Embed Size (px)

Citation preview

Monkey See!Monkey See!

Monkey Do….Monkey Do….

The Collapse The Collapse of aof a

Hurricane Claim WebcastHurricane Claim Webcast

Proper Preparation Precedes Proper Preparation Precedes Powerful PerformancePowerful Performance

Clowning around with Clowning around with

America's largest America's largest

monkey farm.monkey farm.

And guess who slipped on the banana peels?And guess who slipped on the banana peels?

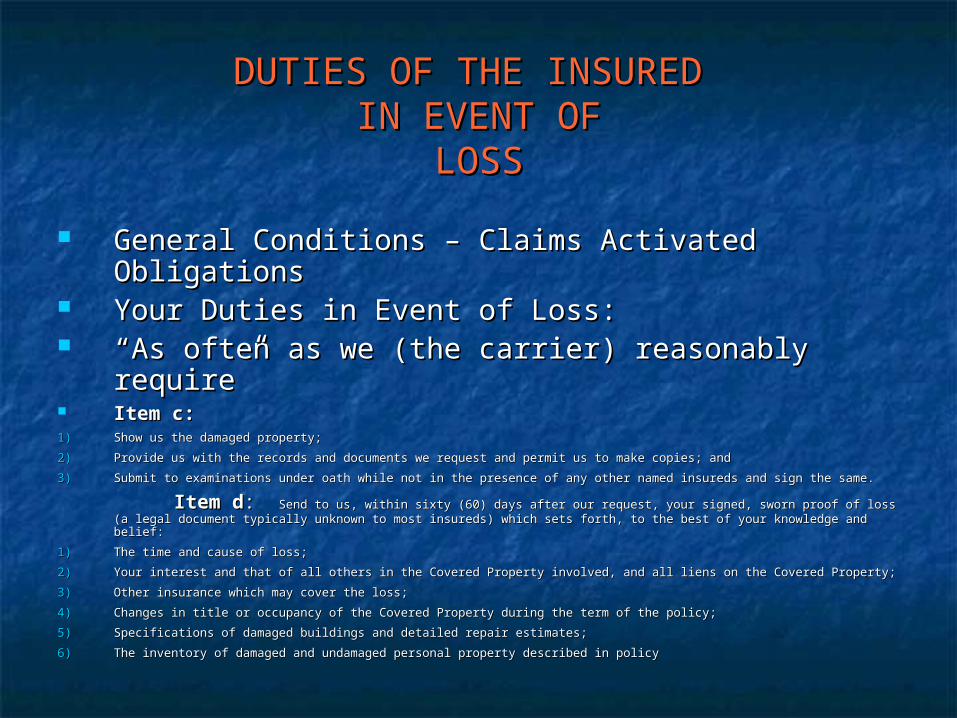

DUTIES OF THE INSURED DUTIES OF THE INSURED IN EVENT OFIN EVENT OF

LOSSLOSS

General Conditions – Claims Activated General Conditions – Claims Activated ObligationsObligations

Your Duties in Event of Loss:Your Duties in Event of Loss: ““As often as we (the carrier) reasonably require”As often as we (the carrier) reasonably require” Item c:Item c:1)1) Show us the damaged property; Show us the damaged property;

2)2) Provide us with the records and documents we request and permit us to make copies; andProvide us with the records and documents we request and permit us to make copies; and

3)3) Submit to examinations under oath while not in the presence of any other named insureds and sign the same.Submit to examinations under oath while not in the presence of any other named insureds and sign the same.

Item dItem d: : Send to us, within sixty (60) days after our request, your signed, sworn proof of loss (a legal Send to us, within sixty (60) days after our request, your signed, sworn proof of loss (a legal document typically unknown to most insureds) which sets forth, to the best of your knowledge and belief:document typically unknown to most insureds) which sets forth, to the best of your knowledge and belief:

1)1) The time and cause of loss;The time and cause of loss;

2)2) Your interest and that of all others in the Covered Property involved, and all liens on the Covered Property;Your interest and that of all others in the Covered Property involved, and all liens on the Covered Property;

3)3) Other insurance which may cover the loss;Other insurance which may cover the loss;

4)4) Changes in title or occupancy of the Covered Property during the term of the policy;Changes in title or occupancy of the Covered Property during the term of the policy;

5)5) Specifications of damaged buildings and detailed repair estimates;Specifications of damaged buildings and detailed repair estimates;

6)6) The inventory of damaged and undamaged personal property described in policyThe inventory of damaged and undamaged personal property described in policy

