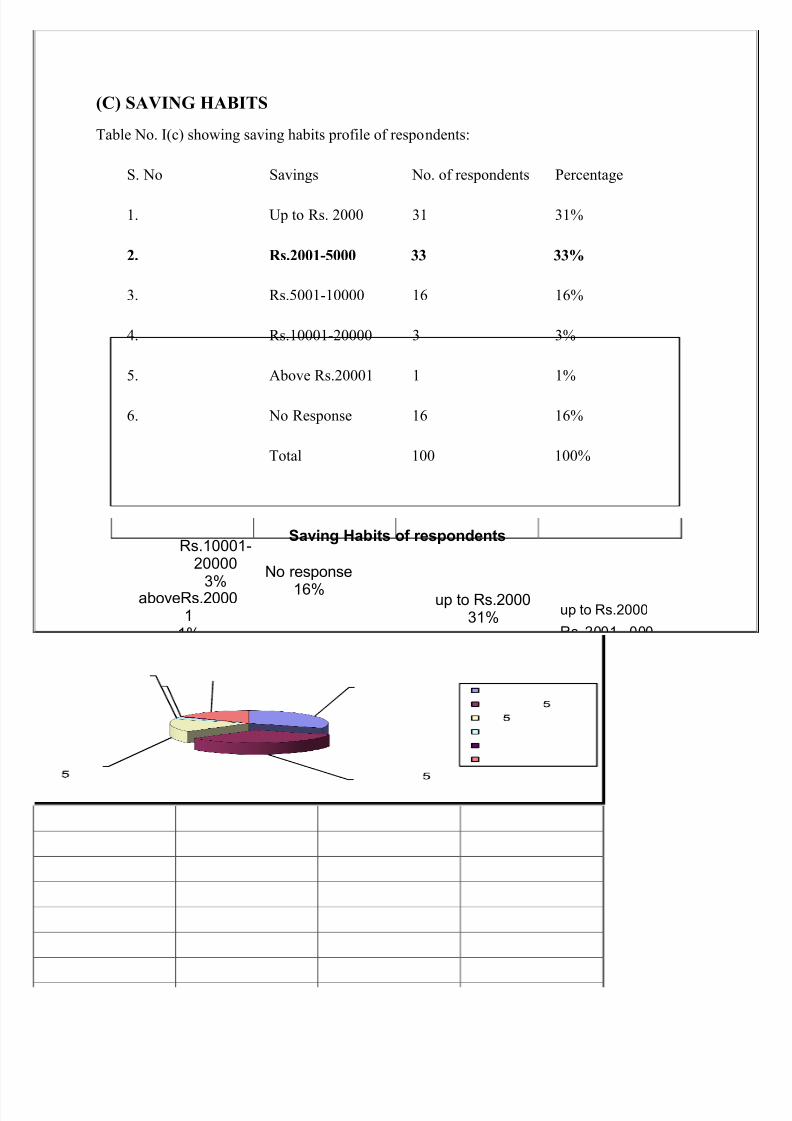

(C) SAVING HABITS

Table No. I(c) showing saving habits profile of respondents:

S. No Savings No. of respondents Percentage

1. Up to Rs. 2000 31 31%

2. Rs.2001-5000 33 33%

3. Rs.5001-10000 16 16%

4. Rs.10001-20000 3 3%

5. Above Rs.20001 1 1%

6. No Response 16 16%

Total 100 100%

INTERPRETATION: In this survey around 33% of the respondents reported to have a saving

in the range of Rs.2001-5000 per month .only 1% of the respondents reported having in higher

bracket i.e more then 20001 per month.

up to Rs.200031%

Rs. 2001- 00033%

Rs. 001-1000016%

Rs.10001-20000

3%aboveRs.20001

1%

No response

16%

Saving Habits of respondents

up to Rs.2000

Rs. 2001- 000

Rs. 001-10000

Rs.10001-20000

aboveRs.20001

No response

8/9/2019 Mutual Fund Report Final

http://slidepdf.com/reader/full/mutual-fund-report-final 44/66

44

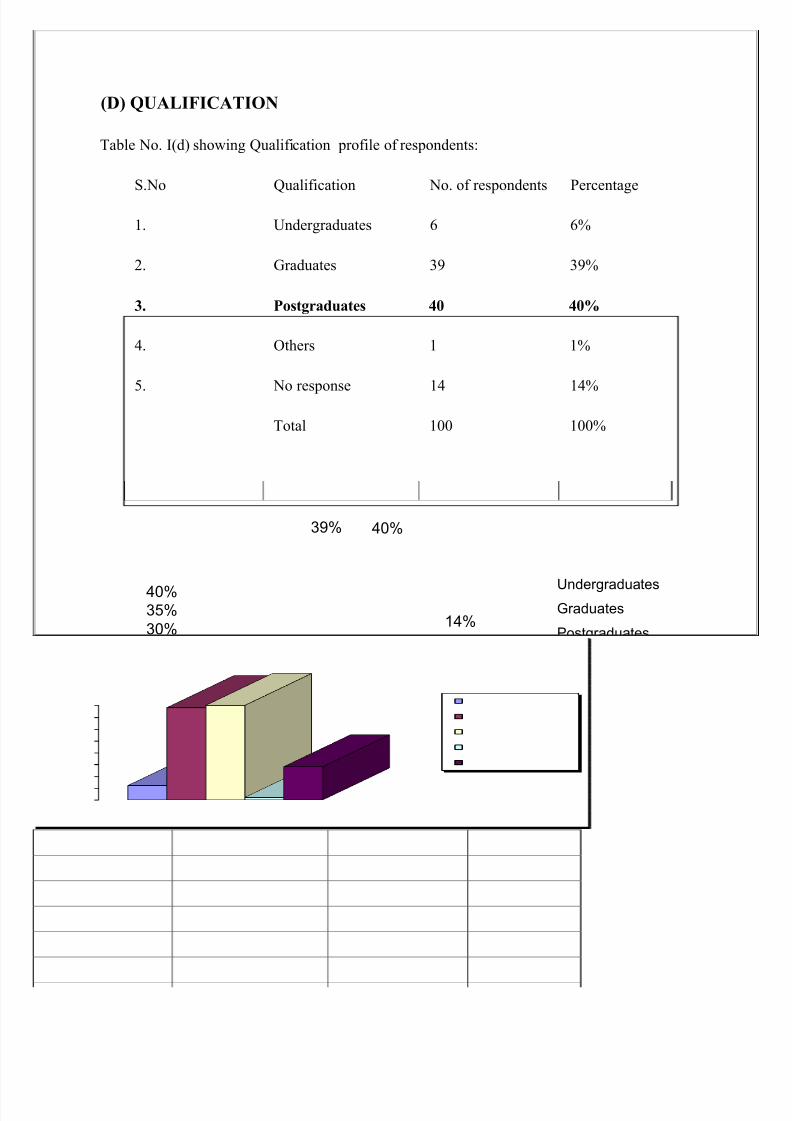

(D) QUALIFICATION

Table No. I(d) showing Qualification profile of respondents:

S.No Qualification No. of respondents Percentage

1. Undergraduates 6 6%

2. Graduates 39 39%

3. Postgraduates 40 40%

4. Others 1 1%

5. No response 14 14%

Total 100 100%

INTERPRETATION:

The surveyed group is well educated group with 40% being post graduates and 39% being

graduates. Around 6% of the samples collected were undergraduates.

