Embed Size (px)

Citation preview

1

VLCC chartering activity is good,

though charter rates are a little

down. Market fundamentals

seem to support optimism for

rate upturn within the next

month. The Suezmax charter-

market is going strong, and

Aframaxes are gaining on

weather related delays. This

continues to feed the positive

S&P sentiment, and there is

little trouble finding buyers for

crude tankers nowadays, willing

(and realistic) sellers however

are rather thin on the

ground. China has witnessed

much of the S&P action with GC

Tankers (HNA) offloading four

VLCCs this month and

Rongsheng associate Roxen

Shipping selling two Suezmaxes

in an uncharacteristic second

hand swoop by Fredriksen.

Since it began 30 years ago, the

BDI has never been this

low. Whilst the composition of

the index may well have

changed somewhat since the

last record low in 1986, this is

cold comfort to owners having

to face the daily reality of this

market with no obvious end in

sight. So are there any reasons

to be cheerful amidst all this

charter market gloom? Well,

more Capes have been

scrapped in the last month than

in the whole of last year, and

we may finally be starting to

see a healthier rate of scrap-

ping despite lower demolition

prices. In S&P asset prices are

falling gradually, more pro-

nouncedly on distressed

units. Accordingly, there has

been a noticeable increase in

the number of failing deals.

We have completed quite a few

2nd hand transactions of both

13’dwt IMO2 coated tankers,

19’stst IMO2 tankers, and

smaller stst specialized tankers

since the new year. While we

cannot comment on specific

details of in house transactions,

we can confirm that the last

deals in all these segments of

the chemical tanker fleet reflect

a market where asset values

remain under pressure, and

positive notes (from a seller’s

perspective) are limited to con-

tinued low bunker prices which

move some buyers’ focus off

new buildings and on to second

hand ships, along with the

weak JPY against USD where

applicable. However, from a

buyer’s perspective; at time of

writing the market does sup-

port schemes where obtainable

2-3 year TC rates justify pur-

chases at market levels, and as

such investors entering now

should be in good shape to ride

out the storm on the back of

longer time charter commit-

ments, before assets again start

to pick up value.

More S&P activity has been

seen for LPG ships. Contracting

activity was limited to one fully

ref. MGC of 38,000cbm ordered

by KSS Line at Hyundai Mipo at

US$ 52 million. Two VLGCs

were reported sold, the Hellas

Argosy (80530cbm, 2013 built)

realized US$ 66 million and the

Gas Sapphire (75358cbm, 1993

built) US$40 million. Levels

were below expectations for

the modern ship and above

expectations for the oldest

ship. The smaller gas vessel, the

Gas Pacu, was sold from Prime

to Asian buyers for US$ 5.8

million. Demolition of smaller

gas carriers has been more ac-

tive lately with three sales con-

cluded over the past month,

the ethylene carriers Gas Coral,

East Med Gas and Capricorn

Gas. No new activity was rec-

orded in LNG.

HIGHLIGHTS

Crude: High

activity in VLCC

second hand

market

Dry: BDI at all-time

low cutting

expectations for

recovery

Product/Chemical:

