Embed Size (px)

Citation preview

Moscow, RussiaMarch 2020

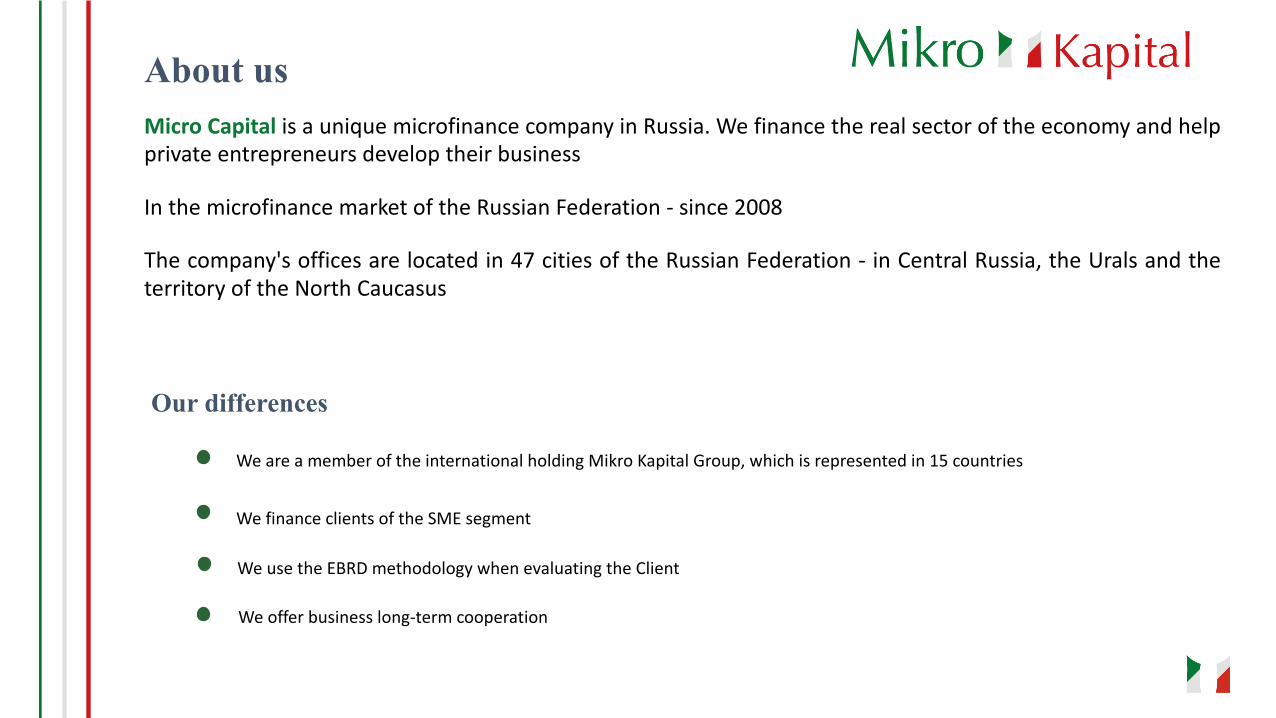

About usMicro Capital is a unique microfinance company in Russia. We finance the real sector of the economy and helpprivate entrepreneurs develop their business

In the microfinance market of the Russian Federation - since 2008

The company's offices are located in 47 cities of the Russian Federation - in Central Russia, the Urals and theterritory of the North Caucasus

We finance clients of the SME segment

We are a member of the international holding Mikro Kapital Group, which is represented in 15 countries

We use the EBRD methodology when evaluating the Client

We offer business long-term cooperation

Our differences

History

1999 - The company began operations in Russia in 1999 in the Samara city under the FINCA brand.

2005 - The merger of several separate FINCA divisions operating as separate legal entities under one TIN

with its head office in the Samara city

2011 - Obtaining the status of microfinance company

2017 - The company continues to work under the new Mikro Kapital brand in connection with a change of

ownership

2018 - MCC Mikro Kapital Russia LLC transfers its assets and liabilities to the Company, as a result of which

the Company becomes one of the largest portfolio size among microfinance organizations in Russia

engaged in financing SMEs

2020 - The company has 47 offices and 220 employees, serves 7300 customers

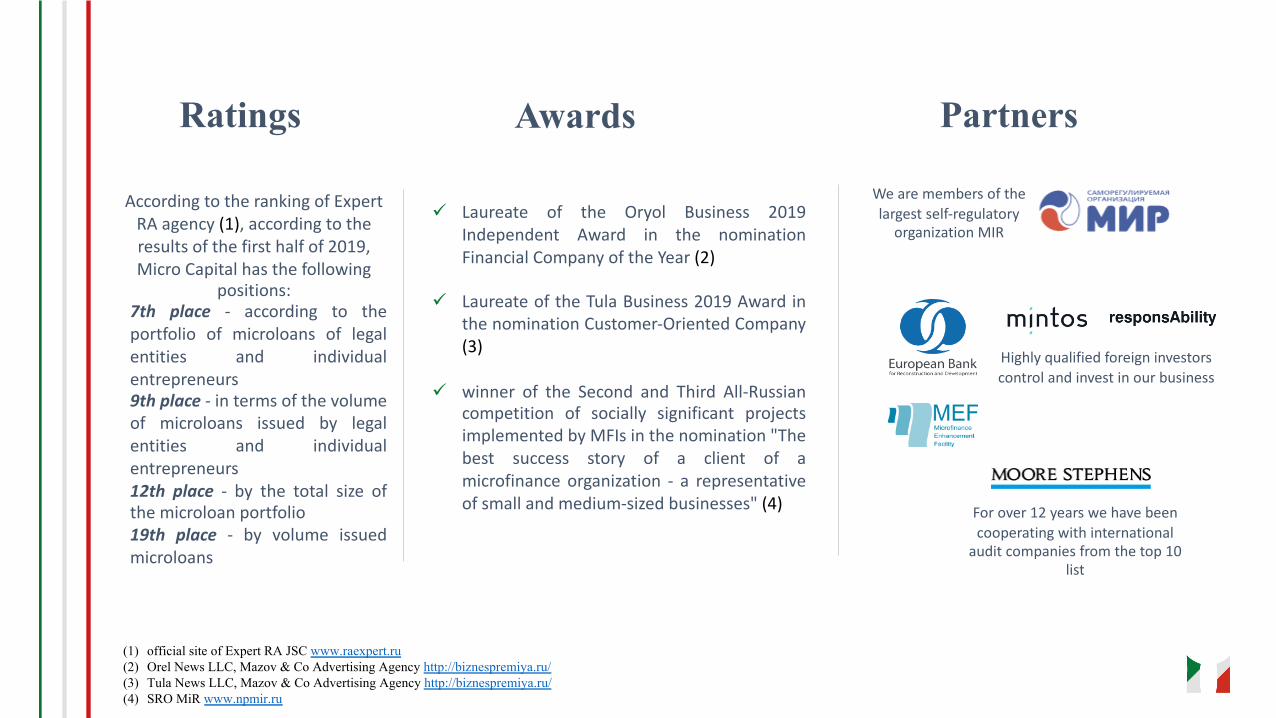

Ratings

7th place - according to theportfolio of microloans of legalentities and individualentrepreneurs9th place - in terms of the volumeof microloans issued by legalentities and individualentrepreneurs12th place - by the total size ofthe microloan portfolio19th place - by volume issuedmicroloans

Highly qualified foreign investors control and invest in our business

For over 12 years we have been cooperating with international

audit companies from the top 10 list

According to the ranking of Expert RA agency (1), according to the results of the first half of 2019,Micro Capital has the following

positions:

Partners

We are members of the largest self-regulatory

organization MIR

Awards

ü Laureate of the Oryol Business 2019Independent Award in the nominationFinancial Company of the Year (2)

ü Laureate of the Tula Business 2019 Award inthe nomination Customer-Oriented Company(3)

ü winner of the Second and Third All-Russiancompetition of socially significant projectsimplemented by MFIs in the nomination "Thebest success story of a client of amicrofinance organization - a representativeof small and medium-sized businesses" (4)

(1) official site of Expert RA JSC www.raexpert.ru(2) Orel News LLC, Mazov & Co Advertising Agency http://biznespremiya.ru/(3) Tula News LLC, Mazov & Co Advertising Agency http://biznespremiya.ru/(4) SRO MiR www.npmir.ru