0%

5%

10%

15%

20%

25%

30%

35%40%

No. of respondents

6%

39% 40%

1%

14%

Undergr a

dua

tesGr aduates

Postgr aduates

Others

No response

8/9/2019 Mutual Fund Report Final

http://slidepdf.com/reader/full/mutual-fund-report-final 45/66

45

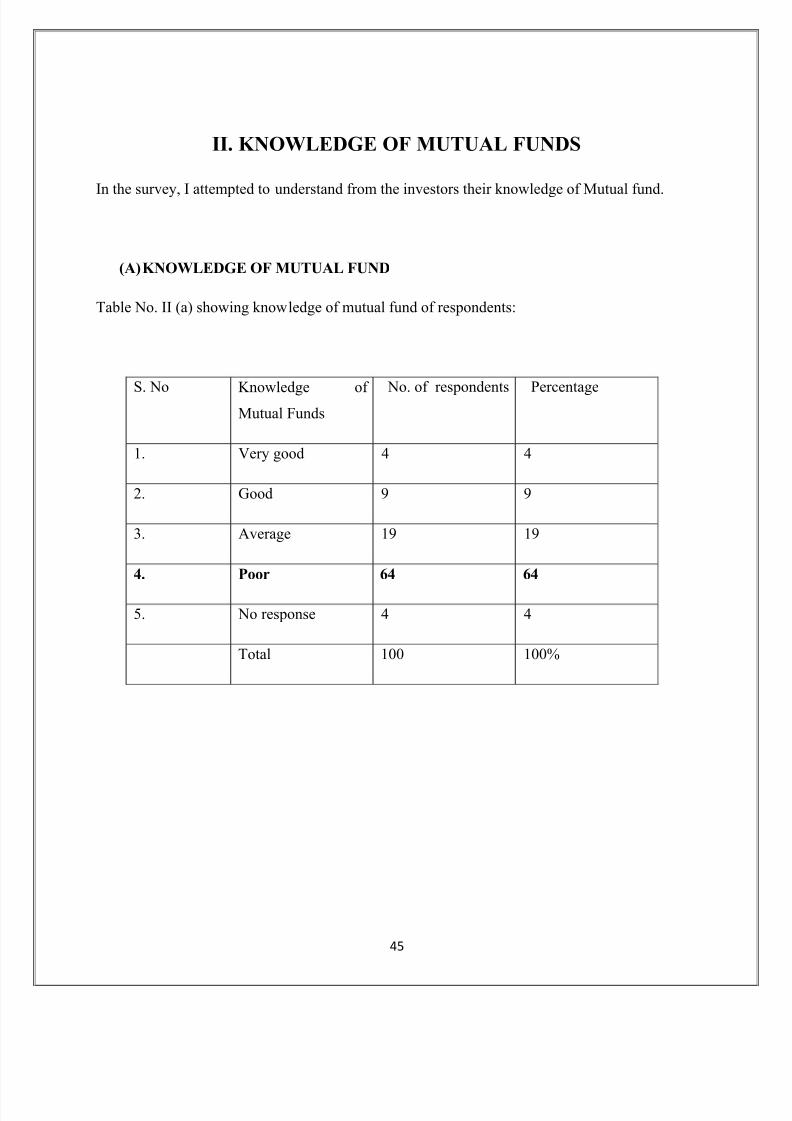

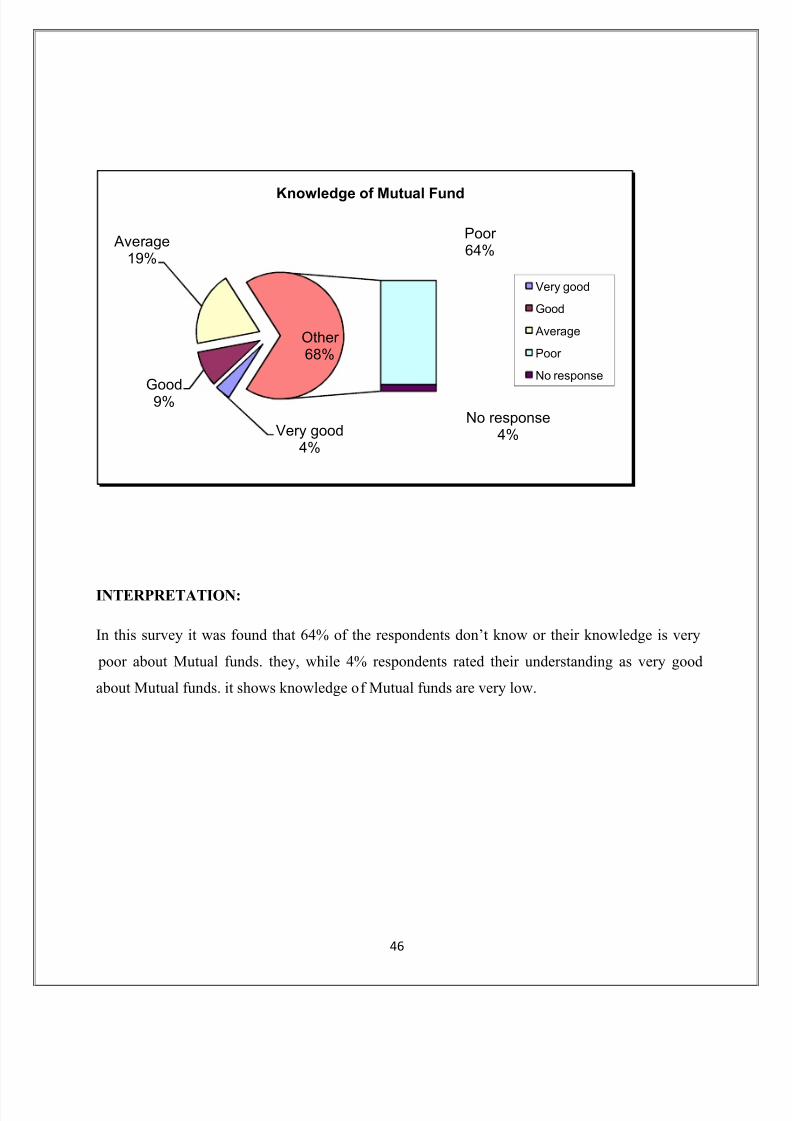

II. KNOWLEDGE OF MUTUAL FUNDS

In the survey, I attempted to understand from the investors their knowledge of Mutual fund.

(A) KNOWLEDGE OF MUTUAL FUND

Table No. II (a) showing knowledge of mutual fund of respondents:

S. No Knowledge of Mutual Funds

No. of respondents Percentage

1. Very good 4 4

2. Good 9 9

3. Average 19 19

4. Poor 64 64

5. No response 4 4

Total 100 100%

8/9/2019 Mutual Fund Report Final

http://slidepdf.com/reader/full/mutual-fund-report-final 46/66

46

INTERPRETATION:

In this survey it was found that 64% of the respondents don¶t know or their knowledge is very

poor about Mutual funds. they, while 4% respondents rated their understanding as very good

about Mutual funds. it shows knowledge of Mutual funds are very low.

