Embed Size (px)

Citation preview

1

Mortgage and Protection Induction Course eWorkbook

Version 2.8 June 2018

Name

Course Trainer

Week Commencing

2

Induction Course Agenda

Day 1 – Start 10am Day 2 Day 3 Day 4

Session 1 - Course introduction • Housekeeping• Course Aims and Objectives• Course Agenda / Introductions

Session 2 – Client Outcomes and RightFirst Time

Session 3 – Mortgage and Protection Advice Process • Materials and Systems that support

advice process

Session 4 – Extranet

Session 5 – Introduction and setting the scene

Session 6 - Verifying the identity of your client • Intrinsic identification process• Financial crime

Session 7 - Introduction and setting the scene – 1st • Disclosure

Session 8 – Establishing needs • Know your customer• Factfinds

Session 9 – Supporting documentation and financial crime

Session 10 – Financial Crime case study • Practical exercise

Session 11 – Introduction to Intrinsic systems • Intrinsic systems and how they

interact

Session 12 – XPLAN Part 1 – Adding a Client and adding client details

Session 13 – Priorities and Options • Intrinsic mortgage proposition• Designing the solution

Session 14 – XPM Part 2 – Sourcing software • Topaz

Session 15 - Technical session part 1

Session 16 – Recommendation and next steps • Presenting a solution

Intrinsic advice process gap analysis assessment

Session 17 – Applying to a Lender • Application process• Lender websites

Session 18 – XPM Part 3 – Mortgage Suitability Report • Generating a letter in XPM

Session 19 – XPLAN Part 4 – Submitting of a case • Creating a case for submission to Intrinsic

Session 20 – Buy to Let

Session 21 – XPM – Part 5 – XPM Case study – delegate exercise

Session 22 – State of the protection nation

Session 23 – Protection solutions

Session 24 Intrinsic Protection Panel • Intrinsic Panel• Intrinsic protection benefits

Session 25 – Protection needs analysis and fact-finding

Session 26 – Protection providers and what they offer • Delegate exercise

Session 27 – XPM Part 6 – Adding a protection case to XPM and sourcing

Session 28 - Presenting protection solutions

Session 29 – XPM Part 7 – Submitting a Protection case in XPM

Session 30 – Life Quote protection service • Application service offered by

LifeQuote

Session 31 - Route to Competent Adviser • What happens next?

Session 32 - Course summary

Session 33 – XPM Part 7 – Delegate final exercise • Inputting a protection case into XPM

3

Interactive index for this e-WorkbookInduction Course Agenda ................................................................................. 2

Interactive index for this e-Workbook .................................................... 3

Intrinsic Advice Process - Gap Analysis Assessment ................................ 4

PDP - Initial meeting discussion points ................................................... 5

Session 2 – Client Outcomes and Right First Time ....................................... 6

Session 3 – The Mortgage and Protection advice process ..................... 7

Session 4 – The Extranet .................................................................................... 8

Session 5 – Introduction and Setting the Scene ......................................... 9

Vulnerable Clients Exercise ................................................................... 10

Session 6 – Verifying the identity of your client ........................................ 11

Session 7 – Introduction and Setting the Scene – The First Meeting ... 12

Session 8 – Establishing Client Needs .......................................................... 13

Session 9 – Supporting documentation and financial crime................ 14

Supporting Document and Financial Crime Exercise ............................. 15

Session 10 – Sam Schofield – Case Study Exercise .................................. 16

Session 11 – Introduction to Intrinsic Systems ........................................... 19

Session 12 – XPM – Pt 1 – Adding a client and adding client details . 20

Session 13 – Priorities and Options ............................................................... 21

Session 14 – XPM – Pt 2 – Sourcing Software ............................................. 22

Session 15 – Technical Session ...................................................................... 23

Session 16 – Recommendations and Next Steps ..................................... 24

Advice Process Gap Analysis ........................................................................ 25

Session 17 – Applying to the Lender ............................................................ 26

Session 18 – XPM Pt 3 – Mortgage Suitability Report .............................. 27

Session 19 – XPM Pt 4 – Submission of a Case ......................................... 28

Session 20 – Buy to Let Mortgages ............................................................... 29

Session 21 – XPM Pt 5 – Delegage Buy to Let Exercise .......................... 30

Session 22 – Protection – Introduction and State of Nation .................. 31

Session 23 – Protection Solutions ................................................................. 32

Session 24 – The Intrinsic Protection Propositon ........................................ 33

Session 25 – Protection Needs Analysis and Factfinding ...................... 34

Session 26 – Protection Providers and what they offer ........................... 35

Session 27 – XPM Pt 6 – Adding a Protection case to XPM and Sourcing ........................................................................................................... 36

Session 28 – Presenting Protection Solutions ............................................. 37

Session 29 – XPM Pt 7 – Submitting a Protection Case in XPM ............. 38

Session 30 – Lifequote Protection Service .................................................. 39

Session 31 – Route to Competent Adviser Status ..................................... 40

Session 32 – Course Summary ....................................................................... 41

Session 33 – XPM – Pt 8 – Final XPM Exercise ............................................ 42

APPENDIX ............................................................................................................. 44

Links to useful documents ..................................................................... 44

Links to useful websites & links .............................................................. 46

Video Guides .......................................................................................... 47

INDEX

4

Priorities & Options

Recommendations & Next Steps

Establishing Client Needs GDPR

Introduction & Setting the Scene

Intrinsic Advice Process - Gap Analysis Assessment

On day 3, there will be a gap fill assessment which will be series of multi choice questions designed to determine any gaps in your knowledge. The test will cover topics covered on this course but also the Intrinsic Advice process which you will need to research.

Use the link buttons below which will take you to the various areas of the extranet you need to study. These pages will give you the reading materials upon which the assessment will be based.

My Learning Academy Login Page

Please do not attempt to complete the Gap Analysis Test until instructed to do so by the trainer.

INDEX

5

PDP - Initial meeting discussion points

Which areas do you feel you need initial support/help with?

