Embed Size (px)

Citation preview

Motor Vehicle Demand in the United StatesPresentation to the GM Board of Directors

Weyman and Morris Consulting

Agenda

US Motor Vehicle Demand and GM position – Abdulmohsen Alkhulayfi

SWOT and Research Methodology – Brett Weyman

Prediction Model Development – Abhinav Veeraraghavan

Total Vehicle Demand Forecast – Abhinav Veeraraghavan

Implications and Recommendations to the Board – Lorenzo Ruiz Pricing

Production

Inventory

Technology – Ta’Chelle Morris

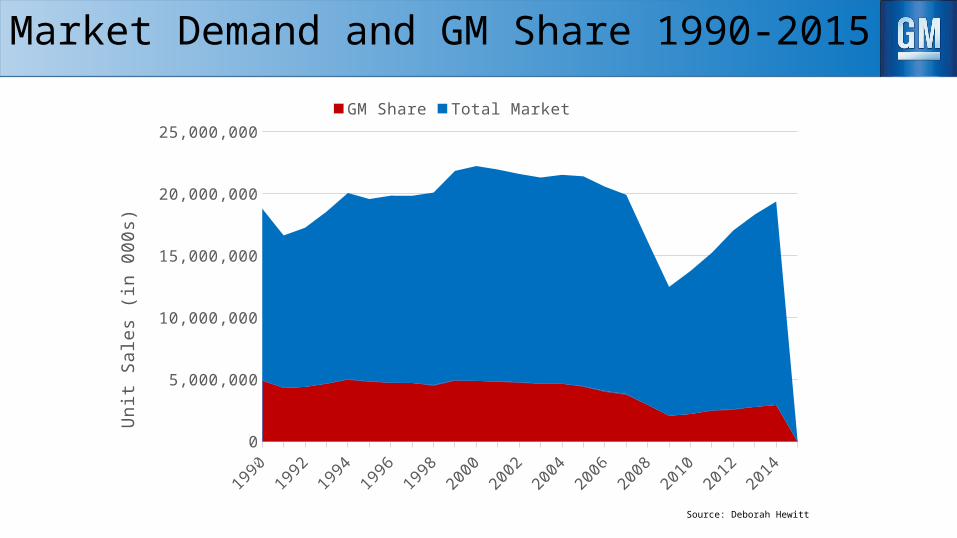

Market Demand and GM Share 1990-2015

19901992

19941996

19982000

20022004

20062008

20102012

20140

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

GM Share Total MarketU

nit S

ales

(in

000s

)

Source: Deborah Hewitt

35.6% 17.9%

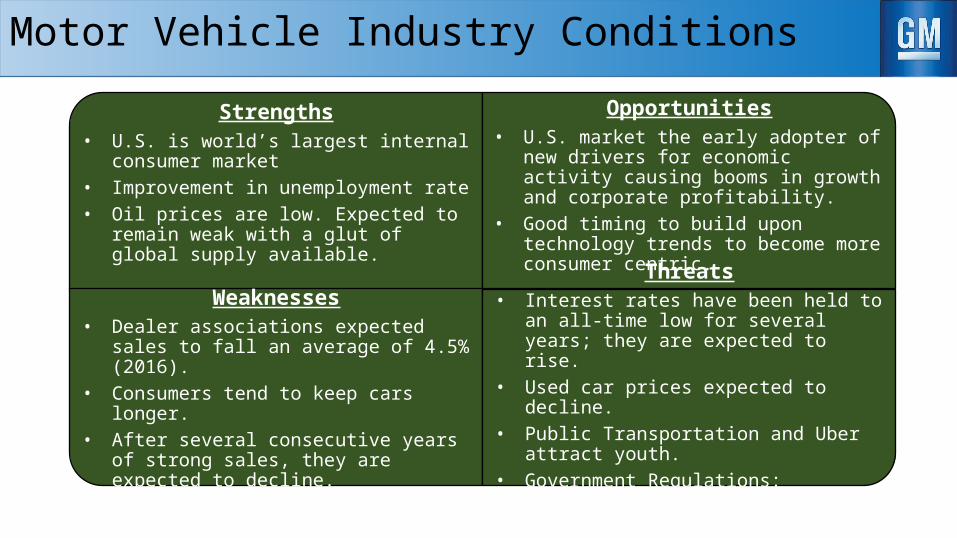

Motor Vehicle Industry Conditions

Strengths• U.S. is world’s largest internal consumer market• Improvement in unemployment rate• Oil prices are low. Expected to remain weak

with a glut of global supply available.

Opportunities• U.S. market the early adopter of new drivers for

economic activity causing booms in growth and corporate profitability.

• Good timing to build upon technology trends to become more consumer centric.

Weaknesses• Dealer associations expected sales to fall an

average of 4.5% (2016).• Consumers tend to keep cars longer.• After several consecutive years of strong sales,

they are expected to decline.

Threats• Interest rates have been held to an all-time low

for several years; they are expected to rise. • Used car prices expected to decline.• Public Transportation and Uber attract youth.• Government Regulations: Efficiency / Safety.

