Embed Size (px)

Citation preview

More AboutMedicare and

Changes in 2014

A Public Service Presentation Provided by the Society of Certified Senior

Advisors® (SCSA)

Agenda• Common misconceptions • Differences among Medicare Parts A, B, C

and D; Medigap• Enrollment • Medicare: 2014 changes • Valuable resources

Common Misconceptions • “Medicare is free and covers everything.”• “Medicare Part A with a Medigap policy is enough.”• “I can enroll in Medicare whenever I want to.” • My doctor will tell me what I need for Medicare

coverage.”• “Medicare will cover my long-term care.”

What Seniors Are Saying . . .

• “I turn 65 next year and I’m counting on my Medicare to replace my current insurance. There are so many moving parts to Medicare, I’m confused.” • “Where would I find

information to help me understand my Medicare insurance benefits?”

Benefits of Understanding Medicare• CSAs – – Learn and share

knowledge; guide seniors to

resources– Increase client

loyalty and trust – Assist their own

families

Seniors• Make better decisions for their health care, short- and long-term

Medicare - Since 1965… • Changes in coverage• Increasing premiums• More out-of-pocket expenses• Added prescription drug coverage• Healthcare Reform

Do you think things might keep changing?

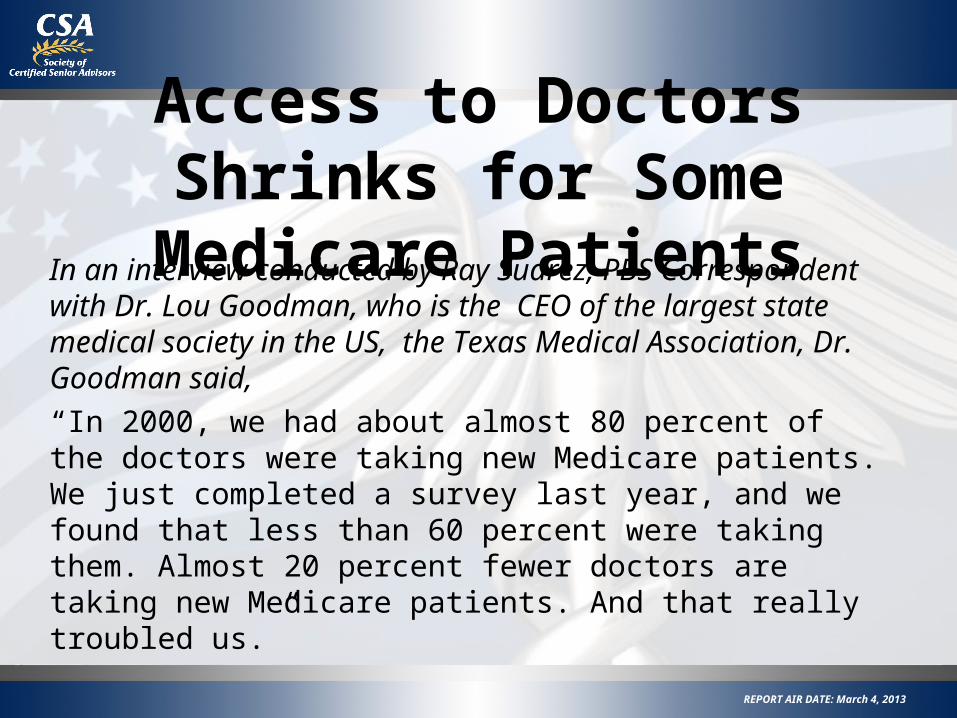

Access to Doctors Shrinks for Some Medicare Patients

In an interview conducted by Ray Suarez, PBS Correspondent with Dr. Lou Goodman, who is the CEO of the largest state medical society in the US, the Texas Medical Association, Dr. Goodman said, “In 2000, we had about almost 80 percent of the doctors were taking new Medicare patients. We just completed a survey last year, and we found that less than 60 percent were taking them. Almost 20 percent fewer doctors are taking new Medicare patients. And that really troubled us.”

REPORT AIR DATE: March 4, 2013

What is Medicare?Medicare is health insurance for people:

•Age 65 or older

•Under age 65 with certain disabilities

•Any age with End-Stage Renal Disease (ESRD) -- permanent kidney failure requiring dialysis or a kidney transplant

Medicare’s GoalTo make it easy for you to get the highest quality health care at the most affordable price.

To transform itself from a program which simply pays the bills to a program which actively supports a high quality health care system.

