Embed Size (px)

Citation preview

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 1/73

Munich Personal RePEc Archive

Valuation of 2G spectrum in India- A

real option approach

Pankaj Sinha and Nataraj Sathiyanarayanan

Faculty of Management Studies, University of Delhi

21. May 2012

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 2/73

Valuation of 2G spectrum in India- A real option approach

Pankaj Sinha and Nataraj Sathiyanarayanan

Faculty of Manaement Studies

!ni"ersity of #elhi

Abstract

The phenomenal growth of telecommunication sector in India has largely been possible due to

the contributory factors such as the efforts made by private and public telecom service providers

to make services affordable to the mass market, reduction in entry barrier due to drastically

lowered entry level price for devices, changing demographic profile and the increasing per-capita

income. However, it the issue of spectrum pricing that has captured the centre stage with the high

prices realized from the 3 and !"# spectrum auction and the outburst of the $ %pectrum

scam in India.

In this paper, we use both the traditional valuation method-&iscounted 'ash (low as well as the

)eal *ption approach that takes into consideration managerial fle+ibility and strategic decision

making aspects. The analyses have been done individually as the factors determining revenues

and thereby the spectrum values are e+pected to be different. !y dividing the &'( or )* value

thus arrived by the total spectrum allotted so far in the service areas, we obtain the price of

Hz of spectrum # sensitivity analysis has also been done to check the variations arising in the

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 3/73

1. Introduction

The last two decades have seen India emerging as one of the biggest telecom markets in the

world. The Indian telecommunication sector in India is the third largest sector across the globe

and the second largest among the emerging economies of #sia. This rapid growth has been

possible due to various proactive and positive decisions of the overnment and contribution of

both the public and the private sector. The rapid strides in the telecom sector have been

facilitated by liberal policies of the overnment providing the telecom e7uipments an easy

access to the market and a fair regulatory framework for offering telecom services to the Indian

consumers at affordable prices. However, it the issue of spectrum pricing that has captured the

centre stage with the high prices realized from the 3 and !"# spectrum auction and the

outburst of the $ %pectrum scam.

"ith the recent cancellation of $$ license awarded in $552 by the %upreme 'ourt and the

impending auction of spectrum, it is imperative for 'ompanies to arrive at a price that they can

pay to ac7uire a piece of the spectrum. #lso, from a overnment perspective, it is important to

set a base price for the auction, given its ob8ectives of overall benefit to the larger mass and

ma+imization of overnment revenues.

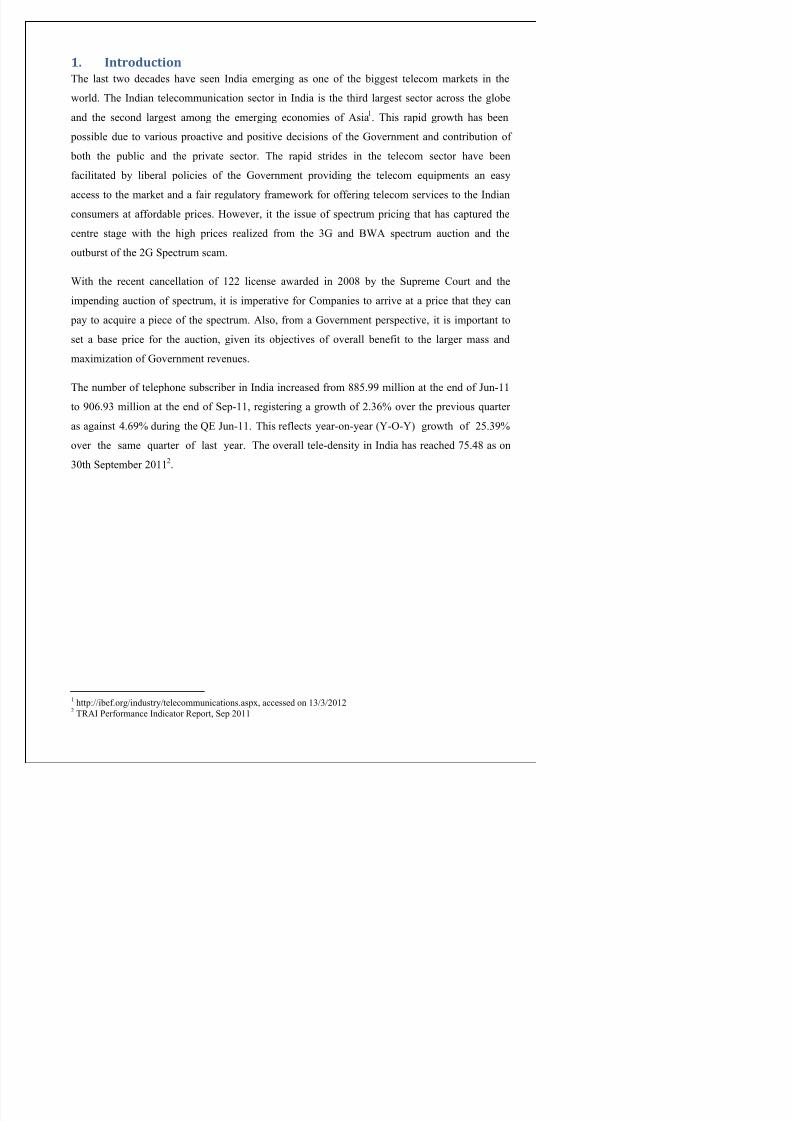

The number of telephone subscriber in India increased from 221.99 million at the end of :un-to 954.93 million at the end of %ep-, registering a growth of $.34; over the previous 7uarter

as against <.49; during the => :un-. This reflects year-on-year ?@-*-@A growth of $1.39;

over the same 7uarter of last year. The overall tele-density in India has reached 1.<2 as on

35th %eptember $5$.

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 4/73

Fiure $% &rends in &elephone su'scri'ers and &eledensity in India

Source% &(AI

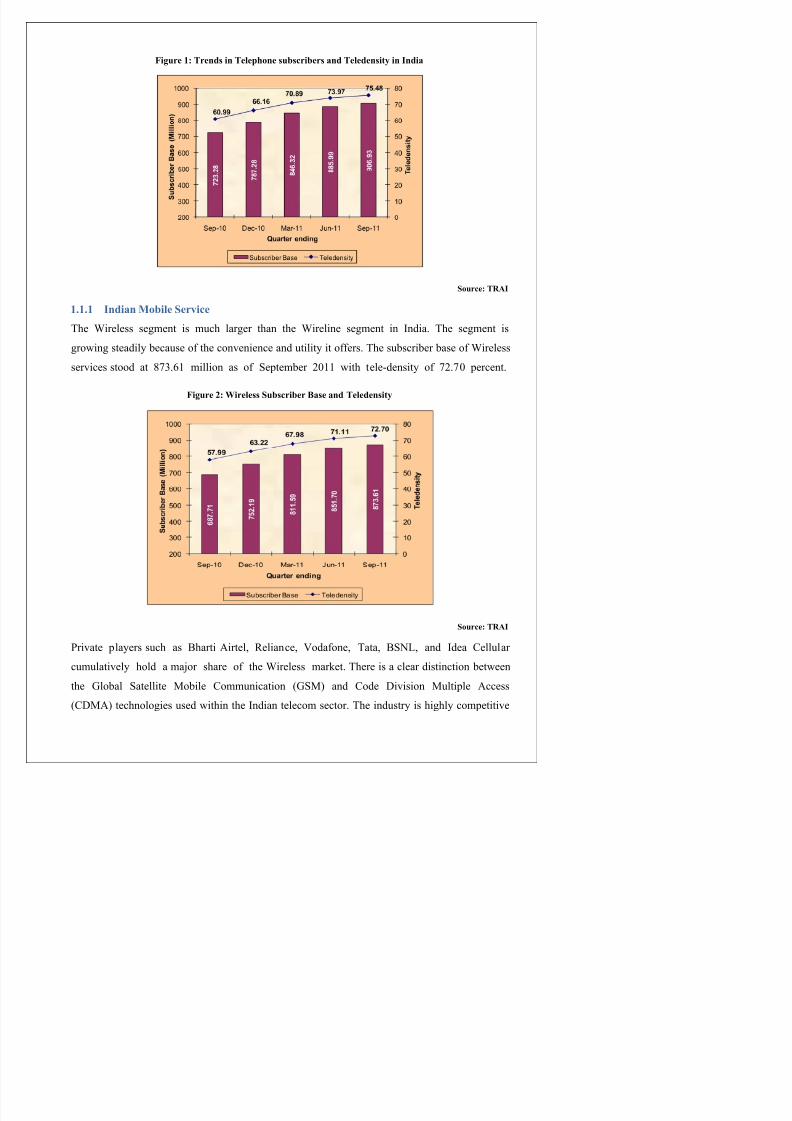

$)$)$ Indian Mo'ile Ser"ice

The "ireless segment is much larger than the "ireline segment in India. The segment is

growing steadily because of the convenience and utility it offers. The subscriber base of "ireless

services stood at 23.4 million as of %eptember $5 with tele-density of $.5 percent.

Fiure 2% *ireless Su'scri'er +ase and &eledensity

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 5/73

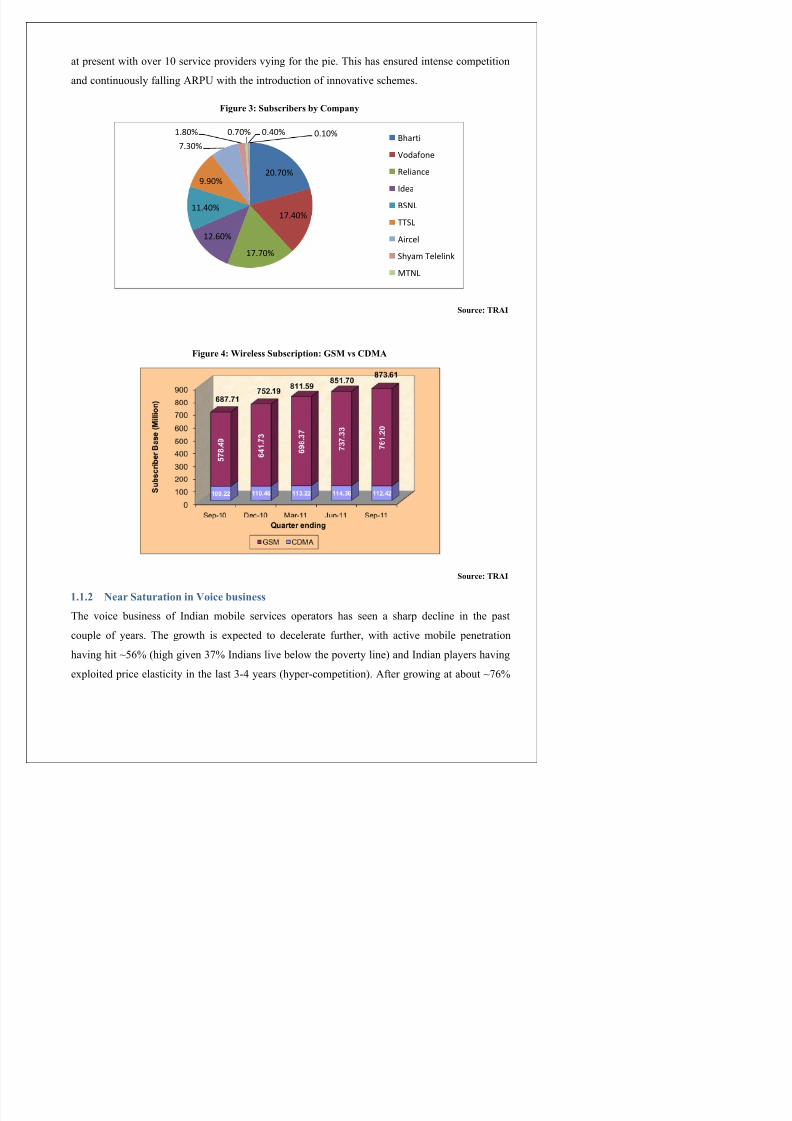

at present with over 5 service providers vying for the pie. This has ensured intense competition

and continuously falling #)/0 with the introduction of innovative schemes.

Fiure ,% Su'scri'ers 'y ompany

Source% &(AI

Fiure .% *ireless Su'scription% GSM "s #MA

20.70%

17.40%

17.70%

12.60%

11.40%

9.90%

7.30%

1.80% 0.70% 0.40% 0.10%Bharti

Vodafone

Reliance

Idea

BSNL

SL

!ircel

Sh"a# elelin$

NL

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 6/73

'#) over (@51-59, voice growth has slowed to $2; over (@59- and is likely to fall further

to $; in (@$3.

This is a structural shift in voice minutes and a build in volume growth of 2; for (@$-<>.

$)$), /ih ompetition in the sector

The Indian wireless market has witnessed very high competition. Typically, the wireless market

is an oligopoly of 3-1 players. However, the Indian telecom market has < operators with a

Harfindahl inde+ of less than 5.$. #lthough a recent %upreme 'ourt order cancelling $$ licenses

issued in :anuary $552 may reduce the number of players, competitive intensity is likely to

remain high with at least 4- players with sizeable presence andC or deep pockets.

1.2

Spectrum Allocation and Pricing

The 'ountry is divided into $$ %ervice #reas consisting of 9 Telecom 'ircle %ervice #reas and

3 etro %ervice #reas for providing 'ellular obile Telephone %ervice ?'T%A.

$)2)$ Supreme ourt0s ancellation of 2G !AS license

The %upreme 'ourt of India ordered all the $$ 0#% licences issued in :anuary $552 following

$ spectrum auction. The companies whose licenses were scrapped are 0ninor, %istema

%hyam, %Tel, ideocon, Idea 'ellular, Tata Teleservices, Eoop Telecom and >tisalat &!.These eight companies invested a total of ID) 315-<55 mn to ac7uire $ license. The court also

ordered Tata Teleservices, 0nitech "ireless roup and >tisalat &! Telecom to pay ID) 15 mn

and Eoop Telecom Etd, % Tel Etd, #llianz Infratech Etd and %istema %hyam Teleservices Etd to

pay ID) 1 mn as fine each. The cancellation of licenses will release <5 Hz of $

spectrum across India. %upreme 'ourt also asked Telecom )egulatory #uthority of India

?T)#IA to prepare fresh recommendations within two months, to grant license and allocate

$ spectrums in $$ service areas via auction, similar to previous 3 auction.

$)2)2 #1&0s recent #ecisions

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 7/73

#dditionally, assignment of balance of contracted spectrum may need to be ensured for e+isting

licensees who have so far been allocated only the start up spectrum of <.< Hz. *nly in respect

of the licences that will be found valid after the process is completed, the additional .2

Hz will be assigned on their becoming eligible, but the spectrum will be assigned to them

at a price determined under the new policy.

Do more 0#% licences linked with spectrum will be awarded. #ll future licences will be 0nified

Eicences and allocation of spectrum will be delinked from the licence. %pectrum, if re7uired,

will have to be obtained separately. The prescribed limit on spectrum assigned to a service

provider will be $+2 HzC$+1 Hz for %C'&# technologies for all service areas other

than in &elhi and umbai where it will be $+5HzC$+4.$1Hz. However, the licensee can

ac7uire additional spectrum beyond prescribed limits, in the open market, should there be an

auction of spectrum sub8ect to the limits prescribed for merger of licences.

In respect of spectrum obtained through auction, spectrum sharing will be permitted only if the

auction conditions provide for the same. %pectrum trading will not be allowed in India, at

this stage.

$), Spectrum Pricin

iven, the above scenario, we have attempted to price the spectrum. "e do this by finding the

value generated to a potential buyerCoperator on ac7uiring this license. %ince, value changes

depending on the circle of operationG we have calculated the price of hz of spectrum in

etros, 'ategory # and 'ategory ! service areas.

2) iterature (e"ie3

In this section, we shall first look at the various attempts made to price the $ telecom spectrum,

specifically the consulting papers issued by T)#I and the responses from the telecom

i E l k i h ) l * i l i # h i d i l i

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 8/73

$. The %ubstitution approach where the 'obb-&ouglas function is used to arrive at the

opportunity cost of spectrum which is treated as an input for supply of mobile services.

ost of the telecom companies have been critical of the suggested price arrived at by T)#I in

the above consultation paper. %pecifically, /lum 'onsulting in its report for odafone 1 critically

e+amines the shortcomings and also lists down some of the practices applied in some of the other

countries in finding the spectrum price. The report talks about two approaches to pricing

spectrum viz. arket !enchmarks and !ottom-up approaches. iven the drawbacks of arket

!enchmarks, the focus is on the !ottom-up approach. The two approaches, as also used by

T)#I, falling under this category are the &'( approach and the cost reduction value. The two

approaches give a range of values for pricing the spectrum, the ma+imum value being

determined by the &'( approach and the minimum value determined by the cost reduction

approach.

Eet us now look at the literature review of the &'( and the )eal *ptions #pproach.

&iscounted 'ash (low ?&'(A valuation is the most common method to value real assets whose

future cash flows can be forecasted with certain degree of predictability. The net present value of

a pro8ect can be calculated by discounting the cash flows which are e+pected from the pro8ect at

a certain discount rate which represents the risk of the pro8ect. This discount rate is weighted

average cost of capital for a pro8ect whose risk matches the average risk of the pro8ects of the

firm. However if a pro8ects risk differs considerably from the firms average risk then the

"#'' is ad8usted upwards or downwards to arrive at the new discount rate for the pro8ect

depending on whether the pro8ect is more risky or less risky respectively ?!randao, &yer,

Hahn, $551A.

&'( method is criticized for one of its inherent and structural weakness which is that the

pro8ects value will remain same and unaffected despite any future decisions by the management

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 9/73

'onsider an investment where a pharmaceutical company invests in the trial of a new drug, if the

trial is successful the company will launch the new drug in the market if it is not then the

company would stop further research and development in this new drug. Though this is a pretty

straight forward scenario where the financial manager can incorporate decision tree analysis to

evaluate the scenario, however actual problems in real life can be very different and in such

cases instead of investing all capital upfront a more strategic investment plan might be the need.

%ome of the e+amples of pro8ect fle+ibilities are ?!randao, &yer, Hahn, $551A,

• >+panding operations in response to affirmative response from the market

• &eferring a particular investment or abandoning it completely if it underperforms

• %caling down the pro8ect in case the pro8ect has reached a maturity state and the returns

have hit the cap.

#s the uncertainty in various facets of long term and strategic investments increases )eal options

will find broad application as a strategic tool. Eeslie and ichaels ?Eeslie ichaels, 99A

discuss some of the fundamental differences that e+ist between the traditional discounted cash

flow valuation ?&'(A and the )eal option valuation using !lack %choles erton options

theory.

They argue that traditional methods like &'( ignore the value of fle+ibility and strategic

decision making and hence they tend to ignore the additional value embedded in investment

opportunities where the investment is irreversible and constitutes a huge cost to the company

?Eeslie ichaels, 99A. )eal option methodology empowers the management to capture the

value of this fle+ibility ?#lleman, $55$A.

&'( methodology assumes that the capital investment decision is a one-time decision, however

when a high amount of capital is involved such huge investment decisions are rarely taken in one

go and rather they are strategic decisions and receive a continuous feedback from the limited

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 10/73

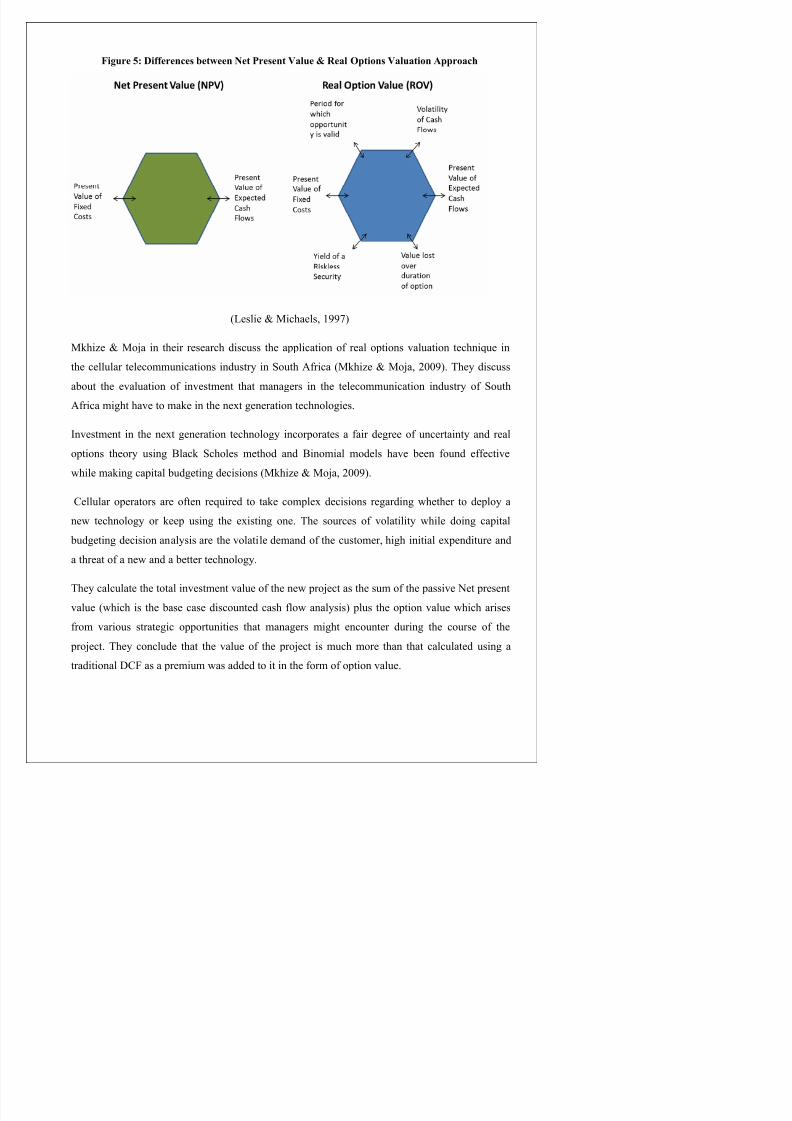

Fiure 4% #ifferences 'et3een Net Present Value 5 (eal 1ptions Valuation Approach

?Eeslie ichaels, 99A

khize o8a in their research discuss the application of real options valuation techni7ue in

the cellular telecommunications industry in %outh #frica ?khize o8a, $559A. They discuss

about the evaluation of investment that managers in the telecommunication industry of %outh#frica might have to make in the ne+t generation technologies.

Investment in the ne+t generation technology incorporates a fair degree of uncertainty and real

options theory using !lack %choles method and !inomial models have been found effective

while making capital budgeting decisions ?khize o8a, $559A.

'ellular operators are often re7uired to take comple+ decisions regarding whether to deploy a

new technology or keep using the e+isting one. The sources of volatility while doing capital

budgeting decision analysis are the volatile demand of the customer, high initial e+penditure and

h f d b h l

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 11/73

#nother application of real options valuation techni7ue is e+plained by !asili (ontini in their

valuation of the 3 license in the 0nited Lingdom ?!asili (ontini, $553A. They calculated the

aggregate option value of the 3 licenses which were auctioned in 0L in the year $555.

Telecommunications industry is considered to be one of the central bones of the economy and

the application of auction to allocate 3 airwaves to various bidders is considered to be one of

the most effective economic paradigms of a real life problem ?!asili (ontini, $553A.

The revenues which were generated in the auction e+ceeded the governments initial estimate by

a far greater amount. Though the government received a windfall in the auction process the

operators were tied down under huge debt burden and within $ years after the auctions >uropean

telecommunication firms started doubting the ability of an auction to ma+imize the total surplus

and not 8ust the governments surplus. The stocks of the firms which had bid for the license

performed badly after the auctions which led analysts to believe that the market is discountingthe future earnings of these firms at a higher discount rate because of the perceived risk because

of heavy debt burden ?!asili (ontini, $553A.

The option value of the license is calculated in the article and it has been shown that the value of

the pro8ect roughly corresponds to the value of the fees e+tracted from the bidders ?!asili

(ontini, $553A.

It is widely believed that the telecommunication firms in the >urope lost a lot market value

because of the perceived high price paid for the 3 spectrum, nonetheless, a real option

valuation shows that the value e+tracted from the pro8ect is appro+imately e7ual to the value paid

for the licenses.

The loss in value of the telecom firms could not be e+plained on the basis of the high prices paid

for the license, instead the authors brings in the discussion of a very crucial aspect of the 3

technology which is the killer application that is re7uired to get the users hooked to your network

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 12/73

#nother recent literature in this field tries to evaluate the value of the transferability value of the

telecommunication license. The driver behind such kind of research is the fact that in most of the

nation when government allots a telecommunication license it also stipulates that the license

could not be transferred to another telecom operators. %tipulation like the one mentioned above

might cause inconvenience to the customers and hence removal of the option is the best solution

in such cases. "hen removal is considered there is an added value to the original license and

hence an option is embedded in the original license which should be valued to arrive at the final

price of the license ?astroeni Daldi, $55A.

In most of the countries when the government assigns the telecommunication licenses to various

firm, they also set out certain time bound conditions like rollout etc. In case a company is not

able to achieve its target within the stipulated time, the government might reassign the spectrum

but that would take a lot of time and resources. If the government allows reselling of the

spectrum the bidders would look at this as an embedded option in the license which gives them

an option to e+it the pro8ect in case it doesnt suit their operations. This also will increase the

value of the license at the time of the auction ?astroeni Daldi, $55A.

In their paper %tille, Eimme and !randao analyze the real option methodology in the &ecision

making process in the Telecommunication Industry. They study the 3 license auctions whichallocated 3 spectrums to various operators who wish to operate 3 mobile services in !razil

?%tille, Eemme, !randao, $55A. They had calculated 4<; premium on the license when the

value of the license was calculated using )eal options methodology as compared to discounted

cash flow methodology.

The degree of similarity that they brought forward between a license and auction so as to 8ustify

their methodology of following real options valuation is ?%tille, Eemme, !randao, $55A,

• There are a large number of factors which make the investment in the rollout of the

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 13/73

• The third characteristic of the license that increases its option value and thus 8ustifying

the use of real options methodology is that the license represents a strong barrier to entry

from the competition and hence increases the value of the option.

The methodology that they follow is a pretty straightforward one. The follow the following

se7uence ?%tille, Eemme, !randao, $55A,

• 'alculate the static D/ of the asset which in this case is license. D/ is calculated

using e+pected level of cash flows generated from the license and the "#''.

• In the ne+t step they calculated the volatility of the returns of the pro8ect.

• *nce they had the volatility they proceeded to the option valuation step.

%o far we have discussed the advantages of real option valuation methodology versus the

discounted cash flow valuation methodologyG we then discussed some of the relevant literature

e+ploiting the importance of real option valuation methodology.

Though real options have wide applications across various 'apital investment decision situations

practitioners do get bogged down by the higher mathematics involved in the real options

valuation theory. # simple framework which could be applied to various practical situations and

is backward compatible with the &iscounted 'ash (low valuation method and valuation sheets is

provided by Euehrman in an article in Harvard Business Review ?Euehrman, 992A.

Though the framework is not that effective when the analysis re7uires absolute precision

however it gives a good starting point to analyze strategic decision making under uncertainty. *n

top of giving a good head start the valuation and insights that the framework provides are

definitely better than the base case &'( analysis. Euehrman draws an analogy between an

investment opportunity before a company to a call option as the organization has a right to invest

but is not under the obligation to do so. Euehrman considers the case of a >uropean 'all *ption

and then he tries to map the parameters of the investment opportunity over the parameters of the

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 14/73

have tried to calculate the value of hz of spectrum block for which the methodology has been

e+plained below,

• # discounted cash flow analysis has been done on the e+pected earnings ?cash-flowsA

which would accrue in a service area from $ operations, considering the current level of

revenues. The &'( analysis serves as the base case for our real option valuation purpose and

some of the outputs which would be generated in the process of doing &'( would be used to

calculate the option value of the pro8ect. The pro8ections and assumptions used for estimating the

future earningsCcash-flows are e+plained in a later chapter.

• %ensitivity analysis is done on the D/ obtained from the &'( model to see the risk

associated with the pro8ect.

• )eal option valuation is the last step in the valuation process to calculate the value of the

option. The model which is used is e+plained in a further section.

,)$ #iscounted ash Flo3 Valuation

0nder the purview of discounted cash flow valuation the following two methods are used,

• Net Present Value Method . 0nder D/ method, net present value of the company is

calculated by discounting the cash flows from a pro8ect at a risk ad8usted rate of return. D/ is

the difference of the present value of cash inflows from the pro8ect and the present value of the

investment overlay that will go into the pro8ect.

= ( 1 + )

Where,

T – Useful life of the projet

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 15/73

The above e7uation could be re-written as,

= −

Where,

& – Net present value of the ash inflows fro$ the projet

' – Net present value of the invest$ent overla% for the projet

The figure thus arrived gives the value of spectrum. However, the price charged to the operator

must allow a reasonable rate of return on their investment. "e have taken the value to be $5;4.

The shadow price of spectrum to be charged is then calculated using the formula.

= + 20 ! ( " 20#)

Though we discussed the disadvantages of the &'( valuation in the previous section, 8ust to

reiterate, the main disadvantage of using D/ method is aptly highlighted by ?!randao, &yer,

Hahn, $551A contending that D/ method doesnt take into consideration managerial fle+ibility

and hence strategies like Jwait and seeK and Jpilot pro8ectK cant be taken into account while

valuing the pro8ect.

%ince &'( valuation will serve as a base case scenario we will first try to calculate the D/ of

the pro8ect before doing a real option valuation.

