Embed Size (px)

Citation preview

For data requests, please contact:Moody's Global Client [email protected]

CONTACTS

This monthly report contains collateral performance metrics for 41 structured finance sectors around the world: 12 asset classes in

September 30, 2010

1 March 2013

Global Structured Finance Collateral Performance Review

Please send comments, questions, andrequests to be on our distribution list to:[email protected]

This monthly report contains collateral performance metrics for 41 structured finance sectors around the world: 12 asset classes in the US, 19 in Europe, seven in Japan, two in Australia and one in Canada. The report contains typical aggregate performance metrics such as delinquencies and losses, as well as sector‐specific metrics such as residential and commercial property prices, loans in special servicing, refinancing profiles, average WARF levels, senior OC levels, payment rates, and excess spread. We also include the underlying data, as well as sector commentary and outlooks, and projected losses by vintage where applicable.

Print All TabsPrint All Tabs

More about the report

Who should I contact to be added to the distribution list?

What is Moody's RMBS Loss Tracker?

How does the report differ from what is currently offered in the market?

Where can I get more information on an index?

Moody's Global Structured Finance Collateral Performance Review presents the underlying collateral performance o

What does the report offer?

Why do cumulative losses sometimes decline at the end of the seasoning curve?

When is the report available?

How is the data as-of date defined?What is the data source behind each index?

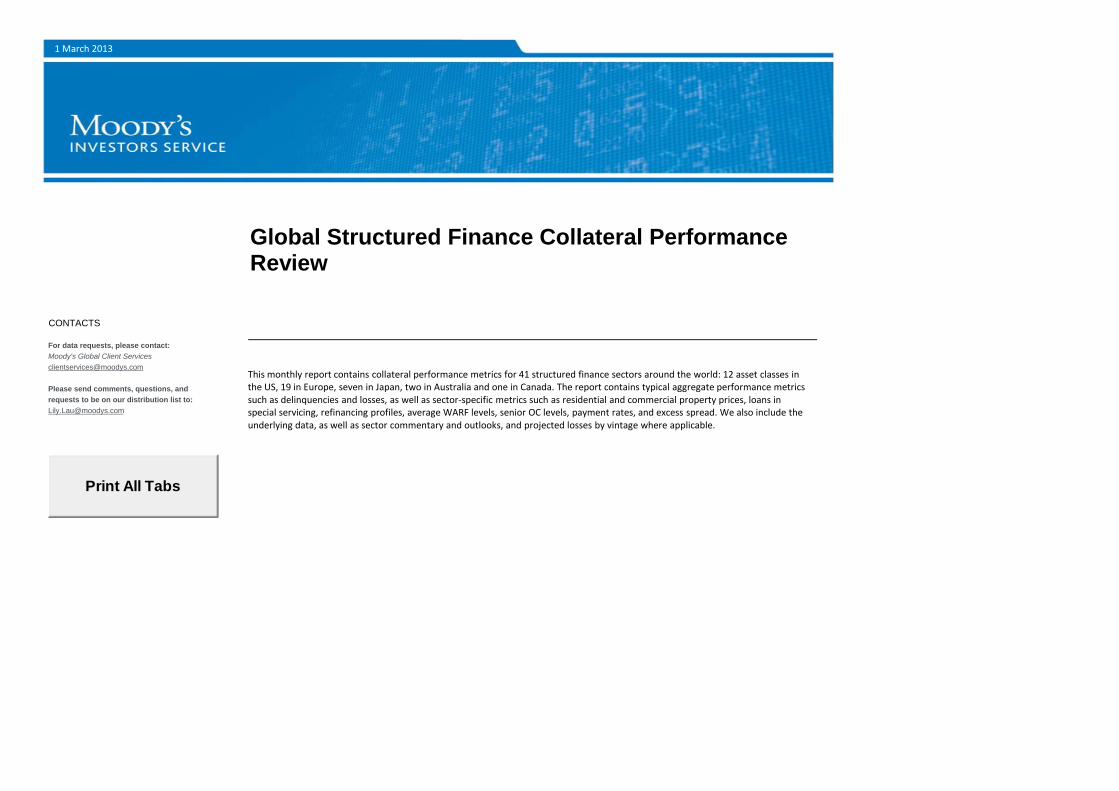

Table of Contents

Page # Title As of Date Report Frequency Contacts3 US Subprime RMBS Dez 12 Monthly Peter McNally Debash Chatterjee Amita Shrivastava4 US Alt-A RMBS Dez 12 Monthly Peter McNally Debash Chatterjee Amita Shrivastava5 US Option ARM RMBS Dez 12 Monthly Peter McNally Debash Chatterjee Amita Shrivastava6 US Jumbo RMBS Dez 12 Monthly Peter McNally Debash Chatterjee Amita Shrivastava7 US Subprime CES RMBS Dez 12 Monthly Peter McNally Debash Chatterjee Amita Shrivastava8 US Prime CES RMBS Dez 12 Monthly Peter McNally Debash Chatterjee Amita Shrivastava9 US HELOC RMBS Dez 12 Monthly Peter McNally Debash Chatterjee Amita Shrivastava

10 US Home Prices Jan 13 Monthly Peter McNally Debash Chatterjee Amita Shrivastava11 UK NC RMBS Nov 12 Quarterly Johannes Ebner Barbara Rismondo12 UK Prime RMBS Nov 12 Quarterly Johannes Ebner Barbara Rismondo13 Spanish RMBS Dez 12 Quarterly Johannes Ebner Barbara Rismondo14 Dutch RMBS Dez 12 Quarterly Johannes Ebner Barbara Rismondo15 Italian RMBS Nov 12 Quarterly Johannes Ebner Barbara Rismondo16 Irish RMBS Okt 12 Quarterly Johannes Ebner Barbara Rismondo17 South African RMBS Sep 12 Semi-annually Johannes Ebner Barbara Rismondo18 Greek RMBS Nov 12 Quarterly Johannes Ebner Barbara Rismondo19 UK Buy-To-Let RMBS Nov 12 Quarterly Johannes Ebner Barbara Rismondo20 Portuguese RMBS Okt 12 Quarterly Johannes Ebner Barbara Rismondo21 German RMBS Okt 12 Semi-annually Johannes Ebner Barbara Rismondo22 French RMBS Sep 12 Semi-annually Johannes Ebner Barbara Rismondo23 Belgian RMBS Dez 12 Semi-annually Johannes Ebner Barbara Rismondo24 European Home Prices Jan 13 Monthly Johannes Ebner25 Japanese RMBS Dez 12 Monthly Mieko Nakamura26 Australian Prime RMBS Dez 12 Monthly Bryan Reid27 Australian Non-conforming RMBS Dez 12 Monthly Bryan Reid28 Australian Home Prices Jan 13 Monthly Bryan Reid29 US CMBS Jan 13 Monthly Kevin Fagan30 EMEA CMBS Feb 13 Quarterly Viola Karoly31 Japanese CMBS Jan 13 Monthly Koji Kumamaru32 US Autos - prime Dez 12 Monthly Sarah Huang McGinnis Caldwell33 EMEA Autos Nov 12 Quarterly Johannes Ebner Carole Gintz34 US Cards (part1) Jan 13 Monthly Sarah Huang Jeff Hibbs35 US Cards (part2) Jan 13 Monthly Sarah Huang Jeff Hibbs36 UK Cards (part1) Nov 12 Quarterly Johannes Ebner Alex Cataldo37 UK Cards (part2) Nov 12 Quarterly Johannes Ebner Alex Cataldo38 Canadian Cards (part1) Mrz 12 Quarterly Raymond Lai39 Canadian Cards (part2) Mrz 12 Quarterly Raymond Lai40 US Private Student Loan Sep 12 Quarterly Sarah Huang Tracy Rice41 Spanish ABS SME Sep 12 Quarterly Johannes Ebner Carole Gintz42 European Consumer Loan Okt 12 Quarterly Johannes Ebner Carole Gintz43 Italian Leasing Jul 12 Quarterly Johannes Ebner Carole Gintz44 Japanese ABS Dez 12 Monthly Mieko Nakamura45 Global CLOs (part1) Dez 12 Monthly Oktay Veliev Min Xu Guillaume Jolivet46 Global CLOs (part2) Dez 12 Monthly Oktay Veliev Min Xu Guillaume Jolivet

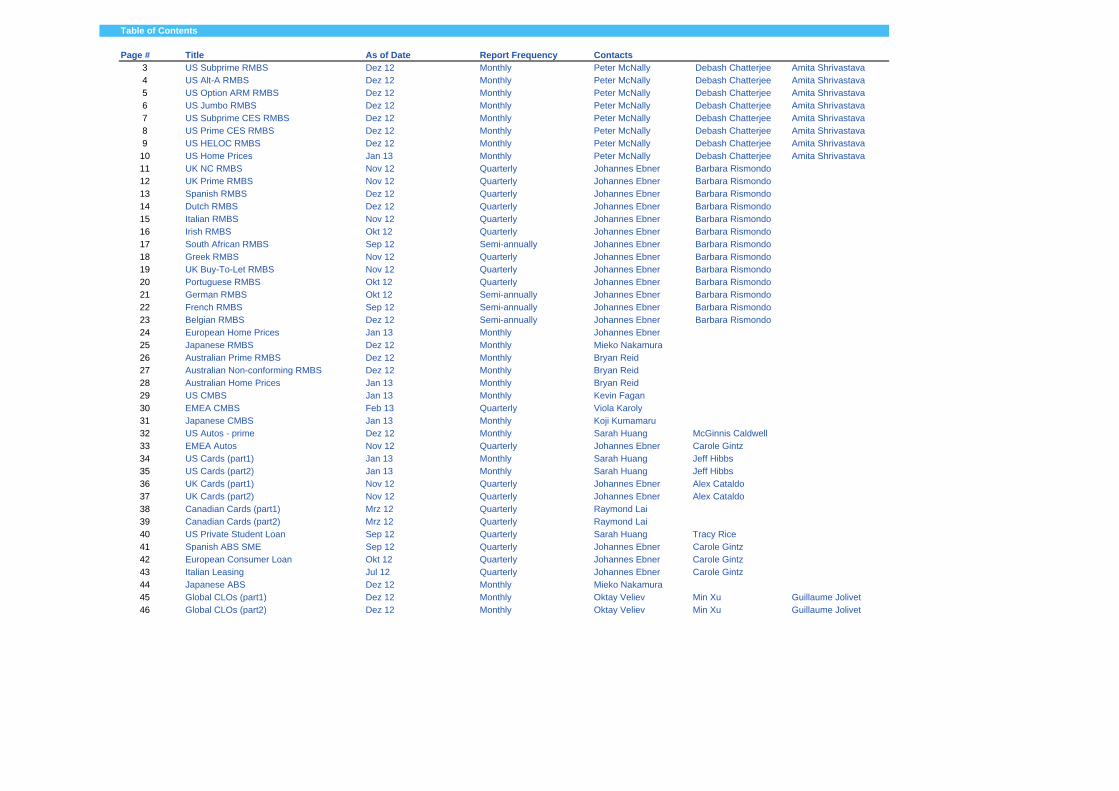

US First Lien Subprime RMBS Loan Performance Page 3As of Dez 12 Link: U.S. Home Equity Index Composite:January 2013 Reporting Period

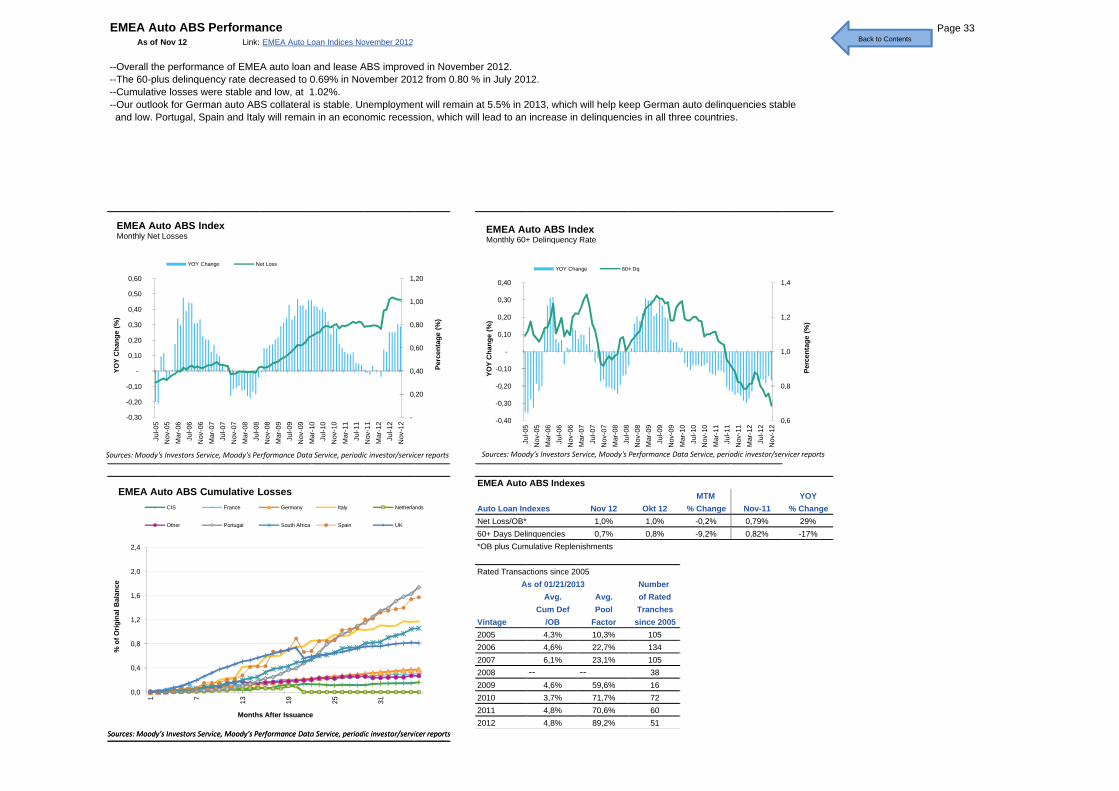

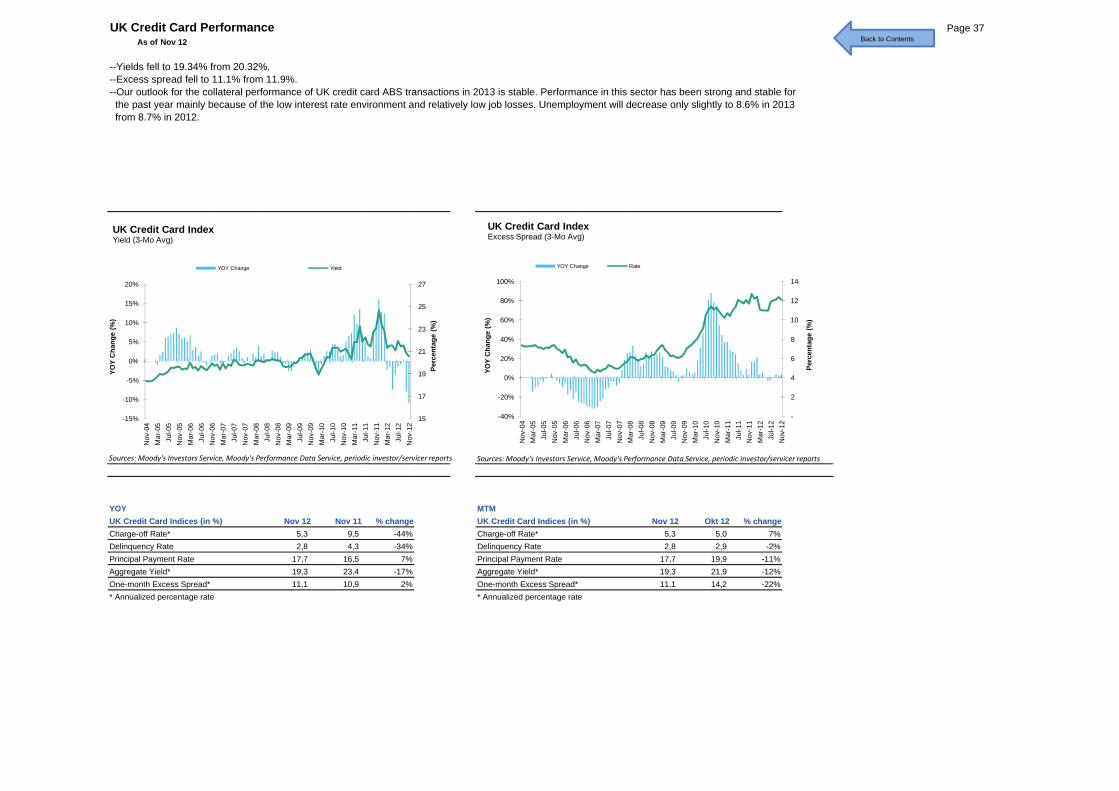

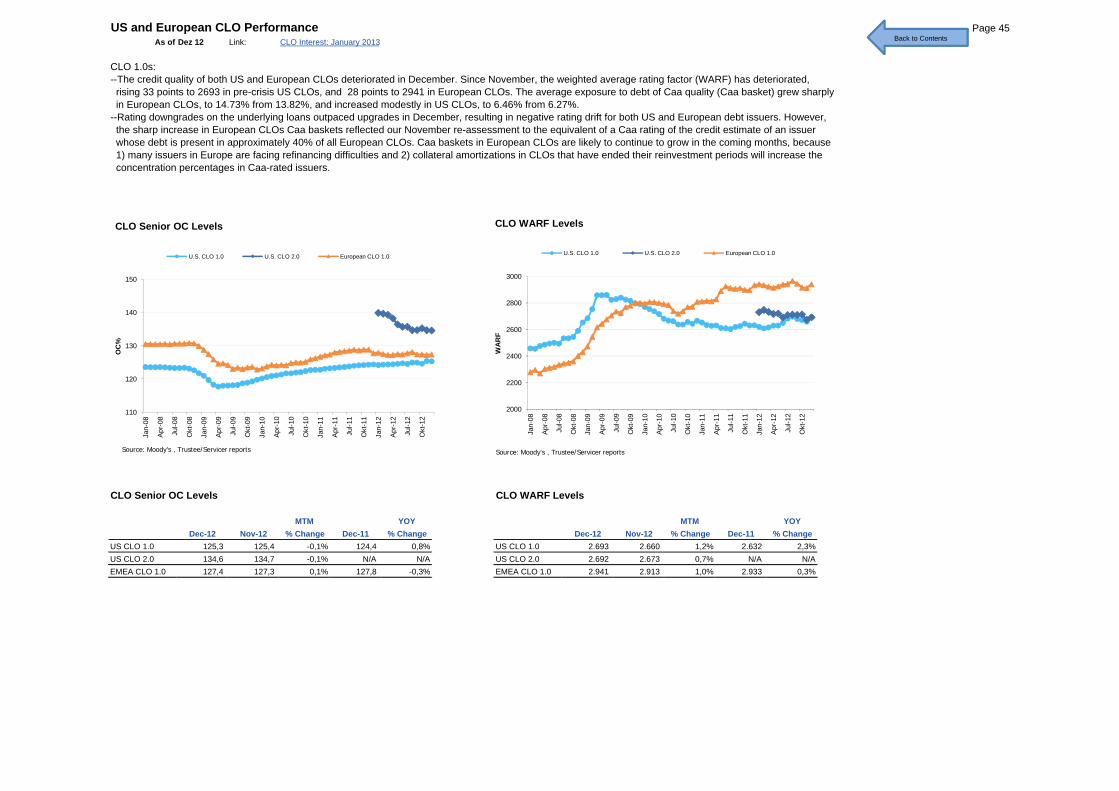

-- In December 2012, subprime mortgage delinquency rates declined while net losses rose.-- The 60-plus delinquency rate index fell to 35.9% from 36.2% in November.-- The net loss rate index increased to 9.95% from 9.43%.-- Although performance varies by transaction, the overall performance of 2005-08 vintage subprime RMBS has improved over the past year. Average delinquencies remain high, but the proportion of current borrowers becoming delinquent for the first time is declining. -- In some transactions, delinquencies have declined more quickly than we had previously forecast. Also, in some transactions, some of the bonds with payment priority have paid down more quickly than we had previously projected.

