Embed Size (px)

Citation preview

MULTIFINANCE INDUSTRY

Industry Profile

� Finance industry plays a big role in the country's economic development in general.

� The multi-finance industry in Indonesia has grown � The multi-finance industry in Indonesia has grown rapidly and expanded in scale remarkably in recent years, and motorcycle finance is one of the brightest areas of business potential, a result of sound business factors, as we shall see below.

Industry Characteristic

� In 1975 the first multifinance company opened for business.

� Early 1985 this sector was known primarily for facilitating leases for heavy industrial equipment, aimed at construction companies which often aimed at construction companies which often could not afford the major outlay necessary for such purchases.

� After crisis 1997, The multi-finance industry in Indonesia has grown rapidly in the consumer financing sector like motorcycle, automobile, electronic

Industry Characteristic

� Multi-finance industry in Indonesia is under supervision of the Financing and Guranteeing Bureau of the Capital Market and Financial Agency Watch Dog (Bapepam LK) of the financeministry. ministry.

� Multi-finance industry includes leasing, factoring, consumer finance and credit card financing.

Industry Characteristic

� Leasing Leasing is financing system by companies for lessees for certain period to be repaid by installments. The lessees pay a specified rent on specified terms on a certain period. After the period is over the lessee is allowed to buy the capital goods or extend the leasing allowed to buy the capital goods or extend the leasing period.

� Factoring Factoring is a system transferring company's short term claims resulting from a trade transaction at home or abroad.

Industry Characteristic

� Consumer finance (consumer credits)

Consumer finance is a financing service provided by a company for the procurement of certain consumer goods or services to be repaid by installments in a certain period. installments in a certain period.

� Credit card

Credit card is a card shown by card holder to buy goods or services on credit to be repaid to the credit card issuer after a certain period.

Industry –Related Regulation

� The first policy on multi-finance industry was issued in 1974. At that time there was only one type of financing business that is leasing business.

� The main government regulation on multi-finance business is a decision of the financeminister No. 448/KMK.017/2000 in October 2000 minister No. 448/KMK.017/2000 in October 2000 and No. 178/LMK.06/2002 in April 2002. � procedure of establishment� Capital and ownership � board of directors� the opening of branch offices� loans and investments � limits of operations and other related aspects.

Industry –Related Regulation

� Establishment of Financing Companies Multi-finance companies could be established and owned by:

� Indonesia citizens and/or Indonesian companies

� Foreign companies and Indonesian citizens and /or joint � Foreign companies and Indonesian citizens and /or joint venture

� The companies must be PT (limited liabilities) or cooperates

Industry –Related Regulation

� Establishment of Financing Companies Multi-finance companies could be established and owned by:

� Indonesia citizens and/or Indonesian companies

� Foreign companies and Indonesian citizens and /or joint � Foreign companies and Indonesian citizens and /or joint venture

� The companies must be PT (limited liabilities) or cooperates

Growth of Industry

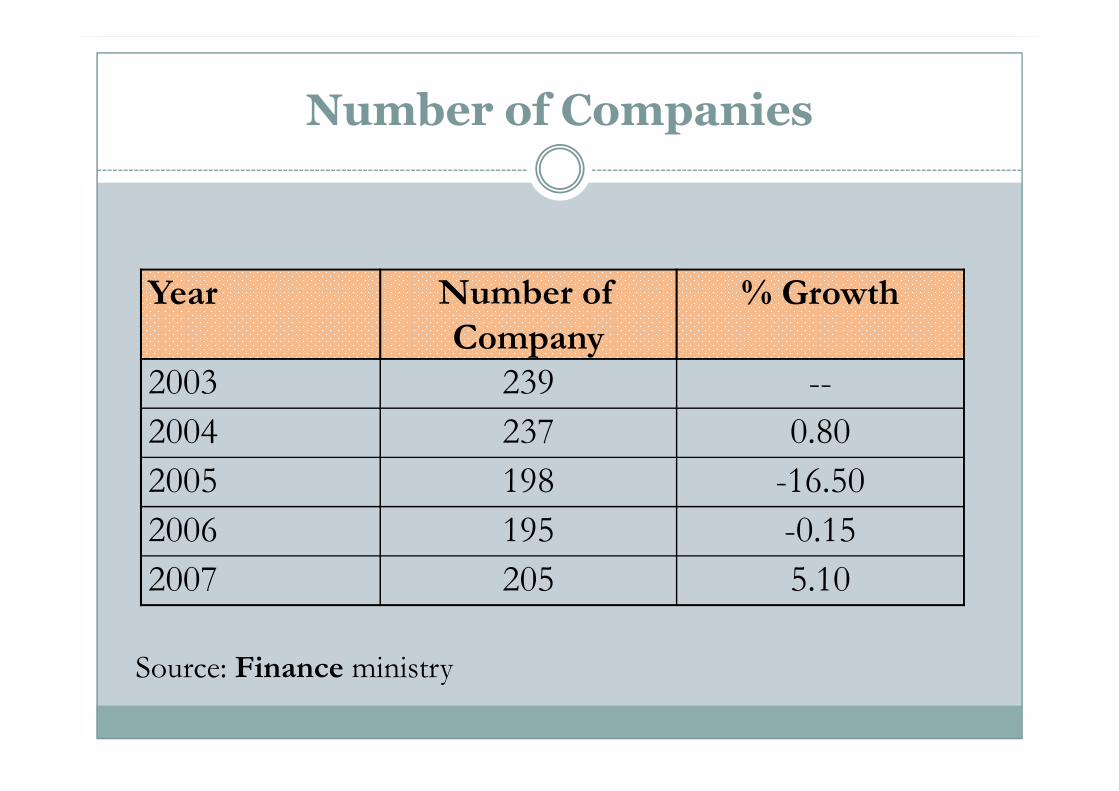

� Based on official data of Bank Indonesia (BI), there were 239 companies in 2004, but the number declined to 2005 in 2007.

� In 2006, there were 24 multi-finance companies suspended by the finance ministry for failure to suspended by the finance ministry for failure to submit audited financial report for 2004.

Number of Companies

Year Number of

Company

% Growth

2003 239 --2003 239 --

2004 237 0.80

2005 198 -16.50

2006 195 -0.15

2007 205 5.10

Source: Finance ministry

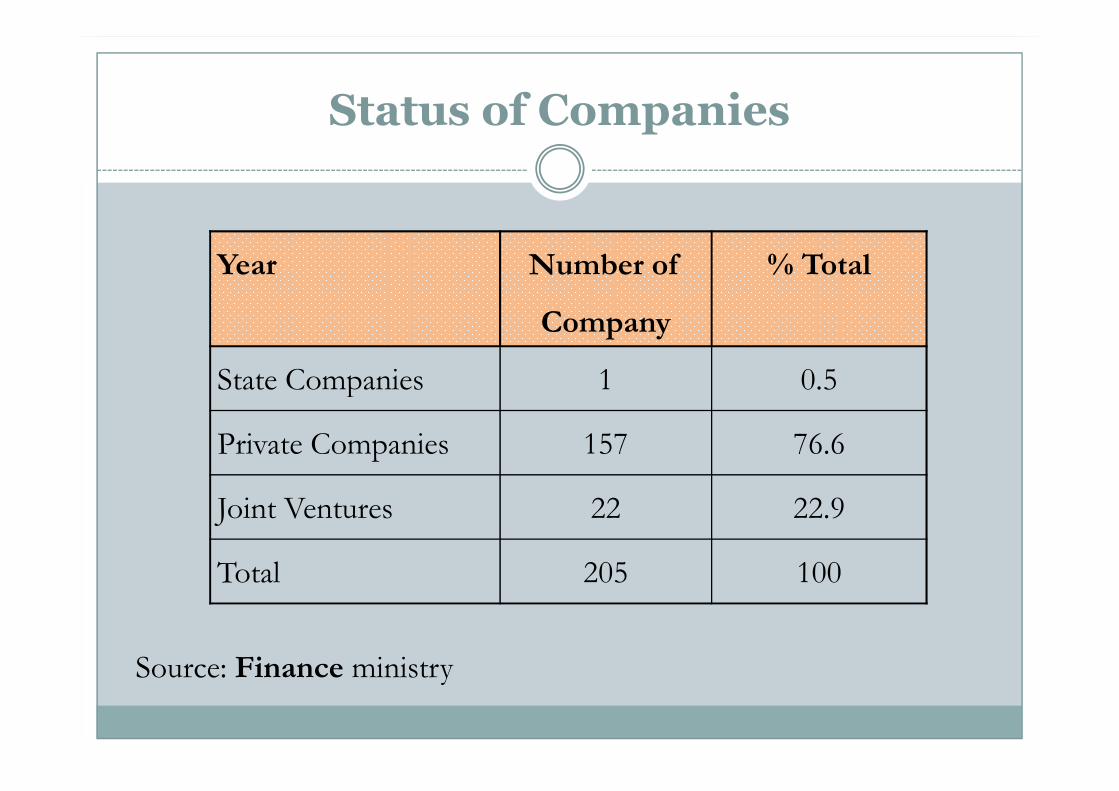

Status of Companies

Year Number of

Company

% Total

State Companies 1 0.5

Source: Finance ministry

State Companies 1 0.5

Private Companies 157 76.6

Joint Ventures 22 22.9

Total 205 100

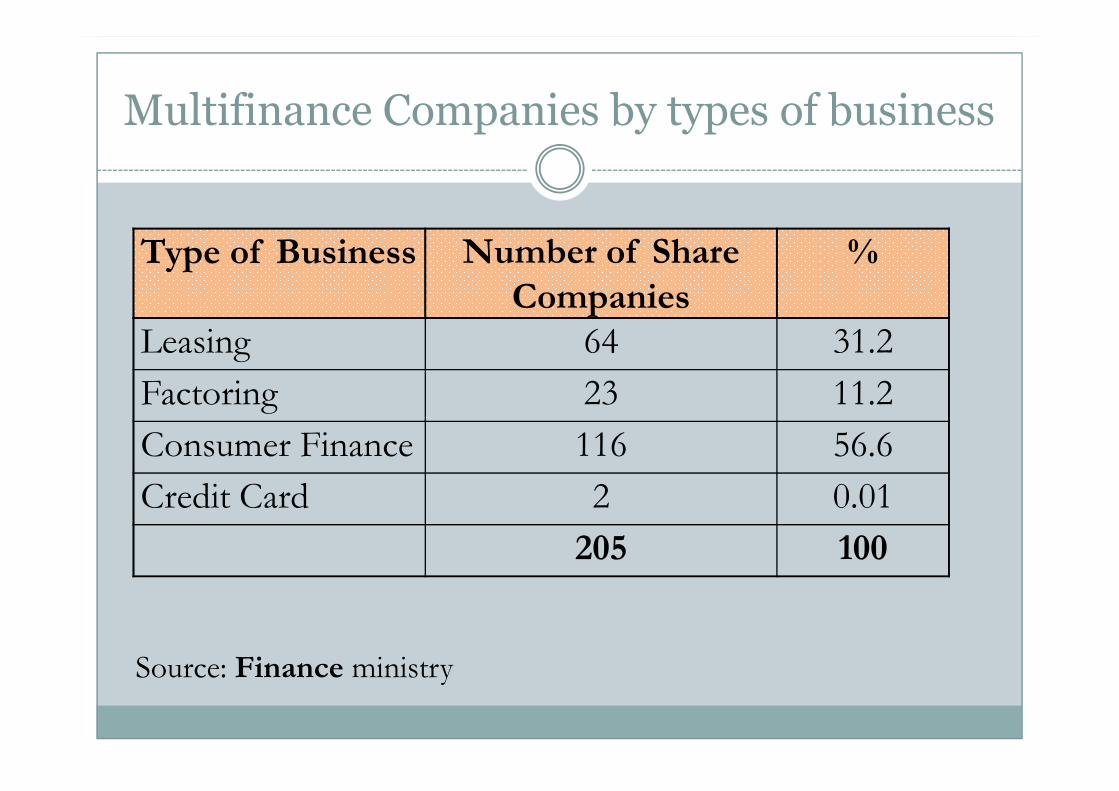

Multifinance Companies by types of business

Type of Business Number of Share

Companies

%

Leasing 64 31.2

Factoring 23 11.2

Source: Finance ministry

Factoring 23 11.2

Consumer Finance 116 56.6

Credit Card 2 0.01

205 100

Big Player - FIF

� Federal International Finance (FIF) which was established in 1989 with the name of PT. Mitrapusaka Artha Finance.