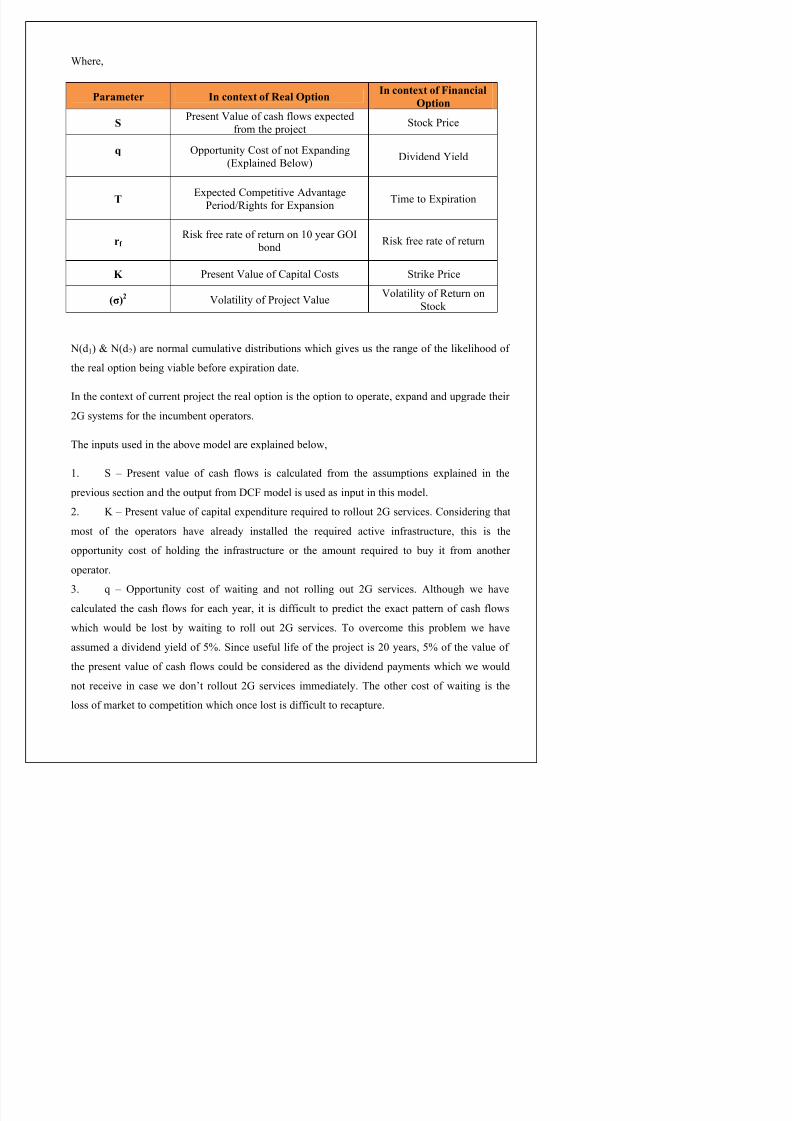

,)2 (eal 1ption Valuation

"e will now discuss the model that we will use to calculate the value of the real option. (or

calculating the value we will use the !lack-%choles model ?&amodaran, $555A,

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 16/73

"here,

Parameter In conte6t of (eal 1ption

In conte6t of Financial

1ption

S/resent alue of cash flows e+pected

from the pro8ect%tock /rice

7 *pportunity 'ost of not >+panding

?>+plained !elowA&ividend @ield

&>+pected 'ompetitive #dvantage

/eriodC)ights for >+pansion Time to >+piration

rf )isk free rate of return on 5 year *I

bond)isk free rate of return

8 /resent alue of 'apital 'osts %trike /rice

9:;2 olatility of /ro8ect alue olatility of )eturn on%tock

D?dA D?d$A are normal cumulative distributions which gives us the range of the likelihood of

the real option being viable before e+piration date.

In the conte+t of current pro8ect the real option is the option to operate, e+pand and upgrade their

$ systems for the incumbent operators.

The inputs used in the above model are e+plained below,

. % 6 /resent value of cash flows is calculated from the assumptions e+plained in the

previous section and the output from &'( model is used as input in this model.

$.

L 6 /resent value of capital e+penditure re7uired to rollout $ services. 'onsidering that

most of the operators have already installed the re7uired active infrastructure, this is the

opportunity cost of holding the infrastructure or the amount re7uired to buy it from another

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 17/73

<. t 6 This is the time period over which the option should be e+ercised lest the telecom

operators will lose competitive edge. *n top of that T)#I has set certain rollout obligations

which involve covering 95; of the metro areas and 15; of &H=s within $ years of allotment of

$ license which effectively translates the e+pansion of $ services by a company as a series of

call options. However we are taking an appro+imation here that the telecom operators need to

rollout the $ services within $ years.

1.

r f 6 )isk free rate on 5 year *I. The yield on 5 year *I bond is .9<; in arch .

6.

M 6 olatility of pro8ect is difficult to estimate and theoretically a onte-'arlo analysisneeds to be done with all relevant probability distributions of the input variables. %ince we dont

have the relevant probability distribution we have used annualized standard deviation of returns

of !ombay %tock >+change Technology, edia and Telecom Inde+ ?!%> T>'LA as a pro+y

which is e7ual to F$2;.

.) #ata 5 Assumptions

The data for the purpose of valuation has been taken from public sources and sector reports. &ata

has also been estimated for some of the years by taking assumptions. "e will now discuss

various data points and assumptions. "e will take the e+ample of aharashtra to show the

assumptions used. #ssumptions for all the other states can be found in the #ppendi+.

.)$ (e"enue Projections

To calculate future revenues and cash-flows it becomes important for us to look at the drivers of

the revenue. In telecommunication industry the important metrics which are looked at are the

number of subscribers and the average revenue per user ? ARPU A.

8 = 9: ;< !

Dow we have two variables to forecast on the basis of above e7uation. "e will look into them

one by one. %ince, we have both % and '&# operators in a service area, we further split

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 18/73

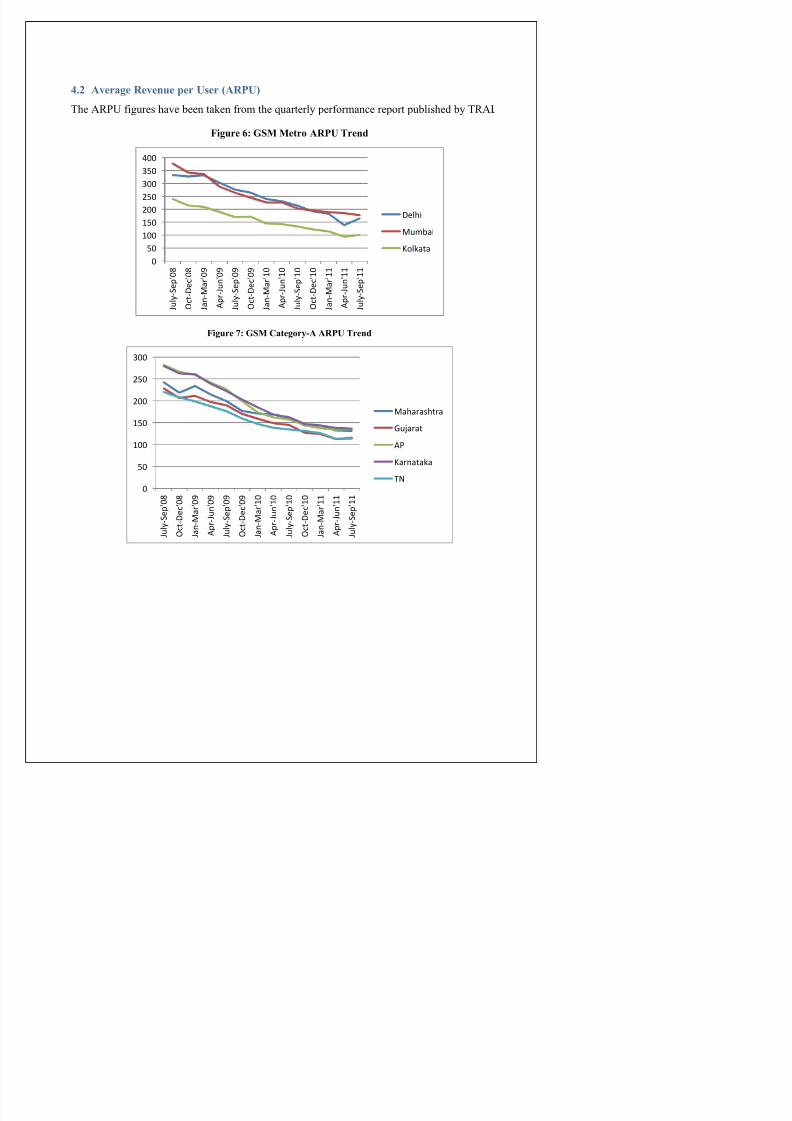

.)2 A"erae (e"enue per !ser 9A(P!;

The #)/0 figures have been taken from the 7uarterly performance report published by T)#I.

Fiure <% GSM Metro A(P! &rend

Fiure =% GSM ateory-A A(P! &rend

0

&0

100

1&0

2002&0

300

3&0

400

' ( l " ) S e * + 0 8

, c t ) - e c + 0 8

' a n ) % a r + 0 9

! * r

) ' ( n + 0 9

' ( l " ) S e * + 0 9

, c t ) - e c + 0 9

' a n ) % a r + 1 0

! * r

) ' ( n + 1 0

' ( l " ) S e * + 1 0

, c t ) - e c + 1 0

' a n ) % a r + 1 1

! * r

) ' ( n + 1 1

' ( l " ) S e * + 1 1

-elhi

(#ai

/ol$ata

0

&0

100

1&0

200

2&0

300

' ( l " ) S e * + 0 8

, c t ) - e c + 0 8

' a n ) % a r + 0 9

! * r ) ' ( n + 0 9

' ( l " ) S e * + 0 9

, c t ) - e c + 0 9

' a n ) % a r + 1 0

! * r ) ' ( n + 1 0

' ( l " ) S e * + 1 0

, c t ) - e c + 1 0

' a n ) % a r + 1 1

! * r ) ' ( n + 1 1

' ( l " ) S e * + 1 1

aharahtra

(arat

!

/arnata$a

N

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 19/73

Fiure >% GSM ateory-+ A(P! &rend

Fiure ?% GSM ateory- A(P! &rend

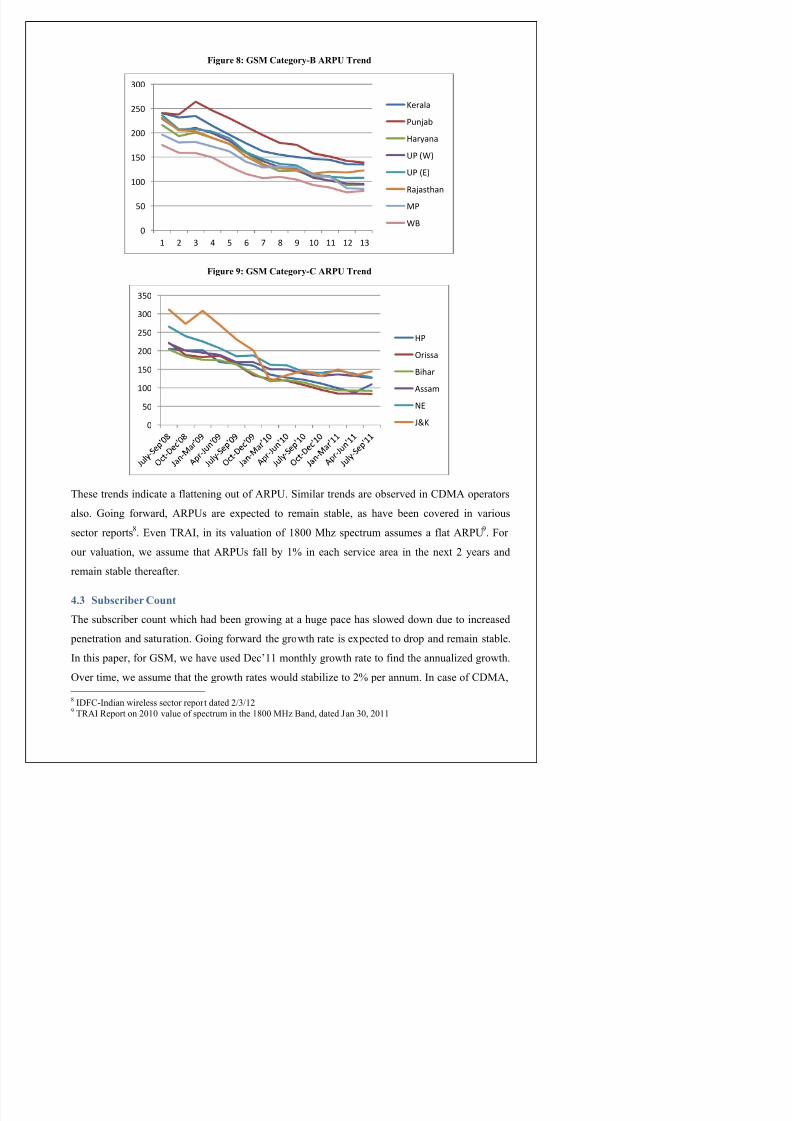

These trends indicate a flattening out of #)/0. %imilar trends are observed in '&# operators

also. oing forward, #)/0s are e+pected to remain stable, as have been covered in various

sector reports2. >ven T)#I, in its valuation of 255 hz spectrum assumes a flat #)/09. (or

our valuation, we assume that #)/0s fall by ; in each service area in the ne+t $ years and

0

&0

100

1&0

200

2&0

300

1 2 3 4 & 6 7 8 9 10 11 12 13

/erala

(na

ar"ana

5

5

Raathan

B

0

&0

100

1&0

200

2&0

300

3&0

,ria

Bihar

!a#

N

':/

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 20/73

most of the states have e+perienced very low rated of around $;-<; and some even negative,

we have assumed a flat rate of $; growth rate.

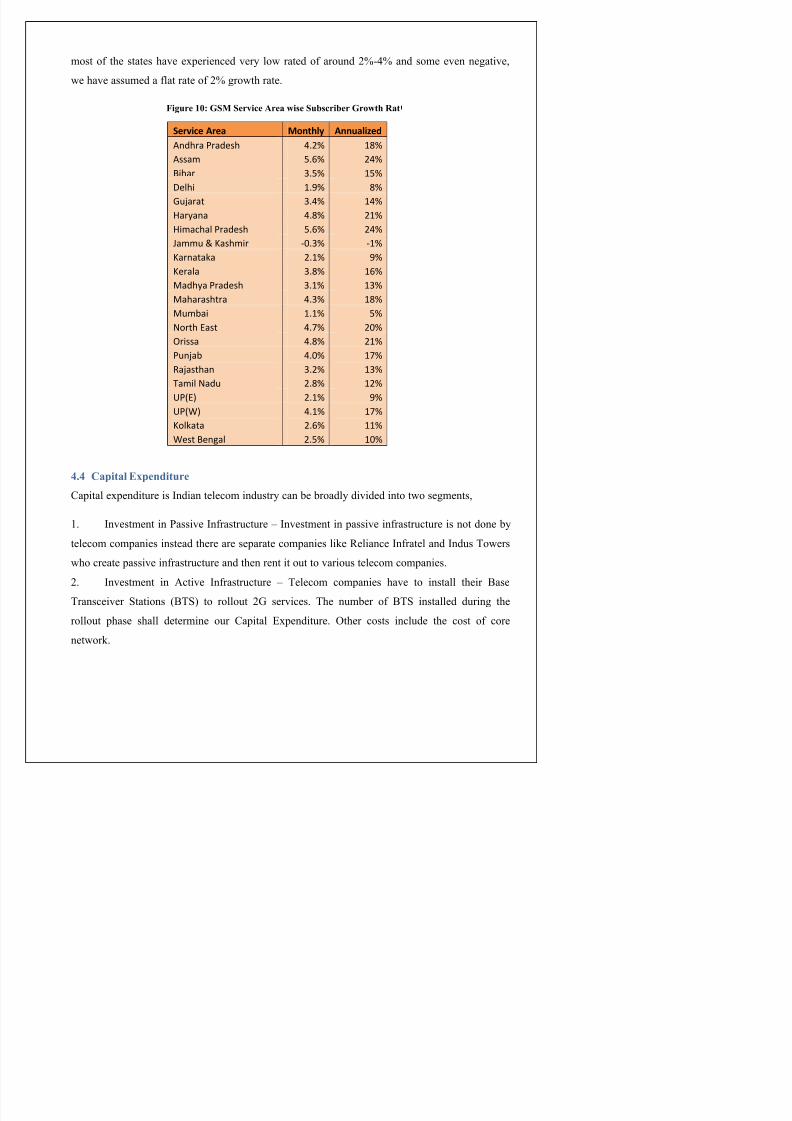

Fiure $@% GSM Ser"ice Area 3ise Su'scri'er Gro3th (at

Service Area Monthly Annualized

!ndhra radeh 4.2% 18%

!a# &.6% 24%

Bihar 3.&% 1&%

-elhi 1.9% 8%

(arat 3.4% 14%

ar"ana 4.8% 21%

i#achal radeh &.6% 24%

'a##( : /ah#ir )0.3% )1%

/arnata$a 2.1% 9%

/erala 3.8% 16%

adh"a radeh 3.1% 13%

aharahtra 4.3% 18%

(#ai 1.1% &%

North at 4.7% 20%

,ria 4.8% 21%

(na 4.0% 17%

Raathan 3.2% 13%

a#il Nad( 2.8% 12%

5 2.1% 9%

5 4.1% 17%

/ol$ata 2.6% 11%

et Ben;al 2.&% 10%

.). apital 6penditure

'apital e+penditure is Indian telecom industry can be broadly divided into two segments,

.

Investment in /assive Infrastructure 6 Investment in passive infrastructure is not done by

telecom companies instead there are separate companies like )eliance Infratel and Indus Towers

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 21/73

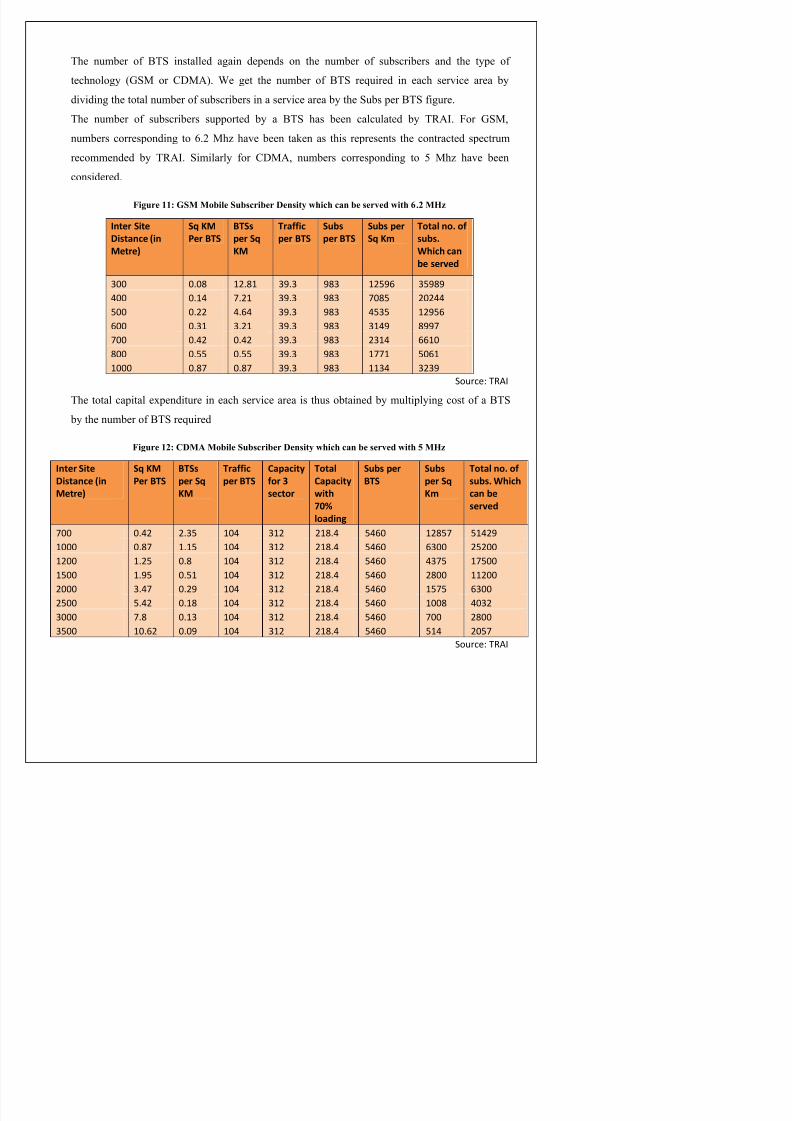

The number of !T% installed again depends on the number of subscribers and the type of

technology ?% or '&#A. "e get the number of !T% re7uired in each service area by

dividing the total number of subscribers in a service area by the %ubs per !T% figure.The number of subscribers supported by a !T% has been calculated by T)#I. (or %,

numbers corresponding to 4.$ hz have been taken as this represents the contracted spectrum

recommended by T)#I. %imilarly for '&#, numbers corresponding to 1 hz have been

considered.

Fiure $$% GSM Mo'ile Su'scri'er #ensity 3hich can 'e ser"ed 3ith <)2 M/B

Inter Site

Distance (in

Metre)

Sq KM

Per BTS

BTSs

per Sq

KM

Traffic

per BTS

Sus

per BTS

Sus per

Sq K!

Total no" of

sus"

#hich can

e served

300 0.08 12.81 39.3 983 12&96 3&989

400 0.14 7.21 39.3 983 708& 20244&00 0.22 4.64 39.3 983 4&3& 129&6

600 0.31 3.21 39.3 983 3149 8997

700 0.42 0.42 39.3 983 2314 6610

800 0.&& 0.&& 39.3 983 1771 &061

1000 0.87 0.87 39.3 983 1134 3239

So(rce< R!I

The total capital e+penditure in each service area is thus obtained by multiplying cost of a !T%

by the number of !T% re7uired

Fiure $2% #MA Mo'ile Su'scri'er #ensity 3hich can 'e ser"ed 3ith 4 M/B

Inter Site

Distance (in

Metre)

Sq KM

Per BTS

BTSs

per Sq

KM

Traffic

per BTS

$apacity

for %

sector

Total

$apacity

&ith'

loadin*

Sus per

BTS

Sus

per Sq

K!

Total no" of

sus" #hich

can eserved

700 0.42 2.3& 104 312 218.4 &460 128&7 &1429

1000 0.87 1.1& 104 312 218.4 &460 6300 2&200

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 22/73

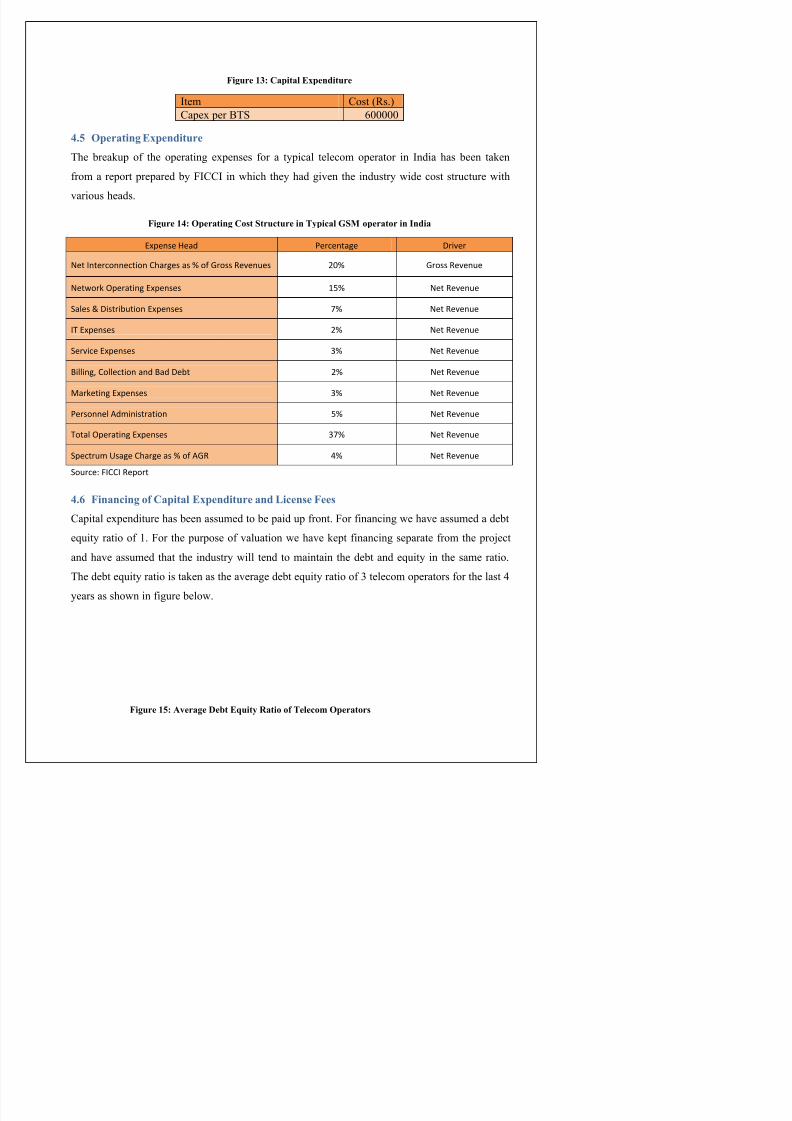

Fiure $,% apital 6penditure

Item 'ost ?)s.A'ape+ per !T% 455555

.)4 1peratin 6penditure

The breakup of the operating e+penses for a typical telecom operator in India has been taken

from a report prepared by (I''I in which they had given the industry wide cost structure with

various heads.

Fiure $.% 1peratin ost Structure in &ypical GSM operator in India

=*ene ead ercenta;e -ri>er

Net Interconnection ?har;e a % of ro Re>en(e 20% ro Re>en(e

Net@or$ ,*eratin; =*ene 1&% Net Re>en(e

Sale : -itri(tion =*ene 7% Net Re>en(e

I =*ene 2% Net Re>en(e

Ser>ice =*ene 3% Net Re>en(e

Billin;A ?ollection and Bad -et 2% Net Re>en(e

ar$etin; =*ene 3% Net Re>en(e

eronnel !d#initration &% Net Re>en(e

otal ,*eratin; =*ene 37% Net Re>en(e

S*ectr(# 5a;e ?har;e a % of !R 4% Net Re>en(e

So(rce< I??I Re*ort

.)<

Financin of apital 6penditure and icense Fees

'apital e+penditure has been assumed to be paid up front. (or financing we have assumed a debt

e7uity ratio of . (or the purpose of valuation we have kept financing separate from the pro8ect

d h d th t th i d t ill t d t i t i th d bt d it i th ti

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 23/73

Debt Equity Ratio

'ompany $552 $559 $55 $5 #verage

!harti #irtel 5.< 5.33 5.$2 5.< 5.351

Idea 'ellular .91 .2< 5.4 5.1 .$11

)eliance 'ommunications 5. 5.2$ 5.4 5.<2 5.41$1

#verage 5.32

%ourceB oneycontrol

.)= #epreciation 5 AmortiBation

(or depreciation of capital e+penditure and amortization of license fees a period of $5 years has

been considered and straight line method has been assumed.

.)> ost of apital

"eighted average cost of capital is calculated using the following formula,

D9 = E ; DE + F ; DF ; (1 − 6)

"here,

E 6 'ost of >7uity ?'alculated from '#/A

F 6 'ost of &ebt ?#ssumed to be 9.1;A

DE 6 "eight of >7uity in 'apital %tructure

DF 6 "eight of &ebt in 'apital %tructure

T – Ta+ )ate ?#ssumed to be 35;A

(or calculating 'ost of >7uity, arket )eturn on Difty is calculated in $55 '@. )isk free rate

of return is considered as yield on 5 @ear *I bonds which is .9<; in arch. These values

have then been substituted in 'apital #sset /ricing odel ?'#/A,

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 24/73

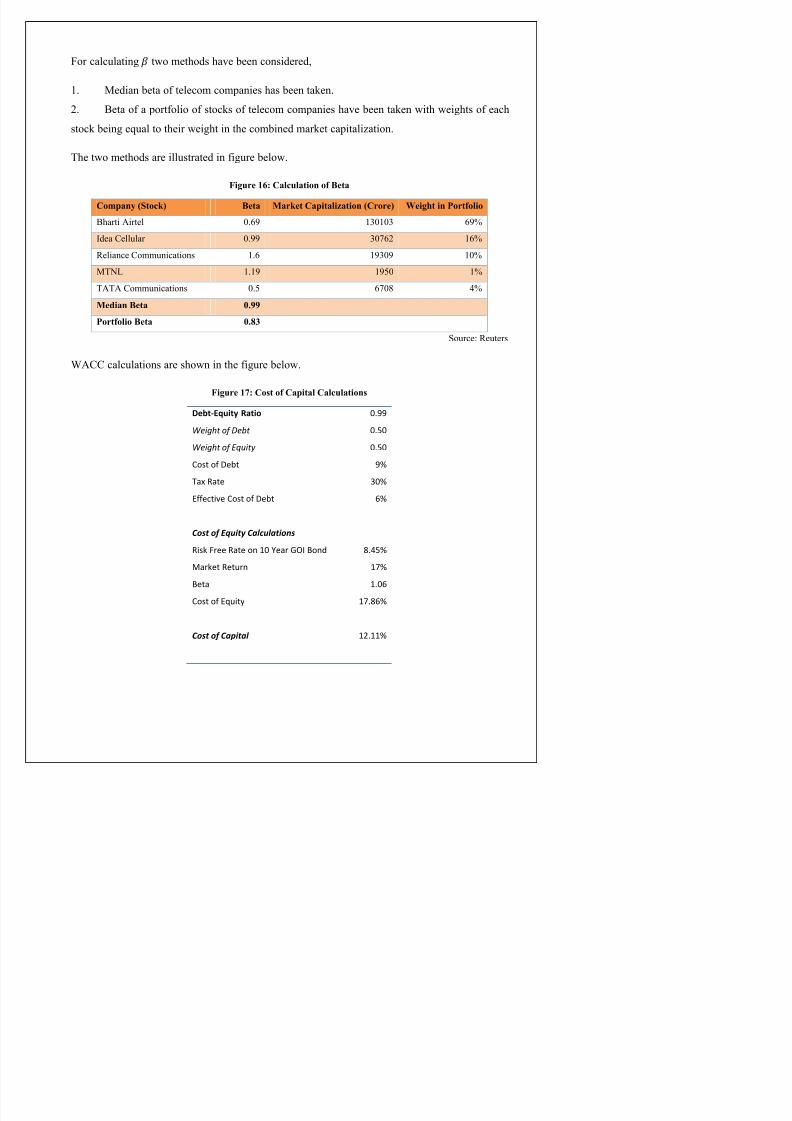

(or calculating G two methods have been considered,

. edian beta of telecom companies has been taken.

