Embed Size (px)

Citation preview

Motilal Oswal Real Estate

Contents

3 Current Real Estate Scenario

6 Funding Sources for Real Estate Projects

9 Direct V/s. Indirect Investing

16 About Motilal Oswal Real Estate

21 Key Emerging Trends

2

CURRENT REAL ESTATE SCENARIO

3

o Residential sales declined across the seven leading cities of the country, largely due to

high price points, sticky interest rates and cautious buyer sentiments

o Keeping in mind subdued end-user/investor sentiments, many developers in major

markets have abstained from launching new projects, and instead directed their focus

towards reducing the existing inventory pile-up

o While the sector is currently facing short term challenges, the Indian real estate story

will remain intact due to its inherent strong fundamentals, favorable demographics,

high domestic savings, focus on infrastructure and continued urbanization will boost

the demand of residential real estate

o Our view is that time correction is underway for past 2 years and may continue for

another 1 – 2 years. The recent rate cuts should augur well for the real estate sector

as it translates into an eventual reduction in mortgage rates; and with economic

revival expected to improve buyer affordability, residential sales shall resume its

upward trend

Current Residential Market Scenario

o With offshoots of economic recovery visible, office market turned the corner in 2014

and is poised for further improvement in 2015

o In terms of absorption of 8.5 mn sq. ft. (in Q1’2015), Bengaluru leads the pack (3.82

mn sq. ft.) followed by NCR-Delhi, Gurgaon and Noida (1.48 mn sq. ft.), Mumbai (1.33

mn sq. ft.), Pune (0.89 mn sq. ft.) and Chennai (0.81 mn sq. ft.)

o E Commerce, IT / ITES and BFSI are the primary sectors driving the demand

o With an expanding economy, improving business sentiment and increasing job

creations, the momentum in demand for office real estate is expected to stay.

However, developer sentiment towards speculative construction of office buildings