A

BCDMedigap

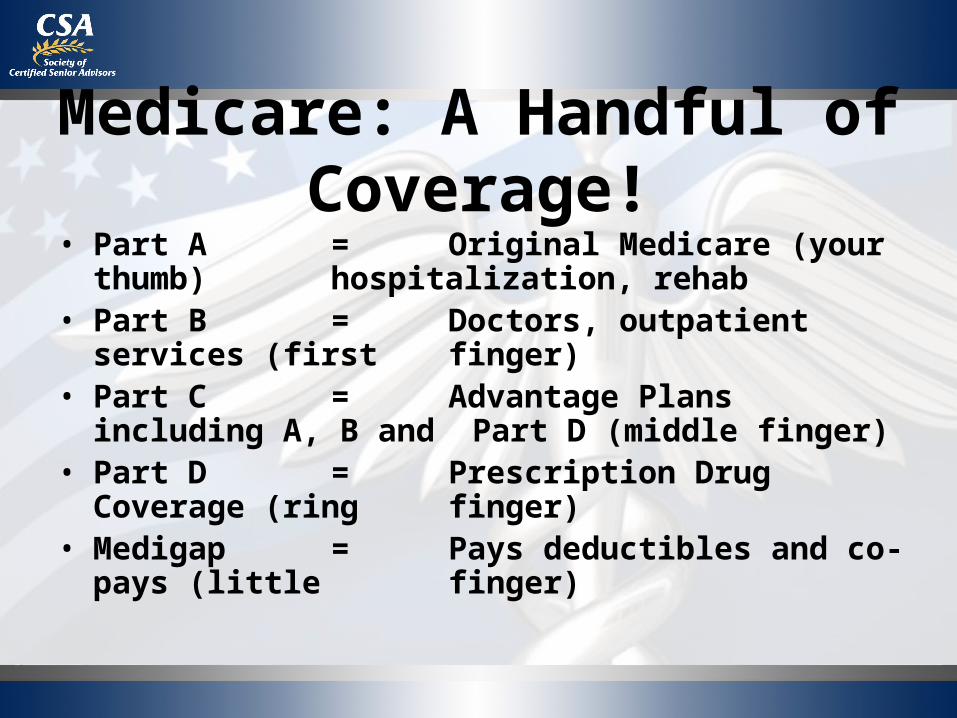

Medicare: A Handful of Coverage!• Part A = Original Medicare (your thumb)

hospitalization, rehab• Part B = Doctors, outpatient services (first

finger)• Part C = Advantage Plans including A, B

and Part D (middle finger)• Part D = Prescription Drug Coverage (ring

finger) • Medigap = Pays deductibles and co-pays

(little finger)

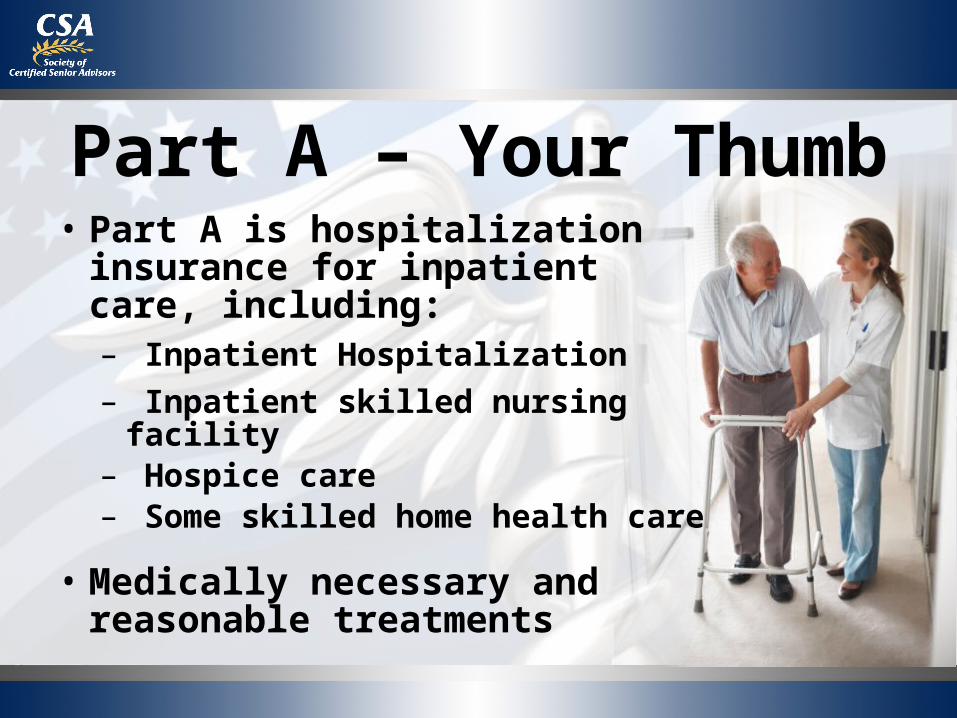

Part A – Your Thumb• Part A is hospitalization insurance

for inpatient care, including: – Inpatient Hospitalization– Inpatient skilled nursing facility – Hospice care– Some skilled home health care