� In 1991, its name was changed with PT. Federal International Finance (FIF), with the majority shares held by PT. Astra International.

� FIF operates in financing the purchases of Honda � FIF operates in financing the purchases of Honda motorcycles, which are produced by PT. Astra Honda Motor, a subsidiary of the Astra Group.

� FIF has expanded operation to financing the purchases of electronic goods through FIF Spektra and in sharia financing through FIF Syariah.

� FIF has financial support mainly from Bank Permata, which is partly owned by the Astra Group.

Big Player - ASF

� Astra Sedaya Finance (ASF), which was established in 1982 with the name of PT. Rahardja Sedaya.

� After being taken over by Astra International, its name was changed in 1992 with Astra Sedaya Finance.

� ASF became the holding company for a number of subsidiaries including Astra Auto Finance, Estetika subsidiaries including Astra Auto Finance, Estetika Sedaya Finance, Stacomitra Sedaya Finance and Swadharma Bhakti Sedaya Finance.

� The combination of the companies is known as Astra Credit Company (ACC) offering financing service for the purchases of car products of the Astra Group including Toyota, Daihatsu, Isuzu, BMW, Peugeot and Nissan Diesel trucks.

Big Player - BAF

� Bussan Auto Finance (BAF), which started operation in 1997. It was originally named Danamon Mitsui Otomotif Finance, with shareholders including PT. Danamon Sanggrahan and Mitsui Co Ltd from Japan.

� In 1998, Danamon quit and the name of the company was changed with Bussan Auto Finance.

� BAF offer financing service for specially the purchases of Yamaha � BAF offer financing service for specially the purchases of Yamaha motorcycles.

� Oto Multiartha, which was established in 1994 with the name of Manunggal Multi Finance.

� In 1995, its name was changed with Oto Multiartha. In 1996 Sumitomo Corp from japan took over the majority shares of the company.

� Oto offer financing service for the purchases of cars. Its sister company Summit Oto Finance offer financing service for the purchases of motorcycles.

Big Player - WOM

� Wahana Otomitra Multiartha (WOM), which was established 1982 with the name of PT. Jakarta Tokyo Leasing by PT. Fuji Semeru Leasing.

� In 1997 the company was 50.03% acquired by Bank International Indonesia (BII) and its name was International Indonesia (BII) and its name was changed with Wahana Otomitra Multiartha.

� WOM offers financing service for the purchases of Japanese motorcycles including Honda, Yamaha and Suzuki, which dominate the domestic market.

� Leasing companies generally offer financing service for heavy equipment such as tractors, loaders. excavators, and other capital goods.

Big Player - Adhira

� PT Adira Quantum Multifinance (Adira)

� Adira was established in 2006 to provide financing service for electronic products.

� Previously, or 2004, the business was operated by PT. Adira Dinamika Multifinance, which has core PT. Adira Dinamika Multifinance, which has core business in financing the purchases of car and motorcycle.

� Until 2005, the company still reported operating loss. That year the company posted a loss of Rp 3.7 billion, but in 2006 it began to chalk up a net profit of Rp 4.4 billion.

Big Player - Sunprima

� Sunprima was established in 2003 to support its business in electronic retail operated by Columbia. Columbia was originally a distributor of household electronic products imported from Europe and Japan.

� It started business in financing service only in 1982. � It started business in financing service only in 1982.

� Sunprima utilizes the wide networks of Columbia, which has gained good reputation in service facility and sales.

� Its service f acility is especially needed by consumers far from service centers offered by electronic goods producers. I

� n 2006, Sunprima reported net profit at Rp 15.13 billion.

Big Player – GE Finance

� GE Finance Indonesia (Sumber Kredit)

� Sumber Kredit is an electronic financing service product of GE, which started operation in 1992. GE is aggressive in its operation in consumer financebusiness in the electronic sector. business in the electronic sector.

� Currently Sumber Kredit has 300,000 clients. The company cooperates with Carrefour hypermarket.

Big Player – FMF

� PT. Finansia Multi Finance (FMF) PT. Finansia MultiFinance was established in June, 1994 holding the license to operate as a factoring, leasing, consumer finance and credit card company Its product of consumer finance is known with the brand of Kredit Plus.

� FMF already has 27 branches all over the country including � FMF already has 27 branches all over the country including three in Sumatra, 16 in Java, 1 in Bali, 5 in Kalimantan, and 2 in Sulawesi.

� The company has 150,000 clients. It cooperates with Bank BRI to facilitate on line payment system.

� The shareholders of FMF include Finansia Pacifica Raya (67%), ND Investment Pte.Ltd (24.9%) and Growmoto Kendall Pte.Ltd (8.10%).

Role of Modern Retail

� The retail sector is a major partner of financing companies supporting each other in expanding business notably in the electronic sectors.

� Retail sector especially hypermarkets such as Carrefour, Giant and Hypermart are among major business players in household electronic products such as TV sets, AC, refrigerators and hand-phones. in household electronic products such as TV sets, AC, refrigerators and hand-phones.

� The past several years saw a fast growth in the number of hypermarket outlets--from 83 units in 2005, up to 90 units in 2006 and to 94 units in 2007. The number of outlets is expected to increase further as the Lippo Group and Matahari Putra Prima plan to open new outlets this year.

Leasing Player - CJP

� Central Java Power (CJP) which is a subsidiary of PT. PLN. In May 2003 CJP and PLN resumed the construction of a coal fired power plant (PLTU) of Tanjung Jati B, which was valued at US$ 1.65 billion after being long delayed. after being long delayed.

� The 2 x 660 megawatt PLTU is located in Jepara, Central Java.

� Agreement between CJP and PLN in the form of leasing was on build, lease and transfer (BLT) scheme. In 2006, CJP as a lessor handed over the maintenance, production and sales of power to PLN as a lessee.

� The leasing is for 20 years.

Leasing Player - CSUL

� Chandra Sakti Utama Leasing (CSUL), which was established in the 1990s.

� CSUL is a subsidiary of the Trakindo Group with CSUL is a subsidiary of the Trakindo Group with PT. Trakindo Utama a a holding company.

� CSUL offer leasing service for the purchases of Caterpillar heavy equipment from the United States with Trakindo as the agent.

� CSUL has branches in Medan and Surabaya.

Leasing Player - ORIF

� Orix Indonesia Finance (ORIF), which was established in 1975 with the name of PT.Orient Bina Usaha Leasing (OBUL).

� The company is a joint venture between ORIX � The company is a joint venture between ORIX Corporation (85%) and Yayasan Kesejahteraan Karyawan (workers' welfare foundation) of Bank Indonesia (15%).

� ORIF offers financing services for the purchases of heavy equipment, ships, office equipment, industrial machines, as well as cars.

Factoring

� Factoring financing business has not expanded as expected in the country.

� There are few transaction of companies transferring claims to financing companies. transferring claims to financing companies. Therefore, business players in this sector are few in number.

� The main players in this business sector are: � Koexim Mandiri Finance

� Clemont Finance Indonesia Corp

Credit Card Financing

� Credit card financing companies offer service for the purchases of goods and service using credit cards.

� Based on data at Bank Indonesia (BI), the principals of credit card in Indonesia at present principals of credit card in Indonesia at present are Visa International, Mastercard International, Diners and Amex.

� There are 22 issuers of credit cards in the country including 20 banks and two multi-finance companies.

Credit Card Financing - Diner

� Diner Jaya Indonesia International is the issuer of credit card under license of the U.S. based Diners Club. based Diners Club.

� Diners Club's share of the market in Indonesia is relatively small compared with those of Visa and Master Card.

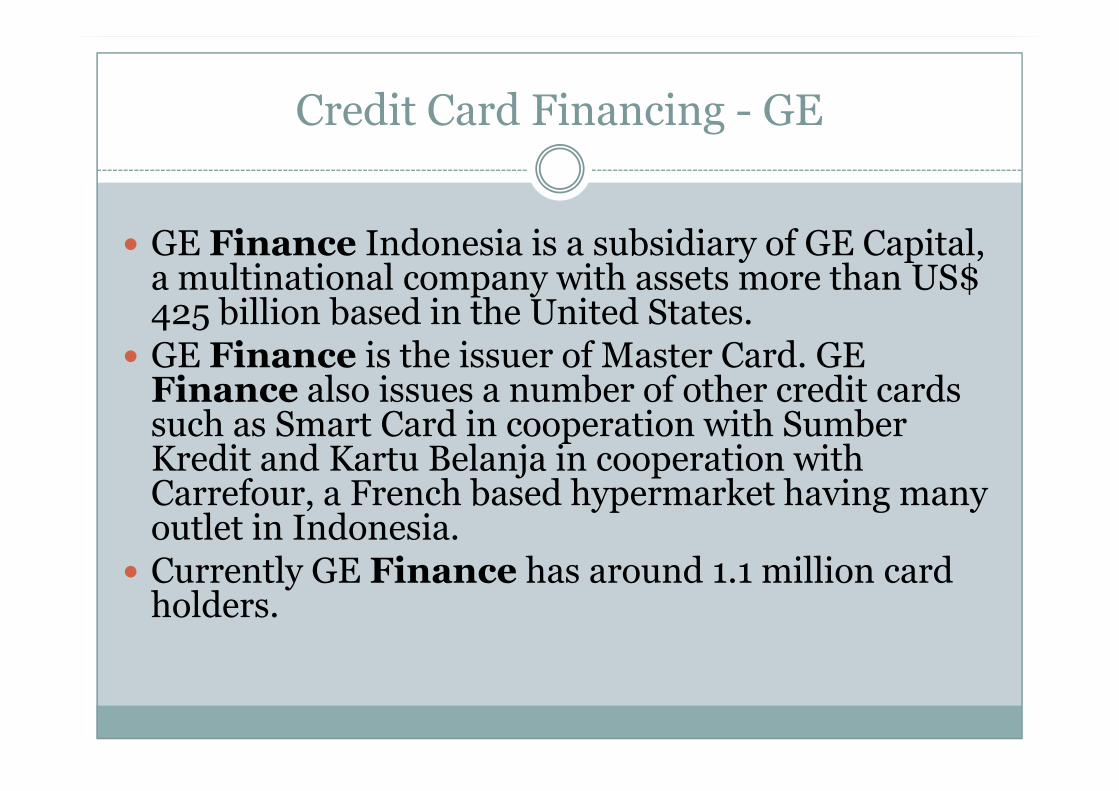

Credit Card Financing - GE

� GE Finance Indonesia is a subsidiary of GE Capital, a multinational company with assets more than US$ 425 billion based in the United States.

� GE Finance is the issuer of Master Card. GE Finance also issues a number of other credit cards Finance also issues a number of other credit cards such as Smart Card in cooperation with Sumber Kredit and Kartu Belanja in cooperation with Carrefour, a French based hypermarket having many outlet in Indonesia.

� Currently GE Finance has around 1.1 million card holders.

