Embed Size (px)

Citation preview

b

Marcello Milman (55 21 3212 3202) [email protected]

MORE THAN JUST A CYCLE

SWING…

BRAZIL

Espí

rito

Sant

o R

esea

rch

February, 2006 SECTOR: PETROCHEMICAL

Enticing valuations, but sluggish spreads’s improvment

and BRL strengh suggest caution in the short term

1

PETROQUEMICAL SECTOR: “More than just a cycle swing...”

Enticing valuations, but sluggish spread’s improvement and BRL strength suggest caution in the short term

General Index:

1. EXECUTIVE SUMMARY .............................................................. 02

2. PETROCHEMISTRY: FROM CRUDE OIL TO FINAL CONSUMER. 05

3. GLOBAL OUTLOOK: CLIMBING THE FLY UP........................... 12

4. DOMESTIC OUTLOOK: CONSUMPTION POISED TO GROW... 23

5. SECTOR CONFIGURATION IN BRAZIL AND LATIN AMERICA 27

6. CONSOLIDATION: WHERE IS THE HEADING........................... 38

7. ES RESEARCH FORECASTS..................................................... 43

8. COMPANIES............................................................................. 46

Braskem.................................................................................................. 47

Copesul................................................................................................... 50

Suzano Petroquímica............................................................................. 53

Petroflex.................................................................................................. 56

Ultrapar........................................................................ .......................... 59

9. APPENDIX.................................................................................... 62

Marcello Milman (55 21 3212 3202) [email protected]

2

Petrochemical Sector, Feb-06

1. EXECUTIVE SUMMARY In this report we try to provide investors, whether they have minimal or extensive previous knowledge of the sector, with an overall view of the petrochemical industry. It goes beyond a simple discussion of the cycle in order to enrich our industry’s coverage. We emphasize the sector’s key features in Brazil, such as: leading companies, corporate structures, growth strategies, production capacities, and market stance on each of main products. We reckon the sector to have an increased relevance on investors’ radars in the coming years. Therefore, the time is ripe to present our views on the consolidation process that the industry may (and should) undergo, as well as our assessment of the cycle, given rencent numerous diverging arguments surrounding the fly-up, which have been impacting the performance of the sector’s shares.

Over the course of our analysis, we elaborate the following issues:

♦ The cyclical nature of the industry, with peaks (denominated fly-ups) influenced by escalations in global capacity utilization rates, and duration of 7-10 years. Our estimates indicate that operating rates remain north of 90% until 2008E, supporting a extended upcycle view, in part propelled by China’s continued net importer position. We thus look for PE/naphtha spreads over the US$600/ton mark by 2008E (vs. US$448/ton in 2003) and for those of PP to inch even higher;

♦ The profitability peak of this current cycle will likely be less pronounced due to the high price of crude oil, which raises end-product prices (suppressing demand), to the structural reduction in the industry’s average cash cost (greater role of Asian producers), and to the (ill a bit unknown) expansion of the secondary market, also indirectly benefited by soaring crude prices;

♦ This positive global scenario shall be magnified in the domes tic market, where economic development and the still low penetration of resin consumption set the stage for robust sales growth potential. As price takers, domestic companies tend to align their prices in the medium term, charging a 15-20% premium on import parity that helps them make up for higher costs of capital. An unrelenting appetite for expansion is one of key the risks (especially in the PE market) as of 2008E, if most of the planned investment is carried out;

♦ In section 5, we present a description of the sector in Brazil (and in Latin America), listing the major players in each market, commercial trade flows, and details of the leading companies.

♦ It is important to highlight that, particularly in second generation, the domestic industry is still very fragmented, as a legacy of its inception (and privatization). However, consolidation is widely expected, and its first steps have already been taken. We identify Braskem as a leader in this shift: it could take the wheels at Politeno (by severing cross-held ownership with Suzano Petroquímica), and, even more importantly, the Southern Complex could be consolidated if setbacks with Ipiranga can be solved. Suzano Petroquímica is also poised to take a solid role in this process, after having incorporated Polibrasil, possibly stablishing its postion in Petroflex, as well as negotiate with Unipar;

♦ The final part of our report presents a summary of our estimates for the companies covered and discusses some key drivers for the equity markets, as well as specific risks for each business;

♦ Additionally, we have elaborated charts and tables (on page 4 and in the annex), aimed to serve as consultancy base by those seeking to follow the sector more closely.

In terms of trading ideas, we recommend that investors a market weight positions, owing chiefly to the appreciating currency. The BRL rise should continue to impact the companies overall during 2006 (particularly in 1H06), offsetting the benefits of the pick-up in international margins. Beginning in the second half of the year (possibly a little sooner), shares should start reacting to the gradual slide of oil prices, stronger domestic sales volumes, and stabilization of the FX curve.

For those willing to invest in the sector, our top pick is Suzano Petroquímica. We also

3

Petrochemical Sector, Feb-06

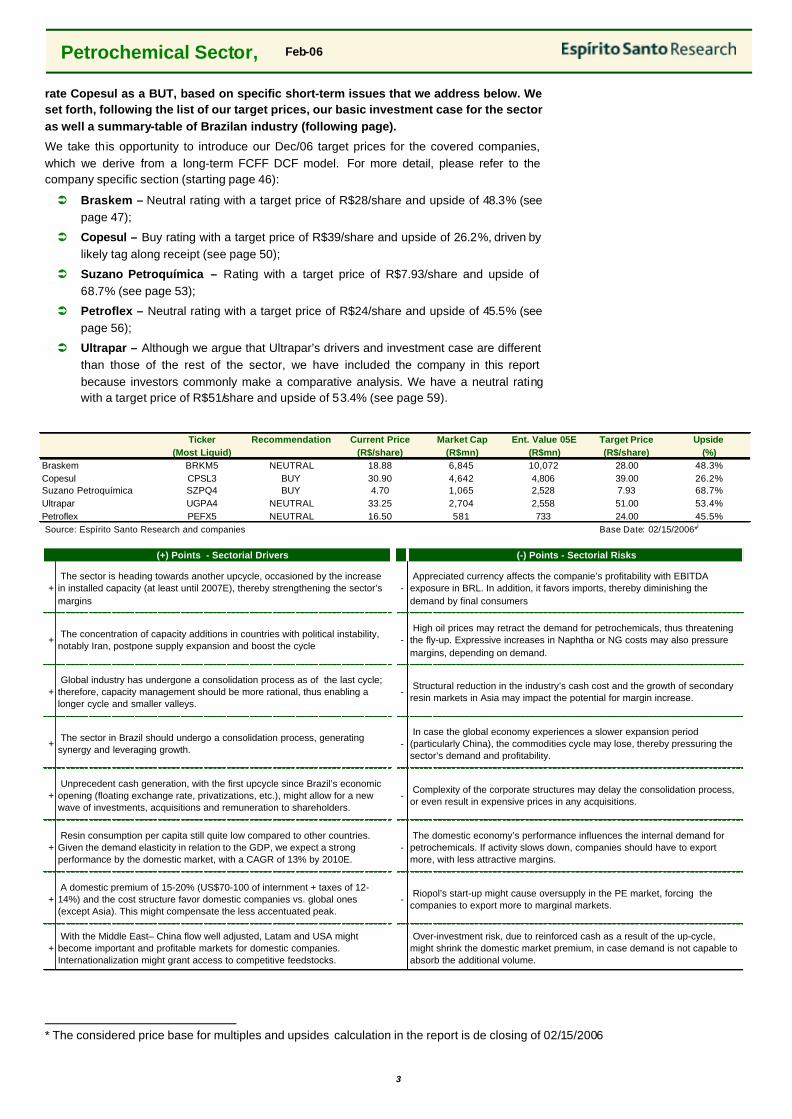

rate Copesul as a BUT, based on specific short-term issues that we address below. We set forth, following the list of our target prices, our basic investment case for the sector as well a summary-table of Brazilan industry (following page).

We take this opportunity to introduce our Dec/06 target prices for the covered companies, which we derive from a long-term FCFF DCF model. For more detail, please refer to the company specific section (starting page 46):

Ü Braskem – Neutral rating with a target price of R$28/share and upside of 48.3% (see page 47);

Ü Copesul – Buy rating with a target price of R$39/share and upside of 26.2%, driven by likely tag along receipt (see page 50);

Ü Suzano Petroquímica – Rating with a target price of R$7.93/share and upside of 68.7% (see page 53);

Ü Petroflex – Neutral rating with a target price of R$24/share and upside of 45.5% (see page 56);

Ü Ultrapar – Although we argue that Ultrapar’s drivers and investment case are different than those of the rest of the sector, we have included the company in this report because investors commonly make a comparative analysis. We have a neutral rating with a target price of R$51/share and upside of 53.4% (see page 59).

Ticker Recommendation Current Price Market Cap Ent. Value 05E Target Price Upside(Most Liquid) (R$/share) (R$mn) (R$mn) (R$/share) (%)

Braskem BRKM5 NEUTRAL 18.88 6,845 10,072 28.00 48.3%Copesul CPSL3 BUY 30.90 4,642 4,806 39.00 26.2%Suzano Petroquímica SZPQ4 BUY 4.70 1,065 2,528 7.93 68.7%Ultrapar UGPA4 NEUTRAL 33.25 2,704 2,558 51.00 53.4%Petroflex PEFX5 NEUTRAL 16.50 581 733 24.00 45.5%Source: Espírito Santo Research and companies Base Date: 02/15/2006*i

(+) Points - Sectorial Drivers (-) Points - Sectorial Risks

+ The sector is heading towards another upcycle, occasioned by the increase in installed capacity (at least until 2007E), thereby strengthening the sector’s margins

- Appreciated currency affects the companie’s profitability with EBITDA exposure in BRL. In addition, it favors imports, thereby diminishing the demand by final consumers

+ The concentration of capacity additions in countries with political instability, notably Iran, postpone supply expansion and boost the cycle

- High oil prices may retract the demand for petrochemicals, thus threatening the fly-up. Expressive increases in Naphtha or NG costs may also pressure margins, depending on demand.

