Embed Size (px)

Citation preview

Heterotic Risk Models

Zura Kakushadze

Quantigicr Solutions LLC, Stamford, CT, USABusiness School & School of Physics, Free University of Tbilisi, Georgia

(Talk presented at Morgan Stanley, Manhattan)

September 10, 2015

Zura Kakushadze (Quantigic & FreeUni) Heterotic Risk Models September 10, 2015 1 / 20

Outline

1 Factor Models for StocksMotivation: Portfolio OptimizationFactor ModelsStyle & Industry Factors

2 Russian-Doll ConstructionRussian-Doll Risk ModelsExamples“Secret Sauce”

3 Principal Components

4 Heterotic Risk ModelsIndustry Clusters as BlocksRussian-Doll ConstructionTestsTriviaConcluding Remarks

5 References

Zura Kakushadze (Quantigic & FreeUni) Heterotic Risk Models September 10, 2015 2 / 20

Factor Models For Stocks

Motivation: Portfolio Optimization

N stocks: i = 1, . . . ,N

Expected returns: Ri

Optimization: e.g., maximize Sharpe ratio

Vanilla: no constraints, costs, etc.

Dollar holdings: Hi = const.×∑

j C−1ij Rj

Sample cov.mat Cij : singular if M ≡ #(observations) < N + 1

Off-diag Cij : not out-of-sample stable unless M N (diag rel. stable)

Liquid portfolios: N ∼ 1000− 2500

5 years: ∼ 1260 daily observations

Short-holding/ephemeral strats: long lookbacks not desirable/avail

Need: replace sample cov.mat

Zura Kakushadze (Quantigic & FreeUni) Heterotic Risk Models September 10, 2015 3 / 20

Factor Models For Stocks

Factor Models

Factor risk & specific (idiosyncratic) risk:

Ri = χi +∑A

ΩiA fA

Risk factors: fA, A = 1, . . . ,K N

Specific risk cov.mat: Cov(χi , χj) ≡ Ξij = ξ2i δij

Factor risk cov.mat: Cov(fA, fB) ≡ ΦAB

Uncorrelated: Cov(χi , fA) = 0

Model cov.mat Γij ≡ Cov(Ri ,Rj):

Γ = Ξ + Ω Φ ΩT

Φ positive-definite: Γ positive-definite, invertible

Zura Kakushadze (Quantigic & FreeUni) Heterotic Risk Models September 10, 2015 4 / 20

Factor Models For Stocks

Style & Industry Risk Factors

Style factors: stocks’ estimated/measured properties

E.g.: size, value, growth, momentum, volatility, liquidity, etc. (∼< 10)

Short-horizons: 4 (price, momentum, volatility, volume) [ZK, 2015a]

Principal components: eigenvectors of Cij (< #(observations))

Stability: out-of-sample unstable (1st prin.comp most stable)

Industry factors: similarity criterion, stocks’ membership in industries

Industry classification: GICS, ICB, BICS, etc.

Hierarchy, e.g., BICS (others use diff names):

Sector→ Industry→ Sub-Industry→ Ticker

Too many industry factors (sub-ind for BICS): ∼ few hundred

Zura Kakushadze (Quantigic & FreeUni) Heterotic Risk Models September 10, 2015 5 / 20

Russian-Doll Construction

Russian-Doll Risk Models [ZK, 2015b]

Ubiquitous industry factors: too many for short-lookbacks

Calc factor cov.mat: problematic (singular)

Simple idea: model factor cov.mat via a factor model

Repeat until: remaining factor cov.mat can/need not be computed

#(remaining factors): dramatically reduced, even to 1 (variance only)

Zura Kakushadze (Quantigic & FreeUni) Heterotic Risk Models September 10, 2015 6 / 20

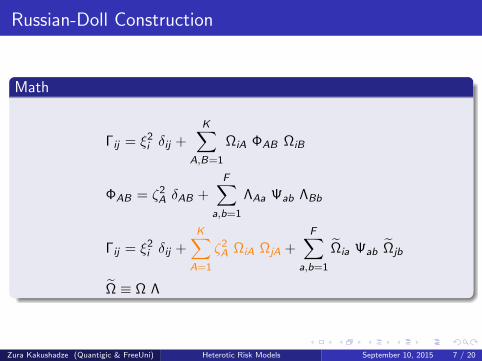

Russian-Doll Construction

Math

Γij = ξ2i δij +K∑

A,B=1

ΩiA ΦAB ΩiB

ΦAB = ζ2A δAB +F∑

a,b=1

ΛAa Ψab ΛBb

Γij = ξ2i δij +K∑

A=1

ζ2A ΩiA ΩjA +F∑

a,b=1

Ωia Ψab Ωjb

Ω ≡ Ω Λ

Zura Kakushadze (Quantigic & FreeUni) Heterotic Risk Models September 10, 2015 7 / 20