Research Methodology Our Approach to the Problem

Design Thinking Primary Research

Secondary Research

INCOME

JOB FUELPRICECOSTS

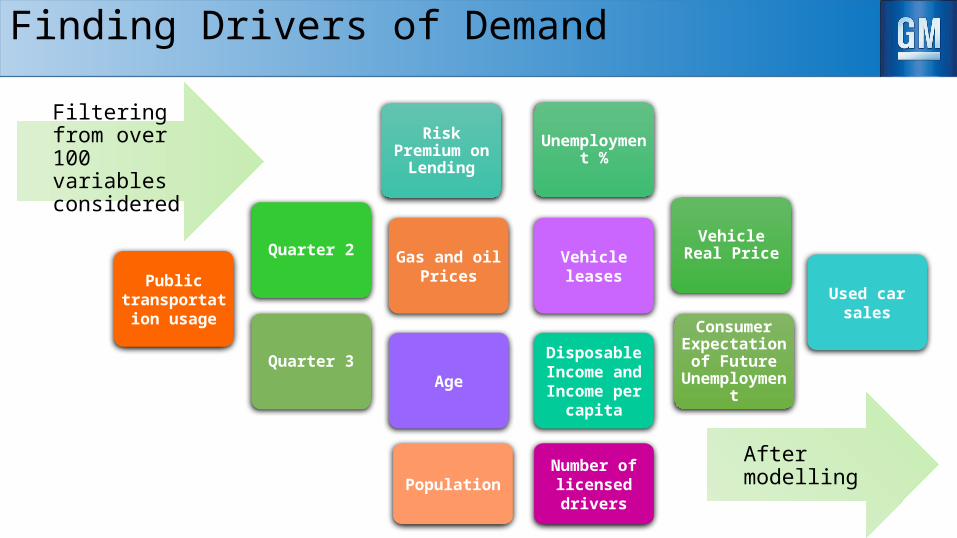

Finding Drivers of Demand

Quarter 3

Quarter 2

Risk Premium on Lending

Unemployment %

Vehicle Real Price

Consumer Expectation of

Future Unemployment

Gas and oil Prices Vehicle leases

Age

Disposable Income and Income per

capita

Number of licensed driversPopulation

Public transportation

usageUsed car sales

Filtering from over 100 variables considered

After modelling

Vehicle Demand

Quarter 2

Quarter 3

Risk Premium on Lending

Unemployment %

Vehicle Real Price

Expectation of Future

Unemployment

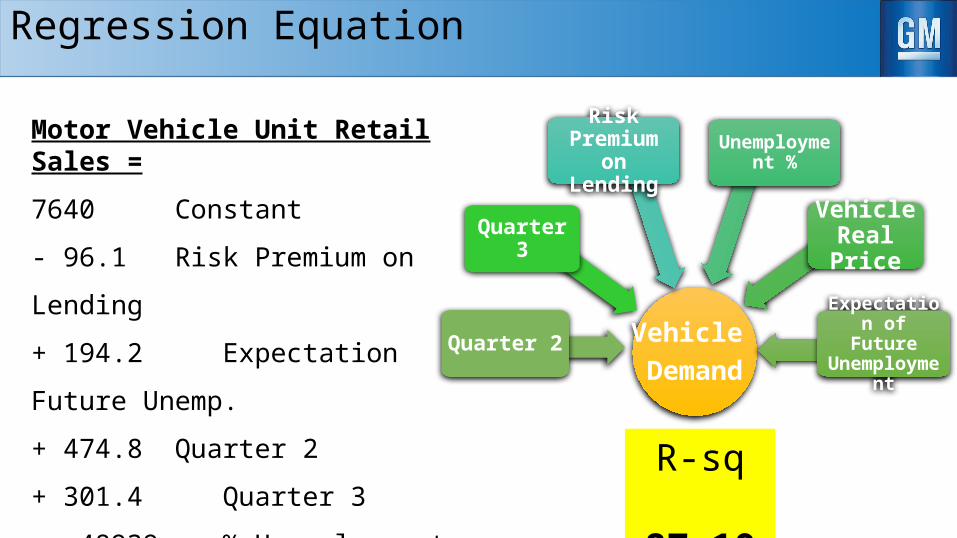

Regression Equation

Motor Vehicle Unit Retail Sales =

7640 Constant

- 96.1 Risk Premium on Lending

+ 194.2 Expectation Future Unemp.

+ 474.8 Quarter 2

+ 301.4 Quarter 3

- 48939 % Unemployment

- 0.02856 Real price R-sq 87.10%

1990 1991 1993 1995 1997 1998 2000 2002 2004 2005 2007 2009 2011 2012 20142,000

2,500

3,000

3,500

4,000

4,500

5,000

Actual Motor Vehicle Unit Retail Sales NSA (000)*Predicted Motor Vehicle Unit Retail Sales NSA (000)*

No. o

f Veh

icles

sol

d (0

00)