Very good4%

Good9%

Aver age19%

Poor 64%

No response4%

Other 68%

Knowledge of Mutual Fund

Very good

Good

Aver age

Poor

No response

8/9/2019 Mutual Fund Report Final

http://slidepdf.com/reader/full/mutual-fund-report-final 47/66

47

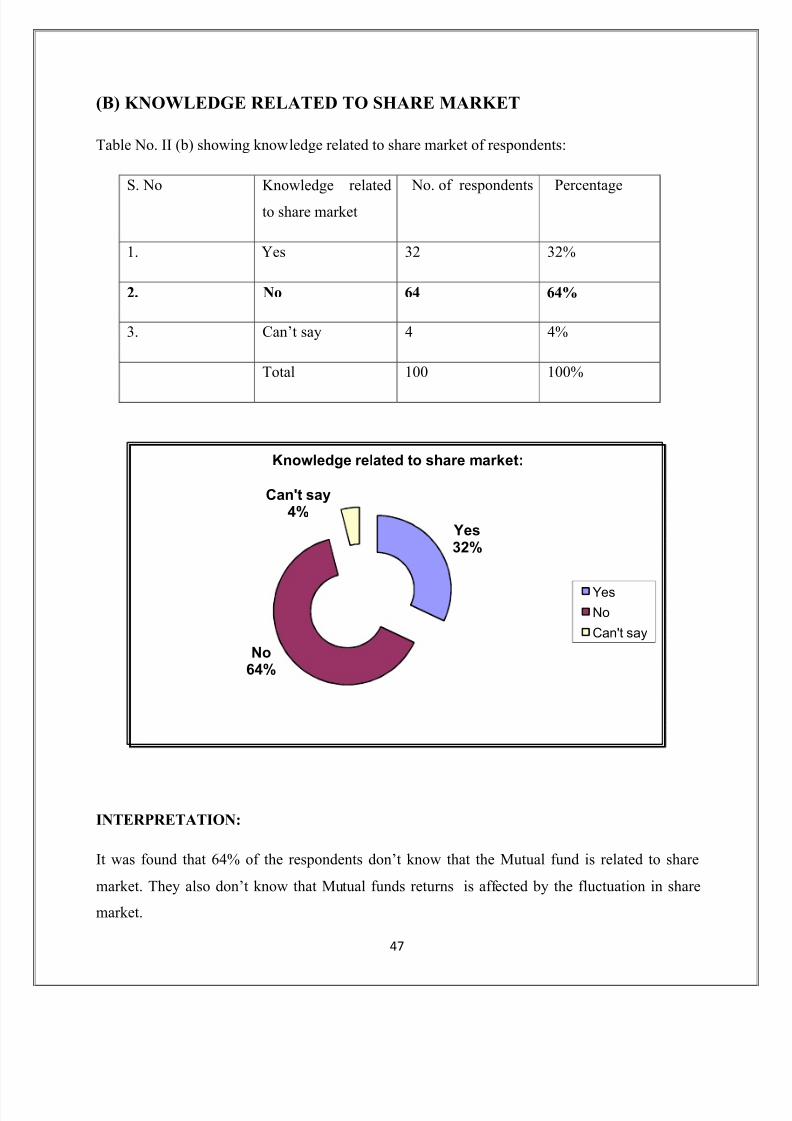

(B) KNOWLEDGE RELATED TO SHARE MARKET

Table No. II (b) showing knowledge related to share market of respondents:

S. No Knowledge related

to share market

No. of respondents Percentage

1. Yes 32 32%

2. No 64 64%

3. Can¶t say 4 4%

Total 100 100%

INTERPRETATION:

It was found that 64% of the respondents don¶t know that the Mutual fund is related to share

market. They also don¶t know that Mutual funds returns is affected by the fluctuation in share

market.

Yes32%

No64%

Can't say4%

Knowledge related to share market:

Yes

No

Can't say

8/9/2019 Mutual Fund Report Final

http://slidepdf.com/reader/full/mutual-fund-report-final 48/66

48

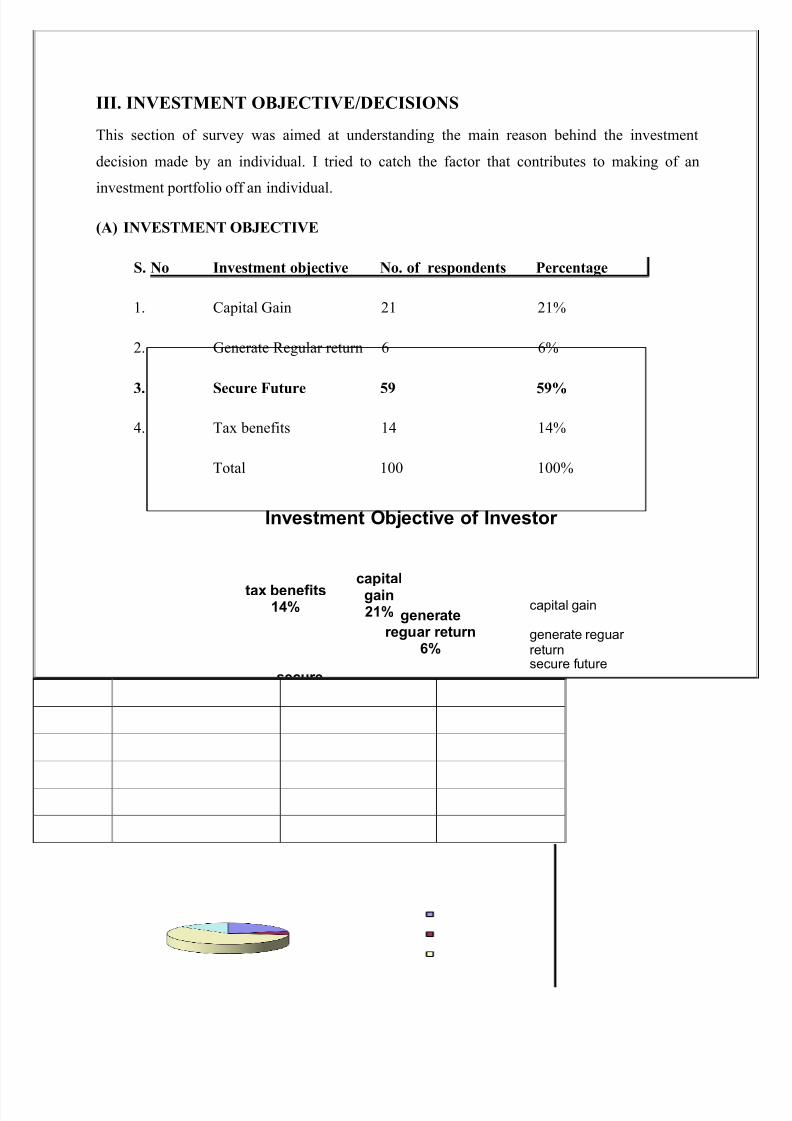

III. INVESTMENT OBJECTIVE/DECISIONS

This section of survey was aimed at understanding the main reason behind the investment

decision made by an individual. I tried to catch the factor that contributes to making of an

investment portfolio off an individual.