• Medically necessary and reasonable treatments

Part A continued• Must show significant improvement or

become ineligible for more coverage

• Entitlement program; majority of beneficiaries do not pay premiums

Part A + Employer PlanFor seniors who continue to work:

• Comprehensive

• Both plans pay; one is primary provider

• The Group health plan pays before Medicare pays

Small Group Plans <20• Less than 20 employees • Medicare is primary, employer plan is

secondary, both are billed• When a person has an employer plan from

their employer or spouse’s employer they should usually enroll in Part B to cover out of pocket costs.

Large Group Health Plans >20• More employees• The large employee group plan is

considered the primary with Medicare secondary.

• If the employee has group coverage or is covered by a spouse’s plan they may not need Part B

Which Plan Pays First?At the time claim is submitted --• Employer plan administrator• Health care provider• Medicare . . .

Determine which plan is the primary coverage based on Medicare rules

2014 Part A Costs• Most people don’t pay a Part A premium

because they paid Medicare taxes while working. If you don’t get premium-free Part A, you pay up to $426 each month depending on how many “credits” you have for working.

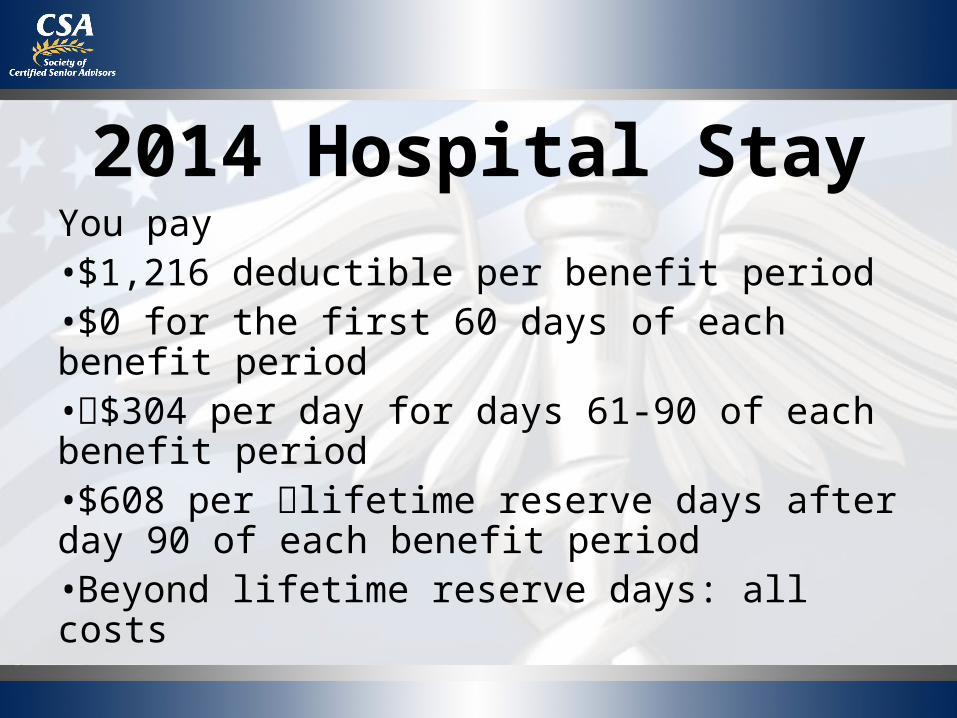

2014 Hospital StayYou pay•$1,216 deductible per benefit period•$0 for the first 60 days of each benefit period•$304 per day for days 61-90 of each benefit period•$608 per lifetime reserve days after day 90 of each benefit period•Beyond lifetime reserve days: all costs

