Embed Size (px)

Citation preview

Project Number: 32298 Loan Number: 2520 October 2009

Multitranche Financing Facility India: Madhya Pradesh Power Sector

Investment Program (Tranche 5 – DISCOM-C – [Part A])

The project administration memorandum is an active document, progressively updated and revised as necessary, particularly following any changes in project or program costs, scope, or implementation arrangements. This document, however, may not reflect the latest project changes.

Asian Development Bank

Project Administration Memorandum

CURRENCY EQUIVALENTS (As of 12 February 2009)

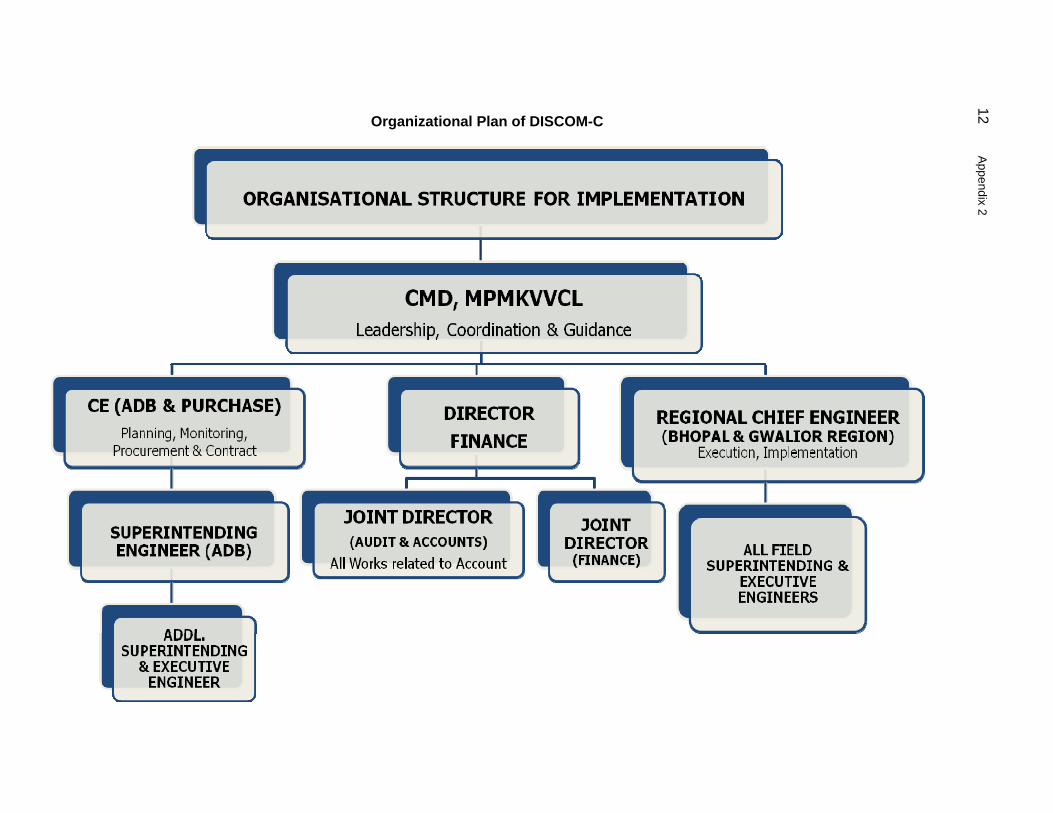

Currency Unit – Indian rupees/s (Re/Rs)

Rs1.00 = $0.020555

$1.00 = Rs48.65

ABBREVIATIONS

ADB – Asian Development Bank DFID – Department for International Development of the United Kingdom DISCOM – distribution company DISCOM-C – Madhya Pradesh Madhya Kshetra Vidyut Vitaran Company Limited DISCOM-E – Madhya Pradesh Poorv Kshetra Vidyut Vitaran Company Limited DISCOM-W – Madhya Pradesh Paschim Kshetra Vidyut Vitaran Company Limited EA – executing agency EARF – environmental assessment and review framework ECF – Energy Conservation Fund EIRR – economic internal rate of return EMP – environmental management plan ERP – enterprise resource planning FFA – framework financing agreement FGIA – first generation imprest account FIRR – financial internal rate of return FMA – financial management assessment FY – fiscal year GOMP – Government of Madhya Pradesh HVDS – high-voltage distribution system ICB – international competitive bidding IEE – initial environmental examination IPDF – indigenous peoples development framework IPDP – indigenous peoples development plan IT – information technology LIBOR – London interbank offered rate LVHS – low-voltage high speed MFF – multitranche financing facility MIS – management information system MOP – Ministry of Power MP – Madhya Pradesh MPERC – Madhya Pradesh Electricity Regulatory Commission MPPSIP – Madhya Pradesh Power Sector Investment Program MPSEB – Madhya Pradesh State Electricity Board MYT – multi-year tariff NEP – National Electricity Policy OCR – ordinary capital resources O&M – operations and maintenance PFC – Power Finance Corporation PFR – periodic financing request PMU – project management unit RF – resettlement framework RP – resettlement plan SGIA – second generation imprest account

2

SIEE – summary initial environmental examination SPRSS – summary poverty reduction and social strategy T&D – transmission and distribution TRANSCO – Madhya Pradesh Power Transmission Company Limited

WEIGHTS AND MEASURES

GWh – gigawatt-hour (1,000 megawatt-hours) ha (hectare) – Unit of area km (kilometer) – 1,000 meters kV – kilovolt (1,000 volts) kW – kilowatt (1,000 watts) kWh – kilowatt-hour MVA – megavolt-ampere(1,000,000 volt-amperes) MW – megawatt (1,000 kilowatts) MWh – megawatt-hour VA – Volt-ampere

NOTES

(i) The fiscal year (FY) of India and its agencies runs from 1 April to 31 March of the following year. FY before a calendar year denotes the year in which the fiscal year ends, e.g., FY2006 ends on 31 March 2006.

(ii) In this report, "$" refers to US dollars.

CONTENTS Page LOAN PROCESSING HISTORY ii DESIGN AND MONITORING FRAMEWORK iii I. PROJECT DESCRIPTION 1 II. COST ESTIMATES AND FINANCING PLAN 1

III. IMPLEMENTATION ARRANGEMENTS 2 IV. PROCUREMENT 3 V. DISBURSEMENT PROCEDURES 3 VI. PROJECT MONITORING AND EVALUATION 4 VII. ACCOUNTING, AUDITING AND REPORTING 5 VIII. SAFEGUARDS 5 IX. MAJOR LOAN COVENANTS 6 X. KEY PERSONS INVOLVED IN THE PROJECT 6 XI. ANTICORRUPTION 8 XII. CONCURRENCE 9 APPENDIXES

1. Detailed Cost Estimates and Financing Plan 10 2. Organizational Structure for Project Implementation 12 3. Indicative Implementation Schedule 13 4. Procurement Plan 14 5. Suggested Format of Progress Report 16 6. Calculation Method of Project Progress 18 7. Copy of Audit Letter 22 8. Major Loan Covenants 26

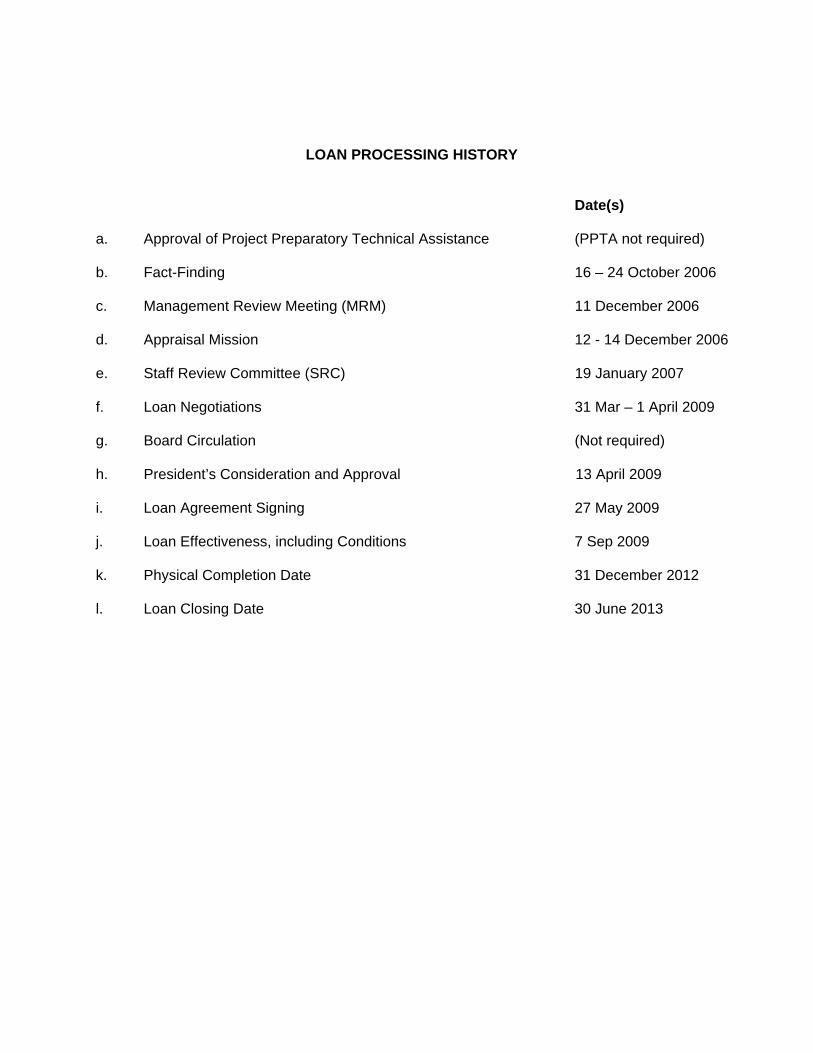

LOAN PROCESSING HISTORY

Date(s) a. Approval of Project Preparatory Technical Assistance (PPTA not required) b. Fact-Finding 16 – 24 October 2006 c. Management Review Meeting (MRM) 11 December 2006 d. Appraisal Mission 12 - 14 December 2006 e. Staff Review Committee (SRC) 19 January 2007 f. Loan Negotiations 31 Mar – 1 April 2009 g. Board Circulation (Not required) h. President’s Consideration and Approval 13 April 2009 i. Loan Agreement Signing 27 May 2009 j. Loan Effectiveness, including Conditions 7 Sep 2009 k. Physical Completion Date 31 December 2012 l. Loan Closing Date 30 June 2013

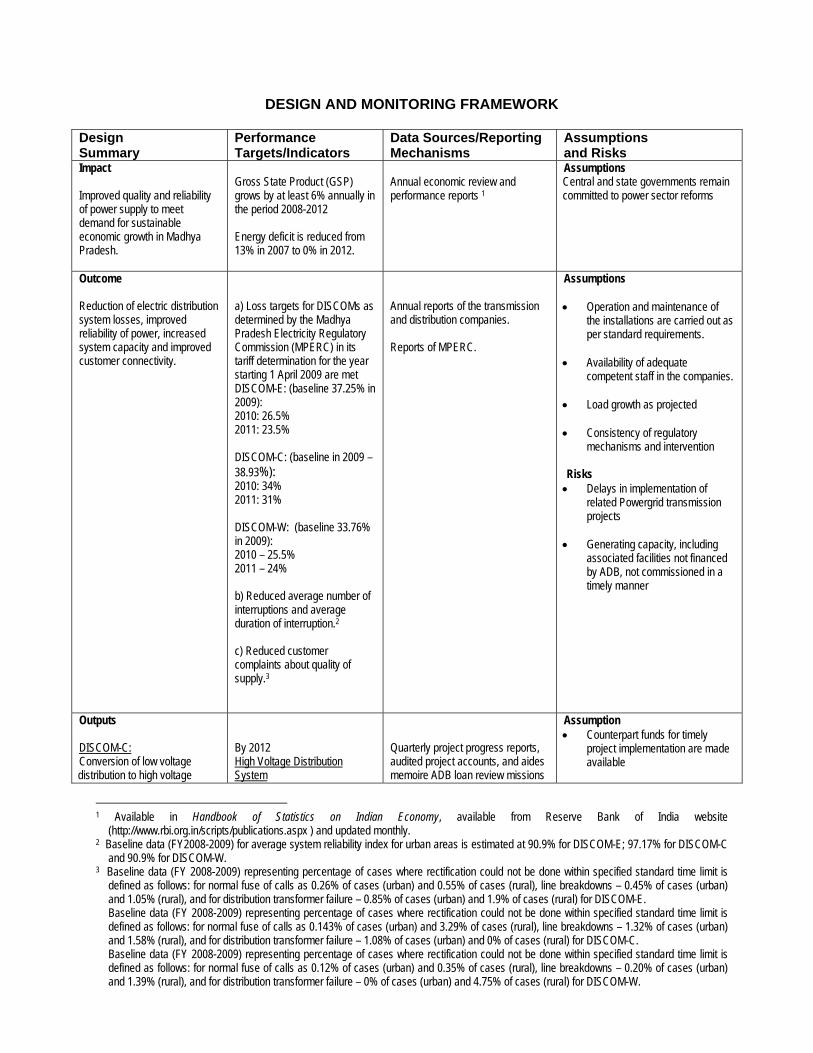

DESIGN AND MONITORING FRAMEWORK

Design Summary

Performance Targets/Indicators

Data Sources/Reporting Mechanisms

Assumptions and Risks

Impact Improved quality and reliability of power supply to meet demand for sustainable economic growth in Madhya Pradesh.

Gross State Product (GSP) grows by at least 6% annually in the period 2008-2012 Energy deficit is reduced from 13% in 2007 to 0% in 2012.

Annual economic review and performance reports 1

Assumptions Central and state governments remain committed to power sector reforms

Outcome Reduction of electric distribution system losses, improved reliability of power, increased system capacity and improved customer connectivity.

a) Loss targets for DISCOMs as determined by the Madhya Pradesh Electricity Regulatory Commission (MPERC) in its tariff determination for the year starting 1 April 2009 are met DISCOM-E: (baseline 37.25% in 2009): 2010: 26.5% 2011: 23.5% DISCOM-C: (baseline in 2009 – 38.93%): 2010: 34% 2011: 31% DISCOM-W: (baseline 33.76% in 2009): 2010 – 25.5% 2011 – 24% b) Reduced average number of interruptions and average duration of interruption.2 c) Reduced customer complaints about quality of supply.3

Annual reports of the transmission and distribution companies. Reports of MPERC.

Assumptions Operation and maintenance of

the installations are carried out as per standard requirements.

Availability of adequate

competent staff in the companies. Load growth as projected Consistency of regulatory

mechanisms and intervention Risks Delays in implementation of

related Powergrid transmission projects

Generating capacity, including

associated facilities not financed by ADB, not commissioned in a timely manner

Outputs DISCOM-C: Conversion of low voltage distribution to high voltage

By 2012 High Voltage Distribution System

Quarterly project progress reports, audited project accounts, and aides memoire ADB loan review missions

Assumption Counterpart funds for timely

project implementation are made available

1 Available in Handbook of Statistics on Indian Economy, available from Reserve Bank of India website

(http://www.rbi.org.in/scripts/publications.aspx ) and updated monthly. 2 Baseline data (FY2008-2009) for average system reliability index for urban areas is estimated at 90.9% for DISCOM-E; 97.17% for DISCOM-C

and 90.9% for DISCOM-W. 3 Baseline data (FY 2008-2009) representing percentage of cases where rectification could not be done within specified standard time limit is

defined as follows: for normal fuse of calls as 0.26% of cases (urban) and 0.55% of cases (rural), line breakdowns – 0.45% of cases (urban) and 1.05% (rural), and for distribution transformer failure – 0.85% of cases (urban) and 1.9% of cases (rural) for DISCOM-E. Baseline data (FY 2008-2009) representing percentage of cases where rectification could not be done within specified standard time limit is defined as follows: for normal fuse of calls as 0.143% of cases (urban) and 3.29% of cases (rural), line breakdowns – 1.32% of cases (urban) and 1.58% (rural), and for distribution transformer failure – 1.08% of cases (urban) and 0% of cases (rural) for DISCOM-C. Baseline data (FY 2008-2009) representing percentage of cases where rectification could not be done within specified standard time limit is defined as follows: for normal fuse of calls as 0.12% of cases (urban) and 0.35% of cases (rural), line breakdowns – 0.20% of cases (urban) and 1.39% (rural), and for distribution transformer failure – 0% of cases (urban) and 4.75% of cases (rural) for DISCOM-W.

