Embed Size (px)

DESCRIPTION

Case Analysis

Citation preview

CROSSING BORDERS: MTC’S JOURNEY THROUGH AFRICA

Group 7 Section B

PGP/16/037

PRIYANK BAVISHI

PGP/16/084

KANUPRIYA TIBREWAL

PGP/16/108

SATNAM SINGH WADHWA

PGP/16/118

VISHWAS ANAND

PGP/16/212

NAGENDRA SINGH

PGP/16/009

VAIBHAV SHARMA

MTC : An OverviewLeading player in telecommunication market of Middle-East

MTC acquired Celtel, leading telecom operator in sub-Saharan Africa

Since 2002 – fastest growing global wireless telecom operator in the world

MTC’s culture – relationship oriented rather than formalized

27million subscribers, $2 billion in EBITDA and a market cap of around $18 billionMTC want to reach 70 million subscribers, $6 billion in EBITDA and $30 billion in market capitalization by 2011

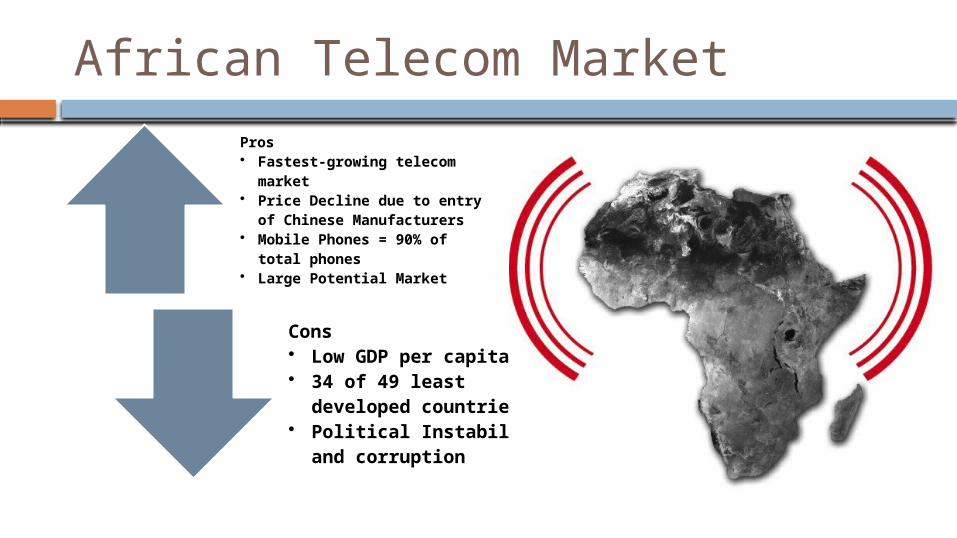

African Telecom MarketPros• Fastest-growing telecom

market• Price Decline due to entry

of Chinese Manufacturers• Mobile Phones = 90% of

total phones• Large Potential Market

Cons• Low GDP per capita• 34 of 49 least

developed countries• Political Instability

and corruption

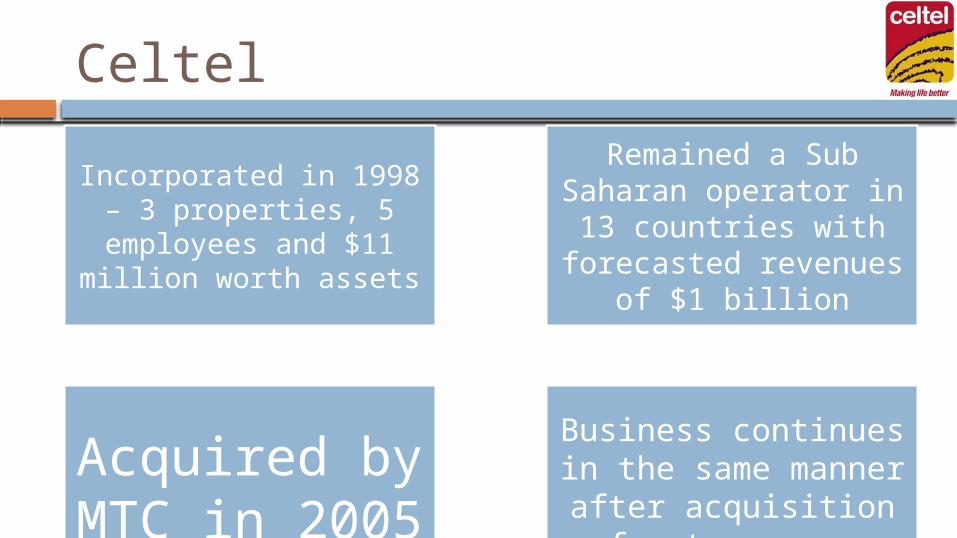

