Embed Size (px)

Citation preview

MONOPOLY• Pure monopoly: a single seller of a good or service

with no close substitutes. The firm IS the industry.Monopoly power: the ability of a firm to control the

market price of it’s good by making more or less of it available to buyers.

Conditions for monopoly to exist 1. A single seller of a good.

The firm is the industry. 2. No close substitutes for this good or service. 3. Very high barriers to entry into this

industry... ...constraint that prevents additional sellers

from entering the industry and competing with the monopolist.

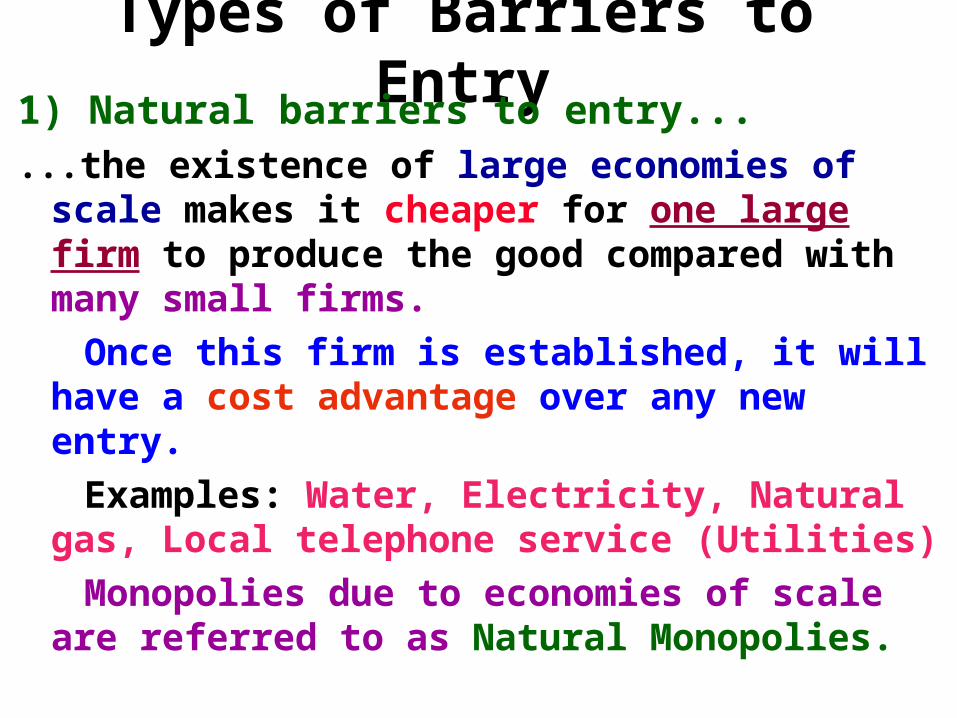

Types of Barriers to Entry1) Natural barriers to entry... ...the existence of large economies of scale makes it

cheaper for one large firm to produce the good compared with many small firms.

Once this firm is established, it will have a cost advantage over any new entry.

Examples: Water, Electricity, Natural gas, Local telephone service (Utilities)

Monopolies due to economies of scale are referred to as Natural Monopolies.

Types of Barriers to Entry 2) Legal barriers to entry a) government franchises and licenseExamples: Postal service, Utilities, Cable TV, Taxi’s,

Medicine, Law Government usually takes Natural Monopolies and

legally prevents any other firm from producing that good. Why?

Since it is more efficient(lowest cost) for one firm to produce this good, the government wants to make sure customers enjoy this efficiency...

...by the government regulating prices that are charged! b) Patents and copyrights......granted to inventors and performers to encourage

research and development. Good for a 20 year period.

Types of Barriers to Entry 3)The ownership of an entire supply of a resource Examples:

Having control over all diamond mines in the world

The special ability or knowledge a person may have. The “best” of the best...

...Performers, actors, songwriters, etc

Monopoly and PriceA Monopoly has control over price (Monopoly power)• Unlike perfect competition, a monopolist can raise

price and still be able to sell some of it’s good. Why? The consumer has no where else to buy the good: Single Firm is the INDUSTRY with barriers to entry• Will a monopolist simply raise prices to outrageous

levels to gouge the consumer? Not if they want to maximize profit!• The monopolist faces the MARKET (Industry)

Demand curve (which is downward sloping)… …if prices are too high consumers can

stop buying the good

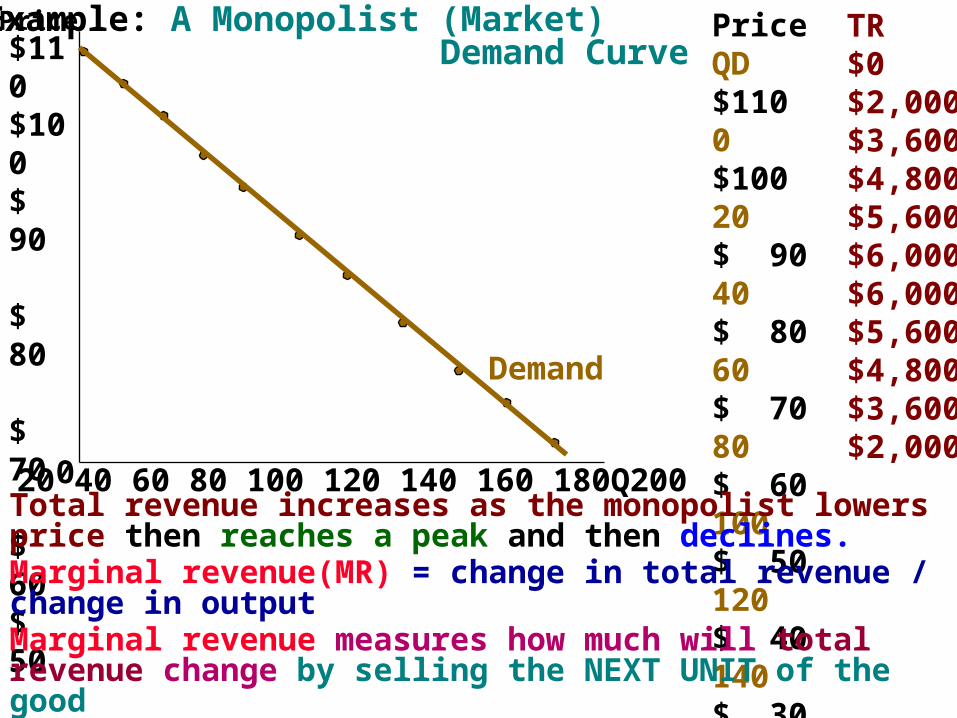

Price QD$110 0$100 20$ 90 40$ 80 60$ 70 80$ 60 100$ 50 120$ 40 140$ 30 160$ 20 180$ 10 200

Price$110 $100 $ 90 $ 80 $ 70 $ 60 $ 50 $ 40 $ 30 $ 20 $ 10

0 20 40 60 80 100 120 140 160 180 200 Q• Assuming a monopolist charges only one price for it’s good it is

clear that if the firm lowers the price of the good it will sell more.What will happen to total revenue as the monopolist sells more?Will Marginal Revenue be equal to Price as in perfect competition?

