Embed Size (px)

Citation preview

MONEY LAUNDERING AND TERRORIST FINANCING TYPOLOGIES AND TRENDS IN CANADIAN BANKINGMAY 2009

Financial Transactions and Reports Analysis Centre of Canada

MESSAGE FROM

THE DIRECTOR

I am pleased to present the first reportintended to address the interests of theCanadian banking sector and other financialentities, Money Laundering and TerroristFinancing Typologies and Trends in CanadianBanking.

The efforts to combat money laundering andterrorist activity financing are, by necessity,collaborative. The Canadian banking sectorand other financial entities are uniquelypositioned through their involvement inhundreds of millions of financial transactionsto make a contribution to this effort. AsCanada’s financial intelligence unit, FINTRAC is able to aggregate and analyze the reportedtransactions from many different sectors inorder to produce financial intelligence.Ultimately, the investigations and prosecutionsthat are assisted by this intelligence are carriedout at yet another stage of the larger initiative.

As FINTRAC’s Director, I am aware of the needfor greater information sharing throughoutthis chain of activity. I hope that this reportand the collaborative spirit within which it hasbeen undertaken are a step in that direction. I look forward to building on this first reportand working collaboratively on similar futureprojects.

As you take the time to read it, I wouldencourage you to comment on its contents and to suggest issues for future explorationand exposition.

Jeanne M. FlemmingDirector

MoneyLaunderingandTerroristFinancingTypologiesandTrendsin

CanadianBanking–May2009

Financial Transactions and Reports Analysis Centre of Canada

TABLE OF CONTENTS

INTRODUCTION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .2

REVIEW OF CASES DISCLOSED BY FINTRAC IN 2007-2008 . . . . . . . . . . . . . . . . . . . .3General observations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .3

Types of suspected activities and predicate offences . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .3Common phases and techniques of money laundering . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .3Sectors used . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .4Types of businesses involved . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .4

Suspicious financial transactions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .6

SANITIZED CASES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .7Sanitized Case 1 – Fraud-related Money Laundering . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .7Sanitized Case 2 – Drug-related Money Laundering . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .7Sanitized Case 3 – Terrorist Financing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .8

TYPOLOGIES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .9Investment companies and trusts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .9Securities industry . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .11

EMERGING VULNERABILITIES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .14Prepaid cards . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .14

Vulnerabilities associated with open-loop prepaid cards . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .14Vulnerabilities associated with closed-loop prepaid cards . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .15

Digital Precious Metals . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .15

CONCLUSION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .18

1

MoneyLaunderingandTerroristFinancingTypologiesandTrendsin

CanadianBanking–May2009

INTRODUCTION

This report is the first of its kind. It has been madepossible through the collaboration of five of Canada’slargest banks and FINTRAC. The exchange between thebanking sector and the financial intelligence unit hasguided the subjects that are examined in this report.

Through this paper FINTRAC seeks to address questionsabout money laundering and terrorist financing that areunique to the Canadian banking sector and have beenobserved in our analysis of financial transactions.Through a better understanding of these patterns andtrends, the banking sector will be better able to combatmoney laundering and terrorist financing and able tocarry out their obligations under the Proceeds of Crime(Money Laundering) and Terrorist Financing Act.

There are four key sections to the report. The firstsection highlights the observations of a review of all thecases FINTRAC disclosed to law enforcement or nationalsecurities agencies in 2007-2008. The second sectionpresents sanitized cases and the third section presentstypologies on money laundering and terrorist financing(ML/TF) related to the banking sector. The differencebetween a sanitized case and typology will be furtherexplained in those sections. The final section identifiestwo emerging vulnerabilities that may be of interest tothe banking sector.

It is important to note that statistics related to theprosecution or asset confiscation of a money launderingor terrorist financing case that may contain informationthat FINTRAC disclosed is not included in the report, asFINTRAC is not an investigative agency. The focus of thisreport is the intelligence that FINTRAC has been able toproduce to assist investigations and the observed trendsas they related to Canadian banking.

2

MoneyLaunderingandTerroristFinancingTypologiesandTrendsin

CanadianBanking–May2009

Financial Transactions and Reports Analysis Centre of Canada

REVIEW OF CASES DISCLOSED

BY FINTRAC IN 2007-2008

For this report, FINTRAC conducted an extensive reviewand analysis of all cases disclosed to various recipientsfor the fiscal year 2007-2008 (April 2007 to March 2008).Annual case reviews provide a complete picture of thetrends and activities related to ML/TF within that year.Every case review better positions FINTRAC to be able toidentify Canadian trends in ML/TF and ultimately sharethis information with reporting entities.

The methodology for the case review involved acomplete examination of all cases with a focus on somekey characteristics within a FINTRAC case disclosure. For clarification, a FINTRAC case disclosure containswhat is referred to as “designated information” that isprescribed by our enabling legislation. This designatedinformation includes key identifying information fromFINTRAC’s analysis (e.g. name, address, bank accountnumbers, etc.). For the purposes of this document, thegeneral observations presented place emphasis on thefollowing characteristics:

• types of case/activities; • most common predicate offences1;• sectors used for various activities associated

to ML/TF;• most common ML/TF stages and techniques used; and • most common types of businesses used in ML/TF

schemes.

In addition, the most common suspicious financialtransactions that FINTRAC observed in moneylaundering (including cases related to drug and fraud)and terrorist financing cases are also presented. It should be noted that the examples of suspiciousfinancial transactions included in the case review arenot necessarily an indication of the frequency in whichthey were used but are included because they wererepresentative and specific of different types of cases.

General observations

TYPES OF SUSPECTED ACTIVITIES AND PREDICATE OFFENCES

In 2007-2008, FINTRAC disclosed a total of 210cases, divided in the following activities:

• 171 cases associated with money laundering • 10 cases associated with money laundering and

terrorist financing • 29 cases associated with terrorist financing and

threats to national security2.

FINTRAC may be informed of the suspectedpredicate offence through voluntary informationreceived from law enforcement or it may beincluded in a suspicious transaction report. Ininstances where FINTRAC was able to link thesuspected money laundering to a suspectedpredicate criminal offence, fraud and drugtrafficking were the most frequently observedoffences. For the cases where fraud was suspected,investment/securities and telemarketing fraudwere the most observed. For cases where drug-related activities were suspected, marijuana growoperations and/or distribution, as well as thetrafficking of cocaine were the most observed.

COMMON PHASES AND TECHNIQUES OF MONEY LAUNDERING

In reviewing the most common phases andtechniques of money laundering appearing in thecases, the results are similar to previous years. Themost observed stages of money laundering wereplacement and layering and the most commontechniques for money laundering were structuringand smurfing. Structuring normally involvesmultiple cash deposits or withdrawals at amountsbelow the reporting threshold and smurfing isdefined as multiple deposits of cash, and/or low-value monetary instruments purchased fromvarious banks or money services businesses byvarious individuals. Nominees (individuals andbusinesses) were also found to be involved in at least nine cases that related to drugs ororganized crime.

3

MoneyLaunderingandTerroristFinancingTypologiesandTrendsin

CanadianBanking–May2009

1 For FINTRAC’s purposes, a “predicate offence” is an offence under the Criminal Code or any other criminal lawstatutes under Parliament’s jurisdiction from which proceeds of crime may be derived (with the exception ofoffences under certain acts including the Income Tax Act and the Excise Tax Act.)

