Embed Size (px)

Citation preview

Municipal Excess Liability Joint Insurance Fund Parsippany. New Jersey

Comprehensive Annual Financial Report For the Years Ended December 31. 2012 and 2011

MUNICIPAL EXCESS LIABILITY JOINT INSURANCE FUND TABLE OF CONTENTS

INTRODUCTORY SECTION (Unaudited)

Letter of Transmittal Roster of Officials and Consultants Organizational Chatt Membership Listing

FINANCIAL SECTION

Independent Auditors' RepOlt

DECEMBER3!. 2012

Management's Discussion and Analysis (Unaudited)

Basic Financial Statements: Statement of Net Position Statement of Revenue, Expenses and Changes in Net Position Statement of Cash Flows Notes to Financial Statements

Required Supplementary Information: (Unaudited) Comparative Reconciliation of Claims Liabilities by Fund Ten-Year Claims Development Information

Combining Supplementary Schedules: Combining Schedule of Net Position Combining Schedule of Operations and Changes in Net Position

Supplementary Data: (Unaudited) Historical Operating Results Analysis (Schedule A) Historical Balance Sheet (Schedule B) Fund Year Operating Results Analysis (Schedule C) Fund Year Account Operating Results Analysis (Schedule D) Fund Year Claims Analysis (Schedule E) Fund Year Expense Analysis (Schedule F) Program Summary (Schedule G) Analysis of Cash and Investments Analysis of Excess Insurance Receivable Analysis of Assessments Receivable Analysis of Other Receivables Analysis of Prepaid Expense Analysis of Excess Insurance Expenses Payable Analysis of Administrative Expenses Payable Analysis of Miscellaneous Liabilities

RepOlt Pursuant to Governmental Auditing Standards: RepOlt on Internal Control Over Financial Reporting and on Compliance and Other Matters Based on an Audit of Financial Statements Performed in Accordance with Government Auditing Standards

Page

1-3 4-5

6 7

8-10 11-12

13 14 15 16

17-26

27 28 29

30 31 32

33 34 35

36-40 41-44 45-48 49-52

53 54 54 55 55 56 56 57 57

58

59-60

MUNICIPAL EXCESS LIABILITY JOINT INSURANCE FUND TABLE OF CONTENTS

DECEMBER 31, 2012

STATISTICAL SECTION (Unaudited)

Schedule of Net Position by Component Schedule of Change in Net Position Member Growth Analysis - by Fund Year Reported Loss History - by Fund Year Reported Claim Activity - by Fund Year

(Continued)

61

62 63 64 65 66

INTRODUCTORY SECTION

Municipal Excess Liability Joint Insurance Fund

April 15,2013

Executive Committee Municipal Excess Liability Joint Insurance Fund 9 Campus Drive, Suite 16 Parsippany, NJ 07054

Dear Executive Committee Members:

9 Campus Drive, Suite 16 Parsippany, New Jersey 07054 Tel (201) 881-7632 Fax (201) 881-7633

1

The Comprehensive Annual Financial Report (CAFR) of the Municipal Excess Liability Joint Insurance Fund (MEL) for the year ended December 31,2012 is hereby respectfully submitted. Responsibility for the accuracy of the presented data and the completeness and fairness of the presentation, including all disclosures, rests with the MEL. We believe the data, as presented, are accurate in all material respects; that they are presented in a manner designed to fairly set forth the financial position and results of the operations of the MEL as measured by the financial activity of its various membership years; and that all disclosures necessary to enable the reader to gain the maximum understanding of the MEL's financial affairs have been included ..

The CAFR is presented in three sections: introductory, financial, and statistical. The introductory section contains this transmittal letter, substantive highlights of the year, a list of the MEL's members, a list of the MEL's officers and an organizational chart. The financial section includes a management discussion and analysis of the financial activities, the basic financial statements, as well as the independent auditors' opinion on the basic financial statements. State schedules are provided pursuant to the specifications of the NJ Department of Banking and Insurance, which, along with the Department of Community Affairs, exercises regulatory control over the MEL. The statistical section includes selected data covering the years that the MEL has been operational.

The MEL was fonned under State statutes which authorize local government entities to pool resources to meet risk management needs. Specifically, along with local joint insurance funds, the MEL administers a program of self funding and commercial insurance, and reinsurance that provides protection to members in the areas of workers' compensation, and automobile, general and professional liability. The MEL also purchases excess property insurance for its affiliated JIPs under a cooperative purchasing arrangement. The MEL perfonns a number of tasks in accomplishing this mission, including contracting for support services such as claims and litigation management, loss control services and training, financial management and reporting, actuarial services, and general management.

Economic Conditions and Outlook

The MEL's economic condition and its outlook continue to be strong. The MEL has provided its members with stable assessments, a long history of dividends, comprehensive insurance, and responsive service. These factors have resulted in steady growth. While the MEL is not expected to continue to grow at its historic rate because its market share is now so large, marginal growth or at least membership stability is expected.

2 MEL Initiatives

2012 marks the 25th Anniversary of the Municipal Excess Liability Joint Insurance Fund.

The MEL's Investment Committee reviewed Asset Management options received following its combined Joint Insurance Fund and Health Insurance Fund Request for Proposals. Committee worked with counsel to develop a Unitized Investment Trust. Effort has continued into 2013.

The MEL held its second annual all-day educational seminar for commissioners, municipal personnel, risk managers and vendor personnel. This seminar is eligible for continuing educational credits for: CFO/CMFO, Public Works, Clerks and insurance producers. The agenda includes the organization and operation of joint insurance fund, the latest trends in claims, and governmental ethics.

The MEL joined with Munich Re, the League of Municipalities, the NJ Association of Chiefs of Police and various other insurance companies to participate in a non-profit organization known as the Safety Institute of New Jersey. The Safety Institute's mission will be to build a culture of safety through legislative advocacy and by mobilizing and educating citizens to take ownership of safety programs in their communities.

The MEL Safety Training Institute (MSI), which began offering regionally scheduled safety training programs in 2003 has begun the process of adding on-line and webinar training. The development of these programs began in 2012 with a targeted operational date in 2013.

The MEL JIP updated its webpage to comply with the latest state informational requirements that had a February 2013 compliance deadline.

Financial Management and Control

The financial statements have been prepared in conformity with generally accepted accounting principles as promulgated by the Governmental Accounting Standards Board and necessarily include amounts based upon reliable estimates and judgments. The MEL's books are maintained on a full accrual basis. A summary of significant accounting policies is discussed in more detail in the notes to the financial statements found in the financial section. The MEL's financial statements differ from the State schedules listed in the supplementary data section as Schedules A through F, as discussed in Note 11 to the financial statements.

Internal Acconnting Structnre

The MEL's accounting system is organized so that each membership year, and line of coverage within each year, can be evaluated separately. The assets, liabilities, revenues, and expenses of each year and line of coverage are reported separately on a full accrual basis. This practice is necessary because the composition of the MEL's membership, and the extent of participation within each line of coverage, varies from year to year.

The MEL's management is responsible for establishing and maintaining an internal control structure designed to ensure that assets are protected from loss, theft, or misuse and to ensure that adequate accounting data are compiled to allow for the preparation of financial statements in conformity with generally accepted accounting principles. Internal accounting controls are designed to provide reasonable assurance that these objectives are being met. The concept of reasonable assurance recognizes that the cost of a control should not exceed the benefits likely to be derived and that the evaluation of costs and benefits requires estimates and judgments by management. All internal control decisions are made within the above framework. Management believes that the MEL's internal accounting controls adequately safeguard assets and provide reasonable assurance of proper recording of financial transactions.

3

Investment Management

MEL investments are made in. accordance with the Local Fiscal Affairs Law and the Fund's Cash and Investment Management Plan. Investments for the year were limited to US Treasury Securities, agency issues, deposits in banks covered by the Governmental Unit Depository Act, and deposits in the New Jersey Cash Management Plan, which is administered by the State of New Jersey's Division of Investments. In planning and executing investments, the MEL emphasizes liquidity and safety. After these objectives are met, the MEL seeks to optimize investment income. The MEL protects itself from realization of capital losses by maintaining the ability to hold all investment. to maturity. Investments with maturities of longer than six months are made by a professional asset manager from the trust department of TD Bank, which is overseen by the Fund Treasurer and the Investment Committee. Short term investments are usually limited to bank deposits and the New Jersey Cash Management Fund, and are undertaken by the Fund Treasurer. Agency issues with a maturity longer than 12 months are purchased in cooperation with the NJ Division ofInvestment.

As of December 31,2012, the MEL's portfolio consisted of the following:

Percentage of Amount Total

Checking Accounts $ 15,046,167 20.49% New Jersey Cash Management 1,067,291 1.45% Investments 57,320,850 78.06%

$ 73,434,308 100.00%

Independent Audit

Nisivoccia LLP, independent accountants, provide an independent, objective review of the fairness of the MEL's reported financial position and results of operations. Their audit includes procedures they deem necessary to express an opinion as to the fairness of the financial statements. Their opinion is included in the financial section of this report.

Acknowledgments

Our sincere appreciation is expressed to the members of the MEL Audit Committee for the leadership they provided in the expansion and improvement of the MEL's financial reporting format.

Our appreciation is also extended to each MEL commissioner, and particularly to Executive and Advisory Committee members, for their commitment to risk management and intergovernmental risk pooling.