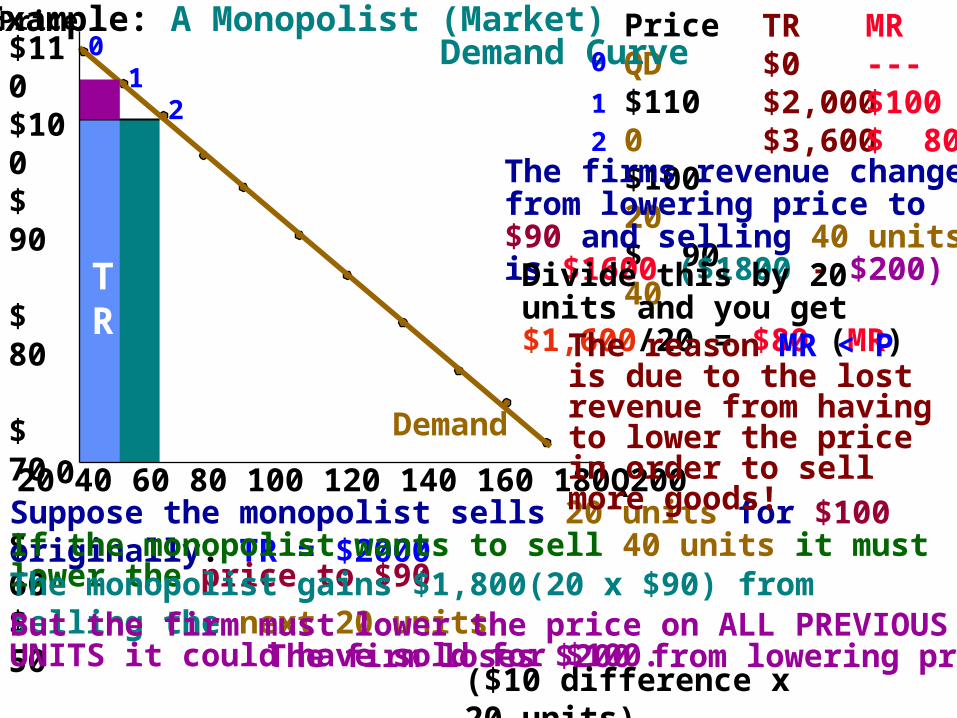

Example: A Monopolist (Market) Demand Curve

Demand

Price QD$110 0$100 20$ 90 40$ 80 60$ 70 80$ 60 100$ 50 120$ 40 140$ 30 160$ 20 180$ 10 200

Price$110 $100 $ 90 $ 80 $ 70 $ 60 $ 50 $ 40 $ 30 $ 20 $ 10

0 20 40 60 80 100 120 140 160 180 200 Q

Example: A Monopolist (Market) Demand Curve

Demand

TR$0$2,000$3,600$4,800$5,600$6,000$6,000$5,600$4,800$3,600$2,000

Total revenue increases as the monopolist lowers price then reaches a peak and then declines.Marginal revenue(MR) = change in total revenue / change in outputMarginal revenue measures how much will total revenue change by selling the NEXT UNIT of the goodWhat will MR be for each level of OUTPUT?

Price QD$110 0$100 20$ 90 40$ 80 60$ 70 80$ 60 100$ 50 120$ 40 140$ 30 160$ 20 180$ 10 200

Price$110 $100 $ 90 $ 80 $ 70 $ 60 $ 50 $ 40 $ 30 $ 20 $ 10

0 20 40 60 80 100 120 140 160 180 200 Q

Example: A Monopolist (Market) Demand Curve

Demand

TR$0$2,000$3,600$4,800$5,600$6,000$6,000$5,600$4,800$3,600$2,000

MR---$100$ 80$ 60$ 40$ 20$ 0$ -20$ -40$ -60$ -80

0

1

2

3

4

5

6

01

23

4

5

6

Marginal revenue(MR) = change in total revenue / change in outputFrom point 1 to point 2 = $1,600 / 20 = $80From point 2 to point 3 = $1,200 / 20 = $60From point 3 to point 4 = $ 800 / 20 = $40

Marginal revenue IS LESS THAN PRICE, and IT DECLINES more rapidly than price. Why?

MarginalRevenue

Price QD$110 0$100 20$ 90 40

Price$110 $100 $ 90 $ 80 $ 70 $ 60 $ 50 $ 40 $ 30 $ 20 $ 10

0 20 40 60 80 100 120 140 160 180 200 Q

Example: A Monopolist (Market) Demand Curve

Demand

TR$0$2,000$3,600

MR---$100$ 80

0

1

2

01

2

Suppose the monopolist sells 20 units for $100 originally. TR = $2000

TR

If the monopolist wants to sell 40 units it must lower the price to $90The monopolist gains $1,800(20 x $90) from selling the next 20 unitsBut the firm must lower the price on ALL PREVIOUS UNITS it could have sold for $100.

The firms revenue change from lowering price to $90 and selling 40 units is $1600 ($1800 - $200)

Divide this by 20 units and you get $1,600/20 = $80 (MR)

The reason MR < P is due to the lost revenue from having to lower the price in order to sell more goods!

The firm loses $200 from lowering price($10 difference x 20 units)

Price ($)

Quantity

DemandMR

Total Revenue

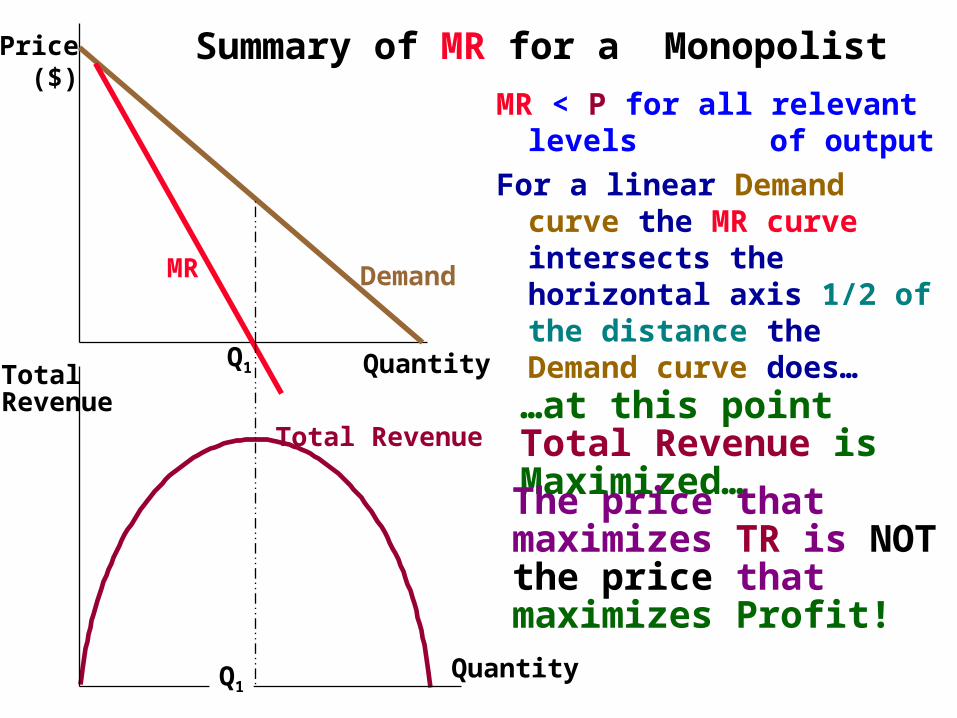

MR < P for all relevant levels of output

For a linear Demand curve the MR curve intersects the horizontal axis 1/2 of the distance the Demand curve does…Q1Total

Revenue

QuantityQ1

Summary of MR for a Monopolist

…at this point Total Revenue is Maximized…

The price that maximizes TR is NOT the price that maximizes Profit!