(A) INVESTMENT OBJECTIVE

S. No Investment objective No. of respondents Percentage

1. Capital Gain 21 21%

2. Generate Regular return 6 6%

3. Secure Future 59 59%

4. Tax benefits 14 14%

Total 100 100%

INTERPRETATION: Total number of 100 responses was generated for this question and

multiple responses were sought for the various investment objectives. the analysis brings out the

fact that investor were more concerned about the secure future(59%) and capital gains(21%), and

after that they considered tax benefits(14%) and regular return(6%) as their main investment

objectives.

capitalgain21% gener ate

reguar return6%

securefuture

59%

tax benefits14%

Investment Objective of Investor

capital gain

gener ate reguar returnsecure f uture

8/9/2019 Mutual Fund Report Final

http://slidepdf.com/reader/full/mutual-fund-report-final 49/66

49

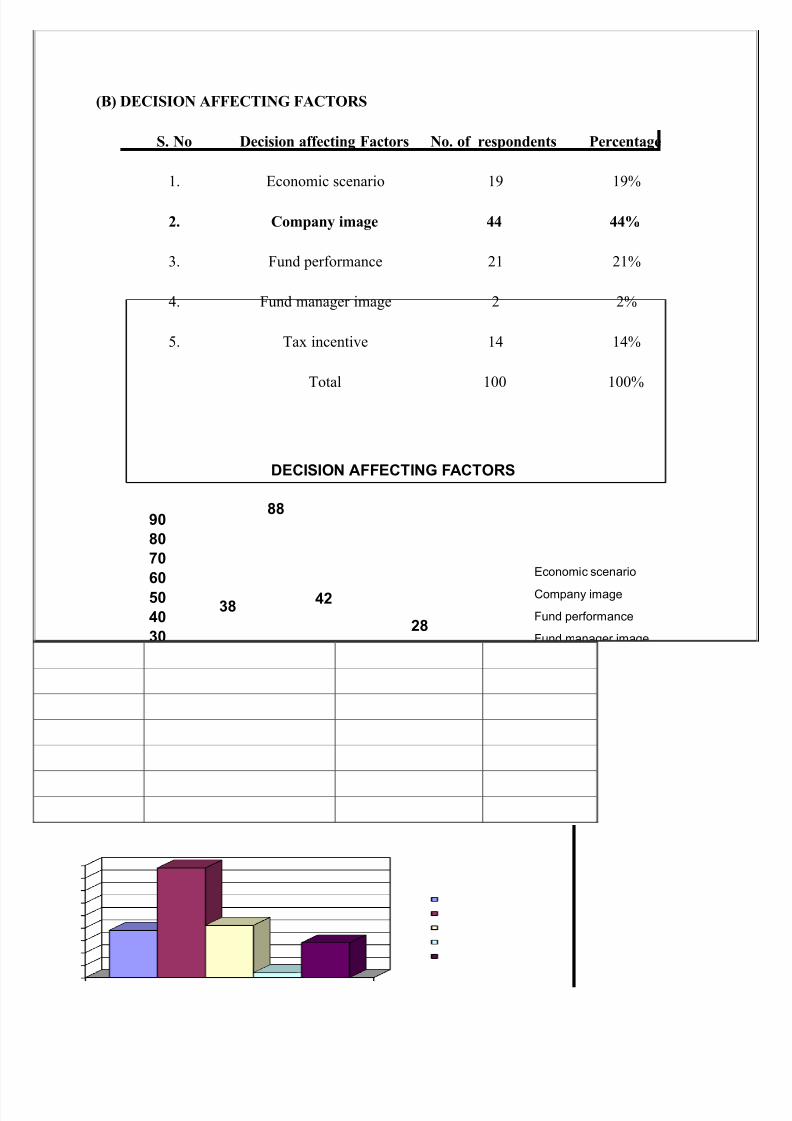

(B) DECISION AFFECTING FACTORS

S. No Decision affecting Factors No. of respondents Percentage

1. Economic scenario 19 19%

2. Company image 44 44%

3. Fund performance 21 21%

4. Fund manager image 2 2%

5. Tax incentive 14 14%

Total 100 100%

INTERPRETATION:

There are certain overall factors that tend to affect the investment decision of the investor, such

as economic scenario. I tried to know the respondents opinion on these macro factors that further

tend to affect their investment decisions. This survey showed that company image acts as the

determining factor for their investment with 44%.the second most important factor was fund

performance (21%) and economic scenario (19%).