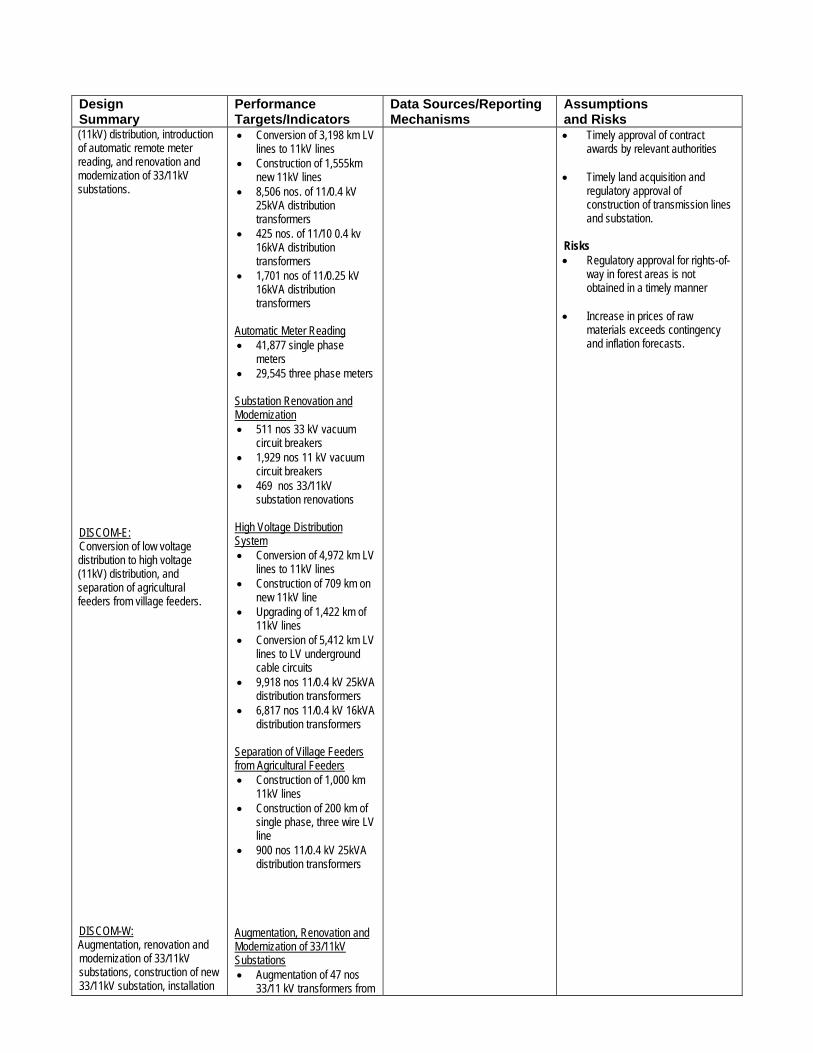

Design Summary

Performance Targets/Indicators

Data Sources/Reporting Mechanisms

Assumptions and Risks

(11kV) distribution, introduction of automatic remote meter reading, and renovation and modernization of 33/11kV substations. DISCOM-E: Conversion of low voltage distribution to high voltage (11kV) distribution, and separation of agricultural feeders from village feeders. DISCOM-W: Augmentation, renovation and modernization of 33/11kV substations, construction of new 33/11kV substation, installation

Conversion of 3,198 km LV lines to 11kV lines

Construction of 1,555km new 11kV lines

8,506 nos. of 11/0.4 kV 25kVA distribution transformers

425 nos. of 11/10 0.4 kv 16kVA distribution transformers

1,701 nos of 11/0.25 kV 16kVA distribution transformers

Automatic Meter Reading 41,877 single phase

meters 29,545 three phase meters Substation Renovation and Modernization 511 nos 33 kV vacuum

circuit breakers 1,929 nos 11 kV vacuum

circuit breakers 469 nos 33/11kV

substation renovations High Voltage Distribution System Conversion of 4,972 km LV

lines to 11kV lines Construction of 709 km on

new 11kV line Upgrading of 1,422 km of

11kV lines Conversion of 5,412 km LV

lines to LV underground cable circuits

9,918 nos 11/0.4 kV 25kVA distribution transformers

6,817 nos 11/0.4 kV 16kVA distribution transformers

Separation of Village Feeders from Agricultural Feeders Construction of 1,000 km

11kV lines Construction of 200 km of

single phase, three wire LV line

900 nos 11/0.4 kV 25kVA distribution transformers

Augmentation, Renovation and Modernization of 33/11kV Substations Augmentation of 47 nos

33/11 kV transformers from

Timely approval of contract awards by relevant authorities

Timely land acquisition and

regulatory approval of construction of transmission lines and substation.

Risks Regulatory approval for rights-of-

way in forest areas is not obtained in a timely manner

Increase in prices of raw

materials exceeds contingency and inflation forecasts.

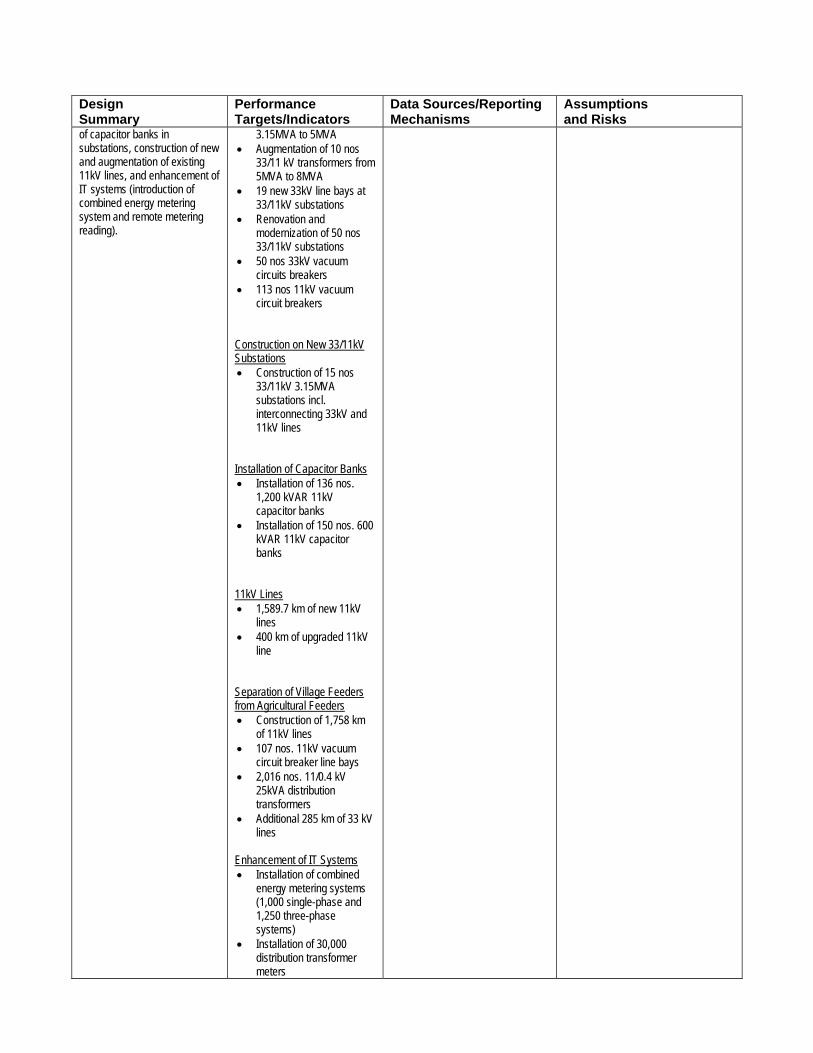

Design Summary

Performance Targets/Indicators

Data Sources/Reporting Mechanisms

Assumptions and Risks

of capacitor banks in substations, construction of new and augmentation of existing 11kV lines, and enhancement of IT systems (introduction of combined energy metering system and remote metering reading).

3.15MVA to 5MVA Augmentation of 10 nos

33/11 kV transformers from 5MVA to 8MVA

19 new 33kV line bays at 33/11kV substations

Renovation and modernization of 50 nos 33/11kV substations

50 nos 33kV vacuum circuits breakers

113 nos 11kV vacuum circuit breakers

Construction on New 33/11kV Substations Construction of 15 nos

33/11kV 3.15MVA substations incl. interconnecting 33kV and 11kV lines

Installation of Capacitor Banks Installation of 136 nos.

1,200 kVAR 11kV capacitor banks

Installation of 150 nos. 600 kVAR 11kV capacitor banks

11kV Lines 1,589.7 km of new 11kV

lines 400 km of upgraded 11kV

line Separation of Village Feeders from Agricultural Feeders Construction of 1,758 km

of 11kV lines 107 nos. 11kV vacuum

circuit breaker line bays 2,016 nos. 11/0.4 kV

25kVA distribution transformers

Additional 285 km of 33 kV lines

Enhancement of IT Systems Installation of combined

energy metering systems (1,000 single-phase and 1,250 three-phase systems)

Installation of 30,000 distribution transformer meters

Design Summary

Performance Targets/Indicators

Data Sources/Reporting Mechanisms

Assumptions and Risks

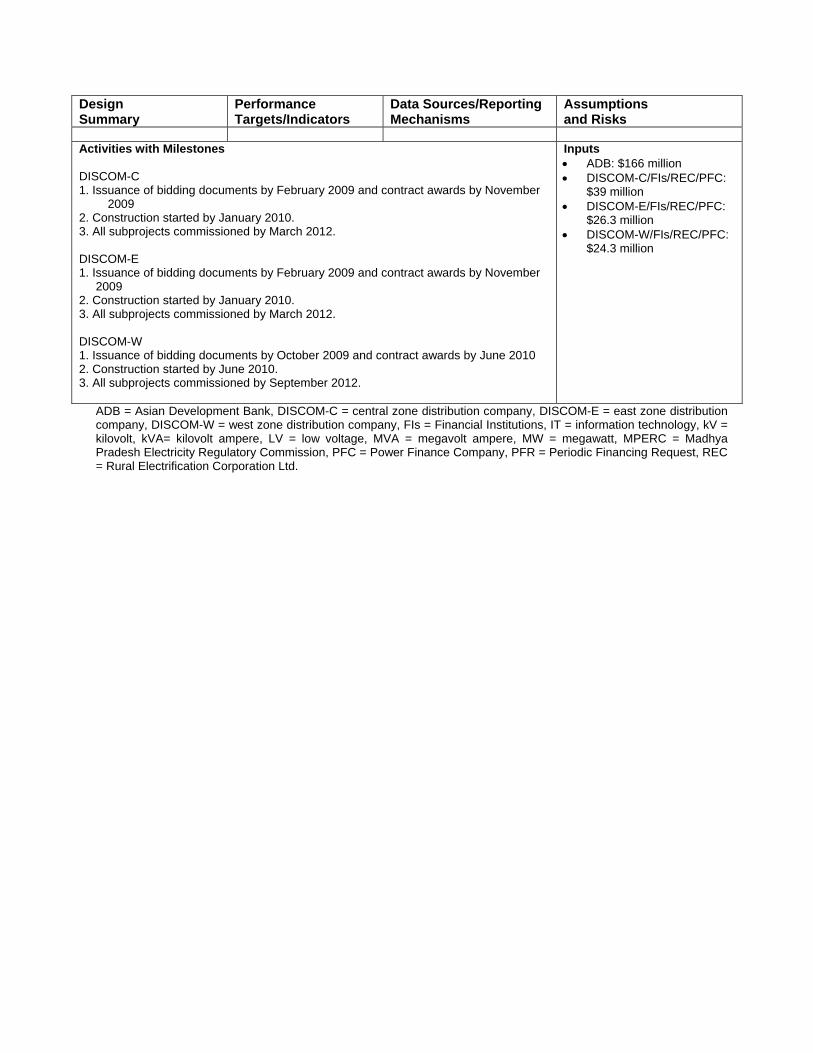

Activities with Milestones DISCOM-C 1. Issuance of bidding documents by February 2009 and contract awards by November

2009 2. Construction started by January 2010. 3. All subprojects commissioned by March 2012. DISCOM-E 1. Issuance of bidding documents by February 2009 and contract awards by November

2009 2. Construction started by January 2010. 3. All subprojects commissioned by March 2012. DISCOM-W 1. Issuance of bidding documents by October 2009 and contract awards by June 2010 2. Construction started by June 2010. 3. All subprojects commissioned by September 2012.

Inputs ADB: $166 million DISCOM-C/FIs/REC/PFC:

$39 million DISCOM-E/FIs/REC/PFC:

$26.3 million DISCOM-W/FIs/REC/PFC:

$24.3 million

ADB = Asian Development Bank, DISCOM-C = central zone distribution company, DISCOM-E = east zone distribution company, DISCOM-W = west zone distribution company, FIs = Financial Institutions, IT = information technology, kV = kilovolt, kVA= kilovolt ampere, LV = low voltage, MVA = megavolt ampere, MW = megawatt, MPERC = Madhya Pradesh Electricity Regulatory Commission, PFC = Power Finance Company, PFR = Periodic Financing Request, REC = Rural Electrification Corporation Ltd.

I. PROJECT DESCRIPTION

A. Project Area and Location

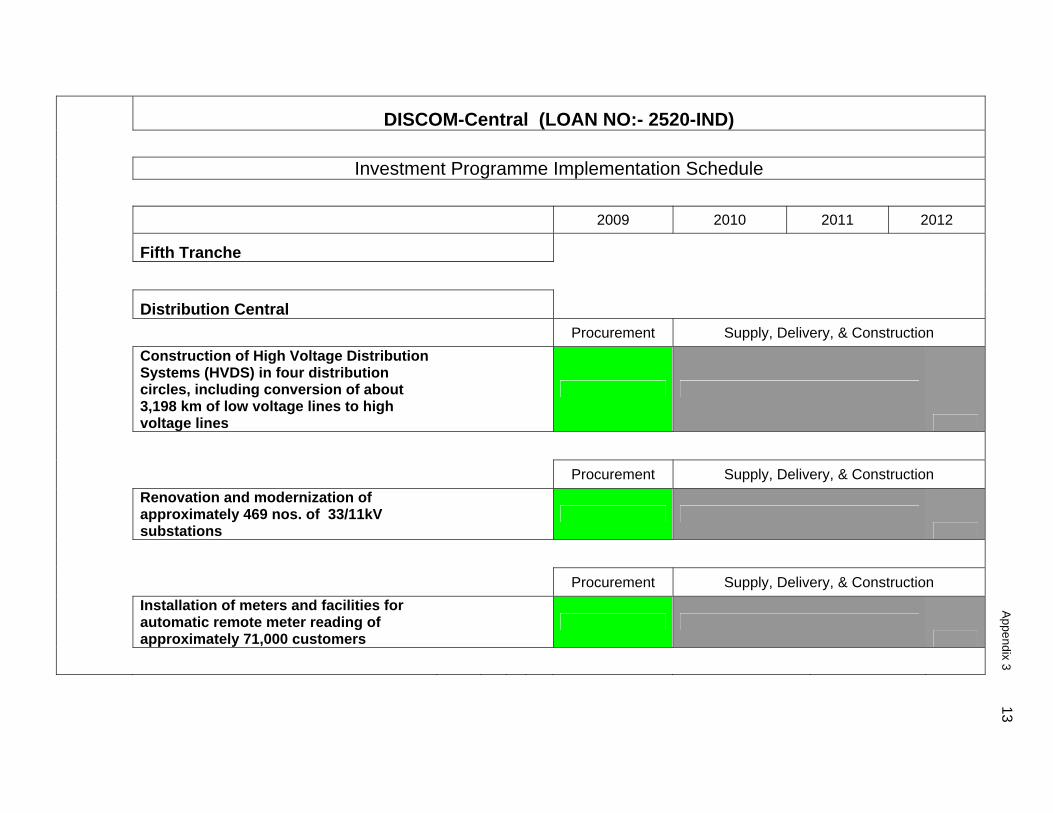

1. The distribution efficiency enhancement proposed to be undertaken in this Project is located in two distribution circles in the central distribution zone and various locations across the State of Madhya Pradesh. B. Impact and Outcome 2. The loan will partially fund distribution system investments to deliver power to consumers more reliability, more efficiently, and at a higher quality. Improvements in voltage profiles will be evident through better lighting and fewer equipment failures. Supply will be more consistent and momentary outages will be significantly reduced. Furthermore, technical and non-technical losses will be reduced. These outcomes will provide support to achieve sector profitability and financial sustainability. C. Project Components 3. The distribution component (DISCOM-C: Part A) consists of the following: (i) construction of High Voltage Distribution Systems (HVDS) in four distribution circles,

including conversion of about 3,198 km of low voltage lines to high voltage lines; (ii) renovation and modernization of approximately 469 nos. of 33/11kV substations; (iii) installation of meters and facilities for automatic remote meter reading of approximately

71,000 customers.