$.

!eta of a portfolio of stocks of telecom companies have been taken with weights of each

stock being e7ual to their weight in the combined market capitalization.

The two methods are illustrated in figure below.

Fiure $<% alculation of +eta

ompany 9Stock; +eta Market apitaliBation 9rore; *eiht in Portfolio

!harti #irtel 5.49 3553 49;

Idea 'ellular 5.99 354$ 4;

)eliance 'ommunications .4 9359 5;

TDE .9 915 ;

T#T# 'ommunications 5.1 452 <;

Median +eta @)??

Portfolio +eta @)>,

%ourceB )euters

"#'' calculations are shown in the figure below.

Fiure $=% ost of apital alculations

Det+,quity -atio 0.99

Weight of Debt 0.&0

Weight of Equity 0.&0

?ot of -et 9%

a= Rate 30%

ffecti>e ?ot of -et 6%

Cost of Equity Calculations

Ri$ ree Rate on 10 Cear ,I Bond 8.4&%

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 25/73

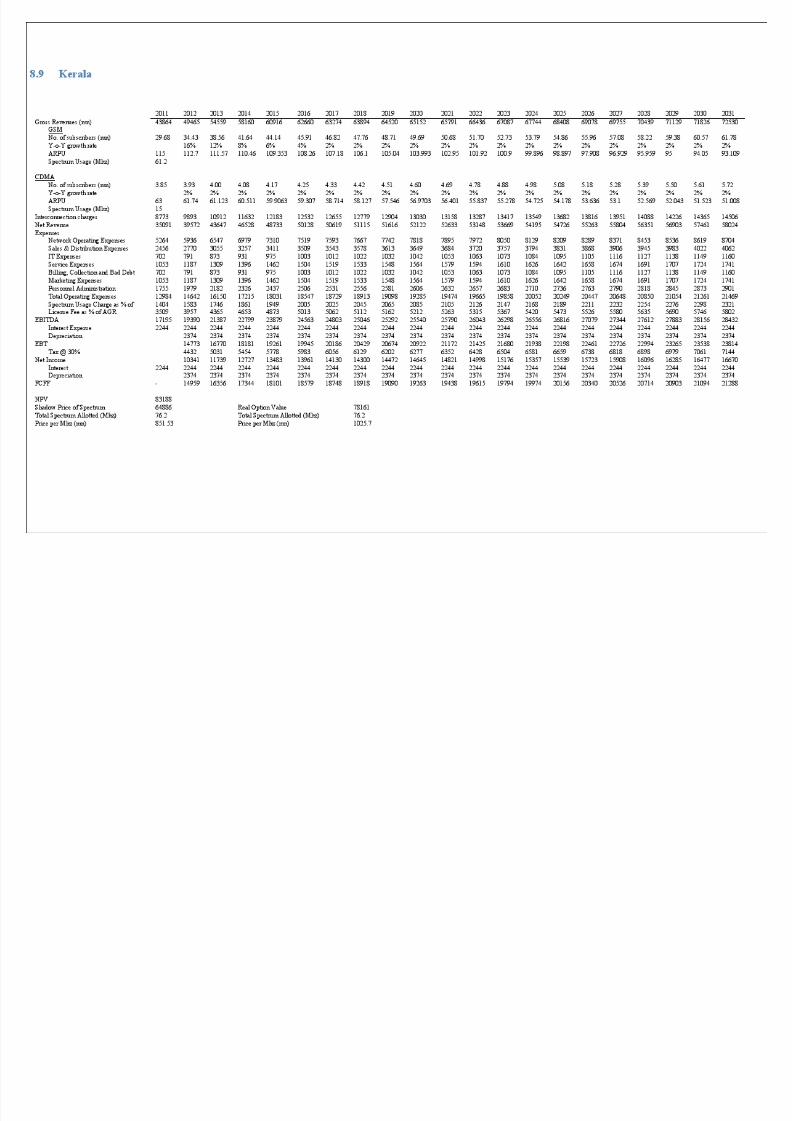

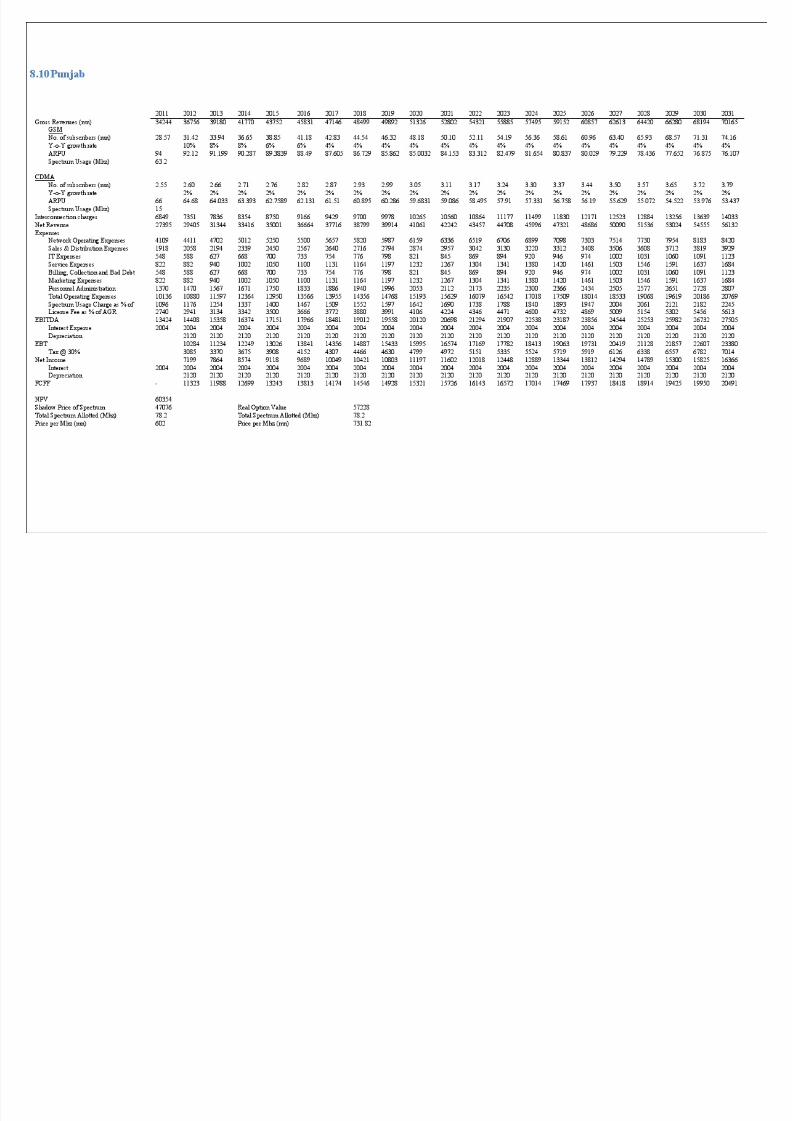

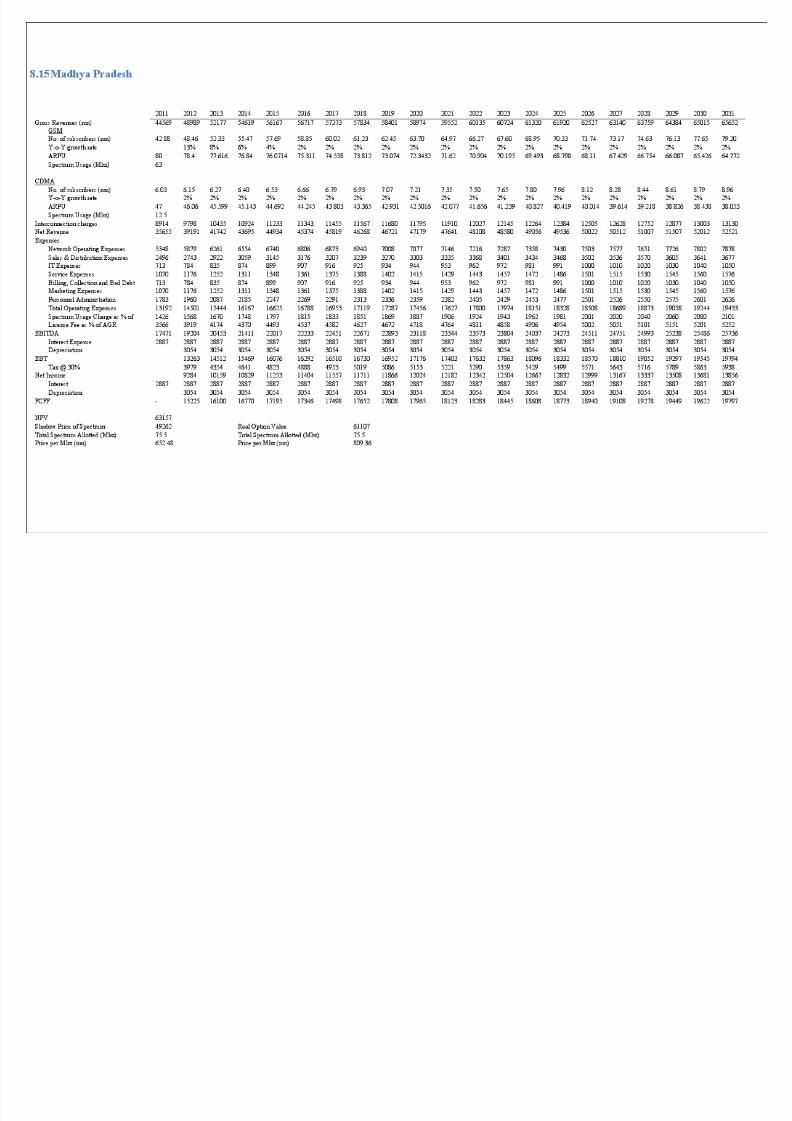

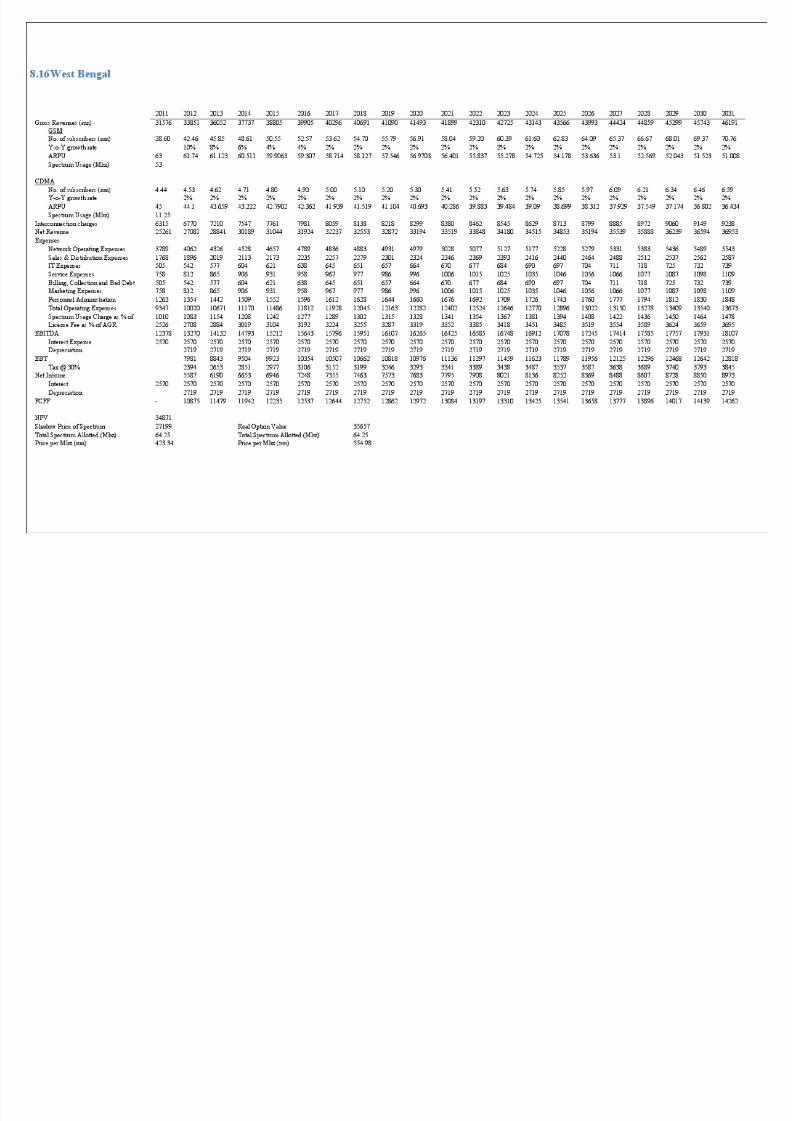

4) (esults

In this chapter first the base case &'( valuation results are presented along with the sensitivity

analysis of key variables. #fter the &'( valuation, real option value of the license has been

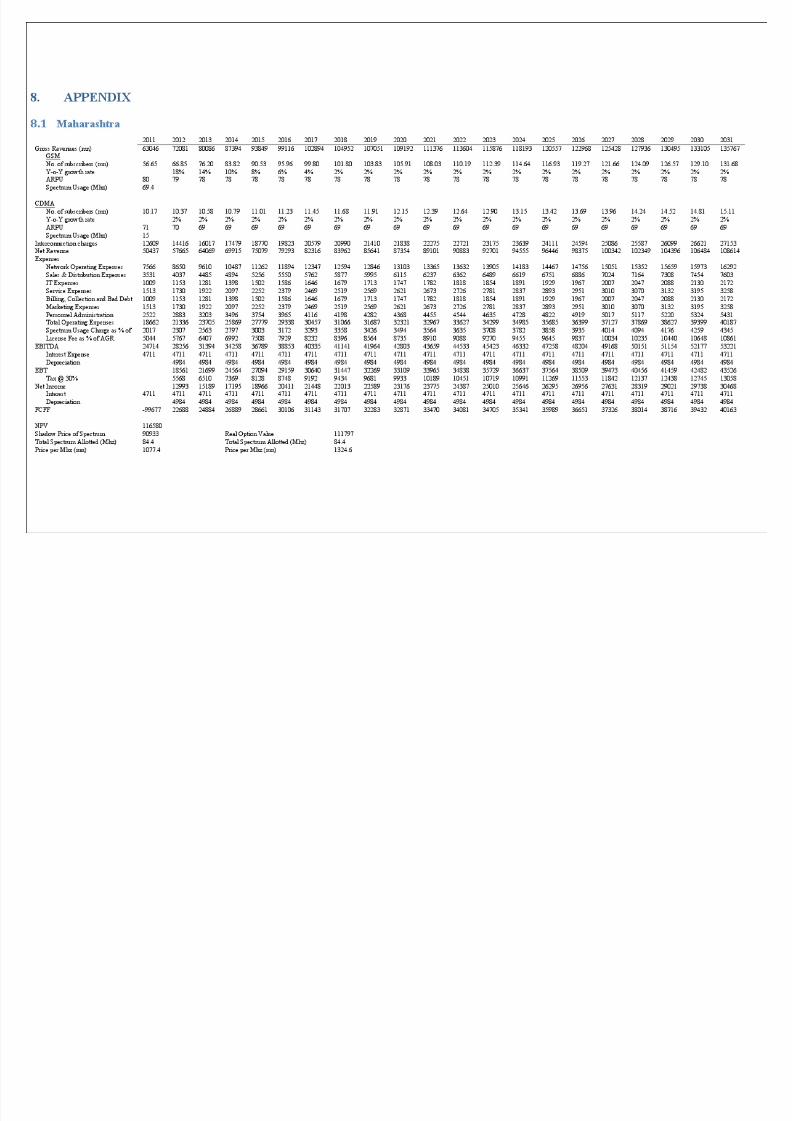

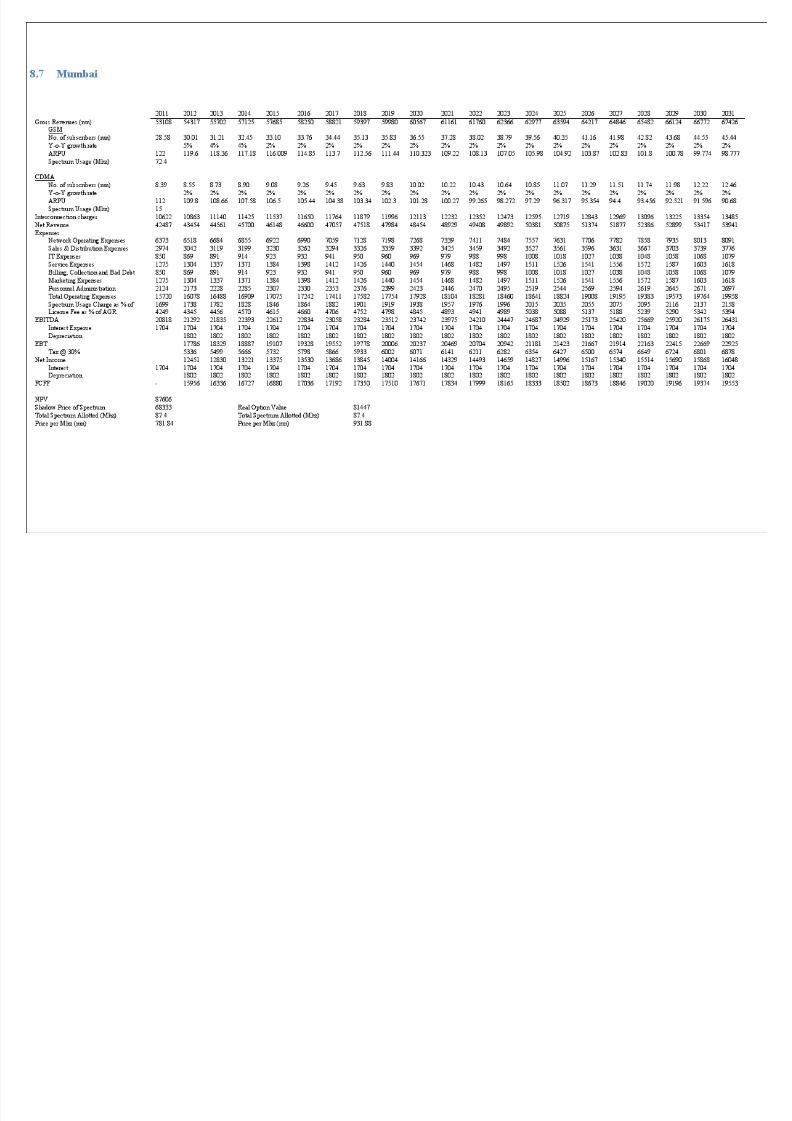

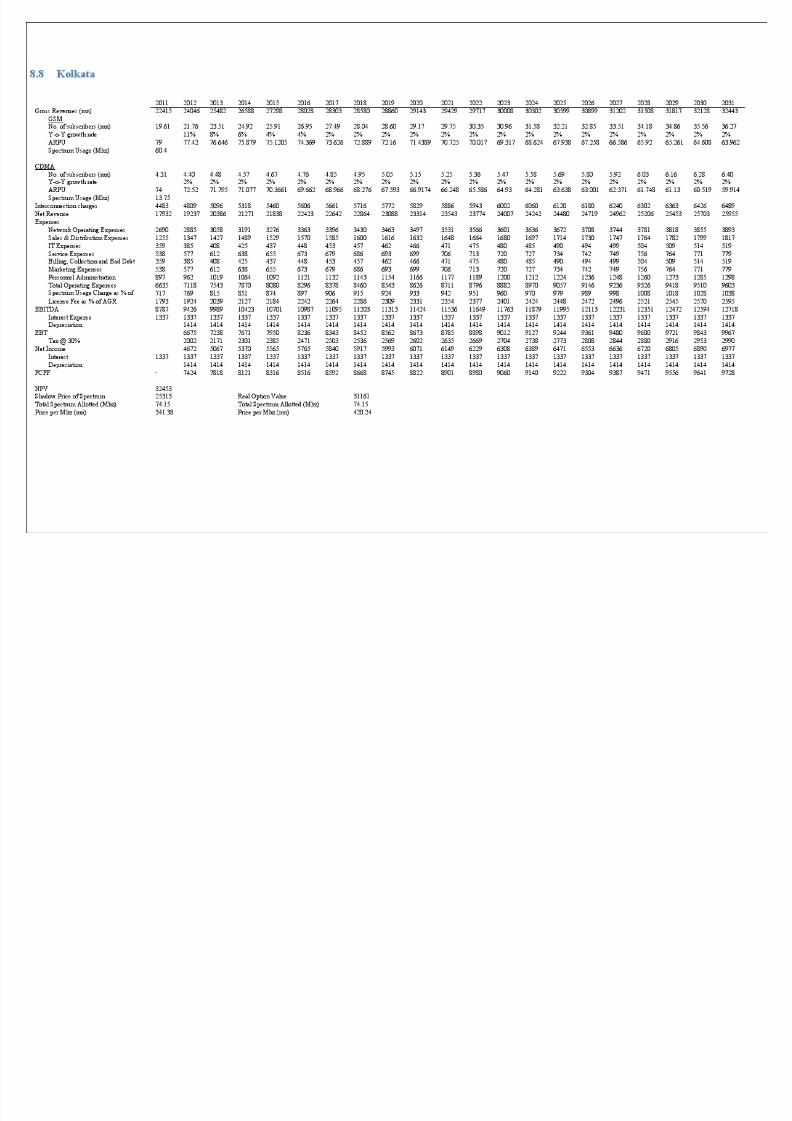

given which is calculated on the basis of 'hapter < 1. The results shown are for aharashtra

service area. )esult for other service areas can be found in the #ppendi+.

4)$ #F Valuation

4)$)$

NPV

The value of Hz of spectrum is obtained by dividing the &'( value obtained for aharashtra

by the total amount of spectrum allotted so far 5.

"e then calculated the shadow price of spectrum using the methodology given in chapter 1.

It is found out to be (s) $@==). mn or $@=)=. crores.

This is the price that an operator might be willing to pay for Hz of spectrum in aharashtra

and should be considered while deciding whether to operate in a service area or not.