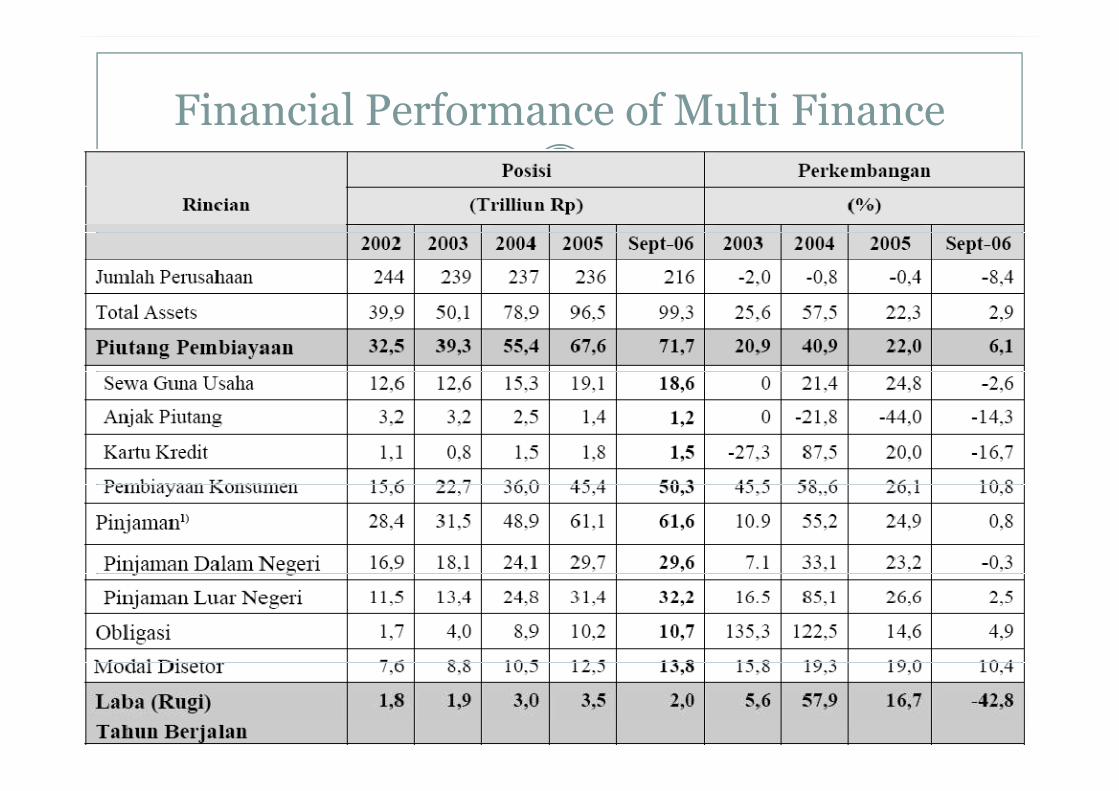

Financial Performance of Multi Finance

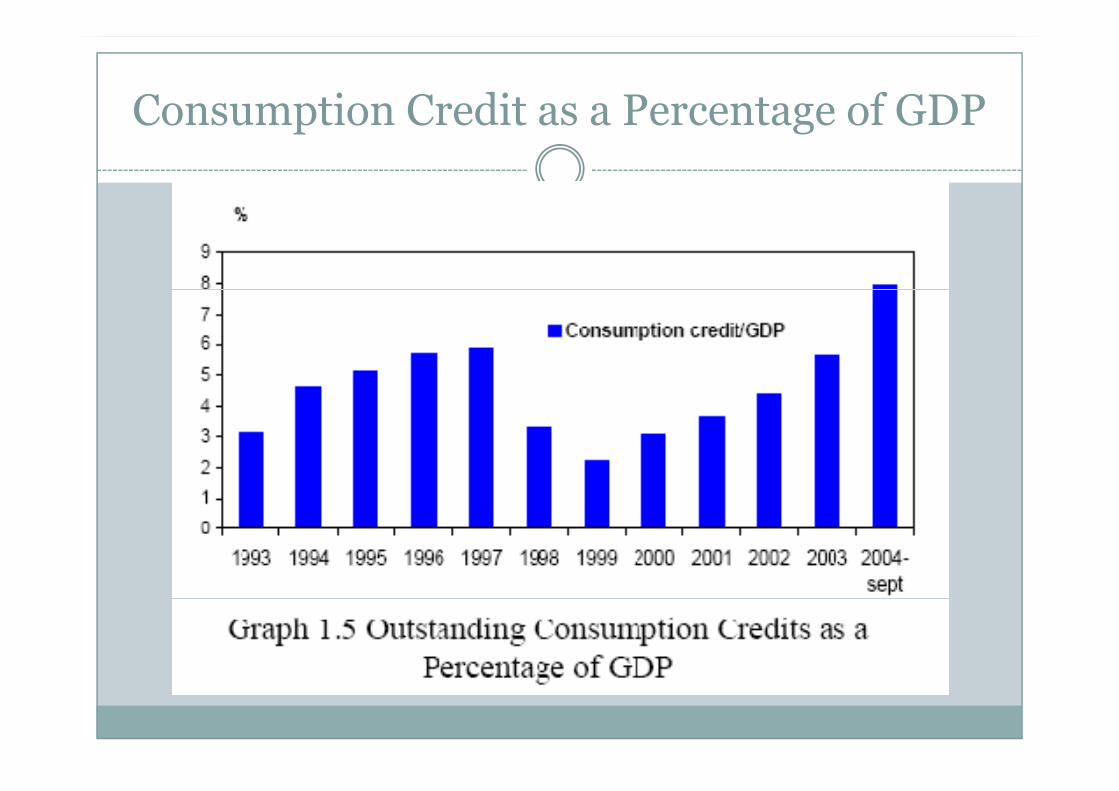

Consumption Credit as a Percentage of GDP

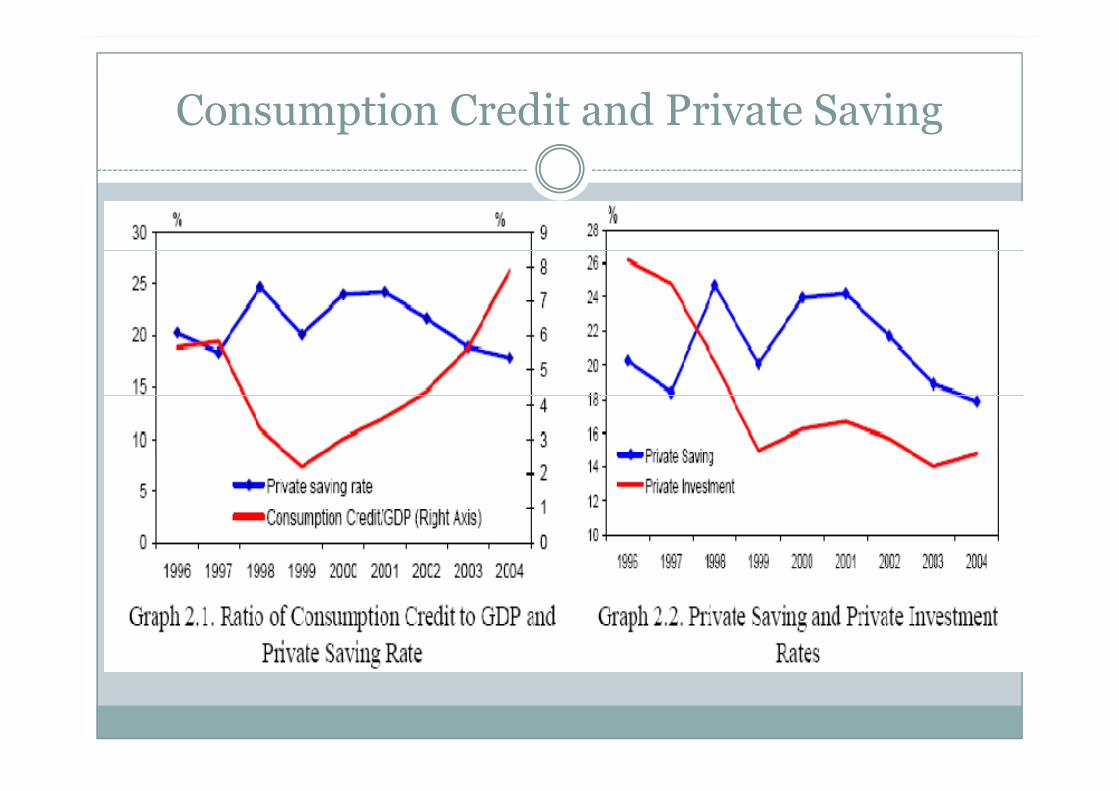

Consumption Credit and Private Saving

Business Process

� Multi-finance company doesn’t have specific product because it function as a financial intermadiary like bank.

� Companies operating in consumer finance offer financing service mainly for the purchases of cars and motorcycles, and electronic goods like TV, refrigerators, AC, washing machines, DVD players, etc. AC, washing machines, DVD players, etc.

� Leasing companies generally offer financing service for heavy equipment such as tractors, loaders. excavators, and other capital goods.

� Leasing business grew fast lately with the risker business in the mining and plantation sectors as well in construction sector.

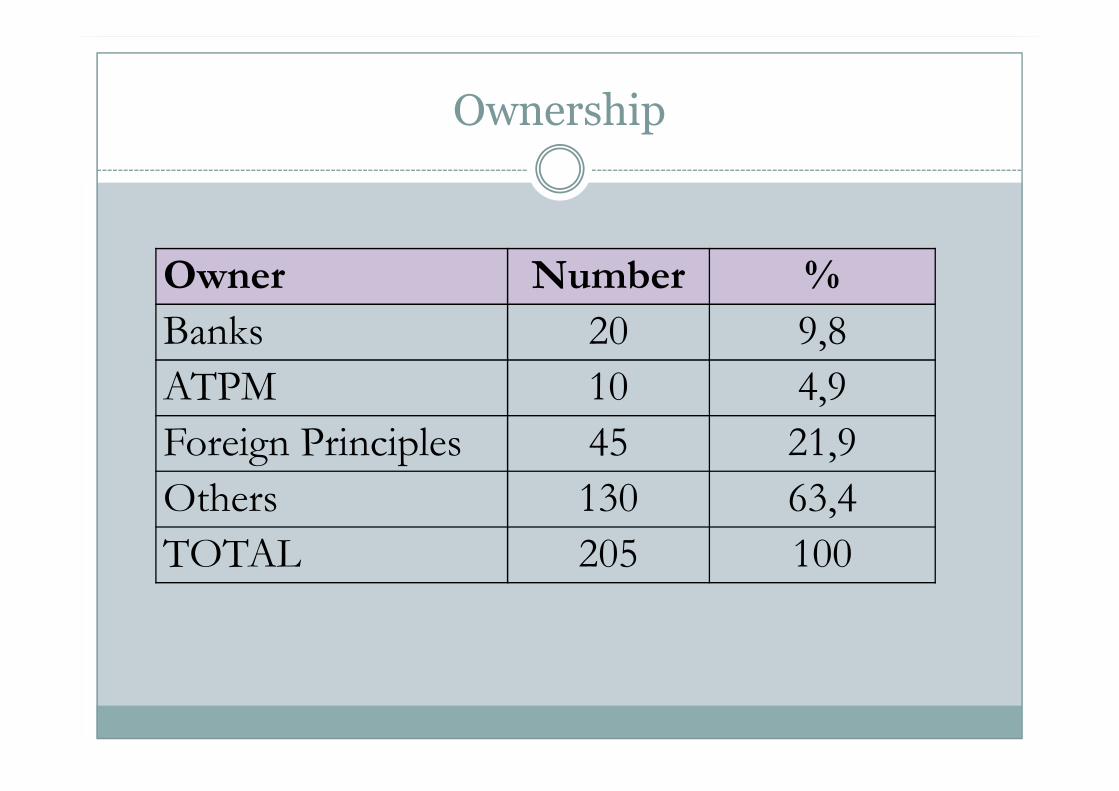

Ownership

� Owners of multi-finance companies include banks, company group, brand holding sole agents (ATPM) of cars and foreign principals of car makers operating in financial service business.

� Powerful financing companies are only those � Powerful financing companies are only those affiliated to banks or car makers and ATPM.