Respectfully submitted,

'Dauid 1t C)ut& David N. Grubb, Executive Director

MUNICIPAL EXCESS LIABILITY JOINT INSURANCE FUND ROSTER OF OFFICIALS AND CONSULTANTS

DECEMBER 31, 2012

Joseph Wolk Thomas Nolan MeghanJack Christopher Marion Paul Shives Robert Landolfi Richard Hirsch Gary La Venia Jon Rheinhardt Carol Byrne Charles Cuccia David Johnson Mauro Tucci Andrew Brannen Joseph D' Arco John Salvatore William Cottman Anthony Vangeli Roger Butler

Perma Risk Management Services David N. Grubb James J. Kickham

Michael Zambito Dorsey& Semrau, Esqs. Russell Huntington, Esq. Nisivoccia LLP Actuarial Advantage

CB Botta & Associates Qual-Lynx Qual-Lynx Qual-Lynx

Qualcare

Conner StronglBuckelew

Arthur J Gallagher Risk Management Svcs, Inc.

Parente Beard

Carr Riggs & Ingram

TD Bank Wealth Advisors

Fund Chairman Fund Secretary Fund Commissioner Fund Commissioner Fund Commissioner Fund Commissioner Fund Commissioner Fund Commissioner Fund Commissioner Fund Commissioner Fund Commissioner Fund Commissioner Fund Commissioner Fund Commissioner Fund Commissioner Fund Commissioner Fund Commissioner Fund Commissioner Fund Commissioner

Administrator Executive Director Deputy Executive Director

Treasurer Attorney Deputy Attorney Auditor Actuary

Claims Administrators - Excess Liability Claims Administrators - Public OfficiallEPL Claims Administrators - Excess Property Claims Administrators - Worker's Compensation

Managed Care Provider

Underwriting Manager

Producer

Internal Auditor - Insurance Component

Internal Auditor - Financial Component

Asset Manager

4

MUNICIPAL EXCESS LIABll.JTY JOINT INSURANCE FUND ROSTER OF OFFICIALS AND CONSULTANTS

DECEMBER 31. 2012

R.Bent

Kathleen Wilkinson, Esq.

JA Montgomery Risk Control

La Mendola Associates

EFitz Art

New Tech

Lobbyist

Technical Writer

Safety Consultant and MSI Training

Independent Strategic Planner & Communication Consultant

Graphic Designer

Website - Monthly Hosting

5

Commissioners Appt b Members

Executive Dlr/Adm PERMA

Technical Writer K. Wilkinson

Lobbyist R. Bent

Underwriting

MUNICIPAL EXCESS LIABILITY JOINT INSURANCE FUND 2012 ORGANIZATIONAL CHART

I

Board of Fund Commissioners

I H I I Attorney I Deputy Attorney

F. Semrau /J. Dorsey R. Huntington H I I

I I Treasurer l Defense H I L M. Zambito Attorneys

I J Claims POL H I I Qual-Lynx

Claims Excess H I Qual-Lynx Conner Strona/Buckelew I CB Botta & Associates

H Actuary ~ Actuarial Advantage Safety Consultant

- JA Montgomery Risk Control H

Asset Manager

~ TO Bank

Long Range Planner/ --1 Producer

Arthur J. Gallagher RMS H Internal Auditor -Parente Beard and

Carr Riggs & Ingram H ---i Managed Care Qualcare

Strategic Planner r-La Mendola Associates H --1 Graphic Designer I Efitz Art

Y

6

Auditor I NisivQccia LLP

Strategic I Planning

Coverage I Committee

Audit

J Committee

Investment I Committee

Legislative I Committee

Rules and I Contracts

Nominating I Committee

Member/Marketing I Committee

Safety &

J Training

Police I Accreditation

Claims I Review Committee

MUNICIPAL EXCESS LIABILITY JOINT INSURANCE FUND MEMBERSHIP LISTING

AS OF DECEMBER 31. 2012

Atlantic County Municipal Joint Insurance Fund (42 Municipalities)

Bergen County Municipal Joint Insurance Fund (38 Municipalities)

Burlington County Municipal Joint Insurance Fund (25 Municipalities)

Camden County Municipal Joint Insurance Fund (34 Members)

Central Jersey Joint Insurance Fund (8 Municipalities)

GloucesterlSalemlCumberiand Counties Municipalities Joint Insurance Fund (36 Municipalities)

Mid Jersey Municipal Joint Insurance Fund (13 Municipalities)

Monmouth Municipal Joint Insurance Fund (37 Municipalities)

Morris County Municipal Joint Insurance Fund (39 Municipalities)

New Jersey First Responders Joint Insurance Fund (24 Districts)

New Jersey Public Housing Authorities Joint Insurance Fund (89 Authorities)

New Jersey Self Insurers' Joint Insurance Fund (8 Municipalities and 1 Regional Fire and Rescue Squad)

New Jersey Utility Authorities Joint Insurance Fund (73 Authorities)

Ocean County Municipal Joint Insurance Fund (31 Municipalities)

Professional Municipal Management Joint Insurance Fund (4 Municipalities)

Public Alliance Insurance Coverage Fund (26 Municipalities, 1 Authority and 1 County)

South Bergen Municipal Joint Insurance Fund (23 Municipalities)

Suburban Essex Municipal Joint Insurance Fund (11 Member Entities)

Suburban Municipal Joint Insurance Fund (10 Municipalities)

7

FINANCIAL SECTION

8

ONISIVOCCIAup Certified Public Accountants & Advisors Mount Arlington Corporate Center

200 Valley Road, Suite 300 Mt. Arlington, NJ 07856

973-328-1825[973-328-0507 Fax

Independent Auditors' Report

The Honorable Chairperson and Members of the Board of Fund Commissioners Municipal Excess Liability Joint Insurance Fund Parsippany, New Jersey

Report on the Financial Statements

Lawrence Business Center 11 Lawrence Road Newton, NJ 07860

973-383-66991973-383-6555 Fax

We have audited the accompanying financial statements of the Municipal Excess Liability Joint Insurance Fund (the "Fund") as of and for the years ended December 31,2012 and 2011, and the related notes to the financial statements, which collectively comprise the Fund's basic financial statements as listed in the table of contents.

Management's Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error.

Auditor's Responsibility

Our responsibility is to express opinions on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America, audit requirements prescribed by the Division of Local Government Services, Department of Community Affairs, State of New Jersey, and the standards applicable to financial audits contained in Government Auditing Standards. issued by the Comptroller General of the United States. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor's judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity's preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity's internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

www.nisivoccia.com Independent Member of BKR International

The Honorable Chairperson and Members of the Board of Fund Commissioners

Municipal Excess Liability Joint Insurance Fund Page 2

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinions.

Opinions

In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of the Fund as of December 31,2012 and 2011, and the changes in financial position and cash flows thereof for the years then ended in accordance with accounting principles generally accepted in the United States of America.

Other Matters

Required Supplementary Information

Accounting principles generally accepted in the United States of America require that the Management's Discussion and Analysis and the accompanying Comparative Reconciliation of Claims Liabilities by Fund and Ten-Year Claims Development Information Schedules be presented to supplement the basic financial statements. Such information, although not a part of the basic financial statements, is required by the Governmental Accounting Standards Board who considers it to be an essential part of financial reporting for placing the basic financial statements in an appropriate operational, economic, or historical context. We have applied certain limited procedures to the required supplementary information in accordance with auditing standards generally accepted in the United States of America, which consisted of inquiries of management about the methods of preparing the information and comparing the information for consistency with management's responses to our inquiries, the basic financial statements, and other knowledge we obtained during our audit of the basic financial statements. We do not express an opinion or provide any assurance on the information because the limited procedures do not provide us with sufficient evidence to express an opinion or provide any assurance.

Supplementary and Other Information

Our audit was conducted for the purpose of forming opinions on the financial statements that collectively comprise the Fund's basic financial statements. The introductory section, supplementary data, combining supplementary schedules, and statistical section are presented for purposes of additional analysis and are not a required part of the basic financial statements.

The combining supplementary schedules are the responsibility of management and were derived from and relate directly to the underlying accounting and other records used to prepare the basic financial statements. Such information has been subjected to the auditing procedures applied in the audit of the basic financial statements and certain additional procedures, including comparing and reconciling such information directly to the underlying accounting and other records used to prepare the basic financial statements or to the basic financial statements themselves, and other additional procedures in accordance with aUditing standards generally accepted in the United States of America. In our opinion, the combining supplementary schedules are fairly stated, in all material respects, in relation to the basic financial statements as a whole.

The introductory section, supplementary data, and statistical section have not been subjected to the auditing procedures applied in the audit of the basic financial statements, and accordingly, we do not express an opinion or provide any assurance on it.

9

The Honorable Chairperson and Members of the Board of Fund Commissioners

Municipal Excess Liability Joint Insurance Fund Page 3

Other Reporting Required by Government Auditing Standards

In accordance with Government Auditing Standards, we have also issued our report dated April 15, 2013 on our consideration of the Fund's internal control over financial reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements and other matters. The purpose of that report is to describe the scope of our testing of internal control over financial reporting and compliance and the results of that testing, and not to provide an opinion on internal control over financial reporting or on compliance. That report is an integral part of an audit performed in accordance with Government Auditing Standards in considering Fund's internal control over financial reporting and compliance.

Mount Arlington, New Jersey April 15, 2013

/1/~l..C/1 NISIVOCClA LLP

10

MUNICIPAL EXCESS LIABILITY JOINT INSURANCE FUND Management Discnssion and Analysis

(Unaudited)

11

This section of the annual financial report of the Fund presents a discussion and analysis of the financial performance of the Fund for the year ended December 31, 2012. Please read it in conjunction with the basic financial statements, the notes, and supplementary schedules that follow this section.

