Embed Size (px)

Citation preview

© 2017 STR, Inc. All Rights Reserved. Any reprint, use or republication of all or a part of this presentation without the prior written approval of STR, Inc. or STR Global, Ltd. trading as STR (collectively “STR”) is strictly prohibited. Any such reproduction shall specifically credit STR as the source. This presentation is based on data collected by STR. No strategic advice or marketing recommendation is intended or implied.

MPI Nashville ChapterMonthly Meeting – Embassy Suites Cool SpringsSeptember 20, 2017

Veronica Andrews

Director, Digital Data Solutions

@STR_Data

© 2017 STR. All Rights Reserved.

Agenda Industry Update

Pipeline

Nashville Market Performance

Segmentation Insights

Forecasts

Hotel F&B Performance

© 2017 STR. All Rights Reserved.

A few of notes

before we begin…

© 2017 STR. All Rights Reserved.

We are nowOne Brand

© 2017 STR. All Rights Reserved.

Notable Calendar Shifts Impacting Lodging Performance Data in 2017:

Easter From March to April (affects Q1/Q2)

Jewish Holidays From October to September (affects Q3/Q4)

Notable Market Level Events / Comps:

Super Bowl: From San Francisco To Houston

San Francisco: Super Bowl Shift and Moscone Center Renovation

Los Angeles: Porter Ranch Gas Leak

Washington, D.C.: Inauguration & Women’s March (January 2016)

Philadelphia: DNC (July 2016)

Cleveland: RNC (July 2016)

East Tennessee: Wild Fires (November 2016)

East Coast: Hurricane Matthew (October 2016)

Texas/Florida: Hurricanes Harvey and Irma (August/September 2017)

© 2017 STR. All Rights Reserved. U.S. Industry Performance

© 2017 STR. All Rights Reserved.

August 2017 YTD: Demand Growth Continues To Hold

% Change

Room Supply 1.8%

Room Demand 2.4%

Occupancy (*Record*) 67.1% 0.5%

A.D.R. $127 2.1%

RevPAR $85 2.7%

Room Revenue 4.5%

Total US Results - August 2017 YTD

© 2017 STR. All Rights Reserved.

August YTD 2017: New Supply Hits NYC, Miami.

Market OCC %ADR % Change Influenced By

Washington, DC-MD-VA 74.0 5.5 Inauguration / Women’s March

Nashville, TN 74.8 5.3 Bachelorette Parties

Seattle, WA 79.4 4.7

Phoenix, AZ 69.1 4.4

Detroit, MI 67.5 4.3

Houston, TX 62.1 -0.9

New Supply

(Watch for future Harvey Impact)

New York, NY 85.3 -1.8 New Supply

San Francisco/San Mateo, CA 84.1 -2.0

Superbowl L 2016 / Moscone Center

Closed April - August

Philadelphia, PA-NJ 68.8 -3.5 DNC 2016

Miami/Hialeah, FL 78.7 -3.7 New Supply*August 2017 YTD ADR % Change in Top 25: 5 Best / 5 Worst Performing ADR Growth Markets

© 2017 STR. All Rights Reserved.

August 2017 12MMA: Steady RevPAR Growth

Total US Results - August 2017 12MMA

% Change

Room Supply 1.8%

Room Demand 2.4%

Occupancy (*Record*) 65.7% 0.6%

A.D.R. $126 2.4%

RevPAR $83 3.0%

Room Revenue 4.8%

Rooms Revenue($)

Rooms Available(supply)

($)

RevPAR

What Defines Success?

© 2017 STR. All Rights Reserved.

US Industry RevPAR Growth: Erratic Monthly Numbers,But Overall Current Trend Is Steady

-4

0

4

8

12

16

20

2015 2016 2017

Monthly 12MMA

*Total U.S. - RevPAR % Change by month and 12MMA, 1/2015 – 8/2017

© 2017 STR. All Rights Reserved.

Nashville, TN Market RevPAR Growth: Erratic Monthly Numbers; Overall Downward Trend…

-4

0

4

8

12

16

20

2015 2016 2017

Monthly 12MMA

*Nashville, TN Market - RevPAR % Change by month and 12MMA, 1/2015 – 8/2017

© 2017 STR. All Rights Reserved.

Demand Growth Stronger Than Expected.

-0.8

-4.7

-7.1

7.7

-8

-4

0

4

8

1990 2000 2010

Supply % Change

Demand % Change

Total U.S., Supply & Demand % Change, 12 MMA 1/1990 – 8/2017

© 2017 STR. All Rights Reserved.

Nashville, TN Supply Growth Begins to Outpace Demand Growth.