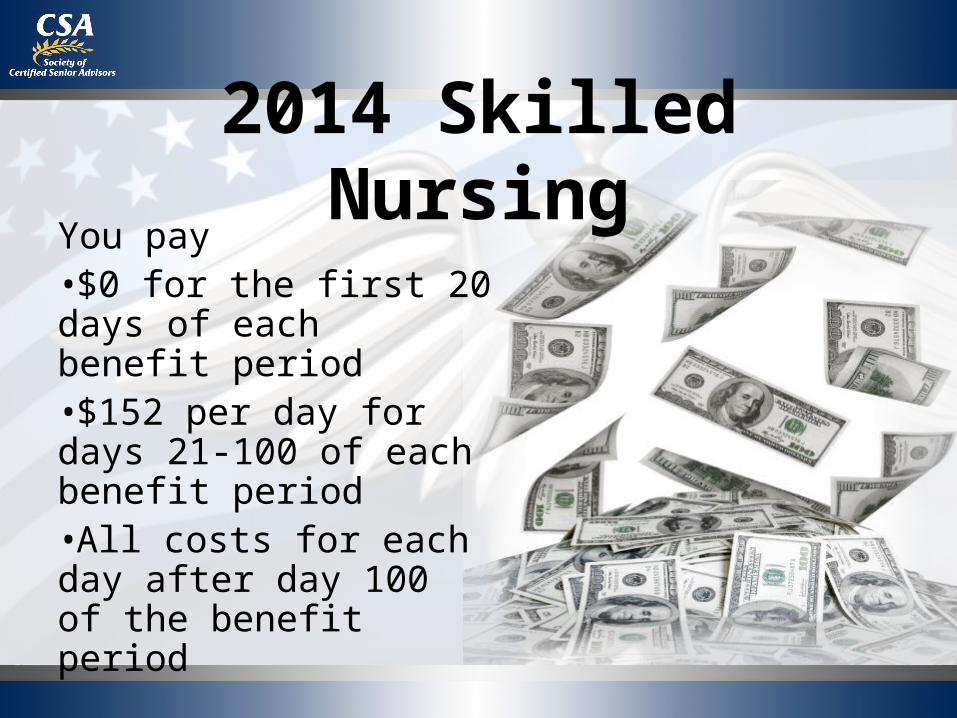

2014 Skilled NursingYou pay•$0 for the first 20 days of each benefit period•$152 per day for days 21-100 of each benefit period•All costs for each day after day 100 of the benefit period

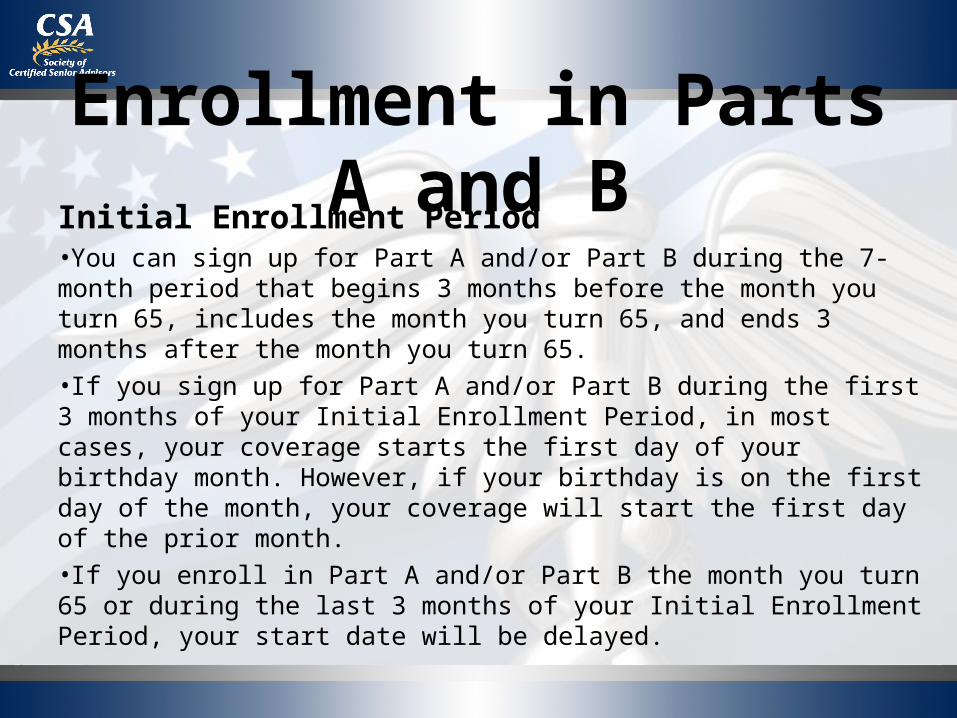

Enrollment in Parts A and BInitial Enrollment Period•You can sign up for Part A and/or Part B during the 7-month period that begins 3 months before the month you turn 65, includes the month you turn 65, and ends 3 months after the month you turn 65.•If you sign up for Part A and/or Part B during the first 3 months of your Initial Enrollment Period, in most cases, your coverage starts the first day of your birthday month. However, if your birthday is on the first day of the month, your coverage will start the first day of the prior month.•If you enroll in Part A and/or Part B the month you turn 65 or during the last 3 months of your Initial Enrollment Period, your start date will be delayed.