2 FINTRAC’s role is to provide CSIS with financial intelligence to assist that agency in fulfilling its mandate ofinvestigating threats to the security of Canada. There will be limited references to threats to national security in this document.

SECTORS USED

The reports submitted by the banking sector toFINTRAC, suspicious transactions reports (STRs), large cash transaction reports (LCTRs) and electronicfunds transfer reports (EFTRs) played a major role in assisting FINTRAC in identifying individuals andentities suspected of being involved in activitiesassociated with ML/TF. This role is attributed to thelarge volume of reports provided by banks andfinancial institutions to FINTRAC and also theimplementation of strong compliance regimes todetect suspicious financial transactions. As observedin the previous years, the majority of suspiciousfinancial transactions associated to cases disclosed tolaw enforcement and the intelligence community in2007-2008 were conducted through banks andother financial institutions.

Casinos, money services businesses (MSBs), andsome trust companies or accounts were also usedto conduct suspicious financial transactions, but to a lesser extent. It was found that suspiciousfinancial transactions were conducted at casinos in twenty-five cases and were mostly related tosuspected drug offences but also to suspectedfraud and terrorist financing. Trust companies oraccounts were involved in at least twelve cases that were suspected to be related to drug, fraud,terrorist financing and organized crime activities.The use of Internet payment systems wasobserved in five cases.

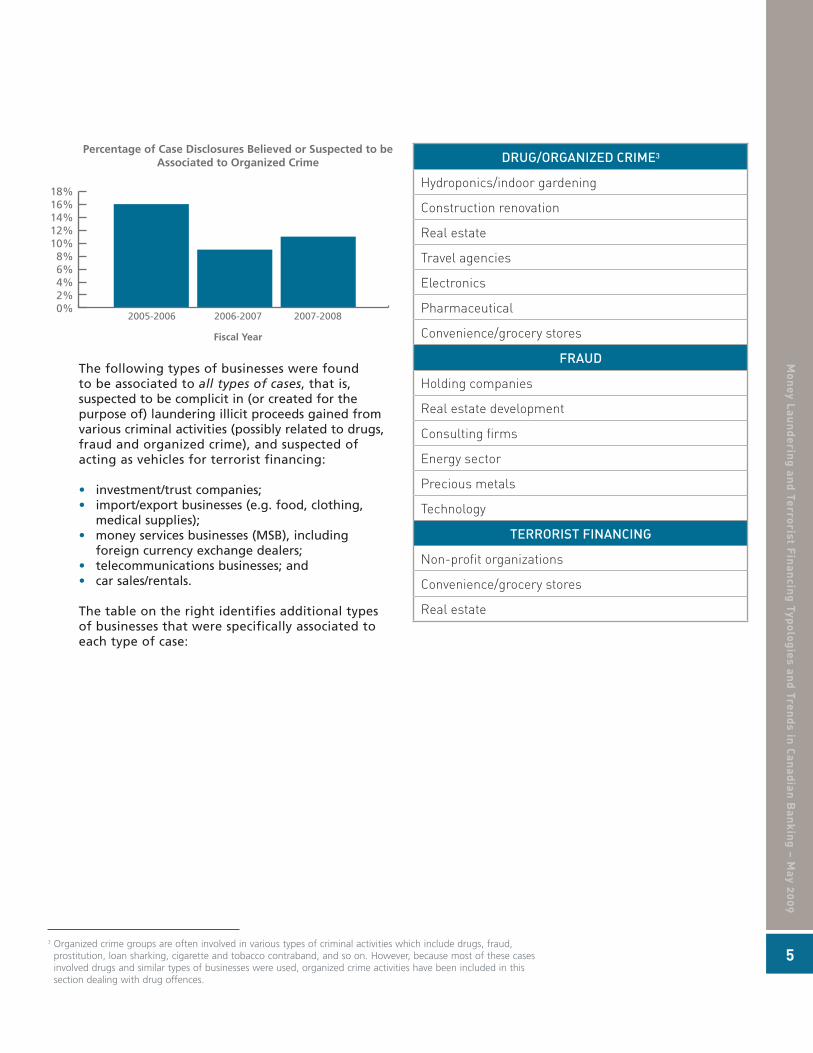

TYPES OF BUSINESSES INVOLVED

In some instances, case disclosures only involveindividuals, but often, they also involve businesses.In fact, the majority of 2007-2008 cases suspectedto be related to drug or fraud involved individualsand at least one business and, in most instances,multiple businesses. The chart below provides anillustration of how the number of cases involvingbusinesses has changed over the last few years:

As observed on the chart, the number of drug-related cases involving businesses continued toincrease for the third year in a row. A slightincrease was also observed in the number of cases involving fraud.

On the other hand, 82% of cases related toterrorist financing and/or other threats to thesecurity of Canada in 2007-2008 also involvedbusinesses and/or non-profit organizations, andremained almost the same.

The chart on page 5 illustrates how the percentageof cases involving individuals and/or businessesbelieved or suspected to be associated to organizedcrime groups has remained fairly stable in the lasttwo years, 11% in 2007-2008 and 9% in 2006-2007,after having decreased to almost half of what itwas in 2005-2006 (16%):

4

MoneyLaunderingandTerroristFinancingTypologiesandTrendsin

CanadianBanking–May2009

Financial Transactions and Reports Analysis Centre of Canada

There are three widely recognized stages in the moneylaundering process:

PLACEMENT involves placing the proceeds of crime inthe financial system.

LAYERING involves converting the proceeds of crimeinto another form and creating complex layers offinancial transactions to disguise the audit trail and thesource and ownership of funds. This stage may involvetransactions such as the buying and selling of stocks,commodities or property.

INTEGRATION involves placing the laundered proceedsback in the economy to create the perception oflegitimacy.

0%10%20%30%40%50%60%70%80%90%

100%

Percentage of FINTRAC Case DisclosuresInvolving at least one Business

Fiscal Year

2005-2006 2006-2007 2007-2008

Drug cases Fraud cases

The following types of businesses were found to be associated to all types of cases, that is,suspected to be complicit in (or created for thepurpose of) laundering illicit proceeds gained fromvarious criminal activities (possibly related to drugs,fraud and organized crime), and suspected ofacting as vehicles for terrorist financing:

• investment/trust companies;• import/export businesses (e.g. food, clothing,

medical supplies); • money services businesses (MSB), including

foreign currency exchange dealers;• telecommunications businesses; and• car sales/rentals.

The table on the right identifies additional typesof businesses that were specifically associated to each type of case:

5

MoneyLaunderingandTerroristFinancingTypologiesandTrendsin

CanadianBanking–May2009

3 Organized crime groups are often involved in various types of criminal activities which include drugs, fraud,prostitution, loan sharking, cigarette and tobacco contraband, and so on. However, because most of these casesinvolved drugs and similar types of businesses were used, organized crime activities have been included in thissection dealing with drug offences.