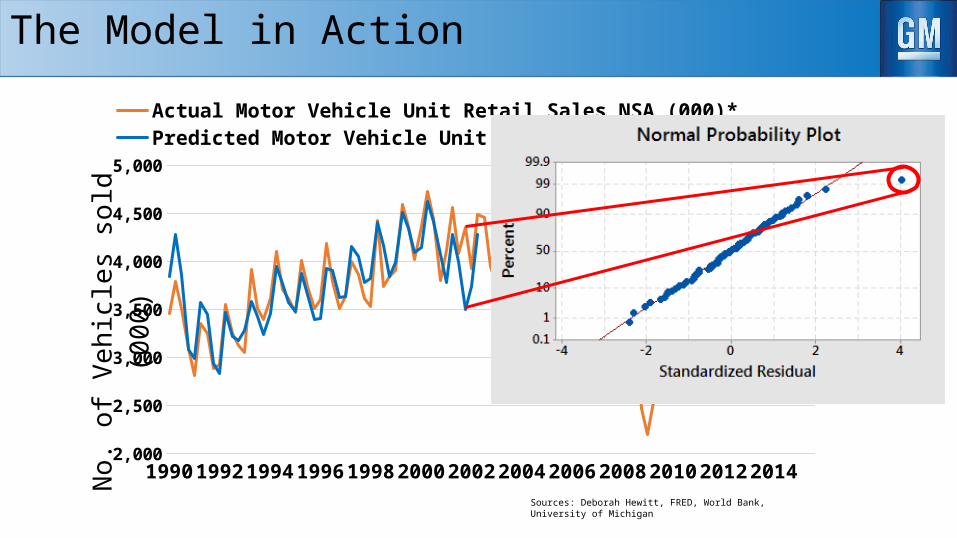

The Model in Action

Sources: Deborah Hewitt, FRED, World Bank, University of Michigan

1990 1991 1992 1993 1995 1996 1997 1998 2000 2001 2002 2003 2005 2006 2007 2008 2010 2011 2012 2013 20152000

2500

3000

3500

4000

4500

5000

Predicted Motor Vehicle Unit Retail Sales NSA (000)*Actual Motor Vehicle Unit Retail Sales NSA (000)*

No.

of V

ehic

les s

old

(000

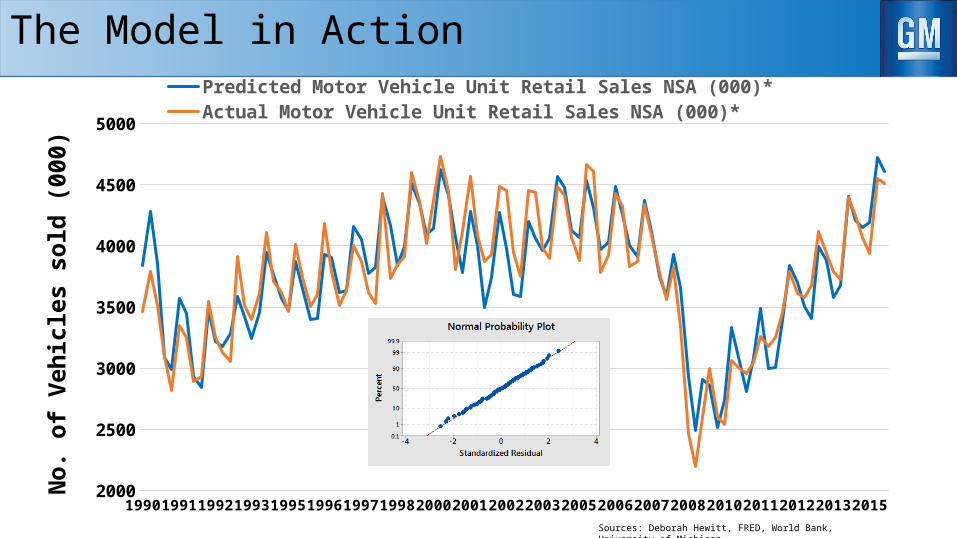

)The Model in Action

Sources: Deborah Hewitt, FRED, World Bank, University of Michigan

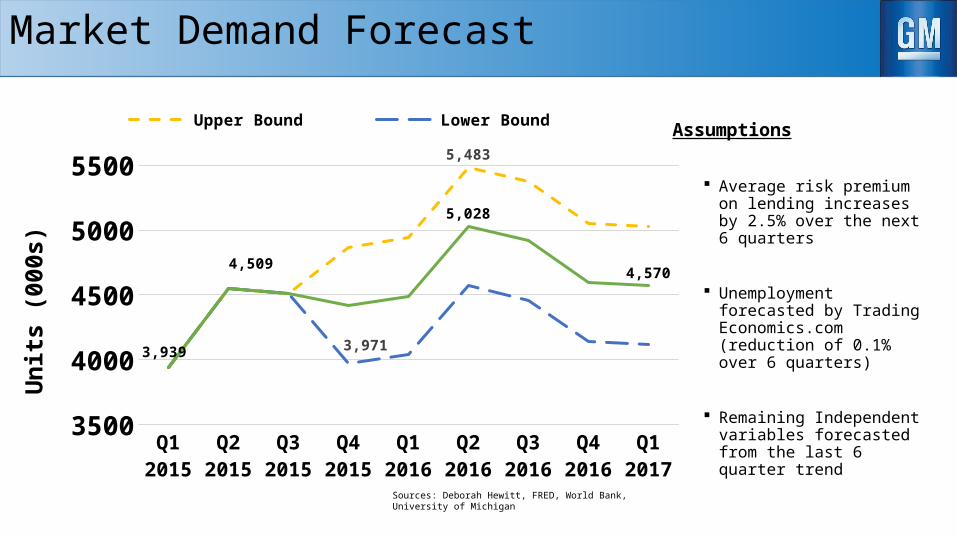

Q1 2015

Q2 2015

Q3 2015

Q4 2015

Q1 2016

Q2 2016

Q3 2016

Q4 2016

Q1 2017

3500

4000

4500

5000

5500 5,483

3,9713,939

4,509

5,028

4,570

Upper Bound Lower BoundForecasted Demand

Uni

ts (0

00s)

