Embed Size (px)

Citation preview

.

MSI Pension Plan

Summary Plan Description January 1, 2018

U.S. Pension Benefits Book i

TABLE OF CONTENTS ABOUT THE PLAN ............................................................................................................ 1

DETERMINING YOUR ELIGIBILITY AND BENEFIT ........................................................ 2 Step One: Determine Your Eligibility. .......................................................................................... 2 Step Two: Determine Your Portable and Traditional Plan Eligibility. ........................................... 2 Step Three: Select a Beneficiary, If You Have a Portable Plan Benefit. ...................................... 3 Step Four: Identify Your Benefit Service...................................................................................... 3 Step Five: Determine Whether You’re Vested. ............................................................................ 4 Step Six: Know How Your Average Earnings Are Calculated. ..................................................... 4 Step Seven: Understand What Your Compensation Includes. .................................................... 5 Step Eight: Learn How Your Social Security Benefit Is Determined. ........................................... 6 Step Nine: Choose a Benefit Payment Option. ............................................................................ 6

THE PORTABLE PLAN ..................................................................................................... 8 Preserving Your Frozen Benefit Amount ..................................................................................... 8 Receiving Your Portable Plan Benefit ......................................................................................... 9 Other Portable Plan Information ................................................................................................ 10

THE TRADITIONAL PLAN ............................................................................................... 14 Portable Plan Participants: Take Note ....................................................................................... 14 Receiving Your Traditional Plan Benefit .................................................................................... 14 Determining Your Retirement Type ........................................................................................... 15 Other Traditional Plan Information ............................................................................................. 16

OTHER IMPORTANT FACTS ABOUT THE PLAN ......................................................... 19 IRS Benefit Limits ...................................................................................................................... 19 Qualified Domestic Relations Order .......................................................................................... 19 Keeping Your Records and Beneficiary Designation Current .................................................... 19 Returning from a Military Service Leave of Absence ................................................................. 19 Payment During Legal Disability or Incapacitation .................................................................... 20 Taking a Break in Service .......................................................................................................... 20 Pension Benefit Guaranty Corporation Insurance ..................................................................... 21

IMPORTANT TAX INFORMATION .................................................................................. 23 Rolling Over Your Lump-Sum Distribution ................................................................................. 23 Direct Rollover to a Traditional IRA (or Another Eligible Plan)................................................... 23 Choosing a Direct Payment Instead of a Rollover Payment ...................................................... 24

FILING A CLAIM FOR BENEFITS ................................................................................... 24 Denied Benefits Requests and the Appeals Process ................................................................ 24 If Your Benefits Claim Is Denied ................................................................................................ 25 Request for Review ................................................................................................................... 25

PLAN ADMINISTRATIVE INFORMATION ...................................................................... 26 Your Plan Rights and Responsibilities ....................................................................................... 26 Statement of ERISA Rights ....................................................................................................... 26 Plan Administration ................................................................................................................... 28 Information About the Plan ........................................................................................................ 29 Contact Information ................................................................................................................... 29

U.S. Pension Benefits Book 1

ABOUT THE PLAN

This document is the official Summary Plan Description (“SPD”) for the MSI Pension Plan (the “Plan”), sponsored by Motorola Solutions, Inc. (together with its corporate predecessors, “Motorola Solutions”). The SPD provides an overview of the Plan provisions. The Portable Pension Plan (the “Portable Plan”) and the Traditional Pension Plan (the “Traditional Plan”) are components of the Plan.

The Motorola Pension Plan and Motorola Solutions Pension Plan are collectively referred to in this SPD as the “Predecessor Plan.” The Predecessor Plan was frozen as to new participants effective January 1, 2005, and frozen as to benefit accruals effective February 28, 2009. Effective September 15, 2014, the accounts of participants, beneficiaries and alternate payees under qualified domestic relations orders who, as of December 1, 2013, had not yet commenced receipt of all benefits under the Predecessor Plan were transferred from the Predecessor Plan to this Plan.

This SPD describes the Plan as in effect on January 1, 2018. Subsequent SPDs or Summaries of Material Modifications (“SMMs”) will be provided to advise you of changes in the Plan as required by the Employee Retirement Income Security Act of 1974, as amended (“ERISA”).

You shouldn’t rely on this SPD other than as a general summary of the Plan’s features. Your rights are governed by the terms of the Plan document. You should refer to the Plan document for complete information on your rights and obligations under the Plan. You may obtain a copy of the Plan document upon written request to the Motorola Solutions Employee Service Center (the “Employee Service Center”). There may be a reasonable charge for such copies.

In the event of any difference between the terms of this SPD and the Plan document, the terms of the Plan document will control.

Motorola Solutions reserves the right, at any time, to amend, modify or terminate the Plan in whole or in part.

U.S. Pension Benefits Book 2

DETERMINING YOUR ELIGIBILITY AND BENEFIT

This section will help you determine whether you have a Plan benefit, calculate your vesting service and average earnings, and understand the different benefit payment options you have under the Plan.

Step One: Determine Your Eligibility. If your account was transferred from the Predecessor Plan to the Plan, as described in the “About the Plan” section above, you are a Plan participant. As under the Predecessor Plan, participants are not eligible for any retirement benefit accruals under the Plan based on earnings or benefit service after February 28, 2009. Per the rules of the Predecessor Plan, you were eligible to participate if, prior to February 28, 2009, (1) you were pension-eligible, (2) you were an employee of Motorola Solutions or a subsidiary participating in the Plan, (3) the U.S. payroll department processed your regular paycheck and (4) you completed an eligibility year of service. “Pension-eligible” means either that you were hired before January 1, 2005 (based on your most recent hire date), or that you were an employee of Crisnet, Inc., MeshNetworks, Inc. or Quantum Bridge Communications on December 31, 2004, and met certain other eligibility requirements.

Step Two: Determine Your Portable and Traditional Plan Eligibility.

Portable Plan If you were hired after June 30, 1999, and before January 1, 2005, you were automatically enrolled in the Portable Plan if you were pension-eligible and you completed a year of eligibility service. If you were hired on or before June 30, 1999, you were eligible for the Portable Plan if either of the following was true:

You elected to participate in the Portable Plan, or didn’t elect to stay in the Traditional Plan, during the April 2000 election period.

You were a former employee who left Motorola Solutions on or before June 30, 1999, and you were rehired as a pension-eligible employee after that date.

Traditional Plan Subject to the above, if you were pension-eligible on or before June 30, 1999, you were enrolled in the Traditional Plan. If you were an active employee or on a leave of absence on June 30, 1999, you were eligible to make a one-time election to continue your participation in the Traditional Plan. If you didn’t make that election, you automatically became a participant in the Portable Plan.

If you became a participant in the Portable Plan (either because you elected to participate in the Portable Plan or didn’t make an election to stay in the Traditional Plan), your Traditional Plan benefit was “frozen” as of June 30, 2000. This frozen benefit is added to your Portable Plan benefit.

U.S. Pension Benefits Book 3

Step Three: Select a Beneficiary, If You Have a Portable Plan Benefit. You can designate primary and contingent beneficiaries for Portable Plan benefits. To designate a beneficiary, log on to Your Benefits Resources and fill out the online designation. The Employee Service Center will send you a Beneficiary Designation Form reflecting your online designation. After you verify the accuracy of your beneficiary designation(s), sign your Beneficiary Designation Form and return it to the Employee Service Center.

If you’re married and designate a beneficiary other than your spouse, your spouse must provide written, notarized consent to your designation before the designation takes effect. Your beneficiary designation isn’t effective until the Employee Service Center receives your signed and notarized form.

If you’re married and you aren’t at least age 35 by the end of the year in which you complete your non-spousal beneficiary designation, the beneficiary designation becomes invalid on January 1 of the year in which you will reach age 35. You’ll need to designate your non-spousal beneficiary again and obtain the appropriate spousal consent after January 1 of the year in which you reach age 35.

SPOUSE/SURVIVING SPOUSE

Throughout this SPD, “spouse” or “surviving spouse” refers to a person to whom you are legally married. Effective September 16, 2013, the Plan recognizes same-sex marriages as legal (even if they occurred before that date), if they were conducted in a state that recognized same-sex marriage at the time of the participant’s marriage. This is the case even if the participant resides in a state that doesn’t recognize same-sex marriages.