� Astra

� Danamon

� BII

Ownership

Owner Number %

Banks 20 9,8

ATPM 10 4,9ATPM 10 4,9

Foreign Principles 45 21,9

Others 130 63,4

TOTAL 205 100

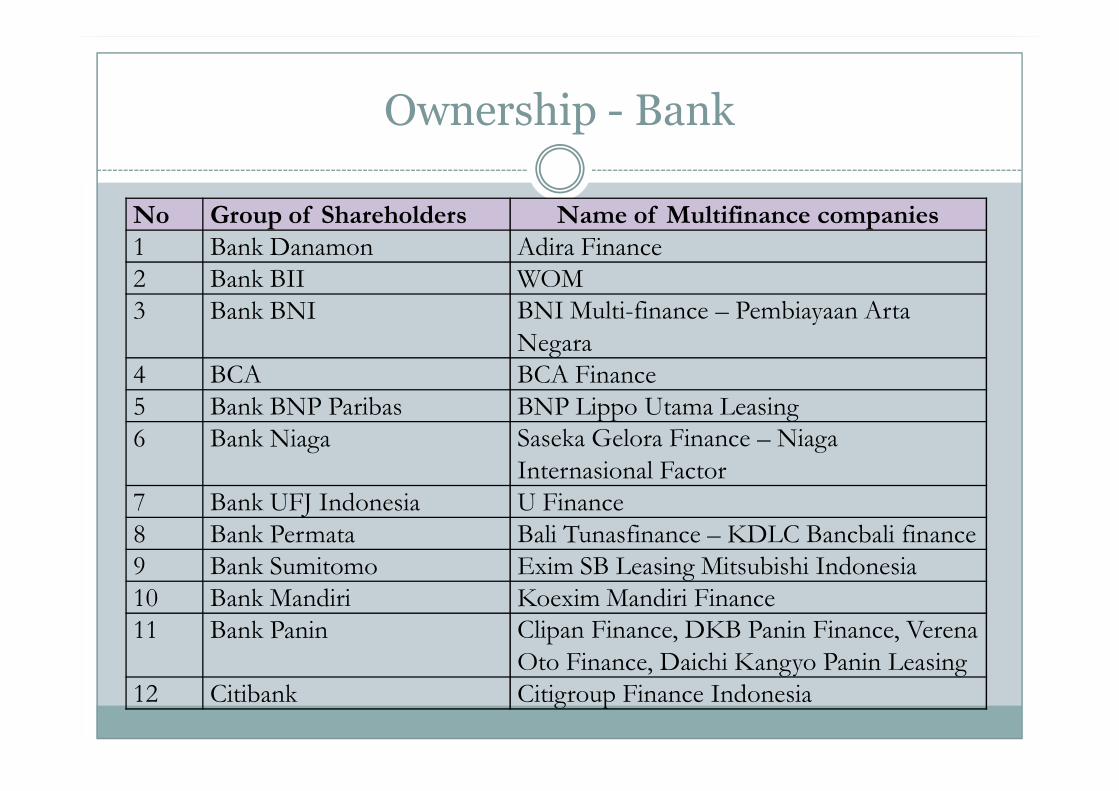

Ownership - Bank

No Group of Shareholders Name of Multifinance companies

1 Bank Danamon Adira Finance

2 Bank BII WOM

3 Bank BNI BNI Multi-finance – Pembiayaan Arta

Negara

4 BCA BCA Finance

5 Bank BNP Paribas BNP Lippo Utama Leasing5 Bank BNP Paribas BNP Lippo Utama Leasing

6 Bank Niaga Saseka Gelora Finance – Niaga

Internasional Factor

7 Bank UFJ Indonesia U Finance

8 Bank Permata Bali Tunasfinance – KDLC Bancbali finance

9 Bank Sumitomo Exim SB Leasing Mitsubishi Indonesia

10 Bank Mandiri Koexim Mandiri Finance

11 Bank Panin Clipan Finance, DKB Panin Finance, Verena

Oto Finance, Daichi Kangyo Panin Leasing

12 Citibank Citigroup Finance Indonesia

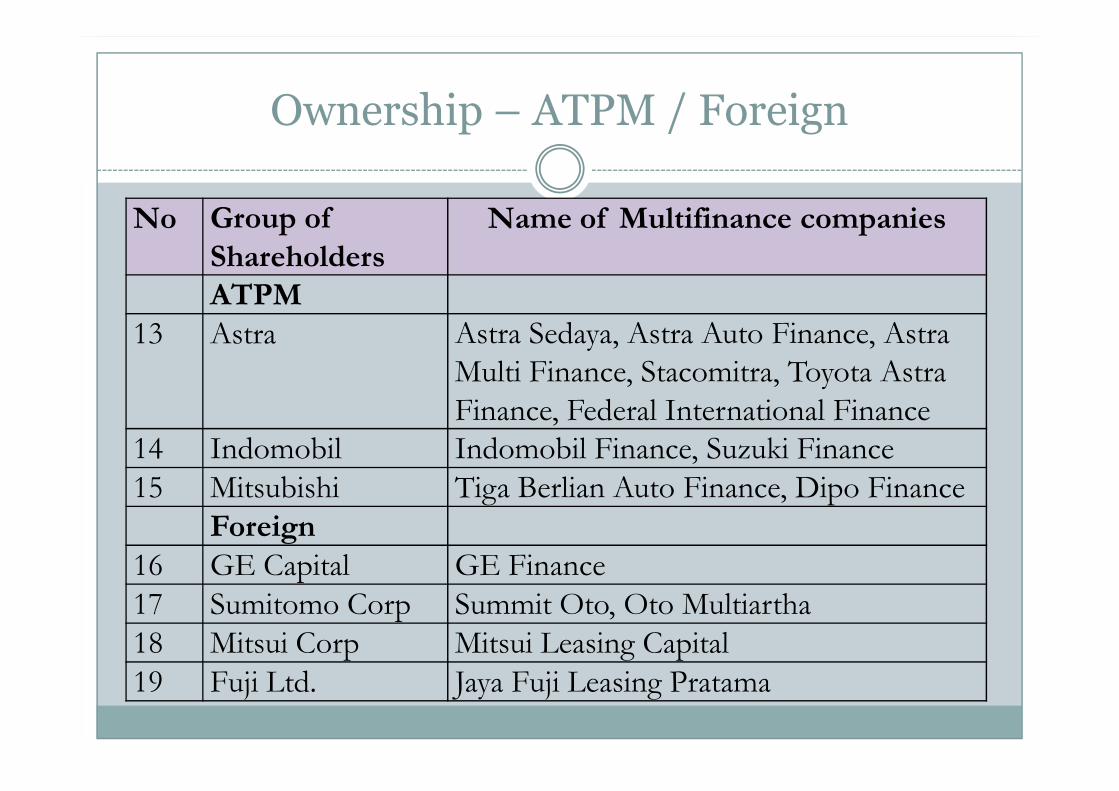

Ownership – ATPM / Foreign

No Group of

Shareholders

Name of Multifinance companies

ATPM

13 Astra Astra Sedaya, Astra Auto Finance, Astra

Multi Finance, Stacomitra, Toyota Astra

Finance, Federal International FinanceFinance, Federal International Finance

14 Indomobil Indomobil Finance, Suzuki Finance

15 Mitsubishi Tiga Berlian Auto Finance, Dipo Finance

Foreign

16 GE Capital GE Finance

17 Sumitomo Corp Summit Oto, Oto Multiartha

18 Mitsui Corp Mitsui Leasing Capital

19 Fuji Ltd. Jaya Fuji Leasing Pratama

Sources of Fund

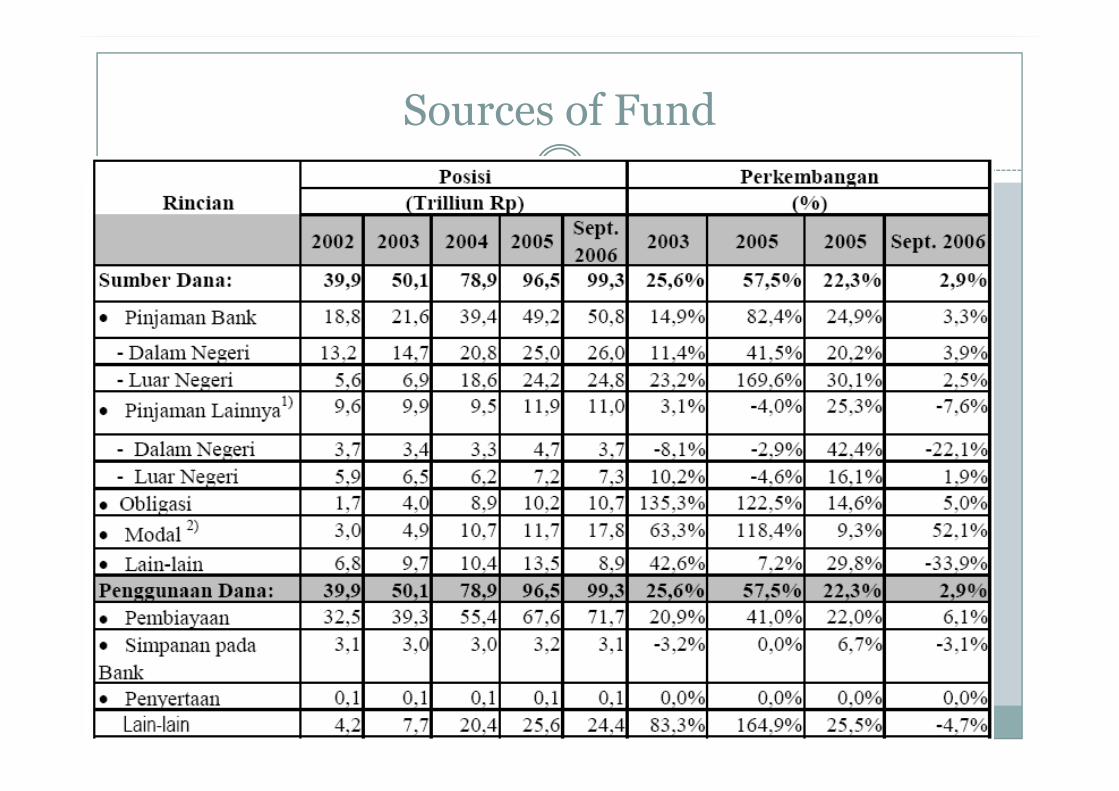

� Source of funds for financing companies include bank and non bank loans, bonds, private placement and other loans.

� Bank Loan

� Loans from local and foreign banks have increased from year to years--from Rp 21.5 trillion in 2003 to Rp 65.7 trillion in 2007. Banks loan account for the largest portion or 73.2% of the total amount of financial support received by multi-finance companies in 2007.

Sources of Fund

Sources of Fund

� Joint Ventures

� Joint venture financing companies (between Indonesian and foreign partners) generally use loans from its foreign shareholders or affiliates. Joint venture companies used foreign loans worth Rp 30.99 trillion in 2007 as against Rp 4.85 trillion used by non joint venture private companies. 4.85 trillion used by non joint venture private companies.

� Join Financing� Joint financing scheme is generally made with banks. Multi-finance companies not involving partners in running their business operations issue bonds or seek syndicated loans if they need additional capital.

