Embed Size (px)

Citation preview

Moving Forward: The Future of Insurance Industry

Investments

Accounting Firm Perspective

Presented by:

William J. Scannell, CPA

Johnson, Lauder & Savidge, LLP

NYIA Educational Seminar, February 12, 2009

Presentation Outline

• Accounting Issues

• Tax Issues

• Regulatory Changes

• Strategies

• Questions & Answers

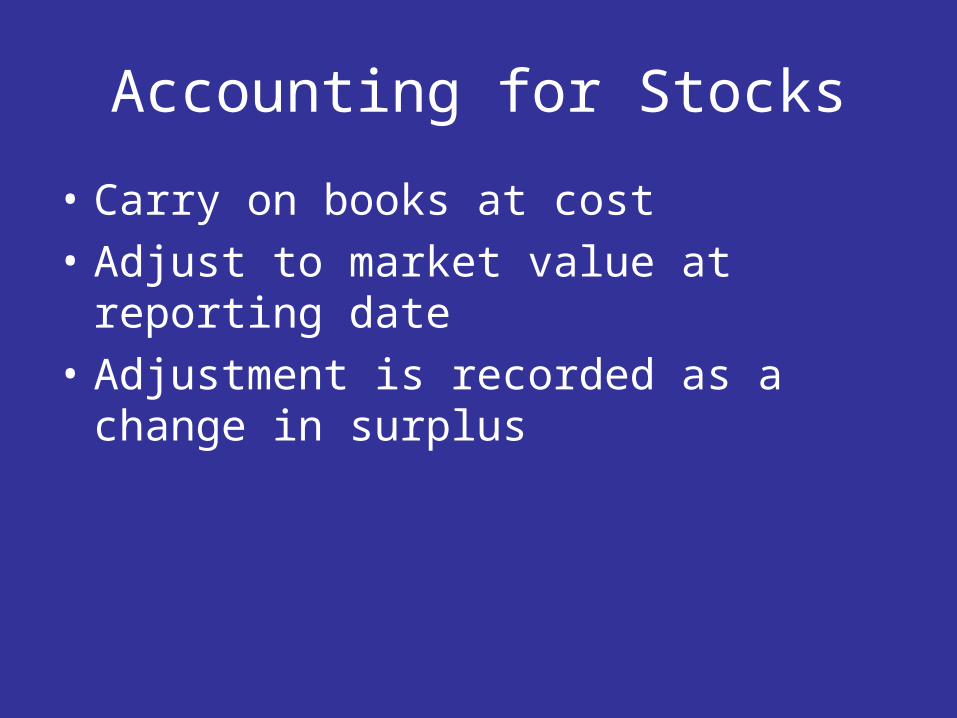

Accounting for Stocks

• Carry on books at cost

• Adjust to market value at reporting date

• Adjustment is recorded as a change in surplus

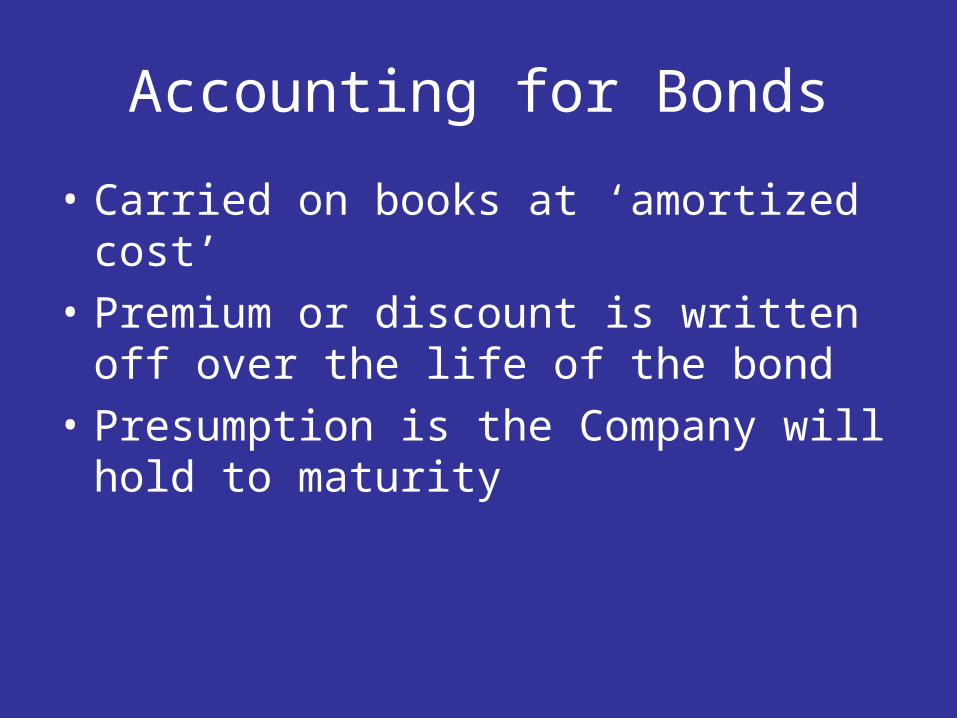

Accounting for Bonds

• Carried on books at ‘amortized cost’

• Premium or discount is written off over the life of the bond

• Presumption is the Company will hold to maturity

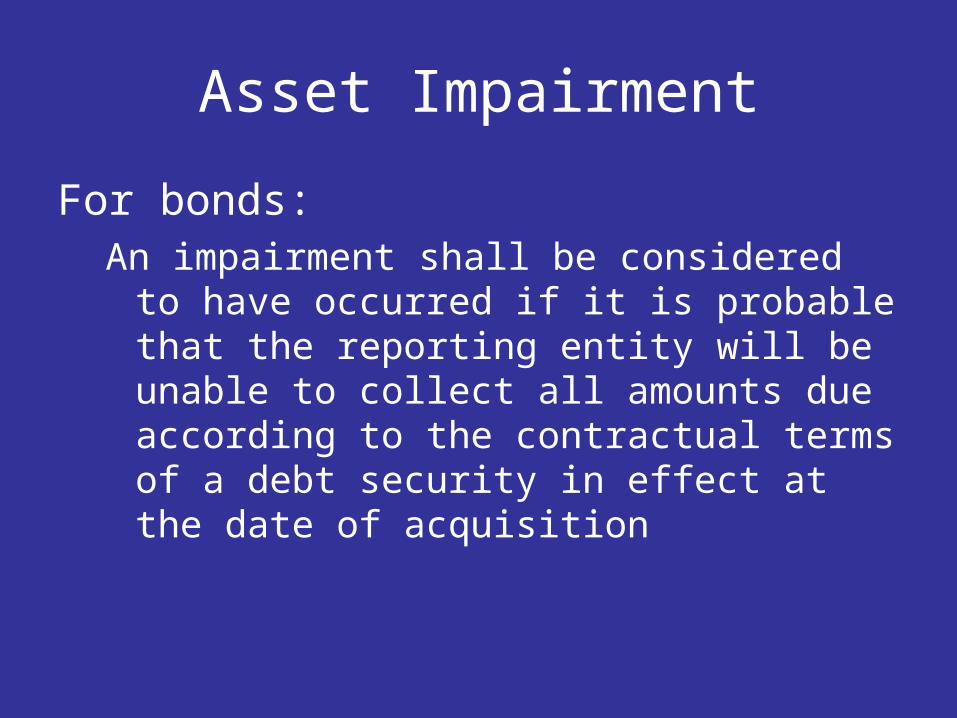

Asset Impairment

For bonds:An impairment shall be considered to have occurred

if it is probable that the reporting entity will be unable to collect all amounts due according to the contractual terms of a debt security in effect at the date of acquisition

Asset Impairment

For stocks:A decline in the fair value of a stock that is

determined to be ‘other than temporary’.

Impairment Determination

• Performed at the individual security level

• Indicating factors:– Length of time to which fair value has been less

than cost– Financial condition and short-term prospects of the

issuer– Intent and ability to retain investment for sufficient

time to allow for recovery in value

Asset Impairment measurement

Rules of Thumb developed to assist in evaluation of impairment:

1. 20% below water

2. 6 months below cost

Identifying impairment is only the beginning of the analysis

Accounting for Impairment

• Write down cost to impaired value

• Loss become ‘recognized’ – reduces net income

• For stocks, moves surplus adjustment ‘above the line’ but no impact on surplus

• bonds, results in immediate reduction in surplus

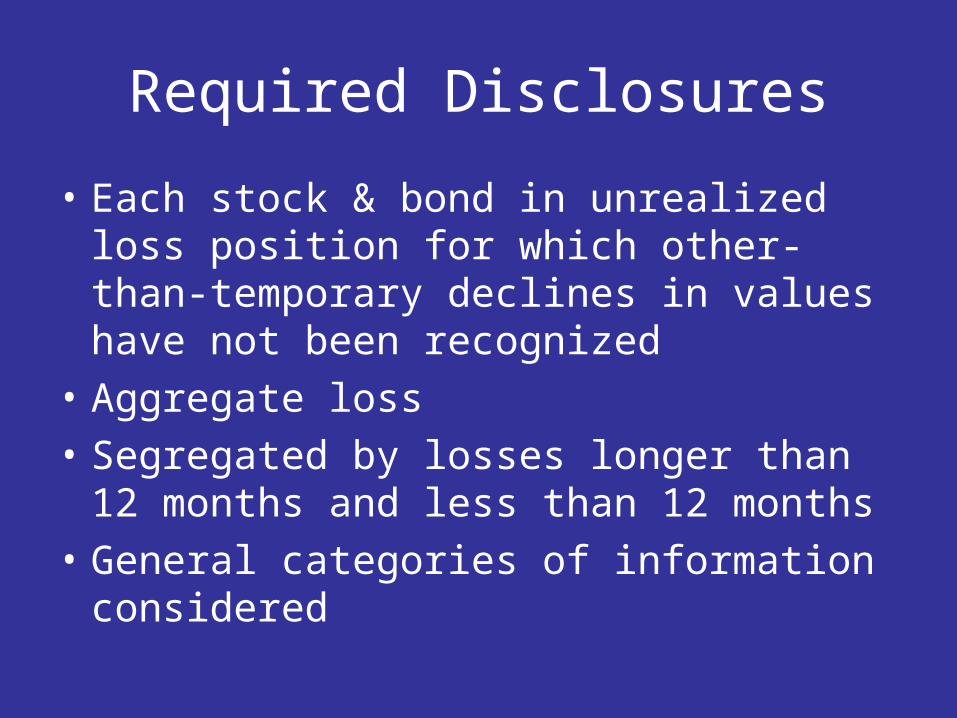

Required Disclosures

• Each stock & bond in unrealized loss position for which other-than-temporary declines in values have not been recognized

• Aggregate loss

• Segregated by losses longer than 12 months and less than 12 months

• General categories of information considered

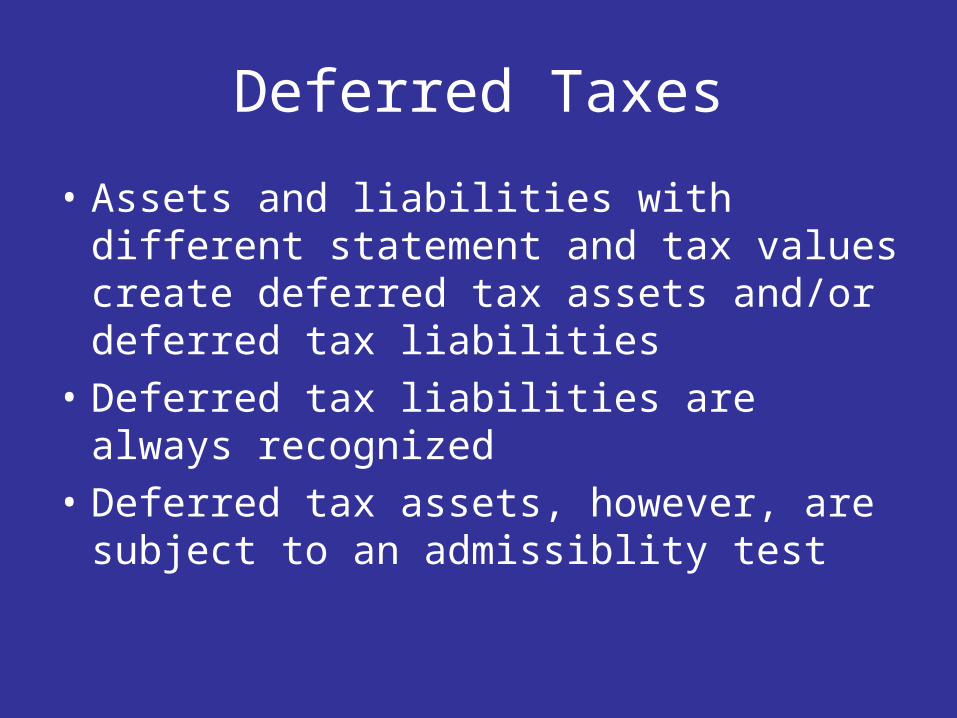

Deferred Taxes

• Assets and liabilities with different statement and tax values create deferred tax assets and/or deferred tax liabilities