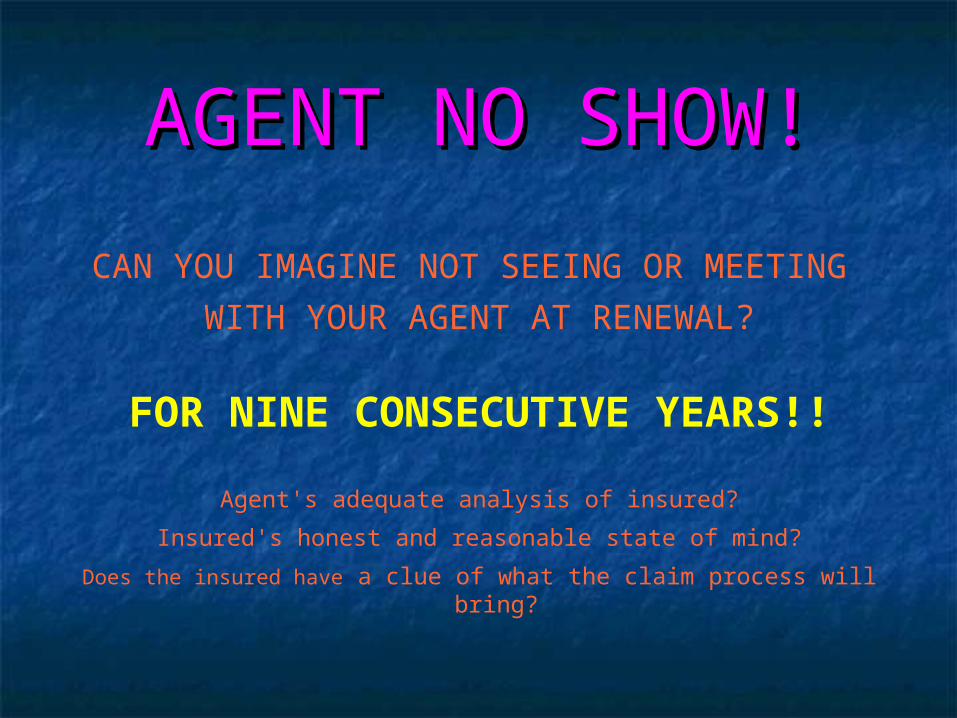

AGENT NO SHOW!AGENT NO SHOW!

CAN YOU IMAGINE NOT SEEING OR MEETING

WITH YOUR AGENT AT RENEWAL?

FOR NINE CONSECUTIVE YEARS!!

Agent's adequate analysis of insured?

Insured's honest and reasonable state of mind?

Does the insured have a clue of what the claim process will bring?

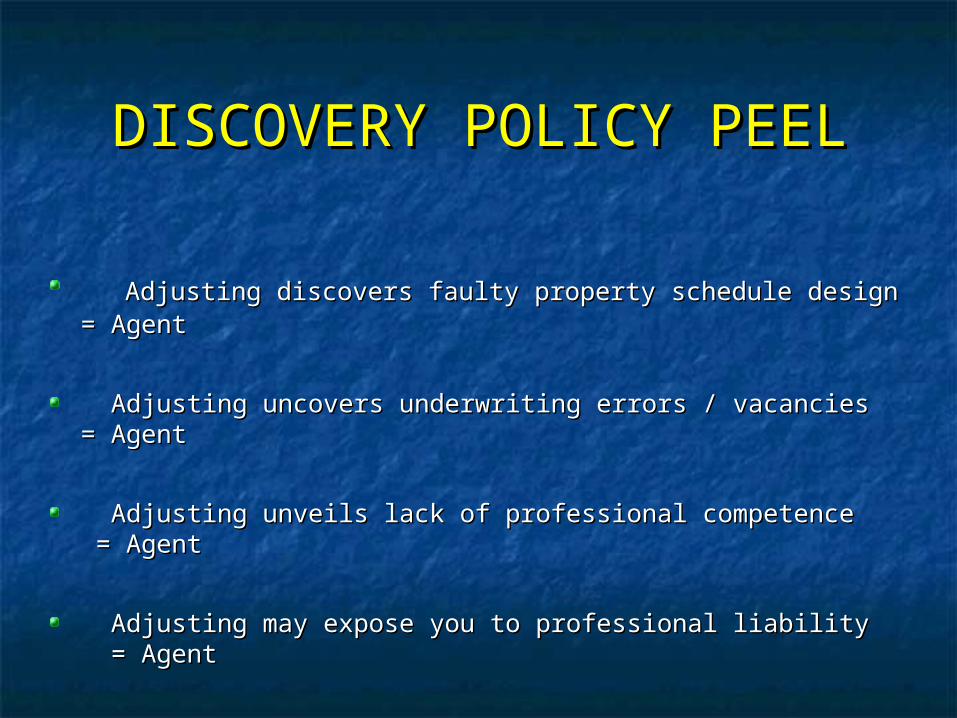

DISCOVERY POLICY PEELDISCOVERY POLICY PEEL

Adjusting discovers faulty property schedule design = AgentAdjusting discovers faulty property schedule design = Agent

Adjusting uncovers underwriting errors / vacancies = AgentAdjusting uncovers underwriting errors / vacancies = Agent

Adjusting unveils lack of professional competence = Adjusting unveils lack of professional competence = AgentAgent

Adjusting may expose you to professional liability = AgentAdjusting may expose you to professional liability = Agent