Document areas you would like to develop further/would like more information on e.g. academies, licences, markets

Details of business plan:Activity following induction – lead source/activity/numbers

Initial clients to contact

First expected advice/sales

INDEX

6

Session 2 – Client Outcomes and Right First Time

INDEX

7

Session 3 – The Mortgage & Protection Advice Process

INDEX

8

Session 4 – The Extranet Find the TERMS OF BUSINESS for Mortgage Planning – RESTRICTED – Intrinsic business

Find the AUTHORITY TO PROCEED for Mortgages Intrinsic / Caerus version

- Download a copy and Save this inyour CLIENTS folder

- Download a copy and Save this inyour CLIENTS folder

Find the RESIDENTIAL MORTGAGES DOCUMENT CHECKLIST in the Mortgage Toolkit

Find the MORTGAGE ADVICE PROCESS – Sales Process document.

- Download a copy and Save this inyour CLIENTS folder

- Download a copy and Save this inyour CLIENTS folder

Hyperlinks & Downloads Intrinsic Advice Standards - Mortgages Intrinsic Advice Process - MortgagesLogin to the Intrinsic

Extranet What does the Intrinsic Advice Standards say about Adviser Remuneration?

When should the Authority to Proceed be dated?

What details of existing arrangements should you capture?

When should the Suitability Report be dated?

What does the advice standards say about product affordability?

When do case documents need to be uploaded to Intrinsic?

INDEX

9

Session 5 – Introduction and Setting the Scene

Hyperlinks & Downloads Aide Memoire verbal disclosure

(handouts) Customer Privacy Notice Initial Enquiry Form Appointment confirmation

email template (handouts) Mortgage Expenditure Form Mortgage Expenditure Form

INDEX

10

Vulnerable Clients Exercise

Instructions: Click the hyperlink above and read the area around vulnerable clients. Once completed answer the questions.

1. At what age would Intrinsic consider any elderly client to be vulnerable?

2. For an inexperienced first-time buyer looking to take out a mortgage, whatshould you remind them if they do not keep up mortgage payments?

3. Intrinsic require all vulnerable clients to have meetings on what basis?

4. What should be offered to all vulnerable clients during a meeting?

Other notes:

INDEX

11

Session 6 – Verifying the identity of your client

Hyperlinks & Downloads Identity requirements matrix

(extranet) Link to the URU ID3 Global site is available at the back

of this workbook in the Useful Websites & Links

section

INDEX

12

Session 7 – Introduction and Setting the Scene – The First Meeting

Hyperlinks & Downloads

1st meeting Agenda Guide to our Mortgage & Protection Services

Terms of Business Borrowing to Buy your Home

Remortgaging your property

Borrowing to invest in rental property

INDEX

13

Session 8 – Establishing Client Needs

Hyperlinks & Downloads James and Vicky

Initial Enquiry Form (handouts)

James and Vicky Factifnd Working Case Study

(download)

James and Vicky Authority to Proceed (handouts)

INDEX

14

Session 9 – Supporting documentation and financial crime

Hyperlinks & Downloads

Certifying documents guidance (extranet)

Certification header sheet (extranet)

Experian report summary (handouts)

Mortgage fraud exercise (handouts)

INDEX

15

Supporting Document and Financial Crime Exercise

Instructions: Click the thumbnail link above and read: • Section 4 Clients Financial Situation• Section 5 Deposits• Section 6 Affordability

1. What evidence of income is required for an individual who is employed andwhat should this be verified against?

2. For a self-employed what is the evidence requirement for SA302’s?

3. What evidence is required for state benefits?

4. What is required as evidence for an employer sponsored pension inpayment?

5. When verifying expenditure what is required?

6. How do you verify a deposit?

7. What do you need to evidence a lump sum deposit?

INDEX

16

Session 10 – Sam Schofield – Case Study Exercise Case Study - Sam Schofield, a 44-year-old pilot, who is moving home

You have completed your first meeting and researched the deals currently available. You have not yet presented a recommendation to Sam. You have the following paperwork:

• Fact Find information• Online Banking - Bank Statements (x3)• Payslips (x3)

You should assume:

• Sam has passed the electronic ID check• You have appropriate ID verification evidence for the lender

(paperwork not included in this pack)

What issues have you noticed? - list each one. Issues related to Financial Crime?

What issues have you noticed? - list each one. Issues related to Affordability?

INDEX

17

Case Study - Sam Schofield, a 44 year old pilot, who is moving home

What issues have you noticed? - list each one. Issues related to Plausibility?

What issues have you noticed? - list each one. Issues related to Intrinsic Advice Process

Fact Find March bank statement

April bank statement May bank statement Wage slip March Wage slip April Wage slip May

INDEX

18

Fact Find Information required

INDEX

19

Session 11 – Introduction to Intrinsic Systems

Hyperlinks & Downl oads

Login to XPM training

INDEX

20

Session 12 – XPM – Pt 1 – Adding a client and adding client details

Hyperlinks & Downloads James & Vicky Case

Documents to Upload Copy the following documents to the James & Vicky Client folder on your desktop:

• Signed Authority to Proceed• 3 months Bank Statements• Mortgage Application form• James Electronic ID• Vicky Electronic ID• Letter confirming Gift• Proof of Deposit• SA302 & Tax overview

Click on the Link above to open the ZIP folder

INDEX

21

Session 13 – Priorities and Options

INDEX

22

Session 14 – XPM – Pt 2 – Sourcing Software

INDEX

23

Session 15 – Technical Session

INDEX

24

Session 16 – Recommendations and Next Steps A

R

C

C

T

T Hyperlinks & Downloads I 2nd Meeting Agenda

C

S

INDEX

25

Advice Process Gap Analysis Development points

1.

2.

3.

4.

5.

6.

7.

8.

INDEX

26

Session 17 – Applying to the Lender

INDEX

27

Session 18 – XPM Pt 3 – Mortgage Suitability Report

Login to XPM training

INDEX

29

Session 19 – XPM Pt 4 – Submission of a Case

Hyperlinks & Downloads Document checklist

Residential Mortgages Intrinsic Advice Standards

(Mortgages)

Login to XPM training

INDEX

30

Session 20 – Buy to Let Mortgages

Hyperlinks & Downloads Mortgage Planning Sales

Processes Buy to let risk

warnings

INDEX

31

Session 21 – XPM Pt 5 – Delegage Buy to Let Exercise

Hyperlinks & Downloads Document checklist

Buy to Let Mortgages

INDEX

32

Session 22 – Protection – Introduction and State of Nation

INDEX

33

Session 23 – Protection Solutions

INDEX

34

Session 24 – The Intrinsic Protection Propositon

INDEX

35

Session 25 – Protection Needs Analysis and Factfinding

Hyperlinks & Downloads LV Risk reality

Calculator James and Vicky Fact FindWorking Case Study p16

Protection disclaimer

Protecting your home

& your Lifestyle Fact Find

INDEX

36

Session 26 – Protection Providers and what they offer

INDEX

37

Session 27 – XPM Pt 6 – Adding a Protection case to XPM and Sourcing

Handouts and Hyperlinks Intrinsic Advice Standards

(Protection)