• Deferred tax liabilities are always recognized

• Deferred tax assets, however, are subject to an admissiblity test

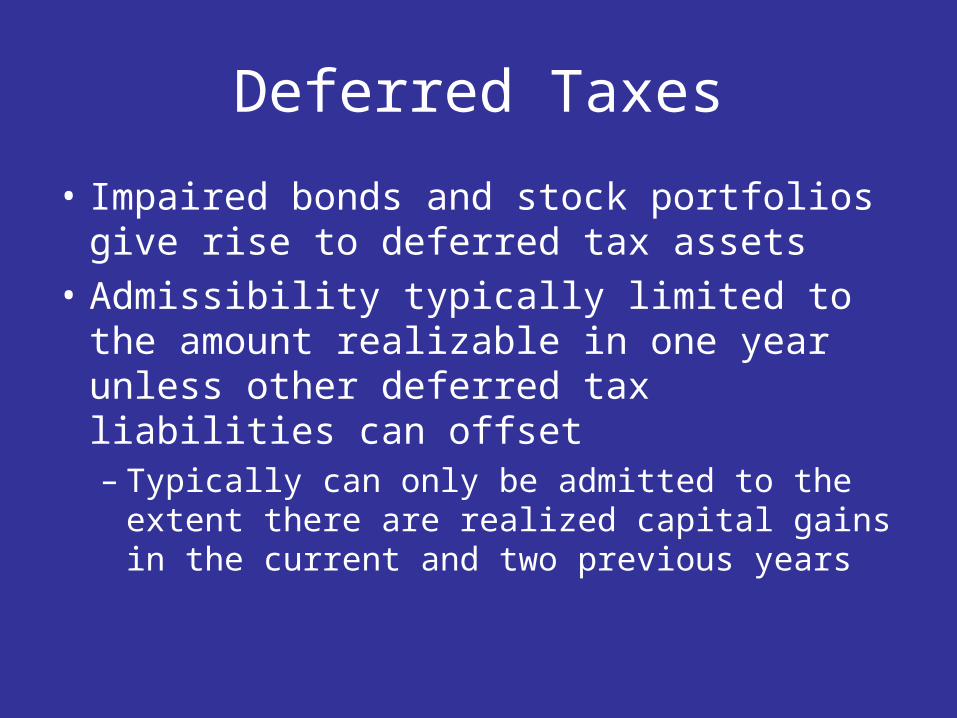

Deferred Taxes

• Impaired bonds and stock portfolios give rise to deferred tax assets

• Admissibility typically limited to the amount realizable in one year unless other deferred tax liabilities can offset– Typically can only be admitted to the extent there