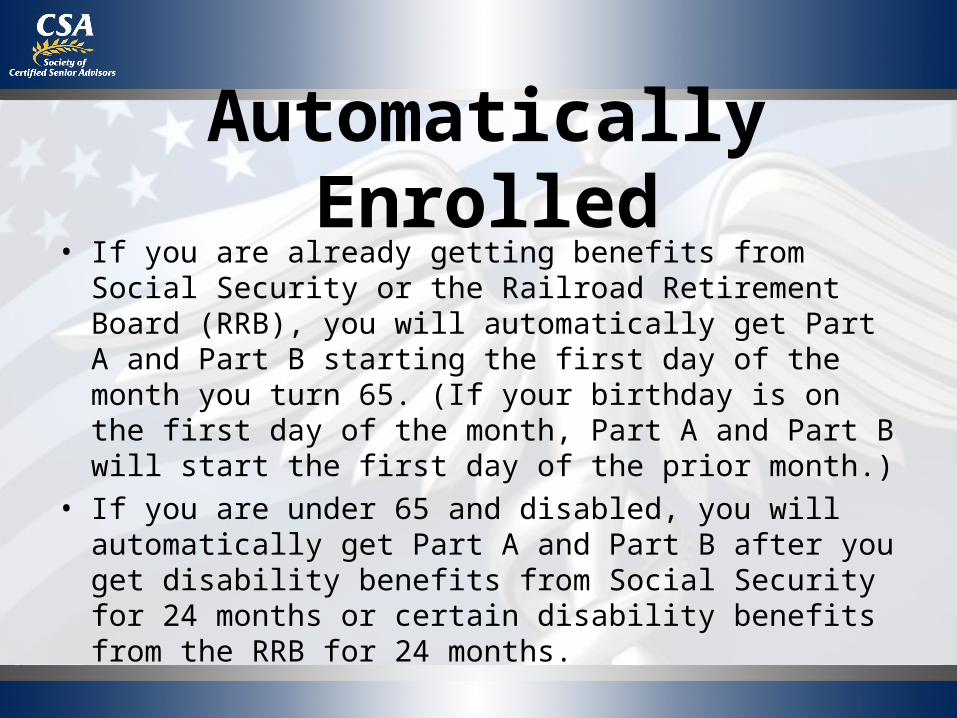

Automatically Enrolled• If you are already getting benefits from Social Security or the

Railroad Retirement Board (RRB), you will automatically get Part A and Part B starting the first day of the month you turn 65. (If your birthday is on the first day of the month, Part A and Part B will start the first day of the prior month.)

• If you are under 65 and disabled, you will automatically get Part A and Part B after you get disability benefits from Social Security for 24 months or certain disability benefits from the RRB for 24 months.

General EnrollmentIf you did not sign up for Part A and/or Part B (for which you must pay premiums) when you were first eligible, you can sign up between January 1–March 31 each year. Your coverage will begin July 1. You may have to pay a higher Part A and/or Part B premium for late enrollment.

Special Enrollment• If you did not sign up for Part A and/or Part B when you were

first eligible because you are covered under a group health plan based on current employment (your own, a spouse's, or a family member’s if you are disabled), you can sign up for Part A and/or Part B

• Anytime you are still covered by the group health plan.• During the 8-month period that begins the month after the

employment ends or the coverage ends, whichever happens first.

Part B – First Finger• Medically necessary services– Doctor services– Preventive care– Durable medical equipment– Home “health” care– X-rays, Labs, Ambulance

services– Therapy (PT, OT, ST)

2014 Part B Costs• Monthly PremiumYou pay a Part B premium each month - $104.90. Most

people will pay the standard premium amount. However, if your modified adjusted gross income as reported on your IRS tax return from 2 years ago is above a certain amount, you may pay more.