Percentage of Case Disclosures Believed or Suspected to beAssociated to Organized Crime

Fiscal Year

2005-2006 2006-2007 2007-20080%2%4%6%8%

10%12%14%16%18%

Suspicious financial transactions

The following identifies the most common types of suspicious financial transactions for ML/TF casesconducted through the banking sector in 2007-2008. In most instances, it is also indicated at whatstage of ML/TF the suspicious financial transactionhad likely occurred:

• Large cash deposits ($20, $50 or $100bills)/cheques/bank drafts (often under thereporting threshold – structuring) to personal/business bank accounts followed by eitherissuance of cheques (often payable to 3rdparties) or purchase of bank drafts or electronicfunds transfers (EFTs) to Canadian or foreignentities/individuals (often associated) or cashwithdrawals – placement, layering and use of pass-through accounts to conceal source of funds

• Deposits of $20 bills (CAD) were sometimesfollowed by USD EFTs – placement and layering

• Deposits of cash or cheques were sometimesfollowed by transfers to accounts held by thesame individual/entity in other Canadian orforeign financial institutions – placement and layering

• Multiple cash deposits were conducted in ashort time frame and below the reportingthreshold, as well as alternating betweenbranches across the country (sometimes throughautomated teller machines), followed by cashwithdrawals – structuring and smurfing in aneffort to place the funds

• Receipt of EFTs followed by purchase of bankdrafts or issuance of cheques payable to 3rdparties – layering

More specifically, for drug-related cases, thesuspicious financial transactions representedplacement and layering activities:

• Large cash deposits (structured and conductedby various individuals in different locations – i.e. smurfing) followed by EFTs sent to foreigncountries (often to Asia)

• USD deposits in bank accounts held by one MSB(in larger amounts than normal for most MSBsas indicated in STR information) followed bypurchase of USD bank drafts payable to anentity with similar name

• Numerous EFTs sent to one MSB and associatedindividuals from an individual in a country of concern

Of the identified drug cases, certain types ofsuspicious financial transactions were found to be particularly associated to grow operations:

• Bank drafts purchased at one bank anddeposited at another bank, then followed by EFTs sent to foreign countries

• Numerous large rounded-sum cash depositsfollowed by payment of large hydro bills

• Cash payments (under threshold) to credit card accounts (sometimes multiple payments in one day and conducted by 3rd parties)

For fraud-related cases suspicious financialtransactions represented mostly layering activities:

• Cheques or bank drafts drawn from a financialinstitution were deposited into business accountsheld at other financial institutions thenfollowed by cash withdrawals

• 3rd parties in the United States purchased, over a short period, large numbers of money orders(in $500 and $1000) payable to companies inCanada – these money orders were deposited inbusiness accounts held in Canada, then EFTswere sent back to accounts in the United States– this scheme was repeated a number of times

Terrorist financing cases were found to include thefollowing types of suspicious financial transactions:

• Large cash deposits (sometimes conducted by third parties) into accounts of non-profitorganizations

• Large number of deposits (into personalaccounts) of cheques drawn from legal trustaccounts followed by withdrawals

• Deposits of U.S. postal money orders ($500 and$1000) or cash were followed by large cashwithdrawals or issuance of cheques or purchaseof bank drafts payable to foreign MSB

6

MoneyLaunderingandTerroristFinancingTypologiesandTrendsin

CanadianBanking–May2009

Financial Transactions and Reports Analysis Centre of Canada

SANITIZED CASES

In an effort to provide additional insight based on thereview of the cases FINTRAC disclosed in 2007-2008, thefollowing are actual cases that were disclosed to lawenforcement or national security agencies. The casesincluded in this section are sanitized, all identifyinginformation has been removed and were chosen forinclusion in this paper as they involve transactionsassociated with both retail (personal) and commercial(business) banking. The “red flags” associated witheach case assisted FINTRAC to reach the threshold forreasonable grounds to suspect that the informationwould be relevant to a money laundering or terroristfinancing investigation, and thus to disclose the case.

Sanitized Case 1 – Fraud-Related

Money Laundering

FINTRAC received one STR from a bank, whichgenerated this case involving ten individuals andtwelve businesses, located in the greater Torontoarea, suspected of possible fraudulent and moneylaundering activities. An additional 22 STRs,provided by the same bank and two others, as well as one MSB, further contributed to this case.

FINTRAC’s analysis revealed that most businesses in this case appeared to be involved in theemployment service industry and the associatedindividuals/officers conducted multiple cashdeposits. Employees of the businesses were alsopaid in cash. These transactions were found to be unusual since this industry is not typically cash-driven. The businesses were linked throughcommon directors/officers, financial transactions,and shared addresses/phone numbers. Theindividuals involved were also linked throughsimilar addresses and joint signing authorities forvarious bank accounts.

One individual was the subject of a previousdisclosure to law enforcement regarding fraud/extortion activities and was suspected to havelinks to Eastern European organized crime.

RED FLAGS associated with this case:

• Individuals made cash deposits (in $100 and $50denominations) into the personal accounts ofmultiple associates who then issued chequespayable to other individuals (i.e. use of pass-through accounts)

• Numerous businesses paid their employees incash and reporting entities indicated in the STR that this was not consistent with typicalbusiness operations

• Cheques were deposited into business accountsthen immediately withdrawn in cash or throughthe issuance of cheques payable “to cash” or payable to the individual making the initial deposit

• Reporting entities also reported excessive cashflow in the business accounts

The transactions conducted in this case weremostly representative of the placement andlayering stages of money laundering. The relevantdesignated information was disclosed to fourdifferent law enforcement agencies.

Sanitized Case 2 – Drug-Related

Money Laundering

FINTRAC received information from lawenforcement regarding a number of individualsand businesses, located in the greater Vancouverarea, under investigation for suspected involvementin the importation of drugs to Canada from anAsian country.

FINTRAC’s analysis revealed financial transactionsassociated to five of the individuals and threeMSBs that were mentioned in the informationprovided by law enforcement. FINTRAC suspectedthat six additional individuals and five businessesspecializing in telecommunications, construction,foreign exchange and interior renovation werealso involved in the scheme.

Thirty-five STRs reported to FINTRAC by multiplebranches of four different banks and threedifferent credit unions were instrumental inallowing FINTRAC to find connections between the various players in this scheme, as well as

7

MoneyLaunderingandTerroristFinancingTypologiesandTrendsin

CanadianBanking–May2009

identifying ones that may not have beenpreviously known to law enforcement. LCTRs and EFTRs also assisted FINTRAC in its analysis.

RED FLAGS associated with this case:

• Large cash deposits (in CAD and USD) intopersonal accounts were sometimes followed bythe purchase of bank drafts payable to trustcompanies or money services/currency exchangebusinesses

• Domestic wire transfers between personalaccounts were followed by the purchase ofbank drafts payable to trust companies

• Bank drafts and cheques issued from otherfinancial institutions were deposited intopersonal and business accounts and weresometimes followed by EFTs to a Middle Eastern country

• EFTs were also received from the same MiddleEastern country

• Multiple transactions were carried out on thesame day at the same branch but with differenttellers, hours apart

• Some cash deposits were structured to keepamounts under the reporting threshold and/orconducted at different branches

• Cash, cheques and bank drafts were depositedby third parties into the business accounts ofMSBs and domestic wires were received into thesame accounts; they were immediately followedby withdrawals to purchase bank drafts payableto other MSBs which then sent EFTs to variousbeneficiaries in foreign countries

• The same MSBs receiving deposits or wires also directly sent EFTs to beneficiaries in foreign countries

Individuals and entities involved in this case appear to have conducted a number of suspiciousactivities mostly representative of the placementand layering stages of money laundering inaddition to furthering their drug traffickingactivities. FINTRAC disclosed all relevant designatedinformation to law enforcement to assist them intheir investigation.