is expected to remain cautious, and this in turn will limit the risk of further

overbuilding

Current Commercial Market Scenario

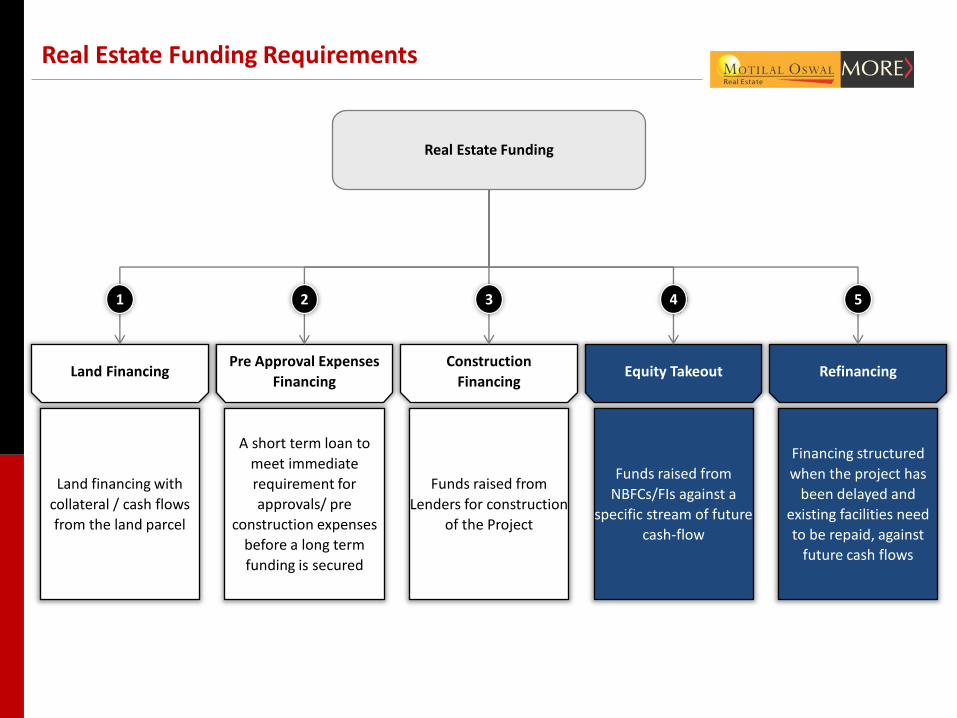

FUNDING SOURCES FOR REAL ESTATE PROJECTS

Land financing with

collateral / cash flows

from the land parcel

Financing structured

when the project has

been delayed and

existing facilities need

to be repaid, against

future cash flows

Funds raised from

Lenders for construction

of the Project

A short term loan to

meet immediate

requirement for

approvals/ pre

construction expenses

before a long term

funding is secured

Funds raised from

NBFCs/FIs against a

specific stream of future

cash-flow

Real Estate Funding

Land Financing Pre Approval Expenses

Financing

Construction

Financing Equity Takeout Refinancing

1 2 3 4 5

Real Estate Funding Requirements

Land Financing Pre Approval Expenses

Financing

Construction

Financing Equity Takeout Refinancing

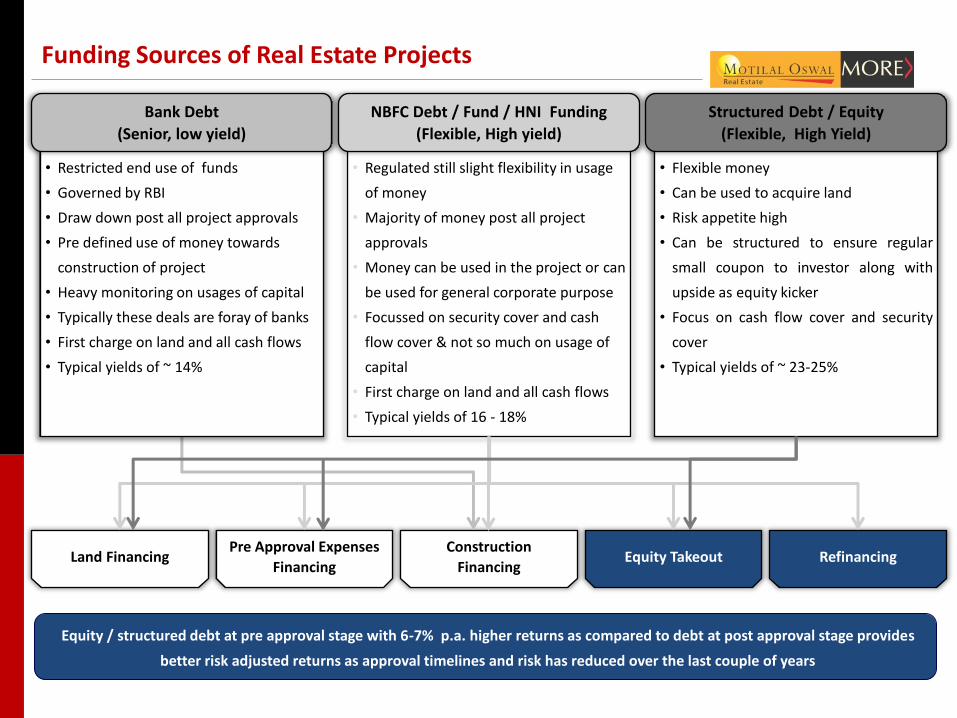

• Restricted end use of funds

• Governed by RBI

• Draw down post all project approvals

• Pre defined use of money towards

construction of project

• Heavy monitoring on usages of capital

• Typically these deals are foray of banks

• First charge on land and all cash flows

• Typical yields of ~ 14%

• Regulated still slight flexibility in usage

of money

• Majority of money post all project

approvals

• Money can be used in the project or can

be used for general corporate purpose

• Focussed on security cover and cash

flow cover & not so much on usage of

capital

• First charge on land and all cash flows

• Typical yields of 16 - 18%

• Flexible money

• Can be used to acquire land

• Risk appetite high

• Can be structured to ensure regular

small coupon to investor along with

upside as equity kicker

• Focus on cash flow cover and security

cover

• Typical yields of ~ 23-25%

Bank Debt

(Senior, low yield)

NBFC Debt / Fund / HNI Funding

(Flexible, High yield)

Structured Debt / Equity

(Flexible, High Yield)

Funding Sources of Real Estate Projects

Equity / structured debt at pre approval stage with 6-7% p.a. higher returns as compared to debt at post approval stage provides

better risk adjusted returns as approval timelines and risk has reduced over the last couple of years

DIRECT INVESTING V/S INDIRECT INVESTING

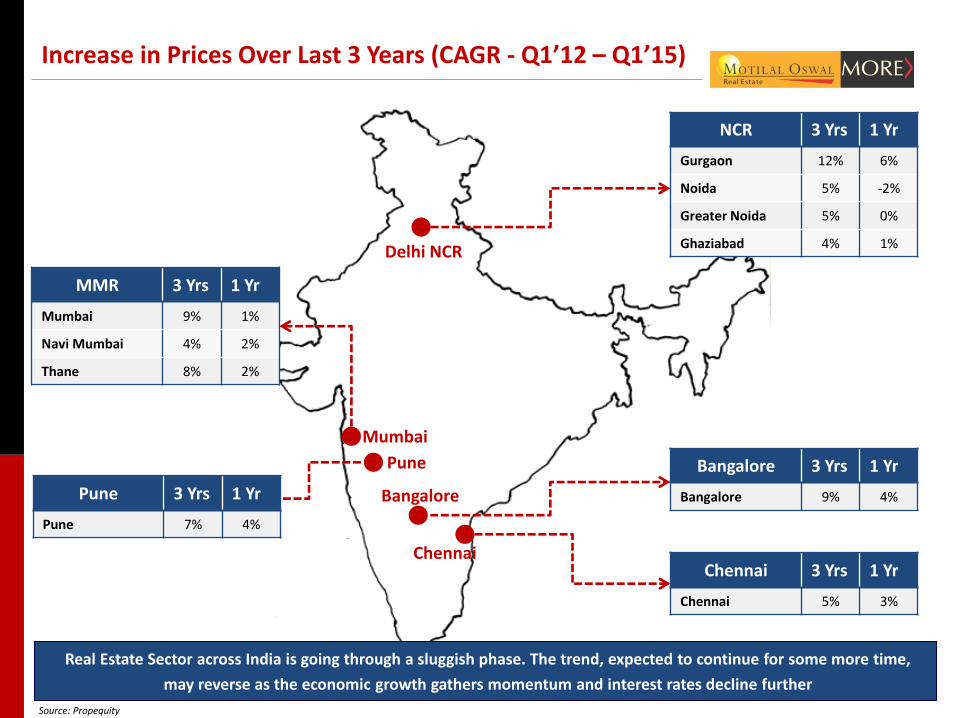

Increase in Prices Over Last 3 Years (CAGR - Q1’12 – Q1’15)

Delhi NCR

Mumbai

Bangalore

Chennai

MMR 3 Yrs 1 Yr

Mumbai 9% 1%

Navi Mumbai 4% 2%

Thane 8% 2%

Pune

Source: Propequity

Pune 3 Yrs 1 Yr

Pune 7% 4%

NCR 3 Yrs 1 Yr

Gurgaon 12% 6%

Noida 5% -2%

Greater Noida 5% 0%

Ghaziabad 4% 1%

Bangalore 3 Yrs 1 Yr

Bangalore 9% 4%

Chennai 3 Yrs 1 Yr

Chennai 5% 3%

Real Estate Sector across India is going through a sluggish phase. The trend, expected to continue for some more time,

may reverse as the economic growth gathers momentum and interest rates decline further

