Embed Size (px)

Citation preview

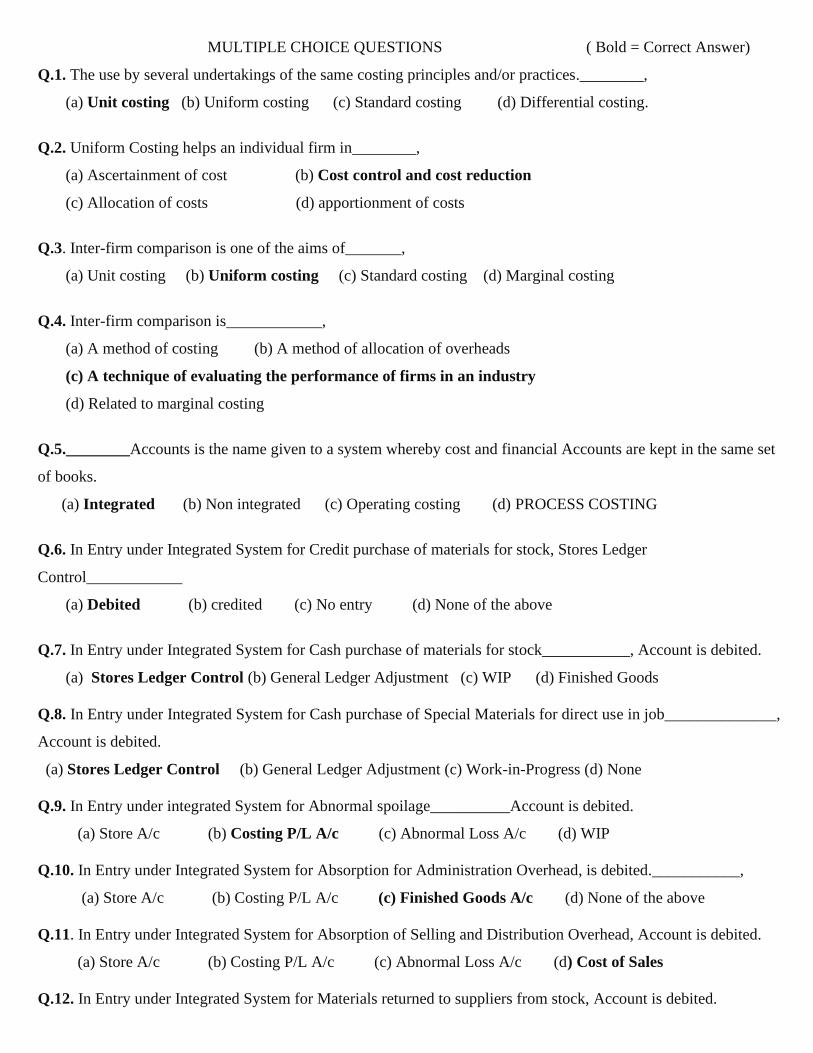

MULTIPLE CHOICE QUESTIONS ( Bold = Correct Answer)