KEEP THIS IN MIND WHEN DESIGNATING BENEFICIARIES

Be sure to periodically review your designated beneficiaries. If you marry after you file a beneficiary designation, your designation becomes invalid to the extent that you need spousal consent but don’t have it.

If you designate your spouse as your beneficiary and you later separate or divorce, your designation remains in effect unless you change it by filling out and submitting a new Beneficiary Designation Form, or you remarry.

Step Four: Identify Your Benefit Service. The Plan uses “benefit service” to calculate your benefit. Your benefit service includes all completed years and months that you worked at Motorola Solutions or a participating subsidiary from January 1, 1978, through February 28, 2009, while you were a pension-eligible employee.

However, if you joined Motorola Solutions as a result of an acquisition, the Plan didn’t count your years of service with an acquired company or business unit for benefit service purposes. For example, if you were a former employee of General Instrument Corporation (“GI”), the Plan didn’t count your years of service with GI before January 1, 2001, as benefit service.

U.S. Pension Benefits Book 4

Keep in mind that any years of service with a Motorola Solutions affiliate or subsidiary counted as benefit service only if (and while) the affiliate or subsidiary was a participating employer in the Plan. Please contact the Employee Service Center if you have questions about whether a certain affiliate or subsidiary was a participating employer under the Plan.

Step Five: Determine Whether You’re Vested. Your total years of service with Motorola Solutions determines whether or not you’re “vested” in (entitled to) your Plan benefit. Your years of service include completed years and months. You’re vested in your benefit once you either:

Complete at least three years of service; or

Reach age 60 while employed with Motorola Solutions or a participating affiliate or subsidiary, and complete at least one year of service.

For Employees Coming from Acquisition-Based Groups Certain groups of employees have different determinations for years of service. If you joined Motorola Solutions as the result of an acquisition before January 1, 2000, the Plan counted your years of service with the acquired company or business unit for vesting purposes, but not for benefit service purposes. For acquisitions from January 1, 2000, through December 31, 2004, you received credit for such service depending on the specific terms of that acquisition.

Step Six: Know How Your Average Earnings Are Calculated. The Plan uses average earnings to calculate your benefit. Before January 1, 2008, your “final average earnings” were used to calculate your benefit. From January 1, 2008, through February 28, 2009, your “modified average earnings” were used to calculate your benefit. (After February 28, 2009, benefits were frozen). Below is an explanation of how these two earnings were calculated.

Your Final Average Earnings Your final average earnings are your average compensation for the five years of your highest pay during the last 10 calendar years (including years you didn’t work a complete year) of your Motorola Solutions employment, on or before March 1, 2009.

Your Modified Average Earnings 1. Add the following figures together:

The amount of your five highest years of annual compensation (or fewer years, if you worked less than five years) of the 10 calendar years before January 1, 2008

Your pay during all years after 2007 and through February 28, 2009 in which you participated in the Plan

U.S. Pension Benefits Book 5

2. Then add these figures together:

The sum of the number of years of your benefit service under the Plan before January 1, 2008, to a maximum of five years (or fewer years, if you worked less than five years)

Your total years of participation in the Plan for all years after 2007 through February 28, 2009

3. Divide the first figure by the second figure to get your modified average earnings.

Step Seven: Understand What Your Compensation Includes. Your compensation is a major factor in calculating your earnings. Your “compensation” or “pay” prior to February 28, 2009, included all of the following:

Regular base salary

Sales Incentive Plan payments or commissions

Engineering Incentive Plan payments

Shift differentials

Overtime

Lump-sum merit pay (beginning January 1, 2000)

Your contributions to the 401(k) Plan, Health Care Flexible Spending Account (FSA) or Dependent Care Account (DCA), or other pretax contributions to a Section 125 plan or qualified transportation fringe benefit program

From January 1, 2000, through February 3, 2002, any payments you received under the Incentive Pay Plan, the Performance Excellence = Rewards Incentive Plan or other similar incentive plans were also included as compensation. After February 3, 2002, these amounts were excluded from “pay” as noted below.

Your pay prior to February 28, 2009, didn’t include any of the following:

Other awards

Payments received under the Motorola Incentive Pay Plan or other similar incentive plans

Individual bonuses

Any payments you received under the Predecessor Plan or Motorola Solutions’ 401(k) Plan

Severance or other termination payments

Moving allowances

Educational allowances

Cost-of-living adjustments

Noncash payments

Overseas allowances

U.S. Pension Benefits Book 6

For purposes of determining your benefit under the Plan, your annual compensation could not exceed the Section 401(a)(17) limit imposed by the Internal Revenue Code (“IRC”) in any year. The IRC limit was $245,000 in 2009, when the Plan was frozen. This limit was lower in previous years; please contact the Employee Service Center if you have any questions about what this limit was for a particular year.

Step Eight: Learn How Your Social Security Benefit Is Determined. The Traditional Plan formula used your Social Security benefit when calculating your benefit accrued through the earlier of your actual retirement date or February 28, 2009. Your Social Security benefit is the estimated amount of your Social Security retirement benefit payable to you at age 65 (projected as of February 28, 2009, if you weren’t yet age 65 on that date), calculated based on both the Social Security law in effect on the earlier of January 1 of the year your employment with Motorola Solutions terminated, or February 28, 2009 and your final or modified average earnings, as applicable.

When the Plan was frozen, if you were a Traditional Plan participant, you were given the opportunity to submit a copy of your actual Social Security award letter or your actual Social Security wage history no later than December 31, 2009 to determine whether you would be entitled to a greater benefit. No adjustments based on actual Social Security will be made after December 31, 2009.

Your spouse’s Social Security benefit doesn’t affect the amount of your benefit. Also, an increase in your Social Security benefit after February 28, 2009, doesn’t affect your benefit in any way.

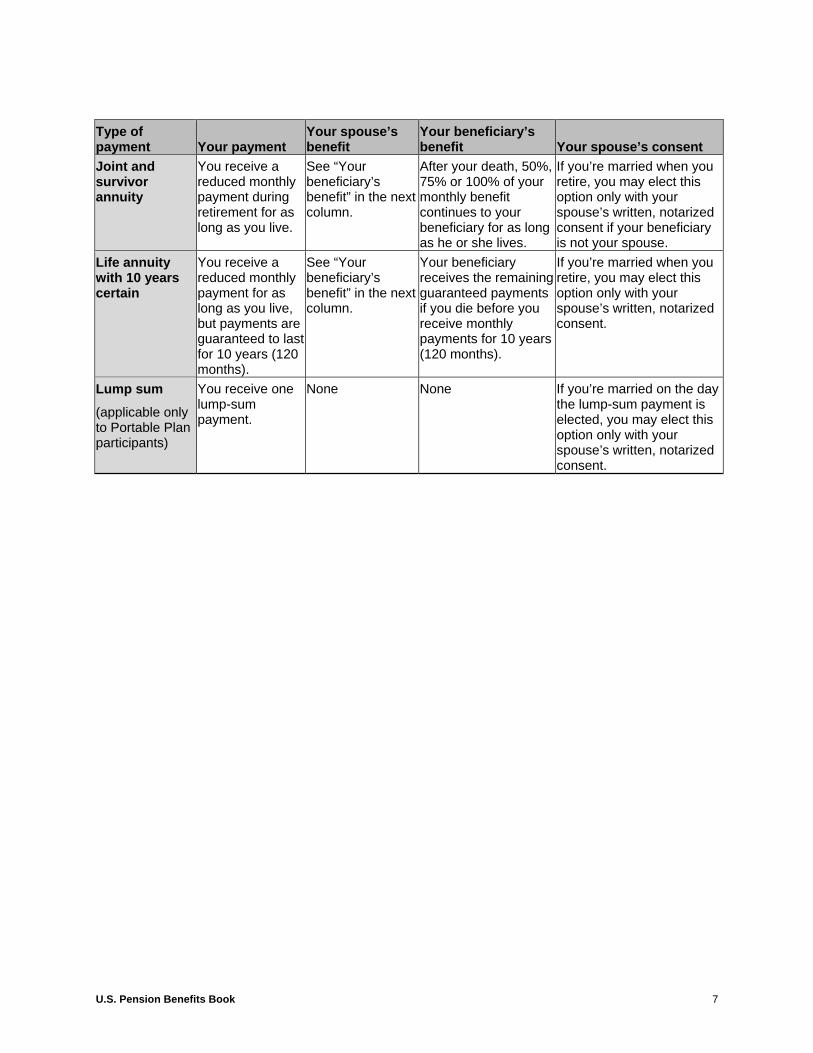

Step Nine: Choose a Benefit Payment Option. The following table generally describes each payment option you have as a Plan participant if your benefit exceeds $5,000. For more information, please see the sections of this SPD entitled “Receiving Your Portable Plan Benefit” and “Receiving Your Traditional Plan Benefit”:

Type of payment Your payment

Your spouse’s benefit

Your beneficiary’s benefit Your spouse’s consent

Single life annuity

You receive a monthly payment during retirement for as long as you live.