8%

12%

16%

20%

24%

28%

32%

% o

f Orig

inal

Bal

ance

U.S. First Lien Subprime RMBS 60+ Day Delinquencies

1999 2000 2001 2002 2003

2004 2005 2006 2007

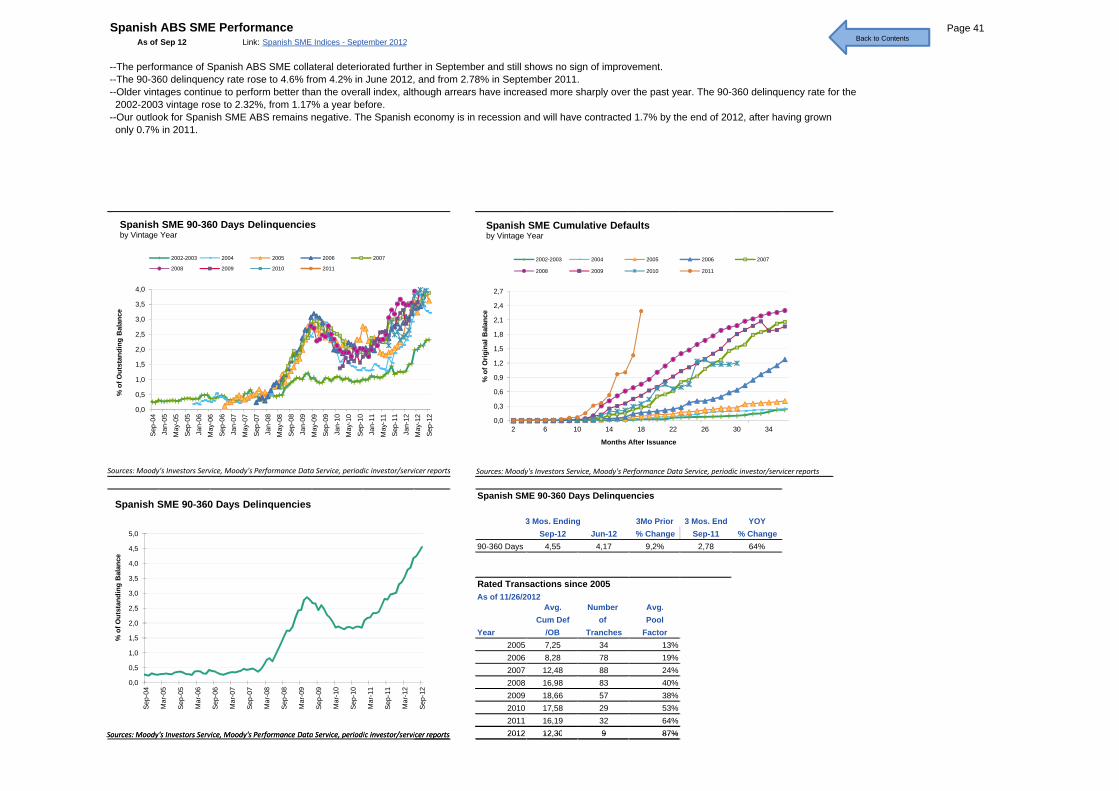

10%

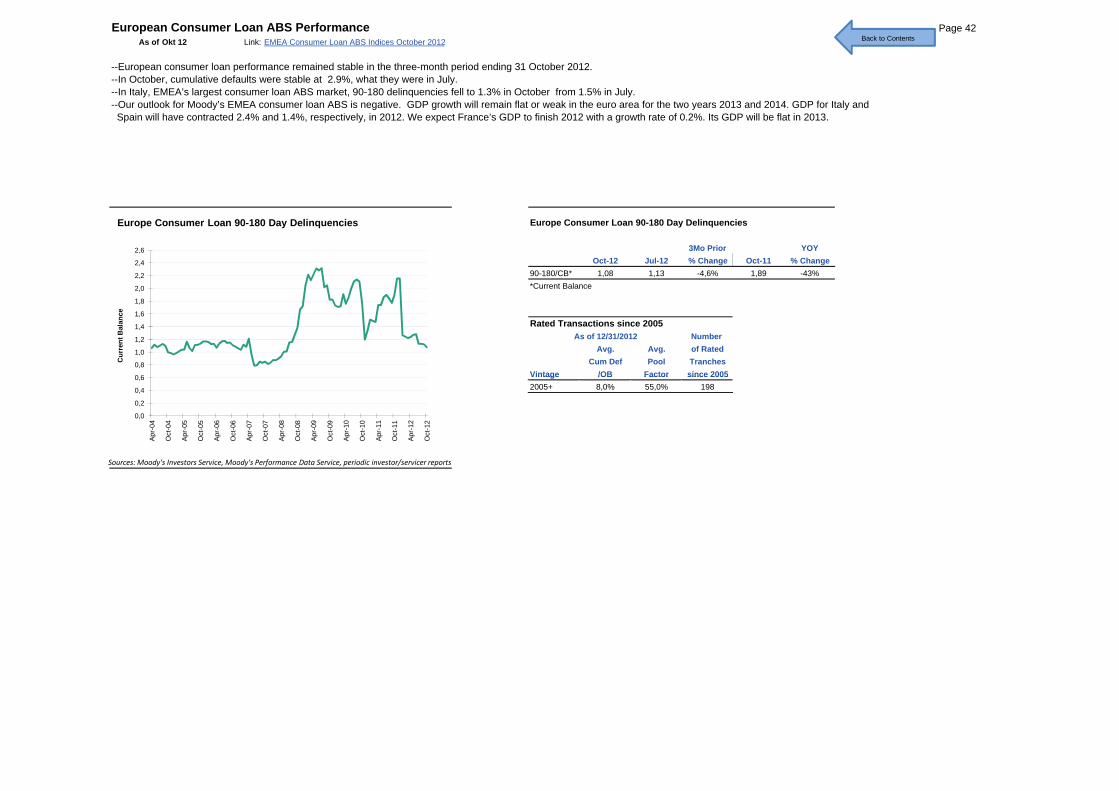

15%

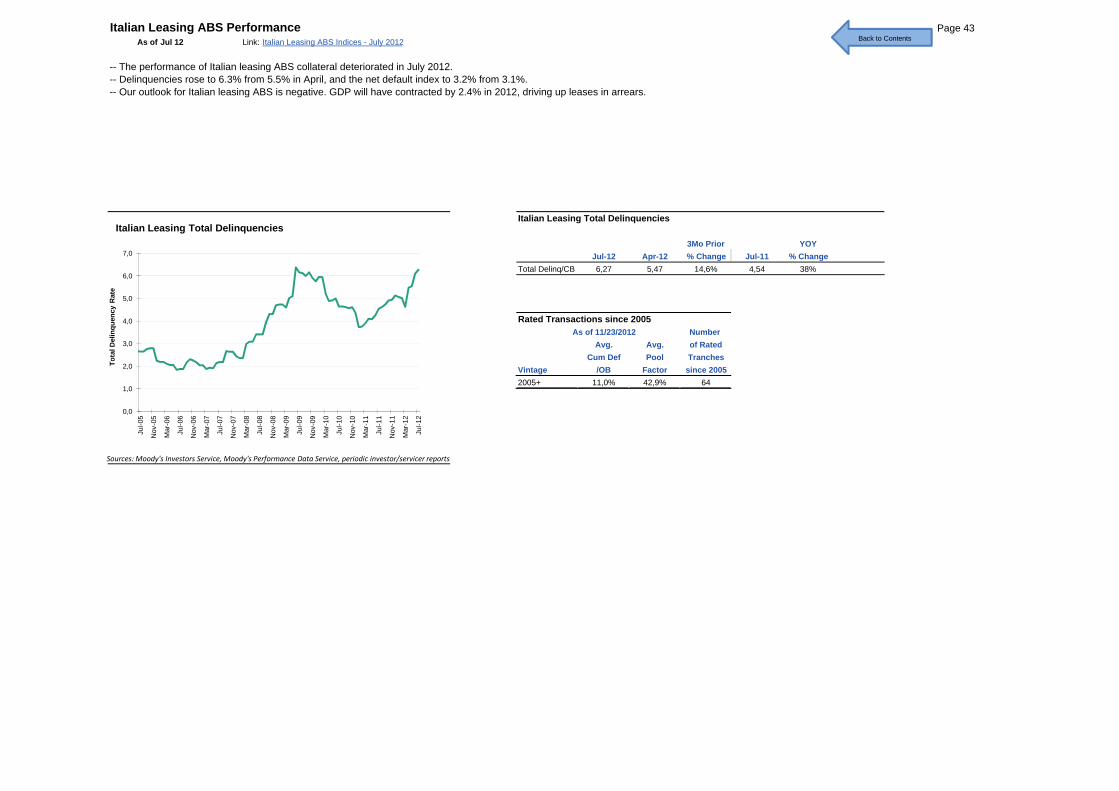

20%

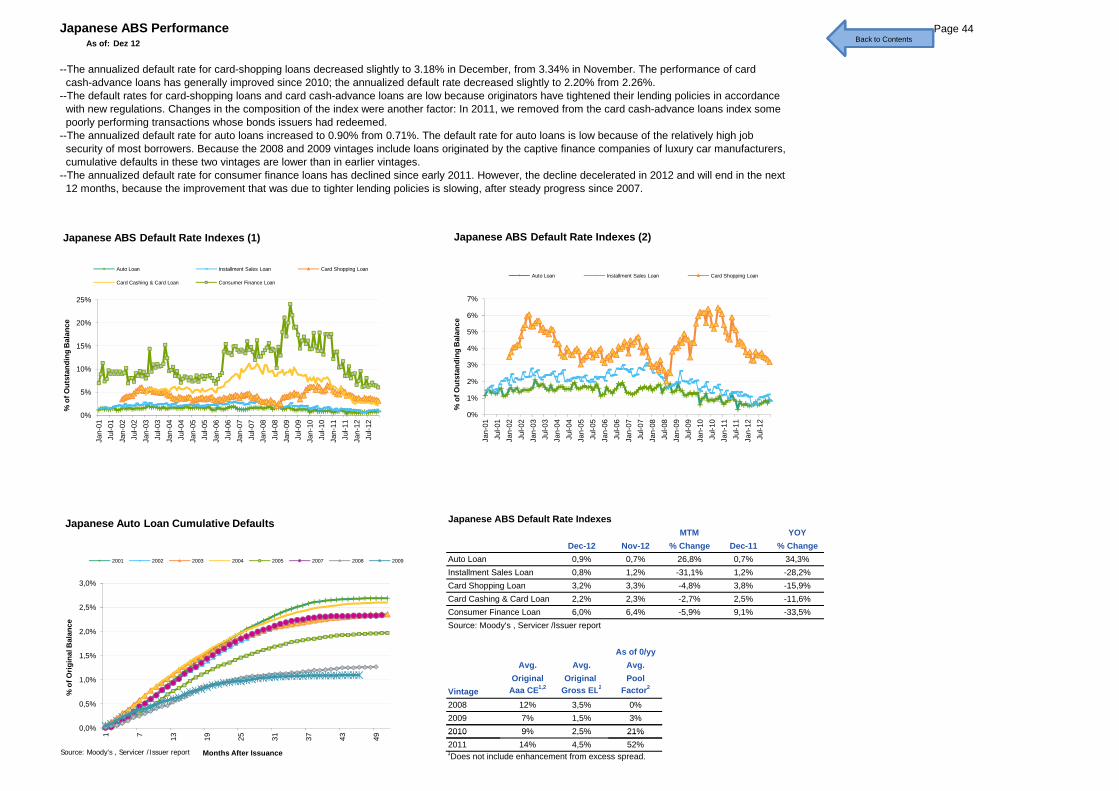

25%

30%

% o

f Orig

inal

Bal

ance

U.S. First Lien Subprime RMBS Cumulative Losses

1999 2000 2001 2002 2003

2004 2005 2006 2007

Back to Contents

Moody's US First Lien Subprime RMBS IndexesMTM YOY

Dec-12 Nov-12 % Change Dec-11 % Change60+ Del. 35,9% 36,2% -0,7% 39,3% -8,6%Net Loss 9,95% 9,43% 5,5% 9,13% 8,9%

As of 7/12 As of 0/yyAvg. Avg. Number Estimated Realized Bond

Cumulative Pool of Rated Principal WritedownsVintage Proj. Loss Factor Tranches $ (mil) % Orig.2005 18,6% 14,9% 5.590 $17.688 4.2%2006 38,7% 26,4% 6.486 $61.219 14.2%2007 48 6% 42 0% 3 049 $25 825 14 5%

As of 1/25/13

0%

4%

8%

12%

3 9 15 21 27 33 39 45 51 57 63 69 75 81 87 93

% o

f Ori

Months After Issuance

0%

5%

10%

3 9 15 21 27 33 39 45 51 57 63 69 75 81 87 93

% o

f Or

Months After Issuance

0%

2%

4%

6%

8%

10%

12%

14%

16%

0%

6%

12%

18%

24%

30%

36%

42%

48%

Apr-

01O

ct-0

1Ap

r-02

Oct

-02

Apr-

03O

ct-0

3Ap

r-04

Oct

-04

Apr-

05O

ct-0

5Ap

r-06

Oct

-06

Apr-

07O

ct-0

7Ap

r-08

Oct

-08

Apr-

09O

ct-0

9Ap

r-10

Oct

-10

Apr-

11O

ct-1

1Ap

r-12

Oct

-12

Ann

ualiz

ed N

et L

oss

Rat

e

60+

Day

Del

inqu

ency

Rat

e

U.S. First Lien Subprime RMBS Indexes60+ Delinquent/Outstanding Net Loss/Outstanding

Sources: Moody's Investors Service, Moody's Analytics

12,3%

26,3%

29,0%

3,3%

7,0%

10,8%

2,9%

5,4%

8,8%

2005

2006

2007

Subprime RMBS Loss Tracker

Loss To Date Pipeline Loss Remaining Loss

18.6%

38.7%

48.6%

Sources: Moody's Investors Service, Moody's Analytics Sources: Moody's Investors Service, Moody's Analytics

2007 48,6% 42,0% 3.049 $25.825 14.5%Sources: Moody's Investors Service, Moody's Analytics

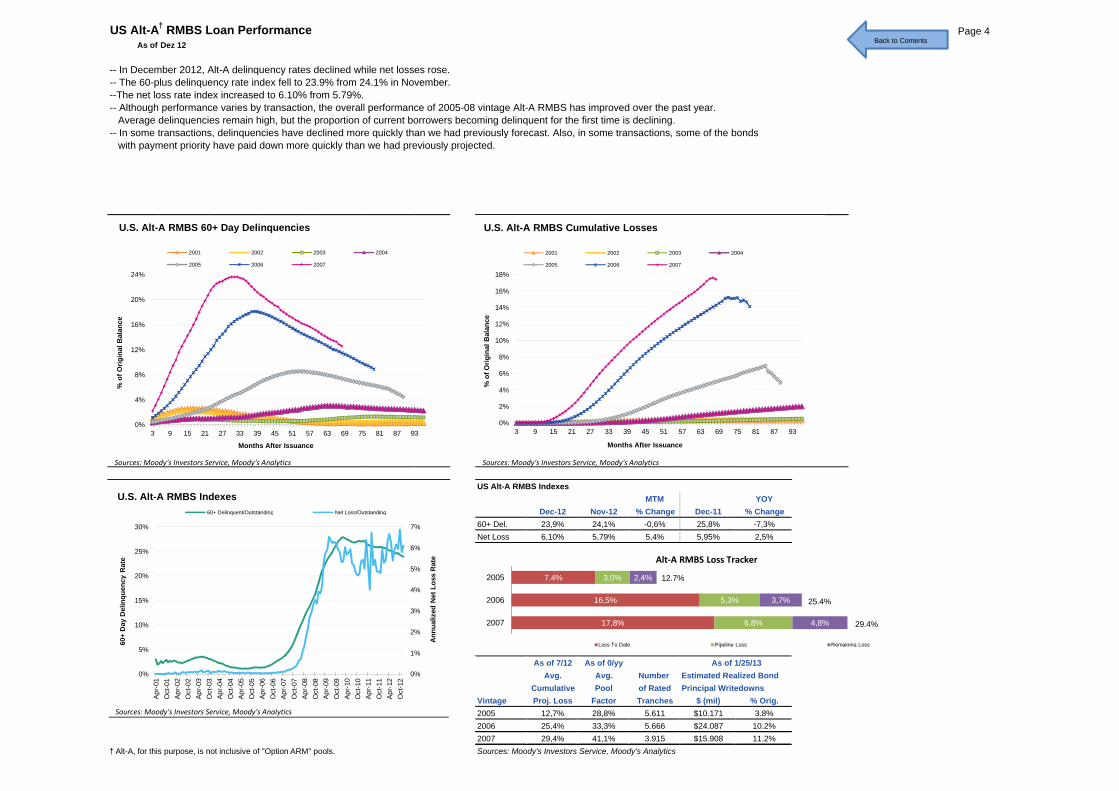

US Alt-A† RMBS Loan Performance Page 4As of Dez 12

-- In December 2012, Alt-A delinquency rates declined while net losses rose.-- The 60-plus delinquency rate index fell to 23.9% from 24.1% in November.--The net loss rate index increased to 6.10% from 5.79%.-- Although performance varies by transaction, the overall performance of 2005-08 vintage Alt-A RMBS has improved over the past year. Average delinquencies remain high, but the proportion of current borrowers becoming delinquent for the first time is declining. -- In some transactions, delinquencies have declined more quickly than we had previously forecast. Also, in some transactions, some of the bonds with payment priority have paid down more quickly than we had previously projected.

8%

12%

16%

20%

24%

of O

rigin

al B

alan

ce

U.S. Alt-A RMBS 60+ Day Delinquencies

2001 2002 2003 2004

2005 2006 2007

6%

8%

10%

12%

14%

16%

18%

of O

rigin

al B

alan

ce

U.S. Alt-A RMBS Cumulative Losses

2001 2002 2003 2004

2005 2006 2007

Back to Contents

US Alt-A RMBS IndexesMTM YOY

Dec-12 Nov-12 % Change Dec-11 % Change60+ Del. 23,9% 24,1% -0,6% 25,8% -7,3%Net Loss 6,10% 5,79% 5,4% 5,95% 2,5%

As of 7/12 As of 0/yyAvg. Avg. Number Estimated Realized Bond

Cumulative Pool of Rated Principal WritedownsVintage Proj. Loss Factor Tranches $ (mil) % Orig.2005 12,7% 28,8% 5.611 $10.171 3.8%2006 25,4% 33,3% 5.666 $24.087 10.2%

% % $ %

As of 1/25/13

7,4%

16,5%

17,8%

3,0%

5,3%

6,8%

2,4%

3,7%

4,8%

2005

2006

2007

Alt‐A RMBS Loss Tracker

Loss To Date Pipeline Loss Remaining Loss

12.7%

25.4%

29.4%

0%

4%

8%

12%

3 9 15 21 27 33 39 45 51 57 63 69 75 81 87 93

% o

f Orig

in

Months After Issuance

0%

2%

4%

6%

8%

3 9 15 21 27 33 39 45 51 57 63 69 75 81 87 93

% o

f Orig

in

Months After Issuance

0%

1%

2%

3%

4%

5%

6%

7%

0%

5%

10%

15%

20%

25%

30%

Apr-

01O

ct-0

1Ap

r-02

Oct

-02

Apr-

03O

ct-0

3Ap

r-04

Oct

-04

Apr-

05O

ct-0

5Ap

r-06

Oct

-06

Apr-

07O

ct-0

7Ap

r-08

Oct

-08

Apr-

09O

ct-0

9Ap

r-10

Oct

-10

Apr-

11O

ct-1

1Ap

r-12

Oct

-12

Ann

ualiz

ed N

et L

oss

Rat

e

60+

Day

Del

inqu

ency

Rat

e

U.S. Alt-A RMBS Indexes60+ Delinquent/Outstanding Net Loss/Outstanding

Sources: Moody's Investors Service, Moody's Analytics

Sources: Moody's Investors Service, Moody's Analytics Sources: Moody's Investors Service, Moody's Analytics

2007 29,4% 41,1% 3.915 $15.908 11.2%† Alt-A, for this purpose, is not inclusive of "Option ARM" pools. Sources: Moody's Investors Service, Moody's Analytics

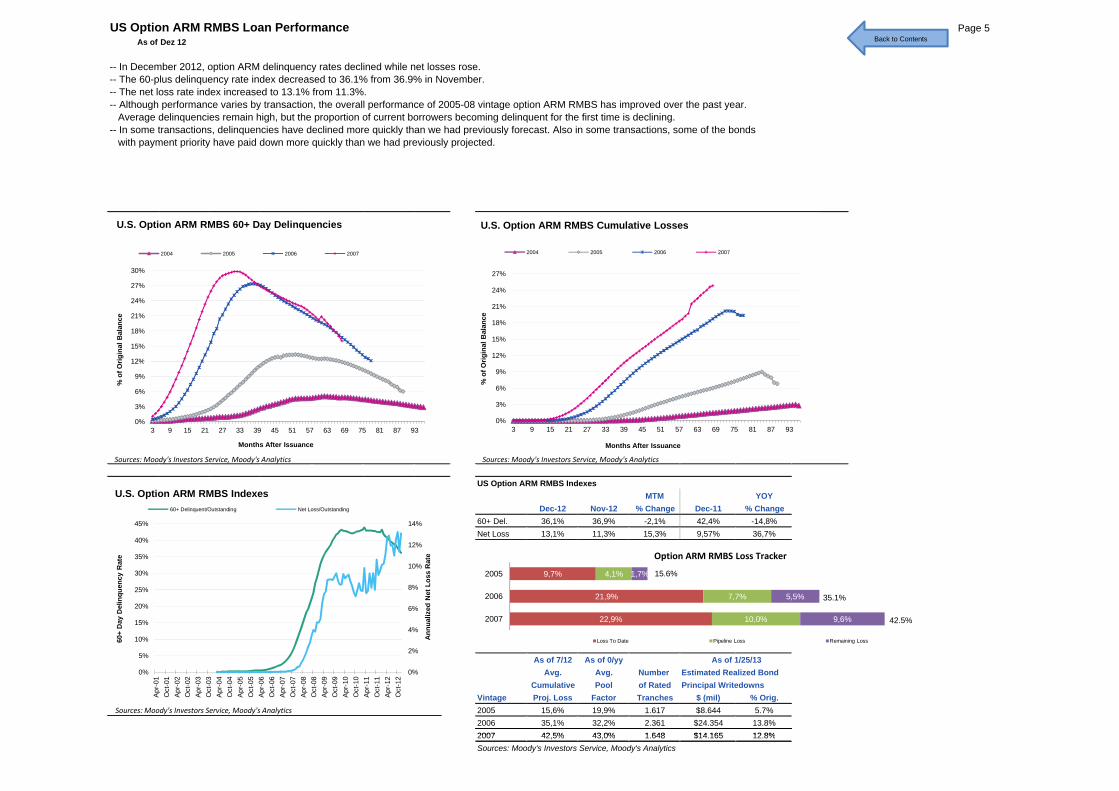

US Option ARM RMBS Loan Performance Page 5As of Dez 12

-- In December 2012, option ARM delinquency rates declined while net losses rose.-- The 60-plus delinquency rate index decreased to 36.1% from 36.9% in November.-- The net loss rate index increased to 13.1% from 11.3%.-- Although performance varies by transaction, the overall performance of 2005-08 vintage option ARM RMBS has improved over the past year. Average delinquencies remain high, but the proportion of current borrowers becoming delinquent for the first time is declining. -- In some transactions, delinquencies have declined more quickly than we had previously forecast. Also in some transactions, some of the bonds with payment priority have paid down more quickly than we had previously projected.