2-3 year TC rates

justifying current

asset values

February 2015

Dry

Crude

Product/Chemical

Gas

Monthly S&P Report

-Shipbrokers and consultants since 1919-

Hot Hulls

2

-Shipbrokers and consultants since 1919-

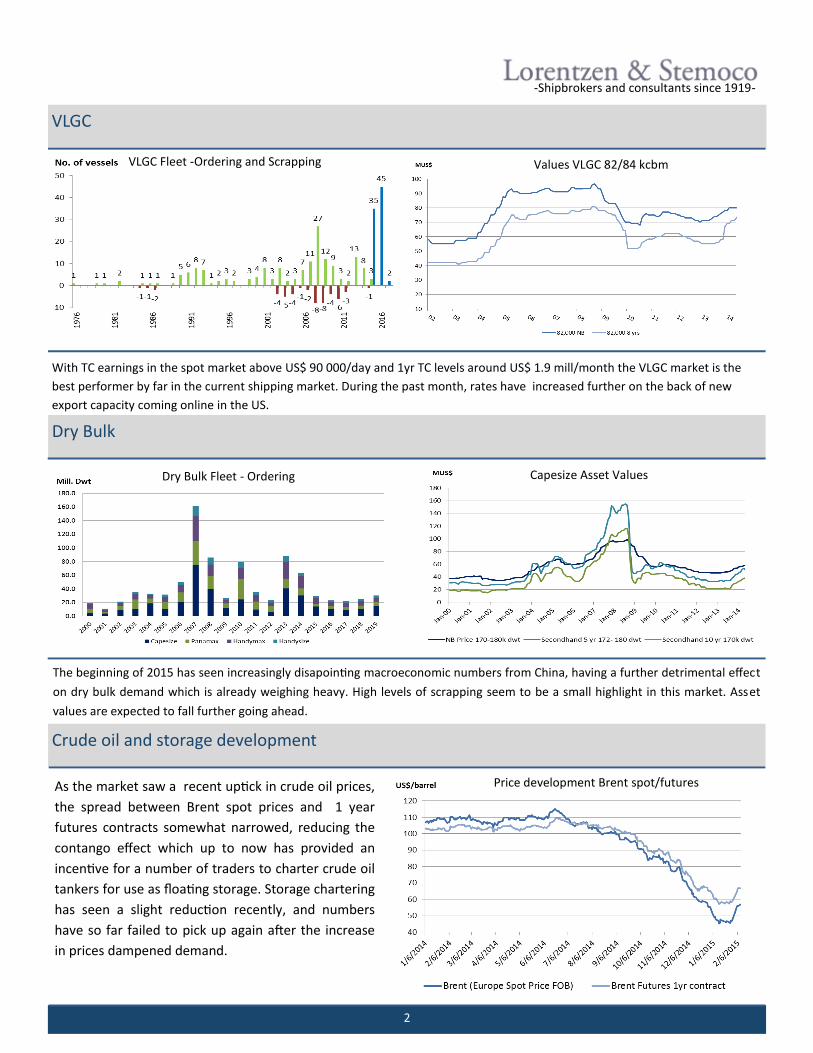

With TC earnings in the spot market above US$ 90 000/day and 1yr TC levels around US$ 1.9 mill/month the VLGC market is the

best performer by far in the current shipping market. During the past month, rates have increased further on the back of new

export capacity coming online in the US.

VLGC

Dry Bulk

Crude oil and storage development

The beginning of 2015 has seen increasingly disapointing macroeconomic numbers from China, having a further detrimental effect

on dry bulk demand which is already weighing heavy. High levels of scrapping seem to be a small highlight in this market. Asset

values are expected to fall further going ahead.

VLGC Fleet -Ordering and Scrapping

Capesize Asset Values Dry Bulk Fleet - Ordering

Values VLGC 82/84 kcbm

Price development Brent spot/futures As the market saw a recent uptick in crude oil prices,

the spread between Brent spot prices and 1 year

futures contracts somewhat narrowed, reducing the

contango effect which up to now has provided an

incentive for a number of traders to charter crude oil

tankers for use as floating storage. Storage chartering

has seen a slight reduction recently, and numbers

have so far failed to pick up again after the increase

in prices dampened demand.

3

Special Report - In a sea of QE -Shipbrokers and consultants since 1919-

A massive economic experiment is underway as cen-

tral banks are getting into the groove of quantitative

easing (QE), in a bid to stimulate the economy and

boost competitiveness. This is the last in a line of poli-

cy strategies attempting to increase spending and in-

flationary pressure, as currencies keep depreciating

and growth slows in Asia and Europe.

Leading the charge is the Japanese Yen, which has

been in a race to the bottom for the past few months,

deprecating almost 10% relative to the US dollar

since November last year (and by around 40% over

the past two years with Abenomics) when the Japa-

nese Government announced the addition of further

measures to its QE program in an attempt to increase

spending and support economic growth.