+ Global industry has undergone a consolidation process as of the last cycle; therefore, capacity management should be more rational, thus enabling a longer cycle and smaller valleys.

- Structural reduction in the industry’s cash cost and the growth of secondary resin markets in Asia may impact the potential for margin increase.

+ The sector in Brazil should undergo a consolidation process, generating synergy and leveraging growth.

- In case the global economy experiences a slower expansion period (particularly China), the commodities cycle may lose, thereby pressuring the sector’s demand and profitability.

+ Unprecedent cash generation, with the first upcycle since Brazil’s economic opening (floating exchange rate, privatizations, etc.), might allow for a new wave of investments, acquisitions and remuneration to shareholders.

- Complexity of the corporate structures may delay the consolidation process, or even result in expensive prices in any acquisitions.

+ Resin consumption per capita still quite low compared to other countries. Given the demand elasticity in relation to the GDP, we expect a strong performance by the domestic market, with a CAGR of 13% by 2010E.

- The domestic economy’s performance influences the internal demand for petrochemicals. If activity slows down, companies should have to export more, with less attractive margins.

+ A domestic premium of 15-20% (US$70-100 of internment + taxes of 12-14%) and the cost structure favor domestic companies vs. global ones (except Asia). This might compensate the less accentuated peak.

- Riopol’s start-up might cause oversupply in the PE market, forcing the companies to export more to marginal markets.

+ With the Middle East– China flow well adjusted, Latam and USA might become important and profitable markets for domestic companies. Internationalization might grant access to competitive feedstocks.

Over-investment risk, due to reinforced cash as a result of the up-cycle, might shrink the domestic market premium, in case demand is not capable to absorb the additional volume.

* The considered price base for multiples and upsides calculation in the report is de closing of 02/15/2006

4

Petrochemical Sector, Feb-06

VALUATION

Ticker (most liquid) BRKM5 SZPQ4 UNIP6 CPSL3 PQUN4 UGPA4 PTIP4 PLTO6 (2) PEFX5 Not listed

Market Cap (R$mn) 6,845 1,065 1,243 4,642 1,012 2,704 1,804 331 581 na.

Actual EV (R$mn) 10,072 2,528 1,673 4,806 1,242 2,558 1,804 383 733 na.

Target Price ES Research (R$/share or thousand shares)

28.00 7.93 na. 39.00 na. 51.00 na. 8.70 24.00 na.

Upside 48% 69% na. 26% na. 53% na. 74% 45% na.

EV/EBITDA 2004 5.1 8.8 6.0 4.8 5.3 4.7 na. 2.5 2.0 na.

EV/EBITDA 2005E 4.4 15.4 na. 4.6 na. 4.6 na. 3.0 3.8 na.

CORPORATE DATA

ControllersOdebretch, Norquisa

Suzano Holding (Feffer family)

Geyer family BRKM and IpirangaUnipar, Dow

Chemical, Unigel, Ultrapar, SZPQ

Ultra SA Grupo IpirangaSZPQ, BRKM,

Sumitomo, ItochuSZPQ, BRKM,

UniparSZPQ, Unipar,

Petrobras, BNDES

Relevant ParticipationsPetroflex, Copesul,

Politeno,RioPol, Politeno,

Petroflex

Polietilenos União, Petroflex, RioPol,

PQU and etc.na. Polibutenos Norquisa Copesul Norquisa Norquisa na.

ACTIVITY SUMMARY

ScopeFirst and Second

GenerationsFirst and Second

GenerationsFirst and Second

GenerationsFirst Generation First Generation Second Generation Second Generation Second Generation Second Generation

First and Second Generations

Key ProductsEthylene,

Prophylene, PE, PP, PVC and etc.

PP Several (holding)Ethylene,

Prophylene and etc.Ethylene,

Prophylene and etc.Glicol Ethylene,

SpecialtiesPE, PP PE SBR PE, Prophylene

Chief Inst. Capacities (kton/year)Ethylene = 1.280 Prophylene = 550

Resins = 2.040PP = 625 Several (holding)

Ethylene = 1.135 Prophylene = 585

Ethylene = 500 Prophylene = 250

EO = 312 EG = 310

PE = 550 PP = 150

PE = 360 SBR = 411Ethylene = 520

PE = 540

Main Feedstocks Naphtha Prophylene Several (holding)Naphtha,

CondensedNaphtha Ethylene

Ethylene, Prophylene

EthyleneButadiene and

StyreneEthane and Propane

(Natural Gas)

Center where Performed NE and S All All S SE All S NE All SE

Main SuppliersPetrobras and

CopesulPetrobras and

CrackersPetrobras and

CrackersPetrobras Petrobras Braskem and PQU Copesul Braskem Braskem, Copesul Petrobras

OPERATING HIGHLIGHTS

Volumes 2004 (R$mn) 4,331 490 1,387 2,811 1,536 518 606 336 365 46

Volumes 2005E (R$mn) 4,522 597 na. 2,690 na. 539 na. 359 325 61

Revenues 2004 (R$mn) 11,043 1,610 2,180 5,440 2,700 1,663 1,839 1,119 1,306 149

Revenues 2005E (R$mn) 11,435 1,977 na. 5,449 na. 1,623 na. 1,156 1,349 185

EBITDA 2004 (R$mn) 2,549 238 396 1,070 349 421 323 165 183 2

EBITDA 2005E (R$mn) 1,990 168 na. 1,053 na. 305 na. 126 193 3

Unitary Revenue 2004 (R$/ton) 2,550 3,284 1,572 1,935 1,758 3,209 3,037 3,333 3,578 3,267

Unitary EBITDA 2004 (R$/ton) 589 485 286 380 227 812 533 492 500 43

EBITDA Margin 2004 (%) 23% 15% 18% 20% 13% 25% 18% 15% 14% 1%

CAGR EBITDA 05-08E 9% 37% na. 6% na. 6% na. 3% 1% >100%

ROIC (EBIT) 2004 (%) 27% 12% na. 44% na. 61% na. 22% 26% 0%

For a further detailed operational analyses, please go to the section “ES RESEARCH FORECASTS” (1) We used Ox iteno’s operating data for comparison (2) More liquid shares are of PNB class, with fixed dividends

5

Setor Petroquímico, Feb-06

2. PETROCHEMISTRY: FROM CRUDE OIL TO FINAL CONSUMER *** This chapter presents an introduction to the sector. Those already familiar and/or interested only in the investment recommendations can go directly to page 12 ***

The petrochemical industry derives from the oil and natural gas exploration activity and came out of the economic need of oil companies to amplify the usage of refining process by-products. The procedure comprised by the petrochemical industry is summarized below:

The petrochemical industry derives from the oil...

CHART 01: Petrochemical Production Flow

Source: Espírito Santo Research

The petrochemical inputs derived from oil or natural gas are taken to reactors, which, through the action of heat and pressure, convert the materials into basic petrochemicals, such as Olefins (Ethylene, Propane, Butadiene etc.) and Aromatics (Benzene, Toluene, Xylene, etc.). This process is called cracking and this stage the 1st generation. Ethylene is the building block of the 1st generation, being the most widely produced and consumed product on a global basis.

These basic products have little direct use and are basically inputed as raw materials for the so-called 2nd generation, that processes the Olefins and/or Aromatics through processes such as the Polymerization, yielding thermoplastic resins (such as Polyethylene, Polypropylene and PVC) and chemical by-products such as solvents and rubbers.

Not only internationally speaking but also on a domestic level, the sector players tend to constitute centers (or complexes) to reap logistics synergies, infra-structure and operational integration, thus minimizing costs. It is worth remembering that basic petrochemicals (particularly Ethylene) are normally volatile, of difficult to transportation and storage. The units comprising the Petrochemical Center are, mainly, of the first and second generation and might or migh not by tied in corporate terms. A model very embraced, around the world, is the integrated (such as Braskem, for example, as we shall comment further ahead), so as to capture most part of the chain margins, increasing operational flexibility.

The petrochemical industry is globalized and the majority of its products are traded as commodities, with a great flow of international commerce and the presence of some global players acting in several countries. These agents can be divided into:

♦ Global diversified chemical corporations (BASF, Bayer, DuPont, Dow Chemical etc.) whose petrochemical production is an important line of their portfolios without, however representing their sole businesses;

♦ Petrochemical arms of integrated oil giants’ downstream operations, (Exxon Mobil, BP, Amoco, Royal Dutch/Shell, etc.), including some state-owned companies such as PDVSA (which was recently spun off from Pequiven) and Saudi Aramco (Sabic) among others;

♦ Companies focused on the segment, with regional presence, such as Braskem and some Asian companies

..and its .input is converted into basic petrochemical in the 1st generation. These products are used in the 2nd generation The characteristics of the process tend to agglomerate companies into Petrochemical Centers.