Price QD$110 0$100 20$ 90 40$ 80 60$ 70 80$ 60 100$ 50 120$ 40 140$ 30 160$ 20 180$ 10 200

Price$110 $100 $ 90 $ 80 $ 70 $ 60 $ 50 $ 40 $ 30 $ 20 $ 10

0 20 40 60 80 100 120 140 160 180 200 Q

Demand

MR---$100$ 80$ 60$ 40$ 20$ 0$ -20$ -40$ -60$ -80

0

1

2

3

4

5

6

01

23

4

5

6

MR

MC----$35$22$32$40$52$68$83$98$115$130

MC

Any firm maximizes profit at the output level where MR = MC

Does the monopolist charge only $40 for it’s product?No, it will seek out the highest price consumers will pay for 80 units. This is represented by the Demand curve(MB).The Monopolist SEARCHES for the highest price, which is $70.

A Monopolist won’t charge more than $70 since it can’t sell 80 units

MC

P

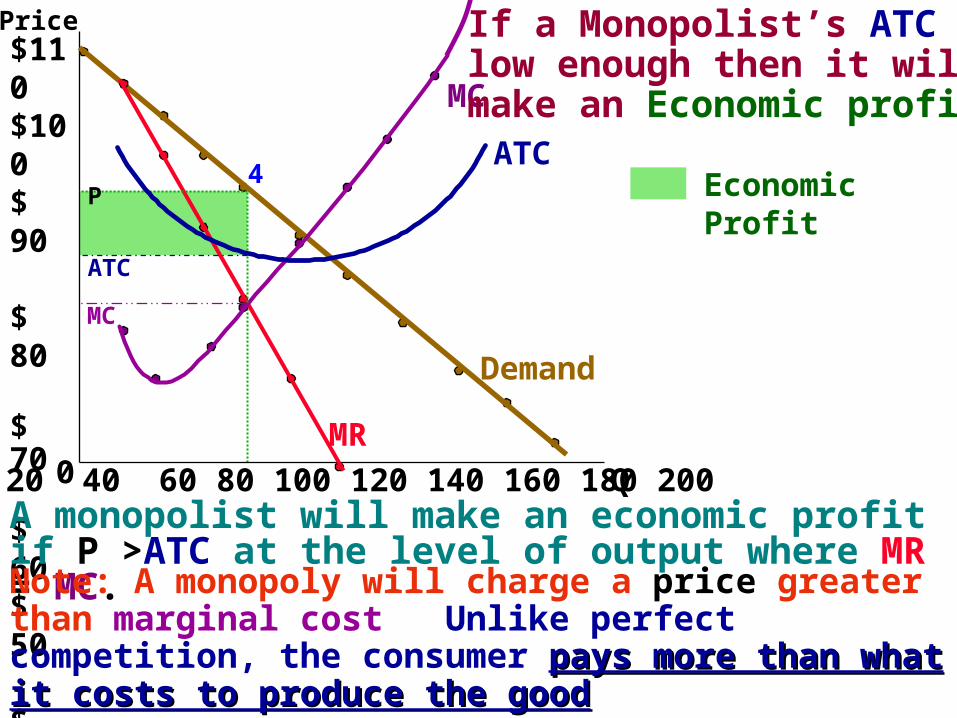

This monopolist will produce 80 units of output when MR = MC.

Price$110 $100 $ 90 $ 80 $ 70 $ 60 $ 50 $ 40 $ 30 $ 20 $ 10

0 20 40 60 80 100 120 140 160 180 200 Q

Demand

4

MR

MC

ATC

ATC

MC

P Economic Profit

If a Monopolist’s ATC is low enough then it will make an Economic profit

A monopolist will make an economic profit if P >ATC at the level of output where MR = MC.Note: A monopoly will charge a price greater than marginal cost Unlike perfect competition, the consumer pays more than pays more than what it costs to produce the goodwhat it costs to produce the good

Price$110 $100 $ 90 $ 80 $ 70 $ 60 $ 50 $ 40 $ 30 $ 20 $ 10

0 20 40 60 80 100 120 140 160 180 200 Q

Demand

MR

MC

ATC

= ATC P

If a Monopolist’s costs (including the ATC) are higher then it may only make a Normal profit

MC

…it depends on the cost of the product and the market demand for the product.If a monopolist has very high costs for a product consumers are not willing to pay a very high price for the monopolist could make a loss...

A monopoly is not guaranteed of making an economic profit…

Price$110 $100 $ 90 $ 80 $ 70 $ 60 $ 50 $ 40 $ 30 $ 20 $ 10

0 20 40 60 80 100 120 140 160 180 200 Q

Demand

MR

MC

ATC ATC

P

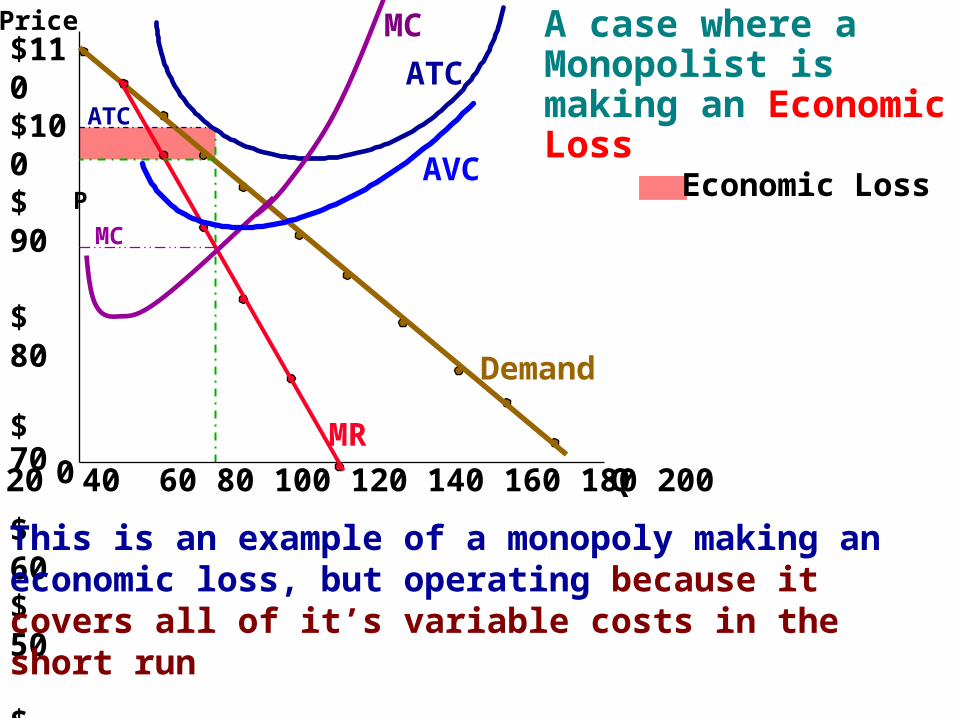

A case where a Monopolist is making an Economic Loss

MC

AVC Economic Loss

This is an example of a monopoly making an economic loss, but operating because it covers all of it’s variable costs in the short run

Is there a Supply curve for a Monopolist? NO. Why?• The supply curve derived in perfect competition

(the firms MC curve) was done based on the fact that a competitive firm is a Price TakerPrice Taker and REACTS to price.