0

10

20

30

40

50

60

70

80

90

No. of Respondents

38

88

42

4

28

DECISION AFFECTING FACTORS

Economic scenario

Company image

Fund performance

Fund manager image

Tax incentive

8/9/2019 Mutual Fund Report Final

http://slidepdf.com/reader/full/mutual-fund-report-final 50/66

50

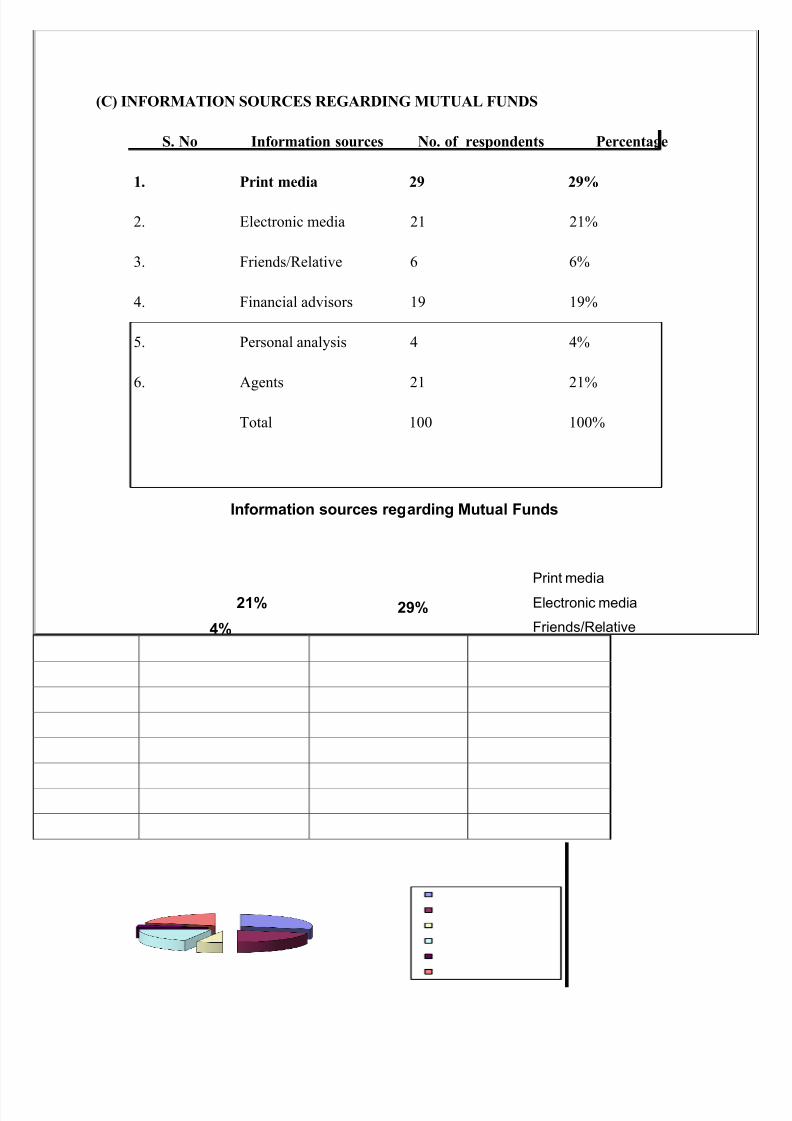

(C) INFORMATION SOURCES REGARDING MUTUAL FUNDS

S. No Information sources No. of respondents Percentage

1. Print media 29 29%

2. Electronic media 21 21%

3. Friends/Relative 6 6%

4. Financial advisors 19 19%

5. Personal analysis 4 4%

6. Agents 21 21%

Total 100 100%

INTERPRETATION:

In this survey I asked from the respondents about the kind of media that affect their investment

decision.29% of the respondents said that the print media is the major influencer in making the

investment decisions, electronic media(21%) and agents(21%) were the second major influencer

in investment decision making.

29%

21%6%19%

4%

21%

Information sources regarding Mutual Funds

Print media

Electronicmedia

Friends/Relative

Financial advisors

Personal analysis

Agents

8/9/2019 Mutual Fund Report Final

http://slidepdf.com/reader/full/mutual-fund-report-final 51/66

51

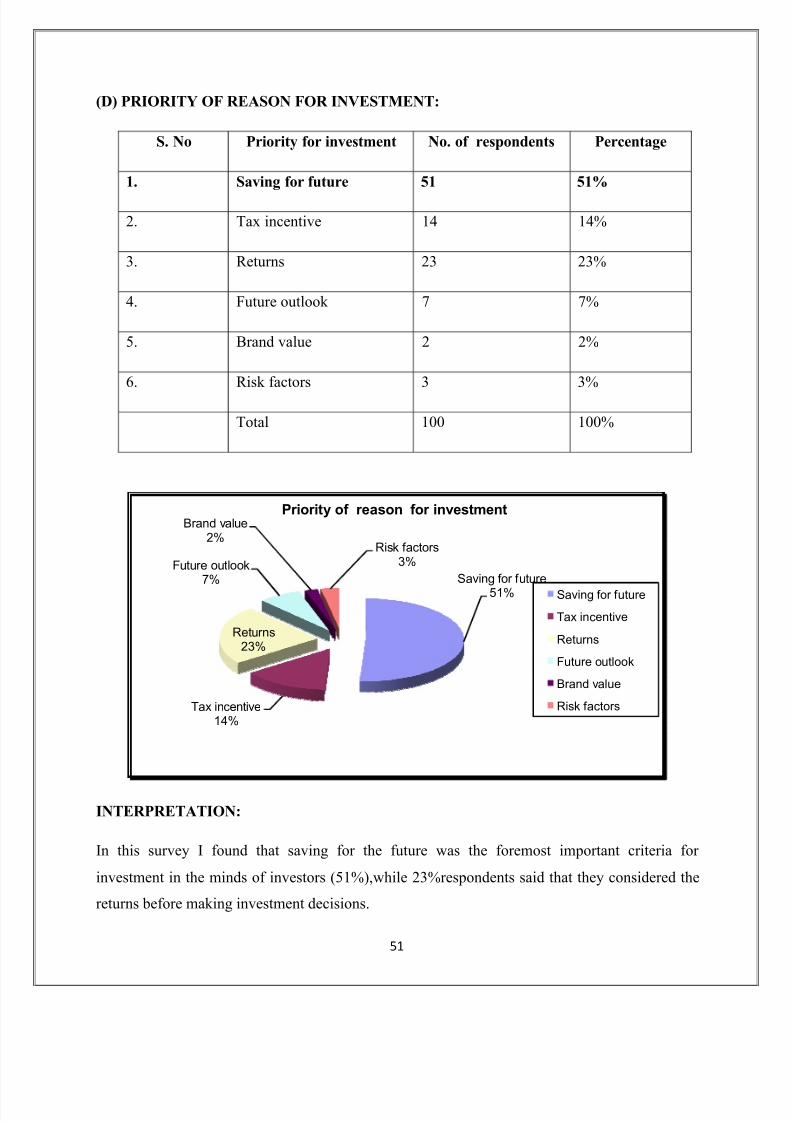

(D) PRIORITY OF REASON FOR INVESTMENT:

S. No Priority for investment No. of respondents Percentage

1. Saving for future 51 51%

2. Tax incentive 14 14%

3. Returns 23 23%

4. Future outlook 7 7%

5. Brand value 2 2%

6. Risk factors 3 3%

Total 100 100%

INTERPRETATION:

In this survey I found that saving for the future was the foremost important criteria for

investment in the minds of investors (51%),while 23%respondents said that they considered the

returns before making investment decisions.