11

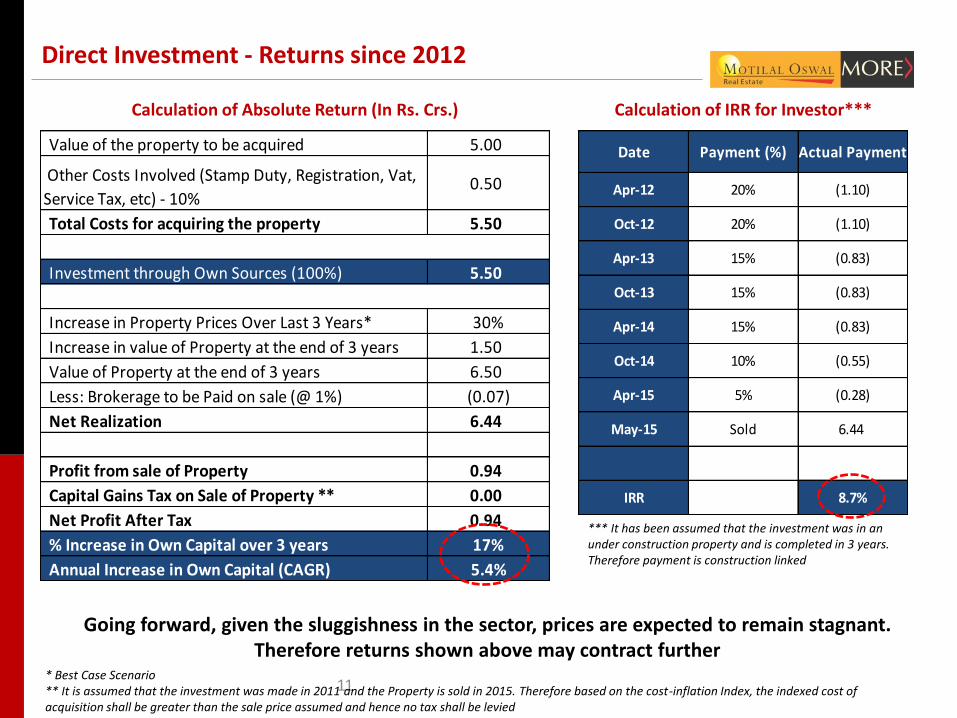

Direct Investment - Returns since 2012

Value of the property to be acquired 5.00

Other Costs Involved (Stamp Duty, Registration, Vat,

Service Tax, etc) - 10% 0.50

Total Costs for acquiring the property 5.50

Investment through Own Sources (100%) 5.50

Increase in Property Prices Over Last 3 Years* 30%

Increase in value of Property at the end of 3 years 1.50

Value of Property at the end of 3 years 6.50

Less: Brokerage to be Paid on sale (@ 1%) (0.07)

Net Realization 6.44

Profit from sale of Property 0.94

Capital Gains Tax on Sale of Property ** 0.00

Net Profit After Tax 0.94

% Increase in Own Capital over 3 years 17%

Annual Increase in Own Capital (CAGR) 5.4%

* Best Case Scenario ** It is assumed that the investment was made in 2011 and the Property is sold in 2015. Therefore based on the cost-inflation Index, the indexed cost of acquisition shall be greater than the sale price assumed and hence no tax shall be levied

Date Payment (%) Actual Payment

Apr-12 20% (1.10)

Oct-12 20% (1.10)

Apr-13 15% (0.83)

Oct-13 15% (0.83)

Apr-14 15% (0.83)

Oct-14 10% (0.55)

Apr-15 5% (0.28)

May-15 Sold 6.44

IRR 8.7%

Calculation of Absolute Return (In Rs. Crs.) Calculation of IRR for Investor***

*** It has been assumed that the investment was in an under construction property and is completed in 3 years. Therefore payment is construction linked

Going forward, given the sluggishness in the sector, prices are expected to remain stagnant. Therefore returns shown above may contract further

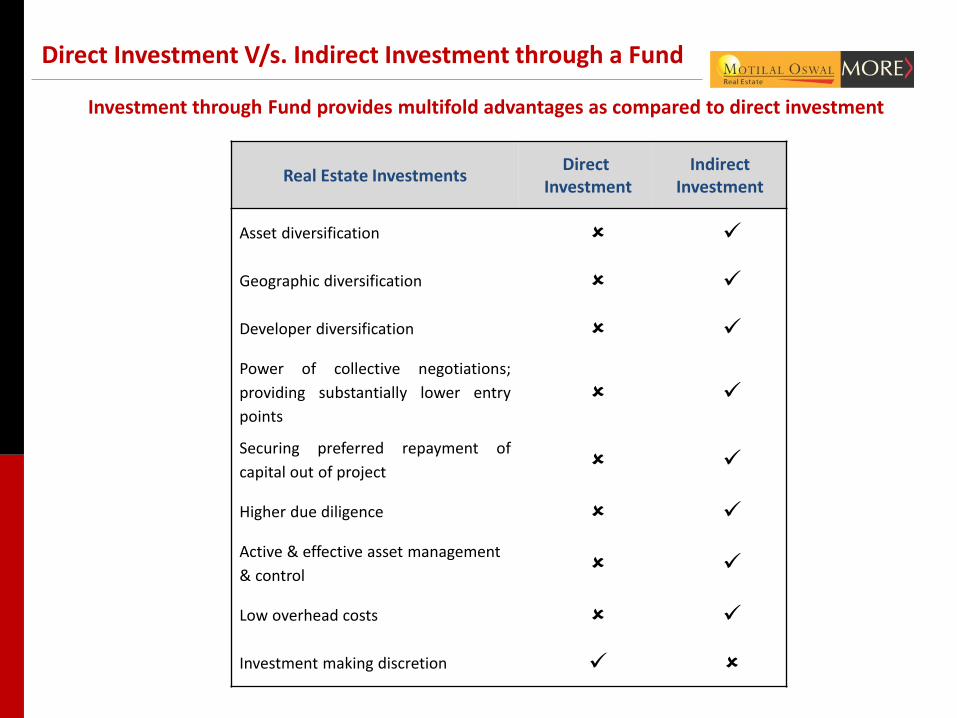

Direct Investment V/s. Indirect Investment through a Fund

Real Estate Investments Direct

Investment Indirect

Investment

Asset diversification

Geographic diversification

Developer diversification

Power of collective negotiations;