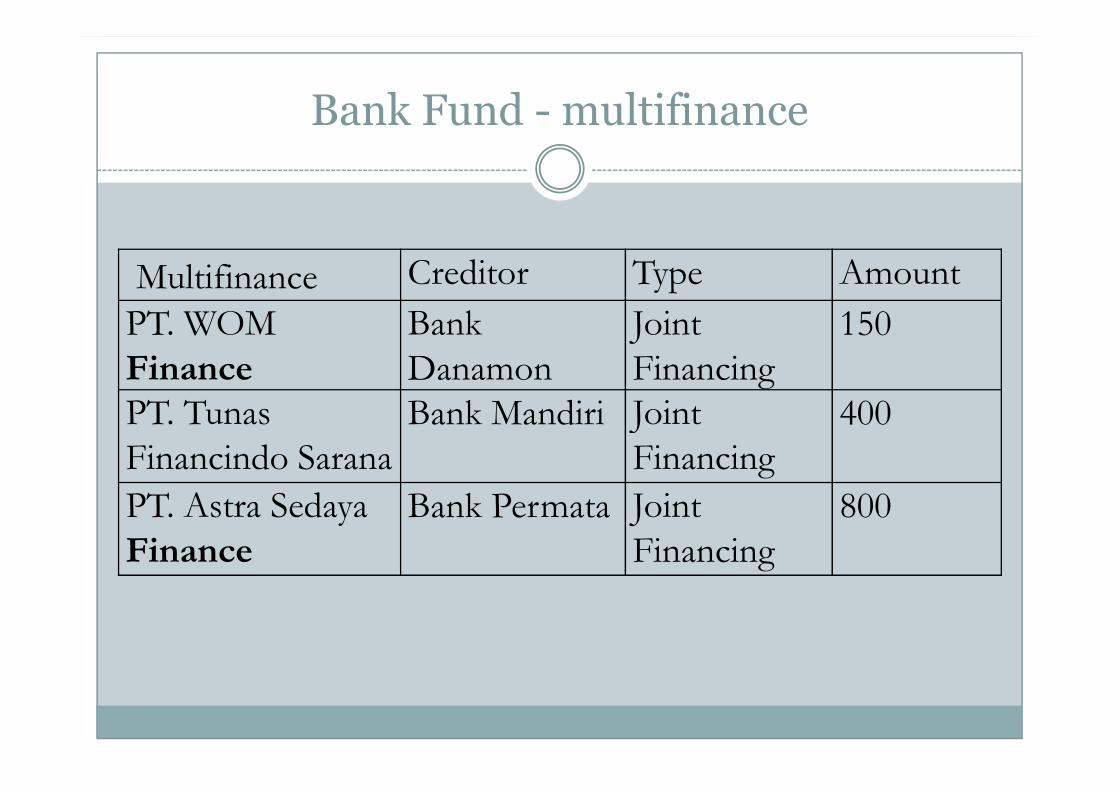

Bank Fund - multifinance

Multifinance Creditor Type Amount

PT. WOM

Finance

Bank

Danamon

Joint

Financing

150

PT. Tunas Bank Mandiri Joint 400PT. Tunas

Financindo Sarana

Bank Mandiri Joint

Financing

400

PT. Astra Sedaya

Finance

Bank Permata Joint

Financing

800

Sources of Fund - Bonds

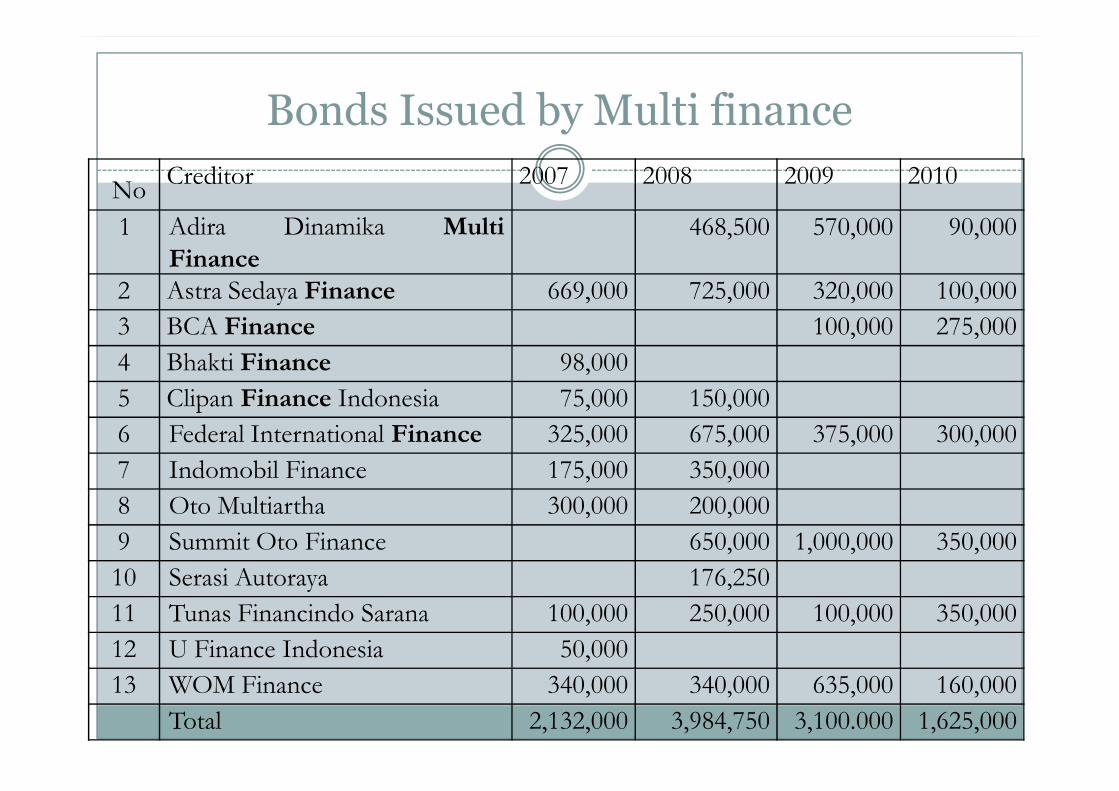

� Meanwhile funds sourced from bonds have continued to increased.

� In 2007, bond funds reached Rp 12.9 trillion or an increase of 29% from Rp 10 trillion in the previous year. year.

� The bond funds accounted for 14.4% of the total funds used for financing service of Rp 89.6 trillion that year.

� Necessitated by growing demand for financing services, a number of multi-finance companies have been more aggressive in issuing bonds.

Bonds Issued by Multi finance

NoCreditor 2007 2008 2009 2010

1 Adira Dinamika Multi

Finance

468,500 570,000 90,000

2 Astra Sedaya Finance 669,000 725,000 320,000 100,000

3 BCA Finance 100,000 275,000

4 Bhakti Finance 98,000

5 Clipan Finance Indonesia 75,000 150,000 5 Clipan Finance Indonesia 75,000 150,000

6 Federal International Finance 325,000 675,000 375,000 300,000

7 Indomobil Finance 175,000 350,000

8 Oto Multiartha 300,000 200,000

9 Summit Oto Finance 650,000 1,000,000 350,000

10 Serasi Autoraya 176,250

11 Tunas Financindo Sarana 100,000 250,000 100,000 350,000

12 U Finance Indonesia 50,000

13 WOM Finance 340,000 340,000 635,000 160,000

Total 2,132,000 3,984,750 3,100.000 1,625,000

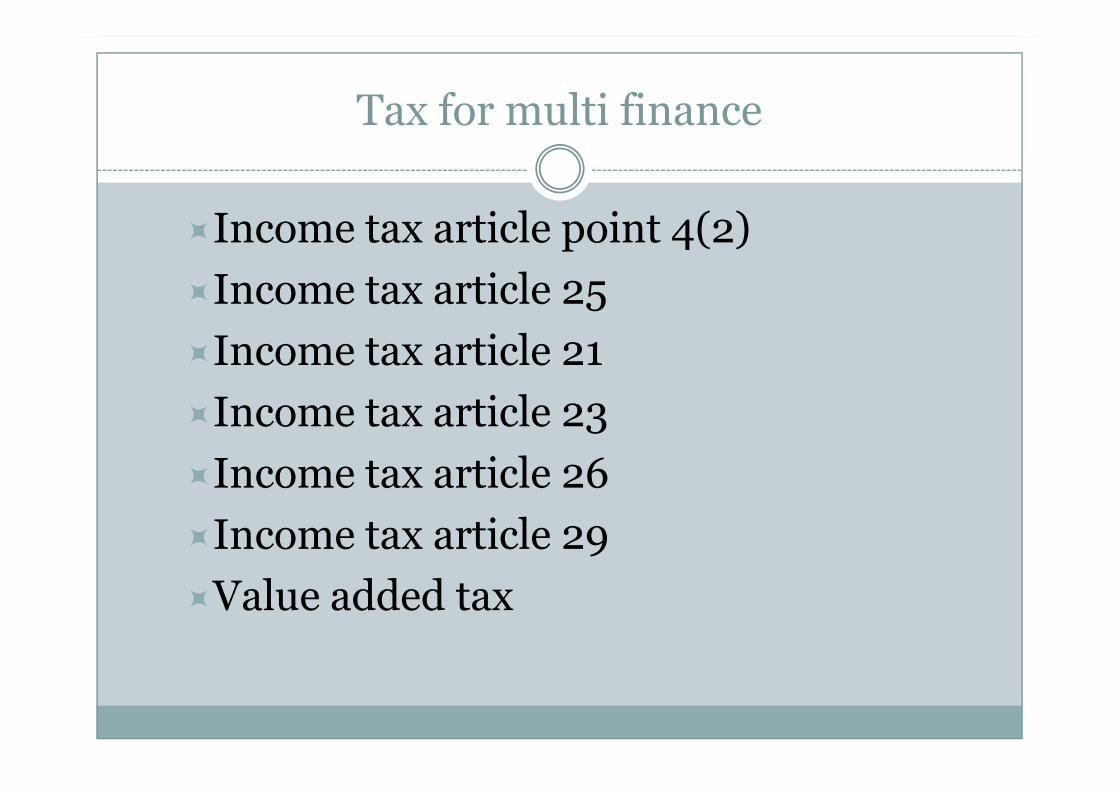

Tax for multi finance

�Income tax article point 4(2)

�Income tax article 25

�Income tax article 21

Income tax article 23�Income tax article 23

�Income tax article 26

�Income tax article 29

�Value added tax

Grey Area - Taxation

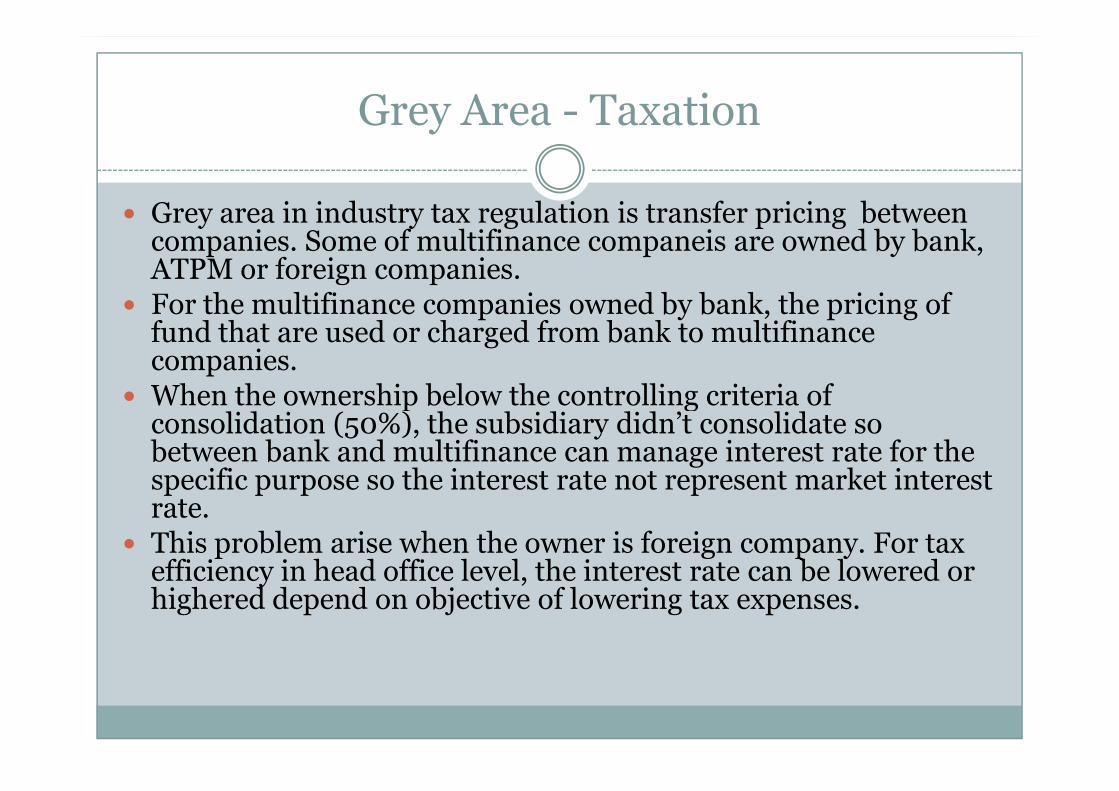

� Grey area in industry tax regulation is transfer pricing between companies. Some of multifinance companeis are owned by bank, ATPM or foreign companies.

� For the multifinance companies owned by bank, the pricing of fund that are used or charged from bank to multifinance companies.

� When the ownership below the controlling criteria of � When the ownership below the controlling criteria of consolidation (50%), the subsidiary didn’t consolidate so between bank and multifinance can manage interest rate for the specific purpose so the interest rate not represent market interest rate.

� This problem arise when the owner is foreign company. For tax efficiency in head office level, the interest rate can be lowered or highered depend on objective of lowering tax expenses.