Market Demand Forecast

Assumptions

Average risk premium on lending increases by 2.5% over the next 6 quarters

Unemployment forecasted by Trading Economics.com (reduction of 0.1% over 6 quarters)

Remaining Independent variables forecasted from the last 6 quarter trend

Sources: Deborah Hewitt, FRED, World Bank, University of Michigan

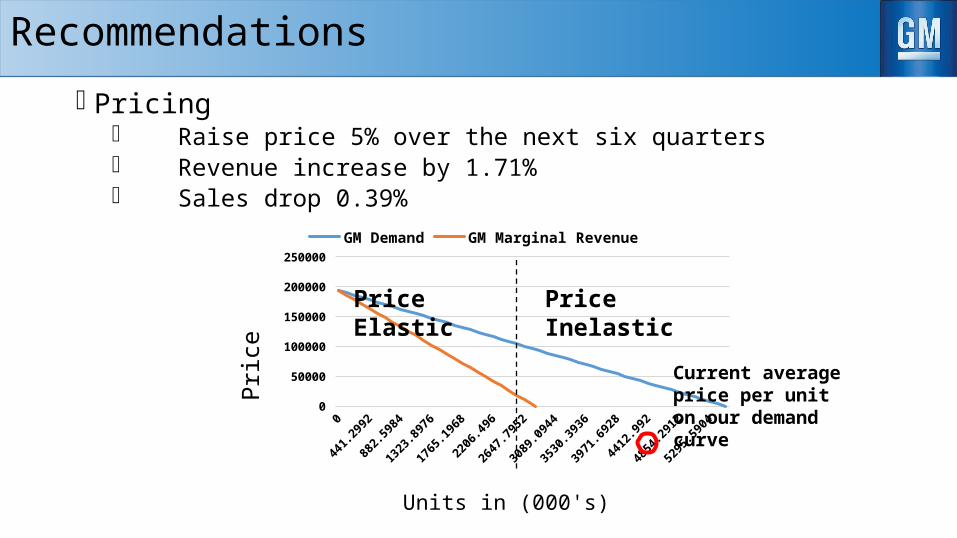

Pricing Raise price 5% over the next six quarters Revenue increase by 1.71% Sales drop 0.39%

Recommendations

0

330.9744

661.9488

992.9232

1323.8976

1654.872

1985.8464

2316.8208

2647.7952

2978.7696

3309.744

3640.7184

3971.6928

4302.6672

4633.6416

4964.616

5295.59040

50000

100000

150000

200000

250000

GM Demand GM Marginal Revenue

Units in (000's)

Pric

e

Current average price per unit on our demand curve

Price InelasticPrice Elastic

Recommendations

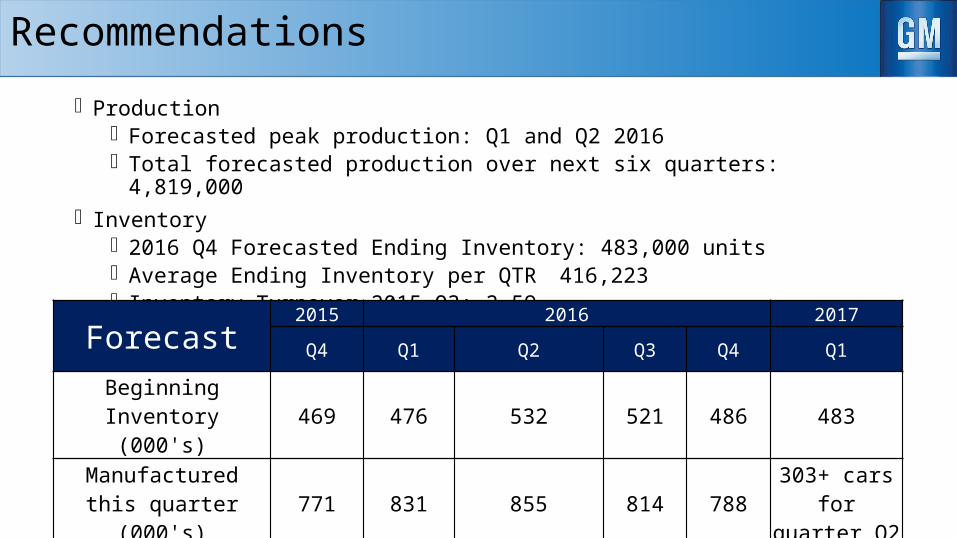

Production Forecasted peak production: Q1 and Q2 2016 Total forecasted production over next six quarters: 4,819,000

Inventory 2016 Q4 Forecasted Ending Inventory: 483,000 units Average Ending Inventory per QTR 416,223 Inventory Turnover 2015 Q3: 2.59

Forecast 2015 2016 2017Q4 Q1 Q2 Q3 Q4 Q1

Beginning Inventory (000's) 469 476 532 521 486 483

Manufactured this quarter (000's) 771 831 855 814 788 303+ cars for

quarter Q2Automobiles Sold in this

quarter (000's) 764 775 867 848 792 786

Ending Inventory (000's) 476 532 521 486 483

Technology

Urban Legend:

“If GM had kept up with the technology like the computer industry we would be driving $25 cars that

got 1,000 miles to the gallon.”-Bill Gates

GM Response:Who would want a car that crashes two times a day?

