Embed Size (px)

Citation preview

2016/17

Montenegro

PKF Worldwide Tax Guide 2016/17 1

FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are there double tax treaties in place? How will foreign source income be taxed? Since 1994, the PKF network of independent member firms, administered by PKF International Limited, has produced the PKF Worldwide Tax Guide (WWTG) to provide international businesses with the answers to these key tax questions. As you will appreciate, the production of the WWTG is a huge team effort and we would like to thank all tax experts within PKF member firms who gave up their time to contribute the vital information on their country's taxes that forms the heart of this publication. The PKF Worldwide Tax Guide 2016/17 (WWTG) is an annual publication that provides an overview of the taxation and business regulation regimes of the world's most significant trading countries. In compiling this publication, member firms of the PKF network have based their summaries on information current on 30 April 2016, while also noting imminent changes where necessary. On a country-by-country basis, each summary such as this one, addresses the major taxes applicable to business; how taxable income is determined; sundry other related taxation and business issues; and the country's personal tax regime. The final section of each country summary sets out the Double Tax Treaty and Non-Treaty rates of tax withholding relating to the payment of dividends, interest, royalties and other related payments. While the WWTG should not to be regarded as offering a complete explanation of the taxation issues in each country, we hope readers will use the publication as their first point of reference and then use the services of their local PKF member firm to provide specific information and advice. Services provided by member firms include: Assurance & Advisory;

Financial Planning / Wealth Management;

Corporate Finance;

Management Consultancy;

IT Consultancy;

Insolvency - Corporate and Personal;

Taxation;

Forensic Accounting; and,

Hotel Consultancy. In addition to the printed version of the WWTG, individual country taxation guides such as this are available in PDF format which can be downloaded from the PKF website at www.pkf.com

Montenegro

PKF Worldwide Tax Guide 2016/17 2

IMPORTANT DISCLAIMER This publication should not be regarded as offering a complete explanation of the taxation matters that are contained within this publication. This publication has been sold or distributed on the express terms and understanding that the publishers and the authors are not responsible for the results of any actions which are undertaken on the basis of the information which is contained within this publication, nor for any error in, or omission from, this publication. The publishers and the authors expressly disclaim all and any liability and responsibility to any person, entity or corporation who acts or fails to act as a consequence of any reliance upon the whole or any part of the contents of this publication. Accordingly no person, entity or corporation should act or rely upon any matter or information as contained or implied within this publication without first obtaining advice from an appropriately qualified professional person or firm of advisors, and ensuring that such advice specifically relates to their particular circumstances. PKF International Limited (PKFI) administers a family of legally independent firms. Neither PKFI nor the member firms of the network generally accept any responsibility or liability for the actions or inactions of any individual member or correspondent firm or firms. PKF INTERNATIONAL LIMITED JUNE 2016 © PKF INTERNATIONAL LIMITED All RIGHTS RESERVED USE APPROVED WITH ATTRIBUTION

Montenegro

PKF Worldwide Tax Guide 2016/17 3

STRUCTURE OF COUNTRY DESCRIPTIONS A. TAXES PAYABLE

COMPANY TAX CAPITAL GAINS TAX BRANCH PROFITS TAX SALES TAX / VALUE ADDED TAX FRINGE BENEFITS TAX LOCAL TAXES OTHER TAXES CUSTOMS DUTIES EXCISE DUTY PROPERTY TAX REAL ESTATE TRANSFER TAX

B. DETERMINATION OF TAXABLE INCOME

DEPRECIATION STOCK / INVENTORY CAPITAL GAINS AND LOSSES DIVIDENDS INTEREST DEDUCTIONS LOSSES FOREIGN SOURCED INCOME INCENTIVES

C. FOREIGN TAX RELIEF D. CORPORATE GROUPS E. RELATED PARTY TRANSACTIONS F. EXCHANGE CONTROL G. PERSONAL INCOME TAX H. TREATY AND NON-TREATY WITHHOLDING TAX RATES