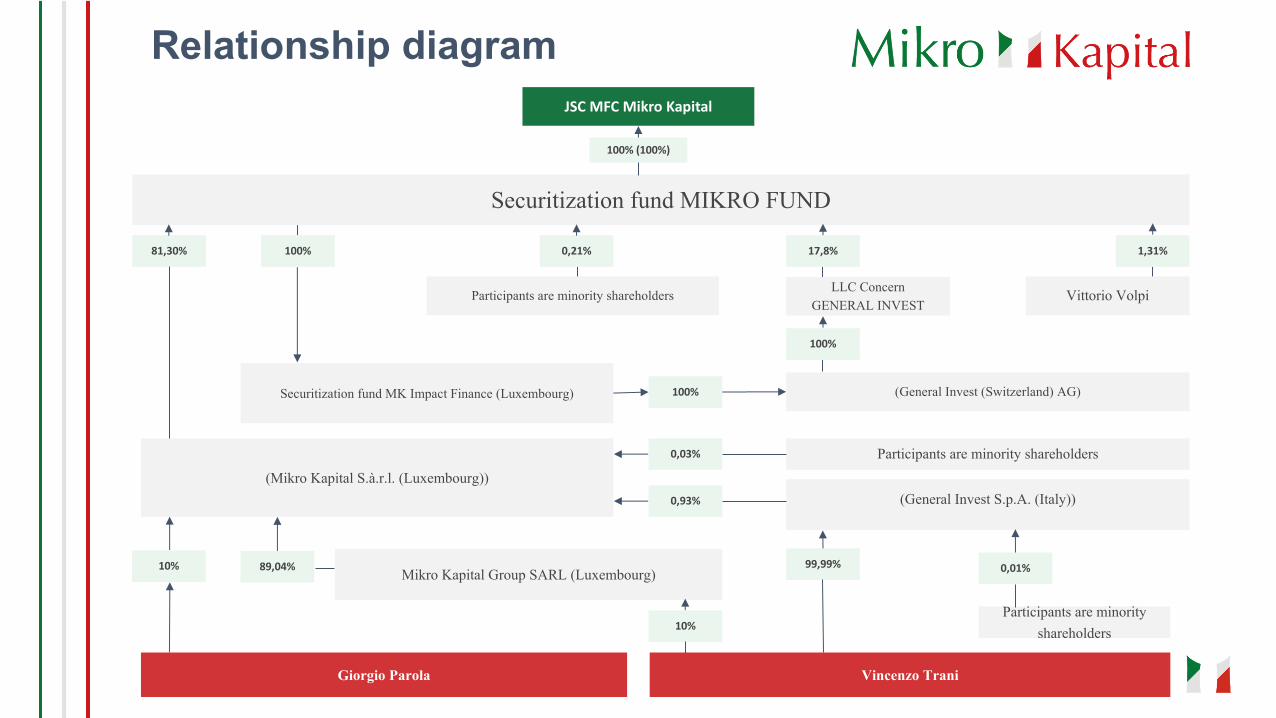

Relationship diagramJSC MFC Mikro Kapital

100% (100%)

Securitization fund MIKRO FUND

81,30% 100% 0,21% 17,8% 1,31%

Participants are minority shareholders LLC ConcernGENERAL INVEST

Vittorio Volpi

Securitization fund MK Impact Finance (Luxembourg) 100%

100%

(General Invest (Switzerland) AG)

(Mikro Kapital S.à.r.l. (Luxembourg))

Vincenzo TraniGiorgio Parola

Participants are minority shareholders

(General Invest S.p.A. (Italy))

0,03%

0,93%

89,04%10%Mikro Kapital Group SARL (Luxembourg)

10%

99,99% 0,01%

Participants are minority shareholders

Vincenzo TraniMember of the Supervisory BoardSince 2008Mr. Trani was born in Naples in 1974. After training in his specialty, he moved to Russia in the late 1990s to work at the European Bank forReconstruction and Development (EBRD) and has since been continuously working in the same market.For eight years, Mr. Trani has led development initiatives on behalf of large private banks and industry groups.Mr. Trani has received official recognition in Russia as the initiator of a number of important projects for the development of small andmedium-sized businesses. He founded General Invest in 2007, and in 2008 Mikro Kapital, a microfinance fund to finance Russian smallbusinesses, which has established itself as one of Europe's most successful projects.

Giorgio ParolaChairman of the Supervisory BoardSince 2008Mr. Parola was born in 1981 in Naples. After gaining experience in Italy at Intesa Consulting, which ranks first in corporate counseling, Mr. Parolamoved to Russia in 2006 as a consultant to the European Bank for Reconstruction and Development (EBRD).Then Mr. Parola worked as the person responsible for creating the financing line for small and medium enterprises. Today, Mr. Parola is one of the founders of Mikro Kapital and, concurrently, is vice president of lending to Mikro Kapital in Russia, Belarus and Italy.

Grigory ChorayanMember of the Supervisory BoardVice President of Mikro Kapital Group (Luxembourg), Mr. Chorayan is a member of the Supervisory Board of a number of microfinance andfactoring companies in Moldova, Romania, Russia and Tajikistan. He has over 20 years of professional international banking experience. Hebegan his career at the largest private bank in southern Russia, moving from an economist to senior positions as a member of the board, headof the treasury and finance department, and also as chairman of the bank’s asset management committee.Since 2012, he has worked in a number of consulting companies in Switzerland, Germany and Austria. For more than 4 years he was DeputyDirector of the Russian EBRD Sustainable Energy Financing Program (RuSEFF) in Moscow.Mr. Chorayan is the author of more than 30 published scientific papers, has a master's degree in economics (Kentucky, USA) and a doctorate.Candidate of Technical Sciences (Russia).

Supervisory Board

Elvina AblaevaMember of the Supervisory BoardProfessional activities of Elvina Ablaeva in the field of lending to small and medium-sized businesses began in 2004. From 2006 to 2008, she led the credit departments of the largest banks in Ukraine, including VTB Bank.From 2008 to 2012, she served as a consultant to the Microcredit Program in Ukraine. Since 2014, she continued to work in the holding MikroKapital Group as the regional director of one of the companies of the Group. Since June 2015, he has been responsible for credit riskmanagement at Micro Capital Group.

John StubMember of the Supervisory BoardJohn is an experienced banker and consultant. Growing up in South Africa and Zimbabwe, he graduated from the University of London ineconomics and politics and subsequently earned a master's degree in political science from Hebrew University in Jerusalem.After a 21-year banking career in Israel and the UK, he worked on 30 banking advisory projects in the UK and CIS countries. He has extensiveexperience in all aspects of banking, including lending, risk management, auditing and strategy.He has served on the boards of directors of several other banks and companies in the UK, Armenia, Tajikistan and Kazakhstan.John Staub has worked with several microfinance companies to convert them into banks, including the transformation of Bai Tushum into abank in the Kyrgyz Republic.

Supervisory Board

Company management

Julia DeleskeCFOJulia graduated from the East Siberian State University of Technology and Management (Ulan-Ude) and then began her career in finance. She worked in credit, audit and consulting organizations before joining the National Leasing Company (Micro Capital Group) in 2014, where she acted as financial director. Since 2017, he has been Deputy Chief Financial Officer, first at Mikro Kapital Russia, and then Mikro Kapital.

Svetlana ChubakovaGeneral directorSvetlana has many years of experience working in commercial banks, has diverse banking knowledge, including banking technology, EBRD programs and various approaches to business management. All of Svetlana's work experience is related to servicing SME clients.Svetlana began her career as a trainee in the credit department of one of the regional banks of Yekaterinburg, reaching the position of Director of the Department, Vice President of large federal banks TOP 10 of the Russian Federation.Also, Svetlana is well acquainted with the regional specifics of the development of the financial sector, at different times sheworked in a number of regions of Russia.

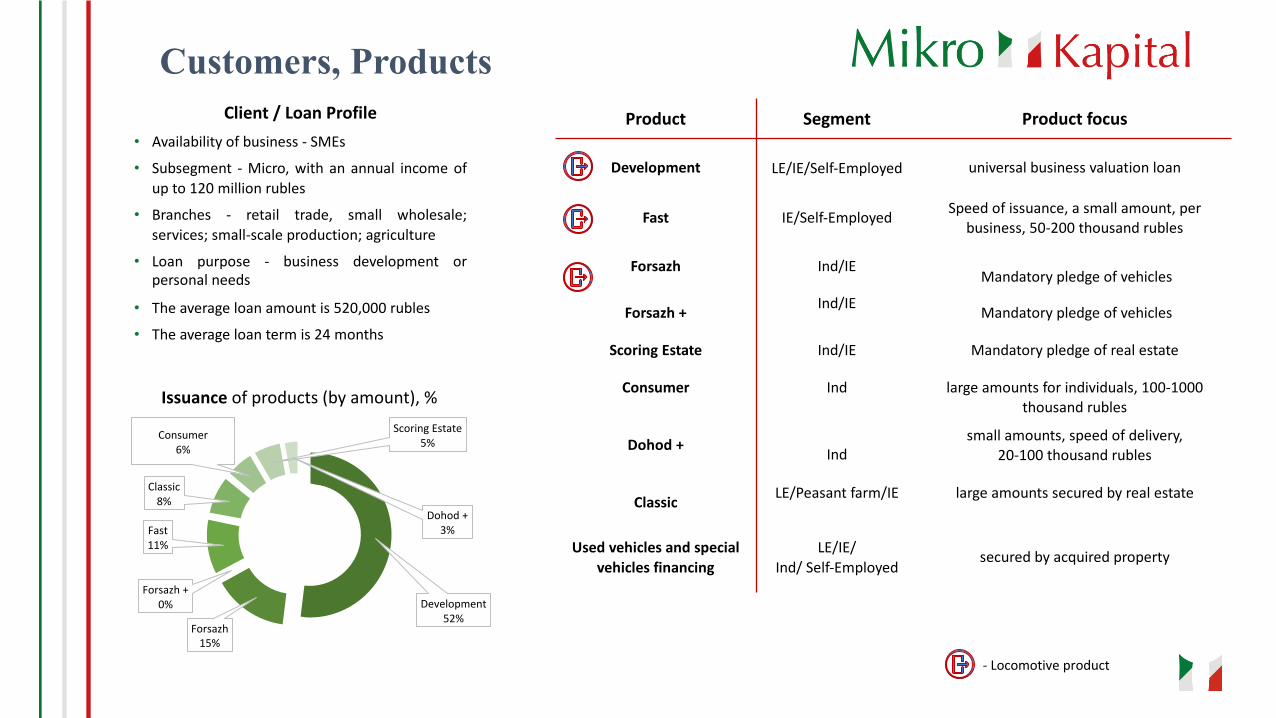

Product Segment Product focus

Development LE/IE/Self-Employed universal business valuation loan

Fast IE/Self-Employed Speed of issuance, a small amount, per business, 50-200 thousand rubles