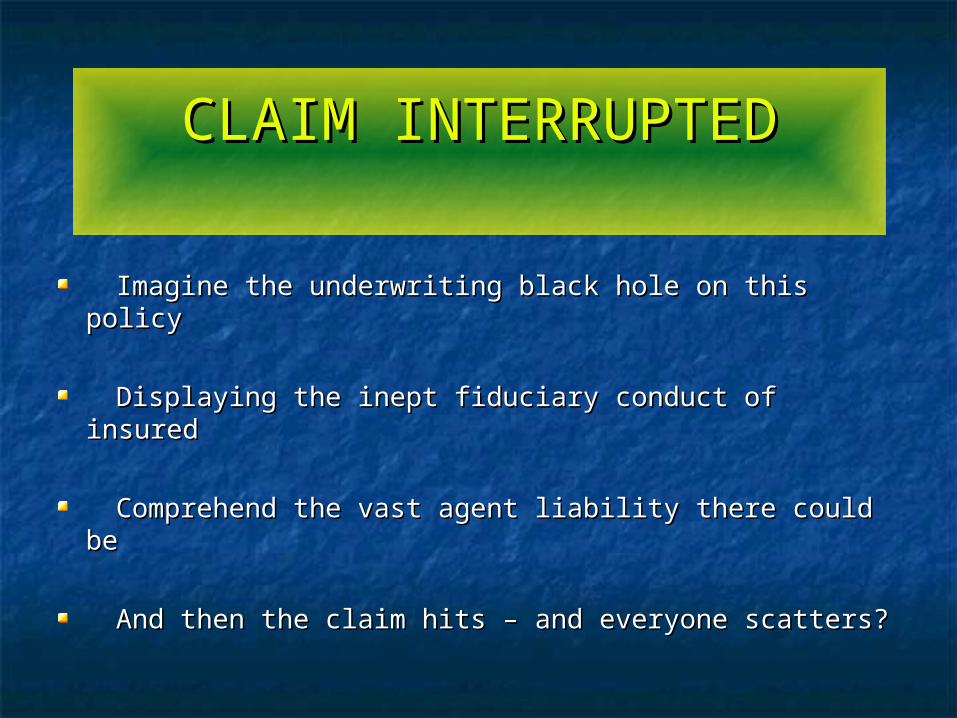

CLAIM INTERRUPTEDCLAIM INTERRUPTED

Imagine the underwriting black hole on this policyImagine the underwriting black hole on this policy

Displaying the inept fiduciary conduct of insuredDisplaying the inept fiduciary conduct of insured

Comprehend the vast agent liability there could beComprehend the vast agent liability there could be

And then the claim hits – and everyone scatters?And then the claim hits – and everyone scatters?

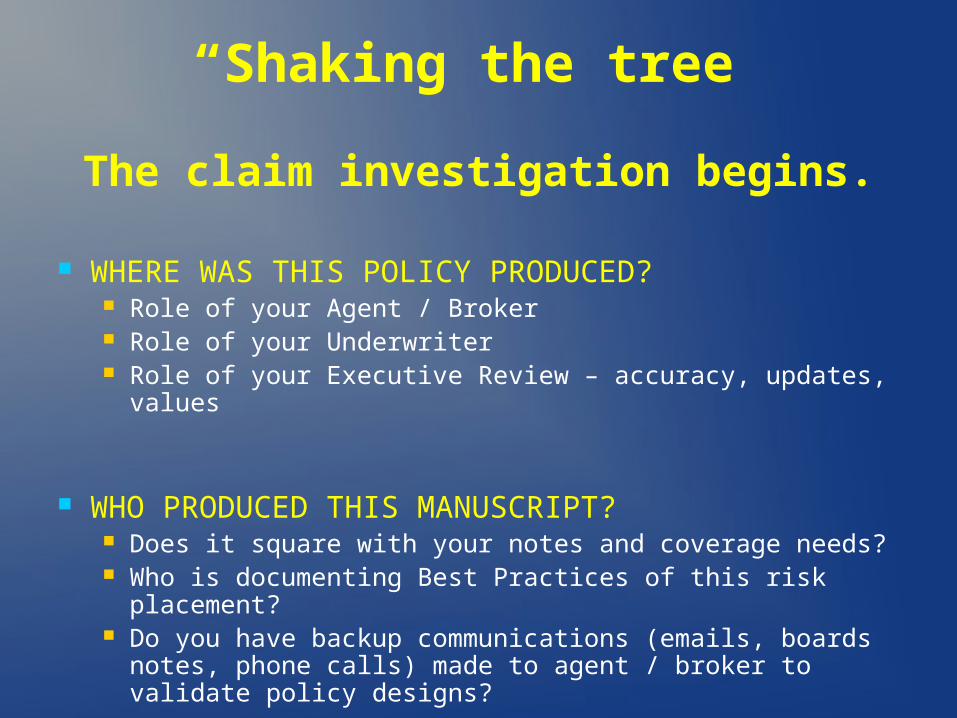

“Shaking the tree”

The claim investigation begins.