are realized capital gains in the current and two previous years

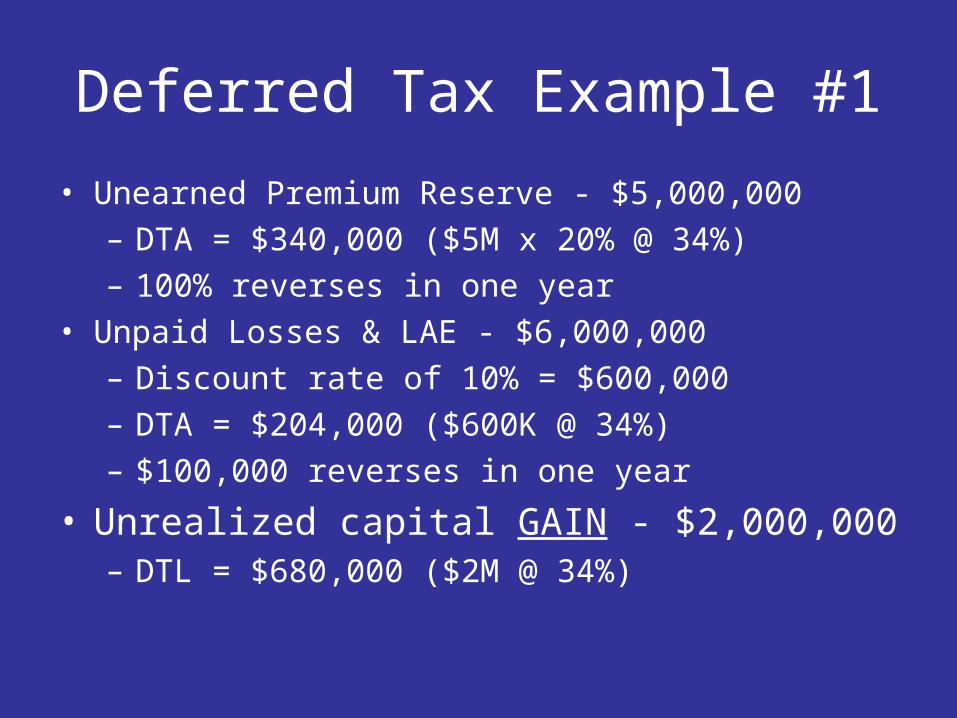

Deferred Tax Example #1

• Unearned Premium Reserve - $5,000,000

– DTA = $340,000 ($5M x 20% @ 34%)

– 100% reverses in one year

• Unpaid Losses & LAE - $6,000,000

– Discount rate of 10% = $600,000

– DTA = $204,000 ($600K @ 34%)

– $100,000 reverses in one year

• Unrealized capital GAIN - $2,000,000– DTL = $680,000 ($2M @ 34%)

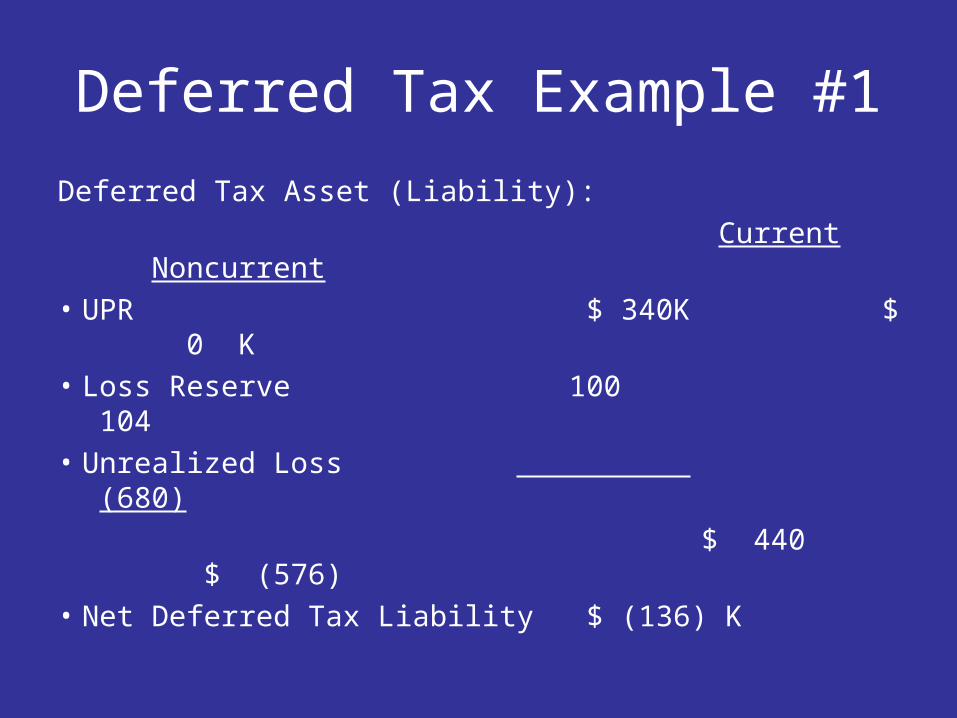

Deferred Tax Example #1

Deferred Tax Asset (Liability):

Current Noncurrent

• UPR $ 340K $ 0 K

• Loss Reserve 100 104

• Unrealized Loss (680)

$ 440 $ (576)