Forsazh Ind/IEMandatory pledge of vehicles

Forsazh + Ind/IE Mandatory pledge of vehicles

Scoring Estate Ind/IE Mandatory pledge of real estate

Consumer Ind large amounts for individuals, 100-1000 thousand rubles

Dohod + Indsmall amounts, speed of delivery,

20-100 thousand rubles

Classic LE/Peasant farm/IE large amounts secured by real estate

Used vehicles and special vehicles financing

LE/IE/Ind/ Self-Employed

secured by acquired property

Customers, Products

Development52%

Forsazh15%

Forsazh +0%

Fast11%

Classic8%

Consumer6%

Scoring Estate5%

Dohod +3%

Issuance of products (by amount), %

Client / Loan Profile• Availability of business - SMEs

• Subsegment - Micro, with an annual income ofup to 120 million rubles

• Branches - retail trade, small wholesale;services; small-scale production; agriculture

• Loan purpose - business development orpersonal needs

• The average loan amount is 520,000 rubles

• The average loan term is 24 months

- Locomotive product

In assessing the creditworthiness of a borrower at Mikro Kapital we rely on:

• Layered Decision Making

• Comprehensive verification process, which includes analysis of information obtained from open and paid sources, such as a credit bureau, social networks and working with big data

• Anti-fraud checks at all stages of the application

• EBRD loan appraisal technology for lending to SMEs

• Cross validation technology

• Cautious assessment of collateral

Process of issuing and evaluating a loan

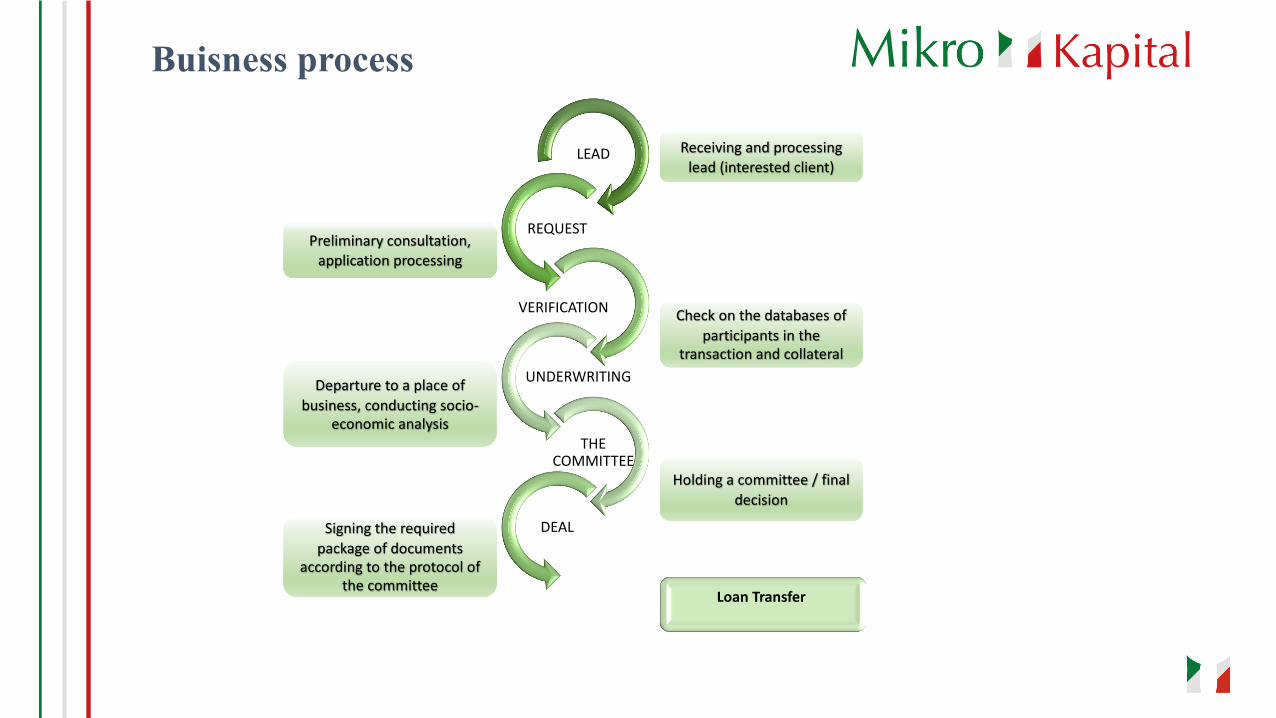

Buisness process

LEAD

REQUEST

VERIFICATION

UNDERWRITING

THE COMMITTEE

DEAL

Loan Transfer

Receiving and processing lead (interested client)

Preliminary consultation, application processing

Check on the databases of participants in the

transaction and collateral

Departure to a place of business, conducting socio-

economic analysis

Holding a committee / final decision

Signing the required package of documents

according to the protocol of the committee

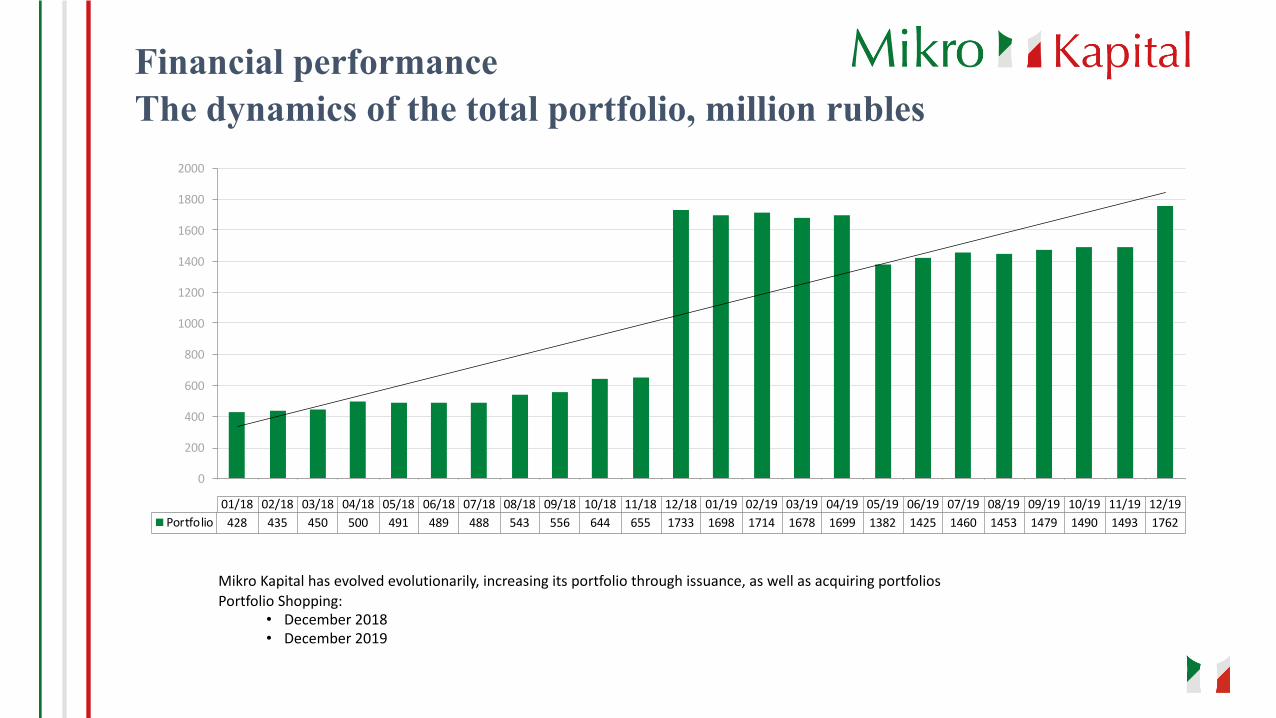

Financial performanceThe dynamics of the total portfolio, million rubles

Mikro Kapital has evolved evolutionarily, increasing its portfolio through issuance, as well as acquiring portfoliosPortfolio Shopping:

• December 2018 • December 2019

0

200

400

600

800

1000

1200

1400

1600

1800

2000

0 1/1 8 0 2/1 8 0 3/1 8 0 4/1 8 0 5/1 8 0 6/1 8 0 7/1 8 0 8/1 8 0 9/1 8 1 0/1 8 1 1/1 8 1 2/1 8 0 1/1 9 0 2/1 9 0 3/1 9 0 4/1 9 0 5/1 9 0 6/1 9 0 7/1 9 0 8/1 9 0 9/1 9 1 0/1 9 1 1/1 9 1 2/1 9