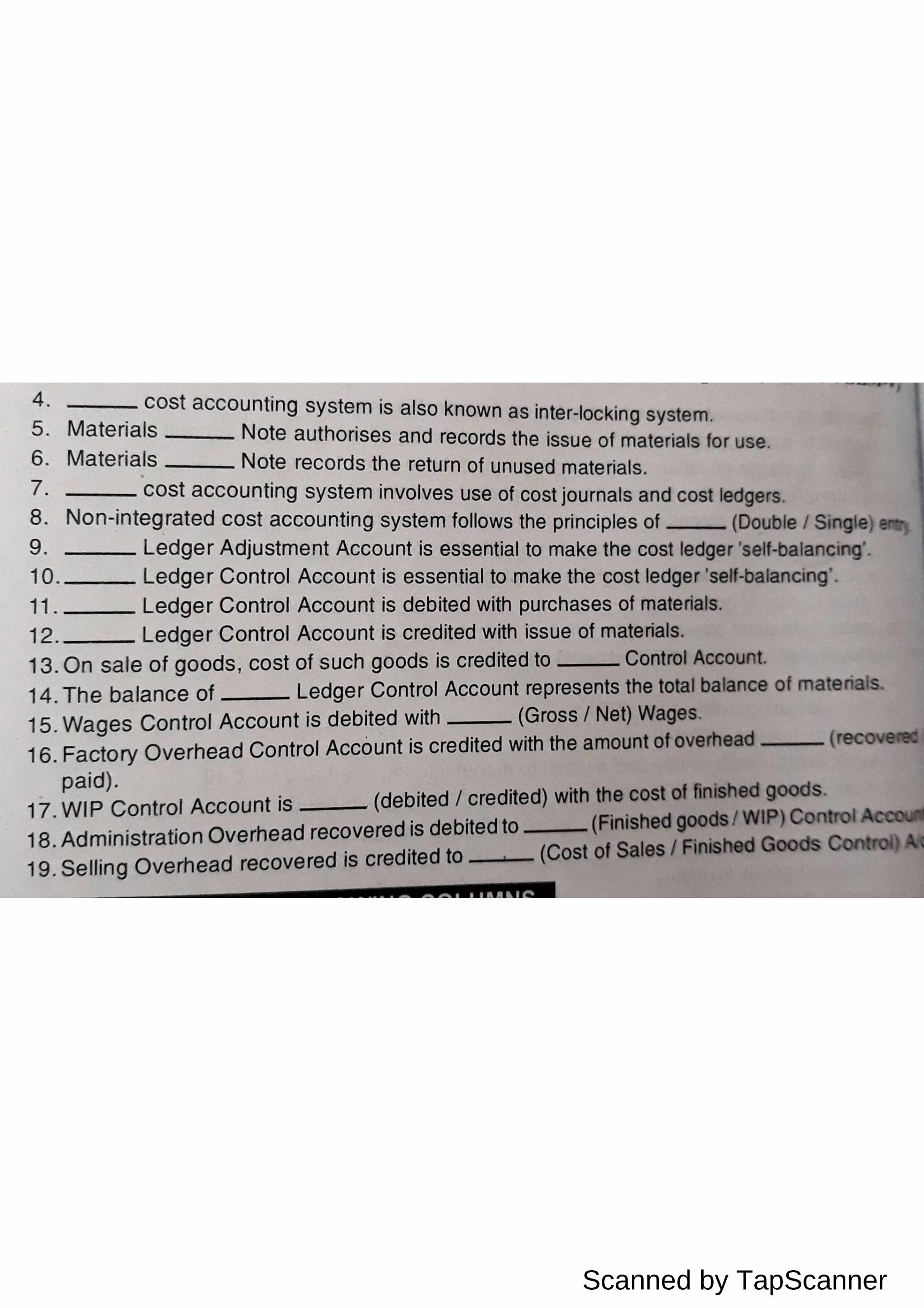

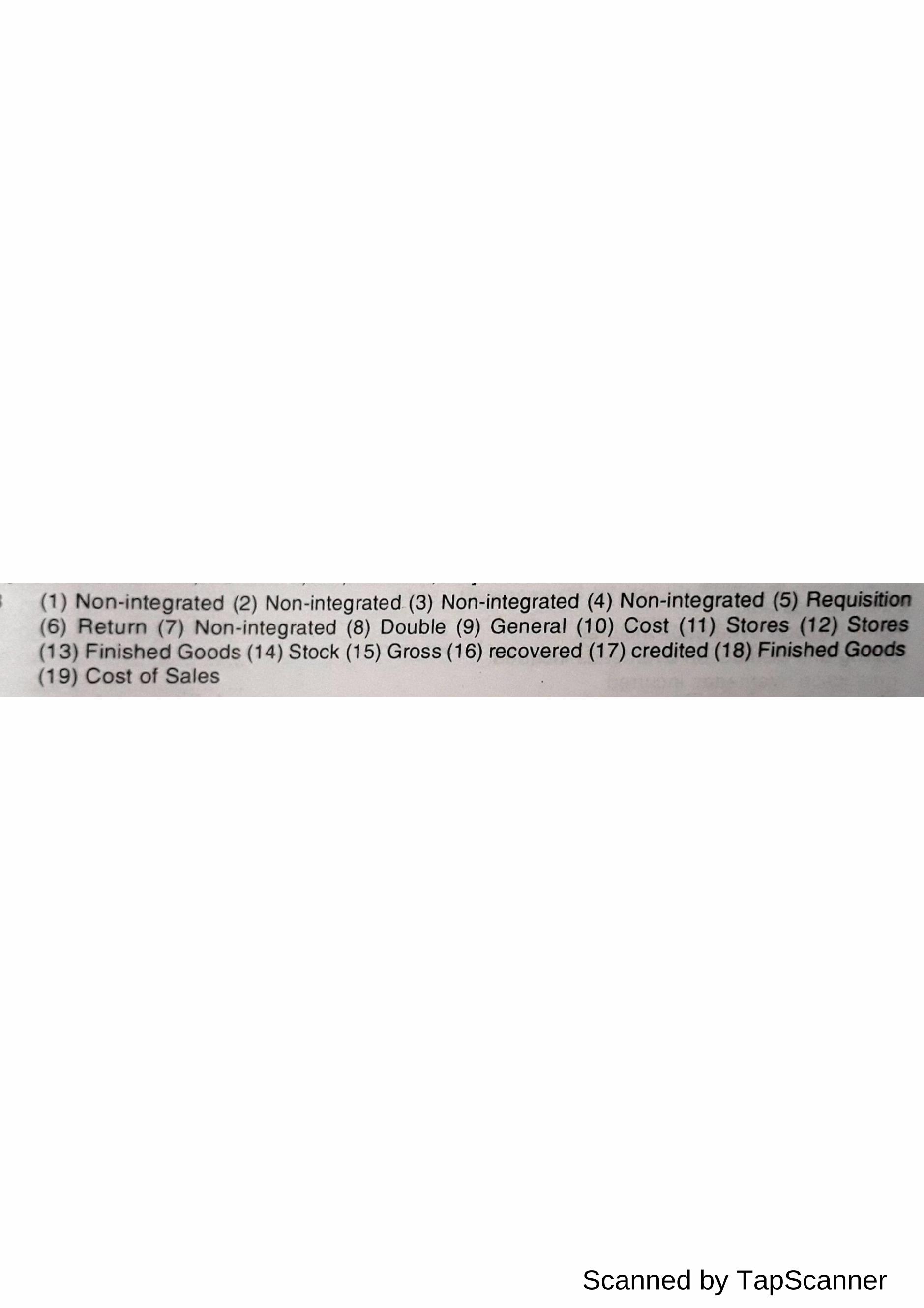

Q.1. The use by several undertakings of the same costing principles and/or practices.________,

(a) Unit costing (b) Uniform costing (c) Standard costing (d) Differential costing.

