Embed Size (px)

Citation preview

Muge TianYanlei XuBen Hier

Mohamed Ibrahim

November 29, 2007

2

Agenda

Company Overview Macroeconomic Outlook Industry Competitors Recent Developments Portfolio Position DCF Valuation Comparable Multiple Valuation Recommendation

3

Company Overview Incorporated as an Illinois corporation in 1909, as a successor to a

business founded in 1901 Nation’s largest retail drugstore chain (based on sales) 33rd year of consecutive sales and earnings growth Sales are expected to continue to grow

• Aging population• Introduction of lower priced generics• Development of innovative drugs

Convenience positioning: 139.1 million people live within 2 miles Traffic: 5 million shoppers in one store location daily As of Aug 31,2007, 5997 stores located in 48 states and Puerto

Rico.

4

Prescription Drugs

Non-Prescription Drugs

Beauty Care

Personal Care

Household Items

Photofinishing

Greeting Cards

Candy

Seasonal Items

Convenience Foods

Walgreens’ Business

Walgreens

5

Product Class

Percentage

2007 2006 2005

Prescription Drugs 65 64 64

Non-Prescription Drugs 10 11 11

General Merchandise 25 25 25

Total Sales 100 100 100

6

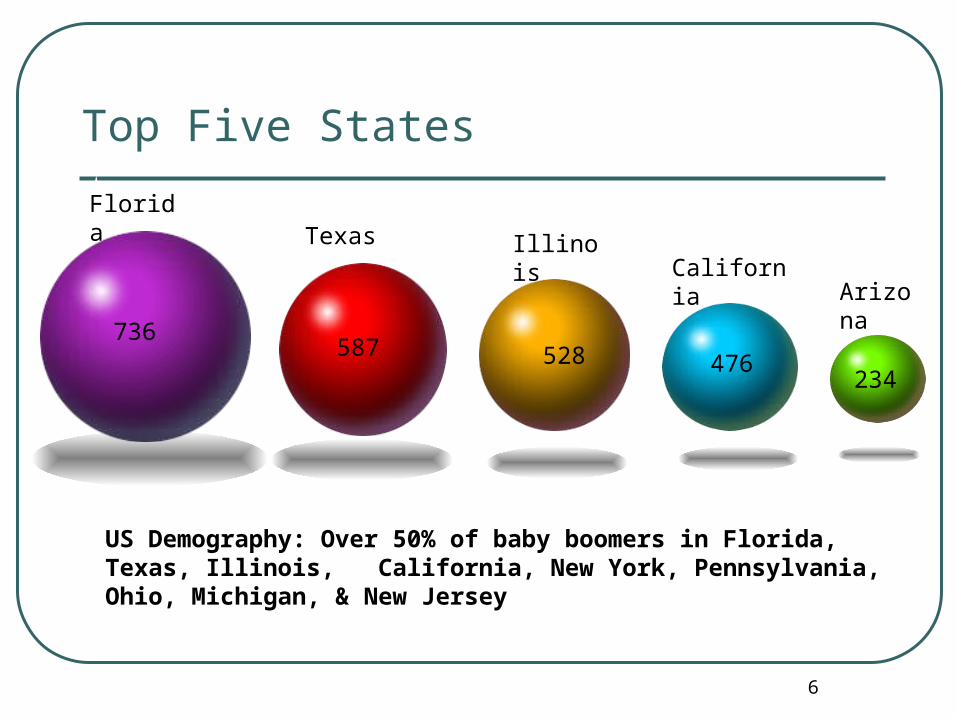

2010~2011

587

California

Florida

528

US Demography: Over 50% of baby boomers in Florida, Texas, Illinois, California, New York, Pennsylvania, Ohio, Michigan, & New Jersey

736

Texas Illinois

476

Arizona

234

Top Five States

7

Growth Strategy

• Store openings• Locating new stores, relocating/closing exiting

stores, site selection (convenience positioning)

• 2007, opened or acquired 563 stores.

• Continue growth, anticipating more than 7000 locations in 2010.

8

Acquisitions In 2006 :

• Merger with Happy Harry’s pharmacy chain

• Purchase of :• Medmark Inc. ( Specialty pharmacy )

• Schraft’s ( Specialty pharmacy)

• Canadian Valley medical ( Home care services)

• Home pharmacy of California (home infusion service)

• Controlling interest in Senior Med

In 2007 :• Option Care Inc. (specialty pharmacy & home infusion service)

• Take care health systems (convenient care clinic operator)

• Remaining interests in Senior Med.