01/18 02/18 03/18 04/18 05/18 06/18 07/18 08/18 09/18 10/18 11/18 12/18 01/19 02/19 03/19 04/19 05/19 06/19 07/19 08/19 09/19 10/19 11/19 12/19Portfolio 428 435 450 500 491 489 488 543 556 644 655 1733 1698 1714 1678 1699 1382 1425 1460 1453 1479 1490 1493 1762

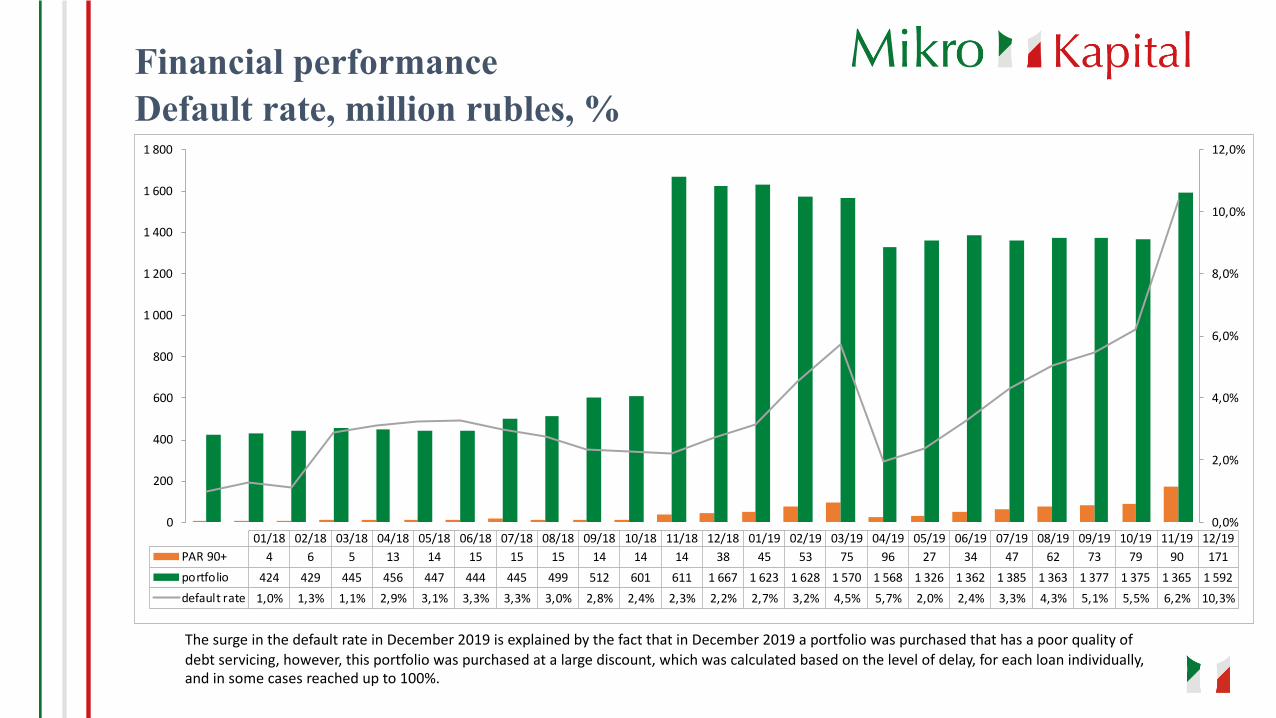

Financial performanceDefault rate, million rubles, %

The surge in the default rate in December 2019 is explained by the fact that in December 2019 a portfolio was purchased that has a poor quality of debt servicing, however, this portfolio was purchased at a large discount, which was calculated based on the level of delay, for each loan individually, and in some cases reached up to 100%.

0

200

400

600

800

1 000

1 200

1 400

1 600

1 800

0,0%

2,0%

4,0%

6,0%

8,0%

10,0%

12,0%

01/18 02/18 03/18 04/18 05/18 06/18 07/18 08/18 09/18 10/18 11/18 12/18 01/19 02/19 03/19 04/19 05/19 06/19 07/19 08/19 09/19 10/19 11/19 12/19PAR 90+ 4 6 5 13 14 15 15 15 14 14 14 38 45 53 75 96 27 34 47 62 73 79 90 171portfolio 424 429 445 456 447 444 445 499 512 601 611 1 667 1 623 1 628 1 570 1 568 1 326 1 362 1 385 1 363 1 377 1 375 1 365 1 592default rate 1,0% 1,3% 1,1% 2,9% 3,1% 3,3% 3,3% 3,0% 2,8% 2,4% 2,3% 2,2% 2,7% 3,2% 4,5% 5,7% 2,0% 2,4% 3,3% 4,3% 5,1% 5,5% 6,2% 10,3%

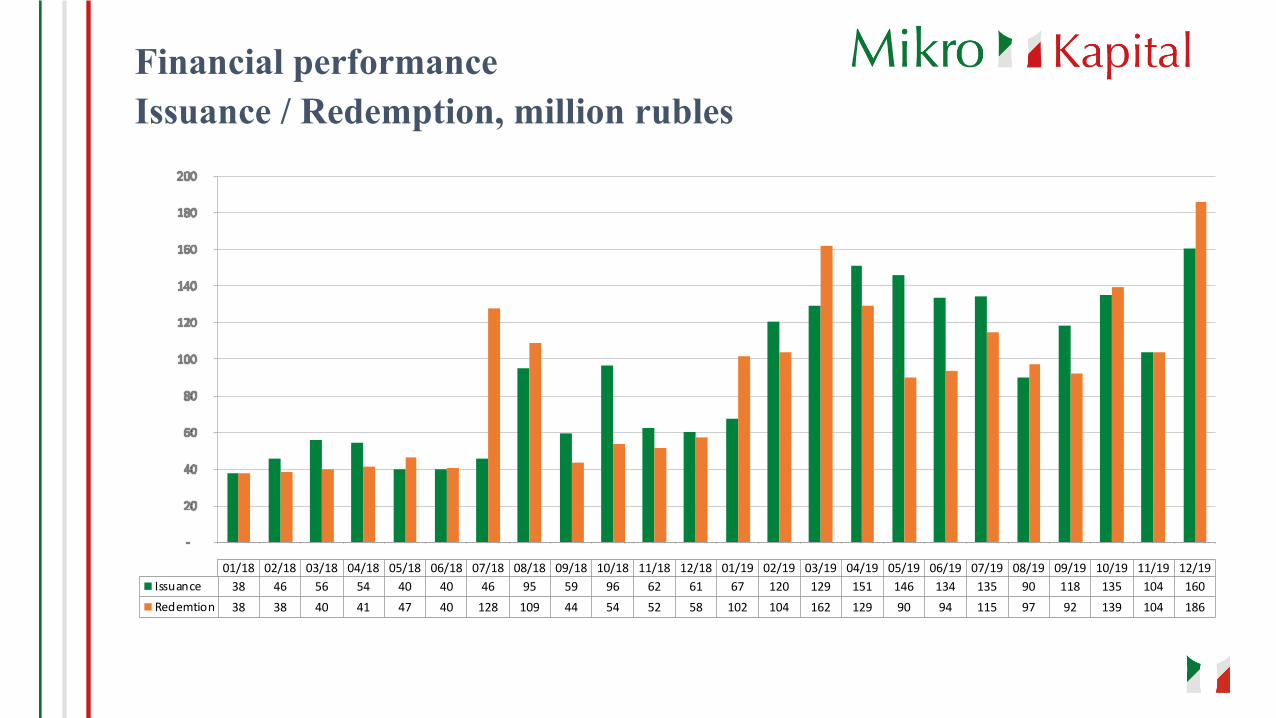

Financial performanceIssuance / Redemption, million rubles

0 1/1 8 0 2/1 8 0 3/1 8 0 4/1 8 0 5/1 8 0 6/1 8 0 7/1 8 0 8/1 8 0 9/1 8 1 0/1 8 1 1/1 8 1 2/1 8 0 1/1 9 0 2/1 9 0 3/1 9 0 4/1 9 0 5/1 9 0 6/1 9 0 7/1 9 0 8/1 9 0 9/1 9 1 0/1 9 1 1/1 9 1 2/1 9

01/18 02/18 03/18 04/18 05/18 06/18 07/18 08/18 09/18 10/18 11/18 12/18 01/19 02/19 03/19 04/19 05/19 06/19 07/19 08/19 09/19 10/19 11/19 12/19Issuance 38 46 56 54 40 40 46 95 59 96 62 61 67 120 129 151 146 134 135 90 118 135 104 160Redemtion 38 38 40 41 47 40 128 109 44 54 52 58 102 104 162 129 90 94 115 97 92 139 104 186