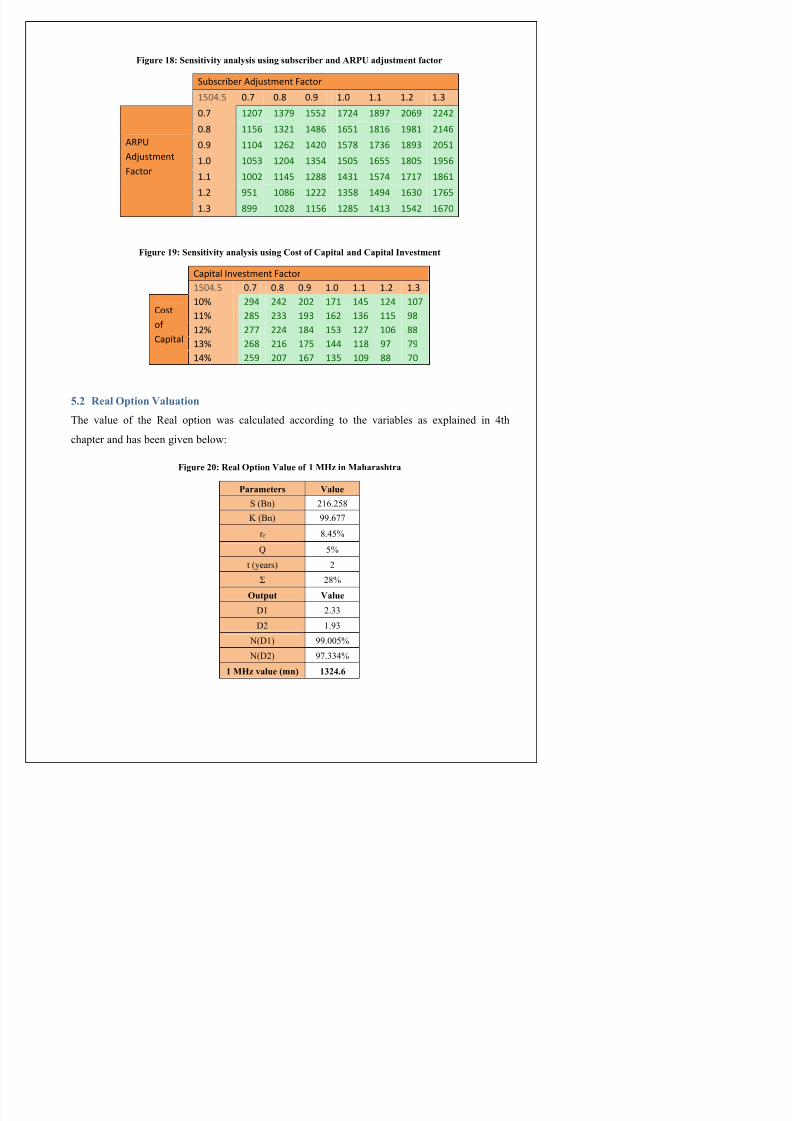

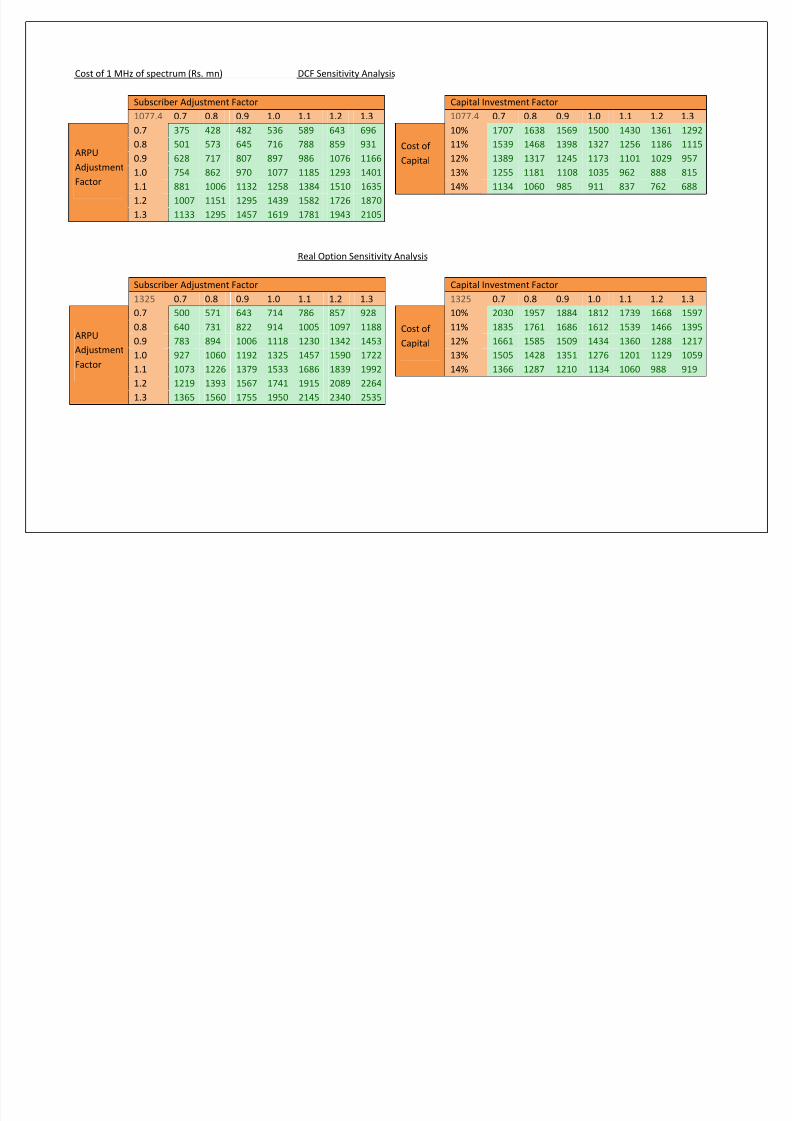

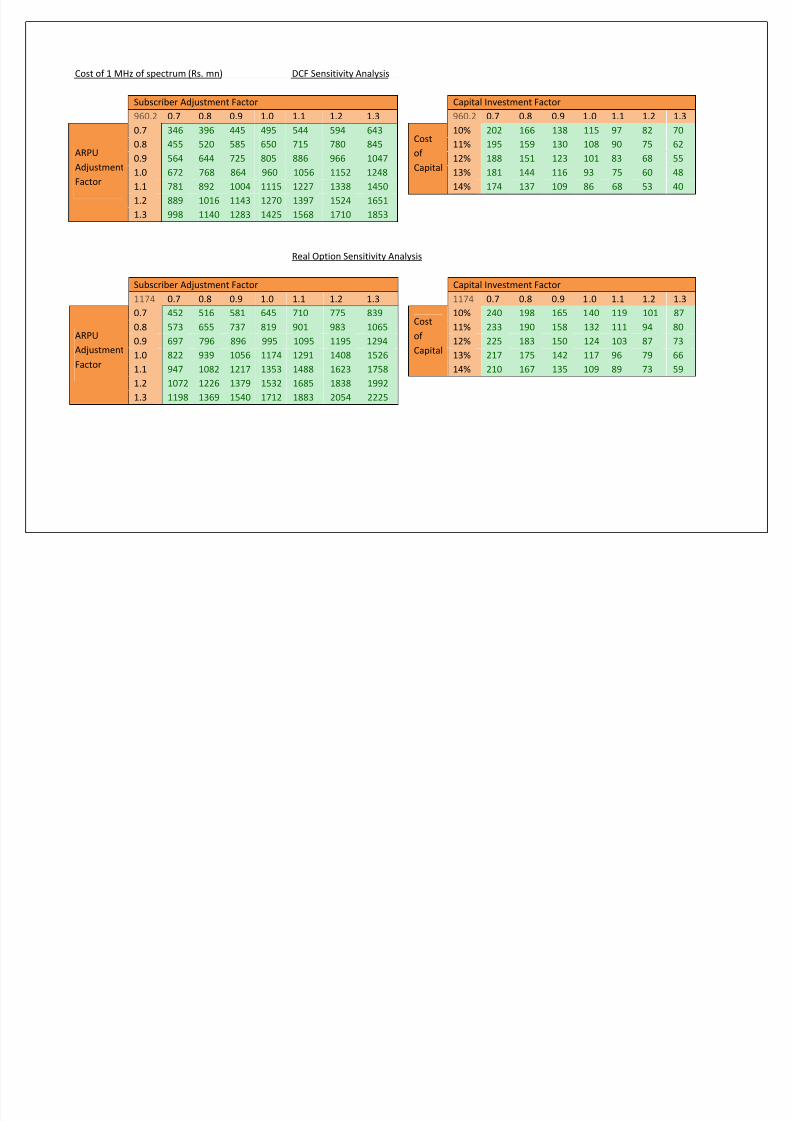

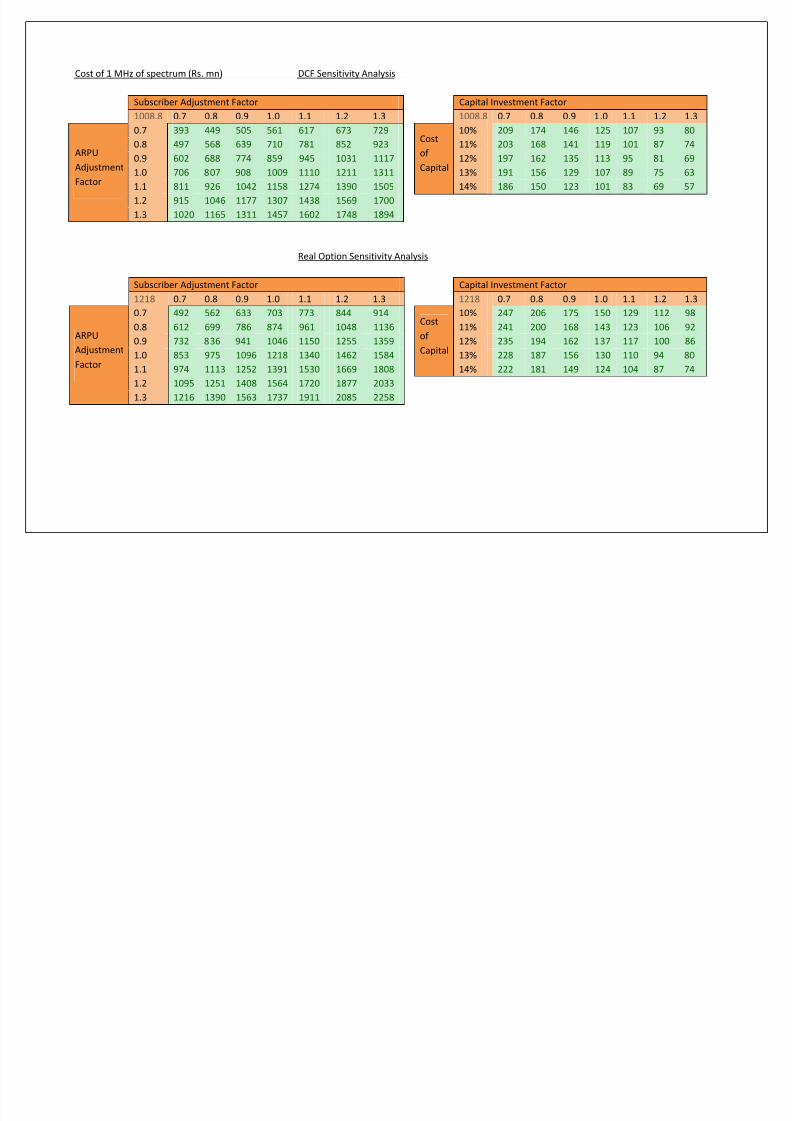

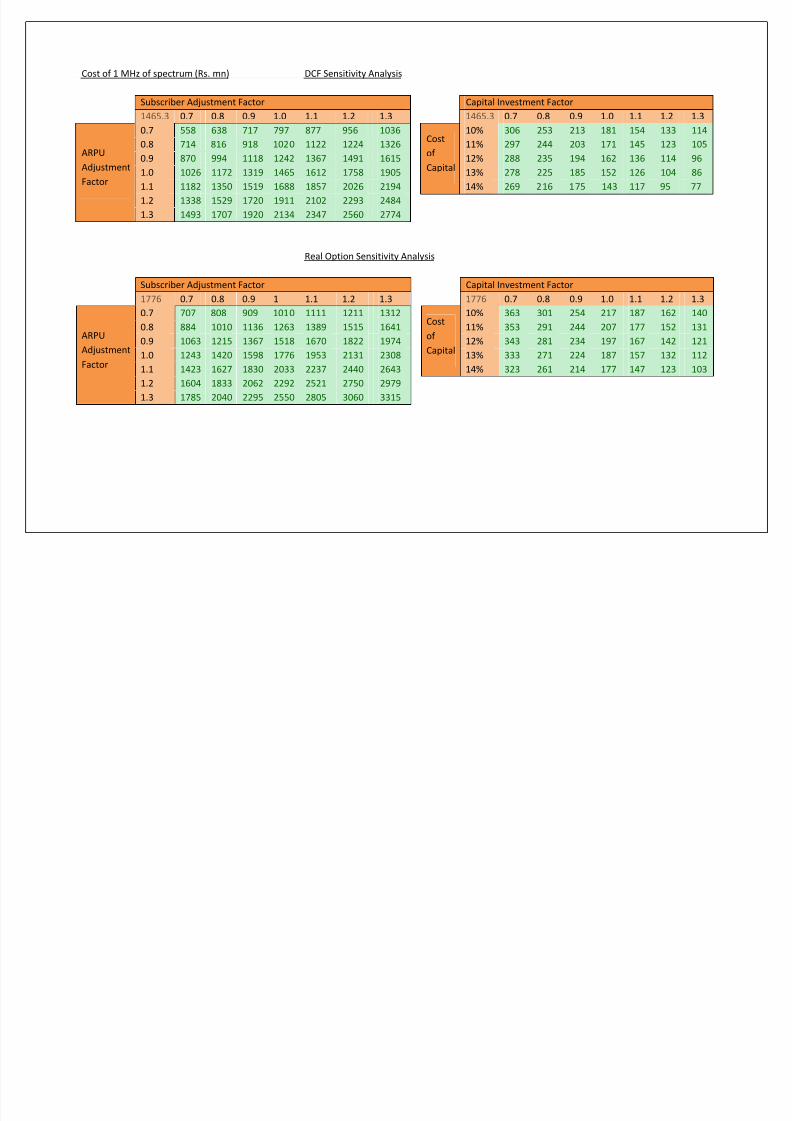

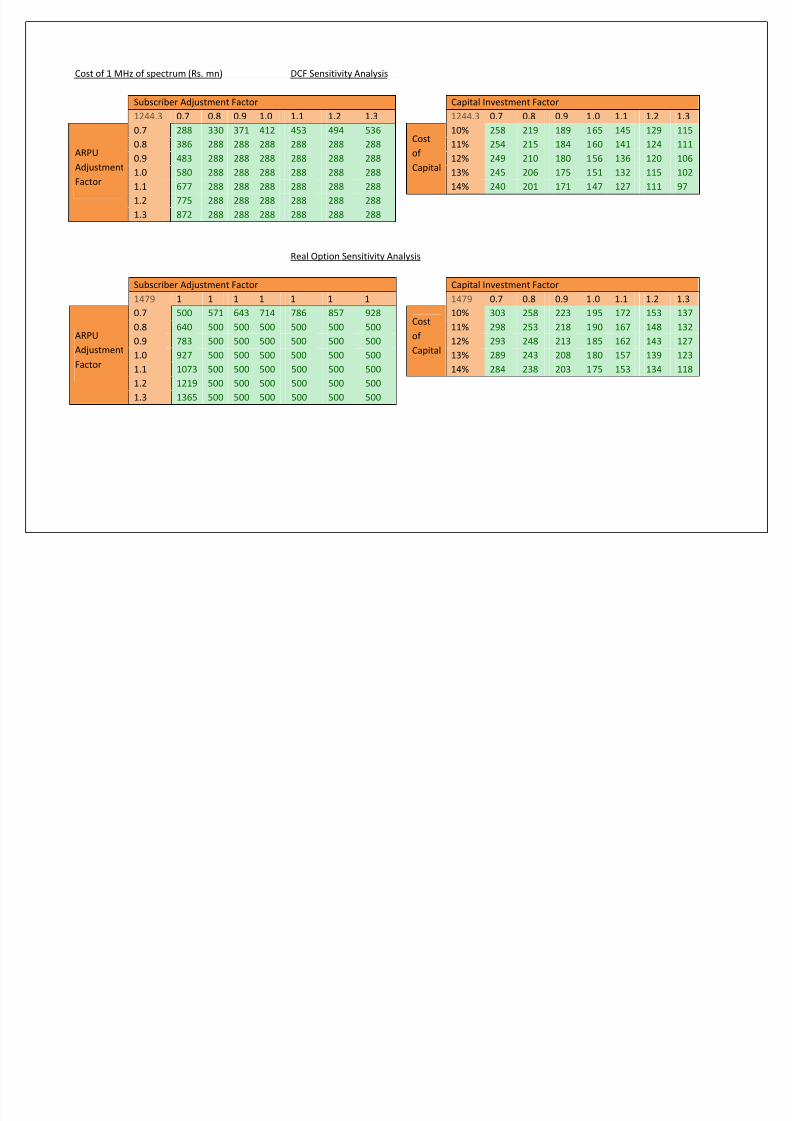

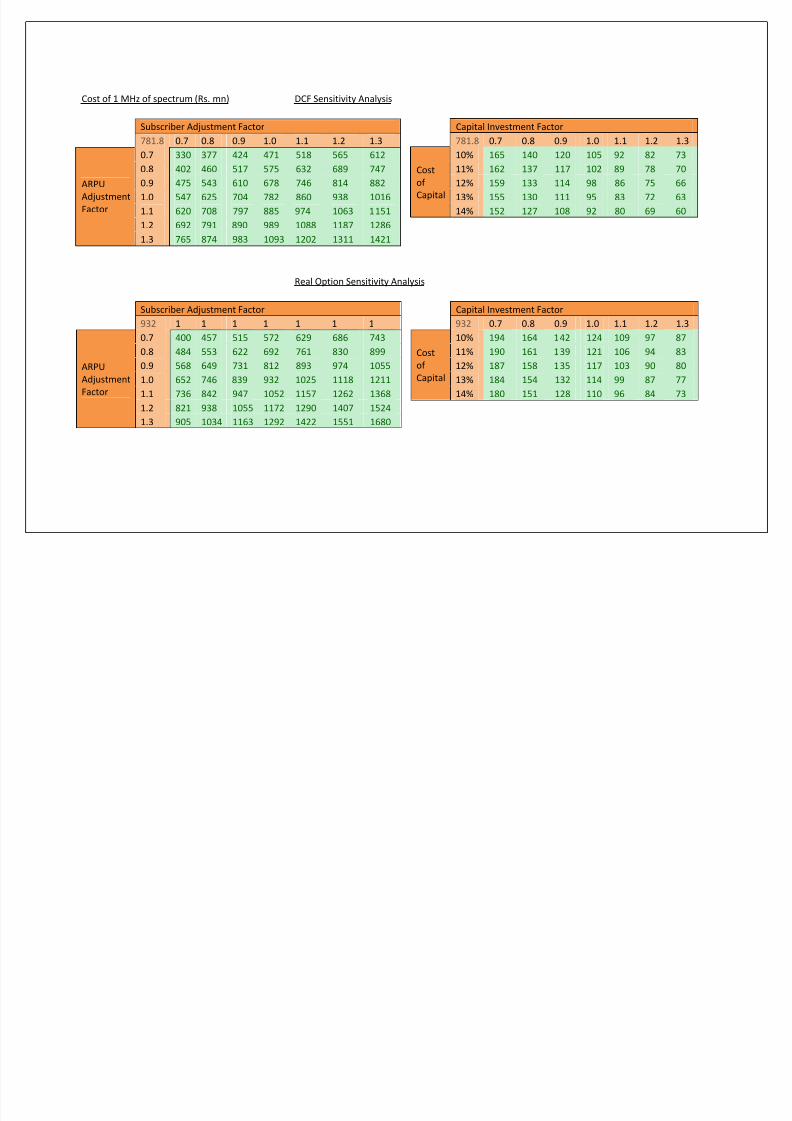

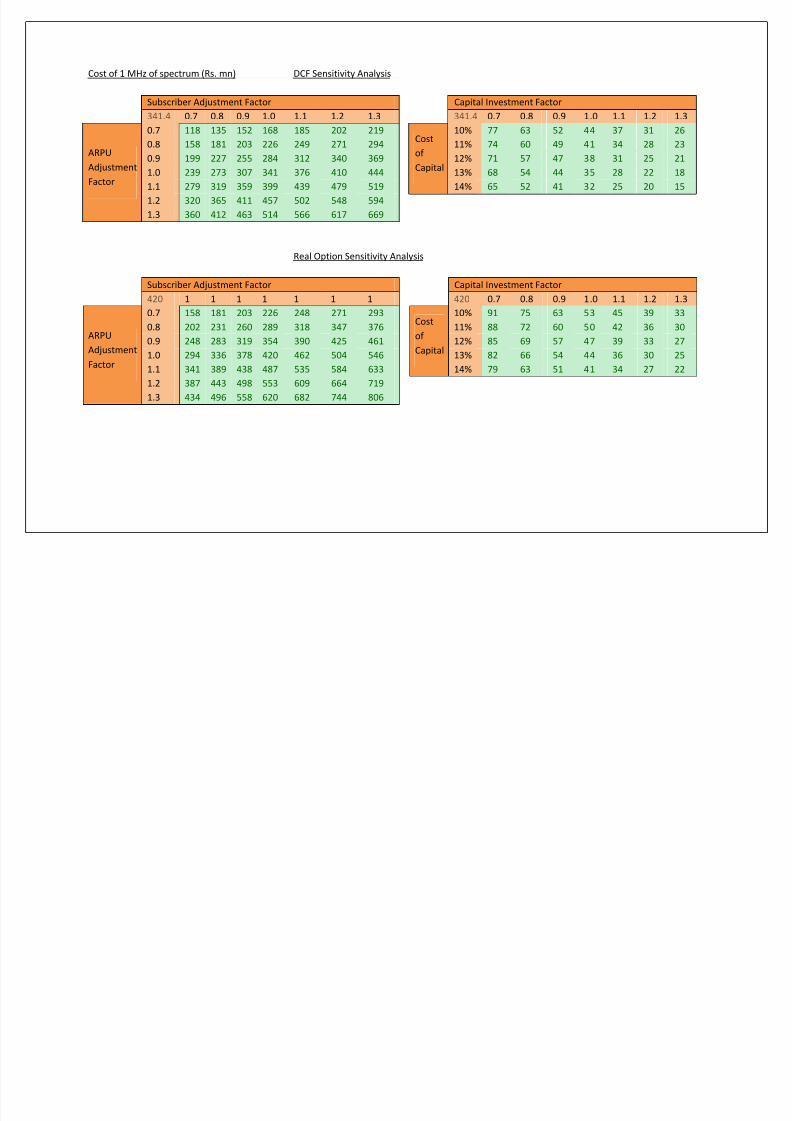

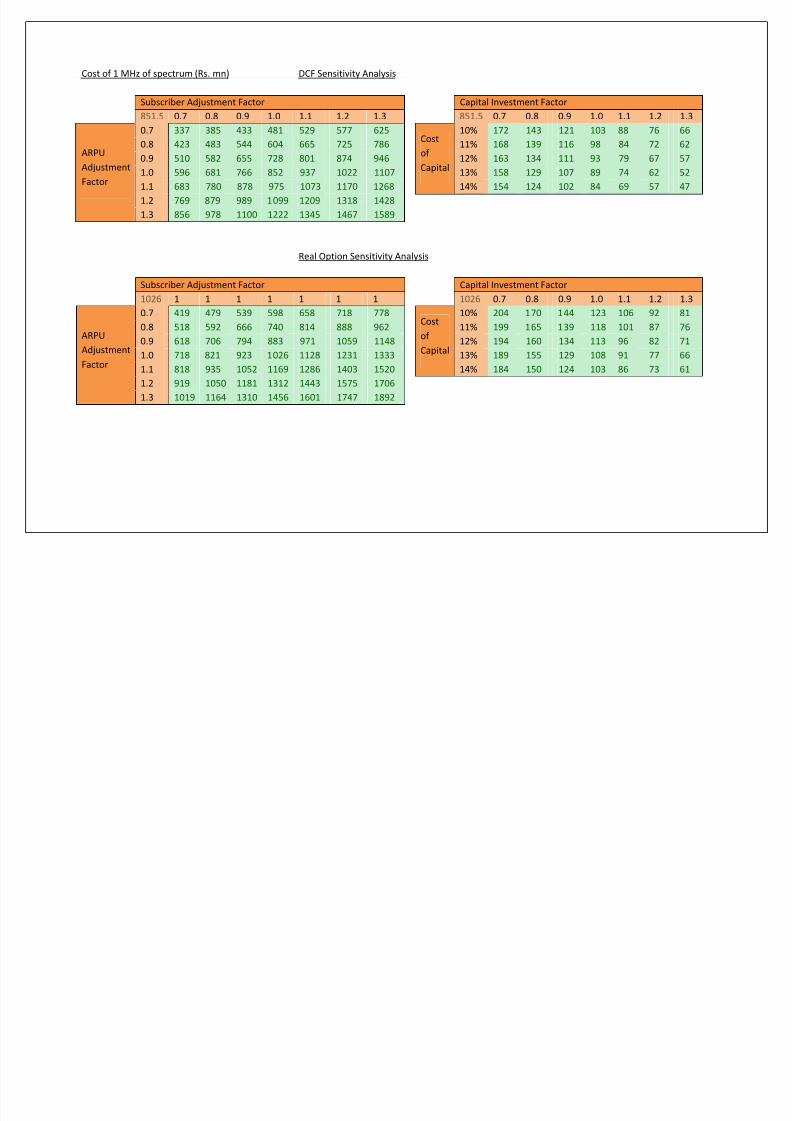

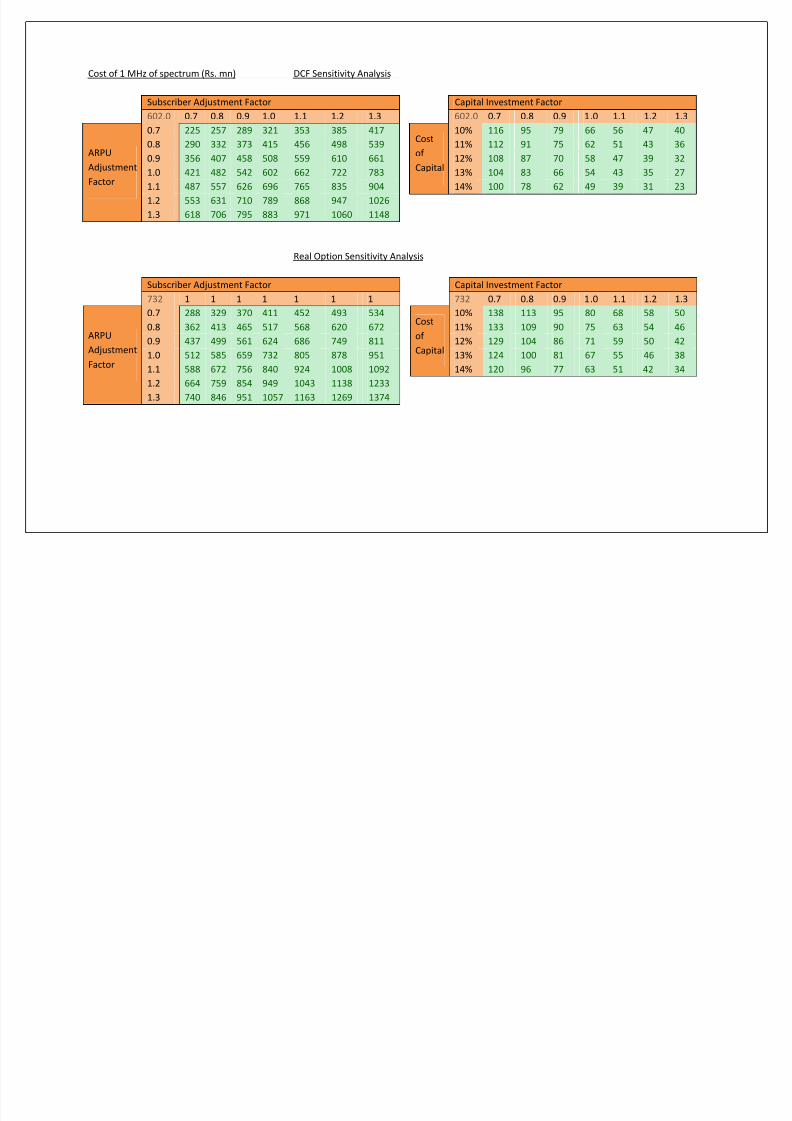

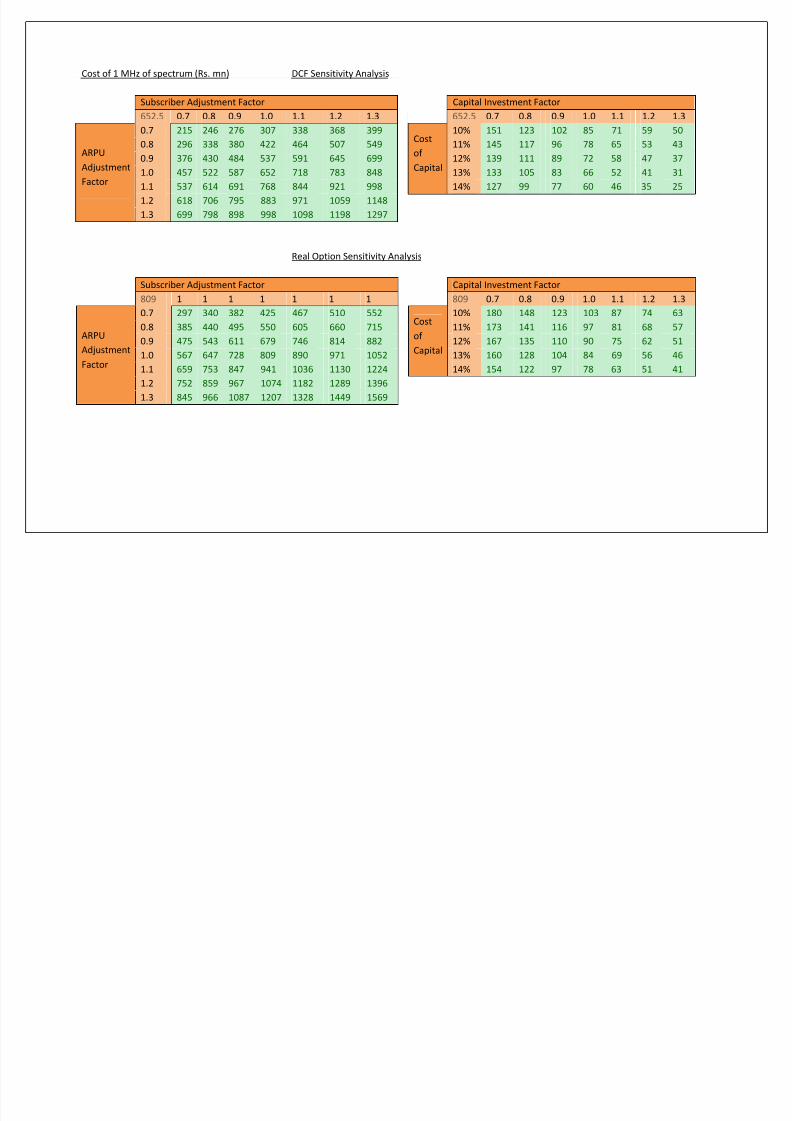

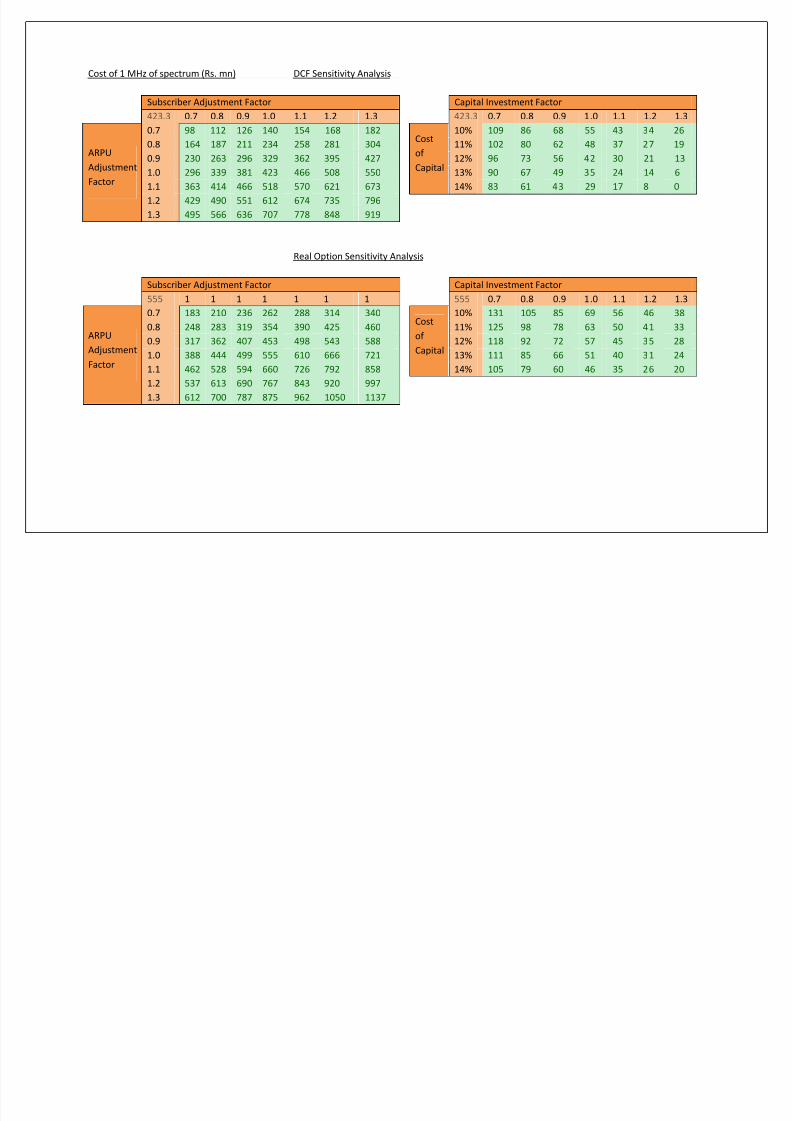

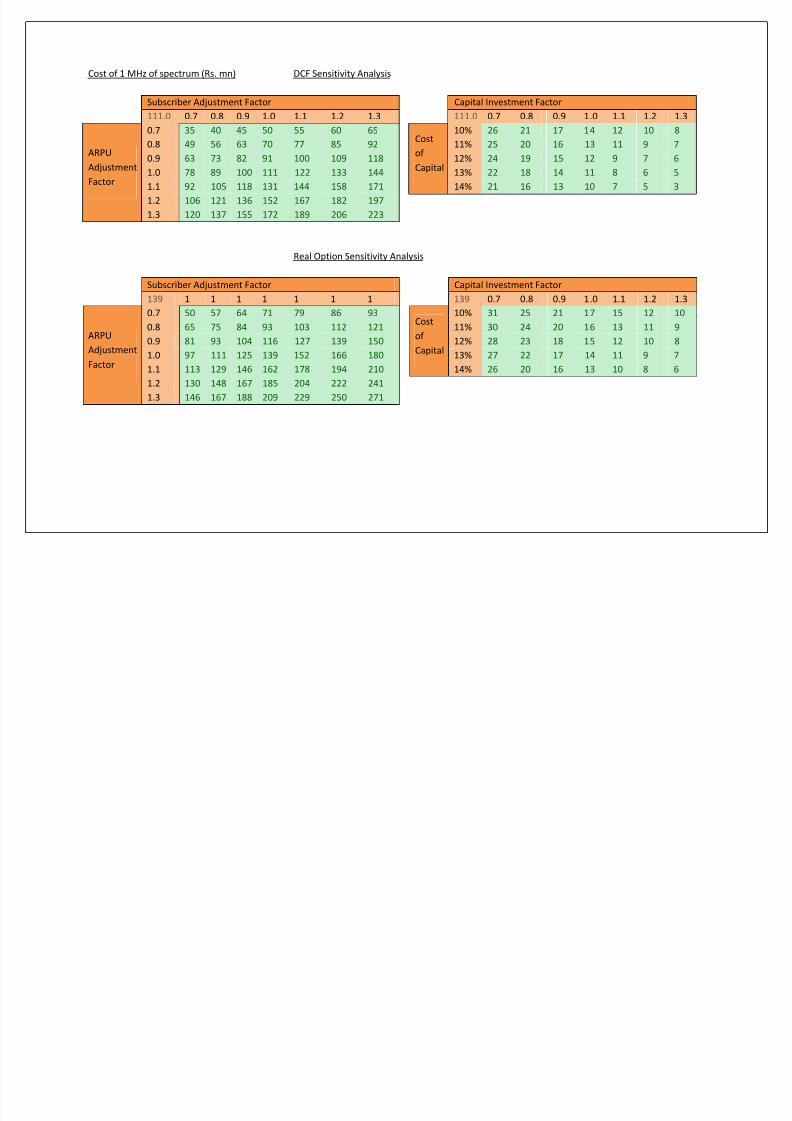

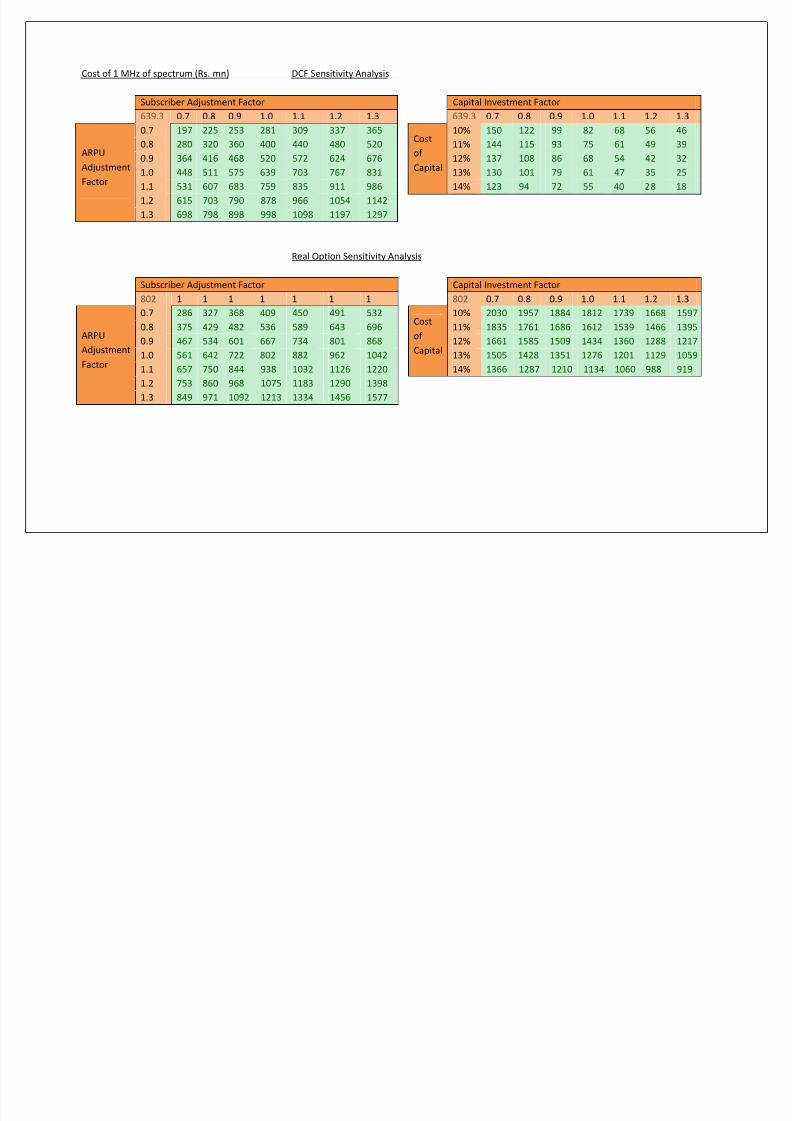

4)$)2 Sensiti"ity Analysis

(rom the understanding of the &'( model, there are many critical factors which decide theoutcome of the &'( and hence they need to be checked for the variance that can be seen in case

the base assumptions are not met. These critical parameters have been selected as %ubscriber

ad8ustment factor and #)/0 ad8ustment factor, amount of capital invested and cost of capital.

%ubscriber ad8ustment factor is important parameter as this decides the number of mobile users

which in turn affects the revenues. %imilarly #)/0 ad8ustment factor has a direct bearing on the

revenues.

Eike in any pro8ect, cost of capital plays an important role in the values derived from the pro8ect

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 26/73

Fiure $>% Sensiti"ity analysis usin su'scri'er and A(P! adjustment factor

S(crier !d(t#ent actor

1&04.& 0.7 0.8 0.9 1.0 1.1 1.2 1.3

!R5

!d(t#ent

actor

0.7 1207 1379 1&&2 1724 1897 2069 2242

0.8 11&6 1321 1486 16&1 1816 1981 2146

0.9 1104 1262 1420 1&78 1736 1893 20&1

1.0 10&3 1204 13&4 1&0& 16&& 180& 19&6

1.1 1002 114& 1288 1431 1&74 1717 1861

1.2 9&1 1086 1222 13&8 1494 1630 176&

1.3 899 1028 11&6 128& 1413 1&42 1670

Fiure $?% Sensiti"ity analysis usin ost of apital and apital In"estment

?a*ital In>et#ent actor

1&04.& 0.7 0.8 0.9 1.0 1.1 1.2 1.3

?ot

of

?a*ital

10% 294 242 202 171 14& 124 107

11% 28& 233 193 162 136 11& 98

12% 277 224 184 1&3 127 106 88

13% 268 216 17& 144 118 97 79