9%

12%

15%

18%

21%

24%

27%

30%

% o

f Orig

inal

Bal

ance

U.S. Option ARM RMBS 60+ Day Delinquencies

2004 2005 2006 2007

6%

9%

12%

15%

18%

21%

24%

27%

% o

f Orig

inal

Bal

ance

U.S. Option ARM RMBS Cumulative Losses

2004 2005 2006 2007

Back to Contents

US Option ARM RMBS IndexesMTM YOY

Dec-12 Nov-12 % Change Dec-11 % Change60+ Del. 36,1% 36,9% -2,1% 42,4% -14,8%Net Loss 13,1% 11,3% 15,3% 9,57% 36,7%

As of 7/12 As of 0/yyAvg. Avg. Number Estimated Realized Bond

Cumulative Pool of Rated Principal WritedownsVintage Proj. Loss Factor Tranches $ (mil) % Orig.2005 15,6% 19,9% 1.617 $8.644 5.7%2006 35,1% 32,2% 2.361 $24.354 13.8%2007 42 5% 43 0% 1 648 $14 165 12 8%

As of 1/25/13

0%

3%

6%

9%

12%

3 9 15 21 27 33 39 45 51 57 63 69 75 81 87 93

% o

f Or

Months After Issuance

0%

3%

6%

9%

3 9 15 21 27 33 39 45 51 57 63 69 75 81 87 93

% o

f Or

Months After Issuance

0%

2%

4%

6%

8%

10%

12%

14%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Apr-

01O

ct-0

1Ap

r-02

Oct

-02

Apr-

03O

ct-0

3Ap

r-04

Oct

-04

Apr-

05O

ct-0

5Ap

r-06

Oct

-06

Apr-

07O

ct-0

7Ap

r-08

Oct

-08

Apr-

09O

ct-0

9Ap

r-10

Oct

-10

Apr-

11O

ct-1

1Ap

r-12

Oct

-12

Ann

ualiz

ed N

et L

oss

Rat

e

60+

Day

Del

inqu

ency

Rat

e

U.S. Option ARM RMBS Indexes60+ Delinquent/Outstanding Net Loss/Outstanding

Sources: Moody's Investors Service, Moody's Analytics

9,7%

21,9%

22,9%

4,1%

7,7%

10,0%

1,7%

5,5%

9,6%

2005

2006

2007

Option ARM RMBS Loss Tracker

Loss To Date Pipeline Loss Remaining Loss

15.6%

35.1%

42.5%

Sources: Moody's Investors Service, Moody's Analytics Sources: Moody's Investors Service, Moody's Analytics

2007 42,5% 43,0% 1.648 $14.165 12.8%Sources: Moody's Investors Service, Moody's Analytics

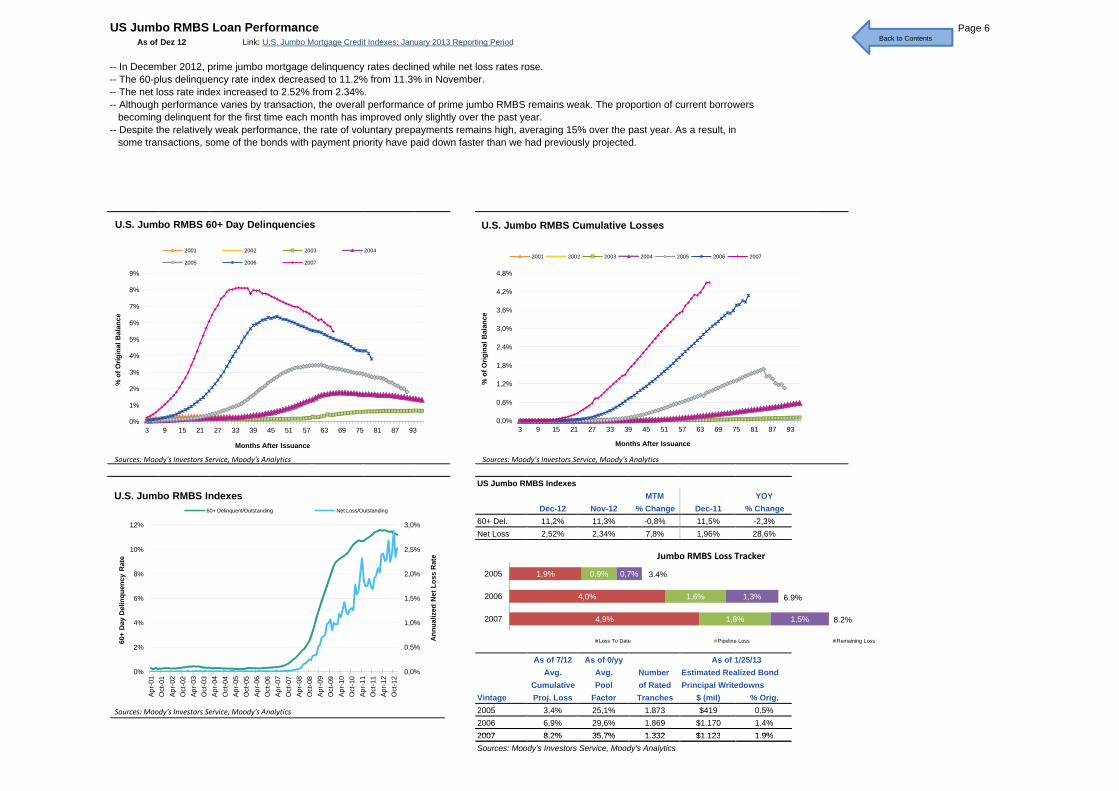

US Jumbo RMBS Loan Performance Page 6As of Dez 12 Link: U.S. Jumbo Mortgage Credit Indexes: January 2013 Reporting Period

-- In December 2012, prime jumbo mortgage delinquency rates declined while net loss rates rose.-- The 60-plus delinquency rate index decreased to 11.2% from 11.3% in November.-- The net loss rate index increased to 2.52% from 2.34%. -- Although performance varies by transaction, the overall performance of prime jumbo RMBS remains weak. The proportion of current borrowers becoming delinquent for the first time each month has improved only slightly over the past year.-- Despite the relatively weak performance, the rate of voluntary prepayments remains high, averaging 15% over the past year. As a result, in some transactions, some of the bonds with payment priority have paid down faster than we had previously projected.

2%

3%

4%

5%

6%

7%

8%

9%

% o

f Orig

inal

Bal

ance

U.S. Jumbo RMBS 60+ Day Delinquencies

2001 2002 2003 2004

2005 2006 2007

1,2%

1,8%

2,4%

3,0%

3,6%

4,2%

4,8%

% o

f Orig

inal

Bal

ance

U.S. Jumbo RMBS Cumulative Losses

2001 2002 2003 2004 2005 2006 2007

Back to Contents

US Jumbo RMBS IndexesMTM YOY

Dec-12 Nov-12 % Change Dec-11 % Change60+ Del. 11,2% 11,3% -0,8% 11,5% -2,3%Net Loss 2,52% 2,34% 7,8% 1,96% 28,6%

As of 7/12 As of 0/yyAvg. Avg. Number Estimated Realized Bond

Cumulative Pool of Rated Principal WritedownsVintage Proj. Loss Factor Tranches $ (mil) % Orig.2005 3,4% 25,1% 1.873 $419 0.5%2006 6,9% 29,6% 1.869 $1.170 1.4%2007 8 2% 35 7% 1 332 $1 123 1 9%

As of 1/25/13

0%

1%

2%

3%

3 9 15 21 27 33 39 45 51 57 63 69 75 81 87 93

% o

f Or

Months After Issuance

0,0%

0,6%

1,2%

1,8%

3 9 15 21 27 33 39 45 51 57 63 69 75 81 87 93

% o

f Or

Months After Issuance

0,0%

0,5%

1,0%

1,5%

2,0%

2,5%

3,0%

0%

2%

4%

6%

8%

10%

12%

Apr-

01O

ct-0

1Ap

r-02

Oct

-02

Apr-

03O

ct-0

3Ap

r-04

Oct

-04

Apr-

05O

ct-0

5Ap

r-06

Oct

-06

Apr-

07O

ct-0

7Ap

r-08

Oct

-08

Apr-

09O

ct-0

9Ap

r-10

Oct

-10

Apr-

11O

ct-1

1Ap

r-12

Oct

-12

Ann

ualiz

ed N

et L

oss

Rat

e

60+

Day

Del

inqu

ency

Rat

e

U.S. Jumbo RMBS Indexes60+ Delinquent/Outstanding Net Loss/Outstanding

Sources: Moody's Investors Service, Moody's Analytics

1,9%

4,0%

4,9%

0,9%

1,6%

1,8%

0,7%

1,3%

1,5%

2005

2006

2007

Jumbo RMBS Loss Tracker

Loss To Date Pipeline Loss Remaining Loss

3.4%

6.9%

8.2%

Sources: Moody's Investors Service, Moody's Analytics Sources: Moody's Investors Service, Moody's Analytics

2007 8,2% 35,7% 1.332 $1.123 1.9%Sources: Moody's Investors Service, Moody's Analytics

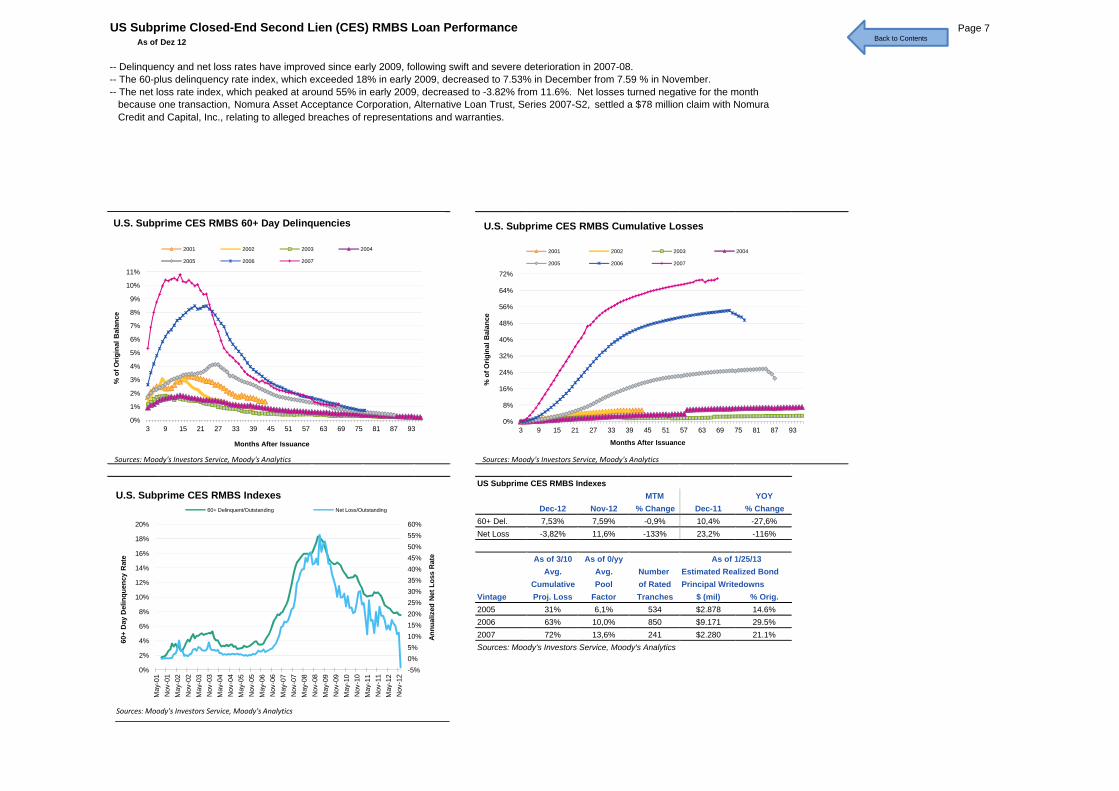

US Subprime Closed-End Second Lien (CES) RMBS Loan Performance Page 7As of Dez 12

-- Delinquency and net loss rates have improved since early 2009, following swift and severe deterioration in 2007-08.-- The 60-plus delinquency rate index, which exceeded 18% in early 2009, decreased to 7.53% in December from 7.59 % in November.-- The net loss rate index, which peaked at around 55% in early 2009, decreased to -3.82% from 11.6%. Net losses turned negative for the month because one transaction, Nomura Asset Acceptance Corporation, Alternative Loan Trust, Series 2007-S2, settled a $78 million claim with Nomura Credit and Capital, Inc., relating to alleged breaches of representations and warranties.

3%

4%

5%

6%

7%

8%

9%

10%

11%

% o

f Orig

inal

Bal

ance

U.S. Subprime CES RMBS 60+ Day Delinquencies

2001 2002 2003 2004

2005 2006 2007

16%

24%

32%

40%

48%

56%

64%

72%

% o

f Orig

inal

Bal

ance

U.S. Subprime CES RMBS Cumulative Losses

2001 2002 2003 2004

2005 2006 2007

Back to Contents

US Subprime CES RMBS IndexesMTM YOY

Dec-12 Nov-12 % Change Dec-11 % Change60+ Del. 7,53% 7,59% -0,9% 10,4% -27,6%Net Loss -3,82% 11,6% -133% 23,2% -116%

As of 3/10 As of 0/yyAvg. Avg. Number Estimated Realized Bond

Cumulative Pool of Rated Principal WritedownsVintage Proj. Loss Factor Tranches $ (mil) % Orig.2005 31% 6,1% 534 $2.878 14.6%2006 63% 10,0% 850 $9.171 29.5%2007 72% 13,6% 241 $2.280 21.1%Sources: Moody's Investors Service, Moody's Analytics

As of 1/25/13

0%

1%

2%

3%

4%

3 9 15 21 27 33 39 45 51 57 63 69 75 81 87 93

% o

f Or

Months After Issuance

0%

8%

16%

24%

3 9 15 21 27 33 39 45 51 57 63 69 75 81 87 93

% o

f Or

Months After Issuance

-5%0%5%10%15%20%25%30%35%40%45%50%55%60%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

May

-01

Nov

-01

May

-02

Nov

-02

Ma y

-03

Nov

-03

May

-04

Nov

-04

May

-05

Nov

-05

May

-06

Nov

-06

May

-07

Nov

-07

May

-08

Nov

-08

Ma y

-09

Nov

-09

May

-10

Nov

-10

May

-11

Nov

-11

May

-12

Nov

-12

Ann

ualiz

ed N

et L

oss

Rat

e

60+

Day

Del

inqu

ency

Rat

e

U.S. Subprime CES RMBS Indexes60+ Delinquent/Outstanding Net Loss/Outstanding

Sources: Moody's Investors Service, Moody's Analytics

Sources: Moody's Investors Service, Moody's Analytics Sources: Moody's Investors Service, Moody's Analytics

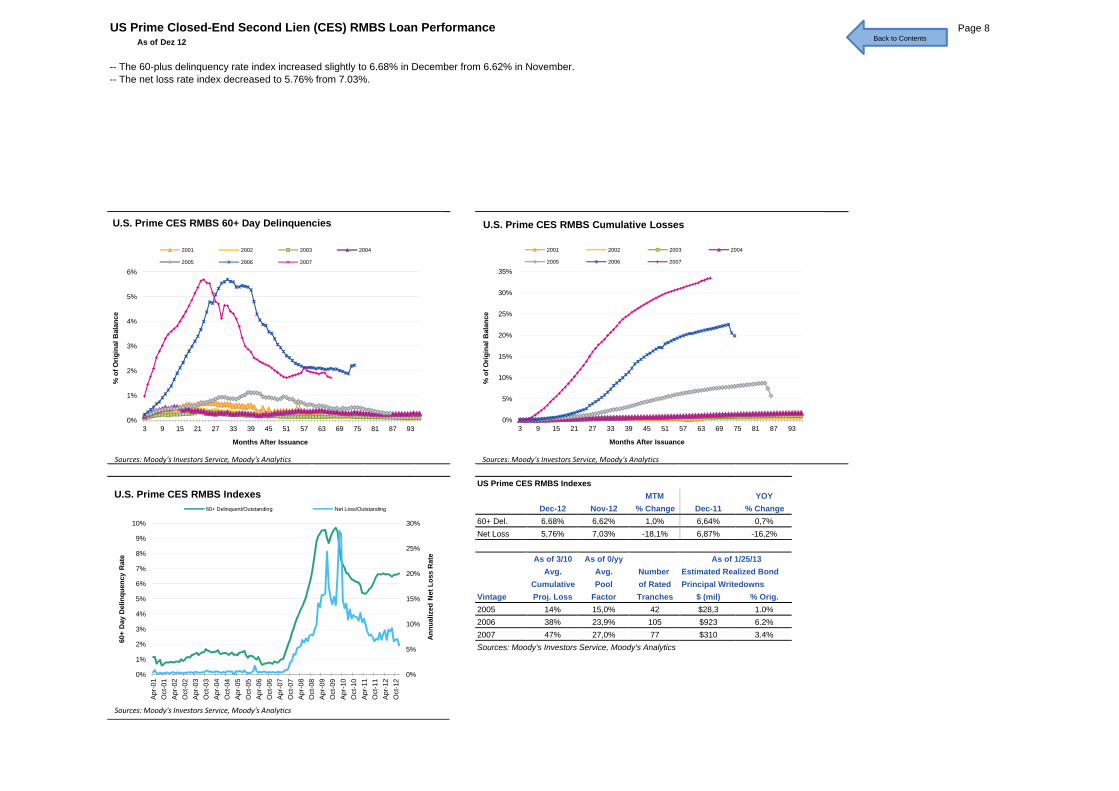

US Prime Closed-End Second Lien (CES) RMBS Loan Performance Page 8As of Dez 12

-- The 60-plus delinquency rate index increased slightly to 6.68% in December from 6.62% in November. -- The net loss rate index decreased to 5.76% from 7.03%.

2%

3%

4%

5%

6%

% o

f Orig

inal

Bal

ance

U.S. Prime CES RMBS 60+ Day Delinquencies

2001 2002 2003 2004

2005 2006 2007

10%

15%

20%

25%

30%

35%

% o

f Orig

inal

Bal

ance

U.S. Prime CES RMBS Cumulative Losses

2001 2002 2003 2004

2005 2006 2007

Back to Contents

US Prime CES RMBS IndexesMTM YOY

Dec-12 Nov-12 % Change Dec-11 % Change60+ Del. 6,68% 6,62% 1,0% 6,64% 0,7%Net Loss 5,76% 7,03% -18,1% 6,87% -16,2%

As of 3/10 As of 0/yyAvg. Avg. Number Estimated Realized Bond

Cumulative Pool of Rated Principal WritedownsVintage Proj. Loss Factor Tranches $ (mil) % Orig.2005 14% 15,0% 42 $28,3 1.0%2006 38% 23,9% 105 $923 6.2%2007 47% 27,0% 77 $310 3.4%Sources: Moody's Investors Service, Moody's Analytics

As of 1/25/13

0%

1%

2%

3 9 15 21 27 33 39 45 51 57 63 69 75 81 87 93

% o

f Or

Months After Issuance

0%

5%

10%

3 9 15 21 27 33 39 45 51 57 63 69 75 81 87 93

% o

f Or

Months After Issuance

0%

5%

10%

15%

20%

25%

30%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

Apr-

01O

ct-0

1Ap

r-02

Oct

-02

Apr-

03O

ct-0

3Ap

r-04

Oct

-04

Apr-

05O

ct-0

5Ap

r-06

Oct

-06

Apr-

07O

ct-0

7Ap

r-08

Oct

-08

Apr-

09O

ct-0

9Ap

r-10

Oct

-10

Apr-

11O

ct-1

1Ap

r-12

Oct

-12

Ann

ualiz

ed N

et L

oss

Rat

e

60+

Day

Del

inqu

ency

Rat

e

U.S. Prime CES RMBS Indexes60+ Delinquent/Outstanding Net Loss/Outstanding

Sources: Moody's Investors Service, Moody's Analytics

Sources: Moody's Investors Service, Moody's Analytics Sources: Moody's Investors Service, Moody's Analytics

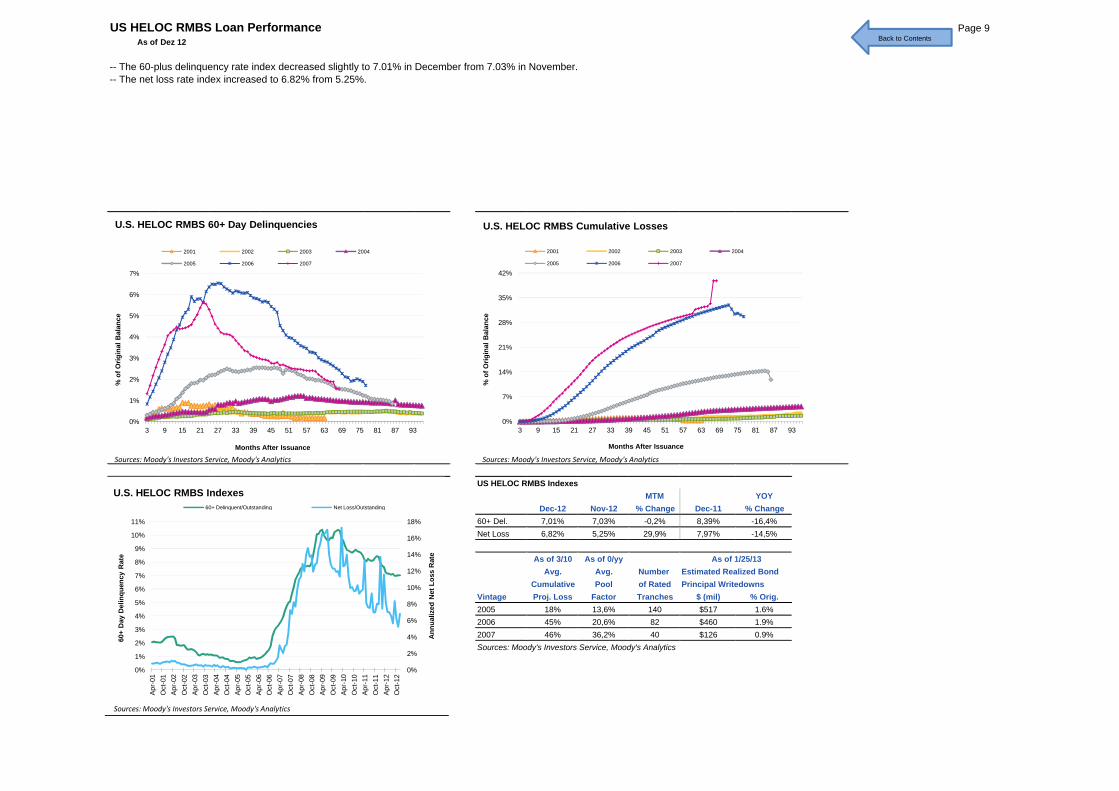

US HELOC RMBS Loan Performance Page 9As of Dez 12

-- The 60-plus delinquency rate index decreased slightly to 7.01% in December from 7.03% in November.-- The net loss rate index increased to 6.82% from 5.25%.