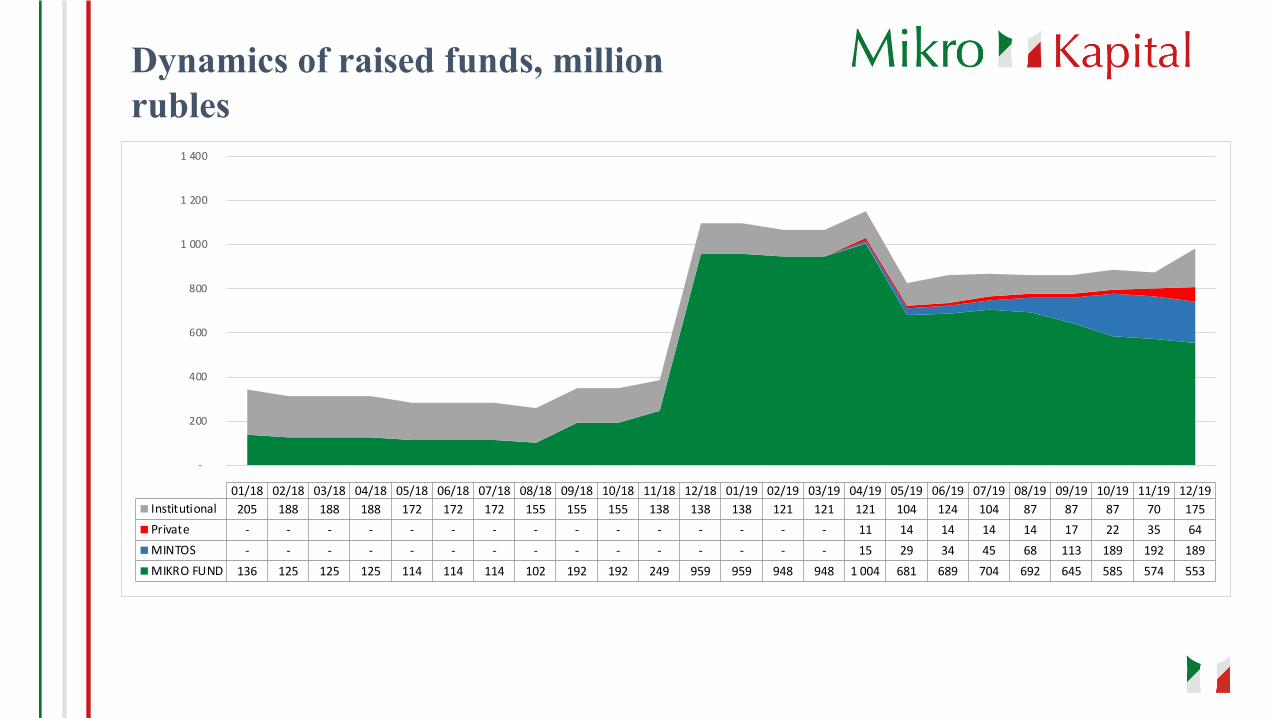

Dynamics of raised funds, million rubles

-

200

400

600

800

1 000

1 200

1 400

0 1/1 8 0 2/1 8 0 3/1 8 0 4/1 8 0 5/1 8 0 6/1 8 0 7/1 8 0 8/1 8 0 9/1 8 1 0/1 8 1 1/1 8 1 2/1 8 0 1/1 9 0 2/1 9 0 3/1 9 0 4/1 9 0 5/1 9 0 6/1 9 0 7/1 9 0 8/1 9 0 9/1 9 1 0/1 9 1 1/1 9 1 2/1 9

01/18 02/18 03/18 04/18 05/18 06/18 07/18 08/18 09/18 10/18 11/18 12/18 01/19 02/19 03/19 04/19 05/19 06/19 07/19 08/19 09/19 10/19 11/19 12/19Institutional 205 188 188 188 172 172 172 155 155 155 138 138 138 121 121 121 104 124 104 87 87 87 70 175Private - - - - - - - - - - - - - - - 11 14 14 14 14 17 22 35 64MINTOS - - - - - - - - - - - - - - - 15 29 34 45 68 113 189 192 189MIKRO FUND 136 125 125 125 114 114 114 102 192 192 249 959 959 948 948 1 004 681 689 704 692 645 585 574 553

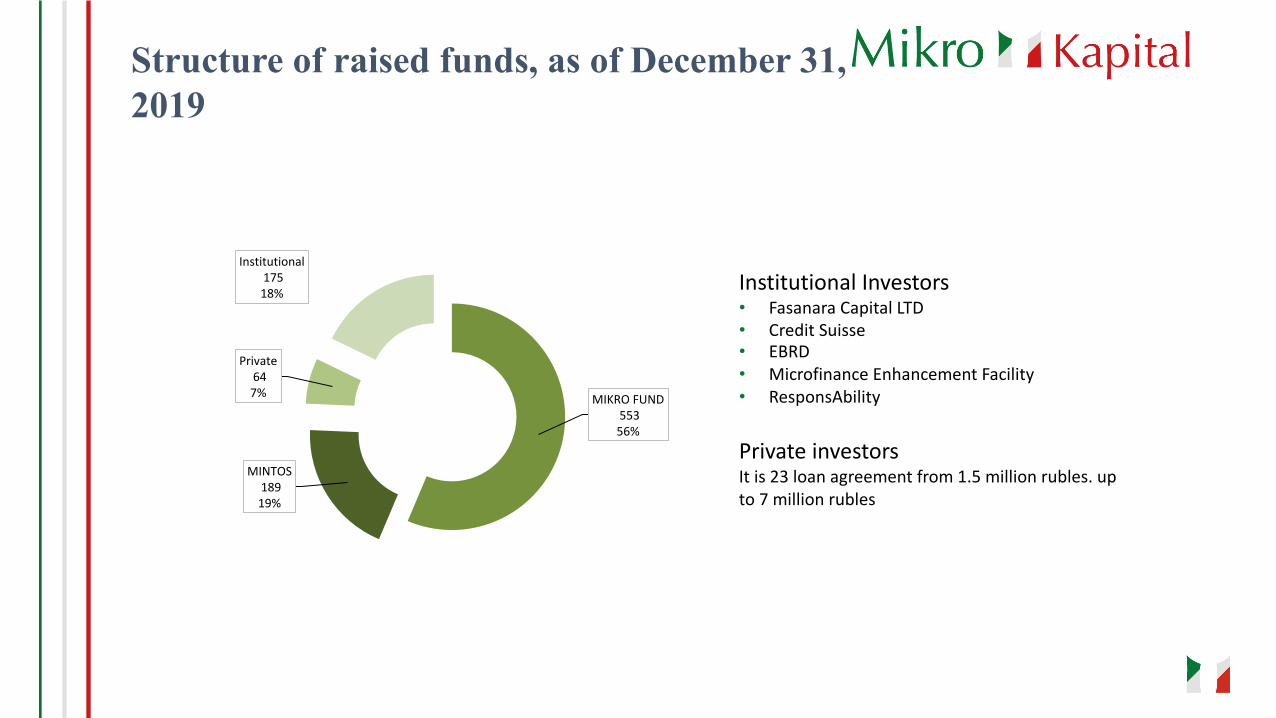

Structure of raised funds, as of December 31, 2019

MIKRO FUND553 56%

MINTOS189 19%

Private64 7%

Institutional175 18% Institutional Investors

• Fasanara Capital LTD • Credit Suisse • EBRD• Microfinance Enhancement Facility• ResponsAbility

Private investorsIt is 23 loan agreement from 1.5 million rubles. up to 7 million rubles

Income, expenses,financial result, million rubles

( 6,0)

( 4,0)

( 2,0)

-

2,0

4,0

6,0

8,0

10,0

12,0

14,0

16,0

-

10,0

20,0

30,0

40,0

50,0

60,0

70,0

0 1/1 8 0 2/1 8 0 3/1 8 0 4/1 8 0 5/1 8 0 6/1 8 0 7/1 8 0 8/1 8 0 9/1 8 1 0/1 8 1 1/1 8 1 2/1 8 0 1/1 9 0 2/1 9 0 3/1 9 0 4/1 9 0 5/1 9 0 6/1 9 0 7/1 9 0 8/1 9 0 9/1 9 1 0/1 9 1 1/1 9 1 2/1 9

01/18 02/18 03/18 04/18 05/18 06/18 07/18 08/18 09/18 10/18 11/18 12/18 01/19 02/19 03/19 04/19 05/19 06/19 07/19 08/19 09/19 10/19 11/19 12/19Income 17,6 16,0 17,6 17,0 17,6 17,1 17,4 17,4 17,4 19,8 20,3 34,5 54,0 50,3 60,1 55,5 52,9 50,2 49,8 53,0 52,4 53,8 50,1 55,6Expenses 15,8 15,2 16,7 15,8 17,1 15,8 16,9 19,2 17,2 18,8 19,8 21,4 51,8 55,1 56,1 51,6 48,9 49,6 48,4 52,8 52,2 53,0 50,0 52,7Financial result 1,8 0,8 0,9 1,2 0,5 1,3 0,5 ( 1,8 0,2 1,0 0,4 13,2 2,2 ( 4,8 4,0 3,9 4,0 0,6 1,5 0,2 0,2 0,8 0,0 2,8