providing substantially lower entry

points

Securing preferred repayment of

capital out of project

Higher due diligence

Active & effective asset management

& control

Low overhead costs

Investment making discretion

Investment through Fund provides multifold advantages as compared to direct investment

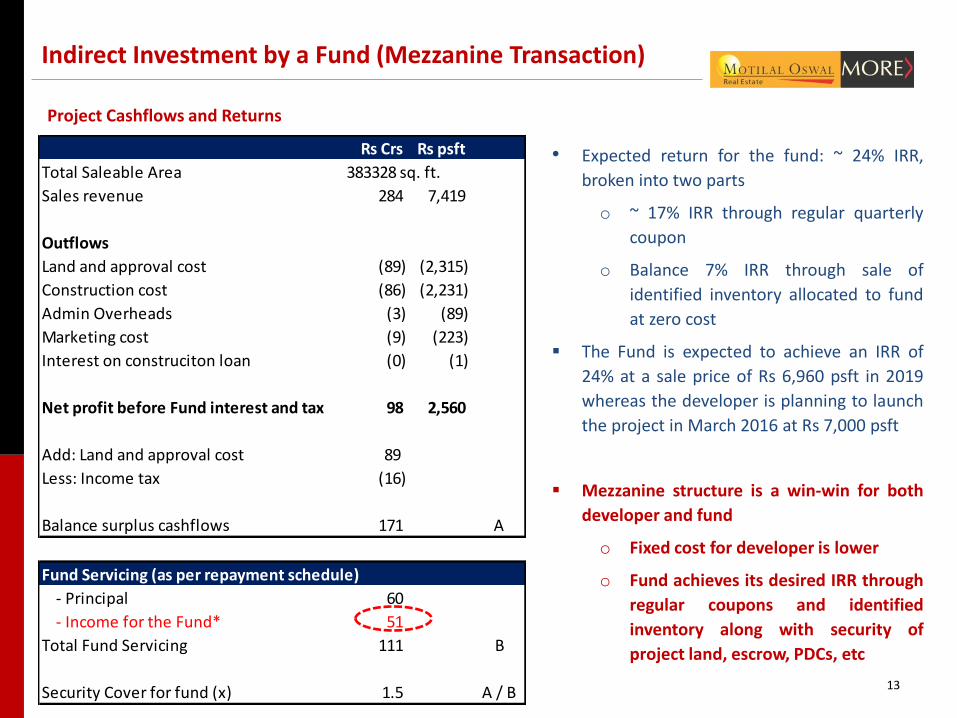

Project Cashflows and Returns

13

Indirect Investment by a Fund (Mezzanine Transaction)

Rs Crs Rs psft

Total Saleable Area 383328 sq. ft.

Sales revenue 284 7,419

Outflows

Land and approval cost (89) (2,315)

Construction cost (86) (2,231)

Admin Overheads (3) (89)

Marketing cost (9) (223)

Interest on construciton loan (0) (1)

Net profit before Fund interest and tax 98 2,560

Add: Land and approval cost 89

Less: Income tax (16)

Balance surplus cashflows 171 A

Fund Servicing (as per repayment schedule)