Saving for f uture

51%

Tax incentive14%

Returns23%

Future outlook7%

Br and value2%

Risk f actors3%

Priority of reason for investment

Saving for f uture

Tax incentive

Returns

Future outlook

Br and value

Risk f actors

8/9/2019 Mutual Fund Report Final

http://slidepdf.com/reader/full/mutual-fund-report-final 52/66

52

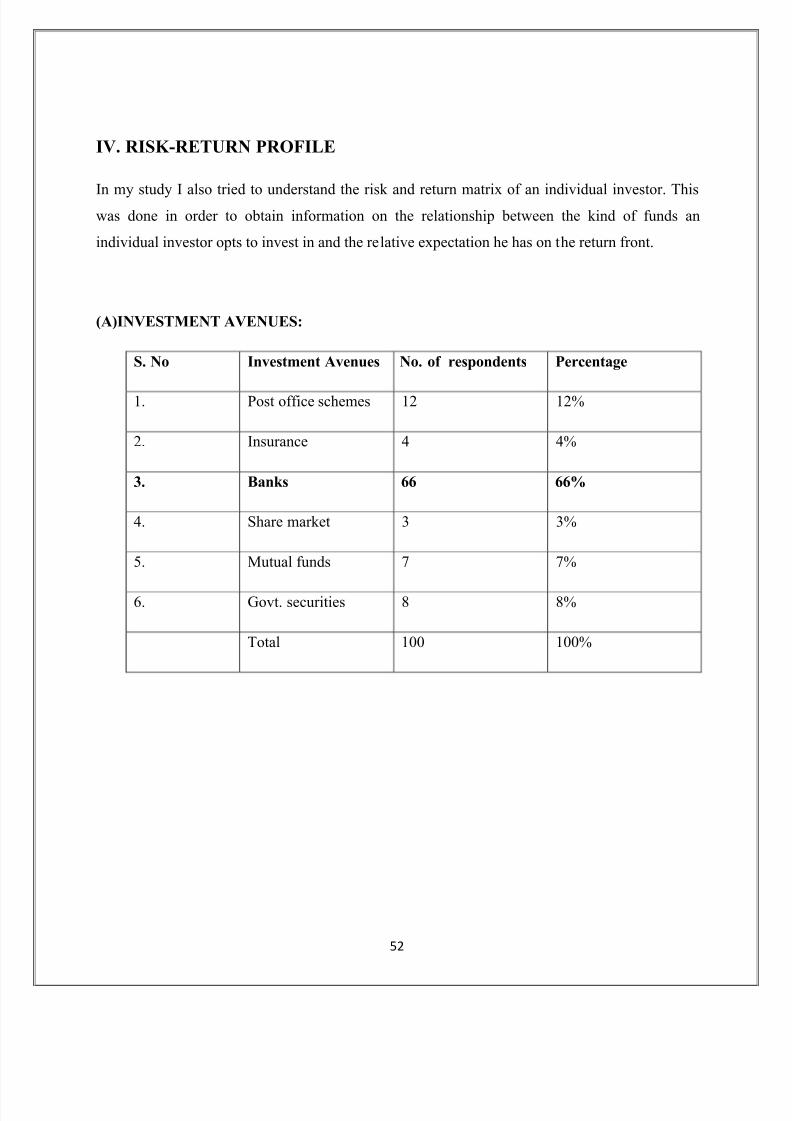

IV. RISK-RETURN PROFILE

In my study I also tried to understand the risk and return matrix of an individual investor. Thiswas done in order to obtain information on the relationship between the kind of funds an

individual investor opts to invest in and the relative expectation he has on the return front.

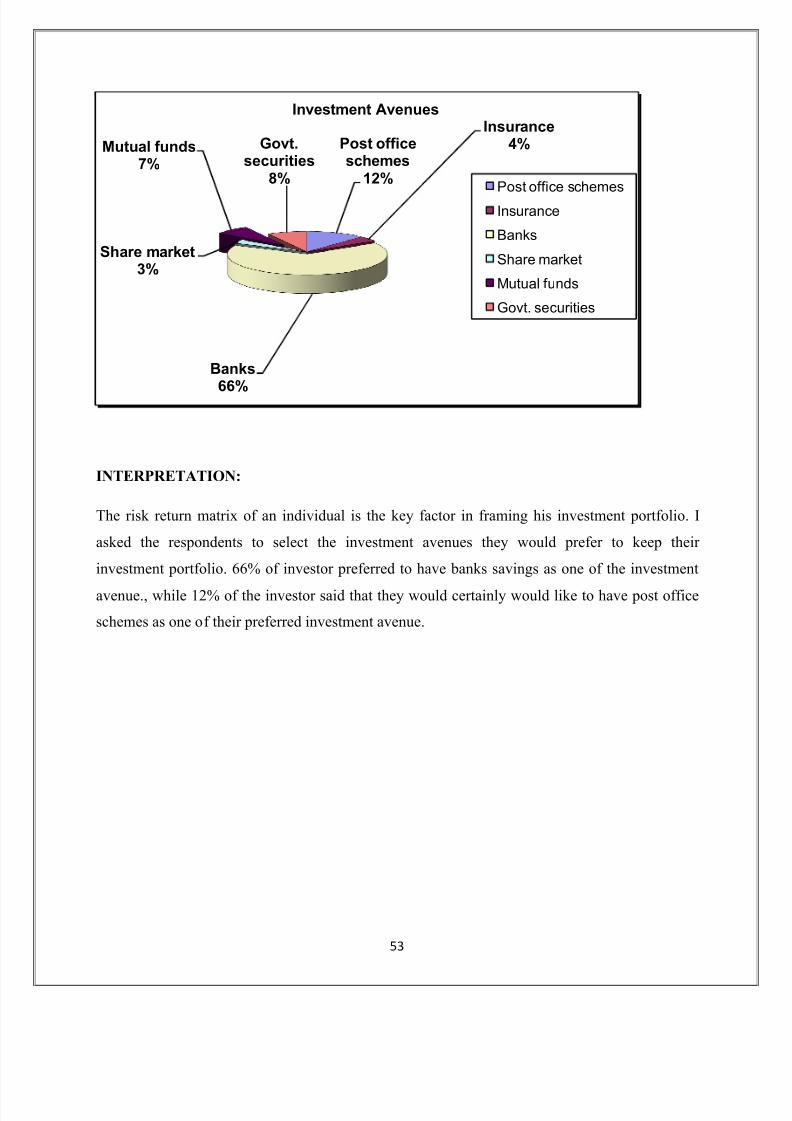

(A)INVESTMENT AVENUES:

S. No Investment Avenues No. of respondents Percentage

1. Post office schemes 12 12%

2. Insurance 4 4%

3. Banks 66 66%

4. Share market 3 3%

5. Mutual funds 7 7%

6. Govt. securities 8 8%

Total 100 100%

8/9/2019 Mutual Fund Report Final

http://slidepdf.com/reader/full/mutual-fund-report-final 53/66

53

INTERPRETATION:

The risk return matrix of an individual is the key factor in framing his investment portfolio. I

asked the respondents to select the investment avenues they would prefer to keep their

investment portfolio. 66% of investor preferred to have banks savings as one of the investment

avenue., while 12% of the investor said that they would certainly would like to have post office

schemes as one of their preferred investment avenue.