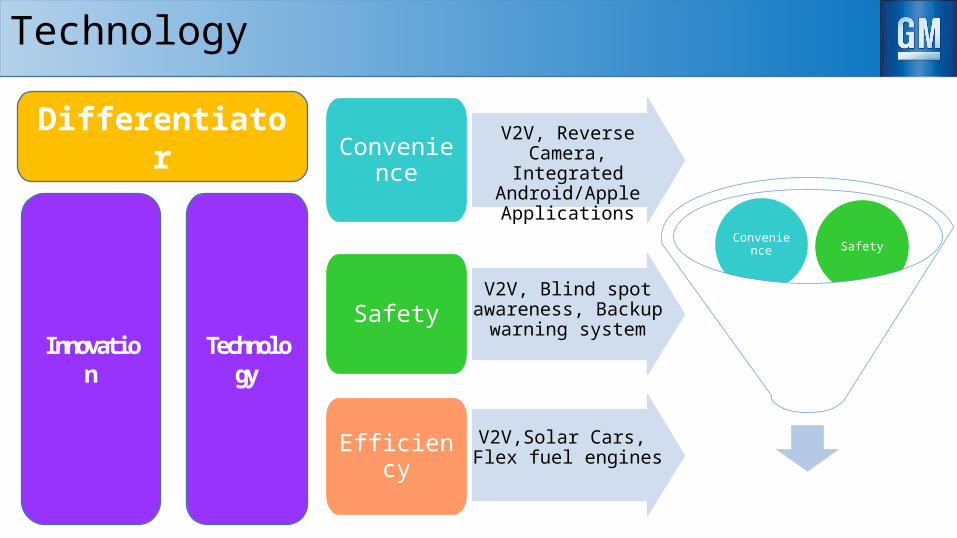

Innovation

Differentiator

Technology

V2V, Reverse Camera, Integrated

Android/Apple Applications

Convenience

V2V, Blind spot awareness, Backup

warning systemSafety

EfficiencyV2V,Solar Cars, Flex fuel

engines

Efficiency

Convenience Safety

Technology

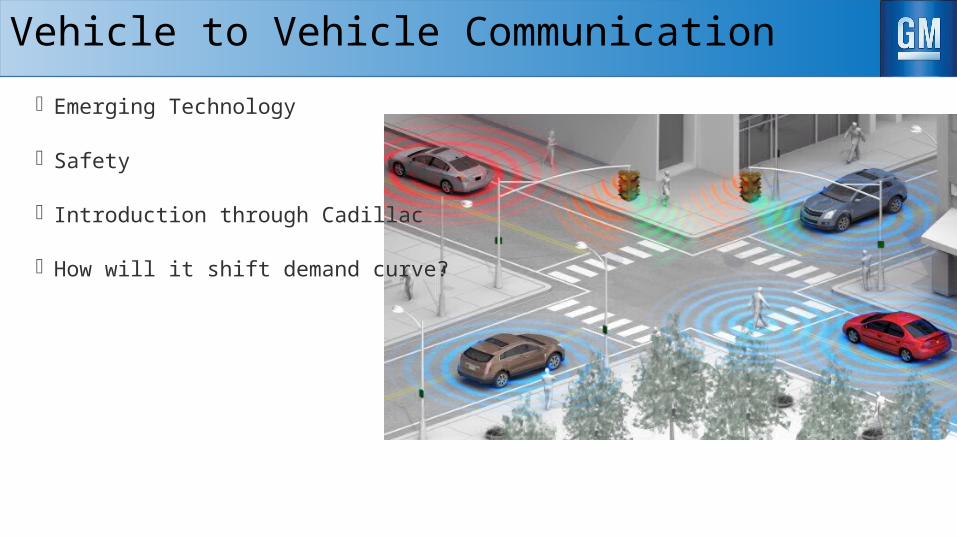

Vehicle to Vehicle Communication

Emerging Technology

Safety

Introduction through Cadillac

How will it shift demand curve?

• 32% of consumers say that safety plays the key role in their vehicle choice.

• We want the consumer to buy “YOUR” vehicle not “A” vehicle.

• OnStar Success

• All major car recalls have been based on safety standards

• Capitalize on advantage

• Minimal Cost

Why Vehicle to Vehicle Communication ?

Action Plan Recap

Forecasted over next six quarters (in units):