Celtel

Incorporated in 1998 – 3 properties, 5

employees and $11 million worth assets

Remained a Sub Saharan operator in

13 countries with forecasted revenues

of $1 billion

Acquired by MTC in 2005

Business continues in the same manner after acquisition for

two years

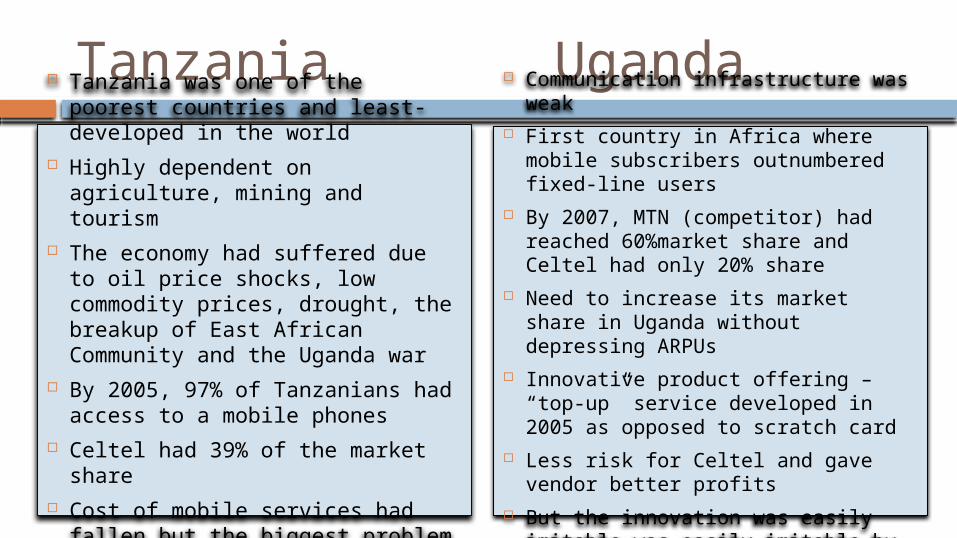

Tanzania Uganda Tanzania was one of the poorest

countries and least-developed in the world

Highly dependent on agriculture, mining and tourism

The economy had suffered due to oil price shocks, low commodity prices, drought, the breakup of East African Community and the Uganda war

By 2005, 97% of Tanzanians had access to a mobile phones

Celtel had 39% of the market share Cost of mobile services had fallen

but the biggest problem was high connection charges

Communication infrastructure was weak

First country in Africa where mobile subscribers outnumbered fixed-line users

By 2007, MTN (competitor) had reached 60%market share and Celtel had only 20% share

Need to increase its market share in Uganda without depressing ARPUs

Innovative product offering – “top-up” service developed in 2005 as opposed to scratch card