With the view to offset deflationary trends in the

global economy, more and more central banks are

employing similar stimulus strategies, lastly the Euro-

pean Central Bank, announcing a massive 1 trillion

Euro asset buying program last month. The result is

what seems to be an ever more aggressive currency

war concealed behind altruistic growth policies. For

any company with receivables in US$ and payables in

Euro, the current situation is a welcome one.

With the Euro expected to depreciate further relative

to other currencies as the ECBs program comes under

way, the Eurobond market is increasingly becoming

an interesting bet, also for the shipping industry. The

China State Shipbuilding Corporation (CSSC) recently

joined other Chinese shipping interests who have

been raising euro-denominated funds, and thereby

taking advantage of a very low coupon rate of 1.7%.

The recent flight to bonds as a ‘safe haven’ compared

to other securities has been pushing rates lower. Eu-

ros should be looking attractive for Chinese players at

the moment, as the comparable rate from Bank of

China is standing at 3.125% for January 2019 maturi-

ty. Of course there is a currency risk involved here,

but the bet nonetheless seems an attractive one for

some.

The shipping market is seeing various dynamics com-

ing forward as a result of currency depreciation, and

especially so in ship building. Some talk has been

heard of Japanese yards making their way back into

segments long dominated by Korean yards, and due

to the lack of other alternatives this trend does not

seem to be abating.

As stimulus programs continue on their way, central

banks are keeping interest rates low (only the US FED

has signaled a possible hike in rates within the end of

the year) meaning capital comes cheap for those with

access to it. The question remains whether we need

more new buildings in all segments, or whether some

markets are increasingly saturated as ordering has

been high on the back of expected growth that has

failed to materialize, such as in dry bulk.

In the second hand market however, the next few

months look set to offer some very interesting oppor-

tunities as the bid-ask spread in various segments

narrows, especially for those thinking about fleet re-

newals and who are able to take advantage of incen-

tives presented by the effects of QE.

4

-Shipbrokers and consultants since 1919-

Scrapping

Newbuilding Prices (China)

Bunker Prices

Panamax and Capesize Scrapping Scrap Price Developments

Dry Bulk NB Prices (China) Tanker NB Prices (China)