• Net Deferred Tax Liability $ (136) K

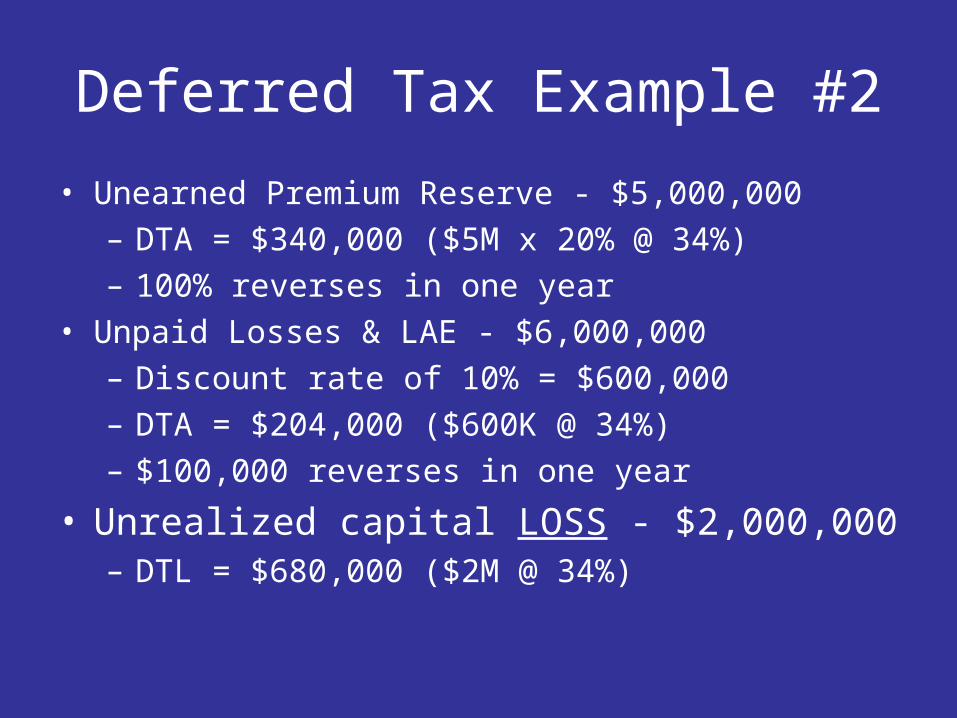

Deferred Tax Example #2

• Unearned Premium Reserve - $5,000,000

– DTA = $340,000 ($5M x 20% @ 34%)

– 100% reverses in one year

• Unpaid Losses & LAE - $6,000,000

– Discount rate of 10% = $600,000

– DTA = $204,000 ($600K @ 34%)

– $100,000 reverses in one year

• Unrealized capital LOSS - $2,000,000– DTL = $680,000 ($2M @ 34%)