Grey Area - Taxation

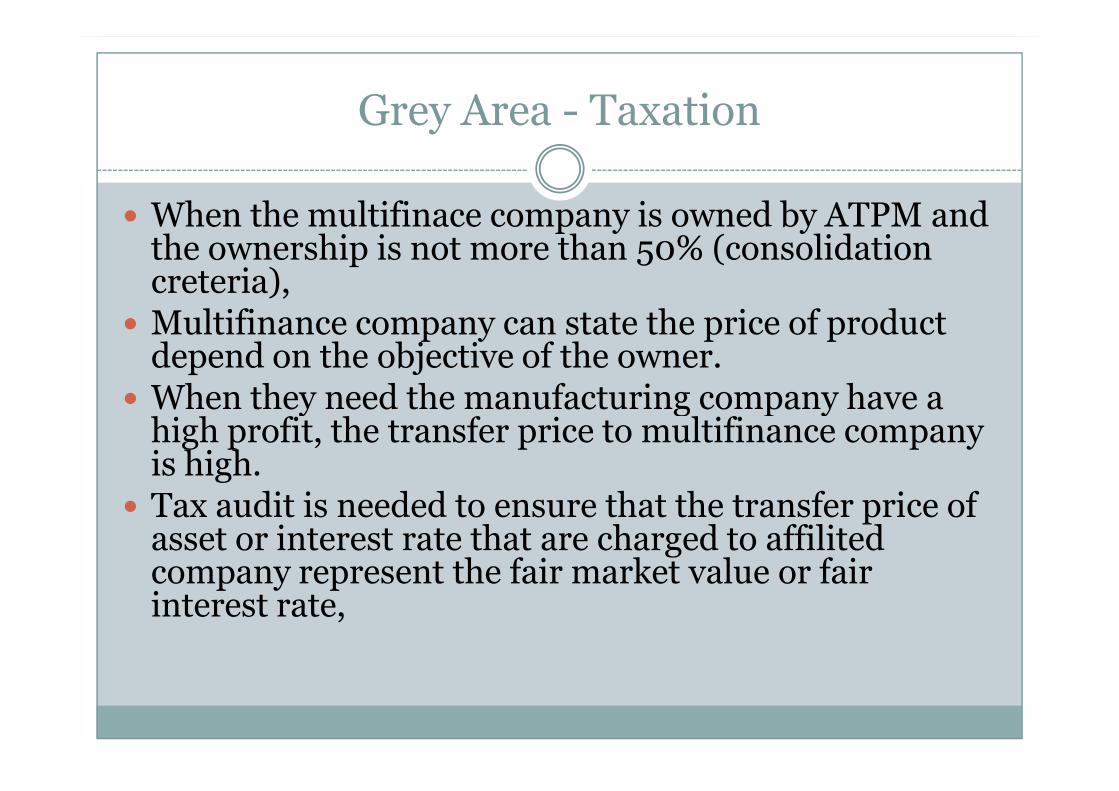

� When the multifinace company is owned by ATPM and the ownership is not more than 50% (consolidation creteria),

� Multifinance company can state the price of product depend on the objective of the owner.

� When they need the manufacturing company have a � When they need the manufacturing company have a high profit, the transfer price to multifinance company is high.

� Tax audit is needed to ensure that the transfer price of asset or interest rate that are charged to affilited company represent the fair market value or fair interest rate,

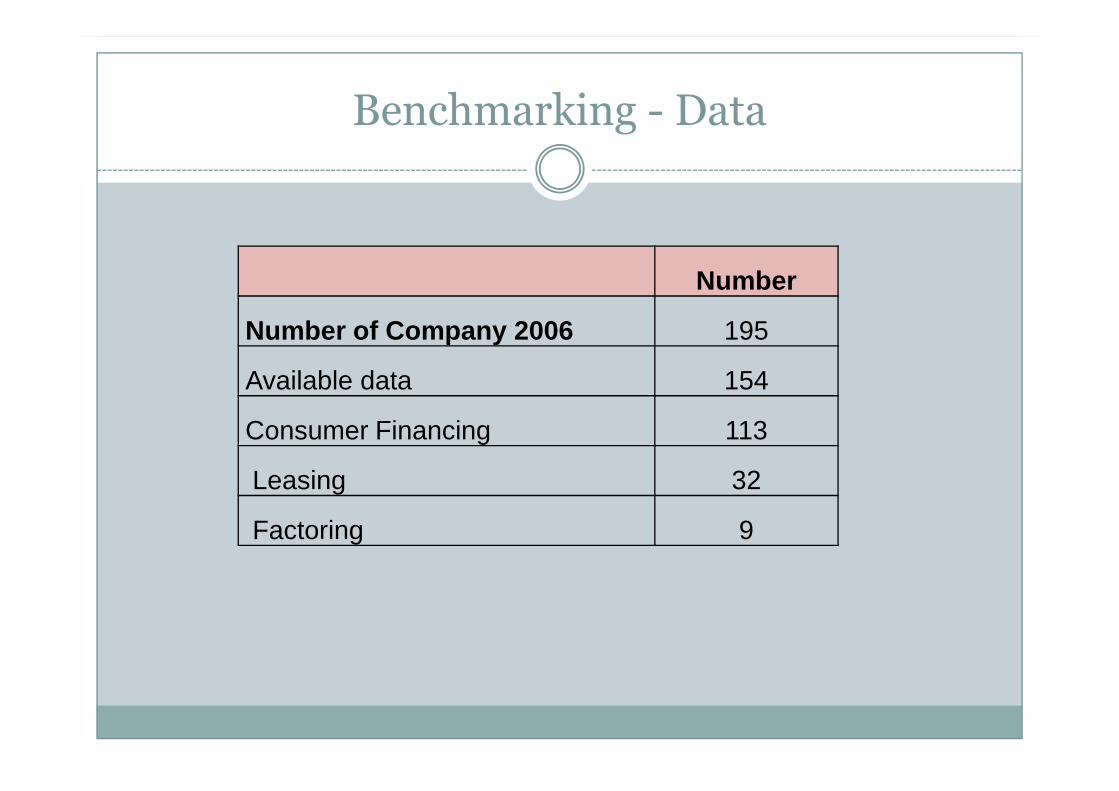

Benchmarking - Data

Number

Number of Company 2006 195

Available data 154

Consumer Financing 113

Leasing 32

Factoring 9

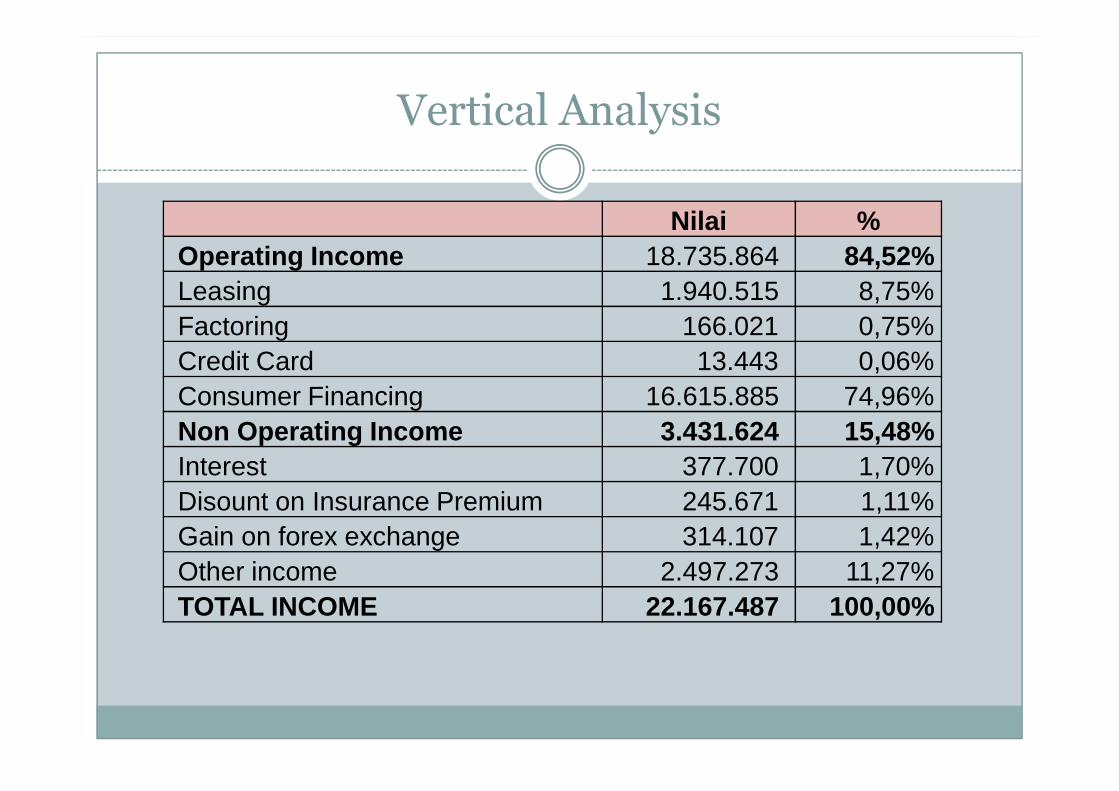

Vertical Analysis

Nilai %Operating Income 18.735.864 84,52%Leasing 1.940.515 8,75%Factoring 166.021 0,75%Credit Card 13.443 0,06%Consumer Financing 16.615.885 74,96%Consumer Financing 16.615.885 74,96%Non Operating Income 3.431.624 15,48%Interest 377.700 1,70%Disount on Insurance Premium 245.671 1,11%Gain on forex exchange 314.107 1,42%Other income 2.497.273 11,27%TOTAL INCOME 22.167.487 100,00%