A Monopolist is a Price Searcher

It DOES NOT REACT to price changes

If demand increases there is no guarantee that a monopoly will decide to produce more.

It depends on the shifting of the MR curve.

There is NO unique relationship between price and quantity made available from a monopolist.

Long run equilibrium.• Will be the same as short-run equilibrium…

...Profits are signals for new firms to enter the industry...

...to take away economic profit...

...but barriers to entry prevent this from happening and a monopolist that makes a profit in the short run can expect to make one in the long run.

A monopolist that makes an economic loss will exit the industry...

....and the industry will cease to exist.

Comparing Perfect competition & Monopoly

Suppose that we are able to transform a constant costs competitive industry into a Pure Monopoly.

• How would that effect the quantity of the good produced by the industry?

• How would that effect the price of the good?

• How would that effect the well being of consumers of that good?

Price

Q(Tomatoes)q (Tomatoes)

Price

D

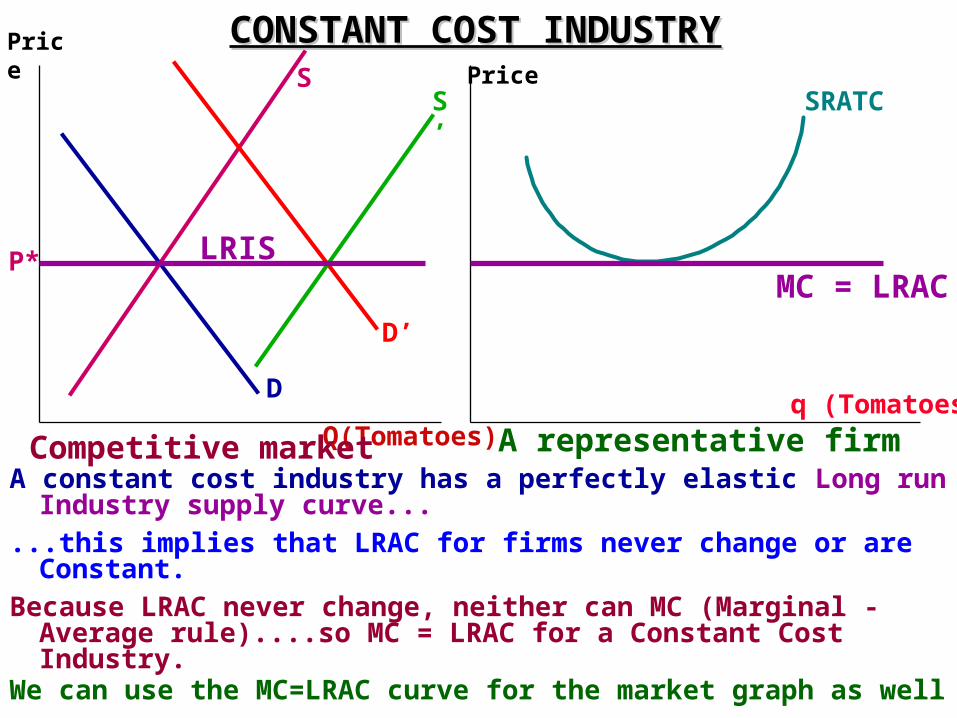

Competitive market A representative firmA constant cost industry has a perfectly elastic Long run Industry

supply curve...

...this implies that LRAC for firms never change or are Constant.

Because LRAC never change, neither can MC (Marginal - Average rule)....so MC = LRAC for a Constant Cost Industry.

We can use the MC=LRAC curve for the market graph as well

SRATCS

P*

D’

S’

LRISMC = LRAC

CONSTANT COST INDUSTRYCONSTANT COST INDUSTRY

Price

Quantity(Tomatoes)

MC =LRAC = LRIS

QPC

PPC

A monopoly maximizes profit at the output level where MR = MC, so the MR curve is added to the graph.

MR

QM

Consumer Surplus

A

BC

PM

A monopolist then searches out the highest price to charge off the Demand curve

Competitive situationMake Industry into a Monopoly

Competitive Equilibrium occurs where LRIS = Demand. P=MC=Min LRAC Consumers are as well off as possible (Maximizing consumer surplus) Triangle ABC

Comparing Monopoly & Perfect Competition A Monopolist will produce LESS

than a Competitive Industry A Monopolist will charge a HIGHER

Price than a Competitive firm

Market for Tomatoes Monopoly Profit

Since PM > LRAC the Monopoly will make an Economic profit

Demand

Price

Quantity(Tomatoes)

MC =LRAC = LRIS

Demand

QPC

PPC

MR

QM

Consumer Surplus

A

BC

PM

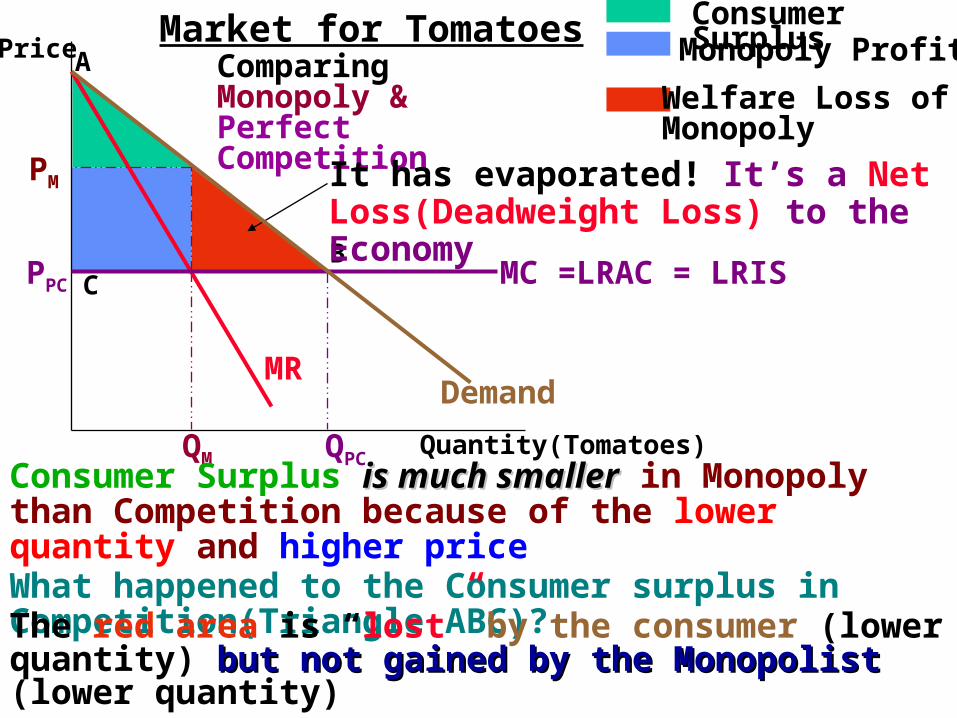

Comparing Monopoly & Perfect Competition

Market for Tomatoes Monopoly Profit

Consumer Surplus is much smalleris much smaller in Monopoly than Competition because of the lower quantity and higher priceWhat happened to the Consumer surplus in Competition(Triangle ABC)?