Sanitized Case 3 –

Terrorist Financing

FINTRAC received information from lawenforcement and intelligence agencies regarding a non-profit organization (NPO), located in thegreater Toronto area, which was suspected ofacting as a front for a terrorist organization. TheNPO and associated individuals were suspected of facilitating the acquisition and aggregation4

of financial resources in Canada, as well as thetransmission of resources ultimately for the benefitof the terrorist organization’s operations overseas.

The NPO was the subject of several FINTRACdisclosures to law enforcement and intelligenceagencies between 2002 and 2007. STRs, LCTRs andEFTRs from financial institutions were instrumentalin assisting FINTRAC in its analysis.

RED FLAGS associated with this case:

• The NPO ordered many EFTs to the benefit ofindividuals and entities (including a foreign NPOalso suspected of being a front for the terroristorganization) located overseas. The EFTs wereordered primarily through major financialinstitutions rather than through domestic MSBs

• Various officers of the NPO made large cashdeposits to the various accounts of the suspectNPO, held at multiple financial institutions, forwhich the source of funds was unknown

• An individual also attempted to deposit anumber of cheques, made payable to thirdparties, to the account of the suspect NPO

• Multiple, recurrent electronic credits were madeto the accounts of the suspect NPO for whichthe original source of funds and remitters’identity were unknown

• The deposit of cash and monetary instruments(cheques, bank drafts etc.) to the account of the suspect NPO, were often followed by the purchase of bank drafts or offshore movement of funds

FINTRAC disclosed all relevant designatedinformation to law enforcement and intelligenceagencies to assist them in their investigation.

4 Acquisition is the initial identifiable movement of funds or goods into the process of terrorist financing andincludes activities such as voluntary donations by individuals/businesses to charitable organizations, loans byindividuals and businesses to terrorist front organizations, and the use of proceeds (funds or goods) from criminalactivities. Aggregation is the stage of terrorist financing involving the pooling of smaller amounts of funds orgoods into larger ones, usually by moving them to financial institution accounts or to other locations.

8

MoneyLaunderingandTerroristFinancingTypologiesandTrendsin

CanadianBanking–May2009

Financial Transactions and Reports Analysis Centre of Canada

TYPOLOGIES

When a series of money laundering or terroristfinancing schemes appear to be constructed in a similarfashion or using the same methods, the similar schemesare generally classified as a typology. By reviewing itscases and conducting targeted environmental scanning,FINTRAC was able to identify a number of typologiesassociated to wealth management. In particular, thissection discusses the use of investment companies/trustsand the securities industry for the purpose of moneylaundering. Case examples are also provided.

Investment companies and trusts

The following typologies have been identified as a result of a comprehensive study conducted byFINTRAC of all cases disclosed between April 2005and March 2007 that involved money launderingthrough the use of investment companies andtrusts5. The review provided FINTRAC with betterknowledge of how investment companies andtrusts located in Canada or associated withCanadian individuals/entities could be used orcontrolled for suspected ML/TF activity. The use ofprofessionals as intermediaries in the creation ofsuch companies or accounts, and the facilitation of some financial transactions was also studied.

The results of this study indicated that investmentcompanies and trusts may be used by individualscommitting various crimes (drug, fraud and otherorganized criminal activities). While both cansometimes be used to commit fraud, they appearedto be mostly used in the layering stage of moneylaundering.

Three typologies were found to be associated,although not exclusively, with the use of investmentcompanies and trusts for suspected moneylaundering and terrorist financing purposes:

1. multi-jurisdictional structures of corporateentities and trusts;

2. involvement of non-financialintermediaries/professionals; and

3. use of nominees (individuals and businesses,including shell companies).

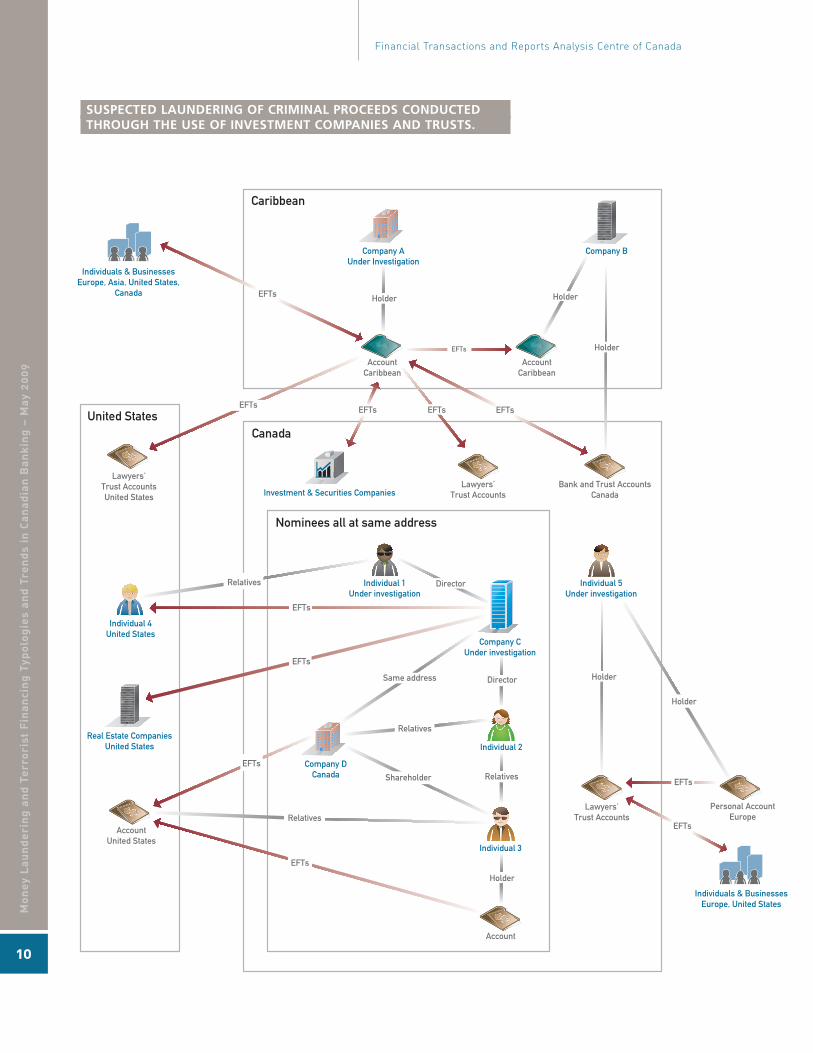

CASE EXAMPLE PROVIDING AN OVERVIEW OF THE THREE TYPOLOGIES

Information from law enforcement indicated thata large number of individuals and businesses,located in the greater Montreal area and with links to organized crime, were under investigationfor money laundering and proceeds of crimerelated offences.

This Canadian organized crime group was believedto be generating illicit revenues and was suspectedof investing these revenues in various businesses(including investment companies) that generatedfurther profits. This was done with the assistanceof nominees (family members and other associates)and through the use of trust accounts set up bylawyers and/or notaries, referred to as lawyers’trust accounts.

Many separately incorporated businesses werefound to be located at the same address and their owners or directors were suspected to benominees, sometimes with no apparent links to the organized crime group. Most of the companieswere located in Canada but many financialtransactions were conducted with offshorecompanies (Company A and Company B), some of them suspected of having been created for thesole purpose of concealing the criminal origins andownership of the funds. As published on their Websites, these two companies were reported to offerfinancial and investment services, which includedthe use of trusts, therefore allowing the clients tokeep their own identity and that of beneficiariescompletely confidential.