Total Demand 4,903,000

Total Production 4,819,000

Average Ending Inventory per QTR 416,223

Increase price 5% over the next six quarters

Invest in and expand V2V to two models per quarter

Questions

Back Up Slides

1990199119931995199719982000200220042005200720092011201220140

500100015002000250030003500400045005000

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

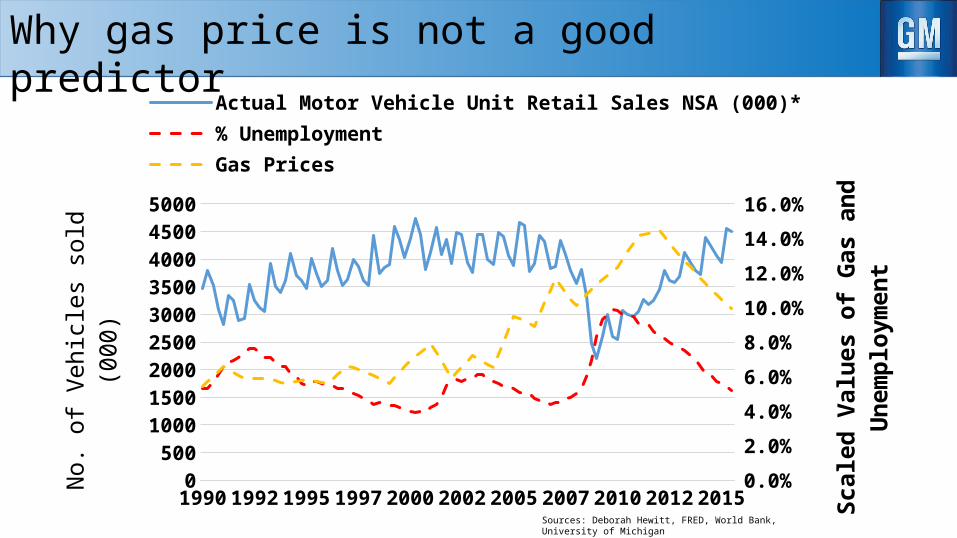

Actual Motor Vehicle Unit Retail Sales NSA (000)*% UnemploymentGas Prices

No. o

f Veh

icle

s sol

d (0

00)

Scal

ed V

alue

s of G

as a

nd U

n-em

ploy

men

t

Why gas price is not a good predictor

Sources: Deborah Hewitt, FRED, World Bank, University of Michigan

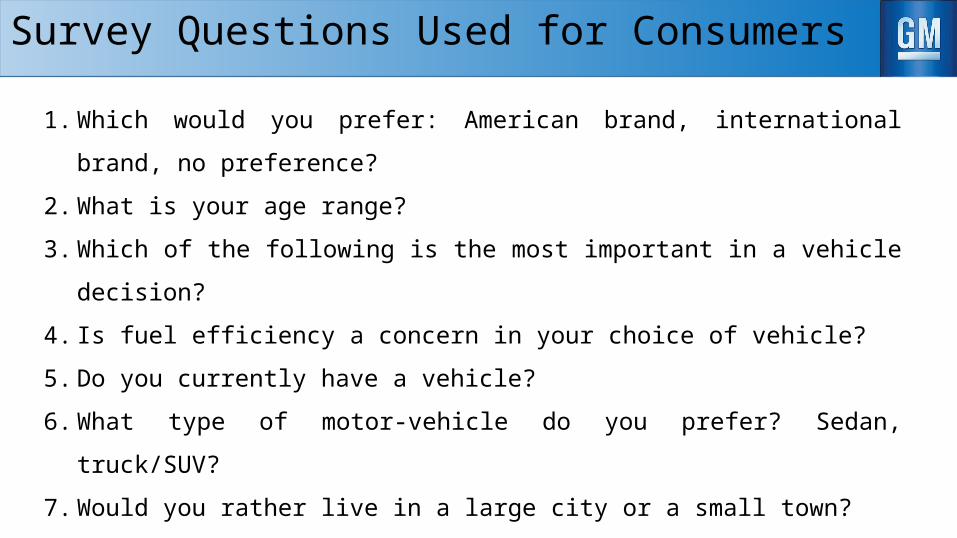

Survey Questions Used for Consumers

1. Which would you prefer: American brand, international brand, no preference?

2. What is your age range?

3. Which of the following is the most important in a vehicle decision?

4. Is fuel efficiency a concern in your choice of vehicle?

5. Do you currently have a vehicle?

6. What type of motor-vehicle do you prefer? Sedan, truck/SUV?

7. Would you rather live in a large city or a small town?

8. How much do you use public transportation?

9. How much are you willing to pay for a vehicle?

10. How long do you expect to keep your vehicle for?

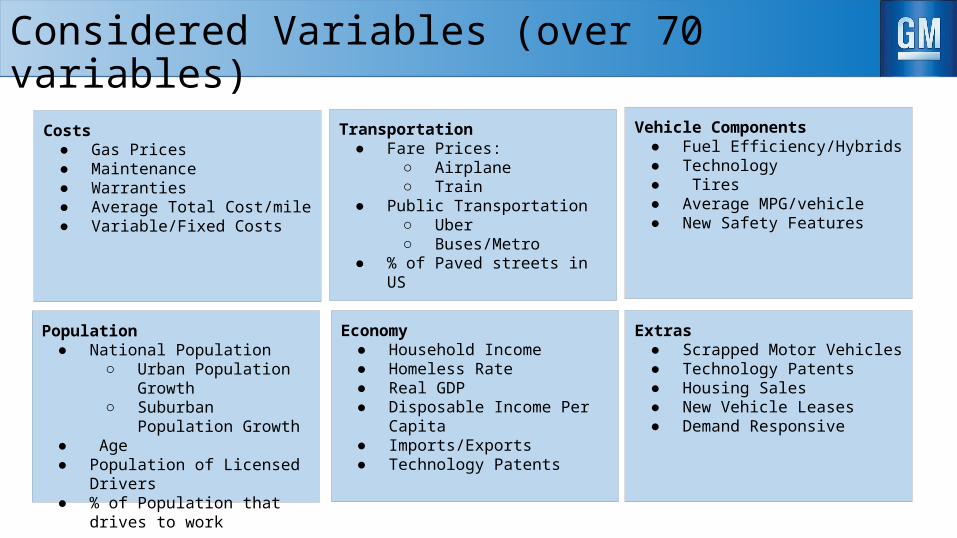

Considered Variables (over 70 variables)