Welfare Loss of Monopoly

The red area is “lost” by the consumer (lower quantity) but not but not gained by the Monopolist gained by the Monopolist (lower quantity)

It has evaporated! It’s a Net Loss(Deadweight Loss) to the Economy

Price

Quantity(Tomatoes)

MC =LRAC = LRIS

Demand

QPC

PPC

MR

QM

Consumer Surplus

A

BC

PM

Comparing Monopoly & Perfect Competition

Market for Tomatoes Monopoly Profit

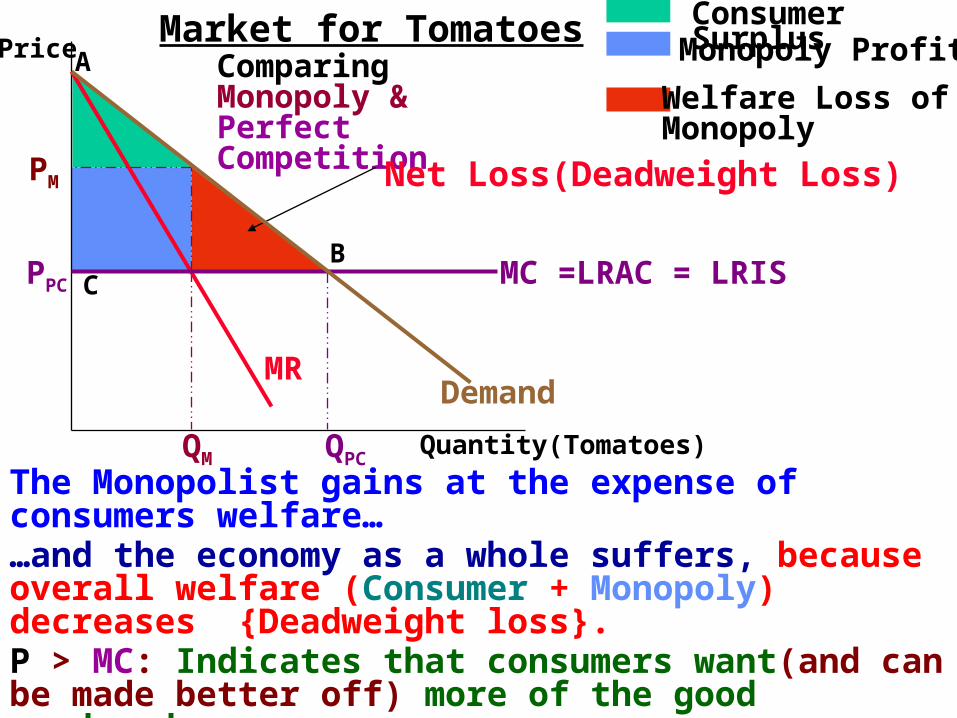

Welfare Loss of Monopoly

Net Loss(Deadweight Loss)

The Monopolist gains at the expense of consumers welfare……and the economy as a whole suffers, because overall welfare (Consumer + Monopoly) decreases {Deadweight loss}.P > MC: Indicates that consumers want(and can be made better off) more of the good produced.

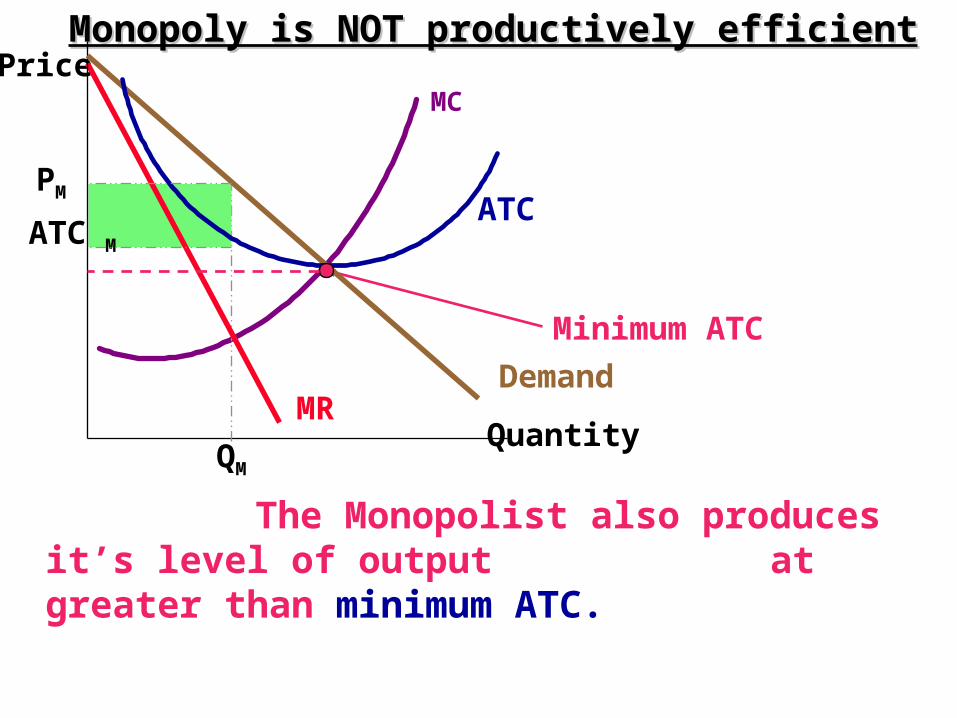

Monopoly is not allocatively efficient

Price

Quantity

Demand MR

MC

PM

QM

Minimum ATC

ATC M

The Monopolist also produces it’s level of output at greater than minimum ATC.