The chart on page 10 summarizes the case, butmost importantly, illustrates the complexity ofmoney laundering schemes.

9

MoneyLaunderingandTerroristFinancingTypologiesandTrendsin

CanadianBanking–May2009

5 For the purpose of this document, “trusts” is used when referring to both trust companies and trust accountsthat are set up by lawyers or notaries, and held within financial institutions.

10

MoneyLaunderingandTerroristFinancingTypologiesandTrendsin

CanadianBanking–May2009

Financial Transactions and Reports Analysis Centre of Canada

Caribbean

CanadaUnited States

Nominees all at same address

AccountCaribbean

AccountCaribbean

Lawyers’Trust AccountsUnited States

AccountUnited States

Holder

Company AUnder Investigation

Company B

Individuals & BusinessesEurope, Asia, United States,

Canada EFTs

HolderEFTs

Investment & Securities CompaniesLawyers’

Trust AccountsBank and Trust Accounts

Canada

EFTs

Individual 5Under investigation

Individual 4United States

Individual 1Under investigation

EFTs EFTs EFTs

Company CUnder investigation

Personal AccountEurope

Director

Individual 2

Director

Relatives

Holder

Lawyers’Trust Accounts

Relatives

EFTs

Holder

EFTs

EFTs

Individual 3

Account

Real Estate CompaniesUnited States

EFTs

Company DCanada

Same address

EFTs

Holder

Relatives

EFTs

Holder

Individuals & BusinessesEurope, United States

Relatives

Shareholder

SUSPECTED LAUNDERING OF CRIMINAL PROCEEDS CONDUCTEDTHROUGH THE USE OF INVESTMENT COMPANIES AND TRUSTS.

HIGHLIGHTS OF THE CASE:

• EFTs were ordered by or for the benefit ofCompany A, located in the Caribbean, andindividuals and businesses from Europe, Asia,and the United States. Furthermore, EFTs wereordered by or for the benefit of Company Aand investment/securities companies, as well astrust accounts (including lawyers’ trust accounts)located in Canada, some of them held byCompany B. Company A also ordered EFTs tothe benefit of a lawyer’s trust account held inthe United States.

• Company C and its Director, Individual 1, bothunder investigation and suspected of beingnominees for the organized crime group, werefound to be associated with another threeinvestment companies (including Company D)and two other individuals (Individual 2 andIndividual 3). All of these entities wereassociated with the same specific address inEastern Canada and were linked through theirpositions within each organization.

• Company C offered financial services andordered EFTs to the benefit of Individual 4, alawyer residing in the United States. Individual4 and Individual 1 had the same last name andwere suspected of being relatives. Company Calso ordered EFTs to the benefit of real estatecompanies located in the United States.

• According to publicly available information,Individual 2 held the position of Director forboth Company C and Company D. In addition,Individual 3, a relative of Individual 2, wasreported to be a major shareholder of Company D.A number of EFTs were ordered by or for thebenefit of Company D to an account in theUnited States held by Individual 3, as well as to another personal account in Canada also held by Individual 3.

• Individual 5, a notary, was also under investi-gation and suspected of facilitating thelaundering of illicit funds through a trustaccount and a personal account. Individual 5transferred funds from a personal account inEurope to the lawyers’ trust account in Canada.Individual 5 was also the beneficiary of EFTsordered by individuals and businesses mainlylocated in Europe and the United States.

Nominees and trust accounts set up by lawyersand/or notaries were used in abundance in thiscase. Some of the companies, located in variousjurisdictions, were suspected of being shellcompanies and used solely for laundering fundsgenerated by the organized crime group.

RED FLAGS associated with this case:

• Frequent movement of funds between sametrust accounts and bank accounts held bybusinesses located in various jurisdictions andwith accounts in different financial institutionsalso located in various jurisdictions

• Multiple and frequent transfers of fundsbetween accounts held by businesses located at the same address and/or owned by the same individuals

Securities industry

In order to gain a better understanding of how the global securities industry may be used orassociated with suspected money launderingactivities, a detailed review of open sources,FINTRAC’s case disclosures, and large cash andsuspicious transaction reports for the period ofNovember 2001 to March 2007 was conducted.Focus was also placed on market manipulation andinsider trading which are the most common crimesin the securities industry.

Based on the results of this study, FINTRAC believesthat the securities industry has been used to launderproceeds generated by various crimes includingdrug trafficking, stock manipulation and fraud. Thefollowing typologies were found to be associatedwith the use of the securities industry for suspectedmoney laundering:

1. use of front companies;2. use of professionals to facilitate the

introduction of proceeds;3. use of margin trading accounts; and 4. use of money orders.

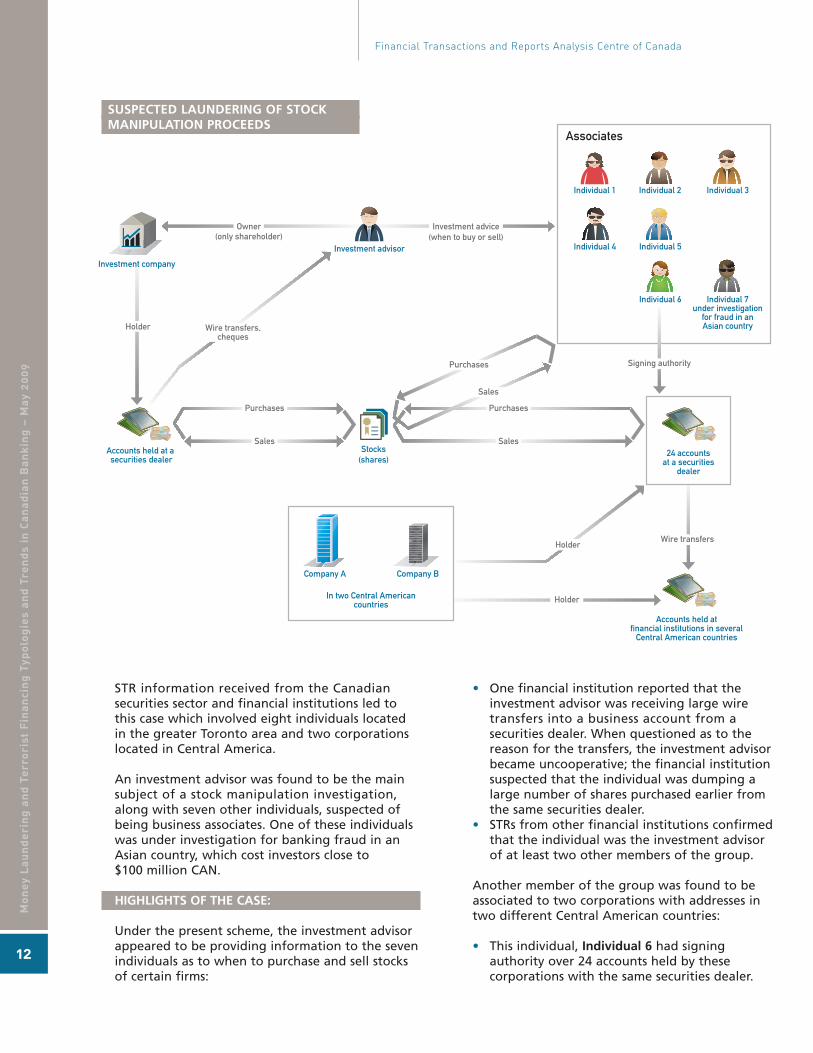

CASE EXAMPLE ILLUSTRATING THE SUSPECTED LAUNDERING OF STOCK MANIPULATIONPROCEEDS AND THE FIRST TWO TYPOLOGIES

This scheme involved the manipulation of stocks to make fraudulent profits which were launderedthrough a number of bank accounts in CentralAmerica and the Caribbean, as well as through thepurchase of monetary instruments made payableto suspected nominees. The chart on page 12provides an overview of the case.