2%

3%

4%

5%

6%

7%

% o

f Orig

inal

Bal

ance

U.S. HELOC RMBS 60+ Day Delinquencies

2001 2002 2003 2004

2005 2006 2007

14%

21%

28%

35%

42%

% o

f Orig

inal

Bal

ance

U.S. HELOC RMBS Cumulative Losses

2001 2002 2003 2004

2005 2006 2007

Back to Contents

US HELOC RMBS IndexesMTM YOY

Dec-12 Nov-12 % Change Dec-11 % Change60+ Del. 7,01% 7,03% -0,2% 8,39% -16,4%Net Loss 6,82% 5,25% 29,9% 7,97% -14,5%

As of 3/10 As of 0/yyAvg. Avg. Number Estimated Realized Bond

Cumulative Pool of Rated Principal WritedownsVintage Proj. Loss Factor Tranches $ (mil) % Orig.2005 18% 13,6% 140 $517 1.6%2006 45% 20,6% 82 $460 1.9%2007 46% 36,2% 40 $126 0.9%Sources: Moody's Investors Service, Moody's Analytics

As of 1/25/13

0%

1%

2%

3 9 15 21 27 33 39 45 51 57 63 69 75 81 87 93

% o

f Or

Months After Issuance

0%

7%

14%

3 9 15 21 27 33 39 45 51 57 63 69 75 81 87 93

% o

f Or

Months After Issuance

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

11%

Apr-

01O

ct-0

1Ap

r-02

Oct

-02

Apr-

03O

ct-0

3Ap

r-04

Oct

-04

Apr-

05O

ct-0

5Ap

r-06

Oct

-06

Apr-

07O

ct-0

7Ap

r-08

Oct

-08

Apr-

09O

ct-0

9Ap

r-10

Oct

-10

Apr-

11O

ct-1

1Ap

r-12

Oct

-12

Ann

ualiz

ed N

et L

oss

Rat

e

60+

Day

Del

inqu

ency

Rat

e

U.S. HELOC RMBS Indexes60+ Delinquent/Outstanding Net Loss/Outstanding

Sources: Moody's Investors Service, Moody's Analytics

Sources: Moody's Investors Service, Moody's Analytics Sources: Moody's Investors Service, Moody's Analytics

US Home Prices Page 10As of Jan 13

160

170

180

190

200

210

220

230

Sale

s Pr

ice

($th

ousa

nds)

NAR Average U.S. Home Sales Price

-10%

-5%

0%

5%

10%

15%

20%

Year

-ove

r-ye

ar %

Cha

nge

NAR Average U.S. Home Sales Price, YOY % Change

Back to Contents

Source: National Association of Realtors

NAR Median Home Sales Price, Seasonally AdjustedMTM YOY

Jan-13 Dec-12 % Change Jan-12 % ChangeSales Price ($thou) $186,2 $182,4 2,1% $165,2 12,7%

150

160

170

Apr-

01

Oct

-01

Apr-

02

Oct

-02

Apr-

03

Oct

-03

Apr-

04

Oct

-04

Apr-

05

Oct

-05

Apr-

06

Oct

-06

Apr-

07

Oct

-07

Apr-

08

Oct

-08

Apr-

09

Oct

-09

Apr-

10

Oct

-10

Apr-

11

Oct

-11

Apr-

12

Oct

-12

S

-20%

-15%

-10%

Apr-

02

Oct

-02

Apr-

03

Oct

-03

Apr-

04

Oct

-04

Apr-

05

Oct

-05

Apr-

06

Oct

-06

Apr-

07

Oct

-07

Apr-

08

Oct

-08

Apr-

09

Oct

-09

Apr-

10

Oct

-10

Apr-

11

Oct

-11

Apr-

12

Oct

-12

Year

- o

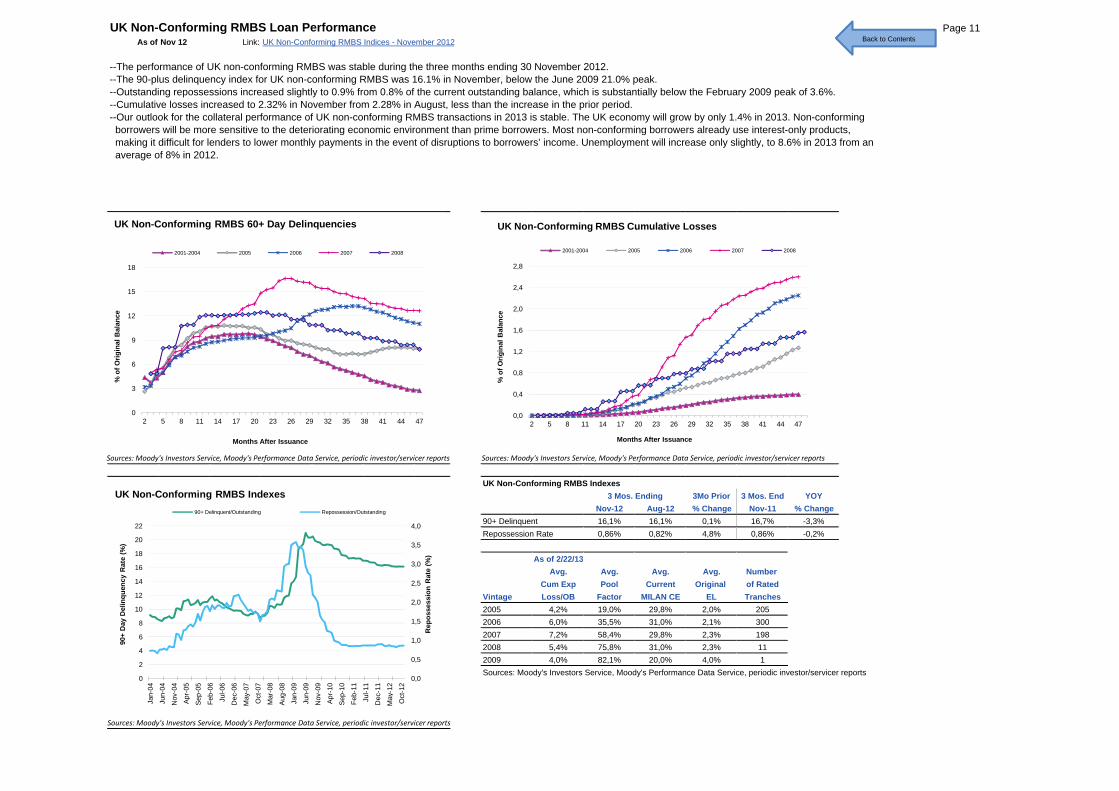

UK Non-Conforming RMBS Loan Performance Page 11As of Nov 12 Link: UK Non-Conforming RMBS Indices - November 2012

--The performance of UK non-conforming RMBS was stable during the three months ending 30 November 2012.--The 90-plus delinquency index for UK non-conforming RMBS was 16.1% in November, below the June 2009 21.0% peak.--Outstanding repossessions increased slightly to 0.9% from 0.8% of the current outstanding balance, which is substantially below the February 2009 peak of 3.6%.--Cumulative losses increased to 2.32% in November from 2.28% in August, less than the increase in the prior period.--Our outlook for the collateral performance of UK non-conforming RMBS transactions in 2013 is stable. The UK economy will grow by only 1.4% in 2013. Non-conforming borrowers will be more sensitive to the deteriorating economic environment than prime borrowers. Most non-conforming borrowers already use interest-only products, making it difficult for lenders to lower monthly payments in the event of disruptions to borrowers’ income. Unemployment will increase only slightly, to 8.6% in 2013 from an average of 8% in 2012.

3

6

9

12

15

18

% o

f Orig

inal

Bal

ance

UK Non-Conforming RMBS 60+ Day Delinquencies

2001-2004 2005 2006 2007 2008

0,8

1,2

1,6

2,0

2,4

2,8

% o

f Orig

inal

Bal

ance

UK Non-Conforming RMBS Cumulative Losses

2001-2004 2005 2006 2007 2008

Back to Contents

UK Non-Conforming RMBS Indexes3Mo Prior 3 Mos. End YOY

Nov-12 Aug-12 % Change Nov-11 % Change90+ Delinquent 16,1% 16,1% 0,1% 16,7% -3,3%Repossession Rate 0,86% 0,82% 4,8% 0,86% -0,2%

As of 2/22/13Avg. Avg. Avg. Avg. Number

Cum Exp Pool Current Original of RatedVintage Loss/OB Factor MILAN CE EL Tranches2005 4,2% 19,0% 29,8% 2,0% 2052006 6,0% 35,5% 31,0% 2,1% 3002007 7,2% 58,4% 29,8% 2,3% 1982008 5,4% 75,8% 31,0% 2,3% 112009 4,0% 82,1% 20,0% 4,0% 1Sources: Moody's Investors Service, Moody's Performance Data Service, periodic investor/servicer reports

3 Mos. Ending

0

3

6

2 5 8 11 14 17 20 23 26 29 32 35 38 41 44 47

% o

f O

Months After Issuance

0,0

0,4

0,8

2 5 8 11 14 17 20 23 26 29 32 35 38 41 44 47

% o

f O

Months After Issuance

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

4,0

0

2

4

6

8

10

12

14

16

18

20

22

Jan-

04

Jun-

04

Nov

-04

Apr-

05

Sep-

05

Feb-

06

Jul-0

6

Dec

-06

Ma y

-07

Oct

-07

Mar

-08

Aug-

08

Jan-

09

Jun-

09

Nov

-09

Apr-

10

Sep-

10

Feb-

11

Jul-1

1

Dec

-11

Ma y

-12

Oct

-12

Rep

osse

ssio

n R

ate

(%)

90+

Day

Del

inqu

ency

Rat

e (%

)

UK Non-Conforming RMBS Indexes90+ Delinquent/Outstanding Repossession/Outstanding

Sources: Moody's Investors Service, Moody's Performance Data Service, periodic investor/servicer reports

Sources: Moody's Investors Service, Moody's Performance Data Service, periodic investor/servicer reports

Sources: Moody's Investors Service, Moody's Performance Data Service, periodic investor/servicer reports

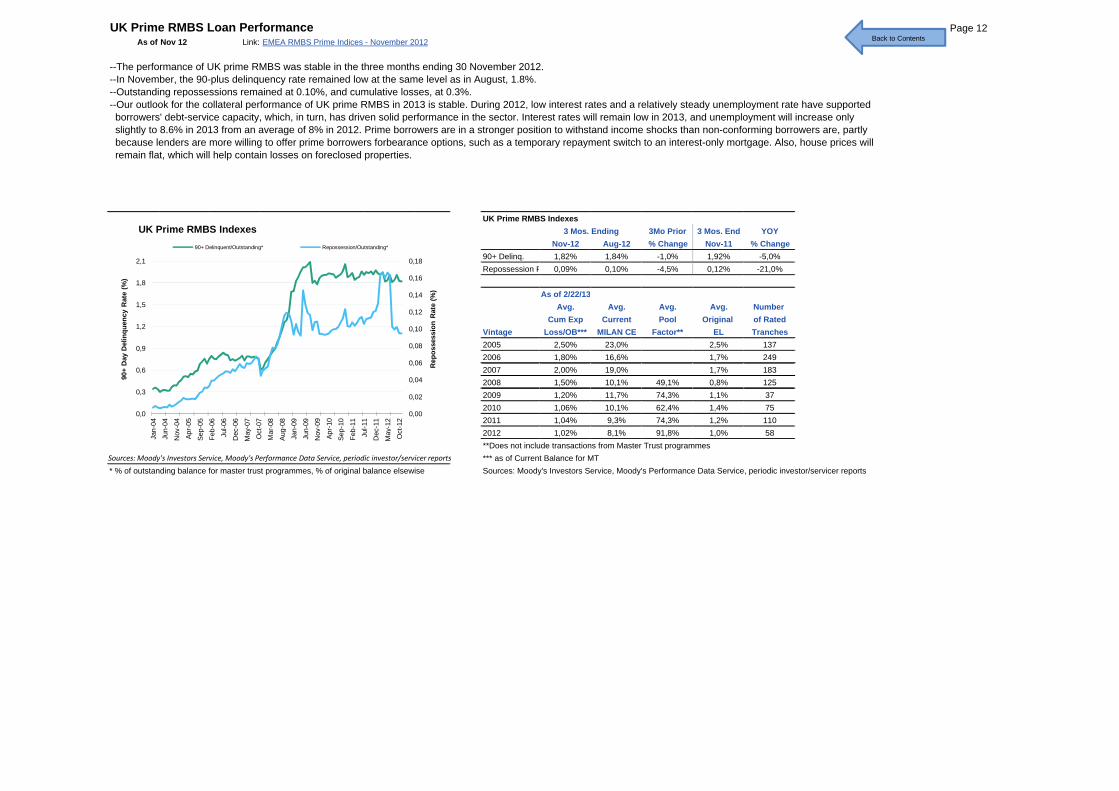

UK Prime RMBS Loan Performance Page 12As of Nov 12 Link: EMEA RMBS Prime Indices - November 2012

--The performance of UK prime RMBS was stable in the three months ending 30 November 2012.--In November, the 90-plus delinquency rate remained low at the same level as in August, 1.8%.--Outstanding repossessions remained at 0.10%, and cumulative losses, at 0.3%.--Our outlook for the collateral performance of UK prime RMBS in 2013 is stable. During 2012, low interest rates and a relatively steady unemployment rate have supported borrowers' debt-service capacity, which, in turn, has driven solid performance in the sector. Interest rates will remain low in 2013, and unemployment will increase only slightly to 8.6% in 2013 from an average of 8% in 2012. Prime borrowers are in a stronger position to withstand income shocks than non-conforming borrowers are, partly because lenders are more willing to offer prime borrowers forbearance options, such as a temporary repayment switch to an interest-only mortgage. Also, house prices will remain flat, which will help contain losses on foreclosed properties.

UK Prime RMBS Indexes3Mo Prior 3 Mos. End YOY

Nov-12 Aug-12 % Change Nov-11 % Change90+ Delinq. 1,82% 1,84% -1,0% 1,92% -5,0%Repossession R 0,09% 0,10% -4,5% 0,12% -21,0%

As of 2/22/13Avg. Avg. Avg. Avg. Number

Cum Exp Current Pool Original of RatedVintage Loss/OB*** MILAN CE Factor** EL Tranches2005 2,50% 23,0% 2,5% 1372006 1,80% 16,6% 1,7% 2492007 2,00% 19,0% 1,7% 183

3 Mos. Ending

0,04

0,06

0,08

0,10

0,12

0,14

0,16

0,18

0,6

0,9

1,2

1,5

1,8

2,1

Rep

osse

ssio

n R

ate

(%)

90+

Day

Del

inqu

ency

Rat

e (%

)

UK Prime RMBS Indexes90+ Delinquent/Outstanding* Repossession/Outstanding*

Back to Contents

2008 1,50% 10,1% 49,1% 0,8% 1252009 1,20% 11,7% 74,3% 1,1% 372010 1,06% 10,1% 62,4% 1,4% 752011 1,04% 9,3% 74,3% 1,2% 1102012 1,02% 8,1% 91,8% 1,0% 58**Does not include transactions from Master Trust programmes*** as of Current Balance for MT

* % of outstanding balance for master trust programmes, % of original balance elsewise Sources: Moody's Investors Service, Moody's Performance Data Service, periodic investor/servicer reports

0,00

0,02

0,04

0,06

0,0

0,3

0,6

Jan-

04Ju

n-04

Nov

-04

Apr-

05

Sep-

05Fe

b-06

Jul-0

6D

ec-0

6

Ma y

-07

Oct

-07

Mar

-08

Aug-

08Ja

n-09

Jun-

09N

ov-0

9

Apr-

10Se

p-10

Feb-

11Ju

l-11

Dec

-11

Ma y

-12

Oct

-12

Re

90+

D

Sources: Moody's Investors Service, Moody's Performance Data Service, periodic investor/servicer reports

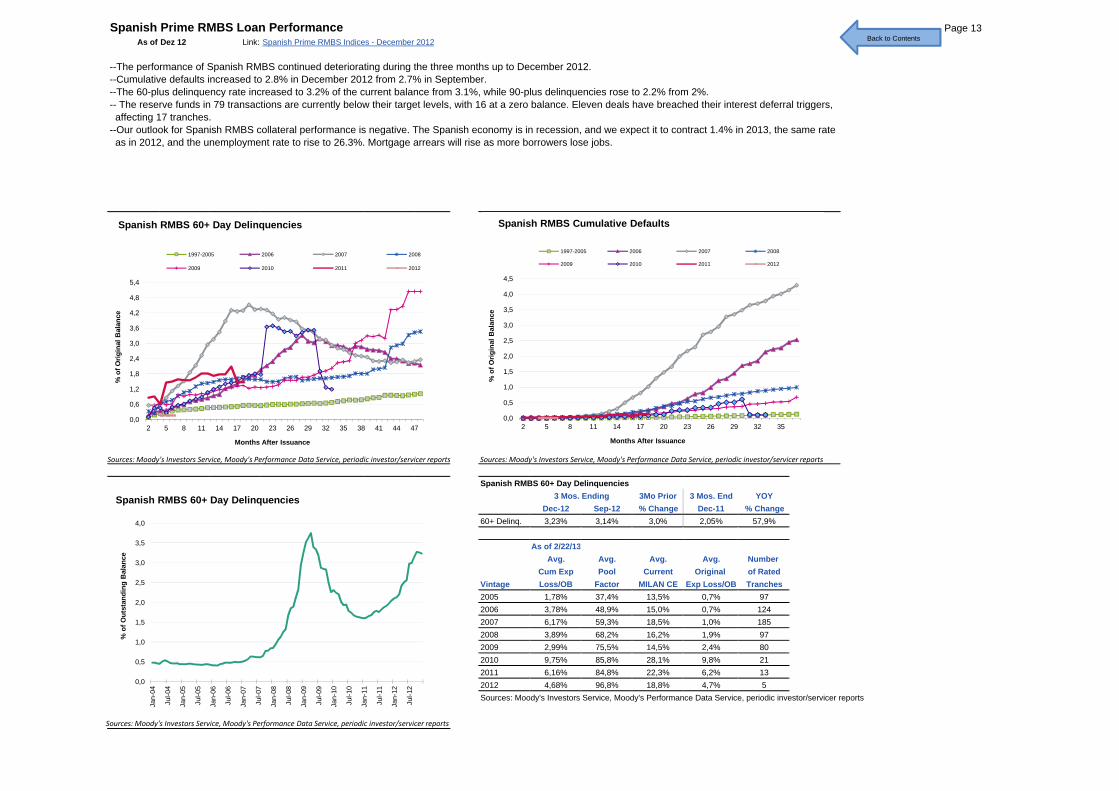

Spanish Prime RMBS Loan Performance Page 13As of Dez 12 Link: Spanish Prime RMBS Indices - December 2012

--The performance of Spanish RMBS continued deteriorating during the three months up to December 2012.--Cumulative defaults increased to 2.8% in December 2012 from 2.7% in September.--The 60-plus delinquency rate increased to 3.2% of the current balance from 3.1%, while 90-plus delinquencies rose to 2.2% from 2%. -- The reserve funds in 79 transactions are currently below their target levels, with 16 at a zero balance. Eleven deals have breached their interest deferral triggers, affecting 17 tranches.--Our outlook for Spanish RMBS collateral performance is negative. The Spanish economy is in recession, and we expect it to contract 1.4% in 2013, the same rate as in 2012, and the unemployment rate to rise to 26.3%. Mortgage arrears will rise as more borrowers lose jobs.