WHERE WAS THIS POLICY PRODUCED? Role of your Agent / Broker Role of your Underwriter Role of your Executive Review – accuracy, updates, values

WHO PRODUCED THIS MANUSCRIPT? Does it square with your notes and coverage needs? Who is documenting Best Practices of this risk placement? Do you have backup communications (emails, boards notes,

phone calls) made to agent / broker to validate policy designs?

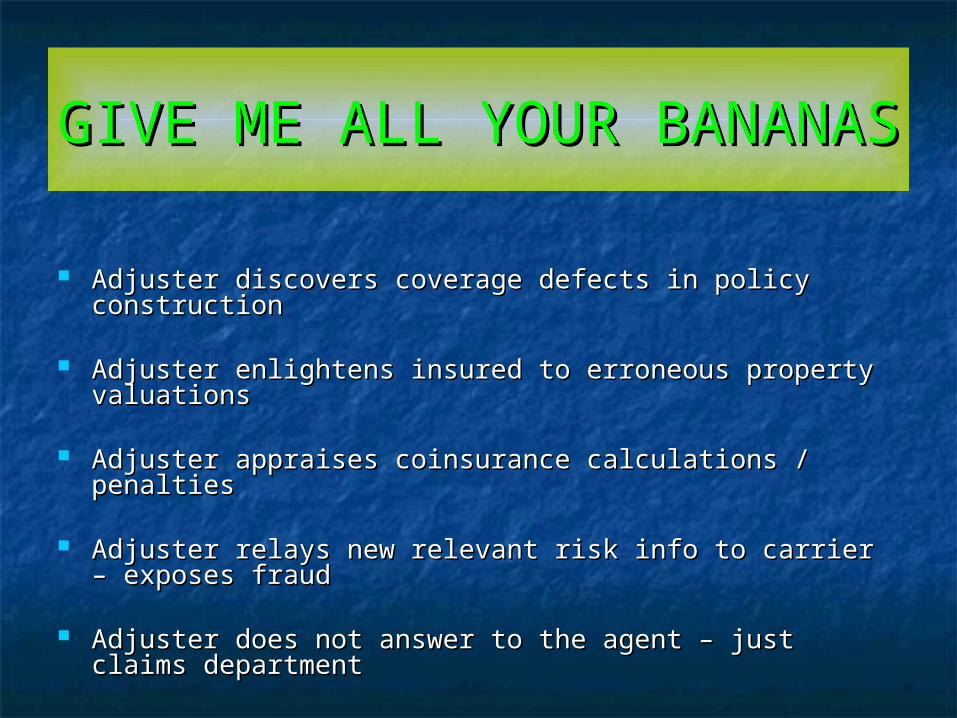

GIVE ME ALL YOUR GIVE ME ALL YOUR BANANASBANANAS

Adjuster discovers coverage defects in policy constructionAdjuster discovers coverage defects in policy construction

Adjuster enlightens insured to erroneous property Adjuster enlightens insured to erroneous property valuationsvaluations

Adjuster appraises coinsurance calculations / penalties Adjuster appraises coinsurance calculations / penalties

Adjuster relays new relevant risk info to carrier – exposes Adjuster relays new relevant risk info to carrier – exposes fraudfraud

Adjuster does not answer to the agent – just claims Adjuster does not answer to the agent – just claims departmentdepartment

DESIGN x DETAILS = SUCCESSDESIGN x DETAILS = SUCCESS

DIGITAL DOCUMENTATION OF BUILDING CONDITIONS DIGITAL DOCUMENTATION OF BUILDING CONDITIONS PRE-HURRICANE SEASON – CRITICAL FOR CLAIMS.PRE-HURRICANE SEASON – CRITICAL FOR CLAIMS.

MATCHING BUILDING VALUES AND LOCATIONS.MATCHING BUILDING VALUES AND LOCATIONS.

COINSURANCE PERCENTAGE AND PENALTIES.COINSURANCE PERCENTAGE AND PENALTIES.

DIGITAL STORAGE OFF-SITE OF NEEDED RECORDS – DIGITAL STORAGE OFF-SITE OF NEEDED RECORDS – WITH AGENTS, CONTRACTORS, LEGAL TEAM.WITH AGENTS, CONTRACTORS, LEGAL TEAM.

MARSHALL & SWIFT REPLACEMENT COST VALUATIONS.MARSHALL & SWIFT REPLACEMENT COST VALUATIONS.

WHAT DEDUCTIBLE PLAN DID YOU BUY?WHAT DEDUCTIBLE PLAN DID YOU BUY?