None None This option is automatic if you aren’t married when you retire and you don’t choose another payment option. If you’re married, you may elect this option only with your spouse’s written, notarized consent.

Qualified joint and survivor annuity

You receive a reduced monthly payment during retirement for as long as you live.

After your death, 50%, 75% or 100% of your monthly benefit continues to your spouse for as long as he or she lives.

None The 50% payment option is automatic if you’re married when you retire, provided you don’t choose another payment option.

U.S. Pension Benefits Book 7

Type of payment Your payment

Your spouse’s benefit

Your beneficiary’s benefit Your spouse’s consent

Joint and survivor annuity

You receive a reduced monthly payment during retirement for as long as you live.

See “Your beneficiary’s benefit” in the next column.

After your death, 50%, 75% or 100% of your monthly benefit continues to your beneficiary for as long as he or she lives.

If you’re married when you retire, you may elect this option only with your spouse’s written, notarized consent if your beneficiary is not your spouse.

Life annuity with 10 years certain

You receive a reduced monthly payment for as long as you live, but payments are guaranteed to last for 10 years (120 months).

See “Your beneficiary’s benefit” in the next column.

Your beneficiary receives the remaining guaranteed payments if you die before you receive monthly payments for 10 years (120 months).

If you’re married when you retire, you may elect this option only with your spouse’s written, notarized consent.

Lump sum

(applicable only to Portable Plan participants)

You receive one lump-sum payment.

None None If you’re married on the day the lump-sum payment is elected, you may elect this option only with your spouse’s written, notarized consent.

U.S. Pension Benefits Book 8

THE PORTABLE PLAN

From January 1, 2008, through February 28, 2009 (unless your employment terminated earlier), your benefit under the Portable Plan was based on your modified average earnings and a “benefit percentage” determined by your vesting benefit service. Before January 1, 2008, your benefits under the Portable Plan were based on your final average earnings through December 31, 2007. This section describes how the Portable Plan works for eligible employees who may receive this benefit.

The Portable Plan lets you receive your benefit as a lump sum or an annuity when you leave Motorola Solutions, provided you have at least three years of service. If you don’t have three years of service, you may still be entitled to a Portable Plan benefit if you leave Motorola Solutions because of disability or after you reach age 60 with at least one year of service.

If you participated in the Traditional Plan before July 1, 2000, the Portable Plan counts your vesting service both before and after July 1, 2000.

With respect to benefit service: your benefit service was calculated on and after July 1, 2000, to determine your Portable Plan benefit, and only your benefit service before July 1, 2000, was used to calculate your frozen Traditional Plan benefit.

WHAT’S THE BENEFIT PERCENTAGE?

The Portable Plan benefit percentage is based on the benefit service you earned on or after July 1, 2000, and your vesting service. It’s determined by taking the sum of the following figures:

4 percent for each year of benefit service earned while you have five or fewer years of vesting service

5 percent for each year of benefit service earned while you have more than five but no more than 10 years of vesting service

6 percent for each year of benefit service earned while you have more than 10 but no more than 15 years of vesting service

7 percent for each year of benefit service earned while you have more than 15 years of vesting service

Preserving Your Frozen Benefit Amount If you continued to work for Motorola Solutions after February 28, 2009, your frozen Portable Plan benefit was calculated as a lump-sum amount and then converted to an age-65 single life annuity amount. This amount, known as the “frozen single life annuity,” is the value that was frozen as of February 28, 2009.

If you elect to receive your benefit as a lump sum after you terminate employment, the frozen single life annuity will be converted to a lump sum payable when you choose to receive it. This conversion will use an interest rate and mortality factor as required by federal regulations. Since the required interest rates and mortality factors fluctuate from time to time, the amount of the lump sum you receive may or may not equal the lump-sum amount that you would have received if it had been paid as of February 28, 2009.

U.S. Pension Benefits Book 9

If you elect an annuity, you’ll receive monthly payments for life. Depending on the annuity option you select, your surviving spouse or beneficiary may also receive monthly payments for the remainder of his or her life. If you start receiving your annuity earlier than age 65, your frozen single life annuity will be adjusted for commencement before age 65 and for survivor benefits, if applicable.

Receiving Your Portable Plan Benefit You may receive your Portable Plan benefit when you terminate employment (regardless of your age), provided you’re vested at the time. You’re vested in this benefit after you’ve completed at least three years of service, or after reaching age 60 with at least one year of service. This section explains the general rules for how to receive this benefit, as well as the types of payment options you may elect.

Your Payment Options In general, if the value of your benefit is $1,000 or less when you terminate employment, you’ll automatically receive this benefit in the form of a lump-sum payment shortly after your employment terminates. If your benefit has a value greater than $1,000 but less than or equal to $5,000, you may elect to take your lump sum after your employment terminates or to defer receipt of the benefit until a later date (but not later than April 1 following the calendar year in which you reach age 70½). You may receive your total benefit in cash, or you may roll it over directly into an individual retirement account (“IRA”) or another eligible plan. Note that spousal consent is not required for lump-sum distributions less than or equal to $5,000.

If the value of your benefit is more than $5,000, you have a variety of payment options. Please refer to the chart in the section of this SPD entitled “Step Nine: Choose a Benefit Payment Option.” for more information.

Selecting and Changing Your Payment Option You must elect a payment option at least seven days before you want your benefit to begin. Once you do so, you may change your election until the time you begin receiving your benefit. If you’re married, you may elect a payment option other than the qualified joint and survivor annuity only if your spouse provides written, notarized consent to your election. Your spouse must provide this consent within 90 days before your benefit start date.

Your election will apply to all subsequent payments and may not be changed once payments begin. However, if you elect the single life annuity payment option and discover within 120 days of the time your benefit is scheduled to begin that you have a terminal illness, in some circumstances, you may be able to change your election to another payment option. Contact the Employee Service Center for more information.

Receiving Your Benefit If You Elected a Lump Sum If you elected to receive your benefit as a lump sum, and your benefit is $5,000 or less, you’ll receive this benefit in the form of a check within 60 days of your last day worked. If you prefer to roll over this lump-sum benefit, you must confirm your request with the Employee Service Center within 30 days of your last day worked. If your lump-sum Portable Plan benefit exceeds $5,000, you may take the distribution, roll the benefit over to an eligible employer plan or IRA, or defer the receipt of your distribution.

U.S. Pension Benefits Book 10

Remember: If you leave Motorola Solutions before age 65 and you defer the receipt of a lump-sum benefit until a later date, the amount of the lump sum payable in a later year is calculated based on your frozen age-65 annuity benefit. The calculation uses interest rate and mortality assumptions for the year of distribution.

Receiving Your Benefit If You Elected an Annuity If you elected to receive your benefit as an annuity and your employment terminates before age 65, you may defer the start date of your annuity payments. The Portable Plan calculates your benefit as an annuity payable for your life, beginning at age 65. The calculation is based on your lump-sum Portable Pension benefit, and it uses the interest rate and mortality assumptions for the year you leave Motorola Solutions. This annuity benefit is “frozen” and doesn’t change as you grow older. If you don’t submit your retirement application in time for your benefit to begin at age 65 (or your later retirement date), the Portable Plan actuarially adjusts your annuity to reflect the deferred payments.

If you choose to receive your Portable Plan benefit as an annuity before age 65, the Plan actuarially reduces your age-65 annuity benefit. This reduction is based on interest rate and mortality assumptions for the year you start to receive your benefit. The reduction also reflects that payments that begin before age 65 are normally paid over a longer period of time. This actuarial adjustment is different from the early retirement reduction that applies to a Traditional Plan benefit.