Overview of Basic Financial Statements

The Fund's basic financial statements are prepared on the basis of accounting principles generally accepted in the United States of America for governmental entities and insurance enterprises where applicable. The primary purpose of the Fund is to provide excess property and casualty insurance for joint insurance funds that are members of the Fund. The Fund maintains separate enterprise funds by incurred years and line of coverage. The basic financial statements are presented on an accrual basis of accounting. The three basic financial statements presented are as follows:

Statement of Net Position - This statement presents information reflecting the Fund's assets, liabilities, and net position. Net position represents the amount of total assets less total liabilities.

Statement of Revenue, Expenses, and Changes in Net Position - This statement reflects the Fund's operating revenues and expenses, as well as non-operating items during the reporting period. The change in net position for an enterprise fund is similar to net profit or loss for any other insurance company.

Statement of Cash Flows - The statement of cash flows is presented on the direct method of reporting, which reflects cash flows from operating and investing activities. Cash collections and payments are reflected in this statement to arrive at the net increase or decrease in cash for the fiscal year.

Financial Highlights

The following tables summarize the financial position and results of operations for the Fund as of and for the years ended December 31,2012,2011 and 2010.

SUMMARY OF STATEMENT OF NET POSITION 11/12 10111 Percent Percent

2012 2011 Change 2010 Change ASSETS:

Cash and Cash Equivalents, Investments and Accrued Interest Receivable $ 73,556,074 $ 80,966,575 -9.15% $ 76,194,467 6.26%

Assessments Receivable 2,065,710 10,872,986 -81.00% 14,233,002 -23.61% Investment in Joint Venture 899,714 1,083,646 -16.97% 1,306,723 -17.07% Other Assets 3,635,456 3,043,031 19.47% 5,559,541 -45.26%

Total 80,156,954 95,966,238 -16.47% 97,293,733 -1.36%

LIABILITIES: Loss Reserves 57,104,193 71,371,105 -19.99% 77,839,198 -8.31 % Other Liabilities and Reserves 2,176,705 2,943,192 -26.04% 742,042 296.63%

Total 59,280,898 74,314,297 -20.23% 78,581,240 -5.43%

NET POSITION $ 20,876,056 $ 21,651,941 -3.58% $ 18,712,493 15.71 %

12

SUMMARY OF STATEMENT OF REVENUE, EXPENSES, AND CHANGES IN NET POSITION 11/12 10/11

Percent Percent 2012 2011 Change 2010 Change

Operating Revenue: Assessments and Other Income $43,245,446 $43,756,127 -1.17% $57,156,175 -23.44%

Operating Expenses: Provision for Claims & Claims Expense 6,999,622 9,291.311 -24.66% 27,208,859 -65.85% Assessment for Participation in RCF 16,384,865 11,781,164 39.08% 9,933,817 18.60% Insurance Premiums 15,709,983 16,184,424 -2.93% 16,599,145 -2.50% Administrative and Operating Expenses 5,361,882 5,029,169 6.62% 5,378,891 -6.50%

Total Operating Expenses 44,456,352 42,286,068 5.13% 59,120,712 -28.48%

Operating Income/(Loss) (1,210,906) 1,470,059 -182.37% (1,964,537) 174.83%

Non-Operating Income/(Expenses): Change in Investment in Joint Venture (183,932) (223,077) 17.55% (59,956) -272.07% Investment Income 618,953 1,692,466 -63.43% 655,152 158.33%

Increase/(Decrease) in Net Position $ (775,885) $ 2,939,448 -126.40% $ (1,369,341) 314.66%

The MEL's asset base decreased by 16.47% during the reporting period and cash and investments decreased by 9.15%. The "Investment in Joint Venture" represents the MEL's share of net assets in the Municipal Excess Liability Residual Claims Fund. The value of this asset decreased by 16.97% reflecting a decrease in equity retained by that entity.

The MEL's liabilities decreased by 20.23% primarily due to an 19.99% decrease in loss reserves.

For 2012 assessments decreased slightly by 1.17%.

For 2011 assessments decreased by 23.44%, due the fact that effective 111111 the MEL transferred public official and employment practices liability coverage to the commercial market.

The provision for claims and claims expense decreased by 24.66%. Insurance premiums decreased by 2.93%, while administrative and operating expenses increased by 6.62%.

Investment income decreased by 63.43% due to the low interest rate environment.

For 2012, the MEL continued the policy started in 2004 of not issuing dividends. The MEL emphasized capital accumulation over continuity of dividends for the members.

The MEL's combined net position for all years is $20,876,056 in 2012 compared to $21,651,941 at the end of 2011; a decrease of 3.58%. Net position values for both reporting periods include the cumulative effect of the discounting of loss reserves.

The future financial position of the MEL will be impacted by medical costs trends that impact upon workers compensation costs. To address this cost area, the MEL continues to reevaluate its managed care contracts and procedures and closely monitor claims.

The MEL and its members were increasingly affected by the development of employment practice laws in 2010 and prior years. To address this problem, the MEL and its sub-committees pursued various options to control these costs and decided to transfer the coverage to the commercial market for 2011. XL Specialty Insurance Company agreed to provide the coverage based on the 2010 pricing and agreed to a two-year commitment.

13

BASIC FINANCIAL STATEMENTS

MUNICIPAL EXCESS LIABILITY JOINT INSURANCE FUND

STATEMENT OF NET POSITION

December 31 2012

ASSETS:

Current Assets: Cash and Cash Equivalents $ 16,113,458

Investments 57,320,850

Assessments Receivable 2,065,710

Accounts Receivable Notes Receivable 237,251 Accrued Interest Receivable 121,766

Insurance Receivables 1,426,443 Due from Municipal Excess Liability Residual Claims Fund 906,296

Prepaid Expenses 92,217 Investment in Joint Venture 899,714

Total Current Assets 79,183,705

Long-Term Assets:

Notes Receivable 973,249 Total Long-Term Assets 973,249

Total Assets 80,156,954

LIABILITIES:

Loss Reserves 57,104,193 Accounts Payable - Vendors 111,964

Other Liabilities 2,064,741

Total Liabilities 59,280,898

NET POSITION:

Unrestricted 20,876,056

Total Net Position $ 20,876,056

THE ACCOMPANYING NOTES TO FINANCIAL STATEMENTS ARE AN INTEGRAL PART OF THIS STATEMENT

2011

$ 10,127,882 70,602,344 10,872,986

12,652 56,000

236,349 2,175,504

628,754

1,083,646 95,796,117

170,121 170,121

95,966,238

71,371,105 265,636

2,677,556

74,314,297

21,651,941

$ 21,651,941

14

MUNICIPAL EXCESS LIABILITY JOINT INSURANCE FUND STATEMENT OF REVENUE, EXPENSES, AND CHANGES IN NET POSITION

Year Ended December 31 2012

Operating Revenue: Assessments from Participating Members $ 43,245,446

Total Operating Revenue 43,245,446

Operating Expenses: Provision for Claims and Claim Adjustment Expense (Net of Reinsurance

of $5,500,803 and $8,895,080 for 2012 and 2011, respectively) 6,999,622 Assessment for Participation in Municipal Excess Liability

Residual Claims Fund 16,384,865 Insurance Premiums 15,709,983 Claims Administration 1,093,718 Other Contractual Services 2,445,527 Non-Contractual Expenses 87,923 Administration 918,536 Insurance Brokerage Expense 469,749 Risk Management Fees 346,429

Total Operating Expenses 44,456,352

Operating Income/(Loss) (1,210,906)

Non-Operating Income/(Expenses): Change in Investment in Joint Venture (183,932) Investment Income 618,953

Change in Net Position (775,885)

Net Position - Beginning of Year 21,651,941

Net Position - End of Year $ 20,876,056

THE ACCOMPANYING NOTES TO FINANCIAL STATEMENTS ARE AN INTEGRAL PART OF THIS STATEMENT

2011

$ 43,756,127

43,756,127

9,291,311

11,781,164 16,184,424

1,075,156 2,176,048

77,853 899,573 460,538 340,001

42,286,068

1,470,059

(223,077) 1,692,466

2,939,448

18,712,493

$ 21,651,941

15

MUNICIPAL EXCESS LIABILITY JOINT INSURANCE FUND STATEMENT OF CASH FLOWS

Year Ended December 31 2012

Cash Flows from Operating Activities: Assessments Collected $ 52,052,722 Refunds 15,672,264 Claims Expense (36,938,798) Professional and Administrative Expenses (7,192,313) Insurance Premiums (14,960,922) Municipal Excess Liability Residual Claims Fund (16,662,407)

Net Cash Provided/(Used) by Operating Activities (8,029,454)

Cash Flows from Investing Activities: Purchase of Investment Securities (59,813,349) Proceeds from Sales and Maturities of Investment Securities 73,028,349 Investment Income 800,030

Net Cash Provided/(Used) by Investing Activities 14,015,030

Net Increase/(Decrease) in Cash and Cash Equivalents 5,985,576

Cash and Cash Equivalents, January 1 10,127,882

Cash and Cash Equivalents, December 31 $ 16,113,458

Reconciliation of Operating Income/(Loss) to Net Cash Provided/(Used) by Operating Activities:

Operating Income/(Loss) $ (1,210,906) Adjustments to Reconcile Operating Income/(Loss) to Net Cash Provided/(Used) by Operating Activities:

Changes in Assets and Liabilities: (Increase)lDecrease in Assets:

Assessments Receivable 8,807,276 Insurance Receivables 749,061 Due from Municipal Excess Liability Residual Claims Fund (277,542) Accounts Receivable 12,652 Prepaid Expense (92,217) Notes Receivable (984,379)

Increase/(Decrease) in Liabilities: Loss Reserves (14,266,912) Accounts Payable (153,672) Other Liabilities (612,815)

Net Cash Provided/(Used) by Operating Activities $ (8,029,454)

THE ACCOMPANYING NOTES TO FINANCIAL STATEMENTS ARE AN INTEGRAL PART OF THIS STATEMENT

2011

$ 47,116,143 4,300,899

(20,060,303) (2,786,792)

(15,734,844) (9,755,461)

3,079,642

(72,782,150) 59,813,500

834,784

(12,133,866)

(9,054,224)

19,182,106

$ 10,127,882

$ 1,470,059

3,360,016 449,580

2,025,703 (12,652)

53,879

(6,468,093) 37,898

2,163,252

$ 3,079,642

16

MUNICIPAL EXCESS LIABILITY JOINT INSURANCE FUND NOTES TO FINANCIAL STATEMENTS

DECEMBER 31, 2012

NOTE I: NATURE OF OPERATIONS

The Municipal Excess Liability Joint Insurance Fund (the "Fund") was created on December 16, 1986, in accordance with PL 1983, C.372, entitled "An act concerning joint insurance funds for local units of government, and supplementing Chapter 10 of Title 40A of the New Jersey statutes". The Fund is both an insured and self-administered group of joint insurance funds established for the purpose of providing low-cost insurance coverage for the members in order to keep local property taxes and fees at a minimum for the municipalities and authorities who form the membership of the joint insurance funds. The participating joint insurance funds must be able to prove satisfactorily to the Fund their compliance with funding and underlying coverage criteria as annually agreed and approved by the Fund. The Fund has 19 members. The following coverages are offered by the Fund to its members:

a) Excess Workers' Compensation and Employers' Liability b) Excess Liability Other than Motor Vehicles c) Excess Motor Vehicle d) Public Officials'lEmployment Practices Liability (For Fund Years 2009 and 2010 only) e) Excess Property t) Volunteer Directors and Officers Liability

Fund members are subject to supplemental assessments in the event of deficiencies. If the assets of the Fund were to be exhausted, members would be responsible for the Fund's liabilities. The Fund considers anticipated investment income when determining if a deficiency exists.

A participating member must remain in the Fund for the full term of membership unless terminated earlier by a majority vote of the Fund Commissioners or a two-thirds vote of the Executive Committee for nonpayment of assessments or continued noncompliance after written notice to comply with the bylaws or other obligations. Termination may occur only after proper notice has been given, in accordance with the Fund's bylaws.

The Executive Director and Administrator are responsible for the overall administration of the Fund. Fees paid to the Executive Director and Administrator encompasses all administrative duties which are performed at their offices. Accordingly, the Fund does not maintain any capital assets or incur any payroll expense.

NOTE 2: SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

The Governmental Accounting Standards Board (GASB) is the accepted standard-setting body for establishing government accounting and financial reporting principles. The more significant of the Fund's accounting policies are described on the next page.

17

MUNICIPAL EXCESS LIABILITY JOINT INSURANCE FUND NOTES TO FINANCIAL STATEMENTS

DECEMBER 31, 2012 (Continued)

NOTE 2: SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Cont'd)

Reporting Entity

Government Accounting Standards Board publication Codification of Government Accounting and Financial Reporting Standards, Section 2100, "Defining the Financial Reporting Entity" establishes standards to determine whether a governmental component unit should be included in the financial reporting entity. The basic criterion for inclusion or exclusion from the financial reporting entity is the exercise of oversight responsibility over agencies, boards and commissions by the primary government and financial accountability. The exercise of oversight responsibility includes financial interdependency and a resulting financial benefit or burden relationship, selection of governing authority, designation of management, ability to significantly influence operations, and accountability for fiscal matters. In addition, certain legally separate, tax-exempt entities that meet specific criteria (i.e. benefit of economic resources, access/entitlement to economic resources, and significance) should be included in the financial reporting entity. The combined financial statements include all funds of the Fund over which the Fund exercises operating control. There were no additional entities required to be included in the reporting entity under the criteria as described above, in the current fiscal year. Furthermore, the Fund is not includable in any other reporting entity on the basis of such criteria.

Basis of Accounting

The Fund utilizes the accrual basis of accounting whereby revenue is recorded as earned and expenses are reflected as the liability is incurred. The Fund utilizes total economic resources as the measurement focus. Operating revenue, such as charges for services, result from exchange transactions associated with the principal activity of the Fund. Exchange transactions are those in which each party receives and gives up essentially equal value. Nonoperating revenue, such as subsidies and investment earnings, results from nonexchange transactions or ancillary activities. Nonexchange transactions, in which the Fund gives or receives value without directly receiving or giving equal value in exchange, generally do not occur, with the exception of investment earnings and the changes in joint ventures.

Investments

The Fund generally records certain investments at fair value and records the unrealized gains and losses as a part of investment income. Fair value is the amount at which an investment could be exchanged in a current transaction between willing parties.

Income Taxes

The Fund is a tax-exempt organization and is not subject to either federal or state income taxes.

18

MUNICIPAL EXCESS LIABILITY JOINT INSURANCE FUND NOTES TO FINANCIAL STATEMENTS

DECEMBER 31, 2012 (Continued)

NOTE 2: SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Cont'd)

Assessments

The gross claim fund assessment is detennined by the actuary and, when combined with expense and premium projections, constitutes the Fund's budget. Assessments for participating joint insurance funds are detennined by underwriting criteria established by the Board of Commissioners.

Unpaid Claims Liabilities

The Fund establishes claims liabilities based on estimates of the ultimate cost of claims that have been reported but not settled, and of claims that have been incurred but not reported. The length of time for which such costs must be estimated varies depending on the coverage involved. Estimated amounts of salvage and subrogation and reinsurance recoverable on unpaid claims are deducted from the liability for unpaid claims. Because actual claims costs depend on such complex factors as inflation, changes in doctrines of legal liability, and damage awards, the process used in computing claims liabilities does not necessarily result in an exact amount, particularly for coverages such as general liability. Claims liabilities are recomputed periodically using a variety of actuarial and statistical techniques to produce current estimates that reflect recent settlements, claim frequency, and other economic and social factors. A provision for inflation in the calculation of estimated future claims costs is implicit in the calculation because reliance is placed both on actual historical data that reflect past inflation and on other factors that are considered to be appropriate modifiers of past experience. The Fund discounts claim liabilities for financial reporting purposes. Adjustments to claims liabilities are charged or credited to expense in the periods in which they are made.

Reinsurance

The Fund uses reinsurance agreements to reduce its exposure to large losses on certain types of insured events. Reinsurance pennits recovery of a portion of losses from reinsurers, although it does not discharge the primary liability of the Fund as direct insurer of the risks reinsured. The Fund does not report reinsured risks as liabilities unless it is probable that those risks will not be covered by reinsurers. Reinsurance premiums amounted to $15,709,983, and $16,184,424 for the years ended December 31,2012 and 2011, respectively. Premiums were reduced for financial reporting purposes by experience refunds from the reinsurer of $-0- for 2012 and 2011, respectively. The amount deducted from claims liabilities for reinsurance was $11,886,205 and $3,108,793 at December 31,2012 and 2011, respectively.

Management Estimates

The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of revenue and expenses during the reporting period. Actual results could differ from those estimates.

19

MUNICIPAL EXCESS LIABILITY JOINT INSURANCE FUND NOTES TO FINANCIAL STATEMENTS

DECEMBER 31. 2012 (Continued)

NOTE 3: LOSS RESERVES

The liability for unpaid losses and loss adjustment expenses represents an estimate of the ultimate net cost of all losses and loss adjustment expenses incurred but not yet paid as of December 31,2012. This estimate is based on the estimated ultimate cost of settling the claims considering the historical experience of the Fund, various other industry statistics, including the effects of inflation and other societal or economic factors. Management believes that the liability for unpaid losses is adequate to cover the ultimate cost of reported and unreported claims incurred but not yet paid. However, the ultimate cost may be more or less than the estimated liability. The unpaid losses are stated net of any recoveries from excess loss insurance and reinsurance coverages. The Fund has created a loss reserve for any reported and potential unreported losses which have taken place but in which the Fund has not received notices or reports oflosses.

Loss reserves, at December 31, 2012 and 2011, which have been estimated by the Fund's Actuary and Servicing Agents, are as follows:

2012 2011

Case Reserves $ 18,705,982 $ 28,885,071 Losses Incurred but not Reported 38,398,211 42,486,034

Total Loss Reserves $ 57,104,193 $ 71,371,105

The following represents changes in the aggregate reserves for the Fund:

2012 2011

Unpaid Claims and Claim Adjustment Expenses, Beginning of Year $ 71,371,105 $ 77,839,198

Incurred Claims and Claim Adjustment Expenses: Provision for Insured Events of the Current Period 16,926,886 17,829,061 (Decrease)lIncrease in Provision for Insured Events of Prior Years (9,927,264) (8,537,750)

Total Incurred Claims and Claim Adjustment Expenses 6,999,622 9,291,311

Payments: Claims and Claim Adjustment Expenses Attributable to Insured Events of the Current Period 1,496,244 1,499,370

Claims and Claim Adjustment Expenses Attributable to Insured Events of Prior Years 19,770,290 14,260,034

Total Payments 21,266,534 15,759,404

Total Unpaid Claims and Claim Adjustment Expenses, End of Year $ 57,104,193 $ 71,371,105

20

MUNICIPAL EXCESS LIABILITY JOINT INSURANCE FUND NOTES TO FINANCIAL STATEMENTS

DECEMBER 31. 2012 (Continued)

NOTE 3: LOSS RESERVES (Cont'd)

In accordance with the method allowed by GASB Statement No. 10, the Fund elected to discount its loss reserves beginning with the year ended December 31, 2003. The Fund believes that the discounting of loss reserves presents a more accurate presentation of the current loss reserves to be paid in future periods.