14% 2&9 207 167 13& 109 88 70

4)2

(eal 1ption Valuation

The value of the )eal option was calculated according to the variables as e+plained in <th

chapter and has been given belowB

Fiure 2@% (eal 1ption Value of $ M/B in Maharashtra

Parameters Value% ?!nA $4.$12

L ?!nA 99.4

r f 2.<1;

= 1;

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 27/73

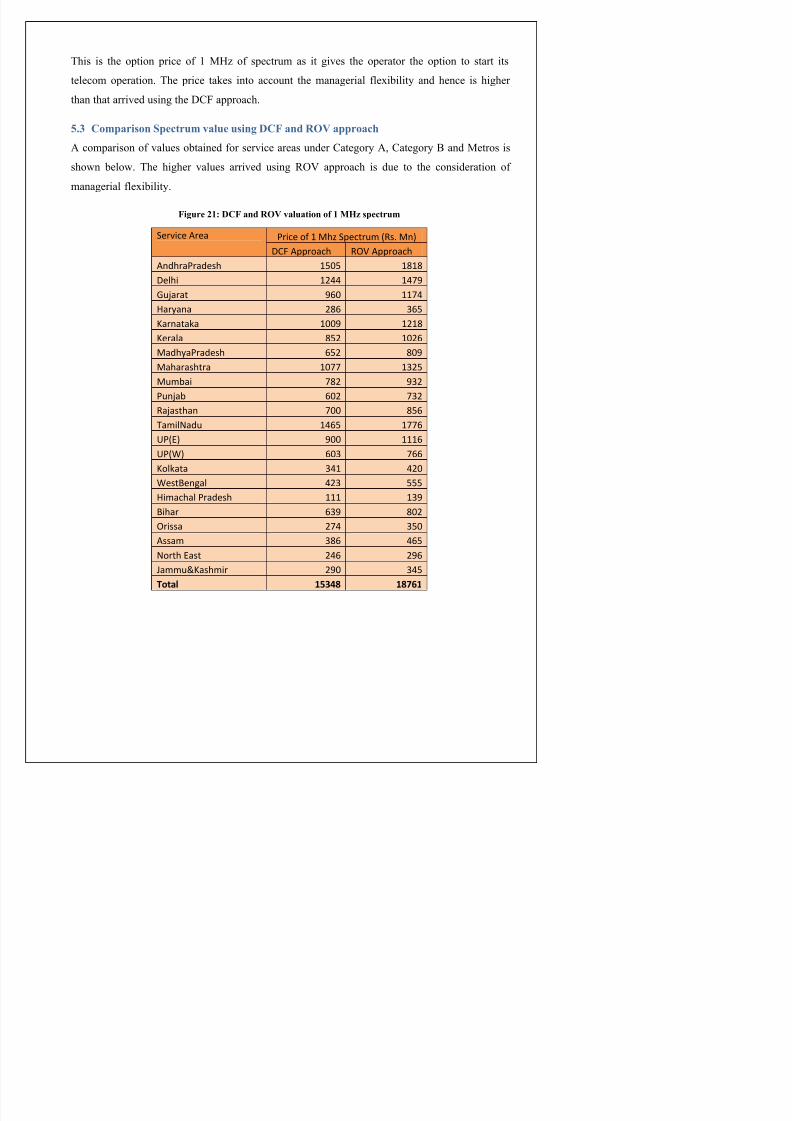

This is the option price of Hz of spectrum as it gives the operator the option to start its

telecom operation. The price takes into account the managerial fle+ibility and hence is higher

than that arrived using the &'( approach.

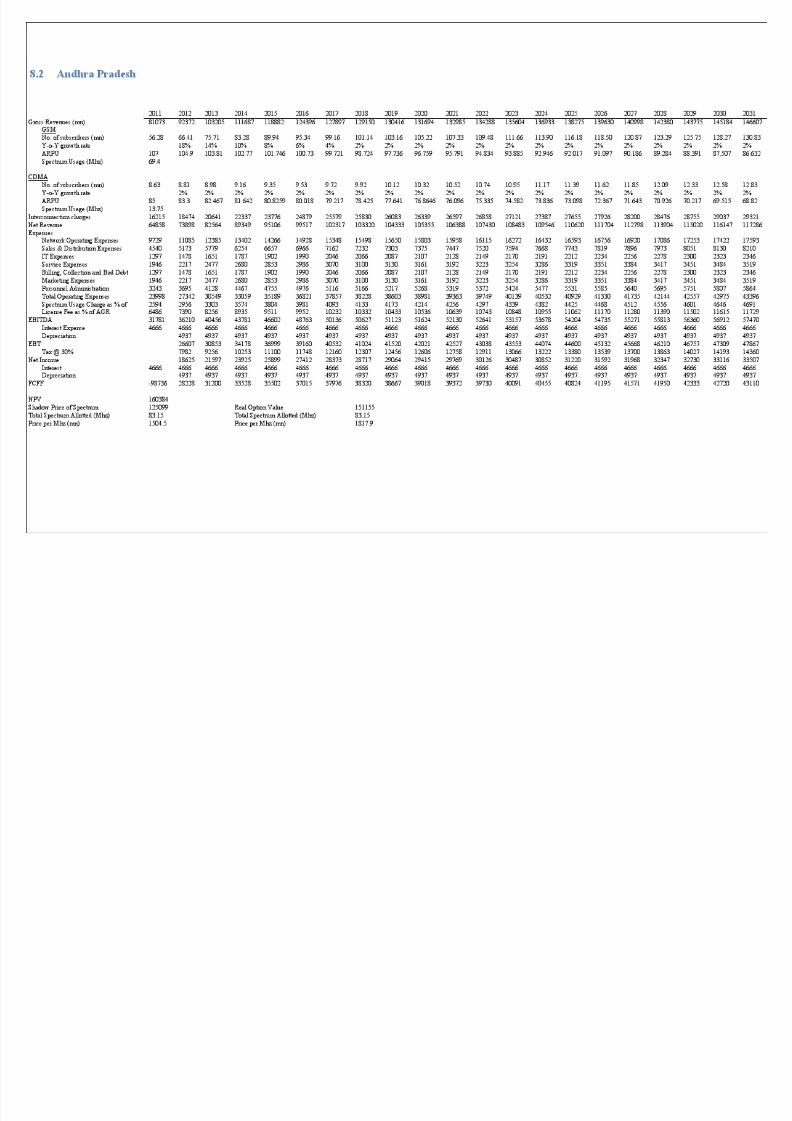

4), omparison Spectrum "alue usin #F and (1V approach

# comparison of values obtained for service areas under 'ategory #, 'ategory ! and etros is

shown below. The higher values arrived using )* approach is due to the consideration of

managerial fle+ibility.

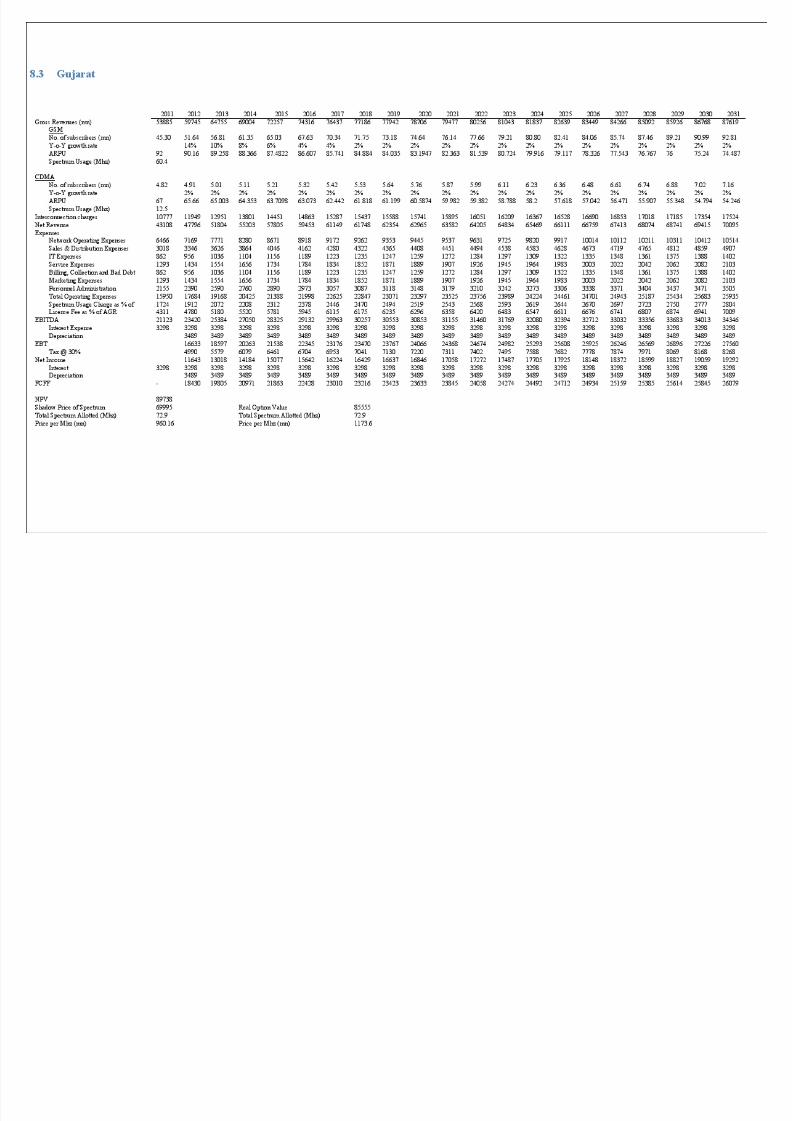

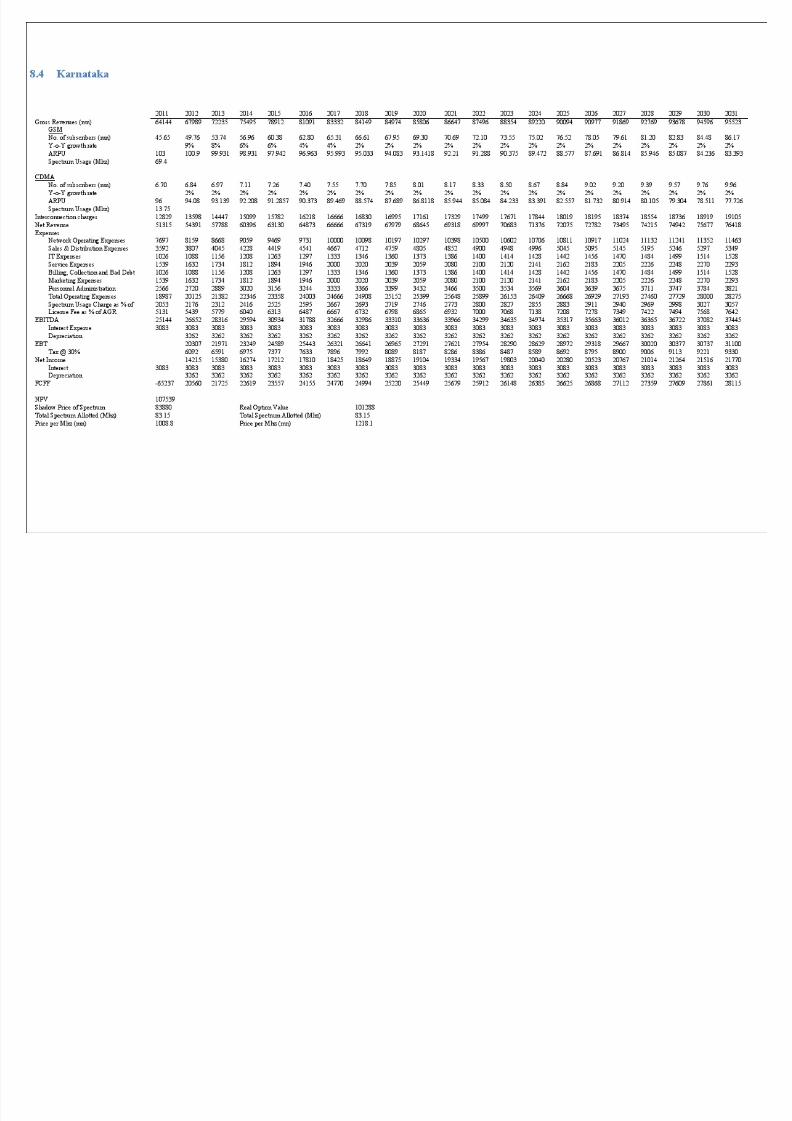

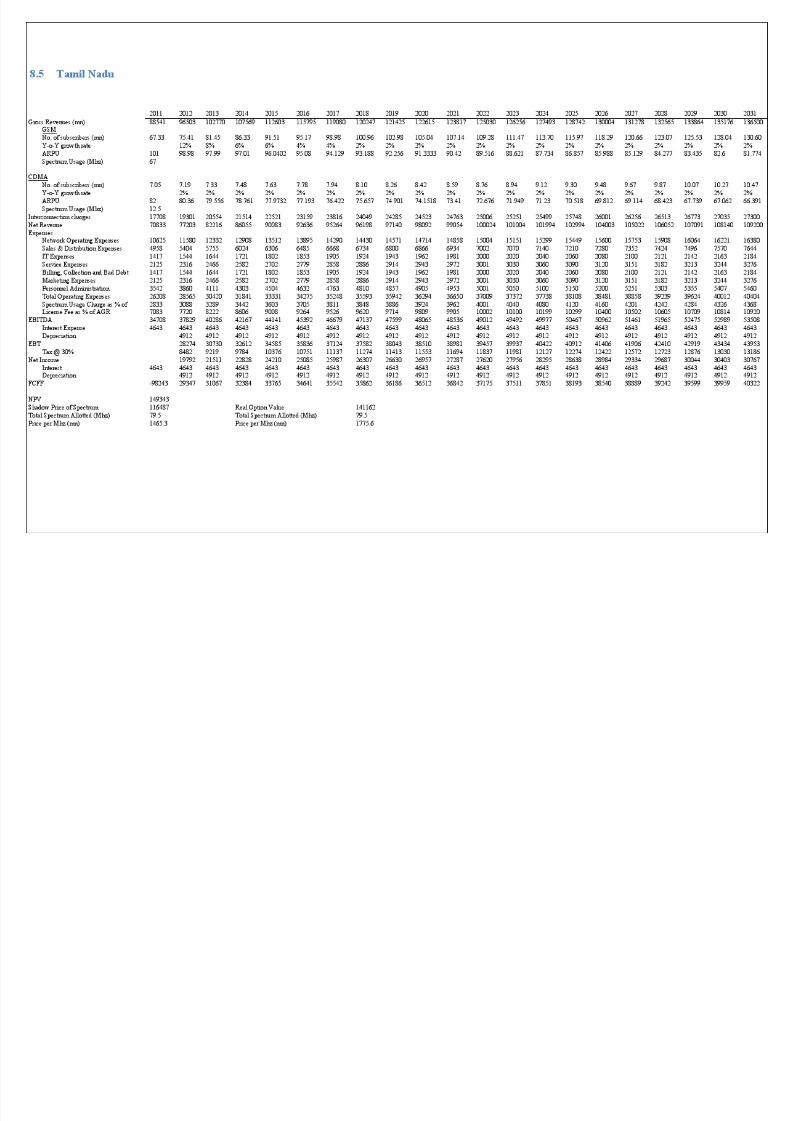

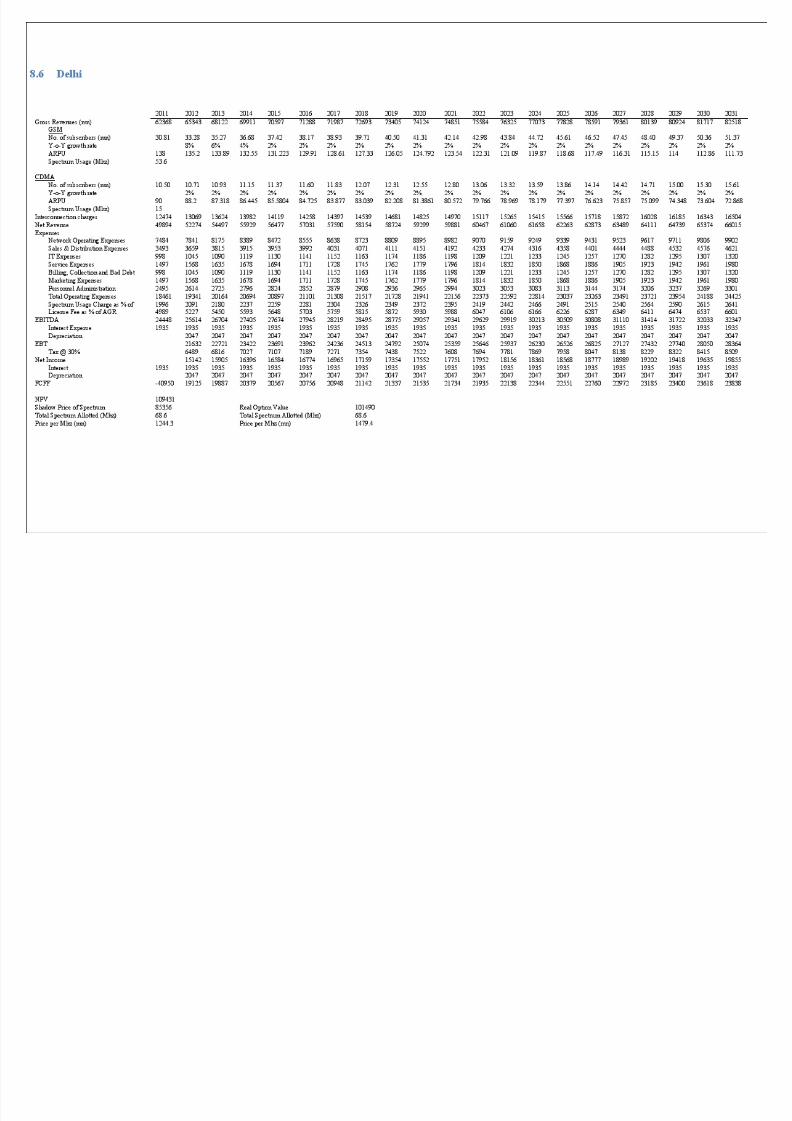

Fiure 2$% #F and (1V "aluation of $ M/B spectrum

Ser>ice !rea rice of 1 hE S*ectr(# R. n

-? !**roach R,V !**roach

!ndhraradeh 1&0& 1818

-elhi 1244 1479

(arat 960 1174ar"ana 286 36&

/arnata$a 1009 1218

/erala 8&2 1026

adh"aradeh 6&2 809

aharahtra 1077 132&

(#ai 782 932

(na 602 732Raathan 700 8&6

a#ilNad( 146& 1776

5 900 1116

5 603 766

/ol$ata 341 420

etBen;al 423 &&&

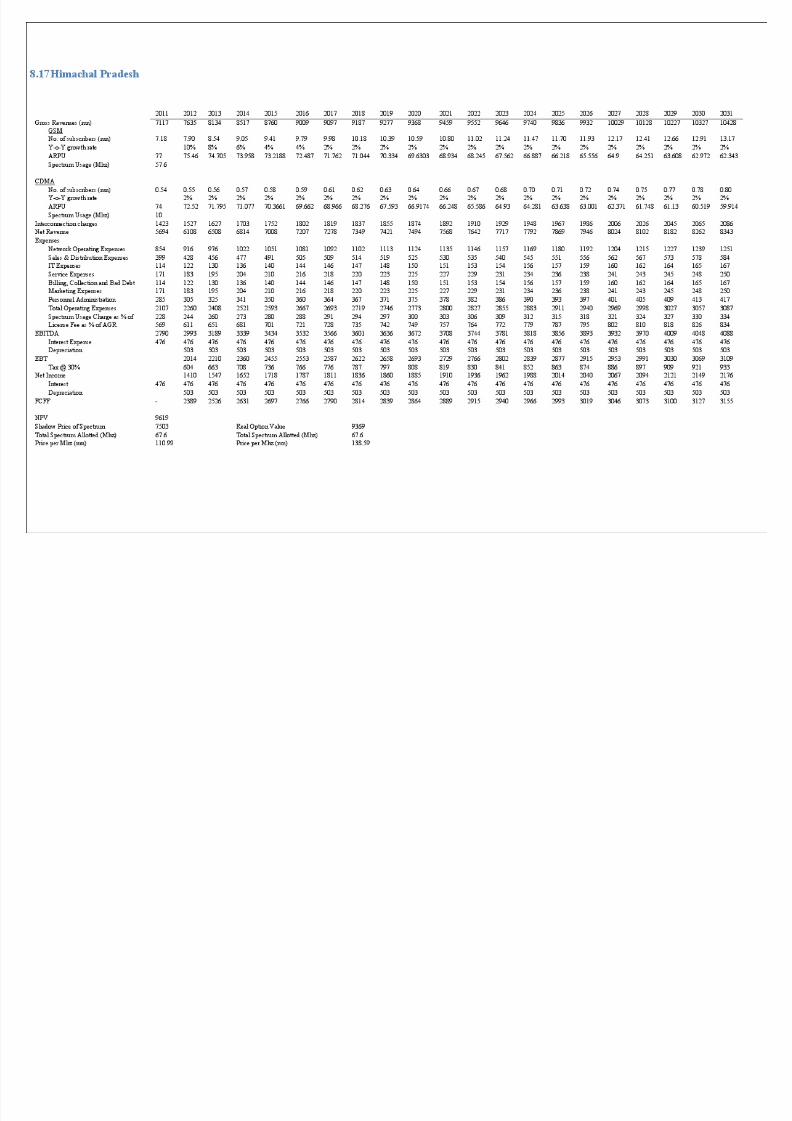

i#achal radeh 111 139

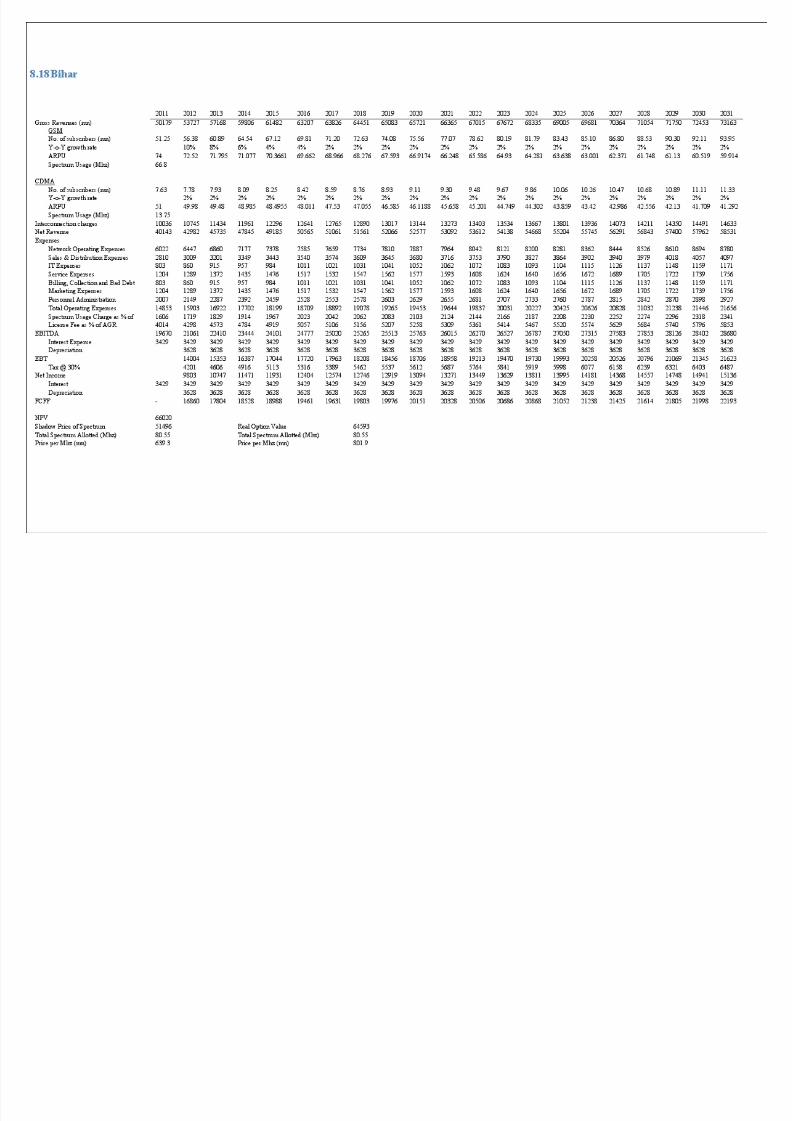

Bihar 639 802

,ria 274 3&0

!a# 386 46&

North at 246 296

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 28/73

<) onclusion and (ecommendation

The motivation behind this research was to find the intrinsic and option value of the spectrum,

Hz in unit in service areas under etros, 'ategory # and 'ategory !. This achieves greater

significance in the light of cancellation of licenses by the %upreme 'ourt and the impending

spectrum auction.