INDEX

38

Session 28 – Presenting Protection Solutions

A

R

C

C

T

T

I

C

S

INDEX

39

Session 29 – XPM Pt 7 – Submitting a Protection Case in XPM

Handouts and Hyperlinks Protection document

checklist

INDEX

40

Session 30 – Lifequote Protection Service

Case Status Total Charge Any application (life, CI or IP) submitted to Aviva or Old Mutual Wealth that are placed on risk

No Charge

Applications to all other panel providers containing either Critical Illness or Income Protection benefits that go on risk

No Charge

Applications that do NOT go on Risk £25

Life Only cases that are accepted and placed on risk within 7 days of submission £45

Life only cases that are accepted and placed on risk after the first 7 days following submission £85

Please note – these charges apply to RESTRICTED ADVISERS. Different charges apply to INDEPENDENT Advisers

INDEX

41

Session 31 – Route to Competent Adviser Status

INDEX

42

Session 32 – Course Summary

Grading Structure for Advice Process Competency

Unsuitable Based on the documentation submitted, it is not believed the advice given is the most suitable for the client.

Unclear There are ommissions in documentation. Therefore, it has not been possible to determine whether the advice give was suitable or not.

Suitable

The advice is demonstrably the most suitable and there are either no, or only minor documentation errors or ommissions.

INDEX

43

Session 33 – XPM – Pt 8 – Final XPM Exercise

INDEX

44

PDP - Initial meeting discussion points

Which areas do you feel you need initial support/help with?

Document areas you would like to develop further/would like more information on e.g. academies, licences, markets

Details of business plan: Activity following induction – lead source/activity/numbers

Initial clients to contact

First expected advice/sales

INDEX

45

APPENDIX Links to useful documents

Mortgage & Protection Factfind (Extranet)

Document Checklists (Extranet)

Suitability Report Templates (Extranet)

Initial Enquiry form (Extranet)

1st meeting agenda (Extranet)

Follow up Email Appointment Template (Extranet)

Unable to Proceed Template (Extranet)

Borrowing to Buy (Extranet)

Remortgage your property (Extranet)

Borrowing to invest in a rental property (Extranet)

INDEX

46

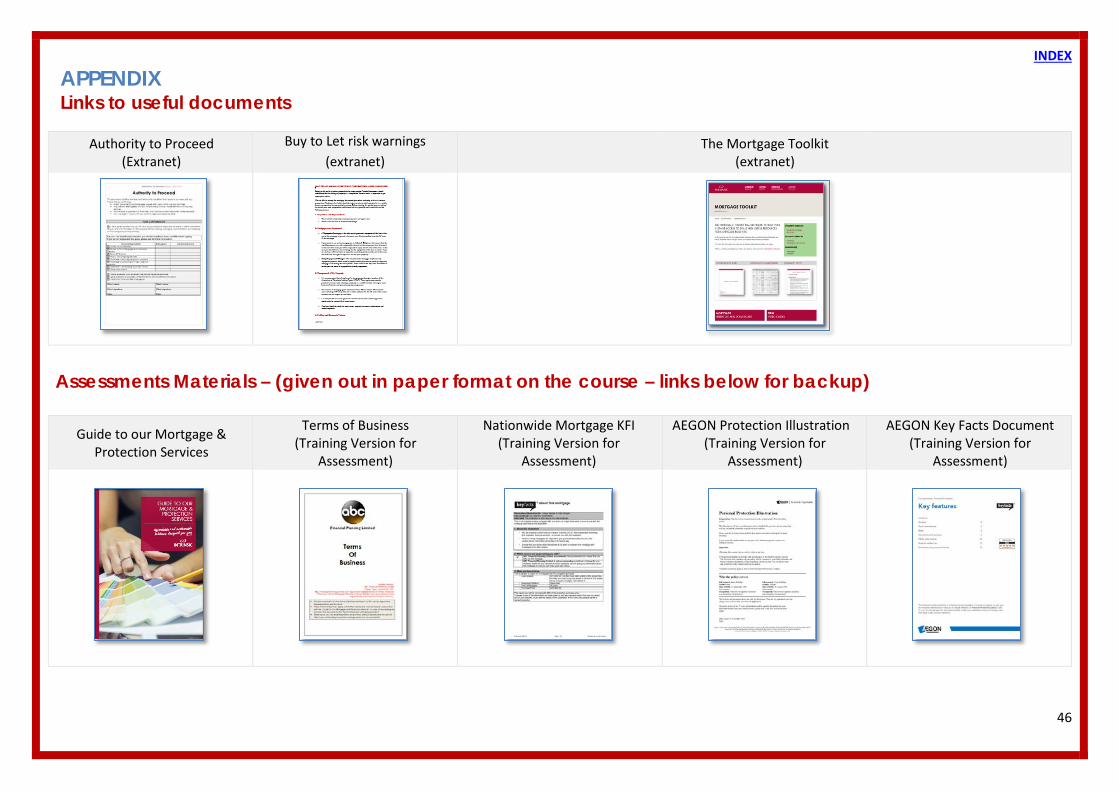

APPENDIX Links to useful documents

Authority to Proceed (Extranet)

Buy to Let risk warnings (extranet)

The Mortgage Toolkit (extranet)

Assessments Materials – (given out in paper format on the course – links below for backup)

Guide to our Mortgage & Protection Services

Terms of Business (Training Version for

Assessment)

Nationwide Mortgage KFI (Training Version for

Assessment)

AEGON Protection Illustration (Training Version for

Assessment)

AEGON Key Facts Document (Training Version for

Assessment)

INDEX

47

Links to useful websites & links

XPM Log in page Intrinsic Extranet Intrinsic Website XPLAN Hub

ID3 Global (URU) Electronic ID LifeQuote Protection Quote Portal

CI Expert Critical Illness Comparisons

Intrinsic Marketing Hub

Risk Reality Calculator & Risk Report

INDEX

47

Video Guides

Mortgage Interview Part 1 - Disclosure

Mortgage Interview Part 2 - Recommendations

XPM Video User Guide Part 1 – Fact Finding & Entering Client details

XPM Video User Guide Part 2 – Creating a Case and Mortgage Sourcing

XPM Video User Guide Part 3 – Completing the Case

Building a Mortgage Suitability Letter

INDEX

48

Video Guides

Manual Sales Process

Course Handouts Sample Email Appointment template

Title: Thank you and follow up.