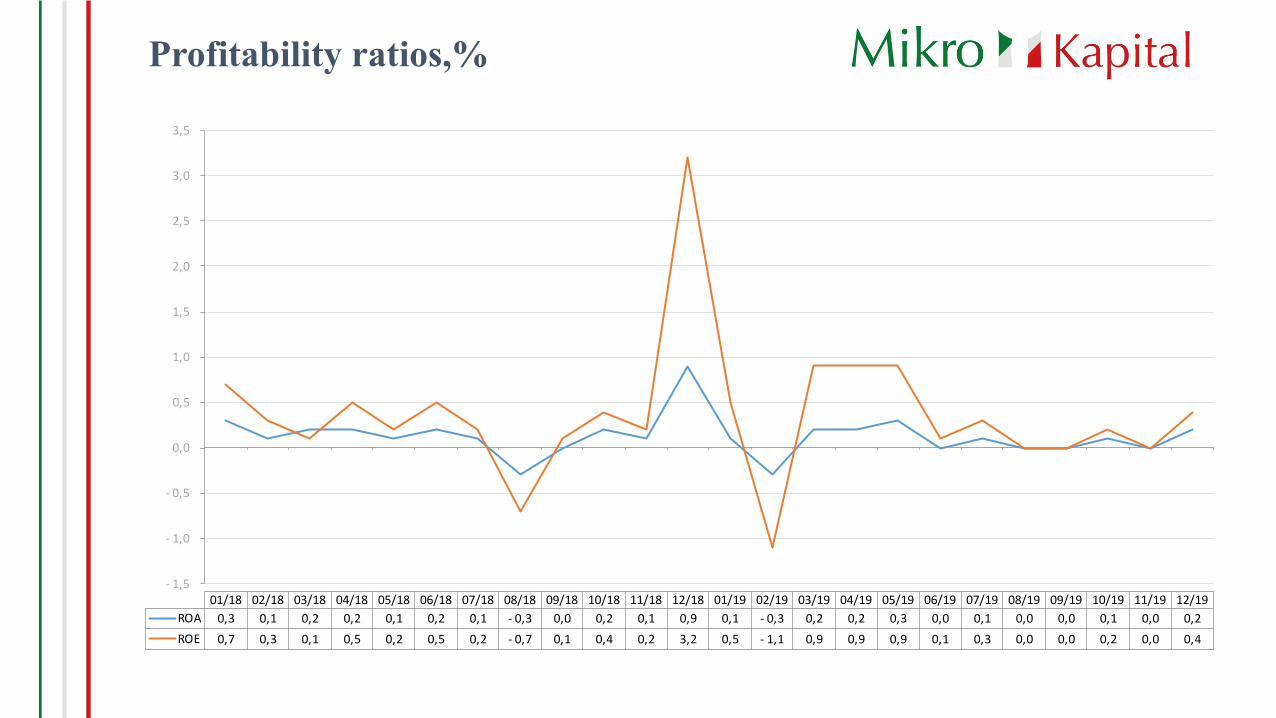

Profitability ratios,%

- 1,5

- 1,0

- 0,5

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

0 1/1 8 0 2/1 8 0 3/1 8 0 4/1 8 0 5/1 8 0 6/1 8 0 7/1 8 0 8/1 8 0 9/1 8 1 0/1 8 1 1/1 8 1 2/1 8 0 1/1 9 0 2/1 9 0 3/1 9 0 4/1 9 0 5/1 9 0 6/1 9 0 7/1 9 0 8/1 9 0 9/1 9 1 0/1 9 1 1/1 9 1 2/1 9

01/18 02/18 03/18 04/18 05/18 06/18 07/18 08/18 09/18 10/18 11/18 12/18 01/19 02/19 03/19 04/19 05/19 06/19 07/19 08/19 09/19 10/19 11/19 12/19ROA 0,3 0,1 0,2 0,2 0,1 0,2 0,1 - 0,3 0,0 0,2 0,1 0,9 0,1 - 0,3 0,2 0,2 0,3 0,0 0,1 0,0 0,0 0,1 0,0 0,2ROE 0,7 0,3 0,1 0,5 0,2 0,5 0,2 - 0,7 0,1 0,4 0,2 3,2 0,5 - 1,1 0,9 0,9 0,9 0,1 0,3 0,0 0,0 0,2 0,0 0,4

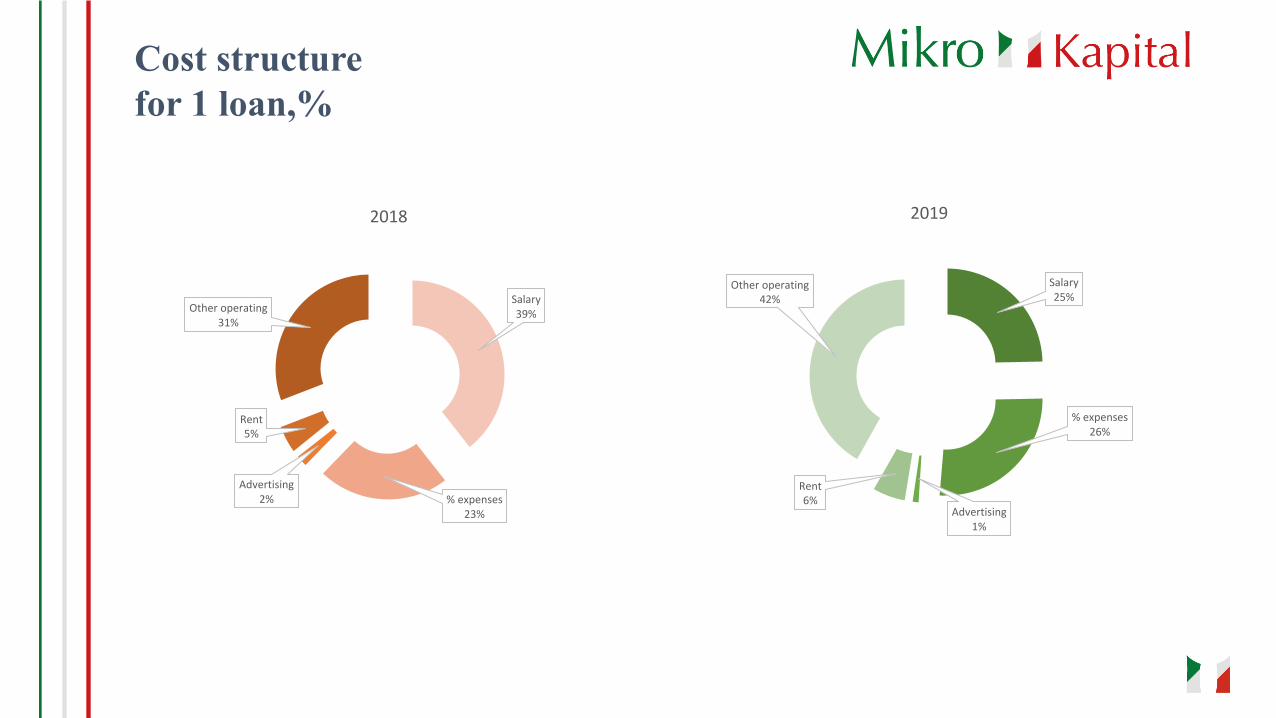

Cost structurefor 1 loan,%

Salary39%

% expenses23%

Advertising2%

Rent5%

Other operating31%

2018

Salary25%

% expenses26%

Advertising1%

Rent6%

Other operating42%

2019

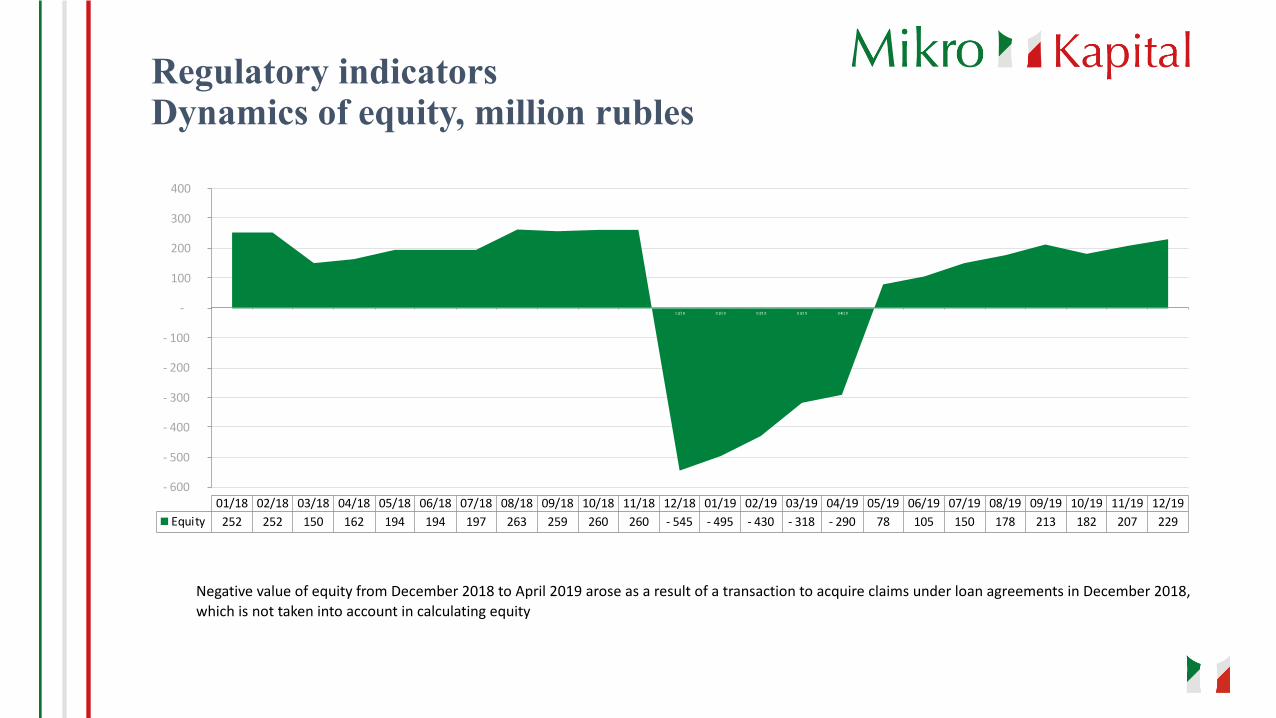

Regulatory indicatorsDynamics of equity, million rubles

Negative value of equity from December 2018 to April 2019 arose as a result of a transaction to acquire claims under loan agreements in December 2018, which is not taken into account in calculating equity