The Plan also adjusts your benefit if the annuity provides a benefit to your surviving spouse or other beneficiary. See the section of this SPD entitled “Step Nine: Choose a Benefit Payment Option.” for a description of the payment options available under the Portable Plan.

Other Portable Plan Information This section addresses how your Plan benefit will be affected if you work past age 65 or if you have a disability retirement, how to receive your preretirement death benefit, and how to receive a payment if you were part of the General Instrument Corporation Pension Plan (the “GI Pension Plan”). The end of this section addresses how Motorola Solutions medical benefits are paid from a 401(h) account.

If You Work Past Age 65 You continued to accrue a pension benefit under the Plan if you worked at Motorola Solutions after age 65, with the exception that all benefit accruals stopped as of February 28, 2009. If you reach age 70½ and continue to work, you must begin receiving your Plan benefit no later than the April 1 following the calendar year in which you retire. If you terminate employment at or after age 65 but before you reach age 70½, you must begin receiving your benefit no later than the April 1 following the calendar year in which you reach age 70½. Your benefit election applies to all subsequent benefit payments. You may not change your election even if your benefit begins before you retire.

U.S. Pension Benefits Book 11

Eligibility for Disability Retirement As a Portable Plan participant, you’re eligible for disability retirement if you have a permanent and total disability that makes you eligible for a disability benefit under the Motorola Solutions Disability Income Plan.

Before February 28, 2009, you could continue to accrue additional benefits until you reached age 65, or until five years after your disability began (whichever occurred later). Additionally, you continued to receive vesting service during this time. However, you immediately stopped earning additional benefits as of February 28, 2009, or earlier if any of the following criteria were met:

You were no longer totally disabled.

You refused to submit to a required medical examination to determine whether your disability persisted.

You began receiving a benefit under the Plan.

Your Long-Term Disability benefit under the Motorola Disability Income Plan ceased for any reason other than a reduction of the disability benefit because you received Social Security disability payments or similar amounts subject to offset.

You died.

Calculating Your Disability Pension Benefit If you were disabled, your benefit was calculated based on either your final or modified average earnings (as the case may be) as of the date your active employment ended because of disability, or as of February 28, 2009, if earlier.

If you receive a disability pension benefit while receiving a Long-Term Disability benefit under the Motorola Solutions Disability Income Plan, your Long-Term Disability benefit is reduced by the amount of your single life annuity benefit. This reduction applies even if you elect another payment option, such as a lump-sum benefit.

In addition, if you were accruing benefit service in 2002 as a result of entitlement to benefits under Title II of the Social Security Act but you were not entitled to benefits under Motorola Solutions’ Disability Income Plan, you stopped accruing additional benefit service and vesting service on November 13, 2002.

On and after February 28, 2009, when the Plan was frozen, if you deferred the receipt of your Disability Pension benefit, you no longer continued to earn additional benefits, but you continued to receive credit for vesting purposes during your period of disability.

DISABLED GI PENSION PLAN PARTICIPANTS

If you were a disabled participant in the GI Pension Plan and were earning a benefit under the GI Pension Plan, this benefit was frozen as of December 31, 2000. Effective January 1, 2001, you continued to earn additional benefits under the Portable Plan while you remained totally disabled. However, you stopped earning additional pension benefits at the earlier of when you began receiving your GI Pension Plan benefit or February 28, 2009. You may elect to receive your GI Pension Plan benefit once you reach age 65. If you had at least 10 years of service, however, you can begin receiving a reduced GI Pension Plan benefit any time after you reach age 55.

U.S. Pension Benefits Book 12

Your Preretirement Death Benefit If you die before you begin receiving your benefit, the Portable Plan pays a preretirement death benefit to your surviving spouse or designated beneficiary. The preretirement death benefit from the Portable Plan equals 100 percent of the actuarial equivalent of your vested accrued benefit as of your date of death.

If you’re married, the Portable Plan automatically pays the preretirement death benefit to your surviving spouse, unless you designated another beneficiary and your spouse provided written, notarized consent to that designation.

If the Portable Plan doesn’t have a beneficiary designation on file, or if your designation is invalid (for example, you need spousal consent and don’t have it, or you didn’t complete a new designation when you got married), the Portable Plan will pay the preretirement death benefit to another relative on file. The order of precedence is as follows:

Your surviving spouse; or if none, then

Your children (in equal shares if more than one); or if none, then

Your parents (in equal shares if both parents survive you); or if none, then

Your estate.

Your surviving spouse may elect to receive the preretirement death benefit in the form of an annuity for his or her life or as a lump-sum payment. If someone other than your spouse is your beneficiary, he or she must receive the benefit as a lump-sum payment.

If you die and you’re already receiving a benefit from the Portable Plan, your surviving spouse or other beneficiary may continue to receive a benefit after your death, depending on the payment option you selected for your benefit. For example, if you received your Portable Pension benefit in the form of a lump sum, no death benefit is paid from the Plan if you die after you received your payment.

U.S. Pension Benefits Book 13

GI PENSION PLAN BENEFITS

Payment of GI Pension Plan benefits If you have a vested benefit in the GI Pension Plan, your benefit is paid in a slightly different way. If you’re a participant in this Plan, you’ll begin receiving your GI Pension Plan benefit when you reach age 65 (or, if later, when you terminate employment). If you had at least 10 years of service with GI and Motorola Solutions when you terminate, you may elect to have your GI Pension Plan benefit begin any time after you reach age 55. Any benefit that begins before age 65 will be reduced to reflect the longer period over which payments will be made. The reduction is based on the terms of the GI Pension Plan.

Your survivor benefit If you die after you’re vested, but before you begin receiving your GI Pension Plan benefit, your surviving spouse will be eligible to receive a survivor annuity benefit attributable to your GI Pension Plan benefit. The survivor annuity is in addition to any benefit payable under the Portable Plan. Note that the lump sum payment option is not available unless the value of the benefit is $5,000 or less.

Your survivor annuity will depend on the number of your years of service. If you had at least 10 years of service as of your date of death, the survivor annuity may begin at any time after you would have reached age 55 (but not later than when you would have reached age 65). The survivor annuity equals 50 percent of the amount you would have received if you had survived and begun receiving your GI Pension benefit in the form of a qualified joint and survivor annuity on the date the benefit began.

If you die and you didn’t have at least 10 years of service, your surviving spouse will receive an annuity beginning on the date you would have reached age 65 (or, if later, the month following your death). The survivor annuity equals 50 percent of the amount you would have received if you had survived and begun receiving your GI Pension Plan benefit in the form of a qualified joint and survivor annuity on the date you reached age 65 (or, if later, the month following your death).

If you die and you’re not married, or if you die and your surviving spouse dies before the survivor annuity begins, no death benefit will be paid with respect to your GI Pension benefit.

Medical Benefits Paid from a 401(h) Account Motorola Solutions has established a Section 401(h) account under the Plan. This account is used to fund medical and dental benefits, provided under the Motorola Solutions Post-Employment Health Benefits Plan to certain participants and their covered dependents.

Motorola Solutions has the right to terminate or amend the section of the Plan under which contributions to the 401(h) account are made.

U.S. Pension Benefits Book 14

THE TRADITIONAL PLAN

Before January 1, 2008, the Traditional Plan provided a benefit based on your final average earnings. This benefit was also calculated based on your benefit service, offset by your estimated Social Security benefit. From January 1, 2008, through February 28, 2009 (unless your employment terminated earlier), your benefit under the Traditional Plan was based on your modified average earnings, rather than your final average earnings.

See the section of this SPD entitled “Step Four: Identify Your Benefit Service.” to learn more about how the Traditional Plan calculates your years of service for vesting and benefit service purposes.

Portable Plan Participants: Take Note The Traditional Plan formula also applies if you were a participant in the Traditional Plan on or before June 30, 1999, but chose to participate in the Portable Plan beginning July 1, 2000. If this is the case, your frozen accrued benefit under the Traditional Plan doesn’t include any service or compensation earned after June 30, 2000. Instead, your benefit after June 30, 2000 is calculated under the Portable Plan formula.

Also, your Social Security offset was determined without regard to increases in Social Security benefits after June 30, 2000.