Q.2. Uniform Costing helps an individual firm in________,

(a) Ascertainment of cost (b) Cost control and cost reduction

(c) Allocation of costs (d) apportionment of costs

Q.3. Inter-firm comparison is one of the aims of_______,

(a) Unit costing (b) Uniform costing (c) Standard costing (d) Marginal costing

Q.4. Inter-firm comparison is____________,

(a) A method of costing (b) A method of allocation of overheads

(c) A technique of evaluating the performance of firms in an industry

(d) Related to marginal costing

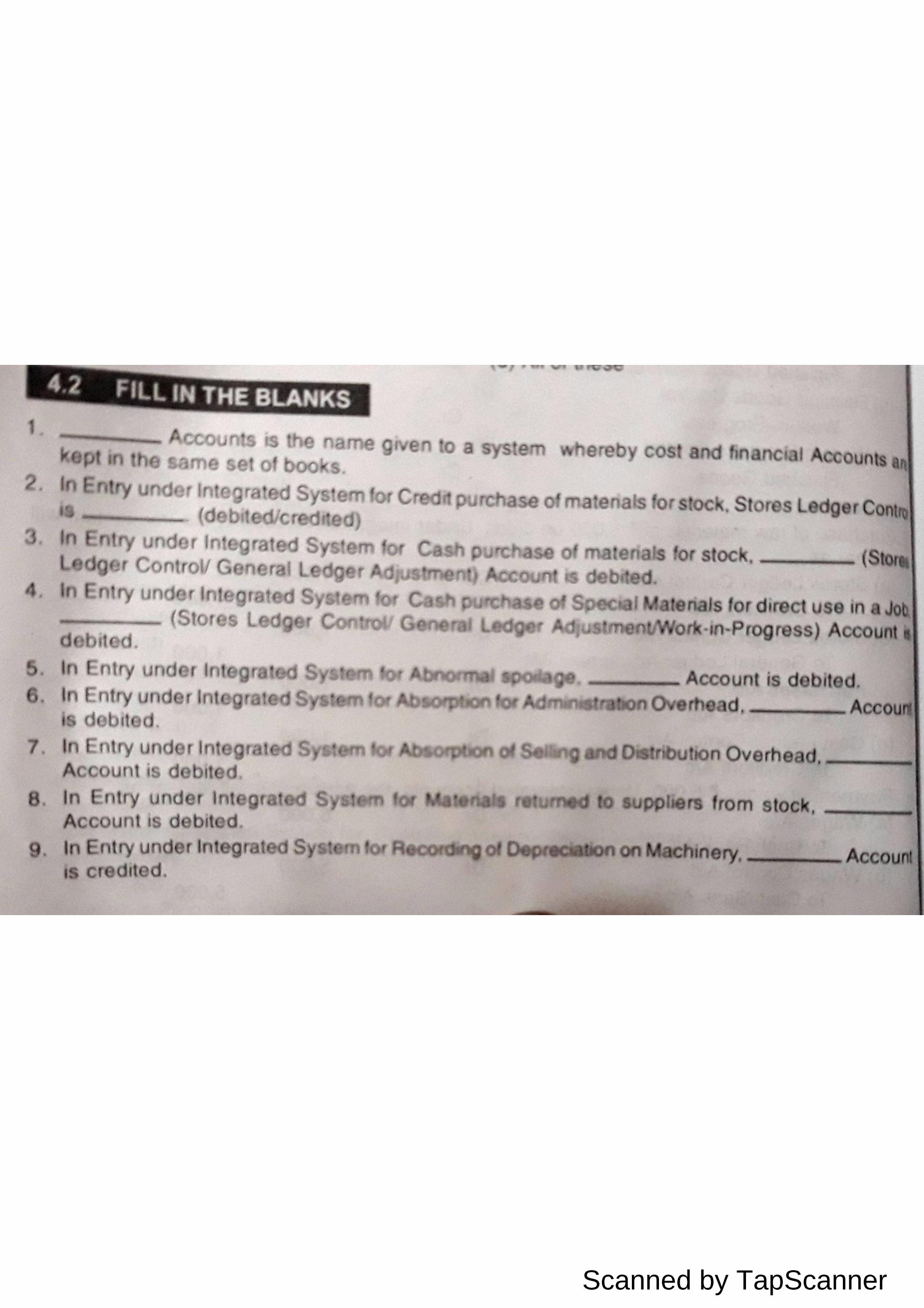

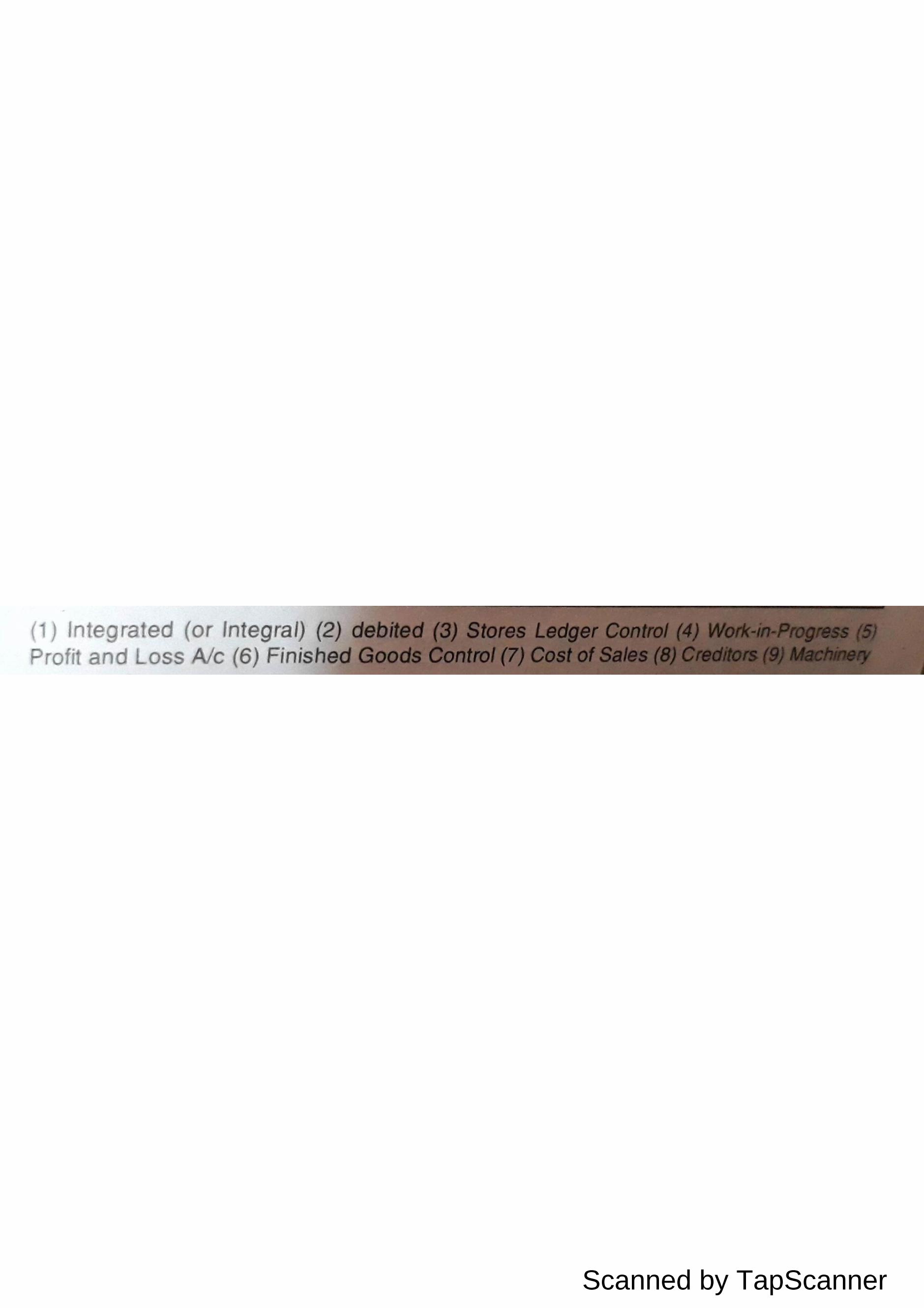

Q.5.________Accounts is the name given to a system whereby cost and financial Accounts are kept in the same set

of books.

(a) Integrated (b) Non integrated (c) Operating costing (d) PROCESS COSTING

Q.6. In Entry under Integrated System for Credit purchase of materials for stock, Stores Ledger

Control____________

(a) Debited (b) credited (c) No entry (d) None of the above

Q.7. In Entry under Integrated System for Cash purchase of materials for stock___________, Account is debited.

(a) Stores Ledger Control (b) General Ledger Adjustment (c) WIP (d) Finished Goods

Q.8. In Entry under Integrated System for Cash purchase of Special Materials for direct use in job______________,

Account is debited.

(a) Stores Ledger Control (b) General Ledger Adjustment (c) Work-in-Progress (d) None

Q.9. In Entry under integrated System for Abnormal spoilage__________Account is debited.

(a) Store A/c (b) Costing P/L A/c (c) Abnormal Loss A/c (d) WIP

Q.10. In Entry under Integrated System for Absorption for Administration Overhead, is debited.___________,

(a) Store A/c (b) Costing P/L A/c (c) Finished Goods A/c (d) None of the above

Q.11. In Entry under Integrated System for Absorption of Selling and Distribution Overhead, Account is debited.

(a) Store A/c (b) Costing P/L A/c (c) Abnormal Loss A/c (d) Cost of Sales

Q.12. In Entry under Integrated System for Materials returned to suppliers from stock, Account is debited.

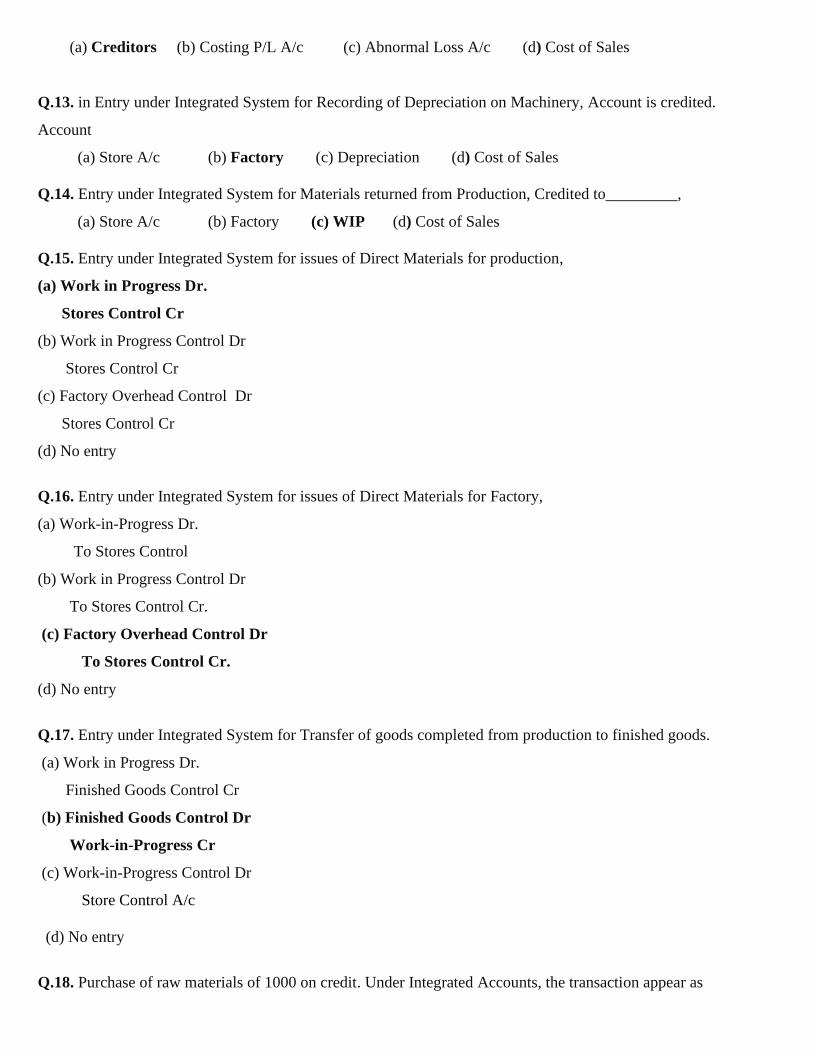

(a) Creditors (b) Costing P/L A/c (c) Abnormal Loss A/c (d) Cost of Sales

Q.13. in Entry under Integrated System for Recording of Depreciation on Machinery, Account is credited.

Account

(a) Store A/c (b) Factory (c) Depreciation (d) Cost of Sales

Q.14. Entry under Integrated System for Materials returned from Production, Credited to_________,

(a) Store A/c (b) Factory (c) WIP (d) Cost of Sales

Q.15. Entry under Integrated System for issues of Direct Materials for production,

(a) Work in Progress Dr.

Stores Control Cr

(b) Work in Progress Control Dr

Stores Control Cr

(c) Factory Overhead Control Dr

Stores Control Cr

(d) No entry

Q.16. Entry under Integrated System for issues of Direct Materials for Factory,

(a) Work-in-Progress Dr.