D. Technical Justification and Selection Criteria 4. All selected subprojects have been subject to a rigorous and strict scrutiny process and met all the criteria listed in Schedule 4 to FFA. These subprojects have been examined by the DISCOMs for their technical, economic and financial feasibility; then by the Madhya Pradesh Electricity Regulatory Commission (MPERC) and the Ministry of Power of the India. ADB’s loan processing missions also visited sites, reviewed all available reports, undertook a comprehensive due diligence assessment including safeguard aspects of the subprojects.

II. COST ESTIMATES AND FINANCING PLAN

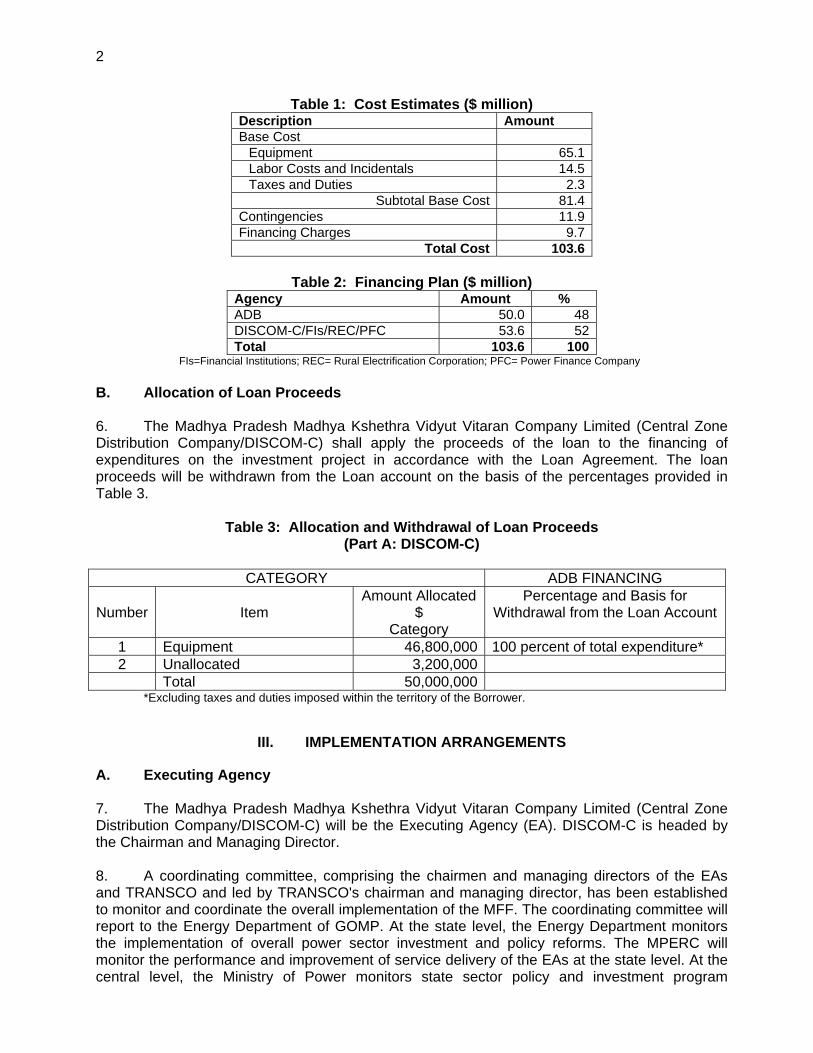

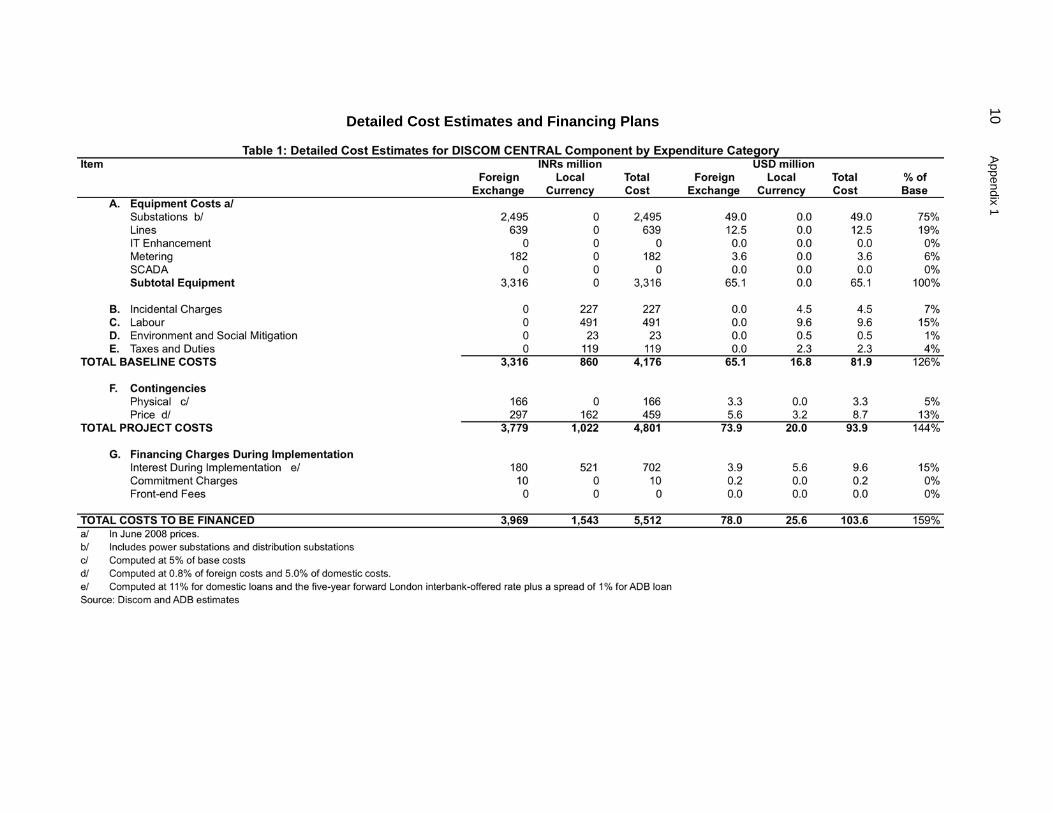

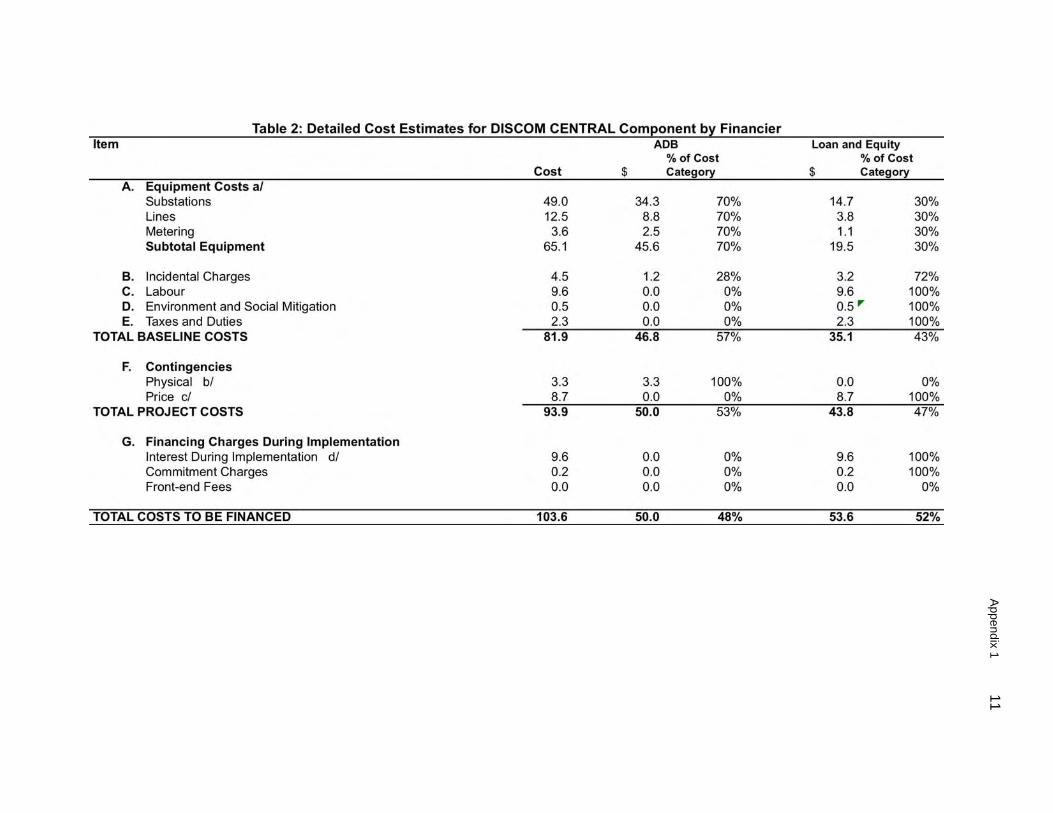

A. Detailed Cost Estimates and Financing Plan 5. The total cost of the investment project is estimated at $103.6 million, inclusive of taxes, duties, and interest and other charges on the loan during construction. Cost estimates are summarized in Table 1, while financing plan is in Table 2. The detailed cost estimates and financing plan are attached as Appendix 1.

2

Table 1: Cost Estimates ($ million) Description Amount Base Cost Equipment 65.1 Labor Costs and Incidentals 14.5 Taxes and Duties 2.3

Subtotal Base Cost 81.4 Contingencies 11.9 Financing Charges 9.7

Total Cost 103.6

Table 2: Financing Plan ($ million) Agency Amount % ADB 50.0 48 DISCOM-C/FIs/REC/PFC 53.6 52 Total 103.6 100

FIs=Financial Institutions; REC= Rural Electrification Corporation; PFC= Power Finance Company

B. Allocation of Loan Proceeds 6. The Madhya Pradesh Madhya Kshethra Vidyut Vitaran Company Limited (Central Zone Distribution Company/DISCOM-C) shall apply the proceeds of the loan to the financing of expenditures on the investment project in accordance with the Loan Agreement. The loan proceeds will be withdrawn from the Loan account on the basis of the percentages provided in Table 3.

Table 3: Allocation and Withdrawal of Loan Proceeds (Part A: DISCOM-C)

CATEGORY ADB FINANCING

Number

Item

Amount Allocated $

Category

Percentage and Basis for Withdrawal from the Loan Account

1 Equipment 46,800,000 100 percent of total expenditure* 2 Unallocated 3,200,000 Total 50,000,000

*Excluding taxes and duties imposed within the territory of the Borrower.

III. IMPLEMENTATION ARRANGEMENTS

A. Executing Agency 7. The Madhya Pradesh Madhya Kshethra Vidyut Vitaran Company Limited (Central Zone Distribution Company/DISCOM-C) will be the Executing Agency (EA). DISCOM-C is headed by the Chairman and Managing Director. 8. A coordinating committee, comprising the chairmen and managing directors of the EAs and TRANSCO and led by TRANSCO's chairman and managing director, has been established to monitor and coordinate the overall implementation of the MFF. The coordinating committee will report to the Energy Department of GOMP. At the state level, the Energy Department monitors the implementation of overall power sector investment and policy reforms. The MPERC will monitor the performance and improvement of service delivery of the EAs at the state level. At the central level, the Ministry of Power monitors state sector policy and investment program

3

implementation. Project management units (PMUs) with technical, financial, procurement and safeguards divisions have been formed. B. Project Management Unit 9. DISCOM-C has established their project management unit (PMU) in Bhopal. The PMU is fully staffed and operational. It has carried out substantial preparatory works such as field survey, preliminary design, economic and financial analysis, preparation of detailed project report (DPR), and preparation of draft bidding documents. During the implementation stage, the PMU conducts day-to-day project management including procurement, construction supervision, inspection and testing of equipment, payments to contractors, monitoring and reporting of progress. The PMU manager reports directly to the Chairman and Managing Director (CMD) DISCOM-C. The organization structure for Project Implementation is in Appendix 2. C. Implementation Schedule 10. The investment project will be implemented over 3 years including procurement and construction activities and is expected to be completed by 31 December 2012. No disbursement from the loan account will be requested or made later than 30 June 2013, or such other date as may from time to time be agreed between the Borrower and ADB. The indicative implementation schedule is shown in Appendix 3.

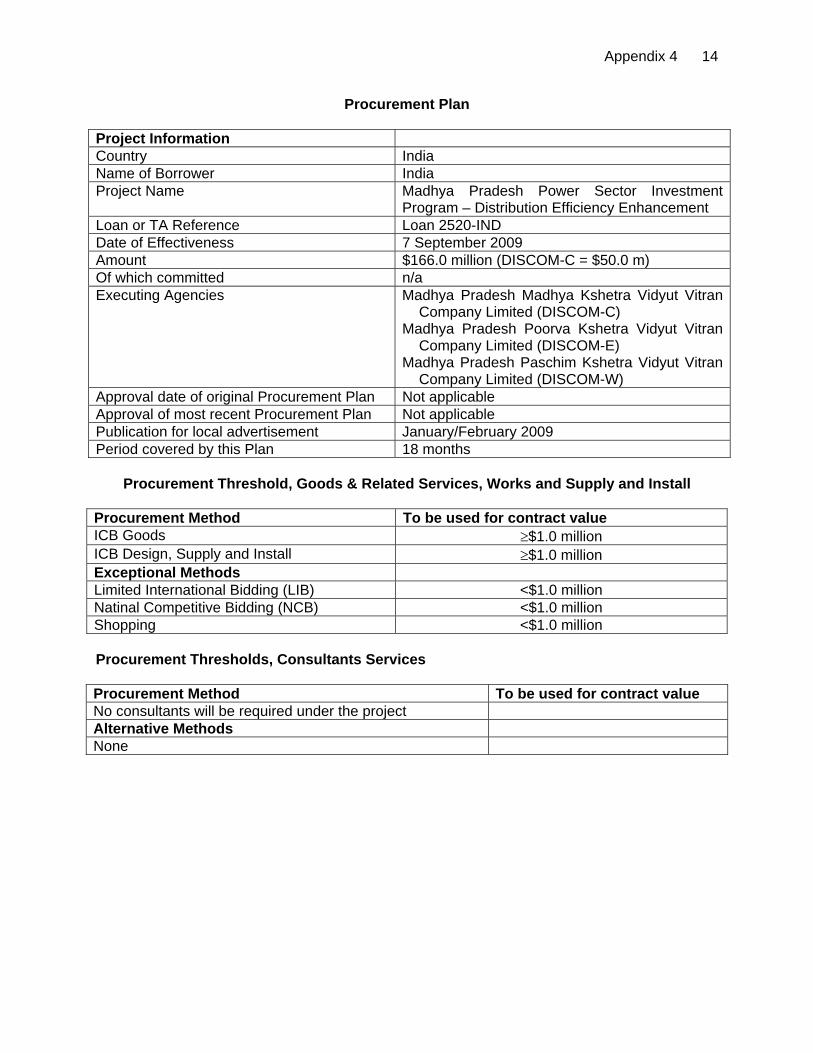

IV. PROCUREMENT

11. Procurement to be financed under MFF will be procured in accordance with ADB’s Procurement Guidelines, 2006 as amended from time to time. International competitive bidding (ICB) will be used for supply of equipment and for contracts estimated to cost more than $1.0 million. The Procurement Plan (including list of contract packages of goods and turnkey contracts) is in Appendix 4. 12. Advance Contracting. To expedite the implementation of the distribution component, at the request of India, ADB approved the advance contracting on 14 January 2009. Bidding documents for most of distribution subprojects have been reviewed and approved by ADB and have been issued in February 2009.