Source: AXS/L&S Research

(US$/mt) February to date January Trend

Rotterdam IFO 380 291.2 254.1 Firming

Rotterdam MGO 528.9 483.4 Firming

Singapore IFO 380 335.2 284.8 Firming

Singapore MGO 541.1 504.5 Firming

Dry Bulk Jan-15 Dec-14 Nov-14 Trend

Newcastlemax 55.7 56.4 56.5 Softening

Capesize 52.5 53.1 53.4 Softening

Kamsarmax 29.1 29.4 29.5 Softening

Panamax 28.0 28.3 28.4 Softening

Handysize 22.9 23.1 23.2 Softening

Tanker

VLCC 94.4 94.5 94.5 Softening

Suezmax 60.5 60.6 60.5 Steady

LR2 51.2 50.9 51.2 Steady

LR1 40.4 40.6 40.2 Firming

MR 35.1 35.1 35.2 Softening

5

-Shipbrokers and consultants since 1919-

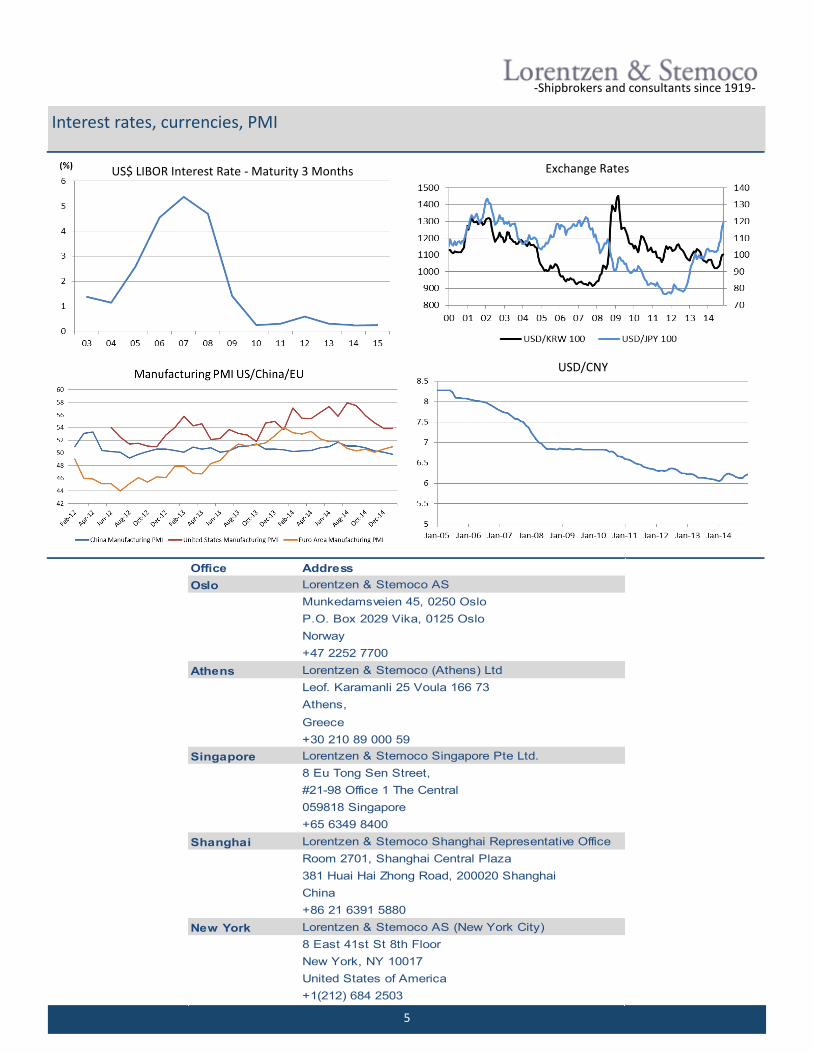

Interest rates, currencies, PMI

Manufacturing PMI US/China/EU

US$ LIBOR Interest Rate - Maturity 3 Months

USD/CNY

Exchange Rates

Office Address

Oslo Lorentzen & Stemoco AS

Munkedamsveien 45, 0250 Oslo

P.O. Box 2029 Vika, 0125 Oslo

Norway

+47 2252 7700

Athens Lorentzen & Stemoco (Athens) Ltd

Leof. Karamanli 25 Voula 166 73

Athens,

Greece

+30 210 89 000 59

Singapore Lorentzen & Stemoco Singapore Pte Ltd.

8 Eu Tong Sen Street,

#21-98 Office 1 The Central

059818 Singapore

+65 6349 8400

Shanghai Lorentzen & Stemoco Shanghai Representative Office

Room 2701, Shanghai Central Plaza

381 Huai Hai Zhong Road, 200020 Shanghai

China

+86 21 6391 5880

New York Lorentzen & Stemoco AS (New York City)