OIL INDUSTRY

Oil and Natural GasExploration

Oil Refining

Processing of Natural Gas

Heavy Cracking

Light Cracking

Production of Resinsand Chemical by-

Products

FIRST GENERATION SECOND GENERATION

Transformationof Products

THIRD GENERATIONOIL INDUSTRY

Oil and Natural GasExploration

Oil Refining

Processing of Natural Gas

Heavy Cracking

Light Cracking

Production of Resinsand Chemical by-

Products

FIRST GENERATION SECOND GENERATION

Transformationof Products

THIRD GENERATION

6

Petrochemical Sector, Feb-06

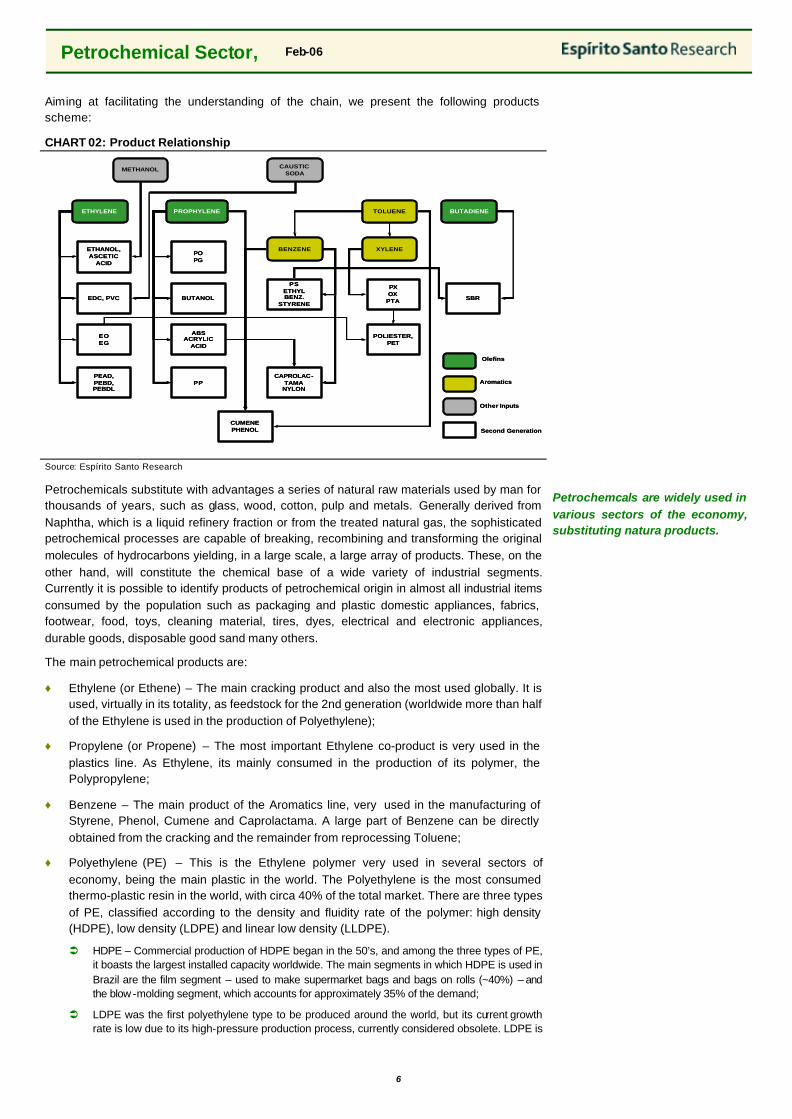

Aiming at facilitating the understanding of the chain, we present the following products scheme:

CHART 02: Product Relationship

Source: Espírito Santo Research

Petrochemicals substitute with advantages a series of natural raw materials used by man for thousands of years, such as glass, wood, cotton, pulp and metals. Generally derived from Naphtha, which is a liquid refinery fraction or from the treated natural gas, the sophisticated petrochemical processes are capable of breaking, recombining and transforming the original molecules of hydrocarbons yielding, in a large scale, a large array of products. These, on the other hand, will constitute the chemical base of a wide variety of industrial segments. Currently it is possible to identify products of petrochemical origin in almost all industrial items consumed by the population such as packaging and plastic domestic appliances, fabrics, footwear, food, toys, cleaning material, tires, dyes, electrical and electronic appliances, durable goods, disposable good sand many others.

The main petrochemical products are:

♦ Ethylene (or Ethene) – The main cracking product and also the most used globally. It is used, virtually in its totality, as feedstock for the 2nd generation (worldwide more than half of the Ethylene is used in the production of Polyethylene);

♦ Propylene (or Propene) – The most important Ethylene co-product is very used in the plastics line. As Ethylene, its mainly consumed in the production of its polymer, the Polypropylene;

♦ Benzene – The main product of the Aromatics line, very used in the manufacturing of Styrene, Phenol, Cumene and Caprolactama. A large part of Benzene can be directly obtained from the cracking and the remainder from reprocessing Toluene;

♦ Polyethylene (PE) – This is the Ethylene polymer very used in several sectors of economy, being the main plastic in the world. The Polyethylene is the most consumed thermo-plastic resin in the world, with circa 40% of the total market. There are three types of PE, classified according to the density and fluidity rate of the polymer: high density (HDPE), low density (LDPE) and linear low density (LLDPE).

Ü HDPE – Commercial production of HDPE began in the 50’s, and among the three types of PE, it boasts the largest installed capacity worldwide. The main segments in which HDPE is used in Brazil are the film segment – used to make supermarket bags and bags on rolls (~40%) – and the blow -molding segment, which accounts for approximately 35% of the demand;

Ü LDPE was the first polyethylene type to be produced around the world, but its current growth rate is low due to its high-pressure production process, currently considered obsolete. LDPE is

Petrochemcals are widely used in various sectors of the economy, substituting natura products.

ETHYLENE PROPHYLENE

CAUSTIC SODA

PEAD, PEBD, PEBDL

BENZENE

BUTADIENE

XYLENE

METHANOL

EOEG

EDC, PVC

ETHANOL, ASCETIC

ACID

PP

ABS ACRYLIC

ACID

BUTANOL

POPG

CUMENE PHENOL

PSETHYL BENZ.

STYRENE

CAPROLAC-TAMA

NYLON

TOLUENE

PXOX

PTA

POLIESTER, PET

SBR

Olefins

Aromatics

Other Inputs

Second Generation

ETHYLENE PROPHYLENE

CAUSTIC SODA

PEAD, PEBD, PEBDL

BENZENE

BUTADIENE

XYLENE

METHANOL

EOEG

EDC, PVC

ETHANOL, ASCETIC

ACID

PP

ABS ACRYLIC

ACID

BUTANOL

POPG

CUMENE PHENOL

PSETHYL BENZ.

STYRENE

CAPROLAC-TAMA

NYLON

TOLUENE

PXOX

PTA

POLIESTER, PET

SBR

Olefins

Aromatics

Other Inputs

Second Generation

7

Petrochemical Sector, Feb-06

generally processed mixed together with LLDPE to produce flexible films for packaging;

Ü LLDPE is a newer product that has a higher demand growth rate than the other Polyethylene. It is very frequently used in the food industry;

♦ Polypropylene (PP) – PP, the Propylene polymer, is the fastest-growing resin around the world due to its diversity of applications, its physical-chemical resistance, easy processing and low density, which is why it is widely used to make plastic films and metal substitutes;

♦ Polyvinyl Chloride (PVC) – PVC is the MVC (monovinyl chloride) polymer that contains EDC (dichloroethane) in its composition. The main difference between PVC and other plastics is that PVC is 55% chlorine (not from the hydrocarbon chain) and only 45% Ethylene. The chlorine is obtained from marine salts, in electrointensive units that separate the chlorine from the caustic soda. PVC is used in rigid installations such as pipes, or in flexible lines;

♦ Polyethylene Terephthalate (PET) – Generated through a combination of other derivatives, such as Paraxylene (PX) and Polyester, PET is widely used to form bottles and packaging material. Initially, the Polyethylene Terephthalate (PET) resin was only used in the textile industry. It was only in the late 70’s that the resin began being used on an industrial scale to produce bottles for the packaging industry in view of several of its characteristics, such as its high mechanical and chemical resistance and its capacity as a barrier against gases and odors, as well as its excellent transparency;

♦ Polystyrene (PS) – Made from Styrene, which is an internationally traded commodity and a intermediate-petrochemical. It is the oldest thermoplastic and is used to make disposable cups, pots and boxes, rigid expanded polystyrene foam (known as Styrofoam) and in electric and electronic appliances. Demand for this product grows at a slower rate than the majority of this chain’s products, and in many cases, it is being replaced by other resins, such as in disposable cups where PP provides a much better solution.

CHART 03: Applications of Petrochemical Products (Brazilian Economy)

Source: Espírito Santo Research and Braskem

The Influence of Feedstocks

It is essential to address the issue of raw materials in order to achieve a better understanding of the sector and the relative attractiveness of the several development opportunities. The following are the principle feedstocks used around the world, the two chief materials being Naphtha and Ethane:

♦ Naphtha – Derived from the refinement of crude oil, it is basically a preliminary fraction of gasoline;

♦ Gasoil – Also a petroleum derivative, gasoil is a intermediary type that is heavier than Naphtha, and can also produce fuels (ex. Diesel);

♦ Condensate – The liquid fraction of the exploration of associated gas, comprised of

The main raw materials can be obtained from crude oil or natural gas...

PEBDL

PEAD

PVC

PP

Food Packings27%

Consumer Goods25%

Civil Construction

19%

PersonalHygiene

11%

Agriculture5%

Autoparts3%

Industrial Utilities2% Others

8%

PEBDL

PEAD

PVC

PP

Food Packings27%

Consumer Goods25%

Civil Construction

19%

PersonalHygiene

11%

Agriculture5%

Autoparts3%

Industrial Utilities2% Others

8%

8

Petrochemical Sector, Feb-06

Oil

Fractioning Tower

Refinary Gas

Naphtha

Gasoline

Kerosene

Diesel and Gasoil

Lubrificants

Oil Fuel

Residue Asphalt

DISTILLED FRACTION:

ATOMS OF C PER

MAIN UTILITIES

1-4

5-9

5-10

10-16

14-20

20-50

30-70

>50

LPG

Petrochemistry

Vehicles

Spurts

Engines of High Power

Waxes

Industrial and Thermogeneration

Asphalt

Pentane, one of the Natural Gas Liquids (NGL’s);

♦ Ethane – One of the components of natural gas, it is the so-called “wet” part that is separated in the processing of the gas;

♦ Propane – Also associated to "wet“ gas, Propane is also a component of LPG. For petrochemical, a mixture containing Ethane and Propane is normally used.

CHART 04: Refining Product Slate

Source: Espírito Santo Research

The range of inputs processed yield a different product slate; however, if we consider the production of Ethylene alone, the natural gas -based crackers provide a better yield, as shown below:

... thereby generating different cost structures and product mixes.