3.5

-3.7

-8.8

4.8

2.4

-10

-5

0

5

10

15

1990 1995 2000 2005 2010 2015

Supply % Change

Demand % Change

Nashville, TN Market Supply & Demand % Change, 12 MMA 1/2002 – 8/2017

© 2017 STR. All Rights Reserved.

Pipeline

© 2017 STR. All Rights Reserved.

US Pipeline: I/C Growth Still Strong(But Growth Rates Used to be 30%+)

Phase 2017 2016 % Change

In Construction 192 170 13%

Final Planning 220 198 11%

Planning 178 174 2%

Under Contract 590 542 9%

*Total US Pipeline, by Phase, ‘000s Rooms, August 2017 and 2016

13%

© 2017 STR. All Rights Reserved. *Total US Pipeline; Rooms In Construction, in ‘000s; 1/2006 – 7/2017

0

50

100

150

200

250

2006 2008 2010 2012 2014 2016

Low: May ‘1150K

August‘17192K

High:Dec ‘07

211K

19K

I/C Pipeline Is Growing But Still Below Prior PeakTh

ou

san

ds

© 2017 STR. All Rights Reserved.

Limited Service Construction Is The Name Of The Game

8.9

26.4

61.3 63.0

9.92.5

20.2

Luxury Upper Upscale Upscale Upper Midscale Midscale Economy Unaffiliated

*US Pipeline, Rooms In Construction , ‘000s Rooms, by Scale, August 2017

65%

© 2017 STR. All Rights Reserved.

Pipeline: Top 26 Markets Have 48% Of All Rooms I/C

92.399.8

83.3

136.6

76.3

101.7

Top 26 Markets Rest of US

In Construction Final Planning Planning

*US Pipeline, Rooms (‘000s), Top 26 Markets vs. All Other Markets, August 2017

BNA Mkt:5.4 6.2 3.4

© 2017 STR. All Rights Reserved.

Projects in the Nashville, TN Pipeline Opening 2017/2018Under Construction (5,389 rooms)• The Unbound Collection Holston House

• The Bobby Hotel

• JW Marriott Nashville

• Dream Nashville

• Hilton Nashville Green Hills

• Hilton Franklin Cool Springs

• Noelle Nashville

• AC Hotels by Marriott Nashville Downtown

• Cambria Hotel & Suites Nashville

• Residence Inn Nashville @ Opryland

• Residence Inn Nashville Downtown

• Residence Inn Nashville Green Hills

• Springhill Suites Nashville Downtown

• Springhill Suites Mount Juliet

• Staybridge Suites Mount Juliet

• Fairfield Inn & Suites Lebanon

• Hampton Inn & Suites Franklin

• Hampton Inn & Suites Nashville Goodlettsville

• Hampton Inn Suites Nashville Downtown

• Holiday Inn & Suites Nashville Downtown

• Holiday Inn Express & Suites Springfield

• Holiday Inn Express Goodlettsville

• Home2 Suites Mount Juliet

• Home2 Suites Murfreesboro

• Home2 Suites Nashville Bellevue

• Home2 Suites Smyrna

• Moxy Nashville Downtown

• My Place Hotel Lebanon

• Towneplace Suites Goodlettsville

• Candlewood Suites Goodlettsville

• Tru By Hilton Murfreesboro

• Tru By Hilton Smyrna Nashville

• Woodspring Suites Nashville North*Nashville, TN Market Pipeline, Rooms (‘000s), due to open 2017/2018 - August 2017

© 2017 STR. All Rights Reserved.

Nashville, TN Market Performance

© 2017 STR. All Rights Reserved.

© 2017 STR. All Rights Reserved.

Nashville, TNMarket

Market Share of Supply

Hotels 345

Rooms 40,557

STR Sample 89%

Key Statistics

%ch

OCC 73.8% -1.0%

ADR $139.28 5.3%

RevPAR $102.84 4.3%

Rm Rev $1.499B 7.9%

Supply 14.6M 3.5%

Demand 10.8M 2.4% Nashville, TN Market Performance – August 2017 12MMA

© 2017 STR. All Rights Reserved.

CBDAirport

I-24 Murfreesboro

I-65 N

Brentwood/Franklin

Other Areas

Occupancy

73.8%

-1.0%81% - 0.6%

72% - 2.0%

74.6% - 1.5% 71.4% - 1.1%

67.9% + 2.4%

68.8% - 3.1%

Nashville, TN Submarket Occupancy Performance – August 2017 12MMA

© 2017 STR. All Rights Reserved.