9

Risk FactorsRisk Factors

CompetitionRegulations

Reduction Reimbursement

WalgreensWalgreens

Pharmacy Personnel

Product Liability

StoreLocation

EconomicCondition

10

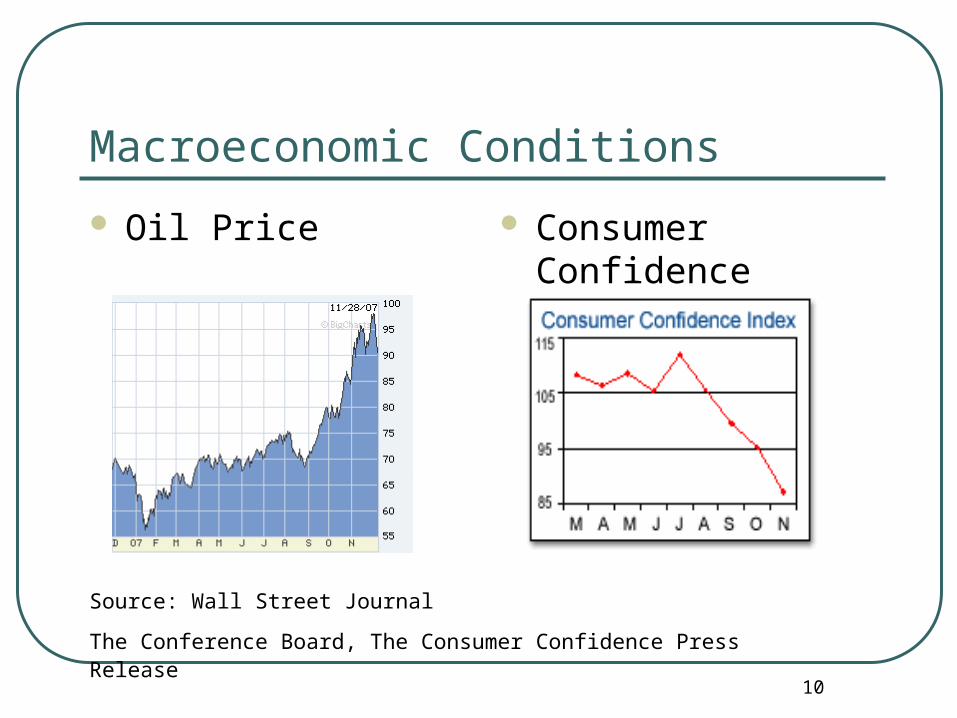

Macroeconomic Conditions

Oil Price Consumer Confidence

Source: Wall Street Journal

The Conference Board, The Consumer Confidence Press Release

11

Industry Overview

• Industry: Drug retail

• CVS/Caremark Corp. (CVS) and Rite Aid Corp. (RAD)

• Business segments: prescription and non-prescription drugs, and general merchandise

12

Industry

Sources and availability of raw materials

• numerous domestic and foreign suppliers Seasonal variation

• timing and severity of cold/flu season, holidays Dependence upon limited number of customers

• no customers counts for 10% or more of consolidated sales Competition

• chain and independent drug stores, mail order prescription providers, grocery stores, convenient stores, mass merchants, and dollar stores

• service, convenience, variety and price

13

5-Year Industry

14

1-Year Stock Performance

15

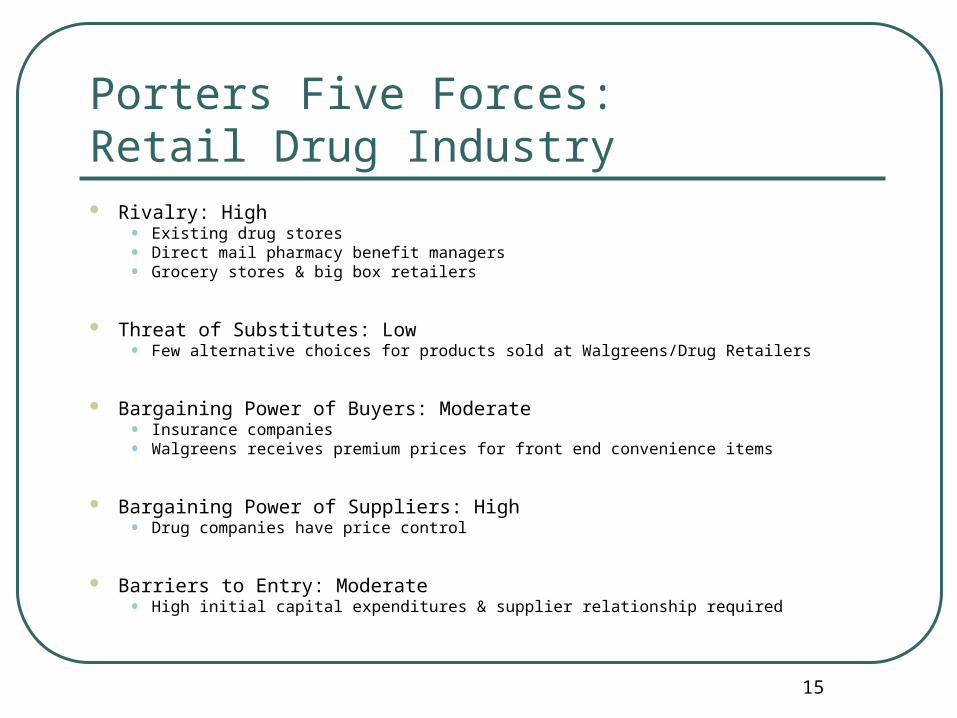

Porters Five Forces: Retail Drug Industry Rivalry: High

• Existing drug stores• Direct mail pharmacy benefit managers• Grocery stores & big box retailers

Threat of Substitutes: Low• Few alternative choices for products sold at Walgreens/Drug Retailers

Bargaining Power of Buyers: Moderate• Insurance companies• Walgreens receives premium prices for front end convenience items