- Principal 60

- Income for the Fund* 51

Total Fund Servicing 111 B

Security Cover for fund (x) 1.5 A / B

• Expected return for the fund: ~ 24% IRR,

broken into two parts

o ~ 17% IRR through regular quarterly

coupon

o Balance 7% IRR through sale of

identified inventory allocated to fund

at zero cost

The Fund is expected to achieve an IRR of

24% at a sale price of Rs 6,960 psft in 2019

whereas the developer is planning to launch

the project in March 2016 at Rs 7,000 psft

Mezzanine structure is a win-win for both

developer and fund

o Fixed cost for developer is lower

o Fund achieves its desired IRR through

regular coupons and identified

inventory along with security of

project land, escrow, PDCs, etc

14 14

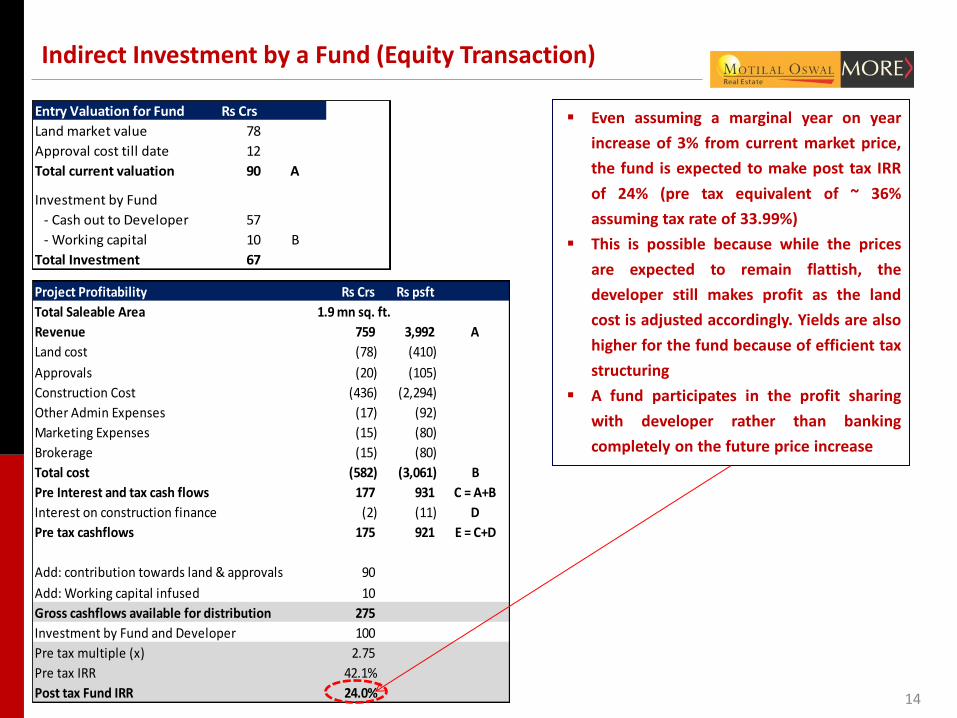

Even assuming a marginal year on year

increase of 3% from current market price,

the fund is expected to make post tax IRR

of 24% (pre tax equivalent of ~ 36%

assuming tax rate of 33.99%)

This is possible because while the prices

are expected to remain flattish, the

developer still makes profit as the land

cost is adjusted accordingly. Yields are also

higher for the fund because of efficient tax

structuring

A fund participates in the profit sharing

with developer rather than banking

completely on the future price increase

Indirect Investment by a Fund (Equity Transaction)

Entry Valuation for Fund Rs Crs

Land market value 78

Approval cost till date 12

Total current valuation 90 A

Investment by Fund

- Cash out to Developer 57

- Working capital 10 B

Total Investment 67

Project Profitability Rs Crs Rs psft

Total Saleable Area 1.9 mn sq. ft.

Revenue 759 3,992 A

Land cost (78) (410)

Approvals (20) (105)

Construction Cost (436) (2,294)

Other Admin Expenses (17) (92)

Marketing Expenses (15) (80)

Brokerage (15) (80)

Total cost (582) (3,061) B

Pre Interest and tax cash flows 177 931 C = A+B

Interest on construction finance (2) (11) D

Pre tax cashflows 175 921 E = C+D

Add: contribution towards land & approvals 90

Add: Working capital infused 10

Gross cashflows available for distribution 275

Investment by Fund and Developer 100

Pre tax multiple (x) 2.75

Pre tax IRR 42.1%

Post tax Fund IRR 24.0%

15

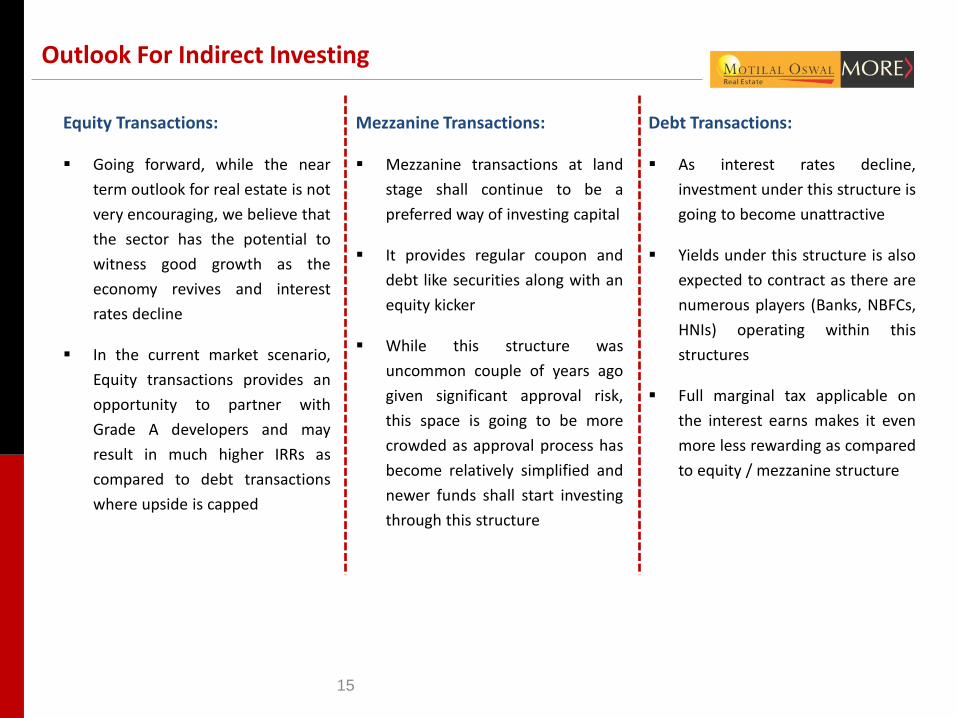

Outlook For Indirect Investing

Equity Transactions:

Going forward, while the near

term outlook for real estate is not

very encouraging, we believe that

the sector has the potential to

witness good growth as the

economy revives and interest

rates decline

In the current market scenario,

Equity transactions provides an

opportunity to partner with

Grade A developers and may

result in much higher IRRs as

compared to debt transactions

where upside is capped

Mezzanine Transactions:

Mezzanine transactions at land

stage shall continue to be a

preferred way of investing capital

It provides regular coupon and

debt like securities along with an

equity kicker

While this structure was

uncommon couple of years ago

given significant approval risk,

this space is going to be more

crowded as approval process has

become relatively simplified and

newer funds shall start investing

through this structure

Debt Transactions:

As interest rates decline,

investment under this structure is

going to become unattractive

Yields under this structure is also

expected to contract as there are

numerous players (Banks, NBFCs,

HNIs) operating within this

structures

Full marginal tax applicable on

the interest earns makes it even

more less rewarding as compared

to equity / mezzanine structure

ABOUT MOTILAL OSWAL REAL ESTATE

16

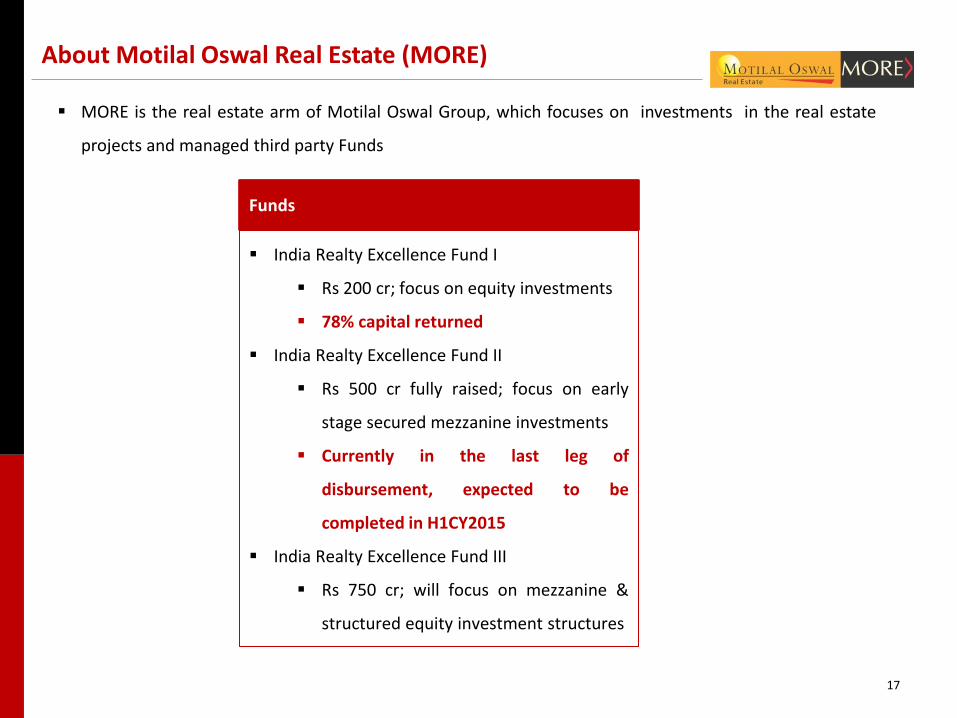

About Motilal Oswal Real Estate (MORE)

MORE is the real estate arm of Motilal Oswal Group, which focuses on investments in the real estate

projects and managed third party Funds

India Realty Excellence Fund I

Rs 200 cr; focus on equity investments

78% capital returned

India Realty Excellence Fund II

Rs 500 cr fully raised; focus on early

stage secured mezzanine investments

Currently in the last leg of

disbursement, expected to be

completed in H1CY2015

India Realty Excellence Fund III

Rs 750 cr; will focus on mezzanine &

structured equity investment structures

Funds

17

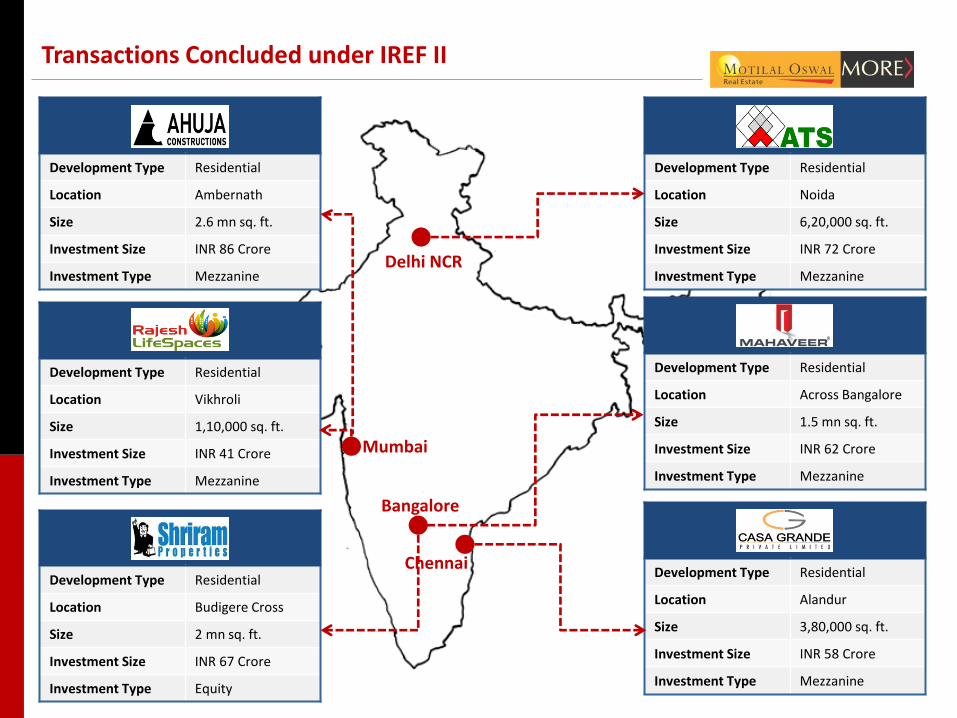

Transactions Concluded under IREF II

18

Delhi NCR

Mumbai

Bangalore

Chennai Development Type Residential

Location Alandur

Size 3,80,000 sq. ft.

Investment Size INR 58 Crore

Investment Type Mezzanine

Development Type Residential

Location Noida

Size 6,20,000 sq. ft.