Montenegro

PKF Worldwide Tax Guide 2016/17 4

MEMBER FIRM City Name Contact Information Beograd Petar Grubor +381 11 30 18 445 [email protected] BASIC FACTS Full name: Montenegro Capital: Podgorica Main languages: Montenegrin (also Serbian, Bosniak, Albanian and Croatian) Population: 620,029 (2011 census) Major religion: Christianity Monetary unit: Euro (EUR) Internet domain: .me Int. dialling code: +382 KEY TAX POINTS • Resident legal entities in Montenegro are liable to pay tax on their worldwide income and non-

resident taxpayers are taxed on their Montenegro-sourced income or income attributed to their Montenegrin permanent establishment (PE).

• Capital gains are included in the taxable income and subjected to 9% tax rate. Capital gains may be offset only against capital losses.

• Tax losses may be carried forward for 5 years; this also applies for capital losses. • Non-residents carrying out business in Montenegro through a permanent establishment are taxed

on their Montenegro-source income at rate of 9%. A branch is also considered to form a permanent establishment.

• The main principles of the Montenegrin VAT are in line with the European Union (EU) Sixth Directive guidelines. Value Added Tax (VAT) is charged at a standard rate of 19%, however, certain supplies are taxed at a reduced rate of 7% (e.g. bread, milk, books, medicines, and computers) and 0% rate is applied on export. Certain exemptions exist for financial services, the sale of land etc.

• Residents of Montenegro are subject to personal income tax on their worldwide income. Non-residents are subject to income tax on their income from Montenegro-source income under the same rules as residents.

• Personal income tax is levied at the rate of 13% on gross personal income above EUR 720 per month, while personal income tax for income below EUR 720 per month is subject to a personal income tax rate of 9%. The tax rate on revenues from interest paid to non-residents is 5%.

A. TAXES PAYABLE COMPANY TAX A resident is a legal entity which is incorporated or has a place of effective management and control on the territory of Montenegro. Resident legal entities in Montenegro are liable to pay tax on their worldwide income and non-resident entities on the income derived from local sources. Non-resident taxpayers are taxed on their Montenegro-sourced income or income attributed to their Montenegrin permanent establishment (PE). The tax year is the calendar year. The tax return for the current year should be submitted to the tax authorities within three months after the year end. Taxable income is established on the basis of accounting profit disclosed in the annual profit and loss statement, further adjusted in the tax return. The tax rate is flat and amounts to 9%.

Montenegro

PKF Worldwide Tax Guide 2016/17 5

CAPITAL GAINS TAX Capital gains are included in the tax base and subject to tax rate of 9%. Capital losses could be carried forward on the account of future capital gains for 5 years. BRANCH PROFITS TAX Non-residents carrying out business in Montenegro through a permanent establishment are taxed on their Montenegro-source income at a rate of 9%. A branch is considered to be a permanent establishment. SALES TAX / VALUE ADDED TAX The main principles of the Montenegrin VAT are in line with the European Union (EU) Sixth Directive guidelines. Taxable supplies are subject to a general 19% VAT rate; however, certain supplies are taxed at a reduced 7% rate (e.g. bread, milk, books, medicines, and computers) and 0% rate (e.g. export of goods, supply of gasoline for vessels in international traffic). Prior to 1st July 2013, the standard VAT rate was 17%. In principle, the VAT base is comprised of consideration (in cash, goods, or services) received for supplies, including taxes (e.g. customs, excise duty), except VAT, and direct costs (e.g. commissions, cost of packing, transport). If the consideration is not paid in cash, or if an exchange of goods for services takes place, the tax base will be the market value of the goods or services received at the time of supply. Registration for VAT in Montenegro may be either voluntary or mandatory. Voluntary VAT registration is possible for small taxpayers who have not realised turnover exceeding EUR 18,000 in the last 12-month period. Once registered, a company may not apply for deregistration for at least three years. VAT registration is mandatory for an entity that realises turnover exceeding the EUR 18,000 threshold in any 12-month period. VAT is calculated and paid on a calendar-month basis (i.e. a VAT return must be submitted and VAT liability cleared monthly). VAT calculated on imports is paid along with customs duties. FRINGE BENEFITS TAX Employment income includes all receipts paid or provided to an individual based on employment (salaries, pensions, benefits in kind, insurance premiums, benefits, and awards above the non-taxable thresholds). Income generated through other types of personal engagements similar to employment (e.g. temporary jobs) is also considered employment income. While employees are the taxpayers, the employer is responsible for calculating and withholding personal income tax (PIT) on behalf of its employees. Income is subject to withholding tax at a flat rate of 9%. Gross salary exceeding EUR 720 is subject to the rate of 13%. The 13% rate applies to the part of the salary exceeding EUR 720, while the 9% rate applies to the part of the salary below (and including) EUR 720. Social security contributions for pension and disability insurance, health insurance, and unemployment insurance are calculated and withheld by an employer from the salary paid to an employee. Unlike the other two types of social security contributions, pension and disability insurance contributions are subject to a specific annual cap (EUR 50,000 for 2016). Social security contributions are payable by the employer and employee at different rates. The amount borne by the employer is treated as an operating cost while the portion payable by the employee is taken from the gross salary. The rates applied by the employer are as follows: • Pension and disability insurance 5.5%; • Health insurance 4.3%; and, • Unemployment insurance 0.5%. The rates applied by the employee are as follows:

Montenegro

PKF Worldwide Tax Guide 2016/17 6

• Pension and disability insurance 15%; • Health insurance 8.5%; and, • Unemployment insurance 0.5%. LOCAL TAXES No local (i.e. municipality) corporate income taxes exist in Montenegro. OTHER TAXES CUSTOMS DUTIES There are no export duties in Montenegro, nor is it forbidden to export any goods. Exceptionally, the Montenegrin government can impose quantity limitation of exports only in case of critical shortage of certain goods or for the purpose of protection of non-renewable natural resources, under certain conditions. Customs duties are paid on goods imported into the customs territory of Montenegro in accordance with the rates and tariffs set forth in the Customs Tariffs, which is in line with the harmonized system of tariff codes prescribed by the World Trade Organization (WTO). Customs duties can be levied in two manners, as ad valorem or specific duty per unit of goods. For agricultural - alimentary products, a combined duty has been determined, that is, both ad valorem and specific duty are charged simultaneously. Ad valorem duties are prescribed within the scope from 0% to 30%. Specific duties range from EUR 0.04 per 1 kg to EUR 1 per 1kg. Customs rates stipulated by international agreements are only applied to goods of preferential origin from countries covered by such agreements. The most important free trade agreements that Montenegro signed are with the European Union, the European Free Trade Association (EFTA), the Central European Free Trade Agreement (CEFTA) states, Russia, Turkey, and Ukraine. EXCISE DUTY Legal entities that are importers or producers of the following products are subject to the excise duty: • Alcohol and alcohol beverages; • Tobacco products; • Mineral oils, their derivatives, and substitutes; • Coffee and coffee products; • Mineralized water with sugar or aroma. Excise duty can be prescribed as a fixed amount and/or as a certain percentage (ad valorem). PROPERTY TAX Property tax is payable by legal entities who own or have user rights over real estate located in Montenegro. The annual tax is levied at proportional rates, ranging from 0.25% to 1% on the market value of assets as of 1st January of the current year. In case of acquisition of new property, the taxpayer is obligated to submit a tax return to the tax authorities within 30 days from the acquisition date (i.e. registration return for property tax) and to declare annual property tax by the submission of annual returns. Tax is payable in two instalments, based on decisions issued by the tax authorities. REAL ESTATE TRANSFER TAX Transfer tax of 3% is payable on the acquisition of ownership rights over immovable property. The taxable base is the market value of the immovable property at the time of the acquisition. A taxpayer (i.e. the acquirer of immovable property) is obligated to self-assess a tax liability, submit a tax return, and settle a tax liability within 15 days from the contract date.