Less risk for Celtel and gave vendor better profits

But the innovation was easily imitable was easily imitable by competitors

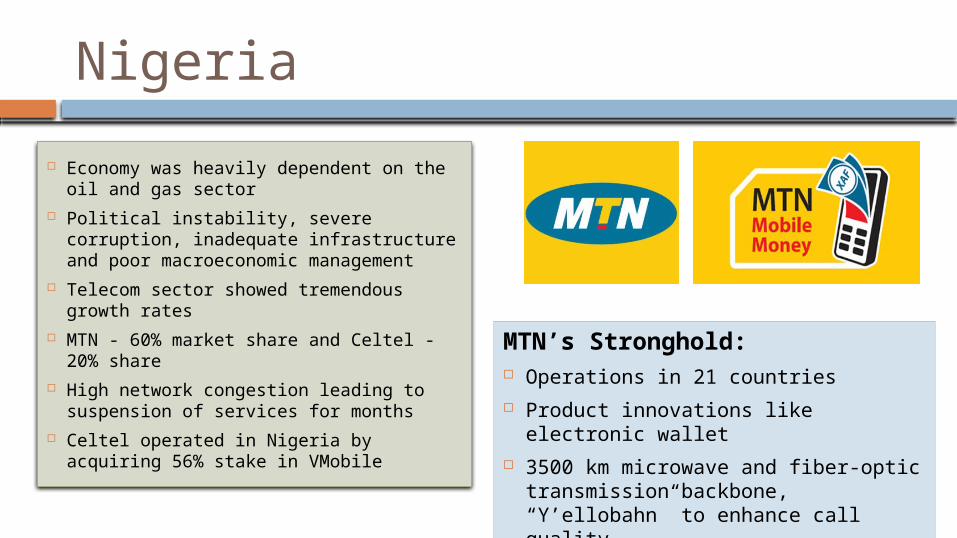

Nigeria

Economy was heavily dependent on the oil and gas sector

Political instability, severe corruption, inadequate infrastructure and poor macroeconomic management

Telecom sector showed tremendous growth rates

MTN - 60% market share and Celtel - 20% share

High network congestion leading to suspension of services for months

Celtel operated in Nigeria by acquiring 56% stake in VMobile

MTN’s Stronghold: Operations in 21 countries Product innovations like electronic

wallet 3500 km microwave and fiber-optic

transmission backbone, “Y’ellobahn” to enhance call quality

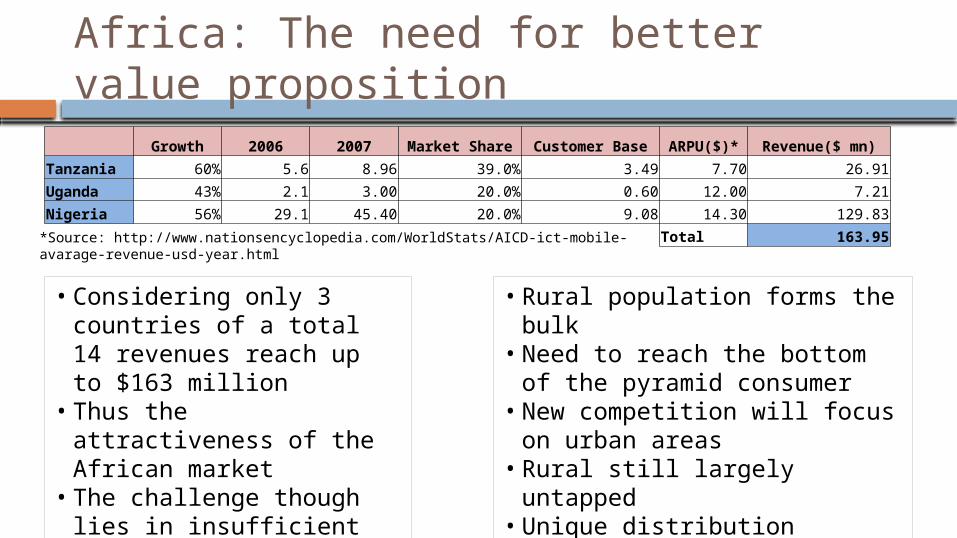

Africa: The need for better value proposition

Growth 2006 2007 Market Share Customer Base ARPU($)* Revenue($ mn)