Post officeschemes

12%

Insur ance4%

Banks66%

Share market3%

Mutual funds7%

Govt.securities

8%

Investment Avenues

Post office schemes

Insur ance

Banks

Share mar ket

Mutual f unds

Govt. securities

8/9/2019 Mutual Fund Report Final

http://slidepdf.com/reader/full/mutual-fund-report-final 54/66

54

(B) RETURN EXPECTATION FROM MUTUAL FUNDS

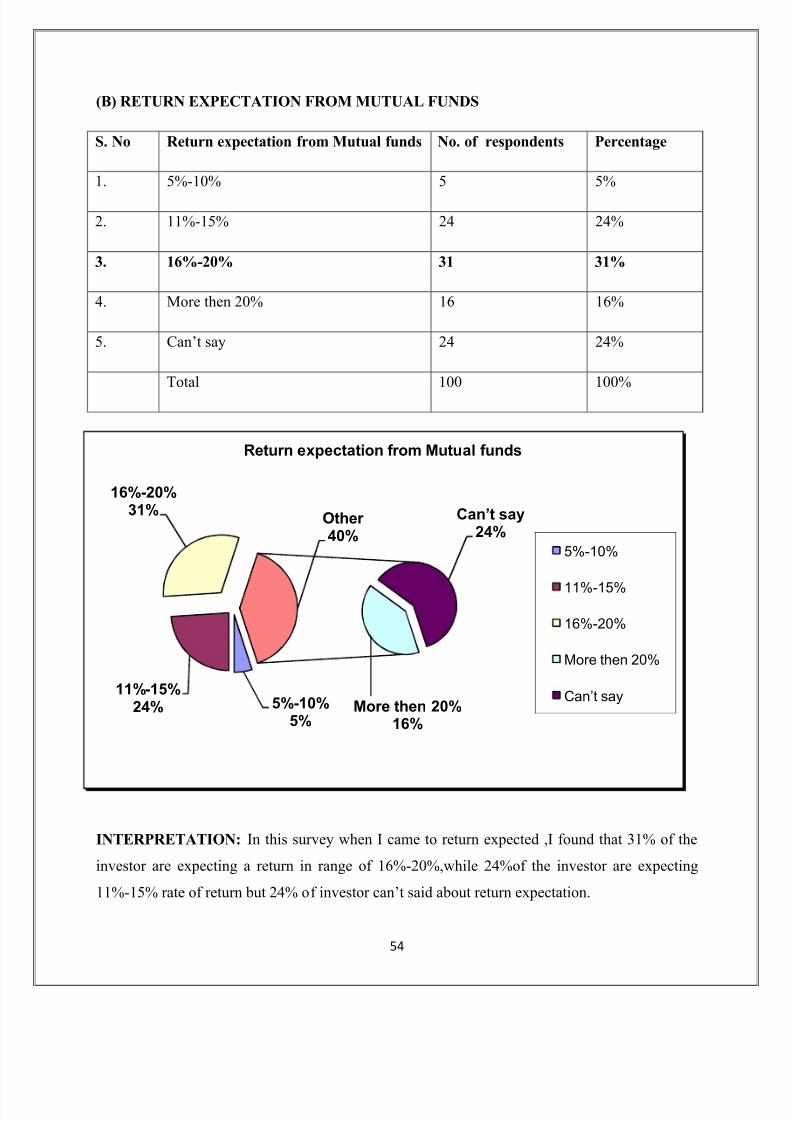

S. No Return expectation from Mutual funds No. of respondents Percentage

1. 5%-10% 5 5%

2. 11%-15% 24 24%

3. 16%-20% 31 31%

4. More then 20% 16 16%

5. Can¶t say 24 24%

Total 100 100%

INTERPRETATION: In this survey when I came to return expected ,I found that 31% of the

investor are expecting a return in range of 16%-20%,while 24%of the investor are expecting

11%-15% rate of return but 24% of investor can¶t said about return expectation.

5%-10%

5%

11%-15%

24%

16%-20%

31%

More then 20%

16%

Can¶t say24%

Other 40%

Return expectation from Mutual funds

5%-10%

11%-15%

16%-20%

More then 20%

Can¶t say

8/9/2019 Mutual Fund Report Final

http://slidepdf.com/reader/full/mutual-fund-report-final 55/66

55

(C) INVESTMENT PATTERN PREFERRED IN MUTUAL FUND BY INVESTOR:

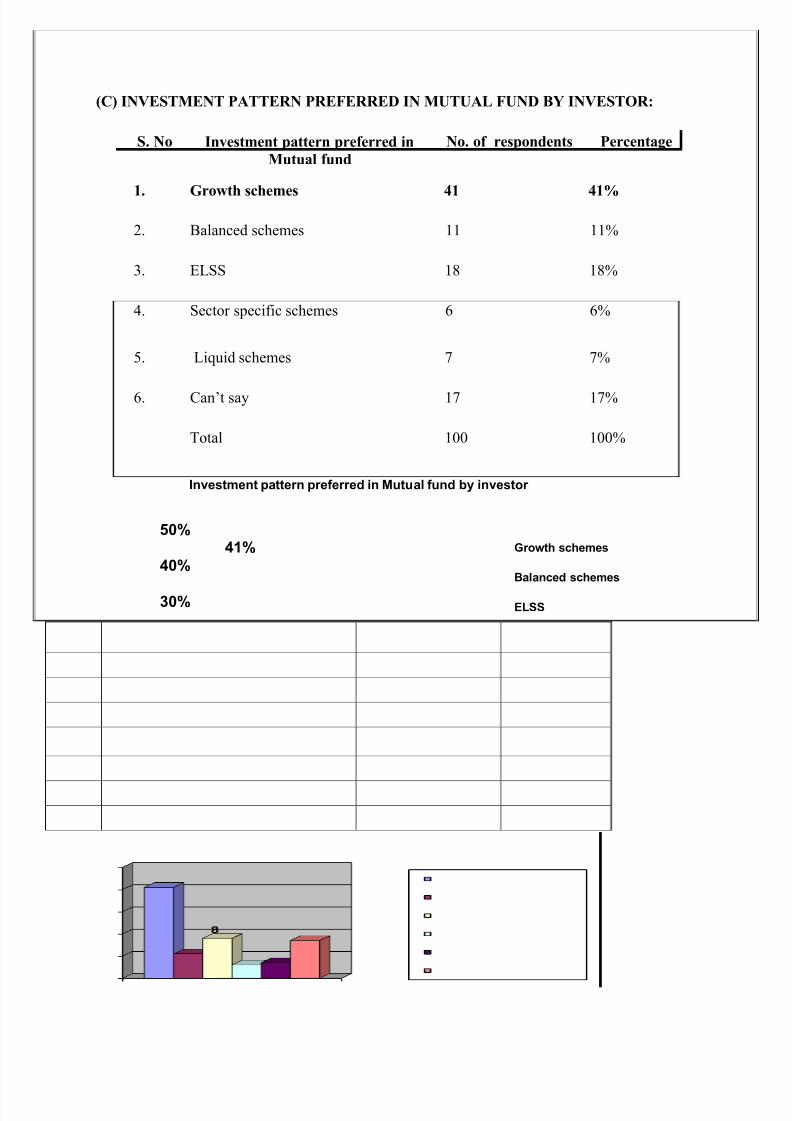

S. No Investment pattern preferred in

Mutual fund

No. of respondents Percentage

1. Growth schemes 41 41%

2. Balanced schemes 11 11%

3. ELSS 18 18%

4. Sector specific schemes 6 6%

5. Liquid schemes 7 7%

6. Can¶t say 17 17%

Total 100 100%

INTERPRETATION:

The type of schemes selected for investment depends largely on the risk return matrix of an

individual and the time horizon of his investment. My findings demonstrate that 41% of

investors prefer to invest in growth schemes,18% of investor in ELSS schemes.