11

MoneyLaunderingandTerroristFinancingTypologiesandTrendsin

CanadianBanking–May2009

STR information received from the Canadiansecurities sector and financial institutions led tothis case which involved eight individuals locatedin the greater Toronto area and two corporationslocated in Central America.

An investment advisor was found to be the mainsubject of a stock manipulation investigation,along with seven other individuals, suspected ofbeing business associates. One of these individualswas under investigation for banking fraud in anAsian country, which cost investors close to $100 million CAN.

HIGHLIGHTS OF THE CASE:

Under the present scheme, the investment advisorappeared to be providing information to the sevenindividuals as to when to purchase and sell stocksof certain firms:

• One financial institution reported that theinvestment advisor was receiving large wiretransfers into a business account from asecurities dealer. When questioned as to thereason for the transfers, the investment advisorbecame uncooperative; the financial institutionsuspected that the individual was dumping alarge number of shares purchased earlier fromthe same securities dealer.

• STRs from other financial institutions confirmedthat the individual was the investment advisorof at least two other members of the group.

Another member of the group was found to beassociated to two corporations with addresses intwo different Central American countries:

• This individual, Individual 6 had signingauthority over 24 accounts held by thesecorporations with the same securities dealer.

12

MoneyLaunderingandTerroristFinancingTypologiesandTrendsin

CanadianBanking–May2009

Financial Transactions and Reports Analysis Centre of Canada

Individual 1

Individual 4 Individual 5

Individual 6 Individual 7under investigation

for fraud in anAsian country

Individual 2 Individual 3

Associates

24 accountsat a securities

dealer

Accounts held at asecurities dealer

Stocks(shares)

Investment company

Company BCompany A

In two Central Americancountries Holder

Accounts held atfinancial institutions in several

Central American countries

Holder

Signing authority

Wire transfers

Owner(only shareholder)

Investment advice(when to buy or sell)

Investment advisor

Wire transfers,cheques

Sales

Purchases

Sales

Purchases

Purchases

Sales

Holder

SUSPECTED LAUNDERING OF STOCK MANIPULATION PROCEEDS

• STR information received from a securities dealerrevealed that this individual sold shares of specificcompanies shortly after purchase.

• The sales were followed by wire transfers to various bank accounts held by the twocorporations and the aforementioned investment advisor at financial institutions in Central America and the Caribbean.

The same type of activity appeared to be conducted byall of the individuals associated to this scheme:

• The purchase of securities (mostly penny stocksthat were not regulated, and therefore easy tomanipulate) would be quickly followed by a sale,which would then be followed by wire transfers ordeposits to bank accounts. Bank drafts would thenbe purchased, or cheques would be issued andmade payable to suspected nominees.

RED FLAGS associated with this case:

• Large number of accounts with (a) securitiesdealer(s)

• Large number of shares were traded shortly afterbeing purchased

• Two companies (possibly front ones) were locatedin a jurisdiction where incorporation is easilyobtained, or where business-related claims aredifficult to confirm

• A significant number of wire transfers were madeto offshore accounts, particularly following thesale of a substantial amount of shares

• Monetary instruments were made payable to anumber of suspected nominees

Additional red flags possibly related to marketmanipulation include:

• Large percentage of securities dealers’commission revenue generated from limitednumber of clients

• Securities agent or advisor purchasing or selling stocks outside his or her jurisdiction of registration

• Financial statements of companies, includingbalance sheets, income statements, andstatements of change in financial position are not publicly available

• Company’s published statements of cash flowindicates the presence of capital, but no cashflow generated by the organization

• Company’s executives reside in jurisdictionswithout extradition treaties with Canada

• Securities sales by insiders such as companyexecutives, their relatives etc.

• Unrealistic increase in share prices withoutmajor announcements in terms of futureprojects, earnings etc.

• Unrealistic increase in share prices with anannouncement that cannot be verified

Relevant designated information regarding thiscase was disclosed to law enforcement to assist in their investigation.

13

MoneyLaunderingandTerroristFinancingTypologiesandTrendsin

CanadianBanking–May2009

EMERGING VULNERABILITIES

Payment system innovations are driven by a number offactors, including economic environment, technology,consumer preferences, costs, regulations, as well asprivate and government policies/practices. In this fast-paced environment, consumers are looking for quickand easy payment methods. In response to these needs,new payment technologies have been introduced andwith them, new risks related to money laundering andterrorist financing have emerged for the banking sector,other reporting entities and FINTRAC.

In 2007-2008, FINTRAC’s environmental scanning ofvarious sources of information related to ML/TF, incombination with the review of cases disclosed duringthe same period, revealed that prepaid cards anddigital precious metals were new payment methodsthat were becoming increasingly popular and possiblyposing certain ML/TF risks. The ML/TF risks associatedwith prepaid cards and digital precious metals arediscussed in this section.

Prepaid cards

Prepaid cards provide access to funds that are paid in advance by the cardholder or a third party.These cards have the same characteristics thatmake cash so attractive to criminals: they areportable, valuable, exchangeable and anonymous.6

In addition, they are not subject to cross-borderreporting since they are not considered monetaryinstruments, making it easier to transfer wealthfrom one jurisdiction to another. The wide varietyof funding mechanisms also means fund originsare difficult to trace and it is difficult to ascertainwhether or not the money is from a legitimatesource.

FINTRAC conducted a vulnerability assessment of prepaid cards after it was identified as anemerging issue throughout our ongoing environ-mental scanning. Within the Canadian market,there are two types of prepaid cards that arecurrently offered: open-system/loop and closed-system/loop. FINTRAC’s assessment of the businessmodels for the two types of prepaid cards thatidentify possible areas of vulnerabilities to ML and TF are provided in the following section.

VULNERABILITIES ASSOCIATED WITH OPEN-LOOP PREPAID CARDS

Open-system/loop prepaid cards are always issuedby financial institutions but can be distributedeither by financial institutions or by MSBs, and arein most cases network-branded with Visa orMasterCard. These cards can be used to makepurchases at any locations which have access tothese networks and also to withdraw cash fromATMs. Open-loop cards can be obtained at thephysical location of the banks or service providers,or online. These cards are not necessarily connectedto a bank account and the verification of cardholderidentity varies from one provider to another.Examples of open-loop cards include payroll cardsand prepaid cards that can be used by thepurchaser or by someone else.

Open-loop cards allow cardholders to move fundseasily and anonymously worldwide because ofpotentially limited identity verification mechanismsand the possibility of multiple cardholders, aroundthe world, using the same card. The onlineavailability of cards means that there is no face-to-face contact between the customer and theservice provider, hence increasing the risk thatstolen information or nominees could be used toobtain cards. In addition, holders of cards of thesame issuer but with different accounts can, insome cases, also transfer funds from one card to another through the Internet. Generally,transactions on the Internet allow a certain degreeof anonymity that can potentially be exploited bymoney launderers or terrorist activity financiers.