Montenegro

PKF Worldwide Tax Guide 2016/17 7

B. DETERMINATION OF TAXABLE INCOME DEPRECIATION Depreciable assets are tangible and intangible assets with a useful life of at least one year and an individual acquisition value of at least EUR 300. Intangible and fixed assets are divided into five depreciation groups, with depreciation rates prescribed for each group (I - 5%, II - 15%, III - 20%, IV - 25%, and V - 30%). A straight-line depreciation method is prescribed for assets classified in the first group (real estate), while a declining-balance method is applicable for assets classified in the other groups. STOCK / INVENTORY Inventory is valued by applying the average weighted cost method or the first in first out (FIFO) method. If another method is used for book purposes, an adjustment for tax purposes should be made. CAPITAL GAINS AND LOSSES Capital gains realised by the sale or transfer of real estate or other property rights, as well as shares and other securities, are subject to the rate of 9%. Capital gains may be offset against capital losses occurring in the same period. A capital loss may be carried forward for five years. DIVIDENDS Dividend income of the recipient is exempt from CIT in Montenegro if the distributor is a Montenegrin corporate taxpayer. INTEREST DEDUCTIONS Interest expenses are generally deductible if they are business related and properly documented. Also, interest and related cost of loans paid out to a creditor with the status of a related party are recognised as expenses only in the amount that does not exceed market interest rates between unrelated parties. The exceeding amount is not recognized as an expense, but it is included in the taxable profit and subject to CIT rate of 9%. Interest paid out to non-resident legal entities (unless it is revenue of a PE of a non-resident legal entity) is subject to WHT levied at 9%. LOSSES Carry forward of losses is available for 5 years. Carry back of losses is not allowed. FOREIGN SOURCED INCOME A Montenegrin resident receiving foreign income is granted a tax credit in the amount of the tax paid abroad but limited to the amount that would be calculated using Montenegrin rates. There are no provisions that provide for the possibility that taxation of income earned abroad may be deferred. INCENTIVES The CIT Law provides only two tax incentives related to businesses: one for newly established businesses in non-developed municipalities and one for non-governmental organisations. An eight year tax holiday is granted to companies engaged in production activities in an underdeveloped area.

Montenegro

PKF Worldwide Tax Guide 2016/17 8

Tax exemption for newly established business in underdeveloped municipalities Newly established production companies located in underdeveloped municipalities are entitled to an eight year tax exemption. The maximum amount of tax exemption for the period of eight years is limited to EUR 200,000. The incentive is applicable to companies whose business units are established in underdeveloped regions. In that case, tax holiday is proportional to the amount of profit generated by such unit over the total profit for the period of eight years from establishment of the unit. The tax incentive is not applicable to a taxpayer operating in the sectors of (i) primary production of agricultural products, (ii) transport, (iii) shipbuilding, (iv) fishery, (v) steel production, (vi) trade, and (vii) catering, except primary catering facilities. Tax exemption for non-governmental organisations Non-governmental organisations (NGOs) registered for business activity are permitted to decrease the corporate tax base by EUR 4,000, with the condition that profit is used for realisation of the main goals of an NGO. C. FOREIGN TAX RELIEF Resident taxpayers are entitled to a tax credit up to the amount of corporate tax paid in another country on income realised in that country. This tax credit is equal to the tax paid in another country but may not exceed the amount of the tax that would have been paid in Montenegro. D. CORPORATE GROUPS Tax consolidation is permitted for a group of companies in which all of the members are Montenegrin residents and the parent company directly or indirectly controls at least 75% of the shares in the other companies. Each company files its own tax return, and the parent company files a consolidated tax return for the entire group. Each company is taxed based on its contribution to the consolidated taxable profit (or loss) of the group. Tax consolidation is binding for at least five years. E. RELATED PARTY TRANSACTIONS The difference between the transfer price and arm’s-length price is included in the taxable profit and is taxed accordingly. Parties considered to be related are the parties between whom special relations exist, which could directly impact the conditions or economical results of the transaction between them. Methods permitted in determining arm’s-length price are the comparable uncontrolled price (CUP) method (as the primary method), resale minus method, or cost plus method. There are no other rules or guidelines introduced apart from the above rules in respect to transfer pricing. F. EXCHANGE CONTROL There are no exchange controls in Montenegro. G. PERSONAL INCOME TAX Residents of Montenegro are subject to personal income tax on their worldwide income. Non-residents are subject to income tax on their income from Montenegro-source under the same rules as residents. Personal income tax is levied at the rate of 15% on gross personal income above EUR 720 per month, while personal income tax for income below EUR 720 per month is subject to a personal income tax rate of 9%. Tax rate on revenues from interest paid to non-residents is 5%. H. TREATY AND NON-TREATY WITHHOLDING TAX RATES Montenegrin CIT Law imposes WHT on income realised from a Montenegro - source and distributed to a non-resident. The scope of the WHT applies to dividends and profit distribution, capital gains, interest, royalties, intellectual property rights fees, and rental income, as well as fees for consulting, market research, and audit services. Distributions of dividends and share of profits are also subject to WHT if