CBDAirport

I-24 Murfreesboro

I-65 N

Brentwood/Franklin

Other Areas

ADR

$139.28

+5.3%$215 + 5.3%

$135 + 3.6%

$122 + 1.3% $85 + 2.8%

$89 + 10.5%

$82 + 7.2%

Nashville, TN Submarket Average Daily Rate Performance – August 2017 12MMA

© 2017 STR. All Rights Reserved.

CBDAirport

I-24 Murfreesboro

I-65 N

Brentwood/Franklin

Other Areas

RevPAR

$102.84

+4.3%$175 + 4.6%

$98 + 1.5%

$91 - 0.2% $60 + 1.7%

$60 + 13.1%

$56 + 4.0%

Nashville, TN Submarket RevPAR Performance – August 2017 12MMA

© 2017 STR. All Rights Reserved.

Airport

Brentwood/Franklin

Central Business District

I-24 Murfreesboro

I-65 North

Other Areas

Nashville, TN Market

Recap: Nashville, TN Market Performance by Submarket

-2.0% 3.6% 1.5%

-1.5% 1.3% -0.2%

-0.6% 5.3% 4.6%

-1.1% 2.8% 1.7%

2.4% 10.5% 13.1%

-3.1% 7.2% 4.0%

-1.0% 5.3% 4.3%

Occupancy ADR RevPAR

Nashville, TN Market and Submarkets – Occupancy, ADR & RevPAR - August 2017 12MMA % Change

© 2017 STR. All Rights Reserved.

Day Of Week Patterns

© 2017 STR. All Rights Reserved.

Nashville, TN Market – 3 Year Occupancy by Day of Week12MMA

56.8

70.0

77.277.2

74.7

79.9

81.0

73.8

0.0

25.0

50.0

75.0

100.0

Sun Mon Tue Wed Thu Fri Sat

Total 3 Yr Sep 14 - Aug 15 Sep 15 - Aug 16 Sep 16 - Aug 17

© 2017 STR. All Rights Reserved.

$121

$127

$132 $133 $131

$137

$139

$132

$128

$134

$139 $139 $137

$145

$148

$139

$110.00

$130.00

$150.00

Sun Mon Tue Wed Thu Fri Sat Total Year

Total 3 Yr Sep 14 - Aug 15 Sep 15 - Aug 16 Sep 16 - Aug 17

Nashville, TN – 3 Year ADR by Day of Week12MMA

© 2017 STR. All Rights Reserved.

$69

$89

$102 $102

$98

$109

$113

$97

+$5

+$5

+$6 +$6

+$5

+$5

+$7

+$5

$60.00

$80.00

$100.00

$120.00

Sun Mon Tue Wed Thu Fri Sat Total YearTotal 3 Yr Sep 14 - Aug 15 Sep 15 - Aug 16 Sep 16 - Aug 17

Nashville, TN Market – 3 Year RevPAR by Day of Week12MMA

+$ *RevPAR premium compared to 3 year average

© 2017 STR. All Rights Reserved.

Group Trends

© 2017 STR. All Rights Reserved.

63.9%

32.2%

20%

30%

40%

50%

60%

70%

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

Transient Mix Group Mix

US Industry Group and Transient Mix12MMA Luxury and Upper-Upscale Classes

Total US Group and Transient Mix, Occupied Rooms12MMA, January 2005 – August 2017, *Luxury & Upper Upscale Classes Only

© 2017 STR. All Rights Reserved.

48.0%

49.5%

20%

30%

40%

50%

60%

70%

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

Transient Mix Group Mix

Nashville, TN Market Group and Transient Mix 12MMA Luxury and Upper-Upscale Classes

Nashville, TN Market Group and Transient Mix, Occupied Rooms12MMA, January 2005 – August 2017, *Luxury & Upper Upscale Classes Only

© 2017 STR. All Rights Reserved.

$219

$194

$125

$150

$175

$200

$225

$250

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

Transient ADR Group ADR

US Industry Group and Transient ADRs12MMA Luxury and Upper-Upscale Classes

Total US Group and Transient ADRs12MMA, January 2005 – July 2017, *Luxury & Upper Upscale Classes Only

7.8%

11.4%

© 2017 STR. All Rights Reserved.

$218

$190

$100

$125

$150

$175

$200

$225

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

Transient ADR Group ADR

Nashville, TN Market Group and Transient ADRs12MMA Luxury and Upper-Upscale Classes

Nashville, TN Market Group and Transient ADRs12MMA, January 2005 – August 2017, *Luxury & Upper Upscale Classes Only

1.3%

14.3%

© 2017 STR. All Rights Reserved.

What markets do you consider “hot” destinations?

© 2017 STR. All Rights Reserved.