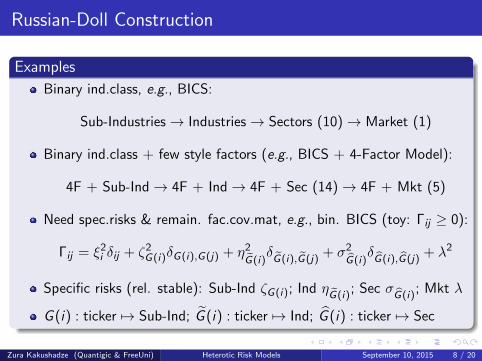

Russian-Doll Construction

Examples

Binary ind.class, e.g., BICS:

Sub-Industries→ Industries→ Sectors (10)→ Market (1)

Binary ind.class + few style factors (e.g., BICS + 4-Factor Model):

4F + Sub-Ind→ 4F + Ind→ 4F + Sec (14)→ 4F + Mkt (5)

Need spec.risks & remain. fac.cov.mat, e.g., bin. BICS (toy: Γij ≥ 0):

Γij = ξ2i δij + ζ2G(i)δG(i),G(j) + η2G(i)

δG(i),G(j)

+ σ2G(i)

δG(i),G(j)

+ λ2

Specific risks (rel. stable): Sub-Ind ζG(i); Ind ηG(i)

; Sec σG(i)

; Mkt λ

G (i) : ticker 7→ Sub-Ind; G (i) : ticker 7→ Ind; G (i) : ticker 7→ Sec

Zura Kakushadze (Quantigic & FreeUni) Heterotic Risk Models September 10, 2015 8 / 20

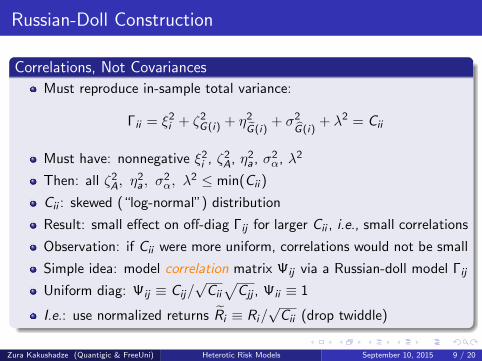

Russian-Doll Construction

Correlations, Not Covariances

Must reproduce in-sample total variance:

Γii = ξ2i + ζ2G(i) + η2G(i)

+ σ2G(i)

+ λ2 = Cii

Must have: nonnegative ξ2i , ζ2A, η2a , σ2α, λ2

Then: all ζ2A, η2a , σ

2α, λ

2 ≤ min(Cii )

Cii : skewed (“log-normal”) distribution

Result: small effect on off-diag Γij for larger Cii , i.e., small correlations

Observation: if Cii were more uniform, correlations would not be small

Simple idea: model correlation matrix Ψij via a Russian-doll model Γij

Uniform diag: Ψij ≡ Cij/√Cii

√Cjj , Ψii ≡ 1

I.e.: use normalized returns Ri ≡ Ri/√Cii (drop twiddle)

Zura Kakushadze (Quantigic & FreeUni) Heterotic Risk Models September 10, 2015 9 / 20

How to Calc Factor Cov.Mat and Spec.Risk?

The “Lore”

Formal ∼ w/ X-sec regression: Ri (ts) = εi (ts) +∑

A βiA(ts)fA(ts)

Identify: βiA(ts) ≡ ΩiA; ΦAB ≡ Cov(fA, fB); ξ2i ≡ Var(εi )

Cov(ε, εT ) = [1− Q] Ψ [1− Q] 6= diag

Γii = ([1− Q] Ψ [1− Q] + Q Ψ Q)ii 6= Ψii

Tr(Γ) = Tr(Ψ)

Q2 = Q ≡ Ω(

ΩT Ω)−1

ΩT

Define: ξ2i ≡ Ψii −∑

A,B ΩiA ΦAB ΩiB?