CHART 05: Cracking Mix per Feedstock CHART 06: Ethylene Yield per Feedstock

30% 23%

41%

16%14%

17%24%

20%

7 %

10%

11%7 %

20%13%

31% 27%

81%

2%1%

3%

0 %

20%

40%

60%

80%

100%

Naphtha Ethane (NG) Gasoil LPG (Propane:Butane)

Ethylene Prophylene BTX Butadiene Others

Source: Espírito Santo Research and Suzano Petroquímica Source: Espírito Santo Research

A barrel of oil is equivalent in energy to approximately 5,82mmBTUs or the equivalent in volume to 0,159m3. Therefore, we could assess the competitiveness of each type of cracker (specially Naphtha and Gas), by monitoring that ratio and the relativa price movement. However, this comparison shortcoming is that it does not take into account the output differences, and the additional revenue of rendered by the co-products, that compensate for the higher input-per-unit-of-Ethylene cost.

Gauging this competitiveness along time, strictly regarding Ethylene, the gas cracker will always have the upper hand. However, analyzing the other Naphtha processing coproducts (Propylene, Benzene, Butadiene, etc.), which generate importante incomes to its producers, we empirically include that for rations around/little under 7, the heavy are actually more profitable. This relationship is a simplified way to express the Naphtha-Ethane comparison, which, on the other hand, tends to indicate the relative profitability advantage of the processes.

0.8 tonEteno

Lig

ht

Cra

ckin

g 1.3 tonEthane (70%) + Propane (30%)

Hea

vyC

rack

ing

3.3 tonNaphtha

1.0 tonEthylene

0.2 tonProphylene (principal)

2.3 tonOther Basics

0.8 tonEteno

Lig

ht

Cra

ckin

g 1.3 tonEthane (70%) + Propane (30%)

Hea

vyC

rack

ing

3.3 tonNaphtha

1.0 tonEthylene

0.2 tonProphylene (principal)

2.3 tonOther Basics

9

Petrochemical Sector, Feb-06

CHART 07: Oil vs. Natural Gas CHART 08: Ratio Oil – Natural Gas

0

10

20

30

40

50

60

70

Jul-0

2

Oct

-02

Jan-

03

Apr

-03

Jul-0

3

Oct

-03

Jan-

04

Apr

-04

Jul-0

4

Oct

-04

Jan-

05

Apr

-05

Jul-0

5

Oct

-05

Jan-

06

Oil

- B

ren

t (U

S$/

ton

)

0

2

4

6

8

10

12

14

16

Nat

ura

l Gas

- H

enry

Hu

b

(US

$/M

NB

tu)

Brent Henry Hub

0

1

2

3

4

5

6

7

8

9

10

Jul-0

2

Oct

-02

Jan-

03

Apr

-03

Jul-0

3

Oct

-03

Jan-

04

Apr

-04

Jul-0

4

Oct

-04

Jan-

05

Apr

-05

Jul-0

5

Oct

-05

Jan-

06

Rat

io B

ren

t/H

enry

Hu

b

Source: Espírito Santo Research and Bloomberg Source: Espírito Santo Research and Bloomberg

A competitivity comparison among the 2 main feedstocks should take into account, in addition to profitability, the kinds of returns each cracker can give. As previously mentioned, the petrochemical industry is a capital intensive one, particularly with regards to its 1st generation plants. The investment needed to install an industrial plant easily exceeds US$1bn, not counting secondary investments in the required infrastructure.

Furthermore, the capex to build a Naphtha (heavy) cracker tends to be greater than the cost related to a light one. Therefore, in terms of return on invested capital, a heavy cracker tends to be less efficient despite having, given market conditions (but very often), potentially higher margins.

The investment is close to US$1bn

CHART 09: Investment per Cracker Type (USD per 100kton/year)

200

140

67 70

0

50

100

150

200

250

Naphtha Cracker Gas Cracker PE Plant PP Plant

Source: Espírito Santo Research and Suzano Petroquímica

Based on the previously shown data, we set forth below the theoretical typical cracker FC equations for each type – based on gas and Naphtha – at the current prices in the Asian market. Note that these equations are dynamic and vary constantly according to the behavior of the various commodities involved; however, the analysis we have provided, helps to understand the relative advantages of each process. The analysis shows that at the current price level (1st generation products and inputs), the Naphtha-based cracker has the edge over Gas, even in terms of profitability (ROIC).

Usually, a Naphtha crackers have higher EBITDA margin...

... whereas NG crackers usually achieve a higher EBIT

Currently, heavy crackers have the advantage.

TABLE 01: Cracker Equations Per Type (Nov/05 Base date) –Theoretical EBITDA Margin (per 1ton Input)

10

Petrochemical Sector, Feb-06

Equation Inputs:Prices: Ethane 517 Naphtha 477 Ethylene 731 Prophylene 850 BTX Avg. 639 Butadiene 1,045 Fuel and Utilities Avg. 500

NG Cracker (Ethane)PRODUCTS YIELDS PRICES UNIT PRICE/COST RESULT

Ethylene 81% 731 590Prophylene 2% 850 21BTX 1% 639 5C4 (Butadiene) 3% 1,045 34Fuel and Utilities 13% 500 64REVENUE 714

Revenue Taxes (@2%) (14)

Ethane 100% 517 (517)Other Costs - - (75) CASH COST (592)

GROSS PROFIT (CASH) 107 Gross Margin (Cash) 15%

Operating Expenses (@3% of Revenue) (21)

EBITDA 86 EBITDA Margin 12%

Necessary Investment* 1,400ROIC EBITDA (before taxes) 6%

Naphtha CrackerPRODUCTS YIELDS PRICES UNIT PRICE/COST RESULT

Ethylene 30% 731 222Prophylene 16% 850 137BTX 24% 639 151C4 (Butadiene) 10% 1,045 105Fuel and Utilities 20% 500 100REVENUE 714

Revenue Taxes (@2%) (14)

Naphtha 100% (477) (477)Other Costs - - (70)CASH COST (547)

GROSS PROFIT (CASH) 152 Gross Margin (Cash) 21%

Operating Expenses (@3% of Revenue) (21)

EBITDA 131 EBITDA Margin 18%

Necessary Investment* 2,000ROIC EBITDA (before taxes) 7%

Source: Espírito Santo Research, Unipar and Bloomberg * US$ per ton/year for competitive scale project

CHART 10: Theoretical EBITDA Margins Evolution CHART 11: Competitiveness vs. Oil/Gas Ratio

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

70%

Jul-0

2

Oct

-02

Jan-

03

Apr

-03

Jul-0

3

Oct

-03

Jan-

04

Apr

-04

Jul-0

4

Oct

-04

Jan-

05

Apr

-05

Jul-0

5

Oct

-05

Jan-

06

Naphtha Margin Gas Margin

(2.0)

(1.5)

(1.0)

(0.5)

0.0

0.5

1.0

jul-0

2

out-0

2

jan-

03

abr-

03

jul-0

3

out-0

3

jan-

04

abr-

04

jul-0

4

out-0

4

jan-

05

abr-

05

jul-0

5

out-0

5

jan-

06

0

2

4

6

8

10

12

Cash Margin Differential Ratio Oil/Gas (rig.)

Source: Espírito Santo Research and Bloomberg Source: Espírito Santo Research and Bloomberg

11

Petrochemical Sector, Feb-06

The charts above demonstrate that, in fact, for ratios under 7x, the heavy cracker usually achieves higher margins. Moreover, it is interesting to note the low level of returns obtained in both cases. Note that we considered the results to be consistent with cracker investments in developed markets, where centrals, despite not producing extraordinary returns, tend to achieve or exceed capital costs. Companies turn to integration and synergy to increase profitability (processing cheaper feedstocks at times). In the Brazilian market, in addition to these tools, companies also rely upon premiums (via margin share agreements as demonstrated farther ahead), given that our calculations show that for a premium of close to 10%, the ROICs tend toward an adequate WACC for the sector.

Eyeing Naphtha, the Brazilian industry’s main input, we note that historically the price of the primary international benchmark, the ARA (Amsterdam, Rotterdam and Antwerp) followed a mark-up of 9-10x the price of the Brent barrel. Recently, the overwhelming advance of crude oil, has given rise to comments from industry players that this 9x correlation would have been broken, as it currently hovers close to 8x, softening the effects of oil price increases on the sector.

In reality, this rate is a simplistic representation of what we call the Naphtha refining spread. By multiplying the oil barrel price by 7.33, in order to convert US$/bbl into US$/ton, we derive the margin/ton for Naphtha, which historically has been between US$30-100/ton, and generally close to US$70/ton. The maintenance of that 9-10x ratio would necessarily entail in an increase in the Naphtha refinement margin, simply due to the increase in oil prices, at a proportion of approximately US$9/ton for every US$1 in the price of a barrel, which does not appear very reasonable. The supply-demand for the derivative, as well as the behavior of substitutes, are the factors that govern this spread (US$/ton). This spread has remained relatively constant, when not in decline, partly due to the fact that the demand for Naphtha hasn’t grown as much as the demand for other derivatives, as well as the fact that the cracking capacity has not been expanding significantly. Nevertheless, with crude oil prices nearing US$70/bbl (or US$513/ton), the Naphtha margin tends to represent proportionally less, hence the Brent/ARA ratio also tends to ease. The recent contraction of this ratio coincides with the compression of light oil refining margins around the world, and we do not see much room for this ratio to drop any further.

The ARA Naphtha has been detaching itself from Brent crude oil, since the refining spread does not follow rising oil prices...

The margin/ton for Naphtha tends towards USD70/ton

CHART 12: Naphtha (ARA) vs. Oil (Brent)

0

100

200

300

400

500

600

700

jan-

98

jul-9

8

jan-

99

jul-9

9

jan-

00

jul-0

0

jan-

01

jul-0

1

jan-

02

jul-0

2

jan-

03

jul-0

3

jan-

04

jul-0

4

jan-

05

jul-0

5

jan-

06

Oil

and

Nap

hth

a (U

S$/

ton

)

0

2

4

6

8

10

12

14

Rat

io B

ren

t/A

RA

ARA Brent Ratio (x)

Source: Espírito Santo Research and Bloomberg

12

Petrochemical Sector, Feb-06

3. GLOBAL OUTLOOK: CLIMBING THE FLY UP ? Cyclicality

The industry is cyclical in nature as it is influenced by the global economy’s expansion cycles and because of its investment-profitability dynamics. Petrochemical plants are complex facilities that take approximately 4-5 years to start-up and require a massive amount of investments. During the high-profitability phase, normally on the back of upbeat global economies, large capacity additions are made, which for times had been delayed until market conditions allowed for the proper cash generation and the required stimulus for such investments to occur. These investments are sometimes sizable enough to alter the supply/demand balance, thus causing prices to drop when they coincide in terms of becoming operational.