Bargaining Power of Suppliers: High• Drug companies have price control

Barriers to Entry: Moderate• High initial capital expenditures & supplier relationship required

16

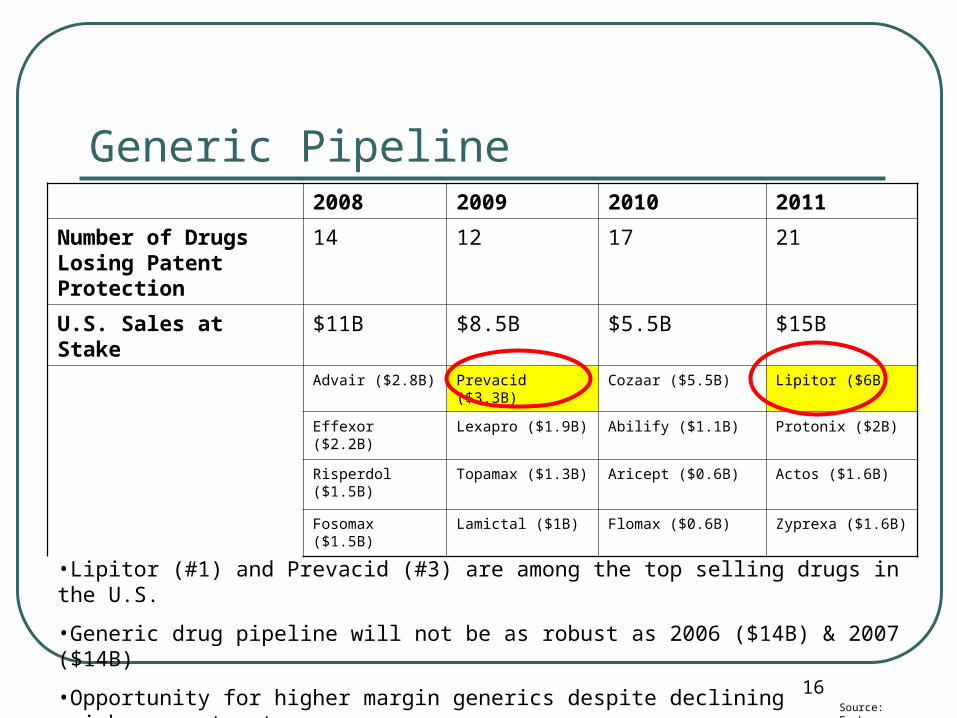

Generic Pipeline2008 2009 2010 2011

Number of Drugs Losing Patent Protection

14 12 17 21

U.S. Sales at Stake $11B $8.5B $5.5B $15B

Advair ($2.8B) Prevacid ($3.3B) Cozaar ($5.5B) Lipitor ($6B)

Effexor ($2.2B) Lexapro ($1.9B) Abilify ($1.1B) Protonix ($2B)

Risperdol ($1.5B) Topamax ($1.3B) Aricept ($0.6B) Actos ($1.6B)

Fosomax ($1.5B) Lamictal ($1B) Flomax ($0.6B) Zyprexa ($1.6B)

•Lipitor (#1) and Prevacid (#3) are among the top selling drugs in the U.S.

•Generic drug pipeline will not be as robust as 2006 ($14B) & 2007 ($14B)

•Opportunity for higher margin generics despite declining reimbursement rates

Source: Forbes.com

17

Path From Branded to Generic

Stage I

1/1/1995 - 1/1/2007 (Est. 12 Yrs)