8 East 41st St 8th Floor

New York, NY 10017

United States of America

+1(212) 684 2503

6

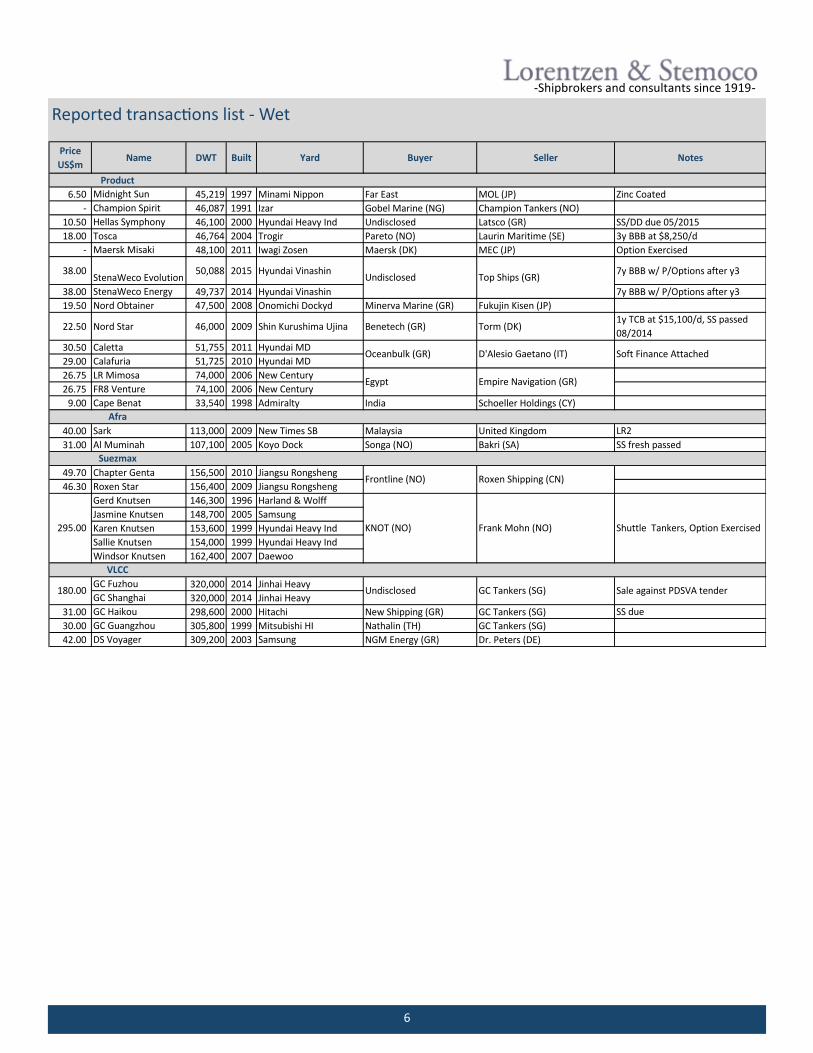

Reported transactions list - Wet

-Shipbrokers and consultants since 1919-

Price

US$mName DWT Built Yard Buyer Seller Notes

6.50 Midnight Sun 45,219 1997 Minami Nippon Far East MOL (JP) Zinc Coated

- Champion Spirit 46,087 1991 Izar Gobel Marine (NG) Champion Tankers (NO)