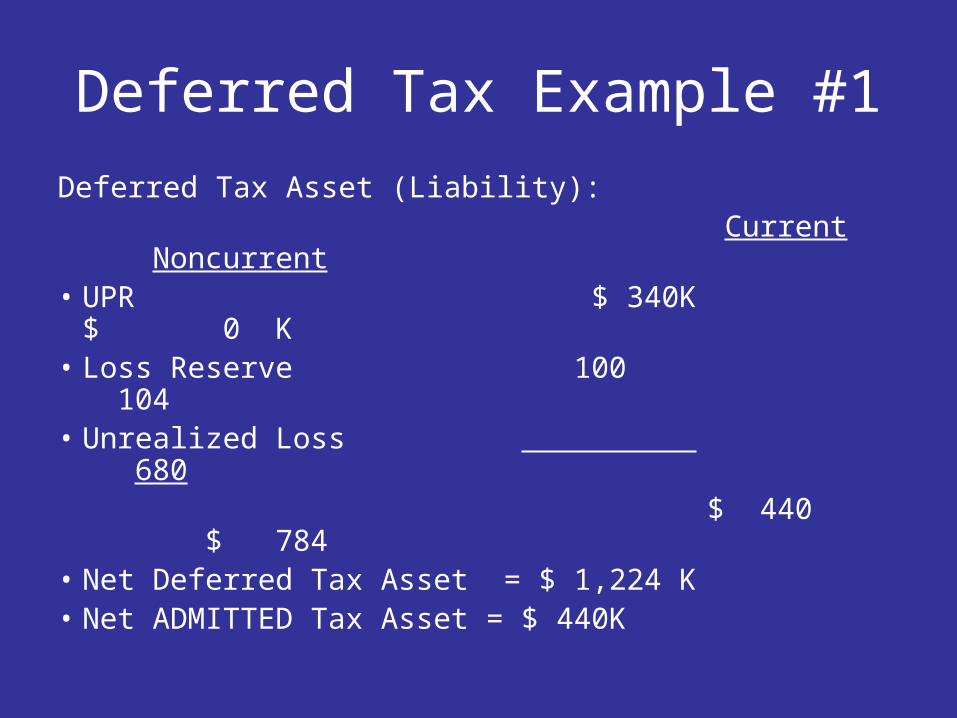

Deferred Tax Example #1

Deferred Tax Asset (Liability): Current Noncurrent• UPR $ 340K $ 0 K• Loss Reserve 100 104• Unrealized Loss 680 $ 440 $ 784 • Net Deferred Tax Asset = $ 1,224 K• Net ADMITTED Tax Asset = $ 440K

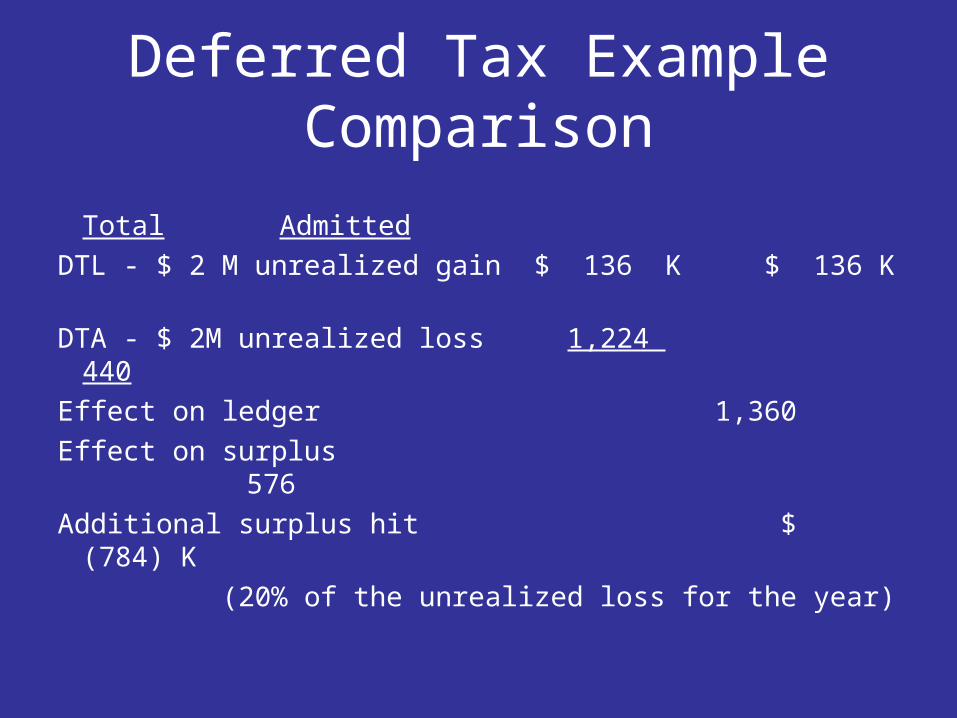

Deferred Tax Example Comparison

Total Admitted

DTL - $ 2 M unrealized gain $ 136 K $ 136 K

DTA - $ 2M unrealized loss 1,224 440

Effect on ledger 1,360

Effect on surplus 576

Additional surplus hit $ (784) K

(20% of the unrealized loss for the year)

Tax Implications

• No deduction for unrealized losses

• Realized capital losses can only offset realized capital gains

• Remaining loss can be carried back 3 years, then carried forward 5 years – then is lost

Regulatory Changes for 2008

• NAIC pending changes relaxing admissibility of deferred tax assets

• NYSID stress testing

• Disclosure of sub-prime mortgage disclosure – Regardless of materiality

Strategies

• Review portfolio for impaired assets– Develop a watch list– Involve investment & business advisors– Document procedure and conclusions

• Analyze deferred assets

• Consider sale of below market assets to recoup capital gain tax paid in 2006, 2007 and 2008– Consider non-tax factors as well before selling

Questions

?

For further information contact:

William J. Scannell, CPA

Managing Partner

Johnson, Lauder & Savidge, LLP

(607) 723-8216