•Full Price “Branded” Drug Available

•Low Margin Product

Stage II

1/2/2007 - 6/2/2007

•First Generic Version Available

•6 Month Exclusivity

•Sold at 94% of “Branded” Price

•Insurance Companies Offer High Reimbursement Rates

Stage III

6/2/2007 - Future

•Generic Exclusivity Ends

•Sold at 52% of Branded Price

•Insurance Companies Reduce Reimbursement

18

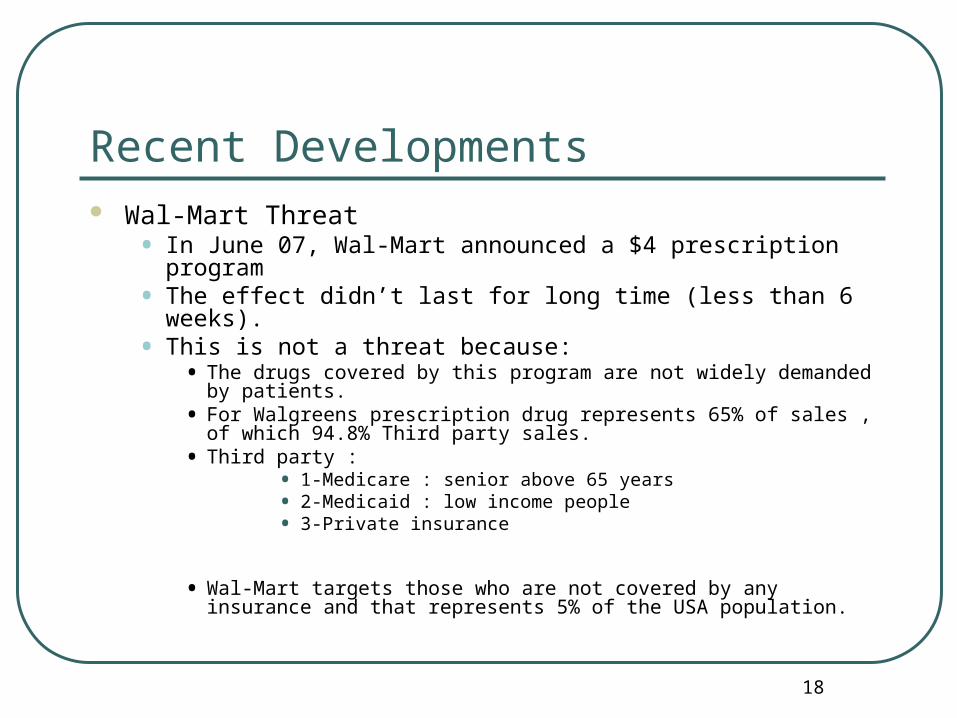

Recent Developments Wal-Mart Threat

• In June 07, Wal-Mart announced a $4 prescription program• The effect didn’t last for long time (less than 6 weeks).• This is not a threat because:

• The drugs covered by this program are not widely demanded by patients.• For Walgreens prescription drug represents 65% of sales , of which 94.8%

Third party sales.• Third party :

• 1-Medicare : senior above 65 years• 2-Medicaid : low income people• 3-Private insurance

• Wal-Mart targets those who are not covered by any insurance and that represents 5% of the USA population.

19

Recent Developments Cont.

On Oct 1st 2007 , Walgreen announced a decline in Q4 earnings by 3.8%. Although the annual data showed an increase in earnings by 16.6%, sales

increased by 13.3%. Walgreen lost 15% ($7.04) on that day. Walgreen is held by many institutional investors, so when Walgreen missed their

expectations, shares sold off abruptly

20

Recent Developments Cont.

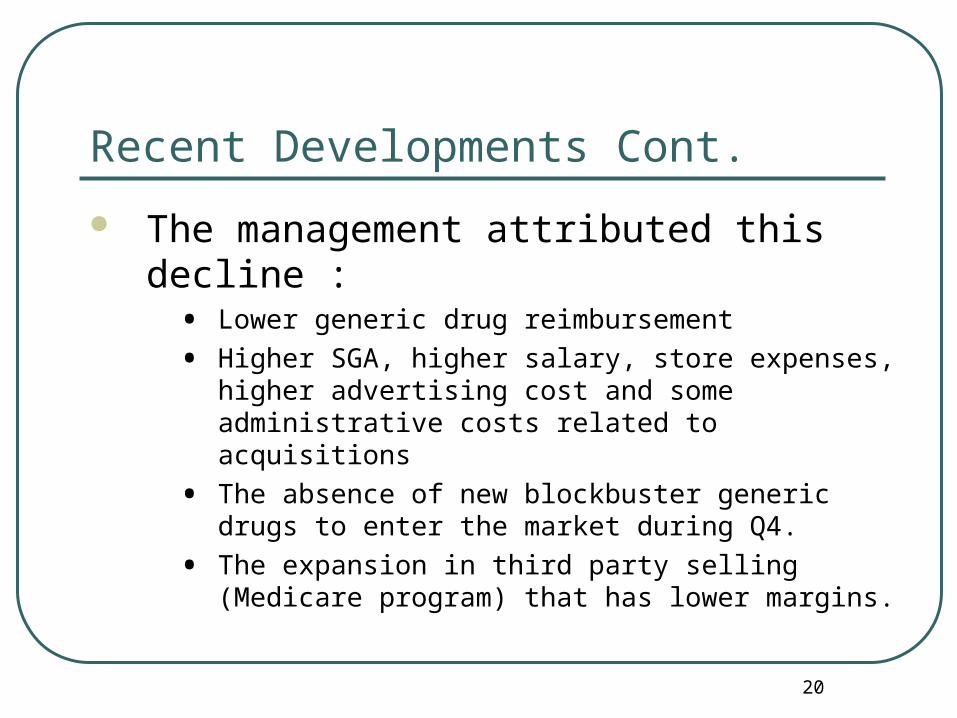

The management attributed this decline :• Lower generic drug reimbursement

• Higher SGA, higher salary, store expenses, higher advertising cost and some administrative costs related to acquisitions

• The absence of new blockbuster generic drugs to enter the market during Q4.

• The expansion in third party selling (Medicare program) that has lower margins.