Tanzania 60% 5.6 8.96 39.0% 3.49 7.70 26.91

Uganda 43% 2.1 3.00 20.0% 0.60 12.00 7.21

Nigeria 56% 29.1 45.40 20.0% 9.08 14.30 129.83

Total 163.95*Source: http://www.nationsencyclopedia.com/WorldStats/AICD-ict-mobile-avarage-revenue-usd-year.html

• Considering only 3 countries of a total 14 revenues reach up to $163 million

• Thus the attractiveness of the African market

• The challenge though lies in insufficient infrastructure and increasing competition

• Rural population forms the bulk• Need to reach the bottom of

the pyramid consumer• New competition will focus on

urban areas• Rural still largely untapped• Unique distribution channels –

mobile vendors and product innovations

“Zain” for All?

MTC wanted to rebrand all the companies under the group as a single entity

The idea – reflect a single, strong and unique identity Zain was chosen from a list of more than 400 options Had positive connotations in various languages and

had the potential to be successful across a global audience

But what about Celtel’s brand loyalty?? Celtel’s slogan – “Celtel. Making Life Better”

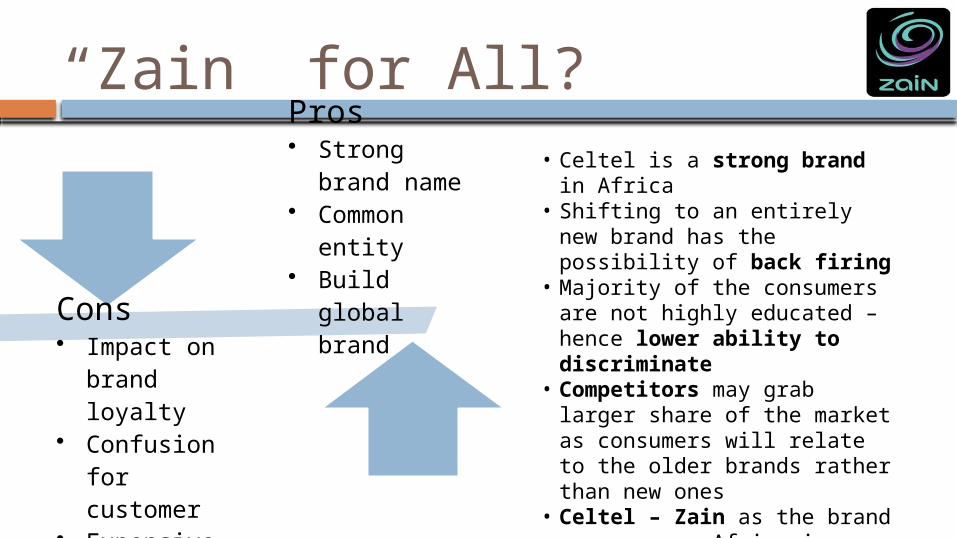

“Zain” for All?Pros• Strong

brand name• Common

entity• Build global

brandCons• Impact on

brand loyalty

• Confusion for customer

• Expensive

• Celtel is a strong brand in Africa

• Shifting to an entirely new brand has the possibility of back firing

• Majority of the consumers are not highly educated – hence lower ability to discriminate

• Competitors may grab larger share of the market as consumers will relate to the older brands rather than new ones