No: ξ2i 6> 0

“Secret sauce”: prop algos

Zura Kakushadze (Quantigic & FreeUni) Heterotic Risk Models September 10, 2015 10 / 20

Principal Components

Diagonalization

V(A)i : first K prin.comp of Ψij w/ eigenvalues λ(A) (A = 1, . . . ,K )

Factor loadings: ΩiA =√λ(A) V

(A)i

Factor cov.mat: ΦAB = δAB

Γij = ξ2i δij +K∑

A=1

λ(A) V(A)i V

(A)j

ξ2i = 1−K∑

A=1

λ(A)[V

(A)i

]2Γii = Ψii = 1

Limitation: K < #(observations)− 1 (too few for short lookbacks)

Out-of-sample unstable: 1st prin.comp most stable

Zura Kakushadze (Quantigic & FreeUni) Heterotic Risk Models September 10, 2015 11 / 20

Heterotic Risk Models [ZK, 2015c]

Industry Clusters as Blocks

E.g.: clusters = BICS sub-industries (A = 1, . . . ,K ∼ a few hundred)

Ticker-to-cluster map G : i → A (sub-ind)

Factor loadings: ΩiA = Ui δG(i),A (blocks)

“Weights”: Ui = [V (A)]i for stocks i in cluster A (i ∈ J(A))

V (A): first prin.comp of sub.mat [ψ(A)]ij ≡ Ψij |i ,j∈J(A)

Γij = ξ2i δij + Ui Uj ΦG(i),G(j)

ξ2i = 1− λ(G (i)) U2i , λ(A) ≡ max.eigenvalue(ψ(A))

ΦAB =∑

k∈J(A)

∑l∈J(B)

Uk Ψkl Ul ,∑

i∈J(A)

[V (A)]2i = 1

Γii = Ψii = 1

Zura Kakushadze (Quantigic & FreeUni) Heterotic Risk Models September 10, 2015 12 / 20

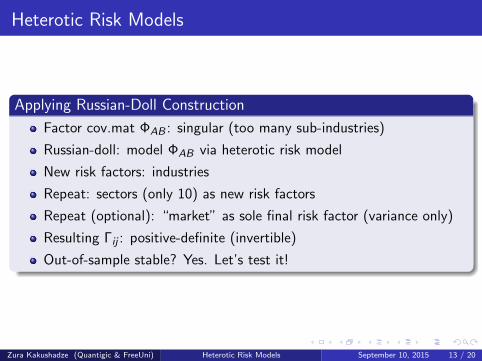

Heterotic Risk Models

Applying Russian-Doll Construction

Factor cov.mat ΦAB : singular (too many sub-industries)

Russian-doll: model ΦAB via heterotic risk model

New risk factors: industries

Repeat: sectors (only 10) as new risk factors

Repeat (optional): “market” as sole final risk factor (variance only)

Resulting Γij : positive-definite (invertible)

Out-of-sample stable? Yes. Let’s test it!

Zura Kakushadze (Quantigic & FreeUni) Heterotic Risk Models September 10, 2015 13 / 20

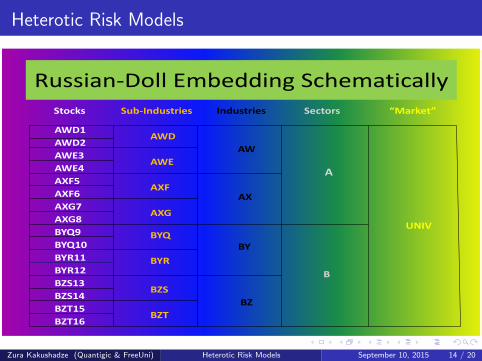

Heterotic Risk Models

Russian-Doll Embedding Schematically

A

B

AW

BZ

BY BYQ

AXF

AXG

AWE

AWD

Stocks Sub-Industries Industries Sectors “Market”

AX

BYR

BZS

BZT

AWD1

AWD2

AWE3

AWE4

AXF5

AXF6

AXG7

AXG8

BYQ9

BYQ10

BYR11

BYR12

BZS13

BZS14

BZT15

BZT16

UNIV

Zura Kakushadze (Quantigic & FreeUni) Heterotic Risk Models September 10, 2015 14 / 20

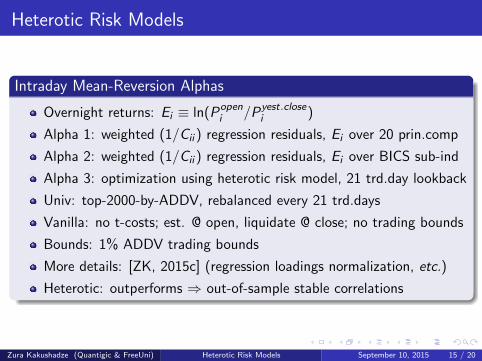

Heterotic Risk Models

Intraday Mean-Reversion Alphas

Overnight returns: Ei ≡ ln(Popeni /Pyest.close

i )