1 2

1,8

2,4

3,0

3,6

4,2

4,8

5,4

% o

f Orig

inal

Bal

ance

Spanish RMBS 60+ Day Delinquencies

1997-2005 2006 2007 2008

2009 2010 2011 2012

1 0

1,5

2,0

2,5

3,0

3,5

4,0

4,5

% o

f Orig

inal

Bal

ance

Spanish RMBS Cumulative Defaults

1997-2005 2006 2007 2008

2009 2010 2011 2012

Back to Contents

Spanish RMBS 60+ Day Delinquencies3Mo Prior 3 Mos. End YOY

Dec-12 Sep-12 % Change Dec-11 % Change60+ Delinq. 3,23% 3,14% 3,0% 2,05% 57,9%

As of 2/22/13Avg. Avg. Avg. Avg. Number

Cum Exp Pool Current Original of RatedVintage Loss/OB Factor MILAN CE Exp Loss/OB Tranches2005 1,78% 37,4% 13,5% 0,7% 972006 3,78% 48,9% 15,0% 0,7% 1242007 6,17% 59,3% 18,5% 1,0% 1852008 3,89% 68,2% 16,2% 1,9% 972009 2,99% 75,5% 14,5% 2,4% 802010 9,75% 85,8% 28,1% 9,8% 212011 6,16% 84,8% 22,3% 6,2% 132012 4,68% 96,8% 18,8% 4,7% 5Sources: Moody's Investors Service, Moody's Performance Data Service, periodic investor/servicer reports

3 Mos. Ending

0,0

0,6

1,2

1,8

,

2 5 8 11 14 17 20 23 26 29 32 35 38 41 44 47

% o

f O

Months After Issuance

0,0

0,5

1,0

1,5

2 5 8 11 14 17 20 23 26 29 32 35

% o

f O

Months After Issuance

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

4,0

Jan-

04

Jul-0

4

Jan-

05

Jul-0

5

Jan-

06

Jul-0

6

Jan-

07

Jul-0

7

Jan-

08

Jul-0

8

Jan-

09

Jul-0

9

Jan-

10

Jul-1

0

Jan-

11

Jul-1

1

Jan-

12

Jul-1

2

% o

f Out

stan

ding

Bal

ance

Spanish RMBS 60+ Day Delinquencies

Sources: Moody's Investors Service, Moody's Performance Data Service, periodic investor/servicer reports Sources: Moody's Investors Service, Moody's Performance Data Service, periodic investor/servicer reports

Sources: Moody's Investors Service, Moody's Performance Data Service, periodic investor/servicer reports

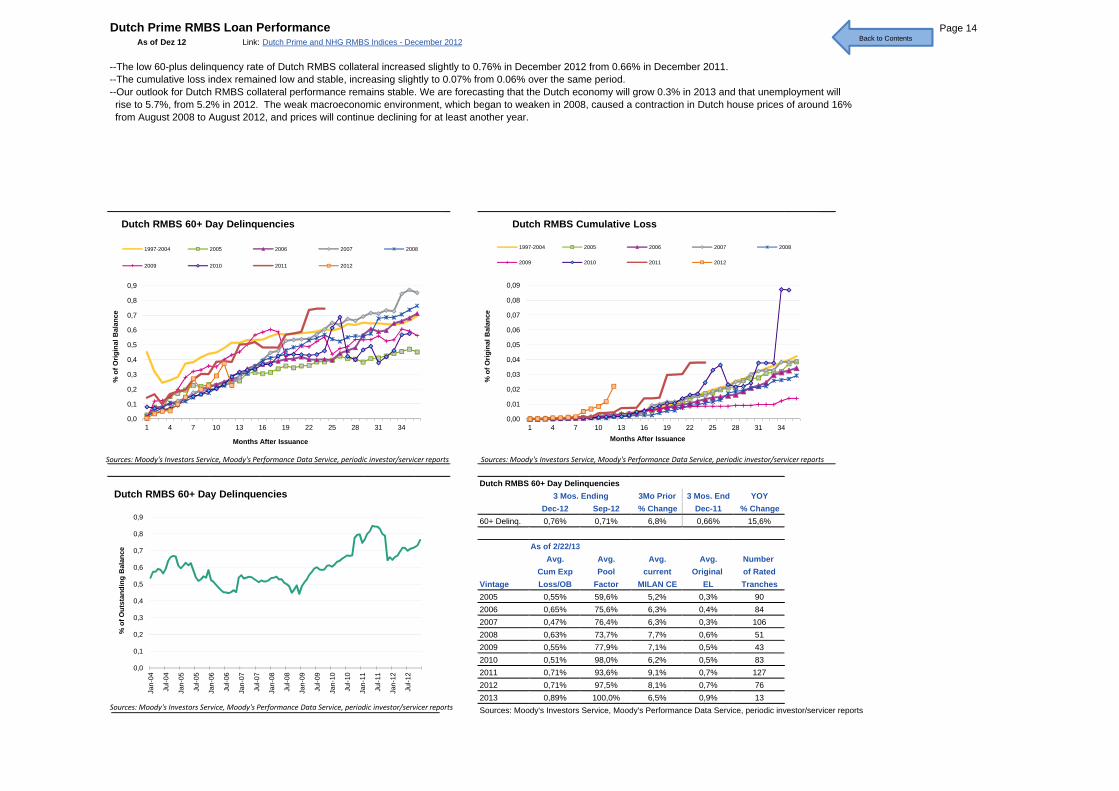

Dutch Prime RMBS Loan Performance Page 14As of Dez 12 Link: Dutch Prime and NHG RMBS Indices - December 2012

--The low 60-plus delinquency rate of Dutch RMBS collateral increased slightly to 0.76% in December 2012 from 0.66% in December 2011.--The cumulative loss index remained low and stable, increasing slightly to 0.07% from 0.06% over the same period. --Our outlook for Dutch RMBS collateral performance remains stable. We are forecasting that the Dutch economy will grow 0.3% in 2013 and that unemployment will rise to 5.7%, from 5.2% in 2012. The weak macroeconomic environment, which began to weaken in 2008, caused a contraction in Dutch house prices of around 16% from August 2008 to August 2012, and prices will continue declining for at least another year.

0 2

0,3

0,4

0,5

0,6

0,7

0,8

0,9

% o

f Orig

inal

Bal

ance

Dutch RMBS 60+ Day Delinquencies

1997-2004 2005 2006 2007 2008

2009 2010 2011 2012

0 02

0,03

0,04

0,05

0,06

0,07

0,08

0,09

% o

f Orig

inal

Bal

ance

Dutch RMBS Cumulative Loss

1997-2004 2005 2006 2007 2008

2009 2010 2011 2012

Back to Contents

Dutch RMBS 60+ Day Delinquencies3Mo Prior 3 Mos. End YOY

Dec-12 Sep-12 % Change Dec-11 % Change60+ Delinq. 0,76% 0,71% 6,8% 0,66% 15,6%

As of 2/22/13Avg. Avg. Avg. Avg. Number

Cum Exp Pool current Original of RatedVintage Loss/OB Factor MILAN CE EL Tranches2005 0,55% 59,6% 5,2% 0,3% 902006 0,65% 75,6% 6,3% 0,4% 842007 0,47% 76,4% 6,3% 0,3% 1062008 0,63% 73,7% 7,7% 0,6% 512009 0,55% 77,9% 7,1% 0,5% 432010 0,51% 98,0% 6,2% 0,5% 832011 0,71% 93,6% 9,1% 0,7% 1272012 0,71% 97,5% 8,1% 0,7% 762013 0,89% 100,0% 6,5% 0,9% 13Sources: Moody's Investors Service, Moody's Performance Data Service, periodic investor/servicer reports

3 Mos. Ending

0,0

0,1

0,2

0,3

0,4

1 4 7 10 13 16 19 22 25 28 31 34

% o

f O

Months After Issuance

0,00

0,01

0,02

0,03

0,04

1 4 7 10 13 16 19 22 25 28 31 34

% o

f O

Months After Issuance

0,0

0,1

0,2

0,3

0,4

0,5

0,6

0,7

0,8

0,9

Jan-

04

Jul-0

4

Jan-

05

Jul-0

5

Jan-

06

Jul-0

6

Jan-

07

Jul-0

7

Jan-

08

Jul-0

8

Jan-

09

Jul-0

9

Jan-

10

Jul-1

0

Jan-

11

Jul-1

1

Jan-

12

Jul-1

2

% o

f Out

stan

ding

Bal

ance

Dutch RMBS 60+ Day Delinquencies

Sources: Moody's Investors Service, Moody's Performance Data Service, periodic investor/servicer reports Sources: Moody's Investors Service, Moody's Performance Data Service, periodic investor/servicer reports

Sources: Moody's Investors Service, Moody's Performance Data Service, periodic investor/servicer reports

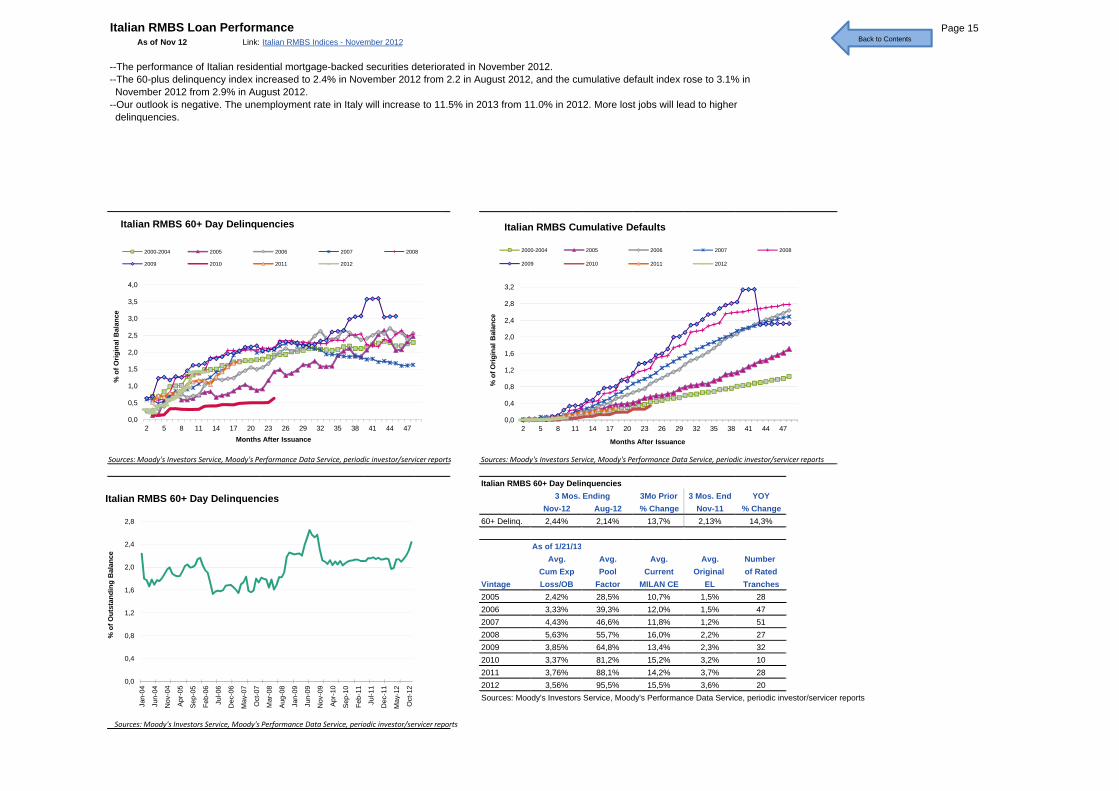

Italian RMBS Loan Performance Page 15As of Nov 12 Link: Italian RMBS Indices - November 2012

--The performance of Italian residential mortgage-backed securities deteriorated in November 2012.--The 60-plus delinquency index increased to 2.4% in November 2012 from 2.2 in August 2012, and the cumulative default index rose to 3.1% in November 2012 from 2.9% in August 2012.--Our outlook is negative. The unemployment rate in Italy will increase to 11.5% in 2013 from 11.0% in 2012. More lost jobs will lead to higher delinquencies.

1,0

1,5

2,0

2,5

3,0

3,5

4,0

% o

f Orig

inal

Bal

ance

Italian RMBS 60+ Day Delinquencies

2000-2004 2005 2006 2007 2008

2009 2010 2011 2012

0 8

1,2

1,6

2,0

2,4

2,8

3,2

% o

f Orig

inal

Bal

ance

Italian RMBS Cumulative Defaults

2000-2004 2005 2006 2007 2008

2009 2010 2011 2012

Back to Contents

Italian RMBS 60+ Day Delinquencies3Mo Prior 3 Mos. End YOY

Nov-12 Aug-12 % Change Nov-11 % Change60+ Delinq. 2,44% 2,14% 13,7% 2,13% 14,3%

As of 1/21/13Avg. Avg. Avg. Avg. Number

Cum Exp Pool Current Original of RatedVintage Loss/OB Factor MILAN CE EL Tranches2005 2,42% 28,5% 10,7% 1,5% 282006 3,33% 39,3% 12,0% 1,5% 472007 4,43% 46,6% 11,8% 1,2% 512008 5,63% 55,7% 16,0% 2,2% 272009 3,85% 64,8% 13,4% 2,3% 322010 3,37% 81,2% 15,2% 3,2% 102011 3,76% 88,1% 14,2% 3,7% 282012 3,56% 95,5% 15,5% 3,6% 20Sources: Moody's Investors Service, Moody's Performance Data Service, periodic investor/servicer reports

3 Mos. Ending

0,0

0,5

1,0

1,5

2 5 8 11 14 17 20 23 26 29 32 35 38 41 44 47

% o

f O

Months After Issuance

0,0

0,4

0,8

1,2

2 5 8 11 14 17 20 23 26 29 32 35 38 41 44 47

% o

f Or

Months After Issuance

0,0

0,4

0,8

1,2

1,6

2,0

2,4

2,8

Jan-

04

Jun-

04

Nov

-04

Apr-

05

Sep-

05

Feb-

06

Jul-0

6

Dec

-06

May

-07

Oct

-07

Mar

-08

Aug-

08

Jan-

09

Jun-

09

Nov

-09

Apr-

10

Sep-

10

Feb-

11

Jul-1

1

Dec

-11

May

-12

Oct

-12

% o

f Out

stan

ding

Bal

ance

Italian RMBS 60+ Day Delinquencies

Sources: Moody's Investors Service, Moody's Performance Data Service, periodic investor/servicer reports Sources: Moody's Investors Service, Moody's Performance Data Service, periodic investor/servicer reports

Sources: Moody's Investors Service, Moody's Performance Data Service, periodic investor/servicer reports

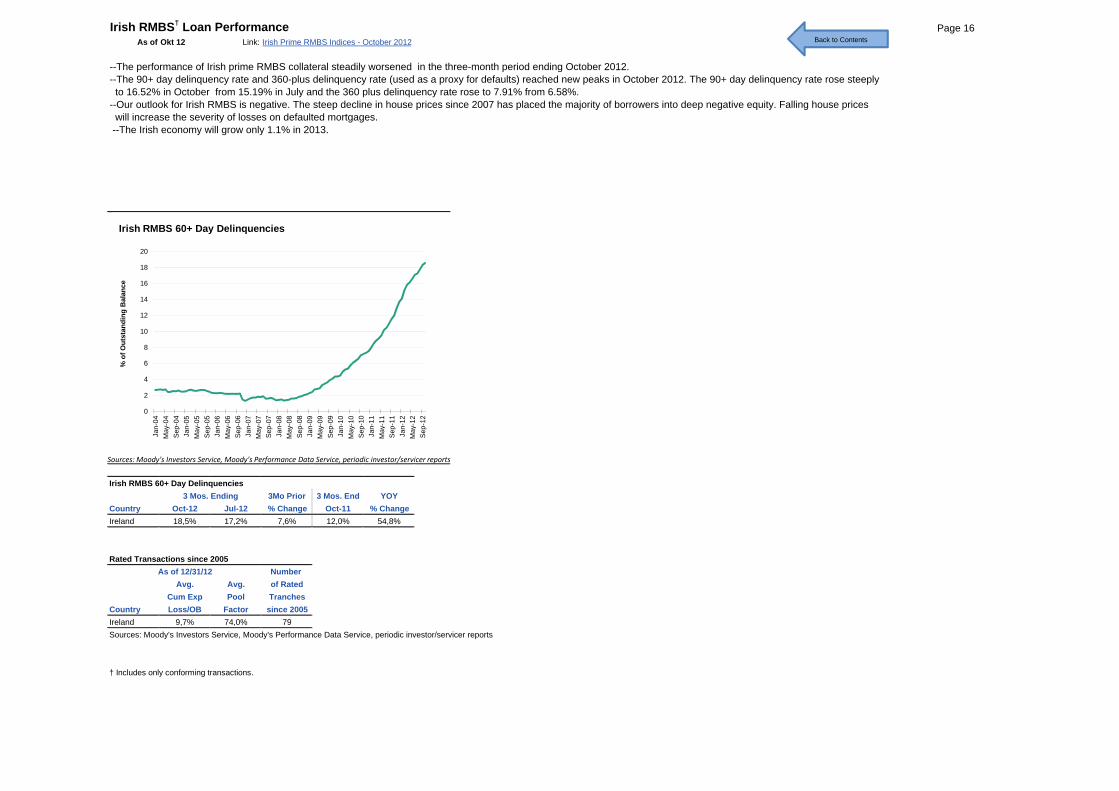

Irish RMBS† Loan Performance Page 16As of Okt 12 Link: Irish Prime RMBS Indices - October 2012

--The performance of Irish prime RMBS collateral steadily worsened in the three-month period ending October 2012.--The 90+ day delinquency rate and 360-plus delinquency rate (used as a proxy for defaults) reached new peaks in October 2012. The 90+ day delinquency rate rose steeply to 16.52% in October from 15.19% in July and the 360 plus delinquency rate rose to 7.91% from 6.58%.--Our outlook for Irish RMBS is negative. The steep decline in house prices since 2007 has placed the majority of borrowers into deep negative equity. Falling house prices will increase the severity of losses on defaulted mortgages. --The Irish economy will grow only 1.1% in 2013.

4

6

8

10

12

14

16

18

20

% o

f Out

stan

ding

Bal

ance

Irish RMBS 60+ Day Delinquencies

Back to Contents

Irish RMBS 60+ Day Delinquencies3Mo Prior 3 Mos. End YOY

Country Oct-12 Jul-12 % Change Oct-11 % ChangeIreland 18,5% 17,2% 7,6% 12,0% 54,8%

Rated Transactions since 2005As of 12/31/12 Number

Avg. Avg. of RatedCum Exp Pool Tranches

Country Loss/OB Factor since 2005Ireland 9,7% 74,0% 79Sources: Moody's Investors Service, Moody's Performance Data Service, periodic investor/servicer reports

† Includes only conforming transactions.

3 Mos. Ending

0

2

4

6

Jan-

04M

ay-0

4Se

p-04

Jan-

05M

a y-0

5Se

p-05

Jan-

06M

a y-0

6Se

p-06

Jan-

07M

a y-0

7Se

p-07

Jan-

08M

ay-0

8Se

p-08

Jan-

09M

ay-0

9Se

p-09

Jan-

10M

a y-1

0Se

p-10

Jan-

11M

a y-1

1Se

p-11

Jan-

12M

ay-1

2Se

p-12

%

Sources: Moody's Investors Service, Moody's Performance Data Service, periodic investor/servicer reports

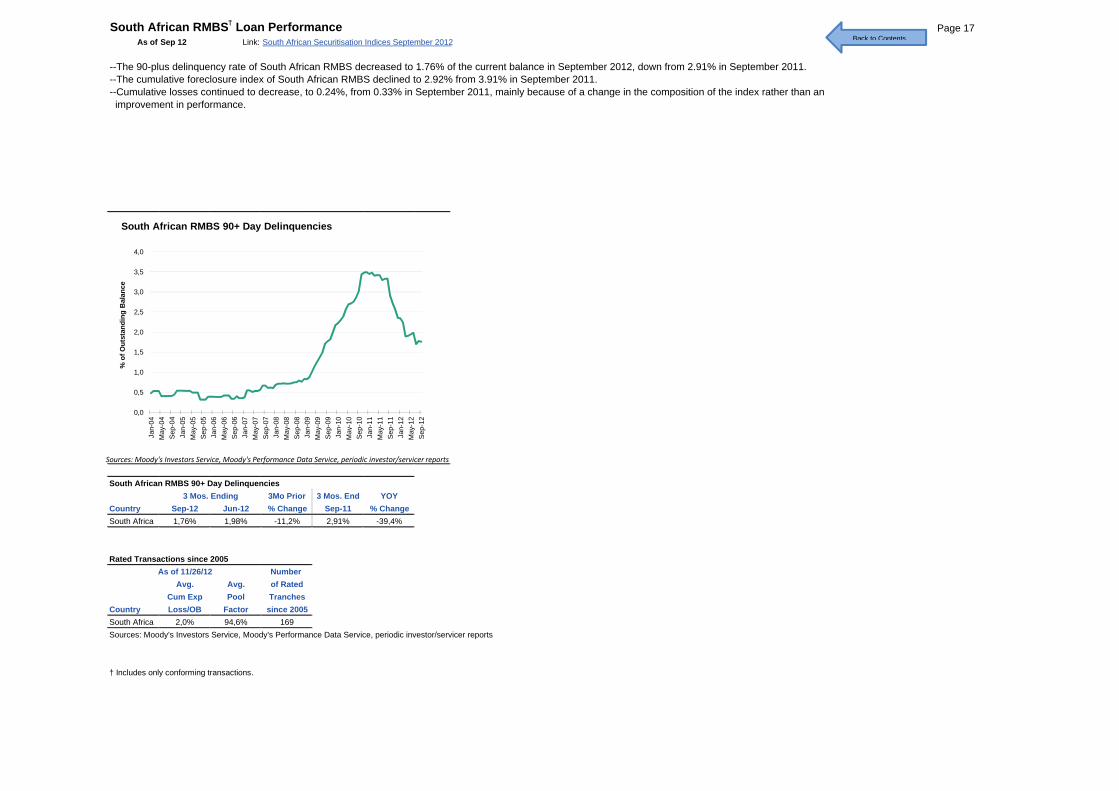

South African RMBS† Loan Performance Page 17As of Sep 12 Link: South African Securitisation Indices September 2012

--The 90-plus delinquency rate of South African RMBS decreased to 1.76% of the current balance in September 2012, down from 2.91% in September 2011. --The cumulative foreclosure index of South African RMBS declined to 2.92% from 3.91% in September 2011. --Cumulative losses continued to decrease, to 0.24%, from 0.33% in September 2011, mainly because of a change in the composition of the index rather than an improvement in performance.

1,0

1,5

2,0

2,5

3,0

3,5

4,0

% o

f Out

stan

ding

Bal

ance

South African RMBS 90+ Day Delinquencies

Back to Contents

South African RMBS 90+ Day Delinquencies3Mo Prior 3 Mos. End YOY

Country Sep-12 Jun-12 % Change Sep-11 % ChangeSouth Africa 1,76% 1,98% -11,2% 2,91% -39,4%

Rated Transactions since 2005As of 11/26/12 Number

Avg. Avg. of RatedCum Exp Pool Tranches

Country Loss/OB Factor since 2005South Africa 2,0% 94,6% 169Sources: Moody's Investors Service, Moody's Performance Data Service, periodic investor/servicer reports

† Includes only conforming transactions.