21

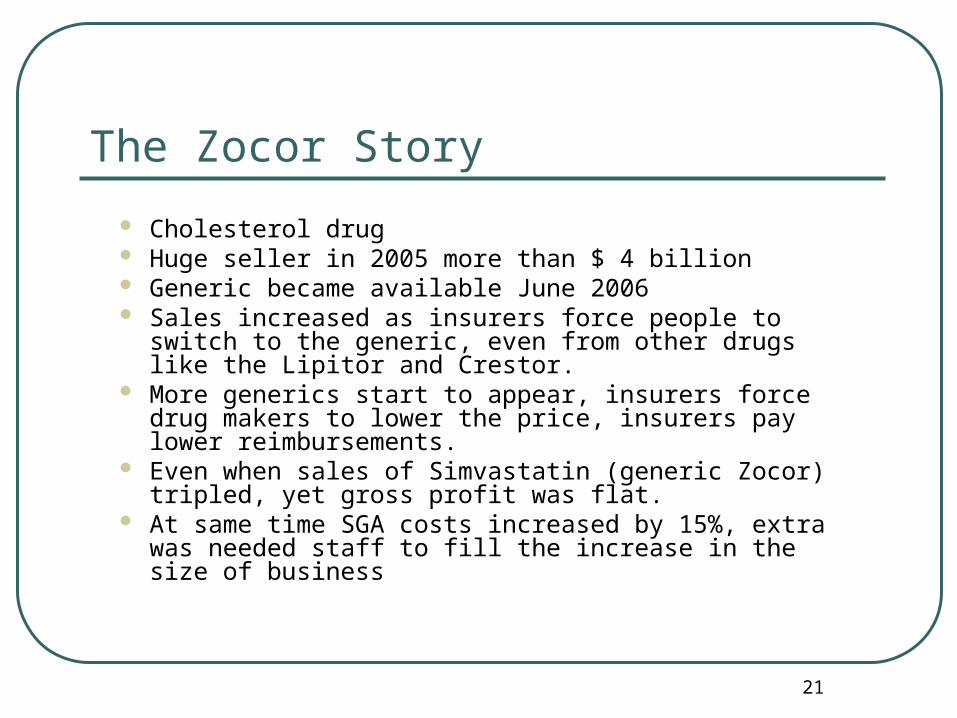

The Zocor Story

Cholesterol drug Huge seller in 2005 more than $ 4 billion Generic became available June 2006 Sales increased as insurers force people to switch to the

generic, even from other drugs like the Lipitor and Crestor.

More generics start to appear, insurers force drug makers to lower the price, insurers pay lower reimbursements.

Even when sales of Simvastatin (generic Zocor) tripled, yet gross profit was flat.

At same time SGA costs increased by 15%, extra was needed staff to fill the increase in the size of business

22

Patent Expiration Schedule

Date Drug Pharmaceutical Company8-Jun-07 Zerit Bristol Mayers Squibb

11-Dec-07 Meredia Abbott Laboratories

25-Dec-07 Zyrtec Pfizer

Jan-08 camptosar Pfizer

6-Feb-08 Fosamax Merck

12-Feb-08 Advair Glaxosmithkline

12-Feb-08 Serevant Glaxosmithkline

1-Oct-08 Casodex AstraZeneca

Jan-10 Lipitor Pfizer

Sep-11 Avapro Bristol Mayers Squibb

Nov-11 Plavix Bristol Mayers Squibb

Jan-13 Orzel Bristol Mayers Squibb

Jan-13 Sustiva Bristol Mayers Squibb

Jan-17 Reyataz Bristol Mayers Squibb

23

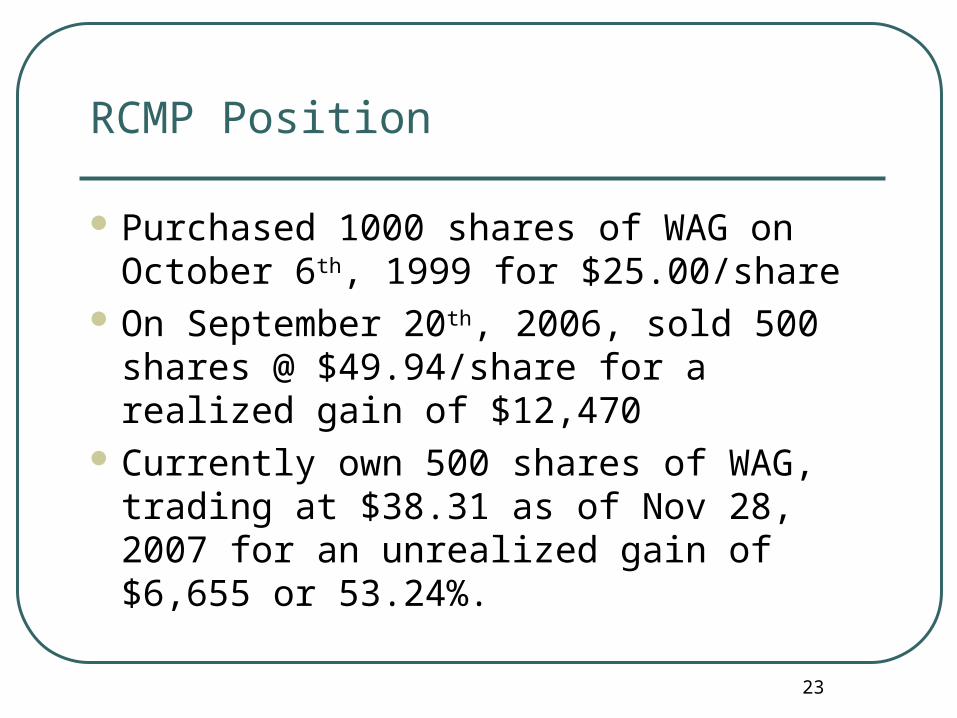

RCMP Position

Purchased 1000 shares of WAG on October 6th, 1999 for $25.00/share

On September 20th, 2006, sold 500 shares @ $49.94/share for a realized gain of $12,470

Currently own 500 shares of WAG, trading at $38.31 as of Nov 28, 2007 for an unrealized gain of $6,655 or 53.24%.