10.50 Hellas Symphony 46,100 2000 Hyundai Heavy Ind Undisclosed Latsco (GR) SS/DD due 05/2015

18.00 Tosca 46,764 2004 Trogir Pareto (NO) Laurin Maritime (SE) 3y BBB at $8,250/d

- Maersk Misaki 48,100 2011 Iwagi Zosen Maersk (DK) MEC (JP) Option Exercised

38.00 StenaWeco Evolution

50,088 2015 Hyundai Vinashin 7y BBB w/ P/Options after y3

38.00 StenaWeco Energy 49,737 2014 Hyundai Vinashin 7y BBB w/ P/Options after y3

19.50 Nord Obtainer 47,500 2008 Onomichi Dockyd Minerva Marine (GR) Fukujin Kisen (JP)

22.50 Nord Star 46,000 2009 Shin Kurushima Ujina Benetech (GR) Torm (DK)1y TCB at $15,100/d, SS passed

08/2014

30.50 Caletta 51,755 2011 Hyundai MD

29.00 Calafuria 51,725 2010 Hyundai MD

26.75 LR Mimosa 74,000 2006 New Century

26.75 FR8 Venture 74,100 2006 New Century

9.00 Cape Benat 33,540 1998 Admiralty India Schoeller Holdings (CY)

40.00 Sark 113,000 2009 New Times SB Malaysia United Kingdom LR2

31.00 Al Muminah 107,100 2005 Koyo Dock Songa (NO) Bakri (SA) SS fresh passed

49.70 Chapter Genta 156,500 2010 Jiangsu Rongsheng

46.30 Roxen Star 156,400 2009 Jiangsu Rongsheng

Gerd Knutsen 146,300 1996 Harland & Wolff

Jasmine Knutsen 148,700 2005 Samsung

Karen Knutsen 153,600 1999 Hyundai Heavy Ind

Sallie Knutsen 154,000 1999 Hyundai Heavy Ind

Windsor Knutsen 162,400 2007 Daewoo

GC Fuzhou 320,000 2014 Jinhai Heavy

GC Shanghai 320,000 2014 Jinhai Heavy

31.00 GC Haikou 298,600 2000 Hitachi New Shipping (GR) GC Tankers (SG) SS due

30.00 GC Guangzhou 305,800 1999 Mitsubishi HI Nathalin (TH) GC Tankers (SG)

42.00 DS Voyager 309,200 2003 Samsung NGM Energy (GR) Dr. Peters (DE)

Product

Afra

Suezmax

VLCC

Undisclosed Top Ships (GR)

Oceanbulk (GR) D'Alesio Gaetano (IT) Soft Finance Attached

Egypt Empire Navigation (GR)

KNOT (NO)295.00 Frank Mohn (NO) Shuttle Tankers, Option Exercised

Frontline (NO) Roxen Shipping (CN)

180.00 Undisclosed GC Tankers (SG) Sale against PDSVA tender

7

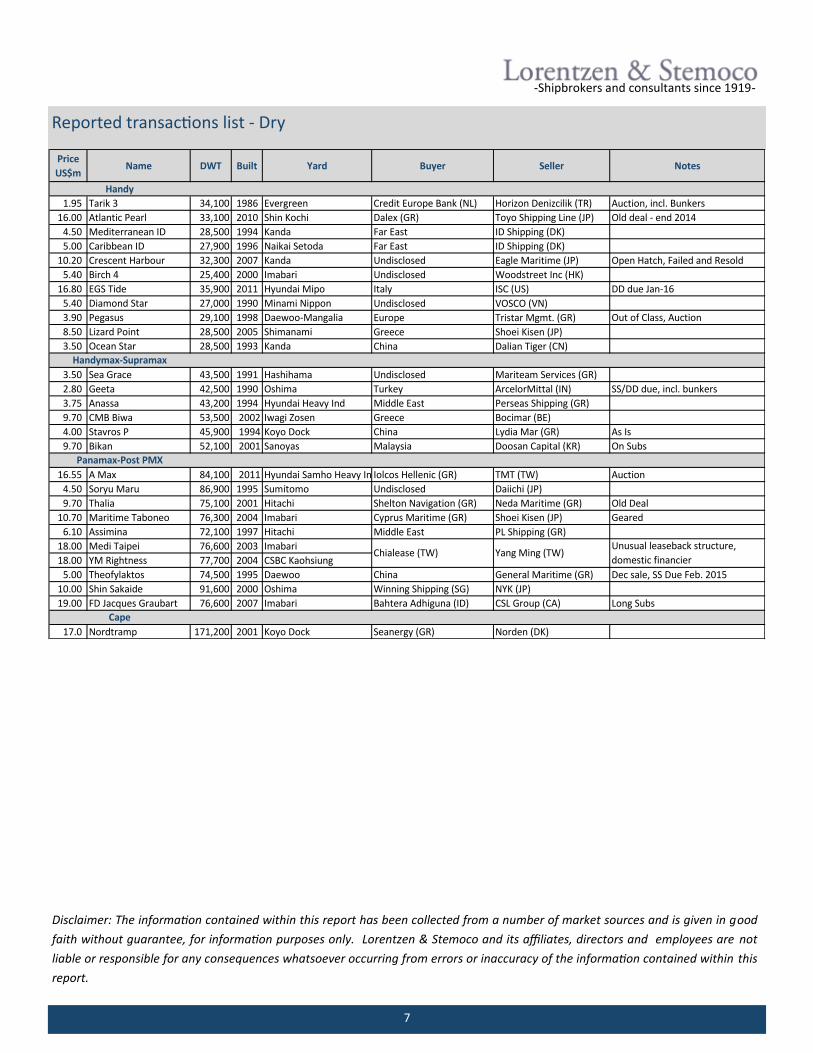

Reported transactions list - Dry

-Shipbrokers and consultants since 1919-

Disclaimer: The information contained within this report has been collected from a number of market sources and is given in good

faith without guarantee, for information purposes only. Lorentzen & Stemoco and its affiliates, directors and employees are not

liable or responsible for any consequences whatsoever occurring from errors or inaccuracy of the information contained within this

report.