V. DISBURSEMENT PROCEDURES

13. The Loan proceeds will be disbursed in accordance with ADB’s Loan Disbursement Handbook (2007, as amended from time to time). 14. For this loan, India will establish immediately after the effective date three (3) first generation imprest accounts at the Reserve Bank of India, one for each DISCOM. A second generation imprest account will be established by each of the DISCOMs at a commercial bank, acceptable to ADB and India. The imprest accounts (first and second generation) will be established, operated, and maintained in accordance with ADB’s Loan Disbursement Handbook. The imprest accounts shall be checking account, which will facilitate withdrawal of funds to meet project expenditures whenever needed. Interest income earned from the imprest accounts, if any, shall be refunded to ADB.

4

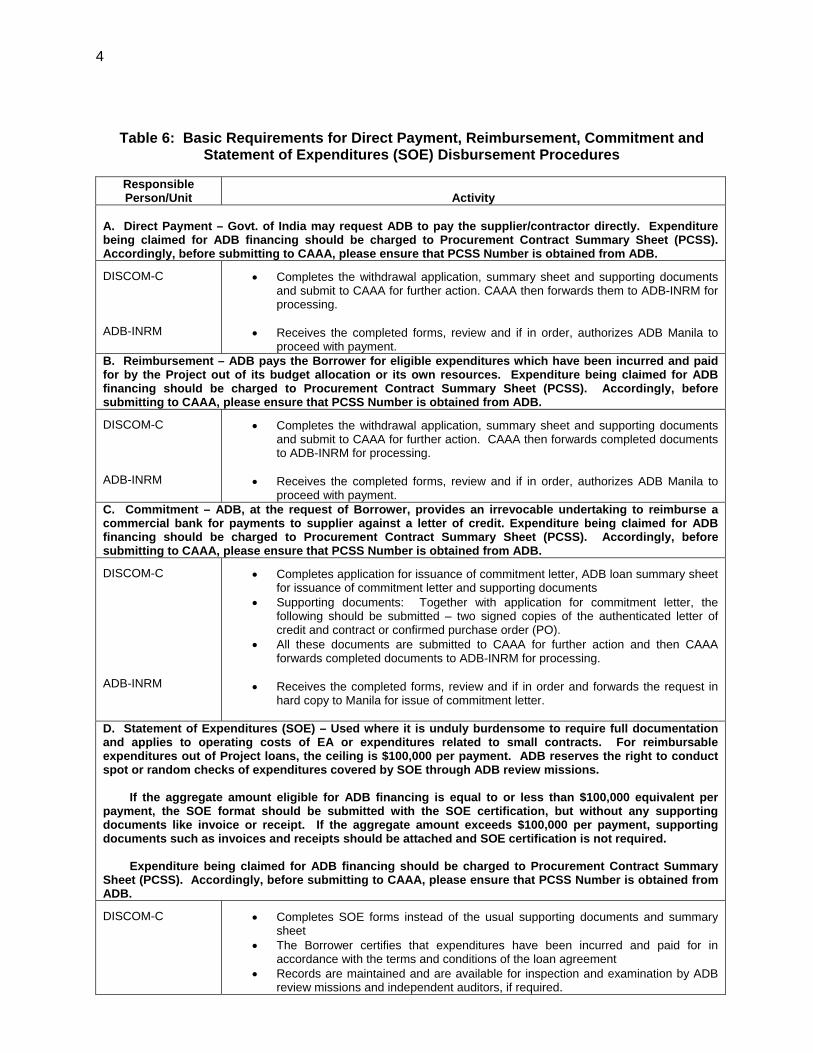

Table 6: Basic Requirements for Direct Payment, Reimbursement, Commitment and Statement of Expenditures (SOE) Disbursement Procedures

Responsible Person/Unit

Activity

A. Direct Payment – Govt. of India may request ADB to pay the supplier/contractor directly. Expenditure being claimed for ADB financing should be charged to Procurement Contract Summary Sheet (PCSS). Accordingly, before submitting to CAAA, please ensure that PCSS Number is obtained from ADB.

DISCOM-C ADB-INRM

Completes the withdrawal application, summary sheet and supporting documents and submit to CAAA for further action. CAAA then forwards them to ADB-INRM for processing.

Receives the completed forms, review and if in order, authorizes ADB Manila to

proceed with payment. B. Reimbursement – ADB pays the Borrower for eligible expenditures which have been incurred and paid for by the Project out of its budget allocation or its own resources. Expenditure being claimed for ADB financing should be charged to Procurement Contract Summary Sheet (PCSS). Accordingly, before submitting to CAAA, please ensure that PCSS Number is obtained from ADB.

DISCOM-C ADB-INRM

Completes the withdrawal application, summary sheet and supporting documents and submit to CAAA for further action. CAAA then forwards completed documents to ADB-INRM for processing.

Receives the completed forms, review and if in order, authorizes ADB Manila to

proceed with payment. C. Commitment – ADB, at the request of Borrower, provides an irrevocable undertaking to reimburse a commercial bank for payments to supplier against a letter of credit. Expenditure being claimed for ADB financing should be charged to Procurement Contract Summary Sheet (PCSS). Accordingly, before submitting to CAAA, please ensure that PCSS Number is obtained from ADB.

DISCOM-C ADB-INRM

Completes application for issuance of commitment letter, ADB loan summary sheet for issuance of commitment letter and supporting documents

Supporting documents: Together with application for commitment letter, the following should be submitted – two signed copies of the authenticated letter of credit and contract or confirmed purchase order (PO).

All these documents are submitted to CAAA for further action and then CAAA forwards completed documents to ADB-INRM for processing.

Receives the completed forms, review and if in order and forwards the request in

hard copy to Manila for issue of commitment letter.

D. Statement of Expenditures (SOE) – Used where it is unduly burdensome to require full documentation and applies to operating costs of EA or expenditures related to small contracts. For reimbursable expenditures out of Project loans, the ceiling is $100,000 per payment. ADB reserves the right to conduct spot or random checks of expenditures covered by SOE through ADB review missions. If the aggregate amount eligible for ADB financing is equal to or less than $100,000 equivalent per payment, the SOE format should be submitted with the SOE certification, but without any supporting documents like invoice or receipt. If the aggregate amount exceeds $100,000 per payment, supporting documents such as invoices and receipts should be attached and SOE certification is not required. Expenditure being claimed for ADB financing should be charged to Procurement Contract Summary Sheet (PCSS). Accordingly, before submitting to CAAA, please ensure that PCSS Number is obtained from ADB.

DISCOM-C

Completes SOE forms instead of the usual supporting documents and summary sheet

The Borrower certifies that expenditures have been incurred and paid for in accordance with the terms and conditions of the loan agreement

Records are maintained and are available for inspection and examination by ADB review missions and independent auditors, if required.

5

ADB-INRM

Receives the completed forms, review and if in order, authorizes ADB Manila to

proceed with payment.

VI. PROJECT MONITORING AND EVALUATION

15. The Government will ensure that within 3 months of the Effective Date, a Project Performance Monitoring System (PPMS) is established by DISCOM-C in a form and with a composition acceptable to ADB in accordance with the Investment Program and Project performance indicators. DISCOM-C will undertake periodic Project performance review, and also for the Investment Program in accordance with the PPMS to evaluate the scope, implementation arrangements, progress and achievements of objectives of the related subproject and overall Investment Program. A. Inception Mission

16. An inception mission was fielded on 5-16 October 2009 to discuss and finalize the PAM, and ensure that all administrative matters pertaining to the Project are properly in place and working relationships are established between concerned ADB staff and DISCOM-C staff. Details in relation to report requirements, accounting system, compliance with loan covenants, disbursement procedures and withdrawal applications were clarified during the mission. B. Review Missions

17. Review missions will be conducted to monitor overall progress of the Project, review expenditures and cost estimates and most importantly discuss problems and issues causing delays in project implementation, monitor the overall performance of DISCOM-C and will be fielded by ADB as and when required but at least twice a year. The mid-term review mission will be fielded by mid-2011.

VII. ACCOUNTING, AUDITING AND REPORTING

18. Quarterly progress reports will be prepared by DISCOM-C/PMU for review by ADB. The first report as of 31 Dec 2009 will be submitted to ADB on or before 30 January 2010. It will include progress made against established targets during the period under review, changes if any of the implementation schedule, problems or difficulties encountered and remedial measures taken, utilization of funds, physical and financial progress and proposed works to be undertaken in the coming quarter. It should be submitted to ADB within 30 days of the close of each quarter, including a summary financial account for each subproject, expenditures to date and report on benefit monitoring. Suggested format of progress report is in Appendix 5. A calculation method of progress report was discussed and agreed during the Inception mission in October 2009 and is presented as Appendix 6. 19. A project completion report will be submitted by the Government within 3 months of the completion of the project by the State, acting through DISCOM-C, and the facility completion report within 3 months of physical completion of the investment program. This report will include a detailed evaluation of the project and the facility covering the design, costs, contractors ‘performance, social and economic impact, economic rate of return, and other details relating to the Project and Facility as may be requested by ADB. 20. Within 6 months of the close of the financial year, the EA will submit audited project accounts and financial statements. An independent auditor acceptable to ADB will be hired by the

6

EA to conduct this audit. The first submission for FY 2009 would be by 30 September 2010. A copy of Audit Letter is in Appendix 7. 21. The DISCOM-C will ensure that in addition to the financial and procurement audits, (i) energy audit, (ii) business process, and (iii) performance audits in all operational areas are conducted annually by independent auditors whose qualifications, experience and terms of reference are acceptable to ADB.

VIII. SAFEGUARDS 22. Social Safeguards. Given the nature of the Tranche 5 investments, there will be no impact regarding land acquisition, resettlement, and indigenous peoples for the components under Tranche 5. In fact, the bulk of this tranche's investments will be upgrading distribution lines and substations within the existing premises. New distributions lines will also be built along roads. It has been assured by the EA and also it has been appraised that there will be no land acquisition and resettlement issues involved in Tranche 5. It has also been verified on the ground that there are no informal settlers in the subproject areas under this tranche. Therefore, no RP and no IPDP are required. Extensive consultations were carried out with the local people who will help for a smooth implementation of the project. 23. Environmental. Environmental assessment revealed that none of the Tranche 5 components will cause any significant adverse impacts. No environmental impact was caused due the location of the subproject activities. Minor negative impacts are anticipated mostly during the construction phase. The IEE has assessed all potential environmental impacts associated with the subprojects. On the basis of the environmental assessment, the components of Tranche 5 were found to be environmentally acceptable and the categorization of the subprojects as “Category B” is appropriate.

IX. MAJOR LOAN COVENANTS

24. In addition to the standard assurances, the Government, DISCOM-C, and ADB agreed to the additional assurances and the summary on status of compliance is shown in Appendix 8.

X. KEY PERSONS INVOLVED IN THE PROJECT

A. Executing Agency The Government of India:

Ministry of Finance Dr. Anup K. Pujari Joint Secretary(MI) Department of Economic Affairs

Tel. No.: (91-11) 2309- Fax No.: (91-11) 2309-2024 Government of Madhya Pradesh Bhopal

Mr. S. P. S. Parihar Secretary, Energy Department E-mail: [email protected]

Tel. No.: (91-755) 244-2055 Fax No. (91-755) 244-1642

7

Project Executing Agency: Madhya Pradesh Madhya Kshethra Vidyut Vitaran Company Limited (Central Zone Distribution Company /DISCOM-C) Bhopal

Mr. Sanjay Shukla Chairman and Managing Director Tel. No.: 0755-2678377 E-mail: [email protected] [email protected]

Mr. M. K. Gupta

Chief Engineer (ADB and S&P) Tel. No.: 0755-4261703 ext 188

E-mail: [email protected] Mr. Y. K. Gupta

Director (Finance) Tel. No.: 0755-2602033 E-mail: [email protected]

Mr. R. Dehariya

Superintending Engineer (ADB Cell) Tel. No.: 0755-4261703 ext 138

E-mail: [email protected]

Mr. Prakash Gupta Executive Engineer (ADB Cell)

Tel. No.: 0755-4261703 ext 184 E-mail: [email protected]

Address & Fax No. (DISCOM-C):

Nishtha Parisar, Govindpura Bhopal, Madhya Pradesh 462 023, India Fax No.: 0755-258-9821

B. ADB Staff

Energy Division (SAEN) Mr. Thevakumar Kandiah South Asia Regional Department (SARD)

Director, SAEN Tel. No.: (63-2) 632-6301

E-mail: [email protected] Mr. Mukhtor Khamudkhanov Senior Energy Specialist, SAEN Tel. No.: (63-2) 632-6289 E-mail: [email protected]

Ms. Marietta L. Marasigan Project Officer Tel. No.: (63-2) 632-6800 E-mail: [email protected]

8

Controller’s Department Mr. Francis Mathew Loan Administration Division Financial Control Specialist (CTLA1) Tel. No.: (63-2) 632-4603 E-mail: [email protected] Address & Fax No. (SAEN):

Asian Development Bank 6 ADB Ave., Mandaluyong City, 1550 Metro Manila, Philippines Fax No. (632) 636-2338 (SAEN)

India Resident Mission (INRM) Mr. Tadashi Kondo Country Director E-mail: tkondo@adb,org Mr. Shigehiko Muramoto Head Project Administration Unit E-mail: [email protected]

Mr. Vallabh Rao Karbar Project Implementation Officer (Energy) E-mail: [email protected]

Mr. J. Srinivasan Senior Control Officer, E-mail: [email protected]

Address & Contact Nos. (INRM):

India Resident Mission (INRM)4 San Martin Marg Chanakyapuri New Delhi 110021, India Tel: + 91 11 2410 7200 Fax: + 91 11 2687 0955 Email: [email protected]

Website Address of ADB: http://www.adb.org

XI. ANTICORRUPTION

25. ADB defines corruption as “abuse of public or private office for personal gain”. ADB will systematically identify, in consultation with its member countries’ opportunities for reducing corruption as part of its broader emphasis on improving good governance and sound development management. ADB’s Anticorruption Policy has set the guidelines and procedures in addressing fraudulent corrupt practices. Anyone coming across evidence of fraud or corruption associated with the Investment Program must contact ADB’s Office of the General Auditor, who will investigate such allegations.