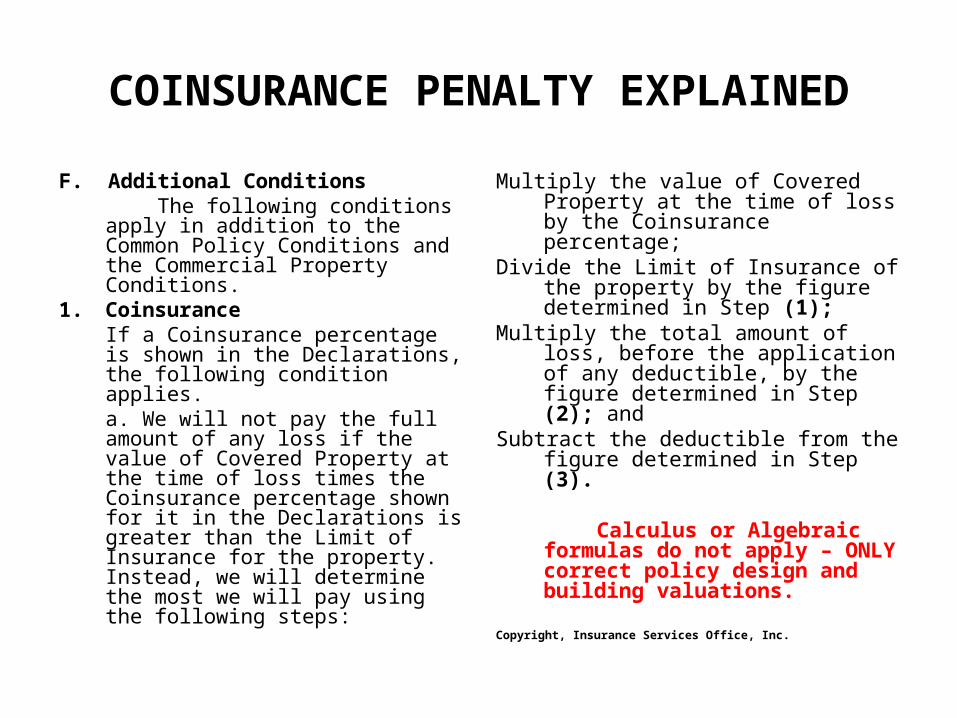

COINSURANCE PENALTY EXPLAINED

F. Additional Conditions The following conditions apply in

addition to the Common Policy Conditions and the Commercial Property Conditions.

1. CoinsuranceIf a Coinsurance percentage is shown in the Declarations, the following condition applies.a. We will not pay the full amount of any loss if the value of Covered Property at the time of loss times the Coinsurance percentage shown for it in the Declarations is greater than the Limit of Insurance for the property. Instead, we will determine the most we will pay using the following steps:

Multiply the value of Covered Property at the time of loss by the Coinsurance percentage;

Divide the Limit of Insurance of the property by the figure determined in Step (1);

Multiply the total amount of loss, before the application of any deductible, by the figure determined in Step (2); and

Subtract the deductible from the figure determined in Step (3).

Calculus or Algebraic formulas do not apply – ONLY correct policy design and building valuations.

Copyright, Insurance Services Office, Inc.

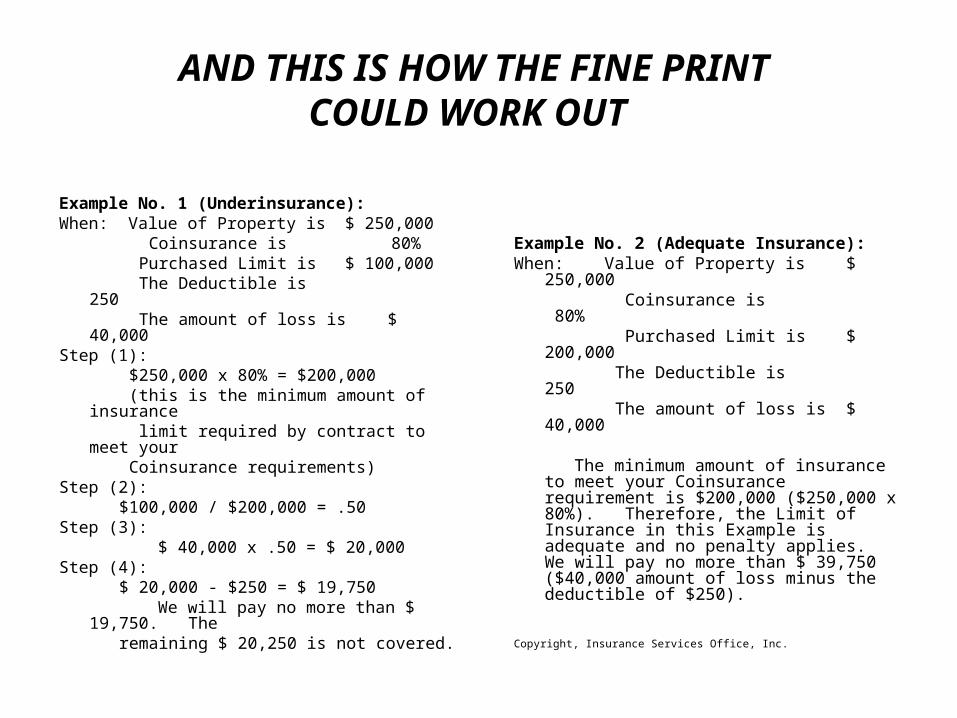

AND THIS IS HOW THE FINE PRINT COULD WORK OUT

Example No. 1 (Underinsurance):When: Value of Property is $ 250,000

Coinsurance is 80% Purchased Limit is $ 100,000 The Deductible is 250 The amount of loss is $ 40,000

Step (1): $250,000 x 80% = $200,000 (this is the minimum amount of insurance limit required by contract to meet your Coinsurance requirements)

Step (2): $100,000 / $200,000 = .50

Step (3): $ 40,000 x .50 = $ 20,000Step (4):

$ 20,000 - $250 = $ 19,750 We will pay no more than $ 19,750. The

remaining $ 20,250 is not covered.