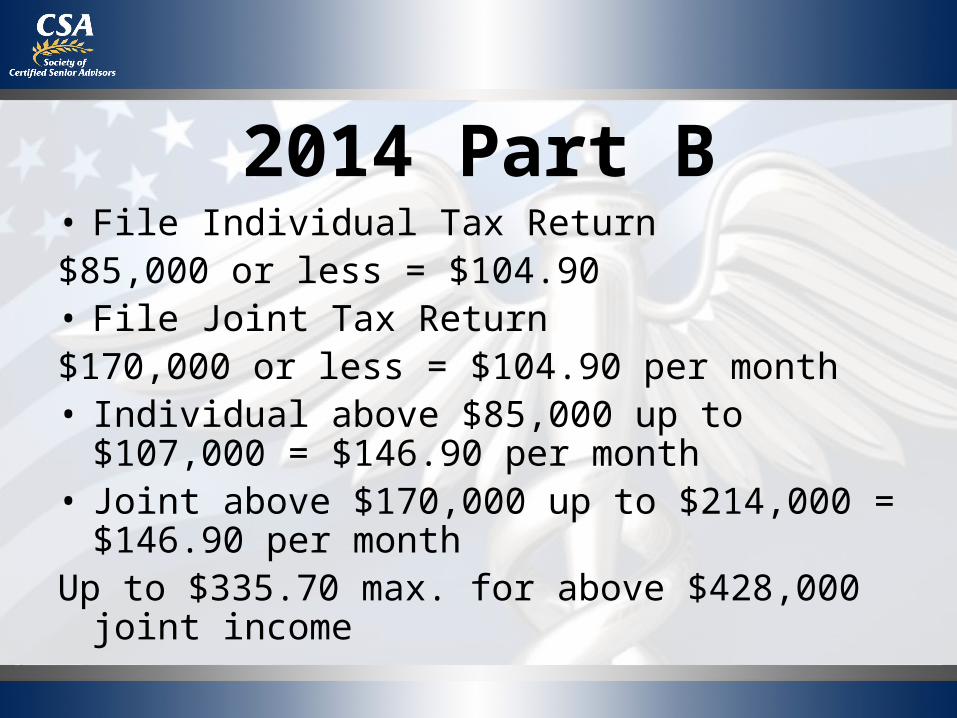

2014 Part B• File Individual Tax Return$85,000 or less = $104.90• File Joint Tax Return$170,000 or less = $104.90 per month• Individual above $85,000 up to $107,000 = $146.90

per month• Joint above $170,000 up to $214,000 = $146.90 per

monthUp to $335.70 max. for above $428,000 joint income

Part C – Middle Finger• Called Medicare Advantage Plans• Cover Parts A and B plus provide additional

coverage• Offered by private companies

Voluntary program; Part C premiums (if any) are paid directly to plan provider; senior must still pay Part B premiums, too

Part C - Medicare Advantage continued

• More coverage than Parts A and B, especially preventive services

• Vision exams and eyeglasses• Dental• Health and wellness programs• Rx (most include Medicare

drug prescriptions)

Think of Part C as brick and mortar…Parts A & B are at the left entrance, all services in the

middle building and you enter from the right entrance to access services.

2014 Part C • Visit www.medicare.gov/find-a-plan to get

plan premiums. You can also call• 1.800.MEDICARE (1-800-633-4227). TTY users

should call 1.877.486.2048.• You can also call the plan or your State Health

Insurance Assistance Program

Enroll or Change Part CIf you want to enroll in, withdraw from, or switch your enrollment in a Medicare Advantage (Medicare Part C) plan, you are allowed to do so -- without any restrictions from the insurance companies based on your age or health history -- during what is called "open enrollment." When you have open enrollment depends on what you want your next coverage to be.

Part D – Ring Finger• Prescription Drug Plan – 2004

• Helps cover the cost of prescription drugs

• Run by Medicare-approved private insurance companies.

• Must have Parts A and B

• Must live in plan’s service area

Part D ContinuedMedicare Part D Plans vary in cost and coverage by State - this means that if you move to a new State during the enrollment year, you may pay a different premium and/or possibly may not have access to the same selection of Medicare Part D plans.

http://www.q1medicare.com/PartD-Medicare-PartD-Overview-by-State.php

• Good overview• List of states• Find plans

Enrollment in Part D• People who are new to Medicare have a seven (7) month period

(called an Initial Enrollment Period) to enroll in a Medicare Part D or Medicare Advantage plan. This window begins 3 months before your month of eligibility, and includes your month of eligibility and three months thereafter. Example: If you turn 65 on July 13th. Your month of Medicare eligibility is July. Your Initial Enrollment Period (IEP) is April to October. If you were to enroll between April 1 and June 31, your plan would take effect on July 1. If you enroll between July 1 and October 31, your plan would take effect the first day of the month after you enroll.