3 Mos. Ending

0,0

0,5

1,0

Jan-

04M

ay-0

4Se

p-04

Jan-

05M

ay-0

5Se

p-05

Jan-

06M

ay-0

6Se

p-06

Jan-

07M

ay-0

7Se

p-07

Jan-

08M

ay-0

8Se

p-08

Jan-

09M

ay-0

9Se

p-09

Jan-

10M

ay-1

0Se

p-10

Jan-

11M

ay-1

1Se

p-11

Jan-

12M

ay-1

2Se

p-12

%

Sources: Moody's Investors Service, Moody's Performance Data Service, periodic investor/servicer reports

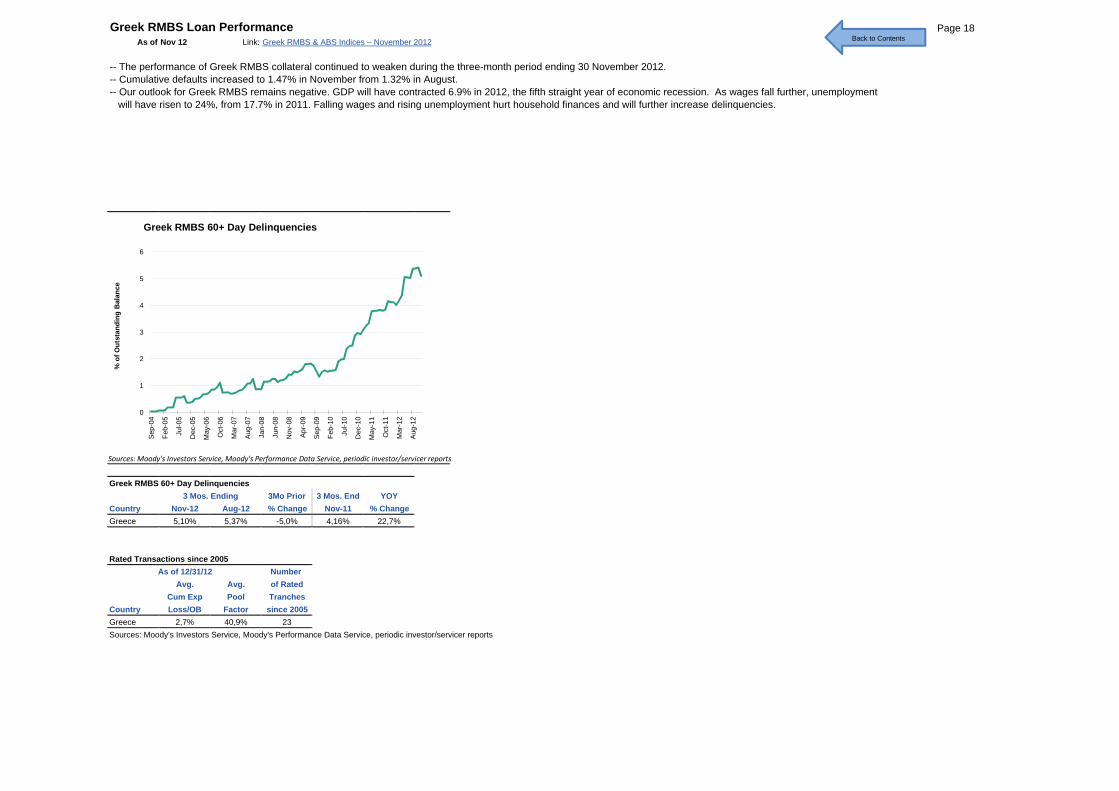

Greek RMBS Loan Performance Page 18As of Nov 12 Link: Greek RMBS & ABS Indices – November 2012

-- The performance of Greek RMBS collateral continued to weaken during the three-month period ending 30 November 2012.-- Cumulative defaults increased to 1.47% in November from 1.32% in August.-- Our outlook for Greek RMBS remains negative. GDP will have contracted 6.9% in 2012, the fifth straight year of economic recession. As wages fall further, unemployment will have risen to 24%, from 17.7% in 2011. Falling wages and rising unemployment hurt household finances and will further increase delinquencies.

1

2

3

4

5

6

% o

f Out

stan

ding

Bal

ance

Greek RMBS 60+ Day Delinquencies

Back to Contents

Greek RMBS 60+ Day Delinquencies3Mo Prior 3 Mos. End YOY

Country Nov-12 Aug-12 % Change Nov-11 % ChangeGreece 5,10% 5,37% -5,0% 4,16% 22,7%

Rated Transactions since 2005As of 12/31/12 Number

Avg. Avg. of RatedCum Exp Pool Tranches

Country Loss/OB Factor since 2005Greece 2,7% 40,9% 23Sources: Moody's Investors Service, Moody's Performance Data Service, periodic investor/servicer reports

3 Mos. Ending

0

1

Sep-

04

Feb-

05

Jul-0

5

Dec

-05

May

-06

Oct

-06

Mar

-07

Aug-

07

Jan-

08

Jun-

08

Nov

-08

Apr-

09

Sep-

09

Feb-

10

Jul-1

0

Dec

-10

May

-11

Oct

-11

Mar

-12

Aug-

12

%

Sources: Moody's Investors Service, Moody's Performance Data Service, periodic investor/servicer reports

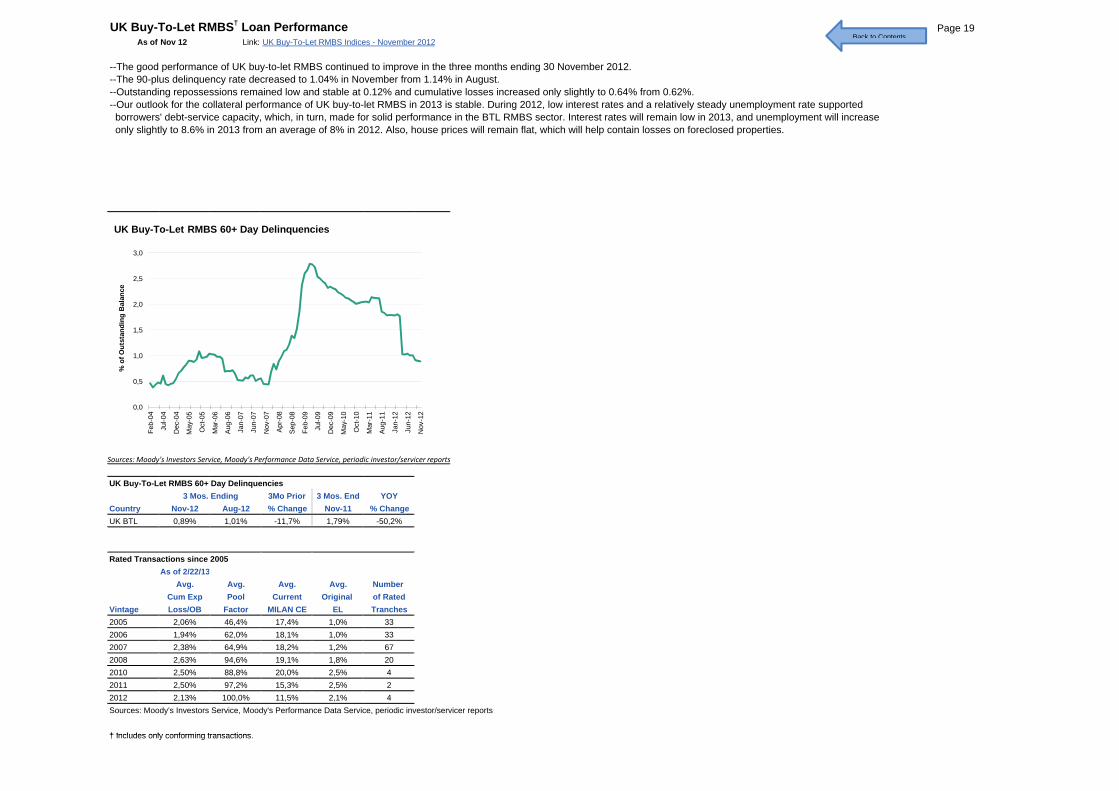

UK Buy-To-Let RMBS† Loan Performance Page 19As of Nov 12 Link: UK Buy-To-Let RMBS Indices - November 2012

--The good performance of UK buy-to-let RMBS continued to improve in the three months ending 30 November 2012.--The 90-plus delinquency rate decreased to 1.04% in November from 1.14% in August.--Outstanding repossessions remained low and stable at 0.12% and cumulative losses increased only slightly to 0.64% from 0.62%.--Our outlook for the collateral performance of UK buy-to-let RMBS in 2013 is stable. During 2012, low interest rates and a relatively steady unemployment rate supported borrowers' debt-service capacity, which, in turn, made for solid performance in the BTL RMBS sector. Interest rates will remain low in 2013, and unemployment will increase only slightly to 8.6% in 2013 from an average of 8% in 2012. Also, house prices will remain flat, which will help contain losses on foreclosed properties.

0,5

1,0

1,5

2,0

2,5

3,0

% o

f Out

stan

ding

Bal

ance

UK Buy-To-Let RMBS 60+ Day Delinquencies

Back to Contents

UK Buy-To-Let RMBS 60+ Day Delinquencies3Mo Prior 3 Mos. End YOY

Country Nov-12 Aug-12 % Change Nov-11 % ChangeUK BTL 0,89% 1,01% -11,7% 1,79% -50,2%

Rated Transactions since 2005As of 2/22/13

Avg. Avg. Avg. Avg. Number Cum Exp Pool Current Original of Rated

Vintage Loss/OB Factor MILAN CE EL Tranches2005 2,06% 46,4% 17,4% 1,0% 332006 1,94% 62,0% 18,1% 1,0% 332007 2,38% 64,9% 18,2% 1,2% 672008 2,63% 94,6% 19,1% 1,8% 202010 2,50% 88,8% 20,0% 2,5% 42011 2,50% 97,2% 15,3% 2,5% 22012 2,13% 100,0% 11,5% 2,1% 4Sources: Moody's Investors Service, Moody's Performance Data Service, periodic investor/servicer reports

† Includes only conforming transactions

3 Mos. Ending

0,0

0,5

Feb-

04

Jul-0

4

Dec

-04

May

-05

Oct

-05

Mar

-06

Aug-

06

Jan-

07

Jun-

07

Nov

-07

Apr-

08

Sep-

08

Feb-

09

Jul-0

9

Dec

-09

May

-10

Oct

-10

Mar

-11

Aug-

11

Jan-

12

Jun-

12

Nov

-12

% o

Sources: Moody's Investors Service, Moody's Performance Data Service, periodic investor/servicer reports

† Includes only conforming transactions.

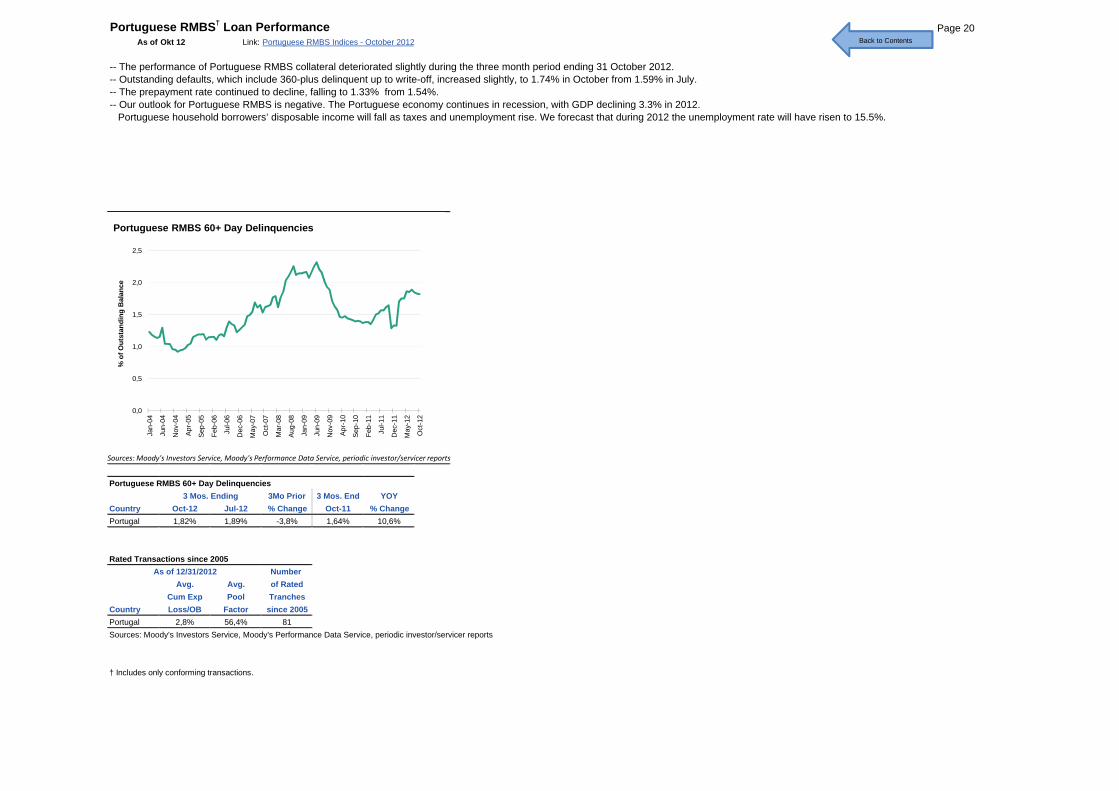

Portuguese RMBS† Loan Performance Page 20As of Okt 12 Link: Portuguese RMBS Indices - October 2012

-- The performance of Portuguese RMBS collateral deteriorated slightly during the three month period ending 31 October 2012.-- Outstanding defaults, which include 360-plus delinquent up to write-off, increased slightly, to 1.74% in October from 1.59% in July.-- The prepayment rate continued to decline, falling to 1.33% from 1.54%.-- Our outlook for Portuguese RMBS is negative. The Portuguese economy continues in recession, with GDP declining 3.3% in 2012. Portuguese household borrowers’ disposable income will fall as taxes and unemployment rise. We forecast that during 2012 the unemployment rate will have risen to 15.5%.

0,5

1,0

1,5

2,0

2,5

% o

f Out

stan

ding

Bal

ance

Portuguese RMBS 60+ Day Delinquencies

Back to Contents

Portuguese RMBS 60+ Day Delinquencies3Mo Prior 3 Mos. End YOY

Country Oct-12 Jul-12 % Change Oct-11 % ChangePortugal 1,82% 1,89% -3,8% 1,64% 10,6%

Rated Transactions since 2005As of 12/31/2012 Number

Avg. Avg. of RatedCum Exp Pool Tranches

Country Loss/OB Factor since 2005Portugal 2,8% 56,4% 81Sources: Moody's Investors Service, Moody's Performance Data Service, periodic investor/servicer reports

† Includes only conforming transactions.

3 Mos. Ending

0,0

0,5

Jan-

04

Jun-

04

Nov

-04

Apr-

05

Sep-

05

Feb-

06

Jul-0

6

Dec

-06

May

-07

Oct

-07

Mar

-08

Aug-

08

Jan-

09

Jun-

09

Nov

-09

Apr-

10

Sep-

10

Feb-

11

Jul-1

1

Dec

-11

May

-12

Oct

-12

%

Sources: Moody's Investors Service, Moody's Performance Data Service, periodic investor/servicer reports

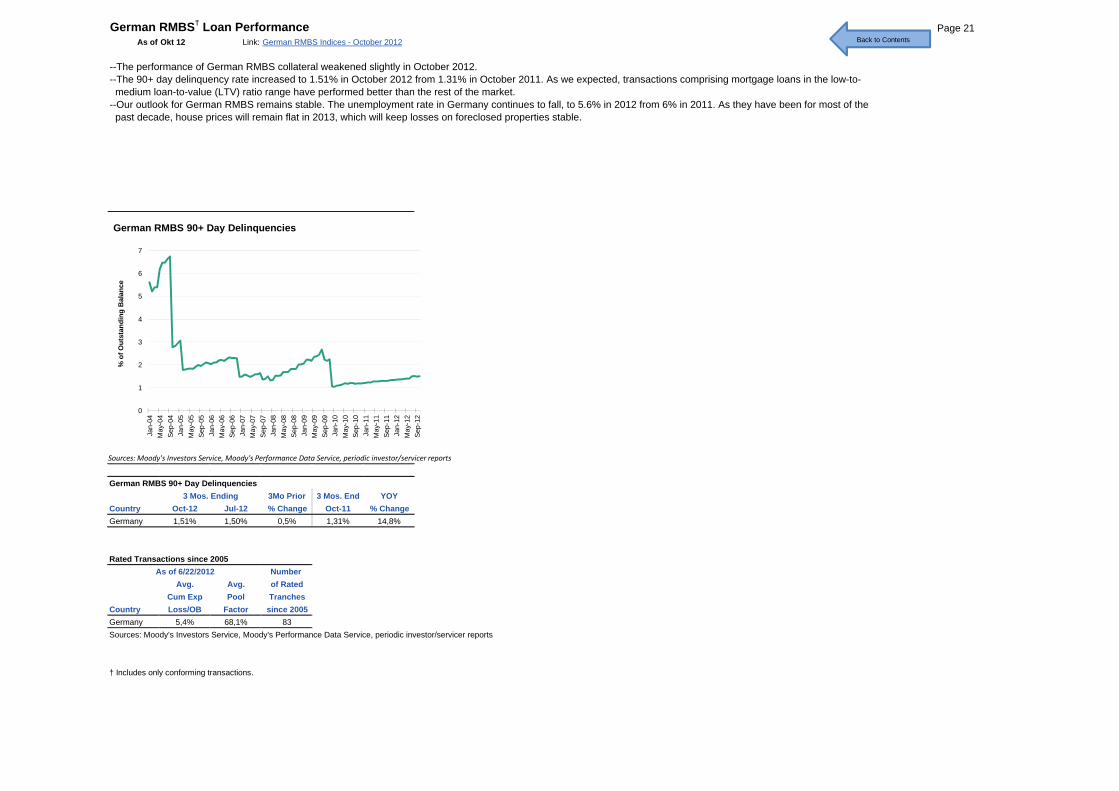

German RMBS† Loan Performance Page 21As of Okt 12 Link: German RMBS Indices - October 2012

--The performance of German RMBS collateral weakened slightly in October 2012.--The 90+ day delinquency rate increased to 1.51% in October 2012 from 1.31% in October 2011. As we expected, transactions comprising mortgage loans in the low-to- medium loan-to-value (LTV) ratio range have performed better than the rest of the market.--Our outlook for German RMBS remains stable. The unemployment rate in Germany continues to fall, to 5.6% in 2012 from 6% in 2011. As they have been for most of the past decade, house prices will remain flat in 2013, which will keep losses on foreclosed properties stable.

1

2

3

4

5

6

7

% o

f Out

stan

ding

Bal

ance

German RMBS 90+ Day Delinquencies

Back to Contents

German RMBS 90+ Day Delinquencies3Mo Prior 3 Mos. End YOY

Country Oct-12 Jul-12 % Change Oct-11 % ChangeGermany 1,51% 1,50% 0,5% 1,31% 14,8%

Rated Transactions since 2005As of 6/22/2012 Number

Avg. Avg. of RatedCum Exp Pool Tranches

Country Loss/OB Factor since 2005Germany 5,4% 68,1% 83Sources: Moody's Investors Service, Moody's Performance Data Service, periodic investor/servicer reports

† Includes only conforming transactions.

3 Mos. Ending

0

1

2

Jan-

04M

ay-0

4Se

p-04

Jan-

05M

a y-0

5Se

p-05

Jan-

06M

a y-0

6Se

p-06

Jan-

07M

ay-0

7Se

p-07

Jan-

08M

a y-0

8Se

p-08

Jan-

09M

ay-0

9Se

p-09

Jan-

10M

a y-1

0Se

p-10

Jan-

11M

ay-1

1Se

p-11

Jan-

12M

a y-1

2Se

p-12

%

Sources: Moody's Investors Service, Moody's Performance Data Service, periodic investor/servicer reports

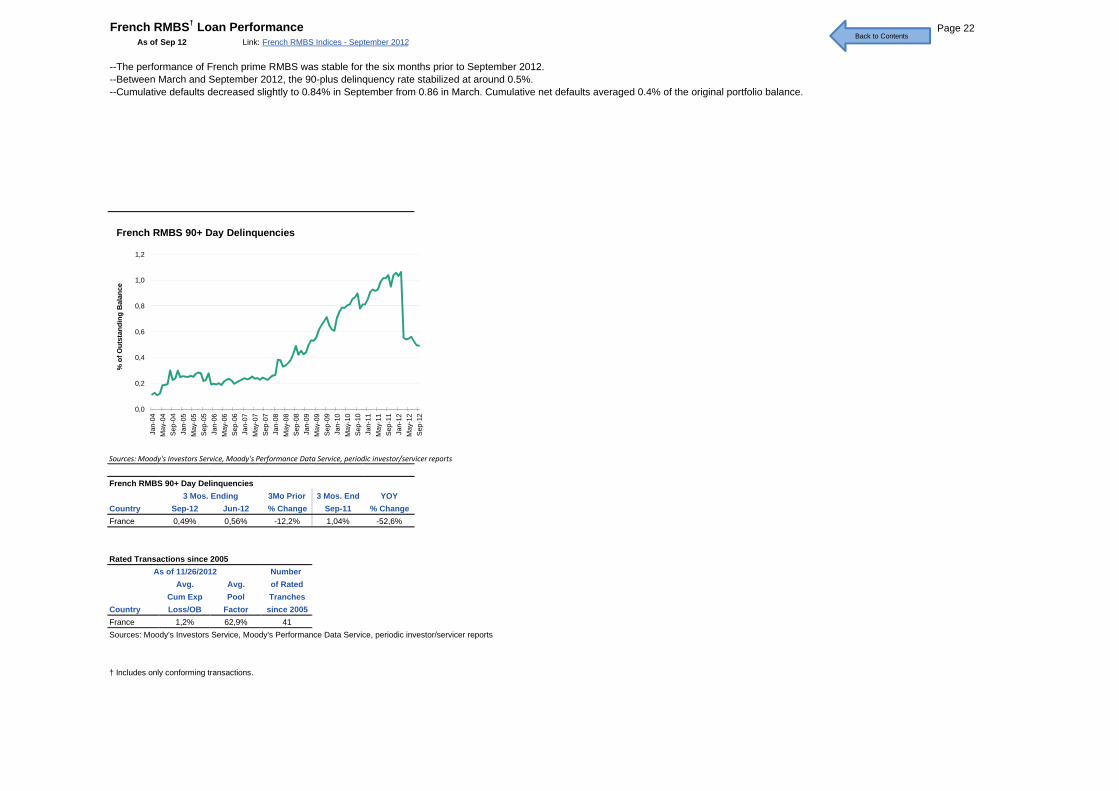

French RMBS† Loan Performance Page 22As of Sep 12 Link: French RMBS Indices - September 2012

--The performance of French prime RMBS was stable for the six months prior to September 2012. --Between March and September 2012, the 90-plus delinquency rate stabilized at around 0.5%.--Cumulative defaults decreased slightly to 0.84% in September from 0.86 in March. Cumulative net defaults averaged 0.4% of the original portfolio balance.