Receiving Your Traditional Plan Benefit As a participant in the Traditional Plan, you can receive your benefit at normal retirement age, age 65. Alternatively, the Plan offers the following options:

An early retirement benefit payable as early as:

– Age 55, provided you complete at least three years of service

– Age 60, provided you complete at least one year of service

A late retirement benefit, payable when you retire after you reach age 65

A terminated vested benefit if you leave Motorola Solutions before age 55 and have at least three years of service, payable as early as age 55

A disability benefit, provided you meet certain requirements

If you die after you complete at least three years of service but before you begin receiving your benefit, your surviving spouse is entitled to a preretirement death benefit from the Traditional Plan. See the section of this SPD entitled “Your Preretirement Death Benefit” for details.

U.S. Pension Benefits Book 15

Your Payment Options If the value of your benefit is $1,000 or less when you terminate employment, you’ll automatically receive this benefit in the form of a lump-sum payment shortly after your employment terminates, unless you choose to roll over your benefit. If your benefit has a value greater than $1,000 but less than or equal to $5,000, you must also receive a lump-sum; however, if you do not take action, your balance will be automatically rolled into an individual retirement account as directed by the Plan Administrator. Note that spousal consent is not required for lump-sum distributions less than or equal to $5,000.

If the value of your benefit is more than $5,000, you may select only an annuity-based payment option for your Transitional Plan benefit. Please refer to the chart in the section of this SPD entitled “Step Nine: Choose a Benefit Payment Option.” for more information.

If you receive your benefit before age 65 or if you receive your benefit in a form other than a single life annuity, the Plan will adjust your benefit, based on actuarial equivalence.

Selecting and Changing Your Payment Option The same rules apply to selecting and changing your payment options under the Traditional Plan as under the Portable Plan. Please see the corresponding section under the Portable Plan portion of this SPD.

Determining Your Retirement Type Your retirement age will determine what type of benefit you receive under the Traditional Plan. Depending on your age upon the termination of your employment with Motorola Solutions, you’ll be classified as having either a “normal,” “early” or “late” retirement.

Option 1: Normal Retirement Your “normal” retirement date under the Traditional Plan is the first day of the month on or after your 65th birthday. If you select this option, your benefit begins on the first day of the month after your last day worked. If your last day falls on the first of the month, your benefit begins the following month.

If you continue to work at Motorola Solutions after age 65, you’ll earn a benefit under the Traditional Plan (up to the 35-year maximum after January 1, 1988). You must begin receiving your benefit before April 1 of the year following the year in which you reach age 70½ (or at your earlier termination at or after age 65).

U.S. Pension Benefits Book 16

Option 2: Early Retirement Under the Traditional Plan, you may retire from Motorola Solutions and receive a Traditional Plan benefit as early as age 55, provided you have at least three years of service. Alternatively, you may retire at age 60, provided you have at least one year of service.

If you retire before age 65 and elect to begin receiving benefits immediately, any benefit you may receive will be reduced (ranging from a 50 percent benefit for retirement at age 55 to a 93.33 percent benefit for a retirement at age 64), because the Plan expects to make payments over a longer period of time. If you retire but you wait until age 65 to receive your benefit, you will receive 100 percent of the monthly amount for which you were eligible as of February 28, 2009.

If you fail to submit your retirement application in time for your benefit to begin at age 65 (or your later retirement date), the Plan will actuarially adjust your annuity to reflect the later commencement of payments.

Option 3: Late Retirement As mentioned above, effective February 28, 2009, the Plan was frozen with respect to all future retirement benefit accruals and participant compensation increases. Before February 28, 2009, if you worked past your normal retirement age (age 65), you continued to earn benefit service under the Plan. Your monthly benefit was calculated the same way as for normal retirement, but used either your final average earnings or modified average earnings, as applicable, and benefit service as of your delayed retirement date. The benefit was actuarially increased to reflect your delayed retirement.

You may delay your retirement until the first day of any month following your normal retirement date. However, you must begin receiving benefits no later than the April 1 following the calendar year in which you reach age 70½ or terminate employment, whichever is later. The benefit will be actuarially increased to reflect your delayed retirement. Your election with respect to the receipt of your benefit applies to all subsequent benefit payments. You may not change your election, even if your benefit begins before you retire.

Option 4: Terminated Vested (If You Leave Before Age 55) You’re still eligible for a benefit if you leave Motorola Solutions before age 55 and have at least three years of service. You may receive your benefit at your normal retirement age, age 65, or you may choose to receive your benefit as early as age 55. If you receive your benefit before age 65, your benefit will be reduced as described under the section of this SPD entitled “Option 2: Early Retirement.”

Other Traditional Plan Information This section addresses how your Plan benefit will be affected if you have a disability retirement and how to receive your preretirement death benefit.

U.S. Pension Benefits Book 17

Eligibility for Disability Retirement As a Traditional Plan participant, you’re eligible for disability retirement if you have a permanent and total disability that makes you eligible for a disability benefit under the Motorola Solutions Disability Income Plan. You don’t need three years of service to qualify for a disability pension benefit.

The date your active employment ends will determine how this disability benefit is calculated. If your active employment ended because you were disabled before December 31, 2007, your benefit was calculated based on your final average earnings as of the date your active employment ended because of such disability. If your active employment ended because you were disabled on or after January 1, 2008, your benefit is calculated based on your modified average earnings as of the date your active employment ended because of such disability or as of February 28, 2009, whichever is earlier.

You may take your benefit beginning as early as age 55 (or your later disability retirement date). If you defer the receipt of your benefit, effective February 28, 2009, you won’t continue to earn additional benefits. However, in this case, you would continue to receive credit for vesting purposes during your period of disability. Before February 28, 2009, you could continue to accrue additional benefits until you reached age 65, or until five years after your disability began (whichever occurred later). However, you immediately stopped earning additional benefits as of February 28, 2009, or earlier if you met any of the following criteria:

You were no longer totally disabled.

You refused to submit to a required medical examination to determine whether your disability persisted.

You began receiving a benefit under the Plan.

Your Long-Term Disability benefit under the Motorola Disability Income Plan ceased for any reason other than a reduction of the disability benefit because you received Social Security disability payments or similar amounts subject to offset.

You died.

Receiving Your Disability Pension Benefit Under the Traditional Plan, you may choose to receive your benefit as early as age 55. If you begin receiving your benefit before age 65, your benefit will be reduced for early payment. (See the section of this SPD entitled “Option 2: Early Retirement” for the reduction that applies.)

If you receive a Disability Pension benefit while you’re receiving a Long-Term Disability benefit under the Motorola Solutions Disability Income Plan, your Long-Term Disability benefit is reduced by the amount of your single life annuity benefit. This reduction applies even if you elect another payment option.

In addition, if you were accruing benefit service in 2002 as a result of entitlement to benefits under Title II of the Social Security Act but you were not entitled to benefits under the Disability Income Plan, you stopped accruing additional benefit service and vesting service on November 13, 2002.

U.S. Pension Benefits Book 18

Your Preretirement Death Benefit If you die before you begin receiving your benefit but after you complete three years of service, your surviving spouse is entitled, by law, to a qualified preretirement survivor annuity under the Traditional Plan. The Traditional Plan doesn’t pay a preretirement death benefit unless you’re legally married at the time of your death. The date this benefit begins and the amount your surviving spouse receives depend on whether you die before or after age 55.

Your Preretirement Death Benefit at or After Age 55 If you die at or after age 55, your surviving spouse will receive the survivor annuity under a qualified 50 percent joint and survivor annuity, as if you had chosen this payment option and begun receiving payments on the day before your death. Your surviving spouse may elect to begin payments at any time between the date of your death and the date on which you would have reached age 65.

Your Preretirement Death Benefit Before Age 55 If you die before age 55 with at least three years of service, your surviving spouse will receive the survivor annuity under a qualified 50 percent joint and survivor annuity. The Traditional Plan calculates the benefit as if you had separated from service on the date of your death (or your earlier termination date), survived to age 55 and retired with this payment option on the day after you reached age 55. Your surviving spouse may begin receiving a preretirement death benefit at any time between your earliest retirement date and the date when you would have reached age 65.

If you die before age 65, your surviving spouse may choose to defer beginning payments to a later date, up until your normal retirement date.

If you die while receiving your benefit, the Traditional Plan may or may not continue to pay a pension benefit to your surviving spouse or designated beneficiary(ies). The benefit payable, as well as the amount, depends on the payment option you elected upon retirement. See the section of this SPD entitled “Step Nine: Choose a Benefit Payment Option.” for details.