The values for spectrum arrived using )* approach were higher than those arrived using the

&'( approach. In other words we can say that )eal option analysis has allowed us to look at the

option value embedded in the $ spectrum allotment. This fle+ibility in the hands of the

managers is not ade7uately represented with a &'( analysis where in the timing of the

investment should be knownCpredicted beforehand. However such kind of information and

knowledge is rarely available at the time of planning and moreover in pro8ects with high degree

of uncertainty and with irreversible investments. )eal options analysis ade7uately captures this

fle+ibility and hence it results in higher valuation for the aggregate $ spectrum. It would be

prudent for an operator to consider the two values as a range within which it can purchase $

spectrum. It is also recommended that in future while allocating telecom licenses or licenses in

sectors where high and irreversible investment is re7uired and there is a scope for the licensees to

invest in phases or in modules, the government should consider real options methodology for

setting the price of the license, or the base price of the licenses in case the government decides to

follow an auction methodology to allocate the licenses to determine a more accurate price of the

license which takes into account the managerial fle+ibility.

The spectrum price range therefore for a pan India hz of spectrum is )s.131 crores to

)s.24 crores. This is definitely higher than the price discovered in $55 6 )s.412 crores for

4.$ hz of spectrum. However, we do not distinguish between the prices for initial spectrum

assignment and incremental spectrum assignment.

T)#I in its consultation paper in (ebruary has suggested models for pricing the spectrum. #s

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 29/73

7. (eferences

. !asili, ., (ontini, (. ?$553A. The *ption alue of the 0L 3 Telecom Eicenses. (nfo

),*, pp. <2-1$.

$. &amodaran, #. ?$555A. The promise of real options. +ournal of pplied "orporate

-inane, Vol. *, pp. $9-<3.

3. !enaroch, ., Lauffman, ). :. ?999A. # 'ase for 0sing )eal *ptions /ricing

#nalysis To >valuate Information Technology /ro8ect Investments. (nfor$ation &%ste$s Researh, Vol. /, No. , pp. 5-24.

<. %inha, /., udgal, H. ?$5A. aluation of 3 spectrum license in IndiaB # real option

approach., MRP Paper No. *01

1.

T)#I ?$5, :anuary 35A, )eport on the $55 value of spectrum in the 255 Hz !and

4. /lum 'onsulting ?$5, arch A, ethodologies for aluing %pectrumB )eview of

>+perts )eport

.

T)#I ?$5$, :anuary 9A, The Indian Telecom %ervices /erformance Indicators

2.

T)#I ?$5$, arch A, 'onsultation /aper on #uction of %pectrum

9. !randao, E. >., &yer, :. %., Hahn, ". :. ?$551, :uneA. 0sing !inomial Trees To %olve

)eal-*ption aluation /roblems. &ecision #nalysis, ol. $, Do. $, pp. 49-22

5.

Eeslie, L. :., ichaels, . /. ?99, Dumber 3A. The real power of real options. The

cLinsey =uarterly.

. Euehrman, T. #. ?992, :uly-#ugustA. Investment *ppurtunities as )eal *ptionsB etting

%tarted on the Dumbers. Harvard !usiness )eview.

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 30/73

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 31/73

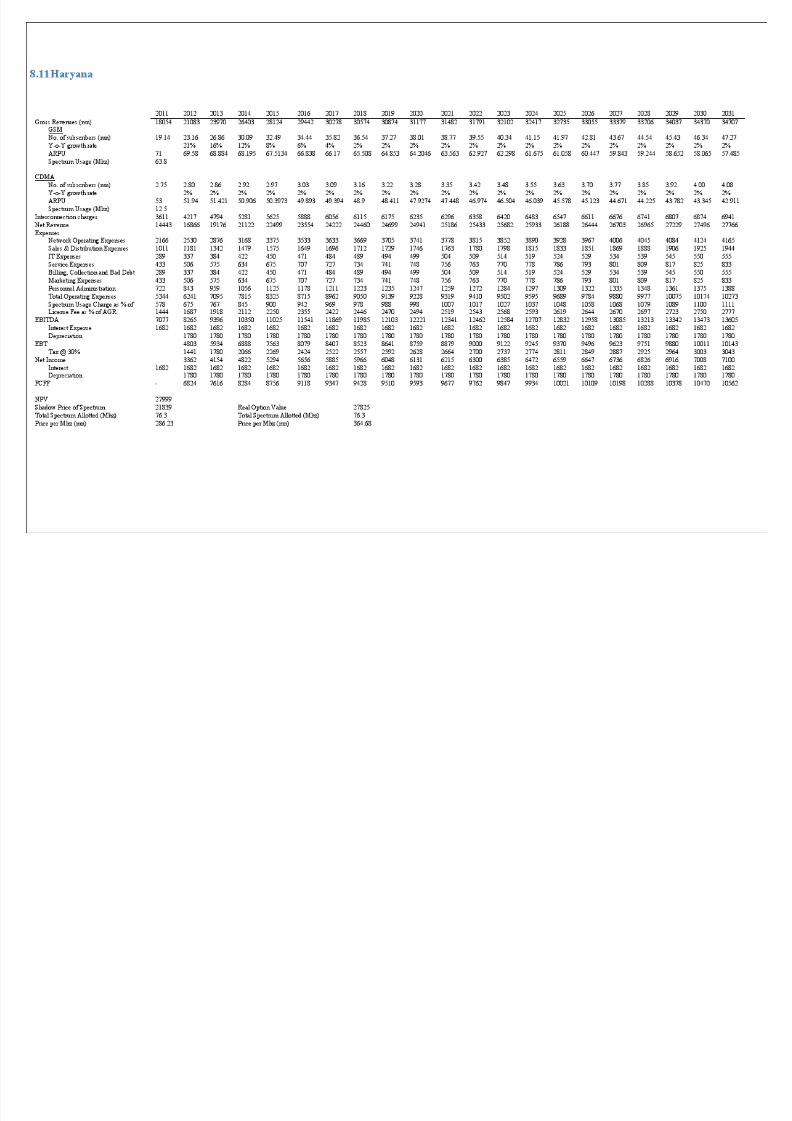

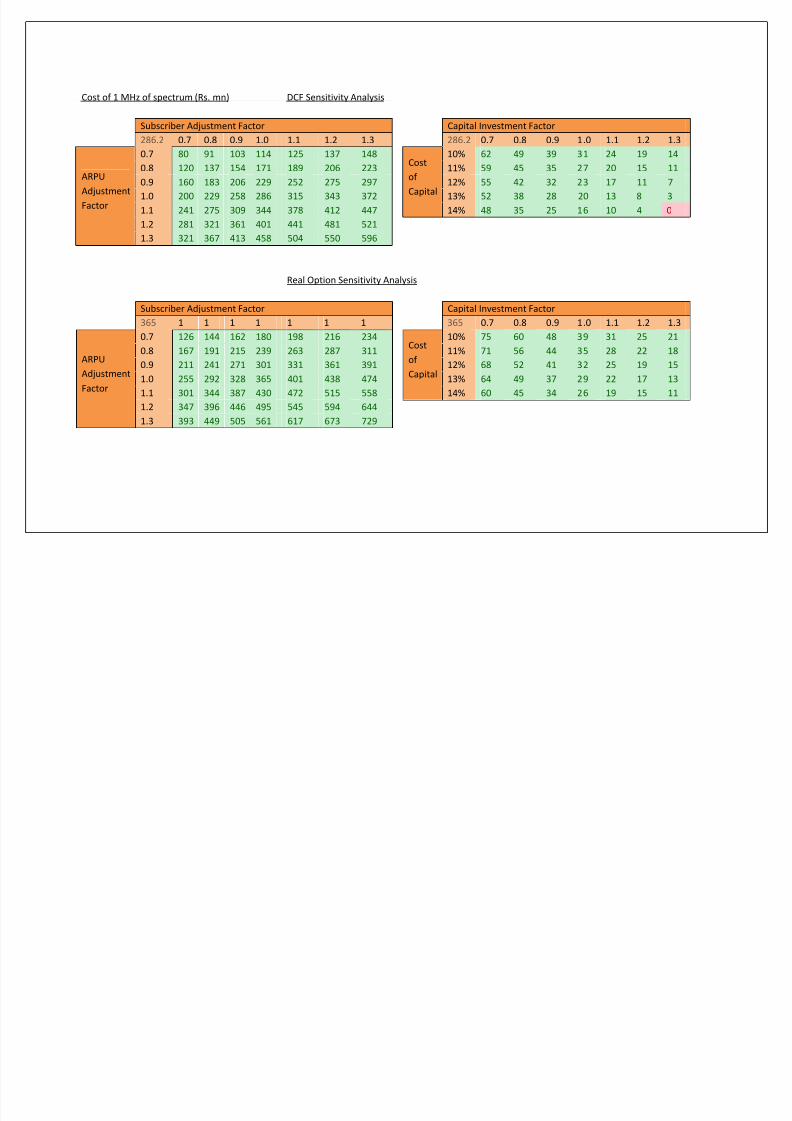

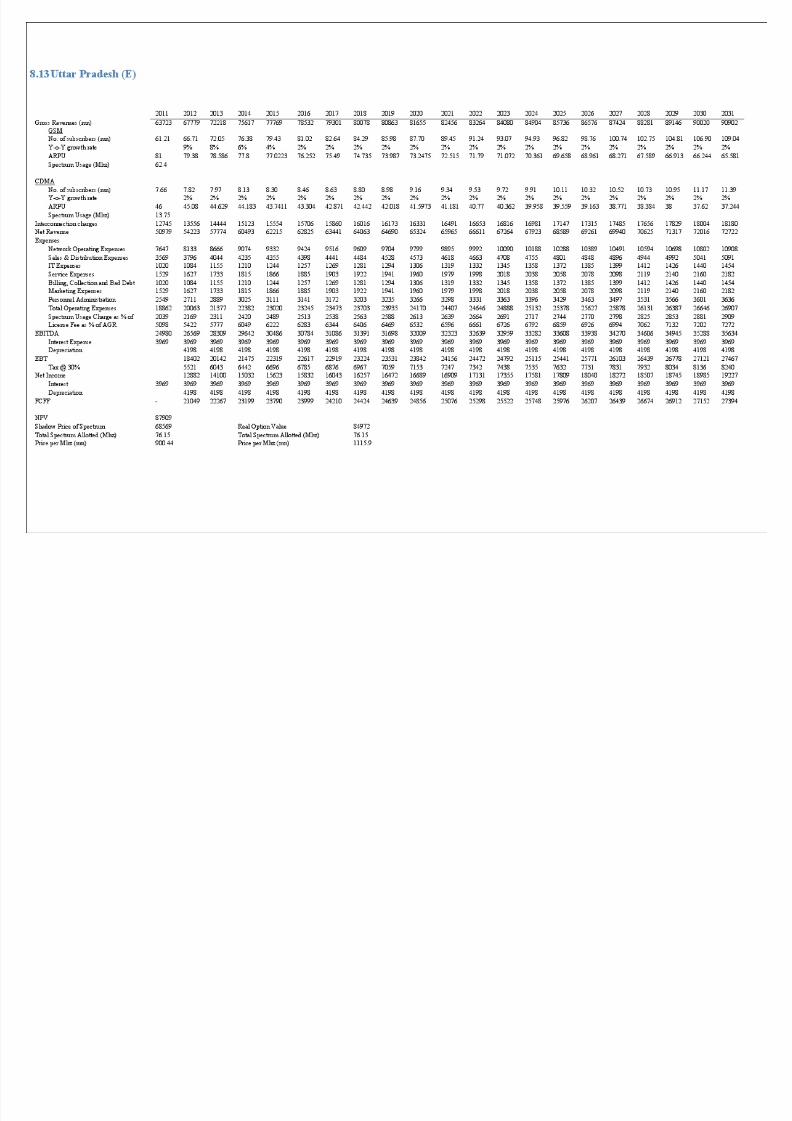

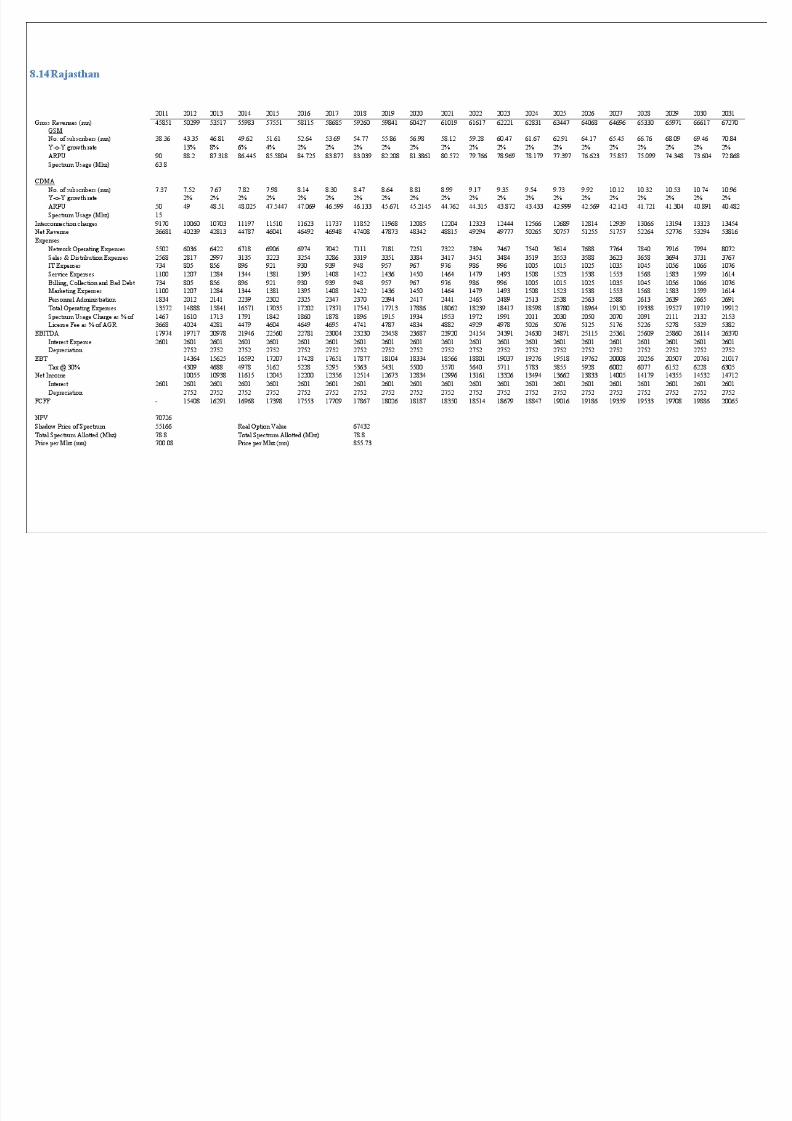

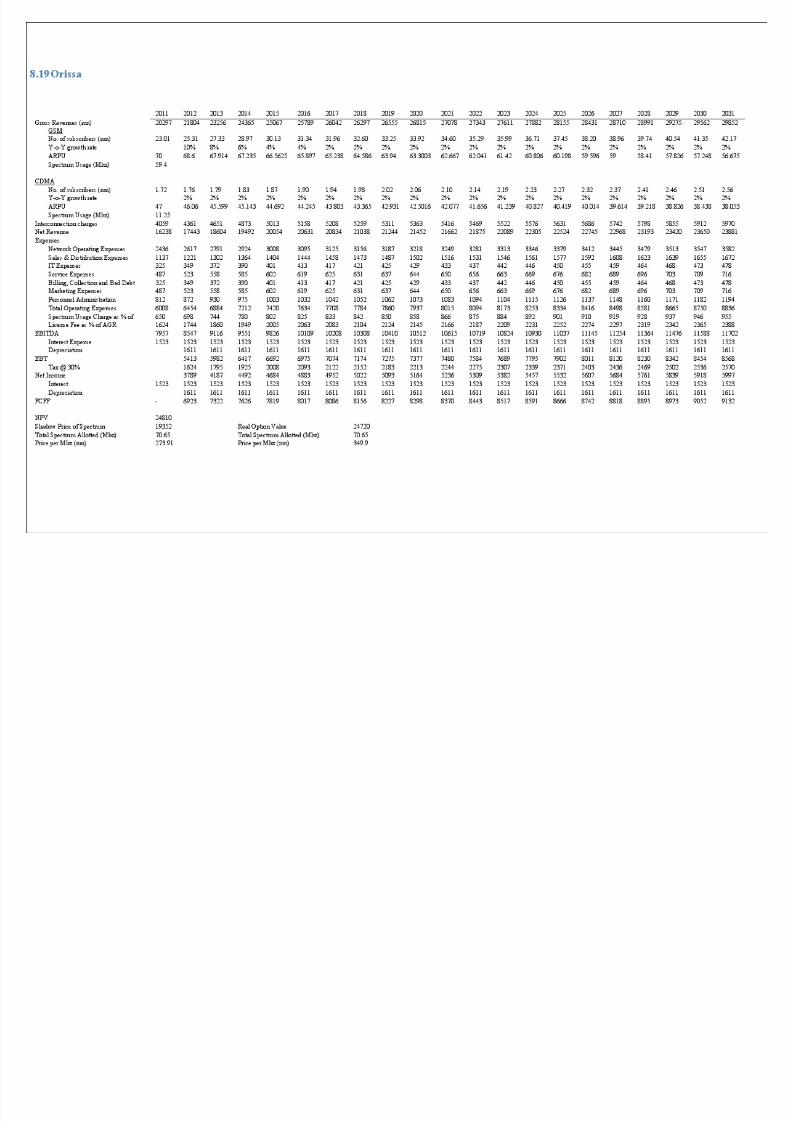

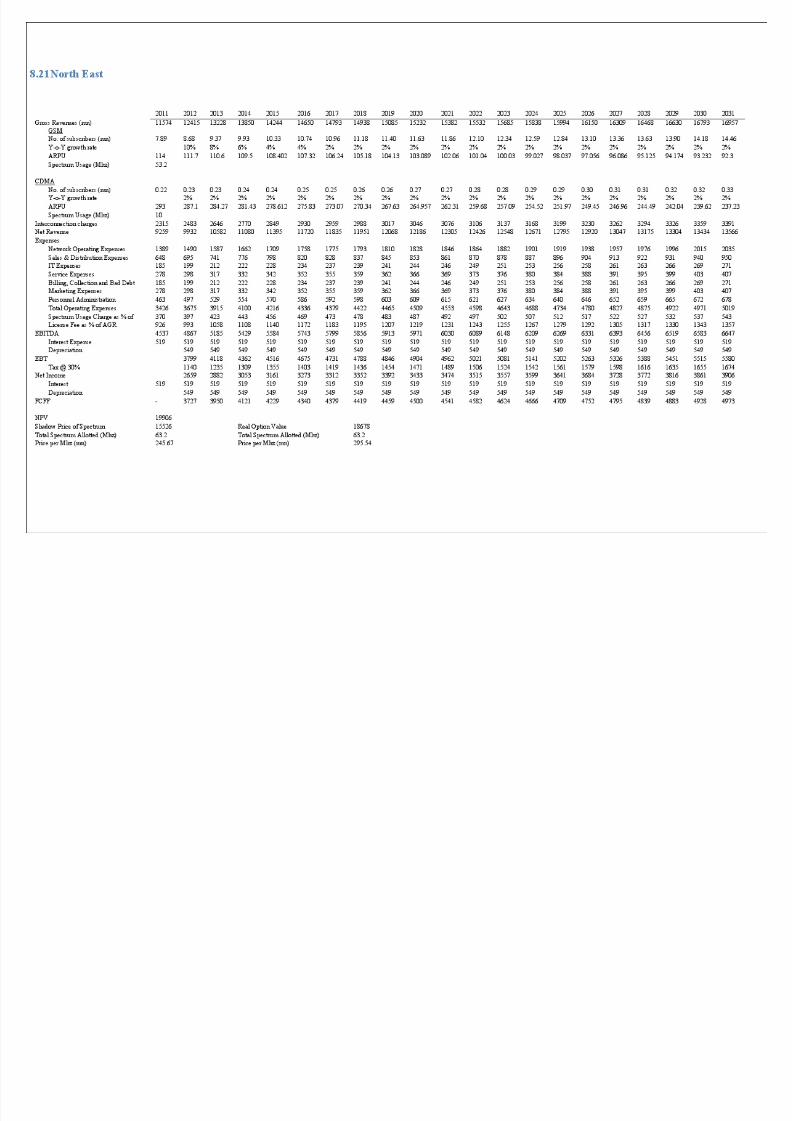

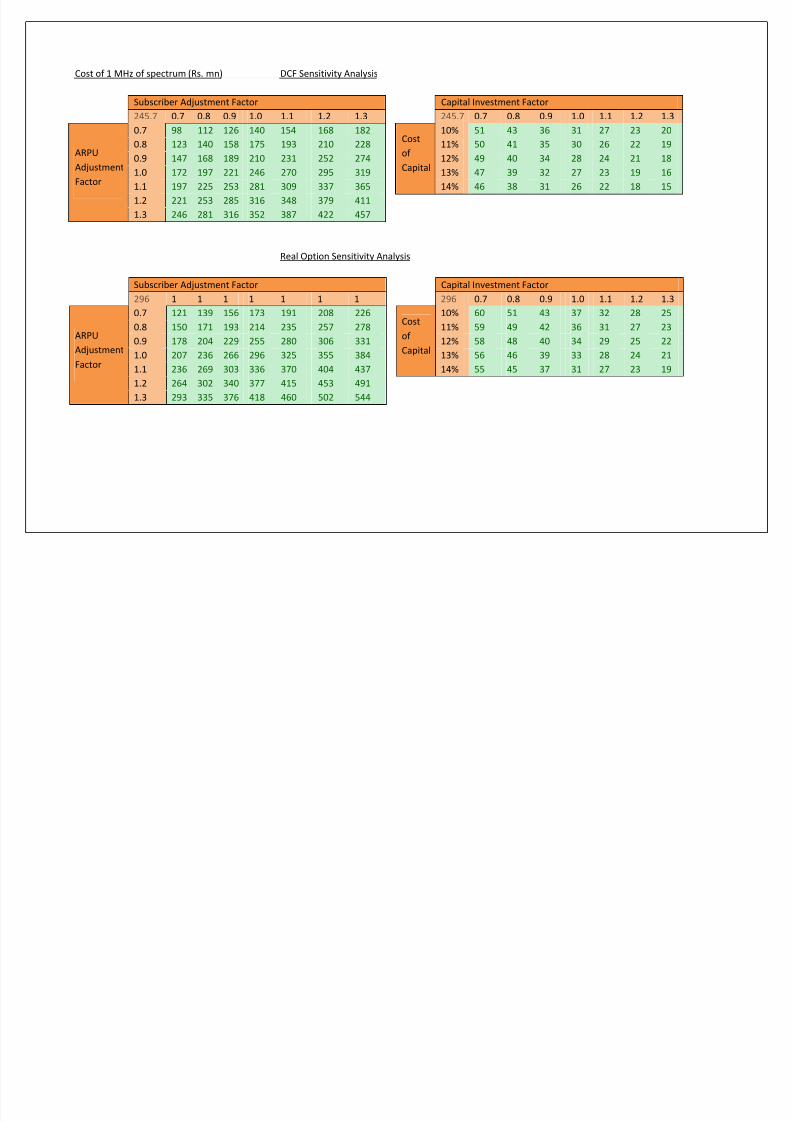

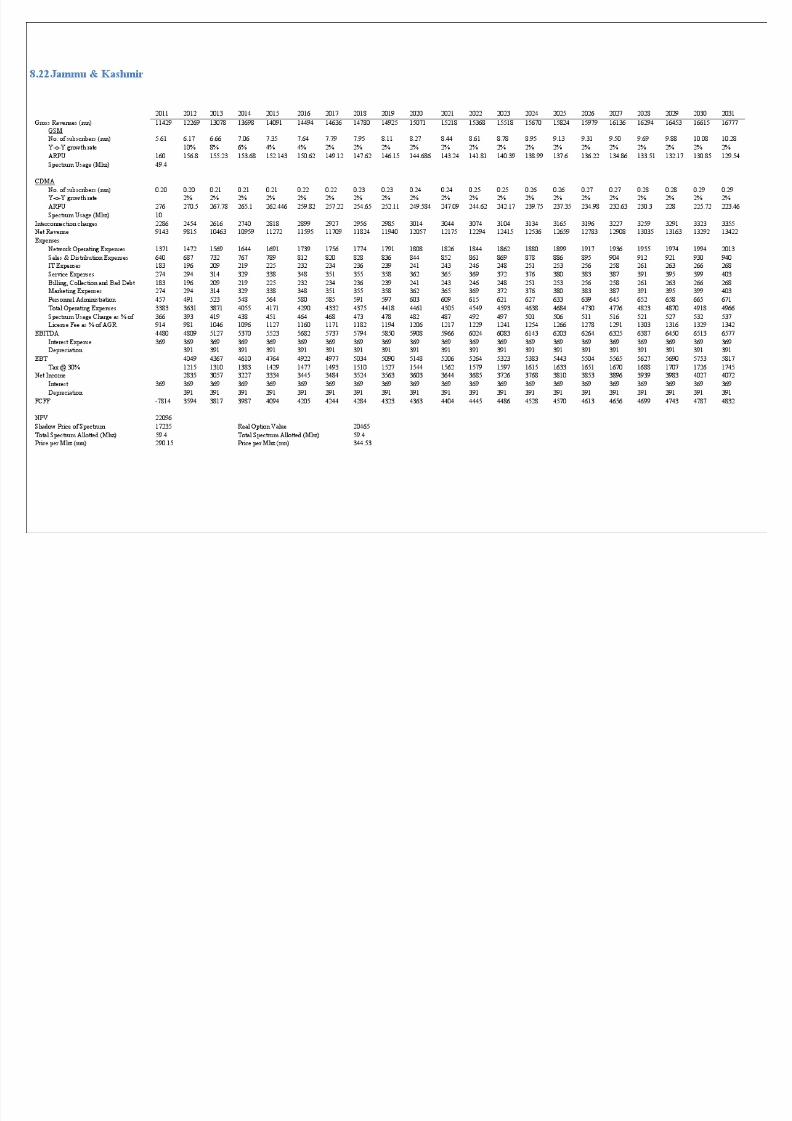

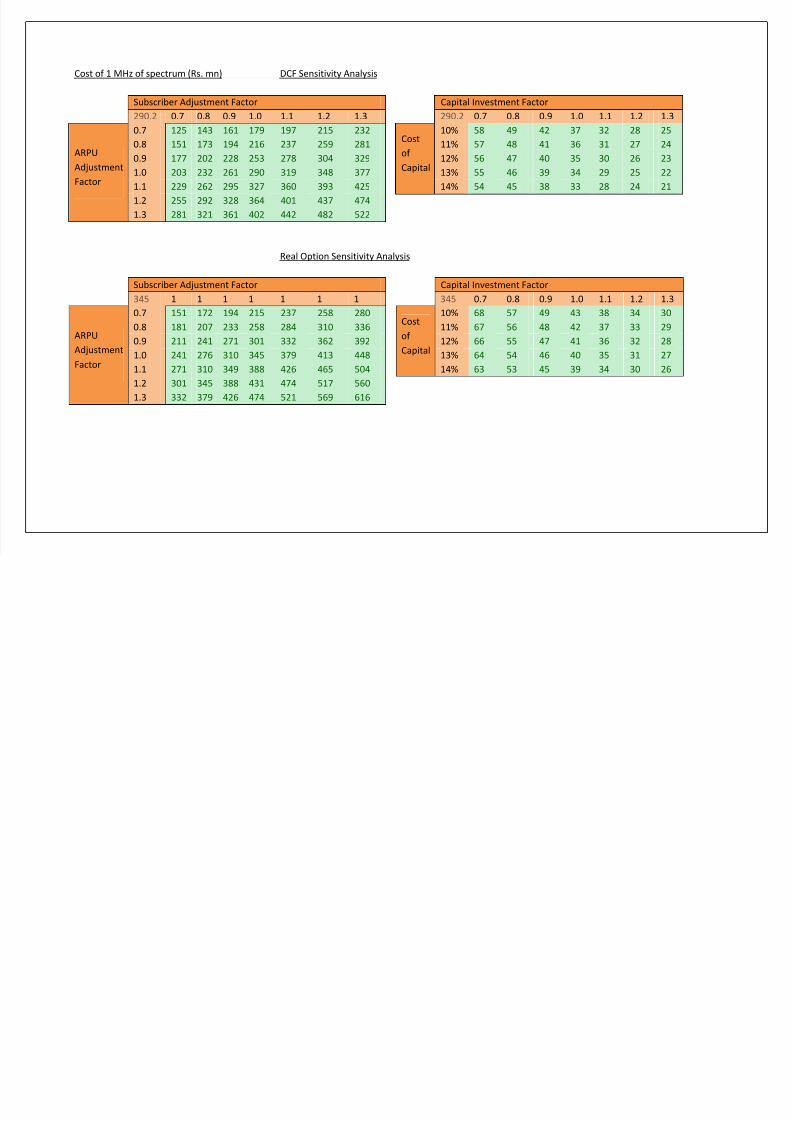

?ot of 1 E of *ectr(# R. #n -?B Seniti>it" !nal"i

S(crier !d(t#ent Bactor ?a*ital In>et#ent Bactor1077.4 0.7 0.8 0.9 1.0 1.1 1.2 1.3 1077.4 0.7 0.8 0.9 1.0 1.1 1.2 1.3