Price

US$mName DWT Built Yard Buyer Seller Notes

1.95 Tarik 3 34,100 1986 Evergreen Credit Europe Bank (NL) Horizon Denizcilik (TR) Auction, incl. Bunkers

16.00 Atlantic Pearl 33,100 2010 Shin Kochi Dalex (GR) Toyo Shipping Line (JP) Old deal - end 2014

4.50 Mediterranean ID 28,500 1994 Kanda Far East ID Shipping (DK)

5.00 Caribbean ID 27,900 1996 Naikai Setoda Far East ID Shipping (DK)

10.20 Crescent Harbour 32,300 2007 Kanda Undisclosed Eagle Maritime (JP) Open Hatch, Failed and Resold

5.40 Birch 4 25,400 2000 Imabari Undisclosed Woodstreet Inc (HK)

16.80 EGS Tide 35,900 2011 Hyundai Mipo Italy ISC (US) DD due Jan-16

5.40 Diamond Star 27,000 1990 Minami Nippon Undisclosed VOSCO (VN)

3.90 Pegasus 29,100 1998 Daewoo-Mangalia Europe Tristar Mgmt. (GR) Out of Class, Auction

8.50 Lizard Point 28,500 2005 Shimanami Greece Shoei Kisen (JP)

3.50 Ocean Star 28,500 1993 Kanda China Dalian Tiger (CN)

3.50 Sea Grace 43,500 1991 Hashihama Undisclosed Mariteam Services (GR)

2.80 Geeta 42,500 1990 Oshima Turkey ArcelorMittal (IN) SS/DD due, incl. bunkers

3.75 Anassa 43,200 1994 Hyundai Heavy Ind Middle East Perseas Shipping (GR)

9.70 CMB Biwa 53,500 2002 Iwagi Zosen Greece Bocimar (BE)

4.00 Stavros P 45,900 1994 Koyo Dock China Lydia Mar (GR) As Is

9.70 Bikan 52,100 2001 Sanoyas Malaysia Doosan Capital (KR) On Subs

16.55 A Max 84,100 2011 Hyundai Samho Heavy IndIolcos Hellenic (GR) TMT (TW) Auction

4.50 Soryu Maru 86,900 1995 Sumitomo Undisclosed Daiichi (JP)

9.70 Thalia 75,100 2001 Hitachi Shelton Navigation (GR) Neda Maritime (GR) Old Deal

10.70 Maritime Taboneo 76,300 2004 Imabari Cyprus Maritime (GR) Shoei Kisen (JP) Geared

6.10 Assimina 72,100 1997 Hitachi Middle East PL Shipping (GR)

18.00 Medi Taipei 76,600 2003 Imabari

18.00 YM Rightness 77,700 2004 CSBC Kaohsiung

5.00 Theofylaktos 74,500 1995 Daewoo China General Maritime (GR) Dec sale, SS Due Feb. 2015

10.00 Shin Sakaide 91,600 2000 Oshima Winning Shipping (SG) NYK (JP)

19.00 FD Jacques Graubart 76,600 2007 Imabari Bahtera Adhiguna (ID) CSL Group (CA) Long Subs

17.0 Nordtramp 171,200 2001 Koyo Dock Seanergy (GR) Norden (DK)

Unusual leaseback structure,

domestic financier

Cape

Handy

Handymax-Supramax

Panamax-Post PMX

Chialease (TW) Yang Ming (TW)