Dear Sean and Lisa,

Thank you for your enquiry and time {today / yesterday}.

I look forward to progressing matters with you next on {time, day, date}. That meeting typically lasts {length of time}.

Please see attached information that will save you time at the meeting, and reminders of what documentation to supply.

• Agenda for our next meeting: this is a suggestion, so feel free to edit as you see fit• Guide to mortgages and protection: clarifying our process, your protection and any jargon• A budget planner: for you to complete, and supply to us• Map: to find our offices• Biog: a one page summary about me, my experience and qualifications• Factsheet: buying your new home• Factsheet: borrowing to invest in property• Factsheet: re-mortgaging your property

Supporting Documentation you need to supply:

Please supply the relevant documentation as listed below, together with your completed budget planner to save you time in the meeting.

Proof of your identity and address

We support the Proceeds of Crime Act and all efforts to eliminate Money Laundering. As part of this, we need to verify the identity of all our clients. We ask that you provide some original documents containing your name and address.

You must provide at least: • one proof of identity document – e.g. Passport or Driver’s Licence• one proof of address document – e.g. utility bill from the last 3 months

To support your mortgage application You will need to provide:

• last 3 month’s consecutive bank statements• a completed budget planner – showing income and expenditure• deposit – evidence of the source of the deposit (e.g. if from your own savings, then your last 12

month’s savings accounts statements)

You will also need to supply evidence of the following (where relevant to your circumstances):

• A copy of your credit file – see below• Employed - last 3 months payslips (or last 13 week’s payslips) and last P60• Self-employed - last 2 year’s SA302s, or last 2 year’s online SA302s with tax year overview• Current mortgage - your last mortgage statement

INDEX

• State benefits - evidence of any state benefits (letter dated within last 12 months for each benefit)• Pension income - evidence of pension income• Gift of a deposit

o if under £5000, a gifted deposit lettero if over £5000, a gifted deposit letter and evidence of lump sum

• Insurance / assurance – details of your current provisions (e.g. provided through your work orprivate plans) to cover short term illness, accident, redundancy, serious illness (e.g. cancer), death,buildings or contents

Credit file With the increase in identity theft, we strongly recommend you obtain a copy of your own credit report. This is to ensure your application is not delayed by uncovering surprises later in the process. It also means that any issues uncovered can addressed, as it does not mean your application is automatically declined – indeed many lenders have provision for this type of business.

Check the initial and ongoing fees that agencies charge as they can vary. The main agencies to approach are Experian, Equifax, Callcredit, Checkmyfile.

As we are meeting at your home, it would be really useful if you can have copies available with the original documents, as I am unable to take originals away with me.

I look foward to helping you

Your sincerely

{insert name}

INDEX

50

BUY TO LET AS AN INVESTMENT PROPOSITION – RISK WARNINGS

Buying to let can be a serious proposition for some people. Potential borrowers should understand that the letting of property is a complicated business and it is important to get appropriate advice.

We are able to arrange the mortgage but cannot give advice on buying to let as a business proposition. Nothing in this leaflet should be taken to indicate that buying to let is a suitable business proposition for any particular person. Before entering this market you are advised to consult your own independent professional advisers generally and in particular on the following matters.

1. Acquisition and Disposal Costs• These include stamp duty, conveyancing costs and agent’s fees.• There is also the cost of furniture and fittings.

2. Mortgage Loan Repayment• A Repayment mortgage is the only way to guarantee repayment of the loan at the end of the mortgage

term and is the most cost effective method over the full term of the mortgage.

• If you intend to set up the mortgage on an Interest Only basis, this means that the monthly payments areonly repaying the interest on the money you have borrowed; at the end of the term you will be required torepay the full value of the loan. In this case you should have a clear strategy for the repayment of the loan atoutset. If you do not have sufficient funds to repay the outstanding balance at the end of the term the lenderhas the right to repossess and sell your property.

• Early Repayment Charges. The recommended mortgage may have early repayment penalties whichcould be payable should you wish to switch or repay the mortgage in full during the initial period. Pleaserefer to the Key Facts Illustration to ensure you are aware of any penalties on early repayment.

3. Management of the Property• It is recommended that all applicants let the property through a member of the Association of Residential

Letting Agents (ARLA). These agents may provide practical assistance with selecting a property in a suitablelocality, advising on rents, location of tenants and general property management.

• The services of managing agents would cost from 10% to around 15% of annual rents excluding VAT. Veryoften this is taken up-front for the full term of the rental contract and can impact on cash flow.

• It is also possible to insure against loss of rent and to cover related legal costs, which could be around 5% ofannual rents.

• Provision should be made for water rates, property insurance, maintenance and sundry expenses.

4. Political and Economic Factors• Applicants should bear in mind the possibility that rent control for Assured Tenancies could be introduced.

• There could be a fall in the value of the property – past performance is not necessarily a guide to the futureand the value could go down as well as up. In the future, this could mean that your mortgage loan exceedsthe property’s current market value, i.e. you could be in a ‘negative equity’ situation.

• There could be a decrease in rental income due to adverse economic conditions or as a result of asubstantial increase in the supply of rented accommodation in a particular area. Rents will also be affected bythe location and condition of the property.

INDEX

51

• Interest rates could increase on any mortgage taken to acquire the property without a correspondingincrease in rental income to cover the interest.

5. Business and Investment Factors• There could be difficulties with tenants in breach of tenancy agreements, including failure to pay rent and in

obtaining possession under the relevant legislation.

• There may be periods of rental void when the property is not tenanted and so no rent is receivable.

• Investing in a single property can result in a lack of spread which should not usually be contemplated wherethe applicant does not already have a good spread of investments in his or her overall investment portfolio.

• The lower the sum borrowed the more the rental income is likely to exceed the expenses and outgoings.

• It will not normally be in the applicant’s interest to realise, cancel or surrender any existing investment inorder to purchase a property to let.