At December 31,2012, $64,103,491 of unpaid claims and claim adjustment expenses are presented at their net present value of $57,104,193. These claims are discounted at an annual rate of 3%.

At December 31, 2011, $79,869,222 of unpaid claims and claim adjustment expenses are presented at their net present value of $71,371,105. These claims are discounted at an annual rate of3%.

The Fund maintains contracts for insurance including excess insurance covering losses in excess of an amount established between the Fund and the insurer up to the limits of coverage set forth in the contract on a specific occurrence, or per accident or annual aggregate basis. The Fund also maintains a contract for reinsurance for Liability other than motor vehicle covering losses in excess of an amount established between the Fund and the Reinsurer up to the limits of coverage set forth in the contract on a specific occurrence or aggregate basis.

A contingent liability exists with respect to insurance coverage which would become an actual liability in the event the insuring companies, or any of them, might be unable to meet their obligations to the Fund under existing reinsurance agreements.

NOTE 4: CASH AND CASH EOUIV ALENTS

Cash and cash equivalents include amounts in deposits, money market accounts, short-term investments with original maturities of three months or less.

GASB Statement No. 40, Governmental Accounting Standards Deposit and Investment Risk Disclosures, requires disclosure of the level of custodial credit risk assumed by the Fund in its cash, cash equivalents and investments, if those items are uninsured or unregistered. Custodial risk is the risk that in the event of bank failure, the government's deposits may not be returned.

Interest Rate Risk - In accordance with its cash management plan, the Fund ensures that any deposit or investments matures within the time period that approximates the prospective need for the funds, deposited or invested, so that there is not a risk to the market value of such deposits or investments.

Credit Risk - The Fund limits its investments to those authorized in its cash management plan which are permitted under state statutes as detailed below.

New Jersey statutes permit the deposit of public funds in institutions located in New Jersey, which are insured by the Federal Deposit Insurance Corporation (FDIC) or by any other agencies of the United States that insure deposits or the State of New Jersey Cash Management Fund.

21

MUNICIPAL EXCESS LIABILITY JOINT INSURANCE FUND NOTES TO FINANCIAL STATEMENTS

DECEMBER 31, 2012 (Continued)

NOTE 4: CASH AND CASH EOUIV ALENTS (Cont'd)

New Jersey statutes require public depositories to maintain collateral deposits or public funds that exceed insurance limits as follows:

The market value of the collateral must equal 5% of the average daily balance of public funds; and

If the public funds deposited exceed 75% of the capital funds of the depository, the depository must provide collateral having a market value equal to 100% of the amount exceeding 75%.

All collateral must be deposited with the Federal Reserve Bank, the Federal Home Loan Bank Board or a banking institution that is a member of the federal reserve system and has capital funds of not less than $25,000,000.

As of December 31, 2012 and 2011, cash and cash equivalents of the Fund consisted of the following:

Checking Accounts Cash Management Funds

Dec. 31, 2012 $ 15,046,167

1,067,291

$ 16,113,458

Dec. 31, 2011 $ 9,061,192

1,066,690

$ 10,127,882

The carrying amount of the Fund's cash at cost as of December 31, 2012 and 2011 was $16,113,458 and $10,127,882 respectively. The bank balances as of December 31, 2012 and 2011 were $21,854,749 and $10,767,160, respectively. The $1,067,291 and $1,066,690 invested with the State of New Jersey Cash Management Fund is uninsured and unregistered.

NOTE 5: INVESTMENTS

New Jersey statutes permit the Fund to purchase the following types of investments:

(I) Bonds or other obligations of the United States of America or obligations guaranteed by the United States of America;

(2) Government money market mutual funds;

(3) Any obligation that a federal agency or a federal instrumentality has issued in accordance with an act of Congress, which security has a maturity date not greater than 397 days from the date of purchase, provided that such obligations bears a fixed rate of interest not dependent on any index or other external factor;

(4) Bonds or other obligations of local units or bonds or other obligations of school districts of which the local units are part or within which the school district is located;

22

MUNICIPAL EXCESS LIABILITY JOINT INSURANCE FUND NOTES TO FINANCIAL STATEMENTS

DECEMBER 31. 2012 (Continued)

NOTE 5: INVESTMENTS (Cont'd)

23

(5) Bonds or other obligations, having a maturity date not more than 397 days from the date of purchase, approved by the Division of Investment of the Department of the Treasury for investment by local units;

(6) Local government investment pools;

(7) Deposits with the State of New Jersey Cash Management Fund; or

(8) Agreements for the repurchase of fully collateralized securities if:

(a) the underlying securities are permitted investments pursuant to paragraph (1) and (3) above;

(b) the custody of collateral is transferred to a third party;

(c) the maturity of the agreement is not more than 30 days;

(d) the underlying securities are purchased through a public depository as defined in statute; and

(e) a master repurchase agreement providing for the custody and security of collateral is executed.

(9) Debt obligations of federal agencies or government corporations with maturities not to exceed 10 years from the date of purchase, excluding mortgage backed or derivative obligations, provided that the investments are purchased through the State Division of Investment and are invested consistent with the rules and regulations of the State Investment Council.

All of the Fund's investments are recorded at fair value based on quoted market prices. The investments are held by the Fund's custodial bank trust department in the Fund's name. The bank's trust department is also its agent in purchasing and selling the securities. The investments are uninsured and unregistered. All of the funds held by the custodial bank are held in a fiduciary account, in the Fund's name, and are backed by the full faith and credit of the U.S. Government. As such, they are protected in the event of bankruptcy of the bank. Investments at December 31, 2012 and 2011 consisted of the following:

Weighted Weighted Average Average

Balance Maturity Balance Maturity Dec. 31, 2012 in Months Dec. 31, 2011 in Months

United States Government Obligations $ 202,164 37.00

Federal Home Loan Bank $ 20,010,400 26.25 20,069,650 43.00

Federal National Mortage Association 30,288,680 48.09 30,239,630 50.60

Federal Home Loan Mortage Corporation 7,021,770 39.44 20,090,900 48.26

$ 57,320,850 39.41 $ 70,602,344 47.74

MUNICIPAL EXCESS LIABILITY JOINT INSURANCE FUND NOTES TO FINANCIAL STATEMENTS

DECEMBER 31. 2012 (Continued)

NOTE 6: NET POSITION

The State of New Jersey has no statutory minimum net position requirements.

The Fund had statutory basis accumulated deficit net position accounts as follows:

Fund Year 2009 - Public Officials'lEmployment Practices Fund Year 2009 - Faithful Performance Bond Fund Year 2010 - Liability Fund Year 2010 - Public Officials'lEmployment Practices Fund Year 2010 - Faithful Performance Bond Fund Year 2011 - Public Officials'lEmployment Practices Fund Year 2012 - Property Fund Year 2012 - Liability

$ 6,617,509 773,431 900,360 261,360 73,969 57,968

1,035,739 455,963

In addition to the above individual deficits, the Aggregate Excess Loss Fund Contingency also had an overall deficit of $1,953,868 at December 31, 2012. The Fund has no current plans to assess the membership to eliminate deficit balances.

NOTE 7: INSURANCE RECEIVABLES

Insurance receivables consist of funds due from an insurance company for claim reimbursements.

NOTE 8: MEMBERSHIP IN JOINT INSURANCE FUND

In 1995, the Fund became a member of the Municipal Excess Liability Residual Claims Fund (the "Residual Fund"). The Residual Fund is a risk-sharing public entity risk pool that is a selfadministered group of joint insurance funds established for the purpose of assuming and discharging the liabilities associated with loss reserves of participating members. The transfer of these loss reserves to the Residual Fund results in the closing of those fund years and the unencumbering of the net assets related to those closed fund years. Each member appoints an official to represent their respective joint insurance fund for the purpose of creating a governing body from which officers for the Residual Fund are elected.

As a member of the Residual Fund, the Fund could be subject to supplemental assessments in the event of deficiencies. If the assets of the Residual Fund were to be exhausted, members would become jointly and severally liable for the Residual Fund's liabilities.

The Residual Fund can declare and distribute dividends to members upon approval of the State of New Jersey Department of Banking and Insurance. These distributions are divided among the members in the same ratio as their individual assessments are related to the total assessment of the membership for that fund year.

During 2012, the Residual Fund assumed the obligation for discharging the Fund's liabilities for claims and losses for the 2008 Fund Year. Loss reserves totaling $16,384,865 at June 30, 2012, were assumed as of June 30, 2012 in exchange for the Fund's assessment for participation in the Residual Fund of $16,384,865.

24

MUNICIPAL EXCESS LIABILITY JOINT INSURANCE FUND NOTES TO FINANCIAL STATEMENTS

DECEMBER 31. 2012 (Continued)

NOTE 8: MEMBERSHIP IN JOINT INSURANCE FUND (Cont'd)

During 2011, the Residual Fund assumed the obligation for discharging the Fund's liabilities for claims and losses for the 2007 Fund Year. Loss reserves totaling $11,781,164 at June 30,2011, were assumed as of June 30, 2011 in exchange for the Fund's assessment for participation in the Residual Fund of $11,781,164.