10 A

ppendix 1

Detailed Cost Estimates and Financing Plans

Appe

ndix 1 11

12 A

ppendix 2

Organizational Plan of DISCOM-C

Appe

ndix 3 13

DISCOM-Central (LOAN NO:- 2520-IND)

Investment Programme Implementation Schedule

2009 2010 2011 2012

Fifth Tranche

Distribution Central

Procurement Supply, Delivery, & Construction

Construction of High Voltage Distribution Systems (HVDS) in four distribution circles, including conversion of about 3,198 km of low voltage lines to high voltage lines

Procurement Supply, Delivery, & Construction

Renovation and modernization of approximately 469 nos. of 33/11kV substations

Procurement Supply, Delivery, & Construction

Installation of meters and facilities for automatic remote meter reading of approximately 71,000 customers

Appendix 4 14

Procurement Plan Project Information Country India Name of Borrower India Project Name Madhya Pradesh Power Sector Investment

Program – Distribution Efficiency Enhancement Loan or TA Reference Loan 2520-IND Date of Effectiveness 7 September 2009 Amount $166.0 million (DISCOM-C = $50.0 m) Of which committed n/a Executing Agencies Madhya Pradesh Madhya Kshetra Vidyut Vitran

Company Limited (DISCOM-C) Madhya Pradesh Poorva Kshetra Vidyut Vitran

Company Limited (DISCOM-E) Madhya Pradesh Paschim Kshetra Vidyut Vitran

Company Limited (DISCOM-W) Approval date of original Procurement Plan Not applicable Approval of most recent Procurement Plan Not applicable Publication for local advertisement January/February 2009 Period covered by this Plan 18 months

Procurement Threshold, Goods & Related Services, Works and Supply and Install

Procurement Method To be used for contract value ICB Goods $1.0 million ICB Design, Supply and Install $1.0 million Exceptional Methods Limited International Bidding (LIB) <$1.0 million Natinal Competitive Bidding (NCB) <$1.0 million Shopping <$1.0 million

Procurement Thresholds, Consultants Services Procurement Method To be used for contract value No consultants will be required under the project Alternative Methods None

Appendix 4 15

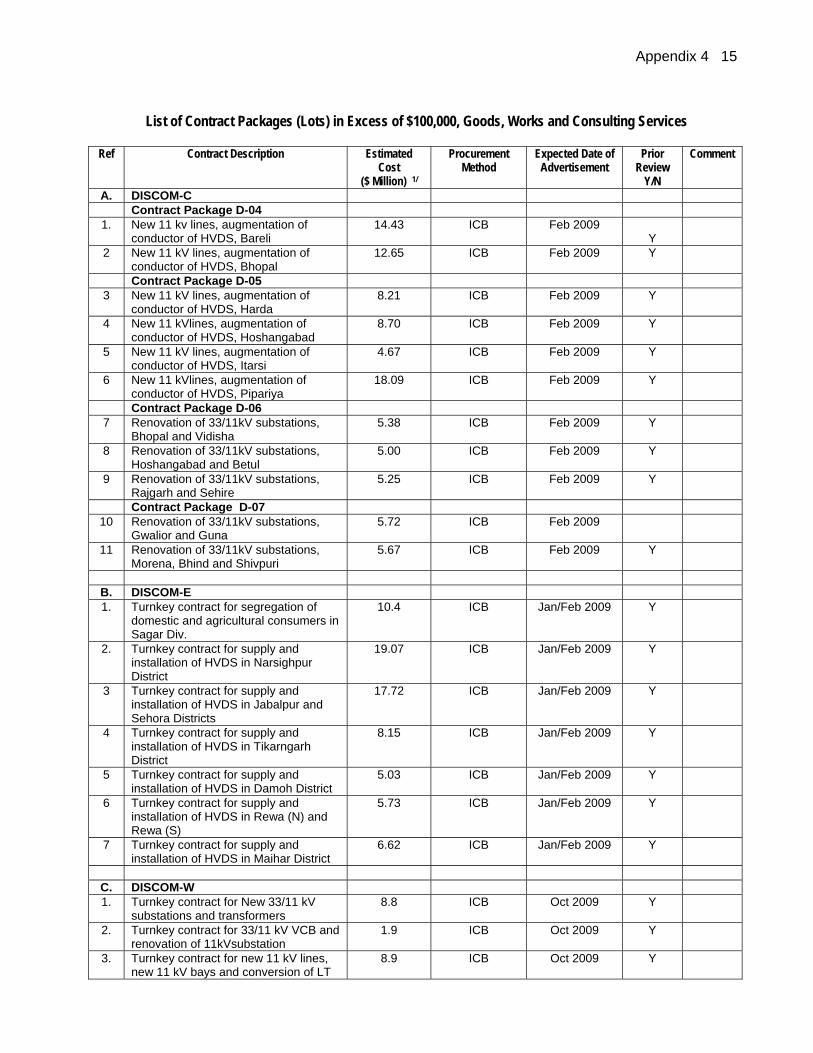

List of Contract Packages (Lots) in Excess of $100,000, Goods, Works and Consulting Services

Ref Contract Description Estimated

Cost ($ Million) 1/

Procurement Method

Expected Date of Advertisement

Prior Review

Y/N

Comment

A. DISCOM-C Contract Package D-04

1. New 11 kv lines, augmentation of conductor of HVDS, Bareli

14.43 ICB Feb 2009 Y

2 New 11 kV lines, augmentation of conductor of HVDS, Bhopal

12.65 ICB Feb 2009 Y

Contract Package D-05 3 New 11 kV lines, augmentation of

conductor of HVDS, Harda 8.21 ICB Feb 2009 Y

4 New 11 kVlines, augmentation of conductor of HVDS, Hoshangabad

8.70 ICB Feb 2009 Y

5 New 11 kV lines, augmentation of conductor of HVDS, Itarsi

4.67 ICB Feb 2009 Y

6 New 11 kVlines, augmentation of conductor of HVDS, Pipariya

18.09 ICB Feb 2009 Y

Contract Package D-06 7 Renovation of 33/11kV substations,

Bhopal and Vidisha 5.38 ICB Feb 2009 Y

8 Renovation of 33/11kV substations, Hoshangabad and Betul

5.00 ICB Feb 2009 Y

9 Renovation of 33/11kV substations, Rajgarh and Sehire

5.25 ICB Feb 2009 Y

Contract Package D-07 10 Renovation of 33/11kV substations,

Gwalior and Guna 5.72 ICB Feb 2009

11 Renovation of 33/11kV substations, Morena, Bhind and Shivpuri

5.67 ICB Feb 2009 Y

B. DISCOM-E 1. Turnkey contract for segregation of

domestic and agricultural consumers in Sagar Div.

10.4 ICB Jan/Feb 2009 Y

2. Turnkey contract for supply and installation of HVDS in Narsighpur District

19.07 ICB Jan/Feb 2009 Y

3 Turnkey contract for supply and installation of HVDS in Jabalpur and Sehora Districts

17.72 ICB Jan/Feb 2009 Y

4 Turnkey contract for supply and installation of HVDS in Tikarngarh District

8.15 ICB Jan/Feb 2009 Y

5 Turnkey contract for supply and installation of HVDS in Damoh District

5.03 ICB Jan/Feb 2009 Y

6 Turnkey contract for supply and installation of HVDS in Rewa (N) and Rewa (S)

5.73 ICB Jan/Feb 2009 Y

7 Turnkey contract for supply and installation of HVDS in Maihar District

6.62 ICB Jan/Feb 2009 Y

C. DISCOM-W 1. Turnkey contract for New 33/11 kV

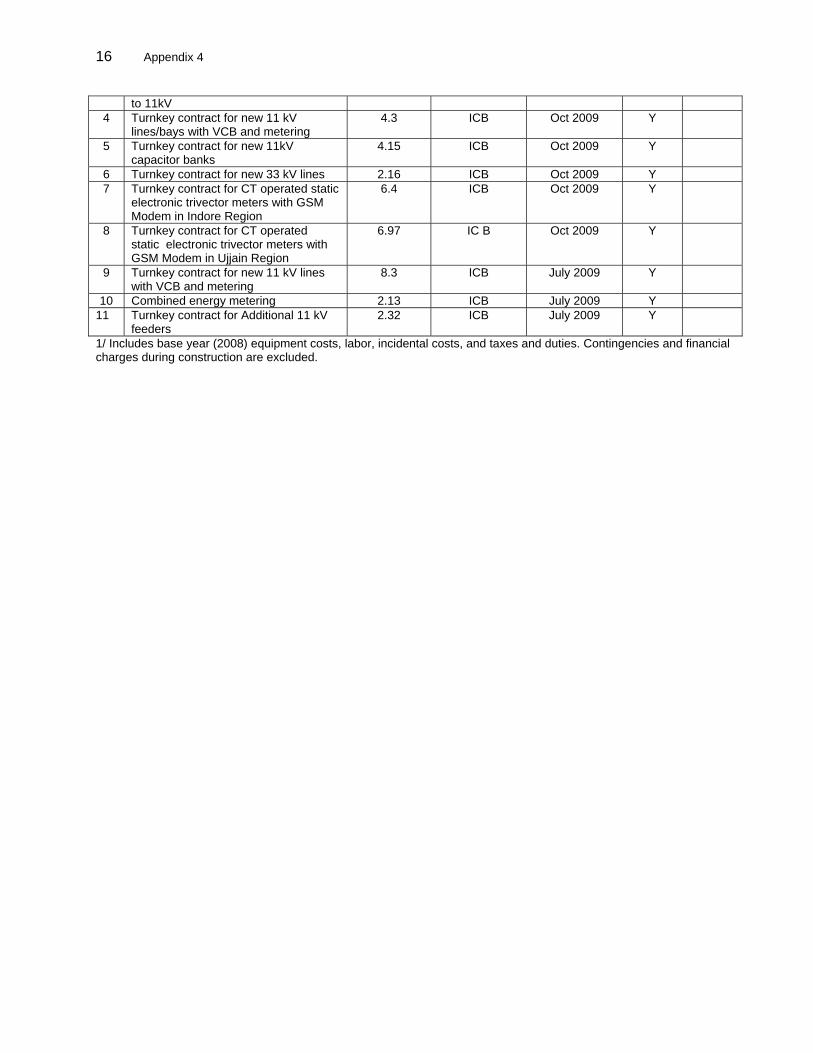

substations and transformers 8.8 ICB Oct 2009 Y

2. Turnkey contract for 33/11 kV VCB and renovation of 11kVsubstation

1.9 ICB Oct 2009 Y

3. Turnkey contract for new 11 kV lines, new 11 kV bays and conversion of LT

8.9 ICB Oct 2009 Y

16 Appendix 4

to 11kV 4 Turnkey contract for new 11 kV

lines/bays with VCB and metering 4.3 ICB Oct 2009 Y

5 Turnkey contract for new 11kV capacitor banks

4.15 ICB Oct 2009 Y

6 Turnkey contract for new 33 kV lines 2.16 ICB Oct 2009 Y 7 Turnkey contract for CT operated static

electronic trivector meters with GSM Modem in Indore Region

6.4 ICB Oct 2009 Y

8 Turnkey contract for CT operated static electronic trivector meters with GSM Modem in Ujjain Region

6.97 IC B Oct 2009 Y

9 Turnkey contract for new 11 kV lines with VCB and metering

8.3 ICB July 2009 Y

10 Combined energy metering 2.13 ICB July 2009 Y 11 Turnkey contract for Additional 11 kV

feeders 2.32 ICB July 2009 Y

1/ Includes base year (2008) equipment costs, labor, incidental costs, and taxes and duties. Contingencies and financial charges during construction are excluded.

Appendix 5 17

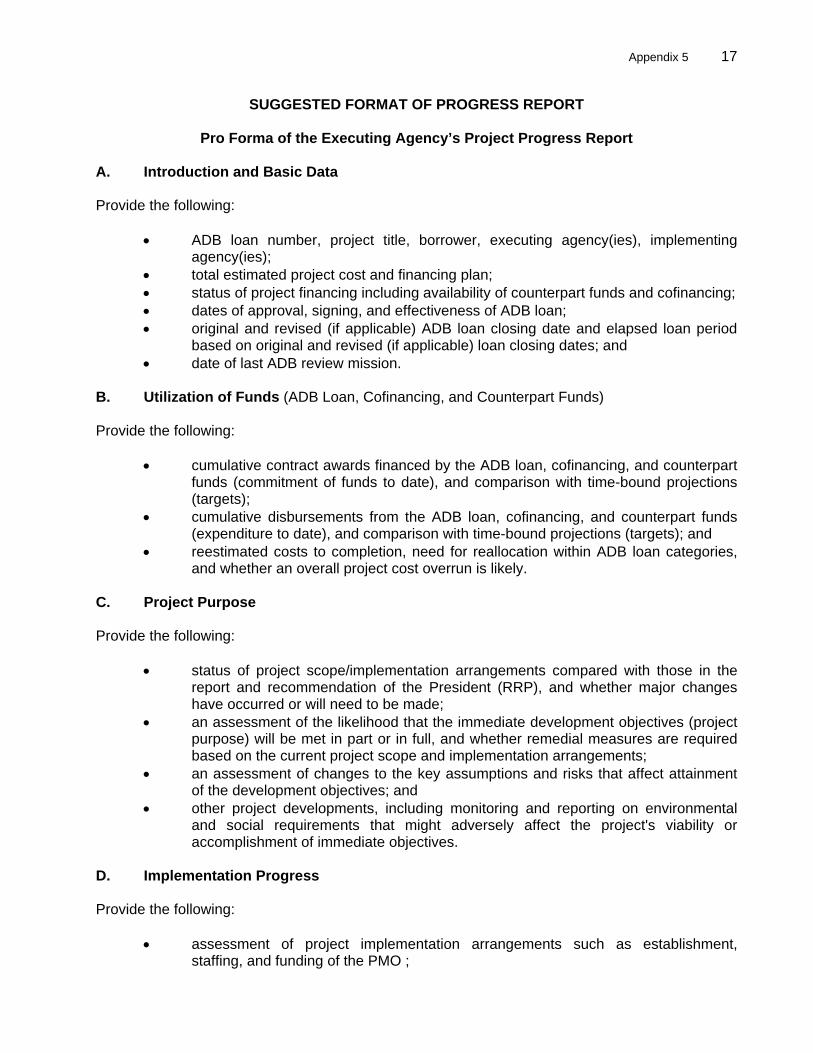

SUGGESTED FORMAT OF PROGRESS REPORT

Pro Forma of the Executing Agency’s Project Progress Report A. Introduction and Basic Data Provide the following:

ADB loan number, project title, borrower, executing agency(ies), implementing agency(ies);

total estimated project cost and financing plan; status of project financing including availability of counterpart funds and cofinancing; dates of approval, signing, and effectiveness of ADB loan; original and revised (if applicable) ADB loan closing date and elapsed loan period

based on original and revised (if applicable) loan closing dates; and date of last ADB review mission.

B. Utilization of Funds (ADB Loan, Cofinancing, and Counterpart Funds) Provide the following:

cumulative contract awards financed by the ADB loan, cofinancing, and counterpart funds (commitment of funds to date), and comparison with time-bound projections (targets);

cumulative disbursements from the ADB loan, cofinancing, and counterpart funds (expenditure to date), and comparison with time-bound projections (targets); and

reestimated costs to completion, need for reallocation within ADB loan categories, and whether an overall project cost overrun is likely.

C. Project Purpose Provide the following:

status of project scope/implementation arrangements compared with those in the report and recommendation of the President (RRP), and whether major changes have occurred or will need to be made;

an assessment of the likelihood that the immediate development objectives (project purpose) will be met in part or in full, and whether remedial measures are required based on the current project scope and implementation arrangements;

an assessment of changes to the key assumptions and risks that affect attainment of the development objectives; and

other project developments, including monitoring and reporting on environmental and social requirements that might adversely affect the project's viability or accomplishment of immediate objectives.