To Stores Control

(b) Work in Progress Control Dr

To Stores Control Cr.

(c) Factory Overhead Control Dr

To Stores Control Cr.

(d) No entry

Q.17. Entry under Integrated System for Transfer of goods completed from production to finished goods.

(a) Work in Progress Dr.

Finished Goods Control Cr

(b) Finished Goods Control Dr

Work-in-Progress Cr

(c) Work-in-Progress Control Dr

Store Control A/c

(d) No entry

Q.18. Purchase of raw materials of 1000 on credit. Under Integrated Accounts, the transaction appear as

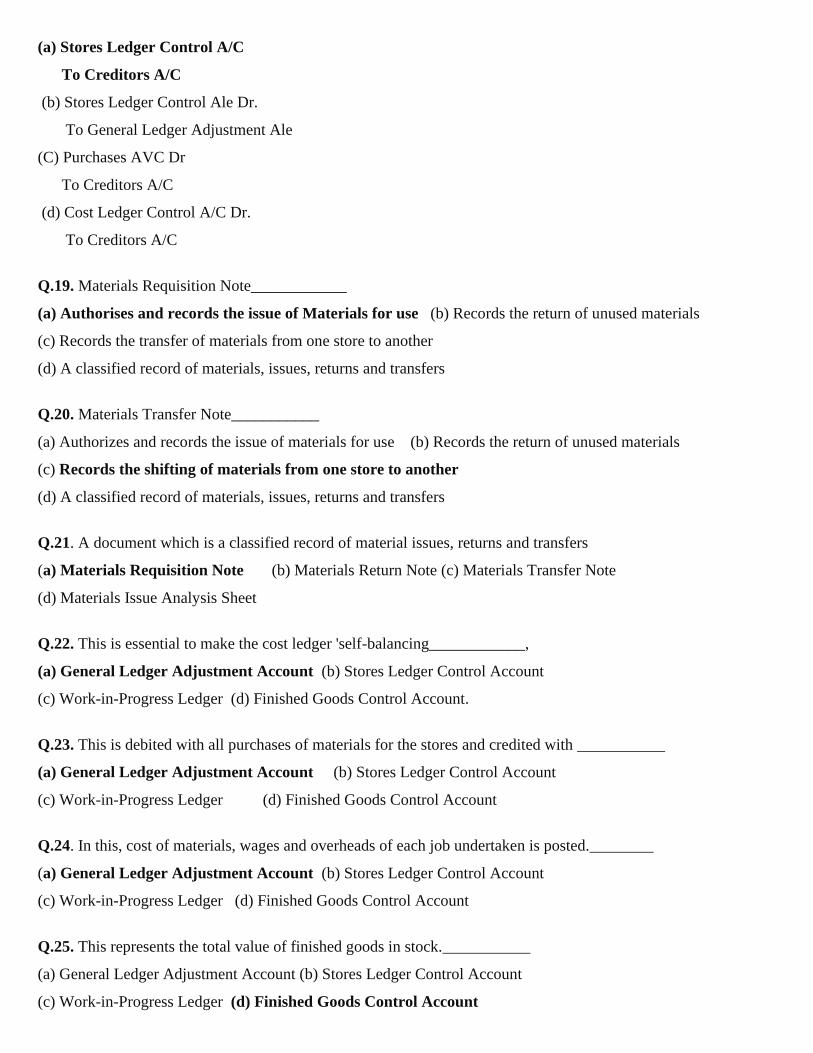

(a) Stores Ledger Control A/C

To Creditors A/C

(b) Stores Ledger Control Ale Dr.

To General Ledger Adjustment Ale

(C) Purchases AVC Dr

To Creditors A/C

(d) Cost Ledger Control A/C Dr.

To Creditors A/C

Q.19. Materials Requisition Note____________

(a) Authorises and records the issue of Materials for use (b) Records the return of unused materials

(c) Records the transfer of materials from one store to another

(d) A classified record of materials, issues, returns and transfers

Q.20. Materials Transfer Note___________

(a) Authorizes and records the issue of materials for use (b) Records the return of unused materials

(c) Records the shifting of materials from one store to another

(d) A classified record of materials, issues, returns and transfers

Q.21. A document which is a classified record of material issues, returns and transfers

(a) Materials Requisition Note (b) Materials Return Note (c) Materials Transfer Note

(d) Materials Issue Analysis Sheet

Q.22. This is essential to make the cost ledger 'self-balancing____________,

(a) General Ledger Adjustment Account (b) Stores Ledger Control Account

(c) Work-in-Progress Ledger (d) Finished Goods Control Account.

Q.23. This is debited with all purchases of materials for the stores and credited with ___________

(a) General Ledger Adjustment Account (b) Stores Ledger Control Account

(c) Work-in-Progress Ledger (d) Finished Goods Control Account

Q.24. In this, cost of materials, wages and overheads of each job undertaken is posted.________

(a) General Ledger Adjustment Account (b) Stores Ledger Control Account

(c) Work-in-Progress Ledger (d) Finished Goods Control Account

Q.25. This represents the total value of finished goods in stock.___________

(a) General Ledger Adjustment Account (b) Stores Ledger Control Account

(c) Work-in-Progress Ledger (d) Finished Goods Control Account

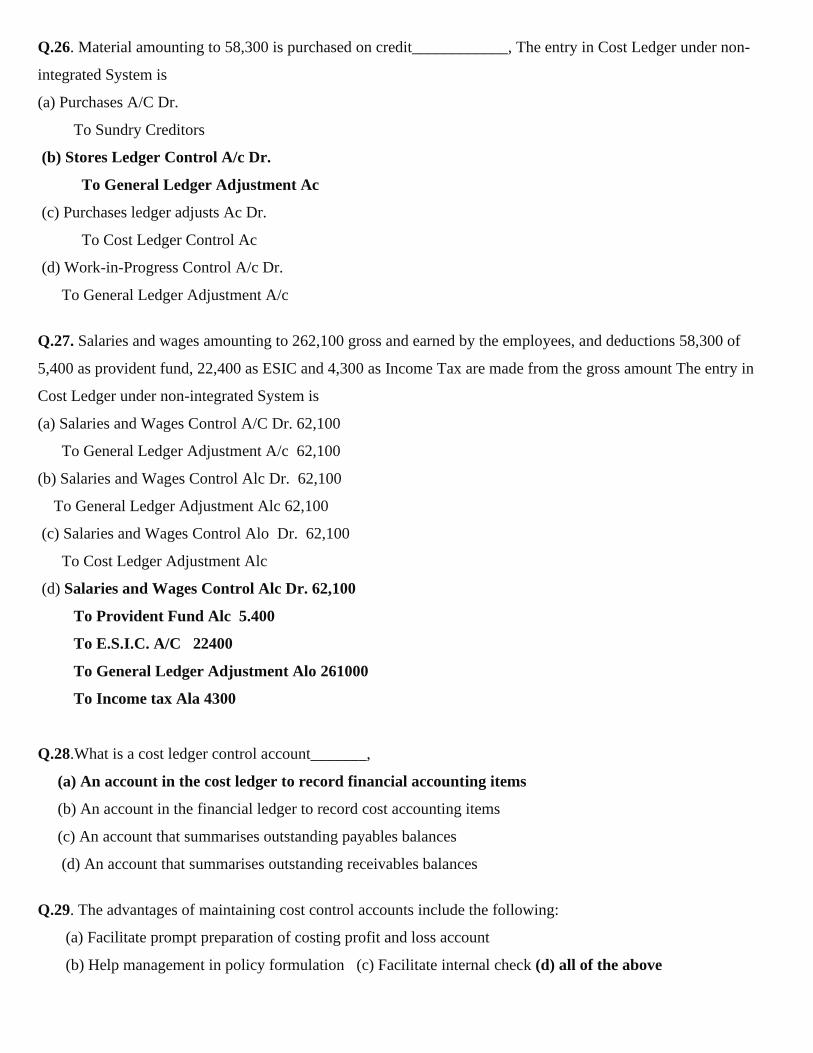

Q.26. Material amounting to 58,300 is purchased on credit____________, The entry in Cost Ledger under non-

integrated System is

(a) Purchases A/C Dr.