Example No. 2 (Adequate Insurance):When: Value of Property is $ 250,000

Coinsurance is 80% Purchased Limit is $ 200,000 The Deductible is 250 The amount of loss is $ 40,000

The minimum amount of insurance to meet your Coinsurance requirement is $200,000 ($250,000 x 80%). Therefore, the Limit of Insurance in this Example is adequate and no penalty applies. We will pay no more than $ 39,750 ($40,000 amount of loss minus the deductible of $250).

Copyright, Insurance Services Office, Inc.

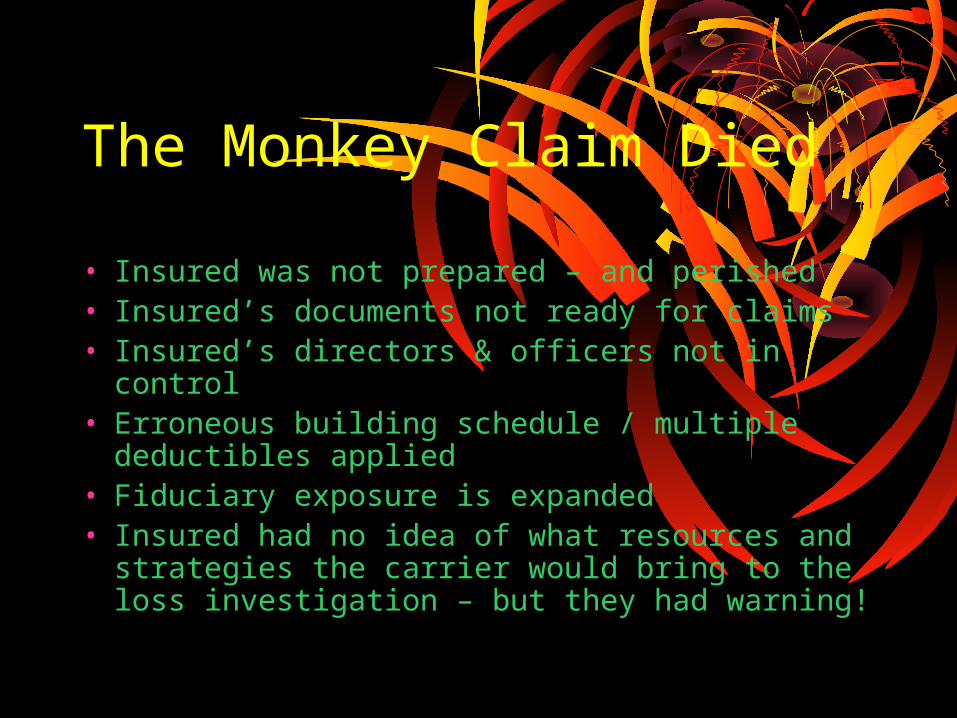

The Monkey Claim Died

• Insured was not prepared – and perished• Insured’s documents not ready for claims• Insured’s directors & officers not in control• Erroneous building schedule / multiple

deductibles applied• Fiduciary exposure is expanded• Insured had no idea of what resources and

strategies the carrier would bring to the loss investigation – but they had warning!