Selected, summarized financial information for the Residual Fund as of December 31, 2011 is as follows:

Municipal Excess Liability

Residual Cl aims Fund

Total Assets $ 67,482,281

Net Position $ 3,099,500

Total Revenue $ 24,735,438

Total Expenses $ 24,502,626

Change in Net Position $ 232,812

Member Dividends $ 400,000

The Fund's equity interest in the Residual Fund was $899,714 and $1,083,646 as of December 31,2012 and 2011, respectively.

Financial statements for the Residual Fund are available at the office of the Residual Fund's Executive Director:

PERMA Risk Management Services 9 Campus Drive, Suite 16 Parsippany, New Jersey, 07054 (201) 881-7632

NOTE 9: CONTINGENCIES

In the normal course of its operations, the Fund has a number of lawsuits filed by claimants in various stages. Although estimated loss reserves have been established by the Fund, a number of these cases may possibly be settled for amounts in excess of the Fund's loss reserves. No provision for these contingencies has been included in the financial statements since the amounts are not reasonably estimable.

25

MUNICIPAL EXCESS LIABILITY JOINT INSURANCE FUND NOTES TO FINANCIAL STATEMENTS

DECEMBER 31, 2012 (Continued)

NOTE 10: NOTES RECEIVABLE

The Fund entered into a Promissory Note agreement with the Township of Robbinsville dated July 13, 2010 to fund the Township's portion of a claim settlement. The total amount of the settlement was $280,000. The Township has agreed to pay the Fund over five years at 2.3% interest. The payments of $56,000 commenced on January 2, 2011,

In 2012 the Fund entered into three additional Promissory Notes with the Township of Fairfield, the Township of Bloomfield, and the Borough of Fair Lawn. The total amounts of the settlements were $712,250, $55,000 and $275,000 respectively. The Township of Fairfield agreed to pay the Fund in installments of $71,250 over ten years. The Township of Bloomfield agreed to pay three installments on January 1,2013,2014, and 2015, in the amount of $18,334, $18,333, and $18,333 respectively. The Borough of Fair Lawn agreed to pay the Fund in installments of $91,666.66 over the next three years.

NOTE 11: RELATIONSHIP WITH STATE SCHEDULES

The information in the Fund's financial statements differs from the State Schedules listed in the supplementary data section as Schedules A through F. Specifically, the Schedules present historical information from the inception of each fund year. In addition, the financial statements reflect the Fund's equity interest in a joint venture and the discounting of loss reserves at the financial statement date. The Supplementary Schedules do not reflect the equity interest in a joint venture and the discounting of loss reserves.

26

27

REQUIRED SUPPLEMENTARY INFORMATION

Property 20[2 20[[

Unpaid claims and claim adjustment expenses at beginning of year $ [,109,838 $ 875,284

Incurred claims and claim adjustment expenses: Provision for insured events of

the current period 3,5[3,22[ 3,045,848 Increases/(decreases) in provision

for insured events of prior year.; (665,024) 0,220,407)

Total incurred claims and claim adjustment expenses 2,848,197 1.825,441

Payments: Claims and claim adjustment expenses attributable to insured events of the current period [,368,5[7 1,450.059

Claims and claim adjustment expenses attributable to insured events of the current period 1.037,775 [40,828

Total payments 2,406,292 [,590,887

Unpaid claims and claim adjustment expenses at end of year $ 1,551,743 $ 1,109,838

MUNICIPAL EXCESS LIABILITY JOINT INSURANCE FUND COMPARATIVE RECONCILIATION OF CLAIMS LIABILITIES BY FUND

FOR THE YEARS ENDED DECEMBER 31 2012 AND 2011

Liability Faithful Petfonnance Bond Worker's Compensation 20[2 2011 20[2 2011 20[2 2011

$ [8,780,082 $ [7,7[4,399 $ 690,806 $ 5[8,542 $ 27,895,645 $ 27,487,830

6,051,120 6,006,5[[ 7,362,545 8,589,055

(2,632,[79) (2,6[6,992) 460,402 286,163 (11,024,332) (5,4[9,053)

3,418,941 3,389,5[9 460,402 286,163 ~66[,787) 3.170,002

[27,727 45,73[

4,654,204 2,323,836 832,68[ 113,899 2,463,685 2,7[6,456

4,654.204 2,323,836 832,681 [[3,899 2,59[,4[2 2,762,187

$[7,544,8[9 $ 18,780,082 $ 318,527 $ 690,806 $2[,642,446 $27,895,645

Public Officials'/ Employment Practices 20[2 2011

$ 22,894,734 $3[,243,[43

187.647

3,933,869 432,539

3,933,869 620,[86

3,580

10,78[,945 8,965,0[5

10,78[,945 8,968,595

$ [6,046,658 $22,894,734

Totals 20[2

$7[,37[,[05

[6,926,886

(9,927,264)

6,999,622

[,496,244

[9,770,290

2[,266,534

$57,[04,[93

2011

$ 77,839,[98

17.829.061

(8,537,750)

9.291,311

[,499,370

14,260.034

[5,759,404

$7[,37[,105

'" (X)

MUNICIPAL EXCESS LIABILITY JOINT INSURANCE FUND TEN-YEAR CLAIMS DEVELOPMENT INFORMATION

Fiscal Period Ended December 31,2012 and Policy Period Ended December 31, 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Required contribution and investment revenue:

Earned $ 35,979,137 $ 41,883,251 $ 45,950,444 $ 48,995,359 $ 52,370,052 $ 55,952,520 $ 56,831,012 $ 57,891,042 $ 43,996,834 $ 43,401,023 Ceded 13,499,654 15,452,240 15,444,162 18,286,578 16,461,478 15,914,456 16,565,698 16,428,516 15,926,686 16,051,969

22,479,483 26,431,011 30,506,282 30,708,781 35,908,574 40,038,064 40,265,314 41,462,526 28,070,148 27,349,054

Unallocated expenses 3,348,552 3,561,698 4,450,051 4,345,056 4,730,526 5,027,496 ~419,816 5,426,618 5,014,018 5,118,544

Estimated claims and expenses, end of policy year:

Incurred 15,356,261 15,985,079 15,802,759 18,800,966 22,047,820 26,171,277 26,586,532 26,597,577 20,481,518 27,880,350 Ceded 177,134 66,276 5,054 59,968 2,652,457 10,953,464 Net Incurred 15,179,127 15,985,079 15,802,759 18,800,966 22,047,820 26,105,001 26,581,478 26,537,609 17,829,061 16,926,886

Paid (cumulative) as of: End of policy year 1,674,551 1,348,708 1,075,029 2,113,155 1,266,553 2,724,964 1,803,382 3,185,765 1,499,370 1,496,244 One year later 5,128,677 5,559,469 4,359,007 5,509,264 6,473,414 6,562,159 5,772,692 6,774,613 2,730,660 Two years later 8,262,517 9,313,827 8,008,612 8,011,974 15,709,789 12,805,334 10,446,895 13,761,525 Three years later 11,206,046 12,282,176 13,482,131 14,497,811 21,883,494 17,189,204 18,245,500 Four years later 12,170,477 13,358,811 15,441.568 16,816,278 23,496,607 20,942,687 Five years later 12,170,477 13,358,811 17,401,005 16,816,278 23,496,607 Six years later 12,170,477 13,358,811 17,401,005 16,816,278 Seven years later 12,170,477 13,358,811 17,401,005 Eight years later 12,170,477 13,358,811 Nine years later 12,170,477

Reestimated ceded claims and expenses 8,521,017 9,413,237 11,233,172 9,933,817 11,781,164 18,217,742 362,746 709,515 1,423,472 10,953,464

Reestimated incurred claims and expense:

End of policy year 15,179,127 15,985,079 15,802,759 ,

18,800,966 22,047,820 26,105,001 26,581,478 26,537,609 17,829,061 16,926,886 One year later 15,888,736 19,422,231 18,540,391 20,319,336 27,146,776 28,791,814 28,731,045 25,131,425 15,622,139 Two years later 17,522,778 20,468,013 19,165,944 20,518,928 31,213,869 32,860,267 29,687,807 28,183,952 Three years later 19,284,058 21,313,655 23,433,499 24,506,741 33,357,562 34,632,894 32,605,145 Four years later 12,170,477 13,358,811 15,441,568 16,816,278 23,496,607 20,942,687 Five years later 12,170,477 13,358,811 17,401.005 16,816,278 23,496,607 Six years later 12,170,477 13,358,811 17,401,005 16,816,278 Seven years later 12,170,477 13,358,811 17,401,005 Eight years later 12,170,477 13,358,811 Nine years later 12,170,477

IncreaseJ(decrease) in estimated incurred claims and expense from end of policy year $ (3,008,650) $ (2.626,268) $ 1,598,246 $ (1.984,688) $ 1.448,787 $ (5.162.314l, $ 6,023.667 $ 1.646,343 $ (2,206,922) $ -O-