6. Tax• The disposal of the property may be subject to capital gains tax under current legislation.

• The rental income will be liable to income tax; it may be possible to offset the loan interest against some ofthe rental income when calculating the taxable income.

• Appropriate advice should be obtained from the applicant’s accountant on the taxation of letting a property.

7. Buy To Let Mortgages and Your Rights• The FCA has been responsible for regulating most mortgage sales from 1ST January 2013, however, the FCA

does not regulate certain Buy To Let mortgage sales.

• I can confirm that your mortgage is a Consumer Buy to Let mortgage (CBTL) because {you currently livein/you have previously lived in, in the future you or a relative intend to live in/you have inherited} theproperty. In addition you do not own any other properties that are rented. As such it is regulated by theFCA.

Or • I can confirm that your mortgage is a Business Buy to Let mortgage (BBTL) because you have entered into

this mortgage by way of business. In other words {you bought the property with the intention to rent it outand neither you nor an immediate relative has lived in the property / you have another property that is letout}. As such this mortgage is NOT regulated by the FCA.

This means that you will not be able to take complaints about this type of mortgage to the Financial Ombudsman Service. Additionally, you will not be able to seek redress from the Financial Services Compensation Scheme if your adviser’s firm becomes insolvent.

INDEX

52

Sample Financial Planning Meeting Agenda 1

Framework for our meeting on XX/XX/XXXX @ 11.00 until 1:00pm

Between Sean and Lisa Sample & Andrew Adviser

What do you want to get from the meeting? • Expectations / Experience / Objectives

What do you know about our firm and myself? • Your protection and peace of mind• The type of advice we provide• The marketplace we review for you• The value of our services

How do we deliver solutions to you? • Our advice process• Ensuring you understand all associated fees and costs

Understanding more about your needs • An initial assessment of your ‘wants and needs’• Understanding more about your current provisions and

circumstances• Your lifestyle expectations• Understanding your appetite for risk versus reward

What we can expect from each other? • What we need to do next• Testimonials

{insert firm details – e.g. XXXX is authorised and regulated by the Financial Conduct Authority. Tax advice, estate planning and will writing are not regulated by the Financial Conduct Authority.

Registered in England & Wales, Registered Number: XXXX. Registered address: XXXX / www.XXX / Tel: XXXX / Fax: XXXX.}

INDEX

53

Experian Report example

Status codes Credit score

Status codes

INDEX

54

Initial Enquiry Form example

Information collected and protected under the Data Protection Act

Initial Enquiry Form - Adviser Name: Andrew Adviser Date: XX/XX/XXXX

Client1: James Surname

Client 2: Vicky Surname

DOB: 22/09/19XX (30) DOB: 30/08/19XX (32)

Objectives of enquiry:

Have found a new house and now want to get a mortgage.

Current address:

58 Street, Town, County SN4 0DG

Best contact number: 07878 765765 Best contact number: 01234 123456

E-mail 1:[email protected]

E-mail 2: [email protected]

New Property Existing Property Purchase price: £248,000 Valuation: £NA

Mortgage required: £208,000 Existing mortgage: £

Term required: 25 years Existing lender:

LTV: 84% Redemption penalties: £ Deposit source: savings and gift from

grannie Redemption penalties until:

Purpose of loan: House purchase Repayment type: Repayment Rental income (for BTL / LTB): £ Property type: (house/flat/new build/above commercial/short lease/rent to buy/ex-Local

Authority/other) Client 1 Client 2

Income Details Occupation: Employed/Sole trader/Partner/Other: Time in role: 2 years

Occupation: Employed/Sole Trader/Partner/Other: Time in role:

Basic Salary/net profit: 30/06/XX £61,230 If net profit-last 3 years:30/06/XX £58,834

Basic Salary/net profit:£ If net profit-last 3 years:£

Bonus/Overtime/Dividends/Other Income:£

Bonus/Overtime/Dividends/Other Income:£

Credit History and liabilities Credit cards limit / outstanding: None Credit cards monthly payment: None

Credit cards limit / outstanding: £5,000 / Nil Credit cards monthly payment: £Nil paid off in

Personal loans outstanding: £2,000 Personal loans monthly: £140 per month

Personal loans outstanding: £None Personal loans monthly: £None

INDEX

55

Missed mortgage or other loan repayments?

Missed mortgage or other loan repayments?

Had a CCJ / IVA / Default / Bankruptcy? Had a CCJ / IVA / Default / Bankruptcy?

Notes:

James and Vicky have found a house and want a mortgage to purchase it.

They have been told by close friends that they should be looking at a fixed rate repayment mortgage over 5 years.

To what extent has the client(s) factored the following fees and costs into their planning? Type Applicable? Estimation in £s

Stamp duty Legal fees Land registry Estate agent Removal company Mortgage valuation Property valuation / survey Mortgage lender’s arrangement fee Early repayment fee on existing loan(s) Higher lending charge Mortgage Advice / Implementation fee

Prompts: (tick all discussed) agreement from client for collecting and storing client data in compliance with Data

Protection Act 1998 explicit consent obtained from client for use of electronic ID verification documents the client needs to supply for proof of ID / proof of address budgets / budgetary constraints that the client had in mind the need and benefit of completing a budget planner new property details from estate agent - if applicable copy of latest mortgage statement - if applicable are any clients smokers? source of lead (e.g. referral/introducer)? check that client is either ‘vulnerable/not vulnerable’ – if ‘vulnerable’, follow advice

guidelines mortgage advice fees and what the fee is for next meeting date & time

NB Advice and production of a KFI can only be carried out after completion of a full fact-find – Version 0.6

Financial dependents: Mikey (Son 3) and Vicky (Wife)

Financial dependents:

INDEX

56

Mortgage Fraud Exercise – Scenario 1 – Hidden Residential

The Adviser submitted a buy to let mortgage application for £131,000 on behalf of Mr & Mrs Taylor to XYZ Lender. Mr & Mrs Taylor are both employed, with joint monthly income of £3027 (gross). Their expenditure, supported by bank statements, includes £200 a month for credit cards and £150 for travel to work. The property they’re looking to buy is a 3 bedroom semi-detached house with a purchase price of £272,000.

They’ve explained to the adviser that they’ve raised the capital for the deposit via a further advance on their current residence, which is a 2 bedroom flat, as it had a lot of equity in it. They bought their flat as a new build 3 years ago for £187,500, with the help of a significant gifted deposit. They’ve told the Adviser that they plan to stay in the flat as they love it there, and are buying the house as an investment opportunity.