If Your Preretirement Death Benefit Is Less Than or Equal to $5,000 The preretirement death benefit is automatically paid to your surviving spouse in a lump sum if the value of your preretirement death benefit is $1,000 or less. If the value of your preretirement death benefit is greater than $1,000 but less than or equal to $5,000, your surviving spouse may elect to receive a lump-sum payment or defer the payment.

Medical Benefits Paid from a 401(h) Account The same information applies to the 401(h) account under both the Portable Plan and the Traditional Plan. Please see the corresponding section of the Portable Plan discussion for more information.

U.S. Pension Benefits Book 19

OTHER IMPORTANT FACTS ABOUT THE PLAN

IRS Benefit Limits In accordance with the Pension Protection Act of 2006, the IRS imposes limits on the benefits that can be paid from the Plan if the Plan’s funding level drops below certain thresholds. The funding level is generally the ratio of total Plan assets, net of any credit balance, to the present value of all benefits accrued under the Plan as of the beginning of a Plan year.

If at any time the Plan is less than 80 percent funded, there may be restrictions placed on the payment of your benefits under the Plan. You will be notified if any such restrictions apply.

Qualified Domestic Relations Order A Qualified Domestic Relations Order (“QDRO”) is a court order, judgment or decree in connection with alimony, marital property rights, or child support requirements. If a Domestic Relations Order complies with the Retirement Equity Act of 1984 (as amended) and the Plan’s QDRO procedures, the Plan recognizes it as a Qualified Domestic Relations Order. In this event, the Plan will make payments to the alternate payee (your spouse, former spouse, child or other dependent) as specified in the order. Procedures and model QDROs for the Plan are available by accessing Aon Hewitt’s Qualified Order Center website at www.qocenter.com or by calling the Employee Service Center. QDRO fees are $350 per order reviewed, and the fee is paid by Motorola Solutions.

Keeping Your Records and Beneficiary Designation Current It’s very important that you keep your Human Resources records up to date. Your current mailing address and beneficiary designation in particular need to be on file in case benefit payments need to be sent to you or your beneficiary. To update your personal address, log on to Your Benefits Resources or call the Employee Service Center if you are a former employee.

To designate a beneficiary, log on to Your Benefits Resources and fill out the online designation. The Employee Service Center will send you a confirmation. If you are married and designated someone other than your spouse as beneficiary, or did not choose a joint and survivor payment option, the Employee Service Center will send you a spousal consent form which your spouse must complete to document his or her approval of the beneficiary designation or payment option.

Returning from a Military Service Leave of Absence If you’re re-employed by Motorola Solutions following a military service leave, you may have special rights and benefits. Contact the Employee Service Center if you would like detailed information. Keep in mind that, because the Plan was frozen February 28, 2009, you’re no longer eligible for any future benefit accruals after February 28, 2009.

U.S. Pension Benefits Book 20

Payment During Legal Disability or Incapacitation If, in the Plan Administrator’s opinion, you (or another individual eligible for your benefit under the Plan) are legally disabled or incapacitated in any way such that you can’t manage your financial affairs, the Plan Administrator may make any Plan benefit payment due to you to your legal representative, relative or friend on your behalf as the Plan Administrator considers advisable. In this situation, any payment made will be considered a complete discharge of any liability for making the payment under the Plan.

Taking a Break in Service You’re no longer eligible for any future retirement benefit accruals based on your earnings or benefit service after February 28, 2009. As such, if you leave Motorola Solutions and return after that date, you won’t re-enter the Plan for additional benefit service; however, depending on the break in service rules listed below, you may be eligible for additional vesting service.

What Is a Break in Service? A break in service begins on the earlier of the day you leave Motorola Solutions, retire or are discharged, or the first anniversary of any leaves of absence, whether paid or unpaid.

If your absence is due to pregnancy, birth, adoption of a child or caring for a child immediately after birth or adoption, your break in service won’t begin before the second anniversary of the leave (unless you leave Motorola Solutions earlier, retire or are discharged). Your leave period won’t count as service for purposes of calculating your Plan benefit. If you’re a former GI employee and you had a break in service for any period that began before January 1, 2001, your break in service will be determined under the terms of the GI Pension Plan.

How a Break in Service Works Before February 28, 2009, if you left Motorola Solutions and later returned, your status under the Plan depended on several things, including both of the following:

Whether you were a Plan participant when you left

Whether you had a break in service

If you’ve been rehired and want to confirm your status under the Plan, please contact the Employee Service Center.

Don’t forget that the Plan was closed to new participants after December 31, 2004. If you were a Plan participant when your employment ended, and you’re re-employed within 12 months from your date of termination, you’ll automatically enter the Plan as a participant on the date you’re rehired. If you weren’t a Plan participant when your employment ended, or if you were a Plan participant when your employment ended and you incurred a one-year break in service, you will not be eligible to participate in the Plan upon your rehire.

If you’re a former GI employee and had a leave period that began before January 1, 2001, the provisions of the GI Pension Plan will determine whether or not your leave period qualifies as a break in service.

U.S. Pension Benefits Book 21

How a Break in Service Affects Prior Benefit Service Before February 28, 2009, the Plan generally counted both your pre-break and post-break service as benefit service upon your rehire. This was valid only if you met one of the following criteria:

You were entitled to a vested benefit from the Plan at the time of your break in service (i.e., you had five years of service or were age 60 with one year of service).

You returned to service before you had a break in service of at least five consecutive years.

Your earlier termination resulted from a transfer to the purchaser in connection with the sale by Motorola Solutions of a subsidiary or business subdivision.

If you don’t meet at least one of the criteria above before February 28, 2009, any benefit service you earned in the first period of service won’t count in the calculation of your benefit. In addition, your pre-break service won’t count as benefit service if you received a lump-sum distribution of your vested benefit. (See the section of this SPD entitled “Disregarding Service Attributable to a Lump Sum” (below) for details.) Additionally, your service after you were rehired doesn’t count as benefit service unless you were pension-eligible.

If your account has been transferred between the Plan and another employer’s plan, or if you’ve been re-employed, your subsequent benefit will be adjusted so that you don’t receive duplicate benefits.

Disregarding Service Attributable to a Lump Sum If you receive your accrued benefit in a lump-sum payment and are subsequently re-employed by Motorola Solutions, your benefit service at the time of your initial termination is disregarded when determining the benefit earned during your subsequent employment. However, the Plan does give you credit for your earlier vesting service when determining whether you’re vested under the Plan.

Remember, you are not pension-eligible if you were rehired after January 1, 2005, and you had a 12-month (or greater) break in service before your rehire date.

RETURN TO SERVICE

If you’re receiving a Plan benefit and return to work with Motorola Solutions on or after January 4, 2011, your Plan benefit payments will continue.

Pension Benefit Guaranty Corporation Insurance Your pension benefits under the Plan are insured by the Pension Benefit Guaranty Corporation (“PBGC”), a federal insurance agency. If the Plan terminates without enough money to pay all the benefits, the PBGC will step in to pay certain pension benefits. In this event, some participants may lose certain benefits.

U.S. Pension Benefits Book 22

The PBGC guarantee generally covers:

Normal and early retirement benefits

Disability benefits if you become disabled before the Plan terminates

Certain benefits for your survivors

The PBGC guarantee generally does not cover:

Benefits greater than the maximum guaranteed amount set forth by law for the year in which the Plan terminates

Some or all of the benefit increases and new benefits based on Plan provisions that have been in place for fewer than five years at the time the Plan terminates

Benefits that aren’t vested because you haven’t worked long enough for Motorola Solutions

Benefits for which you haven’t met all of the requirements at the time the Plan terminates

Certain early retirement payments (such as supplemental benefits that stop when you become eligible for Social Security) that result in an early retirement monthly benefit greater than your monthly benefit at the Plan’s normal retirement age

Non-pension benefits such as health insurance, life insurance, certain death benefits, vacation pay and severance pay

Even if certain benefits aren’t guaranteed, you may still receive some of those benefits from the PBGC, depending on how much money the Plan has and on how much the PBGC collects from the employers.