D. Implementation Progress Provide the following:

assessment of project implementation arrangements such as establishment, staffing, and funding of the PMO ;

18 Appendix 5

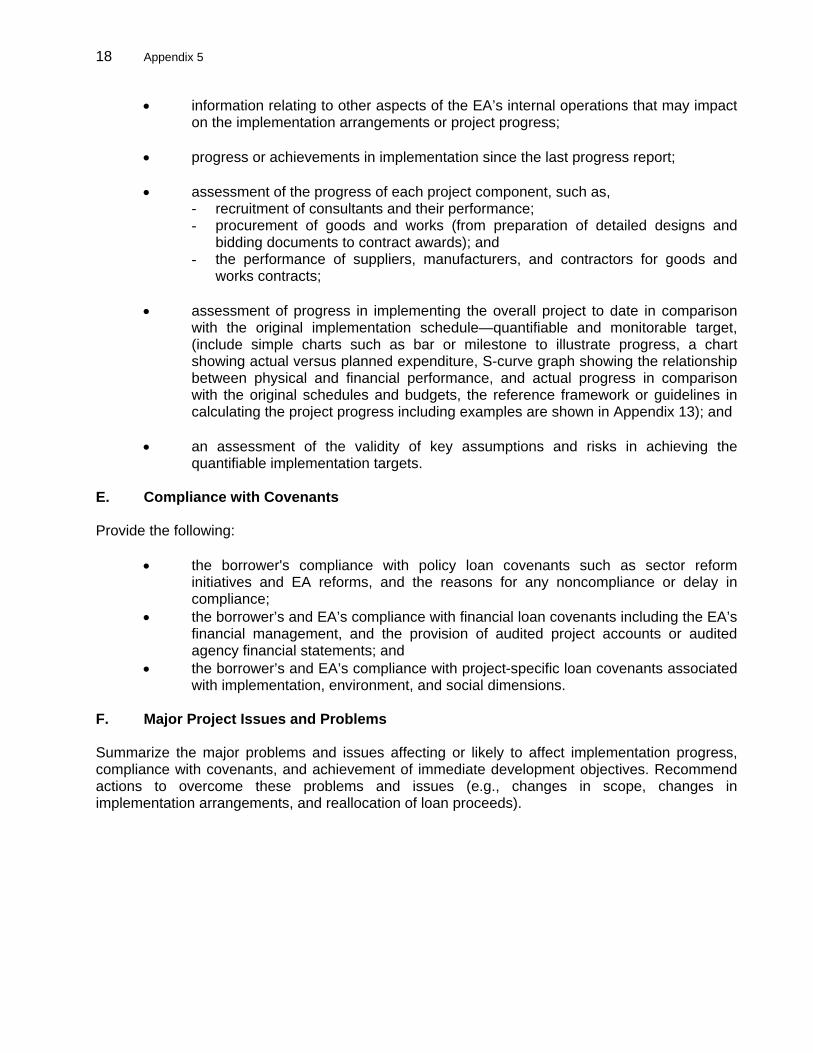

information relating to other aspects of the EA’s internal operations that may impact on the implementation arrangements or project progress;

progress or achievements in implementation since the last progress report; assessment of the progress of each project component, such as,

- recruitment of consultants and their performance; - procurement of goods and works (from preparation of detailed designs and

bidding documents to contract awards); and - the performance of suppliers, manufacturers, and contractors for goods and

works contracts;

assessment of progress in implementing the overall project to date in comparison with the original implementation schedule—quantifiable and monitorable target, (include simple charts such as bar or milestone to illustrate progress, a chart showing actual versus planned expenditure, S-curve graph showing the relationship between physical and financial performance, and actual progress in comparison with the original schedules and budgets, the reference framework or guidelines in calculating the project progress including examples are shown in Appendix 13); and

an assessment of the validity of key assumptions and risks in achieving the

quantifiable implementation targets. E. Compliance with Covenants Provide the following:

the borrower's compliance with policy loan covenants such as sector reform initiatives and EA reforms, and the reasons for any noncompliance or delay in compliance;

the borrower’s and EA’s compliance with financial loan covenants including the EA’s financial management, and the provision of audited project accounts or audited agency financial statements; and

the borrower’s and EA’s compliance with project-specific loan covenants associated with implementation, environment, and social dimensions.

F. Major Project Issues and Problems Summarize the major problems and issues affecting or likely to affect implementation progress, compliance with covenants, and achievement of immediate development objectives. Recommend actions to overcome these problems and issues (e.g., changes in scope, changes in implementation arrangements, and reallocation of loan proceeds).

Appendix 6 19

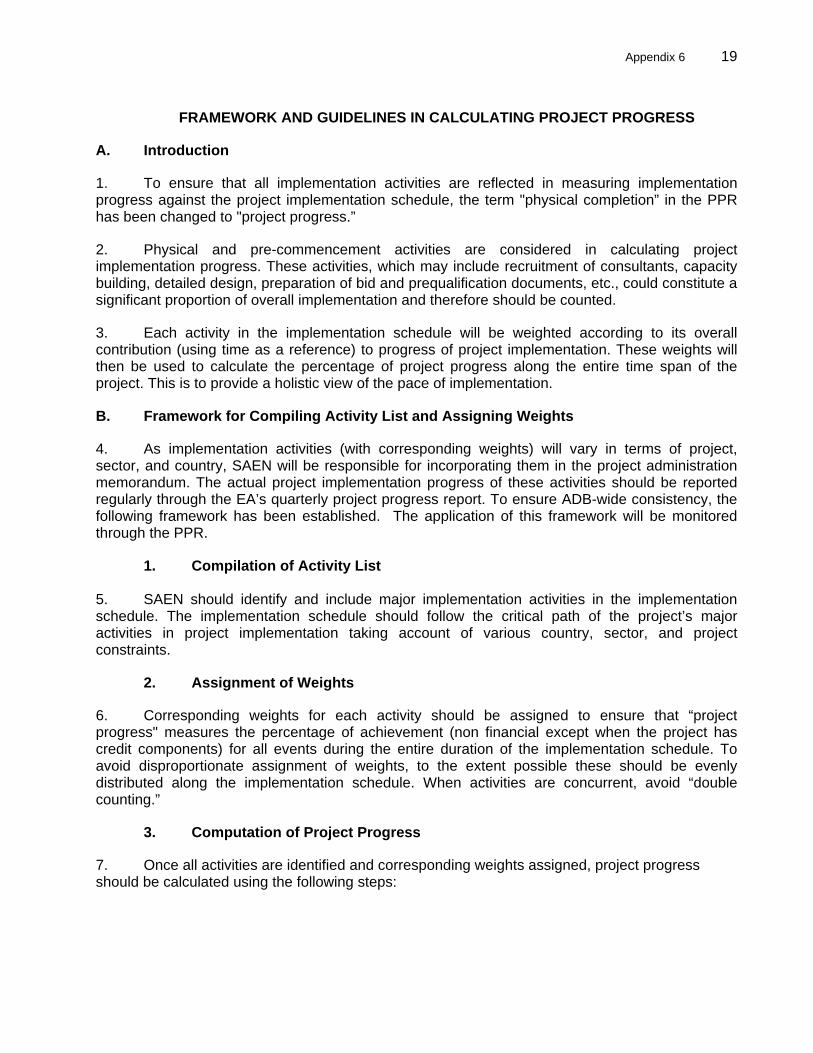

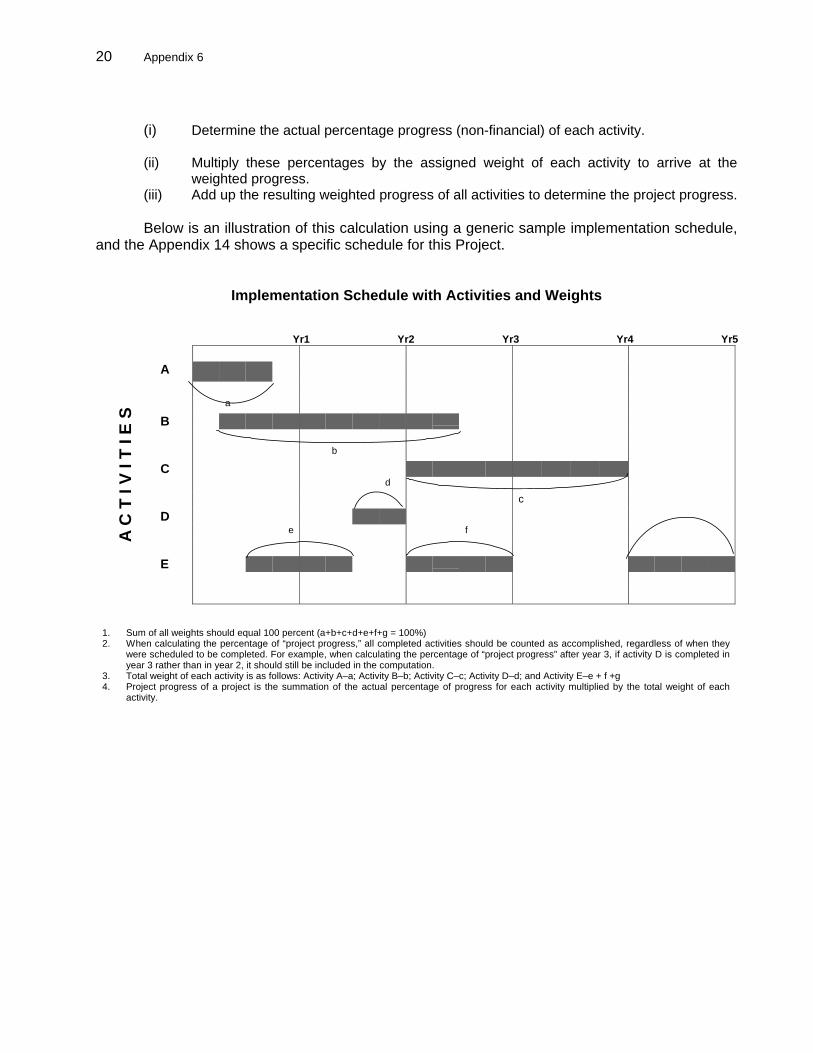

FRAMEWORK AND GUIDELINES IN CALCULATING PROJECT PROGRESS

A. Introduction

1. To ensure that all implementation activities are reflected in measuring implementation progress against the project implementation schedule, the term "physical completion” in the PPR has been changed to "project progress.”

2. Physical and pre-commencement activities are considered in calculating project implementation progress. These activities, which may include recruitment of consultants, capacity building, detailed design, preparation of bid and prequalification documents, etc., could constitute a significant proportion of overall implementation and therefore should be counted.

3. Each activity in the implementation schedule will be weighted according to its overall contribution (using time as a reference) to progress of project implementation. These weights will then be used to calculate the percentage of project progress along the entire time span of the project. This is to provide a holistic view of the pace of implementation.

B. Framework for Compiling Activity List and Assigning Weights

4. As implementation activities (with corresponding weights) will vary in terms of project, sector, and country, SAEN will be responsible for incorporating them in the project administration memorandum. The actual project implementation progress of these activities should be reported regularly through the EA’s quarterly project progress report. To ensure ADB-wide consistency, the following framework has been established. The application of this framework will be monitored through the PPR.

1. Compilation of Activity List 5. SAEN should identify and include major implementation activities in the implementation schedule. The implementation schedule should follow the critical path of the project’s major activities in project implementation taking account of various country, sector, and project constraints.

2. Assignment of Weights

6. Corresponding weights for each activity should be assigned to ensure that “project progress" measures the percentage of achievement (non financial except when the project has credit components) for all events during the entire duration of the implementation schedule. To avoid disproportionate assignment of weights, to the extent possible these should be evenly distributed along the implementation schedule. When activities are concurrent, avoid “double counting.”

3. Computation of Project Progress

7. Once all activities are identified and corresponding weights assigned, project progress should be calculated using the following steps:

20 Appendix 6

(i) Determine the actual percentage progress (non-financial) of each activity. (ii) Multiply these percentages by the assigned weight of each activity to arrive at the

weighted progress. (iii) Add up the resulting weighted progress of all activities to determine the project progress. Below is an illustration of this calculation using a generic sample implementation schedule,

and the Appendix 14 shows a specific schedule for this Project.

Implementation Schedule with Activities and Weights

Yr1 Yr2 Yr3 Yr4 Yr5

A

a

B

b

Cd

c

De f

E

A C

T I

V I

T I

E S

1. Sum of all weights should equal 100 percent (a+b+c+d+e+f+g = 100%)2. When calculating the percentage of “project progress,” all completed activities should be counted as accomplished, regardless of when they

were scheduled to be completed. For example, when calculating the percentage of “project progress” after year 3, if activity D is completed inyear 3 rather than in year 2, it should still be included in the computation.

3. Total weight of each activity is as follows: Activity A–a; Activity B–b; Activity C–c; Activity D–d; and Activity E–e + f +g4. Project progress of a project is the summation of the actual percentage of progress for each activity multiplied by the total weight of each

activity.

Appendix 6 21

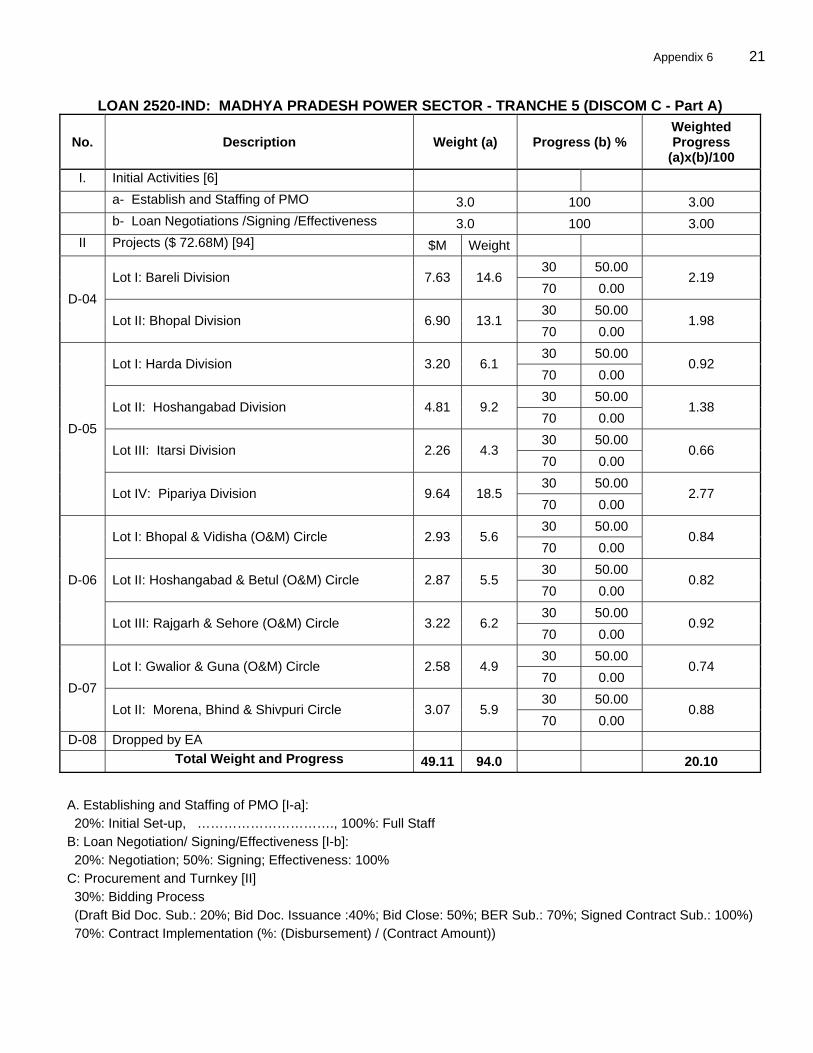

LOAN 2520-IND: MADHYA PRADESH POWER SECTOR - TRANCHE 5 (DISCOM C - Part A)