N (J:J

30

COMBINING SUPPLEMENTARY SCHEDULES

MUNICIPAL EXCESS LIABILITY JOINT INSURANCE FUND COMBINING SCHEDULE OF NET POSITION

DECEMBER 31, 2012

Fund Year MEL

Aggregate Excess Loss Fund

ASSETS Contingency 2009 2010 2011 2012 Total

Cash and Cash Equivalents $ (1,019,812) $ 3,447,000 $ 4,802,914 $ 4,539,386 $ 4,343,970 $ 16,113,458 Investments (3,627,804) 12,262,107 17,085,539 16,148,083 15,452,925 57,320,850 Assessments Receivable 2,065,710 2,065,710 Prepaid Expense 92,217 92,217 Notes Receivable 443,000 767,500 1,210,500 Accrued Interest Receivable 285 25,901 32,003 27,223 36,354 121,766 Insurance Receivables 945,352 102,732 378,359 1,426,443 Due from Municipal Excess Liability

Residual Claims Fund 906,296 906,296 Investment in Joint Venture 899,714 899,714

Total Assets (1,452,969) 16,605,240 22,298,815 20,714,692 21,991,176 80,156,954

LIABILITIES

Loss Reserves 14,359,646 14,422,425 12,891,479 15,430,643 57,104,193 Accounts Payable 4,744 24,433 312 82,475 111,964 Other Liabilities 500,899 498 388,910 1,174,434 2,064,741

Total Liabilities 500,899 14,364,888 14,446,858 13,280,701 16,687,552 59,280,898

NET POSITION

Unrestrictedl(Deficit) (1,953,868) 2,240,352 7,851,957 7,433,991 5,303,624 20,876,056

Total Net Position $ (1,953,868~ $ 2,240,352 $ 7,851,957 $ 7,433,991 $ 5,303,624 $ 20,876,056

w ~

MUNICIPAL EXCESS LIABILITY JOINT INSURANCE FUND COMBINING SCHEDULE OF REVENUE, EXPENSES AND CHANGES IN NET POSITION

FOR THE YEAR ENDED DECEMBER 31, 2012

Fund Year MEL

Aggregate Excess Loss Fund

Contingency 2009 2010 2011

Operating Revenue: Assessments from Participating Members $ 14,081 $ (5,568) $ (5,737)

Total Operating Revenue 14,081 (5,568) (5,737)

Operating Expenses: Provision for Claims and Claim Adjustment Expense (13,690,206) $ 2,917,338 3,052,524 (2,206,921) Assessment for Participation in Municipal Excess Liability

Residual Claims Fund 16,384,865 Insurance Premiums (316,212) (25,436) (338) Claims Administration Other Contractual Services 120,102 113,345 (4,069) Non-Contractual Expenses 12,960 Administration Insurance Brokerage Expense Risk Management Fees 1,000

Total Operating Expenses 2,391,407 3,012,004 3,165,531 (2,209,990)

Operating Income/(Loss) (2,377,326) (3,012,004) (3,l7l ,099) 2,204,253

Non-Operating Income/(Expenses): Change in Investment in Joint Venture (183,932) Investment Income 108 145,620 183,335 131,536

Change in Net Position (2,561,150) (2,866,384) (2,987,764) 2,335,789

Net Position - Beginning of Year 607,282 5,106,736 10,839,721 5,098,202

Net Position - End of Year $ (1,953,868) $ 2,240,352 $ 7,851,957 $ 7,433,991

2012

$ 43,242,670

43,242,670

16,926,887

16,051,969 1,093,718 2,216,149

74,963 918,536 469,749 345,429

38,097,400

5,145,270

158,354

5,303,624

$ 5,303,624

Total

$ 43,245,446

43,245,446

6,999,622

16,384,865 15,709,983 1,093,718 2,445,527

87,923 918,536 469,749 346,429

44,456,352

(1,210,906)

(183,932) 618,953

(775,885)

21,651,941

$ 20,876,056

'" N

33

SUPPLEMENTARY DATA

34

Schedule A MUNICIPAL EXCESS LIABILITY JOINT INSURANCE FUND

HISTORICAL OPERATING RESULTS ANALYSIS

ALL FUND YEARS

DECEMBER 31, 2012

(Unaudited)

1. Underwriting Income:

Regular Contributions (earned) $ 735,664,918

Supplemental Contributions 862,606

Other Income (except investments) 186,209

Total Income $ 736,713,733

2. Incurred Liabilities:

Claims:

Paid 232,658,242

Case Reserves 37,591,485

IBNR Reserve 38,398,211

Subtotal $ 308,647,938 Less Excess Insurance:

Received 18,354,291

Receivable 1,426,443

Recoverable 11,886,205

Subtotal 31,666,939 Limited Incurred Claims (claims-excess) 276,980,999

Expenses:

Excess Insurance Premiums 377,250,297

Administrative 80,411,175

Worker's Compensation 1,836,505

Property Grant 268,908

Subtotal Expenses 459,766,885 Total Incurred Liabilities

(limited claims and expenses) 736,747,884

3. Underwriting Surplus/(Deficitl = 1-2 (34,151)

4. Investment Income <Earned) 57,276,781

5. Gross Operating SurpluslCDeficitl = 3+4 57,242,630

6. Return of Surplus:

Paid 44,265,586

Authorized and Unpaid

Subtotal Return of Surplus 44,265,586

7. Net Current Sumlusl(Deficitl - 5-6 $ 12,977,044

MUNICIPAL EXCESS LIABILITY JOINT INSURANCE FUND

HISTORICAL BALANCE SHEET

ALL FUND YEARS

DECEMBER 31. 2012

(Unaudited)

1. Assets:

Cash and Investments (1) $ 73,434,308

Receivables (1 ):

Excess Insurance 1,426,443

Assessments 2,065,710

Other 2,238,562

Total Receivables

Prepaid Expenses (1)

Other Assets (1)

Total Assets

2. Liabilities:

Claims:

Case Reserves 25,705,280

IBNR Reserve (2) 38,398,211

Subtotal Claims

Expenses (unpaid) (1):

Excess Insurance 29,177

Administrative 82,787

Subtotal Expenses

Other Liabilities:

Unearned Contributions

Authorized Return of Surplus

Miscellaneous Liabilities (1) 2,064,741

Subtotal

Total Liabilities

NET CURRENT SURPLUS/(DEFICIT) = 1-2

Notes: (1) attach schedule itemizing these categories

(2) attach an opinion from the actuary

$ 73,434,308

5,730,715

92,217

64,103,491

111,964

2,064,741

$

$

35

Schedule B

79,257,240

66,280,196

12,977,044

1.

2.

3.

4.

MUNICIPAL EXCESS LIABILITY JOINT INSURANCE FUND FUND YEAR OPERATING RESULTS ANALYSIS

FUND YEAR - MEL AGGREGATE EXCESS LOSS FUND CONTINGENCY DECEMBER 31. 2012

(Unaudited)

Underwriting Income: Regular Contributions (earned) $ 535,720,335

Supplemental Contributions 862,606 Other Income (except investments) 186,209

Total Income

Incurred Liabilities: Claims:

Paid 194,861,321 Case Reserves IBNR Reserve

Subtotal $ 194,861,321 Less Excess Insurance:

Received 17,272,390 Receivable 945,352 Recoverable Subtotal 18,217,742

Limited Incurred Claims (claims-excess) 176,643,579

Expenses: Excess Insurance Premiums 312,277,428 Administrative 61,537,592

Subtotal Expenses 373,815,020 Total Incurred Liabilities

(limited claims and expenses)

Underwriting Surplus/(Deficitl - 1-2

Investment Income (Earnedl

4a. Transfer

5. Gross Operating Surplus/CDeficitl - 3+4

6. Retum of Surplus:

Paid 44,265,586

Authorized and Unpaid Subtotal Return of Surplus

7. Net Current Sumlusl(Deficit) = 5-6

36

Schedule C

$ 536,769,150

550,458,599

(13,689,449)

55,101,453

41,412,004

44,265,586

$ (2,853,582)

I,

2.

3.

4.

5.

6.

7.

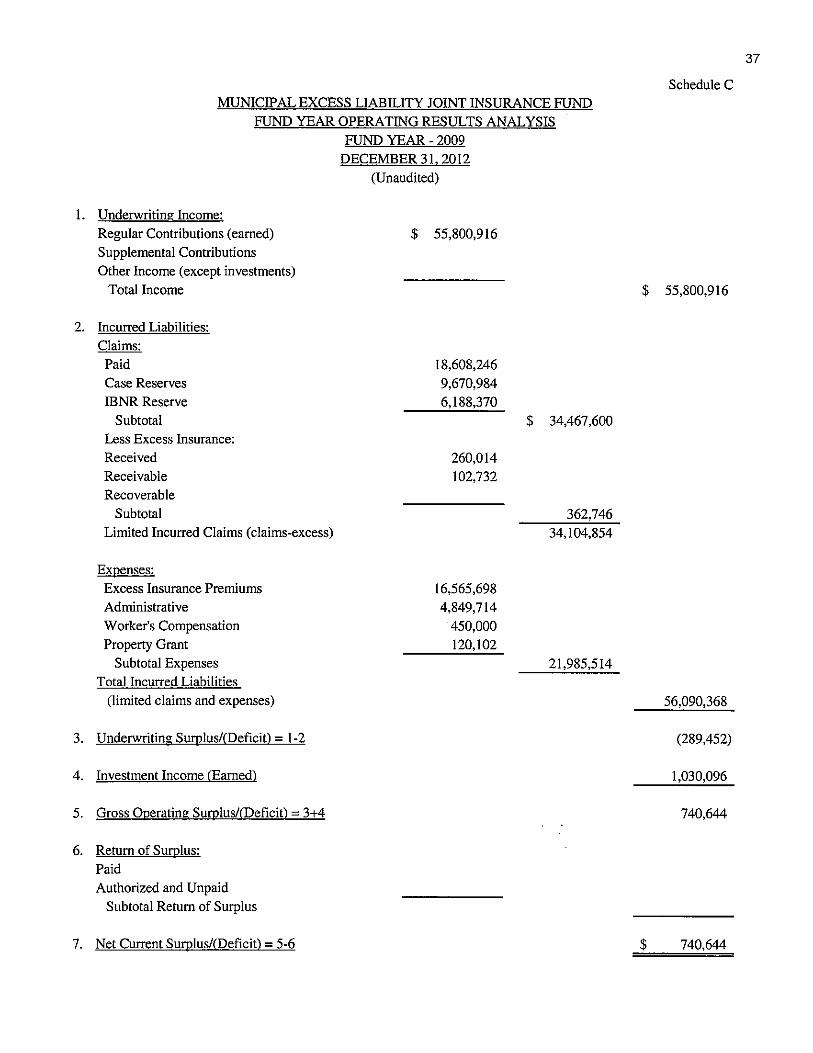

MUNICIPAL EXCESS LIABILITY JOINT INSURANCE FUND FUND YEAR OPERATING RESULTS ANALYSIS

FUND YEAR - 2009

Underwriting Income: Regular Contributions (earned) Supplemental Contributions Other Income (except investments)