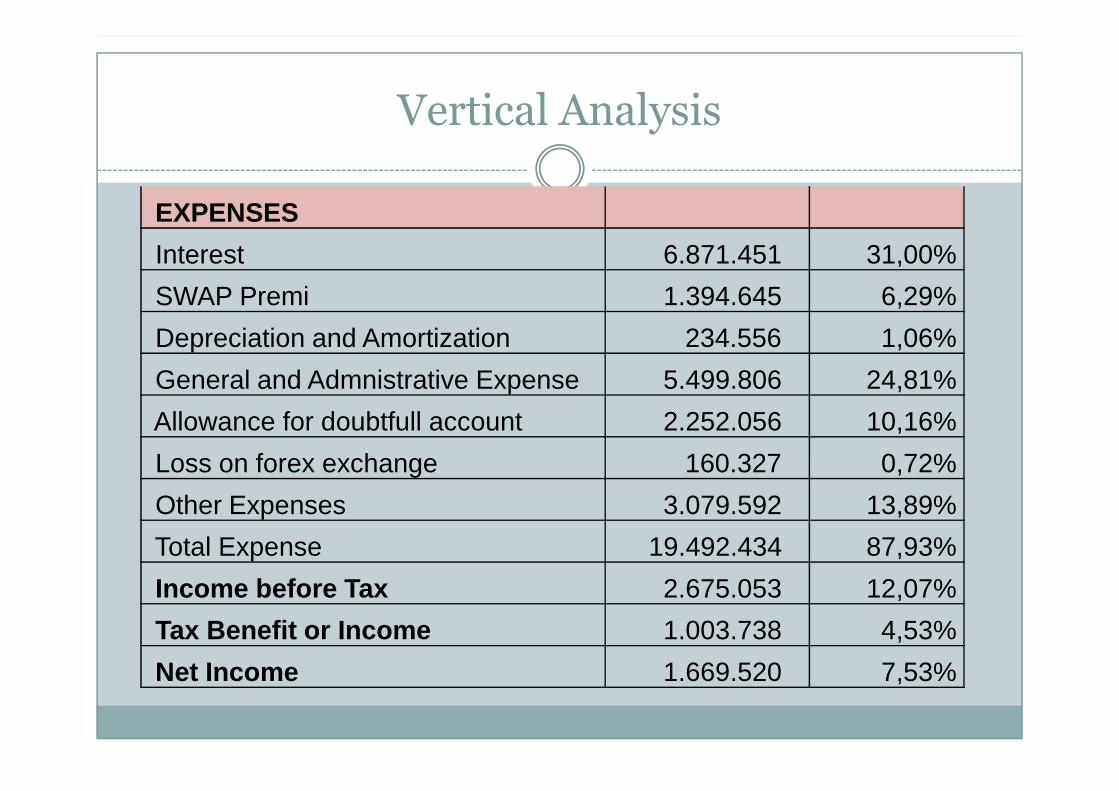

Vertical Analysis

EXPENSES

Interest 6.871.451 31,00%

SWAP Premi 1.394.645 6,29%

Depreciation and Amortization 234.556 1,06%

General and Admnistrative Expense 5.499.806 24,81%

Allowance for doubtfull account 2.252.056 10,16%

Loss on forex exchange 160.327 0,72%

Other Expenses 3.079.592 13,89%

Total Expense 19.492.434 87,93%

Income before Tax 2.675.053 12,07%

Tax Benefit or Income 1.003.738 4,53%

Net Income 1.669.520 7,53%

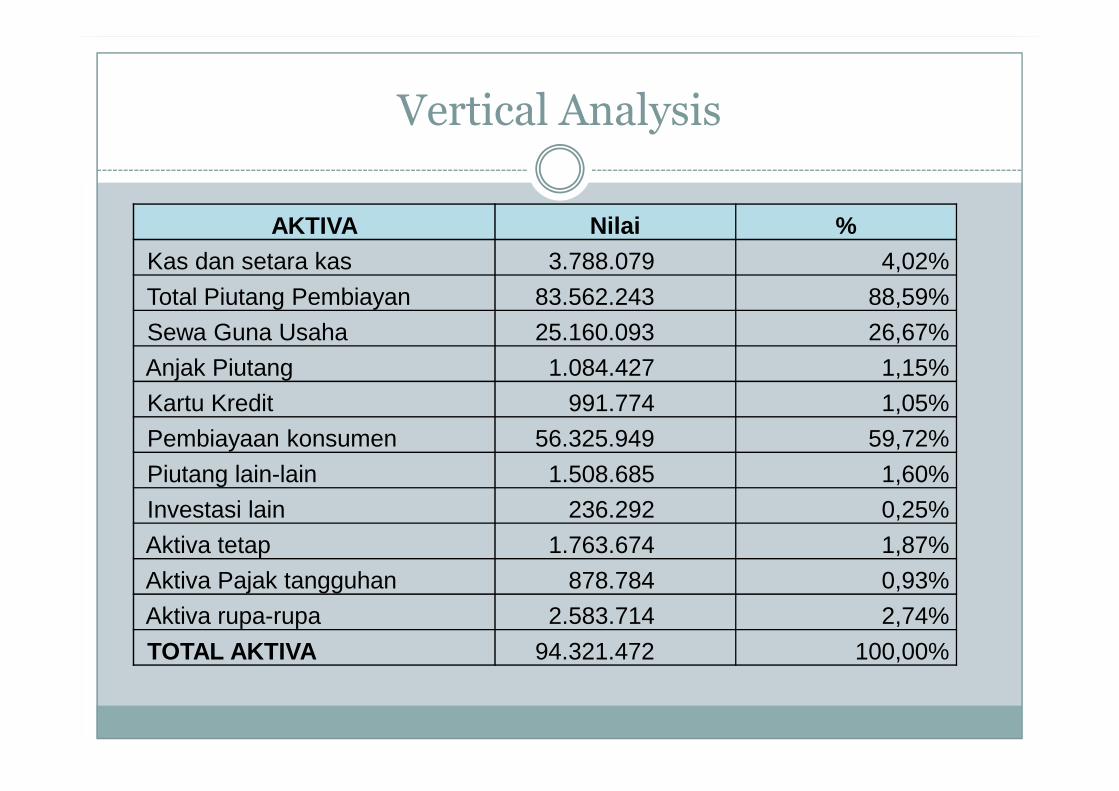

Vertical Analysis

AKTIVA Nilai %Kas dan setara kas 3.788.079 4,02%

Total Piutang Pembiayan 83.562.243 88,59%

Sewa Guna Usaha 25.160.093 26,67%

Anjak Piutang 1.084.427 1,15%

Kartu Kredit 991.774 1,05%Kartu Kredit 991.774 1,05%

Pembiayaan konsumen 56.325.949 59,72%

Piutang lain-lain 1.508.685 1,60%

Investasi lain 236.292 0,25%

Aktiva tetap 1.763.674 1,87%

Aktiva Pajak tangguhan 878.784 0,93%

Aktiva rupa-rupa 2.583.714 2,74%

TOTAL AKTIVA 94.321.472 100,00%

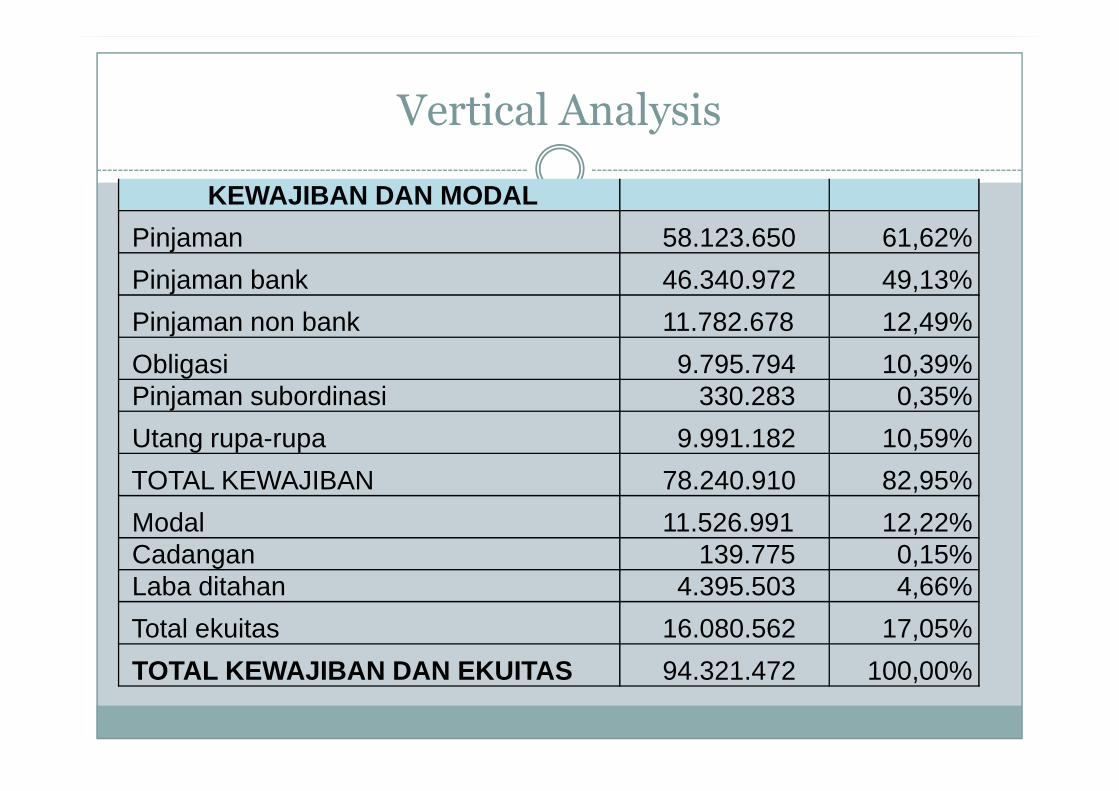

Vertical Analysis

KEWAJIBAN DAN MODAL

Pinjaman 58.123.650 61,62%

Pinjaman bank 46.340.972 49,13%

Pinjaman non bank 11.782.678 12,49%

Obligasi 9.795.794 10,39%Pinjaman subordinasi 330.283 0,35%Pinjaman subordinasi 330.283 0,35%