Monopoly is NOT productively efficientMonopoly is NOT productively efficient

ATC

Price

Quantity(Tomatoes)

MC =LRAC = LRIS

DemandQPC

PPC

MRQM

Consumer SurplusA

BC

PM

Monopoly Profit

Welfare Loss of Monopoly

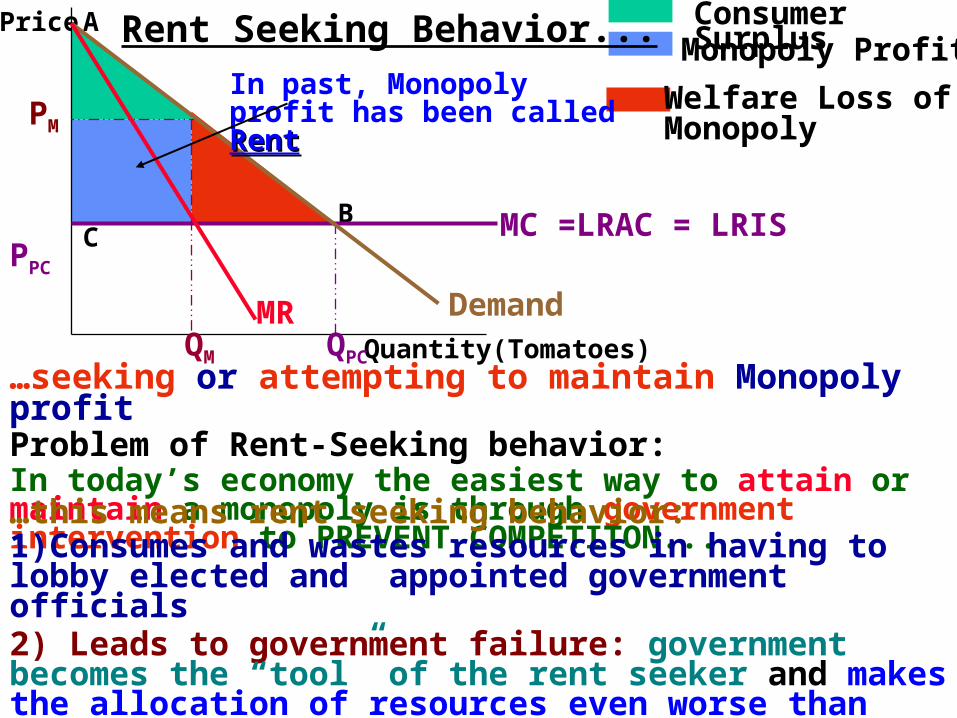

Rent Seeking Behavior...

In past, Monopolyprofit has been calledRentRent

…seeking or attempting to maintain Monopoly profitProblem of Rent-Seeking behavior:In today’s economy the easiest way to attain or maintain a monopoly is through government intervention to PREVENT COMPETITON...…this means rent seeking behavior:1)Consumes and wastes resources in having to lobby elected and appointed government officials2) Leads to government failure: government becomes the “tool” of the rent seeker and makes the allocation of resources even worse than with monopoly alone.

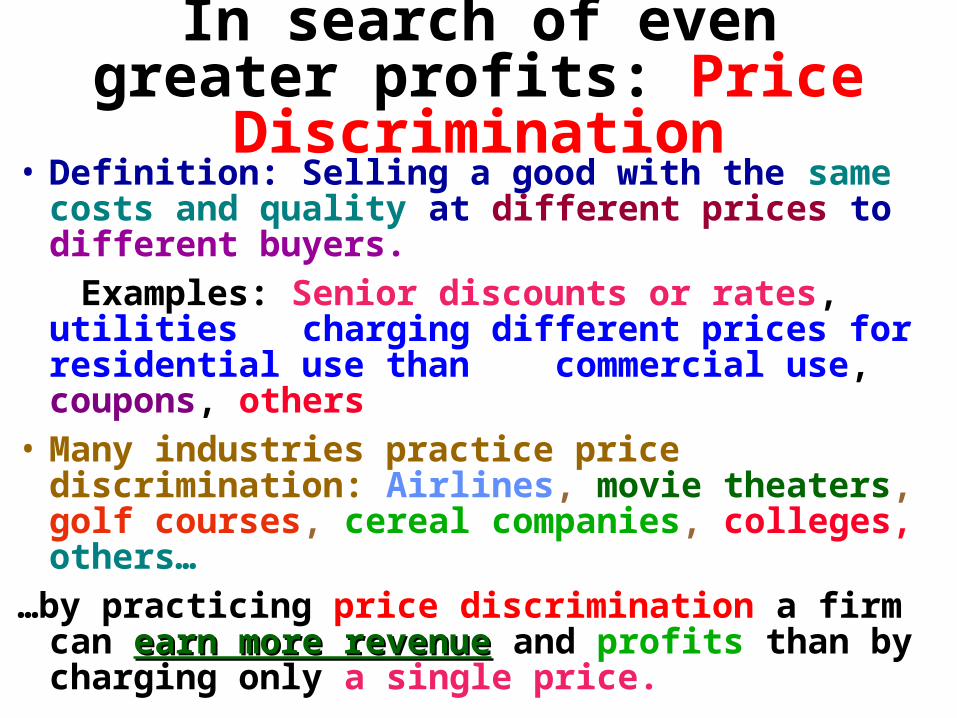

In search of even greater profits: Price Discrimination

• Definition: Selling a good with the same costs and quality at different prices to different buyers.

Examples: Senior discounts or rates, utilities charging different prices for residential use than commercial use, coupons, others

• Many industries practice price discrimination: Airlines, movie theaters, golf courses, cereal companies, colleges, others…

…by practicing price discrimination a firm can earn earn more revenuemore revenue and profits than by charging only a single price.

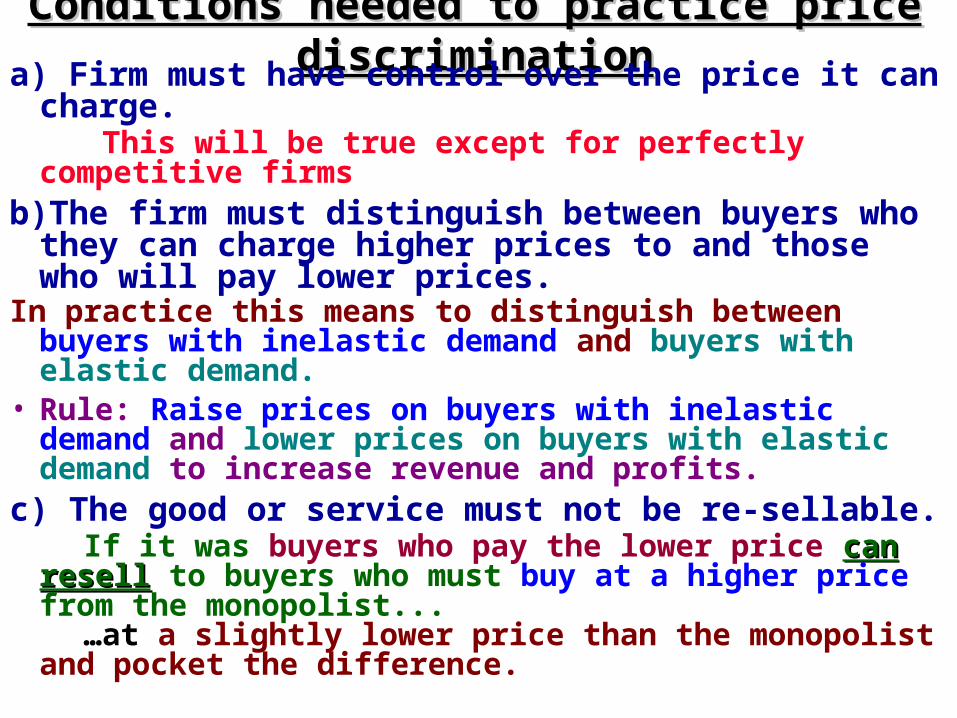

Conditions needed to practice price discriminationConditions needed to practice price discriminationa) Firm must have control over the price it can charge. This will be true except for perfectly competitive firmsb)The firm must distinguish between buyers who they

can charge higher prices to and those who will pay lower prices.