Montenegro

PKF Worldwide Tax Guide 2016/17 9

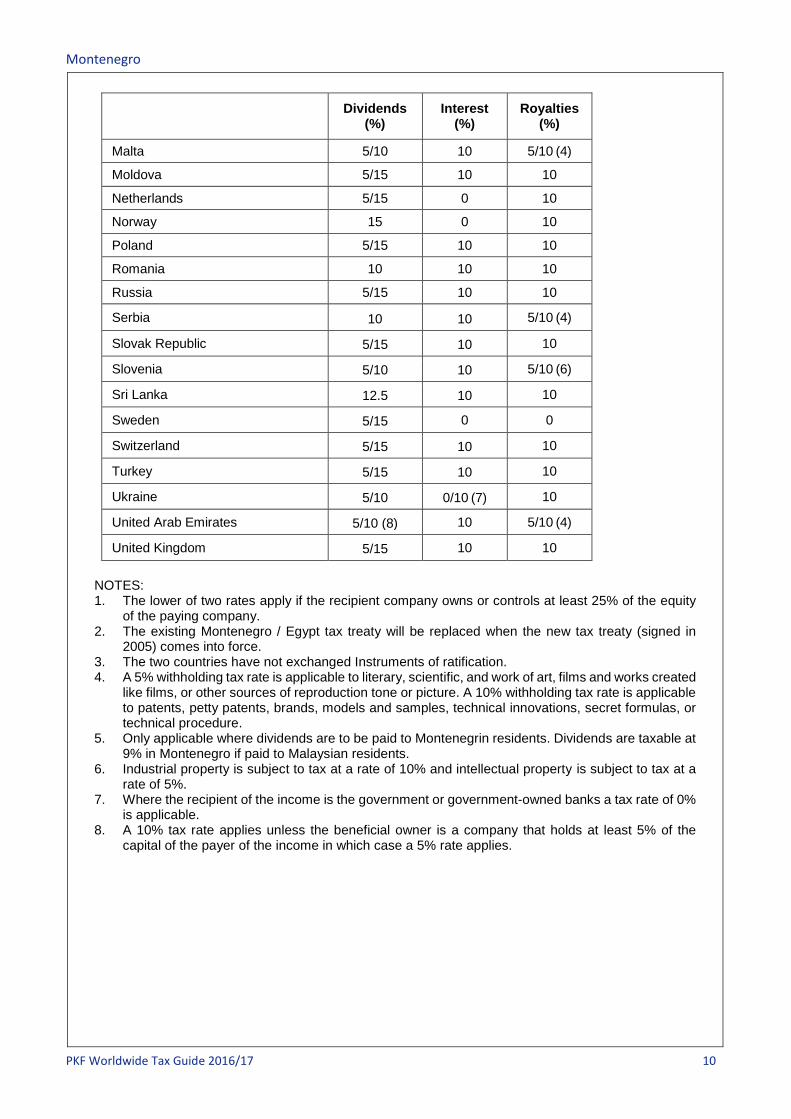

the recipient is a Montenegrin resident (either an individual or legal entity). The general WHT rate is 9%. Application of a double tax treaty (DTT) may reduce or eliminate Montenegrin WHT. To qualify for the beneficial rates prescribed by the treaty, a non-resident must prove tax residency of a relevant treaty country and beneficial ownership over the income. In order to qualify for a preferential tax rate according to a DTT, a non-resident will need to provide the tax residency certificate filled out and stamped by the relevant authority of its country of residence. Although Serbia is regarded as the legal successor of the Serbia and Montenegro State Union that ceased to exist in June 2006, the Republic of Montenegro, upon its Decision on Independence (dated 3rd June 2006), continues to honour international treaties that were applicable in the State Union, including those executed by State Union’s legal predecessors (Federal People’s Republic of Yugoslavia and Socialist Federal Republic of Yugoslavia, i.e. former Yugoslavia). However, a quite low statutory WHT rate of 9%, which was enacted after the most of the treaties had been introduced, is usually more beneficial than treaty rates. The list of the treaties is provided below:

Dividends (%)

Interest (%)

Royalties (%)

Non-treaty countries 9 9 9

Treaty countries:

Albania 5/15 10 10

Azerbaijan 10 10 (7) 10

Belgium 10/15 15 10

Belorussia 5/15 8 10

Bosnia and Herzegovina 5/10 10 10

Bulgaria 5/15 10 10

China 5 10 10

Croatia 5/10 10 10

Cyprus 10 10 10

Czech Republic 10 10 5/10

Denmark 5/15 0 10

Egypt (2) 5/15 15 15

Finland 5/15 0 10

France 5/15 0 0

Germany 15 0 10

Hungary 5/15 10 10

India (3) 5/15 10 10

Ireland 5/10 10 5/10 (4)