For more information about the PBGC and the benefits it guarantees, ask the Plan Administrator or write to the following address:

Pension Benefit Guaranty Corporation Technical Assistance Division 1200 K Street, NW, Suite 930 Washington, DC 20005-4026

You may also call (800) 400-7242 or (202) 326-4000 (not a toll-free number). TTY/TDD users may call the federal relay service toll-free at (800) 877-8339 and ask to be connected to (202) 326-4000. Additional information about the PBGC’s pension insurance program is available through the PBGC’s website at www.pbgc.gov.

U.S. Pension Benefits Book 23

IMPORTANT TAX INFORMATION

You are responsible for reporting any payments you receive from the Plan as taxable income on your annual federal, state and local tax returns. You are also responsible for paying all applicable taxes. You will be provided with a special notice regarding applicable tax liabilities and/or related penalties when you receive a distribution of your Plan benefit. If you would like to receive a sample of this notice, please contact the Employee Service Center. However, the rules that determine your personal tax liabilities with respect to payments from the Plan are very complex and contain many conditions and exceptions that are not included in this document. Therefore, we encourage you to consult a professional tax adviser before you take a payment of your benefit from the Plan.

You can find more specific information on the tax treatment of payments from qualified retirement plans in IRS Publication 575 (Pension and Annuity Income) and IRS Publication 590 (Individual Retirement Arrangements). These publications are available from your local IRS office, on the IRS website at www.irs.gov or by calling (800) 829-3676.

Rolling Over Your Lump-Sum Distribution You may be eligible to receive payment of a lump-sum distribution from the Portable or Traditional Plan either (1) paid as a “direct rollover” to a traditional IRA, a Roth IRA or another eligible plan that will accept it, or (2) paid directly to you. Note that you can’t roll your payment over to a Simple IRA or a Coverdell Education Savings Account. If an employer plan accepts your rollover, the plan may require your spouse’s consent for any subsequent distribution. Check with the administrator of the plan that is to receive your rollover before you actually make the rollover.

Direct Rollover to a Traditional IRA (or Another Eligible Plan) If you choose a direct rollover, any portion of your payment that is an “eligible rollover distribution” is paid directly from the Plan to a traditional IRA, a Roth IRA or another eligible employer plan that accepts rollovers. You won’t be taxed on the payment until you later take it out of the IRA or other eligible employer plan. The Plan Administrator will tell you what portion of your payment is an “eligible rollover distribution” (certain types of payments are not eligible for a rollover).

If your new employer has a qualified retirement plan and you want to make a direct rollover to that plan, ask the administrator of that plan whether or not it will accept a rollover. This can include IRC Section 403(b) annuities and IRC Section 457 governmental plans.

If the employer plan accepts your rollover, the plan may provide restrictions on the circumstances under which you may later receive a distribution of the rollover amount, or the plan may require your spouse’s consent to any subsequent distribution. Check with the administrator of that plan before you make your decision.

Remember: An employer plan isn’t legally required to accept a rollover. If your new employer’s plan doesn’t accept a rollover, you can still choose to make a direct rollover to a traditional IRA or a Roth IRA.

U.S. Pension Benefits Book 24

Choosing a Direct Payment Instead of a Rollover Payment If you choose to have a Plan payment that’s eligible for rollover paid directly to you, you will receive only 80 percent of the payment, and the Plan will withhold 20 percent of the taxable amount of the payment and send it to the IRS on your behalf as income tax withholding. Your payment will be taxed in the current year, unless you roll it over within 60 days to an IRA or another eligible employer plan that accepts rollovers. If you choose to roll over 100 percent of the distribution, you must find other money within the 60-day period to contribute to an IRA or the other eligible employer plan to replace the 20 percent that was withheld. If you receive the payment before age 59½, you may also have to pay an additional 10 percent excise tax.

If any portion of your payment isn’t an eligible rollover distribution but is taxable, the mandatory withholding rules don’t apply. In this case, you may choose not to have withholding apply to that portion. The Plan Administrator can provide you with the appropriate election form.

FILING A CLAIM FOR BENEFITS

Your pension benefit payments may be distributed by direct deposit to a U.S. bank once the Employee Service Center receives the appropriate documentation. If you’re eligible for a benefit, you’ll receive a statement of deferred vested benefits approximately one month after your employment termination date. When you receive this deferred vested benefit statement, you should contact the Employee Service Center regarding when your benefit will start. This start date is subject to any procedural or distribution restrictions imposed by the Plan. The following table shows what information you’ll need, where to send your claim (if necessary) and the deadline to file for your benefits for the Plan.

How to receive benefits

Information needed Where to send your claim Deadline* and initial decision Visit Your Benefits Resources or call the Employee Service Center at (800) 585-5100 to initiate payment (outside U.S., call +1 (646) 254-3472).

Motorola Solutions Employee Service Center P.O. Box 785081 Orlando, FL 32878-5081

Deadlines vary based on the benefit being requested. See each Plan component’s individual section for more details.

Initial decision — made within 90 days after the claim is filed.

*Plus an extension of up to 90 days in special circumstances.

Denied Benefits Requests and the Appeals Process If you apply for a specific benefit and are denied, you can submit a claim to the Employee Service Center. Your claim must be in writing and may be either approved or denied. The decision will generally be made within 90 days of receiving your request. The following addresses what happens if your benefits claim is denied. You’ll also find information about your right to appeal a denial.

U.S. Pension Benefits Book 25

If Your Benefits Claim Is Denied If your claim for benefits is denied, you’ll receive a written notice explaining this denial. The notice will contain the following information:

The specific reasons for the denial

The specific Plan provisions upon which the denial is based

A description of any additional materials or information you’ll need to complete the claim for benefits, as well as an explanation of why those materials are necessary

An explanation of how to appeal the denial, including a statement of your right to bring a civil action under Section 502(a) of ERISA following an adverse benefit determination on final review

You have the right to request and receive reasonable access to and copies of relevant documents, records and other information that are in the possession of either Motorola Solutions or the Plan Administrator. You’re entitled to receive these documents free of charge. Relevant documents, records and other information are those that:

Were relied upon in making the benefit determination;

Were submitted, considered or generated in the course of making the benefit determination; and

Demonstrate compliance with the Plan’s administrative processes or safeguards and with your right to appeal.

If an initial claim for benefits under the Plan is denied, in whole or in part, you may request a review of the denial. Your request for review must be in writing, and it should contain the reasons why you believe you’re entitled to benefits, as well as any additional information or documentation to support your claim.

Request for Review The Plan Administrator will consider your request for review and notify you in writing of its decision within 60 days of receiving your request. If, because of special circumstances, the Plan Administrator can’t make a decision within the initial review period, the review period may be extended for up to an additional 60 days. If an extension is necessary, you’ll be notified before the end of the initial review period.

You’ll receive the final decision about your appeal in writing. This decision will give you the specific reasons for the decision and also provide you with the corresponding Plan provision(s). Except as required by law, the decisions are final and binding on all parties. You or your covered dependents must exhaust all of the internal administrative remedies described above before bringing an action for Plan benefits under Section 502(a) of ERISA.

In some cases, authority to decide appeals has been delegated to a third-party administrator.

U.S. Pension Benefits Book 26

PLAN ADMINISTRATIVE INFORMATION

Your Plan Rights and Responsibilities

No Alienation, Sale or Assignment To the extent permitted by law, and except as specified under the terms of the Plan, no benefits will be subject to alienation, sale, transfer, assignment, garnishment, execution or encumbrance of any kind. Any attempt to do so will be void. However, benefits under the Plan may be subject to a federal tax levy, or to a QDRO. See the “Qualified Domestic Relations Order” section of this SPD for more information or visit www.qocenter.com.

Recovery of Payments Made by Mistake If you receive any benefits or portion of benefits by mistake of fact or law, you are required to return these payments to the Plan.

No Contract of Employment Your participation in the Plan isn’t a guarantee of your continued employment with Motorola Solutions or rights to benefits, except as specified under the terms of the Plan. Nothing in the Plan or in this SPD confers any right of continued employment to any employee.

Severability If a court of competent jurisdiction finds, holds or deems any Plan provision described in this information to be void, unlawful or unenforceable under any applicable statute or other controlling law, the remainder of the Plan shall continue in full force and effect.

Statement of ERISA Rights As a Plan participant, you’re entitled to certain rights and protections under the Employee Retirement Income Security Act of 1974, as amended (“ERISA”). ERISA provides that you’re entitled to:

Receive information about your Plan and benefits.