Transportation● Fare Prices:

○ Airplane ○ Train

● Public Transportation○ Uber○ Buses/Metro

● % of Paved streets in US

Costs● Gas Prices ● Maintenance● Warranties ● Average Total Cost/mile ● Variable/Fixed Costs

Population● National Population

○ Urban Population Growth○ Suburban Population

Growth ● Age ● Population of Licensed Drivers ● % of Population that drives to

work

Economy ● Household Income ● Homeless Rate ● Real GDP ● Disposable Income Per Capita ● Imports/Exports ● Technology Patents

Vehicle Components● Fuel Efficiency/Hybrids● Technology ● Tires ● Average MPG/vehicle ● New Safety Features

Extras ● Scrapped Motor Vehicles ● Technology Patents ● Housing Sales ● New Vehicle Leases ● Demand Responsive

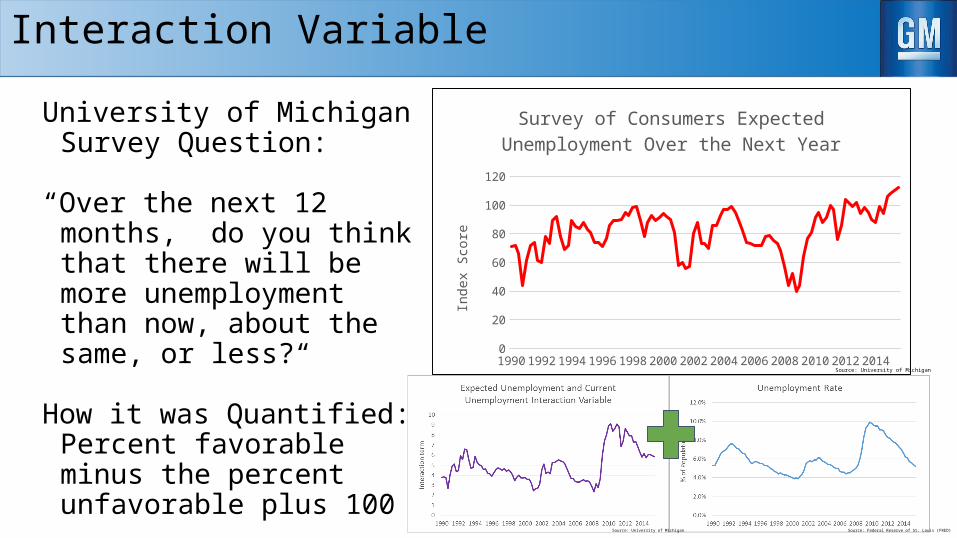

Interaction Variable

University of Michigan Survey Question:

“Over the next 12 months, do you think that there will be more unemployment than now, about the same, or less?“

How it was Quantified:Percent favorable minus the percent unfavorable plus 100

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 20140

20

40

60

80

100

120

Survey of Consumers Expected Unemployment Over the Next Year

Inde

x Sc

ore

Source: University of Michigan

Source: University of Michigan

Source: Federal Reserve of St. Louis (FRED)