0,2

0,4

0,6

0,8

1,0

1,2

% o

f Out

stan

ding

Bal

ance

French RMBS 90+ Day Delinquencies

Back to Contents

French RMBS 90+ Day Delinquencies3Mo Prior 3 Mos. End YOY

Country Sep-12 Jun-12 % Change Sep-11 % ChangeFrance 0,49% 0,56% -12,2% 1,04% -52,6%

Rated Transactions since 2005As of 11/26/2012 Number

Avg. Avg. of RatedCum Exp Pool Tranches

Country Loss/OB Factor since 2005France 1,2% 62,9% 41Sources: Moody's Investors Service, Moody's Performance Data Service, periodic investor/servicer reports

† Includes only conforming transactions.

3 Mos. Ending

0,0

0,2

Jan-

04M

ay-0

4Se

p-04

Jan-

05M

a y-0

5Se

p-05

Jan-

06M

a y-0

6Se

p-06

Jan-

07M

ay-0

7Se

p-07

Jan-

08M

a y-0

8Se

p-08

Jan-

09M

a y-0

9Se

p-09

Jan-

10M

a y-1

0Se

p-10

Jan-

11M

a y-1

1Se

p-11

Jan-

12M

ay-1

2Se

p-12

% o

Sources: Moody's Investors Service, Moody's Performance Data Service, periodic investor/servicer reports

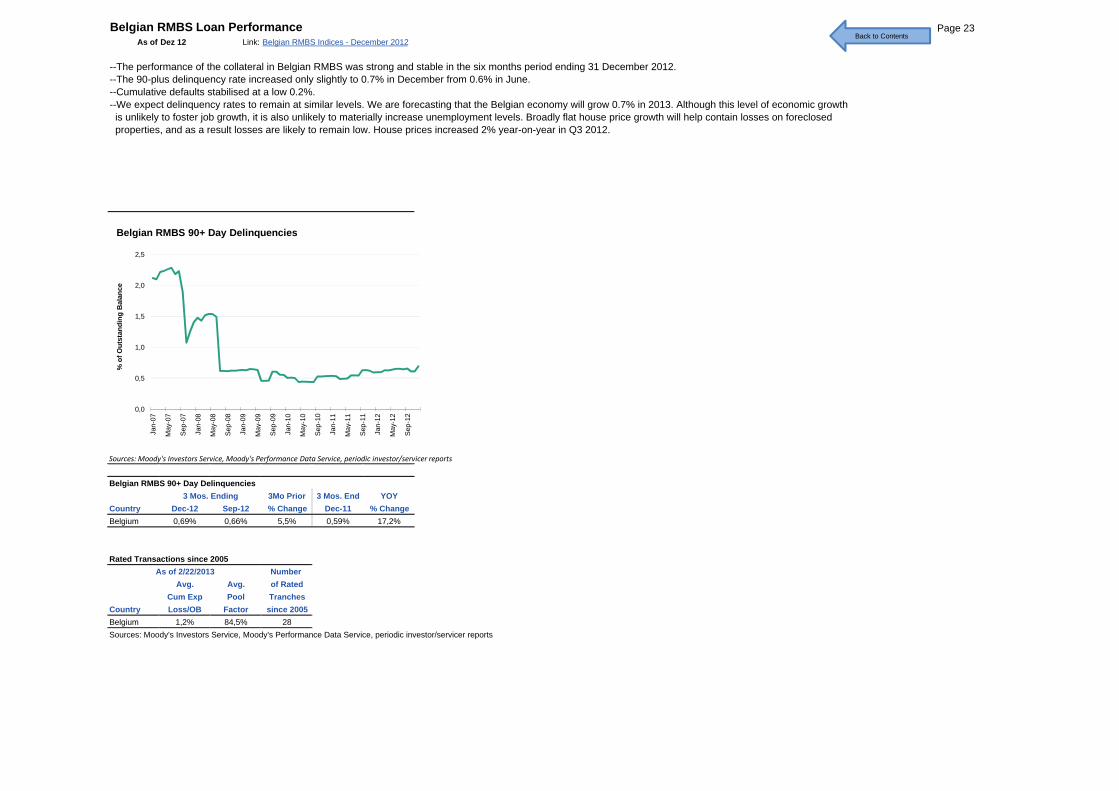

Belgian RMBS Loan Performance Page 23As of Dez 12 Link: Belgian RMBS Indices - December 2012

--The performance of the collateral in Belgian RMBS was strong and stable in the six months period ending 31 December 2012.--The 90-plus delinquency rate increased only slightly to 0.7% in December from 0.6% in June. --Cumulative defaults stabilised at a low 0.2%. --We expect delinquency rates to remain at similar levels. We are forecasting that the Belgian economy will grow 0.7% in 2013. Although this level of economic growth is unlikely to foster job growth, it is also unlikely to materially increase unemployment levels. Broadly flat house price growth will help contain losses on foreclosed properties, and as a result losses are likely to remain low. House prices increased 2% year-on-year in Q3 2012.

0,5

1,0

1,5

2,0

2,5

% o

f Out

stan

ding

Bal

ance

Belgian RMBS 90+ Day Delinquencies

Back to Contents

Belgian RMBS 90+ Day Delinquencies3Mo Prior 3 Mos. End YOY

Country Dec-12 Sep-12 % Change Dec-11 % ChangeBelgium 0,69% 0,66% 5,5% 0,59% 17,2%

Rated Transactions since 2005As of 2/22/2013 Number

Avg. Avg. of RatedCum Exp Pool Tranches

Country Loss/OB Factor since 2005Belgium 1,2% 84,5% 28Sources: Moody's Investors Service, Moody's Performance Data Service, periodic investor/servicer reports

3 Mos. Ending

0,0

0,5

Jan-

07

May

-07

Sep-

07

Jan-

08

May

-08

Sep-

08

Jan-

09

May

-09

Sep-

09

Jan-

10

May

-10

Sep-

10

Jan-

11

May

-11

Sep-

11

Jan-

12

May

-12

Sep-

12

% o

Sources: Moody's Investors Service, Moody's Performance Data Service, periodic investor/servicer reports

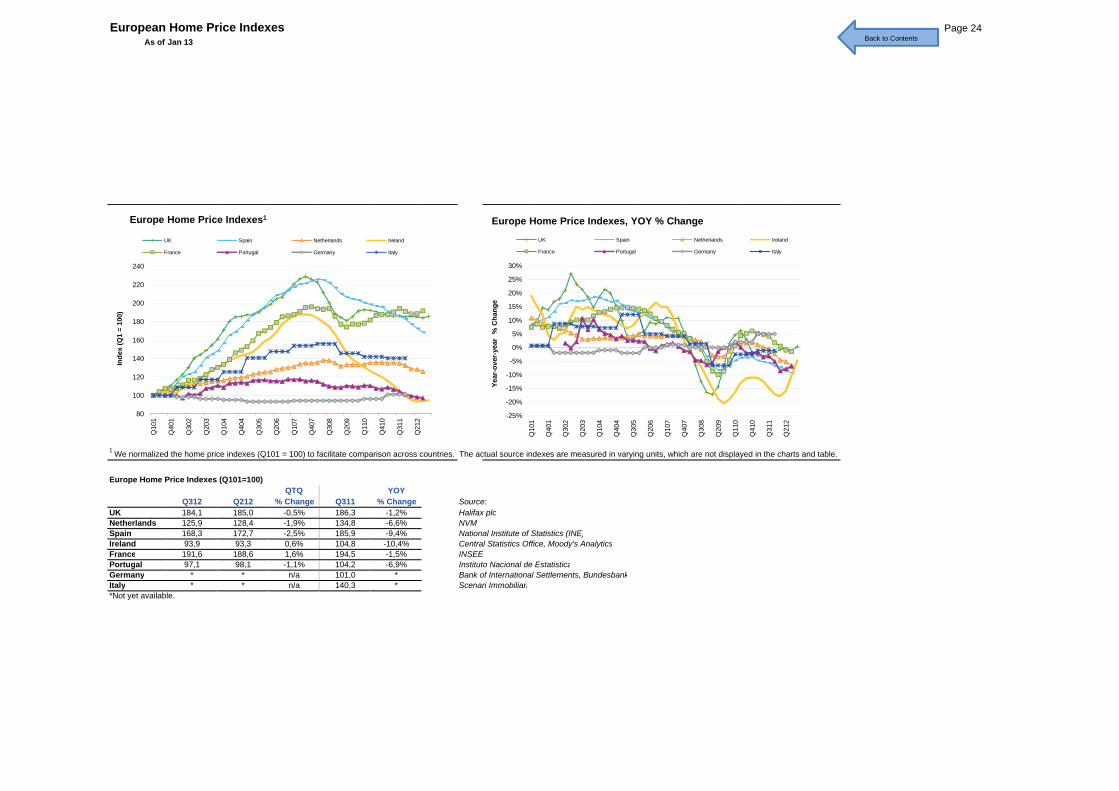

European Home Price Indexes Page 24As of Jan 13

120

140

160

180

200

220

240

Inde

x (Q

1 =

100)

Europe Home Price Indexes1

UK Spain Netherlands Ireland

France Portugal Germany Italy

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

ear-

over

-yea

r %

Cha

nge

Europe Home Price Indexes, YOY % ChangeUK Spain Netherlands Ireland

France Portugal Germany Italy

Back to Contents

1 We normalized the home price indexes (Q101 = 100) to facilitate comparison across countries. The actual source indexes are measured in varying units, which are not displayed in the charts and table.

Europe Home Price Indexes (Q101=100)QTQ YOY

Q312 Q212 % Change Q311 % Change Source:UK 184,1 185,0 -0,5% 186,3 -1,2% 2 Halifax plcNetherlands 125,9 128,4 -1,9% 134,8 -6,6% 8 NVMSpain 168,3 172,7 -2,5% 185,9 -9,4% 5 National Institute of Statistics (INE)Ireland 93,9 93,3 0,6% 104,8 -10,4% 11 Central Statistics Office, Moody's AnalyticsFrance 191,6 188,6 1,6% 194,5 -1,5% 14 INSEEPortugal 97,1 98,1 -1,1% 104,2 -6,9% 17 Instituto Nacional de EstatisticaGermany * * n/a 101,0 * 20 Bank of International Settlements, BundesbankItaly * * n/a 140,3 * 23 Scenari Immobiliari*Not yet available.

80

100

120

140

Q10

1

Q40

1

Q30

2

Q20

3

Q10

4

Q40

4

Q30

5

Q20

6

Q10

7

Q40

7

Q30

8

Q20

9

Q11

0

Q41

0

Q31

1

Q21

2

Ind

-25%

-20%

-15%

-10%

-5%

Q10

1

Q40

1

Q30

2

Q20

3

Q10

4

Q40

4

Q30

5

Q20

6

Q10

7

Q40

7

Q30

8

Q20

9

Q11

0

Q41

0

Q31

1

Q21

2

Year

-ove

r

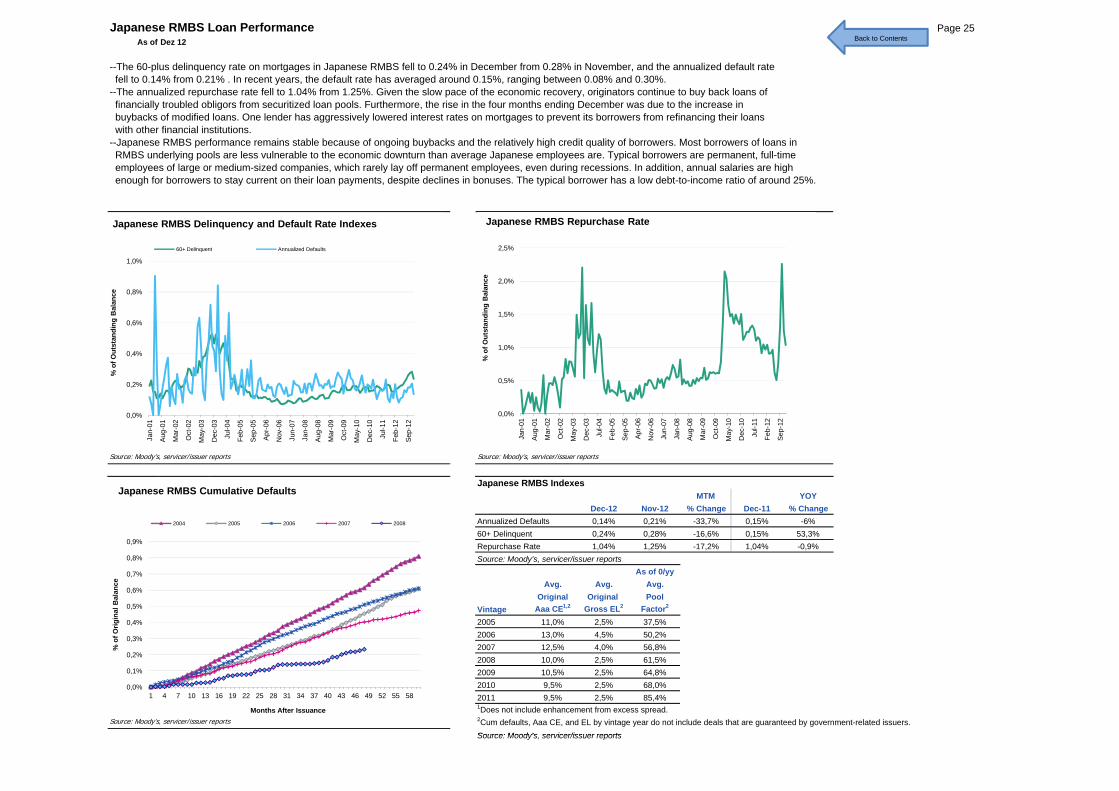

Japanese RMBS Loan Performance Page 25As of Dez 12

--The 60-plus delinquency rate on mortgages in Japanese RMBS fell to 0.24% in December from 0.28% in November, and the annualized default rate fell to 0.14% from 0.21% . In recent years, the default rate has averaged around 0.15%, ranging between 0.08% and 0.30%.--The annualized repurchase rate fell to 1.04% from 1.25%. Given the slow pace of the economic recovery, originators continue to buy back loans of financially troubled obligors from securitized loan pools. Furthermore, the rise in the four months ending December was due to the increase in buybacks of modified loans. One lender has aggressively lowered interest rates on mortgages to prevent its borrowers from refinancing their loans with other financial institutions.--Japanese RMBS performance remains stable because of ongoing buybacks and the relatively high credit quality of borrowers. Most borrowers of loans in RMBS underlying pools are less vulnerable to the economic downturn than average Japanese employees are. Typical borrowers are permanent, full-time employees of large or medium-sized companies, which rarely lay off permanent employees, even during recessions. In addition, annual salaries are high enough for borrowers to stay current on their loan payments, despite declines in bonuses. The typical borrower has a low debt-to-income ratio of around 25%.

0,2%

0,4%

0,6%

0,8%

1,0%

% o

f Out

stan

ding

Bal

ance

Japanese RMBS Delinquency and Default Rate Indexes

60+ Delinquent Annualized Defaults

0,5%

1,0%

1,5%

2,0%

2,5%

% o

f Out

stan

ding

Bal

ance

Japanese RMBS Repurchase Rate

Back to Contents

Japanese RMBS IndexesMTM YOY

Dec-12 Nov-12 % Change Dec-11 % ChangeAnnualized Defaults 0,14% 0,21% -33,7% 0,15% -6%60+ Delinquent 0,24% 0,28% -16,6% 0,15% 53,3%Repurchase Rate 1,04% 1,25% -17,2% 1,04% -0,9%

Source: Moody's, servicer/issuer reports 2As of 0/yy

Avg. Avg. Avg.Original Original Pool

Vintage Aaa CE1,2 Gross EL2 Factor2

2005 11,0% 2,5% 37,5%2006 13,0% 4,5% 50,2%2007 12,5% 4,0% 56,8%2008 10,0% 2,5% 61,5%2009 10,5% 2,5% 64,8%2010 9,5% 2,5% 68,0%2011 9,5% 2,5% 85,4%1Does not include enhancement from excess spread.2Cum defaults, Aaa CE, and EL by vintage year do not include deals that are guaranteed by government-related issuers.Source: Moody's servicer/issuer reports

0,0%

0,1%

0,2%

0,3%

0,4%

0,5%

0,6%

0,7%

0,8%

0,9%

1 4 7 10 13 16 19 22 25 28 31 34 37 40 43 46 49 52 55 58

% o

f Orig

inal

Bal

ance

Months After Issuance

Japanese RMBS Cumulative Defaults

2004 2005 2006 2007 2008

0,0%

0,2%

Jan-

01

Aug-

01

Mar

-02

Oct

-02

May

-03

Dec

-03

Jul-0

4

Feb-

05

Sep-

05

Apr-

06

Nov

-06

Jun-

07

Jan-

08

Aug-

08

Mar

-09

Oct

-09

May

-10

Dec

-10

Jul-1

1

Feb-

12

Sep-

12

% o

f

0,0%

0,5%

Jan-

01

Aug-

01

Mar

-02

Oct

-02

May

-03

Dec

-03

Jul-0

4

Feb-

05

Sep-

05

Apr-

06

Nov

-06

Jun-

07

Jan-

08

Aug-

08

Mar

-09

Oct

-09

May

-10

Dec

-10

Jul-1

1

Feb-

12

Sep-

12

Source: Moody's, servicer/issuer reportsSource: Moody's, servicer/issuer reports

Source: Moody's, servicer/issuer reports

Source: Moody's, servicer/issuer reports

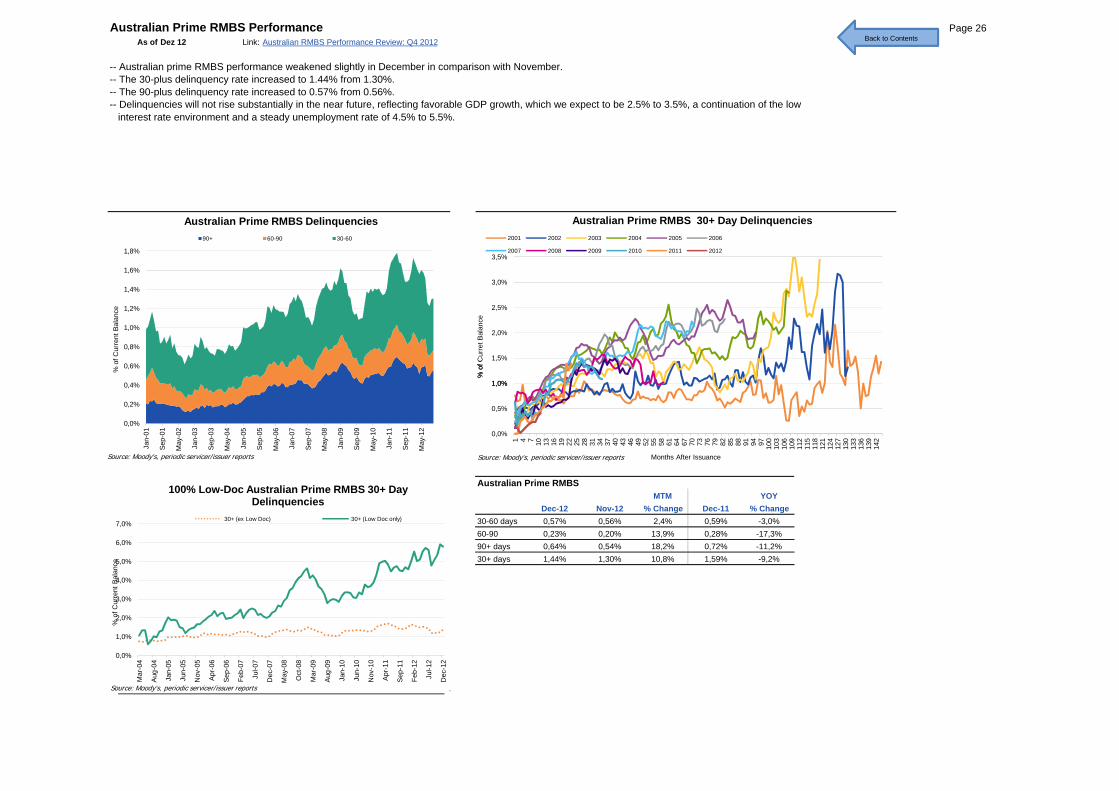

Australian Prime RMBS Performance Page 26As of Dez 12 Link: Australian RMBS Performance Review: Q4 2012

-- Australian prime RMBS performance weakened slightly in December in comparison with November.-- The 30-plus delinquency rate increased to 1.44% from 1.30%.-- The 90-plus delinquency rate increased to 0.57% from 0.56%.-- Delinquencies will not rise substantially in the near future, reflecting favorable GDP growth, which we expect to be 2.5% to 3.5%, a continuation of the low interest rate environment and a steady unemployment rate of 4.5% to 5.5%.