- 600

- 500

- 400

- 300

- 200

- 100

-

100

200

300

400

0 1/1 8 0 2/1 8 0 3/1 8 0 4/1 8 0 5/1 8 0 6/1 8 0 7/1 8 0 8/1 8 0 9/1 8 1 0/1 8 1 1/1 8 1 2/1 8 0 1/1 9 0 2/1 9 0 3/1 9 0 4/1 9 0 5/1 9 0 6/1 9 0 7/1 9 0 8/1 9 0 9/1 9 1 0/1 9 1 1/1 9 1 2/1 9

01/18 02/18 03/18 04/18 05/18 06/18 07/18 08/18 09/18 10/18 11/18 12/18 01/19 02/19 03/19 04/19 05/19 06/19 07/19 08/19 09/19 10/19 11/19 12/19Equity 252 252 150 162 194 194 197 263 259 260 260 - 545 - 495 - 430 - 318 - 290 78 105 150 178 213 182 207 229

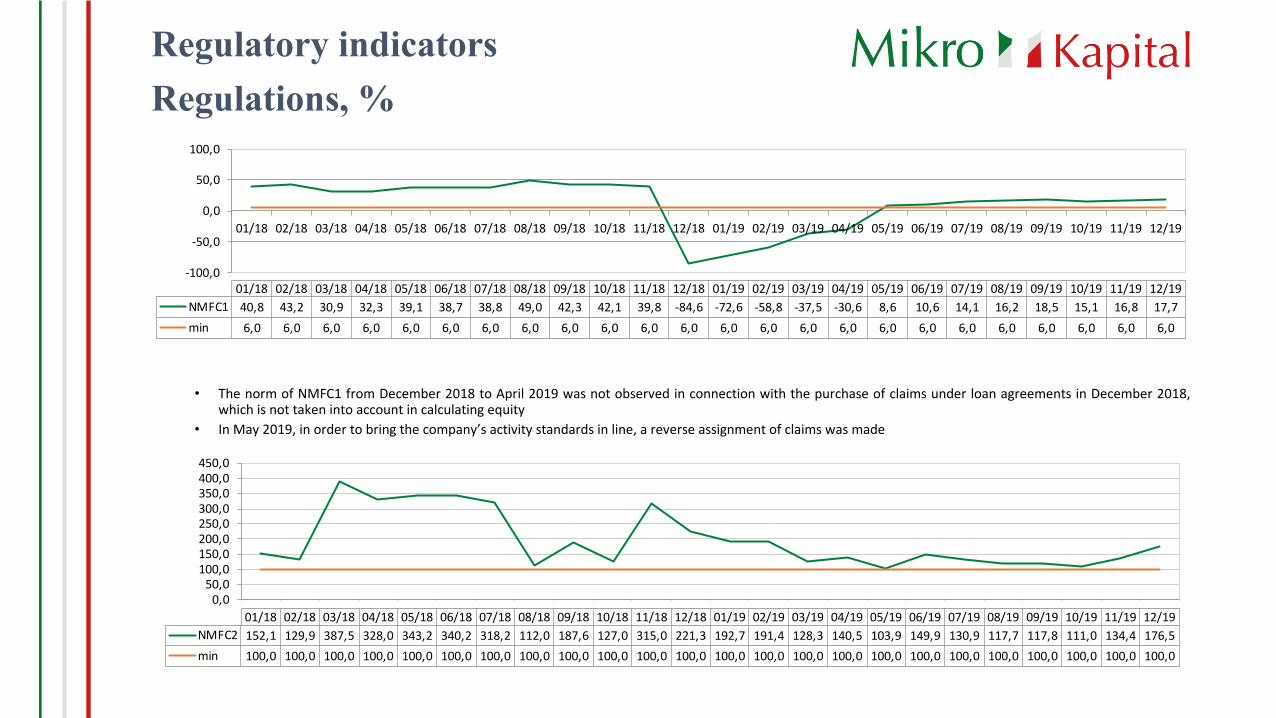

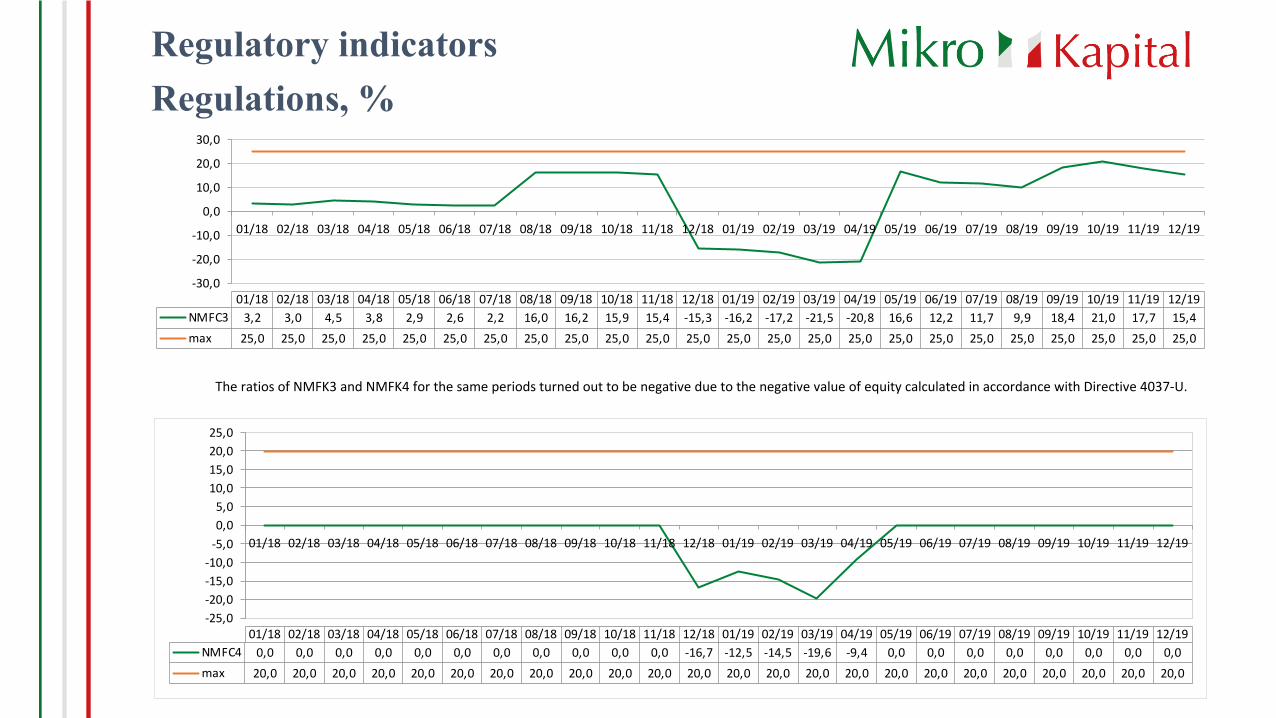

Regulatory indicatorsRegulations, %

• The norm of NMFC1 from December 2018 to April 2019 was not observed in connection with the purchase of claims under loan agreements in December 2018,which is not taken into account in calculating equity

• In May 2019, in order to bring the company’s activity standards in line, a reverse assignment of claims was made

-100,0

-50,0

0,0

50,0

100,0

01/18 02/18 03/18 04/18 05/18 06/18 07/18 08/18 09/18 10/18 11/18 12/18 01/19 02/19 03/19 04/19 05/19 06/19 07/19 08/19 09/19 10/19 11/19 12/19

01/18 02/18 03/18 04/18 05/18 06/18 07/18 08/18 09/18 10/18 11/18 12/18 01/19 02/19 03/19 04/19 05/19 06/19 07/19 08/19 09/19 10/19 11/19 12/19NMFC1 40,8 43,2 30,9 32,3 39,1 38,7 38,8 49,0 42,3 42,1 39,8 -84,6 -72,6 -58,8 -37,5 -30,6 8,6 10,6 14,1 16,2 18,5 15,1 16,8 17,7min 6,0 6,0 6,0 6,0 6,0 6,0 6,0 6,0 6,0 6,0 6,0 6,0 6,0 6,0 6,0 6,0 6,0 6,0 6,0 6,0 6,0 6,0 6,0 6,0

0,050,0

100,0150,0200,0250,0300,0350,0400,0450,0

0 1/1 8 0 2/1 8 0 3/1 8 0 4/1 8 0 5/1 8 0 6/1 8 0 7/1 8 0 8/1 8 0 9/1 8 1 0/1 8 1 1/1 8 1 2/1 8 0 1/1 9 0 2/1 9 0 3/1 9 0 4/1 9 0 5/1 9 0 6/1 9 0 7/1 9 0 8/1 9 0 9/1 9 1 0/1 9 1 1/1 9 1 2/1 9

01/18 02/18 03/18 04/18 05/18 06/18 07/18 08/18 09/18 10/18 11/18 12/18 01/19 02/19 03/19 04/19 05/19 06/19 07/19 08/19 09/19 10/19 11/19 12/19NMFC2 152,1 129,9 387,5 328,0 343,2 340,2 318,2 112,0 187,6 127,0 315,0 221,3 192,7 191,4 128,3 140,5 103,9 149,9 130,9 117,7 117,8 111,0 134,4 176,5min 100,0 100,0 100,0 100,0 100,0 100,0 100,0 100,0 100,0 100,0 100,0 100,0 100,0 100,0 100,0 100,0 100,0 100,0 100,0 100,0 100,0 100,0 100,0 100,0

Regulatory indicatorsRegulations, %

The ratios of NMFK3 and NMFK4 for the same periods turned out to be negative due to the negative value of equity calculated in accordance with Directive 4037-U.