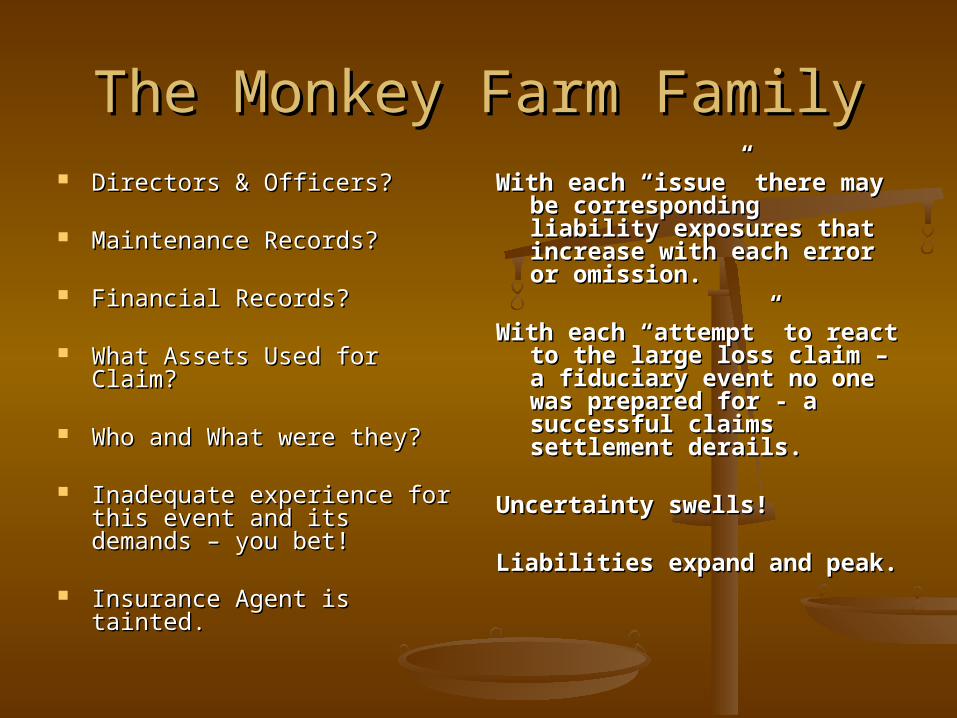

The Monkey Farm FamilyThe Monkey Farm Family Directors & Officers?Directors & Officers?

Maintenance Records?Maintenance Records?

Financial Records?Financial Records?

What Assets Used for Claim? What Assets Used for Claim?

Who and What were they?Who and What were they?

Inadequate experience for this Inadequate experience for this event and its demands – you event and its demands – you bet!bet!

Insurance Agent is tainted.Insurance Agent is tainted.

With each “issue” there may With each “issue” there may be corresponding liability be corresponding liability exposures that increase exposures that increase with each error or with each error or omission.omission.

With each “attempt” to react With each “attempt” to react to the large loss claim – a to the large loss claim – a fiduciary event no one was fiduciary event no one was prepared for - a successful prepared for - a successful claims settlement derails.claims settlement derails.

Uncertainty swells!Uncertainty swells!

Liabilities expand and peak.Liabilities expand and peak.

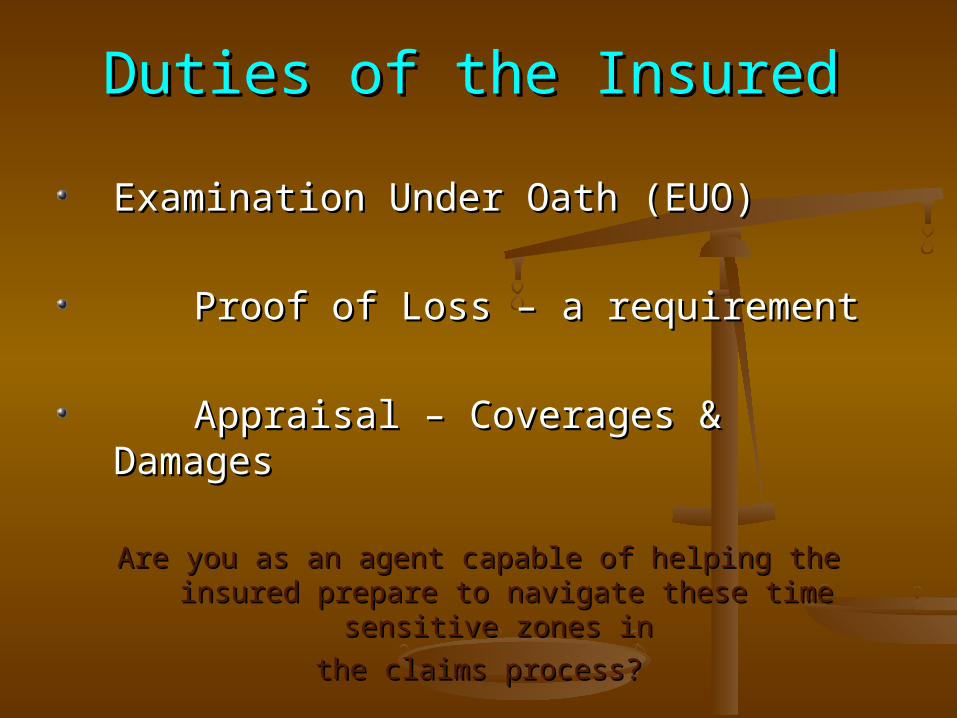

Duties of the InsuredDuties of the Insured

Examination Under Oath (EUO)Examination Under Oath (EUO)

Proof of Loss – a requirementProof of Loss – a requirement

Appraisal – Coverages & DamagesAppraisal – Coverages & Damages

Are you as an agent capable of helping the insured Are you as an agent capable of helping the insured prepare to navigate these time sensitive zones in prepare to navigate these time sensitive zones in

the claims process?the claims process?