• Celtel – Zain as the brand name across Africa is a viable option

• Across Middle East where population is mature Zain can be used

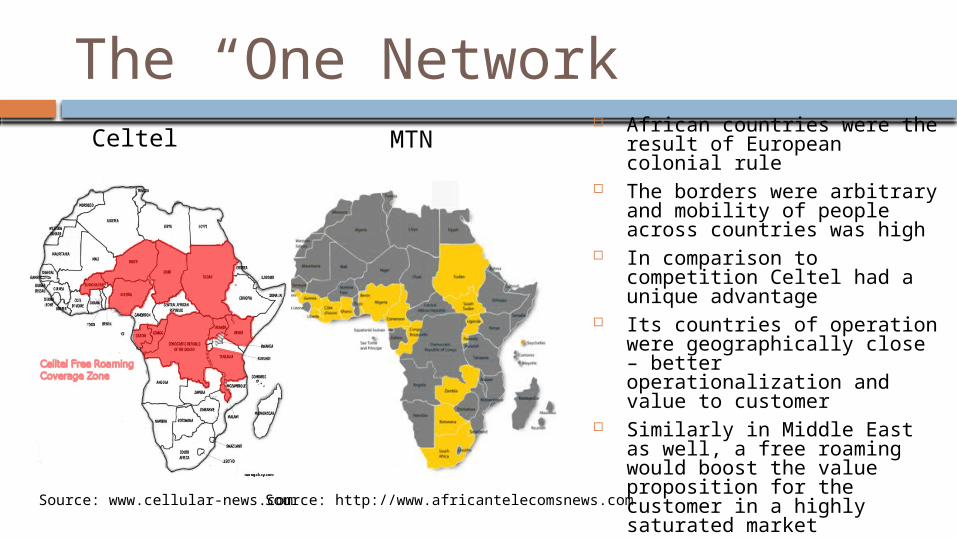

The “One Network”

Source: http://www.africantelecomsnews.comSource: www.cellular-news.com

Celtel MTN African countries were the

result of European colonial rule The borders were arbitrary and

mobility of people across countries was high

In comparison to competition Celtel had a unique advantage

Its countries of operation were geographically close – better operationalization and value to customer

Similarly in Middle East as well, a free roaming would boost the value proposition for the customer in a highly saturated market

Both middle east and Africa are Islamic regions – one network across the two is another competitive advantage – Pilgrims visiting during Hajj season

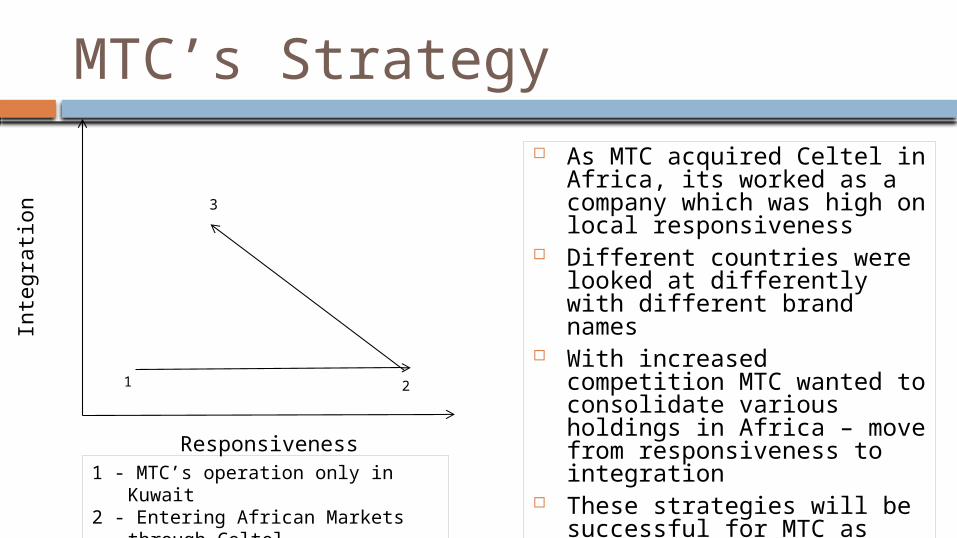

MTC’s Strategy

1 2

3

Responsiveness

Inte

gra

tion

As MTC acquired Celtel in Africa, its worked as a company which was high on local responsiveness

Different countries were looked at differently with different brand names

With increased competition MTC wanted to consolidate various holdings in Africa – move from responsiveness to integration

These strategies will be successful for MTC as they create value for its customers