24

Role in Portfolio

25

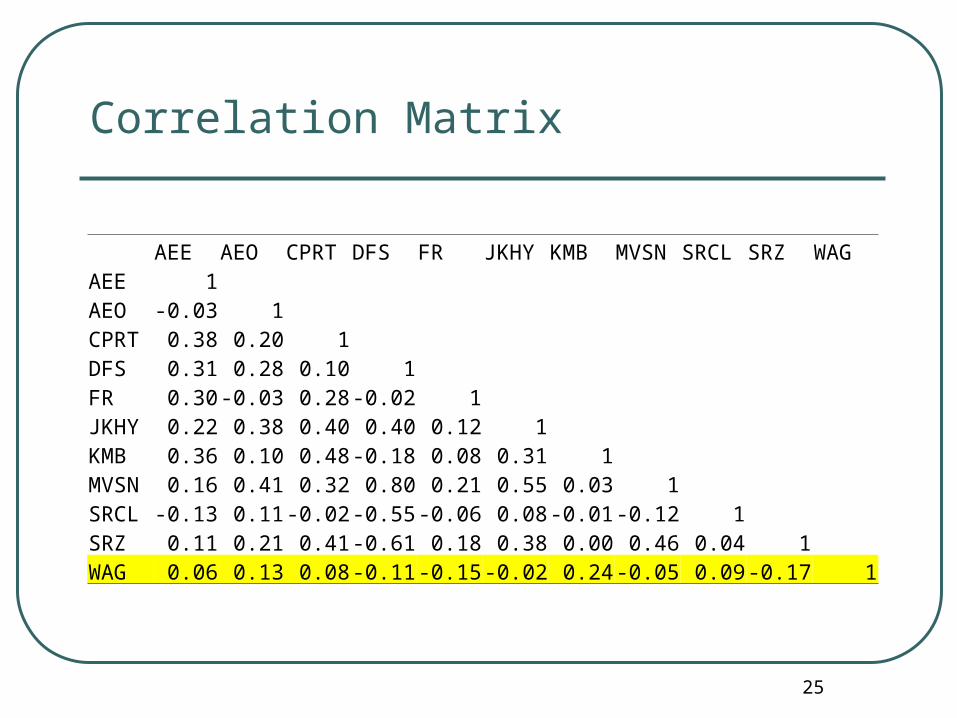

Correlation Matrix

AEE AEO CPRT DFS FR JKHY KMB MVSN SRCL SRZ WAGAEE 1AEO -0.03 1CPRT 0.38 0.20 1DFS 0.31 0.28 0.10 1FR 0.30 -0.03 0.28 -0.02 1JKHY 0.22 0.38 0.40 0.40 0.12 1KMB 0.36 0.10 0.48 -0.18 0.08 0.31 1MVSN 0.16 0.41 0.32 0.80 0.21 0.55 0.03 1SRCL -0.13 0.11 -0.02 -0.55 -0.06 0.08 -0.01 -0.12 1SRZ 0.11 0.21 0.41 -0.61 0.18 0.38 0.00 0.46 0.04 1WAG 0.06 0.13 0.08 -0.11 -0.15 -0.02 0.24 -0.05 0.09 -0.17 1