The application was investigated by the XYZ Lender who determined that Mr & Mrs Taylor were planning to move into the semi-detached house, and the flat had been marketed for sale and subsequently sold. This application was in fact ‘hidden’ residential.

What reasonable steps should the Adviser have taken to assess the plausibility of information provided by Mr & Mrs Taylor?

INDEX

57

Mortgage Fraud Exercise – Scenario 2 – False Income Documentation

Ms Robinson is 38 years old with a young son. She has been employed as an area manager for a supermarket chain for the past 5 and a half years. She is buying her first house, having previously rented, and the Adviser submitted a residential mortgage application to XYZ lender showing Ms Robinsons declared basic income as £34,000 gross a year plus child tax credit. The application also declared no adverse credit or previous mortgage applications. The Adviser included 3 monthly payslips and 3 bank statements with the application.

The application was investigated by the XYZ Lender who determined Ms Robinson had supplied false income documentation. They noted that the payslips showed income paid as cash. The monthly income also did not exactly match the amount shown on the bank statements. In addition, Ms Robinson’s child tax credit amount received on the bank statements did not reflect the total declared income on the application. They also established that Ms Robinson had recently applied for a mortgage elsewhere, which was declined.

What reasonable steps should the Adviser have taken to assess the plausibility of information provided by Ms Robinson?

INDEX

58

Mortgage Fraud Exercise – Scenario 3: False self-employment

The Adviser submitted a residential mortgage application on behalf of Mr Wright who is single with no dependants. The application shows his occupation as a self-employed plumber declared earnings of £39,600 for his last trading year and £38,500 and £40,200 for the preceding 2 years.

The Adviser supplied the lender with an accountant’s letter and explained that the SA302s were to follow once received from the client as Mr Wright was unable to provide them during their meetings. The Adviser noted in his factfind that Mr Wright worked mainly locally on domestic properties.

The application was investigated by the XYZ Lender who determined that this was a case of false employment as they did not receive the SA302s, they were also unable to find any trace of the business. They also established that Mr Wright had 2 unsatisfied CCJs 3 years ago which were not declared on the application.

What reasonable steps should the Adviser have taken to assess the plausibility of information provided by Mr Wright?

INDEX

59

Presentation meeting Agenda - example

Framework for our meeting on XX/XX/XXXX @ 11.00 until 1:00pm

Between James and Vicky Surname & Andrew Adviser

Reconfirming your objectives • Of today’s meeting• Any changes since we spoke? – your objectives, budget, circumstances

Your solution • Checking perceived wants versus needs• What we based our research on• Other options that we decided not included

Checking understanding • Impact of rate changes and your budget• Term – of loan, any initial periods, and tie-ins• Ensuring you understand all associated fees and

costs

Authority to proceed • Completing the application documents• Clarifying the fees• Cancellation rights

What we can expect from each other? • The mortgage journey from here (for us and you)• Managing expectations about things that might not

go to plan• The style and frequency on our ongoing service• Testimonials

{insert firm details – e.g. XXXX is authorised and regulated by the Financial Conduct Authority. Tax advice, estate planning and will writing are not regulated by the Financial Conduct Authority. Registered in England & Wales, Registered Number: XXXX. Registered address: XXXX / www.XXX / Tel: XXXX / Fax: XXXX.}

INDEX

60

Unable to Proceed Email Template Subject Title: Confirmation and follow up

Dear [Forename],

Thank you again for the time you have invested so far in your mortgage journey.

To confirm, my understanding is your application is unable to proceed further with me at this time because:

• You have changed your mind about buying your intended property because [insertreason]

• You have changed your mind about re-mortgaging because [insert reason]• Your current income and expenditure levels are such that we are unable to source a loan

at the level you need• You have not been able to secure a successful offer on your intended property• You have been gazumped• Your application has been rejected by our preferred lender due to your credit score –

please see attached guide to help you address this• Your application has been rejected by our preferred lender due to [insert reason]• Your property valuation has not come back at the level expected• Your rental valuation has not come back at the level expected• You have found another mortgage adviser to progress your application• You are approaching your preferred lender directly• You are unable to provide the required documentation required by our preferred lender• [OTHER?]

I am sorry that I am unable to progress matters further with you at this stage.

I recommend that your next steps are [re apply to another lender / address your credit score etc.]

Please do keep my contact details handy as I look forward to helping you with your next application.

Please be aware that as discussed, I have retained the information you have shared with me which is protected in compliance with Data Protection Act 1998.

We would like to keep in touch with you to keep you informed of products and deals which may be suitable to you as and when they come on to the market. Please see the ‘Express Consent’ form attached for you to sign and return so that we can do this for you.

I will contact you {Insert date} to see how matter are progressing as a matter of courtesy.

Yours sincerely

[Insert name]

INDEX

61

Verbal Disclosure

When speaking to a client for the first time, there are certain areas that must and must not be discussed. All of the points below are based on a verbal client conversation via all formats of communication, e.g. face to face, telephone, skype.

Providing Verbal Disclosure over the Telephone when you first contact a customer, even if this is just to arrange a future appointment you must provide a verbal disclosure by phone.

The statements below cover the areas that you disclose verbally, however when explaining the typical fee you should use the example that you give in your terms of business.

There is an increasing regulatory focus on verbal disclosure, so you will need to put together your own verbal disclosure document script.

You are likely to be asked to demonstrate your verbal disclosure during your annual inspection visit. It is best practice to disclose your mortgage qualifications to the client, so you may wish to add this on to your standard script.

• We offer fully regulated advice on a comprehensive range of mortgages which arerepresentative of the Whole of the Market, but not deals that can only be obtained bygoing direct to a lender.

• I can only provide you with personal advice after we have had the “Fact Find” meeting. Soat this stage I can only provide you with generic information. Please be aware that as I onlyoffer personal advice I will not be able to “order take” or act as an execution only broker.

• We charge a fee of (1% for standard residential mortgages, which on a typical loan size of£150,000 is £1,500. For debt consolidation advice we typically charge a fee of 2%, which ontypical loan size of £100,000 would be £2,000. However this could vary depending onexactly what work we need to do for you, and we will confirm the exact amount during outinitial advice meeting.)

(This is example wording only, you will need to amend this section so that it matches with the fee example in your terms of business).