In practice this means to distinguish between buyers with inelastic demand and buyers with elastic demand.

• Rule: Raise prices on buyers with inelastic demand and lower prices on buyers with elastic demand to increase revenue and profits.

c) The good or service must not be re-sellable. If it was buyers who pay the lower price can resellcan resell to

buyers who must buy at a higher price from the monopolist...

…at a slightly lower price than the monopolist and pocket the difference.

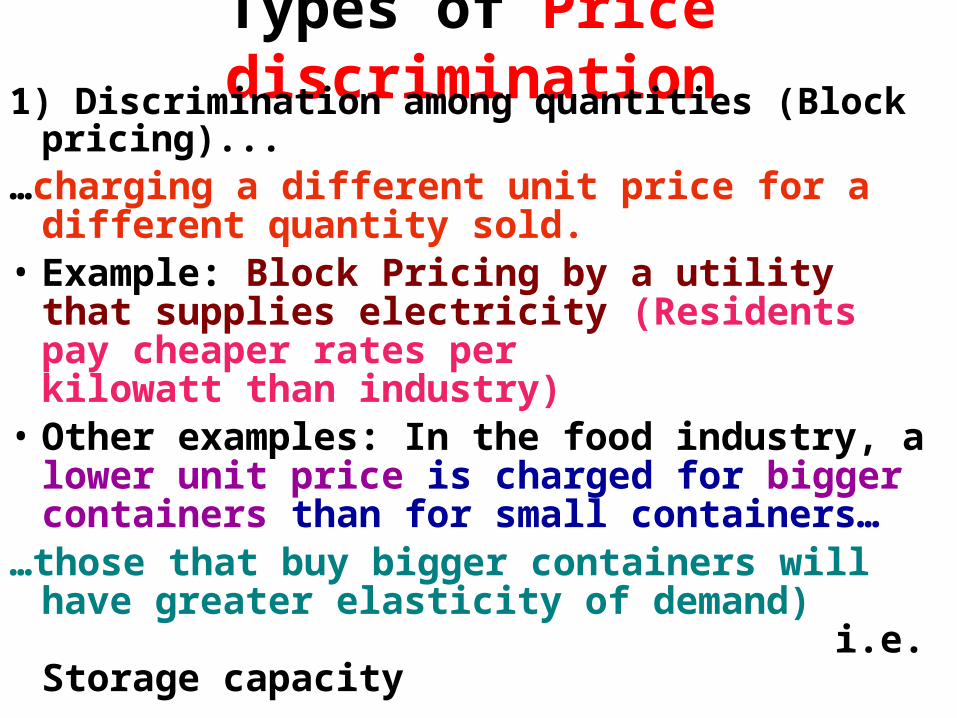

Types of Price discrimination1) Discrimination among quantities (Block pricing)...…charging a different unit price for a different

quantity sold.• Example: Block Pricing by a utility that supplies

electricity (Residents pay cheaper rates per kilowatt than industry)

• Other examples: In the food industry, a lower unit price is charged for bigger containers than for small containers…

…those that buy bigger containers will have greater elasticity of demand) i.e. Storage capacity

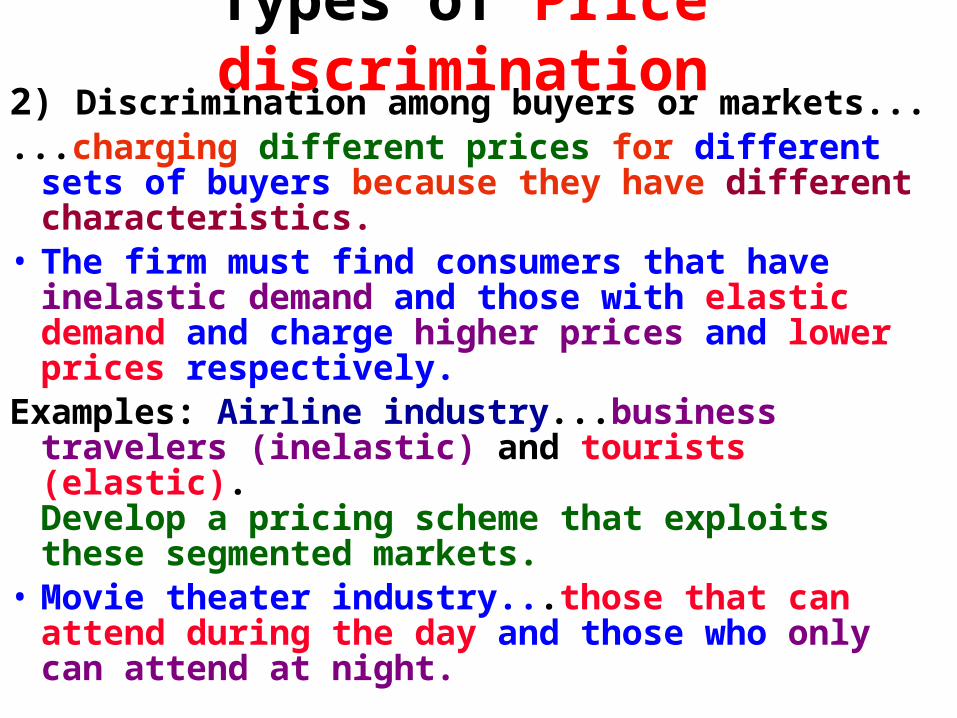

Types of Price discrimination2) Discrimination among buyers or markets......charging different prices for different sets of buyers

because they have different characteristics.• The firm must find consumers that have inelastic

demand and those with elastic demand and charge higher prices and lower prices respectively.

Examples: Airline industry...business travelers (inelastic) and tourists (elastic). Develop a pricing scheme that exploits these segmented markets.

• Movie theater industry...those that can attend during the day and those who only can attend at night.

A possible remedy: Anti-Trust laws• If a monopoly exists the government can break up break up

the firmthe firm (among other penalties) using anti-trust laws to reestablish competition.

• Examples: Standard Oil in 1911, ATT in mid 1980’s NCAA in early 1980’s

• Laws also used to prevent Mergers, if they restrict competition. Ex: Pepsi - Dr. Pepper, Coke -7 UP

• At the discretion of the Justice Department

• IBM was charged for monopoly practices in late 1960’s, but by 1982 the case was dismissed.

• Microsoft was accused of monopoly practices.

Natural monopoly...