26

Lease Obligations

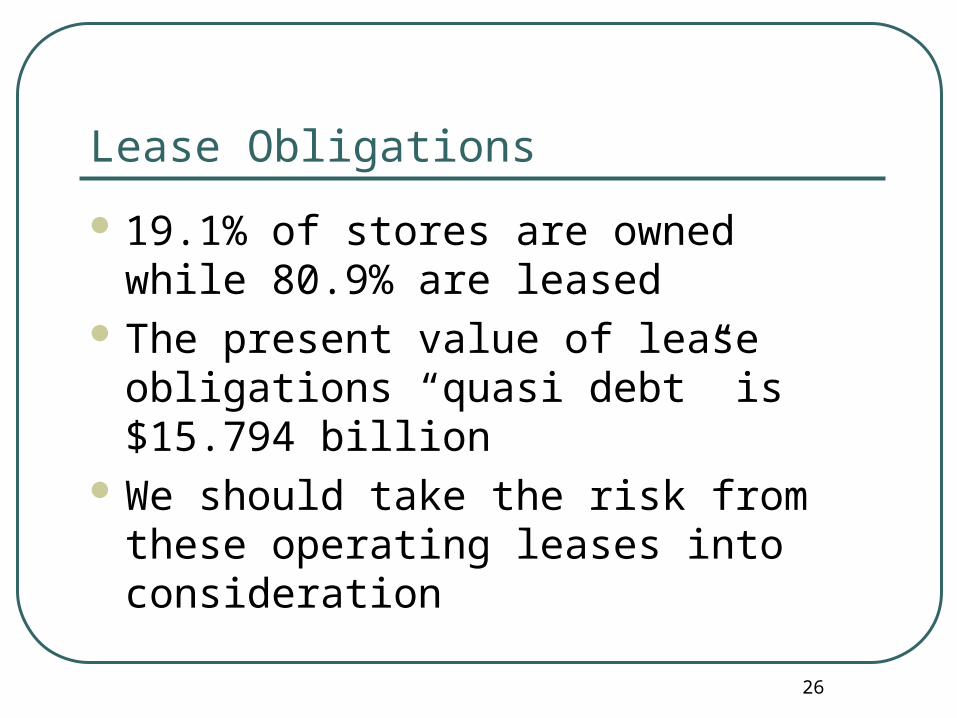

19.1% of stores are owned while 80.9% are leased

The present value of lease obligations “quasi debt” is $15.794 billion

We should take the risk from these operating leases into consideration

27

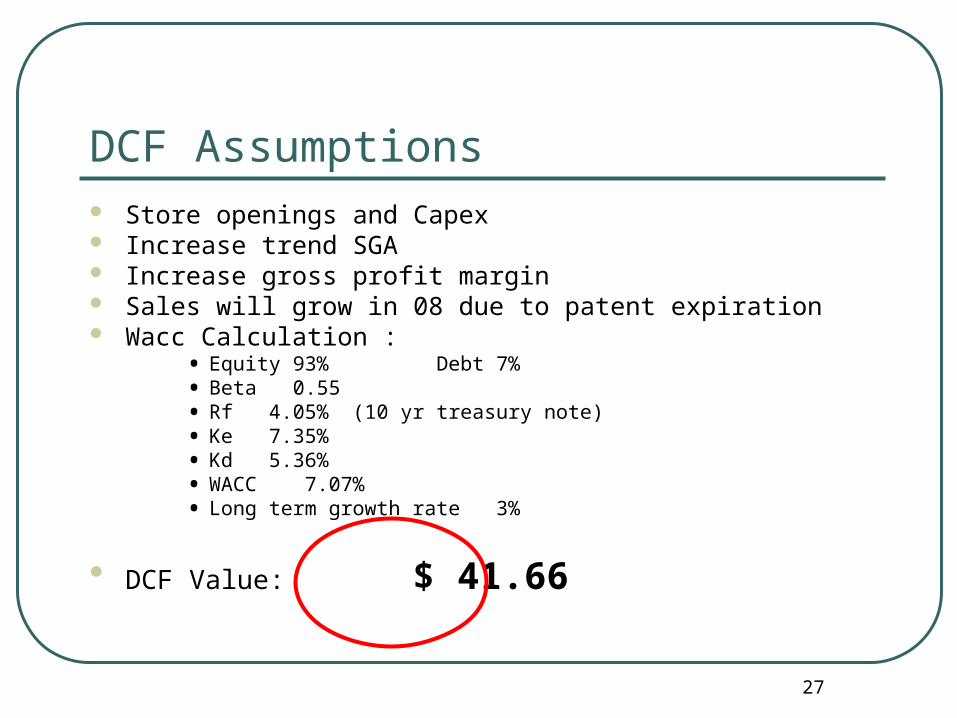

DCF Assumptions Store openings and Capex Increase trend SGA Increase gross profit margin Sales will grow in 08 due to patent expiration Wacc Calculation :

• Equity 93% Debt 7%• Beta 0.55• Rf 4.05% (10 yr treasury note)• Ke 7.35%• Kd 5.36%• WACC 7.07%• Long term growth rate 3%