Convention Center Submarkets2016 Group Demand Variance vs. Prior Peak

Was

hin

gto

n D

C

Las

Ve

gas

Ne

w Y

ork

San

Fra

nci

sco

Bo

sto

n

Ch

icag

o

San

An

ton

io

Mia

mi B

eac

h

Ph

ilad

elp

hia

Tam

pa

Seat

tle

Ch

arlo

tte

St. L

ou

is

Salt

Lak

e C

ity

An

ahe

im

Ro

sem

on

t

Ho

ust

on

San

Jo

se

Lou

isvi

lle

Atl

anta

Fort

Lau

de

rdal

e

Min

ne

apo

lis

Cle

vela

nd

Pit

tsb

urg

h

Po

rtla

nd

Bal

tim

ore

Dal

las

Ph

oe

nix

De

nve

r

Los

An

gele

s

Ne

w O

rle

ans

San

Die

go

Nas

hvi

lle

Ind

ian

apo

lis

Au

stin

Orl

and

o

-500

-400

-300

-200

-100

0

100

200

300

400

500

Gro

up

Ro

om

Nig

hts

(0

00

s)

New Convention Center Hotel

Developing Convention Center HotelProposed Convention Center Hotel

Net Loss of 300,000 Group Room Nights

© 2017 STR. All Rights Reserved.

Top 5 Projects In Construction By Meeting Space

Project Name MarketProjected

Opening DateRoom Count

Total SqFtMeeting Space

Gaylord Rockies Hotel & Conference Center Denver 12/12/2018 1500 400,000

Fairmont Austin Austin 09/30/2017 1048 107,000

Hyatt Regency Seattle Seattle 06/30/2018 1260 100,000

Omni Louisville Louisville 03/31/2018 600 70,000

JW Marriott Nashville Nashville 07/01/2018 533 60,000

1

2

3

45

© 2017 STR. All Rights Reserved.

2017 / 2018 Forecasts

© 2017 STR. All Rights Reserved.

Total United States Key Performance Indicator Outlook(% Change vs. Prior Year) 2017F – 2018F

Outlook

2017Forecast

2018Forecast

Supply 2.0% 2.1%

Demand 2.0% 1.9%

Occupancy 0.0% -0.2%

ADR 2.3% 2.5%

RevPAR 2.3% 2.3%

© 2017 STR. All Rights Reserved.

Total United StatesChain Scale Key Performance Indicator Outlook 2017F by Chain Scale

2017 Year End Outlook

Chain ScaleOccupancy

(% chg)ADR

(% chg)RevPAR(% chg)

Luxury -0.2% 2.3% 2.1%

Upper Upscale -0.2% 2.0% 1.8%

Upscale -0.9% 1.8% 1.0%

Upper Midscale -0.4% 1.7% 1.3%

Midscale 0.1% 2.1% 2.2%

Economy 0.2% 2.2% 2.5%

Independent 0.4% 2.8% 3.3%

Total United States 0.0% 2.3% 2.3%

© 2017 STR. All Rights Reserved.

Total United StatesChain Scale Key Performance Indicator Outlook 2018F by Chain Scale

2018 Year End Outlook

Chain ScaleOccupancy

(% chg)ADR

(% chg)RevPAR(% chg)

Luxury -0.1% 2.6% 2.5%

Upper Upscale -0.2% 2.4% 2.2%

Upscale -0.8% 2.0% 1.2%

Upper Midscale -0.6% 2.0% 1.4%

Midscale -0.3% 2.1% 1.8%

Economy -0.2% 2.1% 1.9%

Independent 0.0% 2.7% 2.6%

Total United States -0.2% 2.5% 2.3%

© 2017 STR. All Rights Reserved.

2017 Year End RevPAR ForecastTop North American Markets, August 2017 Forecast (Markets sorted alphabetically)

-5% to 0% 0% to 5% 5% to 10% Houston, TX Anaheim-Santa Ana, CA Montreal, QC

Miami-Hialeah, FL Atlanta, GA Norfolk-Virginia Beach, VAMinneapolis-St. Paul, MN-WI Boston, MA Seattle, WA

New Orleans, LA Chicago, IL Toronto, ON

San Francisco-San Mateo, CA Dallas, TX Vancouver, BC

Denver, CO Washington, DC-MD-VADetroit, MI

Los Angeles-Long Beach, CA

Nashville, TN

New York, NY

Oahu Island, HI

Orlando, FL

Philadelphia, PA-NJ

Phoenix, AZ

San Diego, CA

St. Louis, MO-IL

Tampa-St. Petersburg, FL

Note: RevPAR Forecast numbers are based on local currency

© 2017 STR. All Rights Reserved. Note: RevPAR Forecast numbers are based on local currency; markets sorted alphabetically

2018 Year End RevPAR ForecastTop North American Markets, August 2017 Forecast

© 2017 STR. All Rights Reserved.