Alpha 1: weighted (1/Cii ) regression residuals, Ei over 20 prin.comp

Alpha 2: weighted (1/Cii ) regression residuals, Ei over BICS sub-ind

Alpha 3: optimization using heterotic risk model, 21 trd.day lookback

Univ: top-2000-by-ADDV, rebalanced every 21 trd.days

Vanilla: no t-costs; est. @ open, liquidate @ close; no trading bounds

Bounds: 1% ADDV trading bounds

More details: [ZK, 2015c] (regression loadings normalization, etc.)

Heterotic: outperforms ⇒ out-of-sample stable correlations

Zura Kakushadze (Quantigic & FreeUni) Heterotic Risk Models September 10, 2015 15 / 20

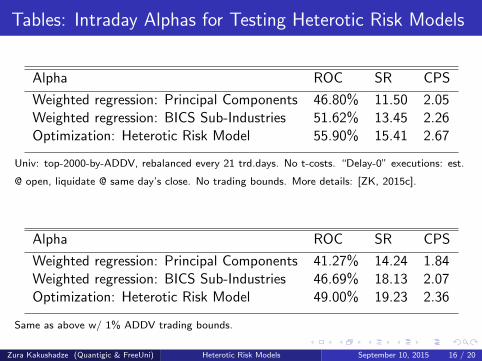

Tables: Intraday Alphas for Testing Heterotic Risk Models

Alpha ROC SR CPS

Weighted regression: Principal Components 46.80% 11.50 2.05Weighted regression: BICS Sub-Industries 51.62% 13.45 2.26Optimization: Heterotic Risk Model 55.90% 15.41 2.67

Univ: top-2000-by-ADDV, rebalanced every 21 trd.days. No t-costs. “Delay-0” executions: est.

@ open, liquidate @ same day’s close. No trading bounds. More details: [ZK, 2015c].

Alpha ROC SR CPS

Weighted regression: Principal Components 41.27% 14.24 1.84Weighted regression: BICS Sub-Industries 46.69% 18.13 2.07Optimization: Heterotic Risk Model 49.00% 19.23 2.36

Same as above w/ 1% ADDV trading bounds.

Zura Kakushadze (Quantigic & FreeUni) Heterotic Risk Models September 10, 2015 16 / 20

Figure: Intraday Alphas for Testing Heterotic Risk Models

0 200 400 600 800 1000 1200

0e+

001e

+07

2e+

073e

+07

4e+

075e

+07

Trading Days

P&

L

Bottom-to-top-performing: i) weighted regression over principal components, ii) weighted

regression over BICS sub-industries, and iii) optimization using heterotic risk model. Investment

level: $10M long plus $10M short.

Zura Kakushadze (Quantigic & FreeUni) Heterotic Risk Models September 10, 2015 17 / 20

Heterotic Risk Models

Some Trivia

Name: inspired by “heterotic string theory”, no other connection

“Heterotic”: adjective from “heterosis”, per Merriam-Webster:“the marked vigor or capacity for growth often exhibitedby crossbred animals or plants – called also hybrid vigor”

Coined: plant geneticist G.H. Shull, 1914, well before string theory. . .

Heterosis – Powerful Approach [1,200+ SSRN downloads]

Granularity of industry classification

Diagonality of prin.comp cov.mat for any sub-cluster

Dramatic reduction of factor cov.mat size in Russian-doll models

Disclaimer: [ZK, 2015c] provides complete algo and source code

Next? General risk model. . .

Zura Kakushadze (Quantigic & FreeUni) Heterotic Risk Models September 10, 2015 18 / 20

References

ZK (2015a) 4-Factor Model for Overnight Returns. Wilmott Magazine(Forthcoming, Sept 2015); http://ssrn.com/abstract=2511874 (October 19, 2014).

ZK (2015b) Russian-Doll Risk Models. Journal of Asset Management 16(3):170-185; http://ssrn.com/abstract=2538123 (December 14, 2014).

ZK (2015c) Heterotic Risk Models. Wilmott Magazine (Forthcoming);http://ssrn.com/abstract=2600798 (April 30, 2015).

Zura Kakushadze (Quantigic & FreeUni) Heterotic Risk Models September 10, 2015 19 / 20

The End

Thank you!

Zura Kakushadze (Quantigic & FreeUni) Heterotic Risk Models September 10, 2015 20 / 20