Utang rupa-rupa 9.991.182 10,59%

TOTAL KEWAJIBAN 78.240.910 82,95%

Modal 11.526.991 12,22%Cadangan 139.775 0,15%Laba ditahan 4.395.503 4,66%

Total ekuitas 16.080.562 17,05%

TOTAL KEWAJIBAN DAN EKUITAS 94.321.472 100,00%

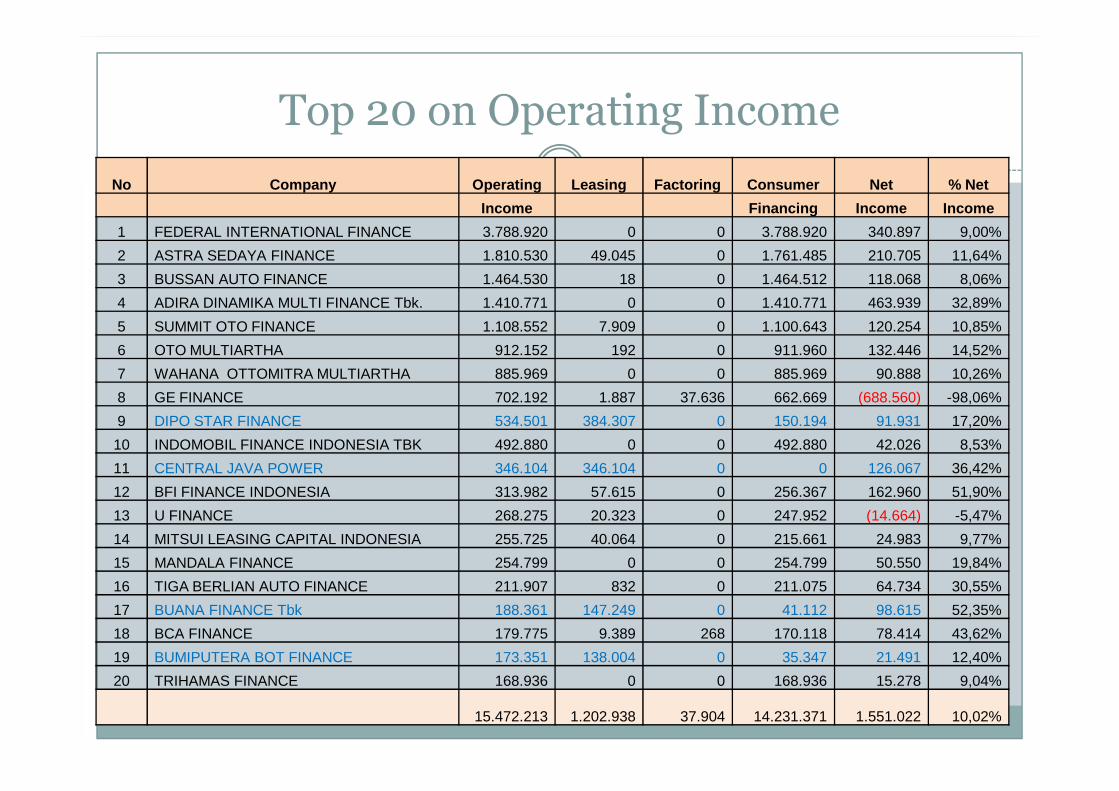

Top 20 on Operating Income

No Company Operating Leasing Factoring Consumer Net % Net

Income Financing Income Income

1 FEDERAL INTERNATIONAL FINANCE 3.788.920 0 0 3.788.920 340.897 9,00%

2 ASTRA SEDAYA FINANCE 1.810.530 49.045 0 1.761.485 210.705 11,64%

3 BUSSAN AUTO FINANCE 1.464.530 18 0 1.464.512 118.068 8,06%

4 ADIRA DINAMIKA MULTI FINANCE Tbk. 1.410.771 0 0 1.410.771 463.939 32,89%

5 SUMMIT OTO FINANCE 1.108.552 7.909 0 1.100.643 120.254 10,85%

6 OTO MULTIARTHA 912.152 192 0 911.960 132.446 14,52%

7 WAHANA OTTOMITRA MULTIARTHA 885.969 0 0 885.969 90.888 10,26%

8 GE FINANCE 702.192 1.887 37.636 662.669 (688.560) -98,06%8 GE FINANCE 702.192 1.887 37.636 662.669 (688.560) -98,06%

9 DIPO STAR FINANCE 534.501 384.307 0 150.194 91.931 17,20%

10 INDOMOBIL FINANCE INDONESIA TBK 492.880 0 0 492.880 42.026 8,53%

11 CENTRAL JAVA POWER 346.104 346.104 0 0 126.067 36,42%

12 BFI FINANCE INDONESIA 313.982 57.615 0 256.367 162.960 51,90%

13 U FINANCE 268.275 20.323 0 247.952 (14.664) -5,47%

14 MITSUI LEASING CAPITAL INDONESIA 255.725 40.064 0 215.661 24.983 9,77%

15 MANDALA FINANCE 254.799 0 0 254.799 50.550 19,84%

16 TIGA BERLIAN AUTO FINANCE 211.907 832 0 211.075 64.734 30,55%

17 BUANA FINANCE Tbk 188.361 147.249 0 41.112 98.615 52,35%

18 BCA FINANCE 179.775 9.389 268 170.118 78.414 43,62%

19 BUMIPUTERA BOT FINANCE 173.351 138.004 0 35.347 21.491 12,40%

20 TRIHAMAS FINANCE 168.936 0 0 168.936 15.278 9,04%

15.472.213 1.202.938 37.904 14.231.371 1.551.022 10,02%

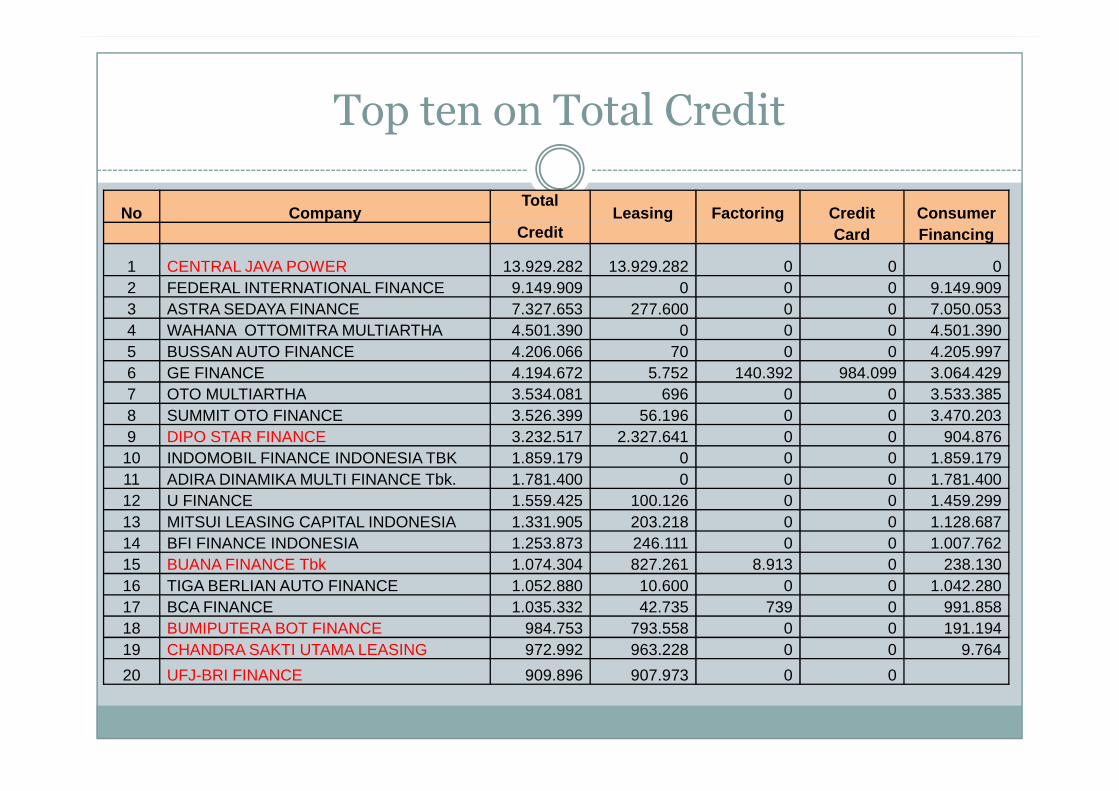

Top ten on Total Credit

No CompanyTotal

Leasing Factoring Credit ConsumerCredit Card Financing

1 CENTRAL JAVA POWER 13.929.282 13.929.282 0 0 0 2 FEDERAL INTERNATIONAL FINANCE 9.149.909 0 0 0 9.149.909 3 ASTRA SEDAYA FINANCE 7.327.653 277.600 0 0 7.050.053 4 WAHANA OTTOMITRA MULTIARTHA 4.501.390 0 0 0 4.501.390 5 BUSSAN AUTO FINANCE 4.206.066 70 0 0 4.205.997 6 GE FINANCE 4.194.672 5.752 140.392 984.099 3.064.429 7 OTO MULTIARTHA 3.534.081 696 0 0 3.533.385 7 OTO MULTIARTHA 3.534.081 696 0 0 3.533.385 8 SUMMIT OTO FINANCE 3.526.399 56.196 0 0 3.470.203 9 DIPO STAR FINANCE 3.232.517 2.327.641 0 0 904.876

10 INDOMOBIL FINANCE INDONESIA TBK 1.859.179 0 0 0 1.859.179 11 ADIRA DINAMIKA MULTI FINANCE Tbk. 1.781.400 0 0 0 1.781.400 12 U FINANCE 1.559.425 100.126 0 0 1.459.299 13 MITSUI LEASING CAPITAL INDONESIA 1.331.905 203.218 0 0 1.128.687 14 BFI FINANCE INDONESIA 1.253.873 246.111 0 0 1.007.762 15 BUANA FINANCE Tbk 1.074.304 827.261 8.913 0 238.130 16 TIGA BERLIAN AUTO FINANCE 1.052.880 10.600 0 0 1.042.280 17 BCA FINANCE 1.035.332 42.735 739 0 991.858 18 BUMIPUTERA BOT FINANCE 984.753 793.558 0 0 191.194 19 CHANDRA SAKTI UTAMA LEASING 972.992 963.228 0 0 9.764

20 UFJ-BRI FINANCE 909.896 907.973 0 0

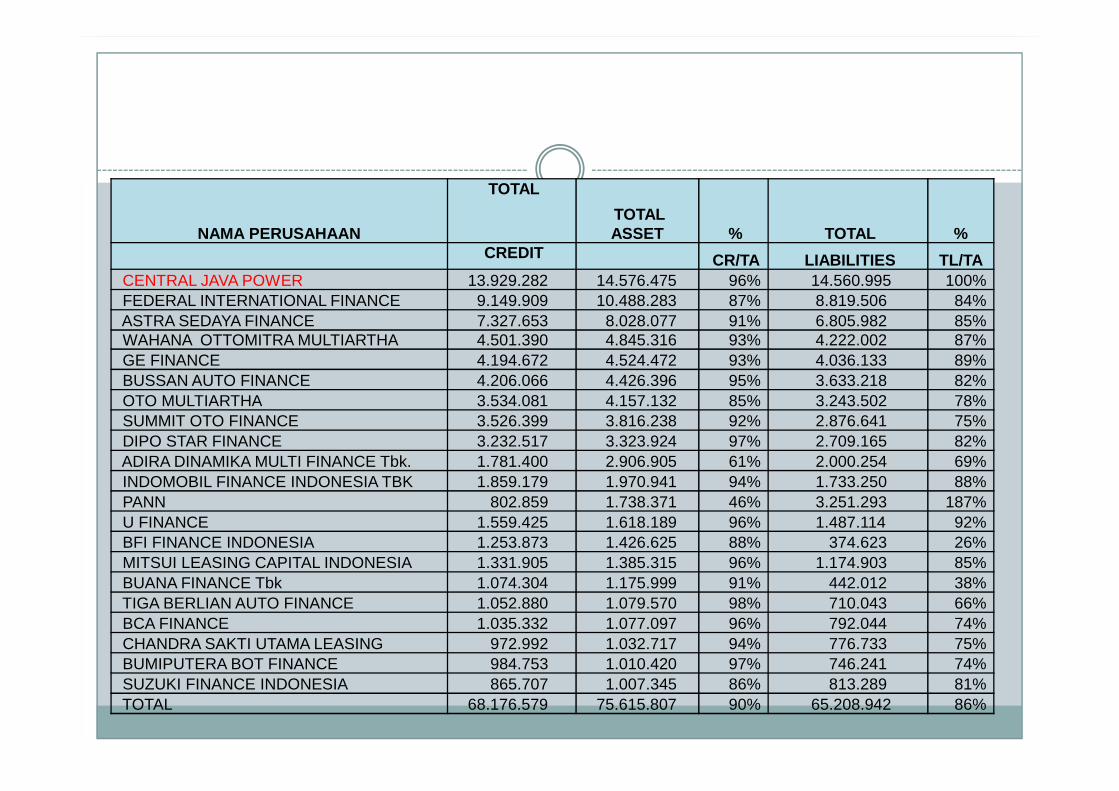

NAMA PERUSAHAAN

TOTAL

TOTAL ASSET % TOTAL %

CREDIT CR/TA LIABILITIES TL/TACENTRAL JAVA POWER 13.929.282 14.576.475 96% 14.560.995 100%FEDERAL INTERNATIONAL FINANCE 9.149.909 10.488.283 87% 8.819.506 84%ASTRA SEDAYA FINANCE 7.327.653 8.028.077 91% 6.805.982 85%WAHANA OTTOMITRA MULTIARTHA 4.501.390 4.845.316 93% 4.222.002 87%GE FINANCE 4.194.672 4.524.472 93% 4.036.133 89%BUSSAN AUTO FINANCE 4.206.066 4.426.396 95% 3.633.218 82%OTO MULTIARTHA 3.534.081 4.157.132 85% 3.243.502 78%OTO MULTIARTHA 3.534.081 4.157.132 85% 3.243.502 78%SUMMIT OTO FINANCE 3.526.399 3.816.238 92% 2.876.641 75%DIPO STAR FINANCE 3.232.517 3.323.924 97% 2.709.165 82%ADIRA DINAMIKA MULTI FINANCE Tbk. 1.781.400 2.906.905 61% 2.000.254 69%INDOMOBIL FINANCE INDONESIA TBK 1.859.179 1.970.941 94% 1.733.250 88%PANN 802.859 1.738.371 46% 3.251.293 187%U FINANCE 1.559.425 1.618.189 96% 1.487.114 92%BFI FINANCE INDONESIA 1.253.873 1.426.625 88% 374.623 26%MITSUI LEASING CAPITAL INDONESIA 1.331.905 1.385.315 96% 1.174.903 85%BUANA FINANCE Tbk 1.074.304 1.175.999 91% 442.012 38%TIGA BERLIAN AUTO FINANCE 1.052.880 1.079.570 98% 710.043 66%BCA FINANCE 1.035.332 1.077.097 96% 792.044 74%CHANDRA SAKTI UTAMA LEASING 972.992 1.032.717 94% 776.733 75%BUMIPUTERA BOT FINANCE 984.753 1.010.420 97% 746.241 74%SUZUKI FINANCE INDONESIA 865.707 1.007.345 86% 813.289 81%TOTAL 68.176.579 75.615.807 90% 65.208.942 86%

LISTED COMPANIES

Adira Dinamika Multi Finance TbkBuana Finance TbkBFI Finance Indonesia TbkClipan Finance Indonesia TbkDanasupra Erapacific Tbk *)Danasupra Erapacific Tbk *)Indocitra Finance TbkMandala Multifinance TbkTrust Finance Indonesia TbkWahana Ottomitra Multiartha

Reconcilitaion Fiscal Analysis

� Permanent Difference

� Final tax income – deposito

� Temporer Difference

Allowance for doubtfull account� Allowance for doubtfull account

� Amortization of income on sale and lease back

� Amortization of acquisition cost (main)

� Depreciation expense

Survey Data - Susenas

� Finance company included small company

� Cooperation

� BMT

� LKM (Lembaga Kredit Masyarakat)

� KUD (Koperasi Unit Desa)� KUD (Koperasi Unit Desa)

� Simpan Pinjam

Reference

� Zulverdi, Doddy, Ferry Syarifuddin dan Tri Yanuarti, (2005) Consumer Finance and Household Indebtedness: The Case of Indonesia, Occasional Paper No 01, Bank Indonesia.

� Expansion of multi-finance industry predicted to slow � Expansion of multi-finance industry predicted to slow down.(FINANCE), http://www.highbeam.com/doc/1G1-141997972.html viewed 5 Oct 2008

� Multi-finance industry shining the brighter.(INDUSTRY PROFILE) http://www.highbeam.com/doc/1G1-177590189.html, viewed 5 Oct 2008.