1 - MTC’s operation only in Kuwait2 - Entering African Markets through

Celtel3 - Zain and One Network Startegies

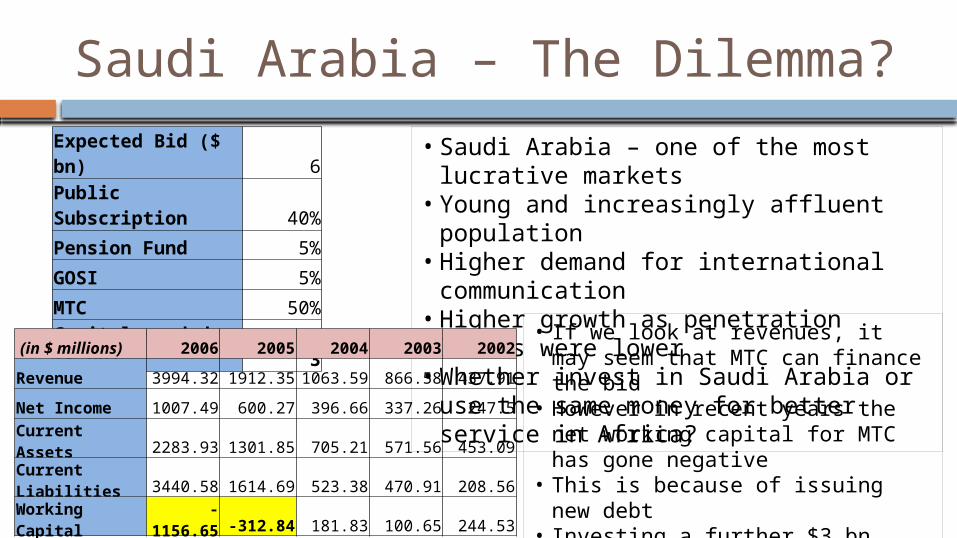

Saudi Arabia – The Dilemma?Expected Bid ($ bn) 6

Public Subscription 40%

Pension Fund 5%

GOSI 5%

MTC 50%

Capital needed ($ bn) 3

• Saudi Arabia – one of the most lucrative markets

• Young and increasingly affluent population

• Higher demand for international communication

• Higher growth as penetration levels were lower

• Whether invest in Saudi Arabia or use the same money for better service in Africa?

(in $ millions) 2006 2005 2004 2003 2002

Revenue 3994.32 1912.35 1063.59 866.58 437.91

Net Income 1007.49 600.27 396.66 337.26 247.5

Current Assets 2283.93 1301.85 705.21 571.56 453.09

Current Liabilities 3440.58 1614.69 523.38 470.91 208.56

Working Capital -1156.65 -312.84 181.83 100.65 244.53

• If we look at revenues, it may seem that MTC can finance the bid

• However in recent years the net working capital for MTC has gone negative

• This is because of issuing new debt• Investing a further $3 bn will strain

the working capital

Recommendations Bringing all companies under one brand has its pros and cons. It will

work in middle east but in Africa may lead to loss of customer base Hence Celtel should be retained in African countries One network plan though imitable by competition will be most

successful for MTC due to its advantageous geographic coverage Efforts can be put in to cover not only the African countries but Middle

East as well in the one network plan Saudi Arabia is definitely a lucrative market nut considering the current

financial position with huge negative capital, an investment worth $3 billion will be risky for MTC

It is hence advisable that MTC concentrate its efforts in Africa to improve infrastructure and rural reach thus gaining market share

THANK YOU

![Western News-Democrat. (Valentine, Nebraska) 1898-10-06 [p ].€¦ · Stanleys Last Journey to Africa Henry M Stanley made a journey Into inner Africa recently which was perhaps even](https://img.pdfslide.us/doc/110x75/5eaac2c54b613b277b6acde9/western-news-democrat-valentine-nebraska-1898-10-06-p-stanleys-last-journey.jpg)