The petrochemical sector has historically been marled by distinct phases of profitability, or cycles, which usually last from 7 to 10 years.

♦ Peaks: Such peaks are marked by elevated use rates, with demand driven by global growth, attaining the effective installed capacity (discounting the portion out of operations). The Ethylene-Naphtha spread can reach the US$700/ton or more mark in accentuated peak periods;

♦ Throughs: With the start-up of newly-constructed plants, coinciding or not with periods of subdued GDP growth, prices dwindle, tightening margins, which converge to production costs. Such level is historically close to US$100/ton over Naphtha for Ethylene, but could potentially reach levels even lower than that, as more low-cost producers enter the market (ex. United Arab Emirates), as we’ll explore further ahead.

The industry is cyclical in nature as it is influenced by the global economy’s cycles, and the dynamic of profitability and investments.

CHART 13: Historic Cash Margin of the American Petrochemical Industry - Index

100

– 82

Bas

e In

dex

= 10

0

Source: Espírito Santo Research and Braskem (orig. Nexant)

Demand

The global economy has demonstrated its resiliency over recent years, with global growth reaching 5.1% in 2004, the highest level in 3 decades. According to its latest global study, released in a recent report, the IMF expects a reasonably healthy rate of growth in 2005 and 2006, despite increasing risks, with the oil crisis and global payment imbalances. In the better part of the industrialized world, inflation once again appears to be under control, despite rising fuel prices, not to mention the beneficial conditions of the capital markets, which support the idea that global growth is well sustained. For the upcoming years, beyond 2006, the IMF expects world GDP growth rate to remain stable at around 4.0-4.5% until 2010, sustained by China, India, Japan, and possibly the US, and maybe even Brazil (?). In our projections, we conservatively consider a lower pace of growth, closer to the inferior band of this range.

This recent recovery of global expansion, with above-average GDP growth, and primarily, the booming Chinese economy, has caused the demand for various commodities (illustrated in

The global economy has grown in recent years (+5.1% in 2004) The IMF estimates that the world GDP’s evolution will continues to be ~ 4.0-4.5% up to 2010, The demand for commodities has increased...

450

400

350

300

250

200

150

100

50

0 1975

1980 1985 1990 1995 2000 2005

9 years 7 years 10 years

13

Petrochemical Sector, Feb-06

chart 15 below), such as several metals, ore and oil, including petrochemicals, to pick up. This demand boost has driven global capacity utilization rates up, and hence spreads and prices.

CHART 14: GDP Growth in Various Regions CHART 15: Global GDP vs. Commodities*

World

Indust.

GEM

USA

China&India

Latam

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

1Q96

3Q96

1Q97

3Q97

1Q98

3Q98

1Q99

3Q99

1Q00

3Q00

1Q01

3Q01

1Q02

3Q02

1Q03

3Q03

1Q04

3Q04

1Q05

3Q05

1Q06

3Q06

World Indust. GEM USA China&India Latam

0%

1%

2%

3%

4%

5%

6%

7%

1Q97

3Q97

1Q98

3Q98

1Q99

3Q99

1Q00

3Q00

1Q01

3Q01

1Q02

3Q02

1Q03

3Q03

1Q04

3Q04

1Q05

3Q05

-70%

-50%

-30%

-10%

10%

30%

50%

70%

90%

110%

130%

150%

Global GDP (left) Ind. Commodities Index Brent

Source: Espírito Santo Research and IMF Source: Espírito Santo Research, IMF and Bloomberg * Goldman Sachs Index

In this scenario, we expect that the demand for petrochemical products will evolve steadily, even without major increases in the level of consumption per capita. Assuming an elasticity of around 1.1x (below the recent historic average of ~1.3x), we estimate that the global Ethylene market, driven by the demand for its derivatives (the primary derivative being PE), will grow 4.6%p.a. until 2010E (the same average witnessed since 1986), or the equivalent to 5,000 kton/year. In our assessment, we mostly refer to Ethylene as it is the product most produced and used, and is the industry’s building block on a global scale.

We expect the demand for Ethylene will have a CAGR of 4,6% by 2010E

CHART 16: GDP Evolution vs. Ethylene Demand CHART 17: Ethylene and PE Demand – HDPE+LDPE+LLDPE (mn tons)

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

E

2007

E

2009

E

-

0.2

0.4

0.6

0.8

1.0

1.2

1.4

Global GDP Ethylene Demand Avg. Elasticity

-

20

40

60

80

100

120

140

160

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

E

2006

E

2007

E

2008

E

2009

E

2010

E45%

47%

49%

51%

53%

55%

57%

59%

61%

63%

65%

Ethylene Polyethylene % Consumed

Source: Espírito Santo Research and IMF Source: Espírito Santo Research, IMF and Bloomberg

Supply

The global Ethylene capacity as of 2004 was of approximately 112mm ton (in 2005E should close at 116mm ton). According to a CMAI consultants (Chemical Markets Associates Inc.) survey, which maps capacity expansion projects throughout the world, in 2006E around 7mm tons (or ~6%) should be added. As for 2007E and 2008E, the expansions should be respectively 5% and 3%, and in the period between 04-10E, the expansions CAGR should reach 5%, leading up to 150mm tons of installed capacity

Most part of the capacity additions are expected in Asia, more precisely in the Middle East, which should respond for approximately half the new capacity. China, destination of most part of this additional Ethylene, with its buoyant consumer market, should also contribute with a good part of the expansions. The rationale behind this clear change in the axle of the global petrochemical industry is to take advantage of attractive raw materials, supplied by the Middle East (for e.g. while in the USA natural gas used to obtain Ethylene is sold at US$7-9/MMBtu, in the Middle East it costs some US$2/MMBtu), apart from lower production costs and the

The global capacity was ~112mn tons in 2004 and should end at 116mn tons in 2005E CAGR 04-10E estimated at 5%, attaining 150mn tons More of the additions are in Asia... ... seeking Middle-Eastern raw materials to supply Chinese growth

14

Petrochemical Sector, Feb-06

proximity with a fast growing market.

In the Middle East, we consider Iran to be case of its own. According to CMAI’s projections, more than 7mm tons of additional Ethylene capacity are expected in the country. In the past, there were significant delays in the effective start-up in relation to what had been initially planned, even regarding small plants in the country. Additionally it is worth reminding that a new government took the country in 2005, which can affect the schedule of these investments in two fronts: (i) radical religious positions which increases the perception of investments risk by western partners; (ii) a more nationalist policy, favoring social investments and demanding a greater level of national (less skilled) participation in the projects.

Another important datum is that the majority of the planned expansion project contemplates the use of natural gas as illustrated in chart 19. With that in mind, the trend is for the Propylene market and its by-products seems even more upbeat than that of Ethylene.

Part of the capacity, from Ira, may be delayed The greater part of the expansions should be in NG crackers

Table 02: Installed Capacity Worldwide– Per Region Region Ethylene PE PP PE/EthyleneMiddle East 10.9 7.2 2.5 66%SE Asia 31.1 21.4 16.9 69%Latam 6.2 4.0 2.4 64%Europe 29.8 19.0 12.0 64%North of America 32.3 19.0 9.1 59%Africa/ Others 1.3 0.8 0.7 64%Total 111.6 71.3 43.6 64%

Source: Espírito Santo Research, CMAI and Polymerupdate

CHART 18: Worldwide Distribution of Ethylene Production (% and mn tons)

13 13 11 12 14 14 15 16 17 16 17 18 19 19 20 21 22 23 27 25 26 23 24 23 25

11 1110 12 13

12 13 14 15 14 14 15 16 16 17 18 18 1819

19 2020 20 21 21

4 44 4 4

4 4 5 5 6 6 6 6 6 6 7 77

78 7

7 7 7 8

8 9 9 11 12 13 15 16 18 18 19 19 21 22 24 24 26 29 2934 37

41 44 47 49

0%

20%

40%

60%

80%

100%

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004

USA Western Europe Japan Rest of the World

The industry’s central axis is shifting to Asia...