0%

10%

20%

30%

40%

50%

No. of respondents

41%

11%

1 %

6% 7%

17%

Investment pattern preferred in Mutual fund by investor

Growth schemes

Balanced schemes

ELSS

Sector specific schemes

Liquid schemes

Can¶t say

8/9/2019 Mutual Fund Report Final

http://slidepdf.com/reader/full/mutual-fund-report-final 56/66

56

(D) SOURCES OF PRODUCT INFORMATION

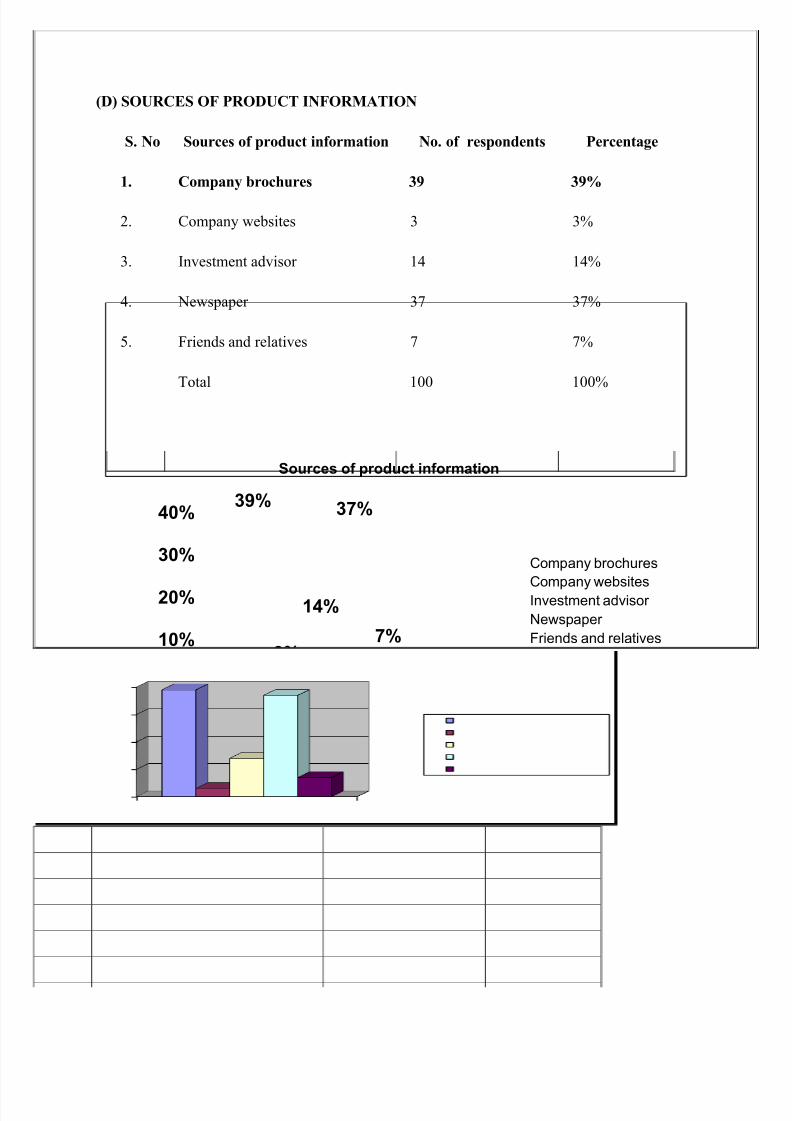

S. No Sources of product information No. of respondents Percentage

1. Company brochures 39 39%

2. Company websites 3 3%

3. Investment advisor 14 14%

4. Newspaper 37 37%

5. Friends and relatives 7 7%

Total 100 100%

INTERPRETATION:

This chart represents the different sources of product information, through which investor

generally tend to know regarding the mutual fund¶s new schemes and products.39% of the

respondents said that they receive the product information from the company brochures and 37%

of the respondents said that they get it from newspaper.

0%

10%

20%

30%

40%

No. of respondents

39%

3%

14%

37%

7%

Sources of product information

Company brochures

Compa

ny websitesInvestment advisor

Newspaper

Friends and relatives

8/9/2019 Mutual Fund Report Final

http://slidepdf.com/reader/full/mutual-fund-report-final 57/66

57

Chapter 6

FINDINGS FROM THE ANALYSIS

8/9/2019 Mutual Fund Report Final

http://slidepdf.com/reader/full/mutual-fund-report-final 58/66

58

FINDINGS FROM THE SURVEY:

The following findings were attained out of the survey conducted.

y

Some People were less interested in knowing about the product.

y They have the impression that these funds are not safe, as the money is locked in for a

particular period, which is known as the lock in period.

y Mutual funds, in a country like India is in its growth stage and it would take some time to

enter into the maturity stage.

y People investing into mutual funds basically invest at the financial year-end.

y They invest into these funds mostly for tax saving purposes other than investment or

return purposes.

8/9/2019 Mutual Fund Report Final

http://slidepdf.com/reader/full/mutual-fund-report-final 59/66

59

Chapter - 7

RECOMMENDATIONS

8/9/2019 Mutual Fund Report Final

http://slidepdf.com/reader/full/mutual-fund-report-final 60/66

60

RECOMMENDATIONS :

y There should be more awareness made about the ICICI mutual fund and their services by

giving more advertisement.

y ICICI mutual fund should organize some events to build its Brand Image in the minds of

the people.

y As per customer¶s point of view, they feel that ICICI mutual fund should open more

number of branches for the convenience of people.

CONCLUSION

AS been analyzed people are very rarely aware of mutual funds as people were not properly

educated about the policies but when made aware they wanted to get more information about the

funds by this we can say that mutual fund is in its infant stage today but it will reach its growth

stage within no time. Mutual funds in this competitive world is very helpful for the people who

are interested into investments as this particular fund can take less investment but give u hefty.

8/9/2019 Mutual Fund Report Final

http://slidepdf.com/reader/full/mutual-fund-report-final 61/66

8/9/2019 Mutual Fund Report Final

http://slidepdf.com/reader/full/mutual-fund-report-final 62/66

62

Questionnaire

Name :

Age :

Gender :

Income :

Saving habits :

Qualification :

Q1. Do you know about the Mutual Funds?

(a) Very good (b) Good (c) Average (d) Poor

(e) No response

Q2. What is your objective /motive behind investment ?

(a) Capital gain (b) Generate regular

(c) Secure future (d) Tax benefits

Q3. Where do you generally invest/save?

(a)Post office schemes (b)Insurance (c)Banks

(d)Share market (e)Mutual funds (f)Govt. securities

8/9/2019 Mutual Fund Report Final

http://slidepdf.com/reader/full/mutual-fund-report-final 63/66

63

Q4. How do you prioritize the reason for investment?

[Rank from 1-5, 1 being highest priority]

Saving for future __________

Tax incentives __________

Returns __________

Future outlook __________

Brand value __________

Risk factor __________

Q5. How did you come to know about mutual fund?

(a) Print media (b) Electronic media (c) Friend/relative

(d) Financial advisor/C.A (c) Personal analysis (f) Agents

Q6. What factors affect your decision for investment in Mutual Fund?

(a) Economic scenario (b) Company image (c) Fund performance

(d) Fund manager image (e) Tax incentive

8/9/2019 Mutual Fund Report Final

http://slidepdf.com/reader/full/mutual-fund-report-final 64/66

64

Q7. How much return you expect from Mutual Fund?

(a)5%-10% (b)11% -15% (c)16%-20%

(d)more than 20% (e)can¶t say

Q8. What kind of investment pattern you prefer in Mutual Fund ?

(a) Growth schemes (b) Balanced schemes (c) ELSS

(d) Sector specific schemes (e) Income schemes (f) Liquid schemes