Italy 10 10 10

Korea 10 10 10

Kuwait 5/10 10 10

Latvia 5/10 10 5/10 (4)

Macedonia 5/15 10 10

Malaysia 0 (5) 10 10

Montenegro

PKF Worldwide Tax Guide 2016/17 10

Dividends (%)

Interest (%)

Royalties (%)

Malta 5/10 10 5/10 (4)

Moldova 5/15 10 10

Netherlands 5/15 0 10

Norway 15 0 10

Poland 5/15 10 10

Romania 10 10 10

Russia 5/15 10 10

Serbia

10

10 5/10 (4)

Slovak Republic

5/15

10 10

Slovenia

5/10

10 5/10 (6)

Sri Lanka

12.5

10 10

Sweden

5/15 0 0

Switzerland

5/15

10 10

Turkey

5/15

10 10

Ukraine

5/10

0/10 (7) 10

United Arab Emirates

5/10 (8) 10 5/10 (4)

United Kingdom

5/15 10 10 NOTES: 1. The lower of two rates apply if the recipient company owns or controls at least 25% of the equity

of the paying company. 2. The existing Montenegro / Egypt tax treaty will be replaced when the new tax treaty (signed in

2005) comes into force. 3. The two countries have not exchanged Instruments of ratification. 4. A 5% withholding tax rate is applicable to literary, scientific, and work of art, films and works created

like films, or other sources of reproduction tone or picture. A 10% withholding tax rate is applicable to patents, petty patents, brands, models and samples, technical innovations, secret formulas, or technical procedure.

5. Only applicable where dividends are to be paid to Montenegrin residents. Dividends are taxable at 9% in Montenegro if paid to Malaysian residents.

6. Industrial property is subject to tax at a rate of 10% and intellectual property is subject to tax at a rate of 5%.

7. Where the recipient of the income is the government or government-owned banks a tax rate of 0% is applicable.

8. A 10% tax rate applies unless the beneficial owner is a company that holds at least 5% of the capital of the payer of the income in which case a 5% rate applies.