Source: Espírito Santo Research and SRI

Chart 19: Global Cracking Capacity Additions – Up to 2010E (000 tons/year)

-

5,000

10,000

15,000

20,000

25,000

Africa Europe America Asia Others Middle Eastern

Naphtha/ Other Liquid Loads Ethane/ Other Gaseous Loads

Source: Suzano Petroquímica (orig. Nexant)

15

Petrochemical Sector, Feb-06

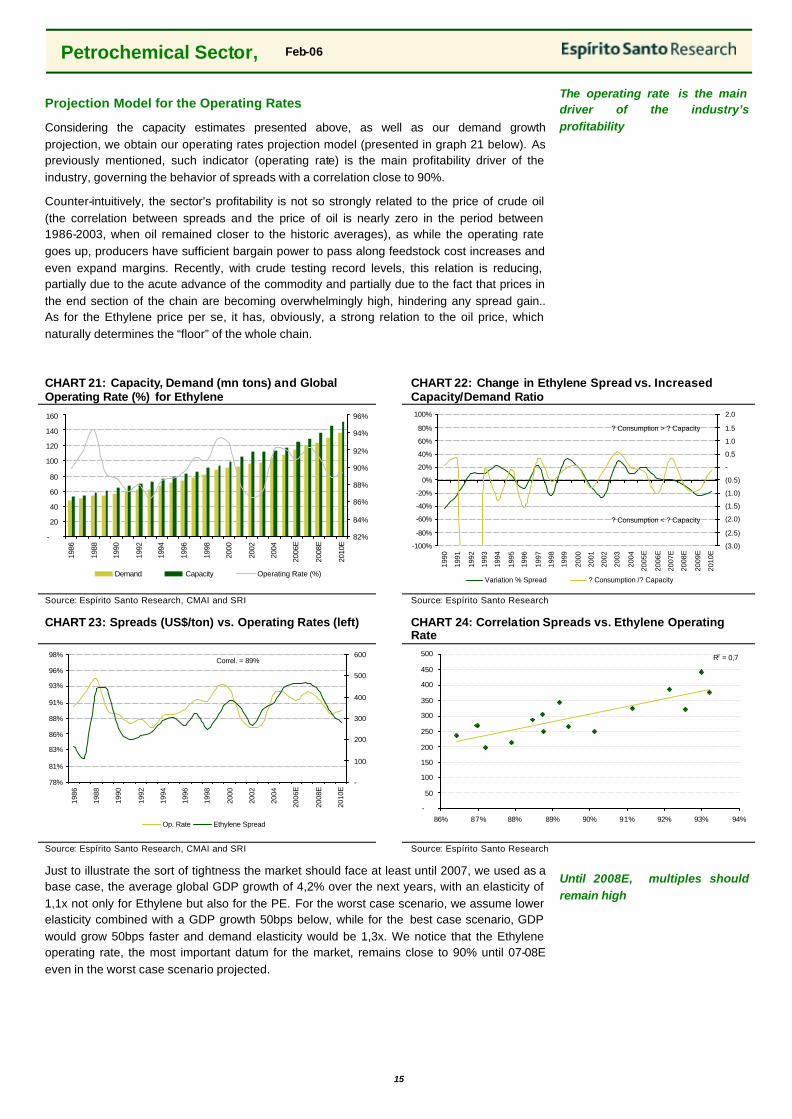

Projection Model for the Operating Rates

Considering the capacity estimates presented above, as well as our demand growth projection, we obtain our operating rates projection model (presented in graph 21 below). As previously mentioned, such indicator (operating rate) is the main profitability driver of the industry, governing the behavior of spreads with a correlation close to 90%.

Counter-intuitively, the sector’s profitability is not so strongly related to the price of crude oil (the correlation between spreads and the price of oil is nearly zero in the period between 1986-2003, when oil remained closer to the historic averages), as while the operating rate goes up, producers have sufficient bargain power to pass along feedstock cost increases and even expand margins. Recently, with crude testing record levels, this relation is reducing, partially due to the acute advance of the commodity and partially due to the fact that prices in the end section of the chain are becoming overwhelmingly high, hindering any spread gain.. As for the Ethylene price per se, it has, obviously, a strong relation to the oil price, which naturally determines the “floor” of the whole chain.

The operating rate is the main driver of the industry’s profitability

CHART 21: Capacity, Demand (mn tons) and Global Operating Rate (%) for Ethylene

CHART 22: Change in Ethylene Spread vs. Increased Capacity/Demand Ratio

-

20

40

60

80

100

120

140

160

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

E

2008

E

2010

E

82%

84%

86%

88%

90%

92%

94%

96%

Demand Capacity Operating Rate (%)

-100%

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

E

2006

E

2007

E

2008

E

2009

E

2010

E

(3.0)

(2.5)

(2.0)

(1.5)

(1.0)

(0.5)

-

0.5

1.0

1.5

2.0

Variation % Spread ? Consumption /? Capacity

? Consumption > ? Capacity

? Consumption < ? Capacity

Source: Espírito Santo Research, CMAI and SRI Source: Espírito Santo Research

CHART 23: Spreads (US$/ton) vs. Operating Rates (left) CHART 24: Correlation Spreads vs. Ethylene Operating Rate

78%

81%

83%

86%

88%

91%

93%

96%

98%

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

E

2008

E

2010

E

-

100

200

300

400

500

600

Op. Rate Ethylene Spread

Correl. = 89%

R2 = 0,7

-

50

100

150

200

250

300

350

400

450

500

86% 87% 88% 89% 90% 91% 92% 93% 94%

Source: Espírito Santo Research, CMAI and SRI Source: Espírito Santo Research

Just to illustrate the sort of tightness the market should face at least until 2007, we used as a base case, the average global GDP growth of 4,2% over the next years, with an elasticity of 1,1x not only for Ethylene but also for the PE. For the worst case scenario, we assume lower elasticity combined with a GDP growth 50bps below, while for the best case scenario, GDP would grow 50bps faster and demand elasticity would be 1,3x. We notice that the Ethylene operating rate, the most important datum for the market, remains close to 90% until 07-08E even in the worst case scenario projected.

Until 2008E, multiples should remain high

16

Petrochemical Sector, Feb-06

Chart 25: Evolution of Global Installed Ethylene Capacity (mn tons) vs. Operating Rate (%)

Chart 26: Evolution of Global Installed Polyethylene Capacity (mn tons) vs. Operating Rate (%)

80%

82%

84%

86%

88%

90%

92%

94%

96%

1999 2000 2001 2002 2003 2004 2005E 2006E 2007E 2008E

Ope

ratin

g Ra

te (%

)

-

20

40

60

80

100

120

140

160

Capa

city

(mn

ton)

Capacity Base Case Best Case Worst Case

78%

81%

83%

86%

88%

91%

93%

96%

98%

1999 2000 2001 2002 2003 2004 2005E 2006E 2007E 2008E

Op

erat

ing

Rat

e (%

)

-

10

20

30

40

50

60

70

80

90

100

Cap

acit

y (m

ton

)

Capacity Base Case Best Case Worst Case

Source: Espírito Santo Research and CMAI Source: Espírito Santo Research and CMAI

The start of the cyclical downturn is expected for 2008E, and should last until 2010-2011E, but this will depend on the intensity of the new investments being made, particularly in the Middle East, and the performance of the Asian and US economies. Geo-political uncertainties in the Middle East (such as the election of the new Iranian Government) may delay the investment schedule considerably.

A few global consulting firms that focus on the sector are projecting that in this upcycle, as opposed to previous ones, capital discipline will be stronger, which may result in a less pronounced margin downturn as of 2008-2010E. One of the main reasons for this discipline belief is the fact that the worldwide petrochemical sector has consolidated considerably, which, albeit makes sense, might be a little premature (and aggressive) to include in our projections.

The general impression we get is that the excessive supply, on a global scale, shouldn’t pose a threat to a fly-up, since capacity increases, at least until 2008E, appear to be (at least) adjusted to the expected increase in demand. Therefore, operating rates should remain high, starting from an already quite strong level in 2004. Based on the figures set forth previously, we envision a sound upswing in margins in 2004-2008E (with spreads over USD400/ton for Ethylene and USD600/ton for PE throughout the period), which, despite not representing an overly sharp peak (slightly lower than the 2H04 level), it may hold steady (and quite profitable) for a relatively prolonged period of time.

Does this mean we are extremely optimistic regarding the sector worldwide in the medium term? No. Although our calculations indicate that the hypothesis of a plateau is feasible, we indeed include a through from 2009E. One of the reasons for this is the small degree of predictability regarding future capacity increases from 08E on, particularly in Middle East and China. Historically, the industry has underestimated capacity increases, and as a result, has consistently over-invested.

Below, we present our outlook for the price of the principal commodities of importance to the sector’s assessment, including resins, basic products and raw materials:

The start of the cyclical downturn is expected for 2009-2011E, but this will depend of made investments intensity

The cyclical downturn may be blander...

Supply excess is not a real threat to the fly-up...

... the spread should remain above US$400/ton until 2008E

The plateau is feasible. However, the sector historically underestimated the capacity additions over the medium term

17

Petrochemical Sector, Feb-06

TABLE 03: ES Research Petrochemical Product Forecasts Annual Averages 2002 2003 2004 2005E 2006E 2007E 2008E 2009E 2010E 2011E 2012E 2013E 2014E 2015EOil - Brent (US$/bbl) 25.01 28.55 38.00 54.88 53.00 45.00 40.00 33.00 32.00 32.00 32.00 32.00 32.00 32.00 Naphtha - ARA 223 280 382 470 452 395 358 307 300 300 300 300 300 300 Ethane - US Gulf 192 292 373 434 425 364 329 282 275 275 275 275 275 275 Ethylene* 450 548 811 923 915 863 790 642 577 570 574 605 632 640 Prophylene* 425 506 742 899 913 879 815 665 598 590 594 626 655 662 Polyethylene (Avg.) 613 727 1,024 1,113 1,100 1,047 958 800 732 724 728 761 790 798 PEAD* 549 686 947 1,044 1,041 990 906 757 692 685 688 720 747 755 PEBD* 749 868 1,172 1,278 1,215 1,156 1,057 883 808 799 803 840 872 881 PEBDL* 541 628 951 1,017 1,046 995 910 761 696 688 692 723 751 758 PolyProphylene* 598 704 952 1,085 1,108 1,097 1,015 863 799 792 798 833 865 874 Spreads (Cash Margins) 2002 2003 2004 2005E 2006E 2007E 2008E 2009E 2010E 2011E 2012E 2013E 2014E 2015EEthylene-Naphtha (1st. Generation) 227 269 428 453 463 468 431 335 278 270 274 305 333 340 Prophylene-Naphtha (1st. Generation) 203 226 360 430 461 484 457 358 298 290 294 327 355 363 PE-Ethylene 163 179 213 191 186 185 168 158 154 154 154 156 158 158 PP-Prophylene 172 198 209 186 195 218 200 198 202 202 204 207 210 212 PE-Naphtha 390 448 641 644 648 652 599 493 432 424 428 461 490 498 PP-Naphtha 375 424 569 616 656 702 657 556 500 493 498 534 565 575 Ratios 2002 2003 2004 2005E 2006E 2007E 2008E 2009E 2010E 2011E 2012E 2013E 2014E 2015EEthylene/Prophylene 1.06 1.08 1.09 1.03 1.00 0.98 0.97 0.97 0.97 0.97 0.97 0.97 0.97 0.97 Naphtha/Ethane 1.16 0.96 1.02 1.08 1.06 1.08 1.09 1.09 1.09 1.09 1.09 1.09 1.09 1.09 Source: Espírito Santo Research and Bloomberg * Average of Asian, American and European markets, when available