• We would like to make you aware that there are sometimes alternative finance optionsavailable. For example an existing lender may be able to make a further advance, orprovide a second charge mortgage.

• I will send you a copy of my disclosure documents which give full details. Please see theadditional sections on fees, charges and service levels on the next few pages.

INDEX

64

Initial Enquiry Form example

Information collected and protected under the Data Protection Act

Initial Enquiry Form - Adviser Name: Andrew Adviser Date: XX/XX/XXXX

Client1: James Surname

Client 2: Vicky Surname

DOB: 22/09/19XX (30) DOB: 30/08/19XX (32)

Objectives of enquiry:

Have found a new house and now want to get a mortgage.

Current address:

58 Street, Town, County SN4 0DG

Best contact number: 07878 765765 Best contact number: 01234 123456

E-mail 1:[email protected]

E-mail 2: [email protected]

New Property Existing Property Purchase price: £248,000 Valuation: £NA

Mortgage required: £208,000 Existing mortgage: £

Term required: 25 years Existing lender:

LTV: 84% Redemption penalties: £ Deposit source: savings and gift from

grannie Redemption penalties until:

Purpose of loan: House purchase Repayment type: Repayment Rental income (for BTL / LTB): £ Property type: (house/flat/new build/above commercial/short lease/rent to buy/ex-Local

Authority/other) Client 1 Client 2

Income Details Occupation: Employed/Sole trader/Partner/Other: Time in role: 2 years

Occupation: Employed/Sole Trader/Partner/Other: Time in role:

Basic Salary/net profit: 30/06/XX £61,230 If net profit-last 3 years:30/06/XX £58,834

Basic Salary/net profit:£ If net profit-last 3 years:£

Bonus/Overtime/Dividends/Other Income:£

Bonus/Overtime/Dividends/Other Income:£

Credit History and liabilities Credit cards limit / outstanding: None Credit cards monthly payment: None

Credit cards limit / outstanding: £5,000 / Nil Credit cards monthly payment: £Nil paid off in

Personal loans outstanding: £2,000 Personal loans monthly: £140 per month

Personal loans outstanding: £None Personal loans monthly: £None

INDEX

65

Missed mortgage or other loan repayments?

Missed mortgage or other loan repayments?

Had a CCJ / IVA / Default / Bankruptcy? Had a CCJ / IVA / Default / Bankruptcy?

Notes:

James and Vicky have found a house and want a mortgage to purchase it.

They have been told by close friends that they should be looking at a fixed rate repayment mortgage over 5 years.

To what extent has the client(s) factored the following fees and costs into their planning? Type Applicable? Estimation in £s

Stamp duty Legal fees Land registry Estate agent Removal company Mortgage valuation Property valuation / survey Mortgage lender’s arrangement fee Early repayment fee on existing loan(s) Higher lending charge Mortgage Advice / Implementation fee

Prompts: (tick all discussed) agreement from client for collecting and storing client data in compliance with Data

Protection Act 1998 explicit consent obtained from client for use of electronic ID verification documents the client needs to supply for proof of ID / proof of address budgets / budgetary constraints that the client had in mind the need and benefit of completing a budget planner new property details from estate agent - if applicable copy of latest mortgage statement - if applicable are any clients smokers? source of lead (e.g. referral/introducer)? check that client is either ‘vulnerable/not vulnerable’ – if ‘vulnerable’, follow advice

guidelines mortgage advice fees and what the fee is for next meeting date & time

NB Advice and production of a KFI can only be carried out after completion of a full fact-find – Version 0.6

Financial dependents: Mikey (Son 3) and Vicky (Wife)

Financial dependents:

APPENDIX P Guidance Owner: Data Guardian

PRIVACY NOTICE

Privacy notice 02

CUSTOMER PRIVACY NOTICE At ABC Financial Planning Limited we respect your privacy and the confidentiality of your personal information.

WHO ARE WE? ABC Financial Planning Limited is an appointed representative of Intrinsic Financial Planning Limited who are part of the Quilter Group of companies. For further details on the companies in our group, please visit www.oldmutualwealth.co.uk/about-us/our-wider-business/

This Privacy Notice explains:

• Who we are • What personal information we collect • How we use your personal information • Who we share your information with and why • How we keep your information secure • Your rights • How to contact us

WHO WE ARE ABC Financial Planning Limited provide financial planning solutions and advice through experienced and qualified advisers based in the UK.

Currently ABC Financial Planning Limited and Intrinsic Financial Services jointly determine the purposes and means of processing personal client data relating to giving advice. This means we are joint data controllers for these core advice giving activities and therefore responsible for managing this client data and ensuring compliance.

However, ABC Financial Planning Limited is solely responsible for some activities, for example any direct marketing that we undertake.

Privacy notice 03

WHAT PERSONAL INFORMATION WE COLLECT Personal information includes your name, address, or phone number and other information that is not otherwise publicly available. We collect personal information about you when you contact us about products and services, visit a financial advisor, visit a website we may have or register to receive one of our newsletters (if applicable).

The type of personal information we collect will depend on the purpose for which it is collected and includes:

• Contact details • Information to verify your identity • Family, lifestyle, health and financial information • Payment details.

We collect personal information directly from you. For example, we ask for personal information at the start of our relationship and in subsequent communications in order to check your identity, and protect you from fraud. This is a legal requirement and is important to help safeguard you against potential crime.

SPECIAL CATEGORY INFORMATION In some instances, it is necessary to collect more sensitive information (such as health or lifestyle information) which is called special category data. This is to allow us to provide our financial advice service to you. We will always obtain your consent during the advice process to gather this data and explain what information we require and why it is needed. Sensitive personal information will always be processed and stored securely. You can withdraw your consent at any time to us processing this data, however, this may mean that you can no longer access the service or product the information was gathered for.

COOKIES

We also collect information about you from other sources. For example, our website automatically collects information from your computer using “cookies” which provides us with limited personal information. Cookies are small text files that are placed on your computer by websites that you visit. They are widely used in order to make websites work, or work more efficiently, as well as to provide information to the website owners. For further information visit www.aboutcookies.org or www.allaboutcookies.org.

You can set your browser not to accept cookies and the above websites tell you how to remove cookies from your browser. However, in a few cases some of our website features may not function as a result.

DATA RETENTION

We keep your personal information only as long as is necessary for the purpose for which it was collected and to meet regulatory or legislative requirements. Personal information will be securely disposed of when it is no longer required, in accordance with our Data

Privacy notice 04

Retention and Disposal Schedule. A copy of this is available from the How to Contact Us address, below.