DCF Value: $ 41.66

28

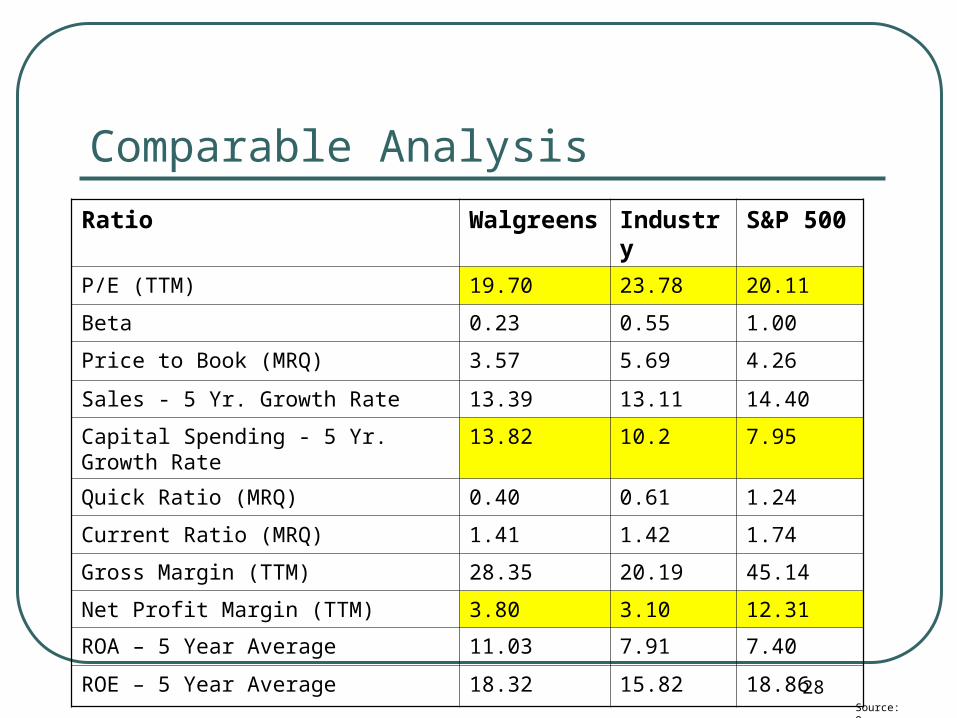

Comparable Analysis

Ratio Walgreens Industry S&P 500

P/E (TTM) 19.70 23.78 20.11

Beta 0.23 0.55 1.00

Price to Book (MRQ) 3.57 5.69 4.26

Sales - 5 Yr. Growth Rate 13.39 13.11 14.40

Capital Spending - 5 Yr. Growth Rate 13.82 10.2 7.95

Quick Ratio (MRQ) 0.40 0.61 1.24

Current Ratio (MRQ) 1.41 1.42 1.74

Gross Margin (TTM) 28.35 20.19 45.14

Net Profit Margin (TTM) 3.80 3.10 12.31

ROA – 5 Year Average 11.03 7.91 7.40

ROE – 5 Year Average 18.32 15.82 18.86

Source: Onesource

29

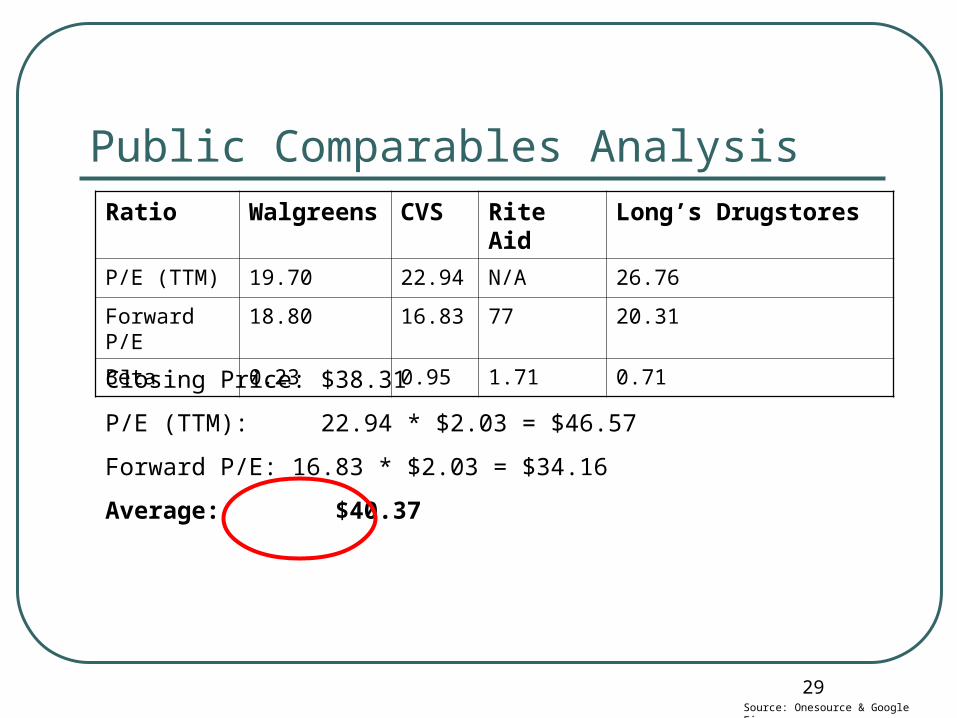

Public Comparables AnalysisRatio Walgreens CVS Rite Aid Long’s Drugstores

P/E (TTM) 19.70 22.94 N/A 26.76

Forward P/E 18.80 16.83 77 20.31

Beta 0.23 0.95 1.71 0.71

Source: Onesource & Google Finance

Closing Price: $38.31

P/E (TTM): 22.94 * $2.03 = $46.57

Forward P/E: 16.83 * $2.03 = $34.16

Average: $40.37

30

Recommendation

Hold 500 Shares• DCF valuation near current stock price

• Generic drug outlook not as robust as 2006-07

• Low correlation to existing portfolio holdings

• Macroeconomic outlook

![[Typ hier] [Typ hier] [Typ hier] - Kees van der Westen · INSTALLATION MANUAL - resume Slim Jim Installation manual page 3 Installation resume Check location 1. Check water quality](https://img.pdfslide.us/doc/110x75/5f1306afc9765c030046c97c/typ-hier-typ-hier-typ-hier-kees-van-der-installation-manual-resume-slim.jpg)

![[Typ hier] [Typ hier] [Typ hier] - Kees van der Westen · Odour and colour clean*, fresh*, odour free*, clear* Taste influencing organic compounds*# Chlorine#, Hypochlorite#, Chloramines#](https://img.pdfslide.us/doc/110x75/5f8c9d514eb2774b9d1c3c27/typ-hier-typ-hier-typ-hier-kees-van-der-westen-odour-and-colour-clean.jpg)

![[Hier klicken und Adresse eingeben]](https://img.pdfslide.us/doc/110x75/62d387108826e22bc0079c00/hier-klicken-und-adresse-eingeben.jpg)