To Sundry Creditors

(b) Stores Ledger Control A/c Dr.

To General Ledger Adjustment Ac

(c) Purchases ledger adjusts Ac Dr.

To Cost Ledger Control Ac

(d) Work-in-Progress Control A/c Dr.

To General Ledger Adjustment A/c

Q.27. Salaries and wages amounting to 262,100 gross and earned by the employees, and deductions 58,300 of

5,400 as provident fund, 22,400 as ESIC and 4,300 as Income Tax are made from the gross amount The entry in

Cost Ledger under non-integrated System is

(a) Salaries and Wages Control A/C Dr. 62,100

To General Ledger Adjustment A/c 62,100

(b) Salaries and Wages Control Alc Dr. 62,100

To General Ledger Adjustment Alc 62,100

(c) Salaries and Wages Control Alo Dr. 62,100

To Cost Ledger Adjustment Alc

(d) Salaries and Wages Control Alc Dr. 62,100

To Provident Fund Alc 5.400

To E.S.I.C. A/C 22400

To General Ledger Adjustment Alo 261000

To Income tax Ala 4300

Q.28.What is a cost ledger control account_______,

(a) An account in the cost ledger to record financial accounting items

(b) An account in the financial ledger to record cost accounting items

(c) An account that summarises outstanding payables balances

(d) An account that summarises outstanding receivables balances

Q.29. The advantages of maintaining cost control accounts include the following:

(a) Facilitate prompt preparation of costing profit and loss account

(b) Help management in policy formulation (c) Facilitate internal check (d) all of the above

Q.30. The Work-in-Progress Control Account is not debited with:

(a) Direct materials and direct labour (b) Direct expenses

c) Production overheads (recovered) (d) Selling and distribution overhead

Q.31. The application of factory overheads usually would be recorded as an increase

(a) Cost of goods sold (b) Work-in-progress control (d) Finished goods control

(C) Factory overheads control

Q.32. The debit balance of the overheads adjustment account may be transferred to

(a) Cost of sales account (b) Profit and loss account (c) Finished goods account (d) WIP Account

Q.33. Materials lost in stores due to fire is__________,

(a) A part of normal loss and hence part of cost (b) Capitalized

(c) A part of abnormal loss and hence excluded from cost (d) Transferred to the next period

Q.34. A credit to Work in Process Inventory represents________

(a) Work still in process (b) Raw material put into production

(c) The application of overhead to production

(d) The transfer of completed items to Finished Goods Inventory

Q.35. A journal entry includes a debit to Work in Process Inventory and a credit to Raw Material Inventory

The explanation for this would be that

(a) Indirect material was placed into production (b) raw material was purchased on account

(c) Direct material was placed into production (d) direct labour was used for production

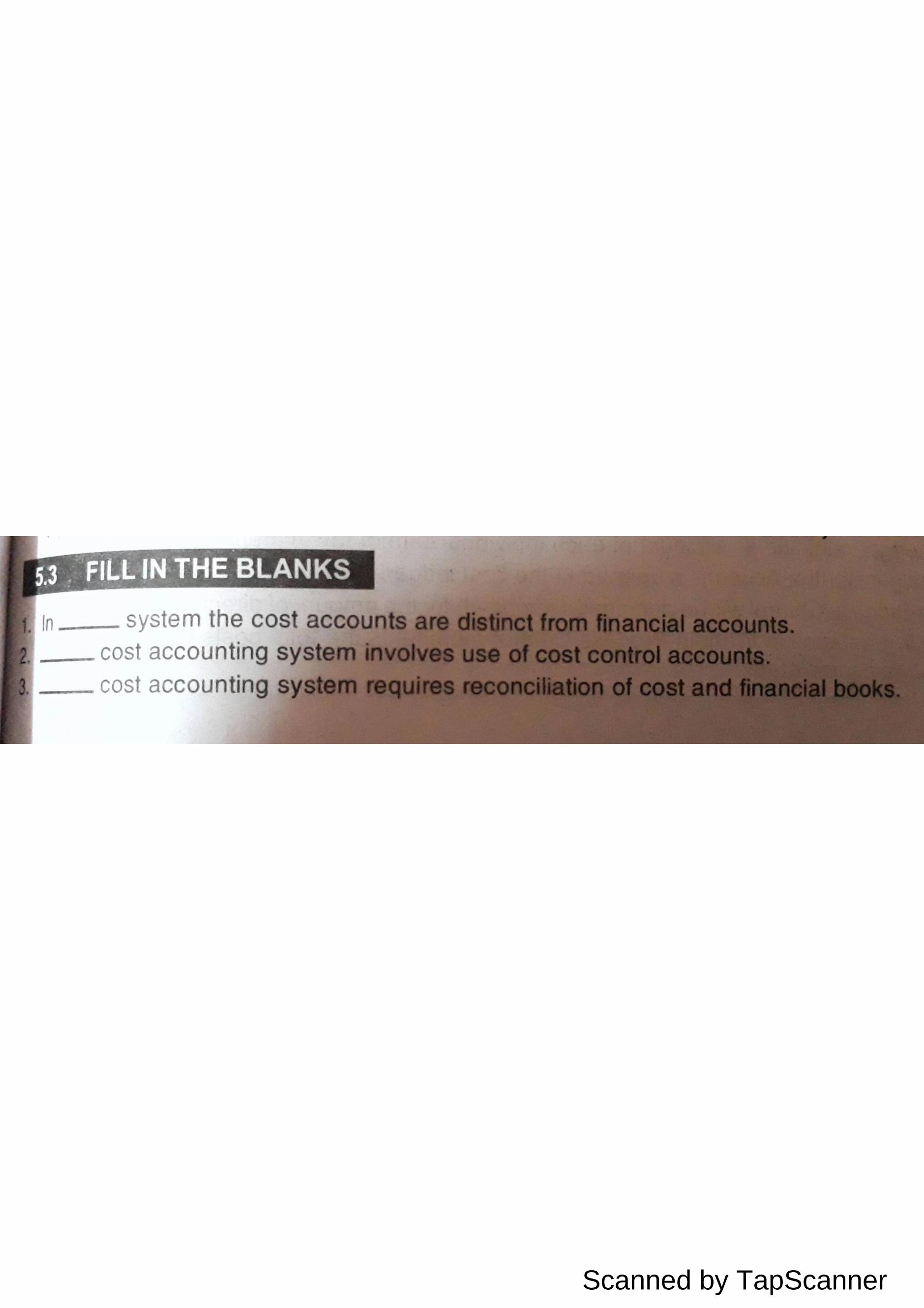

Q.36. Non-integrated cost accounting system follows the principles of-_________

(a) Double (b) Single (c) Mixed (d) none

Q.37. __________ Ledger Control Account is debited with purchases of materials,

(a) Store (b) CLC (c) WIP (d) Finished goods

Q.38.______Ledger Control Account is credited with issue of materials.