0,4%

0,6%

0,8%

1,0%

1,2%

1,4%

1,6%

1,8%

% o

f Cur

rent

Bal

ance

Australian Prime RMBS Delinquencies90+ 60-90 30-60

1,0%

1,5%

2,0%

2,5%

3,0%

3,5%

% o

f Cur

ret B

alan

ce

Australian Prime RMBS 30+ Day Delinquencies2001 2002 2003 2004 2005 2006

2007 2008 2009 2010 2011 2012

Back to ContentsBack to Contents

Australian Prime RMBSMTM YOY

Dec-12 Nov-12 % Change Dec-11 % Change30-60 days 0,57% 0,56% 2,4% 0,59% -3,0%60-90 0,23% 0,20% 13,9% 0,28% -17,3%90+ days 0,64% 0,54% 18,2% 0,72% -11,2%30+ days 1,44% 1,30% 10,8% 1,59% -9,2%

0,0%

0,2%

0,4%

0,6%

Jan-

01

Sep-

01

May

-02

Jan-

03

Sep-

03

May

-04

Jan-

05

Sep-

05

May

-06

Jan-

07

Sep-

07

May

-08

Jan-

09

Sep-

09

May

-10

Jan-

11

Sep-

11

May

-12

% o

0,0%

0,5%

1,0%

1 4 7 10 13 16 19 22 25 28 31 34 37 40 43 46 49 52 55 58 61 64 67 70 73 76 79 82 85 88 91 94 97 100

103

106

109

112

115

118

121

124

127

130

133

136

139

142

% o

f C

Months After Issuance

0,0%

1,0%

2,0%

3,0%

4,0%

5,0%

6,0%

7,0%

Mar

-04

Aug-

04

Jan-

05

Jun-

05

Nov

-05

Apr-

06

Sep-

06

Feb-

07

Jul-0

7

Dec

-07

May

-08

Oct

-08

Mar

-09

Aug-

09

Jan-

10

Jun-

10

Nov

-10

Apr-

11

Sep-

11

Feb-

12

Jul-1

2

Dec

-12

% o

f Cur

rent

Bal

ance

100% Low-Doc Australian Prime RMBS 30+ Day Delinquencies

30+ (ex Low Doc) 30+ (Low Doc only)

Source: Moody's, periodic servicer/issuer reports

Source: Moody's, periodic servicer/issuer reports Source: Moody's, periodic servicer/issuer reports

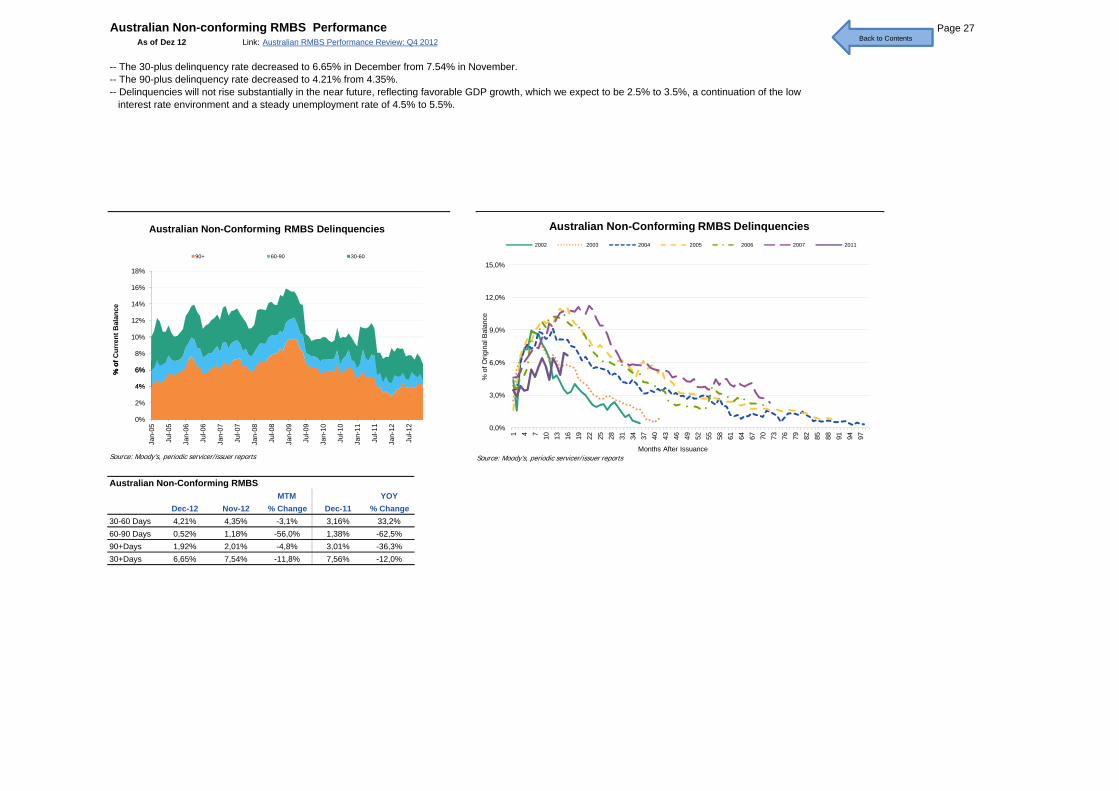

Australian Non-conforming RMBS Performance Page 27As of Dez 12 Link: Australian RMBS Performance Review: Q4 2012

-- The 30-plus delinquency rate decreased to 6.65% in December from 7.54% in November.-- The 90-plus delinquency rate decreased to 4.21% from 4.35%.-- Delinquencies will not rise substantially in the near future, reflecting favorable GDP growth, which we expect to be 2.5% to 3.5%, a continuation of the low interest rate environment and a steady unemployment rate of 4.5% to 5.5%.

4%

6%

8%

10%

12%

14%

16%

18%

% o

f Cur

rent

Bal

ance

Australian Non-Conforming RMBS Delinquencies

90+ 60-90 30-60

6,0%

9,0%

12,0%

15,0%

% o

f Orig

inal

Bal

ance

Australian Non-Conforming RMBS Delinquencies2002 2003 2004 2005 2006 2007 2011

Back to ContentsBack to Contents

Australian Non-Conforming RMBSMTM YOY

Dec-12 Nov-12 % Change Dec-11 % Change30-60 Days 4,21% 4,35% -3,1% 3,16% 33,2%60-90 Days 0,52% 1,18% -56,0% 1,38% -62,5%90+Days 1,92% 2,01% -4,8% 3,01% -36,3%30+Days 6,65% 7,54% -11,8% 7,56% -12,0%

0%

2%

4%

6%

Jan-

05

Jul-0

5

Jan-

06

Jul-0

6

Jan-

07

Jul-0

7

Jan-

08

Jul-0

8

Jan-

09

Jul-0

9

Jan-

10

Jul-1

0

Jan-

11

Jul-1

1

Jan-

12

Jul-1

2

% o

f

0,0%

3,0%

6,0%

1 4 7 10 13 16 19 22 25 28 31 34 37 40 43 46 49 52 55 58 61 64 67 70 73 76 79 82 85 88 91 94 97

% o

f O

Months After IssuanceSource: Moody's, periodic servicer/issuer reports Source: Moody's, periodic servicer/issuer reports

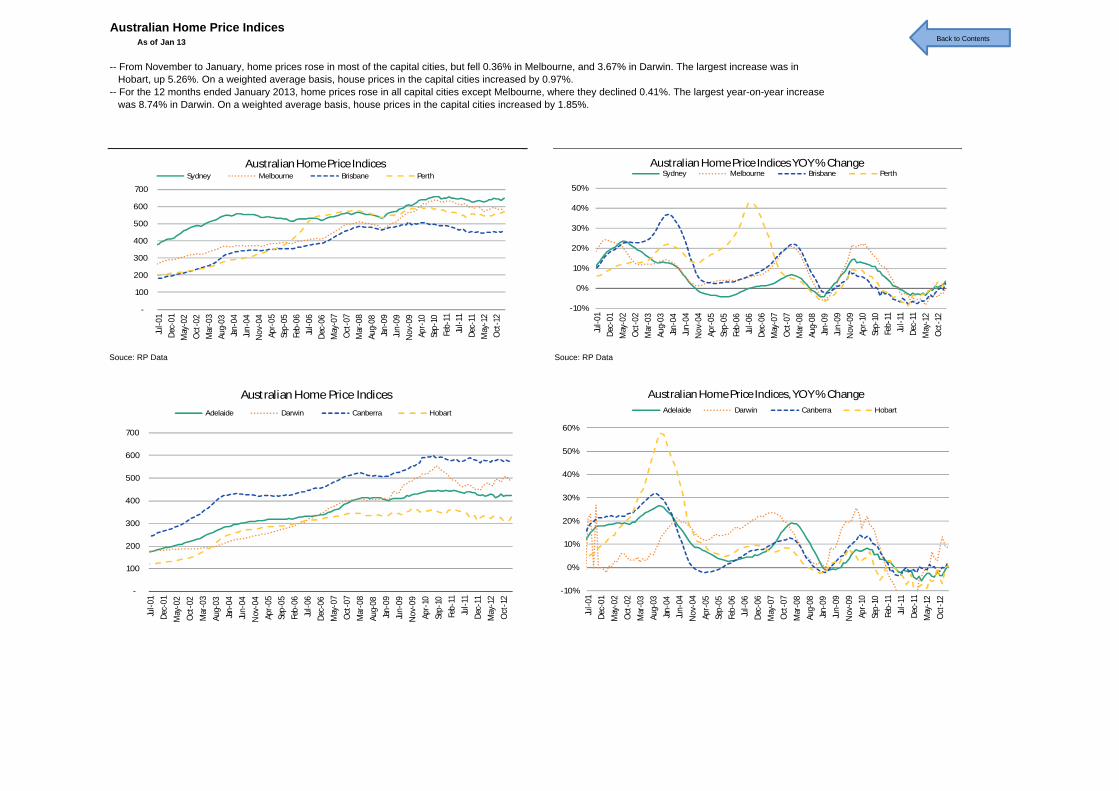

Australian Home Price IndicesAs of Jan 13

-- From November to January, home prices rose in most of the capital cities, but fell 0.36% in Melbourne, and 3.67% in Darwin. The largest increase was in Hobart, up 5.26%. On a weighted average basis, house prices in the capital cities increased by 0.97%.-- For the 12 months ended January 2013, home prices rose in all capital cities except Melbourne, where they declined 0.41%. The largest year-on-year increase was 8.74% in Darwin. On a weighted average basis, house prices in the capital cities increased by 1.85%.

Souce: RP Data Souce: RP Data

Back to Contents

-

100

200

300

400

500

600

700

Jul-0

1De

c-01

May

-02

Oct

-02

Mar

-03

Aug-

03Ja

n-04

Jun-

04N

ov-0

4Ap

r-05

Sep-

05Fe

b-06

Jul-0

6De

c-06

May

-07

Oct

-07

Mar

-08

Aug-

08Ja

n-09

Jun-

09N

ov-0

9Ap

r-10

Sep-

10Fe

b-11

Jul-1

1De

c-11

May

-12

Oct

-12

Australian Home Price IndicesSydney Melbourne Brisbane Perth

-10%

0%

10%

20%

30%

40%

50%

Jul-0

1De

c-01

May

-02

Oct

-02

Mar

-03

Aug-

03Ja

n-04

Jun-

04N

ov-0

4Ap

r-05

Sep-

05Fe

b-06

Jul-0

6De

c-06

May

-07

Oct

-07

Mar

-08

Aug-

08Ja

n-09

Jun-

09N

ov-0

9Ap

r-10

Sep-

10Fe

b-11

Jul-1

1De

c-11

May

-12

Oct

-12

Australian Home Price Indices YOY % ChangeSydney Melbourne Brisbane Perth

-

100

200

300

400

500

600

700

Jul-0

1De

c-01

May

-02

Oct

-02

Mar

-03

Aug-

03Ja

n-04

Jun-

04N

ov-0

4Ap

r-05

Sep-

05Fe

b-06

Jul-0

6De

c-06

May

-07

Oct

-07

Mar

-08

Aug-

08Ja

n-09

Jun-

09N

ov-0

9Ap

r-10

Sep-

10Fe

b-11

Jul-1

1De

c-11

May

-12

Oct

-12

Australian Home Price IndicesAdelaide Darwin Canberra Hobart

-10%

0%

10%

20%

30%

40%

50%

60%

Jul-0

1De

c-01

May

-02

Oct

-02

Mar

-03

Aug-

03Ja

n-04

Jun-

04N

ov-0

4Ap

r-05

Sep-

05Fe

b-06

Jul-0

6De

c-06

May

-07

Oct

-07

Mar

-08

Aug-

08Ja

n-09

Jun-

09N

ov-0

9Ap

r-10

Sep-

10Fe

b-11

Jul-1

1De

c-11

May

-12

Oct

-12

Australian Home Price Indices, YOY % ChangeAdelaide Darwin Canberra Hobart

Page 28

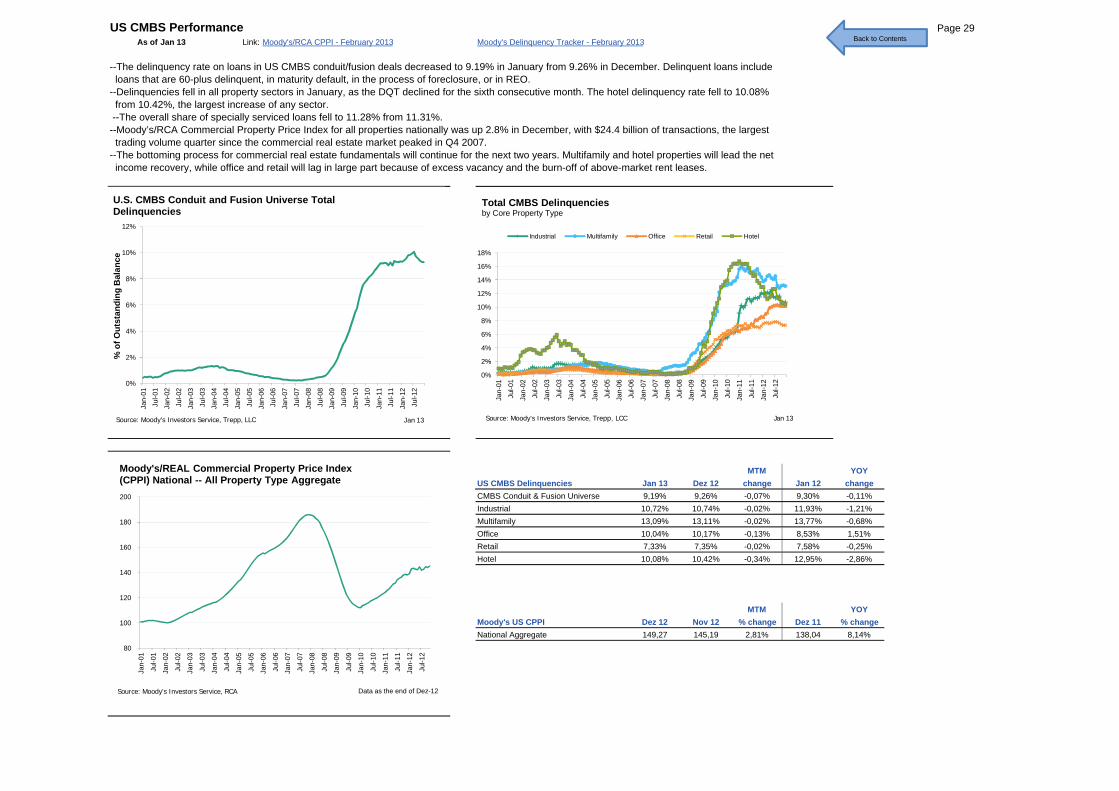

US CMBS Performance Page 29As of Jan 13 Link: Moody's/RCA CPPI - February 2013 Moody's Delinquency Tracker - February 2013

--The delinquency rate on loans in US CMBS conduit/fusion deals decreased to 9.19% in January from 9.26% in December. Delinquent loans include loans that are 60-plus delinquent, in maturity default, in the process of foreclosure, or in REO.--Delinquencies fell in all property sectors in January, as the DQT declined for the sixth consecutive month. The hotel delinquency rate fell to 10.08% from 10.42%, the largest increase of any sector. --The overall share of specially serviced loans fell to 11.28% from 11.31%.--Moody’s/RCA Commercial Property Price Index for all properties nationally was up 2.8% in December, with $24.4 billion of transactions, the largest trading volume quarter since the commercial real estate market peaked in Q4 2007.--The bottoming process for commercial real estate fundamentals will continue for the next two years. Multifamily and hotel properties will lead the net income recovery, while office and retail will lag in large part because of excess vacancy and the burn-off of above-market rent leases.

0%

2%

4%

6%

8%

10%

12%

% o

f Out

stan

ding

Bal

ance

U.S. CMBS Conduit and Fusion Universe Total Delinquencies

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

-01

-01

-02

-02

-03

-03

-04

-04

-05

-05

-06

-06

-07

-07

-08

-08

-09

-09

-10

-10

-11

-11

-12

-12

Total CMBS Delinquenciesby Core Property Type

Industrial Multifamily Office Retail Hotel

Back to Contents

Data as of end of 00 yyyy MTM YOYUS CMBS Delinquencies Jan 13 Dez 12 change Jan 12 changeCMBS Conduit & Fusion Universe 9,19% 9,26% -0,07% 9,30% -0,11%Industrial 10,72% 10,74% -0,02% 11,93% -1,21%Multifamily 13,09% 13,11% -0,02% 13,77% -0,68%Office 10,04% 10,17% -0,13% 8,53% 1,51%Retail 7,33% 7,35% -0,02% 7,58% -0,25%Hotel 10,08% 10,42% -0,34% 12,95% -2,86%

MTM YOYMoody's US CPPI Dez 12 Nov 12 % change Dez 11 % changeNational Aggregate 149,27 145,19 2,81% 138,04 8,14%

Data as the end of Dez-12

0%

Jan-

01Ju

l-01

Jan-

02

Jul-0

2

Jan-

03

Jul-0

3Ja

n-04

Jul-0

4

Jan-

05

Jul-0

5

Jan-

06Ju

l-06

Jan-

07

Jul-0

7

Jan-

08

Jul-0

8Ja

n-09

Jul-0

9

Jan-

10

Jul-1

0

Jan-

11Ju

l-11

Jan-

12

Jul-1

2Jan 13Source: Moody's Investors Service, Trepp, LLC

0%

2%

Jan-

01

Jul-0

1

Jan-

02

Jul-0

2

Jan-

03

Jul-0

3

Jan-

04

Jul-0

4

Jan-

05

Jul-0

5

Jan-

06

Jul-0

6

Jan-

07

Jul-0

7

Jan-

08

Jul-0

8

Jan-

09

Jul-0

9

Jan-

10

Jul-1

0

Jan-

11

Jul-1

1

Jan-

12

Jul-1

2

Jan 13Source: Moody's Investors Service, Trepp, LCC

80

100

120

140

160

180

200

Jan-

01

Jul-0

1

Jan-

02

Jul-0

2

Jan-

03

Jul-0

3

Jan-

04

Jul-0

4

Jan-

05

Jul-0

5

Jan-

06

Jul-0

6

Jan-

07

Jul-0

7

Jan-

08

Jul-0

8

Jan-

09

Jul-0

9

Jan-

10

Jul-1

0

Jan-

11

Jul-1

1

Jan-

12

Jul-1

2

Moody's/REAL Commercial Property Price Index (CPPI) National -- All Property Type Aggregate

Source: Moody's Investors Service, RCA Data as the end of Dez-12

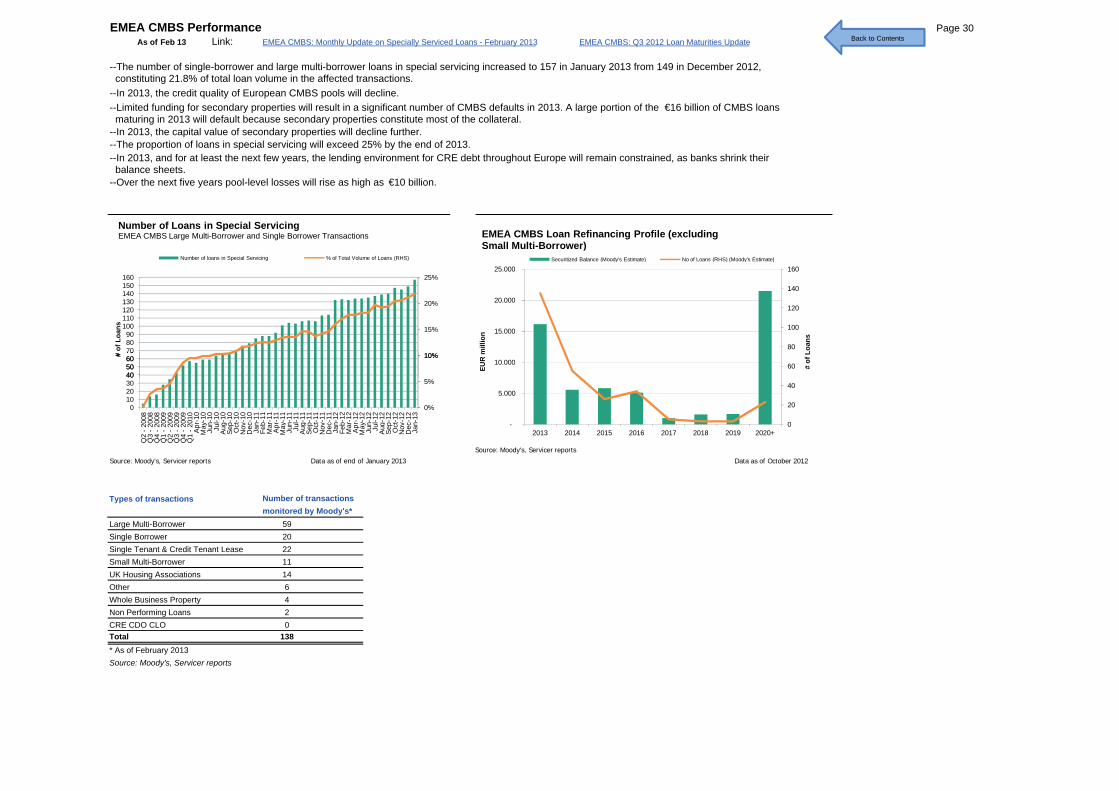

EMEA CMBS Performance Page 30As of Feb 13 Link: EMEA CMBS: Monthly Update on Specially Serviced Loans - February 2013 EMEA CMBS: Q3 2012 Loan Maturities Update