!R5

!d(t#ent

Bactor

0.7 37& 428 482 &36 &89 643 696

?ot of

?a*ital

10% 1707 1638 1&69 1&00 1430 1361 1292

0.8 &01 &73 64& 716 788 8&9 931 11% 1&39 1468 1398 1327 12&6 1186 111&

0.9 628 717 807 897 986 1076 1166 12% 1389 1317 124& 1173 1101 1029 9&7

1.0 7&4 862 970 1077 118& 1293 1401 13% 12&& 1181 1108 103& 962 888 81&

1.1 881 1006 1132 12&8 1384 1&10 163& 14% 1134 1060 98& 911 837 762 688

1.2 1007 11&1 129& 1439 1&82 1726 18701.3 1133 129& 14&7 1619 1781 1943 210&

Real ,*tion Seniti>it" !nal"i

S(crier !d(t#ent Bactor ?a*ital In>et#ent Bactor

132& 0.7 0.8 0.9 1.0 1.1 1.2 1.3 132& 0.7 0.8 0.9 1.0 1.1 1.2 1.3

!R5

!d(t#ent

Bactor

0.7 &00 &71 643 714 786 8&7 928

?ot of

?a*ital

10% 2030 19&7 1884 1812 1739 1668 1&97

0.8 640 731 822 914 100& 1097 1188 11% 183& 1761 1686 1612 1&39 1466 139&

0.9 783 894 1006 1118 1230 1342 14&3 12% 1661 1&8& 1&09 1434 1360 1288 1217

1.0 927 1060 1192 132& 14&7 1&90 1722 13% 1&0& 1428 13&1 1276 1201 1129 10&9

1.1 1073 1226 1379 1&33 1686 1839 1992 14% 1366 1287 1210 1134 1060 988 919

1.2 1219 1393 1&67 1741 191& 2089 2264

1.3 136& 1&60 17&& 19&0 214& 2340 2&3&

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 32/73

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 33/73

?ot of 1 E of *ectr(# R. #n -?B Seniti>it" !nal"i

S(crier !d(t#ent Bactor ?a*ital In>et#ent Bactor1&04.& 0.7 0.8 0.9 1.0 1.1 1.2 1.3 1&04.& 0.7 0.8 0.9 1.0 1.1 1.2 1.3

!R5

!d(t#ent

Bactor

0.7 1207 1379 1&&2 1724 1897 2069 2242?ot

of

?a*ital

10% 294 242 202 171 14& 124 107

0.8 11&6 1321 1486 16&1 1816 1981 2146 11% 28& 233 193 162 136 11& 98

0.9 1104 1262 1420 1&78 1736 1893 20&1 12% 277 224 184 1&3 127 106 88

1.0 10&3 1204 13&4 1&0& 16&& 180& 19&6 13% 268 216 17& 144 118 97 79

1.1 1002 114& 1288 1431 1&74 1717 1861 14% 2&9 207 167 13& 109 88 70

1.2 9&1 1086 1222 13&8 1494 1630 176&1.3 899 1028 11&6 128& 1413 1&42 1670

Real ,*tion Seniti>it" !nal"i

S(crier !d(t#ent Bactor ?a*ital In>et#ent Bactor

1818 0.7 0.8 0.9 1.0 1.1 1.2 1.3 1818 0.7 0.8 0.9 1.0 1.1 1.2 1.3

!R5

!d(t#ent

Bactor

0.7 733 837 942 1046 11&1 12&6 1360?ot

of

?a*ital

10% 349 288 242 20& 176 1&1 131

0.8 911 1041 1172 1302 1432 1&62 1692 11% 339 279 232 196 166 142 122

0.9 1092 1247 1403 1&&9 171& 1871 2027 12% 329 269 223 186 1&7 133 113

1.0 1273 14&4 1636 1818 2000 2181 2363 13% 320 2&9 213 177 147 123 104

1.1 14&4 1662 1869 2077 228& 2492 2700 14% 310 2&0 204 167 138 114 9&

1.2 163& 1869 2103 2336 2&70 2803 3037

1.3 1817 2076 2336 2&96 28&& 311& 3374

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 34/73

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 35/73

?ot of 1 E of *ectr(# R. #n -?B Seniti>it" !nal"i

S(crier !d(t#ent Bactor ?a*ital In>et#ent Bactor960.2 0.7 0.8 0.9 1.0 1.1 1.2 1.3 960.2 0.7 0.8 0.9 1.0 1.1 1.2 1.3

!R5

!d(t#ent

Bactor

0.7 346 396 44& 49& &44 &94 643?ot

of

?a*ital

10% 202 166 138 11& 97 82 70

0.8 4&& &20 &8& 6&0 71& 780 84& 11% 19& 1&9 130 108 90 7& 62

0.9 &64 644 72& 80& 886 966 1047 12% 188 1&1 123 101 83 68 &&

1.0 672 768 864 960 10&6 11&2 1248 13% 181 144 116 93 7& 60 48

1.1 781 892 1004 111& 1227 1338 14&0 14% 174 137 109 86 68 &3 40

1.2 889 1016 1143 1270 1397 1&24 16&11.3 998 1140 1283 142& 1&68 1710 18&3

Real ,*tion Seniti>it" !nal"i

S(crier !d(t#ent Bactor ?a*ital In>et#ent Bactor

1174 0.7 0.8 0.9 1.0 1.1 1.2 1.3 1174 0.7 0.8 0.9 1.0 1.1 1.2 1.3

!R5

!d(t#ent

Bactor

0.7 4&2 &16 &81 64& 710 77& 839?ot

of

?a*ital

10% 240 198 16& 140 119 101 87

0.8 &73 6&& 737 819 901 983 106& 11% 233 190 1&8 132 111 94 80

0.9 697 796 896 99& 109& 119& 1294 12% 22& 183 1&0 124 103 87 73

1.0 822 939 10&6 1174 1291 1408 1&26 13% 217 17& 142 117 96 79 66

1.1 947 1082 1217 13&3 1488 1623 17&8 14% 210 167 13& 109 89 73 &9

1.2 1072 1226 1379 1&32 168& 1838 1992

1.3 1198 1369 1&40 1712 1883 20&4 222&

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 36/73

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 37/73

?ot of 1 E of *ectr(# R. #n -?B Seniti>it" !nal"i

S(crier !d(t#ent Bactor ?a*ital In>et#ent Bactor1008.8 0.7 0.8 0.9 1.0 1.1 1.2 1.3 1008.8 0.7 0.8 0.9 1.0 1.1 1.2 1.3

!R5

!d(t#ent

Bactor

0.7 393 449 &0& &61 617 673 729?ot

of

?a*ital

10% 209 174 146 12& 107 93 80

0.8 497 &68 639 710 781 8&2 923 11% 203 168 141 119 101 87 74

0.9 602 688 774 8&9 94& 1031 1117 12% 197 162 13& 113 9& 81 69

1.0 706 807 908 1009 1110 1211 1311 13% 191 1&6 129 107 89 7& 63

1.1 811 926 1042 11&8 1274 1390 1&0& 14% 186 1&0 123 101 83 69 &7

1.2 91& 1046 1177 1307 1438 1&69 17001.3 1020 116& 1311 14&7 1602 1748 1894

Real ,*tion Seniti>it" !nal"i

S(crier !d(t#ent Bactor ?a*ital In>et#ent Bactor

1218 0.7 0.8 0.9 1.0 1.1 1.2 1.3 1218 0.7 0.8 0.9 1.0 1.1 1.2 1.3

!R5

!d(t#ent

Bactor

0.7 492 &62 633 703 773 844 914?ot

of

?a*ital

10% 247 206 17& 1&0 129 112 98

0.8 612 699 786 874 961 1048 1136 11% 241 200 168 143 123 106 92

0.9 732 836 941 1046 11&0 12&& 13&9 12% 23& 194 162 137 117 100 86

1.0 8&3 97& 1096 1218 1340 1462 1&84 13% 228 187 1&6 130 110 94 80

1.1 974 1113 12&2 1391 1&30 1669 1808 14% 222 181 149 124 104 87 74

1.2 109& 12&1 1408 1&64 1720 1877 2033

1.3 1216 1390 1&63 1737 1911 208& 22&8

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 38/73

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 39/73

?ot of 1 E of *ectr(# R. #n -?B Seniti>it" !nal"i

S(crier !d(t#ent Bactor ?a*ital In>et#ent Bactor146&.3 0.7 0.8 0.9 1.0 1.1 1.2 1.3 146&.3 0.7 0.8 0.9 1.0 1.1 1.2 1.3

!R5

!d(t#ent

Bactor

0.7 &&8 638 717 797 877 9&6 1036?ot

of

?a*ital

10% 306 2&3 213 181 1&4 133 114

0.8 714 816 918 1020 1122 1224 1326 11% 297 244 203 171 14& 123 10&

0.9 870 994 1118 1242 1367 1491 161& 12% 288 23& 194 162 136 114 96

1.0 1026 1172 1319 146& 1612 17&8 190& 13% 278 22& 18& 1&2 126 104 86

1.1 1182 13&0 1&19 1688 18&7 2026 2194 14% 269 216 17& 143 117 9& 77

1.2 1338 1&29 1720 1911 2102 2293 24841.3 1493 1707 1920 2134 2347 2&60 2774

Real ,*tion Seniti>it" !nal"i

S(crier !d(t#ent Bactor ?a*ital In>et#ent Bactor

1776 0.7 0.8 0.9 1 1.1 1.2 1.3 1776 0.7 0.8 0.9 1.0 1.1 1.2 1.3

!R5

!d(t#ent

Bactor

0.7 707 808 909 1010 1111 1211 1312?ot

of

?a*ital

10% 363 301 2&4 217 187 162 140

0.8 884 1010 1136 1263 1389 1&1& 1641 11% 3&3 291 244 207 177 1&2 131

0.9 1063 121& 1367 1&18 1670 1822 1974 12% 343 281 234 197 167 142 121

1.0 1243 1420 1&98 1776 19&3 2131 2308 13% 333 271 224 187 1&7 132 112

1.1 1423 1627 1830 2033 2237 2440 2643 14% 323 261 214 177 147 123 103

1.2 1604 1833 2062 2292 2&21 27&0 2979

1.3 178& 2040 229& 2&&0 280& 3060 331&

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 40/73

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 41/73

?ot of 1 E of *ectr(# R. #n -?B Seniti>it" !nal"i

S(crier !d(t#ent Bactor ?a*ital In>et#ent Bactor1244.3 0.7 0.8 0.9 1.0 1.1 1.2 1.3 1244.3 0.7 0.8 0.9 1.0 1.1 1.2 1.3