(a) Store (b) CLC (c) WIP (d) Finished goods

Q.39.On sale of goods, cost of such goods is credited to______________,

(a) Store (b) CLC (c) WIP (d) Sales A/c

Q.40. The balance of Costing Profit and loss Account. Transfer to____________,

(a) Store (b) CLC (c) WIP (d) Sale A/c

Q.41. Wages Control Account is debited with________

(a)Factory Cr (b) CLC Cr (c) WIP Cr (d) None

Q.42. Administration overhead recovered is debited to___________, Control Account

(a) Finished goods (b)WIP (c) Profit and loss (d) none of the above

Q.43.Selling overhead recovered is credited to__________ Ac

(a) Cost of Sales (b) Finished Goods Control (c) CLC (d) Profit and loss

Q.44.Paseenger transport___________

(a) Per Passenger Seat (b) Per Passenger Day (c) Per Ton day (d) Per Passenger hour

Q.45.Goods transport________,

(a) Per Ton Day (b) Per Ton Kms (c) Per Passenger hour (d) none

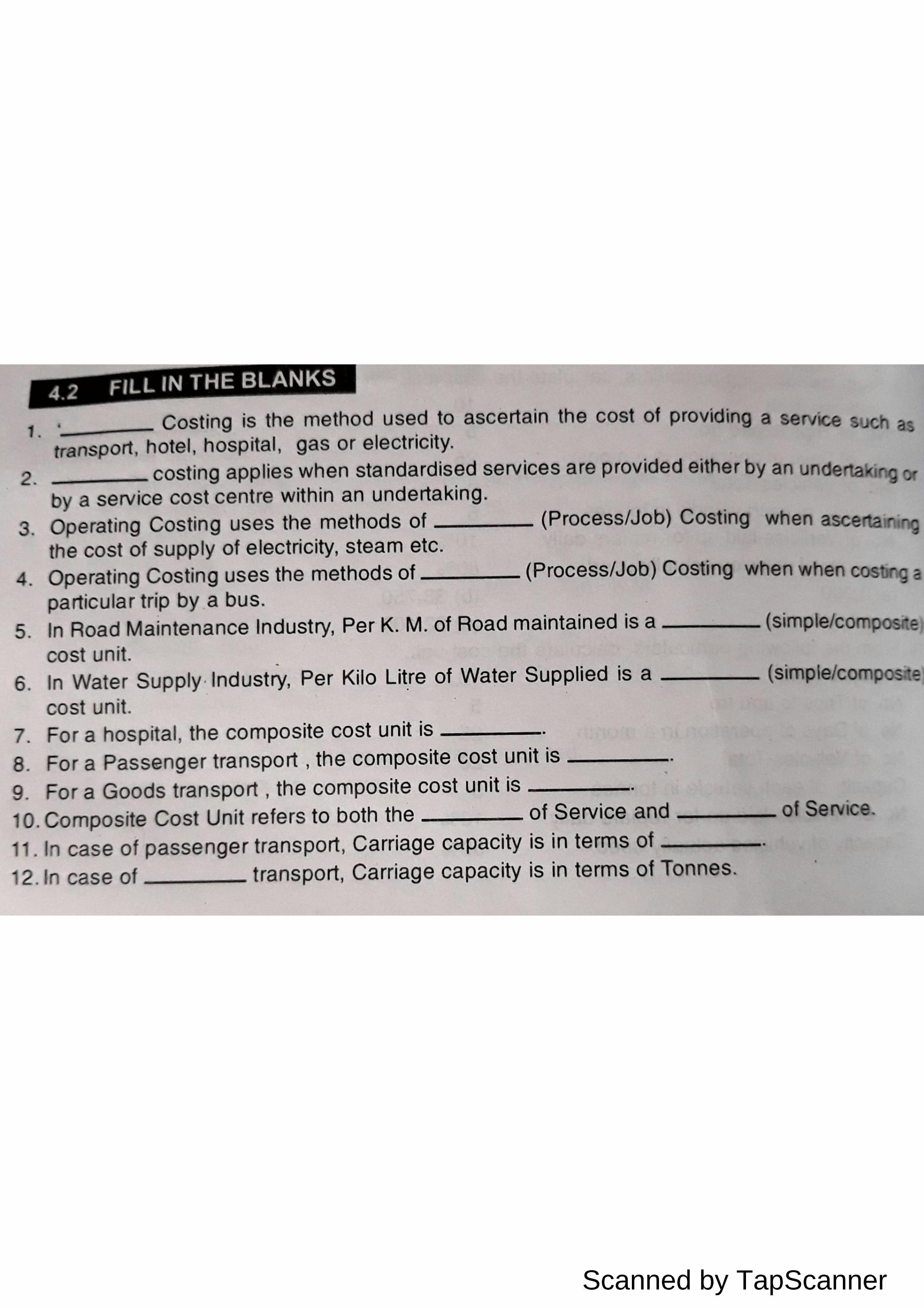

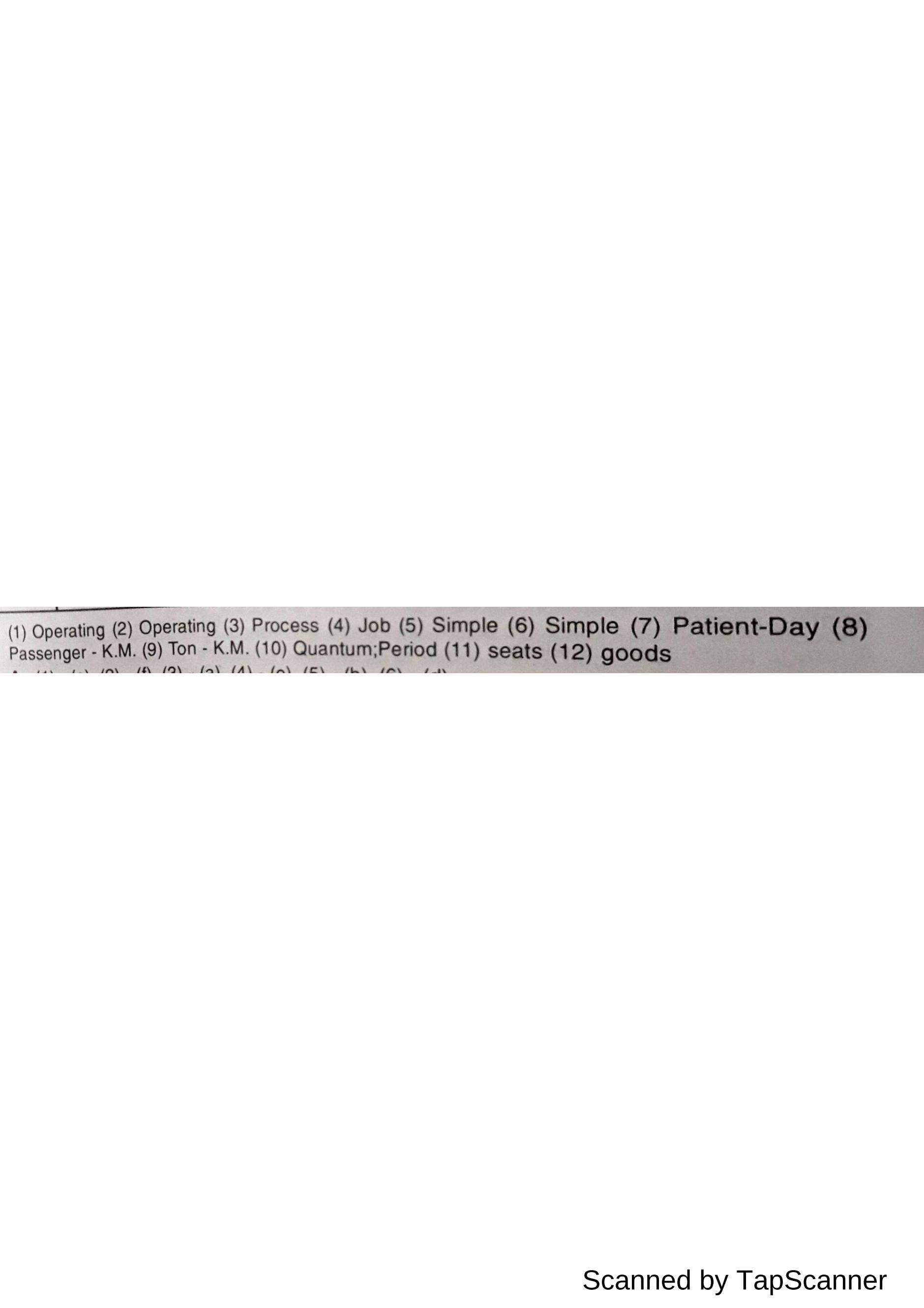

Q.46.______Costing is the method used to ascertain the cost of providing a service such as transport, hotel,

hospital, gas or electricity.

(a) Operation (b) Operating (c) Process (d) Job

Q.47. Operating Costing uses the methods of_________ Costing when ascertaining the cost of supply of electricity,

steam etc.

(a) Operation ( b) Marginal (c) Process (d) Job

Q.48. Operating Costing uses the methods of_________ costing when costing a particular trip by a bus.