No. Description Weight (a) Progress (b) % Weighted Progress

(a)x(b)/100

I. Initial Activities [6]

a- Establish and Staffing of PMO 3.0 100 3.00

b- Loan Negotiations /Signing /Effectiveness 3.0 100 3.00

II Projects ($ 72.68M) [94] $M Weight

30 50.00 Lot I: Bareli Division 7.63 14.6

70 0.00 2.19

30 50.00 D-04

Lot II: Bhopal Division 6.90 13.1 70 0.00

1.98

30 50.00 Lot I: Harda Division 3.20 6.1

70 0.00 0.92

30 50.00 Lot II: Hoshangabad Division 4.81 9.2

70 0.00 1.38

30 50.00 Lot III: Itarsi Division 2.26 4.3

70 0.00 0.66

30 50.00

D-05

Lot IV: Pipariya Division 9.64 18.5 70 0.00

2.77

30 50.00 Lot I: Bhopal & Vidisha (O&M) Circle 2.93 5.6

70 0.00 0.84

30 50.00 Lot II: Hoshangabad & Betul (O&M) Circle 2.87 5.5

70 0.00 0.82

30 50.00

D-06

Lot III: Rajgarh & Sehore (O&M) Circle 3.22 6.2 70 0.00

0.92

30 50.00 Lot I: Gwalior & Guna (O&M) Circle 2.58 4.9

70 0.00 0.74

30 50.00 D-07

Lot II: Morena, Bhind & Shivpuri Circle 3.07 5.9 70 0.00

0.88

D-08 Dropped by EA Total Weight and Progress 49.11 94.0 20.10

A. Establishing and Staffing of PMO [I-a]: 20%: Initial Set-up, …………………………., 100%: Full Staff B: Loan Negotiation/ Signing/Effectiveness [I-b]: 20%: Negotiation; 50%: Signing; Effectiveness: 100% C: Procurement and Turnkey [II] 30%: Bidding Process (Draft Bid Doc. Sub.: 20%; Bid Doc. Issuance :40%; Bid Close: 50%; BER Sub.: 70%; Signed Contract Sub.: 100%) 70%: Contract Implementation (%: (Disbursement) / (Contract Amount))

22 Appendix 7

15 September 2009

Dr. Anup K. Pujari Joint Secretary Department of Economic Affairs Ministry of Finance Government of India Dear Dr. Pujari::

Subject: Loan Nos. 2520-IND: Madhya Pradesh Power Sector Investment Program (MFF) – Projects 5

- FINANCIAL REPORTING AND AUDITING REQUIREMENTS This letter is to ensure your timely compliance with the loan covenants and the quality of financial information as required by ADB. ADB's Handbook on the Financial Management and Analysis of Projects (the Booklet) is enclosed to guide you. ADB, by its Charter, is required to ensure that the proceeds of any loan made, guaranteed, or participated in by ADB are used for the purposes for which the loan was approved. ADB requires accurate and timely financial information from its borrowers to be assured that expenditure was for the purposes stated in the loan agreement. For this particular loan, the requirements are stipulated in Schedule 5, paras 8 and 9 of the Loan Agreement dated 27 May 2009 between ADB and India and Section 2.09, (a) and (b) of the Project Agreement dated 27 May 2009 between ADB and State of Madhya Pradesh, Madhya Pradesh Poorv Kshetra Vidyut Vitaran Company Limited (DISCOM-E), Madhya Pradesh Madya Kshetra Vidyut Vitaran Company Limited (DISCOM-C), and Madhya Pradesh Paschim Kshetra Vidyut Vitaran Company Limited (DISCOM-W). Copies of the Loan/Project Agreements are enclosed for onward transmission by your office to your EA and the auditor(s), together with a copy of this letter. The following are the main requirements:

ADB requires the EA to maintain separate project accounts and records exclusively for the Project to ensure that the loan funds were used only for the objectives set out in the Loan or Project Agreements. The first set of project accounts to be submitted to ADB covers the fiscal year ending 31 March 2009. As stipulated in the Loan or Project Agreements, they are to be submitted up to nine (9) months after the end of the fiscal year. For this loan, the deadline is by 31 December 2010. A sample report format with explanatory notes, is attached as Annex A.

The accounts and records for the project are to be consistently maintained by using sound

accounting principles. Please stipulate that your external auditor is to express an opinion on whether the financial report has been prepared using international or local generally accepted accounting standards and whether they have been applied consistently.

ADB prefers project accounts to use international accounting standards prescribed by the

International Accounting Standards Committee. Please advise your external auditor to comment on

Appendix 7 23

the impact of any deviations, by State of Madhya Pradesh, Madhya Pradesh Poorv Kshetra Vidyut Vitaran Company Limited (DISCOM-E), Madhya Pradesh Madya Kshetra Vidyut Vitaran Company Limited (DISCOM-C), and Madhya Pradesh Paschim Kshetra Vidyut Vitaran Company Limited (DISCOM-W) from international accounting standards.

Please ensure that your external auditor specifies in the Auditor's Report the appropriate auditing

standards they used, and direct them to expand the scope of the paragraph in the Auditor's Report by disclosing the key audit procedures followed. Your external auditor is also to state whether the same audit procedures were followed for all supplementary financial statements submitted.

ADB wishes that auditors conform to the international auditing standards issued by the International Federation of Accountants. In cases where other auditing standards are used, request that your external auditor to indicate in the Auditor's Report the extent of any differences and their impact on the audit.

The external auditor's opinion is also required on whether:

- the proceeds of the ADB's loan have been utilized only for the project as stated in the

Loan Agreement; - the financial information contains data specifically agreed upon between State of Madhya

Pradesh, Madhya Pradesh Poorv Kshetra Vidyut Vitaran Company Limited (DISCOM-E), Madhya Pradesh Madya Kshetra Vidyut Vitaran Company Limited (DISCOM-C), and Madhya Pradesh Paschim Kshetra Vidyut Vitaran Company Limited (DISCOM-W) and ADB to be included in the financial statements;

- the financial information complies with relevant regulations and statutory requirements; and

- compliance has been met with all the financial covenants contained in the Loan or Project Agreements.

The Auditor's Report is to clearly state the reasons for any opinions that are qualified, adverse, or

disclaimers. Actions on deficiencies disclosed by the external auditor in its report are to be resolved by State of

Madhya Pradesh, Madhya Pradesh Poorv Kshetra Vidyut Vitaran Company Limited (DISCOM-E), Madhya Pradesh Madya Kshetra Vidyut Vitaran Company Limited (DISCOM-C), and Madhya Pradesh Paschim Kshetra Vidyut Vitaran Company Limited (DISCOM-W) within a reasonable time. The external auditor is to comment in the subsequent Auditor’s Report on the adequacy of the corrective measures taken by State of Madhya Pradesh, Madhya Pradesh Poorv Kshetra Vidyut Vitaran Company Limited (DISCOM-E), Madhya Pradesh Madya Kshetra Vidyut Vitaran Company Limited (DISCOM-C), and Madhya Pradesh Paschim Kshetra Vidyut Vitaran Company Limited (DISCOM-W).

Compliance with these ADB requirements will be monitored by review missions and during normal project supervision, and followed up regularly with all concerned, including the external auditor. Yours sincerely, Thevakumar Kandiah Director, Energy Division South Asia Department

24 Appendix 7

Attachments Loan and Project Agreements Handbook on Financial Management and Analysis of Projects. cc: Ms. A. Thakur, Deputy Secretary (ADB) Department of Economic Affairs, Ministry of Finance

Mr. S. P. S. Parihar Secretary, Energy Department State of Madhya Pradesh Chairman and Managing Director Madhya Pradesh Madhya Kshetra Vidyut Company Limited ( DISCOM-C)

Chairman and Managing Director Madhya Pradesh Poorv Kshetra Vidyut Vitaran Company Limited (DISCOM-E)

Chairman and Managing Director

Madhya Pradesh Paschim Kshethra Vidyut Vitara Company Limited (DISCOM-W) Mr. Tadashi Kondo Country Director, ADB India Resident Mission

Appe

ndix 7 25

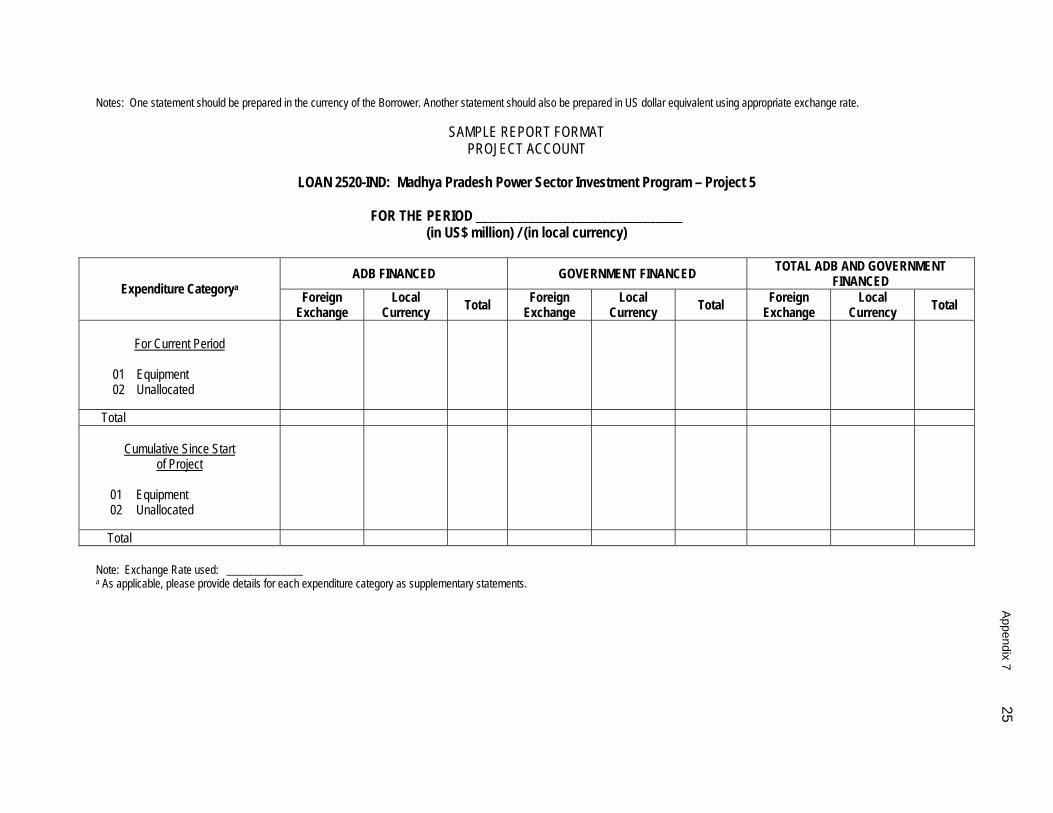

Notes: One statement should be prepared in the currency of the Borrower. Another statement should also be prepared in US dollar equivalent using appropriate exchange rate.

SAMPLE REPORT FORMAT PROJECT ACCOUNT

LOAN 2520-IND: Madhya Pradesh Power Sector Investment Program – Project 5

FOR THE PERIOD _______________________________

(in US$ million) / (in local currency)

ADB FINANCED GOVERNMENT FINANCED TOTAL ADB AND GOVERNMENT

FINANCED Expenditure Categorya

Foreign Exchange

Local Currency Total

Foreign Exchange

Local Currency Total

Foreign Exchange

Local Currency Total

For Current Period

01 Equipment 02 Unallocated

Total

Cumulative Since Start of Project

01 Equipment 02 Unallocated

Total Note: Exchange Rate used: ______________ a As applicable, please provide details for each expenditure category as supplementary statements.

26 Appendix 8

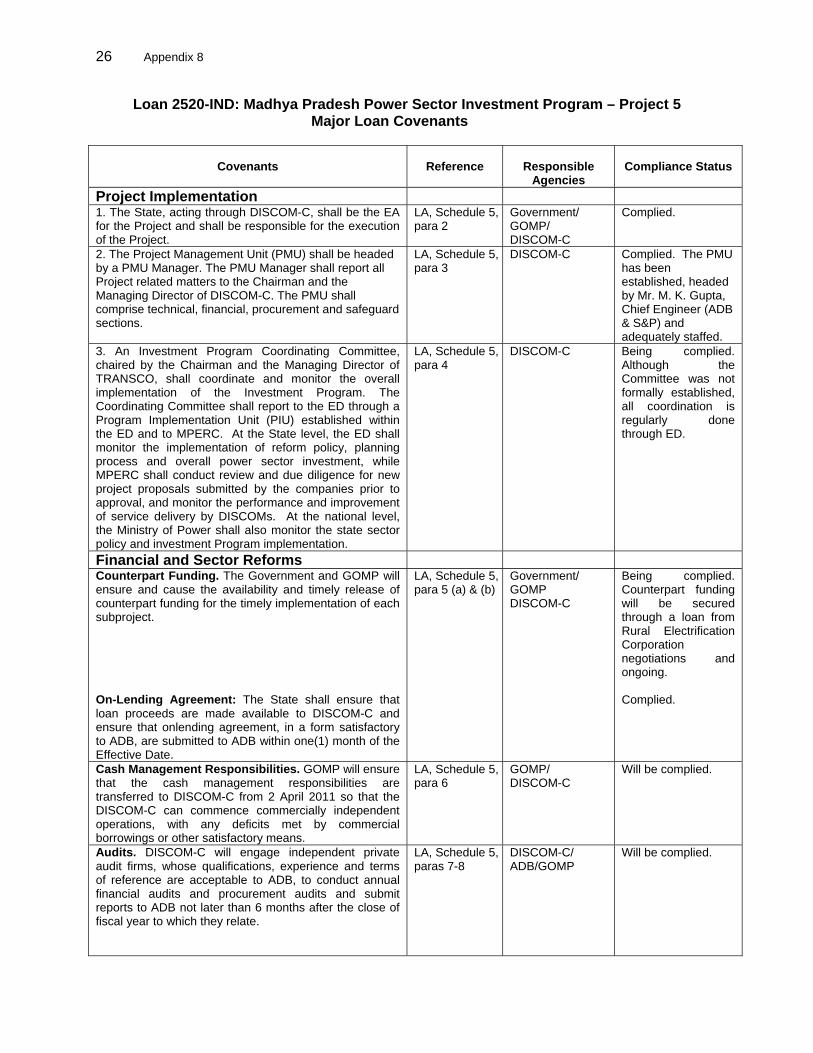

Loan 2520-IND: Madhya Pradesh Power Sector Investment Program – Project 5 Major Loan Covenants

Covenants

Reference

Responsible

Agencies

Compliance Status

Project Implementation

1. The State, acting through DISCOM-C, shall be the EA for the Project and shall be responsible for the execution of the Project.

LA, Schedule 5,para 2

Government/ GOMP/ DISCOM-C

Complied.

2. The Project Management Unit (PMU) shall be headed by a PMU Manager. The PMU Manager shall report all Project related matters to the Chairman and the Managing Director of DISCOM-C. The PMU shall comprise technical, financial, procurement and safeguard sections.

LA, Schedule 5,para 3

DISCOM-C Complied. The PMU has been established, headed by Mr. M. K. Gupta, Chief Engineer (ADB & S&P) and adequately staffed.

3. An Investment Program Coordinating Committee, chaired by the Chairman and the Managing Director of TRANSCO, shall coordinate and monitor the overall implementation of the Investment Program. The Coordinating Committee shall report to the ED through a Program Implementation Unit (PIU) established within the ED and to MPERC. At the State level, the ED shall monitor the implementation of reform policy, planning process and overall power sector investment, while MPERC shall conduct review and due diligence for new project proposals submitted by the companies prior to approval, and monitor the performance and improvement of service delivery by DISCOMs. At the national level, the Ministry of Power shall also monitor the state sector policy and investment Program implementation.

LA, Schedule 5,para 4

DISCOM-C Being complied. Although the Committee was not formally established, all coordination is regularly done through ED.

Financial and Sector Reforms

Counterpart Funding. The Government and GOMP will ensure and cause the availability and timely release of counterpart funding for the timely implementation of each subproject. On-Lending Agreement: The State shall ensure that loan proceeds are made available to DISCOM-C and ensure that onlending agreement, in a form satisfactory to ADB, are submitted to ADB within one(1) month of the Effective Date.

LA, Schedule 5,para 5 (a) & (b)

Government/ GOMP DISCOM-C

Being complied. Counterpart funding will be secured through a loan from Rural Electrification Corporation negotiations and ongoing. Complied.