Investment Size INR 72 Crore

Investment Type Mezzanine

Development Type Residential

Location Ambernath

Size 2.6 mn sq. ft.

Investment Size INR 86 Crore

Investment Type Mezzanine

Development Type Residential

Location Vikhroli

Size 1,10,000 sq. ft.

Investment Size INR 41 Crore

Investment Type Mezzanine

Development Type Residential

Location Across Bangalore

Size 1.5 mn sq. ft.

Investment Size INR 62 Crore

Investment Type Mezzanine

Development Type Residential

Location Budigere Cross

Size 2 mn sq. ft.

Investment Size INR 67 Crore

Investment Type Equity

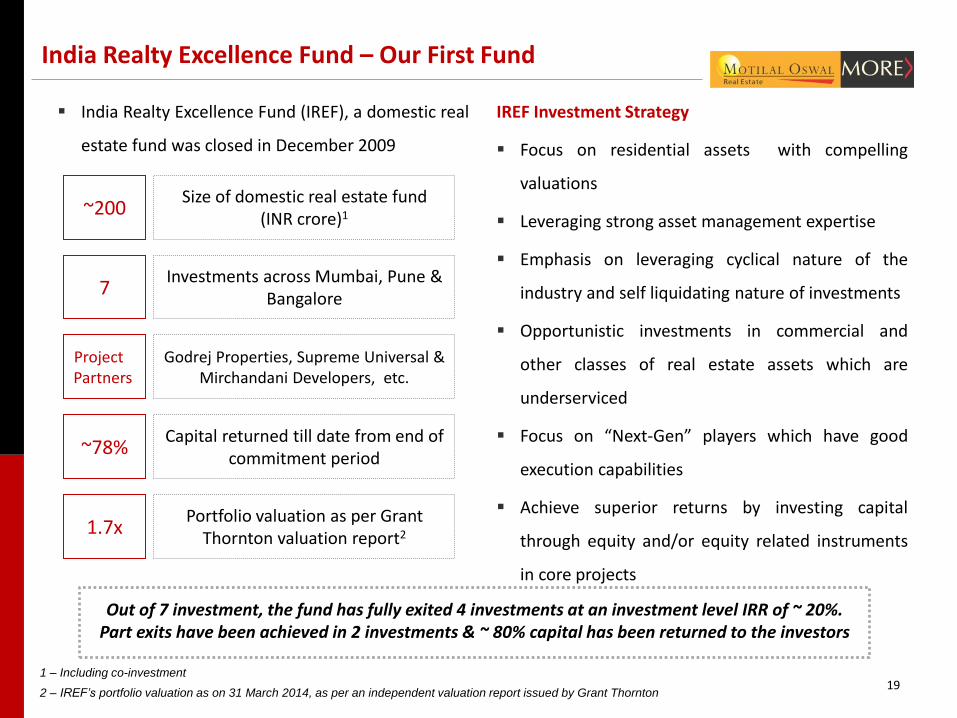

India Realty Excellence Fund – Our First Fund

India Realty Excellence Fund (IREF), a domestic real

estate fund was closed in December 2009

IREF Investment Strategy

Focus on residential assets with compelling

valuations

Leveraging strong asset management expertise

Emphasis on leveraging cyclical nature of the

industry and self liquidating nature of investments

Opportunistic investments in commercial and

other classes of real estate assets which are

underserviced

Focus on “Next-Gen” players which have good

execution capabilities

Achieve superior returns by investing capital

through equity and/or equity related instruments

in core projects

~200 Size of domestic real estate fund

(INR crore)1

7 Investments across Mumbai, Pune &

Bangalore

~78% Capital returned till date from end of

commitment period

1.7x Portfolio valuation as per Grant

Thornton valuation report2

1 – Including co-investment

2 – IREF’s portfolio valuation as on 31 March 2014, as per an independent valuation report issued by Grant Thornton

Project Partners

Godrej Properties, Supreme Universal & Mirchandani Developers, etc.

19

Out of 7 investment, the fund has fully exited 4 investments at an investment level IRR of ~ 20%. Part exits have been achieved in 2 investments & ~ 80% capital has been returned to the investors

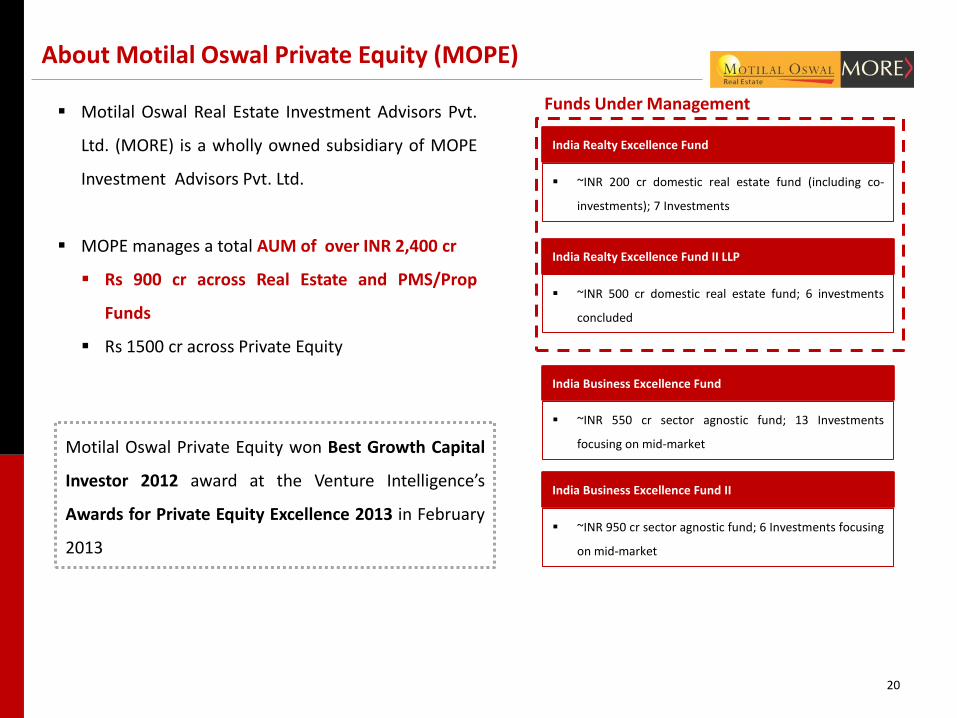

About Motilal Oswal Private Equity (MOPE)

Motilal Oswal Real Estate Investment Advisors Pvt.