Total Income

Incurred Liabilities: Claims: Paid Case Reserves IBNR Reserve

Subtotal Less Excess Insurance: Received Receivable Recoverable

Subtotal Limited Incurred Claims (claims-excess)

Expenses:

Excess Insurance Premiums Administrative Worker's Compensation Property Grant

Subtotal Expenses Total Incurred Liabilities

(limited claims and expenses)

Underwriting Surplus/(Deficit) - 1-2

Investment Income (Earned)

Gross Operating SurpluslCDeficitl - 3+4

Return of Surplus:

Paid Authorized and Unpaid

Subtotal Return of Surplus

Net Current Sumlusl(Deficit) = 5-6

DECEMBER 31, 20\2 (Unaudited)

$ 55,800,916

18,608,246 9,670,984 6,188,370

260,014 102,732

16,565,698 4,849,714

450,000 120,102

$ 34,467,600

362,746 34,104,854

21,985,514

37

Schedule C

$ 55,800,916

56,090,368

(289,452)

1,Q30,096

740,644

$ 740,644

I.

2.

3.

4.

5.

6.

7.

MUNICIPAL EXCESS LIABILITY JOINT INSURANCE FUND FUND YEAR OPERATING RESULTS ANALYSIS

FUND YEAR - 2010

Underwriting Income: Regular Contributions (earned) Supplemental Contributions Other Income (except investments)

Total Income

Incurred Liabilities: Claims:

Paid Case Reserves IBNR Reserve

Subtotal Less Excess Insurance: Received Receivable Recoverable

Subtotal Limited Incurred Claims (claims-excess)

Expenses: Excess Insurance Premiums Administrative Workers' Compensation

Property Grant Subtotal Expenses

Total Incurred Liabilities (limited claims and expenses)

Underwriting Sumlus/<Deficitl - 1-2

Investment Income <Earned)

Gross Operating Sumlus/<Deficitl - 3+4

Return of Sum Ius:

Paid Authorized and Unpaid

Subtotal Return of Surplus

Net Current Sumlus/(Deficitl = 5-6

DECEMBER 31, 2012

(Unaudited)

$ 57,150,605

14,416,039 7,652,010 8,184,926

276,155 378,359

55,001

16,428,516 4,848,474

459,325 118,819

$ 30,252,975

709,515 29,543,460

21,855,134

38

Schedule C

$ 57,150,605

51,398,594

5,752,011

740,437

6,492,448

$ 6,492,448

MUNICIPAL EXCESS LIABILITY JOINT INSURANCE FUND

FUND YEAR OPERATING RESULTS ANALYSIS FUND YEAR - 2011

I. Underwriting Income:

2.

3.

4.

Regular Contributions (earned) Supplemental Contributions Other Income (except investments)

Total Income

Incurred Liabilities: Claims:

Paid Case Reserves IBNR Reserve

Subtotal Less Excess Insurance: Received Receivable Recoverable

Subtotal Limited Incurred Claims (claims-excess)

Expenses: Excess Insurance Premiums Administrative Worker's Compensation Property Grant

Subtotal Expenses Total Incurred Liabilities

(limited claims and expenses)

Underwriting Surolus/CDeficitl - 1-2

Investment Income (Earned)

5. Gross Operating SurolusHDeficit) = 3+4

6. Return of Surolus: Paid Authorized and Unpaid

7. Net Current Surolus/CDeficit) - 5-6

DECEMBER 31. 2012 (Unaudited)

$ 43,750,392

3,276,392 6,604,216 8,989,428

545,732

877,740

15,926,686 4,555,018

459,000

$ 18,870,036

1,423,472 17,446,564

20,940,704

39

Schedule C

$ 43,750,392

38,387,268

5,363,124

246,442

5,609,566

$ 5,609,566

40

Schedule C MUNICIPAL EXCESS LIABILITY JOINT INSURANCE FUND

FUND YEAR OPERATING RESULTS ANALYSIS FUND YEAR - 2012

DECEMBER 31, 2012 (Unaudited)

I. Underwriting Income: Regular Contributions (earned) $ 43,242,670 Supplemental Contributions Other Income (except investments)

Total Income $ 43,242,670

2. Incurred Liabilities: Claims:

Paid 1,496,244 Case Reserves 13,664,275 IBNR Reserve 15,035,487

Subtotal $ 30,196,006 Less Excess Insurance: Received Receivable Recoverable 10,953,464

Subtotal 10,953,464 Limited Incurred Claims (claims-excess) 19,242,542

Expenses: Excess Insurance Premiums 16,051,969 Administrative 4,620,377 Workers Compensation 468,180 Property Grant 29,987

Subtotal Expenses 21,170,513 Total Incurred Liabilities

(limited claims and expenses) 40,413,055

3. Underwriting Surplusf(Deficit) - 1-2 2,829,615

4. Investment Income <Earned) 158,353

4a. Transfer

5. Gross Operating Surplus/(Deficitl = 3+4 2,987,968

6. Return of Surplus:

Paid Authorized and Unpaid

Subtotal Return of Surplus

7. Net Current Surplus/(Deficit) - 5-6 $ 2,987,968

ScheduleD

MUNICIPAL EXCESS LIABILITY JOINT INSURANCE FUND FUND YEAR ACCOUNT OPERATING RESULTS ANALYSIS

FUND YEAR - 2009 DECEMBER 31. 2012

(Unaudited)

Coverages and Other Accounts Public Officials'! Faithful

Worker's Employment Performance General and Property Liability Compensation Practices Bond Contingency Administrative Total

I. Underwriting Income Regular Contributions (earned) $ 8,062,906 $ 13,557,243 $ 16,919,244 $ 11,345,146 $ 238,474 $ 446,751 $ 5,231,152 $ 55,800,916 Supplemental Contributions Other Income (except investments) Total Income 8,062,906 13,557,243 16,919,244 11,345,146 238,474 446,751 5,231,152 55,800,916

2. Incurred Liabilities Claims (limited incurred) 943,217 4,832,435 9,983,921 17,326,643 1,018,638 34,104,854 Expenses 5,294,094 7,635,335 3,388,741 872,566 4,794,778 21,985,514 Total Liabilities 6,237,311 12,467,770 13,372,662 18,199,209 1,018,638 4,794,778 56,090,368

3. Underwriting Surplus!(Deficit) 1,825,595 1,089,473 3,546,582 (6,854,063) (780,164) 446,751 436,374 __ (289,452)

4. Adjustments Investment Income 69,393 205,385 493,450 236,554 6,733 18,581 1,030,096 Transfers Total Adjustments 69,393 205,385 493,450 236,554 6,733 18,581 1,030,096

5. Gross Operating Surplus 1,894,988 1,294,858 4,040,032 (6,617,509) (773,431) 446,751 454,955 740,644

6. Return of Surplus

7. Net Current Surplus $ 1,894,988 $ 1,294,858 $ 4,040,032 $ (6,617,509) $ (773,431) $ 446,751 $ 454,955 $ 740,644

..,. ~

Schedule D MUNICIPAL EXCESS LIABILITY JOINT INSURANCE FUND FUND YEAR ACCOUNT OPERATING RESULTS ANALYSIS

FUND YEAR - 2010 DECEMBER 31, 2012

(Unaudited)

Coverages and Other Accounts Public Officials'! Faithful Loss

Worker's Employment Perfonnance Fund General and Property Liability Compensation Practices Bond Contingency Administrative Total

I. Underwriting Income

Regular Contributions (earned) $ 7,856,196 $ 13,243,899 $ 15,470,894 $ 13,910,910 $ 241,898 $ 1,240,486 $ 5,186,322 $ 57,150,605 Supplemental Contributions Other Income (except investments) Total Income 7,856,196 13,243,899 15,470,894 13,910,910 241,898 1,240,486 5,186,322 ~150,605

2. Incurred Liabilities Claims (limited incurred) 1,564,999 6,849,999 7,212,670 13,590,836 324,956 29,543,460 Expenses 5,477,921 7,438,203 3,250,482 840,054 4,848,474 21,855,134 Total Liabilities 7,042,920 14,288,202 10,463,152 14,430,890 324,956 4,848,474 51,398,594

3. Underwriting SumlusHDeficit) 813,276 (1,044,303) 5,007,742 (519,980) (83,058) 1,240,486 337,848 5,752,011