ON WHAT BASIS DO WE COLLECT DATA The processing of your personal data is allowed under a number of lawful basis. The data required for the provision of products and services is processed on the basis there is a contract with you to do so. Any relevant marketing activity we undertake is done because as a firm we have a legitimate interest to do so however you have rights, as listed below, which impact how we can use and process your data.

HOW WE USE YOUR PERSONAL INFORMATION We process your information in order to support and maintain our contractual relationship with you and to comply with legal and regulatory requirements. This includes the following:

• Providing our advice, products or services to you • Carrying out transactions you have requested • Confirming and verifying your identity for security purposes • Credit scoring and assessment, and credit management (where applicable) • Detecting and preventing fraud, crime, money laundering or other malpractice.

We also process your data for specific business purposes to enable us to give you the best products and services and the best and most secure experience. For example, we process your information to send you marketing that is tailored to your interests. Our business purposes include the following:

• Enhancing, modifying, and personalizing our services for the benefit of our customers

• Providing communications which we think will be of interest to you • Market or customer satisfaction research or statistical analysis • Audit and record keeping purposes • Enhancing the security of our network and information systems.

You have the right to object to this processing if you wish, please see “YOUR RIGHTS” section below. Please bear in mind that if you object this may affect our ability to carry out the tasks above for your benefit.

We may also process your personal data as part of an acquisition or sale. Should this happen, you will notified about any change to processing or data controller arising as a result of this activity.

Privacy notice 05

WHO WE SHARE YOUR INFORMATION WITH AND WHY We share your information with trusted third parties who perform tasks for us and help us to provide the services you require these include:

• Intrinsic Financial Services Limited • Other adviser firms in the network for the purpose of providing you with advice (with

your knowledge) • The Quilter Group of companies to enhance the services and products we can offer

you • Third parties to verify your identity, in line with money laundering or other requirements

(this may involve carrying out checks with credit reference databases) • Third parties who perform tasks for us to help us set up or service your plan (these third

parties may be based in countries outside the European Economic Area (EEA) but where they are, we will undertake an assessment of safeguards in place)

• Other organizations, including regulatory bodies, the police and fraud prevention agencies, to prevent and detect fraud

• Third parties where required by law, court order or regulation • Third parties as part of an acquisition or sale.

HOW WE KEEP YOUR INFORMATION SECURE We are committed to ensuring the confidentiality of the personal information that we hold and we continue to review our security controls and related policies and procedures to ensure that your personal information remains secure.

When we contract with third parties, we impose appropriate security, privacy and confidentiality obligations on them to ensure that personal information is kept secure. If we work with third parties in countries outside the EU we ensure these are countries that the European Commission has confirmed have an adequate level of protection for personal information, or the organization receiving the personal data has provided adequate safeguards. In limited circumstances data may be accessed outside of the EEA ie by employees when they travel. In these circumstances we ensure there are appropriate information security measures in place to safeguard your information.

YOUR RIGHTS ABC Financial Planning Limited tries to be as open as it can be in terms of giving people access to their personal information and therefore have outlined your rights below. This privacy notice was drafted with brevity and clarity in mind, therefore further information can be gathered by contacting us using the details below, or more information about

Privacy notice 06

your data protection rights can be found here: https://ico.org.uk/for-organisations/guide-to-the-general-data-protection-regulation-gdpr/individual-rights/

MARKETING You have the right to opt out of marketing information and tell us what your communication preferences are by contacting Intrinsic Financial Services using the details provided at the end of this notice or by using the opt out option below or on any email marketing. You may opt out at any time if you don’t want to receive any further communications of this nature.

INDIVIDUAL DATA RIGHTS AND REQUESTS • the purposes of the processing • The right to be informed – You can request that we provide ‘fair processing

information’, typically through this privacy notice • The right of access - You may request a copy of the personal information we hold

about you using the contact details found on the end of this policy • The right to rectification - The accuracy of your personal information is important to us.

You have the right to ask us to update or correct your personal information • The right to erasure – You may request the deletion or removal of personal data where

there is no compelling reason for its continued processing • The right to object – You may object to the processing of your data based on

legitimate interests • The right to restrict processing - You have a right to request we ‘block’ or suppress

processing of your personal data • The right to data portability – You may request to obtain and reuse your data • The right not to be subject to automated decision-making including profiling. If you wish to correct, restrict, delete or make changes to your personal information, or any of the data subject rights listed above, please contact us at the number/address listed below.

HOW TO CONTACT US If you have questions about this notice, need further information about our privacy practices, or wish to give or withdraw consent, exercise preferences or correct your personal information, please contact us using the following details. ABC Financial Planning Limited will liaise with IFS on your behalf to effect your requests.

The Office of Data Protection Intrinsic Financial Services Limited Wiltshire Court Farnsby Street Swindon SN1 5AH

Telephone: 0161 488 3559

Privacy notice 07

HOW TO COMPLAIN If you wish to raise a complaint about how we have handled your personal data, you can contact The Office of Data Protection who will investigate the matter.

If you are not satisfied with our response or believe we are not processing your personal data in accordance with the law you can complain to our regulator:

Information Governance department Information Commissioner's Office Wycliffe House Water Lane Wilmslow Cheshire SK9 5AF

0303 123 1113

www.ico.org.uk/concerns

CONSENT TO GATHER SPECIAL CATEGORY DATA As detailed above, in some instances, it is necessary for us to collect more sensitive information (such as health or lifestyle information) which is called special category data. This is to allow us to provide our financial advice service to you. This is where we need to gather your consent to the collection and processing of this data. You can withdraw your consent at any time to us processing this data, however, this may mean that you can no longer access the service or product the information was gathered for.

Date……………………………….

By ticking this box you are giving consent for special category personal data to be collected stored in order for your adviser to provide you with a tailored advice service

ELECTRONIC MARKETING We may want to send you relevant marketing electronically from time to time. If you do not wish to receive electronic marketing then please tick the box below to opt out.

I do not wish to receive electronic marketing of relevant products or services

![Pioneer Pdp 434cmx Pdp 43mxe1 s [ET]](https://img.pdfslide.us/doc/110x75/55cf8eae550346703b948a48/pioneer-pdp-434cmx-pdp-43mxe1-s-et.jpg)