Late Enrollment or Changes• Between October 15 – December 7 anyone can join, switch,

or drop Medicare Advantage Plan. Your coverage will begin on January 1, as long as the plan gets your request by December 7.

• Leave Medicare Advantage for Medicare Part A and Part B• To withdraw from a Medicare Advantage plan and return to

traditional Medicare Part A and Part B, you may do so from January 1 to February 14, 2014. If you do, and your Medicare Advantage plan covered prescription drugs, during the same period you may also enroll in a Medicare Part D prescription drug plan.

2014 Part D Premiums• File Individual Tax Return $85,000 or less or

File Joint Tax Return $170,000 or less, Pay the plan premium

• Depending on income, up to a max of $69.30 per month per person and there may be additional premiums for higher earners.

Part D CostsPlans vary in cost and drugs covered• Co-pays or coinsurance• Deductibles• Monthly premiums• Drug costs

Voluntary program; senior pays premiums out-of-pocket or premiums are included in Part C Medicare Advantage Plan

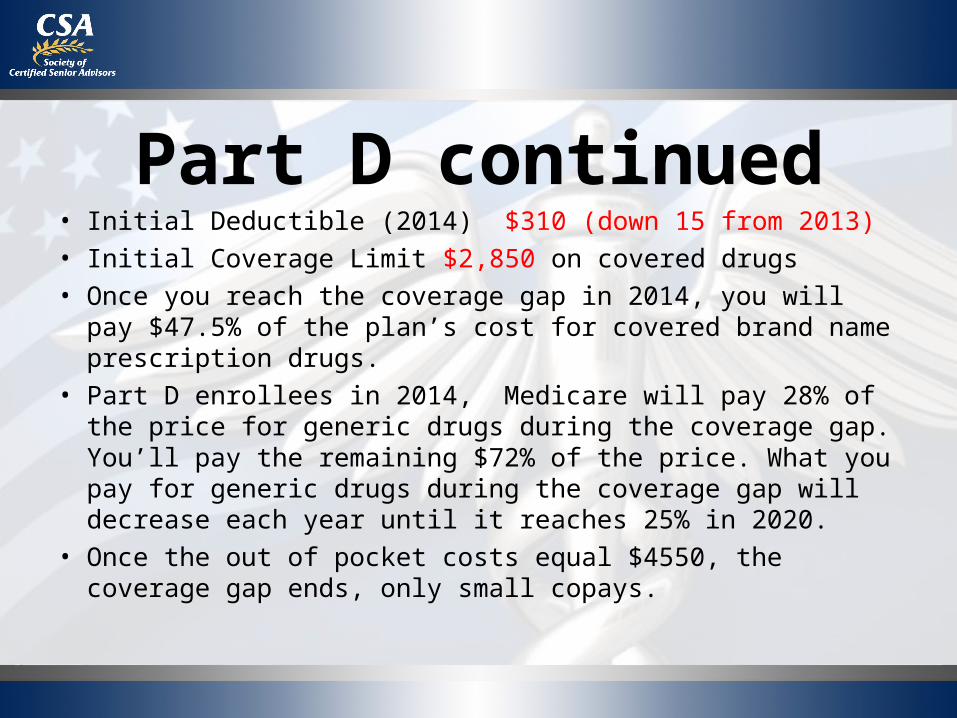

Part D continued• Initial Deductible (2014) $310 (down 15 from 2013)• Initial Coverage Limit $2,850 on covered drugs• Once you reach the coverage gap in 2014, you will pay $47.5%

of the plan’s cost for covered brand name prescription drugs.• Part D enrollees in 2014, Medicare will pay 28% of the price

for generic drugs during the coverage gap. You’ll pay the remaining $72% of the price. What you pay for generic drugs during the coverage gap will decrease each year until it reaches 25% in 2020.

• Once the out of pocket costs equal $4550, the coverage gap ends, only small copays.

Medigap – Little Finger• Also called Medicare Supplement Plans

• Sold by private insurance agents

• MUST have Parts A and B to buy

• Covers only 1 person

Medigap Continued• Helps pay costs that

Parts A and B don’t:– Co-pays– Coinsurance– Deductibles

Voluntary program; senior pays for it

Medigap Continued• 10 Standardized plans – A through N

A is basic coverage; more in the others, some offer out-of-country coverage, most popular to cover most costs is plan F.