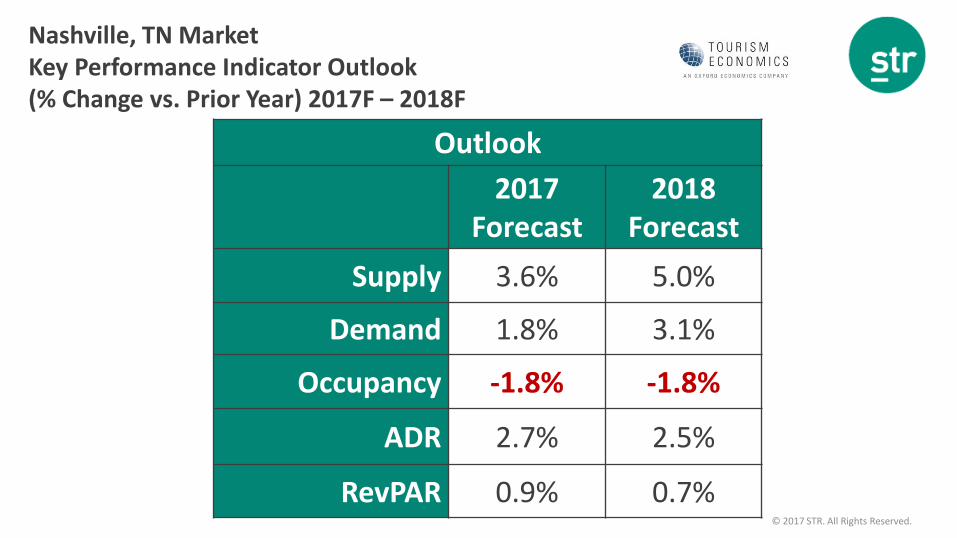

Nashville, TN MarketKey Performance Indicator Outlook(% Change vs. Prior Year) 2017F – 2018F

Outlook

2017Forecast

2018Forecast

Supply 3.6% 5.0%

Demand 1.8% 3.1%

Occupancy -1.8% -1.8%

ADR 2.7% 2.5%

RevPAR 0.9% 0.7%

© 2017 STR. All Rights Reserved.

Food for Thought…

© 2017 STR. All Rights Reserved.

Total U.S. F&B Performance

+2.0%+1.4%

-3.6%

+1.4% +1.5%

Catering & Banquets

RevPAS

F&B Venues Rev/Avail

Seat

In-Room Dining Rev/Occ Room

Total F&B

RevPOR

Total F&B

Revenue

Total U.S. F&B Performance – June 2017 12MMA

© 2017 STR. All Rights Reserved.

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

2015 2016 2017

Hu

nd

red

s

Total F&B RevPOR C&B RevPAS

C&B RevPAS Outpaces Total F&B RevPOR Growth

U.S. Properties – 12MMA Percent Change, January 2015 – June 2017 Catering & Banquets Revenue Per Available SqFt %ch, F&B Revenue Per Occupied Room %ch*Participating and Eligible Luxury & Upper Upscale Classes Only

© 2017 STR. All Rights Reserved.

C&B RevPAS by Class

Food Beverage Other

Luxury $0.67 +1.0% $0.12 +1.2% $0.39 +0.4%

Upper Upscale $0.40 +3.3% $0.05 +3.5% $0.23 +1.1%

Upscale $0.15 -0.7% $0.02 -4.6% $0.09 +1.3%

Total $0.44 +2.5% $0.07 +2.5% $0.25 +0.9%

Catering & Banquets RevPAS by Class with Percent ChangeJune 2017 12MMA

© 2017 STR. All Rights Reserved.

C&B Revenue per Group Roomnight

$35

$4

$22

Upscale

$158

$29

$91

Luxury

Food Beverage Other

$96

$12

$54

Upper Upscale

Catering & Banquets Revenue Contribution per Group Roomnight, by ClassJune 2017 12MMA

$163

$279

$61

© 2017 STR. All Rights Reserved.

Questions?

© 2017 STR, Inc. All Rights Reserved. Any reprint, use or republication of all or a part of this presentation without the prior written approval of STR, Inc. or STR Global, Ltd. trading as STR (collectively “STR”) is strictly prohibited. Any such reproduction shall specifically credit STR as the source. This presentation is based on data collected by STR. No strategic advice or marketing recommendation is intended or implied.

Thank You

Veronica Andrews

Director, Digital Data Solutions

@STR_Data