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

5

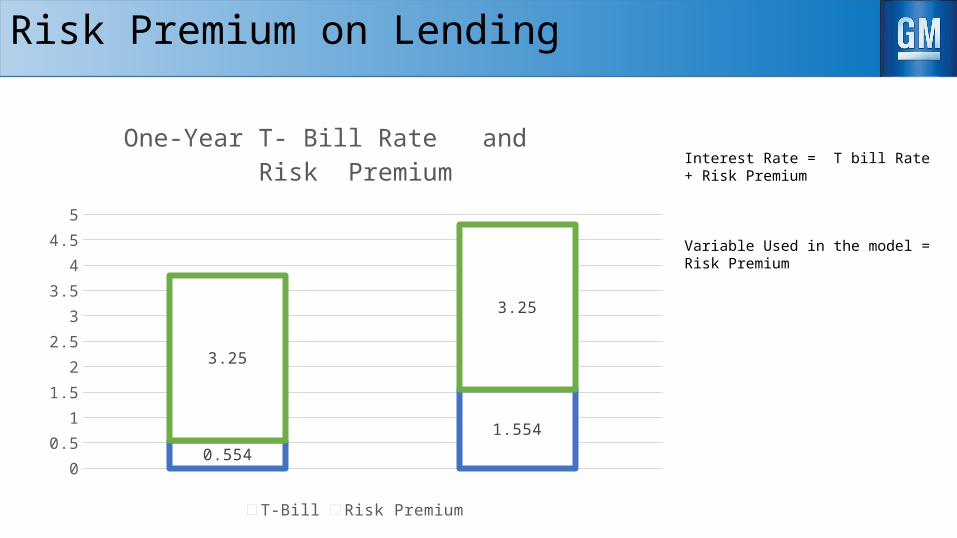

0.554

1.554

3.25

3.25

One-Year T- Bill Rate and Risk Premium

T-Bill Risk Premium

Interest Rate = T bill Rate + Risk Premium

Variable Used in the model =Risk Premium

Risk Premium on Lending

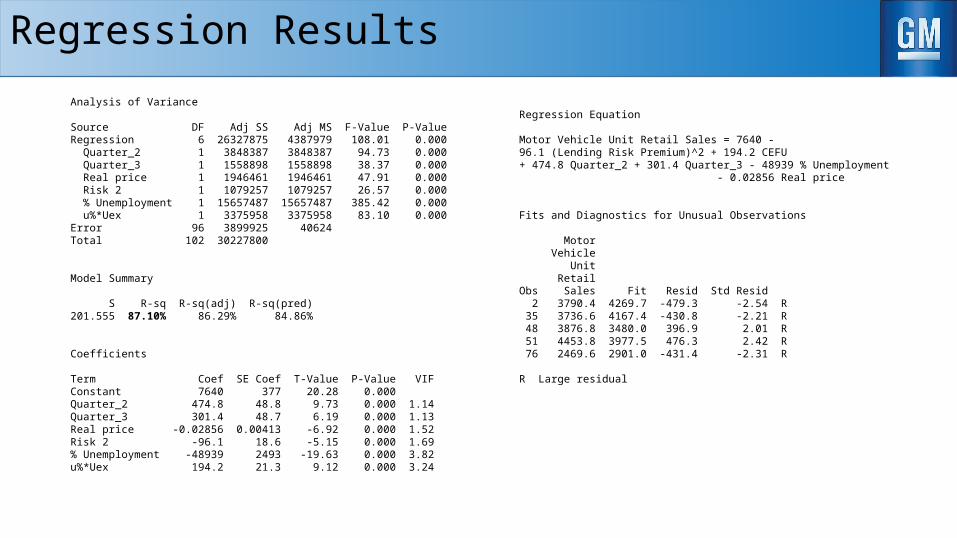

Analysis of Variance

Source DF Adj SS Adj MS F-Value P-ValueRegression 6 26327875 4387979 108.01 0.000 Quarter_2 1 3848387 3848387 94.73 0.000 Quarter_3 1 1558898 1558898 38.37 0.000 Real price 1 1946461 1946461 47.91 0.000 Risk 2 1 1079257 1079257 26.57 0.000 % Unemployment 1 15657487 15657487 385.42 0.000 u%*Uex 1 3375958 3375958 83.10 0.000Error 96 3899925 40624Total 102 30227800

Model Summary

S R-sq R-sq(adj) R-sq(pred)201.555 87.10% 86.29% 84.86%

Coefficients

Term Coef SE Coef T-Value P-Value VIFConstant 7640 377 20.28 0.000Quarter_2 474.8 48.8 9.73 0.000 1.14Quarter_3 301.4 48.7 6.19 0.000 1.13Real price -0.02856 0.00413 -6.92 0.000 1.52Risk 2 -96.1 18.6 -5.15 0.000 1.69% Unemployment -48939 2493 -19.63 0.000 3.82u%*Uex 194.2 21.3 9.12 0.000 3.24

Regression Equation

Motor Vehicle Unit Retail Sales = 7640 -96.1 (Lending Risk Premium)^2 + 194.2 CEFU + 474.8 Quarter_2 + 301.4 Quarter_3 - 48939 % Unemployment - 0.02856 Real price

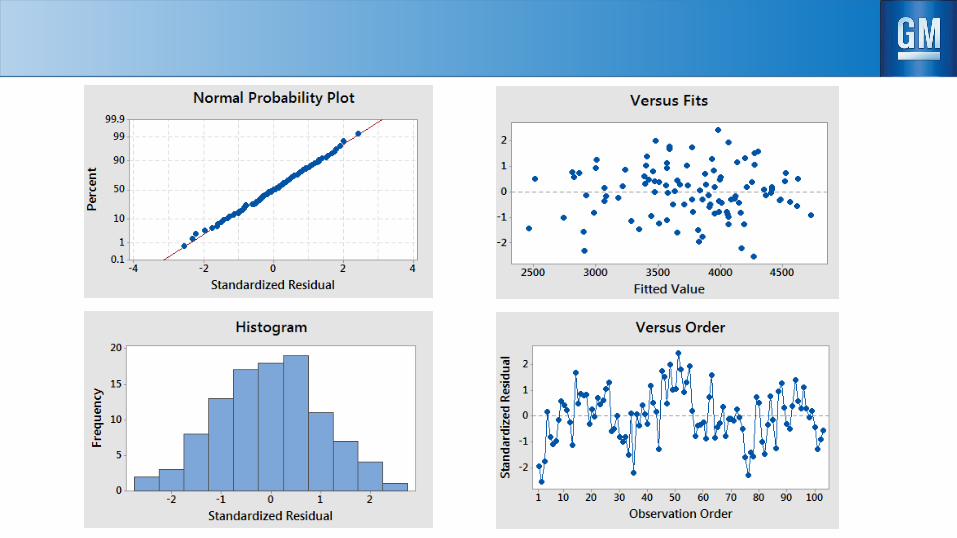

Fits and Diagnostics for Unusual Observations

Motor Vehicle Unit RetailObs Sales Fit Resid Std Resid 2 3790.4 4269.7 -479.3 -2.54 R 35 3736.6 4167.4 -430.8 -2.21 R 48 3876.8 3480.0 396.9 2.01 R 51 4453.8 3977.5 476.3 2.42 R 76 2469.6 2901.0 -431.4 -2.31 R

R Large residual

Regression Results