Medigap Continued• Medigap plans are sold by private insurers.

Rates for the plans vary by insurer and state, but federal rules require that all plans with the same letter must offer the same coverage.

Medigap Plans continued• Cost varies

Don’t need a Medigap plan if you have a Part C Medicare Advantage plan

Purchasing Medigap Policy• You have a one-time 6-month Medigap Open

Enrollment Period which starts the first month you’re 65 and enrolled in Part B. This period gives you a guaranteed right to buy any Medigap policy sold in your state regardless of your health status. You will be underwritten if you change plans.

New in 2014

Medicare now covers:•Depression screenings•Screening and counseling for alcohol misuse•Screening and counseling for obesity •Behavioral therapy for cardiovascular disease

Last Thoughts…Median age: total: 37.2 years male: 35.8 years female: 38.5 years (2012 est.)

This entry is the age that divides a population into two numerically equal groups; that is, half the people are younger than this age and half are older. It is a single index that summarizes the age distribution of a population. Source: CIA World Factbook

Life Expectancy• In the late 1800s American men and women had

about equal life expectancies of 40 to 48 years.• It depends on gender and geography. In the U.S.,

women live longer—81 years on average, 76 for men—but a recent study by the Institute for Health Metrics and Evaluation reveals a promising trend. While women gained 2.7 years from 1989 to 2009, men are catching up, gaining 4.6 years.

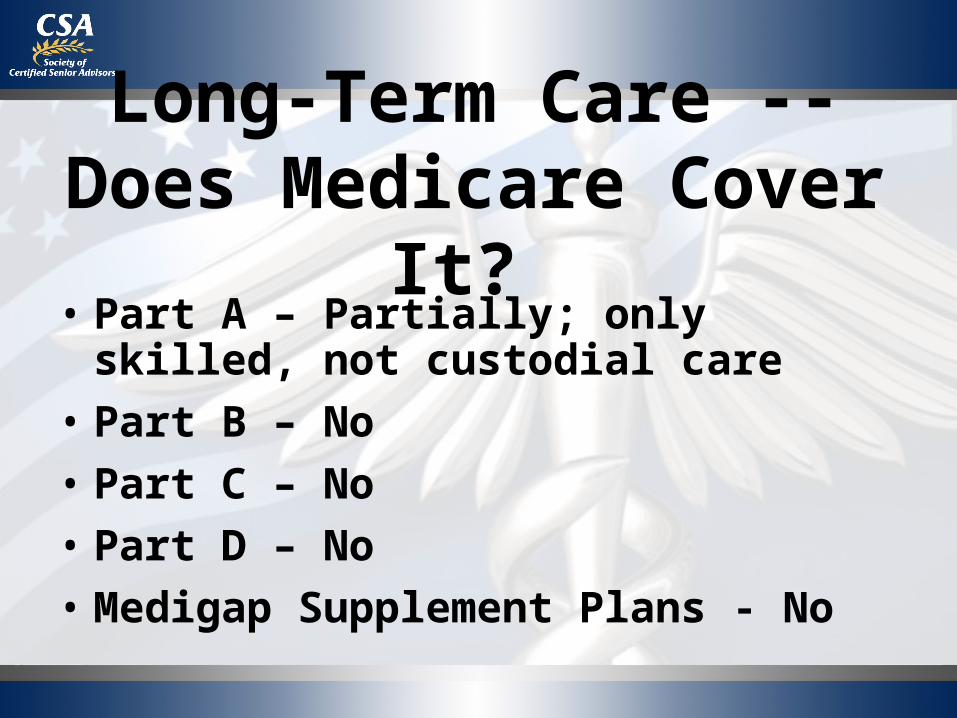

Long-Term Care -- Does Medicare Cover It?

• Part A – Partially; only skilled, not custodial care

• Part B – No• Part C – No• Part D – No• Medigap Supplement Plans - No

Valuable Resources1-800-MEDICAREwww.medicare.gov

Medicare & You 2013 Handbookhttp://www.medicare.gov/Publications/Pubs/pdf/10050.pdf

Where to Get Your Medicare Questions Answered

ResourcesPresentation provided by Nancy A. Dykeman, CSANancy is a professional speaker, instructor, long-term care consultant, CSA faculty member and independent insurance agent. She has been working with families and issues of aging for 30 years. Before entering the insurance industry, Nancy was the owner and manager of a funeral service, a licensed nursing home administrator and the director of an assisted living facility. Her depth of knowledge in long-term care has been enriched by her own experience caring for family members.