(a) Operation (b) Standard Costing (c) Process (d) Job

Q.49. In Road Maintenance Industry, Per K. M. of Road maintained is a___________,

(a) Simple (b) Composite (c) Average (d) None

Q.50. In Water Supply Industry, Per Kilo Litre of Water Supplied is a ___________,

(a) Simple (b) Composite (c) Average (d) None

Q.51. For a hospital, the composite cost unit is____,

(a) Patient –day (b) Visitor – day (c) Bed –day (d) none

Q.52. For a Passenger transport, the composite cost unit is__________,

(a) Patient –day (b) Visitor – day (c) Bed –day (d) Passenger -kms

Q.53. In case of passenger transport, Carriage capacity is in terms of__________,

(a) Seat (b) Visitor (c) Bed (d) kms

Q.54. In case of______transport, Carriage capacity is in terms of Tonnes.

(a) Seat (b) Goods (c) Bed (d) km

Q.55.Normal Loss is equal to

(a) Normal Output - Actual Output (b) Actual Output - Normal Output

(c) Input x % of Normal Loss (d) None of the above

Q.56. Normal Output is equal to

(a) Input - Abnormal Loss (b) Input - Normal Loss (c) Input - Abnormal Gains (d) output - loss

Q.57. Unit Cost is equal to__________,

(a) Normal Cost - Normal Output (b) Total Cost / Normal Output (c) Normal Cost Total Output

(d) Total Cost Total Output

Q.58. Abnormal Loss is equal to_________,

(a) Input - Actual Output (b) Actual Output - Normal Output (c) Normal Output - Actual Output

(d) Actual Output – Input

Q.59. Abnormal Gains are equal to________,

(a) Actual Output - Normal Output (b) Normal Output - Actual Output

(c) Actual Output – Input (d) Input - Actual Output

Q.60. Which of the following does not use process costing?

(a) Oil refining (b) Distilleries (c) Sugar (d) Aircraft manufacturing

Q.61. Process Cost is based on the concept of_____________,

(a) Average Cost (b) Marginal Cost (c) Standard Cost (d) Differential Cost

Q.62. Process costing is applied when____________,

(a) Small number of different products are manufactured

(b) Large number of different products are manufactured

(c) Large number of identical products are manufactured

(d) Fixed costs exceed variable costs

Q.63. The following statements relate to process costing__________,

(1) The higher the net realisable value of normal losses the lower will be the cost per unit of normal output.

(2) The higher the abnormal losses the higher will be the cost per unit of normal output.

Are the statements true or false?

Statement 1

Statement 2

(a) False, False

(b) False , True

(c) True, False

(d) True , True

Q.64. Consider the following statements relating to process costing:

Statement 1: normal losses are credited to the process account at the cost per unit incurred on normal production.

Statement 2: abnormal gains are debited to the process account at the cost per unit incurred on normal production,

Which statement(s) is/are true?

(a) Both statements are true

(b) Neither statement is true

(c) Statement 1 only is true

(d) Statement 2 only is true

Q.65. When FIFO method is used in process costing, the opening stock costs are:

(a) kept separate from the costs of the new period

(b) added to new costs

(c) subtracted from the new costs

(d) averaged with other costs to arrive at total costs

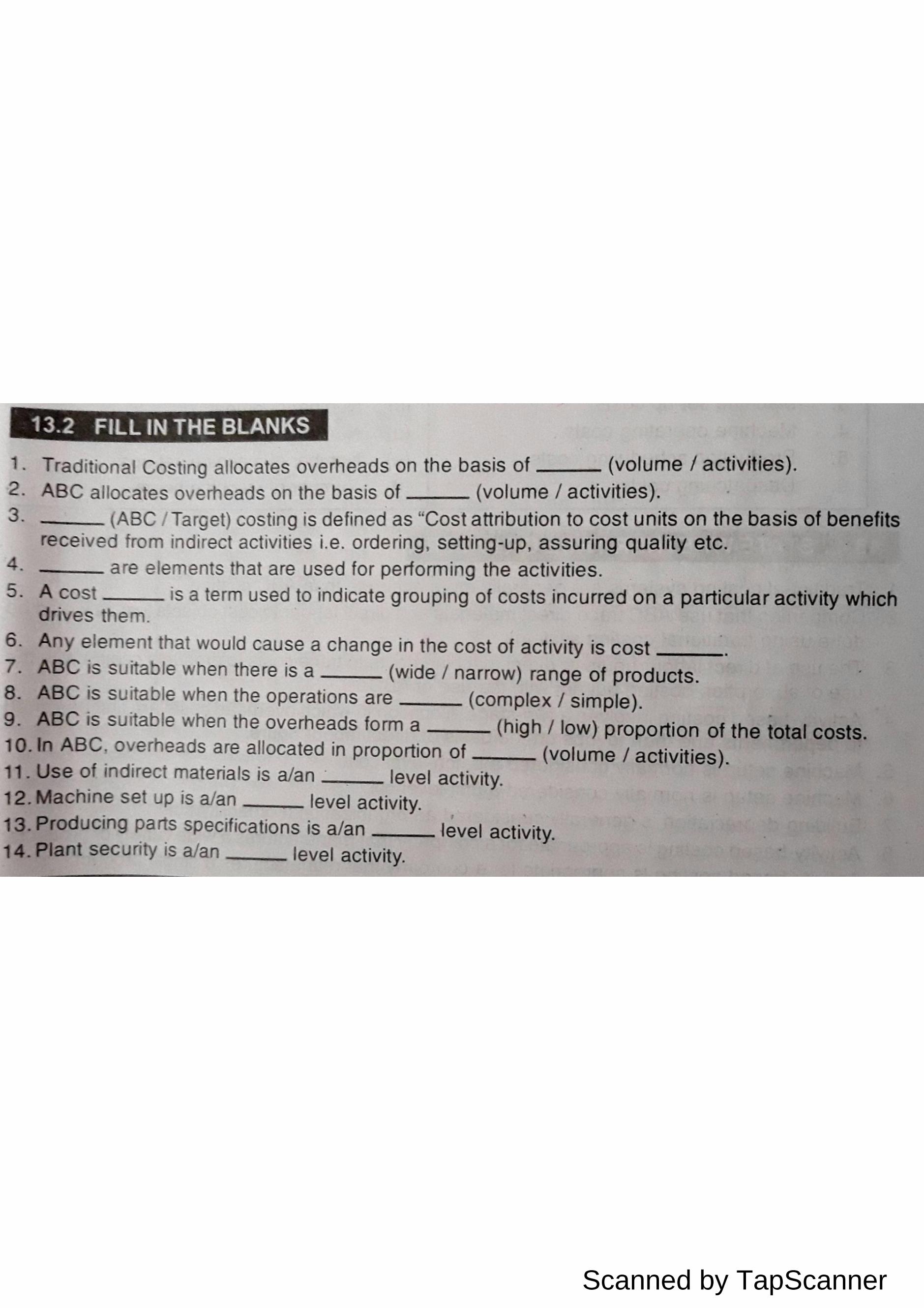

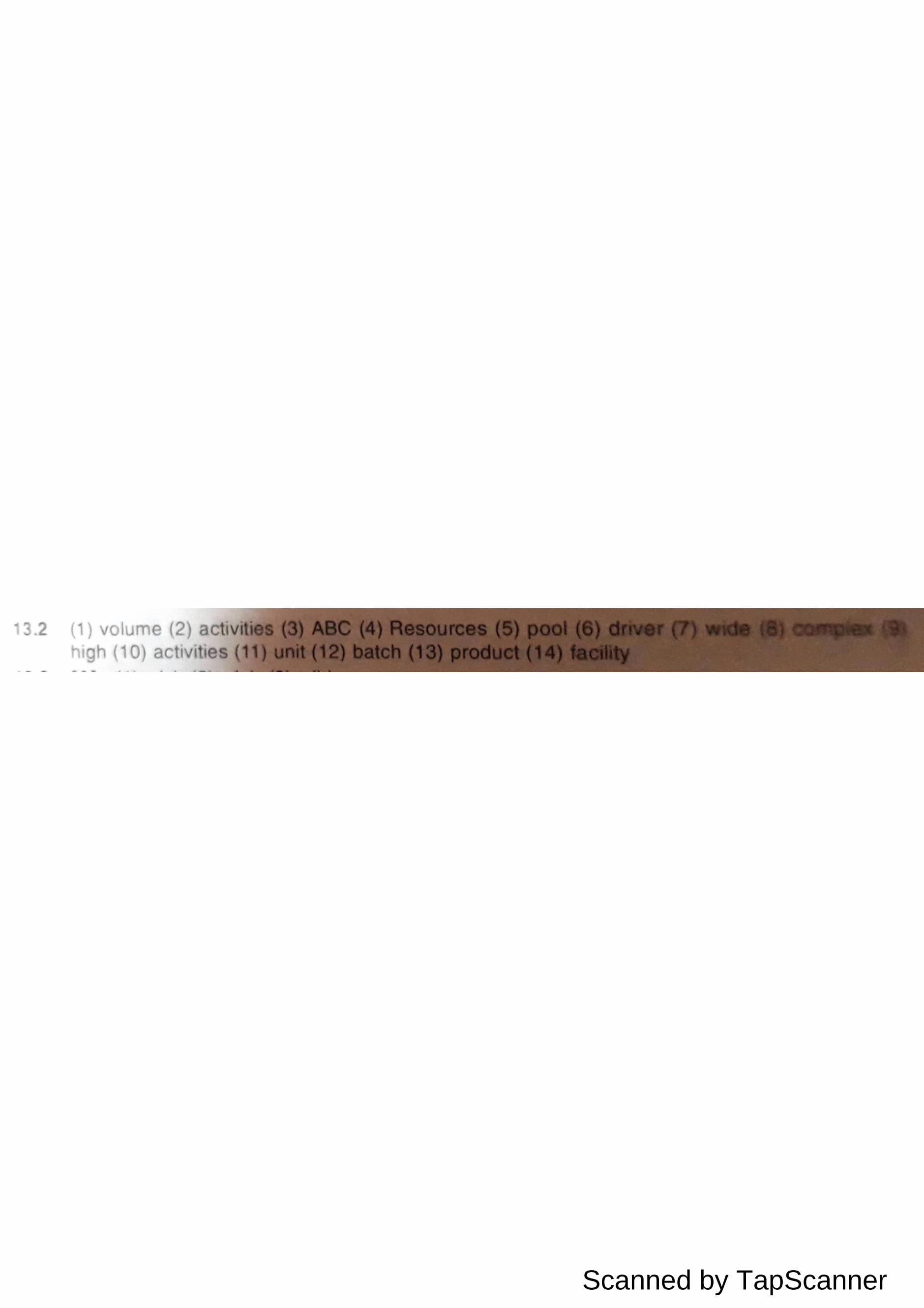

Q.66. Traditional Costing allocates overheads on the basis of______,

(a) Volume (b) activities (c) Events (d) job

Q.67. ABC allocates overheads on the basis of __________,

(a) Volume (b) activities (c) Events (d) job

Q.68. ____costing is defined as "Cost attribution to cost units on the basis of benefits received from indirect

activities i.e. ordering, setting-up, assuring quality etc.

(a) ABC (b Target (c) Joint Cost (d) job

Q.69________. are elements that are used for performing the activities?

(a) ABC (b) Target (c) Joint Cost (d) Resources

Q.70. A cost___ is a term used to indicate grouping of costs incurred on a particular activity which drives them

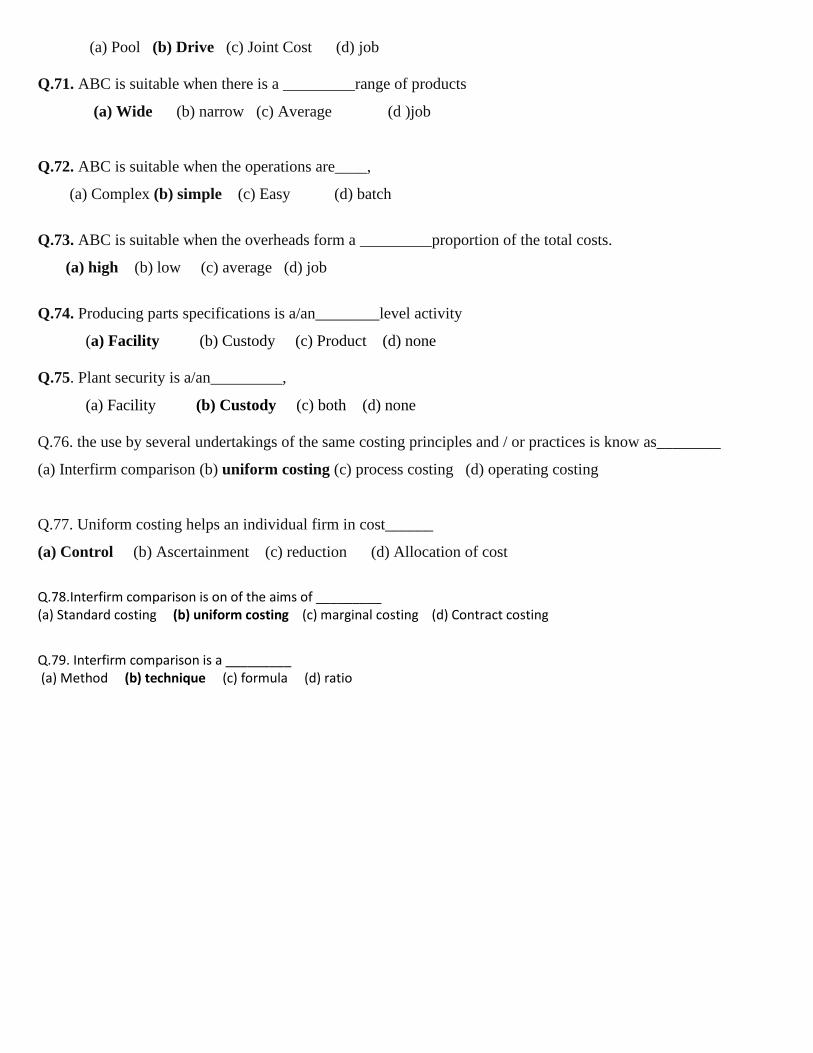

(a) Pool (b) Drive (c) Joint Cost (d) job

Q.71. ABC is suitable when there is a _________range of products

(a) Wide (b) narrow (c) Average (d )job

Q.72. ABC is suitable when the operations are____,

(a) Complex (b) simple (c) Easy (d) batch

Q.73. ABC is suitable when the overheads form a _________proportion of the total costs.

(a) high (b) low (c) average (d) job

Q.74. Producing parts specifications is a/an________level activity

(a) Facility (b) Custody (c) Product (d) none

Q.75. Plant security is a/an_________,

(a) Facility (b) Custody (c) both (d) none

Q.76. the use by several undertakings of the same costing principles and / or practices is know as________

(a) Interfirm comparison (b) uniform costing (c) process costing (d) operating costing

Q.77. Uniform costing helps an individual firm in cost______

(a) Control (b) Ascertainment (c) reduction (d) Allocation of cost

Q.78.Interfirm comparison is on of the aims of _________ (a) Standard costing (b) uniform costing (c) marginal costing (d) Contract costing

Q.79. Interfirm comparison is a _________ (a) Method (b) technique (c) formula (d) ratio

Scanned by TapScanner

Scanned by TapScanner

Scanned by TapScanner

Scanned by TapScanner

Scanned by TapScanner

Scanned by TapScanner

Scanned by TapScanner

Scanned by TapScanner

Scanned by TapScanner

![· Web viewAhmed rounds 1846 to the nearest 100. Bold. or underline the correct answer. [1] 19001850184618401800. Here are three angles A, B and C. [2] Bold or underline the word](https://img.pdfslide.us/doc/110x75/5f4581708131e54f9b24411f/web-view-ahmed-rounds-1846-to-the-nearest-100-bold-or-underline-the-correct-answer.jpg)