In addition, cards can be anonymously loaded withfunds. For example, some cards can be loaded withcash at a third party reseller location. The loader isnot required to show identification, and the sourceof funds is not determined. The large variety ofloading options makes it possible for a moneylaunderer to fund a card with illicit proceeds.

High or no value limit open-loop prepaid cardssignificantly increase the risk of ML and TF.7 Forinstance, many offshore financial institutions,sometimes located in countries with weak AMLlegislation, offer unlimited value prepaid cards and market the cards in a way that specifically

6 http://www.moneylaundering.com/Agent.aspx?Page=/NewsBriefDisplay.aspx?id=963 7 “Report on New Payment Methods”, FATF Report, October 2006. Available at: http://www.fatf-gafi.org/dataoecd/30/47/37627240.pdf14

MoneyLaunderingandTerroristFinancingTypologiesandTrendsin

CanadianBanking–May2009

Financial Transactions and Reports Analysis Centre of Canada

promotes the movement of money in ananonymous fashion.8 The high card limits allow for large amounts of funds to be moved aroundthe world.

VULNERABILITIES ASSOCIATED WITH CLOSED-LOOPPREPAID CARDS

Closed-system/closed-loop prepaid cards can beobtained in many retail stores, online and incasinos. They can be used to make purchases orconduct gaming transactions within an internalnetwork. Most closed-loop cards are not providedby financial institutions, and little or no identifi-cation is required to obtain them. Examples ofclosed-system prepaid cards include gift cards andprepaid long distance phone cards. These cards areeither limited to the original value placed on thecards or can be reloaded, within limits determinedby the company.

Since identification is not required whenpurchasing most closed-loop prepaid cards, theycan be obtained and used anonymously to makepurchases. The lack of customer identification blurstransaction trails, making it more difficult for lawenforcement to track cardholders.9 Closed-loopcards are also more easily traded, making themideal for commodity trading or as an alternativefor bulk cash smuggling, especially since thesecards are not monetary instruments and are,therefore, not subject to cross-border reporting.

Gift cards have also been reported to be used in“cyber money laundering” or “e-fencing” in whichcriminals use stolen credit card numbers to buy giftcards online, and then sell them to the highestbidder at an online auction Web site or for a setdiscount at a gift-card exchange Web site.10 Similarly,gift cards can be purchased with any illicit proceedsand then re-sold for the sole purpose of moneylaundering. This method has been found to be verylucrative for criminals since stolen or illegitimate giftcards can typically be re-sold for 80 per cent of theirface value, compared to just 30 per cent for typicalgoods on the black market.11 Since late 2002, giftcards have been increasingly turning up for resale at eBay, Craigslist and card-exchange sites such as cardavenue.com, plasticjungle.com andswapagift.com. In July 2007, eBay was listing

more than 3,400 gift cards for resale.12

The U.S. Drug Enforcement Agency has alsoindicated that prepaid cards are often beingtargeted by thieves normally stealing credit cards,drug rings and terrorist cells for terroristfinancing.13 For example, these cards could be used to purchase supplies necessary for terroristactivities or be smuggled cross-border in lieu ofcash. In fact, the Singapore Internal SecurityDepartment has found that the Liberation Tigersof Tamil Eelam (LTTE)14 has made extensive use of mobile phones loaded with prepaid cards. 15

The Singapore Government is therefore planning to regulate the sale of prepaid cards formobile phones.

To date, a limited number of cases disclosed byFINTRAC have involved the use of prepaid cards.Businesses involved in the sales of prepaid phonecards (closed-loop) have been part of suspiciousschemes possibly related to both ML and TF. On theother hand, FINTRAC suspects that open-loop cardshave been used to conduct illegal online gamblingactivities, i.e. mainly to redeem gamblingwinnings/proceeds.

Digital Precious Metals

Through environmental scanning of publiclyavailable information and the review of 2006-2007case disclosures, FINTRAC identified Internetpayment systems (IPS) and their variants, includingdigital precious metals (DPMs), to be possiblyexploited for money laundering and terroristfinancing activities. Consequently, FINTRAC studiedthe various business models of IPS and of DPMs toidentify the features/characteristics that wouldmake them vulnerable to ML and/or TF.

The study was divided in two parts, the first partfocused on payment processing and debit-accountIPS, while the second one focused solely on DPMs.Payment processing IPS offer services only to onlinemerchants, debit-account IPS allow person-to-person transfers across jurisdictions, and DPMsallow users to convert national currencies intoelectronic currencies via an exchange maker. Payment processing and debit-account variants of IPS are vulnerable in part because two of

15

MoneyLaunderingandTerroristFinancingTypologiesandTrendsin

CanadianBanking–May2009

8 http://www.usdoj.gov/ndic/pubs11/20777/20777p.pdf 9 “Report on New Payment Methods”, FATF Report, October 2006. Available at: http://www.fatf-gafi.org/dataoecd/30/47/37627240.pdf10 “Online Resale of Gift Cards Raises Fraud Alarms”, ABC News, July 23, 2007.11 “Scam may be tied to stolen TJX data”, The Boston Globe, March 24, 2007.12 “Online Resale of Gift Cards Raises Fraud Alarms”, ABC News, July 23, 2007.13 http://moneycentral.msn.com/content/Banking/P137668.asp 14 The Canadian Government listed the Liberation Tigers of Tamil Eelam (LTTE) as a terrorist group on April 8, 2006, pursuant to the Criminal Code.15 http://www.texturally.org/textually/archives/2005/03/007377.htm

their key attributes, anonymity and paymentdisintermediation (i.e. untraceable transactions),match those of physical cash, the ideal method ofvalue transfer for criminal activity. Moreover,debit-account IPS offer a greater layering riskthan payment processing IPS because their designfeatures facilitate person-to-person (P2P) transfersacross jurisdictions with relative speed and ease.16

Digital precious metals appear to be morevulnerable to ML/TF than the other two variants.Digital precious metals operators (DPMOs) are IPS providing users with “digital currencies”purportedly backed by precious metals that can beused for e-commerce, bill payments, person-to-person payments and other typical transactions. In contrast with payment processing and debitaccount type IPS, using a DPMO involves the use of two separate service providers. A user accountfirst needs to be set up with the DPMO. Then to fund the account, the user needs to remitcurrency into “digital currencies” via a digitalcurrency exchange service (DCES). Upon receipt ofthe remittance, the DCES funds the user’s accountwith the DPMO. DCES and DPMOs operateindependently from one another.

FINTRAC’s analysis revealed that DPMOs and DCEShave features that may be suitable for each phaseof money laundering. It was found that exploitableweaknesses such as user anonymity and theexistence of a network of exchange services—someaccepting cash deposits to fund DPM accounts—may facilitate the placement phase. In the layeringphase, a launderer can “cash in” and “cash out”his/her DPM account with multiple DCES, converte-currencies into other e-currencies and transfer e-currencies to another user who can then redeem his/her account in currency. Finally, cashwithdrawals with so-called “digital gold cards”may facilitate the integration phase of ML.

While there is a legitimate market demand forsuch alternative payment systems, FINTRACbelieves that there is a real potential for DCES/DPMOs to be exploited for ML/TF because of thetwo-layer transaction process. This results in:

1. A higher degree of anonymity than with other IPS• DPM accounts are not tied to bank accounts

that are subject to customer identificationverifications. DCES are under no obligation tovet the source of funds they transfer to DPMaccounts. Similarly, DPMOs cannot trulyascertain the origins of the funds they receivefrom DCES. The relationship between theDPMO and the DCES is almost entirely online,raising risk.