!R5

!d(t#ent

Bactor

0.7 288 330 371 412 4&3 494 &36?ot

of

?a*ital

10% 2&8 219 189 16& 14& 129 11&

0.8 386 288 288 288 288 288 288 11% 2&4 21& 184 160 141 124 111

0.9 483 288 288 288 288 288 288 12% 249 210 180 1&6 136 120 106

1.0 &80 288 288 288 288 288 288 13% 24& 206 17& 1&1 132 11& 102

1.1 677 288 288 288 288 288 288 14% 240 201 171 147 127 111 97

1.2 77& 288 288 288 288 288 2881.3 872 288 288 288 288 288 288

Real ,*tion Seniti>it" !nal"i

S(crier !d(t#ent Bactor ?a*ital In>et#ent Bactor

1479 1 1 1 1 1 1 1 1479 0.7 0.8 0.9 1.0 1.1 1.2 1.3

!R5

!d(t#ent

Bactor

0.7 &00 &71 643 714 786 8&7 928?ot

of

?a*ital

10% 303 2&8 223 19& 172 1&3 137

0.8 640 &00 &00 &00 &00 &00 &00 11% 298 2&3 218 190 167 148 132

0.9 783 &00 &00 &00 &00 &00 &00 12% 293 248 213 18& 162 143 127

1.0 927 &00 &00 &00 &00 &00 &00 13% 289 243 208 180 1&7 139 123

1.1 1073 &00 &00 &00 &00 &00 &00 14% 284 238 203 17& 1&3 134 118

1.2 1219 &00 &00 &00 &00 &00 &00

1.3 136& &00 &00 &00 &00 &00 &00

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 42/73

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 43/73

?ot of 1 E of *ectr(# R. #n -?B Seniti>it" !nal"i

S(crier !d(t#ent Bactor ?a*ital In>et#ent Bactor

781.8 0.7 0.8 0.9 1.0 1.1 1.2 1.3 781.8 0.7 0.8 0.9 1.0 1.1 1.2 1.3

!R5

!d(t#ent

Bactor

0.7 330 377 424 471 &18 &6& 612

?ot

of

?a*ital

10% 16& 140 120 10& 92 82 73

0.8 402 460 &17 &7& 632 689 747 11% 162 137 117 102 89 78 70

0.9 47& &43 610 678 746 814 882 12% 1&9 133 114 98 86 7& 66

1.0 &47 62& 704 782 860 938 1016 13% 1&& 130 111 9& 83 72 63

1.1 620 708 797 88& 974 1063 11&1 14% 1&2 127 108 92 80 69 60

1.2 692 791 890 989 1088 1187 1286

1.3 76& 874 983 1093 1202 1311 1421

Real ,*tion Seniti>it" !nal"i

S(crier !d(t#ent Bactor ?a*ital In>et#ent Bactor

932 1 1 1 1 1 1 1 932 0.7 0.8 0.9 1.0 1.1 1.2 1.3

!R5

!d(t#ent

Bactor

0.7 400 4&7 &1& &72 629 686 743

?ot

of

?a*ital

10% 194 164 142 124 109 97 87

0.8 484 &&3 622 692 761 830 899 11% 190 161 139 121 106 94 83

0.9 &68 649 731 812 893 974 10&& 12% 187 1&8 13& 117 103 90 80

1.0 6&2 746 839 932 102& 1118 1211 13% 184 1&4 132 114 99 87 77

1.1 736 842 947 10&2 11&7 1262 1368 14% 180 1&1 128 110 96 84 73

1.2 821 938 10&& 1172 1290 1407 1&24

1.3 90& 1034 1163 1292 1422 1&&1 1680

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 44/73

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 45/73

?ot of 1 E of *ectr(# R. #n -?B Seniti>it" !nal"i

S(crier !d(t#ent Bactor ?a*ital In>et#ent Bactor

341.4 0.7 0.8 0.9 1.0 1.1 1.2 1.3 341.4 0.7 0.8 0.9 1.0 1.1 1.2 1.3

!R5

!d(t#ent

Bactor

0.7 118 13& 1&2 168 18& 202 219?ot

of

?a*ital

10% 77 63 &2 44 37 31 26

0.8 1&8 181 203 226 249 271 294 11% 74 60 49 41 34 28 23

0.9 199 227 2&& 284 312 340 369 12% 71 &7 47 38 31 2& 21

1.0 239 273 307 341 376 410 444 13% 68 &4 44 3& 28 22 18

1.1 279 319 3&9 399 439 479 &19 14% 6& &2 41 32 2& 20 1&

1.2 320 36& 411 4&7 &02 &48 &94

1.3 360 412 463 &14 &66 617 669

Real ,*tion Seniti>it" !nal"i

S(crier !d(t#ent Bactor ?a*ital In>et#ent Bactor

420 1 1 1 1 1 1 1 420 0.7 0.8 0.9 1.0 1.1 1.2 1.3

!R5

!d(t#ent

Bactor

0.7 1&8 181 203 226 248 271 293?ot

of

?a*ital

10% 91 7& 63 &3 4& 39 33

0.8 202 231 260 289 318 347 376 11% 88 72 60 &0 42 36 30

0.9 248 283 319 3&4 390 42& 461 12% 8& 69 &7 47 39 33 27

1.0 294 336 378 420 462 &04 &46 13% 82 66 &4 44 36 30 2&

1.1 341 389 438 487 &3& &84 633 14% 79 63 &1 41 34 27 22

1.2 387 443 498 &&3 609 664 719

1.3 434 496 &&8 620 682 744 806

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 46/73

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 47/73

?ot of 1 E of *ectr(# R. #n -?B Seniti>it" !nal"i

S(crier !d(t#ent Bactor ?a*ital In>et#ent Bactor

8&1.& 0.7 0.8 0.9 1.0 1.1 1.2 1.3 8&1.& 0.7 0.8 0.9 1.0 1.1 1.2 1.3

!R5

!d(t#ent

Bactor

0.7 337 38& 433 481 &29 &77 62&?ot

of

?a*ital

10% 172 143 121 103 88 76 66

0.8 423 483 &44 604 66& 72& 786 11% 168 139 116 98 84 72 62

0.9 &10 &82 6&& 728 801 874 946 12% 163 134 111 93 79 67 &7

1.0 &96 681 766 8&2 937 1022 1107 13% 1&8 129 107 89 74 62 &2

1.1 683 780 878 97& 1073 1170 1268 14% 1&4 124 102 84 69 &7 47

1.2 769 879 989 1099 1209 1318 1428

1.3 8&6 978 1100 1222 134& 1467 1&89

Real ,*tion Seniti>it" !nal"i

S(crier !d(t#ent Bactor ?a*ital In>et#ent Bactor

1026 1 1 1 1 1 1 1 1026 0.7 0.8 0.9 1.0 1.1 1.2 1.3

!R5

!d(t#ent

Bactor

0.7 419 479 &39 &98 6&8 718 778?ot

of

?a*ital

10% 204 170 144 123 106 92 81

0.8 &18 &92 666 740 814 888 962 11% 199 16& 139 118 101 87 76

0.9 618 706 794 883 971 10&9 1148 12% 194 160 134 113 96 82 71

1.0 718 821 923 1026 1128 1231 1333 13% 189 1&& 129 108 91 77 66

1.1 818 93& 10&2 1169 1286 1403 1&20 14% 184 1&0 124 103 86 73 61

1.2 919 10&0 1181 1312 1443 1&7& 1706

1.3 1019 1164 1310 14&6 1601 1747 1892

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 48/73

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 49/73

?ot of 1 E of *ectr(# R. #n -?B Seniti>it" !nal"i

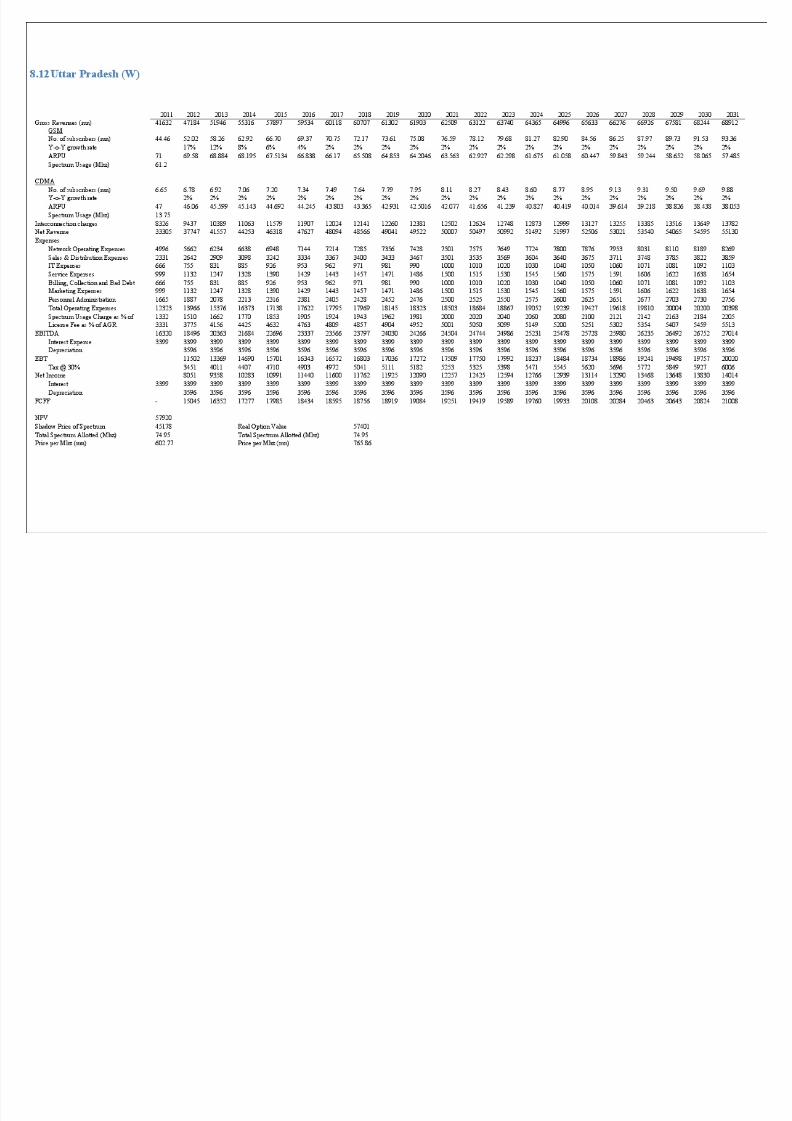

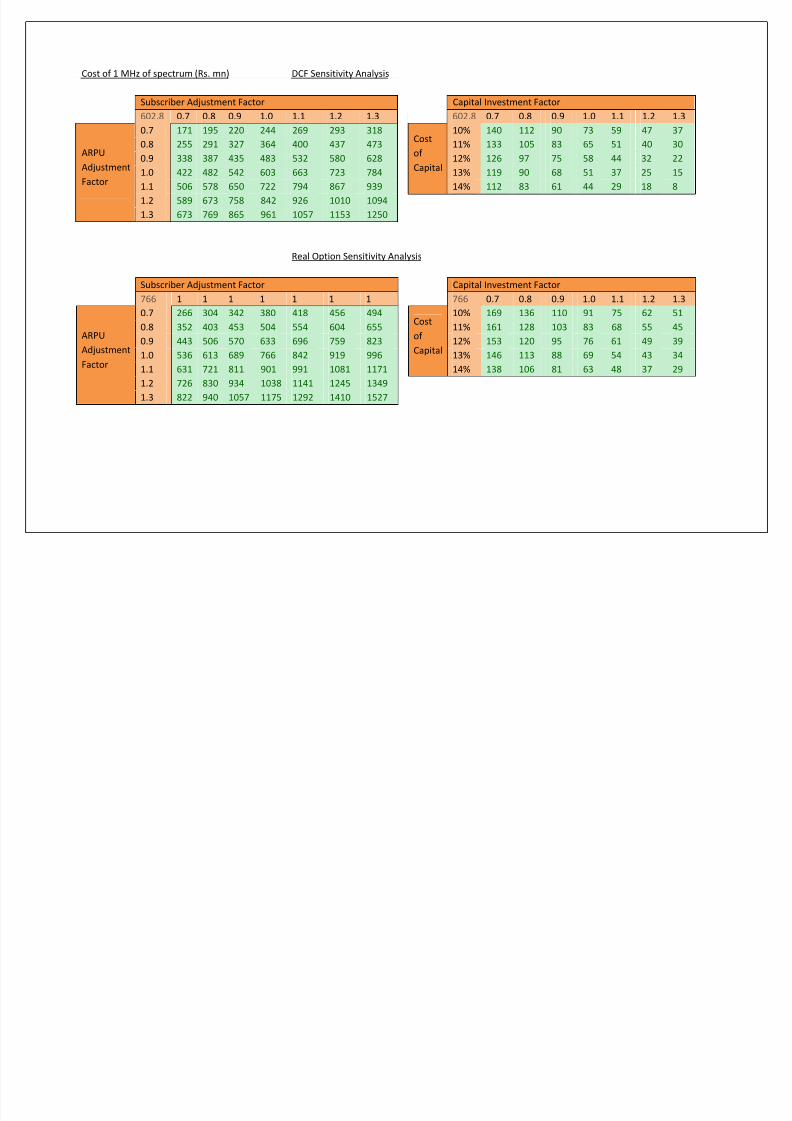

S(crier !d(t#ent Bactor ?a*ital In>et#ent Bactor

602.0 0.7 0.8 0.9 1.0 1.1 1.2 1.3 602.0 0.7 0.8 0.9 1.0 1.1 1.2 1.3

!R5

!d(t#ent

Bactor

0.7 22& 2&7 289 321 3&3 38& 417?ot

of

?a*ital

10% 116 9& 79 66 &6 47 40

0.8 290 332 373 41& 4&6 498 &39 11% 112 91 7& 62 &1 43 36

0.9 3&6 407 4&8 &08 &&9 610 661 12% 108 87 70 &8 47 39 32

1.0 421 482 &42 602 662 722 783 13% 104 83 66 &4 43 3& 27

1.1 487 &&7 626 696 76& 83& 904 14% 100 78 62 49 39 31 23

1.2 &&3 631 710 789 868 947 1026

1.3 618 706 79& 883 971 1060 1148

Real ,*tion Seniti>it" !nal"i

S(crier !d(t#ent Bactor ?a*ital In>et#ent Bactor

732 1 1 1 1 1 1 1 732 0.7 0.8 0.9 1.0 1.1 1.2 1.3

!R5

!d(t#ent

Bactor

0.7 288 329 370 411 4&2 493 &34?ot

of

?a*ital

10% 138 113 9& 80 68 &8 &0

0.8 362 413 46& &17 &68 620 672 11% 133 109 90 7& 63 &4 46

0.9 437 499 &61 624 686 749 811 12% 129 104 86 71 &9 &0 42

1.0 &12 &8& 6&9 732 80& 878 9&1 13% 124 100 81 67 && 46 38

1.1 &88 672 7&6 840 924 1008 1092 14% 120 96 77 63 &1 42 34

1.2 664 7&9 8&4 949 1043 1138 1233

1.3 740 846 9&1 10&7 1163 1269 1374

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 50/73

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 51/73

?ot of 1 E of *ectr(# R. #n -?B Seniti>it" !nal"i

S(crier !d(t#ent Bactor ?a*ital In>et#ent Bactor

286.2 0.7 0.8 0.9 1.0 1.1 1.2 1.3 286.2 0.7 0.8 0.9 1.0 1.1 1.2 1.3

!R5

!d(t#ent

Bactor

0.7 80 91 103 114 12& 137 148?ot

of

?a*ital

10% 62 49 39 31 24 19 14

0.8 120 137 1&4 171 189 206 223 11% &9 4& 3& 27 20 1& 11

0.9 160 183 206 229 2&2 27& 297 12% && 42 32 23 17 11 7

1.0 200 229 2&8 286 31& 343 372 13% &2 38 28 20 13 8 3

1.1 241 27& 309 344 378 412 447 14% 48 3& 2& 16 10 4 0

1.2 281 321 361 401 441 481 &21

1.3 321 367 413 4&8 &04 &&0 &96

Real ,*tion Seniti>it" !nal"i

S(crier !d(t#ent Bactor ?a*ital In>et#ent Bactor

36& 1 1 1 1 1 1 1 36& 0.7 0.8 0.9 1.0 1.1 1.2 1.3

!R5

!d(t#ent

Bactor

0.7 126 144 162 180 198 216 234?ot

of

?a*ital

10% 7& 60 48 39 31 2& 21

0.8 167 191 21& 239 263 287 311 11% 71 &6 44 3& 28 22 18

0.9 211 241 271 301 331 361 391 12% 68 &2 41 32 2& 19 1&

1.0 2&& 292 328 36& 401 438 474 13% 64 49 37 29 22 17 13

1.1 301 344 387 430 472 &1& &&8 14% 60 4& 34 26 19 1& 11

1.2 347 396 446 49& &4& &94 644

1.3 393 449 &0& &61 617 673 729

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 52/73

? t f 1 f t R -?B S iti it ! l i

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 53/73

?ot of 1 E of *ectr(# R. #n -?B Seniti>it" !nal"i

S(crier !d(t#ent Bactor ?a*ital In>et#ent Bactor

602.8 0.7 0.8 0.9 1.0 1.1 1.2 1.3 602.8 0.7 0.8 0.9 1.0 1.1 1.2 1.3

!R5

!d(t#ent

Bactor

0.7 171 19& 220 244 269 293 318?ot

of

?a*ital

10% 140 112 90 73 &9 47 37

0.8 2&& 291 327 364 400 437 473 11% 133 10& 83 6& &1 40 30

0.9 338 387 43& 483 &32 &80 628 12% 126 97 7& &8 44 32 22

1.0 422 482 &42 603 663 723 784 13% 119 90 68 &1 37 2& 1&

1.1 &06 &78 6&0 722 794 867 939 14% 112 83 61 44 29 18 8

1.2 &89 673 7&8 842 926 1010 1094

1.3 673 769 86& 961 10&7 11&3 12&0

Real ,*tion Seniti>it" !nal"i

S(crier !d(t#ent Bactor ?a*ital In>et#ent Bactor

766 1 1 1 1 1 1 1 766 0.7 0.8 0.9 1.0 1.1 1.2 1.3

!R5

!d(t#ent

Bactor

0.7 266 304 342 380 418 4&6 494?ot

of

?a*ital

10% 169 136 110 91 7& 62 &1

0.8 3&2 403 4&3 &04 &&4 604 6&& 11% 161 128 103 83 68 && 4&

0.9 443 &06 &70 633 696 7&9 823 12% 1&3 120 9& 76 61 49 39

1.0 &36 613 689 766 842 919 996 13% 146 113 88 69 &4 43 34

1.1 631 721 811 901 991 1081 1171 14% 138 106 81 63 48 37 29

1.2 726 830 934 1038 1141 124& 1349

1.3 822 940 10&7 117& 1292 1410 1&27

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 54/73

?ot of 1 E of *ectr(# R #n -?B Seniti>it" !nal"i

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 55/73

?ot of 1 E of *ectr(# R. #n -?B Seniti>it" !nal"i

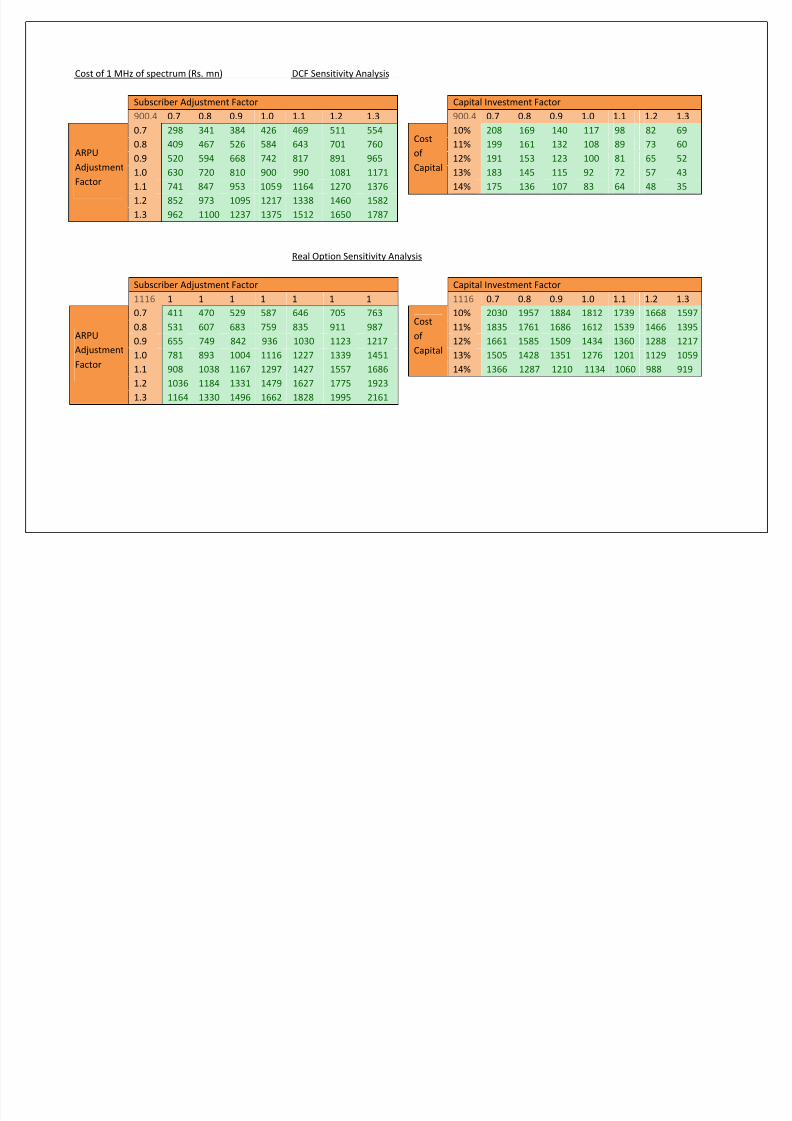

S(crier !d(t#ent Bactor ?a*ital In>et#ent Bactor

900.4 0.7 0.8 0.9 1.0 1.1 1.2 1.3 900.4 0.7 0.8 0.9 1.0 1.1 1.2 1.3

!R5

!d(t#ent

Bactor

0.7 298 341 384 426 469 &11 &&4?ot

of

?a*ital

10% 208 169 140 117 98 82 69

0.8 409 467 &26 &84 643 701 760 11% 199 161 132 108 89 73 60

0.9 &20 &94 668 742 817 891 96& 12% 191 1&3 123 100 81 6& &2

1.0 630 720 810 900 990 1081 1171 13% 183 14& 11& 92 72 &7 43

1.1 741 847 9&3 10&9 1164 1270 1376 14% 17& 136 107 83 64 48 3&

1.2 8&2 973 109& 1217 1338 1460 1&82

1.3 962 1100 1237 137& 1&12 16&0 1787

Real ,*tion Seniti>it" !nal"i

S(crier !d(t#ent Bactor ?a*ital In>et#ent Bactor

1116 1 1 1 1 1 1 1 1116 0.7 0.8 0.9 1.0 1.1 1.2 1.3

!R5

!d(t#ent

Bactor

0.7 411 470 &29 &87 646 70& 763?ot

of

?a*ital

10% 2030 19&7 1884 1812 1739 1668 1&97

0.8 &31 607 683 7&9 83& 911 987 11% 183& 1761 1686 1612 1&39 1466 139&

0.9 6&& 749 842 936 1030 1123 1217 12% 1661 1&8& 1&09 1434 1360 1288 1217

1.0 781 893 1004 1116 1227 1339 14&1 13% 1&0& 1428 13&1 1276 1201 1129 10&9

1.1 908 1038 1167 1297 1427 1&&7 1686 14% 1366 1287 1210 1134 1060 988 919

1.2 1036 1184 1331 1479 1627 177& 1923

1.3 1164 1330 1496 1662 1828 199& 2161

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 56/73

?ot of 1 E of *ectr(# R. #n -?B Seniti>it" !nal"i

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 57/73

* " "

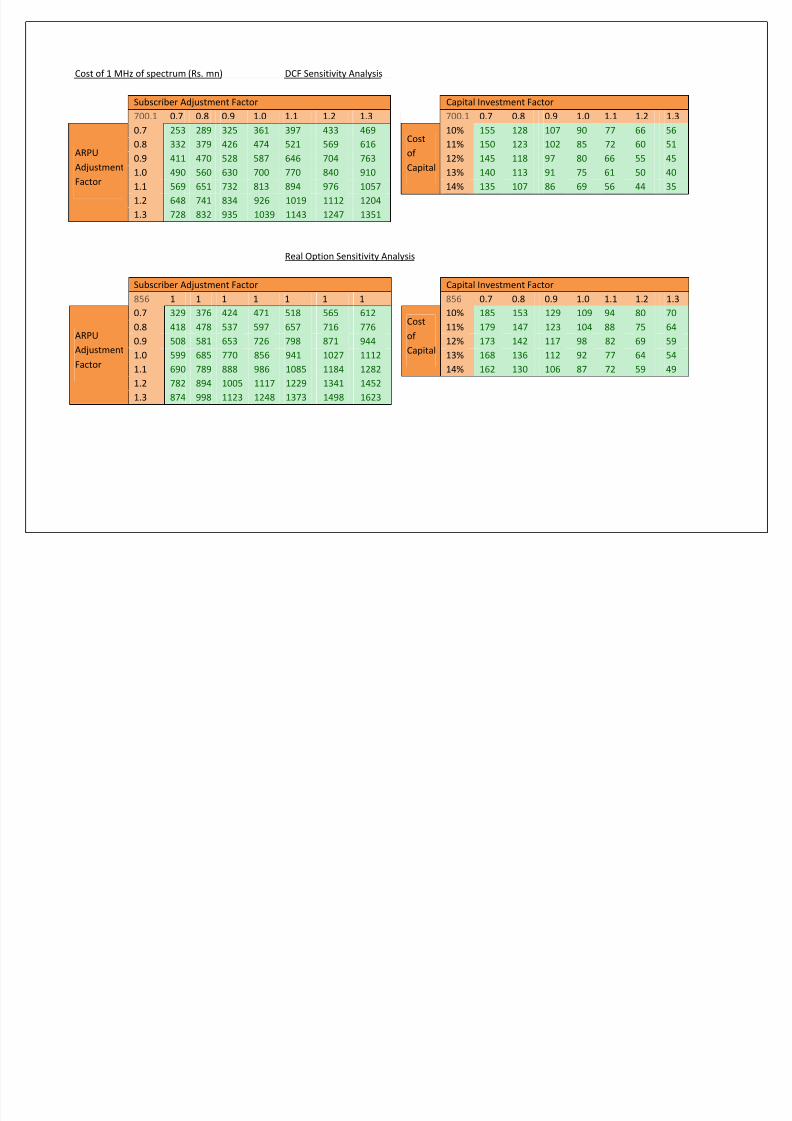

S(crier !d(t#ent Bactor ?a*ital In>et#ent Bactor

700.1 0.7 0.8 0.9 1.0 1.1 1.2 1.3 700.1 0.7 0.8 0.9 1.0 1.1 1.2 1.3

!R5

!d(t#ent

Bactor

0.7 2&3 289 32& 361 397 433 469?ot

of

?a*ital

10% 1&& 128 107 90 77 66 &6

0.8 332 379 426 474 &21 &69 616 11% 1&0 123 102 8& 72 60 &1

0.9 411 470 &28 &87 646 704 763 12% 14& 118 97 80 66 && 4&

1.0 490 &60 630 700 770 840 910 13% 140 113 91 7& 61 &0 40

1.1 &69 6&1 732 813 894 976 10&7 14% 13& 107 86 69 &6 44 3&

1.2 648 741 834 926 1019 1112 1204

1.3 728 832 93& 1039 1143 1247 13&1

Real ,*tion Seniti>it" !nal"i

S(crier !d(t#ent Bactor ?a*ital In>et#ent Bactor

8&6 1 1 1 1 1 1 1 8&6 0.7 0.8 0.9 1.0 1.1 1.2 1.3

!R5

!d(t#ent

Bactor

0.7 329 376 424 471 &18 &6& 612?ot

of

?a*ital

10% 18& 1&3 129 109 94 80 70

0.8 418 478 &37 &97 6&7 716 776 11% 179 147 123 104 88 7& 64

0.9 &08 &81 6&3 726 798 871 944 12% 173 142 117 98 82 69 &9

1.0 &99 68& 770 8&6 941 1027 1112 13% 168 136 112 92 77 64 &4

1.1 690 789 888 986 108& 1184 1282 14% 162 130 106 87 72 &9 49

1.2 782 894 100& 1117 1229 1341 14&2

1.3 874 998 1123 1248 1373 1498 1623

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 58/73

?ot of 1 E of *ectr(# R. #n -?B Seniti>it" !nal"i

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 59/73

S(crier !d(t#ent Bactor ?a*ital In>et#ent Bactor

6&2.& 0.7 0.8 0.9 1.0 1.1 1.2 1.3 6&2.& 0.7 0.8 0.9 1.0 1.1 1.2 1.3

!R5

!d(t#ent

Bactor

0.7 21& 246 276 307 338 368 399?ot

of

?a*ital

10% 1&1 123 102 8& 71 &9 &0

0.8 296 338 380 422 464 &07 &49 11% 14& 117 96 78 6& &3 43

0.9 376 430 484 &37 &91 64& 699 12% 139 111 89 72 &8 47 37

1.0 4&7 &22 &87 6&2 718 783 848 13% 133 10& 83 66 &2 41 31

1.1 &37 614 691 768 844 921 998 14% 127 99 77 60 46 3& 2&

1.2 618 706 79& 883 971 10&9 1148

1.3 699 798 898 998 1098 1198 1297

Real ,*tion Seniti>it" !nal"i

S(crier !d(t#ent Bactor ?a*ital In>et#ent Bactor

809 1 1 1 1 1 1 1 809 0.7 0.8 0.9 1.0 1.1 1.2 1.3

!R5

!d(t#ent

Bactor

0.7 297 340 382 42& 467 &10 &&2?ot

of

?a*ital

10% 180 148 123 103 87 74 63

0.8 38& 440 49& &&0 60& 660 71& 11% 173 141 116 97 81 68 &7

0.9 47& &43 611 679 746 814 882 12% 167 13& 110 90 7& 62 &1

1.0 &67 647 728 809 890 971 10&2 13% 160 128 104 84 69 &6 46

1.1 6&9 7&3 847 941 1036 1130 1224 14% 1&4 122 97 78 63 &1 41

1.2 7&2 8&9 967 1074 1182 1289 1396

1.3 84& 966 1087 1207 1328 1449 1&69

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 60/73

?ot of 1 E of *ectr(# R. #n -?B Seniti>it" !nal"i

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 61/73

S(crier !d(t#ent Bactor ?a*ital In>et#ent Bactor

423.3 0.7 0.8 0.9 1.0 1.1 1.2 1.3 423.3 0.7 0.8 0.9 1.0 1.1 1.2 1.3

!R5

!d(t#ent

Bactor

0.7 98 112 126 140 1&4 168 182?ot

of

?a*ital

10% 109 86 68 && 43 34 26

0.8 164 187 211 234 2&8 281 304 11% 102 80 62 48 37 27 19

0.9 230 263 296 329 362 39& 427 12% 96 73 &6 42 30 21 13

1.0 296 339 381 423 466 &08 &&0 13% 90 67 49 3& 24 14 6

1.1 363 414 466 &18 &70 621 673 14% 83 61 43 29 17 8 0

1.2 429 490 &&1 612 674 73& 796

1.3 49& &66 636 707 778 848 919

Real ,*tion Seniti>it" !nal"i

S(crier !d(t#ent Bactor ?a*ital In>et#ent Bactor

&&& 1 1 1 1 1 1 1 &&& 0.7 0.8 0.9 1.0 1.1 1.2 1.3

!R5

!d(t#ent

Bactor

0.7 183 210 236 262 288 314 340?ot

of

?a*ital

10% 131 10& 8& 69 &6 46 38

0.8 248 283 319 3&4 390 42& 460 11% 12& 98 78 63 &0 41 33

0.9 317 362 407 4&3 498 &43 &88 12% 118 92 72 &7 4& 3& 28

1.0 388 444 499 &&& 610 666 721 13% 111 8& 66 &1 40 31 24

1.1 462 &28 &94 660 726 792 8&8 14% 10& 79 60 46 3& 26 20

1.2 &37 613 690 767 843 920 997

1.3 612 700 787 87& 962 10&0 1137

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 62/73

?ot of 1 E of *ectr(# R. #n -?B Seniti>it" !nal"i

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 63/73

S(crier !d(t#ent Bactor ?a*ital In>et#ent Bactor

111.0 0.7 0.8 0.9 1.0 1.1 1.2 1.3 111.0 0.7 0.8 0.9 1.0 1.1 1.2 1.3

!R5

!d(t#ent

Bactor

0.7 3& 40 4& &0 && 60 6&?ot

of

?a*ital

10% 26 21 17 14 12 10 8

0.8 49 &6 63 70 77 8& 92 11% 2& 20 16 13 11 9 7

0.9 63 73 82 91 100 109 118 12% 24 19 1& 12 9 7 6

1.0 78 89 100 111 122 133 144 13% 22 18 14 11 8 6 &

1.1 92 10& 118 131 144 1&8 171 14% 21 16 13 10 7 & 3

1.2 106 121 136 1&2 167 182 197

1.3 120 137 1&& 172 189 206 223

Real ,*tion Seniti>it" !nal"i

S(crier !d(t#ent Bactor ?a*ital In>et#ent Bactor

139 1 1 1 1 1 1 1 139 0.7 0.8 0.9 1.0 1.1 1.2 1.3

!R5

!d(t#ent

Bactor

0.7 &0 &7 64 71 79 86 93?ot

of

?a*ital

10% 31 2& 21 17 1& 12 10

0.8 6& 7& 84 93 103 112 121 11% 30 24 20 16 13 11 9

0.9 81 93 104 116 127 139 1&0 12% 28 23 18 1& 12 10 8

1.0 97 111 12& 139 1&2 166 180 13% 27 22 17 14 11 9 7

1.1 113 129 146 162 178 194 210 14% 26 20 16 13 10 8 6

1.2 130 148 167 18& 204 222 241

1.3 146 167 188 209 229 2&0 271

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 64/73

?ot of 1 E of *ectr(# R. #n -?B Seniti>it" !nal"i

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 65/73

S(crier !d(t#ent Bactor ?a*ital In>et#ent Bactor

639.3 0.7 0.8 0.9 1.0 1.1 1.2 1.3 639.3 0.7 0.8 0.9 1.0 1.1 1.2 1.3

!R5

!d(t#ent

Bactor

0.7 197 22& 2&3 281 309 337 36&?ot

of

?a*ital

10% 1&0 122 99 82 68 &6 46

0.8 280 320 360 400 440 480 &20 11% 144 11& 93 7& 61 49 39

0.9 364 416 468 &20 &72 624 676 12% 137 108 86 68 &4 42 32

1.0 448 &11 &7& 639 703 767 831 13% 130 101 79 61 47 3& 2&

1.1 &31 607 683 7&9 83& 911 986 14% 123 94 72 && 40 28 18

1.2 61& 703 790 878 966 10&4 1142

1.3 698 798 898 998 1098 1197 1297

Real ,*tion Seniti>it" !nal"i

S(crier !d(t#ent Bactor ?a*ital In>et#ent Bactor

802 1 1 1 1 1 1 1 802 0.7 0.8 0.9 1.0 1.1 1.2 1.3

!R5

!d(t#ent

Bactor

0.7 286 327 368 409 4&0 491 &32?ot

of

?a*ital

10% 2030 19&7 1884 1812 1739 1668 1&97

0.8 37& 429 482 &36 &89 643 696 11% 183& 1761 1686 1612 1&39 1466 139&

0.9 467 &34 601 667 734 801 868 12% 1661 1&8& 1&09 1434 1360 1288 1217

1.0 &61 642 722 802 882 962 1042 13% 1&0& 1428 13&1 1276 1201 1129 10&9

1.1 6&7 7&0 844 938 1032 1126 1220 14% 1366 1287 1210 1134 1060 988 919

1.2 7&3 860 968 107& 1183 1290 1398

1.3 849 971 1092 1213 1334 14&6 1&77

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 66/73

?ot of 1 E of *ectr(# R. #n -?B Seniti>it" !nal"i

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 67/73

S(crier !d(t#ent Bactor ?a*ital In>et#ent Bactor

273.9 0.7 0.8 0.9 1.0 1.1 1.2 1.3 273.9 0.7 0.8 0.9 1.0 1.1 1.2 1.3

!R5

!d(t#ent

Bactor

0.7 7& 86 97 107 118 129 139?ot

of

?a*ital

10% 67 &3 43 3& 28 23 18

0.8 114 130 147 163 179 19& 212 11% 63 &0 40 32 2& 19 1&

0.9 1&3 17& 197 218 240 262 284 12% 60 47 36 28 21 16 11

1.0 192 219 247 274 301 329 3&6 13% &7 43 33 2& 18 12 8

1.1 231 264 297 329 362 39& 428 14% &3 40 29 21 1& 9 4

1.2 269 308 346 38& 423 462 &00

1.3 308 3&2 396 441 48& &29 &73

Real ,*tion Seniti>it" !nal"i

S(crier !d(t#ent Bactor ?a*ital In>et#ent Bactor

3&0 1 1 1 1 1 1 1 3&0 0.7 0.8 0.9 1.0 1.1 1.2 1.3

!R5

!d(t#ent

Bactor

0.7 120 138 1&& 172 189 206 224?ot

of

?a*ital

10% 80 6& &3 44 36 30 2&

0.8 160 183 206 229 2&2 274 297 11% 77 61 49 40 33 27 22

0.9 202 231 260 288 317 346 37& 12% 73 &8 46 37 29 24 19

1.0 24& 280 31& 3&0 38& 420 4&& 13% 69 &4 42 33 26 21 16

1.1 289 330 371 413 4&4 49& &36 14% 66 &1 39 30 24 18 14

1.2 333 381 428 476 &23 &71 619

1.3 378 432 486 &40 &94 648 702

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 68/73

?ot of 1 E of *ectr(# R. #n -?B Seniti>it" !nal"i

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 69/73

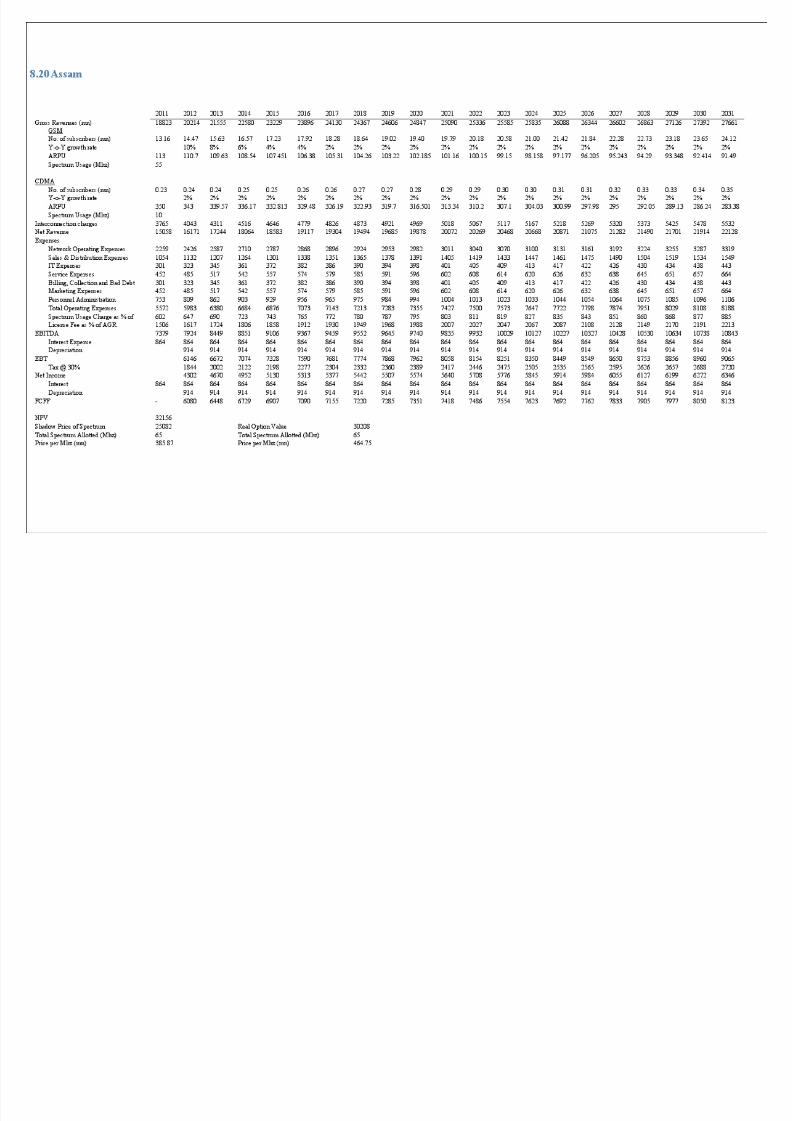

S(crier !d(t#ent Bactor ?a*ital In>et#ent Bactor

38&.9 0.7 0.8 0.9 1.0 1.1 1.2 1.3 38&.9 0.7 0.8 0.9 1.0 1.1 1.2 1.3

!R5

!d(t#ent

Bactor

0.7 1&3 174 196 218 240 262 283?ot

of

?a*ital

10% 81 67 &7 49 42 37 32

0.8 192 219 247 274 301 329 3&6 11% 79 6& && 47 40 34 30

0.9 231 264 297 330 363 396 429 12% 76 63 &3 4& 38 32 28

1.0 270 309 347 386 424 463 &02 13% 74 61 &1 42 36 30 26

1.1 309 3&3 398 442 486 &30 &74 14% 72 &9 48 40 34 28 23

1.2 348 398 448 498 &48 &97 647

1.3 388 443 498 &&4 609 664 720

Real ,*tion Seniti>it" !nal"i

S(crier !d(t#ent Bactor ?a*ital In>et#ent Bactor

46& 1 1 1 1 1 1 1 46& 0.7 0.8 0.9 1.0 1.1 1.2 1.3

!R5

!d(t#ent

Bactor

0.7 190 217 244 271 298 326 3&3?ot

of

?a*ital

10% 9& 80 68 &8 &1 44 39

0.8 23& 268 302 33& 369 403 436 11% 93 77 6& &6 48 42 37

0.9 280 320 360 400 440 480 &20 12% 91 7& 63 &4 46 40 34

1.0 32& 372 418 46& &11 &&8 604 13% 88 73 61 &1 44 37 32

1.1 371 424 477 &30 &83 63& 688 14% 86 71 &9 49 41 3& 30

1.2 416 476 &3& &94 6&4 713 773

1.3 461 &27 &93 6&9 72& 791 8&7

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 70/73

?ot of 1 E of *ectr(# R. #n -?B Seniti>it" !nal"i

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 71/73

S(crier !d(t#ent Bactor ?a*ital In>et#ent Bactor

24&.7 0.7 0.8 0.9 1.0 1.1 1.2 1.3 24&.7 0.7 0.8 0.9 1.0 1.1 1.2 1.3

!R5

!d(t#ent

Bactor

0.7 98 112 126 140 1&4 168 182?ot

of

?a*ital

10% &1 43 36 31 27 23 20

0.8 123 140 1&8 17& 193 210 228 11% &0 41 3& 30 26 22 19

0.9 147 168 189 210 231 2&2 274 12% 49 40 34 28 24 21 18

1.0 172 197 221 246 270 29& 319 13% 47 39 32 27 23 19 16

1.1 197 22& 2&3 281 309 337 36& 14% 46 38 31 26 22 18 1&

1.2 221 2&3 28& 316 348 379 411

1.3 246 281 316 3&2 387 422 4&7

Real ,*tion Seniti>it" !nal"i

S(crier !d(t#ent Bactor ?a*ital In>et#ent Bactor

296 1 1 1 1 1 1 1 296 0.7 0.8 0.9 1.0 1.1 1.2 1.3

!R5

!d(t#ent

Bactor

0.7 121 139 1&6 173 191 208 226?ot

of

?a*ital

10% 60 &1 43 37 32 28 2&

0.8 1&0 171 193 214 23& 2&7 278 11% &9 49 42 36 31 27 23

0.9 178 204 229 2&& 280 306 331 12% &8 48 40 34 29 2& 22

1.0 207 236 266 296 32& 3&& 384 13% &6 46 39 33 28 24 21

1.1 236 269 303 336 370 404 437 14% && 4& 37 31 27 23 19

1.2 264 302 340 377 41& 4&3 491

1.3 293 33& 376 418 460 &02 &44

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 72/73

?ot of 1 E of *ectr(# R. #n -?B Seniti>it" !nal"i

S i !d t t B t ? it l I t t B t

7/23/2019 MPRA Paper 40470

http://slidepdf.com/reader/full/mpra-paper-40470 73/73

S(crier !d(t#ent Bactor ?a*ital In>et#ent Bactor

290.2 0.7 0.8 0.9 1.0 1.1 1.2 1.3 290.2 0.7 0.8 0.9 1.0 1.1 1.2 1.3

!R5

!d(t#ent

Bactor

0.7 12& 143 161 179 197 21& 232?ot

of

?a*ital

10% &8 49 42 37 32 28 2&

0.8 1&1 173 194 216 237 2&9 281 11% &7 48 41 36 31 27 24

0.9 177 202 228 2&3 278 304 329 12% &6 47 40 3& 30 26 23

1.0 203 232 261 290 319 348 377 13% && 46 39 34 29 2& 22

1.1 229 262 29& 327 360 393 42& 14% &4 4& 38 33 28 24 21

1.2 2&& 292 328 364 401 437 474

1.3 281 321 361 402 442 482 &22

Real ,*tion Seniti>it" !nal"i

S(crier !d(t#ent Bactor ?a*ital In>et#ent Bactor

34& 1 1 1 1 1 1 1 34& 0.7 0.8 0.9 1.0 1.1 1.2 1.3

!R5

!d(t#ent

Bactor

0.7 1&1 172 194 21& 237 2&8 280?ot

of

?a*ital

10% 68 &7 49 43 38 34 30

0.8 181 207 233 2&8 284 310 336 11% 67 &6 48 42 37 33 29

0.9 211 241 271 301 332 362 392 12% 66 && 47 41 36 32 28

1.0 241 276 310 34& 379 413 448 13% 64 &4 46 40 3& 31 27

1.1 271 310 349 388 426 46& &04 14% 63 &3 4& 39 34 30 26

1.2 301 34& 388 431 474 &17 &60

1.3 332 379 426 474 &21 &69 616