Cash Management Responsibilities. GOMP will ensure that the cash management responsibilities are transferred to DISCOM-C from 2 April 2011 so that the DISCOM-C can commence commercially independent operations, with any deficits met by commercial borrowings or other satisfactory means.

LA, Schedule 5,para 6

GOMP/ DISCOM-C

Will be complied.

Audits. DISCOM-C will engage independent private audit firms, whose qualifications, experience and terms of reference are acceptable to ADB, to conduct annual financial audits and procurement audits and submit reports to ADB not later than 6 months after the close of fiscal year to which they relate.

LA, Schedule 5,paras 7-8

DISCOM-C/ ADB/GOMP

Will be complied.

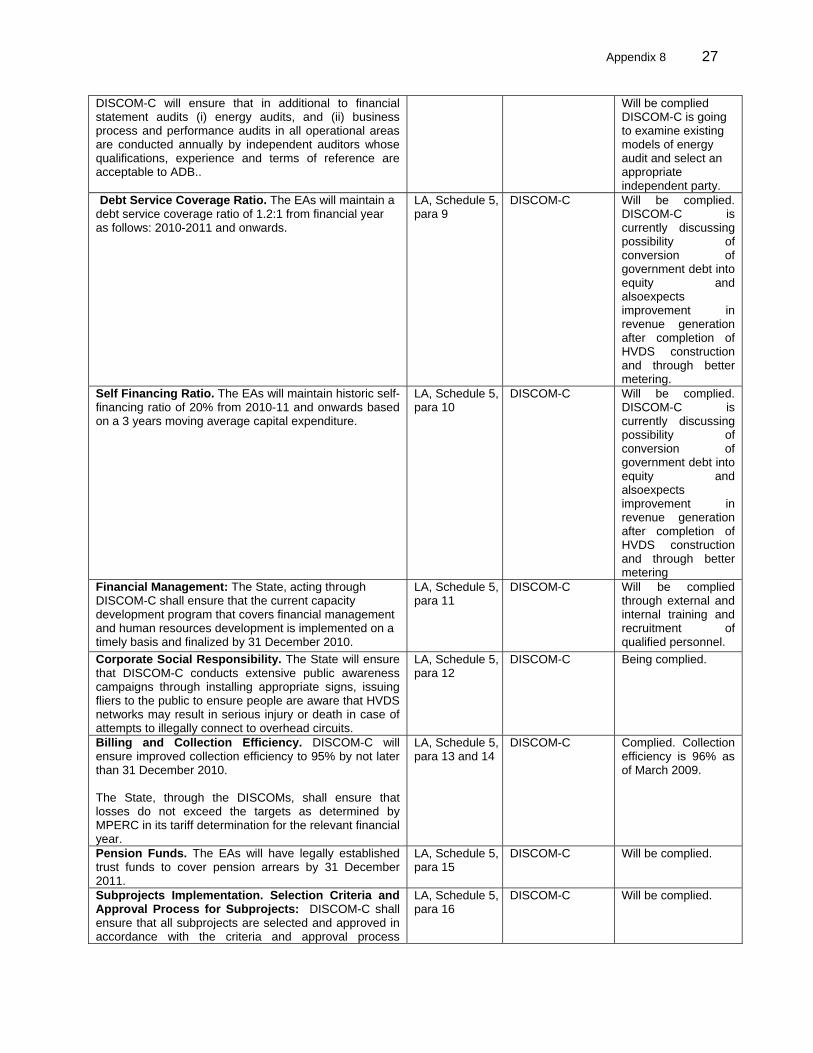

Appendix 8 27

DISCOM-C will ensure that in additional to financial statement audits (i) energy audits, and (ii) business process and performance audits in all operational areas are conducted annually by independent auditors whose qualifications, experience and terms of reference are acceptable to ADB..

Will be complied DISCOM-C is going to examine existing models of energy audit and select an appropriate independent party.

Debt Service Coverage Ratio. The EAs will maintain a debt service coverage ratio of 1.2:1 from financial year as follows: 2010-2011 and onwards.

LA, Schedule 5,para 9

DISCOM-C Will be complied. DISCOM-C is currently discussing possibility of conversion of government debt into equity and alsoexpects improvement in revenue generation after completion of HVDS construction and through better metering.

Self Financing Ratio. The EAs will maintain historic self-financing ratio of 20% from 2010-11 and onwards based on a 3 years moving average capital expenditure.

LA, Schedule 5,para 10

DISCOM-C Will be complied. DISCOM-C is currently discussing possibility of conversion of government debt into equity and alsoexpects improvement in revenue generation after completion of HVDS construction and through better metering

Financial Management: The State, acting through DISCOM-C shall ensure that the current capacity development program that covers financial management and human resources development is implemented on a timely basis and finalized by 31 December 2010.

LA, Schedule 5,para 11

DISCOM-C Will be complied through external and internal training and recruitment of qualified personnel.

Corporate Social Responsibility. The State will ensure that DISCOM-C conducts extensive public awareness campaigns through installing appropriate signs, issuing fliers to the public to ensure people are aware that HVDS networks may result in serious injury or death in case of attempts to illegally connect to overhead circuits.

LA, Schedule 5,para 12

DISCOM-C Being complied.

Billing and Collection Efficiency. DISCOM-C will ensure improved collection efficiency to 95% by not later than 31 December 2010. The State, through the DISCOMs, shall ensure that losses do not exceed the targets as determined by MPERC in its tariff determination for the relevant financial year.

LA, Schedule 5,para 13 and 14

DISCOM-C Complied. Collection efficiency is 96% as of March 2009.

Pension Funds. The EAs will have legally established trust funds to cover pension arrears by 31 December 2011.

LA, Schedule 5,para 15

DISCOM-C Will be complied.

Subprojects Implementation. Selection Criteria and Approval Process for Subprojects: DISCOM-C shall ensure that all subprojects are selected and approved in accordance with the criteria and approval process

LA, Schedule 5,para 16

DISCOM-C Will be complied.

28 Appendix 8

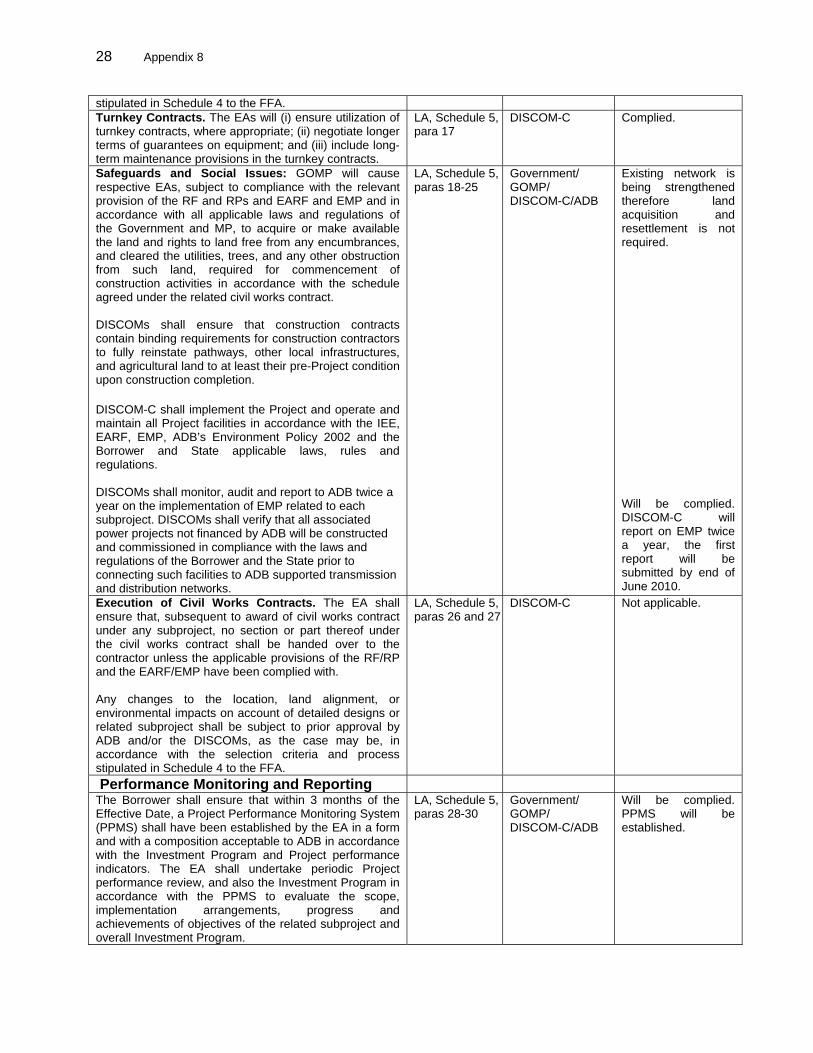

stipulated in Schedule 4 to the FFA. Turnkey Contracts. The EAs will (i) ensure utilization of turnkey contracts, where appropriate; (ii) negotiate longer terms of guarantees on equipment; and (iii) include long-term maintenance provisions in the turnkey contracts.

LA, Schedule 5,para 17

DISCOM-C Complied.

Safeguards and Social Issues: GOMP will cause respective EAs, subject to compliance with the relevant provision of the RF and RPs and EARF and EMP and in accordance with all applicable laws and regulations of the Government and MP, to acquire or make available the land and rights to land free from any encumbrances, and cleared the utilities, trees, and any other obstruction from such land, required for commencement of construction activities in accordance with the schedule agreed under the related civil works contract. DISCOMs shall ensure that construction contracts contain binding requirements for construction contractors to fully reinstate pathways, other local infrastructures, and agricultural land to at least their pre-Project condition upon construction completion. DISCOM-C shall implement the Project and operate and maintain all Project facilities in accordance with the IEE, EARF, EMP, ADB’s Environment Policy 2002 and the Borrower and State applicable laws, rules and regulations. DISCOMs shall monitor, audit and report to ADB twice a year on the implementation of EMP related to each subproject. DISCOMs shall verify that all associated power projects not financed by ADB will be constructed and commissioned in compliance with the laws and regulations of the Borrower and the State prior to connecting such facilities to ADB supported transmission and distribution networks.

LA, Schedule 5,paras 18-25

Government/ GOMP/ DISCOM-C/ADB

Existing network is being strengthened therefore land acquisition and resettlement is not required. Will be complied. DISCOM-C will report on EMP twice a year, the first report will be submitted by end of June 2010.

Execution of Civil Works Contracts. The EA shall ensure that, subsequent to award of civil works contract under any subproject, no section or part thereof under the civil works contract shall be handed over to the contractor unless the applicable provisions of the RF/RP and the EARF/EMP have been complied with. Any changes to the location, land alignment, or environmental impacts on account of detailed designs or related subproject shall be subject to prior approval by ADB and/or the DISCOMs, as the case may be, in accordance with the selection criteria and process stipulated in Schedule 4 to the FFA.

LA, Schedule 5,paras 26 and 27

DISCOM-C Not applicable.

Performance Monitoring and Reporting

The Borrower shall ensure that within 3 months of the Effective Date, a Project Performance Monitoring System (PPMS) shall have been established by the EA in a form and with a composition acceptable to ADB in accordance with the Investment Program and Project performance indicators. The EA shall undertake periodic Project performance review, and also the Investment Program in accordance with the PPMS to evaluate the scope, implementation arrangements, progress and achievements of objectives of the related subproject and overall Investment Program.

LA, Schedule 5,paras 28-30

Government/ GOMP/ DISCOM-C/ADB

Will be complied. PPMS will be established.

Appendix 8 29

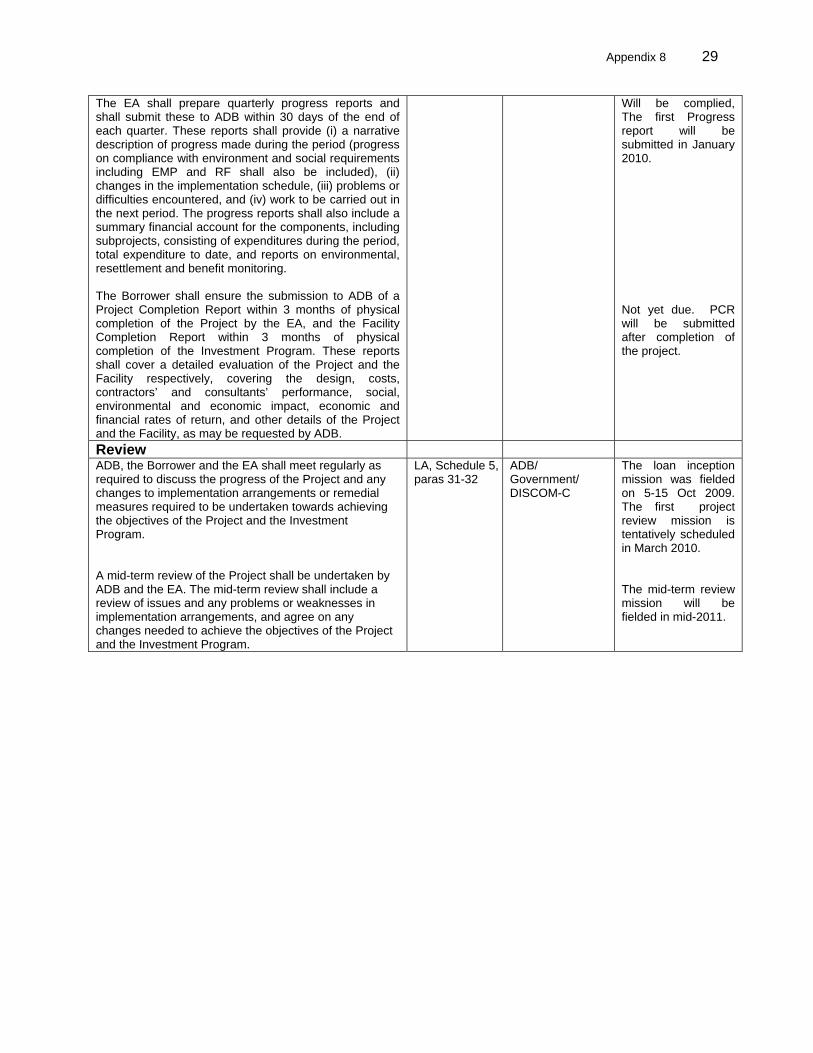

The EA shall prepare quarterly progress reports and shall submit these to ADB within 30 days of the end of each quarter. These reports shall provide (i) a narrative description of progress made during the period (progress on compliance with environment and social requirements including EMP and RF shall also be included), (ii) changes in the implementation schedule, (iii) problems or difficulties encountered, and (iv) work to be carried out in the next period. The progress reports shall also include a summary financial account for the components, including subprojects, consisting of expenditures during the period, total expenditure to date, and reports on environmental, resettlement and benefit monitoring. The Borrower shall ensure the submission to ADB of a Project Completion Report within 3 months of physical completion of the Project by the EA, and the Facility Completion Report within 3 months of physical completion of the Investment Program. These reports shall cover a detailed evaluation of the Project and the Facility respectively, covering the design, costs, contractors’ and consultants’ performance, social, environmental and economic impact, economic and financial rates of return, and other details of the Project and the Facility, as may be requested by ADB.

Will be complied, The first Progress report will be submitted in January 2010. Not yet due. PCR will be submitted after completion of the project.

Review

ADB, the Borrower and the EA shall meet regularly as required to discuss the progress of the Project and any changes to implementation arrangements or remedial measures required to be undertaken towards achieving the objectives of the Project and the Investment Program. A mid-term review of the Project shall be undertaken by ADB and the EA. The mid-term review shall include a review of issues and any problems or weaknesses in implementation arrangements, and agree on any changes needed to achieve the objectives of the Project and the Investment Program.

LA, Schedule 5,paras 31-32

ADB/ Government/ DISCOM-C

The loan inception mission was fielded on 5-15 Oct 2009. The first project review mission is tentatively scheduled in March 2010. The mid-term review mission will be fielded in mid-2011.