2. A greater potential to disguise the origin anddestination of funds than with other IPS• The existence of a web of DCES offering

different options for receiving and sendingfunds — some accepting cash, some allowingusers to convert e-currencies into othere-currencies — can make it challenging toaudit a user’s full transaction activity.Moreover, the recent introduction on themarket of so called “digital gold ATM cards”offers the potential for launderers to re-integrate proceeds into the conventionalfinancial system.

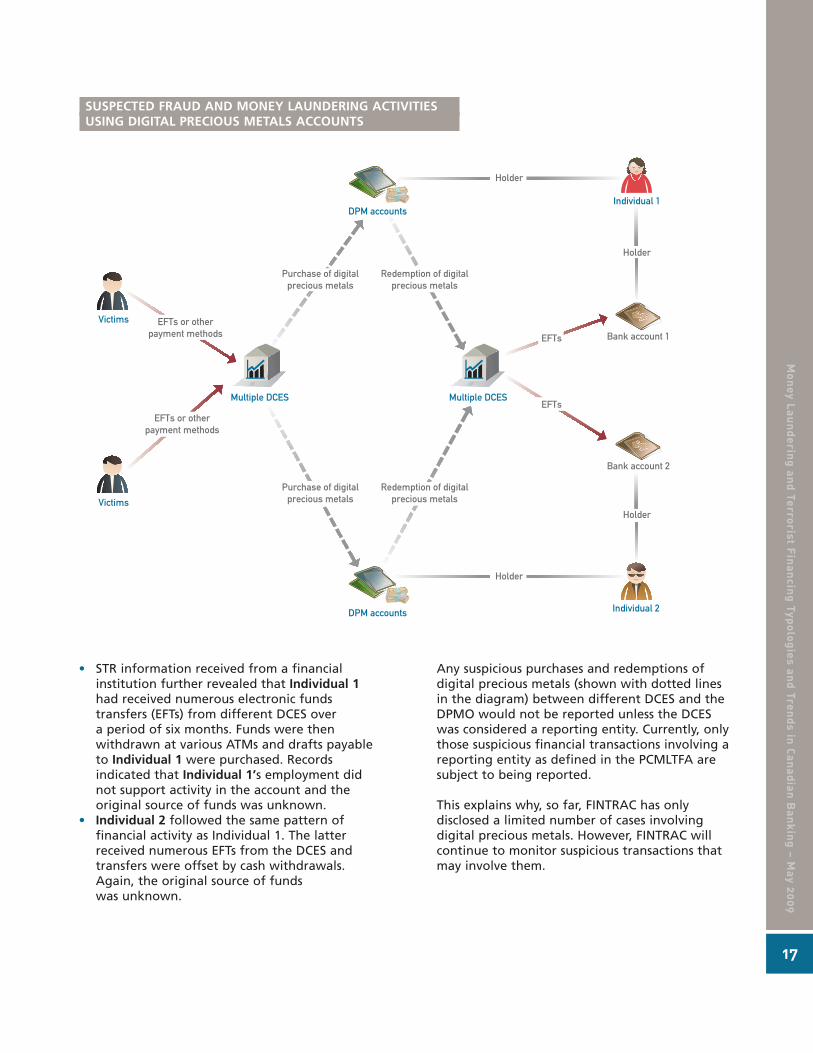

The following sanitized case example (see charton page 17) illustrates how the user anonymity,the two-tier transaction process (i.e. DPMO andDCES) and the possible network of DCES involvedin transactions associated to one DPM accountcan facilitate fraudulent and money launderingactivities:

• According to voluntary information FINTRACreceived from law enforcement, Individuals 1and 2 were suspected of being involved in an“online investment fraud” scam. Victims weretold to send their payments to Individuals 1 and2’s DPM accounts through multiple DCES. Thelatter then funded Individuals 1 and 2’s DPMaccounts with digital precious metals. Uponreceipt, the digital currencies were exchangedvia different DCES and wired into Individual 1’sand 2’s bank accounts.

16 While debit-account and payment processing IPS both offer payment disintermediation, the design features ofthe former potentially increase the money laundering risk. While it may be true that debit-account IPS userswhose virtual accounts are tied to their bank accounts theoretically leave an audit trail, the most vulnerable typeof transactions to money laundering, P2P ones, can only occur within a closed network of users. Thus, if there isno central vetting process to effectively trace and scrutinize all this P2P exchange of financial value over a certainmonetary threshold, and therefore no reporting of such potentially suspicious information, there is a greaterpossibility for disintermediation and the money laundering risk increases accordingly.

16

MoneyLaunderingandTerroristFinancingTypologiesandTrendsin

CanadianBanking–May2009

Financial Transactions and Reports Analysis Centre of Canada

• STR information received from a financialinstitution further revealed that Individual 1had received numerous electronic fundstransfers (EFTs) from different DCES over a period of six months. Funds were thenwithdrawn at various ATMs and drafts payableto Individual 1 were purchased. Recordsindicated that Individual 1’s employment didnot support activity in the account and theoriginal source of funds was unknown.

• Individual 2 followed the same pattern offinancial activity as Individual 1. The latterreceived numerous EFTs from the DCES andtransfers were offset by cash withdrawals.Again, the original source of funds was unknown.

Any suspicious purchases and redemptions ofdigital precious metals (shown with dotted lines in the diagram) between different DCES and theDPMO would not be reported unless the DCES was considered a reporting entity. Currently, onlythose suspicious financial transactions involving areporting entity as defined in the PCMLTFA aresubject to being reported.

This explains why, so far, FINTRAC has onlydisclosed a limited number of cases involvingdigital precious metals. However, FINTRAC willcontinue to monitor suspicious transactions thatmay involve them.

17

MoneyLaunderingandTerroristFinancingTypologiesandTrendsin

CanadianBanking–May2009

Individual 1

Holder

Holder

Bank account 1

Bank account 2

Victims

Victims

DPM accounts

DPM accounts Individual 2

Multiple DCES Multiple DCES

EFTs

EFTs

Holder

Holder

EFTs or otherpayment methods

EFTs or otherpayment methods

Purchase of digitalprecious metals

Purchase of digitalprecious metals

Redemption of digitalprecious metals

Redemption of digitalprecious metals

SUSPECTED FRAUD AND MONEY LAUNDERING ACTIVITIESUSING DIGITAL PRECIOUS METALS ACCOUNTS

CONCLUSION FINTRAC continues to value the work and efforts of the Canadianbanking sector and other reporting entities in the fight againstmoney laundering and terrorist financing. The information provided in this document is intended to further assist the banking sector andother financial entities in detecting and deterring ML/TF activities.FINTRAC is committed to providing the banking sector with thenecessary information to assist in the development of new andbetter tools/systems and also train staff.

18

MoneyLaunderingandTerroristFinancingTypologiesandTrendsin

CanadianBanking–May2009

Financial Transactions and Reports Analysis Centre of Canada

![Money Laundering [ML] & Terrorist Financing [TF] Risk](https://img.pdfslide.us/doc/110x75/623d5cf4c270f02e150e5c02/money-laundering-ml-amp-terrorist-financing-tf-risk-.jpg)