CHART 27: Basic Products Price (USD/ton) CHART 28: Thermoplastic Resins Price (US$/ton)

-

200

400

600

800

1,000

1,200

1Q02

4Q02

3Q03

2Q04

1Q05

4Q05

E

3Q06

E

2Q07

E

1Q08

E

4Q08

E

3Q09

E

2Q10

E

1Q11

E

4Q11

E

3Q12

E

2Q13

E

1Q14

E

4Q14

E

3Q15

E

Naphtha - ARA Ethylene Prophylene

-

200

400

600

800

1,000

1,200

1,400

1,6001Q

02

4Q02

3Q03

2Q04

1Q05

4Q05

E

3Q06

E

2Q07

E

1Q08

E

4Q08

E

3Q09

E

2Q10

E

1Q11

E

4Q11

E

3Q12

E

2Q13

E

1Q14

E

4Q14

E

3Q15

E

PEAD PEBD PEBDL PP

Source: Espírito Santo Research Source: Espírito Santo Research

CHART 29: Basic Products Spreads (USD/ton) CHART 30: Resins’ Spreads (USD/ton)

-

100

200

300

400

500

600

1Q02

3Q02

1Q03

3Q03

1Q04

3Q04

1Q05

3Q05

E

1Q06

E

3Q06

E

1Q07

E

3Q07

E

1Q08

E

3Q08

E

1Q09

E

3Q09

E

1Q10

E

3Q10

E

1Q11

E

3Q11

E

1Q12

E

3Q12

E

1Q13

E

3Q13

E

1Q14

E

3Q14

E

1Q15

E

3Q15

E

Prophylene - Naphtha Ethylene - Naphtha

-

100

200

300

400

500

600

700

800

1Q02

3Q02

1Q03

3Q03

1Q04

3Q04

1Q05

3Q05

E

1Q06

E

3Q06

E

1Q07

E

3Q07

E

1Q08

E

3Q08

E

1Q09

E

3Q09

E

1Q10

E

3Q10

E

1Q11

E

3Q11

E

1Q12

E

3Q12

E

1Q13

E

3Q13

E

1Q14

E

3Q14

E

1Q15

E

3Q15

E

PE - Naphtha PP - Naphtha Source: Espírito Santo Research Source: Espírito Santo Research

Risks

If oil prices remain at current soaring levels for a prolonged period of time, it may halt global growth, as the most part of consumer income is spent in fuel-related expenditures (transportation, energy, and heating, etc.), in addition to favoring the implementation of substitutes for plastics. Therefore, the demand for such products would be smaller, which would reduce the potential for margin expansion, thereby reducing operating rates, this being

The high in oil prices may decrease the world demand, thus creating a risk to the fly up.

18

Petrochemical Sector, Feb-06

the biggest threat to a fly-up. Current market conditions, which we’ll discuss later on, suggest that the all-time high level of feedstock prices has prevented a more substantial expansion of margins, even though the simple S/D imbalance could ustifiy bigger spreads.

Another issue that hovers over the sector, and more specifically over the prospect of favorable prices for producers, is the trajectory of global growth and especially the rate of China’s landing. China is currently the major driver of the global petrochemical commodities market (responsible for 50-60% of global resin imports), and, if it begins to show sign of slowing down (including any changes in economic policy) or if it implements policies that entail in inventory buying schedule oscillations (which it does for times), it may hamper the sector’s level of profitability. Specifically in Brazil, the “Chinese Threat” comes in another form: producers in that region, as previously mentioned, benefit from almost unmatchable competitiveness, and the appreciated exchange rate facilitates further the local market’s supply of such products, thereby affecting end demand. We will discuss the Chinese industry in greater detail further on.

As previously mentioned, the global petrochemical gameboard is currently being rearranged, with a clear shift towards Asia. This being the case, it is expected that the cash cost will fall, since the proportion of low-cost producers, like the Middle Eastern and Chinese, will increase. The effect of such trend may be the shrinkage of average global spreads, when gauged for those producers that run less competitive inputs (such as Naphtha ARA, for example) in their plants. In terms of cash cost, Brazil is on a similar level to that of the more competitive European producers (still better than global average); therefore, it is in a better shape than more than half the worldwide aggregated capacity. In any case, this is another aspect that will probably reduce the intensity of the margin peak in this high cycle.

Global and China’s growth can threaten resins’ demand In Brazil, the threat is the overwhelming influx of transformed products from China The global average cash cost is falling and can reduce the spreads for less competitive producers

CHART 31: Global Ethylene Production Costs - Geographical Comparison

0

100

200

300

400

500

600

Middle Eastern SE of Asia Latam Europe North of America

0%

20%

40%

60%

80%

100%

120%

Cash Cost/ton % of World Capacity (rig.)

Source: Espírito Santo Research and SRI

Lastly, we must point out one final risk that has largely escaped the market’s radar: the growth in the plastic recycling market (secondary). This market is still relatively small, focusing primarily on PET and HDPE, due to certain technical difficulties involving the separation and cleansing of less rigid plastics. Collecting recycled products (including plastics and paper, among others) is quite developed in Asia, taking advantage of a vast network of collectors among the poorer populations. PE recycling has also increased substantially and may cause a fall in the demand for PE products, especially when the end prices are throguh the roof

The proportion of recyclable plastics is considerably less today than those found for aluminum or glass, due mainly to a lesser range of uses for the product. As a result, the price for secondary products tends to be less than for primary products. However, when elevated oil prices force price increases along the petrochemical chain, a proliferation in the plastics market then becomes more economically viable.

Growth of secondary market: recycling

19

Petrochemical Sector, Feb-06

Why Has This Scenario Remained Elusive?

Since the beginning of 2004, all projections appeared fairly upbeat on the worldwide petrochemical front, despite the fact that the primary raw material (oil) continued to be a worrisome point. This belief was finally corroborated with the rise in prices and margins in the main products at the end of that year.

During 2H04, there were heavy stock build-ups in China in anticipation of higher crude prices and derivatives that propelled prices upwards and created expectations (to some extent unrealistic) that the petrochemical market was heading for exceptionally strong margins sooner than the most optimistic of fly-up projections had initially indicated, as we can see in table 34. In reality, the oscillations in Asian transformer inventories were the one variable overlooked. Just as the spread widening was overly sharp during 2H04, the correction (as we will explain below) was also markedly exaggerated, alarm ing the international community that soon began to dispute the notion that the sector would actually undergo a fly-up at all. Along the same line, investors began contemplating that the fly-up, with respect to margin peaks, would take place in 2004 rather than the inittally-expected 2006.

In the 2H04, there was a process of stock-buildup which increased demand and elevated prices... ... giving the impression that the fly-up would be greater and would occur sooner

CHART 32: Petrochemical Prices in SE of Asia (US D/ton)

CHART 33: Spreads in SE of Asia (USD/ton)

CHART 34: Recent Trend – PEBD Spread in Asia (US D/ton)

-

200

400

600

800

1,000

1,200

1,400

1,600

Jan-

02

May

-02

Sep

-02

Jan-

03

May

-03

Sep

-03

Jan-

04

May

-04

Sep

-04

Jan-

05

May

-05

Sep

-05

Jan-

06

HDPE LDPE PP Ethylene Prophylene

-

200

400

600

800

1,000

1,200

Jan-

02

May

-02

Sep

-02

Jan-

03

May

-03

Sep

-03

Jan-

04

May

-04

Sep

-04

Jan-

05

May

-05

Sep

-05

Jan-

06

HDPE LDPE Ethylene Prophylene PP

-

200

400

600

800

1,000

1,200

Jul-0

3

Sep

-03

Nov

-03

Jan-

04

Mar

-04

May

-04

Jul-0

4

Sep

-04

Nov

-04

Jan-

05

Mar

-05

May

-05

Jul-0

5

Sep

-05

Nov

-05

Jan-

06

Source: Espírito Santo Research and Bloomberg Source: Espírito Santo Research and Bloomberg Source: Espírito Santo Research

With the end of the stock build-up phase in November of 2004, the first inventory correction movement began, significantly pressuring the price of resins and affecting the 4Q04 results in the sector. Prices, however, did eventually begin to recover their upward trend at the end of Jan/05 with the return of the Chinese to the market, once again carrying inventories beyond the normal.

In Mar/05 Chinese traders began a second, and more marked stock correction (or rather clearance) that resulted in a profound reduction in the apparent Ethylene consumption of that country, turning China to a net exporter status. Such movement initially took Ethylene prices back to Jun/04 lows, with thermoplastic resins to follow suit soon after. That effect was magnified by the start-up of two plants in the region, adding capacity of 1,600 ktons/year. Though in itself not a significant number when compared to the total global capacity of approximately 112-114mn tons per year, it did contribute to the deterioration of the market and consequently had an effect on the results of 2Q05 as well as the sector’s shares pricing around the world.

In summary, it seems clear to us that the implosion of petrochemical prices, particularly in Asia, was a combination of an unforeseen variation in Chinese demand coupled with an erroneous reading of the market on the part of producers in the region who lapsed in their production discipline and kept their output elevated.