-30,0

-20,0

-10,0

0,0

10,0

20,0

30,0

01/18 02/18 03/18 04/18 05/18 06/18 07/18 08/18 09/18 10/18 11/18 12/18 01/19 02/19 03/19 04/19 05/19 06/19 07/19 08/19 09/19 10/19 11/19 12/19

01/18 02/18 03/18 04/18 05/18 06/18 07/18 08/18 09/18 10/18 11/18 12/18 01/19 02/19 03/19 04/19 05/19 06/19 07/19 08/19 09/19 10/19 11/19 12/19NMFC3 3,2 3,0 4,5 3,8 2,9 2,6 2,2 16,0 16,2 15,9 15,4 -15,3 -16,2 -17,2 -21,5 -20,8 16,6 12,2 11,7 9,9 18,4 21,0 17,7 15,4max 25,0 25,0 25,0 25,0 25,0 25,0 25,0 25,0 25,0 25,0 25,0 25,0 25,0 25,0 25,0 25,0 25,0 25,0 25,0 25,0 25,0 25,0 25,0 25,0

-25,0-20,0-15,0-10,0

-5,00,05,0

10,015,020,025,0

01/18 02/18 03/18 04/18 05/18 06/18 07/18 08/18 09/18 10/18 11/18 12/18 01/19 02/19 03/19 04/19 05/19 06/19 07/19 08/19 09/19 10/19 11/19 12/19

01/18 02/18 03/18 04/18 05/18 06/18 07/18 08/18 09/18 10/18 11/18 12/18 01/19 02/19 03/19 04/19 05/19 06/19 07/19 08/19 09/19 10/19 11/19 12/19NMFC4 0,0 0,0 0,0 0,0 0,0 0,0 0,0 0,0 0,0 0,0 0,0 -16,7 -12,5 -14,5 -19,6 -9,4 0,0 0,0 0,0 0,0 0,0 0,0 0,0 0,0max 20,0 20,0 20,0 20,0 20,0 20,0 20,0 20,0 20,0 20,0 20,0 20,0 20,0 20,0 20,0 20,0 20,0 20,0 20,0 20,0 20,0 20,0 20,0 20,0

Work processwith distressed assets

1. Compliance with the requirements of the Federal Law "On the Protection of the Rights and Legal Interests of Individuals when Carrying Out Activities for the Return of Overdue Debts of July 3, 2016 N 230-ФЗ

2. Multilevel decision making system.

3. Preventive measures to reduce the level of arrears, timely notification of customers about the date of payment repayment.

4. Multi-stage system for working with distressed assets:

• Debt restructuring option (repayment date change, deferred payment)

• the presence of a department for working with overdue debts (lack of collectors, the possibility of pre-trial settlement on an individual basis)

• in the event of a judicial relationship, the ability to sign a settlement at any stage of the process

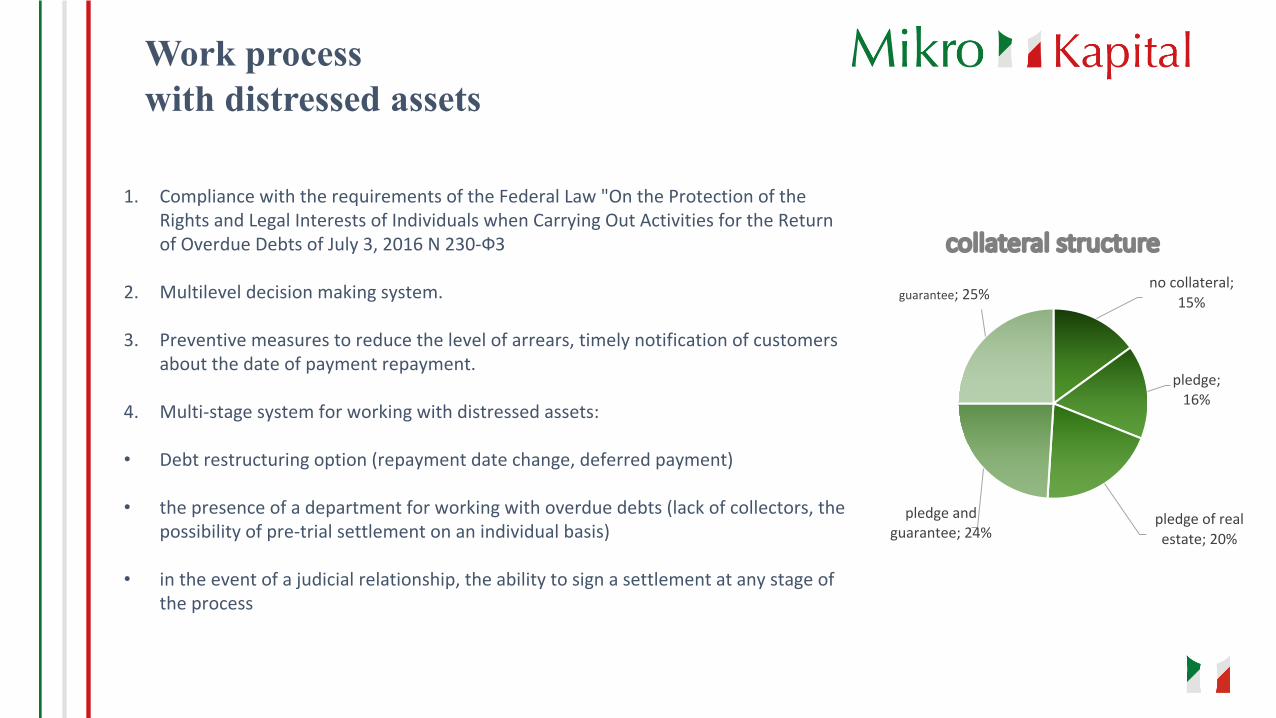

no collateral; 15%

pledge; 16%

pledge of real estate; 20%

pledge and guarantee; 24%

guarantee; 25%

collateral structure

Work processwith distressed assets1. Stage - preventive (0 days delay)Before issuing and at the time of signing the contract. A conversation is being held on the implications of the assumption. Penalties are being clarified.After issue. Informing the client about the upcoming payment. Call, SMS informing.2. Stage - early stage of delay (1-30 days of delay)On day 4, a call is made to find out the reasons for late payment + SMS informing.From 8 to 14, a trip to the Client is carried out with the aim of negotiating, monitoring the Client’s business and assessing the condition of the collateral.From 15 to 30, re-departure, drawing up a protocol of arrangements, delivery of a notice Requirements for the need to pay off debt.3. Stage - the average stage of delay (31-60 days of delay)Based on the information already available, as well as in the presence of certain agreements, an Overdue Debt Committee is held to develop an action plan for the return of the Client to the schedule. Repeated verification. By the decision of the Committee, the Client may be transferred to the Department for work with a distressed asset.4. Stage - Hard CollectionDecisions regarding the Client (restructuring, sale of collateral, filing a claim) are taken by the Committee on arrears. The composition of the Committee is determined depending on the size of the main debt.5. Stage - judicial6. Stage - enforcement proceedings

Development Vectors for 2020

Improving the process of issuing loans

• Differentiated approach to managing client flow (zoning and differentiation of procedures)• Risk management and forecasting through underwriting and portfolio management• Cost and process control• Change of decision making system, subsequent controls• Automation (checks, contracts, etc.)

Product Improvement • Optimization of current products• Search for new customer niches, customer needs• Introducing attractive product terms

Increase in channels of attraction

• Channel diversification• Customer Retention Activities• Analysis and control of each channel

Human Resources • Personal Performance Monitoring• Bonus system reform• Training

• Source:

• Note:

Thank you!

![arXiv:1909.02799v1 [eess.IV] 6 Sep 20194 Moscow Gamma-Knife Center, Moscow, Russia 5 Burdenko Neurosurgery Institute, Moscow, Russia m.belyaev@skoltech.ru Abstract. Stereotactic radiosurgery](https://img.pdfslide.us/doc/110x75/5f97243497bac815b47f8d13/arxiv190902799v1-eessiv-6-sep-2019-4-moscow-gamma-knife-center-moscow-russia.jpg)