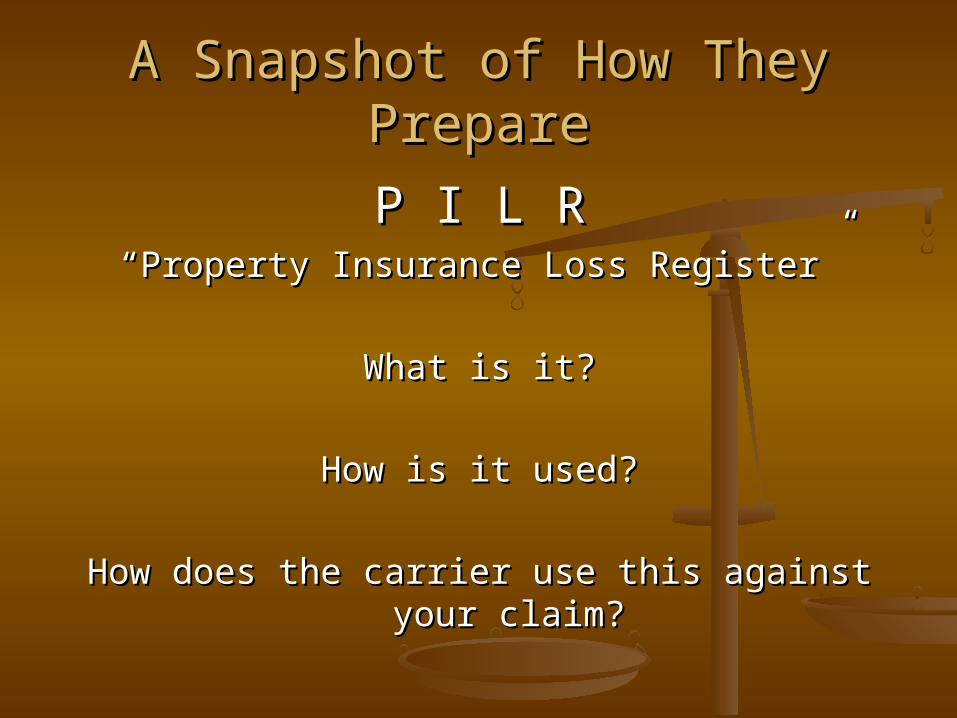

A Snapshot of How They PrepareA Snapshot of How They Prepare

P I L RP I L R““Property Insurance Loss Register”Property Insurance Loss Register”

What is it?What is it?

How is it used?How is it used?

How does the carrier use this against your How does the carrier use this against your claim?claim?

Plan for RecoveryPlan for Recovery

This Policy May be Your Biggest Asset.This Policy May be Your Biggest Asset. A large loss claim event may be the A large loss claim event may be the

biggest corporate viability challenge you biggest corporate viability challenge you have faced.have faced.

Know the strategies and tools of the Know the strategies and tools of the carrier’s claims adjusting process – know carrier’s claims adjusting process – know how they come to play.how they come to play.

Equip your professional advisors ahead of Equip your professional advisors ahead of time – no reactive magic has been found.time – no reactive magic has been found.

Court’s Response – Your failure to plan Court’s Response – Your failure to plan does not make for their emergency!does not make for their emergency!

Coverage RewardsCoverage Rewardsor Regrets?or Regrets?

Florida Property Insurance Reform – 2011Florida Property Insurance Reform – 2011

Senate Bill 408Senate Bill 408

ACVACV – depreciated settlement amount paid – depreciated settlement amount paid first (hopefully within 90-days first (hopefully within 90-days undisputed)undisputed)

RCVRCV – remaining difference of total loss – remaining difference of total loss settlement paid when work to restore or settlement paid when work to restore or replace is actually completed.replace is actually completed.

Unauthorized Entities Updated Verbiage:Unauthorized Entities Updated Verbiage:An entity that is required to be licensed or registered with the Florida Office of An entity that is required to be licensed or registered with the Florida Office of

Insurance Regulation but is operating without the proper authorization is identified as an Insurance Regulation but is operating without the proper authorization is identified as an unauthorized insurerunauthorized insurer. All persons have the responsibility of conducting reasonable . All persons have the responsibility of conducting reasonable

research to ensure they are not writing policies or placing business with an unauthorized research to ensure they are not writing policies or placing business with an unauthorized insurer. Any person who, directly or indirectly, aid or represent an unauthorized insurer insurer. Any person who, directly or indirectly, aid or represent an unauthorized insurer can lose their licenses or face other disciplinary sanctions. Please see section 626.901, can lose their licenses or face other disciplinary sanctions. Please see section 626.901,

Florida Statutes, to read the laws. Lack of careful screening can result in significant Florida Statutes, to read the laws. Lack of careful screening can result in significant financial loss to Florida consumers due to unpaid claims and/or theft of premiums. Under financial loss to Florida consumers due to unpaid claims and/or theft of premiums. Under

Florida law, a person can be charged with a third-degree felony and also held liable for Florida law, a person can be charged with a third-degree felony and also held liable for any unpaid claims and refund of premiums when representing an unauthorized insurer. It any unpaid claims and refund of premiums when representing an unauthorized insurer. It

is the person’s responsibility to give fair and accurate information regarding the is the person’s responsibility to give fair and accurate information regarding the companies they represent.companies they represent.