In the 1H05, China there was heavy inventory clearances, causing China to become a net exporter of Ethylene, thereby reducing prices and margins in Asia Weak 1H05 prices = stock correction + little production discipline +weak primary demand

20

Petrochemical Sector, Feb-06

CHART 35: Net Imports vs. Ethylene Spread – China Effect

CHART 36: Apparent Resin Consumption and Ethylene Consumption in China (ktons)

0

100

200

300

400

500

600

700

800

900

Dec

-03

Jan-

04

Feb

-04

Mar

-04

Apr

-04

May

-04

Jun-

04

Jul-0

4

Aug

-04

Sep

-04

Oct

-04

Nov

-04

Dec

-04

Jan-

05

Feb

-05

Mar

-05

Apr

-05

May

-05

Jun-

05

Jul-0

5

Aug

-05

Sep

-05

US

$/to

n

(25)

(20)

(15)

(10)

(5)

0

5

10

15

20

25

kto

ns

Net Importations (rig.) Korean Ethylene Price

810 8 2 3 883742 739724 778 775788 7716 8 6 758 7767947029 2 7 828 7789591,0031,0229 9 1

6 6 8 6 2 9660

6 8 96 3 65966 4 16076 2 76 2 5

6 3 5649 618 5 8 7

556

672639 641

708 735 751 7 6 0

510 557627

6 0 36 0 2560

572 5 6 8 5 6 5593545

614 5 9 9 5 8 56 3 2

6 9 0623 5 9 4

6 0 06 3 5 6 9 5 719

0

500

1,000

1,500

2,000

2,500

3,000

Dec

-03

Jan-

04

Feb

-04

Mar

-04

Apr

-04

May

-04

Jun-

04

Jul-0

4

Aug

-04

Sep

-04

Oct

-04

Nov

-04

Dec

-04

Jan-

05

Feb

-05

Mar

-05

Apr

-05

May

-05

Jun-

05

Jul-0

5A

ug-0

5

Sep

-05

0

125

250

375

500

625

750

PE PP PVC Ethylene Production (rig.)

Source: Espírito Santo Research and ISI Source: Espírito Santo Research and ISI

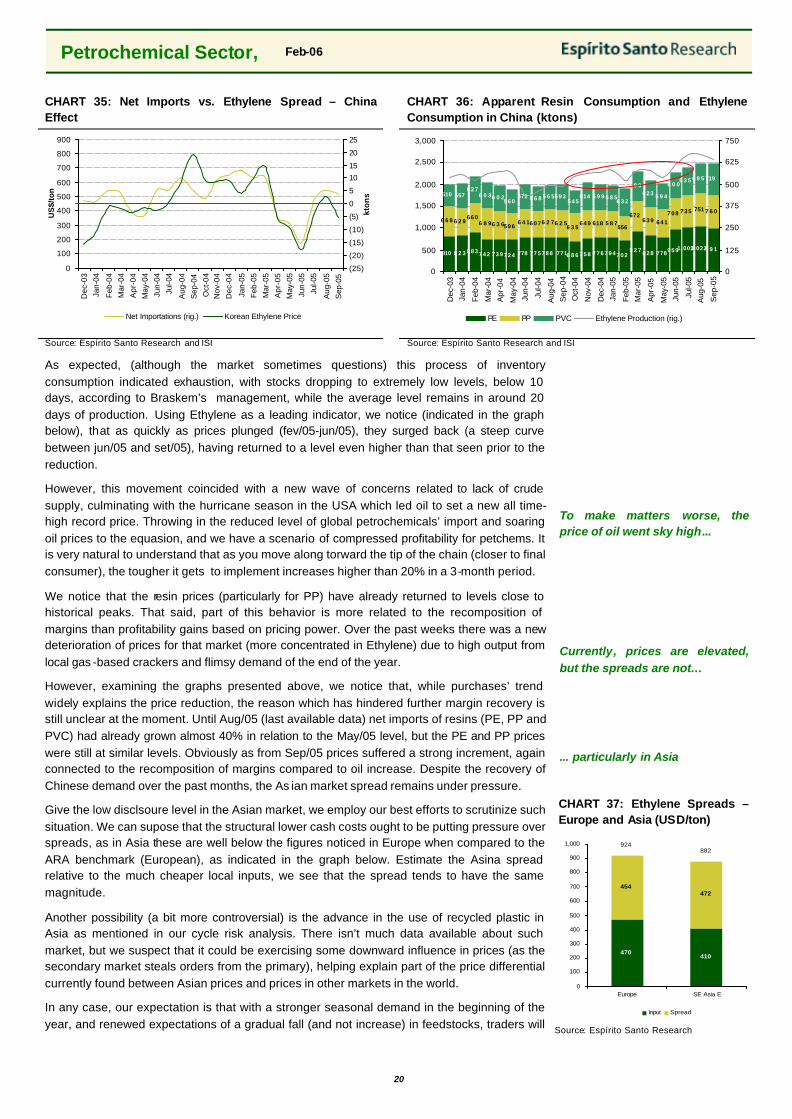

As expected, (although the market sometimes questions) this process of inventory consumption indicated exhaustion, with stocks dropping to extremely low levels, below 10 days, according to Braskem’s management, while the average level remains in around 20 days of production. Using Ethylene as a leading indicator, we notice (indicated in the graph below), that as quickly as prices plunged (fev/05-jun/05), they surged back (a steep curve between jun/05 and set/05), having returned to a level even higher than that seen prior to the reduction.

However, this movement coincided with a new wave of concerns related to lack of crude supply, culminating with the hurricane season in the USA which led oil to set a new all time-high record price. Throwing in the reduced level of global petrochemicals’ import and soaring oil prices to the equasion, and we have a scenario of compressed profitability for petchems. It is very natural to understand that as you move along torward the tip of the chain (closer to final consumer), the tougher it gets to implement increases higher than 20% in a 3-month period.

We notice that the resin prices (particularly for PP) have already returned to levels close to historical peaks. That said, part of this behavior is more related to the recomposition of margins than profitability gains based on pricing power. Over the past weeks there was a new deterioration of prices for that market (more concentrated in Ethylene) due to high output from local gas -based crackers and flimsy demand of the end of the year.

However, examining the graphs presented above, we notice that, while purchases’ trend widely explains the price reduction, the reason which has hindered further margin recovery is still unclear at the moment. Until Aug/05 (last available data) net imports of resins (PE, PP and PVC) had already grown almost 40% in relation to the May/05 level, but the PE and PP prices were still at similar levels. Obviously as from Sep/05 prices suffered a strong increment, again connected to the recomposition of margins compared to oil increase. Despite the recovery of Chinese demand over the past months, the As ian market spread remains under pressure.

Give the low disclsoure level in the Asian market, we employ our best efforts to scrutinize such situation. We can supose that the structural lower cash costs ought to be putting pressure over spreads, as in Asia these are well below the figures noticed in Europe when compared to the ARA benchmark (European), as indicated in the graph below. Estimate the Asina spread relative to the much cheaper local inputs, we see that the spread tends to have the same magnitude.

Another possibility (a bit more controversial) is the advance in the use of recycled plastic in Asia as mentioned in our cycle risk analysis. There isn’t much data available about such market, but we suspect that it could be exercising some downward influence in prices (as the secondary market steals orders from the primary), helping explain part of the price differential currently found between Asian prices and prices in other markets in the world.

In any case, our expectation is that with a stronger seasonal demand in the beginning of the year, and renewed expectations of a gradual fall (and not increase) in feedstocks, traders will

To make matters worse, the price of oil went sky high...

Currently, prices are elevated, but the spreads are not...

... particularly in Asia

CHART 37: Ethylene Spreads – Europe and Asia (USD/ton)

470410

454472

924882

0

100

200

300

400

500

600

700

800

900

1,000

Europe SE Asia E

Input Spread

Source: Espírito Santo Research

21

Petrochemical Sector, Feb-06

return to the market - purchasing, which could bring sounder figures for the spreads.

And what about China?

Due to the growing importance of China in the world commodities market (it wouldn’t be any different for resins), we deem relevant to include a specific section on the country in our discussion.

CMAI estimates the Chinese market demands in Ethylene equivalent terms of around 18 mm ton/year in the form of polymers. The resins production capacity (including PE, PP and PVC) adds to something close to 9mn tons/year and the PE alone is responsible for almost 5mm ton/year. As for Ethylene, these figures are a bit below 8 mm ton/year, so that we estimate China should be self-sufficient in less than 40% of its needs of derivatives, importing the remaining amount.

This imported volume has been presenting a considerable evolution, continuously increasing the country’s presence in the international market of resins, for which it is estimated that China is responsible for 50-60% of purchases despite having only 7% and 9% global capacity of PE and PP. For PE, in 2004 China’s net importing needs was of 4,8mm tons, considering the total world exports close to 9mm tons of equivalent Ethylene (~53%).

China requires ~18mn tons/year of equivalent Ethylene and needs to import more than 60% of it Representing 50-60% of the global importations

CHART 38: PE Production, NAC and Imports CHART 39: PP Production, NAC and Imports

0

100

200

300

400

500

600

700

800

Dec

-03

Jan-

04

Feb-

04

Mar

-04

Apr

-04

May

-04

Jun-

04

Jul-0

4

Aug

-04

Sep

-04

Oct

-04

Nov

-04

Dec

-04

Jan-

05

Feb-

05

Mar

-05

Apr

-05

May

-05

Jun-

05

Jul-0

5

Aug

-05

Sep

-05

050

100150

200

250300

350

400450

500550

Production CAN Net ImportationsNAC

Source: Espírito Santo Research and ISI Source: Espírito Santo Research and ISI

The main petrochemicals suppliers to China are the neighboring countries, namely South Korea, Taiwan, Thailand and Japan apart from shipments from the Middle East.

CHART 40: Ethylene Equivalent Chinese Market (mn tons) CHART 41: China’s Imports Market Share (2004)

-

2

4

6

8

10

12

14

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005E0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Domestic Production Consumption Net Import. % Auto sufficiency

South Korea

20%

Taiwan14%

Middle Eastern12%

Tailand11%

Japan10%

Cingapura9%

USA8%

Malasia6%

India4%

Russia4%

Others2%

Source: Espírito Santo Research and CMAI

Source: Espírito Santo Research and Polymerupdate

0

200

400

600

800

1,000

1,200

Dec

-03

Jan-

04

Feb

-04

Mar

-04

Apr

-04

May

-04

Jun-

04

Jul-0

4

Aug

-04

Sep

-04

Oct

-04

Nov

-04

Dec

-04

Jan-

05

Feb

-05

Mar

-05

Apr

-05

May

-05

Jun-

05

Jul-0

5