Examine without charge, at Motorola Solutions, 1303 East Algonquin Road, Schaumburg, IL 60196, all Plan documents, including insurance contracts, and copies of all documents filed by the Plan with the U.S. Department of Labor and available at the Public Disclosure Room of the Employee Benefits Security Administration.

Obtain copies of documents governing the operation of the Plan, including insurance contracts, and copies of the latest annual report (Form 5500 Series) and updated Summary Plan Descriptions upon written request to the Plan Administrator. The Plan Administrator may make a reasonable charge for the copies.

U.S. Pension Benefits Book 27

Receive the Plan’s annual funding notice. The Plan Administrator is required by law to furnish each participant a copy of the notice each year.

Obtain a statement telling you whether you have a right to receive a benefit at normal retirement age (age 65) and, if so, what your benefit would be at normal retirement age if you stop working under the Plan now. This statement must be requested in writing. It’s not required to be given more than once every 12 months. The Plan must provide the statement free of charge.

Prudent Actions by Plan Fiduciaries In addition to creating rights for Plan participants, ERISA imposes duties upon the people who are responsible for operating the Plan. The people who operate the Plan, called fiduciaries, have a duty to do so prudently and in the interest of you and other Plan participants and beneficiaries.

No one, including your employer or any other person, may discharge you or otherwise discriminate against you in any way to prevent you from obtaining a benefit or exercising your rights under ERISA.

Enforce Your Rights If your claim for a benefit is denied, in whole or in part, you must receive a written explanation of the reasons for the denial. You have the right to know why this was done, to obtain copies of documents related to the decision without charge, and to appeal any denial, all within certain time schedules.

Under ERISA, there are steps you can take to enforce the above rights. For instance, if you request materials about the Plan and don’t receive them within 30 days, you may file suit in a federal court. In such a case, the court may require the Plan Administrator to provide the materials and pay you up to $110 a day until you receive the materials, unless the materials weren’t sent because of reasons beyond the control of the Plan Administrator.

If you have a claim for benefits that’s denied or ignored, in whole or in part, you may file suit in a state or federal court after you’ve exhausted the Plan’s claims procedures. In addition, if you disagree with the Plan’s decision or lack thereof concerning the qualified status of a Domestic Relations Order, you may file suit in federal court after you’ve exhausted the Plan’s claims procedures. If Plan fiduciaries misuse the Plan’s money, or if you’re discriminated against for asserting your rights, you may seek assistance from the U.S. Department of Labor or you may file suit in a federal court. The court will decide who should pay court costs and legal fees. If you’re successful, the court may order the person you’ve sued to pay these costs and fees. If you lose, the court may order you to pay these costs and fees if, for example, it finds your claim is frivolous.

Assistance with Your Questions For general questions regarding the Plan, contact the Employee Service Center. If you have any questions about this statement or about your rights under ERISA, or if you need assistance in obtaining documents from the Plan Administrator, contact the nearest office of the Employee Benefits Security Administration, U.S. Department of Labor, listed in your telephone directory, or the Division of Technical Assistance and inquiries, U.S. Department of Labor, Employee Benefits Security Administration, 200 Constitution Avenue, NW, Washington, DC 20210. You can also obtain certain publications about your rights and responsibilities under ERISA by calling the publications hotline of the Employee Benefits Security Administration Plan information.

U.S. Pension Benefits Book 28

Plan Administration The Plan Administrator has the sole and complete discretionary authority to determine eligibility for Plan benefits and to construe the terms of the Plan. This includes making any factual determinations. Plan benefits will be paid only if the Plan Administrator decides that the applicant is entitled to receive them. The Plan Administrator’s decisions shall be final and conclusive with respect to all questions related to the Plan.

The Plan Administrator may delegate responsibilities for performing certain duties under the terms of the Plan to others. The Plan Administrator may also seek such expert advice deemed reasonably necessary with respect to the Plan. The Plan Administrator will be entitled to rely upon the information and advice furnished by such delegates and experts, unless actually knowing such information and advice to be inaccurate or unlawful.

In addition, the Plan Administrator may adopt uniform rules for the administration of the Plan from time to time, as is deemed necessary or appropriate.

Amendment and Termination of the Plan Motorola Solutions reserves the sole discretionary right to modify, amend or terminate the Plan in any respect, at any time and from time to time, retroactively or otherwise, to the extent permitted by law.

If the Plan is modified, amended or terminated, you’ll be notified about how your Plan benefits or coverage will change. However, the modification, amendment or termination may be effective before you receive any notification. Motorola Solutions doesn’t need the consent of any employee or any other person in order to modify, amend or terminate the Plan described in this SPD.

No amendment of the Plan can divest any participant of his or her accrued benefit under the Plan, except in accordance with the terms of the Plan. If the Plan is terminated, benefits may be paid for vested benefits as of the date of Plan termination.

Representations Contrary to the Plan No employee, director or officer of Motorola Solutions has the authority to alter, vary or modify the terms of the Plan, except by means of a duly authorized written amendment to the Plan. No verbal or written representations contrary to the terms of the Plan are binding upon the Plan, the Plan Administrator or Motorola Solutions.

Applicable Law The Plan described here is governed and construed in accordance with the laws of the state of Illinois to the extent not pre-empted by federal law.

U.S. Pension Benefits Book 29

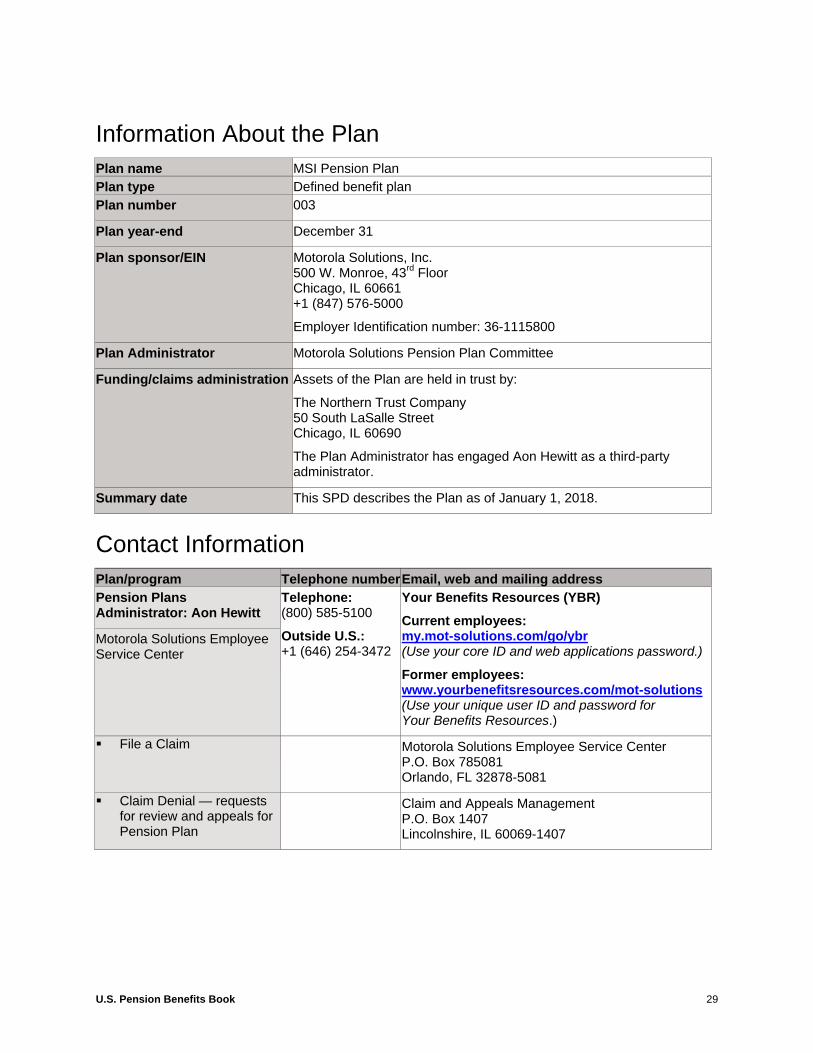

Information About the Plan

Plan name MSI Pension Plan Plan type Defined benefit plan Plan number 003

Plan year-end December 31