…an Industry with such large economies of scale LRAC always declines as more of the good is produced (for the relevant market)

• Implies that one large firm can produce this good at much lower cost than many small firms…

…so breaking up a Natural Monopoly does no good…

Price

Quantity of Electricity

Demand

LRACLRMC

MR

PM

QM

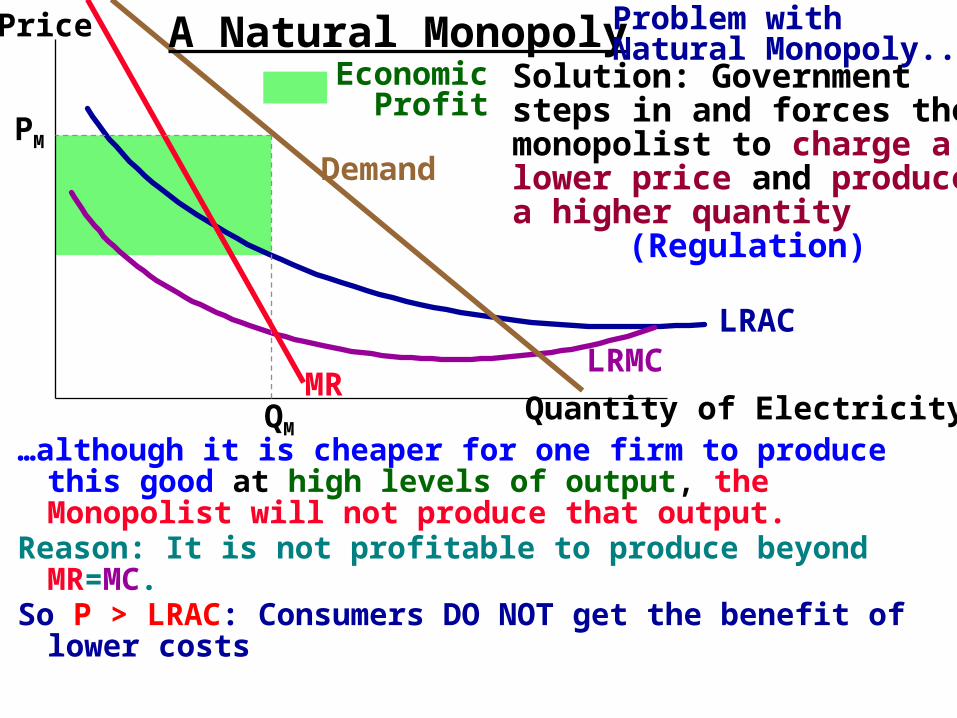

A Natural Monopoly Economic Profit

…although it is cheaper for one firm to produce this good at high levels of output, the Monopolist will not produce that output.

Reason: It is not profitable to produce beyond MR=MC.So P > LRAC: Consumers DO NOT get the benefit of

lower costs

Problem with Natural Monopoly...

Solution: Government steps in and forces the monopolist to charge a lower price and produce a higher quantity

(Regulation)

Price

Quantity of Electricity

Demand

LRACLRMC

MR

PM

QM

A Natural Monopoly Economic Profit

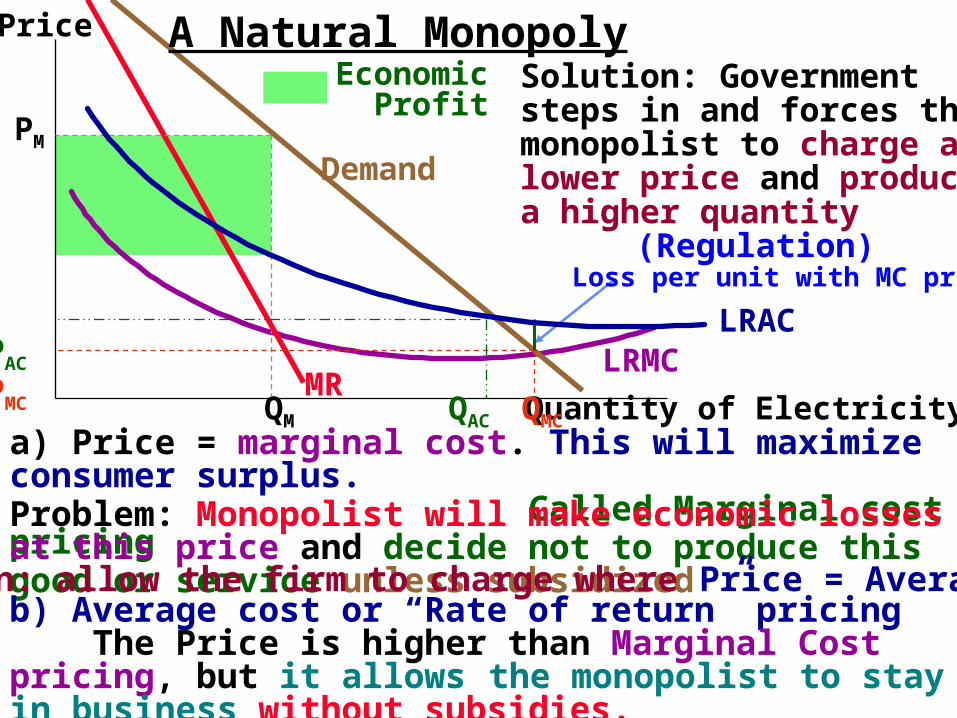

Solution: Government steps in and forces the monopolist to charge a lower price and produce a higher quantity

(Regulation)

a) Price = marginal cost. This will maximize consumer surplus. Called Marginal cost pricing

PMC

QMC

Problem: Monopolist will make economic losses at this price and decide not to produce this good or service unless subsidized

Loss per unit with MC price

Solution: allow the firm to charge where Price = Average cost.b) Average cost or “Rate of return” pricing The Price is higher than Marginal Cost pricing, but it allows

the monopolist to stay in business without subsidies.

PAC

QAC

Rate of Return: Reality problems1) A commission is set up to establish and monitor

prices for the utility. a. Usually, commission members are former

members of the particular industry they regulate. b. This may grant some additional power to the

monopolist when it comes to asking for price increases.

2)The monopolist will be granted a “fair rate of return” over it’s costs, most of which will be capital.

Example: No matter the firm’s per unit costs it will always receive a 5% return over those costs

Cost can be difficult to establish. The firm has an incentive to exaggerate the cost of

providing this product.

Rate of Return: Reality problems• Since the monopolist is guaranteed a “fair rate of

return” over their costs, they have no incentive to minimize costs...

…the firm can purchase expensive machinery, staff, offices, etc that may not be necessary to produce this product...

…the consumer will have to pick up the tab in the form of higher prices if the commission allows the price increase to go through

(which it probably will if “taken over” by the firm).

Benefits of a Monopoly? • Research and development of new technologies......without monopoly profits as an incentive firms may

not spend resources to develop new technologies and goods.

• Joseph Schumpeter : “Creative Destruction” Even if a firm has a Monopoly today, other firms will

try to develop substitutes for the good and attempt to create their own monopoly.

This “destroys” the old monopoly and “creates” a new one Ballpoint pens replaced fountain pens• If a firm is not protected from competition by the

government it is increasingly difficult to maintain monopoly profits…

…due to other firms developing substitute products.