Ltd. (MORE) is a wholly owned subsidiary of MOPE

Investment Advisors Pvt. Ltd.

MOPE manages a total AUM of over INR 2,400 cr

Rs 900 cr across Real Estate and PMS/Prop

Funds

Rs 1500 cr across Private Equity

Motilal Oswal Private Equity won Best Growth Capital

Investor 2012 award at the Venture Intelligence’s

Awards for Private Equity Excellence 2013 in February

2013 ~INR 950 cr sector agnostic fund; 6 Investments focusing

on mid-market

India Business Excellence Fund II

~INR 200 cr domestic real estate fund (including co-

investments); 7 Investments

India Realty Excellence Fund

~INR 550 cr sector agnostic fund; 13 Investments

focusing on mid-market

India Business Excellence Fund

Funds Under Management

~INR 500 cr domestic real estate fund; 6 investments

concluded

India Realty Excellence Fund II LLP

20

KEY EMERGING TRENDS IN REAL ESTATE

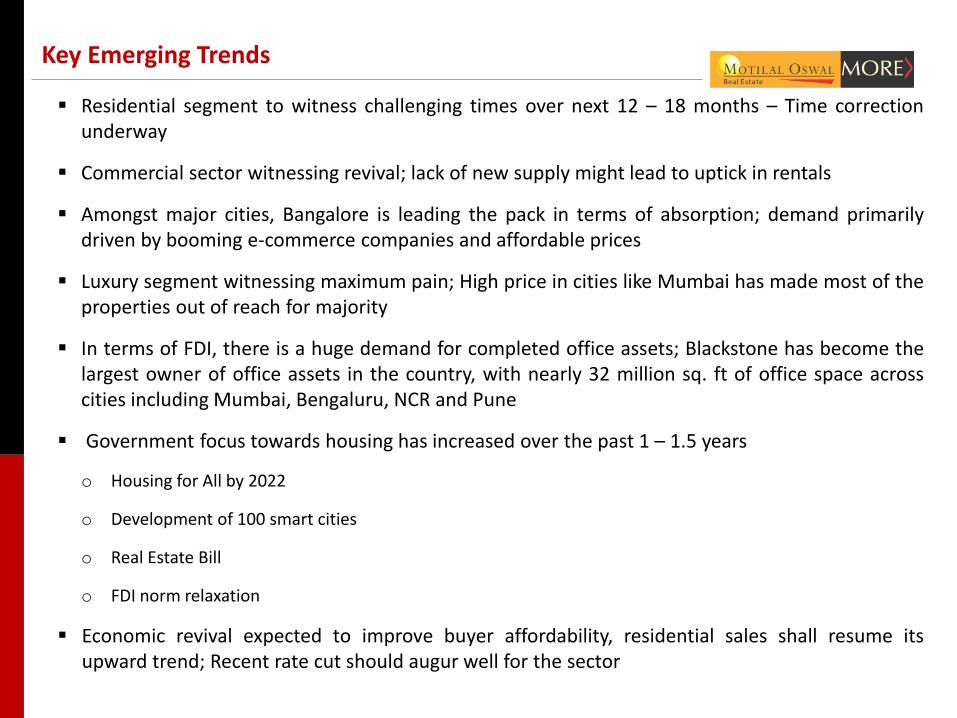

Key Emerging Trends

Residential segment to witness challenging times over next 12 – 18 months – Time correction underway

Commercial sector witnessing revival; lack of new supply might lead to uptick in rentals

Amongst major cities, Bangalore is leading the pack in terms of absorption; demand primarily driven by booming e-commerce companies and affordable prices

Luxury segment witnessing maximum pain; High price in cities like Mumbai has made most of the properties out of reach for majority

In terms of FDI, there is a huge demand for completed office assets; Blackstone has become the largest owner of office assets in the country, with nearly 32 million sq. ft of office space across cities including Mumbai, Bengaluru, NCR and Pune

Government focus towards housing has increased over the past 1 – 1.5 years

o Housing for All by 2022

o Development of 100 smart cities

o Real Estate Bill

o FDI norm relaxation

Economic revival expected to improve buyer affordability, residential sales shall resume its upward trend; Recent rate cut should augur well for the sector

23

Disclaimer:- This report is for information purposes only and does not construe to be any investment, legal or taxation advice. It is not intended as an offer or solicitation for the purchase or sale of any financial instrument. Any action taken by you on the basis of the information contained herein is your responsibility alone and India Realty Excellence Fund II LLP, Motilal Oswal Real Estate Investment Advisors II Private Limited and its subsidiaries or its employees or directors, associates will not be liable in any manner for the consequences of such action taken by you. We have exercised due diligence in checking the correctness and authenticity of the information contained herein, but do not represent that it is accurate or complete. India Realty Excellence Fund II LLP, Motilal Oswal Real Estate Investment Advisors II Private Limited or any of its subsidiaries or associates or employees shall not be in any way responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this publication.

THANK YOU